A stochastic control problem with linearly bounded control rates in a Brownian model

Abstract.

Aiming for more realistic optimal dividend policies, we consider a stochastic control problem with linearly bounded control rates using a performance function given by the expected present value of dividend payments made up to ruin. In a Brownian model, we prove the optimality of a member of a new family of control strategies called delayed linear control strategies, for which the controlled process is a refracted diffusion process. For some parameters specifications, we retrieve the strategy initially proposed in [avanzi-wong_2012] to regularize dividend payments, which is more consistent with actual practice.

Key words and phrases:

Stochastic control, linear strategies, dividend payments, Brownian motion, Ornstein-Uhlenbeck process.1. Introduction and main result

In this paper, we consider an optimal stochastic control problem with absolutely continuous and linearly bounded control strategies in a Brownian model. Our problem is a version of de Finetti’s dividend problem in which payment/control strategies can be at most a (fixed) fraction of the current wealth/state. For this problem, an optimal strategy is formed by a delayed linear control strategy. Loosely speaking, for such a strategy, no dividends are paid below a barrier and level-dependent dividend payments are made when the process is above that barrier, allowing for more regular dividend payments over time. As the underlying state process is a Brownian motion, in order to solve this stochastic control problem, we study a specific refracted diffusion process, i.e., a dynamic alternating between a Brownian motion with drift and an Ornstein-Uhlenbeck process.

1.1. Model and problem formulation

On a filtered probability space , let be a Brownian motion with drift, i.e.

| (1) |

where and , and where is a standard Brownian motion. Using the language of ruin theory, is the (uncontrolled) surplus process.

A dividend strategy is represented by a non-decreasing, left-continuous and adapted stochastic process , where represents the cumulative amount of dividends paid up to time under this strategy. For a given strategy , the corresponding controlled surplus process is defined by .

While de Finetti’s classical dividend problem is a singular stochastic control problem, we are interested in an adaptation where the admissible strategies are absolutely continuous with a linearly bounded rate.

Definition 1.1 (Admissible strategies).

Fix a constant . A strategy is said to be admissible if it is absolutely continuous and linearly bounded, i.e., , with , for all . The set of admissible dividend strategies will be denoted by .

Thus, for an admissible strategy , we have

For a given discounting rate , the value/performance function associated to an admissible strategy and initial value is given by

where . Note that for all . For notational simplicity, but without loss of generality, we have chosen the ruin level to be , as it is often the case in ruin theory when dealing with space-homogeneous surplus processes.

The goal of this stochastic control problem is to find the optimal value function defined by

and, if it exists, an optimal strategy such that

for all .

1.2. Main result

As alluded to above, the optimal control strategy is of bang-bang type, i.e., dividends are either paid out at the maximal surplus-dependent rate or nothing is paid, depending on the value of the controlled process. Mathematically, let us define the following refracted diffusion process: for fixed , let be given by

| (2) |

We prove the existence of a strong solution to this stochastic differential equation in Appendix A. This process is the controlled process associated to the (admissible) control strategy , which consists of paying out at the maximal surplus-dependent rate when the controlled process is above level and pay nothing below . This control strategy will be denoted by and called a delayed linear control strategy at level with rate , when , and simply a linear control strategy with rate , when . In both cases, it is an admissible strategy, i.e., for any .

Define

| (3) |

where the function is defined in (9). Note that depends on both the control problem parameters and and the model parameters and . Define also as the (unique) root of Equation (10); see below.

Here is an explicit solution to the control problem:

Theorem 1.2.

Fix and . The following hold:

-

(i)

If , then the linear control strategy with rate is optimal.

-

(ii)

If , then the delayed linear control strategy at level with rate is optimal.

1.3. Related literature

If a delayed linear control strategy at level with rate is implemented, then dividends are paid continuously only when the process is above level , according to an Ornstein-Uhlenbeck process with mean-reverting level . In other words, when , we have to wait for sufficient capital before paying out dividends according to this linear strategy. If the linear strategy with rate is implemented, i.e., when , then dividends are paid without interruption up to the time of ruin, according to an Ornstein-Uhlenbeck process with mean-reverting level . This last strategy is the one initally proposed in [avanzi-wong_2012] to regularize dividend payments; it is also studied in [albrecher-cani_2017] for a compound Poisson process with drift. In Section 6 of [avanzi-wong_2012], the authors hinted at delayed linear control strategies. In some sense, delaying dividend payments brings additional safety by avoiding payments when the process is close to the ruin level. Theorem 1.2 tells us that, for our control problem, either the optimal strategy is a linear control strategy, as studied in [avanzi-wong_2012], or it is a member of the family of delayed linear control strategies. In the latter case, Proposition 2.2 tells us how to find the optimal level .

