Multifractal temporally weighted detrended partial cross-correlation analysis to quantify intrinsic power-law cross-correlation of two non-stationary time series affected by common external factors

Abstract

When common factors strongly influence two cross-correlated time series recorded in complex natural and social systems, the results will be biased if we use multifractal detrended cross-correlation analysis (MF-DXA) without considering these common factors. Based on multifractal temporally weighted detrended cross-correlation analysis (MF-TWXDFA) proposed by our group and multifractal partial cross-correlation analysis (MF-DPXA) proposed by Qian et al., we propose a new method—multifractal temporally weighted detrended partial cross-correlation analysis (MF-TWDPCCA) to quantify intrinsic power-law cross-correlation of two non-stationary time series affected by common external factors in this paper. We use MF-TWDPCCA to characterize the intrinsic cross-correlations between the two simultaneously recorded time series by removing the effects of other potential time series. To test the performance of MF-TWDPCCA, we apply it, MF-TWXDFA and MF-DPXA on simulated series. Numerical tests on artificially simulated series demonstrate that MF-TWDPCCA can accurately detect the intrinsic cross-correlations for two simultaneously recorded series. To further show the utility of MF-TWDPCCA, we apply it on time series from stock markets and find that there exists significantly multifractal power-law cross-correlation between stock returns. A new partial cross-correlation coefficient is defined to quantify the level of intrinsic cross-correlation between two time series.

keywords:Partial cross-correlation; multifractal temporally weighted detrended partial cross-correlation analysis (MF-TWDPCCA); partial cross-correlation coefficient.

1 Introduction

Complex systems with interacting constituents exist in all aspects of nature and society, such as geophysics [1], solid state physics, climate system, ecosystem, financial system [3, 2], etc. In order to study the micro-mechanisms of these complex systems and their operating mechanisms in a statistical sense, people record and analyze the time series of observable quantities. The study of these time series will help us to understand things correctly, grasp the laws of nature, and make scientific decisions. There are relatively mature models and methods for the study of stationary time series, but unfortunately, the time series of real-world complex systems are usually non-stationary and possess long-range power-law cross correlations. Examples of this nature that have been reported include econophysical variables [4, 5, 6, 7, 8], traffic signals [9] and traffic flows [10], brain activity and heart rate variability in healthy humans [11], topographic indices and crop yield in agronomy [12, 13], self-affine time series of taxi accidents [14], wind patterns and land surface air temperatures [15], nitrogen dioxide and ground-level ozone [16], the temperature and concentration fields of turbulent flows embedded in the same space as joint multifractal measures [17, 18], sunspot numbers and river flow fluctuations [19] and temporal and spatial seismic data [20].

So far, various methods have been proposed for the long-range power law relationship of the cross-correlation between two non-stationary time series. In order to study the correlation between two time series, in 2008, Podobnik and Stanley proposed a Detrended Cross-Correlation Analysis (DCCA) [21] algorithm based on the Detrended Fluctuation Analysis (DFA) [22]. This provides a basis for succeeding study of cross-correlation. Since then, this method was continuously promoted and improved. In the same year, Zhou extended DCCA to multifractal case and proposed a Multifractal Detrended Cross-Correlation Analysis (MF-DXA) [23] to study the multifractal cross-correlation property of two non-stationary time series. Oświȩcimka et al. found that in the MF-DXA algorithm, taking the absolute value on the fluctuation function may lead to pseudo-correlation. That is, time series that do not have cross-correlation by themselves, but previous methods gave wrong results of existing cross-correlations between some time series. To solve this problem, Oświȩcimka et al. proposed a multifractal detrended cross-correlation analysis (MFDCCA) [24]. This method introduces the sign of fluctuation function when calculating generalized moments. In 2010, Zhou and Leung proposed the multifractal sliding window detrending fluctuation analysis (MF-MWDFA) and the multifractal temporally weighted detrended fluctuation analysis (MF-TWDFA) [25] for single time series. The innovation of MF-TWDFA is that it uses the idea of temporal weighting to remove the local trend in the sliding window, which can avoid the sharp oscillation of the crossing position. Based on MF-TWDFA and MFDCCA, for analyzing the cross-correlation of multifractals of two time series, our group (Wei et al.) introduced the sign of the fluctuation function and adopted a Geographically Weighted Regression Model (GWR) [26] to propose a new method— multifractal temporally weighted detrended cross-correlation analysis (MF-TWXDFA) [27] in 2017.

