False (and Missed) Discoveries in Financial Economics

Multiple testing plagues many important questions in finance such as fund and factor selection. We propose a new way to calibrate both Type I and Type II errors. Next, using a double-bootstrap method, we establish a -statistic hurdle that is associated with a specific false discovery rate (e.g., 5%). We also establish a hurdle that is associated with a certain acceptable ratio of misses to false discoveries (Type II error scaled by Type I error), which effectively allows for differential costs of the two types of mistakes. Evaluating current methods, we find that they lack power to detect outperforming managers.

Keywords: Type I, Type II, Multiple testing, False discoveries, Odds ratio, Power, Mutual funds, Anomalies, Bayesian, Factors, Backtesting, Factor Zoo

In manager selection (or, equivalently, the selection of factors or trading strategies), investors can make two types of mistakes. The first involves selecting a manager who turns out to be unskilled — this is a Type I error, or a false positive.111Throughout our paper, we follow the empirical literature on performance evaluation and associate manager skill with alpha. In particular, we take skilled managers to be those that generate positive alpha. Our notion of manager skill is thus different from that in Berk and Green (2004), where skilled managers generate a zero net alpha in equilibrium. The second error is not selecting or missing a manager that the investor thought was unskilled but was not — this is a Type II error, or a false negative. Both types of errors display economically important variation. On the false positives side, for instance, one manager might slightly underperform while another manager might have a large negative return. Moreover, the cost of a Type II error is likely different from the cost of a Type I error, with the costs depending on the specific decision at hand. However, while an investor may want to pick managers using the criterion that Type I errors are, say, five times more costly than Type II errors, current tools do not allow for such a selection criterion. On the one hand, current methods ignore the Type II error rate, which may lead us to miss outperforming managers. On the other hand, it is difficult to simply characterize Type I errors because of multiple testing — using a single-hypothesis testing criterion (e.g., two standard errors from zero) will lead to massive Type I errors because, when there are thousands of managers, many will look good (i.e., appear to outperform) purely by luck. Statisticians have suggested a number of fixes that take multiple testing into account. For example, the simplest is the Bonferroni correction, which multiplies each manager’s -value by the number of managers. But this type of correction does not take the covariance structure into account. Further, it is not obvious what the Type I error rate would be after implementing the correction. We know that the error rate would be less than that under a single testing criterion –- but how much less?

In this paper we propose a different approach. Using actual manager data, we first determine the performance threshold that delivers a particular Type I error rate (e.g., 5%). We next characterize the Type II error rate associated with our optimized Type I error rate. It is then straightforward to scale the Type II error by the Type I error and solve for the cutoff that produces the desired trade-off of false negatives and false positives.

Our focus on both Type I and Type II errors echoes recent studies in economics that highlight the importance of examining test power. For example, in a survey of a large number of studies, Ioannidis, Stanley, and Doucouliagos (2017) show that 90% of results in many research areas are under powered, leading to an exaggeration of the results. Ziliak and McCloskey (2004) further show that only 8% of the papers published in the American Economic Review in the 1990s consider test power. The question of test power thus represents one more challenge to research practices common in economics research (Leamer (1983), De Long and Lang (1992), Ioannidis and Doucouliagos (2013), Harvey and Liu (2013), Harvey, Liu, and Zhu (2016), Harvey (2017)).

Why is test power important for research in financial economics? On the one hand, when a study’s main finding is the non existence of an effect (i.e., the null hypothesis is not rejected), test power directly affects the credibility of the finding because it determines the probability of not rejecting the null hypothesis when the effect is true. For example, in one of our applications, we show that existing studies lack power to detect outperforming mutual funds. On the other hand, when the main finding is the rejection of the null hypothesis (i.e., the main hypothesis), this finding often has to survive against alternative hypotheses (i.e., alternative explanations for the main finding). Low test power for alternative explanations generates a high Type I error rate for the main hypothesis (Ioannidis (2005)).

Our paper addresses the question of test power in the context of multiple tests. Our contribution is threefold. First, we introduce a framework that offers an intuitive definition of test power. Second, we employ a double-bootstrap approach that can flexibly (i.e., specific to a particular data set) estimate test power. Finally, we illustrate how taking test power into account can materially change our interpretation of important research findings in the current literature.

In a single-hypothesis test, the Type II error rate at a particular parameter value (in our context, the performance metric for the manager) is calculated as the probability of failing to reject the null hypothesis at this value. In multiple tests, the calculation of the Type II error rate is less straightforward because, instead of a single parameter value, we need to specify a vector of non zero parameters, where each parameter corresponds to a single test under the alternative hypothesis.

We propose a simple strategy to estimate the Type II error rate. Assuming that a fraction of managers have skill, we adjust the data so that of managers have skill (with their skill level set at the in-sample estimate) and the remaining of managers have no skill (with their skill level set to a zero excess return or alpha). By bootstrapping from these adjusted data, we evaluate the Type II error rate through simulations. Our method thus circumvents the difficulty of specifying the high-dimensional parameter vector under the alternative hypothesis. We set the parameter vector at what we consider a reasonable value — the in-sample estimate corresponding to a certain . In essence, we treat as a sufficient statistic, which helps estimate the Type II error rate. We interpret from both a frequentist and a Bayesian perspective.

Our strategy is related to the bootstrap approach in performance evaluation proposed by Kosowski et al. (2006, KTWW) and Fama and French (2010).222See Harvey and Liu (2019) for another application of the bootstrap approach to the test of factor models. These papers use a single-bootstrap approach to adjust for multiple testing. In particular, under the assumption of no skill for all funds (), they demean the data to create a “pseudo” sample, , for which holds true in-sample. They then bootstrap to test the overall hypothesis that all funds have zero alpha. Because we are interested in both the Type I and the Type II error rates associated with a given testing procedure (including those of KTWW and Fama and French (2010)), our method uses two rounds of bootstrapping. For example, to estimate the Type I error rate of Fama and French (2010), we first bootstrap to create a perturbation, , for which the null hypothesis is true. We then apply Fama and French (2010) (i.e., second bootstrap) to each and record the testing outcome ( if rejection). We estimate the Type I error rate as the average . The Type II error rate can be estimated in similar fashion.

After introducing our framework, we turn to two empirical applications to illustrate how our framework helps address important issues related to Type I and Type II errors associated with multiple tests. We first apply our method to the selection of two sets of investment factors. The first set includes hundreds of backtested factor returns. For a given , our method allows investors to measure the Type I and Type II error rates for these factors and thus make choices that strike a balance between Type I and Type II errors. When is uncertain, investors can use our method to evaluate the performance of existing multiple-testing adjustments and select the adjustment that works well regardless of the value of or for a range of values. Indeed, our application shows that multiple-testing methods usually follow an ordering (best to worst) in performance, regardless of the value of .

The second set of investment factors includes around 18,000 anomaly strategies constructed and studied by Yan and Zheng (2017). Relying on the Fama and French (2010) approach to adjust for multiple testing, Yan and Zheng (2017) claim that a large fraction of the 18,000 anomalies in their data are true and conclude that there is widespread mispricing. We use our model to estimate the error rates of their approach and obtain results that are inconsistent with their narrative.

We next apply our approach to performance evaluation, revisiting the problem of determining whether mutual fund managers have skill. In particular, we use our double-bootstrap technique to estimate the Type I and Type II error rates of the popular Fama and French (2010) approach. We find that their approach lacks power to detect outperforming funds. Even when a significant fraction of funds are outperforming, and the returns that these funds generate in the actual sample are large, the Fama and French (2010) method may still declare, with a high probability, a zero alpha across all funds. Our result thus calls into question their conclusions regarding mutual fund performance and helps reconcile the difference between KTWW and Fama and French (2010).

Our paper is not alone in raising the question of power in performance evaluation. Ferson and Chen (2017), Andrikogiannopoulou and Papakonstantinou (2019), and Barras, Scaillet, and Wermers (2018) focus on the power of applying the false discovery rate approach of Barras, Scaillet, and Wermers (2010) in estimating the fraction of outperforming funds. Our paper differs by proposing a non parametric bootstrap-based approach to systematically evaluate test power. We also apply our method to a wide range of questions in financial economics, including the selection of investment strategies, identification of equity market anomalies, and evaluation of mutual fund managers. Chordia, Goyal, and Saretto (2020) study an even larger collection of anomalies than Yan and Zheng (2017) and use several existing multiple-testing adjustment methods to estimate the fraction of true anomalies. In contrast to Chordia, Goyal, and Saretto (2020), we compare different methods using our bootstrap-based approach. In particular, we show exactly what went wrong with the inference in Yan and Zheng (2017).

