Algorithms and Learning for Fair Portfolio Design

Abstract

We consider a variation on the classical finance problem of optimal portfolio design. In our setting, a large population of consumers is drawn from some distribution over risk tolerances, and each consumer must be assigned to a portfolio of lower risk than her tolerance. The consumers may also belong to underlying groups (for instance, of demographic properties or wealth), and the goal is to design a small number of portfolios that are fair across groups in a particular and natural technical sense.

Our main results are algorithms for optimal and near-optimal portfolio design for both social welfare and fairness objectives, both with and without assumptions on the underlying group structure. We describe an efficient algorithm based on an internal two-player zero-sum game that learns near-optimal fair portfolios ex ante and show experimentally that it can be used to obtain a small set of fair portfolios ex post as well. For the special but natural case in which group structure coincides with risk tolerances (which models the reality that wealthy consumers generally tolerate greater risk), we give an efficient and optimal fair algorithm. We also provide generalization guarantees for the underlying risk distribution that has no dependence on the number of portfolios and illustrate the theory with simulation results.

1 Introduction

In this work we consider algorithmic and learning problems in a model for the fair design of financial products. We imagine a large population of individual retail investors or consumers, each of whom has her own tolerance for investment risk in the form of a limit on the variance of returns. It is well known in quantitative finance that for any set of financial assets, the optimal expected returns on investment are increasing in risk.

A large retail investment firm (such as Vanguard or Fidelity) wishes to design portfolios to serve these consumers under the common practice of assigning consumers only to portfolios with lower risks than their tolerances. The firm would like to design and offer only a small number of such products — much smaller than the number of consumers — since the execution and maintenance of portfolios is costly and ongoing. The overarching goal is to design the products to minimize consumer regret — the loss of returns due to being assigned to lower-risk portfolios compared to the bespoke portfolios saturating tolerances — both with and without fairness considerations.

We consider a notion of group fairness adapted from the literature on fair division. Consumers belong to underlying groups that may be defined by standard demographic features such as race, gender or age, or they may be defined by the risk tolerances themselves, as higher risk appetite is generally correlated with higher wealth. We study minmax group fairness, in which the goal is to minimize the maximum regret across groups — i.e. to optimize for the least well-off group. Compared to the approach of constraining regret to be equal across groups (which is not even always feasible in our setting), minmax optimal solutions have the property that they Pareto-dominate regret-equalizing solutions: every group has regret that can only be smaller than it would be if regret were constrained to be equalized across groups.

Related Work.

Our work generally falls within the literature on fairness in machine learning, which is too broad to survey in detail here; see [3] for a recent overview. We are perhaps closer in spirit to research in fair division or allocation problems [1, 13, 2], in which a limited resource must be distributed across a collection of players so as to maximize the utility of the least well-off; here, the resource in question is the small number of portfolios to design. However, we are not aware of any technical connections between our work and this line of research. Within the fairness in machine learning literature, our work is closest to fair facility location problems [9, 10], which attempt to choose a small number of “centers” to serve a large and diverse population and “fair allocation” problems that arise in the context of predictive policing [6, 5, 4].

There seems to have been relatively little explicit consideration of fairness issues in quantitative finance generally and optimal portfolio design specifically. An exception is [8], in which the interest is in fairly amortizing transaction costs of a single portfolio across investors rather than designing multiple portfolios to meet a fairness criterion.

Our Results and Techniques.

In Section 3, we provide a dynamic program to find products that optimize the average regret of a single population. In Section 4, we divide the population into different groups and develop techniques to guarantee minmax group fairness: in Section 4.1, we show a separation between deterministic solutions and randomized solutions (i.e. distributions over sets of products) for minmax group fairness; in Section 4.2, we leverage techniques for learning in games to find a distribution over products that optimizes for minmax group fairness; in Section 4.3, we focus on deterministic solutions and extend our dynamic programming approach to efficiently optimize for the minmax objective when the number of groups is constant; in Section 4.4, we study the natural special case in which groups are defined by disjoint intervals on the real line and give algorithms that are efficient even for large numbers of groups. In Section 5, we show that when consumers’ risk tolerances are drawn i.i.d. from an unknown distribution, empirical risk bounds from a sample of consumers generalize to the underlying distribution, and we prove tight sample complexity bounds. Finally, in Section 6, we provide experiments to complement our theoretical results.

2 Model and Preliminaries

We aim to create products (portfolios) consisting of weighted collections of assets with differing means and standard deviations (risks). Each consumer is associated with a real number , which is the risk tolerance of the consumer — an upper bound on the standard deviation of returns. We assume that consumers’ risk tolerances are bounded.

2.1 Bespoke Problem

We adopt the standard Markowitz framework [11] for portfolio design. Given a set of assets with mean and covariance matrix , and a consumer risk tolerance , the bespoke portfolio achieves the maximum expected return that the consumer can realize by assigning weights over the assets (where the weight of an asset represents the fraction of the portfolio allocated to said asset) subject to the constraint that the overall risk – quantified as the standard deviation of the mixture over assets – does not exceed her tolerance . Finding a consumer’s bespoke portfolio can be written down as an optimization problem. We formalize the bespoke problem in Equation (1) below, and call the solution .

| (1) |

Here we note that optimal portfolios are summarized by function , which is non-decreasing. Since consumer tolerances are bounded, we let denote the maximum value of across all consumers.

2.2 A Regret Notion

Suppose there are consumers to whom we want to offer products. Our goal is to design products that minimize a notion of regret for a given set of consumers. A product has a risk (standard deviation) which we will denote by . We assume throughout that in addition to the selected products, there is always a risk-free product (say cash) available that has zero return; we will denote this risk-free product by throughout the paper (). For a given consumer with risk threshold , the regret of the consumer with respect to a set of products is the difference between the return of her bespoke product and the maximum return of any product with risk that is less than or equal to her risk threshold. To formalize this, the regret of products for a consumer with risk threshold is defined as . Note since always exists, the term is well defined. Now for a given set of consumers , the regret of products on is simply defined as the average regret of on :

| (2) |

When includes the entire population of consumers, we call the population regret. The following notion for the weighted regret of on , given a vector of weights for each consumer, will be useful in Sections 3 and 4:

| (3) |

Absent any fairness concern, our goal is to design efficient algorithms to minimize for a given set of consumers and target number of products : . This will be the subject of Section 3. We can always find an optimal set of products as a subset of the consumer risk thresholds , because if any product is not in , we can replace it by without decreasing the return for any consumer111We consider a more general regret framework in Appendix B which allows consumers to be assigned to products with risk higher than their tolerance, and in this case it is not necessarily optimal to always place products on the consumer risk thresholds.. We let represent the set of all subsets of size for a given set of consumers : . We therefore can reduce our regret minimization problem to the following problem:

| (4) |

Similarly, we can reduce the weighted regret minimization problem to the following problem:

| (5) |

2.3 Group Fairness: ex post and ex ante

Now suppose consumers are partitioned into groups: , e.g. based on their attributes like race or risk levels. Each consists of the consumers of group represented by their risk thresholds. We will often abuse notation and write to denote that consumer has threshold . Given this group structure, minimizing the regret of the whole population absent any constraint might lead to some groups incurring much higher regret than others. With fairness concerns in mind, we turn to the design of efficient algorithms to minimize the maximum regret over groups (we call this maximum “group regret”):

