First exit-time analysis for an approximate Barndorff-Nielsen and Shephard model with stationary self-decomposable variance process

Shantanu Awasthi111Email: shantanu.awasthi@ndus.edu, Indranil SenGupta222Email: indranil.sengupta@ndsu.edu Department of Mathematics

North Dakota State University

Fargo, North Dakota, USA

Abstract

In this paper, an approximate version of the Barndorff-Nielsen and Shephard model, driven by a Brownian motion and a Lévy subordinator, is formulated. The first-exit time of the log-return process for this model is analyzed. It is shown that with a certain probability, the first-exit time process of the log-return is decomposable into the sum of the first exit time of the Brownian motion with drift, and the first exit time of a Lévy subordinator with drift. Subsequently, the probability density functions of the first exit time of some specific Lévy subordinators, connected to stationary, self-decomposable variance processes, are studied. Analytical expressions of the probability density function of the first-exit time of three such Lévy subordinators are obtained in terms of various special functions. The results are implemented to empirical S&P 500 dataset.

Key Words: Lévy process, Subordinator, Self-decomposability, First-exit time, Laplace transform.

1 Introduction

The time required for a stochastic process, starting at a given initial state, to reach a threshold for the first time is referred to as the first-exit time or the first hitting time. It is typically very useful in determining expected lifetime of mechanical devices. The first-exit time processes are very useful for understanding various financial sectors, especially the insurance industry and investment firms. The first-exit time processes arise naturally in the studies of various disciplines. For example, this is used in [42] to model the death probability density function for a decaying stochastic process that represents either the end of functionality for a machine, or a zero health state for an organism. The paper [22] provides an expanded first-exit time density function that expresses the human death distribution. The first-exit time analysis of a two-dimensional symmetric stable process is discussed in detail in the paper [14]. This is further developed in [24, 46] where the first-exit time process of an inverse Gaussian Lévy process is considered. The one-dimensional distribution function of the first-exit time process is obtained. The first-exit time analysis related to a geophysical data is provided in [16]. The paper [32], provides generalized notions and analysis methods for the exit-time of random walks on graphs.

The first-exit time process of the standard Brownian motion is well-studied in the literature (see [3]). The paper [26] studies the first-exit time of Brownian motion for a parabolic domain. In [15], the Fokker-Planck equation is solved for the Brownian motion with drift, in the presence of a fixed initial point and elastic boundaries. An explicit expression is obtained for the density of the first-exit time. The paper [20] studies the first-exit time problem for the solutions of some stochastic differential equations for bounded or unbounded intervals. Studies in [29, 44, 45] discuss the first-exit time process for strictly increasing Lévy processes. In the pioneering paper [23], the authors study the first-exit-time to flat boundaries for a double exponential jump diffusion process. The related stochastic process consists of a continuous Brownian motion-driven part, and a jump part with jump sizes given by a double exponential distribution. In general, with the help of a fluctuation identity, the paper [2] provides, a generic link between a number of known identities for the first-exit time and the overshoot above/below a fixed level of a Lévy process. In [31], a class of increasing Lévy processes perturbed by an independent Brownian motion is considered, and the problem of determining the distribution of the first-exit time is addressed. The first-exit time analysis of the Ornstein-Uhlenbeck (OU) process to a boundary is a long-standing problem with no known closed-form solution for the general case. In [28] a general mean-reverting process is considered to investigate the long-and short-time asymptotics using a combination of Hopf-Cole and Laplace transform techniques.

Many problems in finance are related to the first-exit time processes. A deeper understanding of such processes leads to a wiser estimation of fluctuations in the market. In [43], the first-exit time distributions of stock price returns in different time windows are analyzed. The probability distribution obtained by such analysis is compared with those obtained from different models for stock market evolution. The paper [19] shows that for continuous time transformations, independent of the Brownian motion, analytical results for the double-barrier problem can be obtained via the Laplace transform of the time change. The analysis provides a power series representation for the resulting first-exit time probabilities. In [27], explicit analytical characterizations are provided for the first-exit time densities for the Cox-Ingersoll-Ross (CIR) and OU diffusions. Such characterizations are obtained in terms of the relevant Sturm-Liouville eigenfunction expansions. In [49], a doubly skewed CIR process is studied. A modified spectral expansion is used to obtain the first-exit time distribution of a doubly skewed CIR process. A detailed study of the first-exit times of diffusion processes and their applications to finance is provided in [25]. The studies in [34, 35] discuss the first-exit time analysis related to some financial processes from a data-science and sequential hypothesis testing perspective. In [9], the authors provide a solution to the optimal stopping problem of a Brownian motion subject to the constraint that the stopping time’s distribution is a given measure consisting of finitely many atoms. The distribution constraints lead to an application in mathematical finance to model-free super-hedging with an outlook on volatility.

Some analytically tractable formulas are available for the density of the first-exit time process (see [46]). However, in general, an explicit expression for the density of the first-exit time process for a financial model is mostly unknown. In this paper, we analyze the first-exit time processes in connection to the Barndorff-Nielsen and Shephard (BN-S) model, a popularly used stochastic volatility model for financial analysis. In this paper we provide various analytical formulas related the distribution of the first-exit time processes in connection to an approximate version of the BN-S model. For this study we use various properties of the Laplace transform and their relations to special functions. In particular, the first-exit time processes for some well-known self-decomposable Lévy subordinators are analyzed.

