Asymmetric linear double autoregression

Abstract

This paper proposes the asymmetric linear double autoregression, which jointly models the conditional mean and conditional heteroscedasticity characterized by asymmetric effects. A sufficient condition is established for the existence of a strictly stationary solution. With a quasi-maximum likelihood estimation (QMLE) procedure introduced, a Bayesian information criterion (BIC) and its modified version are proposed for model selection. To detect asymmetric effects in the volatility, the Wald, Lagrange multiplier and quasi-likelihood ratio test statistics are put forward, and their limiting distributions are established under both null and local alternative hypotheses. Moreover, a mixed portmanteau test is constructed to check the adequacy of the fitted model. All asymptotic properties of inference tools including QMLE, BICs, asymmetric tests and the mixed portmanteau test, are established without any moment condition on the data process, which makes the new model and its inference tools applicable for heavy-tailed data. Simulation studies indicate that the proposed methods perform well in finite samples, and an empirical application to S&P500 Index illustrates the usefulness of the new model.

Keywords: Asymmetry tests; Autoregressive time series model; Model selection; Portmanteau test; Quasi-maximum likelihood estimation; Stationary solution.

1 Introduction

Volatility clustering is a major feature of financial time series, and the ability to forecast volatility is of vital importance for the pricing and risk management of financial assets. To capture the time-varying volatility, many conditional heteroscedastic models are proposed, and among them, the autoregressive conditional heteroscedastic (ARCH) and the generalized autoregressive conditional heteroscedastic (GARCH) models (Engle, 1982; Bollerslev, 1986) are very successful specifications. However, empirical facts indicate that the autocorrelation and volatility dynamics usually coexist in time series; see, for example, the daily returns of NASDAQ Composite Index in Kuester et al. (2006) and the weekly or monthly returns of S&P500 index in Linton and Mammen (2005). As a result, to better capture the volatility dynamics in the presence of data autocorrelations, it is necessary to jointly model the conditional mean and volatility (Li et al., 2002). The autoregressive moving average models with GARCH errors (ARMA-GARCH) and double autoregressive (DAR) models are popular specifications for this purpose.

In financial applications, ARMA-GARCH models are commonly used to fit return series (Francq and Zakoian, 2019). Many researchers have studied the estimation for ARMA-GARCH models; see among others, Francq and Zakoian (2004) and Zhu and Ling (2011). Francq and Zakoian (2004) has shown that, a finite fourth moment on the data process is required to establish the asymptotic normality of the Gaussian quasi-maximum likelihood estimator (QMLE) for the ARMA-GARCH model. This largely narrows down the application of ARMA-GARCH models since the heavy-taildeness is very common for financial data. Meanwhile, the DAR model proposed by Ling (2007) has recently attracted growing attention. The DAR model of order is defined as

| (1.1) |

where , for , and are independent and identically distributed () innovations with zero mean and unit variance. In contrast to the ARMA-GARCH model, the Gaussian QMLE of model (1.1) is asymptotically normal provided that has a fractional moment (Ling, 2007). This important property makes model (1.1) suitable for handling heavy-tailed data in application. In addition, the DAR model with order can still be stationary even if or , thus it enjoys a larger parameter space than conventional AR and AR-ARCH models.

Many variants of DAR models have been widely proposed and studied, such as the threshold DAR (Li et al., 2016), the mixture DAR (Li et al., 2017), the linear DAR (Zhu et al., 2018) and the augmented DAR (Jiang et al., 2020) models. Specifically, the linear DAR model of order has the form of

| (1.2) |

where the innovations and parameters are defined as in model (1.1). Model (1.2) assumes that the conditional standard deviation rather than the conditional variance of is in a linear structure, which can lead to more robust inference than model (1.1); see Taylor (2008) and Zhu et al. (2018). As shown by Zhu et al. (2018), the linear DAR model has a larger parameter space than conventional AR and AR-ARCH models as for DAR models. Moreover, the asymptotic normality of the Gaussian QMLE can also be established for model (1.2) without any moment restrictions on ; see Liu et al. (2020). As a result, the linear DAR model enjoys the important property of DAR models and hence can also be used to fit heavy-tailed data.

It is well known that financial time series are usually characterized by asymmetry (leverage) effects, in the sense that the volatility of financial returns tends to be higher after a decrease than an equal increase. The leverage effect was documented by many authors as a stylized fact of stock returns; see, for example, Black (1976), Rabemananjara and Zakoian (1993) and Francq and Zakoian (2013). To account for the leverage phenomenon, many variants of classical GARCH models are introduced and studied, such as the exponential GARCH (Nelson, 1991), the threshold GARCH (Zakoian, 1994) and the power GARCH (Pan et al., 2008) models. Specifically, Engle and Ng (1993) defined the news impact curve to measure how new information is incorporated into volatility estimates, and based on this curve they provided diagnostic tests to detect asymmetric effects of news on volatility. However, limited literatures investigate the leverage effect in the presence of the conditional mean structure, even rare in the framework of DAR models. To fill this gap, we propose an asymmetric linear DAR model, which can be regarded as a modification of the linear DAR model along the lines of the threshold GARCH model. Hopefully, the new model can preserve the advantages of DAR type models in handling with heavy-tailed data and meanwhile be able to capture the asymmetric effect successfully. The main contributions of this paper are listed as follows.

First, Section 2 introduces an asymmetric linear DAR model to capture leverage effects, where the coefficients for positive and negative parts of in the conditional standard deviation can be different. We establish a sufficient condition for the strict stationarity and ergodicity of the new model by showing that the Markov chain is -irreducible and satisfies Tweedie’s drift criterion (Tweedie, 1983); see also Zhu et al. (2018). It is shown that the stationary region of the proposed process depends on the moment condition of innovations and the degree of asymmetry. Moreover, the proposed process can still be stationary even if some AR coefficient is greater than one, leading to a large stationary region as for the DAR and linear DAR models.

Secondly, Section 3 proposes the Gaussian QMLE for the new model and establishes its consistency and asymptotic normality. Particularly, the consistency is carefully considered to avoid the identification problem due to the coexistence of the positive and negative parts of , and the asymptotic normality is established without any moment condition on . Hence, the new model can be used to fit heavy-tailed data. Moreover, based on the QMLE, a Bayesian information criterion (BIC) is proposed for model selection, and a modified BIC is introduced to improve the finite-sample performance. It is shown that both BICs enjoy the selection consistency without any moment condition on the process , and the modified BIC usually outperforms the unmodified BIC especially for small and moderate samples. As a result, the first two stages of Box-Jenkins’ procedure including model specification and estimation are constructed for the new model in a robust way, which facilitates its application to financial time series.

Thirdly, to detect the asymmetry in volatility, the Wald, Lagrange multiplier (LM) and quasi-likelihood ratio (QLR) tests are constructed in Section 4. Under the null and local alternative hypotheses, the Wald and LM test statistics are shown to have the same limiting distributions, while the QLR test statistic converges to weighted sums of central and noncentral chi-squared random variables, respectively. It is noteworthy that, to show the asymptotic distributions of three test statistics under local alternatives, we need to verify the local asymptotic normality (LAN) of the proposed model. However, without the normal assumption on the innovation term, the Le Cam’s third lemma cannot be employed to show the LAN property (van der Vaart, 2000). Alternatively, we show that the new model satisfies the LAN in a direct way; see also Jiang et al. (2020). Moreover, we conduct simulation experiments to compare the local power of all three tests in finite samples, and simulation results further support the theoretical findings.

