Fair Regression with Wasserstein Barycenters

Abstract

We study the problem of learning a real-valued function that satisfies the Demographic Parity constraint. It demands the distribution of the predicted output to be independent of the sensitive attribute. We consider the case that the sensitive attribute is available for prediction. We establish a connection between fair regression and optimal transport theory, based on which we derive a close form expression for the optimal fair predictor. Specifically, we show that the distribution of this optimum is the Wasserstein barycenter of the distributions induced by the standard regression function on the sensitive groups. This result offers an intuitive interpretation of the optimal fair prediction and suggests a simple post-processing algorithm to achieve fairness. We establish risk and distribution-free fairness guarantees for this procedure. Numerical experiments indicate that our method is very effective in learning fair models, with a relative increase in error rate that is inferior to the relative gain in fairness.

1 Introduction

A central goal of algorithmic fairness is to ensure that sensitive information does not “unfairly” influence the outcomes of learning algorithms. For example, if we wish to predict the salary of an applicant or the grade of a university student, we would like the algorithm to not unfairly use additional sensitive information such as gender or race. Since today’s real-life datasets often contain discriminatory bias, standard machine learning methods behave unfairly. Therefore, a substantial effort is being devoted in the field to designing methods that satisfy “fairness” requirements, while still optimizing prediction performance, see for example [5, 10, 13, 16, 17, 20, 22, 24, 25, 27, 32, 45, 46, 47, 49] and references therein.

In this paper we study the problem of learning a real-valued regression function which among those complying with the Demographic Parity fairness constraint, minimizes the mean squared error. Demographic Parity requires the probability distribution of the predicted output to be independent of the sensitive attribute and has been used extensively in the literature, both in the context of classification and regression [1, 12, 19, 23, 34]. In this paper we consider the case that the sensitive attribute is available for prediction. Our principal result is to show that the distribution of the optimal fair predictor is the solution of a Wasserstein barycenter problem between the distributions induced by the unfair regression function on the sensitive groups. This result builds a bridge between fair regression and optimal transport, [see e.g., 41, 38].

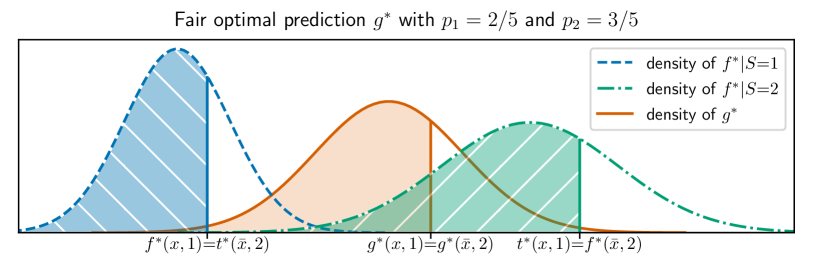

We illustrate our result with an example. Assume that represents a candidate’s skills, is a binary attribute representing two groups of the population (e.g., majority or minority), and is the current market salary. Let be the regression function, that is, the optimal prediction of the salary currently in the market for candidate . Due to bias present in the underlying data distribution, the induced distribution of market salary predicted by varies across the two groups. We show that the optimal fair prediction transforms the regression function as

where is the frequency of group and the correction is determined so that the ranking of relative to the distribution of for group (e.g., minority) is the same as the ranking of relative to the distribution of the group (e.g., majority). We elaborate on this example after Theorem 2.3 and in Figure 1. The above expression of the optimal fair predictor naturally suggests a simple post-processing estimation procedure, where we first estimate and then transform it to get an estimator of . Importantly, the transformation step involves only unlabeled data since it requires estimation of cumulative distribution functions.

Contributions and organization. In summary we make the following contributions. First, in Section 2 we derive the expression for the optimal function which minimizes the squared risk under Demographic Parity constraints (Theorem 2.3). This result establishes a connection between fair regression and the problem of Wasserstein barycenters, which allows to develop an intuitive interpretation of the optimal fair predictor. Second, based on the above result, in Section 3 we propose a post-processing procedure that can be applied on top of any off-the-shelf estimator for the regression function, in order to transform it into a fair one. Third, in Section 4 we show that this post-processing procedure yields a fair prediction independently from the base estimator and the underlying distribution (Proposition 4.1). Moreover, finite sample risk guarantees are derived under additional assumptions on the data distribution provided that the base estimator is accurate (Theorem 4.4). Finally, Section 5 presents a numerical comparison of the proposed method w.r.t. the state-of-the-art.

Related work. Unlike the case of fair classification, fair regression has received limited attention to date; we are only aware of few works on this topic that are supported by learning bounds or consistency results for the proposed estimator [1, 34]. Connections between algorithmic fairness and Optimal Transport, and in particular the problem of Wasserstein barycenters, has been studied in [12, 19, 23, 43] but mainly in the context of classification. These works are distinct from ours, in that they do not show the link between the optimal fair regression function and Wasserstein barycenters. Moreover, learning bounds are not addressed therein. Our distribution-free fairness guarantees share similarities with contributions on prediction sets [31, 30] and conformal prediction literature [42, 48] as they also rely on results on rank statistics. Meanwhile, the risk guarantee that we derive, combines deviation results on Wasserstein distances in one dimension [7] with peeling ideas developed in [3], and classical theory of rank statistics [40].

