On weak conditional convergence of bivariate Archimedean and Extreme Value copulas, and consequences to nonparametric estimation

Abstract.

Looking at bivariate copulas from the perspective of conditional distributions and considering weak convergence of almost all conditional distributions yields the notion of weak conditional convergence. At first glance, this notion of convergence for copulas might seem far too restrictive to be of any practical importance - in fact, given samples of a copula the corresponding empirical copulas do not converge weakly conditional to with probability one in general. Within the class of Archimedean copulas and the class of Extreme Value copulas, however, standard pointwise convergence and weak conditional convergence can even be proved to be equivalent. Moreover, it can be shown that every copula is the weak conditional limit of a sequence of checkerboard copulas. After proving these three main results and pointing out some consequences we sketch some implications for two recently introduced dependence measures and for the nonparametric estimation of Archimedean and Extreme Value copulas.

Keywords

Archimedean copula, Extreme Value copula, Checkerboard copula, weak convergence, estimation, dependence measure

1. Introduction

Suppose that is a parametric class of bivariate copulas with for some and let denote the corresponding conditional distributions (Markov kernels), i.e., if are uniformly distributed on and has distribution function then . Many standard classes of copulas are not only continuous in the parameter with respect to pointwise/uniform convergence (see [10, 30]) but exhibit the even stronger property that if converges to then almost all conditional distributions converge weakly to . In the sequel we will refer to weak convergence of almost all conditional distributions as weak conditional convergence. It is straightforward to verify that (among many others) the family of Gaussian copulas and the family of -copulas exhibit the just mentioned continuity with respect to the parameter. Moreover, leaving the absolutely continuous setting, the same is true, e.g., for the Marshall-Olkin family.

Despite the afore-mentioned examples, at first glance, weak conditional convergence might seem as a concept far too restrictive to be of any practical importance outside the purely parametric setting. This impression is reinforced by the fact that given samples from a copula and letting denote the corresponding empirical copula (bivariate interpolation of the induced subcopula, see [30]) we do not have weak conditional convergence of to unless is completely dependent in the sense that random variable is a measurable function of random variable (see [26]).

As we will demonstrate in this contribution, however, within the class of Archimedean copulas and the class of Extreme Value copulas (neither of them being a parametric class of the afore-mentioned type) standard pointwise/uniform convergence and weak conditional convergence are even equivalent, a result having direct implications for the dependence measures and introduced in [36] and [9], respectively, as well as for the nonparametric estimation of Archimedean and Extreme Value copulas (see [1, 13, 14] and [15, 19]). We will show that convexity of the univariate ‘generating’ functions (the normalized generator in the Archimedean and the Pickands dependence function in the Extreme Value case) is the key property entailing weak conditional convergence. Additionally, building upon the theorems in [27] we will derive a universal approximation result with respect to weak conditional convergence and show that for every bivariate copula we can find a sequence of checkerboard copulas that converges weakly conditional to the copula .

The authors’ interest in studying convergence of Archimedean copulas was triggered by [4] where the authors among other things showed that pointwise/uniform convergence of a sequence of Archimedean copulas to an Archimedean copula is equivalent to convergence of the corresponding sequence of Kendall distribution functions. In our contribution we first derive a slightly modified version of this result (including the fact that we can have convergence of the copulas without having convergence of the corresponding generators in , see Theorem 4.1) and then go one step further (see Theorem 4.2) and prove the equivalence of six different notions of convergence (some involving the copulas, some the generators), weak conditional convergence being one of them.

The rest of this contribution is organized as follows: Section 2 gathers preliminaries and notations that will be used throughout the paper. In Section 3 we formally define weak conditional convergence, prove that checkerboard copulas are dense with respect to weak conditional convergence, and show that weak conditional convergence implies convergence with respect to the metric introduced in [36] but in general not vice versa. Section 4 derives the afore-mentioned equivalence of pointwise/uniform and weak conditional convergence within the family of Archimedean copulas in several steps. In Section 5 we prove an analogous characterization of convergence within the class of Extreme Value copulas. Direct consequences of these two main results to the estimation of Archimedean and Extreme Value copulas are sketched and illustrated via simulations in Section 6. Finally, we use the obtained results for estimating the recently introduced coefficient of correlation (see [5]) and compare the performance of the estimators incorporating or ignoring the Extreme Value/Archimedean information.

2. Notation and preliminaries

In the sequel we will let denote the family of all bivariate copulas. For each copula the corresponding doubly stochastic measure will be denoted by , i.e. for all , will denote the family of all doubly stochastic measures. For more background on copulas and doubly stochastic measures we refer to [10, 30]. For every metric space the Borel -field on will be denoted by .

In what follows Markov kernels will play a prominent role. A Markov kernel from to is a mapping such that for every fixed the mapping is (Borel-)measurable and for every fixed the mapping is a probability measure. Given two real-valued random variables on a probability space we say that a Markov kernel is a regular conditional distribution of given if holds -almost surely for every . It is well-known (see, e.g., [22, 25]) that for as above, a regular conditional distribution of given always exists and is unique for -a.e. . If has distribution function (in which case we will also write and let denote the corresponding probability measure on ) we will let denote (a version of) the regular conditional distribution of given and simply refer to it as Markov kernel of . If is a copula then we will consider the Markov kernel of automatically as mapping . Defining the -section of a set as the so-called disintegration theorem (see [22, 25]) yields

| (2.1) |

As a direct consequence, for every we get

for every , whereby denotes the Lebesgue measure on . For more background on conditional expectation and general disintegration we refer to [22, 25].

We call a copula completely dependent if there exists a -preserving transformation (i.e., a transformation fulfilling for every ) such that is a Markov kernel of . For more properties of complete dependence we refer to [26] as well as to [36] and the references therein.