| (6) |

The set of products that solves the above minmax problem222In Appendix C, we show that optimizing for population regret can lead to arbitrarily bad group regret in relative terms, and vice-versa. will be said to satisfy ex post minmax fairness (for brevity, we call this “fairness” throughout). One can relax problem (6) by allowing the designer to randomize over sets of products and output a distribution over (as opposed to one deterministic set of products) that minimizes the maximum expected regret of groups:

| (7) |

where represents the set of probability distributions over the set , for any . The distribution that solves the above minmax problem will be said to satisfy ex ante minmax fairness — meaning fairness is satisfied in expectation before realizing any set of products drawn from the distribution — but there is no fairness guarantee on the realized draw from . Such a notion of fairness is useful in settings in which the designer has to make repeated decisions over time and has the flexibility to offer different sets of products in different time steps. In Section 4, we provide algorithms that solve both problems cast in Equations (6) and (7). We note that while there is a simple integer linear program (ILP) that solves Equations (6) and (7), such an ILP is often intractable to solve. We use it in our experiments on small instances to evaluate the quality of our efficient algorithms.

3 Regret Minimization Absent Fairness

In this section we provide an efficient dynamic programming algorithm for finding the set of products that minimizes the (weighted) regret for a collection of consumers. This dynamic program will be used as a subroutine in our algorithms for finding optimal products for minmax fairness.

Let be a collection of consumer risk thresholds and be their weights, such that (w.l.o.g). The key idea is as follows: suppose that consumer index defines the riskiest product in an optimal set of products. Then all consumers will be assigned to that product and the consumers will not be. Therefore, if we knew the highest risk product in an optimal solution, we would be left with a smaller sub-problem in which the goal is to optimally choose products for the first consumers. Our dynamic programming algorithm finds the optimal products for the first consumers for all values of and .

More formally for any , let and denote the lowest risk consumers and their weights. For any and , let be the optimal weighted regret achievable in the sub-problem using products for the first weighted consumers. We make use of the following recurrence relations:

Lemma 1.

The function defined above satisfies the following properties:

-

1.

For any , we have .

-

2.

For any and , we have

Proof.

See Appendix G.1. ∎

The running time of our dynamic programming algorithm, which uses the above recurrence relations to solve all sub-problems, is summarized below.

Theorem 1.

There exists an algorithm that, given a collection of consumers with weights and a target number of products , outputs a collection of products with minimal weighted regret: . This algorithm runs in time .

Proof.

The algorithm computes a table containing the values for all values of and using the above recurrence relations. The first column, when , is computed using property 1 from Lemma 1, while the remaining columns are filled using property 2. By keeping track of the value of the index achieving the minimum in each application of property 2, we can also reconstruct the optimal products for each sub-problem.

To bound the running time, observe that the sums appearing in both properties can be computed in time, after pre-computing all partial sums of the form and for . Computing these partial sums takes time. With this, property 1 can be evaluated in time, and property 2 can be evaluated in time (by looping over the values of ). In total, we can fill out all table entries in time. Reconstructing the optimal set of products takes time. ∎

4 Regret Minimization with Group Fairness

In this section, we study the problem of choosing products when the consumers can be partitioned into groups, and we want to optimize minmax fairness across groups, for both the ex post minmax fairness Program (6) and the ex ante minmax fairness Program (7).

We start the discussion of minmax fairness by showing a separation between the ex post objective in Program (6) and the ex ante objective in Program (7). More precisely, we show in subsection 4.1 that the objective value of Program (6) can be times higher than the objective value of Program (6).

In the remainder of the section, we provide algorithms to solve Programs (6) and (7). In subsection 4.2, we provide an algorithm that solves Program (7) to any desired additive approximation factor via no-regret dynamics. In subsection 4.3, we provide a dynamic program approach that finds an approximately optimal solution to Program (6) when the number of groups is small. Finally, in subsection 4.4, we provide a dynamic program that solves Program (6) exactly in a special case of our problem in which the groups are given by disjoint intervals of consumer risk thresholds.

4.1 Separation Between Randomized and Deterministic Solutions

The following theorem shows a separation between the minmax (expected) regret achievable by deterministic versus randomized strategies (as per Programs (6) and (7)); in particular, the regret of the best deterministic strategy can be times worse than the regret of the best randomized strategy:

Theorem 2.

For any and , there exists an instance consisting of groups such that

Proof.

The proof is provided in Appendix G.2. ∎

In the following theorem, we show that for any instance of our problem, by allowing a multiplicative factor blow-up in the target number of products , the optimal deterministic minmax value will be at least as good as the randomized minmax value with products.

Theorem 3.

We have that for any instance consisting of groups, and any ,

Proof.

Fix any instance and any . Let which is the best set of products for group . We have that

where the last inequality follows from the definition of and it holds for any distribution . ∎

4.2 An Algorithm to Optimize for ex ante Fairness

In this section, we provide an algorithm to solve the ex ante Program (7). Remember that the optimization problem is given by

| (7) |

Algorithm (1) relies on the dynamics introduced by Freund and Schapire [7] to solve Program (7). The algorithm interprets this minmax optimization problem as a zero-sum game between the designer, who wants to pick products to minimize regret, and an adversary, whose goal is to pick the highest regret group. This game is played repeatedly, and agents update their strategies at every time step based on the history of play. In our setting, the adversary uses the multiplicative weights algorithm to assign weights to groups (as per Freund and Schapire [7]) and the designer best-responds using the dynamic program from Section 3 to solve Equation (8) to choose an optimal set of products, noting that

where denotes the weight assigned to agent , at time step .

| (8) |

Theorem 4 shows that the time-average of the strategy of the designer in Algorithm 1 is an approximate solution to minmax problem (7).

Theorem 4.

Suppose that for all , . Then for all , Algorithm 1 runs in time and the output distribution satisfies

| (9) |

Proof.

Note that the action space of the designer and the action set of the adversary are both finite, so our zero-sum game can be written in normal form. Further, , noting that the return of each agent is in — so must be the average return of a group. Therefore, our minmax game fits the framework of Freund and Schapire [7], and we have that

The approximation statement is obtained by noting that for any distribution over groups,

With respect to running time, note that at every time step , the algorithm first solves

We note that this can be done in time as per Section 3, remembering that

i.e., Equation (8) is a weighted regret minimization problem. Then, the algorithm computes for each group , which can be done in time (by making a single pass through each customer and updating the corresponding for ). Finally, computing the weights takes time. Therefore, each step takes time , and there are such steps, which concludes the proof. ∎

Importantly, Algorithm 1 outputs a distribution over -sets of products; Theorem 4 shows that this distribution approximates the ex ante minmax regret . can be used to construct a deterministic set of product with good regret guarantees: while each -set in the support of may have high group regret, the union of all such -sets must perform at least as well as and therefore meet benchmarks and . However, this union may lead to an undesirable blow-up in the number of deployed products. The experiments in Section 6 show how to avoid such a blow-up in practice.