If the two non-stationary time series to be studied are driven by a common third-party force or by common external factors, then the power law relationship of the cross-correlation between them observed by the method mentioned above may not reflect by their intrinsic relationship [28, 30, 29]. Fortunately, Baba et al. [31] found that if two time series affected by the external factors are additive, the levels of intrinsic cross-correlation between two time series can be measured by the partial cross-correlation coefficient. Yuan et al. [32] focused on the detrended partial cross-correlation analysis (DPXA) coefficient in complex systems and gave a general calculation method. Almost at the same time, Qian et al. [33] gave a general framework for DPXA and multifractal detrended partial cross-correlation analysis (MF-DPXA) for additive models.

In this paper, based on MF-TWXDFA and MF-DPXA, we propose a new method—multifractal temporally weighted detrended partial cross-correlation analysis (MF-TWDPCCA) to quantify intrinsic power-law cross-correlation of two non-stationary time series affected by common external factors. Compared with MF-TWXDFA, our new method MF-TWDPCCA removes the influence of common factors and then can accurately detect the intrinsic cross-correlations of the two time series in the additive model. Compared with MF-DPXA, we use the idea of MF-TWXDFA to avoid the possibility of the pseudo-correlation.

2 Multifractal temporally weighted detrended partial cross-correlation analysis

(a) .

(b).

(b).

(c) .

(c) .

In this section, based on MF-TWXDFA and MF-DPXA, we propose a new method-multifractal temporally weighted detrended partial cross-correlation analysis (MF-TWDPCCA), which can be used to quantify the intrinsic multifractal cross-correlation properties between two non-stationary time series subject to a common external force.

For a given two non-stationary time series recorded simultaneously, and , who are affected by time series , the main steps of MF-TWDPCCA are as follows:

Step 1: First we remove the effect of . The additive model for models of and can be given respectively as:

| (3) |

where, . When using regression analysis to find the residual sequence, in a window of length , we use the idea in MF-TWXDFA [27] to remove the effect of the sequence on and point by point as follows. For a given integer (), the points contained in a sliding window corresponding to the point should satisfy . When the length of time series is different, we take different value for . Usually the value of is determined by experience. Accordingly, the weight function of the geographic weighted regression model is:

| (6) |

In the window , We perform linear regression for on or on , respectively. We can get the regression values and of and , respectively. Then we get the corresponding residual sequence:

| (9) |

Step 2: For the newly obtained residual sequences and , calculate their cumulative dispersion respectively:

| (12) |

where and .

Step 3: Split into non-overlapping intervals of length , where . Considering that the sequence length may not be an integer multiple of , in order to make full use of all data and avoid losing the tail data information, the are divided twice, that is, once from front to back and from back to front, and then we get subintervals.

Step 4: Calculate the local trends and of and in window by the geographic weighted regression method as MF-TWXDFA [27].

Step 5: For the th interval, calculate the detrended partial cross-correlation fluctuation function

Step 6: For the intervals, calculate the average of to get the order fluctuation function :

Step 7: Determine the scale index of . If there is a long-range cross-correlation between the time series and , then satisfies the following power law relationship:

As we know, the scale index is a fractal exponent that quantifies the intrinsic cross-correlation between and . If is independent of , the intrinsic cross-correlation of and corresponds to single fractal case; If changes with the change of , the intrinsic cross-correlation of and corresponds to multifractal case[33].

According to the standard multifractal formalism, multifractal properties can also be characterized by the multifractal mass exponent , i.e.,

where is the fractal dimension of the geometric support of the multifractal measure[34].