Finally, we investigate diagnostic checking for fitted models using a mixed portmanteau test in Section 5. The portmanteau test for pure mean models (Ljung and Box, 1978) is constructed using the sample autocorrelation functions (ACFs) of residuals, while that for volatility models (Li and Li, 2008) employs the ACFs of squared or absolute residuals. As validated by simulation findings of Li and Li (2005), the portmanteau test based on absolute residuals is less powerful than that based on squared residuals under heavy-tailed situations. As a result, this paper proposes a mixed portmanteau test (Wong and Ling, 2005) using the ACFs of residuals and absolute residuals to detect inadequacy in the conditional mean and volatility of the fitted new model. The joint limiting distribution for ACFs of residuals and absolute residuals is established without any moment condition on the process . Simulation results validate that the mixed test can detect inadequacy of fitted models due to either the conditional mean or the volatility. Therefore, as the last stage of Box-Jenkins’ procedure, the diagnostic checking tool is successfully constructed in a robust way as well.

In addition, Section 6 conducts simulation studies to evaluate the finite-sample performance of all inference tools for the proposed model. Section 7 illustrates the usefulness of the new model by analyzing the S&P500 Index and demonstrates the forecasting superiority over its counterparts especially for the skewed and heavy-tailed data. The conclusion and discussion appear in Section 8. All technical details are relegated to the Appendix. Throughout the paper, denotes the integer, and denote the convergences in probability and in distribution, respectively, and denotes a sequence of random variables converging to zero in probability.

2 Asymmetric linear double autoregression

Consider the asymmetric linear double autoregressive (DAR) model of order ,

| (2.1) |

where for , and are positive and negative parts of , respectively, and is a sequence of random variables with mean zero and variance one. The asymmetric linear DAR model in (2.1) is an extension of the linear DAR model (Zhu et al., 2018) along the lines of the threshold GARCH model (Zakoian, 1994). Although the linear DAR model can be extended to allow for asymmetries in both the conditional mean and conditional heteroscedasticity, this paper focuses on model (2.1) to take account for the asymmetry in volatilities. The real example of stock index returns in Section 7 provides evidence for this motivation.

For general distributions of , it is difficult to derive a necessary and sufficient condition for the strict stationarity due to the nonlinearity of model (2.1); see also Li et al. (2016) and Zhu et al. (2018). Alternatively, a sufficient condition is provided below.

Assumption 1.

The density function of is continuous and positive everywhere on , and for some .

Theorem 1.

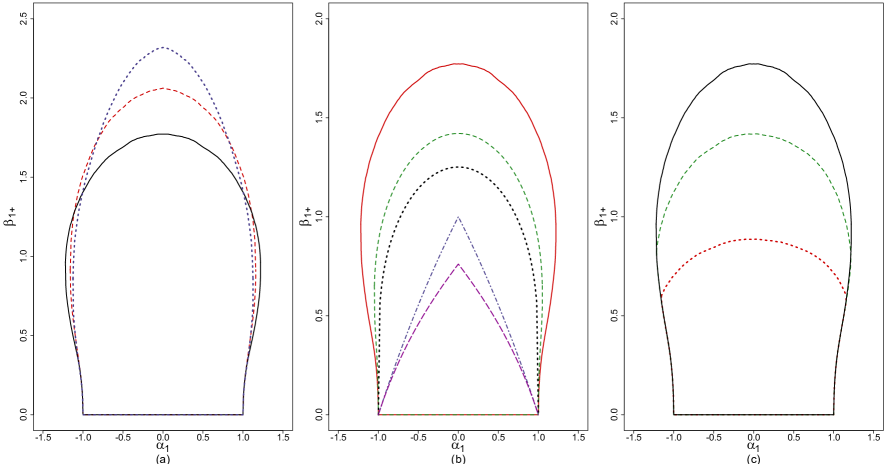

The stationarity region in Theorem 1 depends on the distribution of and implies a moment condition on . In addition, when has a symmetric distribution and the asymmetric linear DAR model reduces to a linear DAR model, that is , then it simplifies to for , and to for . Since the stationarity region of model (2.1) is at least three-dimensional, for illustration, we provide the stationarity regions of model (2.1) of order one, and consider with the constant being different positive values. Figure 1(a) indicates that model (2.1) of order one can be stationary if , hence model (2.1) preserves a large parameter space as DAR and linear DAR models. As shown in Figure 1(b), a larger value of in Theorem 1 leads to a higher moment of , and hence results in a narrower stationarity region. Moreover, Figure 1(c) shows that the stationarity region gets smaller as the asymmetry in volatilities becomes greater.

Remark 1.

The order of model (2.1) can be different for the conditional mean and volatility, that is, we can consider the asymmetric linear DAR model of order

where and are positive integers. For the strict stationarity of this general model setting, Theorem 1 still holds by letting with for and for . However, if , the conditional scale structure cannot be used to reduce the moment condition on for showing the asymptotic normality of the quasi-maximum likelihood estimator in Section 3. To establish the asymptotic normality without any moment condition on , other estimation methods such as the self-weighted approach (Ling, 2005) should be considered. We leave this extension for future research, and consider the same order in this paper.

3 Model estimation

3.1 Quasi-maximum likelihood estimation

Let be the parameter vector of model (2.1), where , with and . Denote the true parameter vector by and the parameter space by , where is a compact subset of with .

Let and , where and . The conditional log-likelihood function (ignoring a constant) can be written as

| (3.1) |

Then the quasi-maximum likelihood estimator (QMLE) of can be defined as

| (3.2) |

Assumption 2.

is strictly stationary and ergodic with for some .

Assumption 3.

The density function of is continuous and positive everywhere on .

Assumption 4.

The parameter space is compact with , for , where are some positive constants. The true parameter vector is an interior point in .

For the strict stationarity of in Assumption 2, a sufficient condition is given in Theorem 1. Assumption 3 is imposed for identifying the unique maximizer of at ; see also Francq and Zakoian (2012). Assumption 4 is required to ensure the log-likelihood function, score function and information matrix to be bounded without any moment restrictions on ; see also Ling (2007). As a result, the model based on the QMLE can be applied to heavy-tailed data.

Let and . Define the matrices

and

| (3.3) |

Theorem 2.

Note that the positive definiteness of is satisfied for continuous with ; see Jiang et al. (2020). If is normal, then and , thus the QMLE reduces to the MLE and its asymptotics in Theorem 2 can be simplified to as . To calculate the asymptotic covariance of , we use sample averages to replace matrices and , and the QMLE to replace .

3.2 Model selection

This subsection considers the selection of order for model (2.1) in practice. We first introduce the Bayesian information criterion (BIC) below to select the order ,

| (3.4) |

where is the QMLE when the order is set to , and is the log-likelihood evaluated at . However, model (2.1) is fitted by the Gaussian QMLE, hence the model misspecification should be considered in deriving the asymptotic expansion of the Bayesian principle, which leads to the modified BIC below

| (3.5) |

where is a consistent estimator of defined as in (3.3) at order , and is its determinant. In practice, can be calculated with replaced by and the expectation approximated by the sample average. The modified BIC in (3.5) is adapt to the generalized BIC proposed by Lv and Liu (2014), where the addtional term of their generalized BIC is introduced to account for model misspecifications. For more details of the derivation of the above BICs, please refer to Appendix A.3.1.

