thmTheorem \newtheoremreplemLemma

Project selection with partially verifiable information††thanks: We are grateful to Laura Doval, Federico Echenique and Amit Goyal for helpful comments and suggestions. We would also like to thank seminar audiences at Caltech and Delhi School of Economics for valuable feedback.

Abstract

We consider a principal agent project selection problem with asymmetric information. There are projects and the principal must select exactly one of them. Each project provides some profit to the principal and some payoff to the agent and these profits and payoffs are the agent’s private information. We consider the principal’s problem of finding an optimal mechanism for two different objectives: maximizing expected profit and maximizing the probability of choosing the most profitable project. Importantly, we assume partial verifiability so that the agent cannot report a project to be more profitable to the principal than it actually is. Under this no-overselling constraint, we characterize the set of implementable mechanisms. Using this characterization, we find that in the case of two projects, the optimal mechanism under both objectives takes the form of a simple cutoff mechanism. The simple structure of the optimal mechanism also allows us to find evidence in support of the well-known ally-principle which says that principal delegates more authority to an agent who shares their preferences.

1 Introduction

Suppose a principal has to chose exactly one of available projects but does not know how profitable they are. There is an agent who is fully informed about these profits but also has its own preference over the projects. The principal would like to use the agent’s information and chose a profitable project. Assuming the principal has commitment power and cannot use transfers to incentivize the agent, we consider the problem of finding the optimal mechanism for the principal in this project selection framework.

Let’s first quickly consider the standard setting where the agent can lie arbitrarily. So for any principal and agent payoff vectors , the agent can report any . Consider any mechanism and suppose its range is . Under this mechanism, the agent will always report a so that its favorite project in defined by is chosen. Thus, the principal can only fix a set and commit to choosing agent’s favorite project in . This means that if the payoffs are i.i.d. across projects, all mechanisms lead to expected payoff for the principle. And the probability of the principal choosing the best project is for any mechanism. Thus, the principle may as well choose a constant mechanism and commitment power doesn’t buy anything for the principal.

An important assumption in the above setting is that the agent can lie arbitrarily. But the agent’s ability to manipulate may be limited if it is required to support its claims with some form of evidence. For instance, if a tech firm wants to a hire a programmer and the hiring committee is biased towards candidates with better social skills, the firm can require the hiring committee to provide certificates that support the reported coding skills of the candidates. Now the hiring committee can still potentially hide certificates and understate the coding ability of an applicant, but it cannot furnish fake certificates and overstate its coding abilities. Thus, by requiring some kind of supporting evidence, the principal can constraint the kind of manipulations that the agent can make.

In this paper, we consider a setting where the agent cannot oversell a project to the principal. That is, the agent cannot say a project is more profitable for the principal than it actually is. So if the true state is , the agent’s message space is . Since the set of manipulations that the principal has to guard against is now smaller, the class of truthful mechanisms is potentially bigger. Note that our message correspondence satisfies the nested range condition () from Green and

Laffont [15] and thus, we can without loss of generality restrict attention to truthful mechanisms.

Under the partial verifiability constraint of no overselling-constraint, we first characterize the class of truthful mechanisms and call them table mechanisms. A table mechanism is defined by an increasing set function which determines the set of projects on the table as a function of the reported profit values . The mechanism then chooses the agent’s favorite project according to the reported from those on the table. Thus, the class of truthful mechanisms is now significantly bigger. We use this characterization to find the optimal mechanism for the principal under two different objectives.

First, we consider the objective of maximizing the expected profit for the principal. For the case of two projects, we show that the optimal table mechanism is a simple cutoff mechanism. In this mechanism, one project is always on the table and the other project is on the table if its reported profit meets a cutoff that depends on the bivariate distribution from which the principal and agent payoffs are drawn for each project. When the payoffs are independent, this cutoff equals the expected profit. We also discuss the well-known ally principle in our framework by considering the case where is bivariate normal. In this case, we find that the optimal cutoff is decreasing in the correlation between the principal and agent payoffs and thus, the principal lends more leeway to an agent who shares their preferences. For the case of projects, we obtain a relatively weak result. Assuming is uniform on , we show that a single cutoff mechanism is optimal in the simple subclass of cutoff mechanisms. Next, we also consider the objective of maximizing the probability of choosing the best project. Again, for the case of two projects, we show that a cutoff mechanism is optimal and when the project payoffs are independent, the optimal cutoff equals the median of the principal’s profit.