The organization of the paper is as follows. In Section 2, a description of the BN-S model is provided. An approximation of the BN-S model is formulated based on the stationary, self-decomposable distributions of the variance process. In Section 3, the first-exit time for a combination of a Brownian motion and a Lévy subordinator is analyzed. In Section 4, the first-exit time distribution is studied in connection to various self-decomposable Lévy subordinators. It is shown that the analysis is related to the first-exit time analysis of the log-return for the approximation of the BN-S model presented in Section 2. In Section 5 some numerical results are provided based on S&P 500 close price dataset for a period of ten years. Finally, a brief conclusion is provided in Section 6.

2 Barndorff-Nielsen and Shephard model, self-decomposability, and an approximation

Financial time series of different assets share many common features which are successfully captured by the stochastic model introduced in various works of Ole Barndorff-Nielsen and Neil Shephard. The model is known in modern literature as the Barndorff-Nielsen and Shephard (BN-S) model (see [5, 7, 8]). This model is revised and refined in various recent works in literature such as [37, 38]. This model is successfully implemented in the commodity markets as well (see [40, 47]). Recently, this model is improved using various machine-learning driven algorithms (see [39, 41]).

For the BN-S model, a frictionless financial market is considered where a risk-less asset with constant interest rate , and a stock, are traded up to a fixed horizon date . It is assumed that the price process of the stock is defined on some filtered probability space and is given by:

(2.1)

where the log-return is given by

(2.2)

with the variance process

(2.3)

where the parameters with and . In (2.2) and (2.3), and are a Brownian motion and a Lévy subordinator, respectively. The Lévy subordinator is referred to as the background driving Lévy process (BDLP). Also and are assumed to be independent and is assumed to be the usual augmentation of the filtration generated by the pair . Without loss of generality, we assume .

We assume satisfies the assumptions described in [30]. It follows that the cumulant transform , where it exists, takes the form

, where is the Lévy density for . It is shown in [30] (Theorem 3.2) that there exists an equivalent martingale measure (EMM) , under which equations (2.2) and (2.3) can be written as:

(2.4)

(2.5)

where and are a Brownian motion and a Lévy subordinator respectively with respect to . For the rest of this paper we assume that the risk-neutral dynamics (with respect to ) of the stock price is given by (2.1), (2.4) and (2.5).

It is trivial to show that the solution of (2.5) is given by

(2.6)

From (2.6), the positivity of the process is obvious. In fact, is bounded below by the deterministic function . In addition, the instantaneous variance of log-return is given by . Consequently, the continuous realized variance in the interval , denoted as , is given by .

Therefore, by (2.6) we obtain

(2.7)

We state some results for the analysis of the variance process , when the process is stationary and self-decomposable. The results are motivated by [17, 18, 21]. The pricing formulas for various derivatives are dependent on the variance process.

Definition 2.1.

The distribution of a random variable is said to be self-decomposable if for any constant , , there exists an independent random variable , such that , where stands for the equality in the distribution.

For self-decomposable laws the associated densities are unimodal (see [13, 36]). It is proved in [6, 48] that, if is self-decomposable then there exists a stationary stochastic process , and a Lévy subordinator , independent of , such that for all and

Conversely, if , is a stationary stochastic process and is a Lévy subordinator independent of , such that and satisfy

for all , then is self-decomposable.

It is clear from [36] (Theorem 17.5(ii)) that for any self-decomposable law there exists a Lévy subordinator such that the process of OU type driven by has invariant distribution given by . The following theorem (see [17, 18, 38]) gives the relation between the Lévy densities of such process generated by and in (2.5).

Theorem 2.2.

A random variable has law in if and only if has a representation of the form

, where is a Lévy subordinator. In this case the Lévy measure and of and are related by .

In addition, if , the Lévy density of is differentiable, then the Lévy measure has a density , and and are related by

(2.8)

There are many known self-decomposable distributions, such as inverse Gaussian (IG), Gamma, positive tempered stable (PTS), etc.

Consequently, if the stationary distribution of is given by law, with the Lévy density , , then by (2.8), the Lévy density of is given by , . Alternatively, if the stationary distribution of is given by gamma law , where the Lévy density of is given by , , then by (2.8) we obtain , .

A three-parameter self-decomposable process is positive tempered stable (PTS) process (see [11, 12]). It is denoted as , where , , and . For process the Lévy density is simple and is given by (see [17, 18])

If the stationary distribution of is given by law, then by (2.8) we obtain that the Lévy density of is given by

In the above discussions we find that the distribution of is analytically tractable when the stationary distribution of in (2.5) is given by a stationary, self-decomposable distribution. We denote (as is stationary),

We refer to (2.1), (2.11), and (2.5), as an approximation of the BN-S model (2.1), (2.4), and (2.5). For most of the empirical financial data .

We write , with , , and , . For financial applications . For the subsequent sections we develop a general procedure to compute the first-exit time of the stochastic process .