Let for and 2, where is a predetermined positive integer. Note that, when the sample size is sufficiently large, the additional terms and can be ignored as they are . As a result, and are asymptotically equivalent in order selection. Simulation results in Section 6 indicate that the modified BIC in (3.5) performs better than the original BIC in (3.4) for moderate and small samples, although the two BICs have very similar performance for large samples. Hence, for moderate and small samples, we suggest to use (3.5). The following theorem verifies their selection consistency.

Theorem 3.

Under the assumptions of Theorem 2, if , then as ,

where is the true order, and is a predetermined positive integer.

4 Testing for asymmetry

This section studies the Wald, Lagrange multiplier (LM) and quasi-likelihood ratio (QLR) tests to detect the asymmetry (leverage) effect of news on volatilities.

4.1 Asymmetry Tests

For model (2.1), the asymmetry testing is of the form

| (4.1) |

where . Let be the matrix, where is the zero matrix and is the identity matrix. Then the null hypothesis can be represented as , where is the true parameter vector and is a -dimensional zero vector. Hence, the Wald, LM and QLR test statistics are defined as

| (4.2) | ||||

respectively, where is the restricted QMLE under while is the unrestricted QMLE, is the sample estimate of with estimated by and the expectation replaced by sample average, while (or ) is the sample estimate of (or ) with estimated by and the expectation replaced by sample average.

Let be the chi-squared distribution with degrees of freedom. Define the matrix with . For , let ’s be the eigenvalues of , and ’s be the random variables following the distribution. The following theorem gives the limiting distributions of three test statistics under .

Theorem 4.

Theorem 4 shows that the limiting null distribution of is not the usual distribution but a distribution of the weighted sum of random variables. This is because in the absence of normality assumption on ; see also MaCurdy (1981). If is normally distributed, then for and reduces to a distribution, and hence has the standard limiting null distribution as and . For general cases of , we adopt the Pearson’s three-moment central chi-square approach (Pearson, 1959) to approximate -values of the QLR test; see also Imhof (1961) and Liu et al. (2009). The detailed procedure of Pearson’s method is summarized in Remark 2 below.

Remark 2.

(Calculation of -values for the QLR test) First, calculate , and , where for . Then, the -value of the QLR test is approximated by , where is the observed value of the QLR test statistic.

4.2 Power analysis

We next discuss the efficiency of the proposed asymmetry tests through Pitman analysis. Note that with under . Denote , where , , and . Let such that for sufficiently large . Consider the local alternatives, that is, for each , the observed time series are generated by

| (4.3) |

where the subscript is used to emphasize the dependence of on , is defined as in the model (2.1), , with and . satisfies the condition below.

Assumption 5.

There exists a positive integer such that for , is strictly stationary and geometrically ergodic with for some .

Based on , the QMLE under can be defined as

| (4.4) |

where

Denote as the law of . The asymptotic distribution of under sequences of local alternatives is given below.

Theorem 5.

Theorem 5 verifies that model (4.3) is locally asymptotically normal (van der Vaart, 2000) at . If follows a normal distribution, we can show Theorem 5 by Le Cam’s third lemma. However, when is not normal, the sequences and are not mutually contiguous; see Example 6.5 in van der Vaart (2000) for more discussions. Therefore, we show Theorem 5 in a direct way; see also Jiang et al. (2020).

Denote , and define as an orthogonal matrix such that , where ’s are eigenvalues of . Denote , and let be its -th component for . Let be the noncentral chi-squared distribution with degrees of freedom and noncentrality parameter , and be its th quantile.

Theorem 6.

Suppose the assumptions of Theorem 5 hold and . Then, under , as ,

where , and ’s are independent random variables following the distribution for .

Theorem 6 obtains the asymptotic distributions of three test statistics under the local alternatives, which shows that the Wald and LM tests have the same local asymptotic powers. If is normally distributed, then reduces to a distribution, and the QLR test is as efficient as the Wald and LM tests. Moreover, note that holds for , then it follows that the proposed three tests are equivalent in the local asymptotic power when . For general cases of with , it is difficult to compare the local asymptotic power of the QLR test with the other two tests. Alternatively, the simulation study in Section 6.3 compares the local power of all three tests in finite samples, and it is found that three tests perform very similarly when the sample size is as large as 2000.

5 Model checking

To check adequacy of the fitted asymmetric linear DAR model, we construct a mixed pormanteau test to detect misspecifications in the conditional mean and standard deviation jointly; see Wong and Ling (2005). In the literature, diagnostic checking the conditional mean and standard deviation, can be conducted by checking the significance of sample autocorrelation functions (ACFs) of residuals and absolute residuals, respectively.

The ACFs of and at lag can be defined by and , respectively. If the data generating process is correctly specified by model (2.1), then and are such that and hold for any . For model (2.1) fitted by the QMLE, the corresponding residuals can be defined as , and then the residual ACF and absolute residual ACF at lag can be calculated as

respectively, where and . Clearly, (or ) is the sample version of (or ). Accordingly, if the value of (or ) deviates from zero significantly, it indicates that the conditional mean (or standard deviation) structure in model (2.1) is misspecified.

Let and , where is a predetermined positive integer. Denote and . Let , then and . Define the matrices and , where

Denote the matrix below

Let , and .

Theorem 7.

Theorem 7 can be used to check the significance of or individually. We can construct consistent estimators of and using sample averages, which are denoted by and , respectively. Then we can approximate the asymptotic distribution in Theorem 7, and obtain confidence intervals for and .

To check the first lags jointly, we construct a portmanteau test statistic below

| (5.1) |

Theorem 7 and the continuous mapping theorem imply that, as . Therefore, we reject the null hypothesis that and () are jointly insignificant at level , if exceeds the th quantile of distribution.

6 Simulation experiments

This section presents four simulation experiments to evaluate the finite-sample performance of the proposed QMLE, model selection method, three asymmetry tests and the mixed pormanteau test.

6.1 Model estimation

The first experiment aims to examine the finite-sample performance of the quasi-maximum likelihood estimator , for which the data generation process is

where are standard normal, or follow standardized Student distribution with unit variance, or standardized skewed distribution, denoted by , with unit variance and skew parameter (Jiang et al., 2020). The sample size is set to or 2000, with 1000 replications for each sample size. The projection newton method (Bertsekas, 1982) is employed for solving the optimization (3.2) in each replication. Table 1 lists the biases, empirical standard deviations (ESDs) and asymptotic standard deviations (ASDs) of for different innovation distributions and sample sizes. As the sample size increases, most of the biases, ESDs and ASDs become smaller, and the ESDs get closer to the corresponding ASDs. Moreover, when the distribution of gets more heavy-tailed or skewed, all ESDs and ASDs increase. This is as expected since either heavier tails or severer skewness of will lead to lower efficiency of the QMLE. In addition, we also consider other parameter settings for the data generation process, and the simulation findings are similar as prevous.