3 Numerical experiments

In order to evaluate the performance of MF-TWDPCCA, in this section, we use the additive models of and as Eq. (1) to perform numerical simulation and verify the effectiveness of our method.

In the experiments, we repeated the experiment times. The sequence length was selected as . After calculation and comparison, we take in this work.

3.1 TWDPCCA coefficient

We define a new partial correlation coefficient (TWDPCCA coefficient) which is very similar to the DPXA coefficient in [33]. Firstly we define:

| (16) |

Then we get

It is easy to find that satisfies .

We use a mathematical model in equation (1) for numerical simulation, where is a fractal Gaussian noise with index , and and are the incremental series of the two components of a bivariate fractional Brownian motion (BFBMs) with Hurst indices and [35, 36, 37]. In the simulations we set , where is the cross-correlation coefficient between and . And then we generate sets of sequences of length to verify the validity of TWDPCCA.

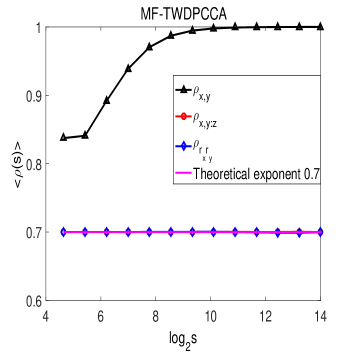

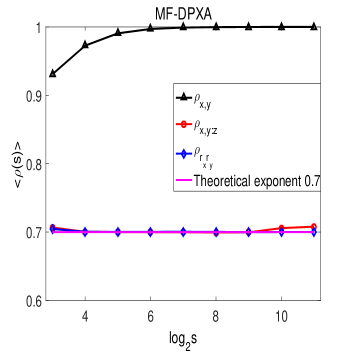

As shown in Figure 1, because has a strong effect on and , the performance of and is dominated by . The cross-correlation coefficients calculated by both MF-TWXDFA and MF-DCCA are all close to especially when the window length is relatively large. Compare left part and right part of Figure 1, we could find that the partial correlation coefficients calculated by MF-TWDPCCA are more accurate than that calculated by MF-DPXA. In addition, MF-TWDPCCA can be applied to a wider window length.

3.2 Bivariate Fractional Brownian Motion (BFBMs)

In this section, in order to further test the performance of MF-TWDPCCA, we use it to calculate the multifractal properties of BFBMs in the three sets of the above additive models (Eq. (1)). Same as in the previous section, is a fractal Gaussian noise with index , and and are the incremental series of the two components of BFBMs with Hurst indices and . Extensive research on BFMS has been made. We know that BFBMs is a single fractal process and there is a relationship [38, 39, 40]. Here is used to represent the theoretical value of the cross-correlation coefficient between and . In the simulations, the length of all the sequences that we generated is and we set: ; .

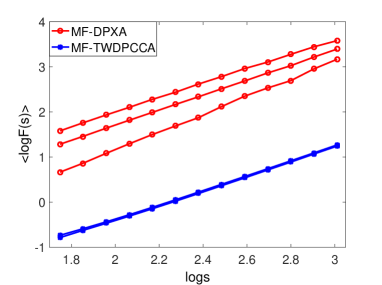

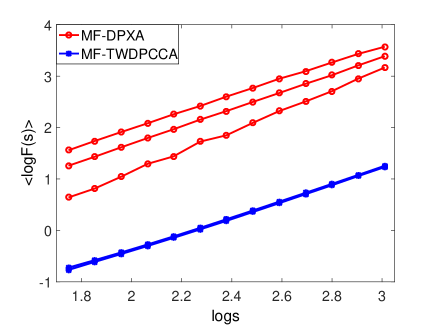

From the left figures in Figure 2, we know that the relationships calculated by both MF-TWDPCCA and MF-TWDPXA between the fluctuation functions and the time scale are all approximately power law relationship, which shows that BMBFs is fractal process. And within a certain error range, each fitted straight line is approximately parallel, which further indicates that BMBFs is a single fractal process. However, we can also find that compared with MF-DPXA, MF-TWDPCCA can get a smoother logarithmic plot, which is more accurate in fitting the results.