4.3 An ex post Minmax Fair Strategy for Few Groups

In this section, we present a dynamic programming algorithm to find products that approximately optimize the ex post maximum regret across groups, as per Program (6). Remember the optimization problem is given by

| (6) |

The algorithm aims to build a set containing all -tuples of average regrets that are simultaneously achievable for groups . However, doing so may be computationally infeasible, as there can be as many regret tuples as there are ways of choosing products among consumer thresholds, i.e. of them. Instead, we discretize the set of possible regret values for each group and build a set that only contains rounded regret tuples via recursion over the number of products . The resulting dynamic program runs efficiently when the number of groups is a small constant and can guarantee an arbitrarily good additive approximation to the minmax regret. We provide the main guarantee of our dynamic program below and defer the full dynamic program and all technical details to Appendix E

Theorem 5.

Fix any . There exists a dynamic programming algorithm that, given a collection of consumers , groups , and a target number of products , finds a product vector with in time .

This running time is efficient when is small, with a much better dependency in parameters and than the brute force approach that searches over all ways of picking products.

4.4 The Special Case of Interval Groups

We now consider the case in which each of the groups is defined by an interval of risk thresholds. I.e., there are risk limits so that contains all consumers with risk limit in . Equivalently, every consumer in has risk limit strictly smaller than any member of .

Our main algorithm in this section is for a decision version of the fair product selection problem, in which we are given interval groups , a number of products , a target regret , and the goal is to output a collection of products such that every group has average regret at most if possible or else output Infeasible. We can convert any algorithm for the decision problem into one that approximately solves the minmax regret problem by performing binary search over the target regret to find the minimum feasible value. Finding an -suboptimal set of products requires runs of the decision algorithm, where is a bound on the minmax regret.

Our decision algorithm processes the groups in order of increasing risk limit, choosing products when processing group . Given the maximum risk product chosen for groups , we choose to be a set of products of minimal size that achieves regret at most for group (together with the product ). Among all smallest product sets satisfying this, we choose one with the product with the highest risk. We call such a set of products efficient for group . We argue inductively that the union is the smallest set of products that achieves regret at most for all groups. In particular, if then we have a solution to the decision problem, otherwise it is infeasible. We may also terminate the algorithm early if at any point we have already chosen more than products.

Formally, for any set of consumer risk limits, number of products , default product , and target regret , define to be the (possibly empty) collection of all sets of at most products selected from for which the average regret of the consumers in falls below using the products together the default product . For any collection of product sets , we say that the product set is efficient in whenever for all we have and if then . That is, among all product sets in , has the fewest possible products and, among all such sets it has a maximal highest risk product. Each iteration of our algorithm chooses an efficient product set from , where is the number of products left to choose and is the highest risk product chosen so far. Pseudocode is given in Algorithm 2.

Input: Interval groups , max products , target regret

-

1.

Let

-

2.

For

-

(a)

If output Infeasible

-

(b)

Otherwise, let be an efficient set of products in .

-

(c)

Let .

-

(a)

-

3.

Output .

Lemma 2.

For any interval groups , …, , number of products , and target regret , Algorithm 2 will output a set of at most products for which every group has regret at most if one exists, otherwise it outputs Infeasible.

Proof.

See Appendix G.3. ∎

It remains to provide an algorithm that finds an efficient set of products in the set if one exists. The following Lemma shows that we can use a slight modification of the dynamic programming algorithm from 1 to find such a set of products in time if one exists, or output Infeasible.

Lemma 3.

There exists an algorithm for finding an efficient set of products in if one exists and outputs Infeasible otherwise. The running time of the algorithm is .

Proof.

A straightforward modification of the dynamic program described in Section 3 allows us to solve the problem of minimizing the regret of population when using products, and the default option is given by a product with risk limit for all (instead of ). The dynamic program runs in time , and tracks the optimal set of products to serve the lowest risk consumers in while assuming the remaining consumers are offered product , for all and . Assuming is non-empty, one of these ’s corresponds to the highest product in an efficient solution, and one of the values of corresponds to the number of products used in said efficient solution. Therefore, the corresponding optimal choice of products is efficient: since it is optimal, the regret remains below . It then suffices to search over all values of and after running the dynamic program, which takes an additional time at most . ∎

Combined, the above results prove the following result:

Theorem 6.

There exists an algorithm that, given a collection of consumers divided into interval groups and a number of products , outputs a set of products satisfying and runs in time , where is a bound on the maximum regret of any group.

Proof.

Run binary search on the target regret using Algorithm 2 together with the dynamic program. Each run takes time, and we need to do runs. ∎

5 Generalization Guarantees

5.1 Generalization for Regret Minimization Absent Fairness

Suppose now that there is a distribution over consumer risk thresholds. Our goal is to find a collection of products that minimizes the expected (with respect to ) regret of a consumer when we only have access to risk limits sampled from . For any distribution over consumer risk limits and any , we define , which is the distributional counterpart of .

In Theorem 7, we provide a generalization guarantee that shows it is enough to optimize when is a sample of size drawn from .

Theorem 7 (Generalization Absent Fairness).

Let be any non-decreasing function with bounded range and be any distribution over . For any and , and for any target number of products , if is drawn from provided that

then with probability at least , we have

Proof.

See Appendix G.4. ∎

The number of samples needed to be able to approximately optimize to an additive factor has a standard square dependency in but is independent of the number of products . This result may come as a surprise, especially given that standard measures of the sample complexity of our function class do depend on . Indeed, we examine uniform convergence guarantees over the function class where 333Note that uniform convergence over is equivalent to uniform convergence over the class of functions. via Pollard’s pseudo-dimension () [12] and show that the complexity of this class measured by Pollard’s pseudo-dimension grows with the target number of products : .

Definition 1 (Pollard’s Pseudo-dimension).

A class of real-valued functions P-shatters a set of points if there exist a set of “targets” such that for every subset of point indices, there exists a function, say such that if and only if . In other words, all possible above/below patterns are achievable for the targets . The pseudo-dimension of , denoted by , is the size of the largest set of points that it P-shatters.

Lemma 4.

Let be any function that is strictly increasing on some interval 444While not always true, most natural instances of the choice of assets are such that is strictly increasing on some interval .. Then for any , the corresponding class of functions has .

Proof.

See Appendix G.4. ∎

5.2 Generalization for Fairness Across Several Groups

In the presence of groups, we can think of as being a mixture over distributions, say , where is the distribution of group , for every . We let the weight of this mixture on component be . Let . In this framing, a sample can be seen as first drawing and then . Note that we have sampling access to the distribution and cannot directly sample from the components of the mixture: .

Theorem 8 (Generalization with Fairness).

Let be any non-decreasing function with bounded range and be any distribution over . For any and , and for any target number of products , if consisting of groups is drawn from provided that

then with probability at least , we have

Proof.

See Appendix G.4. ∎

6 Experiments

In this section, we present experiments that aim to complement our theoretical results. The code for these experiments can be found at https://github.com/TravisBarryDick/FairConsumerFinance.

Data.