1.1 Related literature

Mechanism design has often been used to deal with problems of asymmetric information ( Myerson [25], Myerson and

Satterthwaite [26]). An important theme in the literature on mechanism design is characterizing the set of implementable mechanisms (Gibbard

et al. [14], Satterthwaite [29], Dasgupta

et al. [9], Green and

Laffont [15]). In particular, Green and

Laffont [15] introduce the idea of partially verifiable information in mechanism design and identify a necessary and sufficient condition, called the “Nested Range Condition”, under which the set of implementable mechanisms coincides with the set of truthfully implementable mechanisms (i.e. the revelation principle holds). Later research focuses on identifying implementability conditions in other environments with partially verifiable information; Kartik [19] looks at Nash implementation, Deneckere and

Severinov [10] considers lying with finite costs, Ben-Porath and

Lipman [4] and Singh and

Wittman [32] allow for transfers, and Caragiannis et al. [7] considers probabilistic verification. Some computer scientists have looked at the trade-off between monetary transfers and partial verifiability in terms of implementing social choice functions (Ferraioli

et al. [12], Fotakis

et al. [13]). Our setup belongs to the environment considered by Green and Laffont and satisfies their “Nested Range Condition”. Thus, without loss of generality, we restrict attention to truthfully implementable mechanisms in our analysis.

Our paper contributes to the literature finding optimal or efficient mechanisms in environments with a specific form of partial verifiability (Maggi and

Rodriguez-Clare [22], Lacker and

Weinberg [21], Moore [23], Celik [8]). For instance, Munro

et al. [24] argues using a model in which only some expenditure can be hidden that spouses hiding income and assets from one another is efficient. Deneckere and

Severinov [11] explains the complicated selling practices of real-world monopolists by considering an economy where some agents have limited ability to misrepresent their preferences. This paper considers the partial verifiability constraint of no-overselling and potentially explains the use of cutoff mechanisms in settings that only admit positive evidence which can be hidden but not fabricated.

Our work also relates to the literature studying principal agent project selection problems with different modeling assumptions (Ben-Porath

et al. [2], Mylovanov and

Zapechelnyuk [27], Armstrong and

Vickers [1] and Guo and

Shmaya [16]). Ben-Porath

et al. [2] and Mylovanov and

Zapechelnyuk [27] consider a problem where the principal has to choose one of agents who prefer being chosen and provide some private value to the principal from being chosen. In Ben-Porath

et al. [2], the principal can verify his value from agent at a cost , while Mylovanov and

Zapechelnyuk [27] assumes ex-post verifiability so that the principal can penalize the winner by destroying a certain fraction of the surplus. Armstrong and

Vickers [1] considers a project delegation problem in which the principal can verify characteristics of the chosen project but is uncertain about the set of available projects. These papers find their respective optimal mechanisms for the principal and call them the favored agent mechanism Ben-Porath

et al. [2], shortlisting procedure Mylovanov and

Zapechelnyuk [27], and the threshold rule Armstrong and

Vickers [1]. While these mechanisms have some flavor of the cutoff mechanisms we obtain in this paper, there are important differences in the setup we consider here. Primarily, in their setups, the principal is empowered by ex-post verifiability of the reported values and the ability to use a prohibitively high punishment to deter the agent from telling any lie, whereas in our setup, the agent is constrained in that he cannot oversell, but the principal does not have the power to directly deter the agent from underselling.

The paper proceeds as follows. In section 2, we present the model and definitions. Section 3 characterizes the class of truthful mechanisms. In section 4 and 5, we consider the two different objectives of maximizing expected profit and maximizing probability of choosing the best project for the principal. In section 6, we give some remarks and Section 7 concludes. The more technical proofs are in the appendix.