6.2 Model selection

In the second experiment, we evaluate the performance of the proposed model selection method in Section 3.2, and compare the BIC1 and its modified version BIC2 in finite samples. The data generating process is

where the innovations are defined as in the previous experiment. Three sample sizes, and 1000, are considered, and 1000 replications are generated for each sample size. The BIC1 in (3.4) and BIC2 in (3.4) are employed to select the order with . For or 2, the cases of underfitting, correct selection and overfitting by BICi correspond to being 1, 2 and greater than 2, respectively.

Table 2 reports the percentages of underfitted, correctly selected and overfitted models by the two information criteria. The performance of both information criteria gets better when the sample size increases, while that becomes slightly worse as the distribution of gets more heavy-tailed or more skewed. For the comparison between BIC1 and BIC2, it can be seen that the modified BIC (BIC2) selects the correct model in most of the replications when the sample size is as small as , while BIC1 has comparable performance when the sample size is as large as . Overall, BIC2 has better performance in model selection than that of BIC1, especially for small and moderate samples. This indicates the necessity of the modified BIC in finite samples.

6.3 Asymmetry tests

The third experiment examines the empirical size and power of the proposed asymmetry test statistics , and . The data are generated from

where with and being the sample size, and the innovations are defined as in the first experiment. The null hypothesis of the asymmetry test is , so that the case of corresponds to the size of the tests, the cases of correspond to the local power. Table 3 reports the empirical sizes of three tests at the significance level with and 2000. From this table, we can see that, all tests have accurate sizes when the sample size is large. In addition, and are slightly oversized, especially when the sample size is small.

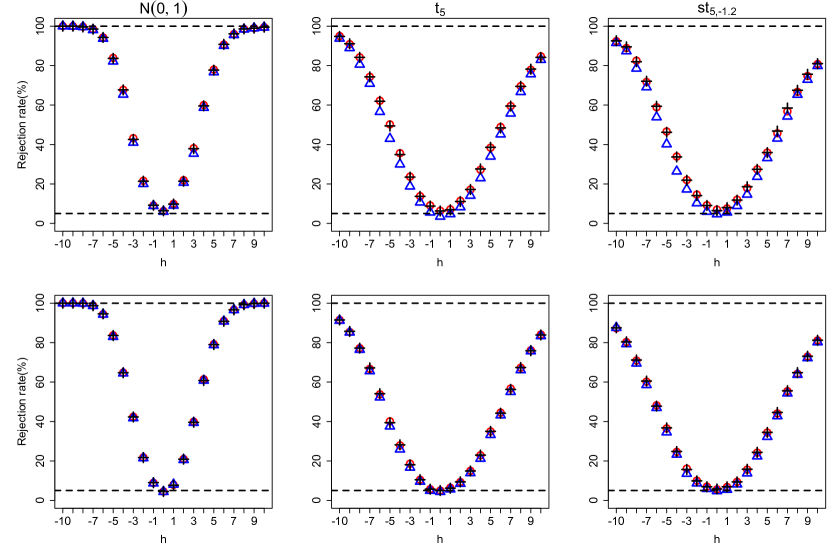

We next compare the local power of all three tests in finite samples at significance level. Figure 2 shows the empirical power of three tests for and 2000. We have the following findings. First, the local powers of and are very similar, and they are slightly higher than that of when the sample size is small (i.e. ), especially when is not normal or is not large. Second, the local power of three tests is close to each other when the sample size is large (i.e. ), which is consistent to the theoretical comparison in Theorem 6 for . Finally, the local power for all three tests gets smaller as the innovations become more heavy-tailed or more skewed. In addition, we also conduct simulation studies for the data generating process with , the general findings are unchanged for the empirical size and power.

6.4 Portmanteau test

In the fourth experiment, we study the proposed mixed portmanteau test . The data are generated from

where the innovations are defined as in the first experiment. We fit an asymmetric linear DAR model with using the same method as in Section 3.1, so that the case of corresponds to the size of the test, the case of corresponds to misspecifications in the conditional mean, and the case of corresponds to misspecifications in the conditional standard deviation. Two departure levels, 0.1 and 0.3, are considered for all and . Table 4 reports the rejection rates of at significance level based on 1000 replications, for sample size and . We have the following findings. First, all sizes are close to the nominal level as the sample size increases, and most powers improve as or the departure level increases. Second, is more powerful in detecting the misspecification in the conditional mean () than that in the conditional standard deviation (, ). Finally, the performance of gets worse as the innovation distribution becomes more heavy-tailed or more skewed. This finding seems to be consistent with the result in the first experiment that, as the innovation distribution becomes more heavy-tailed or skewed, the estimation performance for all parameters tends to worsen.

7 An empirical example

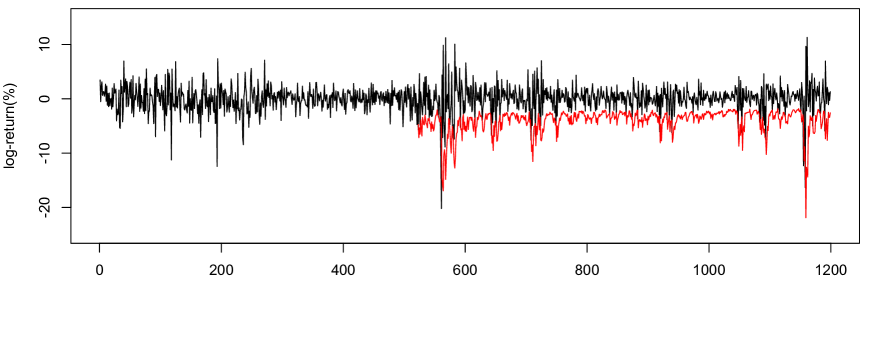

We illustrate the proposed inference tools using the weekly closing prices of S&P500, denoted as , span from January 1998 to December 2020, with 1200 observations in total. The data is downloaded from the website of Yahoo Finance (https://hk.finance.yahoo.com). Let be the log returns in percentage, and denote as the centered log returns in percentage. The time plot of in Figure 3 suggests evident volatility clustering. Table 5 lists summary statistics of , where the sample skewness indicates possible asymmetries in the volatility, and the sample kurtosis implies heavy-tailedness of . Moreover, the ACFs and partial ACFs of and are significant at the first few lags, which suggests that the autocorrelation coexists with the conditional heteroscedasticity in . The above findings motivate us to investigate by our proposed model and inference tools.

Based on , the proposed BIC1 and BIC2 both select . By the quasi-maximum likelihood estimation method in Section 3.1, the fitted model is

| (7.1) |

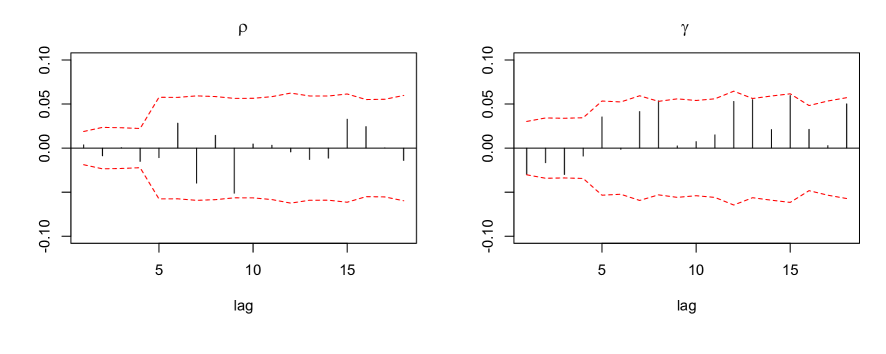

where the subscripts are the standard errors of the estimated coefficients. It can be seen that the coefficients of and are clearly different for , which suggests that there may be asymmetric effects in the conditional volatility of . The Wald, LM and QLR tests in Section 4.1 are conducted for model (7) and all their -values are less than , which corroborates the asymmetric effects in the volatility of . To check the adequacy of the fitted model (7), we perform the mixed portmanteau test in Section 5 for and . The -values of portmanteau tests are and , respectively, which suggests that the fitted model is adequate. In addition, as shown in Figure 4, most of the residual ACFs and fall within their corresponding 95% confidence bounds at the first 18 lags.