3 First-exit time for a combination of a Brownian motion and a Lévy subordinator

In this section, we develop a couple of results related to the first-exit time analysis of log-return processes of the form (2.11). At first, we develop the result related to the first-exit time of a simpler process , where is a Lévy subordinator, with . If and are independent random variables, we denote .

Theorem 3.1.

For a Brownian motion and a Lévy subordinator , and ,

(3.1)

with probability

(3.2)

where

(3.3)

and

(3.4)

where the probability density function of is given by .

Proof.

The first-exit time of a combination of and , in the sense that its value is more than , is given by

For a fixed , we define

(3.5)

(3.6)

We proceed to compute and . We observe,

On the other hand,

As the probability density function of is given by , therefore we obtain

Clearly, , with probability , where is given by (3.2), and and are obtained by (3.3) and (3.4), respectively. This leads to (3.1).

∎

Next, we generalize the result in Theorem 3.1 for the log-return stochastic process (2.11) in the approximation of the BN-S model. In the BN-S model is assumed in order to incorporate the leverage effect of the market. Typically in a derivative market, a significant fluctuation always corresponds to a “big-downward-movement” of the asset prices. Consequently, for the next theorem we focus on the first-exit time corresponding to a “downward-movement” of the log-return process (2.11). For the following theorem we assume .

Theorem 3.2.

For a Brownian motion and a Lévy subordinator , if , , , and , then

(3.7)

with probability

(3.8)

where

(3.9)

and

(3.10)

where the probability density function of is given by .

Proof.

For fixed , we define and compute the following joint probabilities. At first, we compute, for :

With , we compute for ,

where . Since , therefore we obtain (3.10). For , we define a set

The purpose of Theorem 3.1 and Theorem 3.2 is to decompose the first-exit time process of a linear combination of a Brownian motion and a Lévy subordinator into the individual first-exit time processes of a Brownian motion and a Lévy subordinator. However, as observed in both of the theorems, such decomposition holds only with certain probability.

Remark 3.3.

It is well known (see [3, 24]) that for the process , with , known as the inverse Gaussian (IG) process, follows an distribution. As the process is continuous, we also have . The distribution is concentrated on and has probability density:

Consequently, for Theorem 3.2 with and , the first term on the right hand side of (3.2) has the distribution .

The case is not the same if the Brownian motion does not have any drift term. In that case, it is known (see [4]) that , with , satisfies a Lévy distribution with the probability density function

Consequently, for Theorem 3.1, the first term on the right hand side of (3.1), i.e., , with , has the probability density function , . A similar result holds for the first term on the right hand side of (3.2) in Theorem 3.2 with .

Note that, for the case when and , .

We note that for Theorem 3.1, if , then (3.1) is trivially satisfied. Similarly, for Theorem 3.2, if , then (3.2) is trivially satisfied. As , therefore all the related first-exit times are zero in those cases.

4 First-exit time distribution for some self-decomposable processes

Consider the log-return dynamics given by (2.11), in the approximation of the BN-S model (2.1), (2.11), and (2.5). In Theorem 3.2, it is shown that with certain probability, the first-exit time process , is decomposable into the sum of the first exit time of two processes- (1) the Brownian motion with drift, and (2) a Lévy subordinator with drift. We denote three stochastic processes: , , and , with , and . In these expressions and are given by (2.9) and (2.10), respectively. Thus, . Also, in general, for financial applications . With these notations, from Theorem 3.2 we obtain that .

The probability density function of the process , with , is discussed in Remark 3.3. In this section we discuss the probability density function of the process for some special cases. Accordingly, with probability given by (3.8), the probability density function of the process is equal to the convolution of the probability density functions of the processes and .

The goal of this section is to analyze the first-exit time distribution for the Lévy subordinator in the decompositions provided in Theorem 3.1 and Theorem 3.2. For simplicity we assume . We consider the distribution of the corresponding process , for three self-decomposable distributions. As and , in general, can be written as the stochastic process , .

In Subsection 4.1, we describe some results related to special functions and Laplace transforms that are implemented for the subsequent analysis. Subsections 4.2, 4.3, and 4.4, deal with various analysis of in relation to Gamma, IG, and PTS subordinators, respectively.

4.1 Laplace transform and some relevant special functions

At first, we describe some special functions necessary for the development of the rest of this paper.

•

The MacRobert -function is denoted as

For , with , the MacRobert -function is defined as

For , with , the MacRobert -function is defined as

For , the notation is used. The denotes that the term containing corresponding to is omitted. Here is generalized hypergeometric functions, defined as

where is the Pochhammer symbol.

•

The Gauss hypergeometric function is defined as

where is the Pochhammer symbol, , and . For , with , the series can be analytically continued along any path in the complex plane that avoids the branch points 1 and infinity.

An integral representation of the hypergeometric function is given by

.

•

Modified Bessel functions are solutions of the modified Bessel equation. The modified Bessel function of the first kind is defined by , with , and is the Bessel function of the first kind.

•

Upper incomplete gamma function is given by

For , converges for all real . In particular, is the exponential integral .

Next, we describe some results related to the Laplace transform. For , and , we denote the Laplace transform of by , where ) is piecewise continuous function on every finite interval in satisfying , for some and for all . The Laplace transform and the inverse Laplace transform are related by:

and

for some , where is greater than the real part of all singularities of , and is bounded on the line in the complex-plane. We list some useful properties related to the Laplace transform. The following result is elementary and can be found in [33].