2 Model

There are two parties: a principal and an agent. The principal has a set of available projects and must choose one of them. Each project leads to payoffs where denotes the profit for the principal and is the utility to the agent. The payoffs are i.i.d. from a bi-variate distribution and this is all the information that the principal has. The agent knows the true payoffs from all the projects .

We assume that the principal can commit to a mechanism so that if the agent reports payoffs when the true state is , the project is chosen leading to final payoffs for the principal and agent respectively.

As discussed earlier, if the agent can lie arbitrarily, the principal cannot do better than by choosing a project at random. So we assume a natural partial verifiability constraint of no overselling under which the agent cannot report a project to be more profitable than it actually is. Such a constraint on the message space may be inherent in the environment or induced by the principal by requiring the agent to furnish some kind of evidence supporting its claims. Formally, the agent’s state dependent message space takes the form:

Since our message space satisfies the Nested Range condition of Green and Laffont [15],

we can without loss of generality restrict attention to truthful mechanisms.

Definition 2.1.

A mechanism is truthful if for any and

We’ll consider the principal’s problem of finding the optimal truthful mechanism for two different objectives:

-

•

Maximizing the expected profit:

-

•

Maximizing the probability of choosing the best project:

First, we characterize the class of truthful mechanisms.

3 Characterization of truthful mechanisms

We begin by defining a special class of mechanisms which we call table mechanisms.

Definition 3.1.

A mechanism is a table mechanism if there exists a function with the properties

-

•

-

•

-

•

so that

In words, a table mechanism is defined by an increasing set function that determines the set of projects on the table and the mechanism always chooses the agent’s favorite project among those on the table. The first condition says that there is a default project which is always on the table. The second condition says that the set of projects on the table cannot depend on the agent’s payoffs. The third condition is that the set of projects on the table weakly increases as the profit vector increases.

Theorem 1.

is truthful if and only if it is a table mechanism.

It is fairly straightforward from the definitions to check that table mechanisms are truthful. Indeed, under a table mechanism, the agent prefers reporting higher ’s to reporting lower ones and, given any report of ’s, prefers reporting her payoffs to misreporting her payoffs (since such a misrepresentation can only lead the principal to make a choice which gives the agent a lower payoff.) The other direction is more involved.

Proof of Theorem 1.

Suppose is a table mechanism. Consider any profile . If the agent reports some , we know that from the constraint . Since is increasing, it follows that . Since the agent gets his preferred project among those available and reporting truthfully maximizes his set of available projects, the agent cannot gain by misreporting. Therefore, is truthful.

Now suppose that is a truthful mechanism. Define the function so that if and only if there exists some such that . First, we will show that the function satisfies the three properties in the definition of table mechanism:

-

•

Observe that and thus, for any

-

•

The property that does not depend on agent payoffs follows from observing that . Thus, if , and vice versa. Thus, we have for any .

-

•

Take any such that . Suppose which implies that there exists with so that . But then, as well and so . Thus, we get that .

Now we want to show that for any state ,

Suppose towards a contradiction that is not in this set. By definition, . Let . Then and . But the fact that implies that there exists a such that . But then, the agent can misreport at state to and gain from this manipulation. This contradicts the fact that is truthful and so it must be that . It follows then that is a table mechanism. ∎

For simplicity going forward, we will assume (without loss of generality) that for all . That is, in a table mechanism, project is always on the table.

Before discussing the results, we define a subclass of table mechanisms that take a simple cutoff form.

Definition 3.2.

A mechanism is a cutoff mechanism if it is a table mechanism and for , there exist cutoffs , such that if and only if .

In a cutoff mechanism, a project is on the table if the principal’s profit from the project meets a threshold. That is, whether a project is on the table or not depends only on that particular project’s profit value. The principal then chooses the agent’s favorite project among those that meet the cutoff and the default project.

4 Maximizing expected profit

In this section, we consider the principal’s problem of finding the optimal table mechanism for maximizing expected profit . For the most part, we’ll consider and solve the problem for the case of projects. We’ll briefly discuss the case of projects towards the end of this section.