Notation. For any positive integer we denote by the set . For we denote by (resp. ) the minimum (resp. the maximum) between and . For two positive real sequences we write to indicate that there exists a constant such that for all . For a finite set we denote by its cardinality. The symbols and stand for generic expectation and probability. For any univariate probability measure , we denote by its Cumulative Distribution Function (CDF) and by its quantile function (a.k.a. generalized inverse of ) defined for all as with . For a measurable set we denote by the uniform distribution on .

2 The problem

In this section we introduce the fair regression problem and present our derivation for the optimal fair regression function alongside its connection to Wasserstein barycenter problem. We consider the general regression model

| (1) |

where is a centered random variable, on , with , and is the regression function minimizing the squared risk. Let be the joint distribution of . For any prediction rule , we denote by the distribution of , that is, the Cumulative Distribution Function (CDF) of is given by

| (2) |

to shorten the notation we will write and instead of and respectively.

Definition 2.1 (Wasserstein-2 distance).

Let and be two univariate probability measures. The squared Wasserstein-2 distance between and is defined as

where is the set of distributions (couplings) on such that for all and all measurable sets it holds that and .

In this work we use the following definition of (strong) Demographic Parity, which was previously used in the context of regression by [1, 12, 23].

Definition 2.2 (Demographic Parity).

A prediction (possibly randomized) is fair if, for every

Demographic Parity requires the Kolmogorov-Smirnov distance between and to vanish for all . Thus, if is fair, does not depend on and to simplify the notation we will write .

Recall the model in Eq. (1). Since the noise has zero mean, the minimization of over is equivalent to the minimization of over .

The next theorem shows that the optimal fair predictor for an input is obtained by a nonlinear transformation of the vector that is linked to a Wasserstein barycenter problem [2].

Theorem 2.3 (Characterization of fair optimal prediction).

Assume, for each , that the univariate measure has a density and let . Then,

Moreover, if and solve the l.h.s. and the r.h.s. problems respectively, then and

| (3) |

After the completion of this work, we became aware of a similar result derived independently by [28]. Their result applies to a general vector-valued regression problems, under assumptions that are similar to ours. They have proposed an estimator of the optimal fair prediction which leverages the connection of the fair regression and the problem of Wasserstein barycenters and derived asymptotic risk consistency. In contrast, we focus on the one dimensional case, and we provide a plug-in type estimator for which we show distribution-free fairness guarantees and finite-sample bounds for the risk. The proof of Theorem 2.3 relies on the classical characterization of optimal coupling in one dimension (stated in Theorem A.1 in the appendix) of the Wasserstein-2 distance. We show that a minimizer of the -risk can be used to construct and vice-versa, given , we leverage a well-known expression for one dimensional Wasserstein barycenter (see e.g., [2, Section 6.1] and Lemma A.2 in the appendix) and construct .

The case of binary protected attribute. Let us unpack Eq. (3) in the case that , assuming w.l.o.g. that . Theorem 2.3 states that the fair optimal prediction is defined for all individuals in the first group as

and likewise for the second group. This form of the optimal fair predictor, and more generally Eq. (3), allows us to understand the decision made by at individual level. If we interpret as the candidate’s CV and candidate’s group respectively, and as the current market salary (which might be discriminatory), then the fair optimal salary is a convex combination of the market salary and the adjusted salary , which is computed as follows. If say , we first compute the fraction of individuals from the first group whose market salary is at most , that is, we compute . Then, we find a candidate in group , such that the fraction of individuals from the second group whose market salary is at most is the same, that is, is chosen to satisfy . Finally, the market salary of is exactly the adjustment for , that is, . This idea is illustrated in Figure 1 and leads to the following philosophy: if candidates and share the same group-wise market salary ranking, then they should receive the same salary determined by the fair prediction . At last, note that Eq. (3) allows to understand the (potential) amount of extra money that we need to pay in order to satisfy fairness. While the unfair decision made with costs for the salary of and , the fair decision costs . Thus, the extra (signed) salary that we pay is . Since, , will be positive whenever the candidate from the majority group gets higher salary according to , and negative otherwise. We believe that the expression Eq. (3) could be the starting point for further more applied work on algorithmic fairness.

3 General form of the estimator

In this section we propose an estimator of the optimal fair predictor that relies on the plug-in principle. The expression (3) of suggests that we only need estimators for the regression function , the proportions , as well as the CDF and the quantile function , for all . While

the estimation of needs labeled data, all the other quantities rely only on , and , therefore unlabeled data with an estimator of suffices.

Thus, given a base estimator of , our post-processing algorithm will require only unlabeled data.

For each let be a group-wise unlabeled sample.