Our paper also contributes to the growing literature in finance that applies multiple-testing techniques to related areas in financial economics (see, for example, Harvey, Liu, and Zhu (2016), Harvey (2017), Chordia, Goyal, and Saretto (2020), Barras (2019), Giglio, Liao, and Xiu (2018)). One obstacle for this literature is that, despite the large number of available methods developed by the statistics literature, it is unclear which method is most suitable for a given data set. We provide a systematic approach that offers data-driven guidance on the relative performance of multiple-testing adjustment methods.

Our paper is organized as follows. In Section I, we present our method. In Section II, we apply our method to the selection of investment strategies and mutual fund performance evaluation. In Section III, we offer some concluding remarks.

I. Method

A. Motivation: A Single Hypothesis Test

Suppose we have a single hypothesis to test and the test corresponds to the mean of a univariate variable . For a given testing procedure (e.g., the sample mean test), at least two metrics are important for gauging the performance of the procedure. The first is the Type I error rate, which is the probability of incorrectly rejecting the null when it is true (a false positive), and the other is the Type II error rate, which is probability of incorrectly declaring insignificance when the alternative hypothesis is true (a false negative). The Type II error rate is also linked to test power (i.e., power Type II error rate), which is the probability of correctly rejecting the null when the alternative hypothesis is true.

In a typical single-hypothesis test, we try to control the Type I error rate at a certain level (e.g., 5% significance) while seeking methods that generate a low Type II error rate or, equivalently, high test power. To evaluate the Type I error rate, we assume that the null is true (i.e., ) and calculate the probability of a false discovery. For the Type II error rate, we assume a certain level (e.g., ) for the parameter of interest (i.e., the mean of ) and calculate the probability of a false negative as a function of .

In the context of multiple hypothesis testing, the evaluation of Type I and Type II error rates is less straightforward for several reasons. First, for the definition of the Type I error rate, the overall hypothesis that the null hypothesis holds for each individual test may be too strong to be realistic for certain applications. As a result, we often need alternative definitions of Type I error rates that apply even when some of the null hypotheses may not be true.333One example is the False Discovery Rate, as we shall see below. For the Type II error rate, its calculation generally depends on the parameters of interest, which is a high-dimensional vector as we have multiple tests. As a result, it is not clear what value for this high-dimensional vector is most relevant for the calculation of the Type II error rate.

Given the difficulty in determining the Type II error rate, current multiple-testing adjustments often focus only on Type I errors. For example, Fama and French (2010) look at mutual fund performance and test the overall null hypothesis of a zero alpha for all funds. They do not assess the performance of their method when the alternative is true, that is, the probability of incorrectly declaring insignificant alphas across all funds when some funds display skill. As another example, the multiple-testing adjustments studied in Harvey, Liu, and Zhu (2016) focus on the Type I error defined by either the family-wise error rate (FWER), which is the probability of making at least one false discovery, or the false discovery rate (FDR), which is the expected fraction of false discoveries among all discoveries. Whether these methods have good performance in terms of Type I error rates and what the implied Type II error rates would be thus remain open questions.

Second, while we can often calculate Type I and Type II error rates analytically under certain assumptions for a single hypothesis test, such assumptions become increasingly untenable when we have many tests. For example, it is difficult to model cross-sectional dependence when we have a large collection of tests.

Third, when there are multiple tests, even the definitions of Type I and Type II error rates become less straightforward. While traditional multiple-testing techniques apply to certain definitions of Type I error rates such as FWER or FDR, we are interested in a general approach that allows us to evaluate different measures of the severity of false positives and false negatives. For example, while the FWER from the statistics literature has been applied by Harvey, Liu, and Zhu (2016) to evaluate strategies based on anomalies, an odds ratio that weighs the number of false discoveries against the number of misses may be more informative for the selection of investment strategies as it may be more consistent with the manager’s objective function.

Motivated by these concerns, we develop a general framework that allows us to evaluate error rates in the presence of multiple tests. First, we propose a simple metric to summarize the information contained in the parameters of interest and to evaluate Type I and Type II error rates. In essence, this metric reduces the dimensionality of the parameters of interest and allows us to evaluate error rates around what we consider a reasonable set of parameter values. Second, we evaluate error rates using a bootstrap method, which allows us to capture cross-sectional dependence nonparametrically. Because our method is quite flexible in terms of how we define the severity of false positives and false negatives, we are able to evaluate error rate definitions that are appropriate for a diverse set of finance applications.

B. Bootstrapped Error Rates under Multiple Tests

To ease our exposition, we describe our method in the context of testing the performance of many trading strategies. Suppose we have strategies and time periods. We arrange the data into a data matrix .

Suppose one believes that a fraction of the strategies are true. We develop a simulation-based framework to evaluate error rates related to multiple hypothesis testing for a given .

There are several ways to interpret . When , no strategy is believed to be true, which is the overall null hypothesis of a zero return across all strategies. This hypothesis can be economically important. For example, KTWW and Fama and French (2010) examine this hypothesis for mutual funds to test market efficiency. We discuss this hypothesis in detail in Section I.D when we apply our method to Fama and French (2010).

When , some strategies are believed to be true. In this case, can be thought of as a plug-in parameter — similar to the role of in a single test as discussed in Section I.A — that helps us measure the error rates in the presence of multiple tests. As we discuss above in the context of multiple tests, in general one needs to make assumptions about the values of the population statistics (e.g., the mean return of a strategy) for all of the strategies believed to be true in order to determine the error rates. However, in our framework we argue that serves as a single summary statistic that allows us to effectively evaluate error rates without having to condition on the values of the population statistics. As a result, we offer a simple way to extend the error rate analysis for a single hypothesis test to the concept of multiple hypothesis tests.

Note that by choosing a certain , investors are implicitly taking a stand on the plausible economic magnitudes of alternative hypotheses. For example, investors may believe that strategies with a mean return above 5% are likely to be true, resulting in a corresponding . While this is one way to rationalize the choice of in our framework, our model allows us to evaluate the implications of not only or the 5% cutoff but the entire distribution of alternatives on error rates.

The parameter also has a Bayesian interpretation. Harvey, Liu, and Zhu (2016) present a stylized Bayesian framework for multiple hypothesis testing in which multiple-testing adjustment is achieved indirectly through the likelihood function. Harvey (2017) instead recommends the use of the minimum Bayes factor, which builds on Bayesian hypothesis testing but abstracts from the prior specification by focusing on the prior that generates the minimum Bayes factor. Our treatment of lies between Harvey, Liu, and Zhu (2016) and Harvey (2017) in the sense that while we do not go as far as making assumptions on the prior distribution of that is later fed into the full-blown Bayesian framework as in Harvey, Liu, and Zhu (2016), we deviate from the Harvey (2017) assumption of a degenerate prior (i.e., the point mass that concentrates on the parameter value that generates the minimum Bayes factor) by exploring how error rates respond to changes in . While we do not attempt to pursue a complete Bayesian solution to multiple hypothesis testing,444Storey (2003) provides a Bayesian interpretation of the positive FDR. Scott and Berger (2006) include a general discussion of Bayesian multiple testing. Harvey, Liu, and Zhu (2016) discuss some of the challenges in addressing multiple testing within a Bayesian framework. Harvey et al. (2019) present a full-blown Bayesian framework to test market efficiency. the sensitivity of error rates to changes in that we highlight in this paper are important ingredients to both Bayesian and frequentist hypothesis testing.

Although the choice of is inherently subjective, we offer several guidelines as to the selection of an appropriate . First, examination of the summary statistics for the data can help narrow the range of reasonable priors.555See Harvey (2017) for examples of Bayes factors that are related to data-driven priors. For example, about 22% of strategies in our CAPIQ sample (see Section II.A for details on these data) have a -statistic above 2.0. This suggests that, at the 5% significance level, is likely lower than 22% given the need for a multiple-testing adjustment. Second, it may be a good idea to apply prior knowledge to elicit . For example, researchers with a focus on quantitative asset management may have an estimate of the success rate of finding a profitable investment strategy that is based on past experience. Such an estimate can guide their choices of . Finally, while in principle researchers can pick any in our model, in Section II.B we present a simulation framework that helps gauge the potential loss from applying different priors.