Note that our problem has similarities with another variation on de Finetti’s optimal dividends problem, in which admissible strategies have a bounded rate, i.e., , for all , for a fixed constant ; see, e.g., [jeanblanc-shiryaev_1995]. However, for that problem, the optimal control process is a two-valued Brownian motion with drift, also called a refracted Brownian motion with drift. In the classical de Finetti’s control problem, admissible strategies are not necessarily absolutely continuous nor bounded. For the classical problem, the optimal control process is a reflected Brownian motion with drift and the optimal reflection level is known to be

| (4) |

Intuitively, in our problem, if becomes large, then we should get closer to the classical problem.

The rest of the paper is organized as follows. In Section 2, we provide background material on Ornstein-Uhlenbeck diffusion processes, we compute the value function of an arbitrary (delayed) linear control strategy and then we find the (candidate) optimal barrier level . In Section 3, we give a verification lemma for this control problem and prove Theorem 1.2. Finally, Section 4 aims at giving a second look at the main results with a short discussion and numerical illustrations. More technical material is provided in the appendices, including a proof for the existence of a refracted Ornstein-Uhlenbeck diffusion process and ordinary differential equations related to the control problem.

2. Delayed linear control strategies

Before computing the value function of an arbitrary linear control strategy and then finding the optimal barrier level, let us recall some results about Ornstein-Uhlenbeck diffusion processes.

2.1. Preliminaries on Ornstein-Uhlenbeck diffusion processes

First, let us recall some results on first-passage problems for the Brownian motion with drift , given in (1), and the Ornstein-Uhlenbeck diffusion process given by

| (5) |

where . Clearly, if , then . In what follows, we will use the following notation: the law of when starting from is denoted by and the corresponding expected value operator by . Define the following first-passage stopping times: for , let .

In what follows, we assume . First, we consider the case , i.e. the case when is a Brownian motion with drift. It is known (see, e.g., [kyprianou_2014]) that, for ,

| (6) |

where, for ,

| (7) |

and, for , . It is known that is convex.

Now, we consider the case , i.e., the case when is an Ornstein-Uhlenbeck diffusion process. It is known (see, e.g., [alili-et-al_2005] and references therein) that is a recurrent diffusion, so is finite, almost surely. If and , then, for ,

where is the parabolic cylinder function defined, for , by

We see that is increasing and convex.

Consequently, for and , we can deduce that, for ,

| (8) |

where

| (9) |

It is easy to verify that is convex.

For more analytical properties of and , see Appendix B.

2.2. Value function and optimal barrier level

Fix and . Recall that, for an arbitrary , the process is the controlled process associated to the delayed linear strategy . This refracted diffusion process is the solution to the SDE in (2), which we recall here:

Denote the ruin time of this process by . Note that, if , then has the same law as , where is the Ornstein-Uhlenbeck process defined in (5).

Denote the value function associated to by

Proposition 2.1.

For , we have

where

Proof.

Fix . First assume that . By the strong Markov property, we have

where we used the identity in (6). Now, if we assume that , then by the strong Markov property we have

where, using the identity in (8) and using the strong Markov property one last time (as in [avanzi-wong_2012]),

It is well known that, for ,

so we have

Consequently

To compute , we will use approximations of the delayed linear strategy at level . Fix and let us implement the following strategy: when the (controlled) process reaches , then dividends are paid continuously at rate until the controlled process goes back to ; dividend payments resume when the controlled process reaches again. Denote this strategy by and its value function by . Clearly, and thus .

As for above, we have the following decompositions:

and

Solving for , we get

Since

dividing by and taking the limit when , we get

and

Putting the pieces together, we finally get

Similarly, for a fixed , we can implement the following strategy: wait until the (controlled) process reaches before paying dividends at rate and do so until the controlled process goes back to ; dividend payments resume when the controlled process reaches again. Denote this strategy by and its value function by . Clearly, and thus .

It easy to verify that . The result follows after algebraic manipulations. ∎

Remark 2.1.

Note that, if , then the expression just obtained for is in principle the same as the one obtained in [avanzi-wong_2012].

Note also that, if , then a direct computation shows that and . In other words, the continuous and the smooth pasting conditions are verified.

Remark 2.2.

