Pairs Trading with Nonlinear and Non-Gaussian State Space Models††thanks: I am grateful to Zhongjun Qu, Hiroaki Kaido, Jean-Jacques Forneron and seminal participants at the Boston University Economics Department.

Abstract

This paper studies pairs trading using a nonlinear and non-Gaussian state space model framework. We model the spread between the prices of two assets as an unobservable state variable, and assume that it follows a mean reverting process. This new model has two distinctive features: (1) The innovations to the spread is non-Gaussianity and heteroskedastic. (2) The mean reversion of the spread is nonlinear. We show how to use the filtered spread as the trading indicator to carry out statistical arbitrage. We also propose a new trading strategy and present a Monte Carlo based approach to select the optimal trading rule. As the first empirical application, we apply the new model and the new trading strategy to two examples: PEP vs KO and EWT vs EWH. The results show that the new approach can achieve 21.86% annualized return for the PEP/KO pair and 31.84% annualized return for the EWT/EWH pair. As the second empirical application, we consider all the possible pairs among the largest and the smallest five US banks listed on the NYSE. For these pairs, we compare the performance of the proposed approach with that of the existing popular approaches, both in-sample and out-of-sample. Interestingly, we find that our approach can significantly improve the return and the Sharpe ratio in almost all the cases considered.

Keywords: pairs trading, nonlinear and non-Gaussian state space models, Quasi Monte Carlo Kalman filter.

JEL codes: C32, C41, G11, G17.

1 Introduction

In early 1980s, a group of physicists, mathematicians and computer scientists, leaded by quantitative analyst Nunzio Tartaglia, tried to use a sophisticated statistical approach to find the opportunities of arbitrage trading (Gatev et al. 2006). Tartaglia’s strategy, later coined pairs trading, is to find a pair of two stocks whose prices have moved similarly historically, and make profit by applying the simple contrarian principles. Since then, pairs trading has become a popular short-term arbitrage strategy used by hedge funds and is often considered as the “ancestor” of statistical arbitrage.

Pairs trading works by constructing a self financing portfolio with a long position in one security and a short position in the other. Given that the two securities have moved together historically, when a temporary anomaly happens, one security would be overvalued than the other relative to the long-term equilibrium. Then, an investor may be able to make money by selling the overvalued security, buying the undervalued security, and clearing the exposure when the two securities settle back to their long-term equilibrium. Because the effect from movement of the market is hedged by this self financing portfolio, pairs trading is market-neutral.

The methods for pairs trading can be broadly divided into nonparametric and parametric methods. In particular, Gatev et al. (2006) propose a nonparametric distance based approach in determining the securities for constructing the pairs. They choose a pair by finding the securities that minimized the sum of squared deviations between the two normalized prices. They argue this approach “best approximates the description of how traders themselves choose pairs”. They find that average annualized excess returns reach 11% for the top pairs portfolios using CRSP daily data from 1962 to 2002. Other Nonparametric methods on pairs trading can also be found in Bogomolov (2013) among others. Overall, the nonparametric distance based approach provides a simple and general method of selecting “good” pairs; however, as pointed out by Krauss (2016) and others, this selection metric is prone to pick up pairs with small variance of the spread, and therefore limits the profitability of pairs trading.

In contrast, the parametric approach tries to capture the mean-reverting characteristic of the spread using a parametric model. For example, Elliott et al. (2005) propose a mean-reverting Gaussian Markov chain model for the spread which is observed in Gaussian noise. See Vidyamurthy (2004), Cummins and Bucca (2012), Tourin and Yan (2013), Moura et al. (2016), Stübinger and Endres (2018), Clegg and Krauss (2018), Elliott and Bradrania (2018), Bai and Wu (2018) for other parametric methods on pairs trading. Overall, the parametric approach provides tractable methods for the analysis of pairs trading; however, most of the existing parametric models are too simple to be capable of capturing the dynamics of asset price, which substantially limits the returns from pairs trading.

Compared with the existing methods on pairs trading, the proposed approach has the following features: (1) It is based on a nonlinear and non-Gaussian state space model. This modelling can capture several stylized features of financial asset prices, including heavy-tailedness, heteroskedasticity, volatility clustering and nonlinear dependence. (2) The trading strategy is different from the existing ones. It utilizes the features of the model such as heteroskedasticity and volatility clustering, and it can potentially achieve significantly higher returns and Sharpe ratios. (3) The optimal trading rules is also different from the existing ones. Although this rule has no analytic solution, we show that it can be computed effectively using simulations. Finally, the optimal trading rule can adapt to various objectives, such as a high cumulative return, Sharpe ratio, or Calmar ratio.

We apply our approach to two pairs: PEP vs KO and EWT vs EWH. We we find that our approach achieves an annualized return of 0.2186 and Sharpe ratio of 2.9518 on the PEP/KO pair and an annualized return of 0.3184 and Sharpe ratio of 3.8892 on the EWT/EWH pair. In comparison, a conventional approach applied to the same pairs can only achieve an annualized return of 0.1311 and Sharpe ratio of 1.1003 for the PEP/KO pair and an annualized return of 0.1480 and Sharpe ratio of 1.1277 for the EWT/EWH pair. Next, we test our approach using all the possible pairs among the largest 5 banks and the smallest 5 banks listed in NYSE. We find significant improvements over the conventional approach for almost all the pairs. We also find that the pairs between small banks produce higher return than the pairs between large banks. This is likely because the spread between small banks are more volatile, providing more opportunities for active trading.

The main contributions of this paper can be summarized as follows. On the theory side, we propose a complete set of tools for pairs trading that include a model for the dynamics of the spread, a new trading strategy and a Monte Carlo method for determining the optimal trading rule. On the empirical side, we apply our approach to various pairs in practice. The results show that the new approach can achieve significant improvements on the performance of pairs trading.

The remainder of this paper is organized as follows. In Section 2, we propose a new model for pairs trading. In Section 3, we propose a new trading strategy based on the mean-reverting property of spread, and compare it with conventional trading strategies using simulations. In Section 4, we implement the proposed approach to actual data, and in Section 5 we conclude the paper.

2 A New Model for Pairs Trading

We propose the following nonlinear and non-Gaussian state space model for pairs trading:

| (1) | |||||

| (2) |

where is the price of security , is the price of security , is the hedge ratio between two securities, and is the true spread between and . We assume follow a mean-reverting process as in (2), and which could be non-Gaussian. Popular choices for , and could be the followings. Our framework applies to all of them.

-

•

Linear mean-reverting (Ornstein–Uhlenbeck process):

-

•

Nonlinear mean-reverting model:

-

•

Ait-Sahalia’s nonlinear mean-reverting model (Ait-Sahalia, 1996):

-

•

Homoskedasticity model:

-

•

ARCH model:

-

•

APARCH model:

-

•

Gaussian distributed noise:

-

•

Student’s distributed noise:

-

•

Generalized error distributed noise:

In model (1)-(2), we consider as the unobservable true spread between security and , which follows a mean-reverting process. is the observation and is the control variable. Since and in the function can not be identified simultaneously, we let and denote as the parameter of the model (1)-(2). is going to determined based on data set

Our new model has three advantages compared with existing models for pairs trading, such as Elliott et al. (2005) and Moura et al. (2016). First, since can be non-Gaussian, can follow a non-Gaussian process. By allowing for this non-Gaussianity in , the model can capture the distributional deviation from Gaussianity and reproduce heavy-tailed returns.

Second, the model captures heteroskedasticity in financial data. A well-known feature of financial time-series is volatility clustering: \saylarge changes tend to be followed by large changes, of either sign, and small changes tend to be followed by small changes (Mandelbrot, 1963). This feature was documented later in Ding, Granger and Engle (1993), and Ding and Granger (1996) among others. In model (2), the volatility persistence is represented by ARCH-style modeling. Details about the application of ARCH model in finance can be found in Bollerslev, Chou and Kroner (1992).

Third, in order to characterize the nonlinear dependence in financial data, we allow to be nonlinear. Scheinkman and LeBaron (1989) find evidence that indicates the presence of nonlinear dependence in weekly returns on the CRSP value-weighted index. Ait-Sahalia (1996) finds nonlinearity in the drift function of interest rate and concludes that “the principal source of rejection of existing (linear drift) models is the strong nonlinearity of the drift”. We keep the functional form of flexible and, as a result, we can capture the nonlinear dependence in financial data.

3 A New Approach to Pairs Trading

In this section, we discuss the trading strategies and trading rules for pairs trading. In this paper, a trading strategy is the method of buying and selling of assets in markets based on the estimation of the unobservable spread. A trading rule is the predefined values to generate the trading signal for a specific trading strategy with an investing objective. To implement a strategy and rule on pairs trading, we need the following quantities: (i) parameter estimates for the model (1)-(2), (ii) an estimate of the spread, and (iii) choice of a specific strategy and the optimal trading rule, and we discuss these aspects in this section. More specifically, in Section 3.1, we present an algorithm on the filtering of the unobervable spread and parameter estimation. In Section 3.2, We will discuss two benchmark trading strategies. In Section 3.3, we will present and compare three popular trading rules associated with the benchmark trading strategies. In Section 3.4, we propose a new trading strategy. In this new trading strategy, we change the way we open or close a trade, and we will discuss the benefit of this new strategy compared with the benchmark strategies. Since the existing trading rule cannot be simply applied to the model (1)-(2), we propose a new approach to calculate the optimal trading rule based on the simulation of the spread. The detail of this simulation based method is in Section 3.5. In Section 3.6, we summarize the procedure of pairs trading. This procedure can be applied to pairs trading with all of the trading strategies and trading rules discussed in this paper.

3.1 Algorithm for Filtering and Parameter Estimation

For a specification of model (1)-(2), we run the following algorithm of Quasi Monte Carlo Kalman filter for nonlinear and non-Gaussian state space models to estimate the unobservable spread and unknown parameters in the model, based on the observations . Suppose the initial spread follows for any reasonable choices of and .

-

•

Step 1: For non-Gaussian density we use Gaussian mixture density to approximate its pdf and denote the approximation as where is the Gaussian pdf defined by

To get this approximation, we determine the values of by minimizing the relative entropy between the true density and its approximation . The relative entropy is defined by

If is Gaussian, then this step can be dropped.

-

•

Step 2: Generate a Box-Muller transformed Halton sequence with sequence size from . Compute and store

and

When , is sampled from .

-

•

Step 3: Repeat Step 2 for , , and and store and for .