For a given , our method starts by choosing strategies that are deemed to be true. A simple way to choose these strategies is to first rank the strategies by their -statistics and then choose the top with the highest -statistics. While this approach is consistent with the idea that strategies with higher -statistics are more likely to be true, it ignores the sampling uncertainty in ranking the strategies. To take this certainty into account, we perturb the data and rank the strategies based on the perturbed data. In particular, we bootstrap the time periods and create an alternative panel of returns, (note that the original data matrix is ). For , we rank its strategies based on their -statistics. For the top strategies with the highest -statistics, we find the corresponding strategies in . We adjust these strategies so that their in-sample means are the same as the means for the top strategies in .666Alternatively, if a factor model is used for risk adjustment, we could adjust the intercepts of these strategies after estimating a factor model so that the adjusted intercepts are the same as those for the top strategies in . We denote the data matrix for these adjusted strategies by . For the remaining strategies in , we adjust them so they have a zero in-sample mean (denote the data matrix for these adjusted strategies by ). Finally, we arrange and into a new data matrix by concatenating the two data matrices. The data in will be the hypothetical data that we use to perform our follow-up error rate analysis, for which we know exactly which strategies are true and which strategies are false.

Our strategy of constructing a “pseudo” sample under the alternative hypothesis (i.e., some strategies are true) is motivated by the bootstrap approach proposed by the mutual fund literature. In particular, KTWW perform a bootstrap analysis at the individual fund level to select “star” funds. Fama and French (2010) look at the cross-sectional distribution of fund performance to control for multiple testing. Both papers rely on the idea of constructing a “pseudo” sample of fund returns for which the null hypothesis of zero performance is known to be true. We follow their strategies by constructing a similar sample for which some of the alternative hypotheses are known to be true, with their corresponding parameter values (i.e., strategy means) set at plausible values, in particular, their in-sample means associated with our first-stage bootstrap.

Notice that due to sampling uncertainty, what constitutes alternative hypotheses in our first-stage bootstrap may not correspond to the true alternative hypotheses for the underlying data-generating process. In particular, strategies with a true mean return of zero in population may generate an inflated mean after the first-stage bootstrap and thus be falsely classified as alternative hypotheses. While existing literature offers several methods to shrink the in-sample means (e.g., Jones and Shanken (2005), Andrikogiannopoulou and Papakonstantinou (2016), and Harvey and Liu (2018)), we do not employ them into our current paper. In a simulation study in which we evaluate the overall performance of our approach, we treat the misclassification of hypotheses as one potential factor that affects our model performance. Under realistic assumptions for the data-generating process, we show that our method performs well despite the potential misclassification of alternative hypotheses.

For , we bootstrap the time periods times to evaluate the error rates for a statistical procedure, such as a fixed -statistic threshold (e.g., a conventional -statistic threshold of 2.0) or the range of multiple-testing approaches detailed in Harvey, Liu, and Zhu (2016). By construction, we know which strategies in are believed to be true (and false), which allows us to summarize the testing outcomes for the -th bootstrap iteration with the vector , where is the number of tests that correctly identify a false strategy as false (true negative), is the number of tests that incorrectly identify a false strategy as true (false positive), is the number of tests that incorrectly identify a true strategy as false (false negative), and is the number of tests that correctly identify a true strategy as true (true positive). Notice that for brevity we suppress the dependence of on the significance threshold (i.e., either a fixed -statistic threshold or the threshold generated by a data-dependent testing procedure). Table I illustrates these four summary statistics using a contingency table.

| Decision | Null | Alternative | ||

|---|---|---|---|---|

| () | () | |||

| Reject | False positive | True positive | ||

| (Type I error) | () | |||

| () | ||||

| Accept | True negative | False negative | ||

| () | (Type II error) | |||

| () |

With these summary statistics, we can construct several error rates of interest. We focus on three types of error rates in our paper. The first — the realized false discovery rate (FDR) — is motivated by the FDR (see Benjamini and Hochberg (1995), Benjamini and Yekutieli (2001), Barras, Scaillet, and Wermers (2010), and Harvey, Liu, and Zhu (2016)) and is defined as

that is, the fraction of false discoveries (i.e., ) among all discoveries (i.e., ). The expected value of extends the Type I error rate in a single hypothesis test to multiple tests.

The second type of error rate — the realized rate of misses (RMISS), sometimes referred to as the false omission rate or false non discovery rate — is also motivated by the FDR and is defined as

that is, the fraction of misses (i.e., ) among all tests that are declared insignificant (i.e., ). The expected value of extends the Type II error rate in a single hypothesis test to multiple tests.777Alternative error rate definitions include precision (the ratio of the number of correct positives to the number of all predicted positives, that is, ) and recall (also known as the hit rate or true positive rate; the ratio of the number of true positives to the number of strategies that should be identified as positive, that is, ). One can also define the FDR as the expected fraction of false discoveries among all tests for which the null is true, which corresponds more closely to the Type I error rate definition for a single test.

Finally, similar to the concept of the odds ratio in Bayesian analysis, we define the realized ratio of false discoveries to misses (RRATIO) as

that is, the ratio of false discoveries (i.e., ) to misses (i.e., ).888In most of our applications there are misses, so the difference between our current definition (i.e., ) and alternative definitions, such as excluding simulation runs for which , is small.

Notice that by using summary statistics that count the number of occurrences for different types of testing outcomes, we are restricting attention to error rate definitions that depend only on the number of occurrences. Alternative definitions of error rates that involve the magnitudes of the effects being tested (e.g., an error rate that puts a higher weight on a missed strategy with a higher Sharpe ratio) can also be accommodated in our framework.999See DeGroot (1975), DeGroot and Schervish (2011, chapter 9), and Beneish (1997, 1999).

Finally, we account for the sampling uncertainty in ranking the strategies and the uncertainty in generating the realized error rates for each ranking by averaging across both and . Suppose we perturb the data times, and each time we generate bootstrapped random samples. We then have

We refer to as the Type I error rate, as the Type II error rate, and as the odds ratio (between false discoveries and misses). Notice that similar to , our estimated , , and implicitly depend on the significance threshold.

There are several advantages of compared to and . First, links Type I and Type II errors by quantifying the chance of a false discovery per miss. For example, if an investor believes that the cost of a Type I error is 10 times that of a Type II error, then the optimal should be . Second, takes the magnitude of into account. When is very small, is usually much smaller than . However, this mainly reflects the rare occurrence of the alternative hypothesis and does not necessarily imply good model performance in controlling . In this case, may be a more informed metric in balancing Type I and Type II errors. While we do not attempt to specify the relative weight between and (which likely requires specifying a loss function that weighs Type I errors against Type II errors), we use as a heuristic to weigh Type I errors against Type II errors.

To summarize, we follow the steps below to evaluate the error rates.

-

Step I.

Bootstrap the time periods and let the bootstrapped panel of returns be . For , obtain the corresponding vector of -statistics .

-

Step II.

Rank the components in . For the top of strategies in , find the corresponding strategies in the original data . Adjust these strategies so they have the same means as those for the top of strategies ranked by in . Denote the data matrix for the adjusted strategies by . For the remaining strategies in , adjust them so they have zero mean in-sample (denote the corresponding data matrix by ). Arrange and into a new data matrix .

-

Step III.

Bootstrap the time periods times. For each bootstrapped sample, calculate the realized error rates (or odds ratio) for , denoted by ( stands for a generic error rate that is a function of the testing outcomes).

-

Step IV.

Repeat Steps I to III times. Calculate the final bootstrapped error rate as

.

Again, keep in mind that the calculation of the realized error rate (i.e., ) in Step III requires the specification of the significance threshold (or a particular data-dependent testing procedure). As a result, the final bootstrapped error rates produced by our model are (implicitly) functions of the threshold.

C. Type II Error Rates under Multiple Tests

While our definition of the Type I error rate (i.e., the FDR) is intuitive and fairly standard in the finance and statistics literatures, our definition of the Type II error rate (i.e., the false omission rate) deserves further discussion.

First, the way we define the Type II error rate is analogous to how we define the FDR. This can be seen by noting that while the FDR uses the total number of positives (i.e., TP + FP) as the denominator, our Type II error rate uses the total number of negatives (i.e., TN + FN). Several papers in statistics also recommend using the false omission rate — also referred to as the false non discovery rate — to measure the Type II error rate in the context of multiple testing (e.g., Genovese and Wasserman (2002), Sarkar (2006)).

The usual definition of the Type II error rate under single testing translates into the expected fraction of false negatives out of the total number of alternatives (i.e., the false negative rate, ) in multiple testing. While we can easily accommodate this particular definition, we believe that the false omission rate is more appropriate under multiple testing and more suited to situations that are relevant to finance.

Note that these alternative definitions of the Type II error rate are transformations of each other and the Type I error rate, so we do not lose information by focusing on the false omission rate. For a given data set, the number of alternatives (i.e., ) and the number of nulls (i.e., ) are both fixed. There are only two unknowns among the four numbers. So any Type II error rate definition will be implied by the Type I error rate and the false omission rate.101010To be precise, the realized error rates are explicit functions of the two unknowns. So this is only approximately true after taking expectations.