The function plays a fundamental role in de Finetti’s classical problem. It is the value function, when starting from level , of a barrier control strategy at level . As mentioned above, in that problem, the optimal barrier level is given by as defined in (4).

We now want to find the best delayed linear strategy within the sub-class of delayed linear strategies , i.e., we want to find such that outperforms any other . For analytical reasons, namely to be able to apply Ito’s formula, the optimal barrier level should be such that . In this direction, using identities from Appendix B, let us define our candidate for the optimal barrier level : it is the value of such that

| (10) |

Proposition 2.2.

If , then there exists a unique solution to Equation (10).

Proof.

First, note that Equation (10) is equivalent to

| (11) |

Set , with

Elementary algebraic manipulations lead to

From the properties of the hyperbolic cotangent function, we deduce that is increasing on . Note also that , where is given in (4). In other words, is an increasing function crossing zero at , while is a decreasing function crossing zero at . Finally, we see that .

On the other hand, we can verify that, for all ,

| (12) |

thanks to the following identities: and

where . The second identity can be verified easily using integration by parts.

Under our assumptions, . By the intermediate value theorem, since , together with the inequality in (12), we can deduce that there exists a solution to Equation (10).

Assume there exists two solutions to Equation (10). Then, by the mean value theorem, there exists such that

which is a contradiction. Indeed, on one hand, we have

since on , and on the other hand, we have

for all , since is convex. ∎

3. Verification Lemma and proof of Theorem 1.2

Here is the verification lemma of our stochastic control problem.

Lemma 3.1.

Suppose that is such that is twice continuously differentiable and that, for all ,

| (13) |

In this case, is an optimal strategy for the control problem.

This lemma can be proved using standard arguments. The details are left to the reader.

We now provide a proof for Theorem 1.2, the solution to the control problem. First, note that the Hamilton-Jacobi-Bellman (HJB) equation (13) is equivalent to

Using the expression for , obtained in Proposition 2.1, with the background material provided in Appendix B, we have, for ,

and, for ,

Consequently, satisfies the HJB equation (13) if and only if

Since , we can easily verify that , for all , if and only if

Recall that is convex, so is increasing. Thus, if , then is optimal.

If , then, by Proposition 2.2, the optimal level is given by (10) and thus we can show that

Hence, by Proposition 2.1, the HJB equation is equivalent to

The two inequalities are verified because decreases on and , and because is a convex function.

4. Discussion and numerical illustrations

For practical reasons such as solvency purposes, the company and shareholders might prefer to have , so that for some time, i.e., from the up-crossing of level until the process reaches level , dividend payments do not cancel out all of the capital’s growth. Indeed, we see that, below level , the process behaves like a Brownian motion with constant (positive) drift , and above level , it behaves like an Ornstein-Uhlenbeck process with mean-reverting level .

Therefore, let us now investigate the relationship between levels and . First, it is known that ; see, e.g., [gerber-shiu_2004]. If is relatively small, i.e., if

then the optimal barrier level is less than . If is relatively large, i.e., if

then, from Equation (11), we deduce that if and only if

Remark 4.1.

Note that, if , and , then we do have that .