In the following for simplicity we assume that are even for all 111Since we are ready to sacrifice a factor in our bounds, this assumption is without loss of generality..

Let be any fixed partition of such that and .

For each we let be the

restriction of to .

We use to estimate and to estimate .

For each and each , we estimate by

| (4) |

where is the Dirac measure and all , for some positive set by the user. Using the estimators in Eq. (4), we define for all estimators of and of as

| (5) |

That is, and are the empirical CDF and empirical quantiles of based on and respectively. The noise serves as a smoothing random variable, since for all and the random variables are i.i.d. continuous for any and . In contrast, might have atoms resulting in a non-zero probability to observe ties in . This step is also known as jittering, often used for data visualization [11] for tie-breaking. It plays a crucial role in the distribution-free fairness guarantees that we derive in Proposition 4.1; see the discussion thereafter.

Finally, let and for each let be the empirical frequency of evaluated on . Given a base estimator of constructed from labeled samples , we define the final estimator of for all mimicking Eq. (3) as

| (6) |

where is assumed to be independent from every other random variables.

Remark 3.1.

In practice one should use a very small value for (e.g., ), which does not alter the statistical quality of the base estimator as indicated in Theorem 4.4.

A pseudo-code implementation of in Eq. (6) is reported in Algorithm 1. It requires two primitives: sorts the array ar in an increasing order; which outputs the index such that the insertion of into ’th position in ar preserves ordering (i.e., ). Algorithm 1 consists of two for parts: in the for-loop we perform a preprocessing which takes time222It is assumed in this discussion that the time complexity to evaluate is . since it involves sorting; then, the evaluation of on a new point is performed in time since it involves an element search in a sorted array. Note that the for-loop of Algorithm 1 needs to be performed only once as this step is shared for any new .

4 Statistical analysis

In this section we provide a statistical analysis of the proposed algorithm. We first present in Proposition 4.1 distribution-free finite sample fairness guarantees for post-processing of any base learner with unlabeled data and then we show in Theorem 4.4 that if the base estimator is a good proxy for , then under mild assumptions on the distribution , the processed estimator in Eq. (6) is a good estimator of in Eq. (3).

Distribution free post-processing fairness guarantees.

We derive two distribution-free results in Proposition 4.1, the first in Eq. (7) shows that the fairness definition is satisfied as long as we take the expectation over the data inside the supremum in Definition 2.2, while the second one in Eq. (8) bounds the expected violation of Definition 2.2.

Proposition 4.1 (Fairness guarantees).

For any joint distribution of , any base estimator constructed on labeled data, and for all , the estimator defined in Eq. (6) satisfies

| (7) | ||||

| (8) |

where is the union of all available datasets.

Let us point out that this result does not require any assumption on the distribution as well as on the base estimator . This is achieved thanks to the jittering step in the definition of in Eq. (6), which artificially introduces continuity.

Continuity allows us to use results from the theory of rank statistics of exchangeable random variables to derive Eq. (7) as well as the classical inverse transform (see e.g., [40, Sections 13 and 21])

combined with the Dvoretzky-Kiefer-Wolfowitz inequality [33] to derive Eq. (8).

Since basic results on rank statistics and inverse transform are distribution-free as long as the underlying random variable is continuous, the guarantees in Eqs. (7)–(8) are also distribution-free and can be applied on top of any base estimator .

The bound in Eq. (7) might be surprising to the reader.

Yet, let us emphasize that this bound holds because the expectation w.r.t. the data distribution is taken inside the supremum (since stands for the joint distribution of all random variables involved in ).

Similar proof techniques are also used in randomization inference via permutations [18, 21], conformal prediction [42, 30], knockoff estimation [4] to name a few.

However, unlike the aforementioned contributions, the problem of fairness requires a non-trivial adaptation of these techniques.

In contrast, Eq. (8) might be more appealing to the machine learning community as it controls the expected (over data) violation of the fairness constraint with standard parametric rate.

Estimation guarantee with accurate base estimator.

In order to prove non-asymptotic risk bounds we require the following assumption on the distribution of .

Assumption 4.2.

For each the univariate measure admits a density , which is lower bounded by and upper-bounded by .

Although the lower bound on the density assumption is rather strong and might potentially be violated in practice, it is still reasonable in certain situations. We believe that it can be replaced by the assumption that conditionally on for all admits moments. We do not explore this relaxation in our work as it significantly complicates the proof of Theorem 4.4. At the same time, our empirical study suggests that the lower bound on the density is not intrinsic to the problem, since the estimator exhibits a good performance across various scenarios. In contrast, the milder assumption that the density is upper bounded is crucial for our proof and seems to be necessary.

Apart from the assumption on the density of , the actual rate of estimation depends on the quality of the base estimator . We require the following assumption, which states that approximates point-wise with rate and a standard sub-Gaussian concentration for can be derived.

Assumption 4.3.