Since Value-at-Risk (VaR) is an important risk measure for financial assets, we use the fitted model to forecast the conditional quantile of , i.e. the negative VaR. To examine the forecasting performance, we conduct one-step-ahead predictions using a rolling forecasting procedure with a fixed moving window covering ten years’ data points of size . Specifically, we fit an asymmetric linear DAR model of order four (ALDAR) for each moving window, and compute the forecast of the th conditional quantile of , given by , where and are the predicted conditional mean and standard deviation, respectively, and is the th sample quantile of residuals . Then we move the window forward by one and repeat the above procedure until all data are used. Finally, we obtain 677 one-week-ahead negative VaRs for each . For illustration, the rolling forecasts at are displayed in Figure 3, which indicates that the negative VaRs change accordingly to the volatility of the data.

To compare the forecasting performance of the proposed model with other counterparts, we also perform the rolling forecasting procedure using a linear DAR(4) model (LDAR) and an AR model with the threshold GARCH errors (AR-TGARCH). Note that the AR-TGARCH model can depict the asymmetric effect in volatilities, while the LDAR model ignores the asymmetric effect. For comparison, all these models are fitted by the QMLE, and their VaR forecasts are computed in the same way as for the ALDAR model. To evaluate the forecasting performance of each model, we calculate the empirical coverage rate (ECR), and perform VaR backtests for the VaR forecasts at , 5%, 95% and 99%. Specifically, ECR is calculated as the proportion of observations that fall below the corresponding conditional quantile forecast for the last 677 data points. Two VaR backtests, i.e. the likelihood ratio test for correct conditional coverage (CC) in Christoffersen (1998) and the dynamic quantile (DQ) test in Engle and Manganelli (2004) are employed. Denote the hit by . The null hypothesis of CC test is that, conditional on , are Bernoulli random variables with success probability being . For the DQ test, following Engle and Manganelli (2004), we regress on regressors including a constant, four lagged hits , and the contemporaneous VaR forecast. The null hypothesis of DQ test is that all regression coefficients are zero and the intercept equals to the quantile level . If the null hypothesis of each VaR backtest cannot be rejected, then it indicates that the VaR forecasts are satisfactory.

Table 6 reports ECRs and -values of two VaR backtests for the one-step-ahead forecasts by the fitted ALDAR, LDAR and AR-TGARCH models at the lower and upper 1% and 5% conditional quantiles, i.e. 1% and 5% VaRs for long and short positions. We use backtesting as the primary criterion, and the ECR as the secondary criterion. In terms of backtests, none of the methods performs satisfactorily at , and the proposed ALDAR model performs well at other three quantile levels with -values not less than . However, the LDAR model fails at all levels, and the AR-TGARCH model only performs adequately at with the -values smaller than those of the ALDAR model. For the ECRs, it can be seen that those of the ALDAR model are closest to the nominal quantile levels for upper quantiles. The poor performance of the LDAR model is possibly because it ignores the asymmetric effect, while that of the AR-TGARCH model is perhaps because it is not robust to heavy-tailed data as its QMLE needs . Therefore, we conclude that the proposed ALDAR model outperforms the other two competitors in forecasting VaRs for the S&P500 Index.

8 Conclusion and discussion

This paper proposes the asymmetric linear double AR model which takes into account asymmetric effects for conditional heteroscedastic time series in the presence of a conditional mean structure. The strict stationarity of the new model is derived, and inference tools, including a Gaussian QMLE for estimation and a mixed portmanteau test for diagnosis, are constructed without any moment condition on the data. Based on the QMLE, a BIC and its modified version are proposed for order selection, and simulation results suggest that the modified BIC performs better in small and moderate samples. The Wald, Lagrange multiplier and quasi-likelihood ratio test statistics are constructed to detect asymmetric effects, and it is shown that the Wald and Lagrange multiplier tests are asymptotically equivalent in size and power, while the asymptotics of the quasi-likelihood ratio test become non-standard. The usefulness of the new model is confirmed by our empirical evidence, especially when the data are characterized by skewness and heavy-tailedness which are very common features for financial time series.

The study in this paper can be extended in several directions. First, our model can be extended to allow for asymmetric effects in both the conditional mean and the standard deviation, then the proposed asymmetry tests could adapt to detect the asymmetry from the conditional location and scale separately or jointly. Second, since financial time series can be heavy-tailed such that , it is also of interest to consider more robust estimation methods than Gaussian QMLE, for example, the quasi-maximum exponential likelihood estimation of Zhu and Ling (2011). Third, the joint modeling of conditional mean and volatility in the presence of asymmetric effects for univariate case can be generalized to multivariate case. As a result, a vector asymmetric LDAR model is a natural extention and the related inference tools are worth to investigate. We leave these extensions for future research.

Appendix: Technical proofs

This appendix includes technical details for Theorems 1-7. To show Theorems 2 and 5, Lemmas 1-6 are introduced with proofs. Throughout the appendix, for a vector , the -norm is defined as ; for a matrix or column vector , we define , where denotes the trace of a square matrix.

A.1 Proof of Theorem 1

Proof.

Denote and . Let , , and , where are generated by model (2.1). We begin by showing that is -irreducible.

Let be the class of Borel sets of and be the Lebesgue measure on . Let be the projection map onto the first coordinate, i.e. for . Then, is a homogeneous Markov chain on the state space , with transition probability

where , , , and is the density function of . We can further verify that the -step transition probability of is

| (A.1) |

where and . Observe that, by Assumption 1, the transition density kernel in (A.1) is positive everywhere. As a result, is -irreducible.

We next prove that satisfies Tweedie’s drift criterion (Tweedie, 1983, Theorem 4), i.e., there exists a small set with and a non-negative continuous function such that

| (A.2) |

| (A.3) |

for some constant and . We accomplish the proof in two parts, i.e. Case (i) for and Case (ii) for .

We first consider Case (i) for . It can be verified that

where and for . Note that , and we can then find positive values such that

| (A.4) |

Consider the test function , and we have that

where, from (A.4),

| (A.5) |

Denote , and , where is a positive constant such that as . We can verify that (A.2) and (A.3) hold, i.e. Tweedie’s drift criterion holds. Moreover, is a Feller chain since, for each bounded continuous function , is continuous with respect to , and then is a small set. As a result, by Theorem 4(ii) in Tweedie (1983) and Theorems 1 and 2 in Feigin and Tweedie (1985), is geometrically ergodic with a unique stationary distribution , and

which implies that . This accomplishes the first part.

