Measuring Macroeconomic Uncertainty:

The Labor Channel of Uncertainty from a Cross-Country Perspective††thanks: We are grateful to Efrem Castelnuovo, Todd E. Clark, Jan Jacobs, Alexander Rathke, Michael Siegenthaler, Gregor von Schweinitz, and the participants of the Economics Research Seminar at Leipzig University for very helpful comments. We thank Tino Berger, Todd E. Clark, and Haroon Mumtaz for making available their global uncertainty estimates. We further thank Stefan Neuwirth and Roberto Golinelli for providing us with historic German and Italian GDP real time data. A previous version of the paper has been circulated under the title “Measuring Macroeconomic Uncertainty: A Cross-Country Analysis”.

This paper constructs internationally consistent measures of macroeconomic uncertainty. Our econometric framework extracts uncertainty from revisions in data obtained from standardized national accounts. Applying our model to post-WWII real-time data, we estimate macroeconomic uncertainty for 39 countries. The cross-country dimension of our uncertainty data allows us to study the impact of uncertainty shocks under different employment protection legislation. Our empirical findings suggest that the effects of uncertainty shocks are stronger and more persistent in countries with low employment protection compared to countries with high employment protection. These empirical findings are in line with a theoretical model under varying firing cost.

JEL classifications: C51, C53, C82, E32, J8

Keywords: Uncertainty Shocks, Real-Time Data, Rational Forecast Error, Employment Protection Legislation, System of National Accounts

1 Introduction

The COVID-19 crisis has highlighted the relationship between uncertainty and economic fluctuations (e.g. Altig et al. (2020)).111See Bloom (2014) and Castelnuovo (2019) for overview articles on the relationship between uncertainty. This relationship usually differs across countries with conditions on the labor market possibly playing a decisive role.222The other prominent channels are the investment channel (see, for instance, Bloom (2009) and Bloom et al. (2018)) and the financial channel (see, for instance, Gilchrist and Zakrajšek (2012), Ludvigson et al. (2015), and Fernández-Villaverde and

Guerrón-Quintana (2020)) However, while theoretically important, the empirical evidence on labor market specific transmission mechanisms of uncertainty shocks on the overall economy are so far scant.

This paper proceeds in two steps. First it constructs measures of macroeconomic uncertainty that are available for a large set of countries and that are defined as the conditional volatility of an unpredictable forecast as in Jurado et al. (2015).333See also Cascaldi-Garcia et al. (2020) for a comprehensive overview of different types of uncertainty measures. To obtain this goal, we draw on the macroeconomic data revisions literature, thereby treating statistical agencies’ estimates of first releases of macroeconomic variables as forecasting exercises and their subsequent revisions as forecast errors.444See Croushore and Stark (2001) for the construction of real-time data sets and their relevance for macroeconomic research. We extract the unpredictable part of data revisions by decomposing them into news – the error from an unpredictable rational forecast – and noise, which is defined as a classical errors-in-variables. Specifically, we follow the approach of Jacobs and van Norden (2011) in modeling data revisions with news and noise, enriching it with stochastic volatility components. Our measure of macroeconomic uncertainty is thus defined as the conditional volatility of the error corresponding to the unpredictable part of revisions in GDP growth. It is important to note that these estimates of macroeconomic uncertainty are consistent across OECD countries, given the nature of standardized national accounting procedures.555Statistical agencies in OECD countries follow similar national accounting standards. The data provided by the OECD database is based on the 2008 System of National Account. See also the website of the OECD for an overview of national legislation insuring the implementation of international accounting standards (http://www.oecd.org/sdd/na/implementingthesystemofnationalaccount2008.htm). Note also that in constructing coherent macroeconomic variables statistical agencies take into account a plethora of series that include a huge amount of sensitive data partly only available to the statistical agency.666In Appendix D, we show that statistical agencies have valuable information regarding GDP growth that is not even exceeded by financial markets. Thus, in contrast to the bottom-up approach of, e.g., Jurado et al. (2015), we follow a top-down approach, where we partly outsource the information acquisition to the statistical agency.

We apply our procedure to a post WWII real-time dataset collected for 39 countries, deriving an international set of estimates of macroeconomic uncertainty. For the U.S., our measure pinpoints periods of highest uncertainty during the mid-1970s, beginning of 1980s, beginning of 2000s, and during the recent great financial crisis, which is qualitatively consistent with other measures of U.S. uncertainty. However, our measure already peaks in the mid-1970s, highlighting the turmoils during the 1970s. We also construct a global uncertainty measure by using a GDP weighted average of all country specific uncertainty indicators. According to our measure of global uncertainty, the period during the mid-1970s and the great financial crisis stands out in terms of uncertainty, which is in line with most of the measures of global uncertainty.777We compare our measure of uncertainty with the global uncertainty indicators presented in Mumtaz and Theodoridis (2017), Redl (2018), Carriero et al. (2019) and Berger et al. (2017). We also perform a VAR analysis for the U.S. and the G7 countries. The impulse response functions computed for the U.S. are very similar to impulse responses from a VAR including the uncertainty indicator of Jurado et al. (2015). These impulse response functions are qualitatively confirmed by the impulse responses estimated for an aggregate of the G7 countries.

In a second step, we use our newly created international set of indicators to investigate the role of labor adjustment costs in transmitting uncertainty shocks. We subdivide the countries into high employment protection legislation (EPL) countries and low employment protection legislation countries using the OECD Employment Protection Database. In an 8-variable VAR analysis that uses data from 1988Q1 to 2019Q4, we find that the degree of labor protection plays a crucial role in the propagation of uncertainty shocks. Uncertainty shocks affect the economy in countries with stricter employment protection legislation less than in countries with low labor protection standards. To learn more about the role played by EPL in the propagation mechanism of uncertainty shocks, we employ the theoretical model of Bloom et al. (2018). Within their framework, our focus is on the effects of changes in firing costs, assuming that stricter employment protection legislation hinders firms to lay off employees and thus lead to higher firing costs. We first calibrate, solve, and simulate the model of Bloom et al. (2018) twice, once for an economy for low EPL and once for an economy with high EPL. We then use the two calibrated models to simulate the reaction of the economy to an imposed uncertainty shock. According to the theoretical model and in line with our empirical findings, an uncertainty shock has less deteriorating effects in an economy with high EPL than in one with low EPL.

There is a rapidly expanding literature that uses forecast error based procedures to estimate uncertainty as in, e.g., Jurado et al. (2015) and Carriero et al. (2018) who employ factor stochastic volatility models to provide uncertainty measures for the U.S. Mumtaz and Theodoridis (2017), Carriero et al. (2019), Berger et al. (2017) estimate similar uncertainty indicators with a focus on extracting global uncertainty.888See also Redl (2018) for an application of the Jurado et al. (2015) approach to multiple countries and Caggiano et al. (2020) for global uncertainty estimates derived from hierarchical dynamic factor models. We contribute to this literature by using real-time data on GDP growth and by computing forecast errors that incorporate information available to the economic agents up to and including at time . The focus so far has only been on the last vintage of economic series at time thus incorporating information that goes beyond time with .999Rogers and Xu (2019) show that uncertainty indicators based on real-time data can considerable differ from their ex-post counterparts. Limiting the construction of forecast errors to information that economic agents had about aggregate variables at time is in line with the above mentioned definition of macroeconomic uncertainty and might have important implications. Moreover, the forecast error based uncertainty literature estimates uncertainty from models that allow for changes in the underlying conditional volatility only. Drifts in the parameters of a macroeconomic model can however also stem from changes in the structure of the economy, usually modelled with time-varying coefficients. In such a setup, a model that includes stochastic volatility components only is probably misspecified.101010See Cogley and Sargent (2005) for a more detailed discussion of these kind of misspecifications within the context of VARs. See also the discussions in Sims (2001) and Stock (2001). Not including time-varying coefficients possibly attributes too much variation to the stochastic volatility components, thus exaggerating the fluctuations in the uncertainty measures. We tackle this issue by allowing the coefficients of our model to change over time.

The real-time forecast errors constructed with our approach are similar to those that are computed from the survey of professional forecasters as in Jo and Sekkel (2019), Clark et al. (2020), Ozturk and Sheng (2018), and Rossi and Sekhposyan (2015). While the forecast error in our approach is constructed from the unpredictable part of revisions of GDP growth, the forecast error computed from the survey of professional forecasters are focused on single releases of GDP growth and do not incorporate revisions in GDP growth. Data revisions can thus directly affect the uncertainty measures derived from survey of professional forecasters, whereas the uncertainty indicator estimated by our procedure takes these data revisions into account. Moreover, uncertainty estimates from survey of professional forecasters are restricted to a few countries and cannot be applied to a broad-based international setting, which is the focus of this paper. There is also a literature on international uncertainty indicators that are derived from textual data.111111See Baker et al. (2016), Davis (2016), Hassan et al. (2020), and Ahir et al. (2018) for a more detailed discussion. While these methods have their merits especially when it comes to real-time tracking of uncertainty, they coincide only in special cases with forecast error based uncertainty measures. Moreover, comparing uncertainty indicators from textual analysis across countries requires not only mapping the semantic meaning of words into another language but also to consider aspects of intercultural communication in order to ensure a mutual meaning of the textual analysis.121212See, for instance, Harmsen et al. (2003) and Kwon et al. (2009) for the impact of intercultural communication on mutual understanding.

The remainder of the paper is structured as follows: In Section 2, we discuss the econometric framework and the estimation procedure. Section 3 discusses the construction of the real-time data set that serves as the basis for the uncertainty indicator. Section 4 and 5 present the uncertainty indicators and evaluate the macroeconomic relevance of uncertainty shocks. Section 6 examines the role of labor adjustment costs in the propagation of uncertainty shocks and Section 7 concludes.

2 Econometric Framework

In this section, we describe our econometric model, show how to derive direct measures of macroeconomic uncertainty, and how we cope with structural change. Finally, we briefly discuss our estimation procedure.