-

•

Step 4: Based on the results from Step 3, generate a Box-Muller transformed Halton sequences from for . Then generate . Compute and store the followings

-

•

Step 5: Compute , , and .

-

•

Step 6: Repeat Step 4-5 for . Compute and store and where , and

-

•

Step 7: Repeat Step 2-6 for .

from Step 6 is our estimation of the spread. To estimate the unknown parameter in the model, we first write the log-likelihood function as

and MLE of the unknow parameter would be determined to maximize the above likelihood, that is,

3.2 Benchmark Trading Strategies

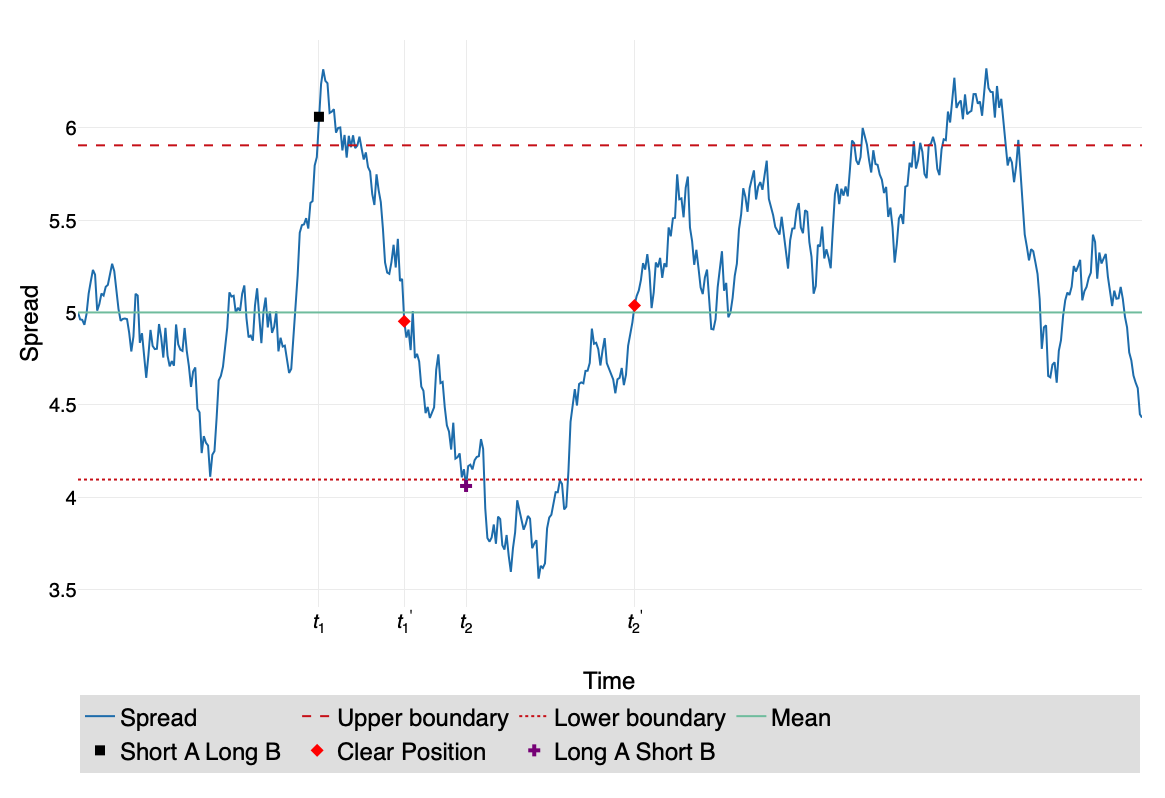

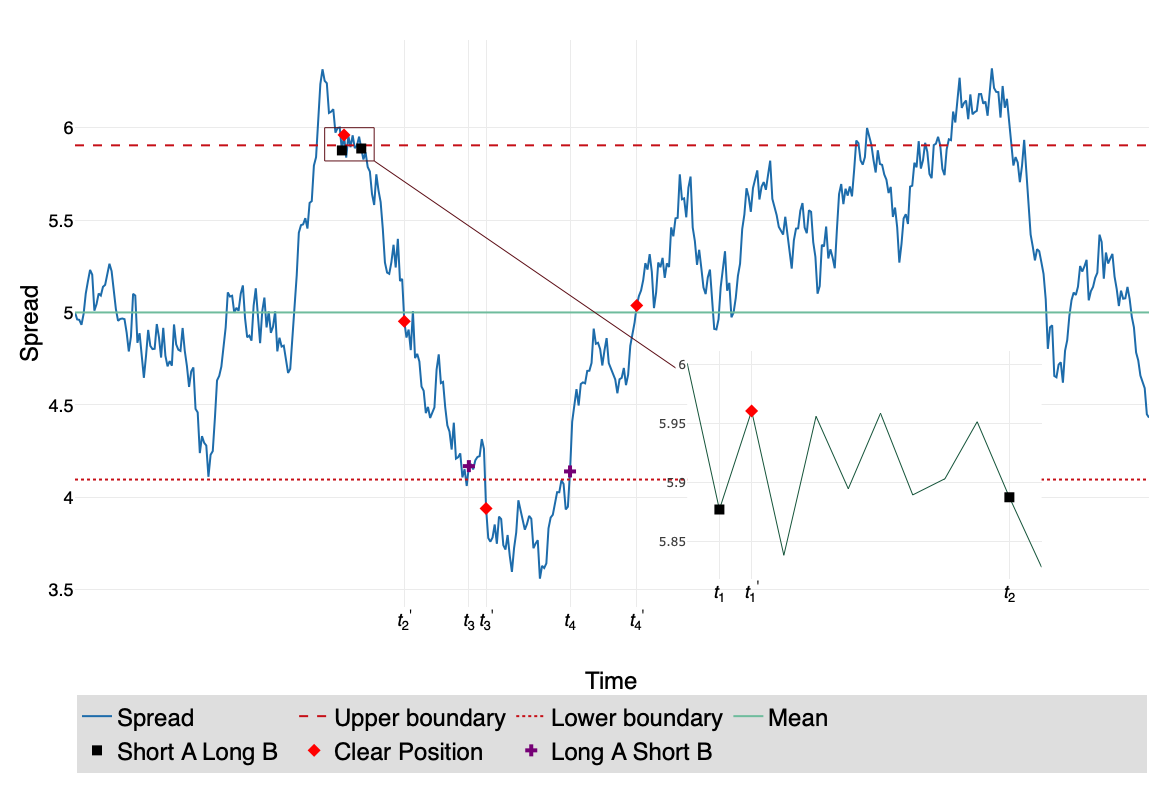

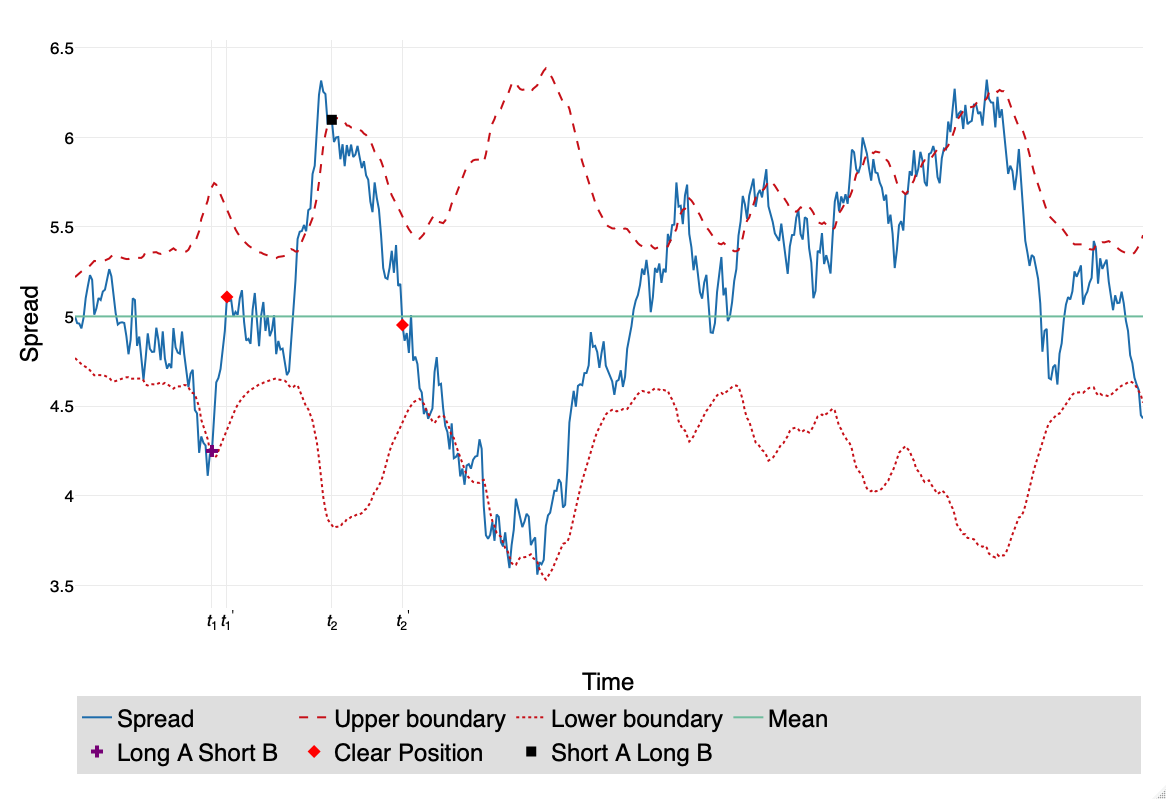

As we discussed in Section 1, the basic idea for pairs trading is to open a trade (short one asset and long the other one) when the spread deviates from the equilibrium and close the trading when the spread settle back to the equilibrium. The trading strategies for pairs trading are constructed based on this idea. We use Figure 1 and Figure 2 to illustrate two benchmark trading strategies (hereafter Strategy A and Strategy B). In Figure 1 and Figure 2, the same estimated spread is plotted as solid lines, and a preset upper-boundary and a preset lower-boundary are plotted as dashed lines. We will discuss how to choose the optimal and in Section 3.2. The upper-boundary and lower-boundary act as thresholds to determine whether the spread deviates from the long-term equilibrium enough, and we use these two criteria to open a trade. Also, a preset value acts as a threshold to determine whether the spread settles back to the long-term equilibrium, and we use this criterion to close a trade. In this paper, we take as the mean of the spread, and plot it as solid green line in both Figure 1 and Figure 2.