Lemma 4.1.

The following results hold: (1) , with , ; (2) ; (3) ; (4) .

The following results provide various relations between the Laplace transform and special functions. These results can be found in [33].

Lemma 4.2.

The following results hold.

(1)

.

(2)

, where is the modified Bessel function of the first kind, and .

(3)

, .

(4)

, where is the upper incomplete gamma function, and .

(5)

, where , .

(6)

, .

(7)

, .

(8)

, where is the MacRobert -function, .

In the above expression denotes that in expression following the summation sign, is to be replaced by and two expressions are to be added.

In the two-dimension, for , let , be the Laplace transform of function with respect to the variable. Note that, for a subordinator , with probability density function , and Lévy measure , the Lévy-Khinchin representation gives (see[10])

(4.1)

where is the Laplace exponent of and is given by , where is the Lévy measure of . The following result can be found in [10].

Theorem 4.3.

The Lévy density and Lévy measure of the subordinator (with ) satisfy , where is the Laplace exponent of the subordinator .

Let be a subordinator with the probability density function . Suppose admits continuous partial derivatives. Let , for , represents the first-exit time process of . Denote the probability density function of by . Then,

(4.2)

where is the Laplace exponent of the subordinator .

Theorem 4.5.

Denote the -th moment of the first-exit time of the subordinator by . Then,

(4.3)

4.2 Gamma subordinators

Let be a Gamma subordinator with Lévy density given by , , with . In this case, the Laplace exponent of is given by (see [17, 30]).

Theorem 4.6.

For , , the probability density function of the first-exit time of is given by

(4.4)

where is the hypergeometric function.

Proof.

By Theorem 4.4, the Laplace transform of probability density of the first-exit time of

Gamma subordinator is given as

where , with ,and . Then . Let the inverse Laplace transforms for and be and , respectively.

Note that , (see [33]). Using Lemma 4.1(1), we obtain,

For , where is a non-negative integer, . Hence, by using Lemma 4.1(1), we obtain . Consequently, by standard convolution procedure, we obtain

Hence, with the application of Lemma 4.1(3), we obtain (4.4).

∎

The next result provides the first and the second order moment of the first-exit time of Gamma subordinator.

Theorem 4.7.

The first order moment (mean) the first-exit time of Gamma subordinator is given by

(4.5)

Proof.

Using Theorem 4.5, we obtain the Laplace transform of the -th moment of the first-exit time of the Gamma subordinator as .

Consequently, the Laplace transform of the first order moment of the first-exit time of the Gamma subordinator is given by

We observe that .

Consequently, using Lemma 4.1(2), we obtain

Consequently, can be computed using Lemma 4.1(3) to obtain (4.5).

∎

We conclude this subsection by considering the case when the subordinator , that appears in (2.11) and (2.5), is related to the Gamma subordinator in the BN-S model. As observed in Section 2, if the stationary distribution of is given by gamma law , then the Lévy density of is given by , .

Theorem 4.8.

The probability density function of the first-exit time of a subordinator with Lévy density , is given by

where is the modified Bessel function of the first kind.

Proof.

For this case, the Lévy measure of is given by . Using Theorem 4.3, we obtain . Consequently, . The Laplace transform of the probability density function of the first-exit time of is given by . Consequently, the probability density function of the first-exit time of is given by , where

Using Lemma 4.1(1) and Lemma 4.2(2), we obtain .

∎

4.3 Inverse Gaussian subordinators

The first-exit time of IG processes is described in [46]. In this subsection we consider the subordinator , that appears in (2.11) and (2.5), is related to the IG subordinator in the BN-S model. As observed in Section 2, if the stationary distribution of is given by law, then the Lévy density of is given by , , and .

For the results in Subsections 4.3 and 4.4, we define the convolution of two functions and by

Consequently, for three functions , , and ,

Theorem 4.9.

The probability density function of the first-exit time of a subordinator with Lévy density , is given by

, where

(4.6)

(4.7)

where is the Dirac delta function, is the modified Bessel function of the first kind, and

(4.8)

Proof.

We obtain the Lévy measure for as

Using Theorem 4.3, Lemma 4.2(4), and Lemma 4.2(5) we obtain,

(4.9)

Consequently, by Theorem 4.4, we obtain that the Laplace transform of the probability density function of the first-exit time of is given by

where

and

We denote the inverse Laplace transforms of , , and by , , and , respectively.

We have .

From this, comparing with (4.9), we note that . Hence is given by (4.6).

Next, we compute using Lemma 4.2(2), Lemma 4.2(1), and Lemma 4.1(4).

Lemma 4.2(2) gives .

With , we find . We notice . Consequently, using Lemma 4.1(4), we have . Hence, we obtain, , and thus , where is the Dirac delta-function.

Using Lemma 4.2(1), we obtain

. Therefore, using Lemma 4.1(1) we obtain

Finally,

Using Lemma 4.2(3), we obtain = .

Consequently, using Lemma 4.1(1), we obtain (4.8).

Finally, if is the probability density function of the first-exit time of , then .

∎

4.4 Positive tempered stable subordinators

Let be a positive tempered stable (PTS) subordinator with Lévy density given by

with , , and .