Markov kernels can be used to define metrics stronger than the standard uniform metric , defined by

| (2.2) |

on . It is well known that the metric space is compact and that pointwise and uniform convergence of a sequence of copulas are equivalent (see [10, 37]). Following [36] and defining

| (2.3) | ||||

it can be shown that are metrics generating the same topology on . In the sequel we will mainly work with and refer to [11, 36] for more information on and . The metric space is complete and separable but not compact. Moreover, we have for every and is maximal if and only if is completely dependent. The metric was originally introduced in order to construct a dependence measure which, contrary to , is capable of separating independence and complete dependence. The resulting -based dependence measure introduced in [36] is defined as

| (2.4) |

for every . In the sequel we will also consider the dependence measure introduced in [9] as

| (2.5) |

It is straightforward to verify that can be expressed in terms of and that holds. Both and attain values in , are if, and only if , and if, and only if is completely dependent.

A symmetric version of -convergence (or, equivalently, -converence) was introduced by Mikusiński and Taylor in [29] under the name -convergence: A sequence -converges to a copula ( for short) if and only if

We will see in the next section that in general weak conditional convergence does not imply -converges (Example 3.4) nor vice versa. For a thorough survey of different notions on convergence of copulas we refer to [35].

3. Weak conditional convergence and checkerboards

Sticking to the idea of viewing bivariate copulas in terms of their conditional distributions and considering weak convergence gives rise to what we refer to as weak conditional convergence in the sequel:

Definition 3.1.

Suppose that are copulas and let be (versions of) the corresponding Markov kernels. We will say that converges weakly conditional to if and only if for -almost every we have that the sequence of probability measures on converges weakly to the probability measure . In the latter case we will write (where ‘wcc’ stands for ‘weak conditional convergence’).

As already mentioned in the Introduction, many standard parametric classes of copulas depend on the parameter weakly conditional in the sense that if converges to then the corresponding sequence converges weakly conditional to . This is obviously true for parametric classes of absolutely continuous copulas whose corresponding densities have the property that if converges to then converges to -almost everywhere (whereby denotes the two-dimensional Lebesgue measure on ). In fact, in this case the corresponding Markov kernels are given by

| (3.1) |

and if we let denote the set of all points fulfilling then disintegration yields for -almost every , so the property follows immediately. It is straightforward to verify that (among many others) the family of Gaussian copulas and the family of -copulas fulfill this property.

The same is true for other, not necessarily absolutely continuous classes like the Marshall-Olkin family (see [7, 10, 30]) given by

| (3.2) |

According to [36] the corresponding Markov kernel is given by

| (3.3) |

and it is straightforward to verify that if the parameter vector converges to then we also have .

Before focusing on the Archimedean and the Extreme Value setting we prove a general approximation result saying that the class of checkerboard copulas is dense in w.r.t. weak conditional convergence (see Theorem 3.2). Recall that a copula is called a checkerboard copula with resolution if and only if distributes its mass uniformly on each rectangle with . We will refer to as the family of all checkerboard copulas with resolution , the set is called the class of all checkerboard copulas (checkerboards for short). For every the (unique) checkerboard copula fulfilling

for all will be referred to as -checkerboard approximation of the copula .

It is well-known that the class of checkerboard copulas is dense in and in , see [10, 27, 36]. The following theorem implies these two interrelations:

Theorem 3.2.

Given a copula , there is a sequence of elements of that converges to with respect to weak conditional convergence. In other words, is dense in with respect to weak conditional convergence.

Proof.

Fix and suppose that is a Markov kernel of . We are going to show that converges weakly conditional to . Using Lipschitz continuity of copulas in each coordinate, for every of the form with and there exists a set with the following three properties:

-

(1)

For every the function is differentiable at and fulfills ,

-

(2)

,

-

(3)

.

Letting denote the set of all points of the form with and

it follows that is countably infinite, hence setting

yields .

Consider and . For every there exists exactly one index

with

Considering that is constant on the interval disintegration yields

from which we directly get

Since was arbitrary we have shown that for each the conditional distribution functions converge to for every , i.e., on a dense set. Having this, weak conditional convergence of to follows immediately. ∎

We conclude this section with an example clarifying the interrelation between the afore-mentioned notions of convergence: According to Lemma 7 in [36] weak conditional convergence of to implies convergence w.r.t. . Additionally, convergence w.r.t. implies convergence in but not vice versa. The following simple example shows that we can have -convergence without having weak conditional convergence.

Example 3.3.

Let and . Define the copula via its Markov kernel by

Then does not converge weakly conditional to since for every the probability measure is, on the one hand, degenerated for infinitely many and, on the other hand, coincides with restricted to infinitely many times too. Nevertheless converges to w.r.t. since

holds and if goes to infinity then so does .

We conclude this section with an example showing that, in contrast to convergence w.r.t. to , neither convergence w.r.t. nor weak conditional convergence is a symmetric concept, i.e., considering Markov kernels instead of , may yield a different notion of convergence (as usual denotes the transpose of , i.e. ).

Example 3.4.

For every define the -preserving transformation by

and let denote the corresponding completely dependent copula. Since is the (discrete) uniform distribution on , converges weakly to for -almost every and we have

implying that converges to w.r.t. . Additionally (see [36, Theorem 14]) holds for every from which it follows immediately that does not converge to neither weakly conditional nor w.r.t. . It can even be shown that does not converge in at all: If would converge to some copula w.r.t. then according to [36, Proposition 15]) would be completely dependent, i.e., there would be some -preserving transformation such that holds. Considering that -convergence implies -convergence would follow, a contradiction since is singular whereas is absolutely continuous.