We follow the standard notation in the data revision literature where denotes an estimate published at time of some real-valued scalar variable at time for and . According to Jacobs and van Norden (2011) the th release of can be express as a function of its “true” value and a measurement error that is decomposed into a news and a noise term

| (1) |

where represents the true value, the news component and the noise component.131313See Kishor and Koenig (2012) for another framework that allows the estimation of both news and noise type measurement errors in data revisions. See Jacobs and van Norden (2011) for a more detailed discussion of the data revision literature.

Within this setup the noise component is interpreted as classical errors-in-variables and the news component as a rational forecast error.141414See Mankiw et al. (1984), Mankiw and Shapiro (1986) and de Jong (1987), where measurement errors are described as news. See Sargent (1989) for a statistical agency that estimates the “true” value making full use of available information and thus resulting into unpredictable revisions. The main assumptions to distinguish between news and noise innovations are their correlation with the underlying true value of the variable. It is thus assumed that the news component carries information about the “true” value of the variable (i.e. ), whereas the noise components are independent of the “true” value of the variable (i.e., ), with for all and .

To estimate those news and noise components, we build on the state space model developed by Jacobs and van Norden (2011), which can be expressed as

| (2) | ||||

| (3) |

where

with , where and are coefficients and represents the standard deviation of for .151515See Jacobs et al. (2020) for a more general specification of this model.

2.1 Estimating Macroeconomic Uncertainty

To obtain direct estimates of macroeconomic uncertainty, we define economic uncertainty similar to Jurado et al. (2015) as the conditional volatility of the unpredictable part of future values of the variable, i.e. in our case of subsequent releases of the variable. We thus treat the estimation procedure of early releases as a forecasting exercise. Within this context, the news components can then be seen as the unpredictable part of the forecast error. We obtain estimates of macroeconomic uncertainty by estimating changes in the variance of the news component. To do this we enrich the Jacobs and van Norden (2011) model with stochastic volatility components, modifying Equation (3) to

| (4) |

where

with for and , , and specified as in (3). The volatility components are modelled as latent variables whose logarithms are assumed to follow independent AR(1) processes:

| (5) |

where , , are parameters, and .161616See, e.g., Kim et al. (1998).

Our measure of macroeconomic uncertainty at time can thus be expressed as

which is a combination of the conditional volatility of the two rational forecast errors.

2.2 Capturing Structural Change

In dynamical systems of macroeconomic developments variations in the underlying volatility are intertwined with changes in the structure of the economy, i.e. time-varying coefficients. If drifts in the system are characterized by structural changes in the economy, a model that includes stochastic volatility components only is possibly misspecified. In such a setup, not allowing for time-varying coefficients would possibly attribute too much time-variation to the stochastic volatility components, exaggerating the time variation in the stochastic volatility components.

In our setup, we model structural changes as variations in the stochastic properties of the “true” value .171717In periodical intervals, statistical agencies adjust the definition of national accounts to account for structural change. Appendix B.4 addresses the nature of these revisions in greater detail. We capture this change by allowing the coefficients in the equation of to vary over time, modifying Equation (4) to:

| (6) |

where

| (7) |

and

with and , and specified as in (4).

2.3 Priors

We use priors that are as diffuse as possible. The prior on is assumed to follow an Inverse Wishart distribution. The shape parameter is set to 3. The prior for the scale parameter is optimized according to the length of the series, in order for the AR(1) to cover the range of possible values. The prior for the variance of the stochastic volatilities is assumed to follow an Inverse Gamma distribution. We set the priors on the variance of the stochastic volatilities as uninformative as possible.

2.4 Estimation Procedure

We obtain draws from the posterior of our model’s parameters using Markov Chain Monte Carlo methods. More specifically, we use Gibbs sampling.181818The Gibbs sampling procedure was programmed in Julia and is available upon request. The Gibbs sampler consists of the following blocks:

-

1.

Draw conditional on , , and data using a forward filtering backward sampling as described in, e.g., Carter and Kohn (1994),

-

2.

Draw , , , for conditional on , , using the ancillarity-sufficiency interweaving approach proposed by Kastner and Frühwirth-Schnatter (2014),

-

3.

Draw and conditional on and using the simulation smoothing approach introduced by McCausland et al. (2011).

-

4.

Draw conditional on , , from an Inverse Wishart distribution.

See Appendix A for a more detailed discussion of our estimation procedure.

3 Real-Time Data

We use data revisions in real GDP growth for 39 countries to construct the uncertainty indicator. Particularly, we use the first year-over-year growth rate of real GDP as a forecast for the final year-over-year growth rate of real GDP that we define as the growth rate published after three years.191919Comparing the first release of GDP and to the 12th release of GDP creates a publication lag of our measure of uncertainty of three years. In order to obtain more recent estimates of macroeconomic uncertainty, we continuously decrease the distance between the first and the last release at the current edge. In order to obtain a comprehensive data set for various countries, we need to tap and combine several data sources. The largest part of our data is provided by the Original Release Data and Revisions Database. The Original Release Data and Revisions Database is part of OECD Main Economic Indicators database (OECD, 2017) and represents the central data source of this project. The database provides different releases of macroeconomic aggregates for many countries. This study uses data from 39 countries. Table 1 provides an overview of the countries included in our study, the data provider and the first available data point.

Unfortunately, the Original Release Data and Revisions Database provides releases of macroeconomic variables only since 1999. For data prior to 1999, we need to rely on other data sources. We primarily use the data made available by the Federal Reserve Bank of Dallas for releases prior to 1999. Fernandez et al. (2011) collect real-time data for various economies including those that we use in this study. The authors assemble the dataset from original quarterly releases of different macroeconomic aggregates from 1962 to 1998. We currently use these data for all countries except the U.S., Germany, Italy, Australia and New Zealand. For the U.S., we use data provided by the Federal Reserve of Philadelphia as they provide more exhaustive data compared to the data provided by Federal Reserve of Dallas. For Germany we rely on data provided by Boysen-Hogrefe and Neuwirth (2012) and for Australia we use data provided by the Australian Real-Time Macroeconomic Database (Lee et al., 2012). For New Zealand we use data provided by the Reserve Bank of New Zealand (Sleeman, 2006) and for Italy, we also use data releases of ISTAT that were kindly provided by Golinelli and Parigi (2008).202020Appendix B describes these various data sources and outlines the construction of our data base in more detail. We will provide the final real-time dataset as well as the code to construct it upon request.

| Countries | MEI Code | Datasource prior to 1999 | Available since |

|---|---|---|---|

| Australia | AUS | Real-Time Macroeconomic Database (U. Melbourne) | 1967 Q3 |

| Austria | AUT | FED Dallas | 1999 Q3 |

| Belgium | BEL | no data | 1999 Q1 |

| Brazil | BRA | no data | 2000 Q2 |

| Canada | CAN | FED Dallas & Bank of Canada | 1961 Q3 |

| Chile | CHL | no data | 2010 Q1 |

| Czech Republic | CZE | no data | 1999 Q1 |

| Denmark | DNK | FED Dallas | 1993 Q2 |

| Estonia | EST | no data | 2010 Q3 |

| Finland | FIN | FED Dallas | 1993 Q4 |

| France | FRA | FED Dallas | 1987 Q2 |

| Germany | DEU | FED Dallas & Boysen-Hogrefe and Neuwirth (2012) | 1964 Q4 |

| Great Britain | GBR | FED Dallas | 1964 Q4 |

| Hungary | HUN | no data | 2002 Q2 |

| Greece | GRC | no data | 2003 Q4 |

| Iceland | ISL | no data | 2002 Q4 |

| India | IND | no data | 2005 Q4 |

| Indonesia | IDN | no data | 2005 Q4 |

| Ireland | IRL | no data | 2002 Q2 |

| Israel | ISR | no data | 2010 Q2 |

| Italy | ITA | FED Dallas & Golinelli and Parigi (2008) | 1974 Q3 |

| Japan | JPN | FED Dallas | 1964 Q3 |

| Korea | KOR | FED Dallas | 1996 Q4 |

| Luxembourg | LUX | no data | 2004 Q4 |

| Mexico | MEX | FED Dallas | 1994 Q2 |

| Netherlands | NLD | FED Dallas | 1993 Q3 |

| New Zealand | NZL | Reserve Bank of New Zealand | 1994 Q4 |

| Norway | NOR | FED Dallas | 1993 Q3 |

| Poland | POL | no data | 2002 Q2 |

| Portugal | PRT | FED Dallas | 1992 Q3 |

| Russia | RUS | no data | 1999 Q3 |

| Slovakia | SVK | no data | 2000 Q3 |

| Slovenia | SVN | no data | 2010 Q1 |

| South Africa | RUS | no data | 2001 Q4 |

| Spain | ESP | FED Dallas | 1993 Q1 |

| Sweden | SWE | FED Dallas | 1989 Q4 |

| Switzerland | CHE | FED Dallas | 1987 Q2 |

| Turkey | TUR | FED Dallas | 1993 Q1 |

| USA | USA | FED Philadelphia | 1961 Q4 |

Notes: Central data source is the Original Release Data and Revisions Database. The column Countries depicts the country and MEI Code the country code from the Original Release Data and Revisions Database. The column Datasource prior to 1999 describes the data source of releases prior to 1999. The column Available since states beginning of a country’s uncertainty indicator. Rows in green highlight countries with data available prior to 1990Q1, rows in gray depict countries with data from 1990Q1 to 2000Q4 and rows in red represent countries with data available only from 2001Q1 onward.