Theorem 4.10.

The probability density function of the first-exit time of is given by , where

(4.10)

where , and

(4.11)

In (4.10), is the MacRobert -function, and denotes that in expression following the summation sign, is to be replaced by and two expressions are to be added.

Proof.

We have

We compute using Theorem 4.3 to obtain the Laplace exponent of density function of as

Now using Theorem 4.4, we obtain the Laplace transform of the probability density function of the first-exit time of as

where . To compute , the probability density function of the first-exit time of , we find

and

and use the convolution result. By using Lemma 4.2(4), we obtain, the expression of as (4.10).

Next, compute . Denote . We observe

Hence, by using Lemma 4.2(8) and Lemma 4.1(1), we obtain the expression of as (4.10).

∎

We conclude this subsection by considering a subordinator related to the PTS subordinator in the BN-S model. If the stationary distribution of is given by law, then that the Lévy density of is given by

(4.12)

As in the previous sections, is the subordinator that appears in (2.11) and (2.5).

Theorem 4.11.

The probability density function of the first-exit time of a subordinator , with Lévy density (4.12), is given by , where

(4.13)

where , and

(4.14)

where

and

(4.15)

where

In the expressions of and , is the MacRobert -function, and denotes that in expression following the summation sign, is to be replaced by and two expressions are to be added.

where . Using Theorem 4.4, we obtain the Laplace transform of the probability density function of the first-exit time of as

where

and

We denote the inverse Laplace transform for , , and , by , , and , respectively. Using Lemma 4.2(4), we obtain .

Also, using Lemma 4.2(4), we obtain . Hence,

we obtain as given by (4.13).

Next, we observe that can be written as:

Hence by using Lemma 4.2(8) and Lemma 4.1(1), we obtain (4.14). Finally, we observe that can be written as

Hence by using Lemma 4.2(8) and Lemma 4.1(1), we obtain (4.15). Finally, by convolution theorem, we obtain the probability density function of the first-exit time of as .

∎

5 Numerical results

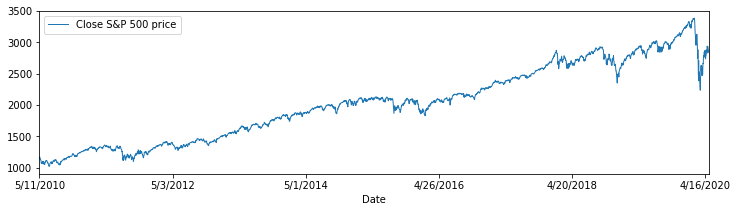

For this section, we use the S&P 500 daily close price dataset for the period May 11, 2010 to May 8, 2020.

Table 1 summarizes some features of this empirical dataset.

Table 1: Properties of the empirical dataset.

S&P 500 daily close price

Mean

2027.003

Median

2036.709

Maximum

3386.149

Minimum

1022.580

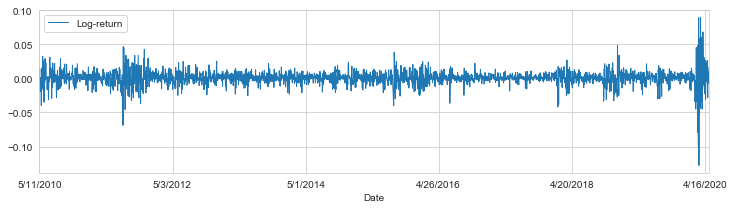

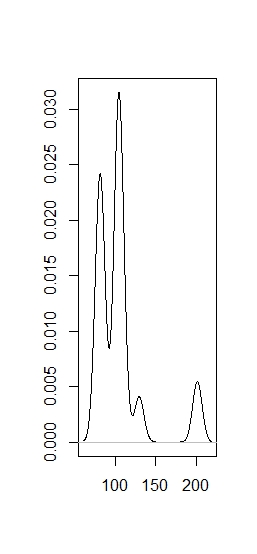

Figure 1 shows a line plot of the empirical dataset. The log-return process for the corresponding dataset is shown in Figure 2. Figure 3 and Figure 4 show the histograms of the S&P 500 daily close price, and corresponding log-returns respectively.

