The Macroeconomy as a Random Forest

First Draft: November 15, 2019

This Draft:

Latest Draft Here

)

Abstract

I develop Macroeconomic Random Forest (MRF), an algorithm adapting the canonical Machine Learning (ML) tool to flexibly model evolving parameters in a linear macro equation. Its main output, Generalized Time-Varying Parameters (GTVPs), is a versatile device nesting many popular nonlinearities (threshold/switching, smooth transition, structural breaks/change) and allowing for sophisticated new ones. The approach delivers clear forecasting gains over numerous alternatives, predicts the 2008 drastic rise in unemployment, and performs well for inflation. Unlike most ML-based methods, MRF is directly interpretable — via its GTVPs. For instance, the successful unemployment forecast is due to the influence of forward-looking variables (e.g., term spreads, housing starts) nearly doubling before every recession. Interestingly, the Phillips curve has indeed flattened, and its might is highly cyclical.

1 Introduction

The rise of Machine Learning (ML) led to great excitement in the econometrics community. In applied macroeconomics, a first wave of papers took ML algorithms off the shelf and went hunting for forecasting gains. With the emerging consensus that some ML offerings can appreciably increase predictive accuracy, a question emerges: what is the place of economics in all that?

The conditional mean is the most basic input to any empirical macroeconomic analysis. Anything else that follows (e.g., structural analysis) depends on it. Thus, getting it right is not merely useful, it is necessary. Clearly, in that regard, ML can help. However, while the latter gladly delivers prediction accuracy gains (and ergo a conditional mean closer to the truth), it is much more reluctant to disclose its inherent model. Consequently, ML is currently of great use to macroeconomic forecasting, but of little help to macroeconomics. I propose a simple remedy: shifting the focus of the algorithmic arsenal away from predicting into modeling , which are economically meaningful coefficients in a time-varying macroeconomic equation. The newly proposed algorithm, Macroeconomic Random Forest (MRF) kills two coveted birds with one stone. First, in most instances, MRF forecasts better than off-the-shelf ML algorithms and traditional econometric approaches. Second, its main output, Generalized Time-Varying Parameters (GTVPs), can be interpreted. Their versatility comes from nesting many popular specifications (structural breaks/change, threshold effects, regime-switching, etc.) and letting the data decide whichever combination of them is most suitable. Ultimately, we get a new methodology leveraging the power of ML and big data to provide a modern take on the decades-old challenge of estimating latent states driving linear macroeconomic equations.

The State of Empirical Macro Affairs. Answering positively two questions guarantees a viable conditional mean: "are all the relevant variables included in the model?" and at a higher level of sophistication, "is linearity a valid approximation of reality?". The first one led to the successful development of factor models and large Bayesian Vector Autoregressions (VARs) over the last two decades. To address the second, applied macroeconomic researchers have proposed many non-linear time series models based on reasonable economic intuition. Most of them amount to have regression coefficients in

evolving through time. The process can take many forms, and a choice must be made a priori out of many equally plausible alternatives. Notable members of the vast time-variations catalog are threshold/switching regressions (Hansen,, 2011), smooth transition (Teräsvirta,, 1994), structural breaks (Perron et al.,, 2006; Stock,, 1994), and random walk time-varying parameters (Sims,, 1993; Cogley and Sargent,, 2001; Primiceri,, 2005). While it is uncontroversial that factor models and large Bayesian VARs have gone a long way in meeting their original goals, less victorious statements are available for the various time-variation proposals. Why?

More often than not, nonlinear time series models use little data and/or restrict stringently the shape of ’s path. While the consequences for forecasting are direct and obvious, those for analysis of macroeconomic relationships are equally problematic. Is the evolving Taylor rule characterized by switching regimes (Sims and Zha,, 2006), a Volker structural break (Clarida et al.,, 2000), or gradually evolving parameters (Boivin,, 2005; Primiceri,, 2005)? This discordance interferes with our understanding of the past while impacting our expectations for tomorrow’s . I now divide popular time-variation approaches into two strands, discuss their shortcomings, and complete by explaining how MRF addresses them.

Observable Time-Variation Via Interaction Terms. Using interaction terms and related refinements is a parsimonious way to create time variation in a linear equation. For instance, switching regimes based on an observed regressor can be obtained by interacting the linear equation with the indicator function , where is some value, and is a threshold variable chosen by the researcher. However, using the FRED-QD US macro data set (McCracken and Ng,, 2016) reveals an overwhelmingly large number of candidates for . Additionally, there may be multiple regimes interacting together. Or the "true" could be an unknown function of available regressors. And structural breaks or slow exogenous variation could get in the way. The list goes on. This renders a credible exploration of the threshold structures’ space impossible and the enterprise of manually specifying the model very much compromised.

Here is an empirical example. auerbach2012measuring and rameyzubairy2018 use a GDP/unemployment indicator to let the effects of fiscal stimulus (potentially) vary with the state of the economy. batini2012successful allow for additional dependence on the origin of the impulse (revenue or spending). Such honorable explorations could go on endlessly. MRF provides a hammer solution to the problem. First, the near-universe of threshold structures can be characterized by regression trees — see section 2.1. Second, MRF embeds, among other things, a powerful greedy algorithm designed to explore such "structure" spaces.

Latent Time-Variation. Some methods with an aura of greater flexibility are labeled as "latent change". In this line of work, either follows a law of motion (random walk, Markov process) or could be subject to discrete breaks.111Simpler derivatives are often used in applied work. In forecasting, rolling-window estimation drops early observations. In empirical macro, pre-defined subsamples are popular (clarida2000; del2020s). At first glance, this appears to solve many of the problems of interaction terms approaches. By treating as a state to be filtered/estimated within the model, the complexity of characterizing its path correctly out of abundant data seems to vanish. Alas, estimating ’s path implies a great number of parameters in fact, often greater than the number of observations, GC2019 which inevitably necessitates strong regularization. That regularization is the law of motion itself, a choice far from innocuous – and akin to that of in "observable" change models. Accordingly, whether it is latent regime-switching, exogenous breaks, or slow change, none can easily accommodate for the additional presence of the other. Yet, these models are routinely fitted separately on the same data. Consequently, methods often detect what they are designed to detect, in near-complete abstraction of imaginable interference from other nonlinearities.

Additionally, while "latent" approaches may sometimes rationalize the data well in-sample, many of them will struggle to outperform a simple benchmark out-of-sample. Often, the very nature of ’s law of motion creates forecasting headaches. Classical TVPs imply a two-sided vs one-sided filtering problem. Analogously, detecting a structural break is much harder without a great amount of data on both sides of it. Moreover, there is the obvious problem of statistical efficiency. If the Phillips curve flattened because an economy became increasingly open, including an interaction term with imports/exports is wildly more efficient than obtaining the whole path non-parametrically. Thus, exogenous structural change should be, in some sense, a time variation of last resort. The advantage of MRF is that it algorithmically search for "observable" low-hanging fruits, and turn to split the sample with only if necessary. Further, it implicitly creates a forecasting function for which is an RF in its own right. This is, almost in any case, much more powerful than existing alternatives – like random walks.

Mechanics. The key difference when adding the M to MRF is the inclusion of a linear part within each of the tree leaves, rather than just an intercept. Motivated in cross-sectional applications to improve the efficiency of nonparametric estimation (in the spirit of local linear regression), trees with linear parts have been considered (among others) in treed and modeltrees. friedberg2019llf expand on this by considering an ensemble of them (i.e., a forest) and focusing on the problem of treatment effect heterogeneity. Of course, the difference here is that a linear part is much more meaningful when one can look at as a process of its own – and as a synthesis of nonlinear time series models. Finally, it is noteworthy that the approach may come in semiparametric partially linear clothing, yet it makes no compromise on the range of nonlinearities it captures. This is a virtue of time-varying coefficients models being able to approximate any nonlinear function (granger2008).

The paper also introduces new devices enhancing MRF’s predictive and interpretability potential. First, I propose Moving Average Factors (MAFs) as a simple way to compress ex-ante the information contained in the lags of a regressor entering the RF part of MRF. They boost the meaningfulness of tree splits and helps avoid running out of them quickly. The transformation is motivated by the literature on constraining/regularizing lag polynomials (shiller1973). Precisely, MAFs’ contribution is to induce similar shrinkage when there are no explicit coefficients to shrink. When it comes to GTVPs themselves, I provide a regularization scheme better suited for time series which procures a desirably smoother path with respect to time. It is inspired by the random walk shrinkage of the classical TVP literature and is implemented within the tree procedure by weighted least-squares. Finally, a variant of the Bayesian Bootstrap provides credible regions that are instrumental for the interpretation of GTVPs.

Results. In simulations, the tool does comparably well to traditional nonlinear time series models when the data generating process (DGP) matches what the latter is designed for. When the time-variation structure becomes out of reach for classical approaches, MRF wins. Additionally, it supplants plain RF whenever persistence is pervasive. In a forecasting application, the MRFs gains are present for almost all variables and horizons under study, a rarity for nonlinear forecasting approaches. For instance, the Autoregressive Random Forest (ARRF) almost always supplant its resilient OLS counterpart. Also, an MRF where the linear part is a compact factor-augmented autoregression generates very accurate forecasts of the 2008 downturn for both GDP and the unemployment rate (UR). Inspection of resulting GTVPs reveals they behave differently from random walk TVPs. For instance, in the UR equation, the contribution of forward-looking variables nearly doubles before every recession — including 2008 where the associated is forecasted to do so out-of-sample. This reinforces the view that financial indicators and other market-based expectations proxies can rapidly capture downside risks around business cycle turning points (adrian2019). MRF learned and applied it to great success.

Inflation is subject to a variety of time-variations, detection of which would be compromised by approaches lacking the generality of MRF. The long-run mean and the persistence evolved slowly and in an exogenous fashion — this has been repeatedly found in the literature e.g., cogley2001evolving. More novel is the finding that the real activity factor’s effect on the price level depends positively on the strength of well-known leading indicators, especially housing-related. Following this lead, I complete the analysis by looking at a traditional Phillips’ curve specification. I report that the inflation/unemployment trade-off coefficient decreased significantly since the 1980s and also varies strongly along the business cycle. Among other things, it is extremely weak following every recession. This nuances current evidence on the flattening Phillips curve, which, by design, focused almost entirely on long-run exogenous change (blanchard2015inflation; galigambetti2019; del2020s). Overall, MRF suggests inflation can rise from a positive unemployment gap, but it goes down much more timidly from economic slack. These findings are made possible by combining different tools within the new framework, such as credible intervals for the GTVPs, new variable importance measures specifically designed for MRF, and surrogate trees as interpretative devices for .

2 Macroeconomic Random Forests

This section introduces MRF. I first motivate the use of trees as basis functions by casting standard switching structures for autoregressions as special cases. Second, I detail the MRF mechanics and how it yields GTVPs. Third, I discuss how the approach relates to both standard RF and traditional random walk TVPs. Fourth, I discuss interpretability potential and provide a way to assess parameter uncertainty.

2.1 Traditional Macro Non-Linearities as Trees

Within the modern ML canon, Random Forest (RF) is an extremely popular algorithm because it allows for complex nonlinearities, handles high-dimensional data, bypasses overfitting, and requires little to no tuning. This is in sharp contrast with, for example, Neural Networks, whose ability to fail upon a bad choice of hyperparameters is largely unmatched. Thus, RF is a reasonable device to look into for constructing GTVPs. But there is more: many common time series nonlinearities fit within a tree structure. Hence, it will be all the more natural to think of MRF as a generalization of previous nonlinear offerings. Overall, it eliminates the arbitrary search for a specification. By creating a unified view, the myriad of time-variations suggested separately can now be tackled jointly.

I now present two examples displaying how common time series nonlinearities imply a tree structure for an AR process. Let us consider the inflation process in a country where inflation targeting (IT) was implemented at a publicly known date (like in Canada). Let be inflation at time and is the onset date of IT. Additionally, is some measure of output gap. A plausible model is reported in the tree graph below. The story is straightforward. Inflation behaved differently before vs after IT. After IT, it is a simple AR process. Before IT, it was a switching AR process which dynamics and mean depended on the sign of the output gap.222Note that a standard regression tree would set all ’s to 0.

[.Full Sample [. [. ] [. ] ] [. ] ]

This is one story out of many that trees can characterize. In practice, none of the above is known. The structure, the splitting variables, and the splitting points could be different. This is both good and bad news. It highlights the flexibility of trees. It also suggests that designing the "true" one from economic deduction is a daunting task — equally plausible alternatives are easily imaginable. Fortunately, algorithms can point out which trees in better agreement with the data.

A global grid search is computationally unfeasible if either is large or if we want to consider more than a few splits (examples above included 2 and 3, respectively). A natural way forward is recursive partitioning of the data set via a greedy algorithm (breiman1984classification).333A single autoregressive tree was proposed in meek2002art. A greedy algorithm optimizes functions by iteratively doing the best local update, rather than directly solving for a global optimum. As a result, it is prone to high variance (ESL). Hence, considering a diversified portfolio of trees appears as the most sensible route. To achieve that, it is highly effective to use Bootstrap Aggregation Bagging, breiman1996bagging of many de-correlated trees. This is the famous Random Forest proposition of breiman2001.

2.2 Generalized Time-Varying Parameters

The general model is

where are the state variables governing time variation and a forest. is oberved macroeconomic data which composition is motivated in section 2.6 and laid out explicitly in section 4. determines the linear model that we want to be time-varying. Typically, is rather small (and focused) compared to . For instance, an autoregressive random forests (ARRF) – which generalizes the cases of the previous section – uses lags of for . The tree fitting procedure underlying plain RF is not adequate, as it sets by default. Thus, analogously to friedberg2019llf, it is modified to

| (1) | ||||

The purpose of this problem is to find the optimal variable (so, finding the best out of the random subset of predictors indexes ) to split the sample with, and at which value of that variable should we split.444Note that, unlike friedberg2019llf, and will differ, which is natural when motivated from a TVP perspective (but not so much from local linear regression one). Forcing their equivalence is not feasible nor desirable in a macro environment. It outputs and which are used to split (the parent node) into two children nodes, and . We start with the leaf being the full sample. Then, we perform a split according to the minimization problem, which procures us with 2 subsamples. Within each of these two newly created subsamples, we run (1) again. Repeating this process recursively constructs an ever-growing set of ’s which are of ever-shrinking size. Doing so until a stopping criteria is met generates a tree.

Let the Trees Run Deep. Recursively splitting into and eventually leads to . However, , by construction, has very little company within its terminal node/leaf. As result, a single tree has low bias, but also very high variance for . When fitting a single tree, the (early) stopping point must be tuned to avoid overfitting. However, this is not necessary when a sufficiently diversified ensemble of trees is considered. Originally, breiman2001 himself provided a bound on the generalization error that grows with the correlation between trees.555Also, duroux2016impact derive a formula (for a ”median” forest) linking tuning parameters related to the depth of the trees and that of diversification. In MSoRF, I go further by showing that RF’s out-of-sample prediction is equivalent to the optimally "stopped" or "pruned" one, provided sufficiently diversified trees. The desirable property is attributed to the peculiar behavior of "randomized greedy algorithms", which are often overlooked as mere computational necessities. Those insights are of even greater use when it comes to time series since dependence and structural change pose challenges to hyperparameter tuning. Given a large enough , a reasonable mtry (see "De-Correlation" below on this) and standard subsampling rate, we can be confident that the out-of-bag prediction and ’s exclude fitted noise. In our specific context, it means the sample will not be over-split, and we are not going to see time variation when it is not there. Naturally, the credible regions proposed in section 2.7 will also help in that regard. The property will be illustrated in section 3.2.

(M)RF prediction is the simple average from those of its single trees. Same goes for . RF is a clever diversification scheme which generates sufficient randomization for that average to inherit the above properties. To achieve that, it mixes elements of re-sampling and model averaging: Bagging and de-correlated trees.666See MSoRF for a discussion on how RF compares and contrast with the forecast combinations/averaging literature.

Bagging. Each tree is "grown" on a bootstrapped sample (or a random subsample) (breiman1996bagging).777This does not preclude from obtaining for all ’s since ’s attached to the excluded observations are simply generated by applying the tree on the ”out-of-bag” data. When the base learner is highly nonlinear in observation and/or unstable, gains from Bagging can be large (breiman1996bagging; grandvalet2004bagging). Nonparametric or "pairs" mackinnon2006bootstrap bootstrap is being used — i.e., we are not shuffling residuals.888Nonetheless, Bagging in itself is not estranged to macro forecasting (inoue2008useful; hillebrand2010benefits; hillebrand2020bagging). However, nearly all studies consider the more common problem of variable selection via hard-thresholding rules – like t-tests (lee2020bootstrap). Rather, we are randomly selecting many observations triples (or pairs for Plain RF), and then fit a tree on them. To deal with the dependence inherent to time series data and other reasons detailed in section 2.7, a slightly more sophisticated bootstrapping/subsampling procedure (involving blocks) will be used for MRF.