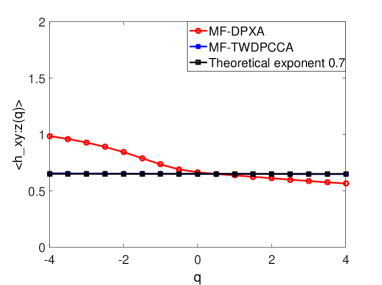

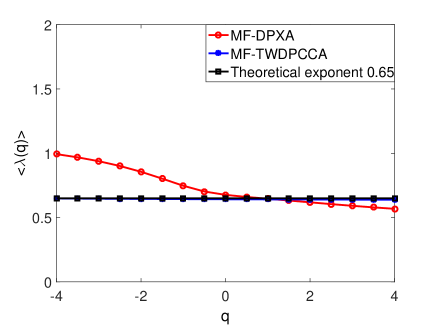

We denote the maximum difference calculated by MF-TWDPCCA as. For the above 3 cases, the maximum and minimum values of are , respectively. So are and . These values are relatively small, indicating that the fluctuation of is small and it is approximately independent on . On the other hand, from the right figures in Figure 2, we can find that the the scale index calculated by MF-TWDPCCA are all approximate straight lines. All these shows that BFBMs is a single fractal process, which is consistent with the fact. However, there is some fluctuation in obtained by MF-DPXA.

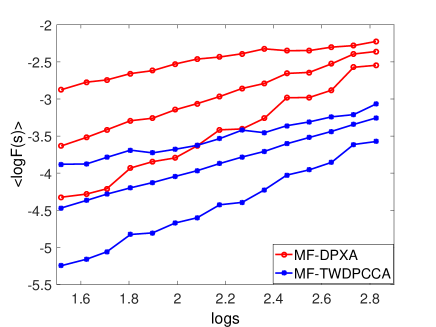

In order to further verify the applicability of MF-TWDPCCA, we select the index as , , for a set of sequences to perform the same numerical simulation. From Figure 3, where the index of the fractal Gaussian noise is , we can find that MF-TWDPCCA still get better results.

3.3 Multifractal binomial measures

As we all know, the binomial measures[41, 42] produced by the model have multifractal properties and its sacale index function is known. We combine them with Gaussian noise to test the performance of MF-TWDPCCA. Two binomial measures and are generated iteratively[27] by using corresponding probability parameters for and for respectively. In the additive model (Eq.(1)) we set , and then we get contaminated signals and , where is Gaussian noise with Hurst index .

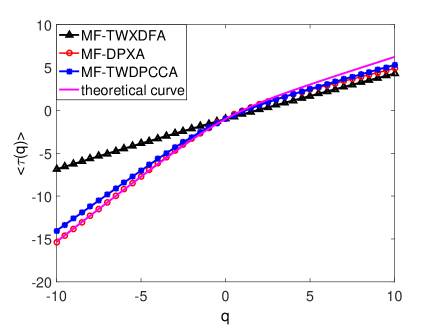

As shown in Figure 4, for the binomial measure, there is no obvious difference between the logarithmic plots obtained by MF-TWDPCCA and MF-DPXA. And these two methods get almost the same , especially when . All these show that the two methods can get almost the same results for binomial measures. However, when using MF-TWXDFA to analyze the cross-correlation between and , without removing the influence of the common potential factor , the multifractal quality index function is approximately a straight line, which fails to uncover any multifractality between . This shows that the multifractal partial cross-correlation analysis is necessary.