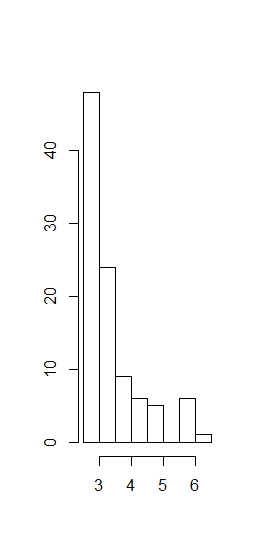

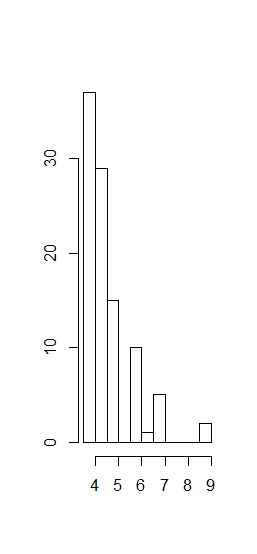

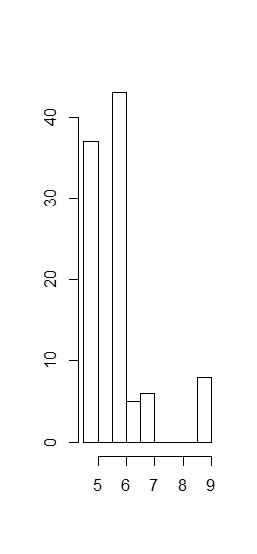

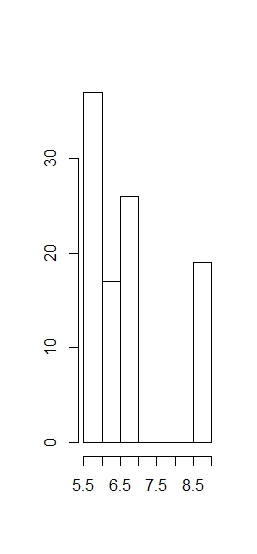

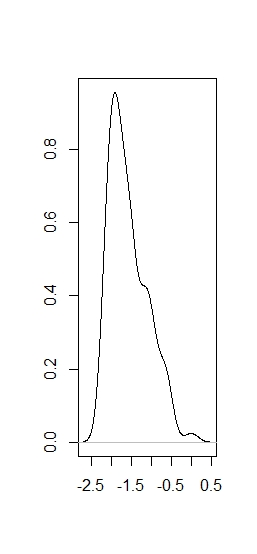

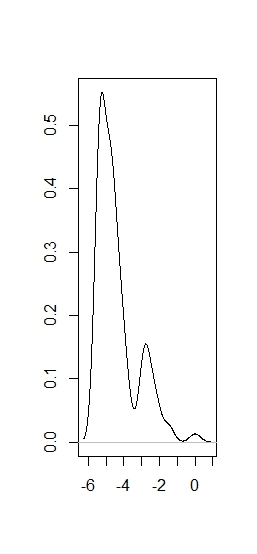

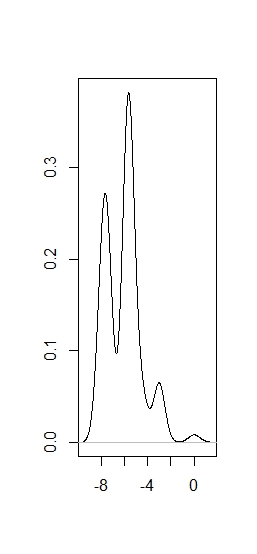

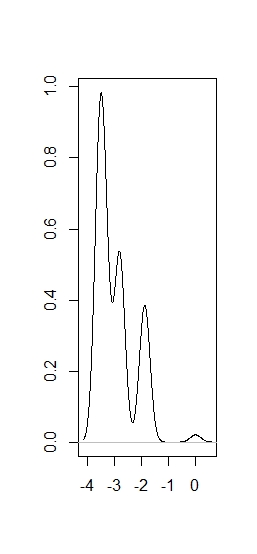

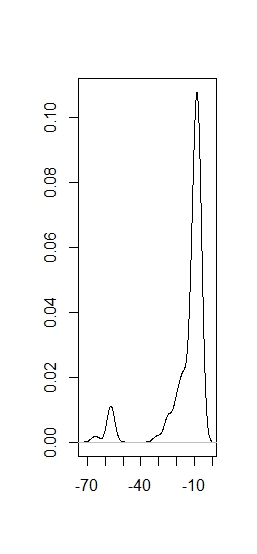

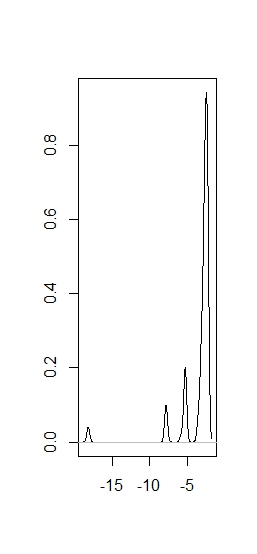

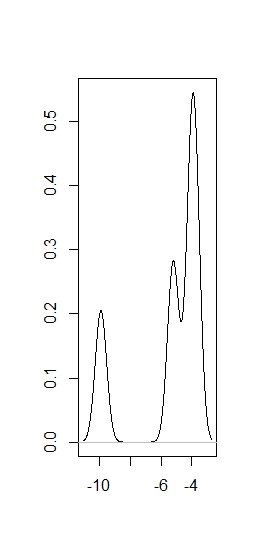

For the empirical dataset we consider the log-return process , with . For the first-exit time process of the log-return, , we consider the associated first-exit time processes of the Brownian motion , and the Lévy subordinator . In the plots in Figure 5, we provide the histograms corresponding to the first-exit time of for the empirical dataset for various values of . In the plots of Figure 6, we use Remark 3.3 to plot the probability density functions of , for . Finally, we use Gamma-type subordinators described in Section 4.2 with Lévy density .

After finding appropriate parameter values, in the plots of Figure 7, we use Theorem 4.8 to plot the probability density functions of , for . From these figures, it is clear that for the time duration when there is no big fluctuation of the empirical dataset, plays the dominant role in determining the distribution of . However, for the time duration of big fluctuation of the empirical dataset, plays the dominant role in determining the distribution of .