The underlying data for our experiments consists of time series of daily closing returns for 50 publicly traded U.S. equities over a 15-year period beginning in 2005 and ending in 2020; the equities chosen were those with the highest liquidity during this period. From these time series, we extracted the average daily returns and covariance matrix, which we then annualized by the standard practice of multiplying returns and covariances by 252, the number of trading days in a calendar year. The mean annualized return across the 50 stocks is 0.13, and all but one are positive due to the long time period spanned by the data. The correlation between returns and risk (standard deviation of returns) is 0.29 and significant at . The annualized returns and covariances are then the basis for the computation of optimal portfolios given a specified risk limit as per Section 2.555For ease of understanding, here we consider a restriction of the Markowitz portfolio model of [11] and Equation (1) in which short sales are not allowed, i.e. the weight assigned to each asset must be non-negative.

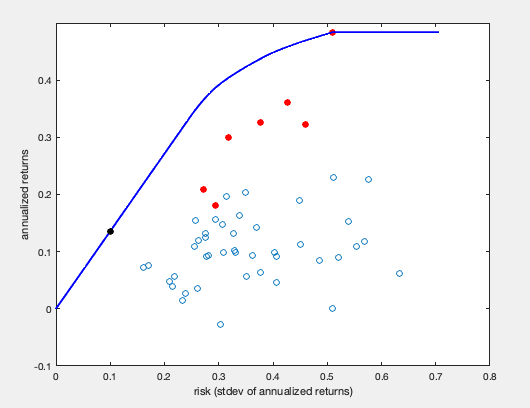

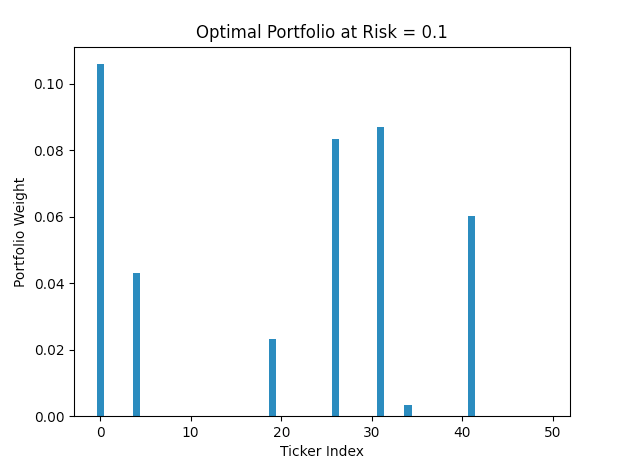

In Figure 1(a), we show a scatter plot of risk vs. returns for the 50 stocks. For sufficiently small risk values, the optimal portfolio has almost all of its weight in cash, since all of the equities have higher risk and insufficient independence. At intermediate values of risk, the optimal portfolio concentrates its weight on just the 7 stocks666These 7 stocks are Apple, Amazon, Gilead Sciences, Monster Beverage Corporation, Netflix, NVIDIA, and Ross Stores. highlighted in red in Figure 1(a). This figure also plots the optimal risk-return frontier, which generally lies to the northwest (lower risk and higher return) of the stocks themselves, due to the optimization’s exploitation of independence. The black dot highlights the optimal return for risk tolerance 0.1, for which we show the optimal portfolio weights in Figure 1(b). Note that once the risk tolerance reaches that of the single stock with highest return (red dot lying on the optimal frontier, representing Netflix), the frontier becomes flat, since at that point the portfolio puts all its weight on this stock.

Algorithms and Benchmarks.

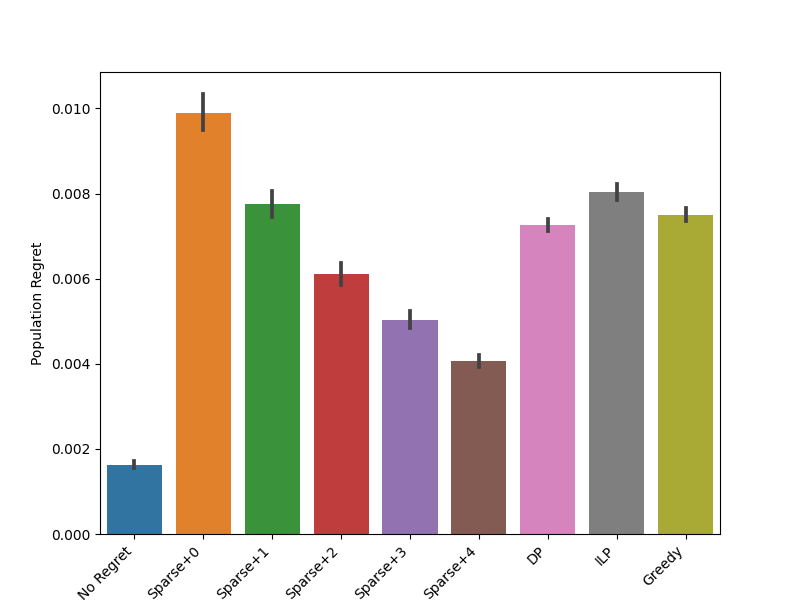

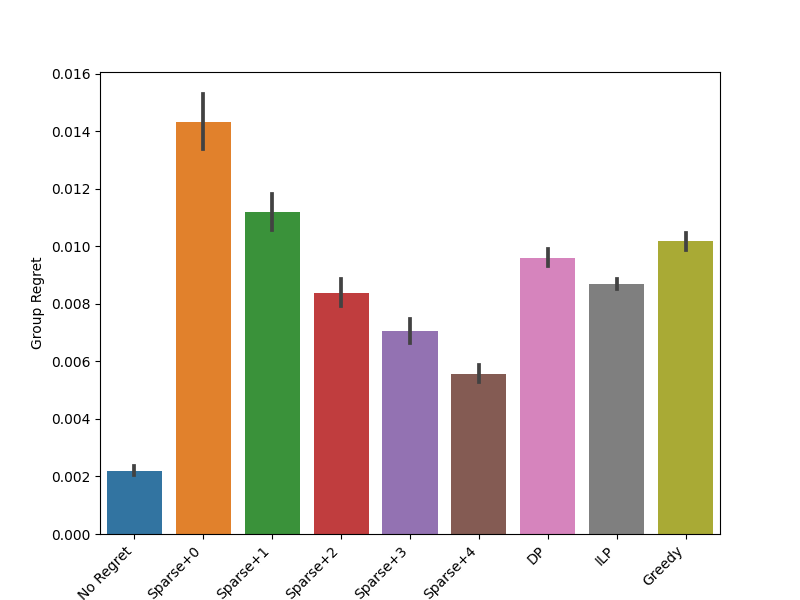

We consider both population and group regret and a number of algorithms: the integer linear program (ILP) for optimizing group regret; an implementation of the no-regret dynamics (NR) for group regret described in Algorithm 1; a “sparsified” NR (described below); the dynamic program (DP) of Section 3 for optimizing population regret; and a greedy heuristic, which iteratively chooses the product that reduces population regret the most.777In Appendix D, we show that the average population return is submodular, and thus the greedy algorithm, which has the advantage of running time compared to the of the DP, also enjoys the standard approximate submodular performance guarantees. We will evaluate each of these algorithms on both types of regret (and provide further details in Appendix F).