De-Correlation. The second ingredient, proposed in breiman2001, is to consider "de-correlated" trees. RF is an average of many trees, and any averaging scheme reduces variance at a much faster rate if its components are uncorrelated. In our context, this is obtained by growing trees semi-stochastically. In equation (1), this is made operational by using rather than . In words, this means that at each step of the recursion, a different subsample of regressors is drawn to constitute candidates for the split. This prevents the greedy algorithm (which, as we know, only "thinks" locally) to always embark on the same optimization route. As a result, trees are further diversified and computing time, reduced. The fraction of randomly selected predictors is a tuning parameter typically referred to as mtry in the literature (and all software), with a default value of for regression settings. This, other algorithmic parameter settings, and some practical aspects are discussed in appendix A.4.

Plain RF has many qualities readily transferable to MRF. It is easy to implement and to tune. That is, it has few tuning parameters that are usually of little importance to the overall performance – robustness. It is relatively immune to the adverse effects of including many irrelevant features (ESL). Given the standard ratio of regressors to observations in macro data, this is a non-negligible advantage. Furthermore, with a sufficiently high mtry, it can adapt nicely to sparsity and discard useless predictors (olson2018making). Finally, its vanilla version already shows good forecasting performance for US inflation (medeiros2019) and macro data in general (chen2019off; GCLSS2018).

2.3 Random Walk Regularization

Equation (1) uses Ridge shrinkage which implies that each time-varying coefficient is implicitly shrunk to 0 at every point in time. and the prior it entails can exert a significant influence. For instance, if a process is highly persistent (AR coefficient lower than 1 but nevertheless quite high) as it is the case for SPREAD (see section 4), shrinking the first lag heavily to 0 could incur serious bias. Fortunately, this can easily be refined to a Minnesota-style prior if corresponds to a Bayesian VAR equation. If is low-dimensional (as it will often be), a simpler alternative consists in using OLS coefficients as prior means. Nonetheless, the specification of previous sections implies that if grows large, (or whatever the prior mean is). is a natural stochastic constraint in a cross-sectional setting, but its time series translation can easily be suboptimal. The traditional regularization employed in macro is rather the random walk

Thus, it is desirable to transform (1) so that it implements the prior that coefficients evolve smoothly (at least, to minimal extent), which is just shrinking to be in the neighborhood of and rather than 0. This is in line with the view that economic states (as expressed by here) last for at least a few consecutive periods. Note that unlike traditional TVP methods which rely extensively on smoothness regularization – as it is the sole regularizer, MRF makes only an very mild use of it to get rid of high-frequency noise that may be left in . The main benefit is to facilitate the interpretation of resulting GTVPs.

I implement the desired regularization by taking the "rolling-window view" of time-varying parameters, which has been exploited recently to estimate large TVP-VARs (giraitis2018inference; petrova2016quasi). That is, the tree, instead of solving a plethora of small ridge problems, will rather solve many weighted least squares problems (WLS) which includes close-by observations. The latter are in the neighborhood (in time) of observations within current leaf. They are included in estimation, but are allocated a smaller weight.

For simplicity and to keep computational demand low, the kernel used by WLS is rather rudimentary: it is a symmetric 5-step Olympic podium. Informally, the kernel puts a weight of 1 on observation , a weight of for observations and and a weight of for observations and . Since some specific ’s will come up many times (for instance, if both observations and are within the same leaf, podiums overlap), I take the maximal weight allocated to as the final weight .

Formally, define as the "lagged" version of leaf . In other words, is a set containing each observation from , with all of them lagged one step. is the "forwarded" version. and are two-steps equivalents. For a given candidate subsample , the podium is

where , a tuning parameter guiding the level of time-smoothing. Then, it is only a matter of how to include those additional (but down weighted) observations in the tree search procedure. The usual candidate splitting sets

are expanded to include all observations of relevance to the podium

The splitting rule becomes

| (2) | ||||

Note that the Ridge penalty is kept in anyway, so the final model has in fact two sources of regularization. With , we are heading back to pure Ridge.

Although not considered in the main applications of this paper, models with a larger linear part are possible. For instance, one could estimate, equation by equation, a high-dimensional VAR. In practice, this simply requires harsher regularization via higher values of , and a larger minimum leaf size. Nevertheless, the forecasting benefits from this strategy could prove limited: MRF is "high-dimensional" whenever is large. The time-varying constant in MRF is a RF in its own right. It can be seen as a complex misspecification function (in the deep learning jargon, it is effectively called the bias) that adaptively controls for omitted variables in a way that is both non-linear and strongly regularized via randomization. Consequently, the cost from omitting a regressor of minor importance in is low since it can be picked up by the time-varying intercept.

Of course, the small strategy treats the extra regressors as exogenous, which could be at odds with some researchers’ will to investigate a large web of impulse response functions. Anyhow, both approaches are possible. The dynamic coefficients of a (large) GTVP-VARs can be estimated by either fitting MRF equation by equation, or modifying the splitting rule in (2) to be multivariate so that each tree is fitted jointly for all equation – pooling time-variation across equations. Finally, elements of the covariance matrix of residuals can be fitted separately with a plain RF, which is very fast.

2.4 Relationship to Random Walk Time-Varying Parameters

GTVPs have many advantages over classical TVPs. While it is known that any nonlinear model can be approximated by a linear one with TVPs (granger2008), nothing is said about how efficient that estimation is going to be. As it turns out, efficiency crucially matters in a macro context, and random-walk TVPs can be quite inefficient (aruoba2017dsge). For example, if the true follows a recurrent switching mechanism, random walk parameters already have two strikes against them. Some dimensionality reduction techniques – like reduced-rank restrictions (dewindgambetti2014; stevanovic2016common; chan-ftvp2018; GC2019) – can help, but nothing in that paradigm can come close to the parsimony of simply interacting with relevant variables. In contrast, MRF considers all time-variations options, and choose the "obvious thing", which may or may not be splitting on . Also, it is absolutely possible that the resulting pools both latent and observable time variation.

Even though MRF is remarkably flexible, its variance remains low thanks to the diversified portfolio of trees. The variance of classical TVPs can be controlled by cross-validation (GC2019) or via an elaborate hierarchical prior (amir2018choosing). A number of applications opt for a "manual" approach (AAG2013). However, it is understood that no tuning, however careful it may be, can overcome the hardship of fitting random-walks when the true ’s look nothing like it.

Econometrically, one way to more formally connect this paradigm to recent work on TVPs is to adopt the view that RF are adaptive kernel estimators (meinshausen2006; athey2019grf; friedberg2019llf). That is, the tree ensemble is a machine generating kernel weights. Once those are obtained, estimation amounts to weighted least squares (WLS) problem with a Ridge penalty. By running (1) recursively, one obtains terminal nodes/leaves to construct kernel weights

to use in

| (3) |

As shown in GC2019, standard random walk TVPs are in fact a smoothing splines problem, and for those, a reproducing kernel exists (dagum2009). giraitis2014inference drop the random walk altogether and proposed to use kernels directly. Anyhow, in both cases, the only variable entering the kernel is . In other words, only proximity in time is considered for the clustering of observations. This makes the seemingly flexible estimator in fact quite restrictive – and dependent on its inherent smoothness prior. Moreover, standard kernel methods are known to break down even in medium dimensions (say <10 variables) (friedberg2019llf). Therefore, augmenting – the sole variable in the kernel (implicit of explicit) of traditional TVP methods – with additional regressors is not an option. No such constraints bind on the RF approach.

2.5 Relationship to Standard Random Forest

The standard RF is a restricted version of MRF where , and . In words, the only regressor is a constant and there is no within-leaf shrinkage. Previous sections motivated MRF as a natural generalization of non-linear time-series models. At this point, a reasonable question emerges from a ML standpoint. Why should we prefer the partially linear MRF to the fully nonparametric RF? One reason is statistical efficiency. The other is potential for interpretation.

2.5.1 Smooth Relationships are Hard Relationships (to estimate)

In finite samples, plain RF can have a hard time learning smooth relationships – like a AR(1) process. This is bad news for time series applications. For prediction purposes, estimating

by OLS implies a single parameter. However, approximating the same relationship with a tree (or an ensemble of them) is far more consuming in terms of degrees of freedom. To get close to the straight line once parsimoniously parametrized by , we now need a succession of many step functions.999In a standard regression setup, nobody would model a continuous variable as an ordinal one unless some wild nonlinearities are suspected. With short time series, modeling smooth/linear relationships in such a way is a luxury one rarely can afford. The mechanical consequence is that RF will waste many splits on capturing the linear part, and may run out of them before it gets to focus more subtle nonlinear phenomena.101010One necessary (but not sufficient) symptom is AR terms being flagged as really important by typical RF variable importance measures (one example is borup2020now). In a language more familiar to economists, this is simply running out (quickly) of degrees of freedom. MRF provides a workaround. Modeling the linear part concisely leaves more room to estimate the nonlinear one. By its more strategic budgeting of degrees of freedom, the resulting (estimated) partially linear model could be, in fact, more non-linear than the fully nonparametric one.

This paper is not the first to recognize the potential need for a linear part in tree-based models. For instance, both treed and modeltrees proposed linear regressions within a leaf of a tree, respectively denominated "Treed Regression" and "Model Trees". More focused on real activity forecasting, woloszko2020adaptive and wochner2020dynamic blend insights from macroeconomics to build better-performing tree-based models.111111Specifically, wochner2020dynamic also note that using trees in conjunction with factor models can improve GDP forecasting. An analogous finding will be reported in section 4. On a different end of the econometrics spectrum, friedberg2019llf proposed to improve the nonparametric estimation of treatment effect heterogeneity by combining those ideas developed for trees into a forest.121212More broadly, this is extending to trees and ensemble of trees the ”classical” non-parametrics literature’s knowledge that local linear regression usually has much better properties (especially at the sample boundaries) than the Naradaya-Watson estimator. To my knowledge, this paper is the first to exploit the link between this strand of work and the sempiternal search for the "true" state-dependence in empirical macroeconomic models.

2.5.2 A Note on Interpretability

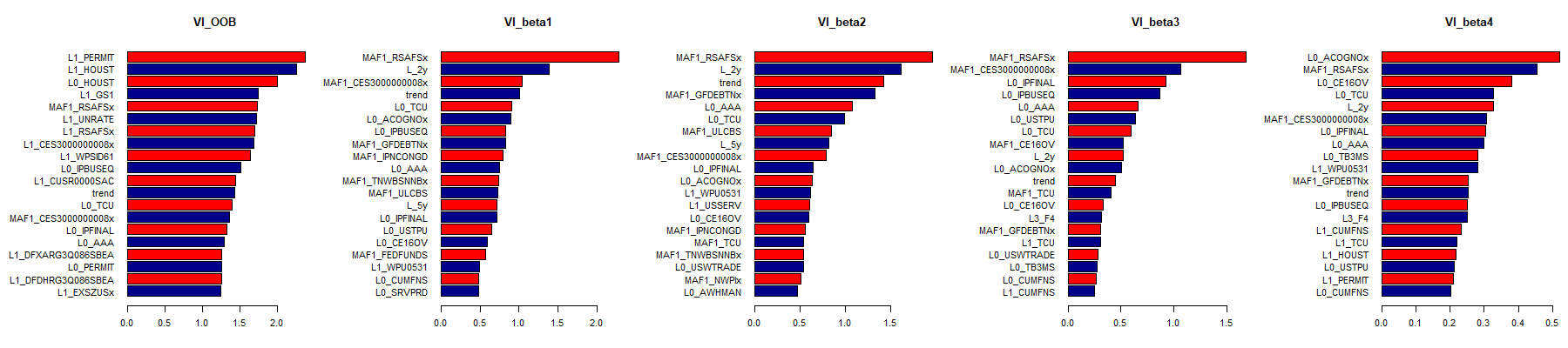

The interpretation of ML outputs is now a field of its own (molnar2019interpretable). RF is widely regarded as a black box model which needs to be interpreted using an external device. Indeed, it usually averages over 100 trees of substantial depth, which makes individual inspection impossible. MRFs partially circumvent the problem by providing time series which can be examined, and have a meaning as time-varying parameters for the linear model. Thus, whatever one may do with TVPs, it can be done with GTVPs. There are also some new avenues. For instance, Variable Importance (VI) measures usually deployed to dissect RF’s prediction can be used to inspect what is driving ’s. Those will be used in section 5.3.

A popular approach to dissect a standard RF is to use interpretable surrogate tree models to partially replicate the black box model’s fit. The idea can be transferred to MRF (molnar2019interpretable). In fact, partial linearity facilitates such an exercise. The linear part in MRF splits the nonparametric atom into different pieces () which can be analyzed separately. Each time series can be dissected with its own surrogate model, and meaningful combination/transformations of coefficients can be considered.

2.6 Engineering

This section discusses principles guiding the composition of , which is the raw material for in both MRF and plain RF. Macroeconomic data sets e.g. FRED, mccracken2020fred typically contains many regressors and few observations. After incorporating lags for each variable, it can easily be the case that predictors outnumber observations. The curse of dimensionality has both computational and statistical ramifications. The former is mostly avoided in RF since it does not rely on inverting a matrix. However, the statistical curse of dimensionality, a feature of the regressors/observations ratio, remains a difficulty to overcome.

There are two extreme ways of reducing dimensionality: sparse or dense. The former selects a small number of features out of the large pool in a supervised way (e.g. LASSO), the latter compresses the data in a set of latent factors that should span most of the original regressors space. This is often seen as a necessity to choose one of them.131313In macro forecasting work using RF, GCLSS2018 follow a dense approach by only including factors while borup2020targeting opt for sparsity by proposing a Lasso pre-selection step. However, in a regularized model, both can be included, and we can let the algorithm select an optimal combination of original features and factors.141414A more detailed discussion of this can be found in Appendix A.1. This is useful — it is not hard to imagine a situation where opting for one or the other would prove suboptimal to a more nuanced solution.

Lag Polynomials. From a predictive standpoint, residuals autocorrelation implies there is forecasting power left on the table. To get rid of it, many lags might be necessary. In multivariate contexts (like that of a VAR), doing so quickly pushes the model to overfit. A standard solution is Bayesian estimation and the use of priors in the line of litterman1984, which are specially designed for blocks of lags structures. Outside of the VAR paradigm, there is an older literature estimating restricted/regularized lag polynomials in Autoregressive Distributed Lags (ARDL) models (almon; shiller1973). More recently, these methods have found new applications in mixed-frequency models (ghysels2007midas) where the design of the model leads to an explosion of lag parameters.

(M)RF experiences an analogous situation. A tree may waste many splits trying to efficiently extract information out of a lag polynomial: for instance, splitting on the first lag, then the 7th one, then the 3rd one. In linear parametric models, the above methods can extract the relevant information out of a lag polynomial without sacrificing many degrees of freedom. A significant roadblock to this enterprise in the RF paradigm is that there are no explicit lag polynomials to penalize. An alternative route is to exploit the insight that RF can choose for itself relevant restrictions. We just have to construct regressors that embodies those, and include them in .

Moving Average Factors. To extract the essential information out of the lag polynomial of a specific variable, a linear transformation can do the job. Consider forming a panel of lags of variable :

We want to form weighted averages of the lags so that it summarizes most efficiently the temporal information of the feature indexed by .151515 is a tuning parameter the same way the set of included variables in a standard factor model is one. The weighted averages with that property will be the first few factors (extracted by PCA) of .161616While I work directly with the latent factors, a related decomposition called singular spectrum analysis works with the estimate of the summed common components. Since this decomposition naturally yields a recursive formula, it has been used to forecast macroeconomic and financial variables (hassani2009forecasting; hassani2013predicting). This can be seen as the time-dimension analog to the traditional cross-sectional factors. The latter are defined such as to maximize their capacity to replicate the cross-sectional distribution of fixing while the Moving Average Factors (MAFs) proposed here seek to represent the temporal distribution of for a fixed in a lower-dimensional space.171717In the spirit of the Minnesota prior, one can assign decaying (in ) weights to each lag before running PCA. This has the analogous effect of shrinking more heavily the distant lags and less so the recent ones. By doing so, our goal to summarize the information of without modifying the RF algorithm (or any other) is achieved: rather than using the numerous lags as regressors, we can use the MAFs which compress information ex-ante. As it is the case for standard factors, MAF are designed to maximize the explained variance in , not the fit of the final target. It is the RF part’s job to select the relevant linear combinations among so to maximize the fit. Finally, it is noteworthy that MAFs facilitate interpretation. As these are moderately sophisticated averages of a single time series, they can be viewed as a smooth index for a specific (but tangible) economic indicator. This is arguably much easier to interpret than a plethora of lags coefficients.