In Strategy A (illustrated in Figure 1), a trade is opened at when the spread is higher than or equal to . In this case, we sell 1 share of stock A and buy share of stock B. At when the spread is less than or equal to the mean (i.e., ), we close the trade and clear the position. The return from this trade is thus . At when the spread is less than or equal to , , we open a trade by buying 1 share of stock A and sell share of stock B. We close this trade and clear the position at when the spread is higher than or equal to the mean. The return from this trade is .

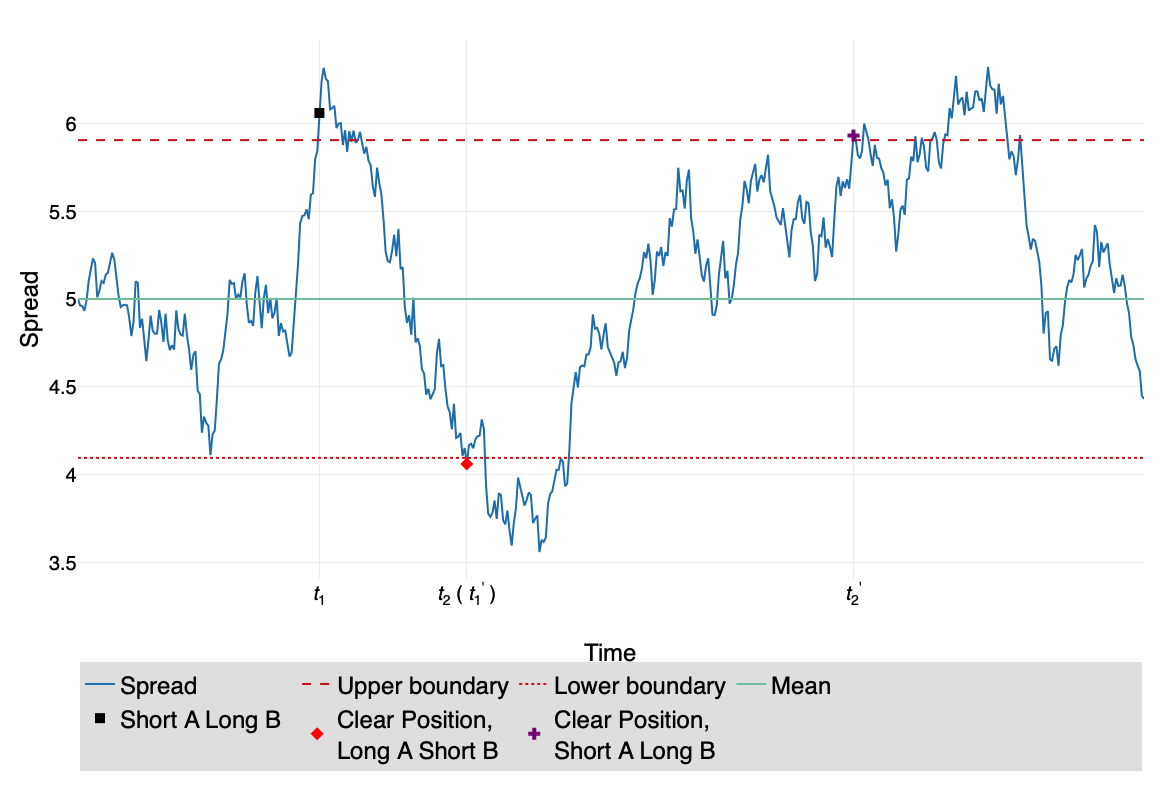

In Strategy B (illustrated in Figure 2), we open a trade when the spread cross the upper-boundary from below (e.g., at ) or cross the lower-boundary from above (e.g., at ). Unlike the Strategy A, We will hold the portfolio until we need to switch the position. Thus in Strategy B, we clear the exposure at the same time when we open a new trade ( i.e., and coincide).

3.3 Conventional Trading Rules

In the implementation of pairs trading, trading rule for a specific trading strategy is the computation of optimal thresholds and based on that strategy to fulfill an investing objective111Investing objective could be various, such as maximizing the expected cumulative return or maximizing the Sharpe ratio.. There are three popular approaches for computing the optimal thresholds and when the model (2) is linear, homoscedastic and Gaussian (i.e., is linear, is a constant and is a Gaussian noise). The optimal trading rule for a general specification of model (2) will be given in Section 3.4.

-

•

Rule I: Ad hoc boundaries

Rule I takes to be one (1- rule) or two (2- rule) standard deviations above the mean, to be one or two standard deviations below the mean and to be the mean of the spread. This rule is simple and popular in practice. In particular, the 2- rule was first applied by Gatev et al. (2006) and later checked by Moura et al. (2016), Zeng and Lee (2014) and Cummins and Bucca (2012). The 1- rule was discussed in Zeng and Lee (2014) and the performance of 1- rule and 2- rule was compared in the same paper.

-

•

Rule II : Boundaries based on the first-passage-time

This rule was first adopted by Elliott et al. (2005) and later by Moura et al. (2016). Suppose follows a standardized Ornstein–Uhlenbeck process:

Let be the first passage time of :

has a pdf known explicitly:

can be maximized at given by:

Here is the most possible time, given the value of current spread, that the spread will settle back to the mean. In model (2), if the spread follows (discrete time) Ornstein–Uhlenbeck process, then we can first standardize , and then above formula for can be used to construct the optimal . Similar idea can be applied to compute the optimal upper-boundary and lower-boundary .

-

•

Rule III: Boundaries based on the renewal theorem

This rule was first proposed by Bertram (2010), and then extended by Zeng and Lee (2014). In this rule, each trading cycle is separated into two parts, where can be used to denote the time from taking (long or short) position to clearing the position, and can be used to denote the time from clearing position to opening next trading. That is,

Suppose is the total trading duration we have for a pair, and is the number of transactions we can have in the period . Then, by the renewal theorem, the return per unit time is given by:

where and can be computed based on the density of first passage time, mentioned in Rule II.

The problem of this rule is, as Zeng and Lee (2014) have pointed out, that when there is no transaction cost, this strategy implies (and ) will be arbitrarily close to . This implies that the trader values the trading frequency more than the profit per trade. Consequently, this could increase the risk of the portfolio significantly.

3.4 The New Trading Strategy

We summarize the new trading strategy (hereafter Strategy C) in Figure 3(b). The basic idea of Strategy C is similar to both Strategy A and Strategy B: open a trade when the spread is far away from the equilibrium and close the trade when the spread settle back to the equilibrium. Unlike the Strategy A and B, in Strategy C, we open a trade when the spread cross the upper-boundary from above (or cross the lower-boundary from below), and we clear the position when the spread cross the mean, or cross the boundaries ( and ) after a trade has been opened (i.e., the spread cross the upper-boundary from below or the lower-boundary from above). For example, in Figure 3(a) for a homoscedastic model, at , , and we open a trade; and at , , , and we clear the exposure. In Figure 3(b) for a heteroscedastic model, we open a trade at and ; and we close the trade at , and .

We now discuss the properties of this trading strategy when the model (2) is homoscedastic (i.e., the function is constant) and when it is heteroscedastic (i.e., is a general function). In the first situation, the main benefit of Strategy C is that we can avoid holding the portfolio when the spread is larger than the upper boundary (or smaller than the lower boundary). This would significantly decrease the risk and drawdown of the portfolio. The main drawback of Strategy C is that the return can be lower because we open the trade when the spread is closer to the mean of the spread than in Strategy A. Therefore, there is a tradeoff between the risk and the return. In the situation when the model (2) is heteroscedastic, this strategy can not only reduce the risk, it can also improve the return. This is because the opening of a trade now depends on the level of the volatility and, as a result, the boundaries are no longer constant over time. The logic of this new strategy is illustrated in Figure 3(a) and 3(b), for homoscedastic and heteroscedastic cases, respectively.

3.5 Simulation Based Method for Optimal Trading Rule

For a general specification of model (1)-(2), the conventional trading rules in Section 3.2 are difficult to be applied. For example, the 1- rule or 2- rule cannot be applied when the model (2) is heteroscedastic; for a complicated specification of model (2), it’s impossible to derive the density of the first passage time explicitly, thus Rule II and Rule III are unavailable in this case.

To compute the optimal trading rule under model (2) for all of the trading strategies, we propose to select the optimal boundaries ( and , we set as the mean of spread by default) based on the Monte Carlo simulation of the spread (equation (2) given the estimation of the unknown parameters). Different criterion or investing objectives, such as expected return, Sharpe ratio or Calmar ratio222Let be the cumulative return of portfolio at time , and we define the maximum drawdown of the cumulative return across time to as : Then the Calmar ratio can be defined in a similar way as the Sharpe ratio: where is the expected return of portfolio . could be used to determine the optimal boundaries for a given trading strategy.

Now we use the following four specifications of model (2) to describe the detail about the computation of the new trading rules.

-

•

Model 1: ,

-

•

Model 2: ,

-

•

Model 3: ,

-

•

Model 4: ,

Model 1 is a linear, homoscedastic, and Gaussian model. This is the most popular model used for pairs trading. See Elliott et al. (2005) and Moura et al. (2016) for examples of this model. Model 2 is a nonlinear model, Model 3 is a heteroscedastic model, and Model 4 is a non-Gaussian model. The last three models are different extensions of Model 1 and have never been discussed in the literature on pairs trading. These four models can be considered as the benchmark models for pairs trading. Further extensions are available based on the combination of these four models, and our simulation based method for optimal trading rule can also be applied to them.

For every specification of Model 1-4, we will calculate the optimal trading rules through the simulations of the spread for Strategy A, B and C respectively, and compare the resulting performances of the three strategies based on the expected return, Sharpe ratio. More specifically, across all of the examples, we represent the optimal trading rule (upper-boundary and lower-boundary ) as the ratio to one standard deviation of the spread, and we consider the upper-boundary between and lower-boundary between for a grid size of 0.1. For every specification of Model 1-4 and every realization of the process of the spread , where , we choose from and from , where , and compute the resulting cumulative return and Sharpe ratio for difference strategies. More specifically, We denote the cumulative return and Sharpe ratio as and respectively, where is for different models, is for difference strategies and is for different realization of the spread in simulation. For Model and strategy , the resulting expected cumulative return and Sharpe ratio are computed as

Then the optimal trading rule (, ) is selected to maximize or , that is,

where or . Across all of the examples, we set the total trading period to be 1000 trading days (or approximately four years), and we set the simulation size to be . For simplicity, we assume the transaction cost is 20 bp (0.2%) 333This transaction cost is on one asset of the pair. Since a complete trading includes transactions on two assets, the total transaction cost of one complete trading is 40 bp., and annualized risk free rate is set to be 0.