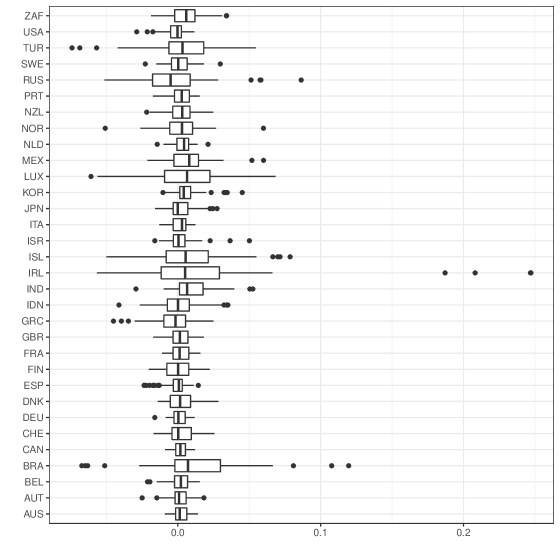

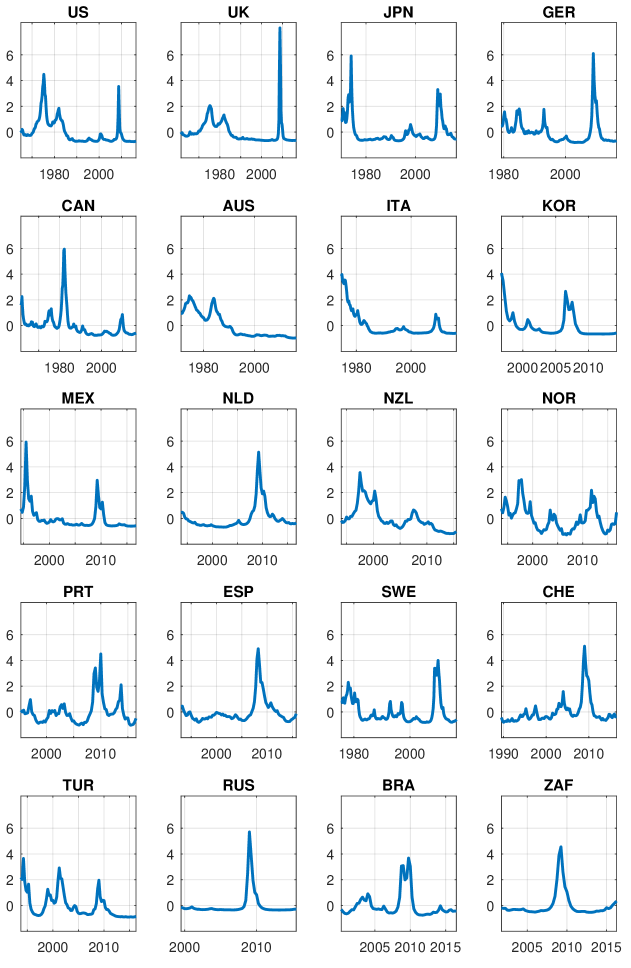

While data availability fluctuates a lot between countries, we have surprisingly long time series for many countries. For 10 countries we have real-time data for more than 30 years (green shaded countries) and for another 16 countries we have more than 20 years of data (gray shaded countries). For four countries only, we have less than 10 years data. Besides data availability, also the average revisions change heavily between single countries. While large countries in terms of GDP, such as the U.S., France, Germany, Canada and Australia tend to have small revisions, smaller countries, including Ireland, Island and Luxembourg, appear to have much larger revisions. Figure 1 visualizes the distribution of the 10th revision of year-over-year growth rates of real GDP for different countries.

Most countries reveal a statistical significant upward revision of their growth rates over time. The 10th release of GDP growth tends on average to be larger than the first release. Only four countries including the U.S., Russia, Greece and Spain, report on average a lower growth rate at the 10th release than on the first release.212121See Figure 9 in Appendix B for a better overview of average revisions.

4 Estimates of Macroeconomic Uncertainty

Using the econometric framework outlined in Section 2 and the real-time dataset described in Section 3, we obtain estimates of macroeconomic uncertainty for 39 countries.222222We provide all uncertainty indicators on our website. We now present and discuss the resulting uncertainty measures. Thereby, we focus on uncertainty in the United States and global uncertainty.

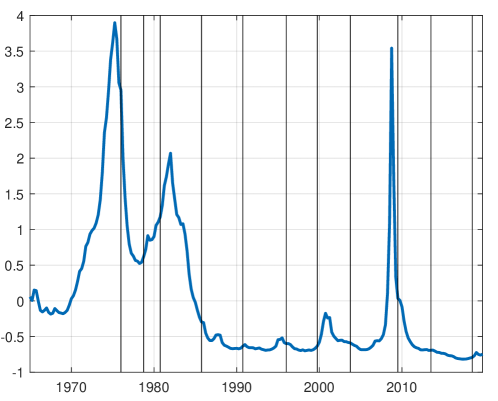

Our methodical framework provides macroeconomic uncertainty estimates for the United States that are similar to existing uncertainty measures. Figure 2 presents our revision-based uncertainty measure for the U.S. (blue solid line) and compares it to existing proxies found in the literature. These alternative measures include the macroeconomic uncertainty indicator proposed by Jurado et al. (2015) (green solid line), the economic policy uncertainty index developed by Baker et al. (2016) (ochre dashed line) and the VIX (purple dashed line), a popular uncertainty indicator that reflects market’s expectation of volatility implied by the S&P 500 index options.

Notes: This figure compares different uncertainty indicators for the United States form 1960Q1 to 2019Q4. In the first pane, the green solid line displays the indicator for macroeconomic uncertainty (quarterly averages, horizon 12, MacroFinanceRealUncertainty_202008_update) developed by Jurado et al. (2015) and the blue solid line shows the newly proposed measure of macroeconomic uncertainty. In the second pane, the dashed ochre line shows quarterly average of the Economic Policy Indicator proposed by Baker et al. (2016). The last pane compares the VIX (realisied volatility before 1989) to the new uncertainty measure. All indicators are demeaned and normalized to unit variance.

Our data revision based indicator reaches its highest levels during the recession in the 70s that was characterized by the first oil price shock and the collapse of the Bretton Woods system and marked the end to the overall Post-World War II economic expansion. The Great Recession of 2008 represents the second highest peak of our uncertainty measure. Further identified times of heighten uncertainty are during the ’82 recession and, to a much lesser extent, at the beginning of the 2000s, during the dotcom bubble burst. Overall, our indicator resembles most the uncertainty measure proposed by Jurado et al. (2015)(henceforth JLN). However, while JLN peaks during the Iran Revolution in 1979, the revision based indicator reaches its highest levels during the 70s recession. Compared to other uncertainty measures, our uncertainty estimate for the U.S. displays a significantly lower volatility and indicates only a few mayor uncertainty shocks during 1965 and 2019. For instance, while both the EPU and the VIX peak in 1987 as a result of the Black Monday, the revision based indicators hardly blinks. Similar, after the Great Recession of 2008, the EPU reaches all-time-high level of economic policy uncertainty. However, the economic policy uncertainty does not translate into macroeconomic uncertainty as both the revision based indicator as well as JLN return to very low levels after the recession.

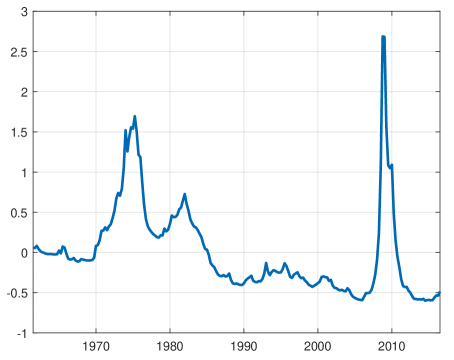

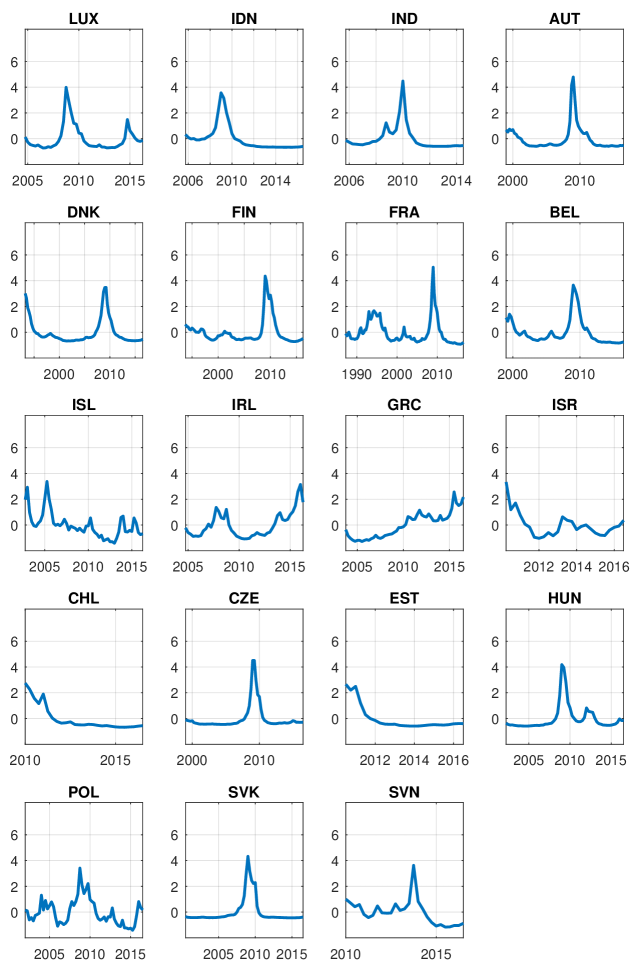

Although we obtain uncertainty estimates for 39 countries, for the sake of brevity, we abstain from discussing all countries in the main text and refer the reader to Appendix C for a presentation of all uncertainty indicators.232323Figure 11 and Figure 3 in the Appendix present the uncertainty estimates of all countries. Instead, we use the comprehensive number of uncertainty indicators to examine uncertainty on a global level. We construct a global uncertainty measure as the weighted mean of single country indicators. We achieve this by first standardizing the uncertainty indicator of each country and then computing the weighted average by weighing each country according to its real GDP.242424The global uncertainty indicator is based on an unbalanced sample. That is, countries’ uncertainty estimates are considered according to their availability. The countries included in the construction of the global uncertainty indicator account for approximately 50% of world GDP during the first half of the sample. During the second half of the sample, the included countries account for more than 75% of world GDP. Figure 3 presents the global uncertainty indicators. From the 1960s to today, our estimates suggest two large global uncertainty shocks. The first occurred during the oil price shock in the 70s, the second global uncertainty shock was experienced during the Great Recession in 2008. The only other notable increase in global uncertainty occurred after the second oil price shock and the subsequent early 80s recession.