There exist positive constants and independent from , , , and a positive sequence such that for all it holds that

We refer to [3, 39, 29, 15, 30] for various examples of estimators and additional assumptions such that the bound in Assumption 4.3 is satisfied. It includes local polynomial estimators, k-nearest neighbours, and linear regression, to name just a few.

Under these assumptions we can prove the following finite-sample estimation bound.

Theorem 4.4 (Estimation guarantee).

The proof of this result combines expected deviation of empirical measure from the real measure in terms of Wasserstein distance on real line [7] with the already mentioned rank statistics and classical peeling argument of [3].

The first term of the derived bound corresponds to the estimation error of by , the second term is the price to pay for not knowing conditional distributions while the last term correspond to the price of unknown marginal probabilities of each protected attribute.

Notice that if , which corresponds to the standard i.i.d. sampling from of unlabeled data, the second and the third term are of the same order.

Moreover, if is sufficiently large, which in most scenarios333One can achieve it by splitting the labeled dataset artificially augmenting the unlabeled one, which ensures that . In this case if , then the first term is always dominant in the derived bound. is w.l.o.g., then the rate is dominated by .

Notice that one can find a collection of joint distributions , such that satisfies demographic parity. Hence, if is the minimax optimal estimation rate of , then it is also optimal for .

5 Empirical study

In this section, we present numerical experiments444The source of our method can be found at https://www.link-anonymous.link. with the proposed fair regression estimator defined in Section 3. In all experiments, we collect statistics on the test set . The empirical mean squared error (MSE) is defined as

We also measure the violation of fairness constraint imposed by Definition 2.2 via the empirical Kolmogorov-Smirnov (KS) distance,

where for all we define the set . For all datasets we split the data in two parts (70% train and 30% test), this procedure is repeated 30 times, and we report the average performance on the test set alongside its standard deviation. We employ the 2-steps 10-fold CV procedure considered by [16] to select the best hyperparameters with the training set. In the first step, we shortlist all the hyperparameters with MSE close to the best one (in our case, the hyperparameters which lead to 10% larger MSE w.r.t. the best MSE). Then, from this list, we select the hyperparameters with the lowest KS.

Methods.

We compare our method (see Section 3) to different fair regression approaches for both linear and non-linear regression. In the case of linear models we consider the following methods: Linear RLS plus [6] (RLS+Berk), Linear RLS plus [34] (RLS+Oneto),

and Linear RLS plus Our Method (RLS+Ours), where RLS is the abbreviation of Regularized Least Squares.

In the case of non-linear models we compare to the following methods. i) For Kernel RLS (KRLS): KRLS plus [34] (KRLS+Oneto), KRLS plus [35] (KRLS+Perez),

KRLS plus Our Method (KRLS+Ours); ii) For Random Forests (RF): RF plus [36] (RF+Raff), RF plus [1]555We thank the authors for sharing a prototype of their code. (RF+Agar),

and RF plus Our Method (RF+Ours).

The hyperparameters of the methods are set as follows.

For RLS we set the regularization hyperparameters and for KRLS we set and .

Finally, for RF we set to the number of trees and for the number of features to select during the tree creation we search in .

Datasets.

In order to analyze the performance of our methods and test it against the state-of-the-art alternatives, we consider five benchmark datasets, CRIME, LAW, NLSY, STUD, and UNIV, which are briefly described below:

Communities&Crime (CRIME) contains socio-economic, law enforcement, and crime data about communities in the US [37] with examples.

The task is to predict the number of violent crimes per

population (normalized to ) with race as the protected attribute.

Following [9], we made a binary sensitive attribute as to the percentage of black population, which yielded instances of with a mean crime

rate and instances of with a mean crime rate .

Law School (LAW) refers to the Law School Admissions Councils National

Longitudinal Bar Passage Study [44] and has examples.

The task is to predict a students GPA (normalized to ) with race as the protected attribute (white versus non-white).

National Longitudinal Survey of Youth (NLSY) involves survey results by the U.S. Bureau of Labor Statistics that is intended to gather information on the labor market activities and other life events of several groups [8].

Analogously to [26] we model a virtual company’s hiring decision assuming that the company does not have access to the applicants’ academic scores.

We set as target the person’s GPA (normalized to ), with race as sensitive attribute

Student Performance (STUD), approaches students achievement (final grade) in secondary education of two Portuguese schools using attributes [14], with gender as the protected attribute.

University Anonymous (UNIV) is a proprietary and highly sensitive dataset containing all the data about the past and present students enrolled at the University of Anonymous.

In this study we take into consideration students who enrolled, in the academic year 2017-2018.

The dataset contains 5000 instances, each one described by 35 attributes (both numeric and categorical) about ethnicity, gender, financial status, and previous school experience.

The scope is to predict the average grades at the end of the first semester, with gender as the protected attribute.