The Type II error rate is linked to power. As a result, our Type II error rate implies a different interpretation of power that is best demonstrated with an example. Suppose that there are 100 managers, of which five are skilled. Suppose further that our test procedure correctly declares all 95 unskilled managers as unskilled and identifies three of the five skilled managers as skilled. The Type II error could be defined as 2/5, implying that 60% () of managers are correctly identified, which corresponds to the usual definition of power in a single test. Now suppose that we increase the total number of managers to 1,000 but we have the same number of skilled managers, five, and the same number of identified skilled managers, three. This would imply the same Type II error rate as before (i.e., 2/5), making the two cases indistinguishable from a Type II error perspective. However, it seems far more impressive for a testing method to correctly identify three out of five skilled managers among 1,000 managers than among 100. Our definition of the Type II error rate gets at exactly this difference — we obtain an error rate of 2/97 () for 100 tests versus 2/997 () for 1,000 tests.

While we focus on the false omission rate in defining the Type II error rate, our bootstrap-based approach can easily accommodate alternative definitions such as the false negative rate or even definitions that have differential weights on individual errors. We view this as an important advantage of our framework in comparison to those provided by existing statistics literature (e.g., Genovese and Wasserman (2002), Sarkar (2006)).

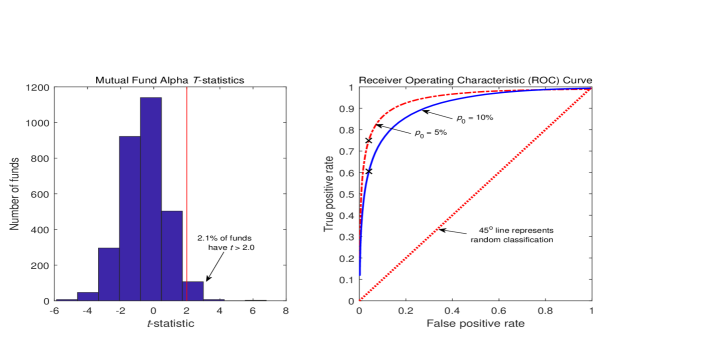

D. Bootstrapped Error Rates for Fama and French (2010)

Fama and French (2010) focus on the overall null hypothesis of zero alpha across mutual funds to test a version of the efficient market hypothesis. Therefore, the relevant error rates in their context are the probability of rejecting this overall null hypothesis when it is true (Type I error) and the probability of not rejecting this null hypothesis when some funds have the ability to generate a positive alpha (Type II error). We apply our framework described in Section I.B and I.C to find the corresponding Type I (denoted by ) and Type II (denoted by ) error rates.

We first focus on the Type I error. This corresponds to the case of in our framework. Let the original data be . Similar to Fama and French (2010), we subtract the in-sample alpha estimate from each fund’s return to generate a “pseudo” sample of funds whose alphas are precisely zero. Let this sample be . We treat as the population of fund returns for which the overall null hypothesis of zero alpha across all funds is true.

Fama and French (2010) bootstrap to generate distributions of the cross-section of -statistics and compare these bootstrapped distributions to the actual distribution to draw inferences. Similar to their strategy (and that in KTWW), if can be treated as the “pseudo” sample of fund returns under the null hypothesis, then any bootstrapped version of can also be regarded as a “pseudo” sample. This provides the basis for our evaluation of the Type I error rate for Fama and French (2010). We bootstrap many times to generate alternative samples for which the overall null hypothesis of zero alpha across funds is true. For each sample, we apply Fama and French (2010) to see if the null hypothesis is (falsely) rejected. We take the average rejection rate as the Type I error rate.

More specifically, we bootstrap the time periods to perturb . This is where our approach departs from Fama and French (2010) — while they make a one-shot decision for , we employ perturbations of to simulate the error rates of the Fama-French (2010) approach. Let the perturbed data be denoted by . Notice that due to sampling uncertainty, fund alphas are no longer zero for , although the overall null hypothesis is still true since is obtained by simply perturbing . For , we perform the Fama-French (2010) approach and let the testing outcome be given by , where is equal to one if we reject the null hypothesis and zero otherwise. Finally, we perturb many times and calculate the empirical Type I error rate (i.e., ) as the average .

We follow a procedure that is similar to that described in Section I.C to generate the Type II error rate. In particular, for a given fraction of funds with a positive alpha, we bootstrap the time periods and identify the top of funds with the highest -statistics for alpha. We find the corresponding funds in the original data and adjust them such that they have the same alphas as those for the top of funds in the bootstrapped sample (denote the data matrix for the adjusted strategies by ). At the same time, we adjust the returns of the remaining funds so that they have zero alpha (denote the corresponding data matrix by ). By joining with , we obtain a new panel. Using this panel, we apply the Fama-French (2010) approach and record the testing outcome as if the null hypothesis is not rejected (and zero otherwise). The empirical Type II error rate (i.e., ) is then calculated as the average .

In summary, while Fama and French (2010) make a one-time decision about whether to reject the overall null hypothesis for a given set of fund returns, our approach allows us to calibrate the error rates of Fama and French (2010) by repeatedly applying their method to bootstrapped data that are generated from the original data.

E. Discussion

While traditional frequentist single-hypothesis testing focuses on the Type I error rate, more powerful frequentist approaches (e.g., likelihood-ratio test) and Bayesian hypothesis testing account for both Type I and Type II error rates. However, as we mention above, in the context of multiple testing, it is difficult to evaluate the Type II error rate for at least two reasons. First, the large number of alternative hypotheses makes such evaluation a potentially intractable multidimensional problem. Second, the multidimensional nature of the data, in particular the dependence across tests, confounds inference on the joint distribution of error rates across tests. Our framework provides solutions to both of these problems.

Given the large number of alternative hypotheses, it seems inappropriate to focus on any particular parameter vector as the alternative hypothesis. Our double-bootstrap approach simplifies the specification of alternative hypotheses by grouping similar alternative hypotheses. In particular, all alternative hypotheses that correspond to the case in which a fraction of the hypotheses are true (and the rest are false and hence set at the null hypotheses) are grouped under a single that is associated with .

While our grouping procedure helps reduce the dimension of the alternative hypothesis space, a large number of alternative hypotheses associated with a given exist. However, we argue that many of these alternative hypotheses are unlikely to be true for the underlying data-generating process and hence irrelevant for hypothesis testing. First, hypotheses with a low in-sample -statistic are less likely to be true than hypotheses with a high in-sample -statistic. Second, the true parameter value for each effect under consideration is not arbitrary, but rather can be estimated from the data. Our bootstrap-based approach takes both of these points into account. In particular, our ranking of -statistics based on the bootstrapped sample in Step I addresses the first issue, and our assignment of the actual (observed returns) as the “true” parameter values to a fraction of tests that are deemed to be true after Step I addresses the second issue.

After we fix and find a parameter vector that is consistent with via the first-stage bootstrap, our second-stage bootstrap allows us to evaluate any function of error rates (both Type I and Type II) nonparametrically. Importantly, bootstrapping provides a convenient method to take data dependence into account, as argued in Fama and French (2010).

Our framework also allows us to make data-specific recommendations for the statistical cutoffs, and to evaluate the performance of any particular multiple-testing adjustment. In our applications, we provide examples of both. Given the large number of multiple testing methods that are available and the potential variation in a given method’s performance across data sets, we view it important to generate data-specific statistical cutoffs that achieve a pre-specified Type I or Type II error constraint (or a combination of both). For example, Harvey, Liu, and Zhu (2016) apply several well-known multiple testing methods to anomaly data to control for the FDR. However, whether these or other methods can achieve the pre-specified FDR for these anomaly data is not known. Our double-bootstrap approach allows us to accurately calculate the FDR conditional on the -statistic cutoff and . We can therefore choose the -statistic cutoff that exactly achieves a pre-specified FDR for values of that are deemed plausible.

While our paper focuses on estimating statistical objectives such as the FDR, one may attempt to apply our approach to economic objectives such as the Sharpe ratio of a portfolio of strategies or funds. However, there are several reasons to caution against such an attempt.

First, there seems to be a disconnect between statistical objectives and economic objectives in the finance literature. This tension traces back to two strands of literature. One is the performance evaluation literature, where researchers or practitioners, facing thousands of funds to select from, focus on simple statistics (i.e., statistical objectives) such as the FDR. The other strand is the mean-variance literature, where researchers record combinations of assets to generate efficient portfolios. Our framework is more applicable to the performance evaluation literature.111111Note that although models used in the performance evaluation literature can generate a risk-adjusted alpha that indicates a utility gain (under certain assumptions of the utility function) by allocating to a particular fund, they still do not account for the cross-sectional correlations in idiosyncratic fund returns that impact allocation across a group of funds, which is the objective of the mean-variance literature. Following the logic of this literature, we are more interested in estimating economically motivated quantities such as the fraction of outperforming funds than trying to find optimal combinations of funds due to either practical constraints (e.g., difficult to allocate to many funds) or computational issues (i.e., the cross-section is too large to reliably estimate a covariance matrix). While certain extensions of conventional statistical objectives in multiple testing (e.g., differential weights on the two types of error rates) are allowed in our framework, these extensions should still be considered rudimentary from the standpoint of economic objectives.