The take-away message from this subsection can be summarized in three points. First, there is no need to choose ex-ante between sparse and dense when the model performs selection/regularization. We can let the algorithm find the optimal balance. Second, to make the inclusion of many lags useful, we need to regularize the lag polynomial. Third, such compression can be achieved most easily by generating MAFs and using those as regressors in RF – or any algorithm.

2.7 Quantifying Uncertainty of ’s Estimates

taddy2015bayesian and taddy2016nonparametric interpret RF’s prediction as the posterior mean of a tree functional (the splitting algorithm) obtained by an approximate Bayesian bootstrap.181818The connection between breiman1996bagging’s bagging and rubin1981bayesian’s Bayesian Bootstrap was acknowledged earlier in clyde2001bagging. Through those lenses, each tree is a posterior draw. Seeing as a Bayesian nonparametric statistic (independently of the DGP) is of even greater interest in the case of MRF.191919An alternative (frequentist) inferential approach is that of friedberg2019llf. However, their asymptotic argument requires estimating the linear coefficients and the kernel weights on two different subsamples. This is hard to reconciliate with our goal of modeling time-variation and different regimes throughout the entire sample. Furthermore, when the sample size is small, splitting the sample in such a way carries binding limitations on the complexity of the estimated function. It provides inference for meaningful time-varying parameters rather than an opaque conditional mean function. Such techniques, originating from ferguson1973bayesian, have seldomly found applications in econometrics, such as chamberlain2003nonparametric for instrumental variable and quantile regressions.

While the Bayesian Bootstrap desirably does not assume many things about the data, it yet makes the assumption that is an iid random variable. Thus, it cannot be used directly as a proper theoretical motivation for using the bag of trees directly to conduct inference. I propose a block extension to make taddy2015bayesian’s convenient approach amenable to this paper’s setup.

Block Bayesian Bootstrap (BBB) is a simple redefinition of so that it is plausibly iid. Hence, in the spirit of traditional frequentist block bootstrap (mackinnon2006bootstrap), blocks of a well-chosen size will be exchangeable. Thus, a new variable can be defined . There will be a total of fixed and non-overlapping blocks. Under covariance stationarity, are iid, for a properly chosen block length.202020In practice, I will use block of two years for both quarterly or monthly data. Analogously to taddy2015bayesian, block-subsampling is preferred to BBB in implementations since it is faster and gives nearly identical results. Details of BB and BBB are available in Appendix A.2.

It is reasonable to wonder how the above procedure deals with the possible presence of heteroscedasticity. Fortunately, the nonparametric bootstrap/subsampling that RF uses is in fact the "pairs" bootstrap of pairsbootstrap which is valid under general forms of heteroscedasticity (mackinnon2006bootstrap). From a Bayesian point of view, lancaster2003 show that the obtained variance for OLS from using such a bootstrap is asymptotically equivalent to that of White’s sandwich formula.212121poirier2011bayesian propose better priors and karabatsos2016dirichlet incorporate such ideas into a generalized ridge regression. Hence, in the spirit of heteroscedasticity-robust estimation, no attempt will be made at directly evolving volatility (which is a GLS approach). Rather, it will be reflected in larger bands for periods of smaller signal-to-noise ratio.

3 Simulations

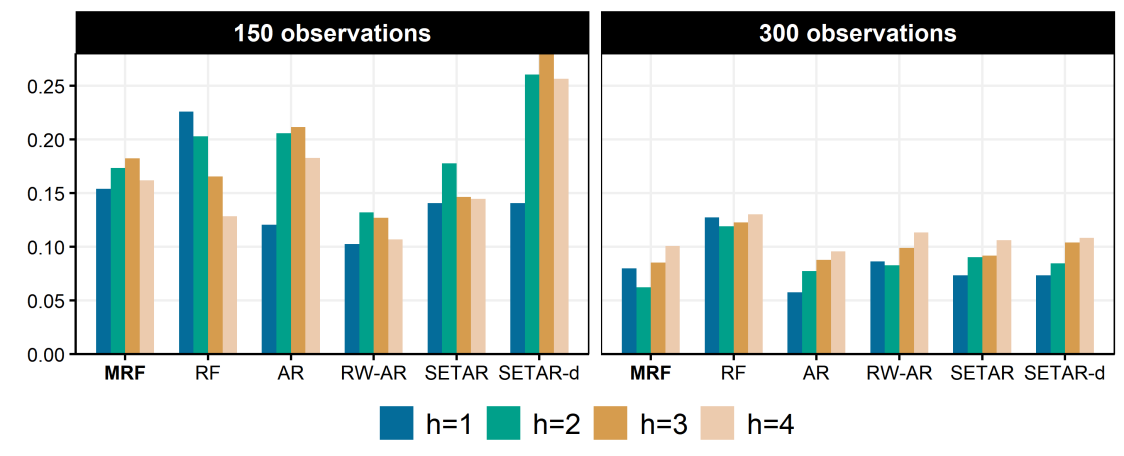

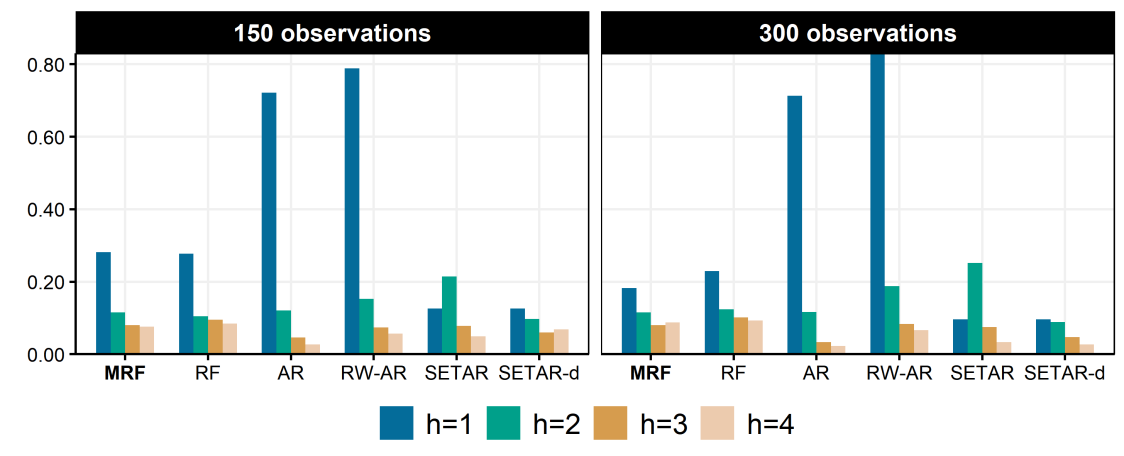

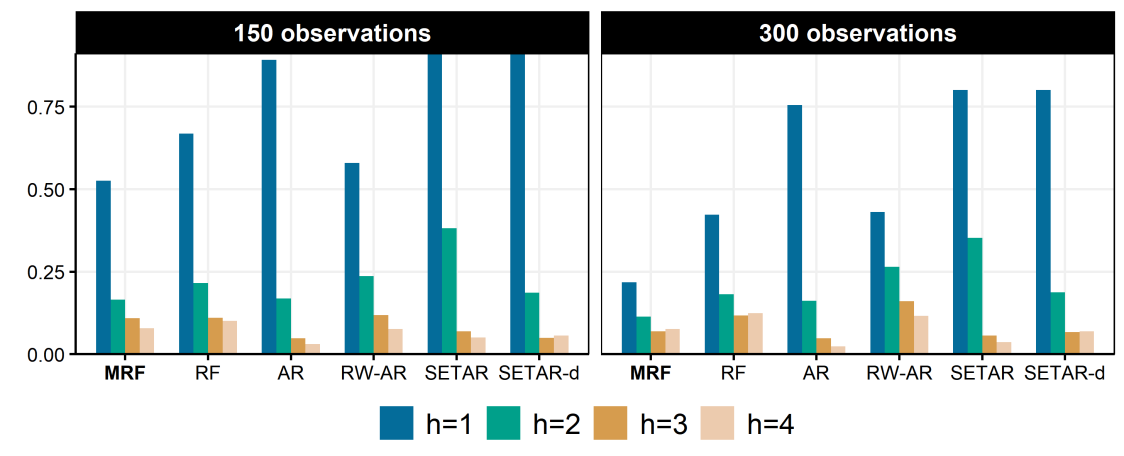

Simulations are divided in two parts. The first shows that Autoregressive Random Forest (ARRF) delivers forecasting gains over standard nonlinear time series model when the true DGP mixes both endogenous and exogenous time-variation. Moreover, the former is very resiliant against traditional approaches, even when the DGP matches the latter’s restrictive assumptions. Additionally, those simulations will numerically document the superiority of ARRF over RF when the AR part is pervasive (as discussed in section 2.5.1). Overall, this helps rationalizing forecasting results from section 4, where ARRF supplants TARs for the vast majority of targets.

The second simulations section considers simpler linear parts and look at how the algorithm behaves when is large. Further, I focus on itself and its credible regions. The main point is to visually show that (i) GTVPs adapts nicely to a wide range of DGPs and (ii) are not prone to discover inexistent time-variation.

3.1 Comparison of ARRF to Traditional Nonlinear Autoregressions

I consider 3 DGPs: Autoregression (AR), Self-Exciting Threshold ARs (SETAR), and a SETAR model that collapse to an AR (via a structural break). Those DGPs include two types of time variations, endogenous () and exogenous ().222222Since a structural break is just a threshold effect with respect to variable , one can conclude without loss of generality that similar results would be obtained using different additional switching variables. They are meant to encapsulate compactly the usual nonlinearities considered in empirical studies, like dependence on the state of the business cycle (AG2012; rameyzubairy2018) and exogenous time variation (clarida2000).

For all DGPs, . The simulated series sample size is either or . The last 40 observations of each sample consist the hold-out sample for evaluation. I forecast 4 different horizons: . Models are estimated once at the last available data point.

Models. SETAR, Rolling-Window (RW) AR, Random Forest (RF) and Autoregressive Random Forest (ARRF) are included. Iterated SETAR forecasts are obtained via the standard bootstrap method (clements1997setar) and all the others are generated via direct forecasting. That is, in the latter case, I fit the model directly on rather than iterating forward the one-step ahead forecast. To certify that the observed differences between SETAR and other models is not merely due to the choice of iterated vs direct forecasts – a non-trivial choice in many environments (chevillon2007direct) –, I also include SETAR-d where "d" means its forecasts were alternatively obtained by direct forecasting.

In all simulations, MRF’s includes 8 lags of and a time trend, which match what will be referred to in section 4 as "Tiny ARRF". Thus, unlike TARs, it is "allowed" to split on what we know (by the DGP choices) to be useless regressors (especially at horizon ). The specified linear part for all models matches that of the true DGP ().

Performance Metric. Performance is evaluated using the mean squared prediction error (MSPE). In simulation , for the forecasted value at time made steps ahead, I compute

100 different simulations are considered, which means the total number of squared errors being averaged for a given horizon and model is 10040=4000. To provide a visually useful normalization, bar plots report ’s relative to that of the oracle, who knows perfectly the law of motion of time-varying parameters .232323Precisely, if the model has a break and a switching variable, it knows exactly the break points, thresholds and AR parameter values in each regime. The only things the oracle does not know are the future shocks (), and the out-of-sample evolution of parameters () – unless the latter is purely deterministic. Formally, the metric is

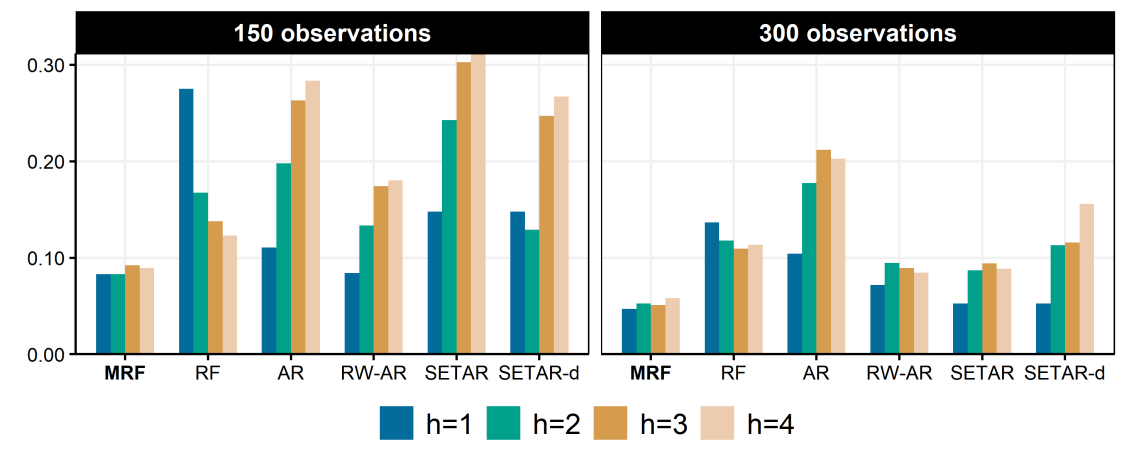

SETAR Morphing Instantly into AR(2). The two sources of time-variation are combined to display MRF’s edge in this not so implausible situation. Further,

can rightfully be hypothesized for some economic time series: complex dynamics up until the mid-1980’s followed by a very simple autoregressive structure during the Great Moderation.242424The AR has and the SETAR has . Results for the latter in isolation are in Appendix A.5. In Figure 1(a), MRF comes out as the best model for all horizons in the smaller sample. RF fails particularly at short horizons because it attempts to model all dynamics nonparametrically. Doubling the sample size helps, but its disimprovement with respect to the oracle remains at least twice as large as that of MRF. SETAR and AR both focus on dynamics but are misspecified. Their increase in relative RMSE is about thrice that of MRF at longer horizons for the shorter sample. For horizon 1, RW-AR does equally well as MRF, which is expected in this DGP since it discards earlier observations we only know ex-post to be harmful. Thus, in this DGP much akin to that of the hypothetical inflation tree of section 2.1, MRF comes out as the clear winner.

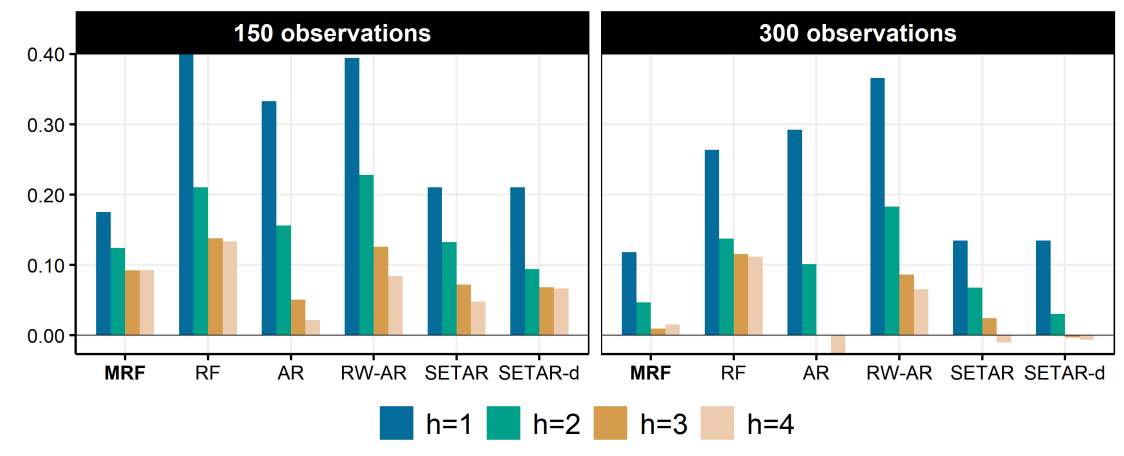

Persistent SETAR. DGP 2, with , represents an endogenous switching process which may suit well real activity variables: it includes high/low regimes, and mildly different dynamics in each of them. Can MRF match traditional nonlinear times series model when the world is nonlinear, yet simple? The broad answer from Figure 1(b) is yes. For all horizons and sample sizes considered, MRF is practically as good as SETAR, the optimal model in this context. Because of its capacity to control overfitting, MRF will be competitive even if nonlinearities turn out to be as simple as often postulated in the empirical macroeconomics literature. With the relative importance of changing persistence, RF cannot match MRF’s performance and is trailing behind with RW-AR.252525In Appendix A.5, the case where the changing persistence is less important is considered. Nevertheless, RF improves substantially at shorter horizons when the sample size increase. Finally, AR is resilient at longer horizons but is much worse than MRF and SETAR at shorter ones.