Next, we consider Case (ii) for . Note that . This together with the multinomial theorem, implies that

where . For positive integers , we have

| (A.6) |

and if ,

| (A.7) |

Then by (A.6) and (A.7), it can be verified that

| (A.8) |

where for . Note that for , by the assumption of Case (ii), we have

As a result, we can find positive values such that (A.4) holds.

Consider the test function as for Case (i). Define as in (A.5). Note that , this together with (A.1), implies that

where as . For any fixed , choose large enough, such that , as . Let , then is a bounded set with . It can be shown that (A.2) and (A.3) hold, i.e. Tweedie’s drift criterion is verified. Similar to the proof of Case (i), we can show that, there exists a strictly stationary solution to model (2.1), and this solution is unique and geometrically ergodic with . This accomplishes the second part.

∎

A.2 Proof of Theorem 2

To show Theorem 2, we introduce the following lemmas.

Proof.

Recall that and , where and with and . It can be derived that

We first show (i). By Assumption 2, there exists a constant such that . Denote and , i.e. if and if . By the inequality and Jensen’s inequality, we have

This together with Assumption 4 and , implies that

| (A.9) |

Note that is independent of , and , then by Assumption 4 and inequality, it can be verified that

| (A.10) |

By (A.2), (A.2) and the triangle inequality, we have

Thus, (i) is verified. Similarly, we can show that (ii) and (iii) hold. ∎

Proof.

We first prove that

| (A.11) |

where and are and constant vectors, respectively. If and , without loss of generality, we can assume , thus . Recall that and is independent of , we have

| (A.12) |

which is a contradiction with , thus .

Denote , if and , without loss of generality, we assume , then . On the one hand, if , then , similar to (A.12), we can find a contradiction with . On the other hand, if , i.e. , note that , then we have

| (A.13) |

Without loss of generality, we assume . Denote

Since the density function of is positive everywhere on by Assumption 3, by a simple transformation on (A.2), we can obtain that , which contradicts the condition that . Thus, if . Hence, (A.11) is verified.

As for (A.11), we can show that

| (A.14) |

The second term in (A.2) reaches its maximum at zero, and this happens if and only if , which holds if and only if by (A.11). For the first term in (A.2), denote where and . We can prove that reaches its maximum at , i.e. , which holds if and only if by (A.11). Therefore, is uniquely maximized at . ∎

Lemma 4.

and are finite and positive definite;

.

Proof.

We first show (i). Recall that , ,

By Assumptions 2 and 4, for some constant , we have

Thus, is finite, and if such that , then is also finite.

Let , where and are arbitrary non-zero constant vectors. It follows that

| (A.15) |

By Cauchy-Schwarz inequality, , and the equality holds when for any , which is equivalent to . Since is positive definite, we have and thus , i.e. is positive definite. Moreover, by (A.11), it can be verified that

As a result, is positive definite. Hence, (i) holds.

Note that . By the Martingale Central Limit Theorem and the Cramér-Wold device, we can show that (ii) holds. ∎

A.3 Technical details for model selection

In this section, notations , , and are employed to emphasize their dependence on the order . We first derive the proposed BICs in Section 3.2, and then establish their consistency in order selection.

A.3.1 Derivation of BICs

Denote as the observed data and as its marginal distribution. Let be a discrete prior over the order set , and be a prior on given the order . Moreover, denote as the likelihood of under the model with order , then we have . By Bayes’ Theorem, the joint posterior of and can be written as

Then the posterior probability of is given by

To maximize , it is equivalent to minimize as below

Consider the noninformative priors for and such that and . Since is constant with respect to , then we have

| (A.17) |

To approximate the above term, we take a second-order Taylor’s expansion of the log-likelihood about , together with , then it follows that

This implies that

Similar to the Laplace method, we then have the following approximation for the integral

This together with (A.17) and , implies that

As , ignoring the terms in the above approximation, we obtain that

Motivated by the above approximations, the BICs are defined as in (3.4) and (3.5).

A.3.2 Proof of Theorem 3

Proof.

Denote the true order of model (2.1) as . Note that , and is bounded as . It suffices to show that, for any ,

| (A.18) |

We first consider the case with , i.e. the model is overfitted. Note that the model with order corresponds to a bigger model, and it holds that

Denote . Similar to the proof of Theorem 3, we can show that . By Taylor’s expansion and Slutsky’s theorem, it can be shown that

| (A.19) |

Similarly, it can be verified that . As a result,

Hence, we have

as . Therefore, (A.18) holds for .

We next consider the case with , i.e. the model is underfitted. Let . Similar to the proof of Theorem 3 and (A.19), we can verify that and

Since the model with order corresponds to a smaller model, we have for some positive constant . By ergodic theorem, we have . Thus it holds that

Therefore, we have

This together with , implies that

as . Hence, (A.18) holds for . The proof is accomplished. ∎

A.4 Proof of Theorem 4

Proof.

The hypotheses of the asymmetry test are , where is the matrix, is the true parameter vector and is a -dimensional zero vector. By Lemma 2, under , we have

| (A.20) |

We show the null distributions of the Wald, LM and QLR test statistics, respectively.

(i) Wald test

By (A.16), we have

Then under , by Lemma 4, it follows that

where . Then by Slutsky’s theorem, under , it holds that

This completes the first part.

(ii) Lagrange Multiplier (LM) test

Let be a vector. Under , the lagrangian can be formulated as

Denote , where is the restricted QMLE under , and is the lagrangian multiplier. Taking the first derivatives of with respect to and at respectively, we have

| (A.21) |

Under , by Taylor’s expansion and (A.20), it holds that

This together with (A.16) and (A.21), implies that

| (A.22) |

Under , note that by (A.21) and , then by Theorem 2, we have

Recall that . Multiplying both sides of (A.22) by , we have

| (A.23) |

This together with (A.22) and Slutsky’s theorem, implies that, under ,

This completes the second part.

(iii) Quasi-likelihood ratio (QLR) test

A.5 Proof of Theorem 5

Recall that the time series are generated by

where and with and . Moreover,

To prove Theorem 5, the following two lemmas are required.

Lemma 5.

Let be a mean-zero triangular array of -mixing sequences that are -bounded for some , and for . Then is a uniformly integrable -mixing. Furthermore, as , and hence in probability as .

Proof.

See Example 4 in Section 3 of Andrews (1988). ∎

Lemma 6.

Proof.

Proof of Theorem 5.

Below we will show that, as , (i) and (ii) , where and .

(i) Similar to the proof of Lemma 1, by Assumptions 4 and 5, we can prove that

| (A.24) |

By Assumption 5, is geometrically ergodic, and hence -mixing. By Theorem 3.49 of White (2001), it follows that is -mixing. Then, by Lemma 5 with , we have

| (A.25) |

Furthermore, the stationarity of ensures that

and the dominated convergence theorem entails that

These together with (A.25) imply that, for any ,

| (A.26) |

Moreover, by similar arguments as for Lemma 1(ii), we can prove that

As a result, Assumption 3A in Nelson (1991) holds. Then by (A.26) and Theorem 2.1 of Nelson (1991), we have

| (A.27) |

Finally, since attains its global maximum at by Lemma 3, (i) holds by (A.27) and Theorem 4.1.1 in Amemiya (1985).