Second, statistical objectives and economic objectives may not be consistent with each other. For example, an individual asset with a high Sharpe ratio, which would likely be declared significant in a multiple-testing framework, may not be as attractive in the mean-variance framework once its correlations with other assets are taken into account.121212Here correlations may be caused by correlations in idiosyncratic risks that are orthogonal to systematic risk factors. As another example, the quest for test power may not perfectly align with economic objectives as methods that have low statistical power may still have important implications from an economic perspective (Kandel and Stambaugh (1996)).

We require that be relatively small so that the top strategies in the first-stage bootstrap always have positive means.131313This is the case for our application since we test the one-sided hypothesis for which the alternative hypothesis is that the strategy mean is positive. We do not require such a restriction on if the hypothesis test is two-sided. This ensures that the population means for strategies that are deemed to be true in the second-stage bootstrap are positive, which is consistent with the alternative hypotheses and is required by our bootstrap approach. This is slightly stronger than requiring that be smaller than the fraction of strategies that have positive means in the original sample, since we need this (i.e., is smaller than the fraction of strategies with positive means) to be the case for all bootstrapped samples.141414While imposing the constraint that is less than the fraction of strategies with a positive mean in the original sample cannot in theory rule out bootstrapped samples for which this condition is violated, we find zero occurrences of such violations in our results since is set to be below the fraction of strategies with a positive mean by a margin. One reason that we believe helps prevent such violations is the stability of order statistics, which ensures that the fraction of strategies with a positive mean in bootstrapped samples is fairly close to that in the original sample. In our applications, we ensure that our choices of always meet this condition. We believe our restriction on is reasonable, as it is unlikely that every strategy with a positive return is true — due to sampling uncertainty, some zero-mean strategies will have positive returns.

II. Applications

We consider two applications of our framework. In the first, we study two large groups of investment strategies. We illustrate how our method can be used to select outperforming strategies and we compare our method to existing multiple-testing techniques. Our second application revisits Fama and French’s (2010) conclusion about mutual fund performance. We show that Fama and French’s (2010) technique is underpowered in that it is unable to identify truly outperforming funds. Overall, our two applications highlight the flexibility of our approach in addressing questions related to the multiple-testing problem.

A. Investment Strategies

A.1. Data Description: CAPIQ and 18,000 Anomalies

We start with Standard and Poor’s Capital IQ (CAPIQ) database, which covers a broad set of “alpha” strategies. This database records the historical performance of synthetic long-short strategies that are classified into eight groups based on the types of their risk exposures (e.g., market risk) or the nature of their forecasting variables (e.g., firm characteristics). Many well-known investment strategies are covered by this database, for example, CAPM beta (Capital Efficiency Group), value (Valuation Group), and momentum (Momentum Group). For our purposes, we study 484 strategies (i.e., long-short strategies) for the U.S. equity market from 1985 to 2014.151515We thank CAPIQ for making these data available to us. Harvey and Liu (2017) also use the CAPIQ data to study factor selection.

The CAPIQ data contain a large number of “significant” investment strategies based on single-hypothesis tests, which distinguishes it from the other data sets that we consider below (i.e., anomaly data or mutual funds). This is not surprising as CAPIQ is biased towards a select group of strategies that are known to historically perform well. As such, it is best to treat these data as an illustration of how our method helps address concerns about Type II errors. One caveat in using the CAPIQ data (or other data that include a collection of investment strategies, such as Hou, Xue, and Zhang (2020)) relates to the selection bias in the data, which is due mainly to publication bias. We do not attempt to address publication bias in this paper. See Harvey, Liu, and Zhu (2016) for a parametric approach to address publication bias.

The second data set comprises the 18,113 anomalies studied in Yan and Zheng (2017). Yan and Zheng (2017) construct a comprehensive set of anomalies based on firm characteristics.161616We thank Sterling Yan for providing us their data on anomaly returns. Using the Fama and French (2010) approach to adjust for multiple testing, they claim that a large portion of the anomalies are true and argue that there is widespread mispricing. We revisit the inference problem faced by Yan and Zheng (2017). Our goal is to use our framework to calibrate the error rates of their approach and offer insights on how many anomalies are true in their data — and we reach a different conclusion.

Overall, the two data sets represent two extreme cases for a pool of investment strategies that researchers or investors may seek to analyze. While the CAPIQ data focus on a select set of backtested strategies, the 18,000 anomalies include a large collection of primitive strategies obtained from a data mining exercise.

A.2. Preliminary Data Analysis

We use the -statistic to measure the statistical significance of an investment strategy. For the CAPIQ data, we simply use the -statistic of the strategy return.171717Our results for the CAPIQ data are similar if we adjust strategy returns using, say, the Fama-French-Carhart four-factor model. For the 18,113 anomalies in Yan and Zheng (2017), we follow their procedure and calculate excess returns with respect to the Fama-French-Carhart four-factor model.181818Yan and Zheng (2017) use several specifications of the benchmark model, including the Fama-French-Carhart four-factor model. We focus only on the Fama-French-Carhart four-factor model to save space as well as to illustrate how benchmark models can be easily incorporated into our framework. Our results are qualitatively similar if we use alternative benchmark models. Yan and Zheng (2017) construct their strategies using firm characteristics and these strategies likely have high exposures to existing factors. While we focus on simple -statistics to describe our framework in the previous section, our bootstrap-based method can be easily adapted to incorporate any benchmark factors.191919To preserve cross-sectional correlations, factors need to be resampled simultaneously with strategy returns when we resample the time periods.

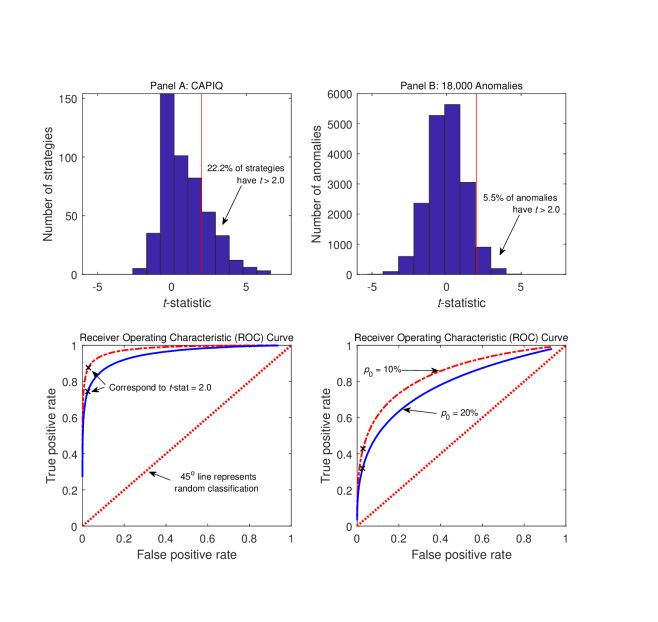

In Figure 1, the top graph in Panel A (Panel B) shows the distribution of the -statistics for the CAPIQ (18,000 anomalies) data. For the CAPIQ data, the distribution is skewed to the right. The fraction of strategies that have a -statistic above 2.0 is 22.1% (=107/484). For the 18,000 anomalies, the distribution is roughly symmetric around zero and the fraction of strategies that have a -statistic above 2.0 is 5.5% (=989/18,113). These statistics are consistent with how these two data sets are assembled.

Notice that the direction of the long-short strategies for the 18,113 anomalies data is essentially randomly assigned, which explains the symmetry of the distribution of the -statistics. This also suggests that we should perform two-sided hypothesis tests, as both significant outperformance and significant underperformance (relative to benchmark factor returns) qualify as evidence of anomalous returns. However, to be consistent, and thus facilitate comparison with our results for CAPIQ, we illustrate our method via one-sided tests and test only for outperformance. Our method can be readily applied to the case of two-sided tests. Moreover, given the data-mining nature of the 18,113 anomalies data (so the two tails of the distribution of the -statistics for anomalies are roughly symmetric), the Type I (Type II) error rates for one-sided tests under are approximately one-half of the Type I (Type II) error rates under . While we present results only for one-sided tests, readers interested in two-sided tests can apply the above transformation to obtain the corresponding error rates for two-sided tests.