4. Archimedean copulas

Recall that a generator of a bivariate Archimedean copula (see [30]) is a convex and strictly decreasing function with . Every generator induces a copula via

| (4.1) |

where denotes the pseudoinverse of defined by

| (4.2) |

where denotes the respective one-sided limit. We refer to as the Archimedean copula induced by and call strict if and non-strict otherwise. In what follows will denote the family of all bivariate Archimedean copulas.

Since is convex obviously holds. Defining the right-continuous version of by

it is straightforward to verify that and generate the same copula. In other words, the value of at is irrelevant and we may, without loss of generality, from now on assume that all generators are right-continuous at . Additionally, since for every generator and every constant we have that generates the same copula we will from now on also assume (without explicit reference) that the generator is normalized in the sense that holds.

Following [12, 30] we define the -level set of the Archimedean copula by

and the -level function by implying that

holds for every .

For every generator we will let () denote the right-hand (left-hand) derivative of at . Convexity of implies that holds for all but at most countably many , i.e. is differentiable outside a countable subset of , and that is non-decreasing and right-continuous (see [23, 32]). In the sequel we will let denote the set of all continuity points of in (by definition, and are not contained in and make use of the fact that is at most countably infinite and has Lebesgue measure . Setting in case of strict as well as (for strict and non-strict ) allows to view as non-decreasing and right-continuous function on the full unit interval . Additionally (again see [23, 32]) we have for every .

If is strict then according to [12]

| (4.3) |

is (a version of) the Markov kernel of , if is non-strict, then

| (4.4) |

is a (version of a) Markov kernel of . Recall that for every Archimedean copula with generator the Kendall distribution function is given by (see, e.g., [14])

| (4.5) |

We now prove in several steps that in weak conditional convergence and pointwise convergence coincide. The following theorem serves as starting point for this result. Up to a slight modification this intermediate theorem was already established by Charpentier and Segers in [4], however, the slight modification will turn out to be crucial in the sequel.

Theorem 4.1.

Let be Archimedean copulas with generators , respectively. Then the following conditions are equivalent:

-

(a)

for all ,

-

(b)

for all Cont,

-

(c)

for all ,

-

(d)

for all Cont.

Proof.

The equivalence of (a) and (b) can be found in [4, Proposition 2] and the equivalence of (a) and (c) is contained in [24, Theorem 8.14] where the authors prove equivalence of pointwise convergence of the sequence of multiplicative generators and the pointwise convergence of the induced continuous Archimedean -norms which readily translates to the copula setting. The fact that (c) implies (d) is a direct consequence of the convexity of the generators, see [33].

Finally, suppose that (d) holds and consider . For every we can find an index such that for all we have . Using monotonicity of we get

for and every . Having this, Dominated convergence yields

for every . Considering that is dense in condition (c) now follows immediately. ∎

The afore-mentioned modification of the result in [4] is that it may happen that a sequence of Archimedean copulas converges to an Archimedean copula although the corresponding generators do not converge to in the point .

We now state the main result of this section saying that pointwise convergence and weak conditional convergence coincide in :

Theorem 4.2.

Let be Archimedean copulas with generators , respectively. Then the following assertions are equivalent:

-

(a)

for all ,

-

(b)

for all Cont,

-

(c)

for all ,

-

(d)

for all Cont,

-

(e)

,

-

(f)

for .

Remark 4.3.

We are now going to prove Theorem 4.2 by showing that each of the conditions (a) to (d) from Theorem 4.1 implies weak conditional convergence. Doing so we will work with level curves and distinguish two cases concerning the -level curve of the limit copula. For the first case, we present two different proofs since they use different ideas - the first one builds upon convexity of the generators and direct consequences to the sequence of derivatives, the second one uses some additional information about the behaviour of the corresponding sequence of level curves as described in the next lemma:

Lemma 4.4.

Let be non-strict Archimedean copulas with generators , respectively. If converges pointwise to on then the following two assertions hold:

-

(i)

,

-

(ii)

for every and every .

Proof.

To prove assertion (i) we proceed as follows: Considering that for every generator and every by convexity we have and applying Theorem 4.1 to the case yields

Since for every we can choose in such a way that holds assertion (i) now follows. To prove assertion (ii) fix and consider . In this case we have implying that there exists an index such that , hence , holds for every . It follows that from which the assertion follows immediately since was arbitrary. ∎

We now use the previous result to show level curve convergence:

Lemma 4.5.

Let be Archimedean copulas with generators converging pointwise on . Then for every the -level curves converge pointwise, i.e.,

| (4.6) |

holds for all . If, in addition, holds then eq. (4.6) is also true for and .

Proof.

Suppose that . As a by-product of [24, Theorem 8.14] we obtain uniform convergence of the sequence

to on each compact interval of the form with .

Fix , set and define

. Then converges to for

and, using the afore-mentioned uniform convergence of

on , the equality follows.

Notice that the second assertion is trivial for strict , so it remains to prove the assertion for . Fix . If then the result follows directly from Lemma 4.4 part (ii).

Suppose therefore that . Then for every

we have and we can find an index

such that , hence , holds for every .

As direct consequence we get , which in combination

with Lemma 4.4 assertion (ii) yields

This completes the proof. ∎

Recall that for univariate distribution functions weak convergence of to is equivalent to pointwise convergence on a dense subset (see, e.g., [2]). In the following two lemmata we prove convergence on a dense set above and below the zero level curve of the limit copula . Notice that the first lemma is sufficient within the family of strict Archimedean copulas since in this case for every .

Lemma 4.6.

Let be Archimedean copulas with generators and assume that one of the conditions of Theorem 4.1 holds. Then there exists a set fulfilling such that for every we have that

| (4.7) |

holds for every , where is dense in .

Proof (1).

Setting we obviously have . We are going to prove the even stronger property that for every the identity

| (4.8) | ||||

holds for -almost all . First of all notice that the set

is of full measure in . In fact, for the function , defined by is an increasing homeomorphism (see [30]) and therefore the set is at most countably infinite. Convexity of the generators implies that the sequence of derivatives converges continuously to on Cont (see [33]), hence we obtain

from which the desired property follows. ∎

Proof (2).