(ii) By Taylor’s expansion, we have

where is between and . Moreover, by the Martingale Central Limit Theorem and the Cramér-Wold device, together with Lemma 6(ii), we can show that, as ,

Recall that . Then by (i) and Lemma 6(i), we have

The proof of this theorem is accomplished. ∎

A.6 Proof of Theorem 6

Proof.

Denote , where

Clearly, , , , , , and .

Based on Theorem 5, we show the limit distributions of the Wald, LM and QLR test statistics under , respectively.

(i) Wald test

Since , under , by Theorem 5, we have

| (A.28) |

Then by Slutsky’s theorem and , it holds that

where .

(ii) Lagrange Multiplier test

Similar to the proof of Theorem 4(ii) and Theorem 5, we can show that

| (A.29) |

as , where is the restricted QMLE under such that . By Theorem 5, if holds, then we have as . Recall that . Therefore, by Slutsky’s theorem and (A.28), we have

(iii) Quasi-likelihood ratio test

Similar to the proof of Theorem 4(iii) and Theorem 5, together with the facts that , , (A.28) and (A.29), it can be verified that

as , where , is an orthogonal matrix such that with being the -th eigenvalue of , is the -th component of , and ’s are independent random variables following the distribution for . The proof is completed. ∎

A.7 Proof of Theorem 7

Proof.

Denote . Recall that , , and . When model (2.1) is correctly specified, by the ergodic theorem and the dominated convergence theorem, it can be shown that, as ,

Hence, it follows that

| (A.30) |

where and with and . It can be verified that

where ,

Note that and . Then by Taylor’s expansion and the ergodic theorem, we have

| (A.31) |

Similarly, it can be shown that

| (A.32) |

As a result, we have

| (A.33) |

Similar to the proof of (A.7), we can show that

Note that . Similar to the proof of (A.7), we have and . Therefore, it holds that

| (A.34) |

Combining (A.33) and (A.34), together with (A.16) and (A.30), we can obtain that

| (A.35) |

where and

Then by the martingale central limit theorem and the Cramér-Wold device, we have

where . The proof of this theorem is accomplished. ∎

References

- Amemiya (1985) Amemiya, T. (1985). Advanced econometrics. Harvard University Press.

- Andrews (1988) Andrews, D. W. (1988). Laws of large numbers for dependent non-identically distributed random variables. Econometric theory 4, 458–467.

- Bertsekas (1982) Bertsekas, D. P. (1982). Projected newton methods for optimization problems with simple constraints. SIAM Journal on control and Optimization 20(2), 221–246.

- Black (1976) Black, F. (1976). Studies of stock market volatility changes. 1976 Proceedings of the American Statistical Association Bisiness and Economic Statistics Section.

- Bollerslev (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroscedasticity. Journal of Econometrics 31, 307–327.

- Christoffersen (1998) Christoffersen, P. F. (1998). Evaluating interval forecasts. International economic review, 841–862.

- Engle (1982) Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50, 987–1007.

- Engle and Manganelli (2004) Engle, R. F. and S. Manganelli (2004). CAViaR: conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics 22, 367–381.

- Engle and Ng (1993) Engle, R. F. and V. K. Ng (1993). Measuring and testing the impact of news on volatility. The journal of finance 48, 1749–1778.

- Feigin and Tweedie (1985) Feigin, P. D. and R. L. Tweedie (1985). Random coefficient autoregressive processes: a markov chain analysis of stationarity and finiteness of moments. Journal of Time Series Analysis 6, 1–14.

- Francq and Zakoian (2004) Francq, C. and J. M. Zakoian (2004). Maximum likelihood estimation of pure GARCH and ARMA-GARCH processes. Bernoulli 10, 605–637.

- Francq and Zakoian (2012) Francq, C. and J. M. Zakoian (2012). QMLE estimation of a class of multivariate asymmetric GARCH models. Econometric Theory, 179–206.

- Francq and Zakoian (2013) Francq, C. and J. M. Zakoian (2013). Inference in nonstationary asymmetric garch models. The Annals of Statistics 41, 1970–1998.

- Francq and Zakoian (2019) Francq, C. and J. M. Zakoian (2019). Garch models: structure, statistical inference and financial applications, 2nd edition. Wiley.

- Imhof (1961) Imhof, J. P. (1961). Computing the distribution of quadratic forms in normal variables. Biometrika 48, 419–426.

- Jiang et al. (2020) Jiang, F., D. Li, and K. Zhu (2020). Non-standard inference for augmented double autoregressive models with null volatility coefficients. Journal of Econometrics 215, 165–183.

- Kuester et al. (2006) Kuester, K., S. Mittnik, and M. Paolella (2006). Value-at-risk prediction: a comparison of alternative strategies. Journal of Financial Econometrics 4, 53–89.

- Li et al. (2016) Li, D., S. Ling, and R. Zhang (2016). On a threshold double autoregressive model. Journal of Business and Economic Statistics 34, 68–80.

- Li and Li (2005) Li, G. and W. K. Li (2005). Diagnostic checking for time series models with conditional heteroscedasticity estimated by the least absolute deviation approach. Biometrika 92, 691–701.

- Li and Li (2008) Li, G. and W. K. Li (2008). Testing for threshold moving average with conditional heteroscedasticity. Statistica Sinica 18, 647–665.

- Li et al. (2017) Li, G., Q. Zhu, Z. Liu, and W. K. Li (2017). On mixture double autoregressive time series models. Journal of Business and Economic Statistics 35, 306–317.

- Li et al. (2002) Li, W. K., S. Ling, and M. McAleer (2002). Recent theoretical results for time series models with GARCH errors. Journal of Economic Surveys 16, 245–269.

- Ling (2005) Ling, S. (2005). Self-weighted least absolute deviation estimation for infinite variance autoregressive models. Journal of the Royal Statistical Society: Series B 67, 381–393.

- Ling (2007) Ling, S. (2007). A double AR(p) model: structure and estimation. Statistica Sinica 17, 161–175.

- Ling and McAleer (2003) Ling, S. and M. McAleer (2003). Asymptotic theory for a vector ARMA–GARCH model. Econometric Theory 19, 280–310.

- Linton and Mammen (2005) Linton, O. and E. Mammen (2005). Estimating semiparametric ARCH () models by kernel smoothing methods. Econometrica 73, 771–836.

- Liu et al. (2020) Liu, H., S. Tan, and Q. Zhu (2020). Quasi-maximum likelihood inference for linear double autoregressive models. arXiv:2010.06103.

- Liu et al. (2009) Liu, H., Y. Tang, and H. H. Zhang (2009). A new chi-square approximation to the distribution of non-negative definite quadratic forms in non-central normal variables. Computational Statistics and Data Analysis 53, 853–856.

- Ljung and Box (1978) Ljung, G. M. and G. E. P. Box (1978). On a measure of lack of fit in time series models. Biometrika 65, 297–303.

- Lv and Liu (2014) Lv, J. and J. S. Liu (2014). Model selection principles in misspecified models. Journal of the Royal Statistical Society, Series B 76, 141–167.

- MaCurdy (1981) MaCurdy, T. E. (1981). Asymptotic properties of quasi-maximum likelihood estimators and test statistics. Technical report, National Bureau of Economic Research.