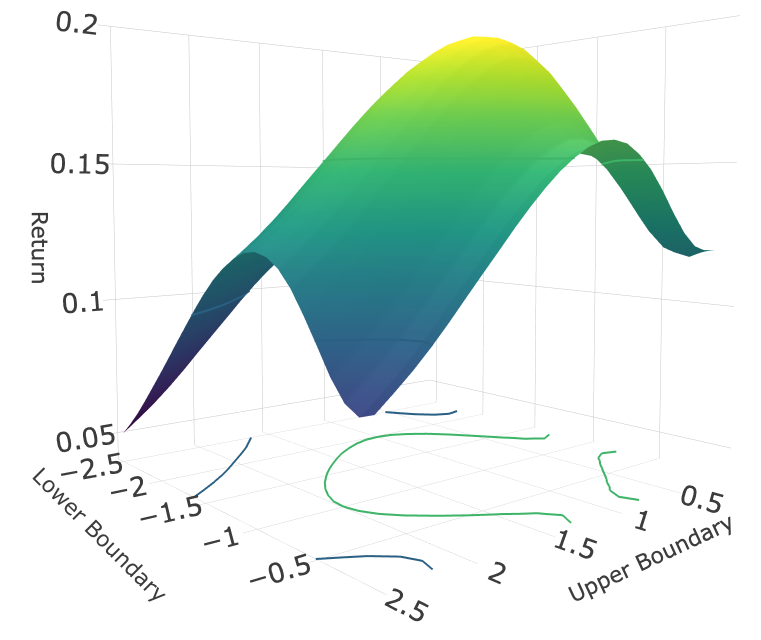

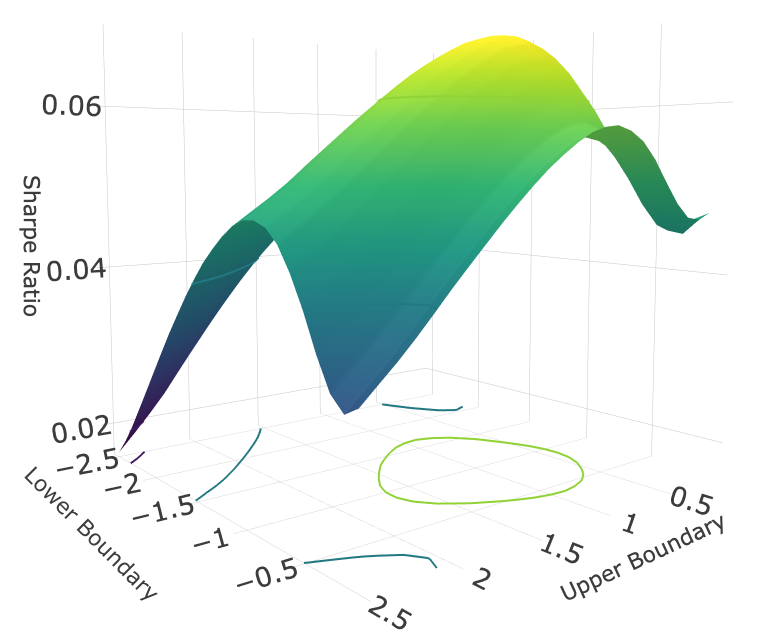

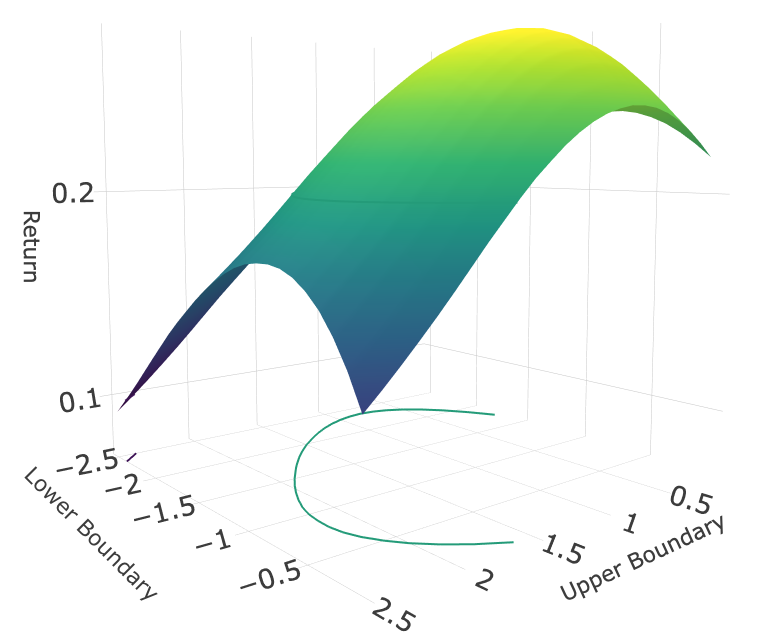

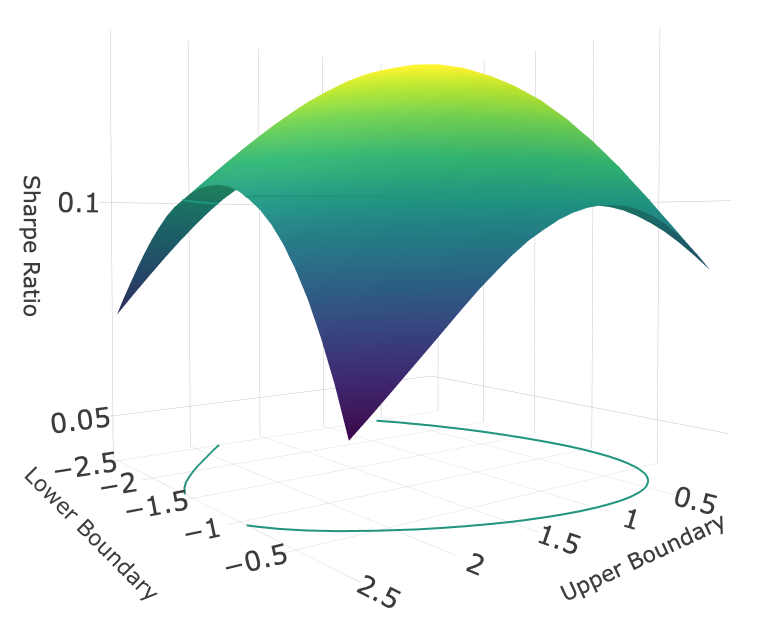

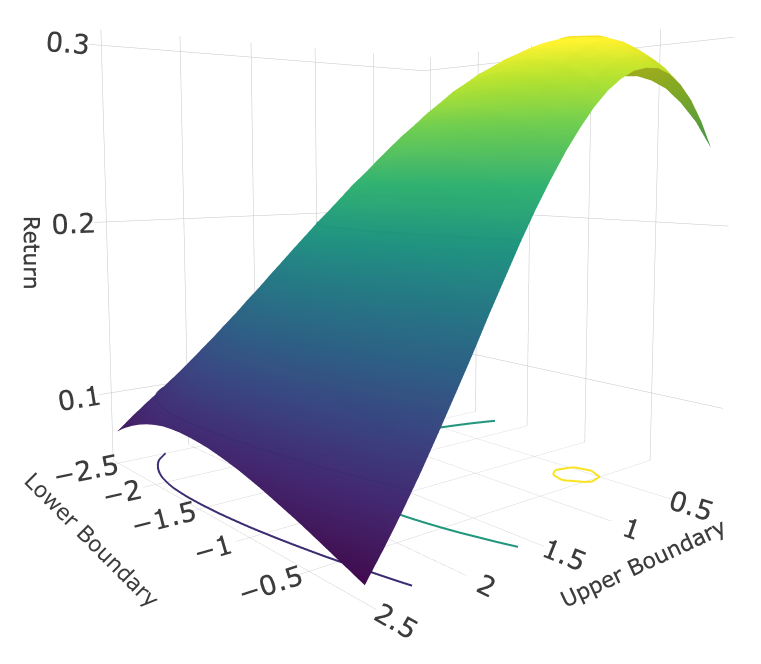

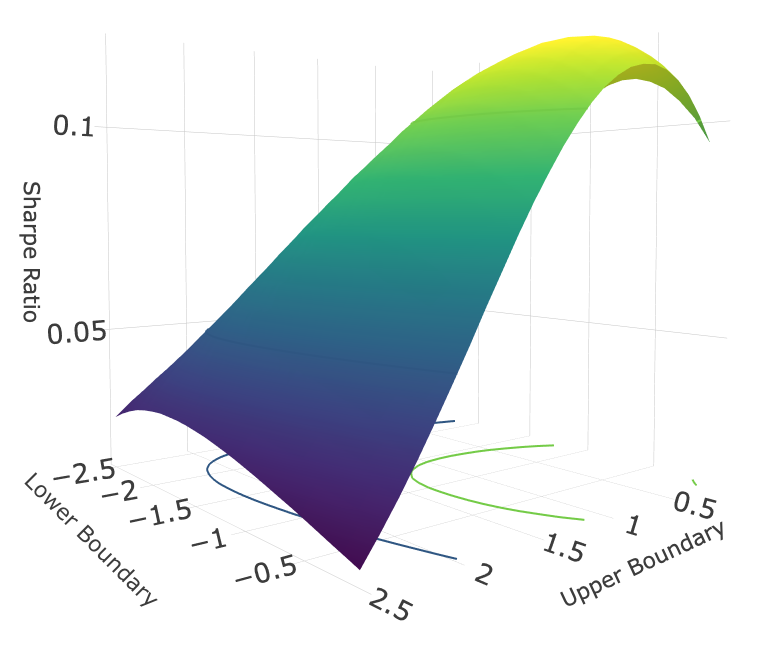

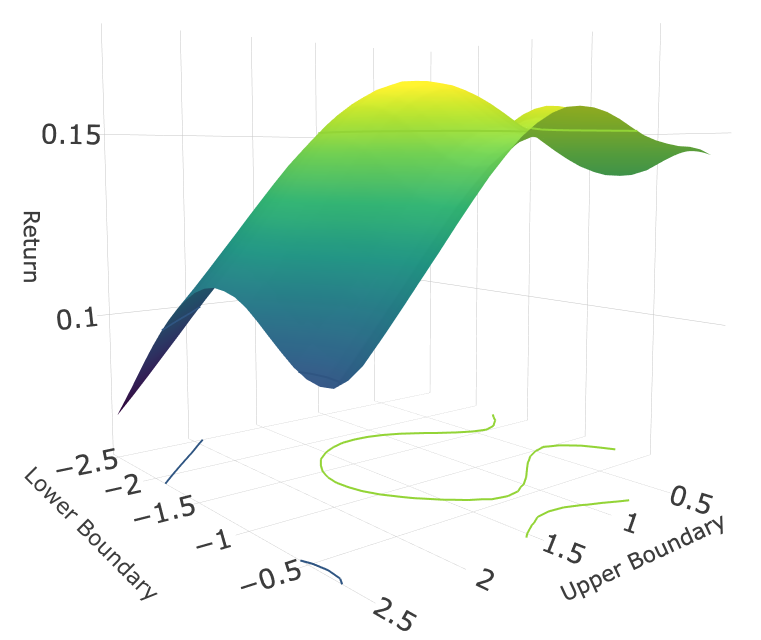

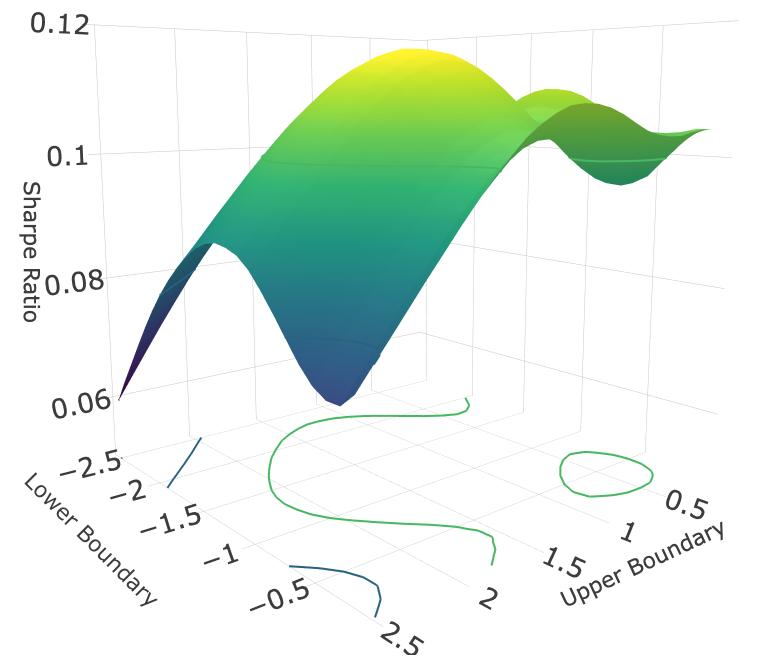

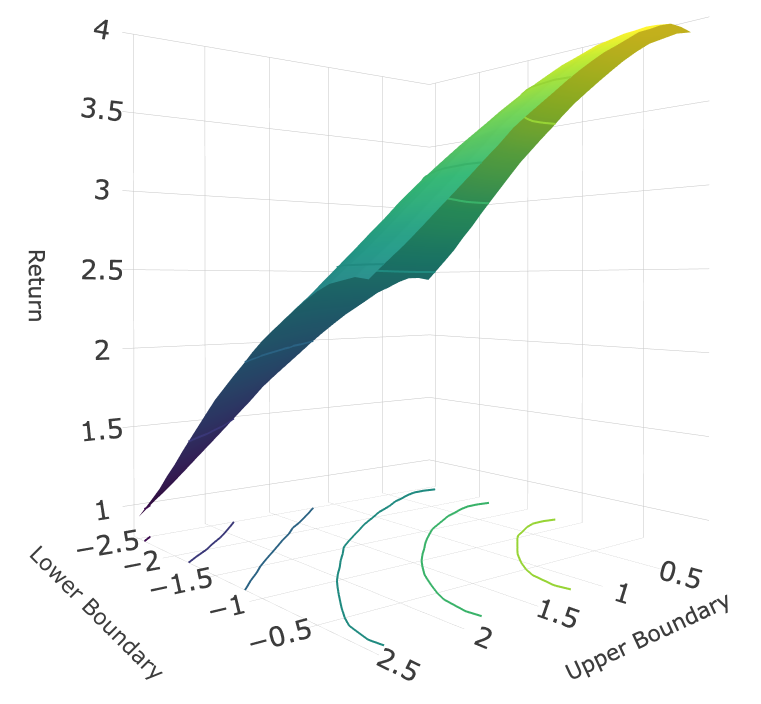

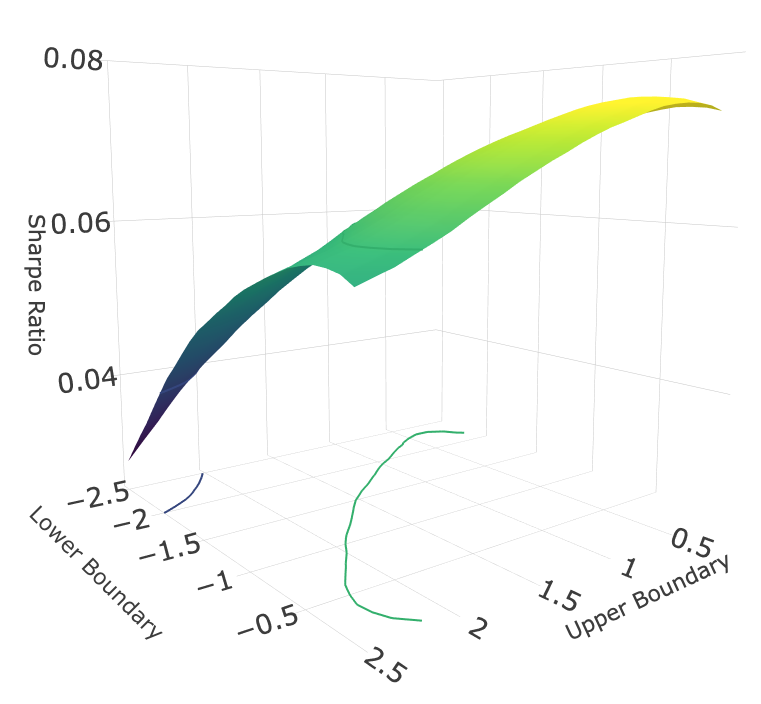

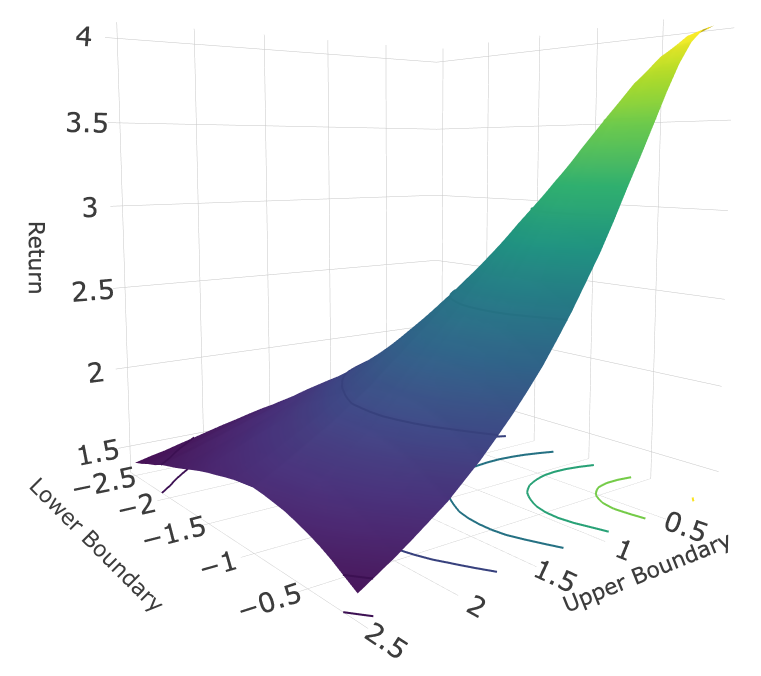

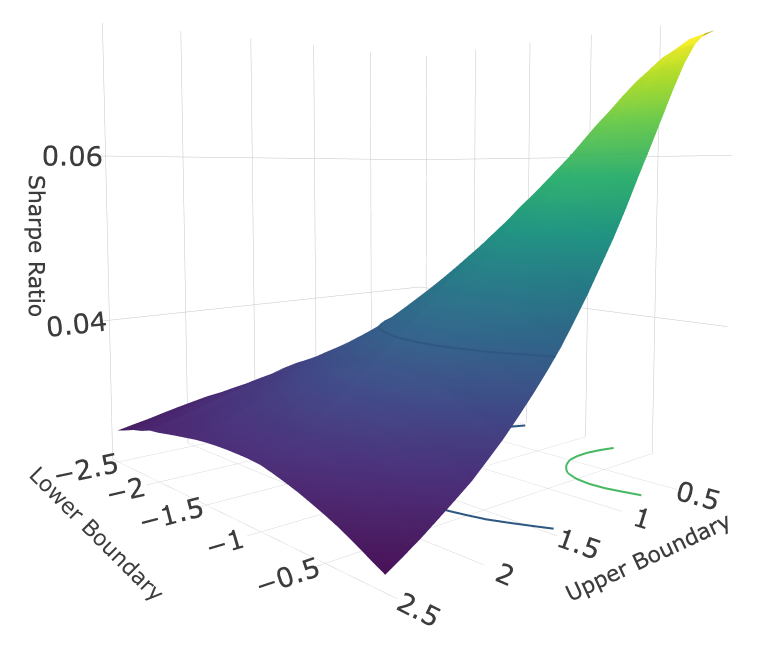

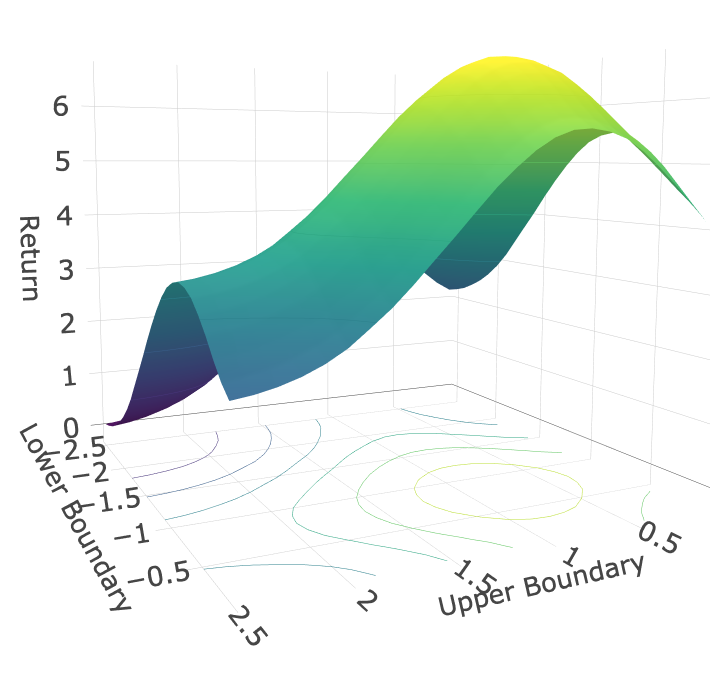

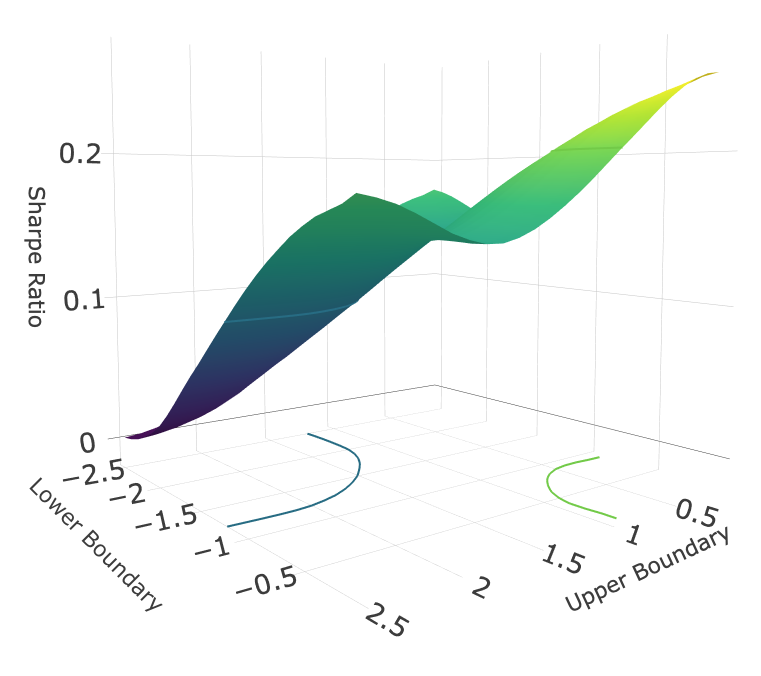

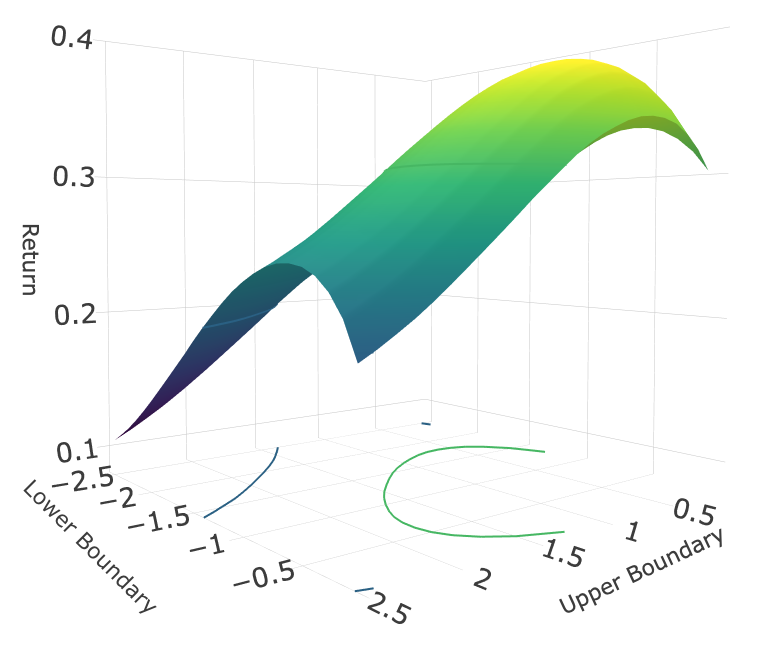

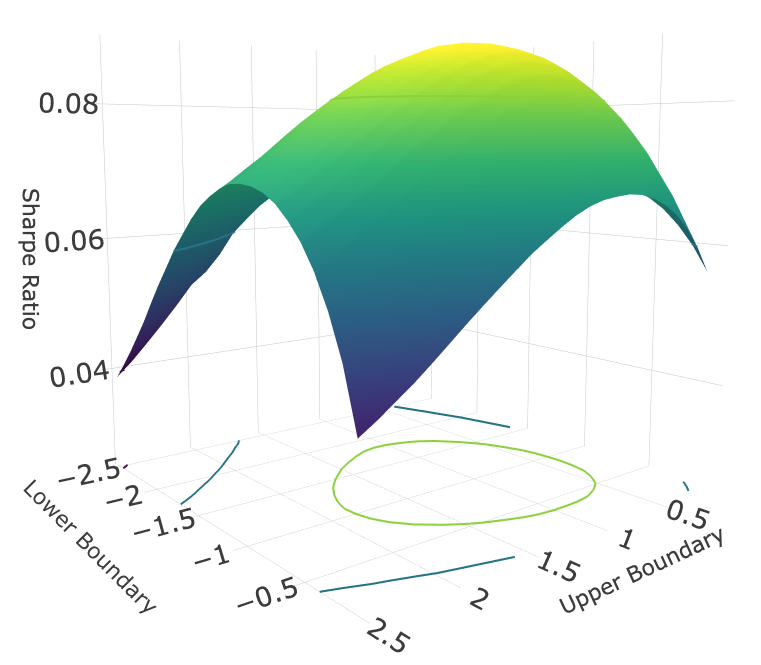

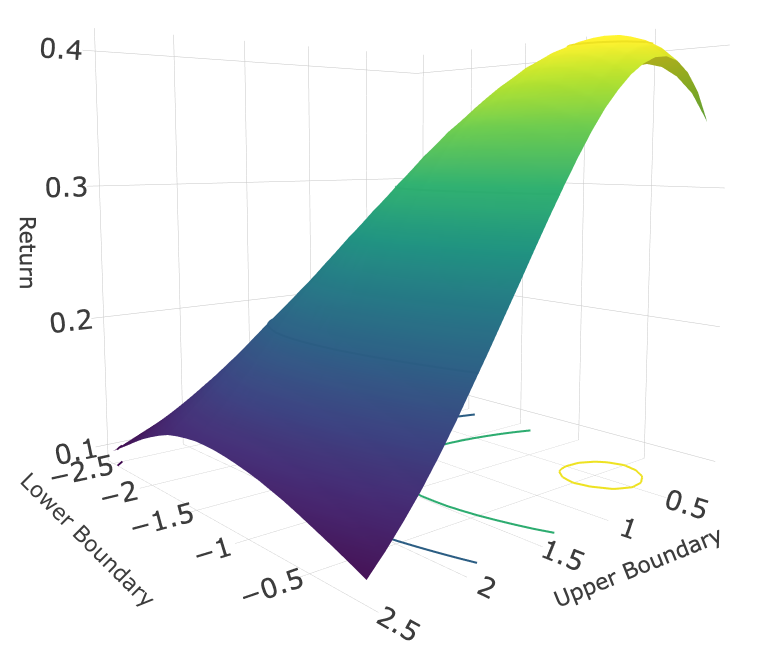

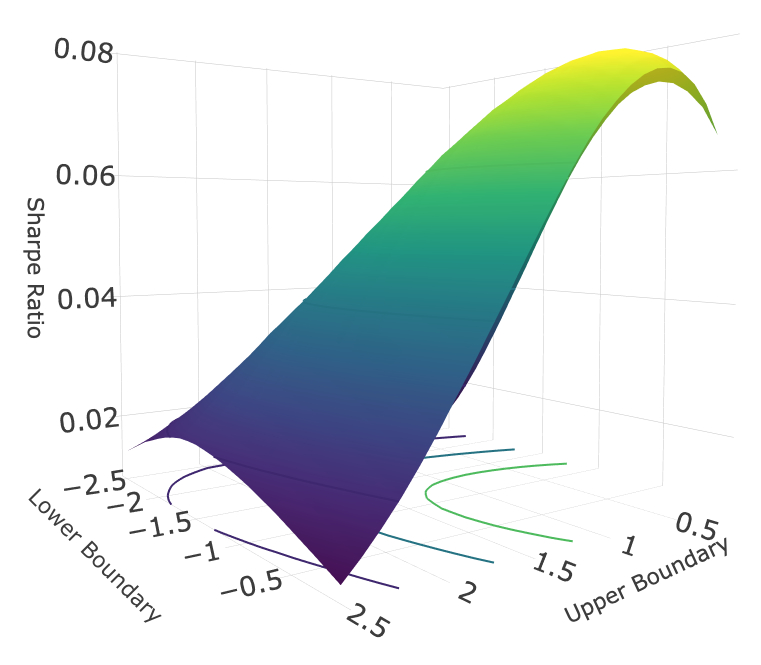

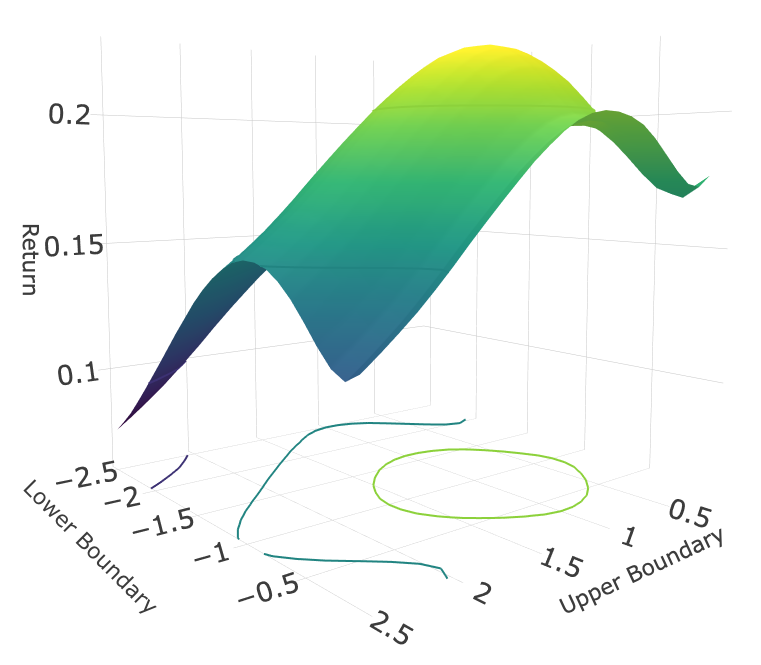

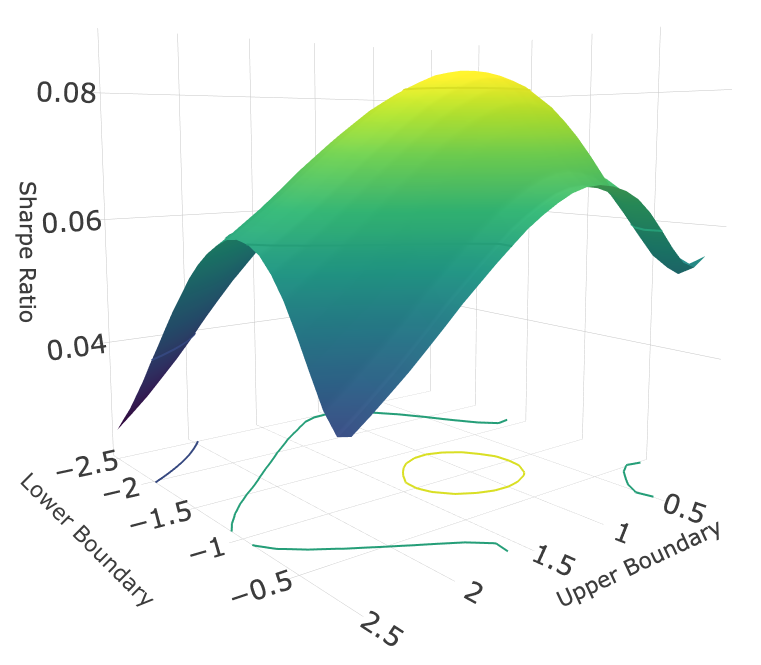