First of all notice that for we have

| (4.9) |

and the right-hand side converges to by Theorem 4.1. Exploiting this fact we consider and proceed as follows: Fix again and let denote a continuity point of the map . Furthermore choose with in such a way that and holds. According to Lemma 4.5 there exists some index such that for all we have , which using eq. (4.6) implies

As a direct consequence we get

Replacing by and proceeding analogously yields

which completes the proof. ∎

As second step we consider the case (implying that is non-strict). The following simple lemma will be crucial for the proof of Lemma 4.8:

Lemma 4.7.

Suppose that is a compact metric space and that is another (not necessarily compact) metric space. Furthermore let be an arbitrary function and a sequence in . If there exists some such that for every convergent subsequence we have then follows.

Proof.

Suppose that the assumptions of the lemma are fulfilled but the sequence with does not converge to for . In this case there exists some and a subsequence with for every . Compactness of implies the existence of a subsequence of , and, by assumption, this sequence fulfills

a contradiction. ∎

To simplify notation we say that if, and only if for every there exists some index such that for all we have . Lemma 4.4 part (i) together with Lemma 4.7 allow us to distinguish the following three types of convergent subsequences of : (a) , (b) or (c) .

Lemma 4.8.

Let be Archimedean copulas with generators and assume that one of the conditions of Theorem 4.1 holds. Then there exists a set fulfilling such that for every we have that

| (4.10) |

holds for every .

Proof.

As in the previous proof we set .

Fix Cont and and distinguish the following two different situations:

(a) Suppose that is a subsequence of

fulfilling .

According to Lemma 4.5 we have , so there exists an index such that , hence ,

holds for every , from which follows immediately.

(b) & (c) Suppose that is a subsequence of

fulfilling or .

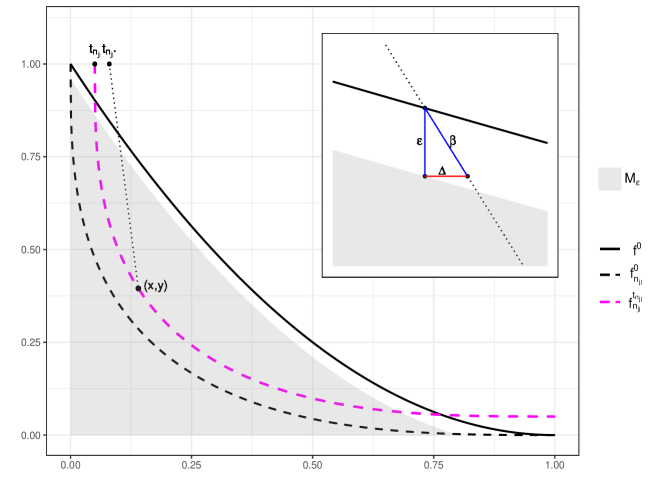

Choose in such a way that holds and define the set (see Figure 2) by

Then and is a -continuity set, so applying Portmanteau’s theorem (see [2]) yields

| (4.11) |

Assume now that there exists some such that would hold for infinitely many and denote the corresponding subsequence by . It follows from eq. (4.4) that holds for every . Set for every and let denote the smallest index fulfilling that holds for all . Using the fact that for every Archimedean copula with generator and for every the mapping

is decreasing in it follows that for every we have

for every . The proof idea now is to use this monotonicity in combination with convexity of the level curves (see [30]) to construct a contradiction to eq. (4.11): In fact, convexity implies that the graph of each restricted to lies below the straight line connecting the points and (again see Figure 2). Hence, defining by

| (4.12) |

it follows that for every we have . As direct consequence it follows that

holds for every which contradicts eq. (4.11).

Altogether in case (b) & (c) we have also shown now that holds.

Taking (a) and (b) & (c) together we have proved that for each convergent subsequence

of we have

The result now follows from Lemma 4.7. ∎

Considering that weak conditional convergence of the copulas implies convergence in the proof of this section’s main result Theorem 4.2 is complete. In Section 6 we will use the following interesting consequence:

Corollary 4.9.

Let be Archimedean copulas with generators , respectively and suppose that converges to on . Then the following identities holds:

| (4.13) |

In other words: Within both and are continuous w.r.t. pointwise convergence of the generators on .

We conclude this section by recalling the fact that the class of Archimedean copulas is not closed w.r.t. uniform convergence, i.e., the limit of a sequence of Archimedean copulas may fail to be Archimedean, see [4] (however, we necessarily have associativity). As easily verified, the same is true if we consider weak conditional convergence or convergence w.r.t. .

5. Extreme Value copulas

We are now going to prove a result similar to Theorem 4.2 for bivariate Extreme Value copulas. Remember that is called bivariate Extreme Value copula if one of the following three equivalent conditions is fulfilled (see [8, 10, 18, 31]):

-

(a)

There is a copula such that for all we have

(5.1) -

(b)

holds for all and all .

-

(c)

There exists a convex map satisfying and for all such that for all the copula can be expressed in terms of as

(5.2)

In the following we will let denote the class of all bivariate Extreme Value copulas, the family of all Pickands dependence functions, i.e., the family of all functions fulfilling assertion (c). Using either max-stability or Arzela-Ascoli theorem [34] it is straightforward to verify that is a compact subset of . Furthermore, letting denote the uniform norm on , obviously the mapping , defined by , is continuous and it is straightforward to verify that a sequence of Extreme Value copulas converges pointwise (hence uniformly) to an Extreme Value copula if, and only if converges uniformly to .