Notes: This figure shows the weighted average of countries’ normalized uncertainty measures. We weight single countries according to their real GDP. While the included countries represent approximately half of world GDP during the first half of the sample, the economies included in the second half represent around 75% of total GDP.

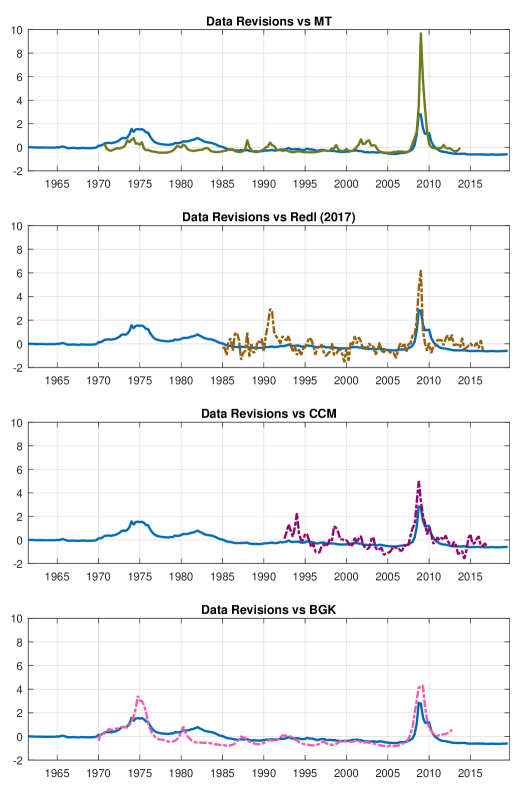

Recently, various papers started to measure and study uncertainty on a global dimension.252525See Castelnuovo (2019) for a recent review on the literature focusing on global uncertainty. While several papers propose measures of global economic policy uncertainty, world risk and global financial uncertainty, studies that attempt to measure global macroeconomic uncertainty are limited: Redl (2017) constructs a JLN based global uncertainty measure that uses global macro and financial data from emerging and advanced economies. Mumtaz and Theodoridis (2017) (henceforth MT) use a factor model with stochastic volatility to decompose the time-varying variance of macroeconomic and financial variables of eleven OECD countries262626These countries include United States, United Kingdom, Canada, Germany, France, Spain, Italy, Netherlands, Sweden, Japan and Australia. into contributions from country-specific uncertainty and uncertainty common to all countries. Carriero et al. (2019) (henceforth CCM) estimate a large, heteroskedastic VAR on 19 industrialized economies to obtain estimates of global uncertainty. Berger et al. (2017) (henceforth BGK) use a dynamic factor model with stochastic volatility to identify the common component of macroeconomic uncertainty from 20 OECD countries. Figure 4 compares these indicators to our data-revision based indicator. While the data revision based indicator matches the other indicators remarkably well, two differences stand out. First, similar to the indicator of the U.S., the data revision based indicator is the least volatile of all indicators. Second, while the other four indicators peak during the great recession of 2008 at 4 standard deviations or higher above their mean, the data revision indicator peaks at 2.5 standard deviations.

Notes: This figure compares different global macroeconomic uncertainty indicators. In the first pane, the green solid line displays the indicator for global macroeconomic uncertainty by Mumtaz and Theodoridis (2017) and the blue solid line shows the data revision based indicator of global macroeconomic uncertainty. In the second pane, the dashed ochre line shows quarterly averages of the global macroeconomic uncertainty measure proposed by Redl (2018). The third pane compares the global uncertainty indicator by Carriero et al. (2019) to the new uncertainty measure. The last pane display the indicator proposed by Berger et al. (2017) together with the revision based indicator. All indicators are demeaned and normalized to unit variance.

5 Cross-Country Impact of Uncertainty Shocks

Following the existing empirical research on uncertainty, we use a VAR analysis to study the dynamic relationships between macroeconomic activity and uncertainty. We consider the following VAR model:

| (8) |

where is a vector containing all endogenous

variables, denotes time, is a vector of constants, for

are parameter matrices and is the one-step

ahead prediction error with , where is the variance-covariance matrix. The prediction error can be written as a linear combination of structural innovations with , where is an identity

matrix and where is a non-singular parameter matrix.

We choose a recursive identification scheme and a VAR similar to the one proposed in Basu and Bundick (2017), augmenting their VAR setup with a stock market index. Similar to Bloom (2009), we include the stock-market level as the first variable in the VAR. We order uncertainty last to make sure that the impact of all other shocks is already considered for when evaluating the impact of uncertainty on the economy. The ordering of our VAR is as follows:272727We have also experimented with the set-up of Bloom (2009) by ordering uncertainty second right after the stock market variable. This reordering did not change the main results of this paper.

| (9) |

We estimate the model using Bayesian methods, specifying diffuse priors.282828We consulted the Bayesian information criterion and the Akaike information criterion for choosing a lag length. For the different countries and the different criterion, the suggested lag-lengths varied from to . We set the length to throughout this paper. The principal findings of the paper do not change when using lag length instead. Similar to Jurado et al. (2015), we use the posterior mean of our uncertainty indicator discussed in the Section 4 as a measure for macroeconomic uncertainty in our VAR. However, as a further robustness check, we have also estimated the VAR taking into account the uncertainty surrounding our uncertainty indicator. To incorporate the whole posterior distribution instead of just the posterior mean, we extend the algorithm in Section 2.4 by one further block. In this additional step, we obtain a draw for the VAR parameters from a Normal-Inverse Wishart distribution, conditional a draw simulated from the posterior of the uncertainty indicator. The resulting posterior distributions are summarized in Figures 14 and 15 in Appendix E.

5.1 Impact of Uncertainty Shock in the U.S.

We employ the described VAR to investigate the impulse responses functions of key macro variables to uncertainty shocks that are derived using our data revision based uncertainty measure. To validate our uncertainty measure, we compare the impulse responses obtained using the data revisions based uncertainty measure to impulse response functions that are computed with the macroeconomic uncertainty index by Jurado et al. (2015). The estimation sample spans the period 1982Q1–2019Q4.292929Due to irregularities in the revision scheme of U.S. GDP during the 1970s, we start the VAR analysis in 1982Q1 and not earlier. See Table 2 in Fernandez et al. (2011) for a more detailed discussion of these irregularities.

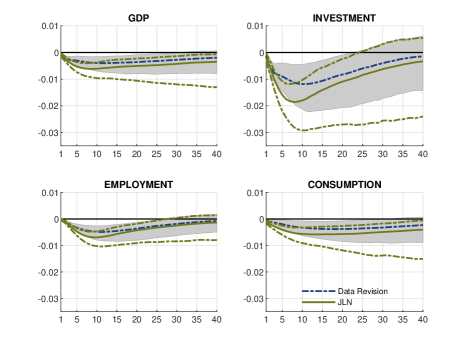

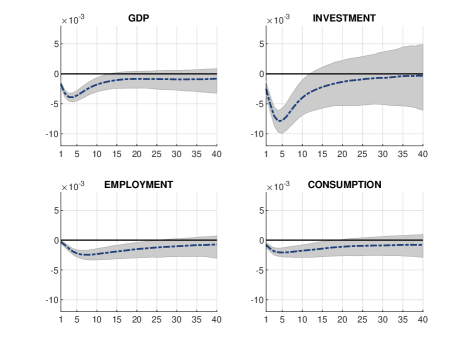

Figure 5 reports the impulse responses of GDP, investment, employment and consumption to an uncertainty shock in the United States. A one standard deviation shock in uncertainty has an adverse and enduring effect on all macroeconomic variables (blue dashed line). For most of the variables the drop lasts for about two years, with most of posterior probability mass lying below zero. During this period output declines by around 0.4%, investment by 1% and, employment and consumption by about 0.5%. The recovery from the uncertainty shock takes up to 10 years and more. While these effects seems somewhat strong and long-lasting, they are very similar to the uncertainty measure of Jurado et al. (2015) (green line).

Notes: The dotted blue line depicts the posterior mean and the grey shaded area the 68% error bands for the impulse responses to an one standard deviation uncertainty shock computed from a VAR model including the uncertainty measure based on data revisions. The solid green line depicts the posterior mean with the dotted green lines representing the 68% error bands for the impulse responses from a model that uses the uncertainty measure of Jurado et al. (2015). The estimation sample spans the period 1982Q1–2019Q4.

5.2 Impact of Uncertainty Shock in G7 countries

In this section, we examine the effects of uncertainty shocks within an international context. Thereby, we use a subset of the uncertainty indicators discussed in Section 4 to estimate the VAR model outlined above for the G7 countries. The intergovernmental economic organization comprises Canada, France, Germany, Italy, Japan, United Kingdom and the United States. In terms of economic importance, the organization makes up for about one third of global GDP based on purchasing power parity. Due to data limitations, we confine our estimates the sample from 1988Q1 to 2019Q4 for all countries. We employ the following country-specific VAR model

| (10) |

where is a country-specific vector containing all endogenous

variables for country and time . is an country specific fixed effect,

are parameter matrices and is the disturbance with , where is the variance-covariance matrix. To obtain an aggregate impulse response for the G7 countries we average across country-specific impulse responses.