- Nelson (1991) Nelson, D. B. (1991). Conditional heteroskedasticity in asset returns: a new approach. Econometrica 59, 347–370.

- Pan et al. (2008) Pan, J., H. Wang, and H. Tong (2008). Estimation and tests for power-transformed and threshold GARCH models. Journal of Econometrics 142, 352–378.

- Pearson (1959) Pearson, E. S. (1959). Note on an approximation to the distribution of non-central . Biometrika 46, 364.

- Rabemananjara and Zakoian (1993) Rabemananjara, R. and J. M. Zakoian (1993). Threshold ARCH models and asymmetries in volatility. Journal of applied econometrics 8, 31–49.

- Taylor (2008) Taylor, S. J. (2008). Modelling financial time series. New York: World Scientific.

- Tweedie (1983) Tweedie, R. L. (1983). Criteria for rates of convergence of Markov chains, with application to queueing and storage theory. In J. F. C. Kingman and G. E. H. Reuter (Eds.), Probability, Statistics and Analysis, pp. 260–276. Cambridge: Cambridge University Press.

- van der Vaart (2000) van der Vaart, A. W. (2000). Asymptotic statistics. Cambridge university press.

- White (2001) White, H. (2001, 2001). Asymptotic theory for econometricians. Academic Press.

- Wong and Ling (2005) Wong, H. and S. Ling (2005). Mixed portmanteau tests for time-series models. Journal of Time Series Analysis 26, 569–579.

- Zakoian (1994) Zakoian, J. M. (1994). Threshold heteroskedastic models. Journal of Economic Dynamics and Control 18, 931–955.

- Zhu and Ling (2011) Zhu, K. and S. Ling (2011). Global self-weighted and local quasi-maximum exponential likelihood estimators for ARMA-GARCH/IGARCH models. The Annals of Statistics 39, 2131–2163.

- Zhu et al. (2018) Zhu, Q., Y. Zheng, and G. Li (2018). Linear double autoregression. Journal of Econometrics 207, 162–174.

| Bias | ESD | ASD | Bias | ESD | ASD | Bias | ESD | ASD | ||

|---|---|---|---|---|---|---|---|---|---|---|

| -0.024 | 0.515 | 0.520 | -0.022 | 0.570 | 0.548 | -0.024 | 0.568 | 0.554 | ||

| 0.022 | 0.371 | 0.369 | -0.019 | 0.378 | 0.392 | -0.001 | 0.401 | 0.395 | ||

| -0.022 | 0.257 | 0.262 | -0.004 | 0.274 | 0.278 | -0.014 | 0.291 | 0.280 | ||

| 0.040 | 0.271 | 0.264 | 0.017 | 0.426 | 0.386 | 0.009 | 0.427 | 0.403 | ||

| 0.016 | 0.193 | 0.187 | 0.016 | 0.324 | 0.290 | 0.008 | 0.333 | 0.311 | ||

| 0.010 | 0.129 | 0.132 | -0.001 | 0.214 | 0.213 | -0.003 | 0.231 | 0.223 | ||

| -0.088 | 0.640 | 0.587 | -0.013 | 1.049 | 0.957 | -0.039 | 1.191 | 1.031 | ||

| -0.051 | 0.418 | 0.416 | -0.006 | 0.819 | 0.724 | -0.022 | 0.860 | 0.793 | ||

| -0.020 | 0.295 | 0.295 | 0.001 | 0.565 | 0.534 | -0.008 | 0.619 | 0.570 | ||

| -0.147 | 0.736 | 0.699 | -0.109 | 1.262 | 1.145 | -0.156 | 1.274 | 1.182 | ||

| -0.045 | 0.509 | 0.498 | -0.059 | 0.896 | 0.860 | -0.075 | 0.962 | 0.914 | ||

| -0.037 | 0.352 | 0.352 | -0.037 | 0.687 | 0.636 | -0.049 | 0.725 | 0.660 | ||

| Under | Exact | Over | Under | Exact | Over | Under | Exact | Over | ||

|---|---|---|---|---|---|---|---|---|---|---|

| BIC1 | 200 | 0 | 49.9 | 50.1 | 0.3 | 55.2 | 44.5 | 0.6 | 53.6 | 45.8 |

| 500 | 0.1 | 94.7 | 5.2 | 2.1 | 91.4 | 6.5 | 2.2 | 91.1 | 6.7 | |

| 1000 | 0 | 100 | 0 | 1.8 | 98.1 | 0.1 | 2.0 | 98.0 | 0 | |

| BIC2 | 200 | 1.1 | 89.8 | 9.1 | 2.7 | 88.3 | 9.0 | 3.8 | 86.6 | 9.6 |

| 500 | 0.4 | 99.5 | 0.1 | 5.1 | 94.6 | 0.3 | 5.4 | 93.6 | 0.1 | |

| 1000 | 0 | 100 | 0 | 4.4 | 95.6 | 0 | 6.4 | 93.6 | 0 | |

| 0.062 | 0.054 | 0.061 | 0.065 | 0.038 | 0.063 | 0.061 | 0.043 | 0.060 | |

| 0.061 | 0.058 | 0.059 | 0.056 | 0.041 | 0.058 | 0.060 | 0.040 | 0.059 | |

| 0.048 | 0.047 | 0.047 | 0.052 | 0.047 | 0.053 | 0.053 | 0.048 | 0.054 | |

| 500 | 1000 | 2000 | 500 | 1000 | 2000 | 500 | 1000 | 2000 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.0 | 0.0 | 0.059 | 0.057 | 0.050 | 0.067 | 0.062 | 0.057 | 0.061 | 0.058 | 0.057 |

| 0.1 | 0.0 | 0.214 | 0.471 | 0.855 | 0.240 | 0.440 | 0.806 | 0.222 | 0.433 | 0.827 |

| 0.3 | 0.0 | 0.997 | 1.000 | 1.000 | 0.994 | 1.000 | 1.000 | 0.999 | 1.000 | 1.000 |

| 0.0 | 0.1 | 0.085 | 0.201 | 0.455 | 0.072 | 0.120 | 0.276 | 0.076 | 0.125 | 0.264 |

| 0.0 | 0.3 | 0.655 | 0.989 | 1.000 | 0.428 | 0.862 | 0.997 | 0.418 | 0.886 | 0.999 |

| Mean | Median | Std.Dev. | Skewness | Kurtosis | Min | Max |

| 0.00 | 0.12 | 2.53 | -0.90 | 7.17 | -20.20 | 11.30 |

| ECR | CC | DQ | ECR | CC | DQ | ECR | CC | DQ | ECR | CC | DQ | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| M1 | 1.48 | 0.16 | 0.10 | 5.76 | 0.58 | 0.89 | 94.68 | 0.93 | 0.98 | 98.82 | 0.82 | 0.96 |

| M2 | 3.54 | 0.00 | 0.00 | 10.04 | 0.00 | 0.00 | 88.18 | 0.00 | 0.00 | 93.80 | 0.00 | 0.00 |

| M3 | 1.33 | 0.19 | 0.06 | 5.02 | 0.26 | 0.33 | 94.68 | 0.35 | 0.06 | 98.22 | 0.15 | 0.02 |