Comparison w.r.t. state-of-the-art.

| CRIME | LAW | NLSY | STUD | UNIV | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Method | MSE | KS | MSE | KS | MSE | KS | MSE | KS | MSE | KS |

| RLS | ||||||||||

| RLS+Berk | ||||||||||

| RLS+Oneto | ||||||||||

| RLS+Ours | ||||||||||

| KRLS | ||||||||||

| KRLS+Oneto | ||||||||||

| KRLS+Perez | ||||||||||

| KRLS+Ours | ||||||||||

| RF | ||||||||||

| RF+Raff | ||||||||||

| RF+Agar | ||||||||||

| RF+Ours | ||||||||||

In Table 1, we present the performance of different methods on various datasets described above. One can notice that LAW and UNIV datasets have a least amount of disciminatory bias (quantified by KS), since the fairness unaware methods perform reasonably well in terms of KS. Furthermore, on these two datasets, the difference in performance between all fairness aware methods is less noticeable. In contrast, on CRIME, NLSY, and STUD, fairness unaware methods perform poorly in terms of KS. More importantly, our findings indicate that the proposed method is competitive with state-of-the-art methods and is the most effective in imposing the fairness constraint. In particular, in all except two considered scenarios (CRIME+RLS, CRIME+RF) our method improves fairness by (and up to in some cases) over the closest fairness aware method. In contrast, the accuracy of our method decreases by up to when compared to the most accurate fairness aware method. However, let us emphasize that the relative decrease in accuracy is much smaller than the relative improvement in fairness across the considered scenarios. For example, on NLSY+RLS the most accurate fairness aware method is RLS+Oneto with mean and mean , while RLS+Ours yields mean and mean . That is, compared to RLS+Oneto our method drops about in accuracy, while gains about in fairness. With RF, which is a more powerful estimator, the average drop in accuracy across all datasets compared to RF+Agar is about while the average improvement in fairness is about .

6 Conclusion and perspectives

In this work we investigated the problem of fair regression with Demographic Parity constraint assuming that the sensitive attribute is available for prediction. We derived a closed form solution for the optimal fair predictor which offers a simple and intuitive interpretation. Relying on this expression, we devised a post-processing procedure, which transforms any base estimator of the regression function into a nearly fair one, independently of the underlying distribution. Moreover, if the base estimator is accurate, our post-processing method yields an accurate estimator of the optimal fair predictor as well. Finally, we conducted an empirical study indicating the effectiveness of our method in imposing fairness in practice. In the future it would be valuable to extend our methodology to the case when we are not allowed to use the sensitive feature as well as to other notions of fairness.

7 Acknowledgement

This work was supported by the Amazon AWS Machine Learning Research Award, SAP SE, and CISCO.

References

- Agarwal et al. [2019] A. Agarwal, M. Dudik, and Z. S. Wu. Fair regression: Quantitative definitions and reduction-based algorithms. In International Conference on Machine Learning, 2019.

- Agueh and Carlier [2011] M. Agueh and G. Carlier. Barycenters in the wasserstein space. SIAM Journal on Mathematical Analysis, 43(2):904–924, 2011.

- Audibert and Tsybakov [2007] J. Y. Audibert and A. Tsybakov. Fast learning rates for plug-in classifiers. The Annals of Statistics, 35(2):608–633, 2007.

- Barber and Candès [2019] R. F. Barber and E. Candès. A knockoff filter for high-dimensional selective inference. The Annals of Statistics, 47(5):2504–2537, 2019.

- Barocas et al. [2018] S. Barocas, M. Hardt, and A. Narayanan. Fairness and Machine Learning. fairmlbook.org, 2018.

- Berk et al. [2017] R. Berk, H. Heidari, S. Jabbari, M. Joseph, M. Kearns, J. Morgenstern, S. Neel, and A. Roth. A convex framework for fair regression. In Fairness, Accountability, and Transparency in Machine Learning, 2017.

- Bobkov and Ledoux [2016] S. Bobkov and M. Ledoux. One-dimensional empirical measures, order statistics and kantorovich transport distances. Memoirs of the American Mathematical Society, 2016.

- Bureau of Labor Statistics [2019] Bureau of Labor Statistics. National longitudinal surveys of youth data set. www.bls.gov/nls/, 2019.

- Calders et al. [2013] T. Calders, A. Karim, F. Kamiran, W. Ali, and X. Zhang. Controlling attribute effect in linear regression. In IEEE International Conference on Data Mining, 2013.

- Calmon et al. [2017] F. Calmon, D. Wei, B. Vinzamuri, K. N. Ramamurthy, and K. R. Varshney. Optimized pre-processing for discrimination prevention. In Neural Information Processing Systems, 2017.

- Chambers [2018] J. M. Chambers. Graphical methods for data analysis. CRC Press, 2018.

- Chiappa et al. [2020] S. Chiappa, R. Jiang, T. Stepleton, A. Pacchiano, H. Jiang, and J. Aslanides. A general approach to fairness with optimal transport. In AAAI, 2020.

- Chierichetti et al. [2017] F. Chierichetti, R. Kumar, S. Lattanzi, and S. Vassilvitskii. Fair clustering through fairlets. In Neural Information Processing Systems, 2017.