No Time-Variation. Given the widespread worry that ML-based algorithms can overfit, a time-invariant DGP is a natural check.262626Also, the incredible resilience of linear AR models is well documented in the macroeconomic forecasting literature (see KLS2019 and references therein). Can MRF still deliver competitive performance if reality equates simple linear dynamics? Results for DGP 3, an AR(2) process with , are reported in Figure 1(c). As expected, AR is the best model for all horizons and both sample sizes. The RW-AR suffers from high variance and it is assumed that tuning the window length in a data-driven way would help. Plain RF struggles irrespective of the sample size. For the smaller sample, MRF performs as well as the tightly parametrized SETARs. Their marginal increases in RMSE with respect to the oracle are typically less than 10%, which is small in contrast to that of previous DGPs. More observations generally helps AR, the iterated SETAR, and MRF especially at longer horizons.

About Misspecification of . Most of the reported gains from using MRF come from avoiding misspecification when a more complex DGP arises. What happens if the arbitrary linear part in MRF, , is itself misspecified? Figure 14 in the appendix report corresponding results. For all DGPs under consideration, a "Bad" MRF, where is composed of two white noise series (instead of the first two lags of ), performs similarly well (or bad) as plain RF.272727This result may not hold, however, when the law of motion for the intercept is highly complex and requires a great number of split (unlike what is considered here). This is due to the linear part restricting the depth of trees (with to what plain RF could allow for), especially if observations are scarce. In that regard, increasing the ridge penalty (via ) will help. Nevertheless, in practice, it is a safer bet to use a small linear part if uncertainty around its composition is high. More on this and the effect of hyperparameters can found in appendix A.4.

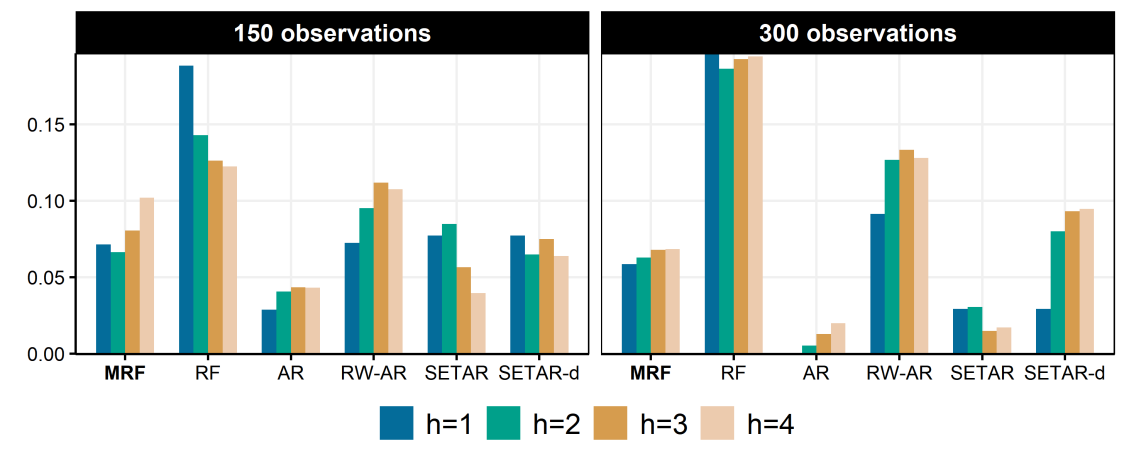

Summary. First, when the true DGP is not that of the tightly parametrized classical nonlinear time series model, the more flexible MRF does better. Second, when classical nonlinear time series model are fitted on their corresponding DGPs, those perform better than MRF – but only marginally. Third, when there are pervasive linear autoregressive relationships, plain RF struggles. Fourth, MRF and RF relative performance both increase with the number of observations but MRF’s one increases faster if the linear part is well-chosen. In Appendix A.5, results for 3 additional DGPs are reported: another SETAR, AR with a structural break, and SETAR morphing in another SETAR (through a break). Again, MRF is shown to have an edge when other models are misspecified and almost as good when those are not.

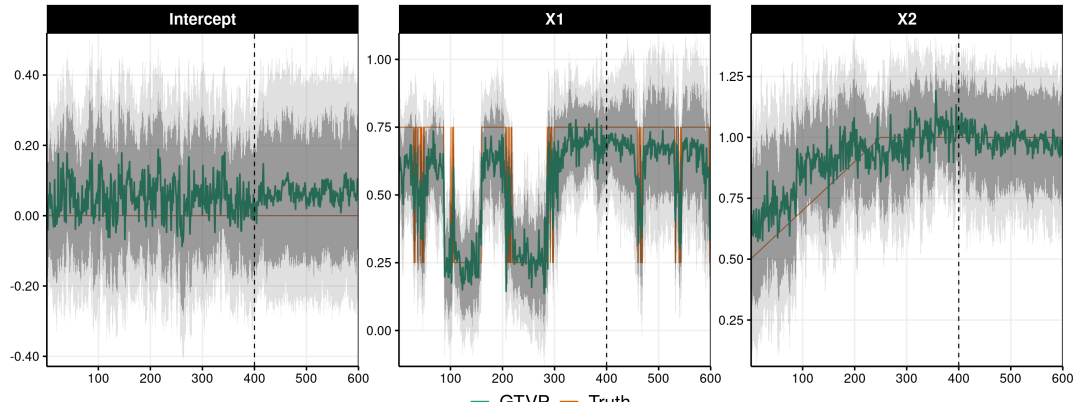

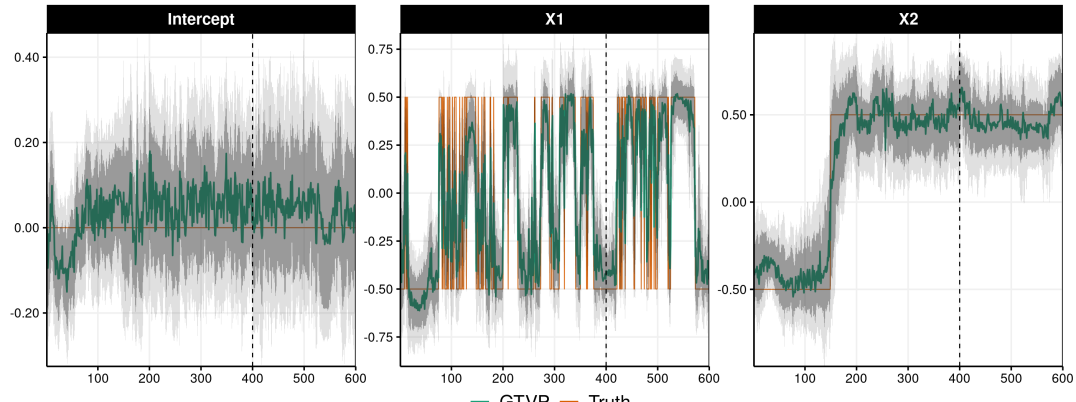

3.2 A Look at GTVPs when is Large

A notable difference between the simulations presented up to now and the applied work being carried in later sections is the size of . In many macro applications, there is no shortage of variables to include in MRF’s . For instance, the FRED-QD data base (mccracken2020fred) contains over 200 potential predictors that can join lags of and a time trend within . As a result, there is now considerable interest in allowing for time variation in empirical models using large information sets. For instance, koop2013large propose large TVP-VARs while abbate2016changing extend bernanke2005measuring’s factor-augmented VAR to be time-varying. Interestingly, those papers (and the corresponding literature) almost exclusively focus on a setup where, in MRF notation, is large and is extremely small (usually just ). Of course, MRF could deal with this case (as discussed in section 2.3), but its edge will be more apparent when we let the RF part deal with large data and keep concise. Indeed, in addition to lessened misspecification concerns, RFs also benefits from more data through increased randomization – which prevents fully grown trees from overfitting (breiman2001; MSoRF).

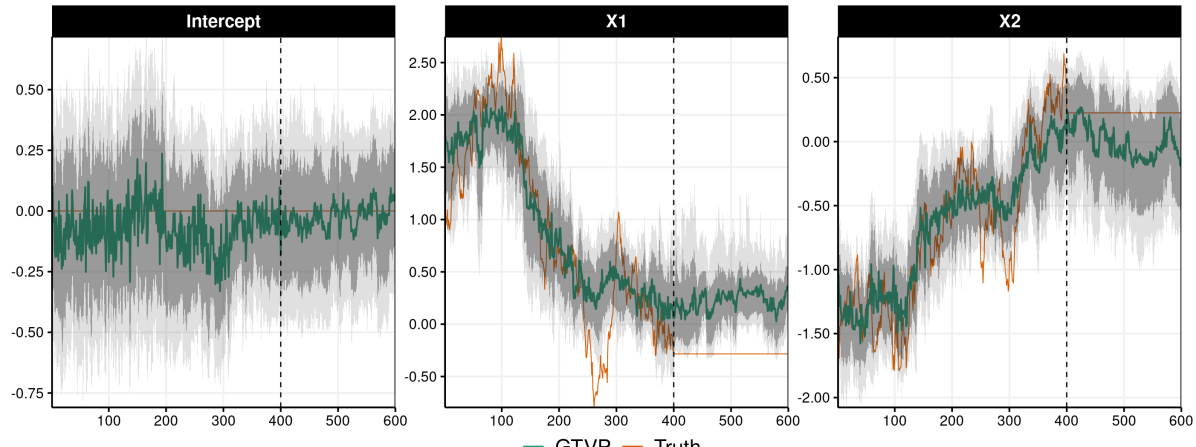

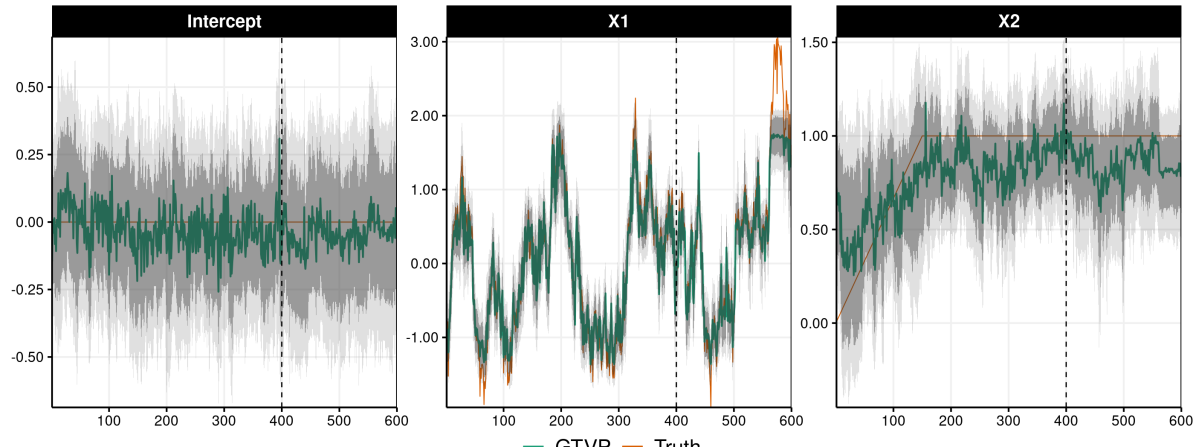

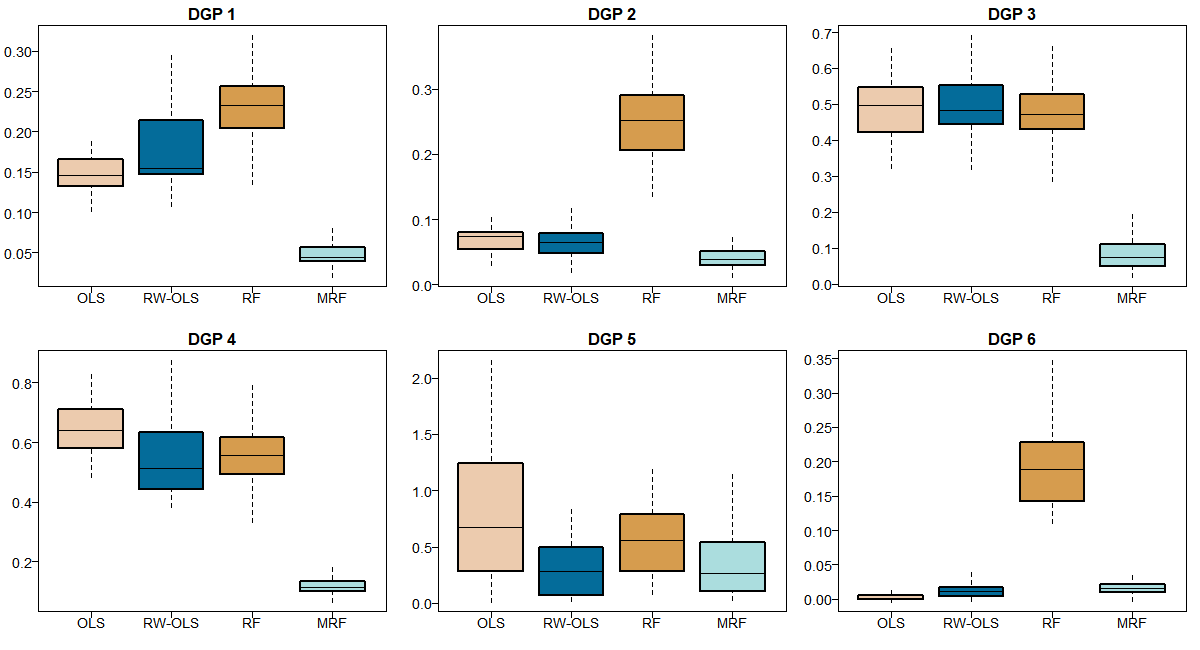

The additional simulations go as follow. First, I simplify the analysis by looking at a static model with mutually orthogonal but autocorrelated regressors and , both driving according to some process. I simulate each of them for 1000 periods and estimate the models with the first 400 observations. The remaining 600 are used to evaluate the out-of-sample performance. The signal to noise ratio is calibrated to which is about what is found (out-of-sample) for most models in the empirical section.