We illustrate how our method can be used to create the receiver operating characteristic (ROC) curve, which is an intuitive diagnostic plot to assess the performance of a classification method (e.g., a multiple-testing method).202020See Fawcett (2006) and Hastie, Tibshirani and Friedman (2009) for applications of the ROC method. It plots the true positive rate (TPR), defined as the number of true discoveries over the total number of true strategies, against the false positive rate (FPR), defined as the ratio of false discoveries to the total number of zero-mean strategies.

Our framework allows us to use bootstrapped simulations to draw the ROC curve. In particular, for a given , the first-round bootstrap of our method classifies all strategies into true strategies and zero-mean strategies. The second-round bootstrap then calculates the realized TPR and FPR for each -statistic cutoff for each bootstrapped simulation. We simulate many times to generate the average TPR and FPR across simulations.

Note that our previously defined FDR is different from FPR. Although the numerator is the same (i.e., the number of false discoveries), the denominator is the total number of true strategies (FPR) versus the total number of discoveries (FDR).212121Conceptually, FDR is a more stringent error rate definition than FPR when there are a large number of false strategies and the signal-to-noise ratio is low in the data. In this case, a high -statistic cutoff generates very few discoveries. But FDR could still be high since it is difficult to distinguish the good from the bad. In contrast, since the denominator for FPR is larger than that for FDR, FPR tends to be much lower than FDR. Our framework can flexibly accommodate alternative error rate definitions that are deemed useful.

Figure 1 also shows the ROC curve for and 20%. On the ROC graph, the ideal classification outcome is given by the point , that is, and . As a result, a ROC curve that is closer to (or further away from the 45-degree line which corresponds to random classification) is deemed better. Two patterns can be seen in Figure 1. First, the ROC curve is better for the CAPIQ data than for the 18,000 anomalies. Second, for each data set, a smaller results in a better ROC curve.

These two patterns reflect key features of the two data sets that we analyze. The better ROC curve for the CAPIQ data stems from the higher average signal-to-noise ratio in these data as the CAPIQ contain a large number of select investment strategies. Although the higher signal-to-noise ratio can also be seen from the distribution of -statistics (i.e., the top graph of Figure 1), the ROC curve quantifies this through FPR and TPR, which are potentially informative metrics in classifying investment strategies.222222Another benefit is that the ROC curve generated in our framework takes test correlations into account (since, similar to Fama and French (2010), our second-stage bootstrap generates the same resampled time periods across all strategies), whereas the -statistic distribution cannot. However, a smaller results in a more select group of strategies (e.g., the average -statistic is higher for a smaller ), which explains the better classification outcome as illustrated by the ROC curve. The ROC curve highlights the trade-off between FPR and TPR for different levels of .232323Note that it is straightforward to find the optimal FPR (and the corresponding -statistic cutoff) associated with a certain trade-off between FPR and TPR. For example, if we equally weight the FPR and the TPR (i.e., we try to maximize TPR FPR), then the optimal FPR is given by the tangency point of a 45-degree tangent line to the ROC curve.

A.3. The Selection of Investment Strategies: Having a Prior on .

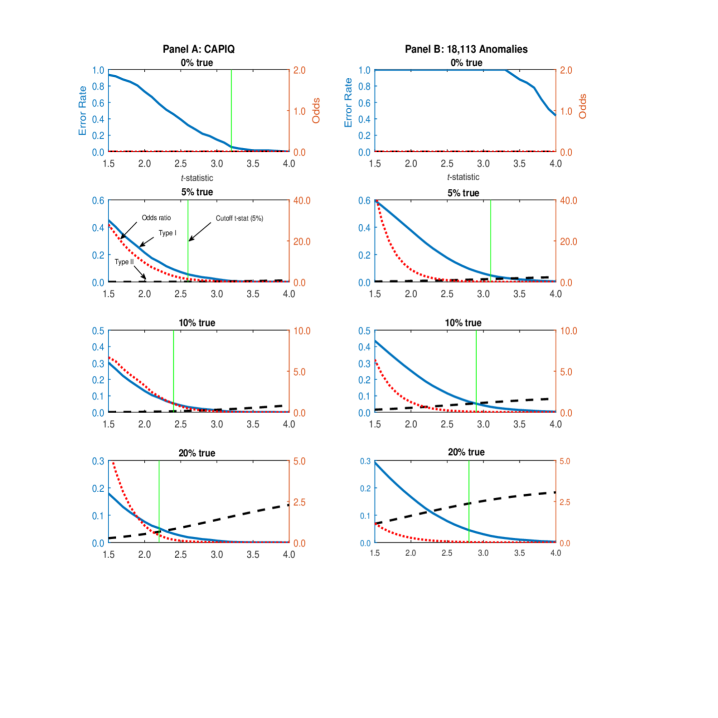

We first apply our method to study how the Type I and Type II error rates vary across different -statistic thresholds. In practice, researchers often use a pre-determined -statistic threshold to perform hypothesis testing, such as 2.0 at the 5% significance level for a single hypothesis test, or a -statistic that exceeds 3.0 based on Harvey, Liu, and Zhu (2016).242424Notice that it was never the intention of Harvey, Liu and Zhu (2016) to recommend the 3.0 threshold as a universal rule that applies to any data set. The purpose of the current paper is to show how one can use our method to calibrate Type I and Type II error rates based on different -statistic thresholds, through which one can obtain the “optimal” -statistic threshold that applies to the particular data set at hand (see also Harvey (2017)). We investigate the implications of these choices using our method.

Figure 2 shows the error rates across a range of -statistics for both the CAPIQ data and the 18,000 anomalies. We see that the classic trade-off between Type I and Type II error rates in single hypothesis tests continues to hold in a multiple testing framework. When the threshold -statistic increases, the Type I error rate (the rate of false discoveries among all discoveries) declines while the Type II error rate (the rate of misses among all non discoveries) increases. In addition, the odds ratio, which is the ratio of false discoveries to misses, also decreases as the threshold -statistic increases. We highlight the threshold -statistic that achieves 5% significance in Figure 2.252525The threshold -statistic is 4.9 for the 18,000 anomalies when . Since we set the range of the -statistic (i.e., x-axis) to span from 1.5 to 4.0, we do not display this -statistic in Figure 2. We see that this threshold -statistic decreases as (the prior fraction of true strategies) increases. This makes sense as a higher prior fraction of true strategies calls for a more lenient -statistic threshold.

How should an investment manager pick strategies based on Figure 2? First, the manager needs to elicit a prior on , which is likely driven by both her previous experience and the data (e.g., the histogram of -statistics that we provide in Section II.A.1). Suppose that the manager believes that a of 10% is plausible for the CAPIQ data. If she wants to control the Type I error rate at 5%, she should set the -statistic threshold to (see Panel A of Figure 2, ). Based on this -statistic threshold, 18% of strategies survive based on the original data.

Alternatively, under the same belief on , suppose that the investment manager is more interested in balancing Type I and Type II errors and wants to achieve an odds ratio of around , that is, on average five misses for each false discovery (alternatively, she believes that the cost of a Type I error is five times that of a Type II error). Then she should set the -statistic threshold to if she is interested in and 15% of the strategies survive.

Therefore, under either the Type I error rate or the odds ratio, neither 2.0 (the usual cutoff for 5% significance) nor 3.0 (based on Harvey, Liu, and Zhu (2016)) is optimal from the perspective of the investor. The preferred choices lie between 2.0 and 3.0 for the examples we consider and depend on both and the CAPIQ data that we study.

Comparing Panels A and B in Figure 2, at , the much higher -statistic cutoff for the 18,113 anomalies (i.e., 4.9) than that for CAPIQ (i.e., 3.2) reflects the larger number of strategies for the anomaly data (thresholds need to be higher when more strategies are tested, that is, when the multiple testing problem is more severe). For alternative values of , the higher -statistic cutoff for the anomaly data is driven by its low signal-to-noise ratio, which is also seen from the analysis of the ROC curve.

The overall message of Figure 2 is that two elements need to be taken into account to select the best strategies. One is investors’ prior on the fraction of true strategies. Most economic agents are subjective Bayesians, so it is natural to try to incorporate insights from the Bayesian approach into a multiple-testing framework.262626See Harvey (2017) for the application of the Bayesian approach to hypothesis testing. Our method allows us to evaluate the sensitivity of the error rates to changes in the prior fraction of true strategies. Instead of trying to control the error rates under all circumstances as in the traditional frequentist hypothesis testing framework, our view is that we should incorporate our prior beliefs into decision-making process, as doing so helps us make informed decisions based on the trade-off between the Type I and Type II errors.