- Cortez and Silva [2008] P. Cortez and A. Silva. Using data mining to predict secondary school student performance. In FUture BUsiness TEChnology Conference, 2008.

- Devroye [1978] L. Devroye. The uniform convergence of nearest neighbor regression function estimators and their application in optimization. IEEE Transactions on Information Theory, 24(2):142–151, 1978.

- Donini et al. [2018] M. Donini, L. Oneto, S. Ben-David, J. S. Shawe-Taylor, and M. Pontil. Empirical risk minimization under fairness constraints. In Neural Information Processing Systems, 2018.

- Dwork et al. [2018] C. Dwork, N. Immorlica, A. T. Kalai, and M. D. M. Leiserson. Decoupled classifiers for group-fair and efficient machine learning. In Conference on Fairness, Accountability and Transparency, 2018.

- Fisher [1936] R. Fisher. Design of experiments. Br Med J, 1(3923):554–554, 1936.

- Gordaliza et al. [2019] P. Gordaliza, E. Del Barrio, G. Fabrice, and J. M. Loubes. Obtaining fairness using optimal transport theory. In International Conference on Machine Learning, 2019.

- Hardt et al. [2016] M. Hardt, E. Price, and N. Srebro. Equality of opportunity in supervised learning. In Neural Information Processing Systems, 2016.

- Hoeffding [1952] W. Hoeffding. The large-sample power of tests based on permutations of observations. The Annals of Mathematical Statistics, pages 169–192, 1952.

- Jabbari et al. [2016] S. Jabbari, M. Joseph, M. Kearns, J. Morgenstern, and A. Roth. Fair learning in markovian environments. In Conference on Fairness, Accountability, and Transparency in Machine Learning, 2016.

- Jiang et al. [2019] R. Jiang, A. Pacchiano, T. Stepleton, H. Jiang, and S. Chiappa. Wasserstein fair classification. arXiv preprint arXiv:1907.12059, 2019.

- Joseph et al. [2016] M. Joseph, M. Kearns, J. H. Morgenstern, and A. Roth. Fairness in learning: Classic and contextual bandits. In Neural Information Processing Systems, 2016.

- Kilbertus et al. [2017] N. Kilbertus, M. Rojas-Carulla, G. Parascandolo, M. Hardt, D. Janzing, and B. Schölkopf. Avoiding discrimination through causal reasoning. In Neural Information Processing Systems, 2017.

- Komiyama and Shimao [2018] J. Komiyama and H. Shimao. Comparing fairness criteria based on social outcome. arXiv preprint arXiv:1806.05112, 2018.

- Kusner et al. [2017] M. J. Kusner, J. Loftus, C. Russell, and R. Silva. Counterfactual fairness. In Neural Information Processing Systems, 2017.

- Le Gouic et al. [2020] T. Le Gouic, J.-M. Loubes, and P. Rigollet. Projection to fairness in statistical learning. arXiv preprint arXiv:2005.11720, 2020.

- Lei [2014] J. Lei. Classification with confidence. Biometrika, 101(4):755–769, 2014.

- Lei and Wasserman [2014] J. Lei and L. Wasserman. Distribution-free prediction bands for non-parametric regression. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):71–96, 2014.

- Lei et al. [2013] J. Lei, James R., and L. Wasserman. Distribution-free prediction sets. Journal of the American Statistical Association, 108(501):278–287, 2013.

- Lum and Johndrow [2016] K. Lum and J. Johndrow. A statistical framework for fair predictive algorithms. arXiv preprint arXiv:1610.08077, 2016.

- Massart [1990] P. Massart. The tight constant in the dvoretzky-kiefer-wolfowitz inequality. The Annals of Probability, 18(3):1269–1283, 1990.

- Oneto et al. [2019] L. Oneto, M. Donini, and M. Pontil. General fair empirical risk minimization. arXiv preprint arXiv:1901.10080, 2019.

- Pérez-Suay et al. [2017] A. Pérez-Suay, V. Laparra, G. Mateo-García, J. Muñoz-Marí, L. Gómez-Chova, and G. Camps-Valls. Fair kernel learning. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases, 2017.

- Raff et al. [2018] E. Raff, J. Sylvester, and S. Mills. Fair forests: Regularized tree induction to minimize model bias. In AAAI/ACM Conference on AI, Ethics, and Society, 2018.

- Redmond and Baveja [2002] M. Redmond and A. Baveja. A data-driven software tool for enabling cooperative information sharing among police departments. European Journal of Operational Research, 141(3):660–678, 2002.

- Santambrogio [2015] F. Santambrogio. Optimal transport for applied mathematicians. Springer, 2015.

- van de Geer [2008] S. van de Geer. High-dimensional generalized linear models and the lasso. The Annals of Statistics, 36(2):614–645, 2008.

- van der Vaart [2000] A. W. van der Vaart. Asymptotic statistics, volume 3. Cambridge university press, 2000.

- Villani [2003] C. Villani. Topics in Optimal Transportation. American Mathematical Society, 2003.