Note that Algorithm 1 outputs a distribution over sets of products; a natural way of extracting a fixed set of products is to take the union of the support (which we refer to as algorithm NR below), but in principle this could lead to far more than products. We thus sparsify this union with a heuristic that extracts only total products (here is a number of additional “slack” products allowed) by iteratively removing the higher of the two products closest to each other until we have reduced to products. This heuristic is motivated by the empirical observation that the NR dynamics often produce clumps of products close together, and we will see that it performs well for small values of .

Experimental Design and Results.

Our first experiment compares the empirical performance of the algorithms we have discussed on both population and group regret. We focus on a setting with desired products and 50 consumers drawn with uniform probability from 3 groups. Each group is defined by a Gaussian distribution of risk tolerances with of and (truncated at if necessary; as per the theory, we add a cash option with zero risk and return). Thus the groups tend to be defined by risk levels, as in the interval groups case, but are noisy and therefore overlap in risk space. The algorithms we compare include the NR algorithm run for steps; the NR sparsified to contain from 0 to 4 extra products; the ILP; the DP, and greedy. We compute population and group regret and average results over instances.

Figure 2 displays the results888We provide additional design details and considerations in Appendix F.. For both population and group regret, NR performs significantly better than ILP, DP, and greedy but also uses considerably larger numbers of products (between 8 and 19, with a median of 13). The sparsified NR using additional products results in the highest regret but improves rapidly with slack allowed. By allowing extra products, the sparsified NR achieves lower population regret than the DP with products and lower group regret as the ILP with 5 products. While we made no attempt to optimize the integer program (besides using one of the faster solvers available), we found sparsified NR to be about two orders of magnitude faster than solving the ILP (0.3 vs. 14 seconds on average per instance).

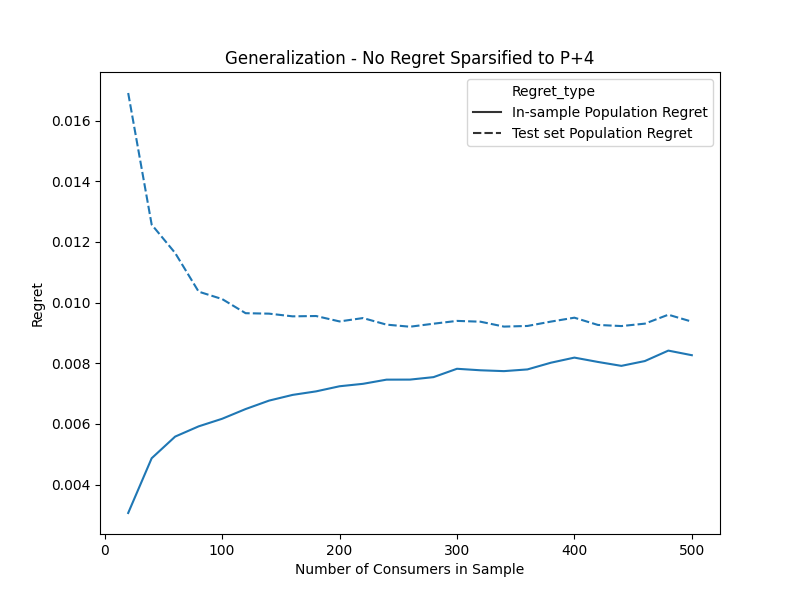

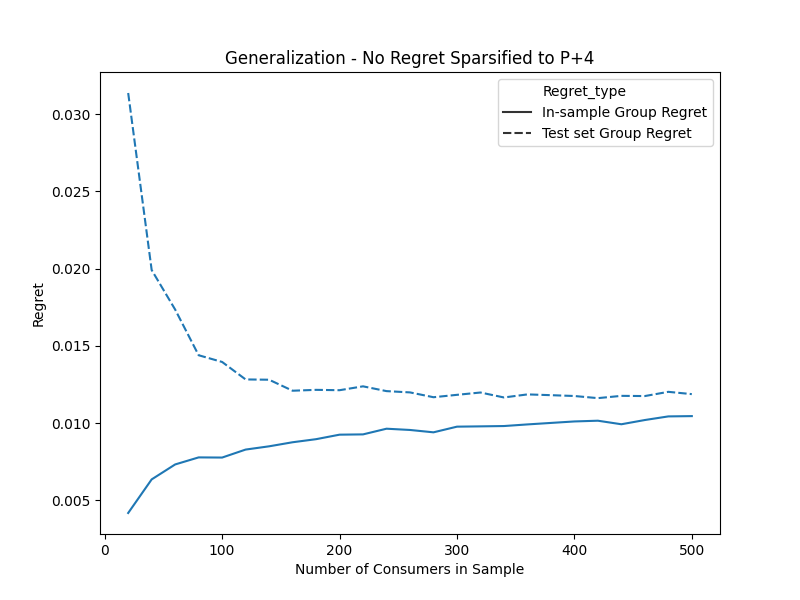

Our second experiment explores generalization. We fix and use sparsified NR with a slack of for a total of 9 products. We draw a test set of 5000 consumers from the same distribution described above. For sample sizes of consumers, we obtain product sets using sparsified NR and calculate the incurred regret using these products on the test set. We repeat this process 100 times for each number of consumers and average them. This is plotted in Figure 3; we observe that measured both by population regret as well as by group regret, the test regret decreases as sample size increases. The decay rate is roughly , as suggested by theory, but our theoretical bound is significantly worse due to sub-optimal constants999The theoretical bound is roughly an order of magnitude higher than the experimental bound; we do not plot it as it makes the empirical errors difficult to see.. Training regret increases with sample size because, for a fixed number of products, it is harder to satisfy a larger number of consumers.

References

- Barman and Krishnamurthy [2017] Siddharth Barman and Sanath Kumar Krishnamurthy. Approximation algorithms for maximin fair division. In Proceedings of the 2017 ACM Conference on Economics and Computation, pages 647–664, 2017.

- Budish [2011] Eric Budish. The combinatorial assignment problem: Approximate competitive equilibrium from equal incomes. Journal of Political Economy, 119(6):1061–1103, 2011.

- Chouldechova and Roth [2020] Alexandra Chouldechova and Aaron Roth. A snapshot of the frontiers of fairness in machine learning. Communications of the ACM, 63(5):82–89, 2020.

- Donahue and Kleinberg [2020] Kate Donahue and Jon Kleinberg. Fairness and utilization in allocating resources with uncertain demand. In Proceedings of the 2020 Conference on Fairness, Accountability, and Transparency, pages 658–668, 2020.

- Elzayn et al. [2019] Hadi Elzayn, Shahin Jabbari, Christopher Jung, Michael Kearns, Seth Neel, Aaron Roth, and Zachary Schutzman. Fair algorithms for learning in allocation problems. In Proceedings of the Conference on Fairness, Accountability, and Transparency, pages 170–179, 2019.

- Ensign et al. [2017] Danielle Ensign, Sorelle A Friedler, Scott Neville, Carlos Scheidegger, and Suresh Venkatasubramanian. Runaway feedback loops in predictive policing. arXiv preprint arXiv:1706.09847, 2017.