Figure 1: S&P 500 daily close price from May, 2010 -May, 2020.Figure 2: S&P 500 log-returns from May, 2010 -May, 2020.Figure 3: Histogram for the S&P 500 daily close price.Figure 4: Histogram for the log-return.Figure 5: Histograms corresponding to , for (left to right) .

Figure 6: Probability density functions of , for (left to right) .

Figure 7: Probability density functions of , for (left to right) .

6 Conclusion

It is shown in this paper that an analytically tractable expression can be obtained for the probability density function of the first-exit time process of an approximate BN-S process. For the financial data, the density function of the first-exit time of the corresponding log-return process provides an important insight. In particular, such density function facilitates the understanding of a “crash-like” future fluctuation of the market. In addition, this analysis has two-fold advantages. Firstly, based on the insight from the probability density function of the first-exit time process, the empirical data analysis for the future market is improved. Secondly, and more importantly, this provides a concrete way to improve existing stochastic models. For example, most of the existing financial models suffer from the lack of long-range dependence problem. An understanding of the density function of the first-exit time of stochastic models driven by a general Lévy process can contribute positively to mitigate this issue.

In the numerical results, we show various plots in support of the theoretical analysis provided in this paper. However, the analysis is dependent on the accurate estimation of model parameters for the empirical dataset. At present, we are implementing various machine learning based calibration techniques to improve the estimates of the parameter values for the empirical dataset. In effect, this may significantly improve the numerical results. These concepts, along with their connection to the first-exit time analysis, will be developed in a sequel of this paper.

References

[1]

[2] L. Alili and A. E. Kyprianou (2005), Some remarks on first passage of Lévy processes, the American put and pasting principles, he Annals of Applied Probability, 15(3), 2062-2080.

[3] D. Applebaum (2009), Lévy Processes and Stochastic Calculus, 2nd ed., Cambridge University Press, Cambridge, UK.

[4] L. Bachelier (1900), The Theory of Speculation, Ann. Sci. Éc. Norm. Supér., Serie 3, 17, 21-89 (Engl. translation by David R. May, 2011).

[5] O. E. Barndorff-Nielsen (2001), Superposition of Ornstein-Uhlenbeck Type Processes, Theory of Probability & Its Applications, 45, 175-194.

[6] O. E. Barndorff-Nielsen, J. L. Jensen and M. Srensen (1998), Some stationary processes in discrete and continuous time, Advances in Applied Probability, 30, 989-1007.

[7] O. E. Barndorff-Nielsen and N. Shephard (2001), Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics, Journal of the Royal Statistical Society: Series B (Statistical Methodology), 63, 167-241.

[8] O. E. Barndorff-Nielsen and N. Shephard (2001), Modelling by Lévy Processes for Financial Econometrics, In Lévy Processes: Theory and Applications (eds O. E. Barndorff-Nielsen, T. Mikosch & S. Resnick), 283-318, Birkhäuser.

[9] E. Bayraktar and C. W. Miller (2019), Distribution‐constrained optimal stopping, Mathematical Finance, 29(1), 368-406.

[10] J. Bertoin (1996), Lévy Processes, Cambridge University Press, Cambridge, UK.

[11] S. I. Boyarchenko and S. Z. Levendorskiĭ (2000), Option pricing for truncated Lévy processes. International Journal of Theoretical and Applied Finance, 3(3), 549-552.

[12] S. I. Boyarchenko and S. Z. Levendorskiĭ (2002), Non-Gaussian Merton-Black-Scholes Theory, volume 9 of Adv. Ser. Stat. Sci. Appl. Probab. World Scientific Publishing Co., River Edge, NJ, 2002.

[13] P. Carr, H. Geman, D. B. Madan and M. Yor (2007), Self-decomposability and option pricing, Mathematical Finance, 17 (1), 31-57.

[14] R. Dante DeBlassie (1990), The First Exit Time of a Two-Dimensional Symmetric Stable Process from a Wedge, Ann. Probab., 18 (3), 1034-1070.

[15] M. Dominé (1996), First passage time distribution of a Wiener process with drift concerning two elastic barriers, Journal of Applied Probability, 33 (1), 164-175.

[16] S. Habtemicael and I. SenGupta (2014), Ornstein-Uhlenbeck processes for geophysical data analysis, Physica A: Statistical Mechanics and its Applications, 399, 147-156.

[17] S. Habtemicael and I. SenGupta (2016), Pricing variance and volatility swaps for Barndorff-Nielsen and Shephard process driven financial markets, International Journal of Financial Engineering, 03 (04), 1650027 (35 pages).

[18] S. Habtemicael and I. SenGupta (2016), Pricing covariance swaps for Barndorff-Nielsen and Shephard process driven financial markets, Annals of Financial Economics, 11, 1650012 (32 pages).

[19] P. Hieber and M. Scherer (2012), A note on first-passage times of continuously time-changed Brownian motion, Statistics & probability Letters, 82(1), 165-172.

[20] P. Imkeller and I. Pavlyukevich (2006), First exit times of SDEs driven by stable Lévy processes, Stochastic Processes and their Applications, 116(4), 611-642.