The only remaining questions are that of the constitution of and the generation of ’s. I create two autocorrelated (but not cross-correlated) factors. Out of each of them, I create 50 series with a varying amount of additional white noise.282828To be precise, their standard deviation is % that of the original factor standard deviation. Joining those 100 series with lags of and a time trend, the final size of is slightly above 100. Finally, ’s are functions of the underlying first factor which (like the second) is not directly included in the data set. In certain DGPs, some ’s will also be a pure function of (like random walks, structural breaks).292929To clarify, the second factor and underlying series are completely useless to the true DGP – arguably mimicking the inevitable when using a data base of the size of FRED-QD. Table 1 summarizes the six DGPs in words.

| DGP # | Intercept | Residuals Variance | ||

|---|---|---|---|---|

| 1 | Switching | Switching | Switching | Flat |

| 2 | Flat | Random Walk | Random Walk | Flat |

| 3 | Flat | Latent factor directly | Slow Change (function of ) | Flat |

| 4 | Flat | Switching | Slow Change (function of ) | Flat |

| 5 | Flat | Switching | Structural Break | Flat |

| 6 | Flat | Flat | Flat | Stochastic Volatility |

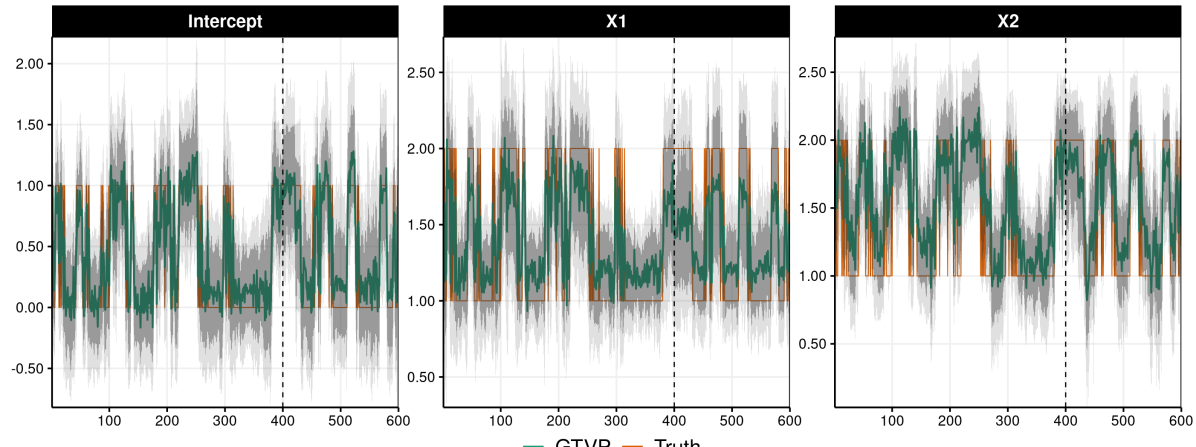

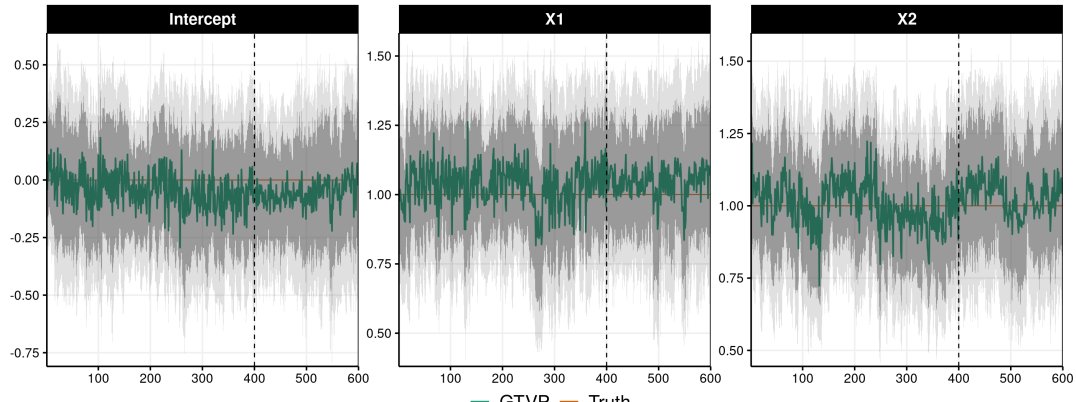

More illustratively, Figures 2 and 15 (appendix) plots one example of each DGPs as well as the estimated GTVPs and their credible region (as discussed in section 2.7). It is visually obvious that GTVPs are adaptive in the sense that it can discover which kind of time-variation is present in the data while estimating it. In Figure 2(a), MRF successfully estimate the rather radical switching regimes present in all coefficients. In Figure 2(b), MRF realizes that almost all of is useless because true follow random walks. Rather, it manages to fit ’s nicely by relying on a multitude of splits. In Figure 2(c), things get "easier" for the true as it is driven directly by the first latent factor. MRF discovers that and leverage it to have a very tight fit for it, both in-sample and out-of-sample. This is merely a reflection that if time variation can be constructed by simple interaction terms, this is certainly the easiest statistical route to by – and MRF chooses it thanks to its inherent ability to perform "time variation selection".

Figure 16 reports distributions of RMSE differentials with respect the oracle (the forecast that knows the ’s law of motion). MRF performance is compared to OLS, Rolling-Window OLS (RW-OLS) and plain RF. As expected, MRF outperforms all alternatives by wide margins for most DGPs. By construction, RW-OLS and OLS also perform well for DGP 5 (random walks) and DGP 6 (constant parameters). Nonetheless, it is reassuring to see that MRF either performs much better than OLS or worse by a thin margin (in cases with no time-variation).

4 Macroeconomic Forecasting

In this section, I present results for a pseudo-out-of-sample forecasting experiment at the quarterly frequency using the dataset FRED-QD (mccracken2020fred). The latter is publicly available at the Federal Reserve of St-Louis’s web site and contains 248 US macroeconomic and financial aggregates observed from 1960Q1. The forecasting targets are real GDP, Unemployment Rate (UR), CPI Inflation (INF), 1-Year Treasury Constant Maturity Rate (IR) and the difference between 10-year Treasury Constant Maturity rate and Federal funds rate (SPREAD). These series are representative macroeconomic indicators of the US economy which is based on GCLSS2018 exercise for many ML models, itself based on KLS2019 and a whole literature of extensive horse races in the spirit of SW1998comparison. The series transformations to induce stationarity for predictors are indicated in mccracken2020fred. For forecasting targets, GDP, UR, CPI and IR are considered and are first-differenced. For the first two, the natural logarithm is applied before differencing. SPREAD is kept in "levels". Forecasting horizons are 1, 2, 4, 6 and 8 quarters.

The pseudo-out-of-sample period starts in 2003Q1 and ends 2014Q4. I use expanding window estimation from 1961Q3. Models are estimated (and tuned, when applicable) every two years. For all models except SETAR and STAR, I use direct forecasts, meaning that is obtained by fitting the model directly to rather than iterating one-step ahead forecasts. TAR iterated forecasts are calculated using the block-bootstrap method which is standard in the literature (clements1997setar).

Following standard practice, the quality of point forecasts is evaluated using the root Mean Square Prediction Error (MSPE). For the out-of-sample (OOS) forecasted values at time of variable made steps ahead, I compute

The standard dieboldmariano (DM) test procedure is used to compare the predictive accuracy of each model against the reference AR(4) model. is the most natural loss function given that all models are trained to minimize the squared loss in-sample.

It has been argued in section 2.6 that feature engineering matters crucially when the number of regressors exceeds the sample size. , the set of variables from which RF can select, is motivated by such concerns. Its exact composition is detailed in Table 2. Among other things, it includes both cross-sectional and moving average factors, which are compressing information along their respective dimensions. The usefulness of MAFs is further studied in MDTM and found to help, mostly with tree-based algorithms. However, it is supplanted by a more computationally demanding (but more general) transformation of the raw data that MDTM propose specifically for ML-based macroeconomic forecasting.

| What | Why | How |

|---|---|---|

| 8 lags of | Endogenous SETAR-like dynamics | – |

| Exogenous "structural" change/breaks | – | |

| 2 lags of FRED | Fast switching behavior | – |

| 8 lags of 5 traditional factors | Compress cross-sectional information ex-ante | Usual PCA |

| 2 MAFs for each variable | Compress lag polynomial information ex-ante | PCA on 8 lags of |

Models. To better understand where the gains from MRF are coming from, I include models that use different subsets of ideas developed in earlier sections. Those are summarized in Table 3. The competitive data-rich models are in the benchmarks group. Non-linear time series models are also included as they share an obvious familiarity with ARRF. "Tiny" versions of both ARRF and RF are considered to gauge the effect from only having access only to a small — this could be the case for many non-US applications. Conversely, this helps quantify how a data-rich environment contributes to the success of ARRF versus its plain flexibility. Indeed, Tiny ARRF corresponds to what was shown in the "data-poor" simulations (section 3) to be a generalization of TARs and related models.

Here are some remarks motivating some inclusions and specifications choices. To assess the marginal effects of MAFs alone, Lasso, Ridge and RF are considered using — those are known to handle high-dimensional feature space. When it comes to FA-ARRF, I opt for a parsimonious linear specification including one lag of the first two factors. First, concise models make interpretation easier. Second, considering compact linear specifications within MRF is usually the better strategy. Parameters (including the intercept) are all RFs in their own right and can palliate to the omission of marginally important features, if need be. Consequently, it is desirable to fix a humble linear part and let ’s take care of the rest.303030Further backing a parsimonious choice (with MRF), mccracken2020fred report that the first two factors account for 30% of the variation in the data while adding two more only bumps it up to 41%, making the last two presumably more disposable in our context. Finally, as discussed in mccracken2020fred, the first factor mostly loads on real activity variables while the second is a composite of forward-looking indicators like term spreads, permits and inventories. They are baptized and interpreted accordingly.

| Name | Acronym | Linear Part () | RF part |

|---|---|---|---|

| Autoregression | AR | ||

| Factor-Augmented Autoregression | FA-AR | ||

| Plain Random Forest | RF | Raw data313131Precisely, this means 8 lags of FRED-QD, after usual transformations for stationarity have been applied. | |

| Low-Dimensional Plain RF | Tiny RF | ||

| Plain RF but using | RF-MAF | ||

| RF-MAF on de-correlated | AR+RF | Filter first with an AR(2), then RF | |

| Autoregressive Random Forest | ARRF | ||

| Low-Dimensional Autoregressive RF | Tiny ARRF | ||

| Factor-Augmented Autoregressive RF | FA-ARRF | ||

| Vector Autoregressive RF323232Note that the VAR appellation refers to the linear equation consisting of typical ”small monetary VAR”. The model remains univariate and direct forecasts are used. | VARRF | ||

| Self-Exciting Threshold AR | SETAR | ||

| Smooth Transition AR333333The state variable is , as in SETAR. | STAR | ||

| 10 years Rolling-Window AR | RW-AR | ||

| Time-Varying Parameters AR343434Estimated and tuned via the Ridge approach proposed in GC2019. | TV-AR | ||

| LASSO using | LASSO-MAF | ||

| Ridge using | Ridge-MAF |

-

Notes: models are classified in 3 categories: benchmarks, MRFs (and related prototypes), and misc (non-linear time series models, other reasonable additions). The main analysis in section 4.1 omits the \nth3 club for parsimony.