4.1 2 projects

In the case of two projects, we have and . In a table mechanism with 2 projects, we can assume without loss of generality that for all and so the principal only really has to decide the set of vectors when .

Theorem 2.

For two projects with , the optimal truthful mechanism is a cutoff mechanism. The optimal cutoff is defined by

Proof.

Suppose is truthful with associated function . From Theorem 1, we know that is a table mechanism. So for all . Define . Define the cutoff mechanism so that . We’ll show that the expected profit for the principal from is at least as high as the expected profit from . In fact, we will show that this holds conditional on , and hence in expectation.

Consider the following (exhaustive and mutually exclusive) cases depending on whether or :

-

•

: For any such , we know both and therefore, the second project is chosen for all such profiles. Thus, the two mechanisms are identical and generate the same profit for the principal in this case.

-

•

: In this case, and thus project 2 is chosen for sure. Note that the principal prefers project 2 over 1 in these profiles and thus, the profit from the cutoff mechanism is weakly higher for any such .

-

•

: Now while can be either or . Observe that the principal strictly prefers project 1 over 2 in all these profiles. Thus, the cutoff mechanism again leads to weakly higher profits for such .

-

•

: Here we have . Thus, the two mechanisms are identical in this set and lead to same profits for the principal.

This shows that for any truthful mechanism, there is a cutoff mechanism under which the principal’s expected profit is weakly higher. Thus, the optimal truthful mechanism must be a cutoff mechanism. Now our problem is just to find the optimal cutoff .

Consider the decision problem of the principal for any given . It can either

-

•

not make project 1 available and get

-

•

make project 1 available and get

The constraint imposed by truthfulness and optimality of cutoff mechanisms imply that the principal can only base this decision on the value of . Thus, taking expectation with respect to , we get that the two alternatives are:

-

•

not make project 1 available and get

-

•

make project 1 available and get

Thus, the principal would want to make project 1 available if and only if

At the optimal cutoff, the principal should be indifferent between the two alternatives and so the cutoff is defined by the solution to the equation

∎

In the special case where the principal and agent payoffs are independent, we get the following corollary.

Corollary 3.

Suppose is such that the principal and agent payoffs are independent. Then the optimal cutoff is given by .

4.2 Ally principle

In this subsection, we discuss the implications of our model for the well-known Ally principle which states that a principal delegates more authority to an agent with more aligned preferences. For this purpose, we assume that the principal agent payoffs for each project is bivariate normal and are drawn i.i.d. across projects. Now the question is whether we can say something systematic about , the optimal cutoff as a function of the correlation .

Theorem 4.

For projects with , the optimal cutoff is defined by the equation

where . The optimal cutoff is decreasing in .

of Theorem 4

We know that the optimal cutoff is the solution to the following equation

Let us simplify the above expression. First, we want to find . We know that if , then the conditional distribution

and so in our case, . Also, since the payoffs are independent across projects, we get that

Using this, we get that

where is the standard normal cdf.

Plugging this into the equation, we get that the optimal cutoff satisfies

We can find that the expectation is equal to

and letting , we have that the optimal cutoff is implicitly defined by

where and represent the standard normal cdf and pdf respectively. Observe that and is increasing in .

Now letting , we can use the implicit function theorem to get that

Note that and so . Also observe from the above expression that is never and so it follows from the smoothness of that for all . Thus, we have that the optimal cutoff is decreasing in .

The proof proceeds by applying the condition obtained in Theorem 2 for the case of the bivariate normal distribution. Using formulas for integrals of normal cdfs from Owen [28], we obtain the condition that the optimal cutoff must satisfy where . We can then differentiate this equation and get that . The smoothness of and the fact that is never zero implies that for all . The formal proof is in the appendix.

4.3 N projects

In this subsection, we discuss the case of projects. We believe that a cutoff mechanism should continue to be optimal but we haven’t been able to prove it yet. Motivated by the result for two projects, we conjecture that a cutoff mechanism is optimal for an arbitrary number of projects and consider the problem of finding the optimal cutoff mechanism.