Following [38] we will let denote the right-hand derivative of the Pickands dependence function on and the left-hand derivative on . Furthermore, convexity implies that holds for all but at most countably infinitely many . In the sequel we will let denote the set of all continuity points of in . Setting we can view as a function on the whole unit interval that attains values in . Furthermore is a non-decreasing, right-continuous function and it is straightforward to verify that can be identified with , defined by

in the sense that for every we have and, given setting yields as well as on (see [38]). For more information on Pickands dependence functions and the approach via right-hand derivatives we refer to [3, 16].

Returning to weak conditional convergence first notice that according to [38]

| (5.3) |

is a Markov kernel of the Extreme Value copula with Pickands dependence function .

We now state the main result of this section saying that in pointwise convergence and weak conditional convergence are equivalent:

Theorem 5.1.

Let be Extreme Value copulas with Pickands dependence functions , respectively. Then the following assertions are equivalent:

-

(a)

for all ,

-

(b)

for all ,

-

(c)

for all Cont,

-

(d)

,

-

(e)

for .

Remark 5.2.

Since for every Extreme Value copula its transpose is an Extreme Value copula with Pickands dependence function given by for every it follows that in the class of bivariate Extreme Value copulas the properties and are equivalent. As a consequence of Theorem 5.1 (and in contrast to Remark 3.5) weak conditional convergence and -convergence are therefore equivalent in .

Theorem 5.1 is a direct consequence of the following analogue of Lemma 4.6 and Lemma 4.8 (notice that the result implies weak conditional convergence for ANY choice of the Markov kernels):

Lemma 5.3.

Let be bivariate Extreme Value copulas with Pickands dependence functions , respectively. Suppose that converges pointwise to and choose the corresponding kernels according to (5.3). Then for every there exists a set that is dense in such that

| (5.4) |

holds for every .

Proof.

If converges pointwise to then, as mentioned before, it follows that holds. Thus (as in the case of Archimedean generators) convexity yields

for every . Defining for every by

| (5.5) |

yields a strictly increasing homeomorphism of . Since is at most countably infinite is as well and

follows. Being a set of full measure is dense in and the result follows. ∎

Altogether we have proved Theorem 5.1 which, in turn, has the following corollary:

Corollary 5.4.

Let be Extreme Value copulas with Pickands dependence functions , respectively and suppose that converges to on . Then the following identities holds:

| (5.6) |

In other words: Within both and are continuous w.r.t. pointwise convergence of the Pickands dependence functions.

We conclude this section with the following remark:

Remark 5.5.

Suppose that are the continuous bivariate distribution functions of the pairs , with corresponding marginal distribution functions and and corresponding copulas . Defining analogously to Definition 3.1 (notice that in this case is replaced by ) it is straightforward to verify that implies but not necessarily vice versa. In the case that all are Extreme Value copulas and the Pickands function of the limit copula is twice differentiable, however, the reverse implication also holds. In the class the two concepts are equivalent too if, for instance, all generators are -monotone.

6. Consequences for the estimation of Archimedean and Extreme Value copulas

6.1. Extreme Value copulas

Suppose that is an Extreme Value copula with Pickands function and suppose that is a random sample from . Letting denote the CFG estimator according to [3, 15] (for an estimator in the multivariate setting see [19]) it can be shown that if is twice continuously differentiable then the corresponding process (in the space of of all continuous functions on the unit interval) has a weak limit, and that, for suitable weight functions, is uniformly, strongly consistent (see [3, Proposition 4.1]). Although the estimator may fail to be convex in general, following an idea from [15] it can be used to construct a convex estimator given by

where id denotes the identity function on . is a Pickands dependence function (see [15, Section 3.3]) and the estimator is uniformly, strongly consistent (the latter follows from [28]). Hence Theorem 5.1 directly yields weak conditional convergence of the sequence of corresponding Extreme Value copulas to Moreover, according to Corollary 5.4

holds and the same is true for the dependence measure studied in [9], i.e., for estimating it suffices to have a good estimator of the Pickands dependence function (we refer to [21] for more details concerning the estimation of ).

Example 6.1.

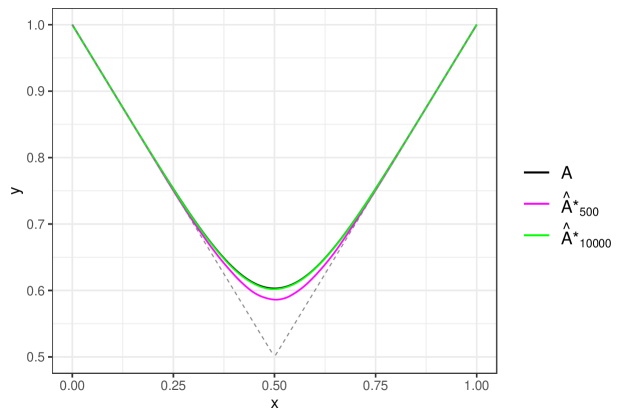

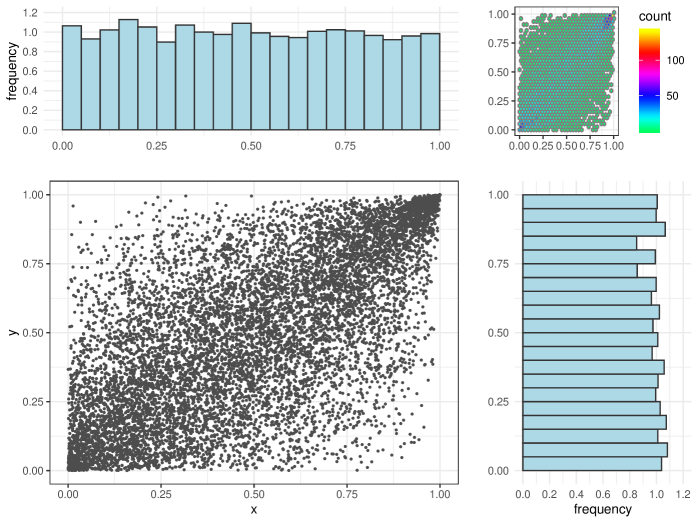

Consider the Galambos copula with parameter , i.e., the Extreme Value copula whose Pickands dependence function is given by . Figure 3 depicts a sample (and corresponding histograms) for the case .