4.1 Main Quarterly Frequency Results

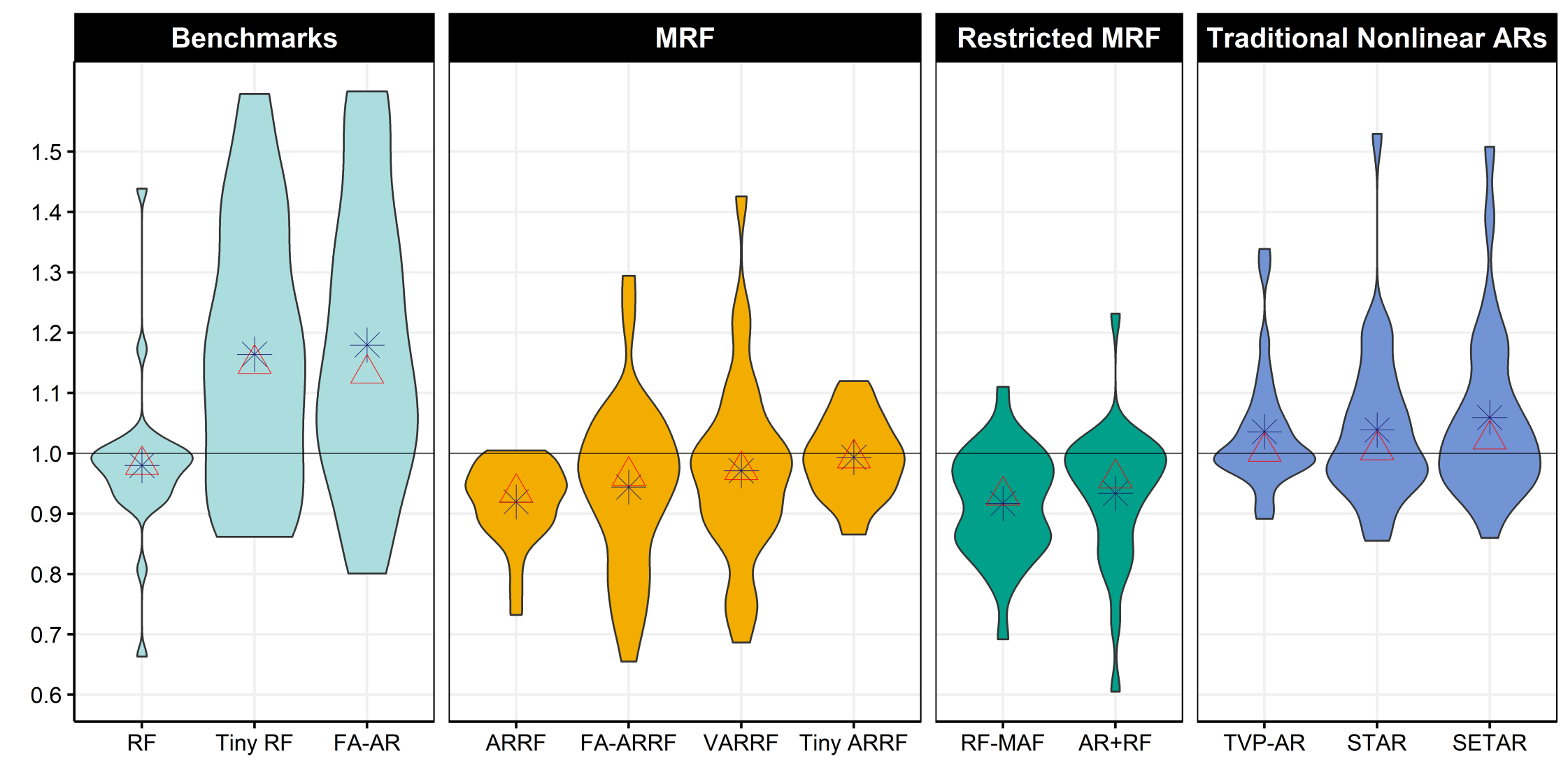

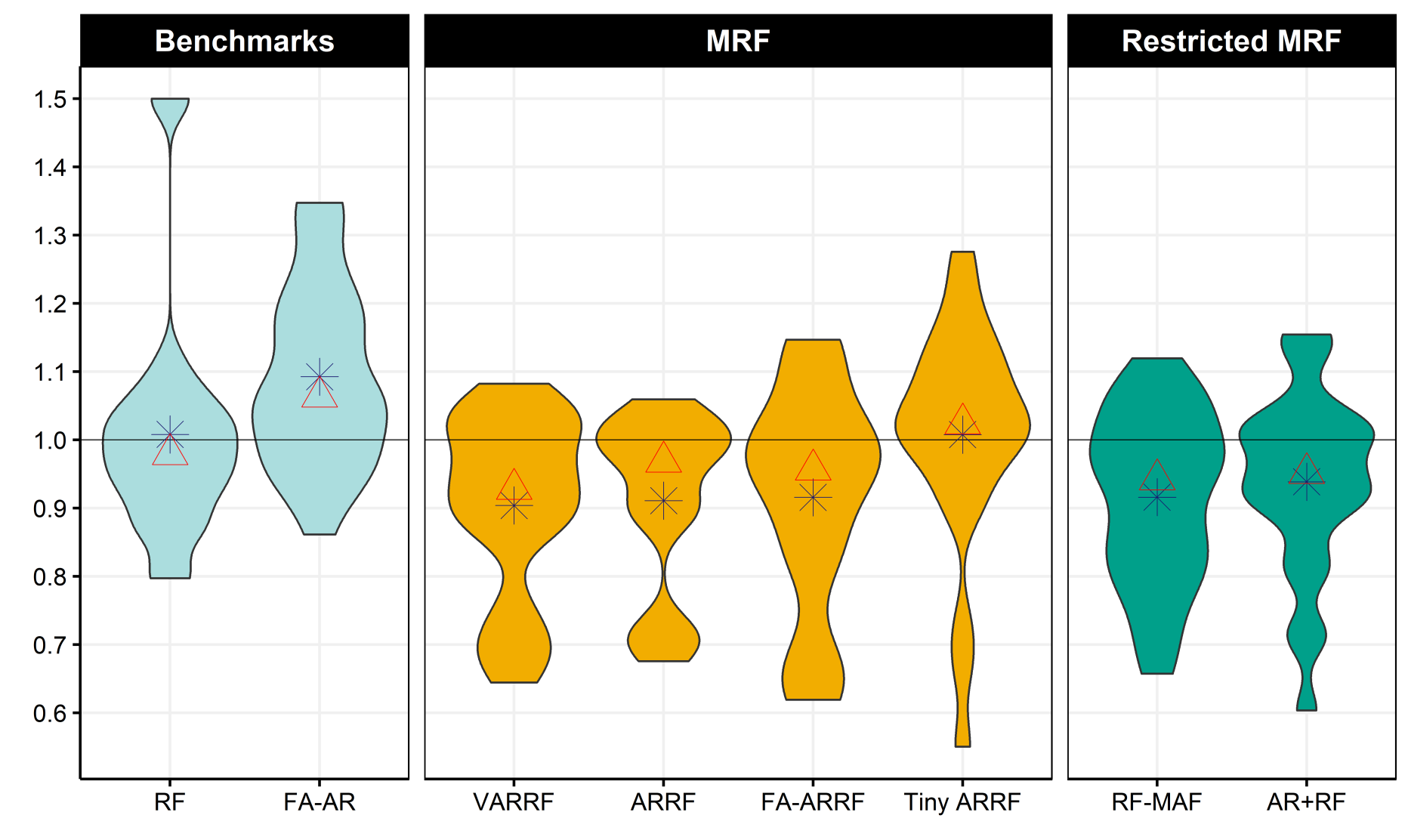

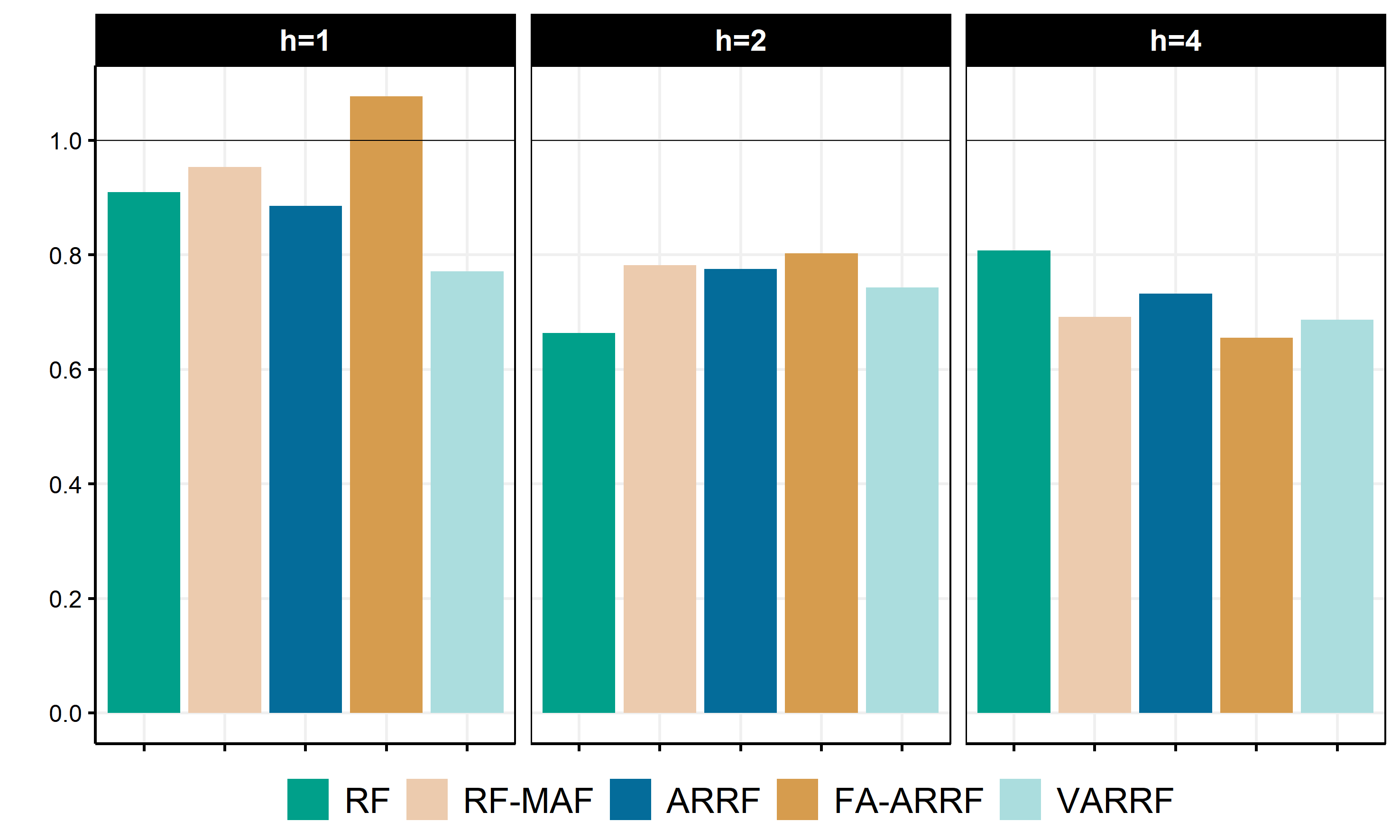

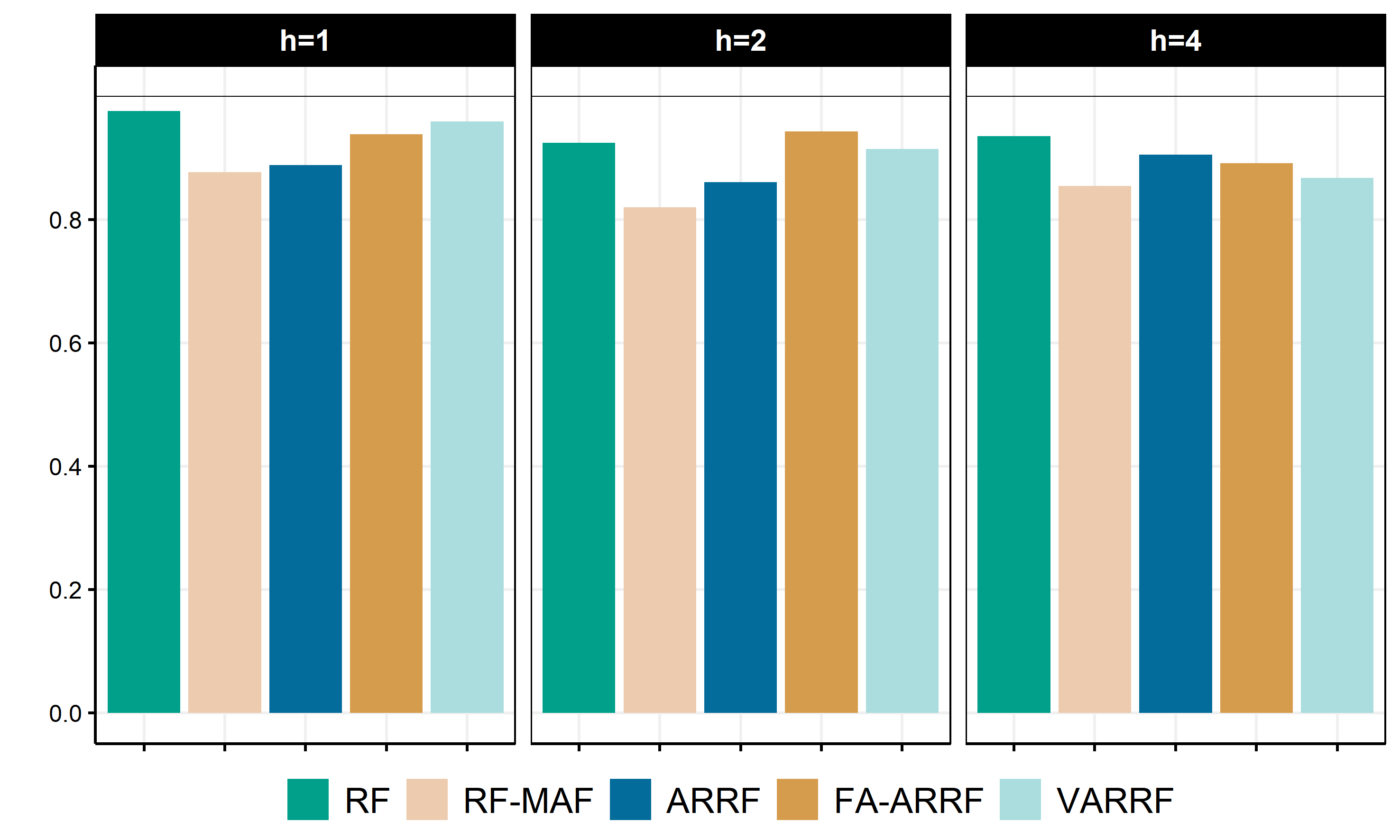

Violin plots are used throughout to summarize dense RMSEs tables (like Table 4). I report the distribution of . This is informative about the overall ranking and versatility of considered models. Of course, being ranked first does not imply being the best model for every and . Rather, it means that it performs better on average, over all targets.

Here are interesting observations from Figure 3. Clearly, MRFs deliver important gains over both the AR and FA-AR benchmarks (the latter is second to last). ARRF has a noticeably small mass above the 1 line. In other words, there are no targets for which ARRF does significantly worse than its OLS counterpart, which makes it atypically adaptable among nonlinear autoregressions. A look at Table 4 confirms this observation also extends to FA-ARRF vs FA-AR. The simplification AR+RF, ranks third with a performance that is much more volatile. This suggests that imposing time-invariant dynamics can sometimes help (see one example in Figure 5), but can also be highly detrimental (as reported for inflation). Of course, that we do not know ex-ante, and it is why AR+RF does not inherit ARRF’s "off-the-shelf" quality.

MAFs are useful: RF-MAF does much better than RF which uses the raw data. The latter only exhibits conservative gains over the benchmark. Thus, it is understood that a fraction of MRFs’ forecasting gains emanates from considering more sensible transformations of time series data – and which are trivially implementable. The relevance of MAFs is studied more systematically in MDTM.

FA-ARRF provides very substantial improvements, but can also fail. This is the linear part’s doing: FA-AR will mostly work well for real activity variables while AR is a jack of all trades. Thus, it is not surprising to see FA-ARRF inherit some of these uneven properties, albeit to a much milder extent. For instance, in Table 4, FA-AR is noticeably worse than AR for all inflation horizons, while FA-ARRF beats AR for all of them. This phenomenon is well summarized by FA-AR being second to last overall, well behind FA-ARRF. VARRF has a behavior similar to that of FA-ARRF, but with less highly noticeable gains.

Does a large pay off? Most of the time, yes. It is worth re-emphasizing that restricting restricts the space of time-variations possibilities as well as the potential for trees diversification. Nonetheless, if the restrictions are "true", gains are possible.353535An interesting specific case is Tiny ARRF being close behind ARRF for inflation. This is intuitive given that INF has often been associated with exogenous time variation. This is reported to be a rare occurrence, with ARRF Tiny ARRF (and RF Tiny RF) for almost any target. Thus, we can safely conclude that a rich is desirable, with being tasked with selection of relevant items.

As discussed in earlier sections, ARRF connects to the wider family of nonlinear autoregressive models. It clearly does better on average than SETAR and Smooth-Transition TAR. This advantage is attributable to both a more flexible law of motion and a large . Tiny ARRF is better than the TAR group, while ARRF is much better. Linking this result to those of simulations, this means that no TAR is likely the true model.

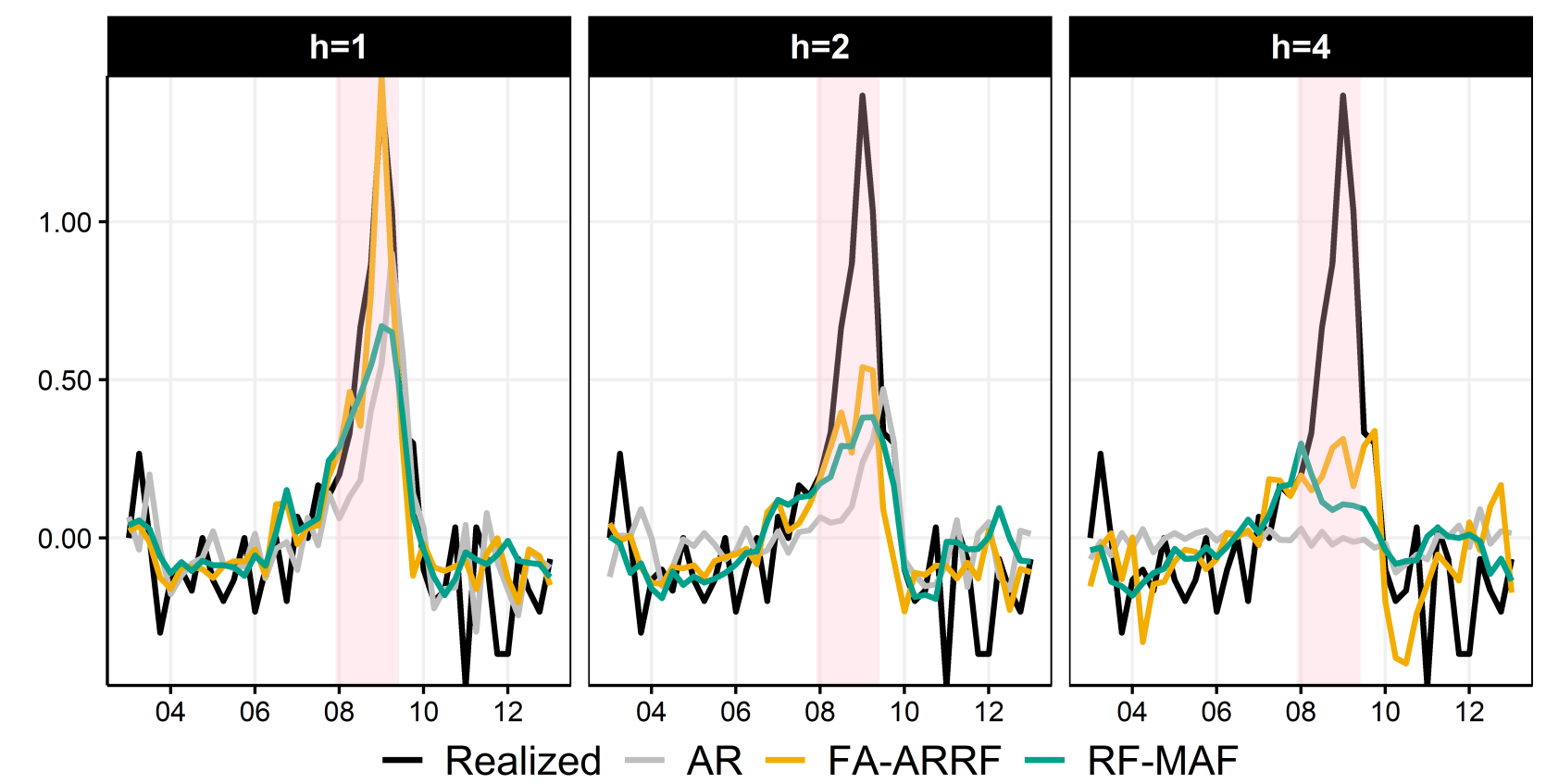

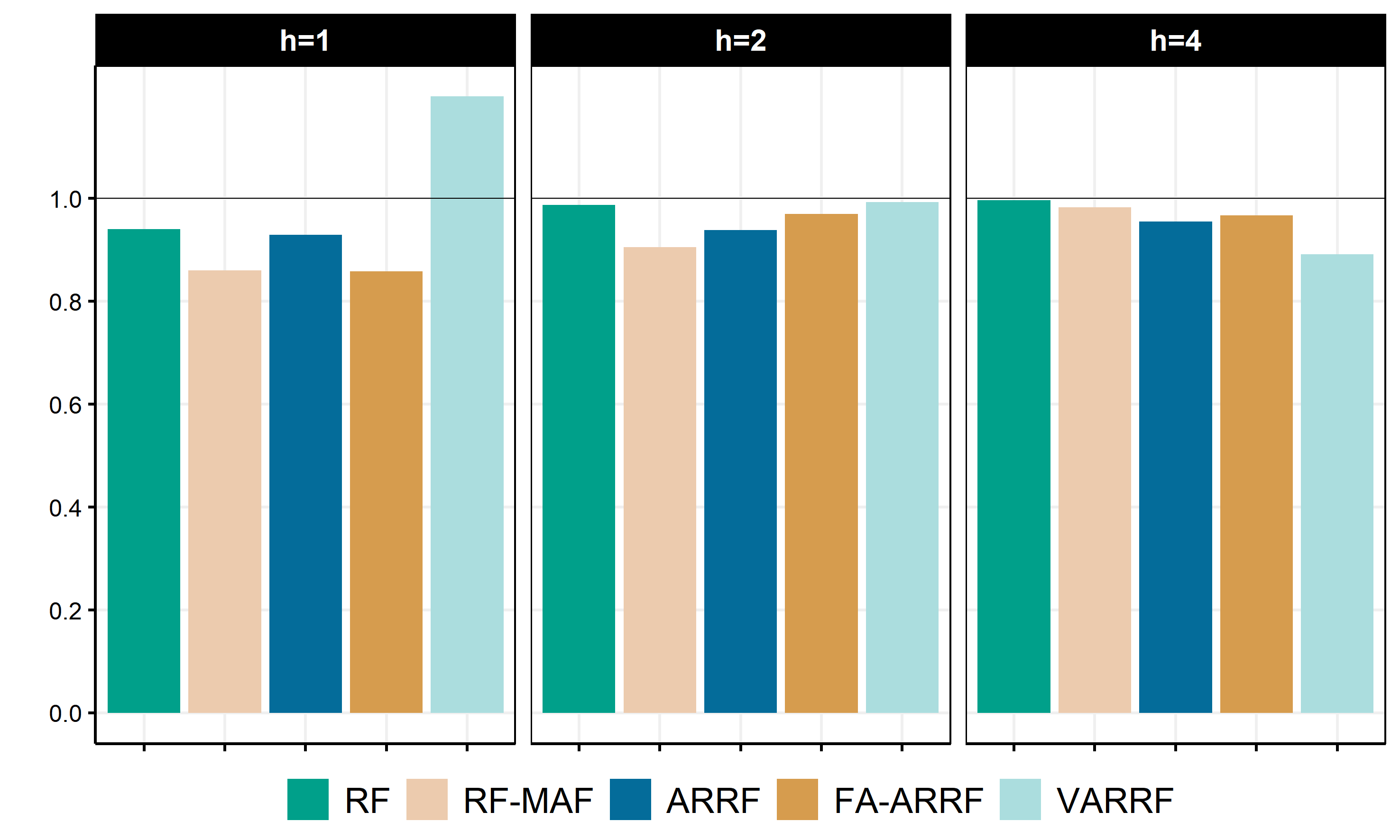

Real Activity Targets. Figure 4 reports results for UR. FA-ARRF dominates strongly. Table 4 confirms it is the best model for all horizons but the last one (8 quarters ahead, where the encompassed RF-MAF is the best). Clearly, at an horizon of one quarter, the preferred model successfully predicts the drastic rise in unemployment during the Great Recession. Rather than responding with a lag to negative shocks (which is what we observe from AR and ARRF), the model visibly predicts them. As a result, improvements in RMSE are between 25% and 30% over AR for all horizons. Specifically, predicting UR (change) with FA-ARRF at yields an unusually high out-of-sample of about 80%. The nearly perfect overlap of the yellow and black lines highlight the absence of a one-step ahead shock around 2008. Note that FA-AR and STAR forecasts are omitted from Figure 4(b) to enhance visibility. STAR forecasts are either similar or worse than the benchmark (as often found for nonlinear time series models). FA-AR forecasts at follows a proactive pattern similar to the yellow line, but with a 1 to 2 quarter delay – hence the inferior results.