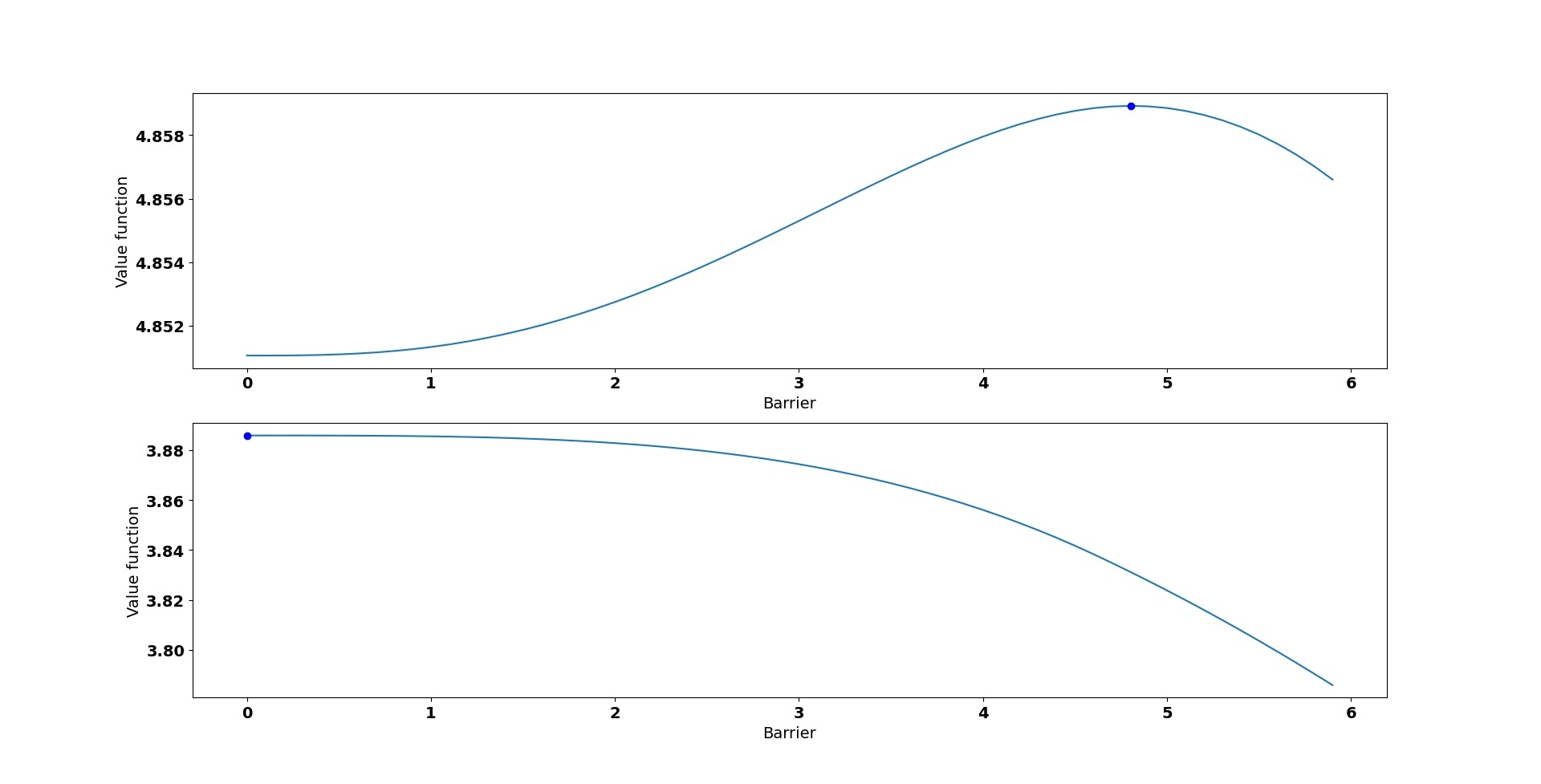

Now, let us further illustrate our main results. First, in Figure 1, we draw the value function for a delayed linear control strategy, as given in Proposition 2.1, as a function of the barrier level , for two sets of parameters. We see that the optimal barrier level, given by the solution to Equation (10), does correspond with the maximum of the function, in both cases. In the top panel, the parameters are such that , which is the condition in Proposition 2.2, for the existence (and uniqueness) of a positive optimal barrier level . In the bottom panel, parameters are such that and we observe that the maximum is indeed attained at zero.