Using the R-package ‘copula’ we calculate the estimator of as described above. Figure 4 depicts the obtained generators together with the true Pickands function . For the dependence measure (again using the R-package ‘qad’) we obtained the following values: .

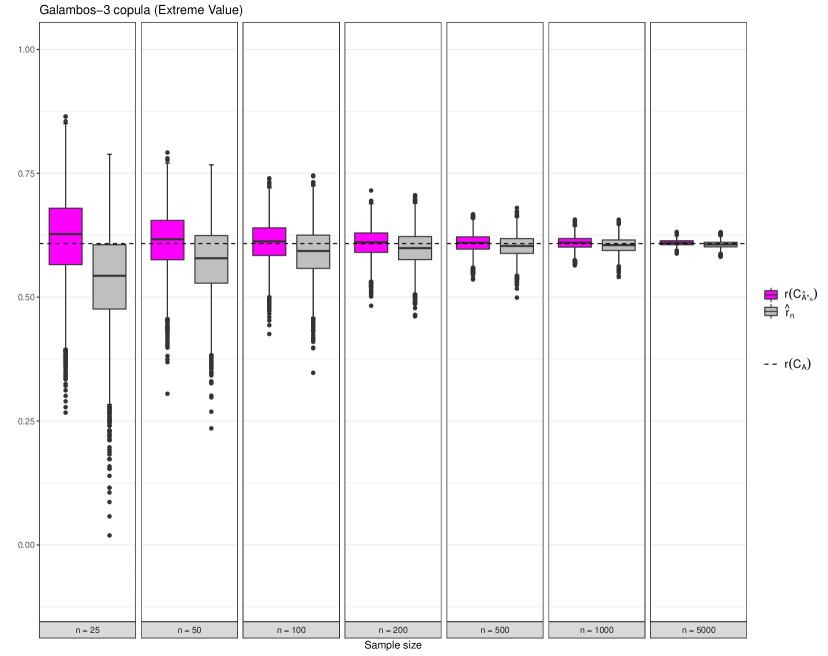

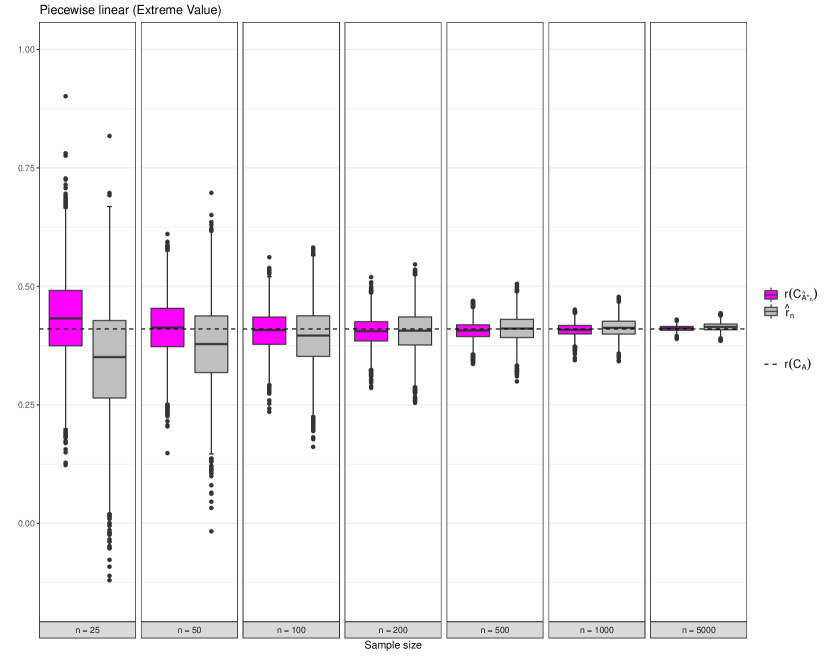

We now focus on the estimation of introduced in [9], denote the estimator of developed by Chatterjee in [5] by (for an implementation see the R-package ‘XICOR’ [6]) and proceed with a small simulation study comparing the afore-mentioned plugin approach (using the Extreme Value information) with (not taking into account the Extreme Value information). In other words: Given a random sample , from we calculate and for different sample sizes a total of times. Doing so we consider two cases of : the Galambos copula with parameter and the Extreme Value copula with piecewise linear Pickands dependence function given by

| (6.1) |

6.2. Archimedean copulas

Turning to the Archimedean setting suppose now that is an Archimedean copula with generator and let be a random sample from . We will let denote the estimator of the Kendall distribution function of called in [13, Lemma 1]. According to [13] (also see [1, 14]), itself is a Kendall distribution function of an Archimedean copula and under mild regularity conditions the so-called empirical Kendall process converges weakly to a centered Gaussian process. If converges weakly to (to the best of authors’ knowledge no sufficient conditions for this property to hold are known in the literature) then, according to Theorem 4.2, we automatically have weak conditional convergence of the sequence of corresponding Archimedean copulas to , whereby denotes the (normalized) generator obtained from . Moreover, according to Corollary 4.9

holds and the same is true for the dependence measure studied in [9], i.e., for estimating it suffices to have a good estimator of the Kendall distribution function .

Example 6.2.