For , the quantitative rise is nowhere near the realized one, but it reveals 6 months ahead the arrival of a significant economic downturn. Additionally, ARRF and FA-ARRF both flag one year ahead the arrival of a rise in unemployment, which is a quality shared by very few models. The barplot in Figure 4 (and Table 4) provides a natural decomposition of FA-ARRF’s gains. Adding the MAFs to an otherwise plain RF procures an improvement of roughly 15% across all horizons (RF-MAF RF, in Table 4). The linear FA-AR part and the rest of algorithmic modifications discussed in section 2 provide an additional reduction of 10% to 15% depending on the forecasted horizon (FA-ARRF RF-MAF and FA-ARRF FA-AR). It is noteworthy that good results for are mechanically close to impossible with a plain RF since it cannot extrapolate – i.e., predict values of that did not occur in-sample. In contrast, this is absolutely feasible within MRF thanks to the linear part.

GDP is known to have a lower signal-to-noise ratio. In Figure 18, FA-ARRF exhibits a bit less than a 20% drop in RMSE over the AR and nicely grasp the 2008 drop one quarter ahead.363636diebold1994measuring proposed an empirically sucessful regime-switching factor model. Given that line of work and more recent results in wochner2020dynamic, the FA-ARRF’s success is not an anomaly. However, FA-ARRF performance does not stand apart as much as it did for UR. One reason can be traced visually to predicting higher post-recession growth than its competitors. Finally, RF-MAF closing in on ARRF will be investigated on its own in section 5.2.1. In short, this occurs because once the time-varying intercept is flexibly modeled by RF, there is very little room left for autoregressive behavior (at the quarterly frequency).

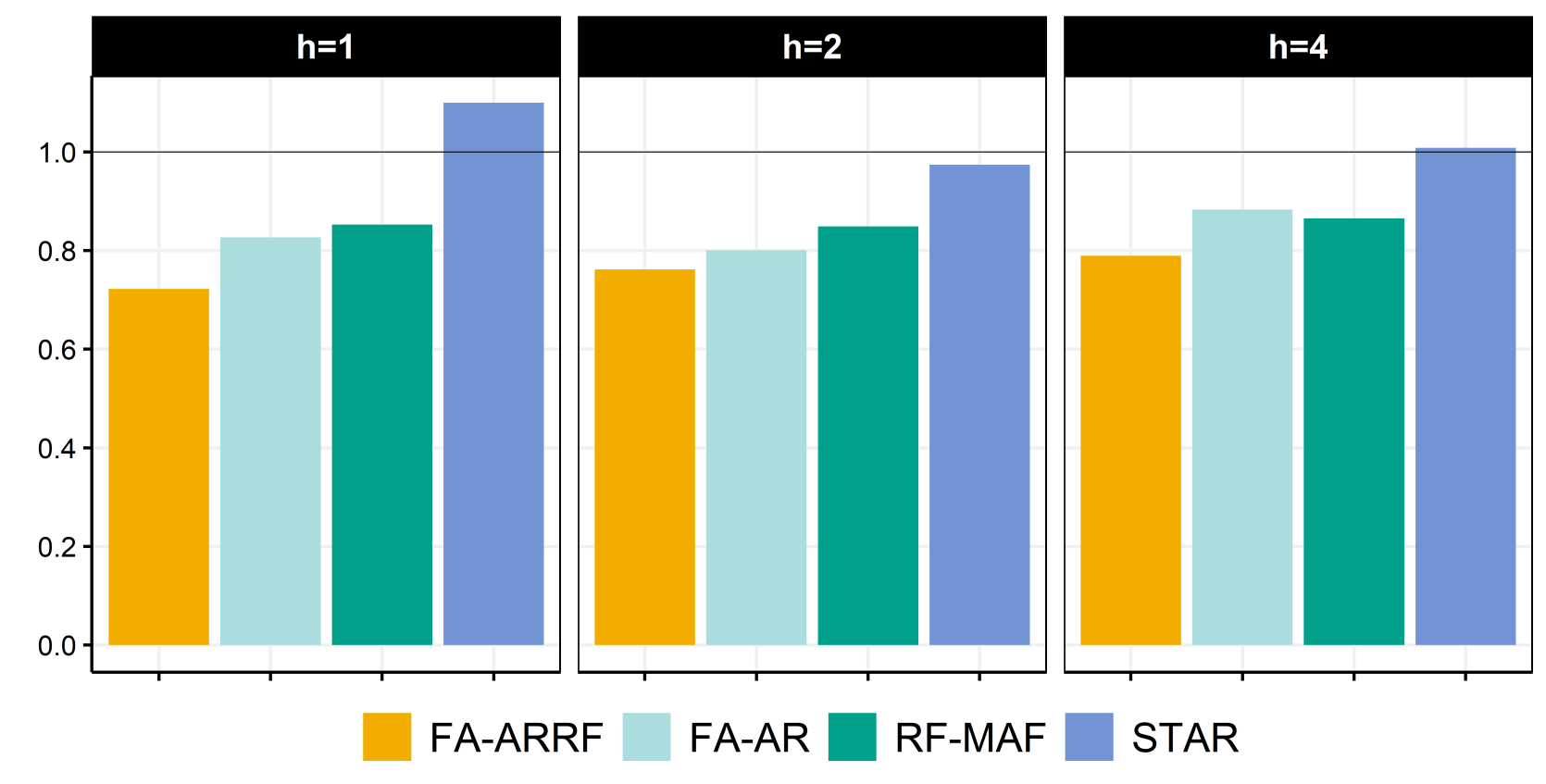

Spread and Inflation. VARRF shines for SPREAD (Figure 19) by capturing key movements, even up to a year ahead. The simpler AR+RF also does remarkably well. FA-ARRF provides successful one-year ahead forecasts. Overall, these results highlight the common importance of the autoregressive part, which is no surprise given SPREAD’s persistence. For INF, Table 4 displays that RF-MAF is the leading model (with ARRF close behind) reducing RMSEs by 12-15% for all horizons. I investigate this with GTVPs in section 5.2.1.

5 Analysis

Based on forecasting results, I concentrate on FA-ARRF’s GTVPs. Additionally, its parameters are easier to interpret (given factors are labeled) since regressors are mechanically orthogonal. First, I look at and analyze their behavior around the Great Recession. Second, I compare GTVPs to random walk TVPs, ex-post vs ex-ante, with a focus on the recessionary episode. Finally, I use a surrogate model approach to explain of the parameters’ paths in terms of observed variables.

5.1 Forecast Anatomy

’s characterize completely MRF’s forecasts. Thus, we can investigate GTVPs to understand results from the previous section. The FA-ARRF forecasting equation is

and naturally . To avoid overfitting, ’s are (as in section 3.2) the mean over draws that did not include observations to (a two-year block) in the tree-fitting process. Intuitively, this mimics in-sample the real out-of-sample experiment that starts here in 2007Q2.373737Note that this is partially different from what gave the results reported in section 4.1, where the model was re-estimated every 2 years. Here, estimation occurs once in 2007Q2.

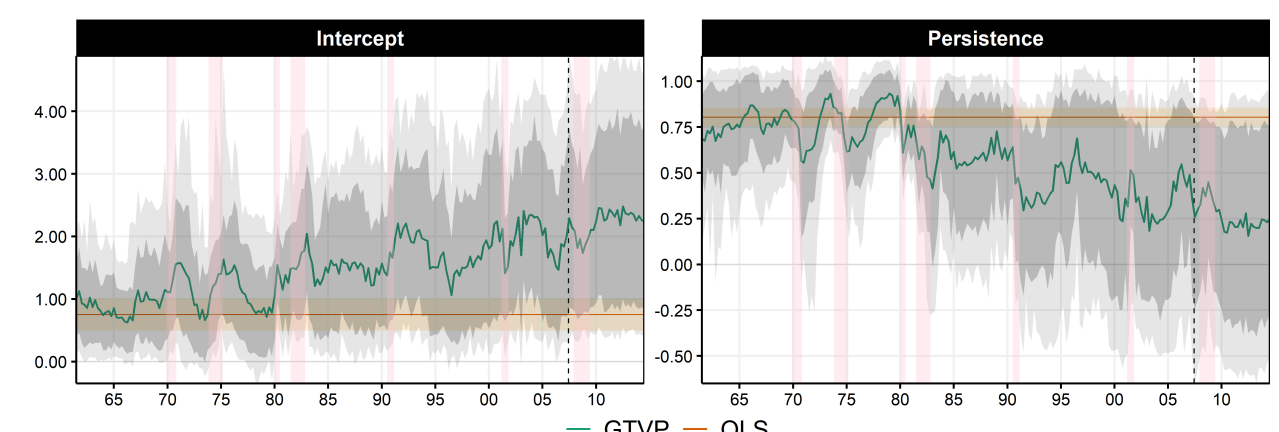

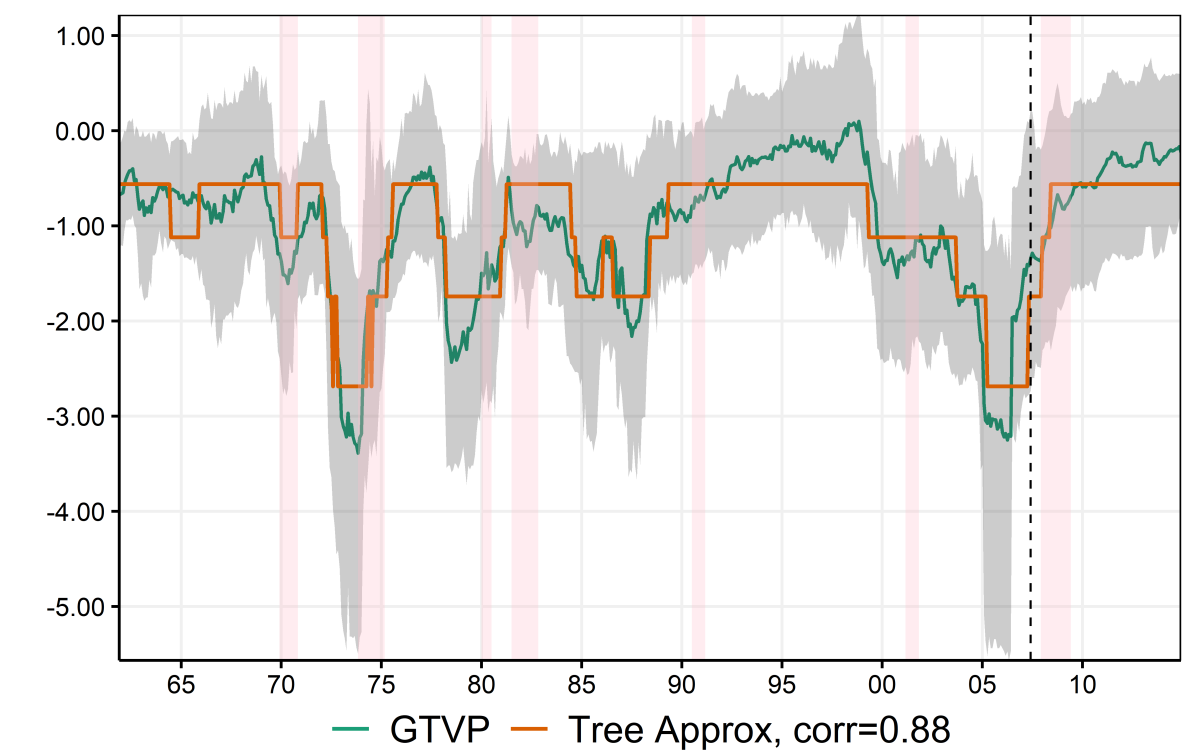

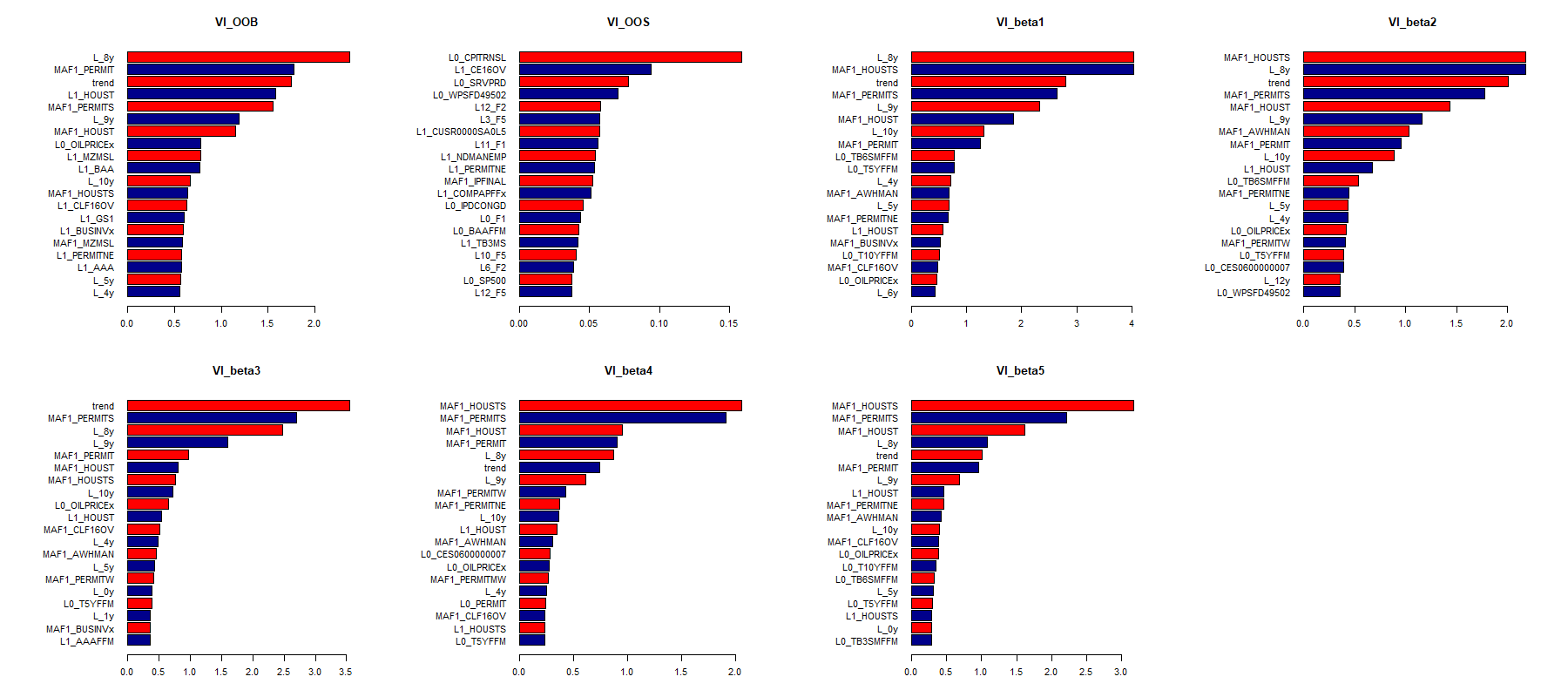

Figure 5 displays GTVPs underlying the successful one-step ahead UR change forecast. The intercept clearly alternates between at least two regimes and the "increasing UR" one is in effect circa 2008. In levels, this translates to UR alternating between a positive and negative (albeit small) trend. Overall persistence is strikingly time-invariant, and marginally smaller than for OLS estimates. The effect of , the real activity factor, is generally within OLS confidence intervals, suggesting that while almost doubles around recessions, this is subject to great uncertainty.