The other element needed to select the best strategies relates to the particular data at hand and the hypothesis that is being tested. While many traditional multiple-testing adjustments work under general assumptions on the dependence structure in the data, they may be too conservative in that they underreject when the null hypothesis is false, leading to too many Type II errors (as we shall see below). Our bootstrap-based framework generates -statistic thresholds that are calibrated to the particular decision being considered and the particular data under analysis.

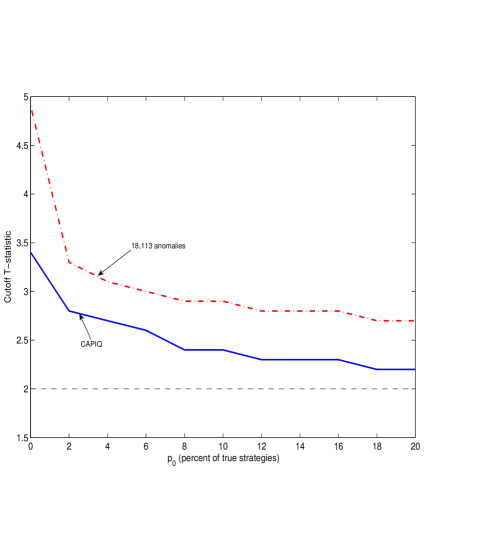

Figure 3 plots the cutoff -statistics that generate a Type I error rate of 5% against . In general, the cutoff -statistic declines as becomes larger, since a discovery is less likely to be false when a larger fraction of strategies are true.272727Our approach of choosing data-dependent cutoffs that guarantee particular Type I error rates is similar to the use of sample-size adjusted -values in the econometrics literature. Both strategies aim to achieve a Type I error rate that is closer to the desired level, and thereby increase test power. Whereas sample-size adjusted -values are usually applied to univariate tests from a time-series perspective, our approach applies to multiple testing and adjusts for the sample size (and distributional properties) for both the cross section and the time series.

A.4. The Selection of Investment Strategies: Unknown

When is unknown, our framework can be used to evaluate the performance of multiple-testing corrections across different values of . While multiple-testing methods are designed to control the FDR at the appropriate level regardless of the value of , their performance in finite samples, particularly for the data under analysis, is unknown. Our method provides guidance on which method to use for a particular data set.

Given our focus on the FDR, we implement several popular multiple-testing adjustments proposed in the statistics literature that aim to control the FDR. Our goal is not to compare all existing methods. Rather, we focus on a few representative methods in terms of their theoretical properties and illustrate how to apply our framework to select the best method for the particular data being analyzed.

We want to emphasize that our data-driven approach is different from the usual simulation exercises carried out by studies that propose multiple-testing methods. Most simulation studies make simple assumptions about the underlying data structure (e.g., a multivariate normal distribution with a certain correlation structure).282828See, for example, the simulation studies in Romano and Wolf (2005) and Romano, Shaikh, and Wolf (2008). However, the data sets we typically encounter in financial economics (e.g., the cross-section of stock returns) have important features (e.g., missing data, cross-sectional dependence, tail dependence, etc.) that may make simplifying assumptions poor approximations. In our multiple-testing context, many methods are known to be sensitive to some of these features (i.e., cross-sectional dependence and tail dependence). It is therefore important to customize the performance evaluation of a multiple-testing method to the data being examined.

The first set of multiple-testing adjustments that we consider are the Benjamini and Hochberg (1995) adjustment, BH, which controls the FDR under the pre-specified value if tests are mutually independent, and Benjamini and Yekutieli (2001) adjustment, BY, which controls the FDR under arbitrary dependence of the tests.292929Benjamini and Yekutieli (2001) show that independence can be replaced by the weaker assumption of positive regression dependency as in Benjamini and Hochberg (1995). BH may not work if tests are correlated in a certain fashion, while BY tends to be overly conservative (i.e., too few discoveries).303030For further details on these two methods and other multiple-testing adjustments, as well as their applications in finance, see Harvey, Liu, and Zhu (2016) and Chordia, Goyal, and Saretto (2020).

Given our focus on test power, we also consider the adjustment of Storey (2002), which sometimes results in an improvement over BH and BY in terms of test power. A plug-in parameter in Storey (2002), denoted by , helps replace the total number of tests in BH and BY with an estimate of the fraction of true null hypotheses. Bajgrowicz and Scaillet (2012) suggest . We experiment with three values for : , , and .

Finally, we consider a multiple-testing method that has strong theoretical properties in terms of the requirement on the data to achieve a pre-specified error rate.313131We thank Laurent Barras for bringing this literature to our attention. In particular, we implement the bootstrap-based approach of Romano, Shaikh, and Wolf (RSW, 2008), which controls the FDR asymptotically under arbitrary dependence in the data.323232See Romano and Wolf (2005) for a companion approach that controls the FWER. Our goal is to analyze the finite-sample performance of the RSW approach for the two data sets we study. However, implementation of RSW is computationally intensive (especially for the 18,000 anomalies) as it requires estimating regression models (where is the number of bootstrapped iterations and is the total number of tests) to derive a single -statistic cutoff. Accordingly, we randomly sample from the 18,000 anomalies to reduce the sample size and apply RSW to the subsamples. But this makes our results not directly comparable with those based on the full sample. We therefore present our results using RSW in the Appendix.

In addition to the aforementioned methods, we report the Type II error rates derived under the assumption that is known ex ante and the -statistic cutoff is fixed. In particular, for a given , our previous analysis allows us to choose the -statistic threshold such that the pre-specified Type I error rate is exactly achieved, thereby minimizing the Type II error rate of the test.333333The Type II error rate is minimized in our framework in the following sense. Suppose we are only allowed to choose a fixed -statistic cutoff for each assumed level of . Imagine that we try to solve a constrained optimization problem where the pre-specified significance level is the Type I error rate constraint and our objective function seeks to minimize the Type II error rate. Given the trade-off between the Type I and Type II error rates, the optimal value for the objective function (i.e., the Type II error rate) is achieved when the constraint is met with equality. This minimized Type II error rate is a useful benchmark to gauge the performance of other multiple-testing methods. Note that other multiple-testing methods may generate a smaller Type II error rate than the optimal rate because their Type I error rates may exceed the pre-specified levels.343434There is also a difference in the Type I error rate between a fixed -statistic cutoff and multiple-testing methods. Using our notation from Section I.B (i.e., denotes a particular parameterization of the hypotheses), while multiple-testing methods seek to control the FDR for each parameterization (i.e., ) of the hypotheses (i.e., ), the fixed -statistic cutoff that we use above aims to control , which is the average across different realizations of for a given .

Before presenting our results, we briefly report summary statistics on the correlations among test statistics for our data sets. For CAPIQ, the percentile, median, and percentile for the pairwise test correlations are -0.377, 0.081, and 0.525; the corresponding absolute values of the pairwise correlations are 0.040, 0.234, and 0.584. For the 18,000 anomalies, these numbers are -0.132, 0.003, and 0.145 (original values) and 0.013, 0.069, and 0.186 (absolute values). While correlations should provide some information on the relative performance of different methods, other features of the data may also be important, as we shall see below.

Tables II and III report results for the CAPIQ and the 18,000 anomalies, respectively. In Table II, BH generates FDRs that are always below and oftentimes close to the pre-specified significance levels, suggesting overall good performance. In comparison, BY is too conservative in that it generates too few discoveries, resulting in higher Type II error rates compared to BH. The three Storey tests generally fail to meet the pre-specified significance levels, although the Type I error rates generated by Storey () are reasonably close. Overall, BH seems to be the preferred choice for CAPIQ among the five tests we examine. Storey ( = 0.4) is also acceptable, although one has to be cautious about the somewhat higher Type I error rates than the desired levels.

The test statistic from our method (i.e., the last column in Table II) provides gains in test power compared to BH, BY, and Storey. In particular, compared to other methods that also meet the pre-specified significance levels (i.e., BH and BY as in Table II), the Type II error rate for this test statistic is uniformly lower. For example, for and a significance level of 10%, all three Storey tests deliver a Type I error that is too high, at 10%. When we perform power comparison, we omit the Storey methods and focus on the two other models (i.e., BH and BY). Between these two, BH is the better-performing model since its Type I error rate is closer to the pre-specified significance level. We therefore use it as the benchmark to evaluate the power improvement. Compared with BH, which generates a Type II error rate of 3.5%, our model produces an error rate of 2.9%.

For the 18,113 anomalies, the results in Table III present a different story than Table II. In particular, BH generally performs worse than the three Storey tests in controlling the FDR when is not too large (i.e., ), although the Storey tests also lead to higher Type I error rates than desired. Overall, BY should be the preferred choice to strictly control the Type I error rate at the pre-specified level, although it appears to be far too conservative. Alternatively, Storey () dominates the other methods in achieving the pre-specified significance levels when .