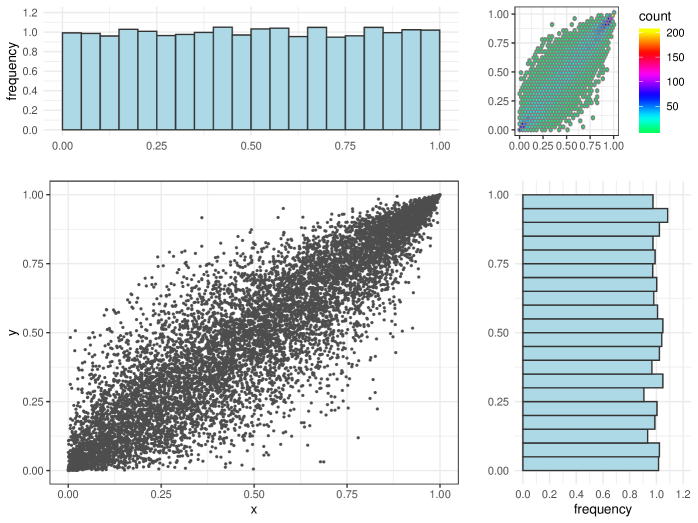

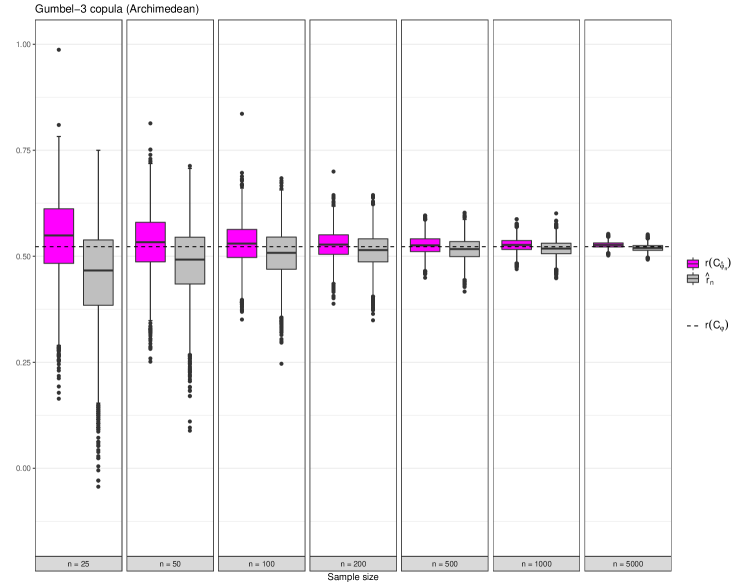

We illustrate the afore-mentioned properties with simulations in R and consider the (normalized) generator of the Gumbel copula with parameter . Figure 7 depicts a sample of size from this copula as well as a two-dimensional and the corresponding marginal histograms.

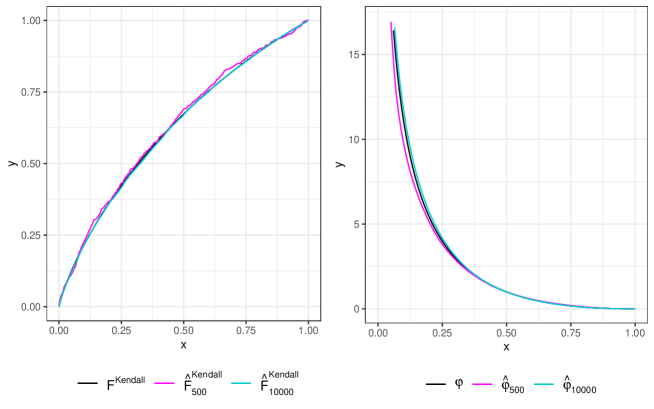

For both samples we use the R-package ‘copula’ (see [20]) to estimate the empirical Kendall distribution function as described in [13]. Figure 8 (left panel) depicts the real as well as the estimated Kendall distribution function for the sample sizes and , respectively.

As in the Extreme Value setting we perform a small simulation study comparing the performance of the plugin estimator with the estimator of the coefficient of correlation (ignoring the Archimedean information). Generating samples of the Gumbel copula with parameter , calculating as well as for these samples and repeating this procedure times yielded the results depicted in Figure 9. Not surprisingly, for small to moderate sample sizes the plugin estimator outperforms the general estimator , for large sample sizes both estimators perform comparably well.

Acknowledgements

The first author gratefully acknowledges the financial support from Porsche Holding Austria and

Land Salzburg within the WISS 2025 project ‘KFZ’ (P1900123).

Moreover, the second and the third author gratefully acknowledge the support of the WISS 2025 project ‘IDA-lab Salzburg’ (20204-WISS/225/197-2019 and 0102-F1901166-KZP).

References

- Barbe et al. [1996] Barbe, P., C. Genest, K. Ghoudi, and B. Rémillard (1996). On Kendall’s process. J. Multivariate Analysis 58(2), 197 – 229.

- Billingsley [2013] Billingsley, P. (2013). Convergence of Probability Measures. Wiley Series in Probability and Statistics. Wiley.

- Capéraà et al. [1997] Capéraà, P., A.-L. Fougéres, and C. Genest (1997). A nonparametric estimation procedure for bivariate extreme value copulas. Biometrika 84, 567–577.

- Charpentier and Segers [2008] Charpentier, A. and J. Segers (2008). Convergence of Archimedean copulas. Statist. Probab. Lett. 78, 412–419.

- Chatterjee [2020a] Chatterjee, S. (2020a). A new coefficient of correlation. Journal of the American Statistical Association 0(0), 1–21.

- Chatterjee [2020b] Chatterjee, S. (2020b). XICOR: Association Measurement Through Cross Rank Increments. R package version 0.3.3.