- Freund and Schapire [1996] Yoav Freund and Robert E Schapire. Game theory, on-line prediction and boosting. In Proceedings of the ninth annual conference on Computational learning theory, pages 325–332, 1996.

- Iancu and Trichakis [2014] Dan A Iancu and Nikolaos Trichakis. Fairness and efficiency in multiportfolio optimization. Operations Research, 62(6):1285–1301, 2014.

- Jung et al. [2019] Christopher Jung, Sampath Kannan, and Neil Lutz. A center in your neighborhood: Fairness in facility location. arXiv preprint arXiv:1908.09041, 2019.

- Mahabadi and Vakilian [2020] Sepideh Mahabadi and Ali Vakilian. (individual) fairness for -clustering. arXiv preprint arXiv:2002.06742, 2020.

- Markowitz [1952] Harry Markowitz. Portfolio selection. The Journal of Finance, 7(1):77–91, 1952. doi: 10.1111/j.1540-6261.1952.tb01525.x. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1540-6261.1952.tb01525.x.

- Pollard [1984] David Pollard. Convergence of stochastic processes. New York: Springer-Verlag, 1984.

- Procaccia and Wang [2014] Ariel D Procaccia and Junxing Wang. Fair enough: Guaranteeing approximate maximin shares. In Proceedings of the fifteenth ACM conference on Economics and computation, pages 675–692, 2014.

Appendix

Appendix A Probabilistic Tools

Lemma 5 (Additive Chernoff-Hoeffding Bound).

Let be a sequence of random variables with and for all . Let . We have that for all ,

Lemma 6 (Standard DKW-Inequality).

Let be any distribution over and be an sample drawn from . Define and to be the cumulative density functions of and the drawn sample, respectively. We have that for all ,

The following Lemma is just a sanity check to make sure that we can apply the DKW inequality to the strict version of a cumulative density function.

Lemma 7 (DKW-Inequality for Strict CDF).

Let be any distribution over and be an sample drawn from . Define and to be the strict cumulative density functions of and the drawn sample, respectively. We have that for all ,

Proof.

The key idea is to apply the standard DKW inequality to the (non-strict) CDF of the random variable . Towards that end, define and . Then we have the following connection to and :

The proof is complete by the standard DKW inequality (see Lemma 6). ∎

Lemma 8 (Multiplicative Chernoff Bound).

Let be a sequence of random variables with and for all . We have that for all ,

Appendix B A More General Regret Notion

In this section we propose a family of regret functions parametrized by a positive real number that captures the regret notion we have been using throughout the paper as a special case. We will show how minor tweaks allow us to extend the dynamic program for whole population regret minization of Section 3, as well as the no-regret dynamics for ex ante fair regret minimization of Section 4.2, to this more general notion of regret. For a given consumer with risk threshold , and for any , the regret of the consumer when assigned to a single product with risk threshold is defined as follows:

| (10) |

When offering more than one product, say products represented by , the regret of a consumer with risk threshold is the best regret she can get using these products. Concretely,

| (11) |

We note that our previous regret notion is recovered by setting . When , a consumer may be assigned to a product with higher risk threshold, and the consumer’s regret is then measured by the difference between her desired risk and the product’s risk, scaled by a factor of . We note that in practice, consumers may have different behavior as to whether they are willing to accept a higher risk product, i.e. different consumers may have different values of ; in this section, we use a unique value of for all consumers for simplicity of exposition and note that our insights generalize to different consumers having different ’s. The regret of a set of consumers is defined as the average regret of consumers, as before. In other words,

| (12) |

We first show in Lemma 9 how we can find one single product to minimize the regret of a set of consumers represented by a set . Note this general formulation of regret will allow choosing products that do not necessarily fall onto the consumer risk thresholds. In Lemma 9 we will show that given access to the derivative function , the problem can be reduced to an optimization problem that can be solved exactly in time. Before that, we first observe the following property of function (Equation (1)) which will be used in Lemma 9:

Claim 1.

is a concave function.

Proof of Claim 1.

Let be the vector of random variables representing assets and recall is the mean of and is its covariance matrix. Fix , and . For , let be an optimal solution to the optimization problem for , i.e., is such that . We want to show that

| (13) |

So all we need to show is that is feasible in the corresponding optimization problem for . Then, by definition, Equation (13) holds. We have that

and

where the second inequality follows from Cauchy-Schwarz inequality. Note also that and , for . ∎

Lemma 9.

Let where . We have that is a convex function and

| (14) |

where for every , ( if does not exist) and

Proof of Lemma 9.

First observe that Claim 1 implies for every , defined in Equation (10) is convex. Hence, is convex because it is an average of convex functions. We have that for a single product ,

Note that for every and for every . We can therefore focus on the domain to find the minimum. The function is differentiable everywhere except for the points given by consumers’ risk thresholds: . This justifies the first term appearing in the term of Equation (14). For every , the function on domain is differentiable and can be written as:

The minimum of on domain is achieved on points where

We note that is a convex function by the first part of this Lemma implying that (if belongs to the domain ) is a local minimum. This justifies the second term appearing in the term of Equation (14) and completes the proof. ∎

Remark 1.

Given any set of weights over consumers, Lemma 9 can be easily extended to optimizing the weighted regret of a set of consumers given by:

In fact, for any and , we have that is a convex function and

| (15) |

where for every , ( if does not exist) and

We now provide the idea behind a dynamic programming approach for choosing products that minimize the weighted regret of a population . The approach relies on the simple observation that there exists an optimal solution such that if the consumers in set are assigned to the -th product , (for a single product )101010On the one hand, for all and given , picking in such a manner provides a lower bound on the achievable average regret. On the other hand, yields as a set of consumers assigned to in an optimal solution. Indeed, if consumers in strictly preferred picking a different product, this could only be because they would get strictly better regret from doing so: by picking a different product, they would then decrease the population regret below our lower bound, which is a contradiction..

Therefore, to find an optimal choice of products, it suffices to i) correctly guess which subset of consumers are assigned to the -th product, then ii) optimize the choice of product for , which can be done using Lemma 9. Noting that is an interval for all , is entirely characterized by , the first agent assigned to , and , the last agent assigned to . In turn, as in Section 3, our dynamic program can be characterized by a recursive relationship of the form

| (16) |

where represents the minimum weighted regret that can be achieved by providing products to consumers to . Our dynamic program will implement this recursive relationship.

Appendix C Optimizing for Population vs. Least Well-Off Group: An Example

In this section, we show that optimizing for population regret may lead to arbitrarily bad maximum group regret, and optimizing for maximum group regret may lead to arbitrarily bad population regret. To do so, we consider the following example: there is a set of consumers, divided into two groups and . We let and and assume the single consumer in group has risk threshold , and the consumers in group all have the same risk threshold . We let be the returns corresponding to risk thresholds . Let , i.e. the designer can pick only one product; either or .

When picking , we have that the average group and population regrets are given by:

When picking instead, we have

Suppose and . Then, the optimal product to optimize for maximum group regret is , and the optimal product to optimize for population regret is . Then, we have that

-

1.