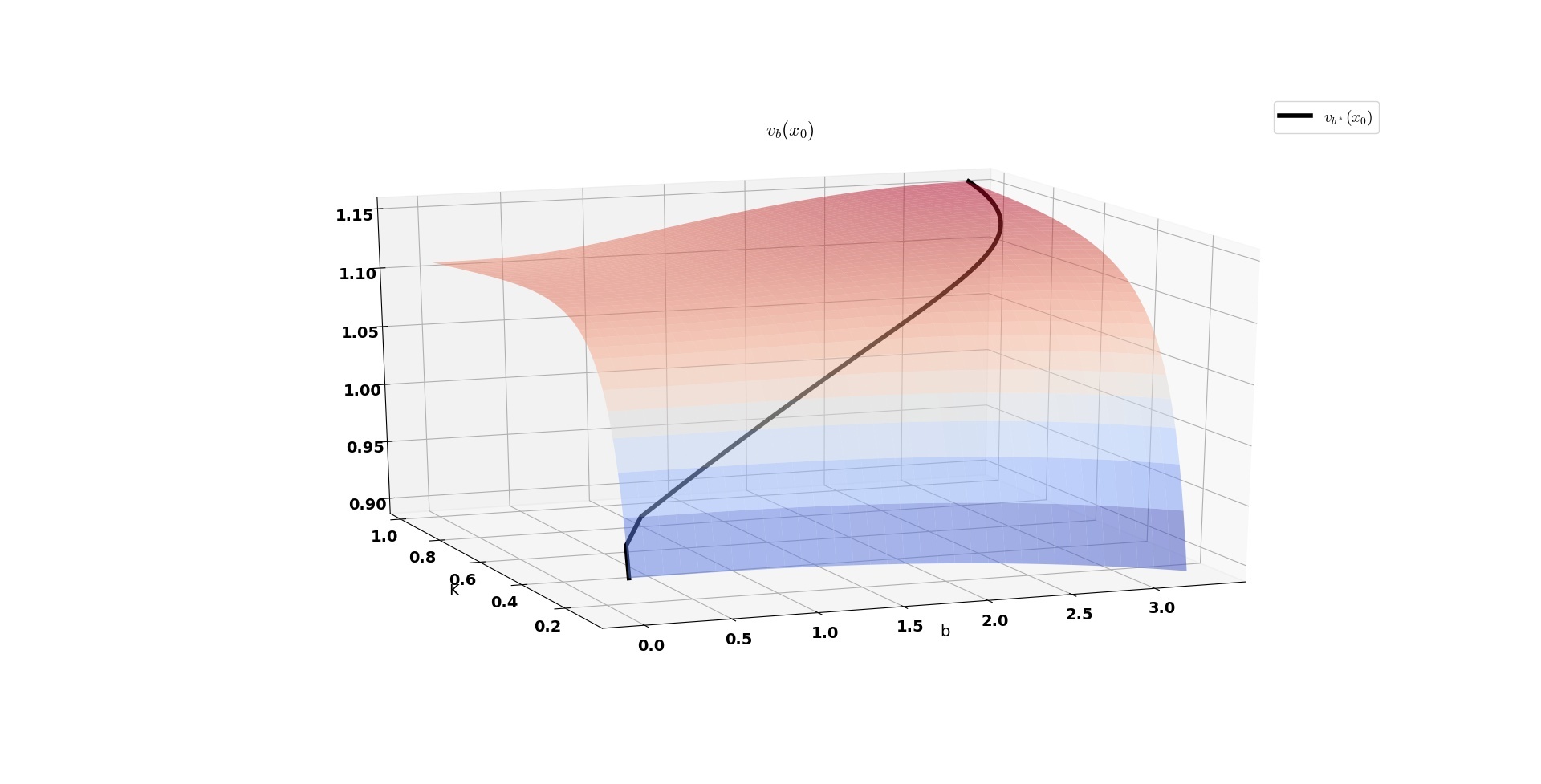

Second, in Figure 2, we draw the value function for a (delayed) linear control strategy as a function of two variables: the barrier level and the parameter . The curve on the surface identifies the value function corresonding to the optimal barrier . For small values of , and we see that the optimal barrier is while for values of such that we see that .