In Table 1, we report the optimal trading rule for every combination of the 4 models and 3 strategies, and the resulting expected cumulative return and Sharpe ratio444If the spread and the strategy is symmetric around the mean, then the optimal upper boundary and lower boundary should also be symmetric around the mean, i.e, . However, due to the approximation error in gridding, the absolute values of and may not be exactly the same in Table 1.. As we can find from this table, Strategy C outperforms other two strategies when the model is heteroscedastic in both the cumulative return and the Sharpe ratio; also, for other homoscedastic models (Model 1, 2 and 4), the Sharpe ratio of Strategy C is competitive, although the cumulative return is not. This supports our discussion of this new strategy in Section 3.3.

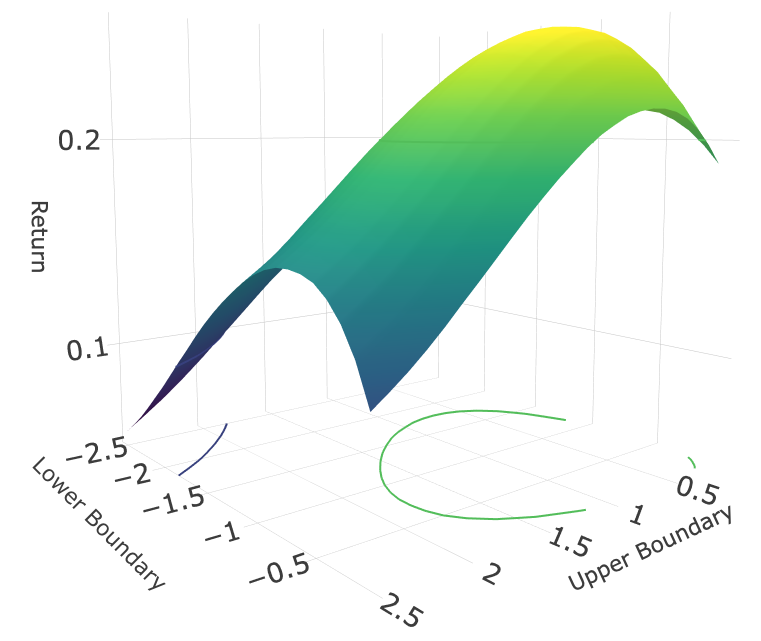

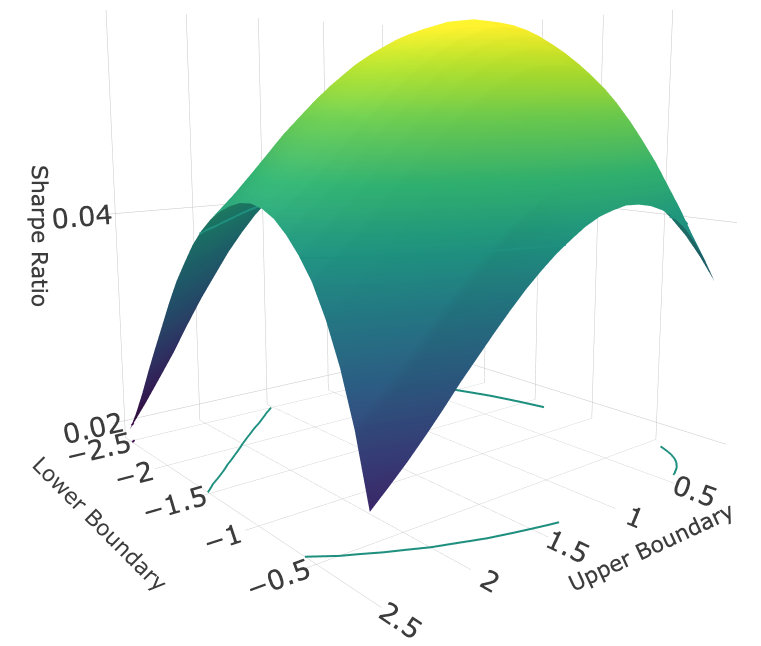

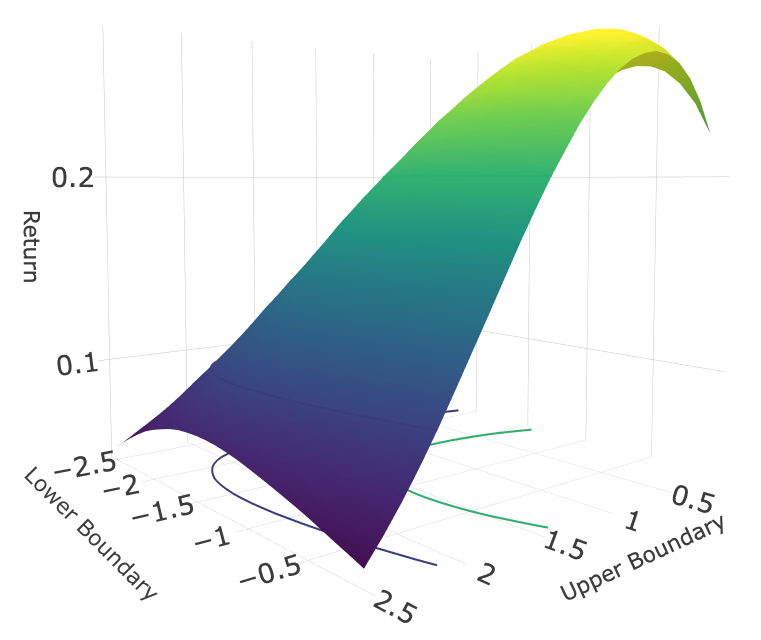

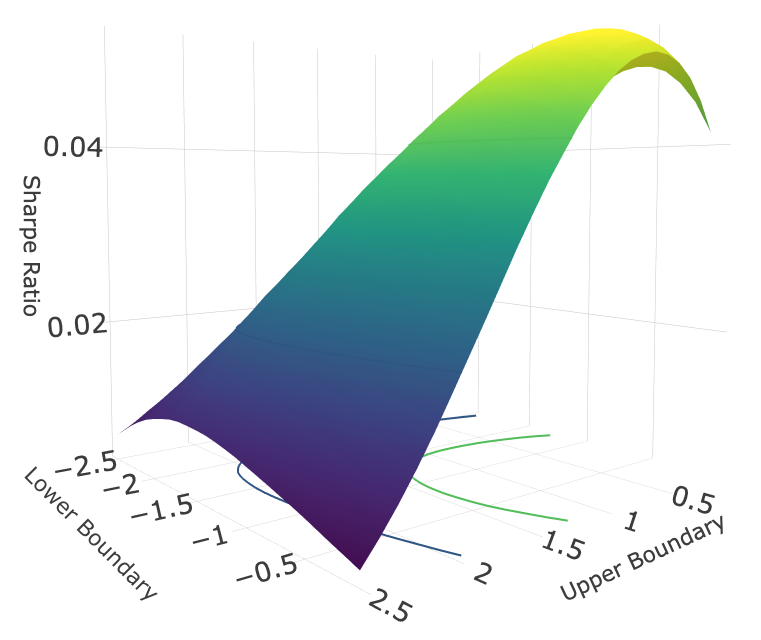

We leave the detailed results of simulation method in appendix. More precisely, the expected cumulative returns and Sharpe ratio as functions of various choices of and are given in Figure 1(f)-4(f) for every possible combination of the three strategies and four models. The return is displayed in number, not in percentage through all figures.

| Model | Strategy | CR | SR | ||||

|---|---|---|---|---|---|---|---|

| Model 1 | A | 0.7 | -0.7 | 0.2508 | 1.1 | -1 | 0.0573 |

| B | 0.5 | -0.5 | 0.2745 | 0.5 | -0.5 | 0.0522 | |

| C | 1 | -1 | 0.1934 | 0.9 | -0.9 | 0.0679 | |

| Model 2 | A | 0.8 | -0.8 | 0.2749 | 1.2 | -1.3 | 0.1302 |

| B | 0.6 | -0.6 | 0.3016 | 0.6 | -0.6 | 0.1198 | |

| C | 1.2 | -1.3 | 0.1640 | 1.2 | -1.3 | 0.1162 | |

| Model 3 | A | 0.3 | -0.2 | 3.9413 | 0.4 | -0.4 | 0.0751 |

| B | 0.1 | -0.1 | 4.0139 | 0.1 | -0.1 | 0.0743 | |

| C | 0.8 | -0.8 | 6.6763 | 0.1 | -0.1 | 0.2499 | |

| Model 4 | A | 0.6 | -0.6 | 0.3792 | 1 | -1 | 0.0881 |

| B | 0.4 | -0.5 | 0.4071 | 0.5 | 0.5 | 0.0782 | |

| C | 1 | -1 | 0.2243 | 1 | -1 | 0.0829 |

-

•

Note: The third and forth columns are the optimal upper-boundary and lower-boundary based on maximizing the cumulative return, and the fifth column is the resulting cumulative return. The sixth and seventh columns are the optimal upper-boundary and lower-boundary based on maximizing the Sharpe ratio, and the eighth column is the resulting Sharpe ratio. The cumulative return is displayed in number, not in percentage.