What is less uncertain, however, is the magnified contribution of the forward-looking factor during recessionary episodes, which stands out as the key difference with OLS. smooth-switching behavior can be best interpreted by remembering that is highly correlated with capacity utilization, manufacturing sector indicators, building permits and financial indicators (like spreads) (mccracken2020fred). Many of those variables are considered "leading" indicators and have often been found to increase forecasting performance, mostly before and during recession periods (stock1989new; estrella1998predicting; leamer2007housing). Recently, there has been renewed attention on the matter, with financial indicators highlighted as capable of capturing economic activity downside risk (adrian2019; delle2020modeling). This brand of nonlinearity can translate to a more active around business cycle turning points. MRF learns that, while OLS provides a clumsy average of two regimes. In Figure 5, the obvious consequence of OLS’ rigidity is being over-responsive to leading indicators during tranquil economic times, and under-responsive when it matters.

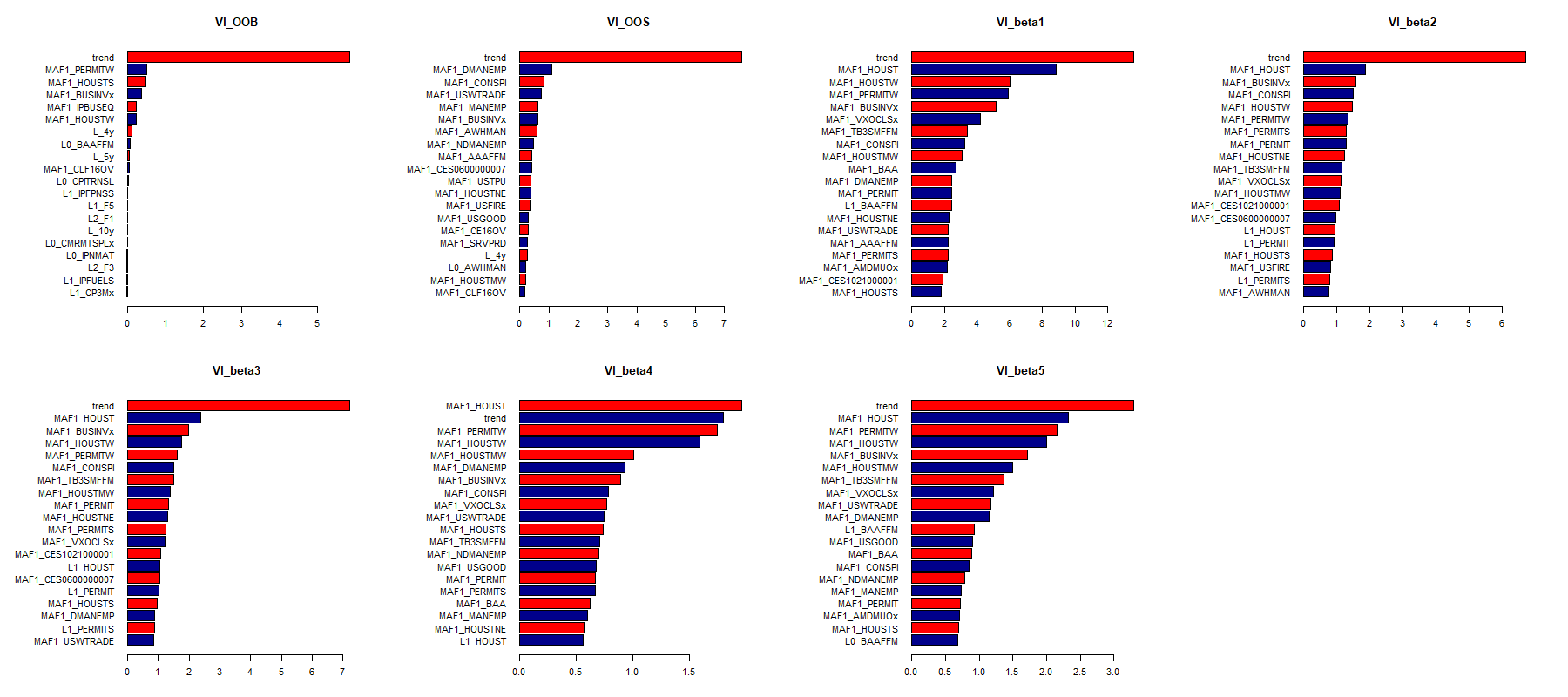

Section 5.3 will investigate formally the underlying variables driving this time variation. Figure 21 displays equivalent for GDP one quarter ahead. The pattern is also visible for GDP, but it is quantitatively weaker and more uncertain – which is is no surprise given GDP being generally noisier than UR. Additionally, slow and relatively mild long-run change is observed. Interestingly, has been shrinking since the mid 1980s, and its regime dependence exhibited in the first four recessions is no more.

5.2 Comparing Generalized TVPs with Random Walk TVPs

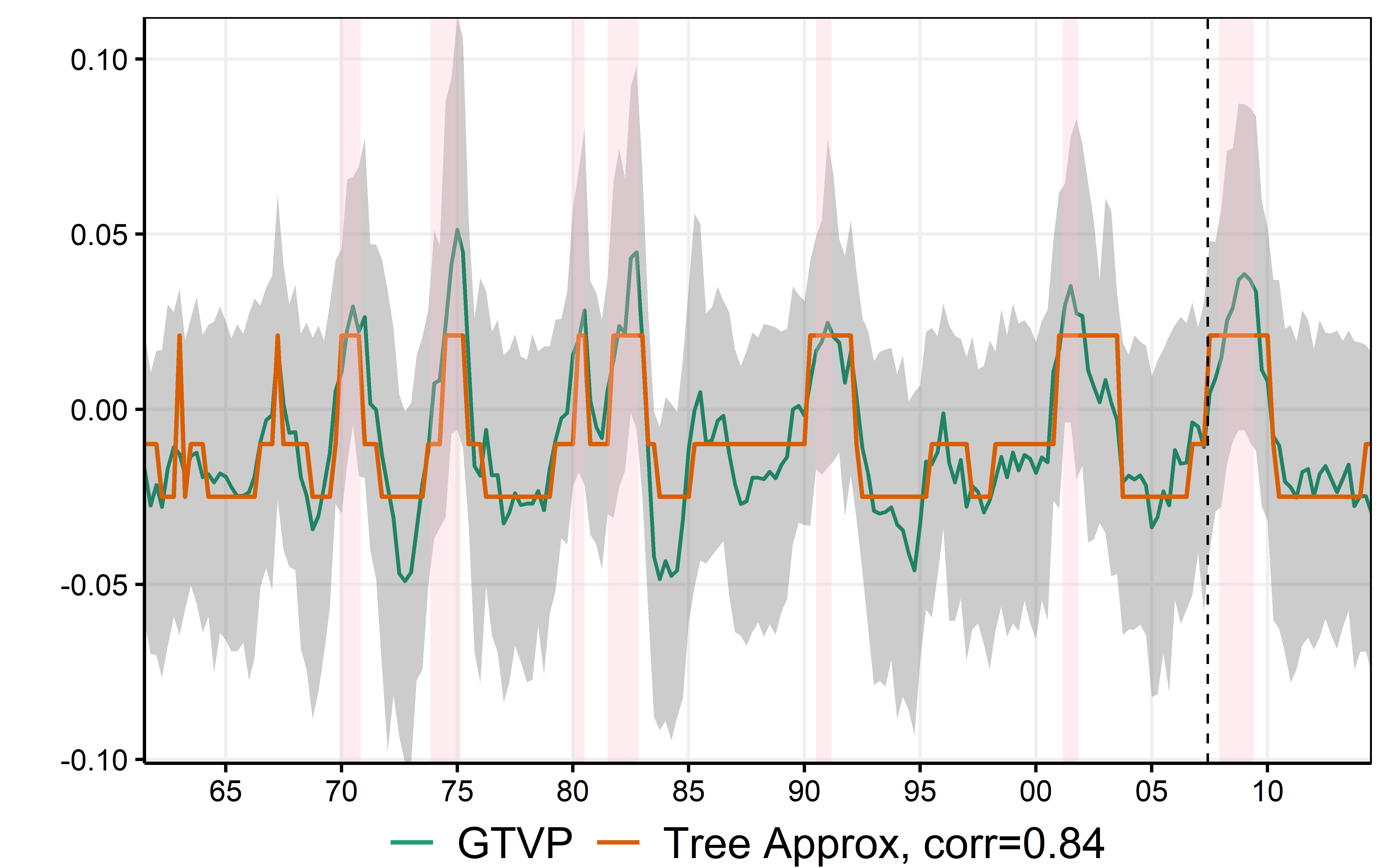

The relationship between random walk TVPs and GTVPs was evoked earlier. I compare them for the small factor model. I estimate standard TVPs using the ridge regression technique developed GC2019. Conveniently, the procedure incorporates a cross-validation step that determines the optimal level of time variation in the random walks.383838I show with simulations that this much easier approach performs similarly well (and sometimes better) to traditional Bayesian TVP-VAR, for model sizes that the latter is able to estimate.

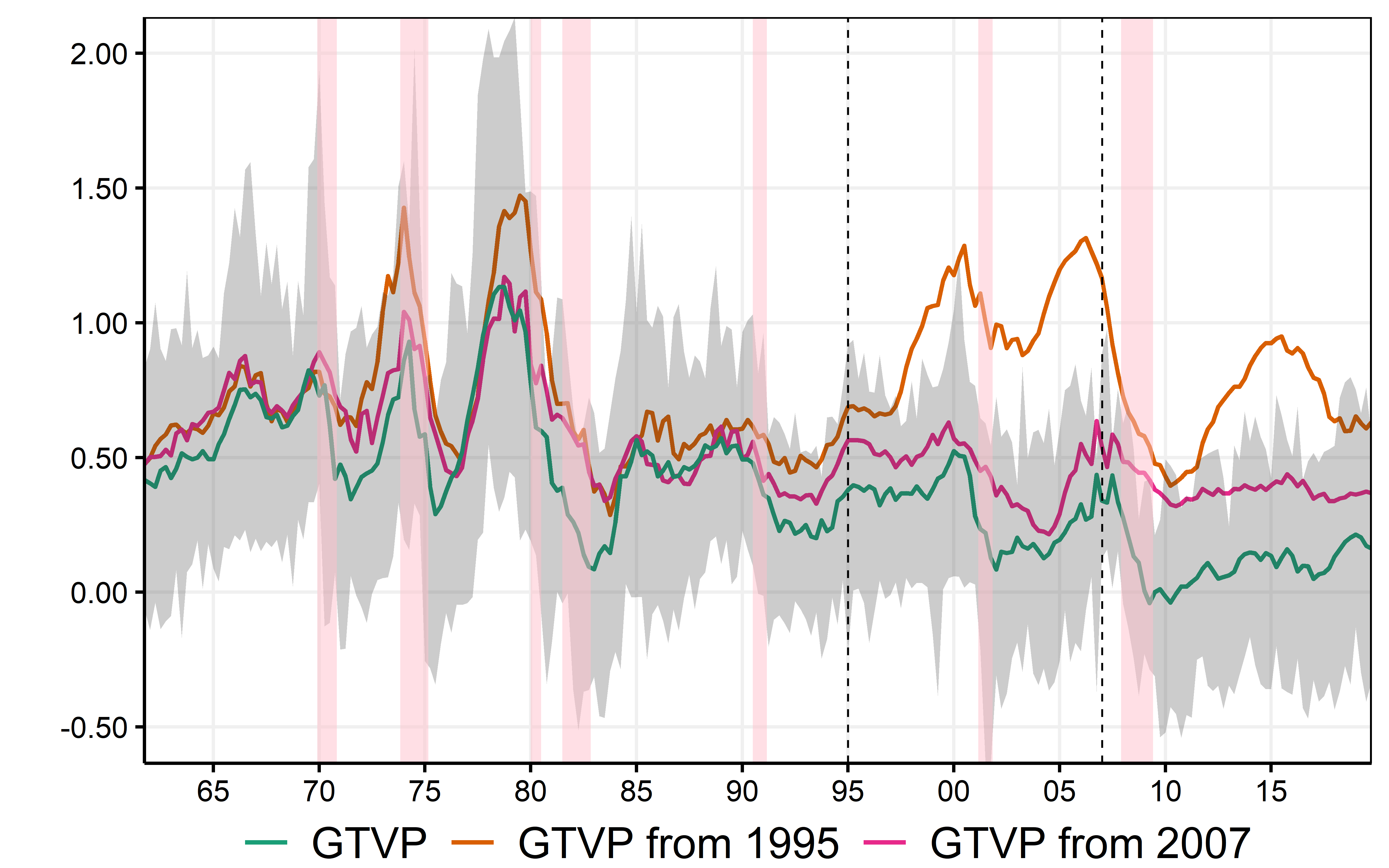

As Figure 5 suggested for and , parameters can be subject to recurrent, rapid and statistically meaningful shifts. Such behavior creates difficulties for random-walk TVPs, which put the accent on smooth and slow structural change. Figure 6 confirms this conjecture. Standard TVPs look for long-run change when regime-switching behavior is the main driving force. As a result, they are flat and within OLS confidence bands, as often reported in the literature (AAG2013). Of course, more action will mechanically be obtained for TVPs when considering a smaller amount of smoothness than what cross-validation proposed. In appendix A.7, I report the same figures, but using the optimal smoothing parameters (as picked by CV) divided by 1000. This provides much more volatile random walk TVPs that are inclined, at certain specific moments, to follow the GTVPs. However, it is clear in Figure 6 that the end-of-sample/revision problem is worsen by the forced lack of smoothing.

It is known in the traditional TVP literature that there is a balance between flexible (but often erratic) paths and very smooth ones where time variation may simply vanish.393939In the case of ridge regression-based TVPs, cross-validation is just a data-driven way of backing this necessary empirical choice. Since random-walk TVPs are unfit for many forms of the time-variation present in macroeconomic data, high bias estimates are usually reported as only them can keep variance at a manageable level. This can have serious implications. Relying too much on time-smoothing can create a mirage of long-run change and/or dissimulate parameters that mostly (but not solely) vary according to expansions/recessions.

Another concern, particularly consequential for forecasting, is the boundary problem. As discussed earlier, random-walk TVP models forecasts can suffer greatly from it because by construction, forecasts are always made at the boundary of the variable on which the kernel is based – i.e., time. One can deploy a 1-sided kernel, but this only alleviate a few pressing symptoms without attacking the heart of the problem. In sharp contrast, GTVPs use a large information set to create the kernel, which implies that the likelihood of making a forecast at the boundary is rather low, unless the RF part constantly selects as splitting variable.

Figures 6 and 22 show, for both random walk and generalized TVPs, their full-sample versions (up to the end of 2014, "ex post") and their version with a training sample ending in 2007Q2 (the dashed blue line). There are two main observations. First, GTVPs are much less prompt to rewrite recent history than random-walk TVPs. Indeed, the green line and the magenta one closely follows each other all the way up to the end of the training sample. Second, while GTVPs can change many quarters after 2007Q2 (like the GDP constant), they are generally very close to each other at the boundary – especially when the time variation is statistically meaningful (like that of and ), which is what matters for forecasting. This is much less true of random walk TVPs as there are clear examples where the two version differ for a long period of time (for instance, the intercept and the coefficient on in the GDP equation), and this often culminates at the boundary.404040In (real) practice, all models would be re-estimated each quarter. However, it is worth pointing out that re-estimating every period is much more important for random-walk TVP than it is for GTVPs. For such reasons, the TV-AR in section 4 was the sole model estimated every period rather than every two years.

5.2.1 Why and When MRF Can Fail to Deliver Better Forecasts

MRF can sometimes be outperformed by simpler alternatives, like standard RF that incorporate MAFs. When that occurs, it is usually due to the inadequacy of the linear part rather than GTVPs themselves. Unlike traditional TVPs, GTVPs rarely provides a model worse than OLS.