- Vovk et al. [2005] V. Vovk, A. Gammerman, and G. Shafer. Algorithmic learning in a random world. Springer Science & Business Media, 2005.

- Wang et al. [2019] H. Wang, B. Ustun, and F. Calmon. Repairing without retraining: Avoiding disparate impact with counterfactual distributions. In International Conference on Machine Learning, 2019.

- Wightman and Ramsey [1998] L. F. Wightman and H. Ramsey. LSAC national longitudinal bar passage study. Law School Admission Council, 1998.

- Yao and Huang [2017] S. Yao and B. Huang. Beyond parity: Fairness objectives for collaborative filtering. In Neural Information Processing Systems, 2017.

- Zafar et al. [2017] M. B. Zafar, I. Valera, M. Gomez Rodriguez, and K. P. Gummadi. Fairness beyond disparate treatment & disparate impact: Learning classification without disparate mistreatment. In International Conference on World Wide Web, 2017.

- Zemel et al. [2013] R. Zemel, Y. Wu, K. Swersky, T. Pitassi, and C. Dwork. Learning fair representations. In International Conference on Machine Learning, 2013.

- Zeni et al. [2020] G. Zeni, M. Fontana, and S. Vantini. Conformal prediction: a unified review of theory and new challenges. arXiv preprint arXiv:2005.07972, 2020.

- Zliobaite [2015] I. Zliobaite. On the relation between accuracy and fairness in binary classification. arXiv preprint arXiv:1505.05723, 2015.

Appendix

The appendix is organized as follows. In Appendix A we provide the proof of Theorem 2.3, in Appendix B we provide the proof of Proposition 4.1, and in Appendix C we prove Theorem 4.4. For reader’s convenience all the results are repeated in this supplementary material and a short overview of classical results is provided.

Appendix A Characterization of the optimal

Before providing the proof of Theorem 2.3, let us give a brief overview of classical results in the Optimal transport theory with one dimensional measures; all the results can be found in [41, 38]

See 2.1 The coupling which achieves the infimum in the definition of the Wasserstein-2 distance is called the optimal coupling.

Also let us mention that the Wasserstein-2 distance between two univariate probability measures , defined in Definition 2.1, can be expressed as

where and and the infimum is taken over all joint distributions of which preserve marginals.

The next result establishes that as long as one of the measures in the definition of the Wasserstein-2 distance admits a density, then the optimal coupling in the infimum in Definition 2.1 is deterministic (see e.g., [41, Theorem 2.18] or [38, Theorems 2.5 and 2.9]).

Theorem A.1.

Let be two univariate measures such that has a density and let . Then there exists a mapping such

that is where is an optimal coupling. Moreover, the transport map is given by .

By the abuse of notation, for an increasing real-valued univariate function we will use to denote its generalized inverse. For instance, if is a CDF, then is the quantile function that was defined in the introduction.

The next result is standard and can be found for instance in [2, Section 6.1] or [38, Section 5.5.5]. It states that for one dimensional Wasserstein barycenter problem, the optimal measure admits a closed form solution.

Lemma A.2.

Let be univariate probability measures admitting densities, for all such that define

Then, the cumulative distribution of is given by

Theorem A.1 and Lemma A.2 are the two main ingredients that are used in the proof of Theorem 2.3. See 2.3

Proof of Theorem 2.3.

We want to show that

Let be a minimizer of the l.h.s. of the above equation and define by the distribution of . Since admits density, using Theorem A.1 for each there exists such that

where we defined for all as

The cumulative distribution of can be expressed as

where the last equality is due to the fact that admits a density for all . The above implies that is fair, thus on the one hand by optimality of we have

on the other hand we have for each

Thus we showed that

| (9) |

This implies that

| (10) |

Now we want to show that the opposite inequality also holds. To this end define as

Set as optimal transport maps from to of the form (provided by Theorem A.1 and our assumption on the density of ) and define for all as

| (11) |

By the definition of in Eq. (11) and Theorem A.1 we clearly have

| (12) |

Moreover since is independent from , using similar argument as above one can show that satisfies the Demographic Parity constraint in Definition 2.2 and thus, Eq. (12) yields

| (13) |

Eqs. (10) and (13) yield the first assertion of the result. Notice that thanks to Eq. (12) we have also shown that

and since is fair we can put . Finally, using Lemma A.2 we derive an explicit form of and conclude using Eq. (11). ∎

Appendix B Proof of Proposition 4.1

Let us first recall the well-known Dvoretzky–Kiefer–Wolfowitz inequality [33, Corollary 1].

Theorem B.1 (Dvoretzky–Kiefer–Wolfowitz inequality).

Let be i.i.d. real valued random variables with cumulative distribution . Let be the empirical cumulative distribution of , then

See 4.1

Proof of Proposition 4.1.

The proof of Eq. (7) is based on standard results in the theory of rank statistics (see e.g. [40, Sec. 13]). Meanwhile, the proof of Eq. (8) is built upon the well-known Dvoretzky–Kiefer–Wolfowitz inequality [33, Corollary 1].