[21] A. Issaka and I. SenGupta (2017), Analysis of variance based instruments for Ornstein-Uhlenbeck type models: swap and price index, Annals of Finance, 13(4), 401-434.

[22] J. Janssen and C.H. Skiadas (1995), Dynamic modelling of life-table data, Appl Stochastic Models Data Anal, 11(1), 35-49.

[23] S. G. Kou and H. Wang (2003), First passage times of a jump diffusion process, Advances in Applied Probability, 35(2), 504-531.

[24] A. Kumar and P. Vellaisamy (2015), Inverse tempered stable subordinators, Statistics & Probability Letters, 103, 134-141.

[26] M. Lifshits and Z. Shi (2002), The first exit time of Brownian motion from a parabolic domain, Bernoulli, 8 (6), 745-765.

[27] V. Linetsky (2004), Computing hitting time densities for CIR and OU diffusions: applications to mean-reverting models, Journal of Computational Finance, 7(4), 1-22.

[28] R. J. Martin, M. J. Kearney and R. V. Craster (2019), Long- and short-time asymptotics of the first-passage time of the Ornstein–Uhlenbeck and other mean-reverting processes, Journal of Physics A: Mathematical and Theoretical, 52 (13), https://doi.org/10.1088/1751-8121/ab0836.

[29] M. M. Meerschaert and H. Scheffler (2008), Triangular array limits for continuous time random walks, Stochastic Process. Appl., 118, 1606-1633.

[30] E. Nicolato and E. Venardos (2003), Option Pricing in Stochastic Volatility Models of the Ornstein-Uhlenbeck type, Mathematical Finance, 13, 445-466.

[31] C. Paroissin and L. Rabehasaina (2015), First and Last Passage Times of Spectrally Positive Lévy Processes with Application to Reliability, Methodol Comput Appl Probab, 17, 351-372.

[32] R. Patel, A. Carron and F. Bullo (2016), The Hitting Time of Multiple Random Walks, SIAM Journal on Matrix Analysis and Applications, 37(3), 933-954.

[33] G. E. Roberts and H. Kaufman (1966), Table of Laplace Transforms, W.B. Saunders, First Edition.

[34] M. Roberts and I. SenGupta (2020), Infinitesimal generators for two-dimensional Lévy process-driven hypothesis testing, Annals of Finance, 16 (1), 121-139.

[35] M. Roberts and I. SenGupta (2020), Sequential hypothesis testing in machine learning, and crude oil price jump size detection, To appear in Applied Mathematical Finance, Accepted on December, 2020.

[36] K-I. Sato (1999), Lévy Processes and Infinitely Divisible Distributions, Cambridge University Press.

[37] I. SenGupta (2014), Option Pricing with Transaction Costs and Stochastic Interest Rate, Applied Mathematical Finance, 21, 399-416.

[38] I. SenGupta (2016), Generalized BN-S stochastic volatility model for option pricing, International Journal of Theoretical and Applied Finance, 19 (02), 1650014 (23 pages).

[39] I. SenGupta, W. Nganje and E. Hanson (2020), Refinements of Barndorff-Nielsen and Shephard model: an analysis of crude oil price with machine learning, to appear in Annals of Data Science, https://doi.org/10.1007/s40745-020-00256-2.

[40] I. SenGupta, W. Wilson and W. Nganje (2019), Barndorff-Nielsen and Shephard model: oil hedging with variance swap and option, Mathematics and Financial Economics, 13(2), 209-226.

[41] H. Shoshi and I. SenGupta (2020), Hedging and machine learning driven crude oil data analysis using a refined Barndorff-Nielsen and Shephard model, submitted, https://arxiv.org/abs/2004.14862.

[42] C.H. Skiadas and C. Skiadas (2019), The First Exit Time Stochastic Theory Applied to Estimate the Life-Time of a Complicated System, Methodol Comput Appl Probab., https://doi.org/10.1007/s11009-019-09699-4

[43] D. Valenti, B. Spagnolo and G. Bonanno (2007), Hitting time distributions in financial markets, Physica A: Statistical Mechanics and its Applications, 382(1), 311-320.

[44] M. Veillette and M.S. Taqqu (2010), Using differential equations to obtain joint moments of first-passage times of increasing Lévy processes, Statist. Probab. Lett., 80, 697-705.

[45] M. Veillette and M.S. Taqqu (2010), Numerical computation of first-passage times of increasing Lévy Processes, Methodol. Comput. Appl. Probab., 12, 695-729.

[46] P. Vellaisamy and A. Kumar (2018), First-exit times of an inverse Gaussian process, Stochastics, 90 (1), 29-48.

[47] W. Wilson, W. Nganje, S. Gebresilasie and I. SenGupta (2019), Barndorff-Nielsen and Shephard model for hedging energy with quantity risk, High Frequency, 2 (3-4), 202-214.

[48] S. J. Wolfe (1982), On a continuous analogue of the stochastic difference equation , Stochastic Processes and their Applications, 12, 301-312.

[49] G. Xu and X. Wang (2020), On the Transition Density and First Hitting Time Distributions of the Doubly Skewed CIR Process, Methodology and Computing in Applied Probability, https://doi.org/10.1007/s11009-020-09775-0.