Figure 6 shows the cross-country average impulse responses of GDP, investment, employment and consumption to an uncertainty shock. All variables unveil a negative relationship with uncertainty. While the impulse responses for the G7 aggregate in Figure 6 are qualitatively similar to the impulse responses obtained for the United States reported in Figure 5, the average G7 effect of uncertainty shock is about half as strong as the one found for the United States.

Notes: The dotted blue line depicts the posterior mean and the grey shaded area the 68% error bands for the impulse responses to an one standard deviation uncertainty shock. The estimation sample spans the period 1988Q1–2019Q4.

6 On the Role of Employment Protection Legislation

Various studies have documented the negative impacts of uncertainty shocks on the labor market.303030Studies documenting a negative effect of uncertainty on employment include, among others, Basu and Bundick (2017), Bloom (2009), Bloom et al. (2018), Caggiano et al. (2014), Caggiano et al. (2017),

Choi and Loungani (2015), Caldara et al. (2016), Carriero et al. (2018), Jo and Lee (2019), Jurado et al. (2015), Leduc and Liu (2016), Mumtaz (2018), Netšunajev and Glass (2017), Oh and Rogantini Picco (2020) and Scotti (2016). However, while the importance of the investment channel for the propagation of uncertainty shocks has been extensively studied in the literature, fewer studies focus on labor markets rigidities as the dominant transmission channel of uncertainty to the real economy. Recently, however, scholars started to explore this channel in more detail. Cacciatore and Ravenna (2015), for instance, show that binding downward rigidity of wages reinforce the negative effects of uncertainty on employment. In a similar fashion, Leduc and Liu (2016) claim that nominal rigidities amplify the option-value channel through which uncertainty transmits the economy. Guglielminetti (2016) shows that firms reduce open vacancies when uncertainty increases in order to avoid expensive search activities and highlights its importance for the transmission of uncertainty shocks. Matute and Amann (2018), Riegler (2014) and Jo and Lee (2019) study the impact of uncertainty shock on labor flows. Summarizing, the authors find that uncertainty reduces hiring and increases lay offs and voluntary quits. In this study, we focus on the role of firing costs as a possible transmission mechanism of uncertainty shocks. We proxy firing costs with the degree of employment protection legislation and argue that stricter employment protection makes it more difficult—and thus more costly—to fire employees.

To obtain a better understanding of the role of employment protection legislation (EPL) in the propagation of uncertainty shocks, we first study the role of EPL within a theoretical framework and, in a second step, we use our newly developed uncertainty measures to empirically test the theoretical predictions.

6.1 Theoretical Model

To study the importance of EPL for uncertainty shocks within a theoretical model, we need a model that features uncertainty shocks and allows us to impose a stricter EPL. The dynamic stochastic general equilibrium model proposed by Bloom et al. (2018) includes these necessary features. The real business cycle model considers an economy with identical households wanting to maximize life-time discounted utility. All households choose how much they want to consume, work, and invest in order to maximize their life-time utilities. Furthermore, the model features an economy with heterogeneous firms that use labor and capital to produce a final good with the objective to maximize the life-time discounted value of their firm. Firms are subject to an exogenous process of productivity that has a firm-level and a macroeconomic component. Both the macroeconomic as well as the idiosyncratic productivity process vary in the first and second moment, with changes in second moment representing changes in uncertainty. Firms react to changes in productivity by adjusting capital and labor. However, adjusting capital and labor comes at a cost that firms have to take into account when maximizing their firm value.

We chose the model by Bloom et al. (2018) because of the exhaustive way to simultaneously model capital and labor adjustment costs. In our case, we are particularly interested in the way the authors model labor adjustment costs. The model includes two types of labor adjustment costs (). Firms face fixed and linear costs when adjusting labor. Fixed costs represent a lump sum cost that arises when employees are hired or fired. This cost does not depend on the size of the adjustment but on the state of the economy. One can think of these costs as arising from the deficiency in production owing to an experienced employee leaving the company or a new employee entering it. In contrast to fixed costs, linear costs depend on the size of the labor adjustment. These costs include, among others, recruiting and training costs for new employees and severance payment when laying off employees. Labor adjustment costs can thus be formally expressed as

| (11) |

where represent fixed labor adjustment costs that depend on the current state of production . represents an indicator function and indicates the change in employment. and represent hiring and firing costs as a percentage of the annual wage bill .

As we aim to examine the effects of stricter employment protection legislation, we adjust the parameter that we associate most with stronger labor protection: firing costs. Stricter employment protection legislation makes it harder for firms to lay off employees. Hence, stricter employment protection legislation increases firing costs. Theoretically, firing costs change the effects of uncertainty on employment in two ways. First, an increase in firing costs reduces firing when uncertainty increases. Second, an increase in firing costs reduces hiring. The reason for this is the following: In the presence of non-convex adjustment costs—firing costs in our case—firms face Ss hiring/firing policy rules (Scarf, 1959). That is, firms do not hire new employees until productivity reaches an upper threshold (the S in Ss) and do not fire employees until its productivity hits a lower threshold (the s in Ss). Stricter employment protection legislation reduces the lower threshold. Hence, productivity needs to fall more before firms start firing employees. Overall employment will fall less compared to an economy with lower employment protection standards. This mechanism is similar to the one described by Bell (2016). Using a partial equilibrium model, the author shows that an increase in firing costs has a negative effect on employment because firms reduce hiring due to precautionary reasons. Overall, however, the negative effect on uncertainty is reversed as the increase in costs discourages firing by more than it does hiring. The reason being that laying off employees causes immediate costs, while hiring costs are discounted as they only become relevant once a firm fills the vacant position again.

In order to study the role of EPL the propagation of uncertainty shocks we calibrate, solve and simulate the model of Bloom et al. (2018) twice, once for an economy for low EPL and once for an economy with high EPL. In order to ensure comparability with Bloom et al. (2018) and the RBC literature in general, we do not change the calibration proposed by Bloom et al. (2018), except for the firing cost parameter. For the United States, Bloom et al. (2018) assume firing costs to be on average 1.8% of an annual wage bill. For continental European economies—countries that according to the OECD Employment Protection Database have on average stricter EPL—studies report substantially higher firing costs (Grund, 2006, Kramarz and Michaud, 2010). It is surprisingly hard to find studies quantifying firing costs for countries other than the US. Del Boca and Rota (1998) interview Italian manufacturing firms and find firing costs that range from less than half a monthly (3.6% of an annual wage bill) of labour cost to up to 20 months of labour costs (166% of an annual wage bill) in cases of a conflict. Unfortunately, the authors do not provide averages. For illustrative purposes, we start from the lowest reported value that is twice as high as in the case of Bloom et al. (2018), i.e. we assume firing costs to be on average 3.6% of an annual wage bill. Table 2 summarizes the labor adjustment parameters.

| Parameter Description | Low EPL | High EPL | |

|---|---|---|---|

| : | fixed hiring/firing costs (% sales) | 0.021 | 0.021 |

| : | per capita hiring (% of annual wage bill) | 0.018 | 0.018 |

| : | per capita firing cost (% of annual wage bill) | 0.018 | 0.036 |

Notes: This table presents the model calibration and parameter choices. The calibration reflects a quarterly calibration of the model and is based on Bloom et al. (2018).

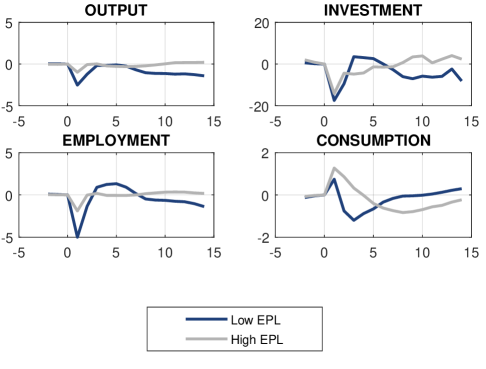

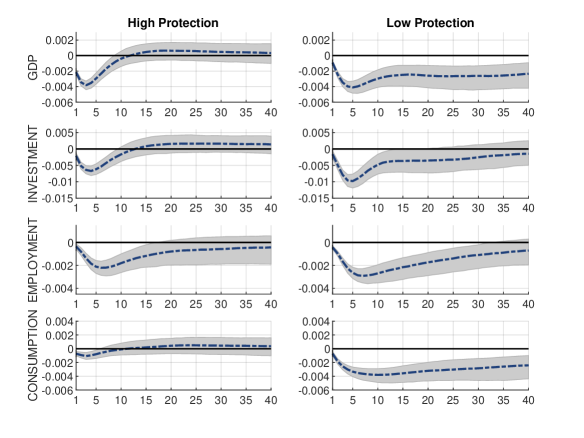

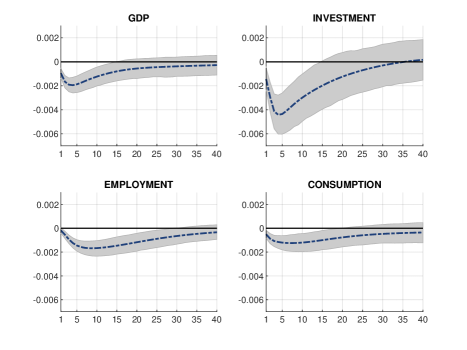

We use two differently calibrated models to simulate the reaction of the economy to an uncertainty shock. In the case of this model, an uncertainty shock corresponds to an increase in variance of the shock distribution from which future realisations of productivity (TFP) will be drawn. Figure 7 presents the impulse responses of output, investment, employment and consumption to an uncertainty shock. The blue lines presents the impulse response of an uncertainty shock under low employment protection legislation and the gray line shows the impulse response of the same uncertainty shock under high employment protection. Both economies contract after an uncertainty shock. The uncertainty shock causes an immediate contraction of output in the first period followed by a recovery starting in the subsequent quarters. Three channels contribute to this fall in output: the investment channel, the employment channel, and the misallocation of factors of production.313131Section 5 of Bloom et al. (2018) provides an in-depth discussion of these channels and dissects the impact of an uncertainty shock in its various components. The presence of capital adjustment costs causes investment to drop sharply after an uncertainty shock. In the first period investment drops by around 15% followed by a rapid recovery. Also employment reacts negatively to an uncertainty shocks. As firms face firing and hiring costs when adjusting their number of employees, an increase in uncertainty reduces hiring and firing activities of firms. Thereby, hiring decreases more than firing. Moreover, employment also decreases because of labor attrition. Finally, the decrease in firing and hiring increases the misallocation of factors of production. Households expect the increase in misallocation to decrease future productivity and thus to lower the expected return on savings making immediate consumption more attractive. These dynamics lead in combination with the available resources in the economy—the capital stock does not adjust to uncertainty in period one—to an increase in consumption in the first period. The increase of consumption following an uncertainty is a well-known artefact of this model. Bloom et al. (2018) extensively discuss this behaviour in their paper. As we focus on role of firing cost on the propagation of uncertainty shocks, we are primarily interested in changes of the consumption dynamics relative to the original specification.