The ratio of population regret using over that of is given by:

This ratio can be made arbitrarily large by letting , at constant.

-

2.

The ratio of maximum group regret using over that of is given by:

This ratio can be made arbitrarily large by letting at constant.

Appendix D Approximate Population Regret Minimization via Greedy Algorithm

Recall that given and set of products, the population regret of is given by

where for any , , and

First, note that when no product is offered, consumers pick the cash option and get return :

Fact 1 (Centering).

For any , .

Second, is immediately monotone non-decreasing, as consumers deviate to an additional product only when they get higher return from doing so:

Fact 2 (Monotonicity).

For any , if , then .

Finally, is submodular:

Claim 2 (Submodularity).

For any , is submodular.

Proof.

We first show that for every , is submodular: for any , we have that

If or , the claim trivially holds. So assume . Let be such that . If , the claim holds because all four terms above will be zero. If , the claim holds because and by Fact 2. The same argument holds when by symmetry. The proof is complete by noting that any simple average of submodular functions (in general, any linear combination with non-negative coefficients) is submodular. ∎

Remark 2.

Claim 2 extends to any weighted set of consumers: fix any set of consumers and any nonnegative weight vector . Then the function given by is submodular.

We therefore have that for any and any target number of products ,

where by Facts 1, 2 and Claim 2, the maximization problem in right-hand side is: maximization of a nonnegative monotone submodular function with a cardinality constraint. Using the Greedy Algorithm (that runs in time), we get products represented by such that

Appendix E An ex post Minmax Fair Strategy for Few Groups, Extended

Given bound on the maximum group regret and a step size of , we let

be a net of discretized regret values in with discretization size . Given any regret , we let be the regret obtained by rounding up to the closest higher regret value in . I.e., is uniquely defined so as to satisfy and . Our dynamic program implements the following recursive relationship:

| (17) | ||||

where for all ,

| (18) |

Note that contains a single regret tuple, whose -th coordinate is the weighted regret of agents when using weight and offering no product.

Intuitively, keeps track of a rounded up version of the feasible tuples of weighted group regrets when using weight in group and when offering products and considering the regret of consumers to only. The corresponding set of products used to construct the regret tuples in can be kept in a hash table whose keys are the regret tuples in ; we denote such a hash table by . While there can be several -tuples of products that lead to the same rounded regret tuple in , the dynamic program only stores one of them in the corresponding entry in the hash table at each time step. The program terminates after computing , and outputting the product vector in corresponding to the regret tuple with smallest regret for the worst-off group in . The sets satisfy the following guarantee:

Lemma 10.

Fix any . Let be any regret tuple that can be achieved using products. There exist consumer indices such that the corresponding regret tuple satisfies

where .

We provide the proof of Lemma 10 in Appendix E. In particular, Lemma 10 implies that the dynamic program run with discretization parameter approximately minimizes the maximum regret across groups (i.e., the optimal value of Program (6)) within an additive approximation factor of . Letting yields an -approximation to the minmax regret.

The running time of our dynamic program is summarized below:

Theorem 9.

Fix any . There exists a dynamic programming algorithm that, given a collection of consumers , groups , and a target number of products , computes and in time .

When the desired accuracy is , the dynamic program uses and has running time .

Proof.

Note that each set and built by the dynamic program has size at most , as only contains regret values in by construction and contains one product tuple per regret tuple in .

Each sum used in the dynamic program can be computed in time , given that and have been pre-computed for all and stored in a hash table. The pre-computation and storage of these partial sums can be done in time.

Now, each time step of the dynamic program corresponds to the -th product with . In each time step , we construct sets , one for each value of . For each value of , the dynamic program searches over i) and ii) at most tuples of regret in . Therefore, building can be done in time

Finally, finding the tuple with the smallest maximum regret in requires searching over at most product tuples in .

Therefore, running the dynamic program requires time . ∎

Proof of Lemma 10

We let be the set of weighted regret tuples that are achievable using thresholds when only agents to are considered, and the regret of agents in group is weighted by – importantly, this reweighting is independent of the choice of and computes the average regret of a group as if all of its consumers were present. The set contains all feasible tuples of average regret given groups . Importantly, is different from : contains all achievable tuples of regret, even those that do not belong to the net ; in turn may contain up to regret tuples. In comparison, is a smaller set of size at most that only contains regret tuples with values in the net . is built with the intent of approximating the true set of achievable regret tuples, .

The proof idea is to show that is a good approximation of , as intended. More precisely, we want to show that for every feasible regret tuple in , the discretized set contains a regret tuple that is at most away from ; further, the corresponding product vector has true, unrounded regret also within of .

We start by showing that obeys the following recursive relationship:

Claim 3.

| (19) | ||||

where

| (20) |

Proof.

When , the result is immediate, noting that agents to are assigned to the cash option with return and incur regret each. The total regret in group , considering agents to and reweighting regret by , is given by

Now, take . Fix the highest offered product to be , corresponding to consumer . First, agents are assigned to product corresponding to consumer ; the weighted regret incurred by these agents, limited to those in group , is exactly

The remaining agents are to and have products available to them; hence, a regret tuple can be feasibly incurred by these agents if and only if , by definition of . To conclude the proof, it is enough to note that the total regret incurred by agents in group is the sum of the regrets of agents and the regret of agents . ∎

We now show that for any , provides a -additive approximation to the true set of possible regret tuples :

Lemma 11.

For all , for all , and for any regret tuple , there exists a regret tuple such that for all .

Proof.

The proof follows by induction on . At step , the induction hypothesis states that for all , for any regret tuple , there exists a regret tuple such that for all .

First, when , the induction hypothesis holds immediately: by definition, . Now, suppose the induction hypothesis holds for . Pick any regret tuple ; we will show that the induction hypothesis holds for this tuple. First, note that there exists and such that

by definition of . Further, by induction hypothesis, there exists a -tuple of rounded regret

in such that

Combining the above two equations, we get that

Now, let . First, is in by definition. Second,

This concludes the induction. ∎

To conclude the proof, let be a tuple of regret that can be achieved using products. The tuple belongs to , by definition of . Therefore, by Lemma 11, there exists a regret tuple such that

Let be the product vector that was used to construct regret tuple . Since at each step , the dynamic program rounds regret tuples to higher values, a simple induction shows that

Combining the two above equations, we get the result:

Appendix F Additional Experiment Details

All experiments were run on a consumer laptop without GPU (13-inch Macbook Pro 2016 with 2 GHz Intel Core i5 and 8 GB of RAM), using Python 3.6.5 (and in particular, NumPy 1.17.1 and Pandas 1.0.3). Experiment 1 took about 16.7 minutes in total. Experiment 2 took about 3.8 hours in total. For reproducibility, we began each experiment with a fixed random seed (10).