The following theorem gives the optimal cutoff mechanism when the principal agent payoffs are i.i.d uniform.

Theorem 5.

For projects and uniform on , the optimal cutoff mechanism has a single cutoff that is defined by the equation

The principal’s expected utility from the corresponding optimal cutoff mechanism is given by

of Theorem 5

For any arbitrary cutoff mechanism with cutoffs , we compute the expected utility of the principal. For the below expressions, consider .

Note that . That is, conditional on , the probability that the decision is is the same as the probability that the decision is when the cutoff and the remaining cutoffs are the same. To find the probability that the last project is chosen, we condition on its rank which is defined in terms of s. That is, the rank of is if there are exactly projects with higher s.

We first argue that cutoffs have to be interior in the optimal cutoff mechanism. Suppose is a cutoff mechanism with cutoffs and . In this case, let denote the expected utility of the principal. Note that . Define a new cutoff mechanism in which all cutoffs remain the same except for which now has the cutoff . Now, with probability , the principal gets and with probability , the principal gets a convex combination of and . This means that his expected payoff under the new mechanism is . Therefore, an optimal mechanism cannot have the cutoff 1. Now, suppose there is an which has a cutoff of 0. Observe that the expected utility from any arbitrary project conditional on being chosen is . Now, consider increasing the cutoff to in the new mechanism while keeping every other cutoff the same. For every , under the old mechanism, the principal’s payoff was some convex combination of and some . Under the new mechanism, it is just . For , the new mechanism is identical to the old one. Therefore, an optimal mechanism cannot have a cutoff of 0. Thus, we know that in the optimal cutoff mechanism, for any .

Now suppose that the mechanism is such that there exist with . Define so that and . From the above calculations, we know that if we write in expanded form and plug in and , we get a polynomial that is at most cubic in . This is because we get a term that is at most quadratic in for for any and in the expected utility calculation, we multiply that with . Note that by the symmetry of the projects, the principal should get the same expected utility if we changed to . Therefore, the polynomial should be of the form . Now, if is or , the principal gains from increasing or decreasing which is possible since we know that the solution is interior and . Therefore, cannot be optimal in either case. When , the principal is indifferent to increasing till one of the cutoffs reaches an extreme of or which we know cannot be optimal. Therefore, a cutoff mechanism with different cutoffs cannot be optimal.

The above discussion implies that the solution to the optimization problem has to be a single cutoff mechanism. Let be the single cutoff. Using the above calculations, we have that

Therefore,

Differentiating with respect to gives the desired optimal cutoff mechanism defined by single cutoff .

Setting it equal to zero gives us:

Plugging in the expected utility expression gives us the maximum utility of the principal in the class of cutoff mechanisms: .

Note that since we are maximizing a continuous function over a compact space, a solution exists. The rest of the proof proceeds in three steps. In step 1, we show that in any cutoff mechanism which has a cutoff that is or cannot be optimal. That is, the solution must be interior. In step 2, we show that a cutoff mechanism with different cutoffs cannot be optimal. Finally, we maximize the principal’s utility with respect to the single cutoff to get the optimal cutoff mechanism. The proof is relegated to the appendix. While it is hard to obtain an exact closed form solution for the optimal single cutoff, we show that it has the following asymptotic property.

The optimal single cutoff

of lemma 4.3

Let

Then for any ,

and so for all sufficiently large , the quantity

is positive if and only if and negative if and only if . Hence, for any , it follows that the unique root of the equation from Theorem 5 satisfies

It follows from Lemma 4.3 that as , the optimal single cutoff and the expected utility of the principal .

5 Maximizing probability of best project

In this section, we consider the objective of maximizing the probability of choosing the best project for the principal . We’ll only focus on the case of projects for this part.

5.1 2 projects

Let’s consider the case of two projects and table mechanisms with project 2 always on the table.

Theorem 6.

For two projects with , the optimal truthful mechanism is a cutoff mechanism. The optimal cutoff is defined by

or more simply

Proof.