When increasing firing costs the reaction of output, investment, employment, and consumption to an uncertainty shock remain similar in their dynamics. However, the amplitude of the time profile changes considerably. Increasing firing costs increases the option value of waiting as it makes it more expensive for firms to lay off employees. Thus, the uncertainty shocks reduces employment less compared to the original specification. In contrast to employment, investment still decreases almost by as much after the uncertainty shocks as in the original specification. As more production factors remain in the economy, output reduces by less than in the original specification. Finally, the increase in firing costs increases the misallocation of factor of production which in combination with higher production increases consumption compared to the original specification. Overall, increasing firing costs causes an uncertainty shock to have less contractionary effects on the economy.

Notes: This figure presents DSGE impulse responses of output, investment, employment and consumption after an uncertainty shock. Thereby, the blue lines presents the impulse response to uncertainty shock under low employment protection legislation and the gray line shows the impulse response of the same uncertainty shock under high employment protection.

6.2 Evidence from a VAR

Now, we use the international set of revision based measures of uncertainty to test this theoretical prediction. We thus split countries into two groups according to their strictness of employment protection.323232We confine this analysis to countries for which we have data since 1990. Hence, we end up with the United States, Canada, United Kingdom, Switzerland, Japan, France, Germany, Sweden and Italy. To split countries according to their degree of employment protection, we use the annual time series data of the OECD Employment Protection Database to calculate the average value of the strictness of employment protection. Specifically, we use the measure of individual and collective dismissals (EPRC_V1) from 1985 to 2013. Table 3 ranks countries according to the strictness of employment protection.

| Country | Average EPL (1985-2013) |

|---|---|

| United States | 0.26 |

| Canada | 0.92 |

| United Kingdom | 1.17 |

| Switzerland | 1.60 |

| Median | 1.62 |

| Japan | 1.62 |

| France | 2.39 |

| Germany | 2.65 |

| Sweden | 2.70 |

| Italy | 2.76 |

Notes: This table ranks countries according to the strictness of employment protection. In order to calculate the ranking, we use the annual time series data of the OECD Employment Protection Database to calculate the average value of the strictness of employment protection – individual and collective dismissals (EPRC_V1) - over time (from 1985 to 2013).

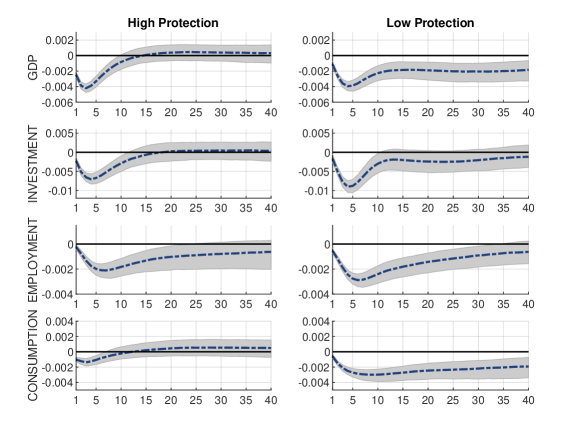

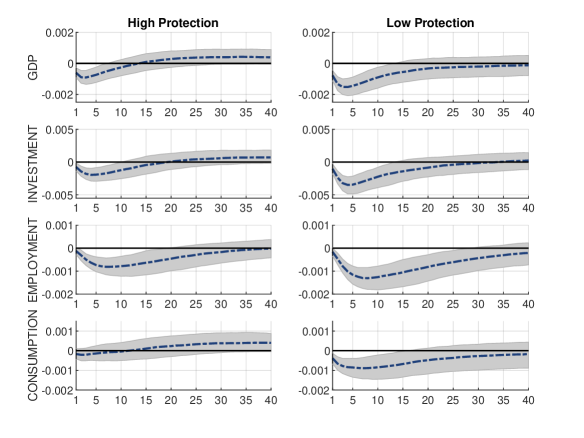

The groups selected in Table 3 mirror our expectations with Anglo-Saxon economies displaying a low degree and continental European countries showing higher degree of employment protection standards. According to OECD Employment Protection Database, Switzerland and Japan have a very similar degree of EPL. In our baseline specification, we include Switzerland in the group with low labor protection and Japan in the group of high EPL countries.333333As a robustness test, we re-run the analysis excluding both Japan and Switzerland. Neglecting the two countries does not significantly change the results (see Figure 13 in Appendix E). To obtain group-specific impulse responses to an uncertainty shock, we use the VAR described in section 5.2, averaging across country-specific impulse responses for each group. Our empirical findings suggest that uncertainty has indeed less deteriorating effects in countries with high employment protection. Figure 8 shows that the effect of a one standard deviation uncertainty shock is not only more contractionary in countries with high protection compared to countries with low labor protection, the negative effects are also more persistent.

Notes: The dotted blue line depicts the posterior mean and the grey shaded area the 68% error bands for the impulse responses to an one standard deviation uncertainty shock. The estimation sample spans the period 1988Q1–2019Q4.

The results presented in Figure 8 are consistent with the theoretical predictions outlined above. In countries with stricter employment protection legislation, it is more costly for firms to reduce employment. Hence, employment drops less in the light of an uncertainty shock.343434We divide countries according to their level of employment protection legislation. Theoretically, the two groups of countries could also differ along other dimension that are relevant for the uncertainty transmission channel, i.e. level of capital adjustment costs. However, we cannot think of a good reason why a country’s employment protection legislation should correlate with its capital adjustment costs. In the absence of comparable capital adjustment cost data, we leave it to future research to control for capital adjustment costs. Because of the lower response of employment and because of the complementarity of capital and labor, firms do not cut investment by as much, causing production to contract less. Finally, uncertainty decreases consumption less in countries with high labor protection. As pointed out in 6.1, an uncertainty shock increases the misallocation in an economy more if firing costs are higher. Households expect the increased missalocation to decrease future return on savings and they decrease consumption less. While this mechanism might explain parts of the differences in the consumption dynamics, precautionary saving might also be part of the story. A higher degree of labor protection transmits into a higher job security of employees. An increase in uncertainty lets employees worry less about their future income in case of high employment protection than in case of low employment protection. Households thus increase precautionary saving less and decrease consumption by less which causes a less pronounced drop of aggregate demand. Our findings are consistent with the evidence presented by Jo and Lee (2019) that indicates that compared to Germany, labor market frictions in the U.S. might be too low for uncertainty to have strong real option effects on employment. Our evidence complements the literature on the importance of the labor channel in explaining the transmission of uncertainty shocks. However, it highlights a different mechanism. In contrast to Guglielminetti (2016), who argues for the importance of hiring costs, our results indicate a prominent role of firing costs in explaining the dynamics of uncertainty shocks.

7 Conclusion

In this paper we have introduced new internationally comparable measures of macroeconomic uncertainty for a large set of countries using data revisions in aggregate variable that are bound to the system of national accounts. We have set up an econometric model and constructed a new real-time data set of real GDP for 39 countries that serves as the basis for our estimations. Using real-time data permits us to obtain accurate estimates of forecast error based uncertainty that an economic agent experienced at any given point in time, whereas existing measures of macroeconomic uncertainty base on forecast errors that are constructed with non real-time data.

In order to obtain real-time uncertainty estimates, we extended the data revision model proposed by Jacobs and van Norden (2011) such that it allows us to extract the volatility of the unpredictable part of future releases of the news component that forms our measure of macroeconomic uncertainty. We showed that the resulting uncertainty indicator for the United States has similar properties than the macroeconomic uncertainty measures proposed by Jurado et al. (2015). The revision based indicator is thereby less volatile than alternative measures such as the economic policy uncertainty index by Baker et al. (2016) or the VIX and the revision based indicator also identifies the same three major uncertainty shocks between 1965 and 2016. Namely, the recession in the 1970s, the early 1980s recession and the Great Recession of 2008. The revision based indicator reaches its highest peak during 1970s. Considering that the recession in the 1970s comprised the first oil price shocks, the collapse of the Bretton Woods System and the end of the post World War II economic expansion this seems coherent with a broader economic history perspective. Our empirical evaluation indicates a strong and negative relationship between the revision based uncertainty measures and the economy. Estimating VARs for the United States and the G7 countries shows that a one standard deviation shock in the revision based uncertainty indicators leads to a contraction in GDP, investment, employment and consumption.

We studied the importance of labor market frictions for the propagation of uncertainty shocks. In a cross-country VAR analysis, we found that uncertainty shocks have more deteriorating effects in countries with a lower degree of EPL compared to countries with stricter EPL. Using the theoretical model of Bloom et al. (2018) with varying degree of firing costs, we show that these empirical findings are in line with theory.

References

- Ahir et al. (2018) H. Ahir, N. Bloom, and D. Furceri. The world uncertainty index. Available at SSRN 3275033, 2018.

- Altig et al. (2020) D. Altig, S. Baker, J. M. Barrero, N. Bloom, P. Bunn, S. Chen, S. J. Davis, J. Leather, B. Meyer, E. Mihaylov, et al. Economic uncertainty before and during the covid-19 pandemic. Journal of Public Economics, 191:104274, 2020.