For the No-Regret experiments, we have two parameters to choose: the number of steps and the step size111111We implement the Multiplicative Weight Update of Algorithm 1 in exponential form; i.e., we write . The code takes the regret values as losses, takes as the step size, and updates the -th weight in each round by a multiplicative factor of , as per Algorithm 1. This allows us to easily translate the weights in space so as to avoid numerical overflow issues.. Note that theory suggests that step size should be a function of the number of steps desired (or vice versa), but common practice among related algorithms is to try many step sizes and run until convergence. We adopt this approach, guided by theory. To do so, we calculate a lower bound on the theoretical instance-specific step size using the sum of rewards as a loose upper bound on the maximum possible group regret. We then consider applying the following multipliers to this lower bound on the step size: we take (1,10,100,1000,10000) as a small set of possible multipliers and examine convergence for each of them. In all experiments, we pick the step size multiplier after empirically observing that it both i) provides a good approximation to the optimal ex ante regret and ii) converges in few time steps; we note that our choices of multipliers enjoy good performance guarantees in practice, as evidenced by Figure 2.

Appendix G Omitted Proofs

G.1 Proof of Lemma 1

The first property is immediate, because when , we do not choose any products, and there is only one valid solution that assigns all consumers to the zero-risk cash product. For this solution, the weighted regret is simply the sum of the weighted returns for each consumer’s bespoke portfolio.

We now turn to proving the second property. For any consumer index , define to be the optimal weighted regret for the first consumers using products subject to the constraint that the highest risk product has risk threshold set to . That is,

The products achieving weighted regret must choose and choose to be optimal products for the consumers indexed , who are not served by the product because it is too high risk. On the other hand, the weighted regret of consumers when assigned to a product with risk limit is given by . Together, this implies that

On the other hand, for any and , we have that , because the optimal products for the first consumers has a largest risk threshold equal to some consumer risk threshold. Combining these equalities gives

as required.

G.2 Proof of Theorem 2

Proof.

Note there is a one-to-one relation (on some domain for risk thresholds) between any risk threshold and its corresponding return given by by Equation (1) — we will therefore (only for simplicity of exposition) construct our instance by defining a set of returns instead of risk thresholds. Let be the set of all possible returns in our instance for some constant . We will take for simplicity but our proof extends to any .

Our instance construction is simple. If , we partition into subsets of size at most , and we let each group be defined as one of the partition elements. In this case, there will be one consumer for every return value in . For e.g., if and , we can define and . If (allowing consumers having the same return) we let each group be defined by a single return value in . For e.g., if and , we can define , , and . To formalize this construction, define and let be a -sized partition of such that . Instance of size is defined as follows.

Let and observe that . We have that

where follows from the definition of in this specific instance that all consumer returns are specified by the set of size . follows from the fact that for any set of products , all groups that have a consumer with return will incur an average regret of . holds because . Next, by looking at the uniform distribution over ,

where follows from the definition of . follows from the fact that for every group and every , there is one (and only one) set of products, namely , that makes incur a regret of . We therefore have that

∎

G.3 Proof of Lemma 2

To ease notation, for any product sets , we let denote the union of the product sets with indices in .

Suppose our feasibility problem has a solution. It is enough to show that there exists product sets such that is a feasible set of at most products and is efficient in for all . Note that by the definition of efficiency and a straightforward induction, any product sets and alternative product sets satisfying these properties must have and for all , hence

does not depend on the specific choice of that satisfies the above assumptions. Since the algorithm may only output Infeasible if is empty for some , it can only do so when no satisfying the above assumptions exists. When such product sets exist, the algorithm outputs one, and is guaranteed to use at most products and have regret at most in each group by definition of .

Assuming our problem is feasible with products, we show the following induction hypothesis: for all there exist product sets such that is efficient in for all , that can be completed in a set products that has size at most and guarantees regret at most in each group, where .

First, the induction hypothesis immediately hold for : since the problem is feasible, there exists a product vector that uses at most products and guarantees group regret of at most . Now, suppose the induction hypothesis holds for ; we will show it holds for . Take that has size at most and guarantees regret at most in each group, such that is efficient in for all . Take to be efficient in ; we have two cases:

-

1.

and . Let us consider product set . Then, . Further, no group has regret over . Indeed, compared to when using , we have that: i) the regret of groups to is unaffected as they only use products ; ii) the regret of group stays below by satisfiability of ; iii) the regret of groups cannot increase because agents who used product get weakly lower regret from using , and the remaining agents can keep using the same products in . Since the regret of all groups remains below under products by the induction hypothesis, this remains true when using products .

-

2.

. In that case, let (where is the smallest threshold in group ). Consider product offering . First, we note that

Second, note that the regrets of all groups remain under . Indeed, compared to when offering products , we have: i) the regrets of groups stay the same, as before; ii) the regret of group stays below by satisfiability of , as before; iii) the regret of groups can also only decrease, because all agents who were assigned to are now assigned to the higher return product , while the remaining agents stay assigned to the same product in .

This concludes the proof.

G.4 Proofs of Generalization Theorems

Proof of Theorem 7.

Let and observe that using this notation, for any , . To prove the claim of the theorem, first note that,

| (21) |

where “” means sampling from the uniform distribution over . We have that by an application of additive Chernoff-Hoeffding bound (see Lemma 5), with probability at least , given the assumption on sample size ,

| (22) |

Now let us focus on the second term appearing in Equation (21). Consider any vector of products where, without loss of generality, we assume . Letting and , these products partition into intervals for such that for all . We can rewrite as a telescoping sum that adds a term for each interval up to and including the interval containing :

remembering for the last equality that is the risk-free cash option and has return and that is the final dummy product that corresponds to having an infinite risk and always satisfies . Taking expectations of this expression converts the indicator into the complementary CDF (CCDF), and therefore we have

| (23) | ||||

where the first inequality follows from the triangle inequality and the fact that is non-decreasing: for . The third inequality holds with probability and follows from the Dvoretzky-Kiefer-Wolfowitz inequality (see Lemma 7). The last inequality follows by the assumption on sample size . Combining Equations (21) and (22) and (23), completes the proof of the theorem. ∎

Proof of Theorem 8.

Let be a set of consumers of size drawn from the distribution that is partitioned into groups: . Let denote the size of group . It follows from the uniform convergence of Theorem 7 that for any group , so long as , with probability , . This implies by a union bound that with probability at least , so long as for all ,

But note for any group , where denotes a binomial random variable with trials and success probability . By an application of the Multiplicative Chernoff bound (see Lemma 8), as well as a union bound, we have that with probability , for any group ,

where the second inequality follows by the assumption on in the theorem statement. We can therefore conclude by another union bound that, with probability at least ,

The proof is complete by noting that

∎

Proof of Lemma 4.

Our goal is to show that the class of functions can P-shatter at least points (or consumer risk limits). Let be any sequence of increasing consumer risk limits. The high-level idea is to design a target and a product for consumer so that the return for consumer is at least the target if and only if the product is included (as opposed to a default product lower than any target). Given that we have products to choose, we can decide to include the product for each consumer or not independently, and therefore we can achieve all above/below target patterns to shatter the consumers.

Formally, define targets and a collection of candidate products so that

Note that this is always possible since the return function is strictly increasing on the interval . For any product vector of product risk thresholds, we have that if and only if there is some product such that . Now, for any , define a product risk threshold vector by if and if . By the above argument, and the definition of and , it follows that if and only if . Therefore shatters and . ∎