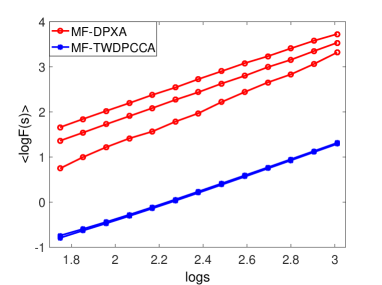

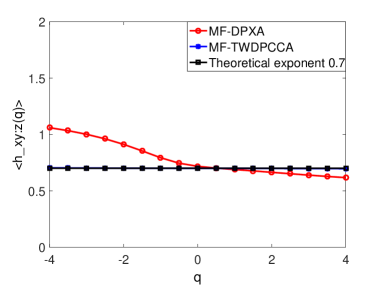

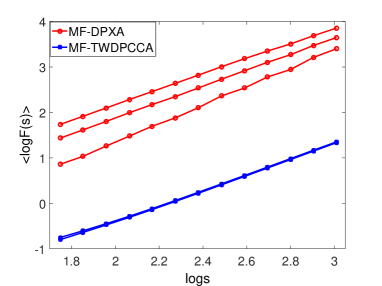

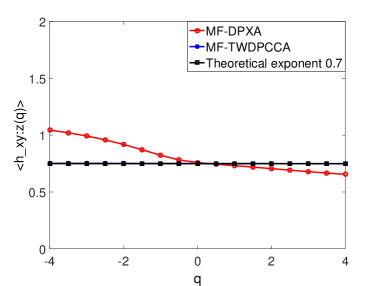

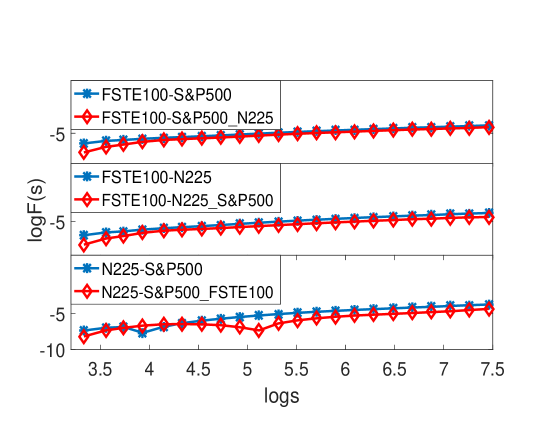

4 Application to stock market index

In this section, we apply the MF-TWDPCCA proposed by us for empirical research. Daily closing data for three stock market indexes, which are FSTE100, SP500 and N225 (finace.yahoo.com database) from January 4, 2001 to January 9, 2019, are used. For the dates without data record, we use the data of five days before and after them to do linear interpolation to complete the data of that day. Here we also take . The daily rate of return is calculated as follows : , where is the closing price on the th days. We can easily find that the mean of all three yield data is close to 0 and less than their standard deviation, which indicates that both low returns and high risks coexist.