- Baker et al. (2016) S. R. Baker, N. Bloom, and S. J. Davis. Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4):1593–1636, 2016.

- Basu and Bundick (2017) S. Basu and B. Bundick. Uncertainty shocks in a model of effective demand. Econometrica, 85(3):937–958, 2017.

- Bell (2016) U.-L. Bell. Adjustment costs, uncertainty and employment inertia. Working Paper Series Bank of Spain, (9620), 2016.

- Berger et al. (2017) T. Berger, S. Grabert, and B. Kempa. Global macroeconomic uncertainty. Journal of Macroeconomics, 53:42–56, 2017.

- Bloom (2009) N. Bloom. The impact of uncertainty shocks. Econometrica, 77(3):623–685, 2009. ISSN 1468-0262. doi: 10.3982/ECTA6248. URL http://dx.doi.org/10.3982/ECTA6248.

- Bloom (2014) N. Bloom. Fluctuations in uncertainty. Journal of Economic Perspectives, 28(2):153–76, 2014. doi: 10.1257/jep.28.2.153. URL http://www.aeaweb.org/articles.php?doi=10.1257/jep.28.2.153.

- Bloom et al. (2018) N. Bloom, M. Floetotto, N. Jaimovich, I. Saporta-Eksten, and S. J. Terry. Really uncertain business cycles. Econometrica, 86(3):1031–1065, 2018.

- Boysen-Hogrefe and Neuwirth (2012) J. Boysen-Hogrefe and S. Neuwirth. The impact of seasonal and price adjustments on the predictability of german gdp revisions. Technical report, Kiel Working Paper, 2012.

- Cacciatore and Ravenna (2015) M. Cacciatore and F. Ravenna. Uncertainty, wages, and the business cycle. In 29th Annual Meeting of the Canadian Macroeconomics Study Group, Montréal, pages 6–7, 2015.

- Caggiano et al. (2014) G. Caggiano, E. Castelnuovo, and N. Groshenny. Uncertainty shocks and unemployment dynamics in us recessions. Journal of Monetary Economics, 67:78–92, 2014.

- Caggiano et al. (2017) G. Caggiano, E. Castelnuovo, and J. M. Figueres. Economic policy uncertainty and unemployment in the united states: A nonlinear approach. Economics Letters, 151:31–34, 2017.

- Caggiano et al. (2020) G. Caggiano, E. Castelnuovo, and J. M. Figueres. Global uncertainty. mimeo, 2020.

- Caldara et al. (2016) D. Caldara, C. Fuentes-Albero, S. Gilchrist, and E. Zakrajšek. The macroeconomic impact of financial and uncertainty shocks. European Economic Review, 88:185–207, 2016.

- Carriero et al. (2018) A. Carriero, T. E. Clark, and M. Marcellino. Measuring uncertainty and its impact on the economy. Review of Economics and Statistics, 100(5):799–815, 2018.

- Carriero et al. (2019) A. Carriero, T. E. Clark, and M. Marcellino. Asssessing international commonality in macroeconomic uncertainty and its effects. Journal of Applied Econometrics, 2019.

- Carter and Kohn (1994) C. K. Carter and R. Kohn. On Gibbs sampling for state space models. Biometrika, 81(3):541–553, 09 1994.

- Cascaldi-Garcia et al. (2020) D. Cascaldi-Garcia, D. Datta, T. RT Ferreira, O. V. Grishchenko, M. R. Jahan-Parvar, J. M. Londono, F. Loria, S. Ma, M. Rodriguez, J. H. Rogers, et al. What is certain about uncertainty? Olesya V. and Jahan-Parvar, Mohammad R. and Londono-Yarce, Juan-Miguel and Loria, Francesca and Ma, Sai and Rodriguez, Marius and Rogers, John H. and Sarisoy, Cisil and Zer, Ilknur, What is Certain About Uncertainty, 2020.

- Castelnuovo (2019) E. Castelnuovo. Domestic and global uncertainty: A survey and some new results. CESifo Working Paper Series, (7900), 2019.

- Choi and Loungani (2015) S. Choi and P. Loungani. Uncertainty and unemployment: The effects of aggregate and sectoral channels. Journal of Macroeconomics, 46:344–358, 2015.

- Clark et al. (2020) T. E. Clark, M. W. McCracken, and E. Mertens. Modeling time-varying uncertainty of multiple-horizon forecast errors. The Review of Economics and Statistics, 102(1):17–33, 2020.

- Cogley and Sargent (2005) T. Cogley and T. J. Sargent. Drifts and volatilities: monetary policies and outcomes in the post wwii us. Review of Economic Dynamics, 8(2):262 – 302, 2005. ISSN 1094-2025. doi: https://doi.org/10.1016/j.red.2004.10.009. URL http://www.sciencedirect.com/science/article/pii/S1094202505000049. Monetary Policy and Learning.

- Croushore and Stark (2001) D. Croushore and T. Stark. A real-time data set for macroeconomists. Journal of Econometrics, 105(1):111 – 130, 2001. ISSN 0304-4076. doi: https://doi.org/10.1016/S0304-4076(01)00072-0. URL http://www.sciencedirect.com/science/article/pii/S0304407601000720. Forecasting and empirical methods in finance and macroeconomics.

- Davis (2016) S. J. Davis. An index of global economic policy uncertainty. Technical report, National Bureau of Economic Research, 2016.

- de Jong (1987) P. de Jong. Rational economic data revisions. Journal of Business & Economic Statistics, 5(4):539–548, 1987.

- Del Boca and Rota (1998) A. Del Boca and P. Rota. How much does hiring and firing cost? survey evidence from a sample of italian firms. Labour, 12(3):427–449, 1998.

- Fernandez et al. (2011) A. Z. Fernandez, H. Branch, E. F. Koenig, and A. Nikolsko-Rzhevskyy. A real-time historical database for the oecd. Globalization and Monetary Policy Institute Working Paper, 96, 2011.

- Fernández-Villaverde and Guerrón-Quintana (2020) J. Fernández-Villaverde and P. A. Guerrón-Quintana. Uncertainty shocks and business cycle research. Technical report, National Bureau of Economic Research, 2020.

- Fox et al. (2017) D. R. Fox, S. H. McCulla, S. Smith, E. P. Seskin, E. Strassner, D. B. Wasshausen, B. R. Moulton, C. E. Moylan, and N. M. Mayerhauser. Methods of the us national income and product account. US Department of Commerce, Bureau of Economic Analysis: Washington, WA, USA, page 447, November 2017.

- Frühwirth-Schnatter (1994) S. Frühwirth-Schnatter. Data augmentation and dynamic linear models. Journal of Time Series Analysis, 15(2), 1994.

- Gilchrist and Zakrajšek (2012) S. Gilchrist and E. Zakrajšek. Credit spreads and business cycle fluctuations. American Economic Review, 102(4):1692–1720, 2012.

- Golinelli and Parigi (2008) R. Golinelli and G. Parigi. Real-time squared: A real-time data set for real-time gdp forecasting. International Journal of Forecasting, 24(3):368–385, 2008.

- Grund (2006) C. Grund. Severance payments for dismissed employees in germany. European Journal of Law and Economics, 22(1):49–71, 2006.

- Guglielminetti (2016) E. Guglielminetti. The labor market channel of macroeconomic uncertainty. Bank of Italy Temi di Discussione (Working Paper) No, 1068, 2016.

- Harmsen et al. (2003) H. Harmsen, L. Meeuwesen, J. Van Wieringen, R. Bernsen, and M. Bruijnzeels. When cultures meet in general practice: intercultural differences between gps and parents of child patients. Patient education and counseling, 51(2):99–106, 2003.

- Hassan et al. (2020) T. A. Hassan, S. Hollander, L. van Lent, and A. Tahoun. The global impact of brexit uncertainty. Technical report, National Bureau of Economic Research, 2020.

- Jacobs and van Norden (2011) J. P. Jacobs and S. van Norden. Modeling data revisions: Measurement error and dynamics of ”true” values. Journal of Econometrics, 161(2):101–109, 2011. URL https://EconPapers.repec.org/RePEc:eee:econom:v:161:y:2011:i:2:p:101-109.

- Jacobs et al. (2020) J. P. Jacobs, S. Sarferaz, J.-E. Sturm, and S. van Norden. Can gdp measurement be further improved? data revision and reconciliation. Journal of Business & Economic Statistics, 2020. URL https://doi.org/10.1080/07350015.2020.1831928.

- Jo and Lee (2019) S. Jo and J. J. Lee. Uncertainty and labor market fluctuations. Technical Report 1904, Federal Reserve Bank of Dallas, 2019.

- Jo and Sekkel (2019) S. Jo and R. Sekkel. Macroeconomic uncertainty through the lens of professional forecasters. Journal of Business & Economic Statistics, 37(3):436–446, 2019. doi: 10.1080/07350015.2017.1356729. URL https://doi.org/10.1080/07350015.2017.1356729.

- Jurado et al. (2015) K. Jurado, S. C. Ludvigson, and S. Ng. Measuring uncertainty. American Economic Review, 105(3):1177–1216, 2015. doi: 10.1257/aer.20131193. URL http://www.aeaweb.org/articles.php?doi=10.1257/aer.20131193.

- Kastner and Frühwirth-Schnatter (2014) G. Kastner and S. Frühwirth-Schnatter. Ancillarity-sufficiency interweaving strategy (asis) for boosting mcmc estimation of stochastic volatility models. Computational Statistics & Data Analysis, 76:408–423, 2014.

- Kim et al. (1998) S. Kim, N. Shephard, and S. Chib. Stochastic volatility: Likelihood inference and comparison with arch models. The Review of Economic Studies, 65(3):361–393, 1998. ISSN 00346527, 1467937X. URL http://www.jstor.org/stable/2566931.