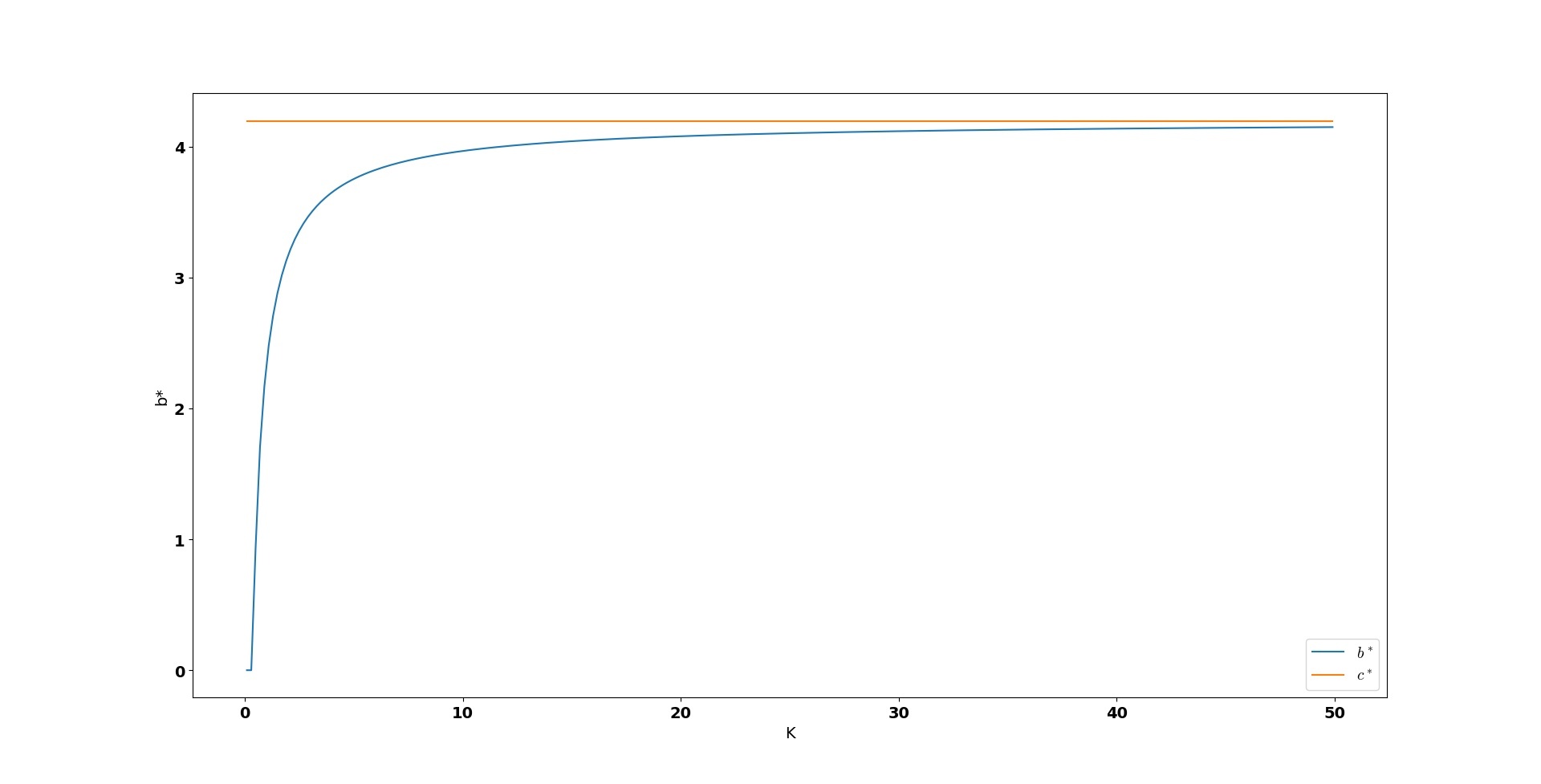

Finally, as alluded to in the introduction, when goes to infinity, one expects to recover de Finetti’s classical control problem, in which the optimal strategy is to pay out all surplus in excess of the barrier level , as given by (4). Recall from Proposition 2.2 that the optimal level in our problem is always less than . In Figure 3, we draw the value of the optimal barrier level as a function of , i.e., . One can see that, for this set of parameters, the optimal barrier level increases to as increases to infinity.

References

Appendix A Existence of the refracted diffusion process given by (2)

It is well known, thanks to Proposition 3.6 in Section 5.3 of [karatzas-shreve_1991], that Equation (2) has a weak solution. However, we can prove the existence of a strong solution by mimicking the proof of Lemma 12 in [Kyprianou/Loeffen_2010].

Fix an arbitrary . For each , let be a sequence of partitions such that and . For , let and, for each , define , if , for . One can show that the sequence of processes converges strongly to , i.e.,

almost surely. Now, define the sequence of processes by: for each , set

Clearly, for each , is a well-defined process. Let us show that is a strong Cauchy sequence and thus converges to a process such that

Define, for all for , , and

Fix . As converges strongly to , there exists an integer such that: if , then . Let us show by contradiction that, for any , we have . Assume it is not verified. Then, from the continuity of and since , there exists such that and such that, for any sufficiently small , there exists such that . Assume that .

Since, for all , and , then and there exists such that for all . Consequently, for each ,

This is a contradiction. A similar argument can be used for the case .

In conclusion, for any , we have and thus, by the triangle inequality, we have .

Appendix B Differential equations and analytical properties

It is well known (and easy to verify) that , defined in (7), is a solution to the following ordinary differential equation (ODE):

Hence, for , we have

We are also interested in the following non-homogeneous ODE:

| (14) |

We are looking for a solution of the form , where is a particular solution and where is a solution of the homogeneous version of (14), that is

| (15) |

On one hand, it is easy to verify that

is a solution to the ODE in (14). On the other hand, from [borodin-salminen_2002], it is known that, for ,

admits

as its increasing solution and its decreasing solution, respectively, where is the parabolic cylinder function defined by: for ,