The argument for why cutoff is optimal is exactly the same as in the proof of Theorem 2. We now derive the optimal cutoff. The principal can either

-

•

make project 1 available and get

-

•

or not make it available and get

Since the principal can only make the decision based on value of , it will chose to make project 1 available if and only if

At the cutoff, the principal must be indifferent between making or not making project 1 available. This gives the desired condition. ∎

In the special case where the principal and agent payoffs are independent, we get the following corollary.

Corollary 7.

Suppose is such that the principal and agent payoffs are independent. Then the optimal cutoff is given by .

5.2 Ally principle

Assume that the principal agent payoffs for each project is bivariate normal and are drawn i.i.d. across projects. Now the question is whether we can say something systematic about , the optimal cutoff as a function of the correlation .

Theorem 8.

For projects with , the optimal cutoff is given by the equation

where and .

of Theorem 8

Given the distributional form, we have

and therefore,

This gives

Then,

Observe that if is the above expectation, then we have . Thus, we can conclude that for all . So let’s focus on and try to argue that the optimal cutoff must be decreasing in .

The expectation above equals

where and and this completes the proof.

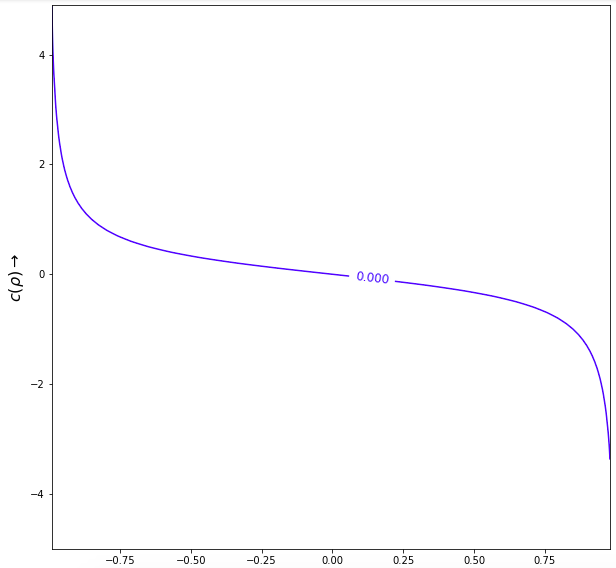

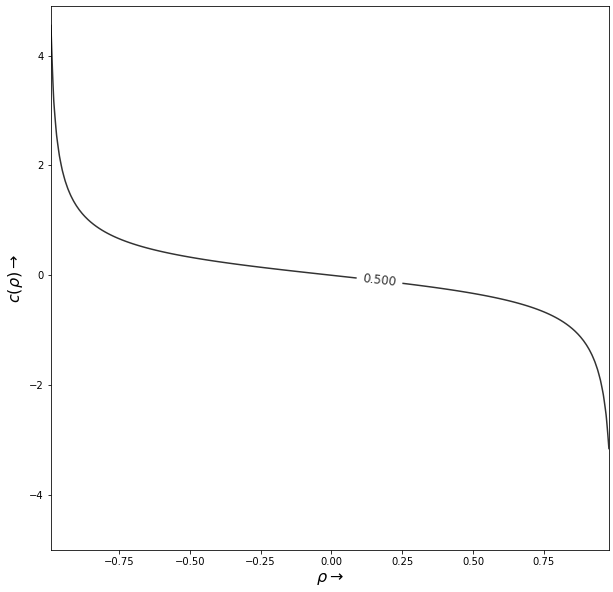

Again, we use the definition of optimal cutoff from Theorem 6 and apply it to the bivariate normal case. Then, using the integral formulas from Owen [28], we show that the optimal cutoff in this case is defined by where and . We haven’t been able to show that this result implies that the optimal cutoff is decreasing in , but the following contour plot from Python suggests that it is:

6 Remarks

-

1.

Comparison of optimal mechanisms for the two objectives We wanted to see how the optimal cutoffs for the two objectives compare when payoffs are bivariate normal. To do so, we plotted the two optimal cutoff curves together and interestingly found that the curves coincide. While we haven’t been able to formally prove that the solutions coincide, we conjecture that they do.