- Kishor and Koenig (2012) K. Kishor and E. F. Koenig. Var estimation and forecasting when data are subject to revision. Journal of Business & Economic Statistics, 30(2):181–190, 2012.

- Kramarz and Michaud (2010) F. Kramarz and M.-L. Michaud. The shape of hiring and separation costs in france. Labour Economics, 17(1):27–37, 2010.

- Kwon et al. (2009) K. Kwon, G. A. Barnett, and H. Chen. Assessing cultural differences in translations: A semantic network analysis of the universal declaration of human rights. Journal of International and Intercultural Communication, 2(2):107–138, 2009.

- Leduc and Liu (2016) S. Leduc and Z. Liu. Uncertainty shocks are aggregate demand shocks. Journal of Monetary Economics, 82:20–35, 2016.

- Lee et al. (2012) K. Lee, N. Olekalns, K. Shields, and Z. Wang. Australian real-time database: An overview and an illustration of its use in business cycle analysis. Economic Record, 88(283):495–516, 2012.

- Ludvigson et al. (2015) S. C. Ludvigson, S. Ma, and S. Ng. Uncertainty and business cycles: Exogenous impulse or endogenous Response? NBER Working Papers 21803, National Bureau of Economic Research, Inc, Dec. 2015. URL https://ideas.repec.org/p/nbr/nberwo/21803.html.

- Mankiw and Shapiro (1986) N. Mankiw and M. Shapiro. News or noise: An analysis of gnp revisions. Survey of Current Business, 66:20–25, 1986.

- Mankiw et al. (1984) N. Mankiw, D. E. Runkle, and M. D. Shapiro. Are preliminary announcements of the money stock rational forecasts? Journal of Monetary Economics, 14(1):15 – 27, 1984. ISSN 0304-3932. doi: https://doi.org/10.1016/0304-3932(84)90024-2. URL http://www.sciencedirect.com/science/article/pii/0304393284900242.

- Matute and Amann (2018) M. M. Matute and A. U. Amann. Uncertainty, firm heterogeneity and labour adjustments: evidence from european countries. Documentos de trabajo del Banco de España, (21):1–32, 2018.

- McCausland et al. (2011) W. McCausland, S. Miller, and D. Pelletier. Simulation smoothing for state-space models: A computational efficiency analysis. Computational Statistics & Data Analysis, 55(1):199–212, 2011. URL https://EconPapers.repec.org/RePEc:eee:csdana:v:55:y:2011:i:1:p:199-212.

- Mumtaz (2018) H. Mumtaz. Does uncertainty affect real activity? evidence from state-level data. Economics Letters, 167:127–130, 2018.

- Mumtaz and Theodoridis (2017) H. Mumtaz and K. Theodoridis. Common and country specific economic uncertainty. Journal of International Economics, 105:205–216, 2017.

- Netšunajev and Glass (2017) A. Netšunajev and K. Glass. Uncertainty and employment dynamics in the euro area and the us. Journal of Macroeconomics, 51:48–62, 2017.

- OECD (2017) OECD. OECD Main Economic Indicators (MEI). Original Release Data and Revisions Database, 2017. http://stats.oecd.org/mei/default.asp?rev=1.

- Oh and Rogantini Picco (2020) J. Oh and A. Rogantini Picco. Macro uncertainty and unemployment risk. (395), 2020.

- Ozturk and Sheng (2018) E. O. Ozturk and X. S. Sheng. Measuring global and country-specific uncertainty. Journal of international money and finance, 88:276–295, 2018.

- Redl (2017) C. Redl. The impact of uncertainty shocks in the united kingdom. Staff Working Paper, (695), 2017.

- Redl (2018) C. Redl. Uncertainty matters: evidence from close elections. 2018.

- Riegler (2014) M. Riegler. The impact of uncertainty shocks on the job-finding rate and separation rate. Mimeo, 2014.

- Rogers and Xu (2019) J. H. Rogers and J. Xu. How well does economic uncertainty forecast economic activity? 2019.

- Rossi and Sekhposyan (2015) B. Rossi and T. Sekhposyan. Macroeconomic uncertainty indices based on nowcast and forecast error distributions. American Economic Review, 105(5):650–55, May 2015. doi: 10.1257/aer.p20151124. URL https://www.aeaweb.org/articles?id=10.1257/aer.p20151124.

- Sargent (1989) T. J. Sargent. Two models of measurements and the investment accelerator. Journal of Political Economy, 97(2):251–287, 1989. ISSN 00223808, 1537534X. URL http://www.jstor.org/stable/1831313.

- Scarf (1959) H. Scarf. The optimality of (5, 5) policies in the dynamic inventory problem. 1959.

- Scotti (2016) C. Scotti. Surprise and uncertainty indexes: Real-time aggregation of real-activity macro-surprises. Journal of Monetary Economics, 82:1–19, 2016.

- Scruton et al. (2018) J. Scruton, M. O’Donnell, and S. Dey-Chowdhury. Introducing a new publication model for gdp. Office for National Statistics, pages 1 – 14, 4 2018. doi: https://doi.org/10.1016/0304-3932(84)90024-2. URL https://www.ons.gov.uk/economy/grossdomesticproductgdp/articles/introducinganewpublicationmodelforgdp/2018-04-27.

- Sims (2001) C. A. Sims. Comment on sargent and cogley’s ’evolving post world war ii us inflation dynamics’. NBER Macroeconomics Annual, 16:373–379, 2001.

- Sleeman (2006) C. Sleeman. Analysis of revisions to quarterly gdp–a real-time database. Reserve Bank of New Zealand Bulletin, 69(1):31–44, 2006.

- Stock (2001) J. H. Stock. Comment on evolving post-world war ii us inflation dynamics. NBER Macroeconomics Annual, 16(1), 2001.

- Yu and Meng (2011) Y. Yu and X.-L. Meng. To center or not to center: That is not the question—an ancillarity–sufficiency interweaving strategy (asis) for boosting mcmc efficiency. Journal of Computational and Graphical Statistics, 20(3):531–570, 2011.

Appendix A Posterior Simulations

In this section we describe the blocks of our Gibbs sampling procedure outlined in section 2. Note that Equations (2) and (6) can be rewritten as

| (12) | ||||

| (13) |

with

A.1 Drawing News, Noise and True Values

A.2 Drawing Stochastic Volatility

Conditional on news, noise, true values and the VAR coefficients of (13), we obtain draws for the stochastic volatilities () using the estimation method proposed in Kastner and Frühwirth-Schnatter (2014). We thus estimate the stochastic volatilities by interweaving estimation models specified in a centered (C) and a non-centered (NC) parameterization using the ancillarity-sufficiency interweaving strategy (ASIS) detailed by Yu and Meng (2011). This estimation strategy addresses the trade-off in terms of sampling efficiency depending on the value of the persistence parameter . Kastner and Frühwirth-Schnatter (2014) show that this estimation strategy outperforms estimators using pure centered or non-centered parameterizations.

Starting from Equation (4), we assume that:

| (14) | ||||

| (15) |

with and . One can express the centered parametrization of Equation (17) as a non-centered parametrization. In the non-centered parametrization the volatility components are assumed to follow the following process:

| (16) |

with and .

We can rewrite Equation (14) as

| (17) |

with and denotes . The fact that we can approximate the distribution of by a mixture of normal distributions, that is, with indicating the mixture component, we can rewrite Equation (17) as a linear and conditionally Gaussian state space model,

| (18) |

with . Based on Equation (18), we apply a MCMC procedure outlined in Kastner and Frühwirth-Schnatter (2014) that interweaves the centered and non-centered specification.

We rely on the priors proposed in Kastner and Frühwirth-Schnatter (2014). That is, follows a normal distribution with mean and variance , i.e. . The persistence parameter follows a Beta distribution, i.e. . Finally, for the volatility parameter , they chose . We use the same priors for the centered and non-centered parameterization. We calibrate the parameters as follows: , , , and .

The MCMC interweaving procedure consists of the following steps:

-

1.

We sample the volatilities using the all without a loop (AWOL) procedure by drawing from . The initial values are drawn from .

-

2.

We sample , and using Bayesian regression. We use a 2-block sampler, where we draw from and we jointly sample and from . Because the chosen priors are not analytically tractable, we calculate updates via a Metropolis-Hastings (MH) algorithm.

-

3.

Move to NC by the deterministic transformation

-

4.

Redraw for NC specification. We need MH only to update by drawing from . We can Gibbs-update and jointly from .

-

5.

Move back to C by calculating for all t

-

6.

Draw the indicators (C). We update the mixture component indicators from using inverse transform sampling.

A.3 Drawing Time-Varying Coefficients

Conditional on news, noise, true values and the stochastic volatilities, we draw the time-varying coefficients of Equation (13), by considering the process of true GDP to be represented by the following state space model

| (19) | ||||

| (20) |

with

| (21) | |||

We obtain estimates for and using the method proposed by McCausland et al. (2011). We set up the diagonal matrix as follows:

Diagonal Matrix

| (22) |

Diagonal Elements

| (23) | ||||

| (24) | ||||

| (25) |

Off-Diagonal Elements

| (27) |

with

| (29) |

We set up the co-vector the following way:

Covector

| (31) |

with

| (32) | ||||

| (33) | ||||

| (34) |

We solve this system by first computing the Cholesky decomposition that we implement directly in Julia. Because of the band structure of , the decomposition is incredibly fast. In a second step, we draw and solve for . Finally, we use back-substitution in order to solve for .

Appendix B Real-Time Data

We use data revisions in macroeconomic aggregates to obtain measures of macroeconomic uncertainty for various OECD countries. Real-time data releases of macroeconomic aggregates are thereby the key ingredient to construct the uncertainty indicator. In our preferred specification, we base the indicator on nominal GDP. In order to obtain a comprehensive data set for various countries, we need to tap and combine several data sources. Appendix B describes these various data sources and outlines the construction of our data base in great detail.

B.1 Real-Time Data: Main Source