The Appendix presents results on the finite-sample performance of RSW applied to our data sets. Despite the strong theoretical appeal of RSW, it often leads to a higher Type I error rate than the desired level for both data sets. In fact, compared to the aforementioned multiple-testing methods we consider, RSW often generates the largest distortion in test size when is relatively small (i.e., ).

Our results highlight the data-driven nature of the performance of alternative multiple-testing methods. While BH works well theoretically when tests are independent, it is not clear how departures from independence affect its performance. Interestingly, our results show that BH performs much worse for the 18,000 anomalies than for CAPIQ, although the data for the 18,000 anomalies appear more “independent” than CAPIQ based on the test correlations.353535Note that we use the average correlation across strategies as an informal measure of the degree of cross-sectional dependence. However, correlation likely provides an insufficient characterization of dependence because certain forms of dependence may not be captured by the correlation. In our context, there may be important departures from independence in the 18,000 anomalies data that impact the performance of BH but are not reflected in the average correlation. Our results thus highlight the data-dependent nature of existing multiple-testing methods. As another example, we show that Storey () and Storey () could be the preferred choice for the two data sets we examine, whereas is the value recommended by Bajgrowicz and Scaillet (2012). Finally, methods that are guaranteed to perform well asymptotically may have poor finite-sample performance, as we show for RSW in the Appendix.

Overall, our method sheds light on which multiple-testing adjustment performs the best for a given data set. Of course, it is also possible to use our method directly to achieve a given false discovery level and to optimize the power across different assumptions for .

| Type I | Type II | ||||||||||||||||||||||||

| Storey | Storey | ||||||||||||||||||||||||

| () | () | () | () | () | () | ||||||||||||||||||||

| (frac. of true) | (sig. level) | ||||||||||||||||||||||||

| 2% | 1% | 0.010 | 0.002 | 0.023 | 0.022 | 0.021 | 0.001 | 0.002 | 0.001 | 0.001 | 0.001 | 0.001 | |||||||||||||

| 5% | 0.044 | 0.009 | 0.058 | 0.058 | 0.058 | 0.000 | 0.001 | 0.000 | 0.000 | 0.000 | 0.000 | ||||||||||||||

| 10% | 0.086 | 0.013 | 0.102 | 0.104 | 0.107 | 0.000 | 0.001 | 0.000 | 0.000 | 0.000 | 0.000 | ||||||||||||||

| 5% | 1% | 0.008 | 0.002 | 0.018 | 0.018 | 0.017 | 0.006 | 0.011 | 0.005 | 0.005 | 0.005 | 0.005 | |||||||||||||

| 5% | 0.047 | 0.007 | 0.060 | 0.060 | 0.060 | 0.003 | 0.006 | 0.002 | 0.002 | 0.002 | 0.002 | ||||||||||||||

| 10% | 0.091 | 0.012 | 0.102 | 0.105 | 0.113 | 0.002 | 0.005 | 0.001 | 0.001 | 0.002 | 0.001 | ||||||||||||||

| 10% | 1% | 0.008 | 0.002 | 0.017 | 0.017 | 0.016 | 0.022 | 0.037 | 0.021 | 0.021 | 0.020 | 0.021 | |||||||||||||

| 5% | 0.046 | 0.006 | 0.058 | 0.059 | 0.063 | 0.011 | 0.024 | 0.010 | 0.010 | 0.010 | 0.010 | ||||||||||||||

| 10% | 0.087 | 0.014 | 0.108 | 0.112 | 0.123 | 0.007 | 0.019 | 0.007 | 0.007 | 0.006 | 0.007 | ||||||||||||||

| 20% | 1% | 0.008 | 0.002 | 0.016 | 0.016 | 0.016 | 0.082 | 0.117 | 0.088 | 0.077 | 0.074 | 0.079 | |||||||||||||

| 5% | 0.042 | 0.006 | 0.061 | 0.064 | 0.071 | 0.049 | 0.088 | 0.044 | 0.043 | 0.041 | 0.047 | ||||||||||||||

| 10% | 0.079 | 0.012 | 0.117 | 0.123 | 0.142 | 0.035 | 0.074 | 0.030 | 0.029 | 0.028 | 0.029 | ||||||||||||||

| 30% | 1% | 0.007 | 0.002 | 0.017 | 0.017 | 0.017 | 0.179 | 0.223 | 0.161 | 0.159 | 0.154 | 0.153 | |||||||||||||

| 5% | 0.037 | 0.005 | 0.064 | 0.068 | 0.078 | 0.126 | 0.188 | 0.104 | 0.101 | 0.096 | 0.095 | ||||||||||||||

| 10% | 0.069 | 0.011 | 0.119 | 0.129 | 0.155 | 0.098 | 0.168 | 0.076 | 0.073 | 0.068 | 0.066 | ||||||||||||||

| *Type II calculated at optimized Type I error | |||||||||||||||||||||||||

| Type I | Type II | ||||||||||||||||||||||||

| Storey | Storey | ||||||||||||||||||||||||

| () | () | () | () | () | () | ||||||||||||||||||||

| (frac. of true) | (sig. level) | ||||||||||||||||||||||||

| 2% | 1% | 0.018 | 0.003 | 0.019 | 0.019 | 0.018 | 0.009 | 0.013 | 0.008 | 0.008 | 0.008 | 0.011 | |||||||||||||

| 5% | 0.077 | 0.008 | 0.072 | 0.072 | 0.070 | 0.005 | 0.010 | 0.005 | 0.005 | 0.005 | 0.007 | ||||||||||||||

| 10% | 0.143 | 0.018 | 0.134 | 0.133 | 0.131 | 0.004 | 0.009 | 0.004 | 0.004 | 0.004 | 0.005 | ||||||||||||||

| 5% | 1% | 0.017 | 0.002 | 0.018 | 0.018 | 0.017 | 0.030 | 0.040 | 0.030 | 0.030 | 0.030 | 0.031 | |||||||||||||

| 5% | 0.072 | 0.008 | 0.069 | 0.069 | 0.067 | 0.020 | 0.033 | 0.020 | 0.020 | 0.020 | 0.021 | ||||||||||||||

| 10% | 0.133 | 0.017 | 0.125 | 0.124 | 0.122 | 0.015 | 0.030 | 0.016 | 0.016 | 0.016 | 0.017 | ||||||||||||||

| 10% | 1% | 0.016 | 0.002 | 0.017 | 0.017 | 0.016 | 0.074 | 0.089 | 0.075 | 0.075 | 0.075 | 0.074 | |||||||||||||

| 5% | 0.067 | 0.008 | 0.067 | 0.067 | 0.065 | 0.055 | 0.080 | 0.056 | 0.055 | 0.055 | 0.054 | ||||||||||||||

| 10% | 0.122 | 0.016 | 0.121 | 0.121 | 0.120 | 0.044 | 0.074 | 0.045 | 0.045 | 0.045 | 0.045 | ||||||||||||||

| 20% | 1% | 0.014 | 0.002 | 0.016 | 0.016 | 0.016 | 0.166 | 0.187 | 0.169 | 0.169 | 0.169 | 0.171 | |||||||||||||

| 5% | 0.058 | 0.008 | 0.063 | 0.063 | 0.063 | 0.135 | 0.175 | 0.138 | 0.137 | 0.137 | 0.143 | ||||||||||||||

| 10% | 0.105 | 0.014 | 0.115 | 0.116 | 0.117 | 0.115 | 0.167 | 0.116 | 0.116 | 0.115 | 0.121 | ||||||||||||||

| 30% | 1% | 0.013 | 0.002 | 0.015 | 0.016 | 0.016 | 0.270 | 0.289 | 0.267 | 0.267 | 0.267 | 0.274 | |||||||||||||

| 5% | 0.051 | 0.007 | 0.060 | 0.061 | 0.062 | 0.238 | 0.278 | 0.231 | 0.230 | 0.229 | 0.235 | ||||||||||||||

| 10% | 0.092 | 0.013 | 0.110 | 0.113 | 0.116 | 0.214 | 0.270 | 0.203 | 0.201 | 0.200 | 0.210 | ||||||||||||||

| *Type II calculated at optimized Type I error | |||||||||||||||||||||||||

A.5. Revisiting Yan and Zheng (2017)

Applying the preferred methods based on Table III to the 18,000 anomalies, the fraction of true strategies is found to be 0.000% (BY) and 0.015% (Storey, ) under a 5% significance level, and 0.006% (BY) and 0.091% (Storey, ) under a 10% significance level.363636Across different values of , BY dominates BH, and Storey () dominates the two other Storey methods in achieving the pre-specified significance levels. We therefore focus on BY and Storey (). The statistics in this paragraph are based on unreported results.