Conjecture 9.

With projects and payoffs drawn iid from bivariate normal , the optimal mechanism for maximizing principal’s expected profit and that for maximizing probability of choosing better project is the same cutoff mechanism with the cutoff defined by where

-

2.

Delegation interpretation of the optimal mechanism The simplest implementation of the optimal cutoff mechanism has a nice delegation interpretation. The principal selects a cutoff profit and a default project and delegates the project choice to the agent, in the sense that the agent can select either the default project or a project which meets the cutoff profit, and the principal signs off on the final decision. Under this delegation, the agent chooses his favorite project among those that meet the cutoff and the default project. Note in particular that this implementation only requires the agent to report information about the chosen project. This is outcome-equivalent to the cutoff mechanism. We note that many instances of “cutoff mechanisms” with flavors similar to ours have appeared in the literature, but the optimality of such mechanisms has been driven by the assumption of ex-post verifiability (Ben-Porath et al. [2], Mylovanov and Zapechelnyuk [27] Armstrong and Vickers [1]). In particular, in most previous models the principal’s ability to punish in the case of a misreport is tantamount to the assumption that the agent cannot lie. Here, we offer an alternative way of rationalizing such cutoff mechanisms via the no-overselling (or more generally, interim partial verifiability) constraint, which alters the agents incentives but not by threatening the agent in the case of a misreport. To help elucidate this point, we make the following observation. If our model were altered so that the agent had an unconstrained message space, but the principal were required to take the default project in case the agent should oversell any of the projects, then all of our results would carry over.

7 Conclusion

We consider a principal agent project selection problem with asymmetric information. When the agent can lie arbitrarily, we find that the principal cannot gain anything from commitment power and may as well choose a project at random. In contrast, if the principal can identify or induce partial verifiability in the environment so that the agent cannot oversell any of the projects, then a simple cutoff mechanism is optimal for the case of two projects, both for maximizing expected profit and for maximizing probability of choosing better project.

In the particular case where payoffs are bivariate normal, we find that the optimal cutoff is decreasing in the correlation between payoffs and thus, our model provides evidence in favor of the ally principle which says that the principal grants more leeway to an agent who shares its preferences. We conjecture that our results for the case of two project extend to settings with more than two projects as well.

References

- Armstrong and Vickers [2010] Armstrong, M. and J. Vickers (2010): “A model of delegated project choice,” Econometrica, 78, 213–244.

- Ben-Porath et al. [2014] Ben-Porath, E., E. Dekel, and B. L. Lipman (2014): “Optimal allocation with costly verification,” American Economic Review, 104, 3779–3813.

- Ben-Porath et al. [2019] ——— (2019): “Mechanisms with evidence: Commitment and robustness,” Econometrica, 87, 529–566.

- Ben-Porath and Lipman [2012] Ben-Porath, E. and B. L. Lipman (2012): “Implementation with partial provability,” Journal of Economic Theory, 147, 1689–1724.

- Bull and Watson [2004] Bull, J. and J. Watson (2004): “Evidence disclosure and verifiability,” Journal of Economic Theory, 118, 1–31.

- Bull and Watson [2007] ——— (2007): “Hard evidence and mechanism design,” Games and Economic Behavior, 58, 75–93.

- Caragiannis et al. [2012] Caragiannis, I., E. Elkind, M. Szegedy, and L. Yu (2012): “Mechanism design: from partial to probabilistic verification,” in Proceedings of the 13th ACM Conference on Electronic Commerce, ACM, 266–283.

- Celik [2006] Celik, G. (2006): “Mechanism design with weaker incentive compatibility constraints,” Games and Economic Behavior, 56, 37–44.

- Dasgupta et al. [1979] Dasgupta, P., P. Hammond, and E. Maskin (1979): “The implementation of social choice rules: Some general results on incentive compatibility,” The Review of Economic Studies, 46, 185–216.

- Deneckere and Severinov [2008] Deneckere, R. and S. Severinov (2008): “Mechanism design with partial state verifiability,” Games and Economic Behavior, 64, 487–513.