Notice that if and is independent from labeled, unlabeled data, and the noise variables , then it holds that

Proof of Eq. (7): We have for all that

where, thanks to the form of in Eq. (6), the inequality follows from the fact that for all

Fix some and let be such that , then by the definition of we have

Notice that the random variables conditionally on labeled data are i.i.d. and continuous. Thus, conditionally on the random variable is distributed uniformly on (see e.g., [40, Lemma 13.1]), so that

Repeating the same argument for and recalling that and , we get

Proof of Eq. (8): Similarly, as in the proof of Eq. (7) we can write

Moreover, thanks to the triangle inequality we have

| (14) |

where for all and all we defined

and we used the fact that is continuous conditionally on all the available data , then the random variable is distributed uniformly on (see e.g., [40, Lemma 21.1]), which means that for all and all

We bound the first term in Eq. (14) and the bound for the second terms follows the same arguments. Fix some , then we can write

Taking supremum on both sides and repeating the same argument for , we get

we conclude applying Dvoretzky–Kiefer–Wolfowitz inequality, recalled in Theorem B.1, conditionally on . ∎

Appendix C Proof of Theorem 4.4

The next simple result states that Assumption 4.3 yields a bound in -norm between and .

Lemma C.1.

Proof.

Applying Fubini’s theorem we can write

where follows from Assumption 4.3. Making change of variables we get

∎

We also need to define Wasserstein and distances.

Definition C.2.

Let and be two univariate probability measures, then Wasserstein and distance between and are defined as

respectively.

Remark C.3.

The final ingredient is [7, Theorem 5.11].

Theorem C.4.

Let be i.i.d. real valued random variables from some probability measure and let be the empirical measure based on . Assume that admits density which is lower-bounded by some constant , then

See 4.4

Proof of Theorem 4.4.

In the proof is going to denote an absolute constant independent from the size of data, which can differ from line to line. First of all, define the random variable

where stands for the expectation w.r.t. the joint distribution of . Recall that

Considering first, we can state that

It is clear that if we can find a bound on which holds for almost all w.r.t. , it would imply an upper bound on for all . Fix some , then on the one hand for all

on the other hand under Assumption 4.2 we can write for all

which implies that and therefore for almost all w.r.t. . Hence, we can write for all

The above implies that

Taking the total expectation we arrive at

where we used the fact that is an unbiased estimator of . For all let be independent from everything, for all set the shorthand notation

Notice that

and therefore we can write

Notice that the term , where is the binomial random variable with parameters , thus using the Cauchy–Schwarz inequality we can write and the above bound reads as

| (15) |

It remains to bound for each . Fix some (they can be equal), then

| (16) | ||||

We bound each of the three terms separately.

First term (): Notice that is distributed uniformly on conditionally on labeled data (see e.g., [40, Lemma 13.1]). Thus, we have

| (17) |

Notice that for all and all it holds that

The above implies that

| (18) |

and the same argument repeated for implies that

| (19) |

Substituting Eqs. (18)-(19) in Eq. (17) and using Definition C.2 we get

where for in Eq. (17) we used the fact that . Using the coupling definition of the Wasserstein distance and the way we have defined , we can write

almost surely. Since are i.i.d. from , then conditionally on the random variables are i.i.d. . Furthermore, using Lemma C.1 we can write

| (20) |

Second term (): Note that under Assumption 4.2, the Lipschitz constant of is upper bounded by . Then, taking supremum and using Definition C.2 we apply Theorem C.4 to get

| (21) |

where is an absolute positive constant ( is sufficient).

Third term (): We can write, using Assumption 4.2 that

| (22) |

with defined for all and all as

| (23) |

The second term in Eq. (22) is bounded by thanks to the Dvoretzky–Kiefer–Wolfowitz inequality recalled in Theorem B.1. Thus, it remains to bound the first term in Eq. (22). We introduce the following shorthand notation for the first term in Eq. (22)

Let and be independent from , and each other. Based on this notation we can write

| (24) |

Furthermore, if , , and , then simple algebra yields

For all it holds that . Applying this fact to Eq. (24) with and we get

By definition of the random variables are exchangeable, hence

Furthermore, using the fact that almost surely we get

| (25) |

Thanks to Assumption 4.2 we have the following bound on the first term in Eq. (25)

For the second term in Eq. (25), we observe that Assumption 4.2 yields almost surely

Thus, taking the total expectation on both sides of this inequality we get

Since , then we have demonstrated that . Substituting this bound into Eq. (22), we derive that

| (26) |

Remark C.5.

Notice that the exact constant in front of the rate of convergence in Theorem 4.4 can be recovered following the proof. Furthermore, this proof can be extended to control norm

for all (the current proof deals only with ). To achieve it one only needs to extend Lemma C.1 while the rest of the proof follows line-by-line using deviation results on Wasserstein- distance on the real line [7]. Finally, it is possible to extend this result under the same assumptions to control , which induces an extra multiplicative polylogarithmic factor in .