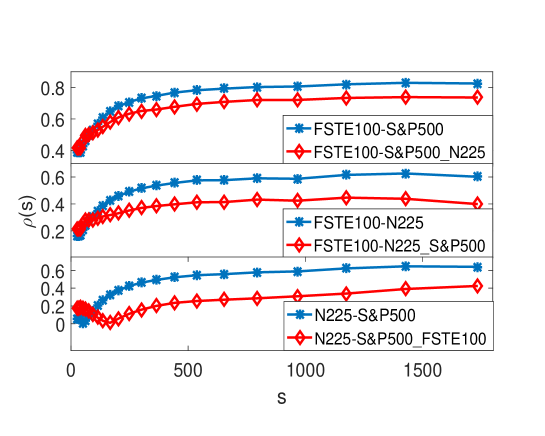

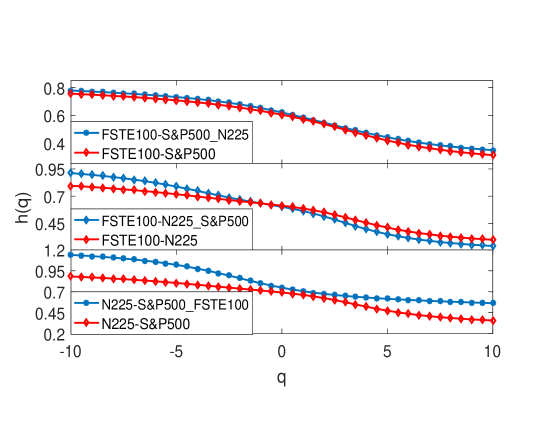

Figures 5, 6 and 7 show the results calculated by us, where ”FSTE100-SP500, FSTE100-N225 and N225-SP500” means they are calculated by MF-TWXDFA, and ”FSTE100-SP500_N225, FSTE100-N225_SP500 and N225-SP500_FSTE100” means they are calculated by MF-TWDPCCA. From Figure 6, we can find that the cross-correlation coefficients between the three sequences studied are overestimated in most cases of scale . Figure 7 shows that there exists multifractal cross-correlation among the three sequences studied.

5 Discussion and conclusions

In this paper, based on the idea of MF-TWXDFA and MF-DPXA, for studying the intrinsic cross-correlation between two non-stationary time series affected by common external factors, we propose a novel method—Multifractal temporally weighted detrended partial cross-correlation analysis (MF-TWDPCCA). In the numerical experiments, we compared MF-TWDPCCA with MF-DPXA. Firstly, as shown in Figure 1, we find that when calculating the detrended partial cross-correlation coefficients of the additive model (Eq. (1)), both MF-TWDPCCA and MF-DPXA reveal the intrinsic relationship between the two time series. However MF-TWDPCCA obtains more accurate results while having a wider range of sliding window length . Secondly, as shown in Figure 2 and Figure 3, when calculating the bivariate fractional Brownian motion with unifractal properties, MF-TWDPCCA not only obtains a smoother bi-logarithmic power law graph, but also obtains the single fractal property which are almost consistent with the theoretical results. And then, comparing the performance of two methods in computing multifractal binomial measures affected by white noise, we find both MF-TWDPCCA and MF-DPXA obtain the intrinsic multifractal relationship over a certain length between the two time series, and the results between the two methods are not significantly different. Finally, we applied MF-TWDPCCA to real stock market data, as show in Figures 6 and 7, we find that there exists multifractal cross-correlation among the three sequences studied. The cross-correlation coefficients between the three sequences studied by MF-TWXDFA are overestimated in most cases of scale . So when we study the correlation between two sequences, if we find that they receive the influence of common external force from the mechanism of their internal background, it is necessary to conduct partial cross-correlation analysis. In a word although MF-TWDPCCA is more time-consuming than MF-DPXA, MF-TWDPCCA can better reveal the intrinsic relationship between two non-stationary time series. At last, we think that we can get more reliable results when we use MF-TWDPCCA to study intrinsic cross correlation between non-stationary time series affected by common external factors.

Acknowledgement

This project was supported by the National Natural Science Foundation of China (Grant No. 11871061), Collaborative Research project for Overseas Scholars (including Hong Kong and Macau) of the National Natural Science Foundation of China (Grant No. 61828203), the Chinese Program for Changjiang Scholars and Innovative Research Team in University (PCSIRT) (Grant No. IRT15R58) and the Hunan Provincial Innovation Foundation for Postgraduate (Grant No. CX2017B265).

References

- [1] Campillo M. and Paul A.:Long-Range Correlations in the Diffuse Seismic Coda, Science 2003,299(5606), 547-549.

- [2] Plerou V. and Stanley H.E.: Stock return distributions: Tests of scaling and universality from three distinct stock markets, 2008 Phys. Rev. E 77(3), 037101.

- [3] Auyang S.Y.: Foundations of complex-system theories: in economics, evolutionary biology, and statistical physics (Cambridge University Press,Cambridge, 1998).

- [4] Lin D.C.:Factorization of joint multifractality, Physica A2008, 387(14), 3461-3470.

- [5] Podobnik B., Horvatic D., Petersen A.M. and Stanley H.E.:Cross-correlations between volume change and price change , Proc. Natl. Acad. Sci. U. S. A. 2009, 106(52),22079-22084.