- Deneckere and Severinov [2001] Deneckere, R. J. and S. Severinov (2001): “Mechanism design and communication costs,” USC CLEO Research Paper.

- Ferraioli et al. [2016] Ferraioli, D., P. Serafino, and C. Ventre (2016): “What to verify for optimal truthful mechanisms without money,” in Proceedings of the 2016 International Conference on Autonomous Agents & Multiagent Systems, International Foundation for Autonomous Agents and Multiagent Systems, 68–76.

- Fotakis et al. [2017] Fotakis, D., P. Krysta, and C. Ventre (2017): “Combinatorial auctions without money,” Algorithmica, 77, 756–785.

- Gibbard et al. [1973] Gibbard, A. et al. (1973): “Manipulation of voting schemes: a general result,” Econometrica, 41, 587–601.

- Green and Laffont [1986] Green, J. R. and J.-J. Laffont (1986): “Partially verifiable information and mechanism design,” The Review of Economic Studies, 53, 447–456.

- Guo and Shmaya [????] Guo, Y. and E. Shmaya (????): “Project Choice from a Verifiable Proposal,” 40.

- Hart et al. [2017] Hart, S., I. Kremer, and M. Perry (2017): “Evidence games: Truth and commitment,” American Economic Review, 107, 690–713.

- Jackson and Tan [2013] Jackson, M. O. and X. Tan (2013): “Deliberation, disclosure of information, and voting,” Journal of Economic Theory, 148, 2–30.

- Kartik [2009] Kartik, N. (2009): “Strategic communication with lying costs,” The Review of Economic Studies, 76, 1359–1395.

- Kitson et al. [1998] Kitson, A., G. Harvey, and B. McCormack (1998): “Enabling the implementation of evidence based practice: a conceptual framework.” BMJ Quality & Safety, 7, 149–158.

- Lacker and Weinberg [1989] Lacker, J. M. and J. A. Weinberg (1989): “Optimal contracts under costly state falsification,” Journal of Political Economy, 97, 1345–1363.

- Maggi and Rodriguez-Clare [1995] Maggi, G. and A. Rodriguez-Clare (1995): “Costly distortion of information in agency problems,” The RAND Journal of Economics, 675–689.

- Moore [1984] Moore, J. (1984): “Global incentive constraints in auction design,” Econometrica: Journal of the Econometric Society, 1523–1535.

- Munro et al. [2014] Munro, A. et al. (2014): “Hide and seek: A theory of efficient income hiding within the household,” Tech. rep., National Graduate Institute for Policy Studies.

- Myerson [1981] Myerson, R. B. (1981): “Optimal auction design,” Mathematics of operations research, 6, 58–73.

- Myerson and Satterthwaite [1983] Myerson, R. B. and M. A. Satterthwaite (1983): “Efficient mechanisms for bilateral trading,” Journal of economic theory, 29, 265–281.

- Mylovanov and Zapechelnyuk [2017] Mylovanov, T. and A. Zapechelnyuk (2017): “Optimal allocation with ex post verification and limited penalties,” American Economic Review, 107, 2666–94.

- Owen [1980] Owen, D. B. (1980): “A table of normal integrals: A table,” Communications in Statistics - Simulation and Computation, 9, 389–419.

- Satterthwaite [1975] Satterthwaite, M. A. (1975): “Strategy-proofness and Arrow’s conditions: Existence and correspondence theorems for voting procedures and social welfare functions,” Journal of economic theory, 10, 187–217.

- Severinov and Deneckere [2006] Severinov, S. and R. Deneckere (2006): “Screening when some agents are nonstrategic: does a monopoly need to exclude?” The RAND Journal of Economics, 37, 816–840.

- Sher and Vohra [2015] Sher, I. and R. Vohra (2015): “Price discrimination through communication,” Theoretical Economics, 10, 597–648.

- Singh and Wittman [2001] Singh, N. and D. Wittman (2001): “Implementation with partial verification,” Review of Economic Design, 6, 63–84.