- Cherubini et al. [2013] Cherubini, U., F. Durante, and S. Mulinacci (2013). Marshall-Olkin Distributions - Advances in Theory and Applications. Springer International Publishing Switzerland: Springer Proceedings in Mathematics & Statistics.

- de Haan and Resnick [1977] de Haan, L. and S. Resnick (1977). Limit theorem for multivariate sample extremes. Z. für Wahrscheinlichkeitstheorie 40, 317–337.

- Dette et al. [2013] Dette, H., K. Siburg, and P. Stoimenov (2013). A Copula-Based Non-parametric Measure of Regression Dependence. Scand. J. Stat. 40, 21–41.

- Durante and Sempi [2016] Durante, F. and C. Sempi (2016). Principles of copula theory. Boca Raton FL: Taylor & Francis Group LLC.

- Fernández Sánchez and Trutschnig [2015a] Fernández Sánchez, J. and W. Trutschnig (2015a). Conditioning based metrics on the space of multivariate copulas, their interrelation with uniform and levelwise convergence and Iterated Function Systems. J. Theoret. Probab. 28, 1311–1336.

- Fernández Sánchez and Trutschnig [2015b] Fernández Sánchez, J. and W. Trutschnig (2015b). Singularity aspects of Archimedean copulas. J. Math. Anal. Appl. 432, 103–113.

- Genest et al. [2011] Genest, C., J. Nešlehová, and J. Ziegel (2011). Inference in multivariate Archimedean copula models. Test 20, 223.

- Genest and Rivest [1993] Genest, C. and L. Rivest (1993). Statistical inference procedures for bivariate Archimedean copulas. J. Amer. Stat. Assoc. 88, 1034–1043.

- Genest and Segers [2009] Genest, C. and J. Segers (2009). Rank-based inference for bivariate extreme-value copulas. Annals of Statistics 37, 2990–3022.

- Ghoudi et al. [1998] Ghoudi, K., A. Khoudraji, and L.-P. Rivest (1998). Propriétés statistiques des copules de valeurs extremes bidimensionnelles. Canad. J. Statist. 26, 187–197.

- Griessenberger et al. [2020] Griessenberger, F., R. R. Junker, and W. Trutschnig (2020). qad: Quantification of Asymmetric Dependence. R package version 0.1.2.

- Gudendorf and Segers [2010] Gudendorf, G. and J. Segers (2010). Extreme-value copulas. In P. Jaworski, F. Durante, K. Härdle, and T. Rychlik (Eds.), Copula Theory and Its Applications, Chapter 6, pp. 127–145. Heidelberg: Springer, Berlin, Heidelberg.

- Gudendorf and Segers [2011] Gudendorf, G. and J. Segers (2011). Nonparametric estimation of an extreme-value copula in arbitrary dimensions. J. Multivariate Analysis 102(1), 37 – 47.

- Hofert et al. [2020] Hofert, M., I. Kojadinovic, M. Maechler, and J. Yan (2020). copula: Multivariate Dependence with Copulas. R package version 0.999-20.

- Junker et al. [2020] Junker, R. R., F. Griessenberger, and W. Trutschnig (2020). Estimating scale-invariant directed dependence of bivariate distributions. Computational Statistics & Data Analysis 153(0), 0.

- Kallenberg [2002] Kallenberg, O. (2002). Foundations of modern probability. New York: Springer-Verlag.

- Kannan and Krueger [2012] Kannan, R. and C. Krueger (2012). Advanced Analysis: on the Real Line. Universitext. Springer New York.

- Klement et al. [2000] Klement, E., R. Mesiar, and E. Pap (2000). Triangular Norms (8 ed.). Springer Netherlands.

- Klenke [2008] Klenke, A. (2008). Wahrscheinlichkeitstheorie. Berlin Heidelberg: Springer Lehrbuch Masterclass Series.

- Lancaster [1963] Lancaster, H. O. (1963, 12). Correlation and complete dependence of random variables. Ann. Math. Statist. 34(4), 1315–1321.

- Li et al. [1998] Li, X., P. Mikusinski, and M. Taylor (1998). Strong approximation of copulas. J. Math. Anal. Appl. 255, 608–623.

- Marshall [1970] Marshall, A. W. (1970). Discussion of barlow and van zwet’s papers. In M. L. Puri (Ed.), Nonparametric Techniques in Statistical Inference, pp. 175–176. London: Cambridge University Press.

- Mikusiński and Taylor [2010] Mikusiński, P. and M. Taylor (2010). Some approximations of n-copulas. Metrika (72), 385–414.

- Nelsen [2006] Nelsen, R. (2006). An Introduction to Copulas. Berlin Heidelberg: Springer-Verlag.

- Pickands [1981] Pickands, J. (1981). Multivariate extreme value distributions. Proceedings 43rd Session International Statistical Institute 2, 859–878.

- Pollard [2001] Pollard, D. (2001). A User’s Guide to Measure Theoretic Probability. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press.

- Rockafellar [1970] Rockafellar, R. (1970). Convex Analysis. Princeton Landmarks in Mathematics and Physics. Princeton University Press.

- Rudin [1987] Rudin, W. (1987). Real and Complex Analysis, 3rd Ed. USA: McGraw-Hill, Inc.

- Sempi [2004] Sempi, C. (2004). Convergence of copulas: Critical remarks. Radovi Matematički 12, 241–249.

- Trutschnig [2011] Trutschnig, W. (2011). On a strong metric on the space of copulas and its induced dependence measure. J. Math. Anal. Appl. 384, 690–705.

- Trutschnig [2012] Trutschnig, W. (2012). Some results on the convergence of (quasi-) copulas. Fuzzy Sets and Systems 191, 113–121.

- Trutschnig et al. [2016] Trutschnig, W., M. Schreyer, and J. Fernández Sánchez (2016). Mass distribution of two-dimensional extreme-value copulas and related results. Extremes 19, 405–427.