- [6] Siqueira Jr.E.L., Sto T., Bejan L. and Sto B.:Correlations and cross-correlations in the Brazilian agrarian commodities and stocks, Physica A 2010, 389(14),2739-2743.

- [7] Wang Y.D., Wei Y. and Wu C.F.:Cross-correlations between Chinese A-share and B-share markets,Physica A 2010, 389(23), 5468-5478.

- [8] He L.Y. and Chen S.P.:Multifractal detrended cross-correlation analysis of agricultural futures markets, Chaos Solitons Fractals 2011, 44(6),355-361.

- [9] Zhao X.J., Shang P.J., Lin A.J and Chen G.:Multifractal Fourier detrended cross-correlation analysis of traffic signals,Physica A 2011, 390(21-22), 3670-3678.

- [10] Xu N., Shang P.J. and Kamae S.:Modeling traffic flow correlation using DFA and DCCA, Nonlinear Dyn.2010,61(1-2), 207-216.

- [11] D.C. and Sharif A.:Common multifractality in the heart rate variability and brain activity of healthy humans, Chaos2010, 20(2),023121.

- [12] Kravchenko A.N., Bullock D.G. and Boast C.W.:Joint multifractal analysis of crop yield and terrain slope, Agron. J.2000, 92(6),1279-1290.

- [13] Zeleke T.B. and Si B.C.:Scaling Properties of Topographic Indices and Crop Yield,Agron. J.2004, 96(4), 1082-1090.

- [14] Zebende G.F., da Silva P.A. and Machado Filho A.:Study of cross-correlation in a self-affine time series of taxi accidents, Physica A2011, 390(9), 1677-1683.

- [15] F.J. Jimnez-Hornero, P. Pavn-Domnguez , E.G. de Rav and A.B. Ariza-Villaverde,Atmos. Res.2011, 99(3-4), 366-376.

- [16] Jimnez-Hornero F.J., Jimnez-Hornero J.E., De Rav E.G. and Pavn-Domnguez P.:Exploring the relationship between nitrogen dioxide and ground-level ozone by applying the joint multifractal analysis, Environ. Monit. Assess.,167(1-4)2010, 675-684.

- [17] Antonia R.A. and Van Atta C.W.:On the correlation between temperature and velocity dissipation fields in a heated turbulent jet, J. Fluid Mech.1975, 67(2),273-288.

- [18] Meneveau C., Sreenivasan K.R., Kailasnath P. and Fan M.S.:Joint multifractal measures: Theory and applications to turbulence, Phys. Rev. A1990, 41(2), 894.

- [19] Hajian S. and Movahed M.S.:Multifractal detrended cross-correlation analysis of sunspot numbers and river flow fluctuations, Physica A2010, 389(21), 4942-4957.

- [20] Shadkhoo S. and Jafari G.R.:Multifractal detrended cross-correlation analysis of temporal and spatial seismic data, Eur. Phys. J. B2009, 72(4), 679.

- [21] Podobnik B. and Stanley H.E.:Detrended cross-correlation analysis: a new method for analyzing two nonstationary time series, Phys. Rev. Lett.2008, 100(8), 084102.

- [22] Peng C.K., Buldyrev S.V., Havlin S., Simons M., Stanley H.E. and Goldberger A.L.:Mosaic organization of DNA nucleotides, Phys. Rev. E1994, 49(2),1685.

- [23] Zhou W.X.:Multifractal detrended cross-correlation analysis for two nonstationary signals,Phys. Rev. E2008, 77(6),066211.

- [24] Oświȩcimka P., Drożdż S., Forczek M., Jadach S. and KwapieńJ.:Detrended cross-correlation analysis consistently extended to multifractality, Phys. Rev. E2014,89(2),023305.

- [25] Zhou Y. and Leung Y.:Multifractal temporally weighted detrended fluctuation analysis and its application in the analysis of scaling behavior in temperature series, J. Stat. Mech.-Theory Exp.2010,2010(06), P06021.

- [26] Leung Y. , Mei C.L. and Zhang W.X.:Statistical tests for spatial nonstationarity based on the geographically weighted regression model, Environ. Plan. A2000, 32(1),9-32.

- [27] Wei Y.L., Yu Z.G., Zou H.L. and Anh V.V.:Multifractal temporally weighted detrended cross-correlation analysis to quantify power-law cross-correlation and its application to stock markets, Chaos2017, 27(6),063111.

- [28] Kenett D.Y., Shapira Y. and Ben-Jacob E.:RMT assessments of the market latent information embedded in the stocks’ raw, normalized, and partial correlations,J. Probab. Stat.2009 , 2009.

- [29] Shapira Y., Kenett D.Y. and Ben-Jacob E.:The index cohesive effect on stock market correlations,Eur. Phys. J. B,200972(4), 657.

- [30] Kenett D.Y., Tumminello M., Madi A., Gur-Gershgoren G., Mantegna R.N. and Ben-Jacob E.:Dominating clasp of the financial sector revealed by partial correlation analysis of the stock market,PLoS One2010,5(12), e15032.

- [31] Baba K., Shibata R. and Sibuya M.:Partial correlation and conditional correlation as measures of conditional independence,Aust. N. Z. J. Stat.2004, 46(4),657-664.

- [32] Yuan N.M., Fu Z.T., Zhang H., piao L., Xoplaki E. and Luterbacher J.:Detrended Partial-Cross-Correlation Analysis: A New Method for Analyzing Correlations in Complex System,Sci Rep2015, 5,8143.

- [33] Qian X.Y., Liu Y.M., Jiang Z.Q., Podobnik B., Zhou W.X. and Stanley H.E.:Detrended partial cross-correlation analysis of two nonstationary time series influenced by common external forces,Phys. Rev. E2015,91(6),062816.

- [33] Wang F., Yang Z.H. and Wang L.:Detecting and quantifying cross-correlations by analogous multifractal height cross-correlation analysis, Physica A2016, 444,954-962.

- [34] Kantelhardt J.W., Zschiegner S.A., Koscielny-Bunde E., Havlin S., Bunde A. and Stanley H.E.:Multifractal detrended fluctuation analysis of nonstationary time series, Physica A2002,316(87).

- [35] Venugopal V., Roux S.G., FoufoulaGeorgiou E. and Arneodo A.:Revisiting multifractality of high-resolution temporal rainfall using a wavelet-based formalism,Water Resour. Res.2006,42(6).

- [36] Yu Z.G., Anh V.V., Wanliss J.A. and Watson S.M.:Chaos game representation of the Dst index and prediction of geomagnetic storm events,Chaos Solitons Fractals2007,31(3),736-746.

- [37] Yu Z.G., Anh V.V. and Eastes R.:Multifractal analysis of geomagnetic storm and solar flare indices and their class dependence, J. Geophys. Res-Space Phys.2009,114(A5).

- [38] Lavancier F., Philippe A. and Surgailis D.:Covariance function of vector self-similar processes, Stat. Probab. Lett.2009, 79(23),2415-2421.

- [39] Coeurjolly J.F., Amblard P.O. and Achard S.:On multivariate fractional Brownian motion and multivariate fractional Gaussian noise, 2010 18th European Signal Processing Conference. IEEE2010, 1567-1571.

- [40] Amblard P.O. and Coeurjolly J.F.:Identification of the multivariate fractional Brownian motion,IEEE Trans. Signal Process.2011,59(11), 5152-5168.

- [41] Yu Z.G., Anh V.V. and Eastes R.:Underlying scaling relationships between solar activity and geomagnetic activity revealed by multifractal analyses, J. Geophys. Res-Space Phys.2014,119(9), 7577-7586.

- [42] Zang B.J. and Shang P.J.:Multifractal analysis of the Yellow River flows,Chinese Phys.2007, 16(3),565.