3.6 Summary

We are now in a position to summarize the procedure for pairs trading based on model (1)-(2) and conclude this section.

- •

-

•

Step 2: Choose a trading strategy, and determine the optimal trading rule (the optimal and ) for a specific criterion based on Monte Carlo simulation based on the data until time . The detail of this step can be found in Section 3.2-3.5.

-

•

Step 3: For , we run QMCKF and estimate with , the estimate of the parameter we get in Step 1 . We use this and follow the preset trading strategy and optimal trading rule from Step 2 to generate the trading signal for trading.

4 Applications

In this section, we test the performance of Pairs Trading through nonlinear and non-Gaussian state space modeling for different trading strategies. Across all of the applications in this section, we assume the transaction cost is 20 bp and the annualized risk free rate is 2%, and we test the performance of Strategy A, B and C for two specifications of model (2):

-

•

Model I: ,

-

•

Model II: ,

4.1 Pepsi vs Coca

In this example, we examine the performance of Pairs Trading for PEP (Pepsi) and KO (Coca). The data is the daily observation of adjusted closing prices of PEP and KO from 01/03/2012-06/28/2019.

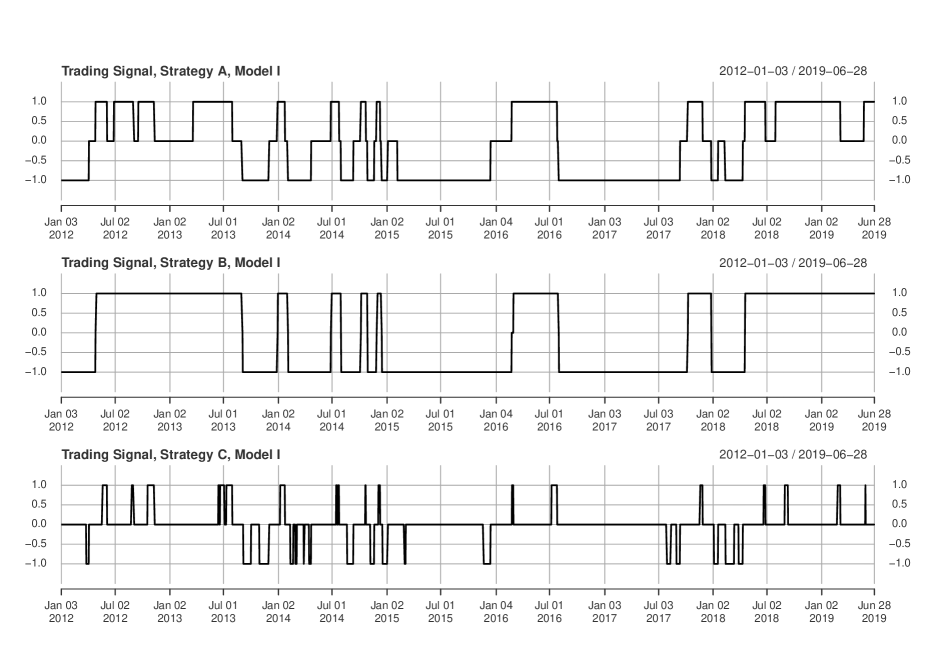

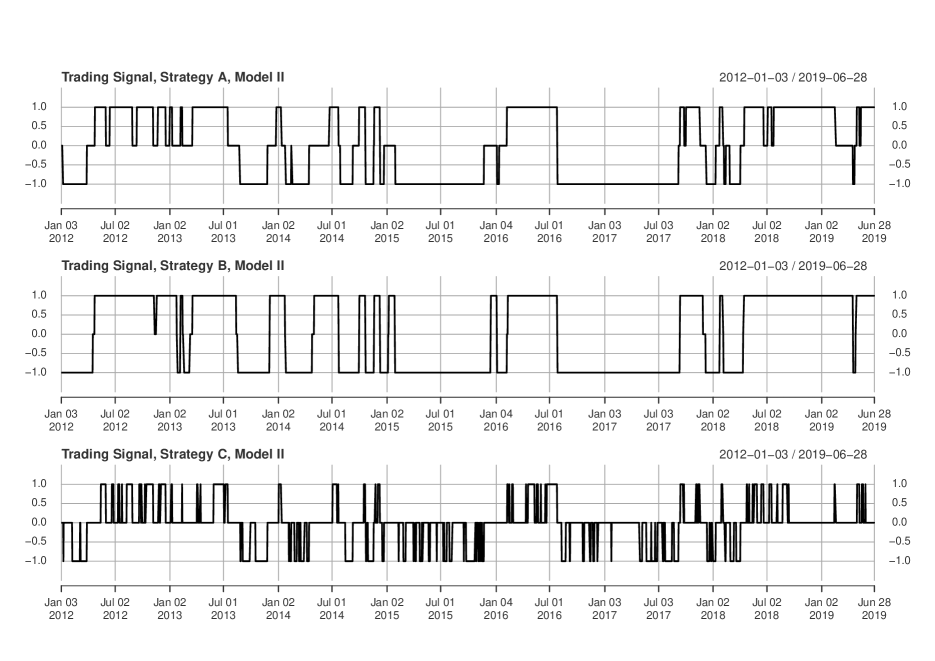

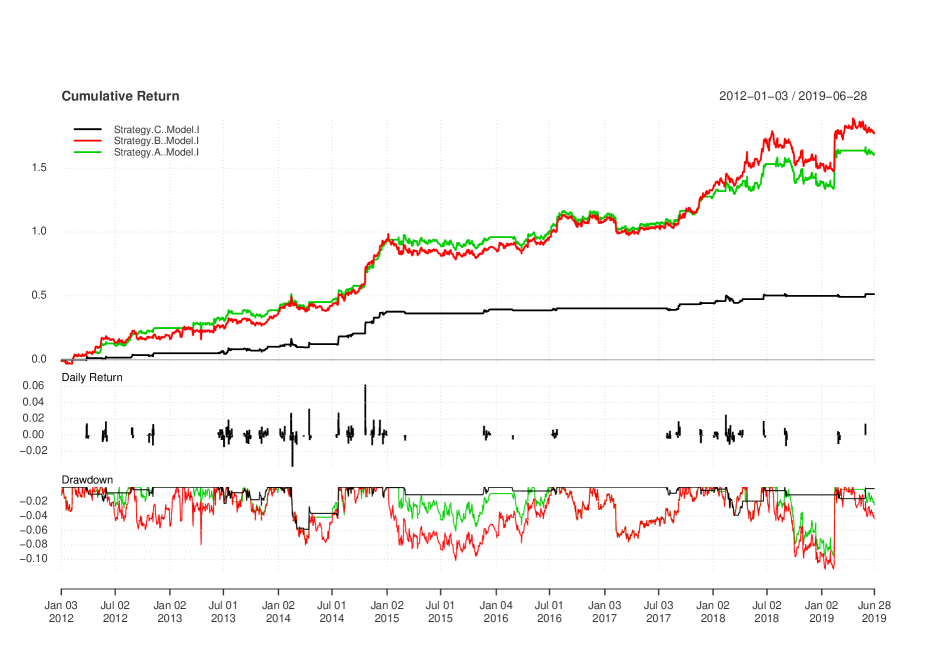

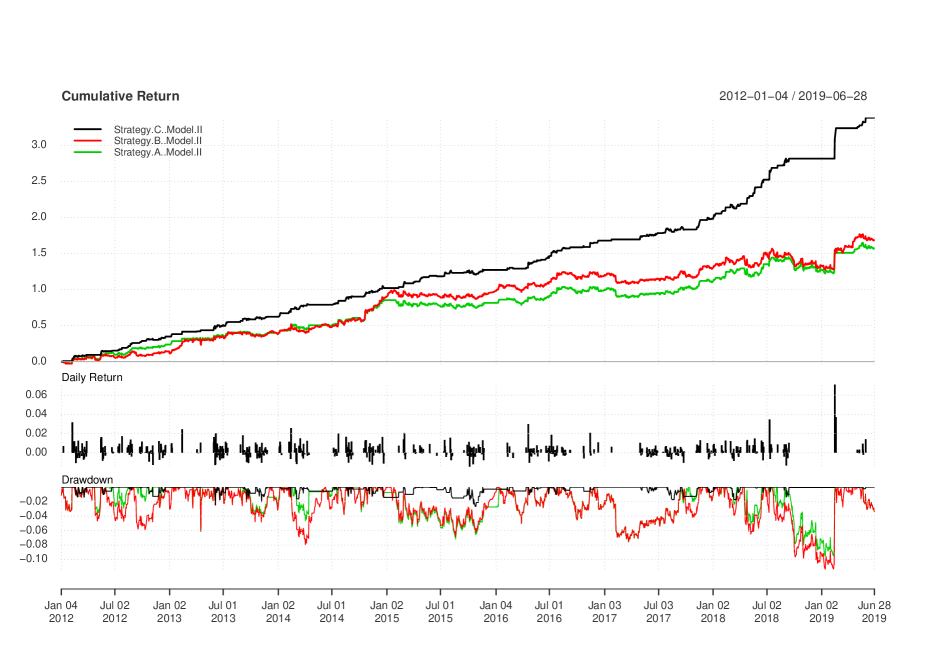

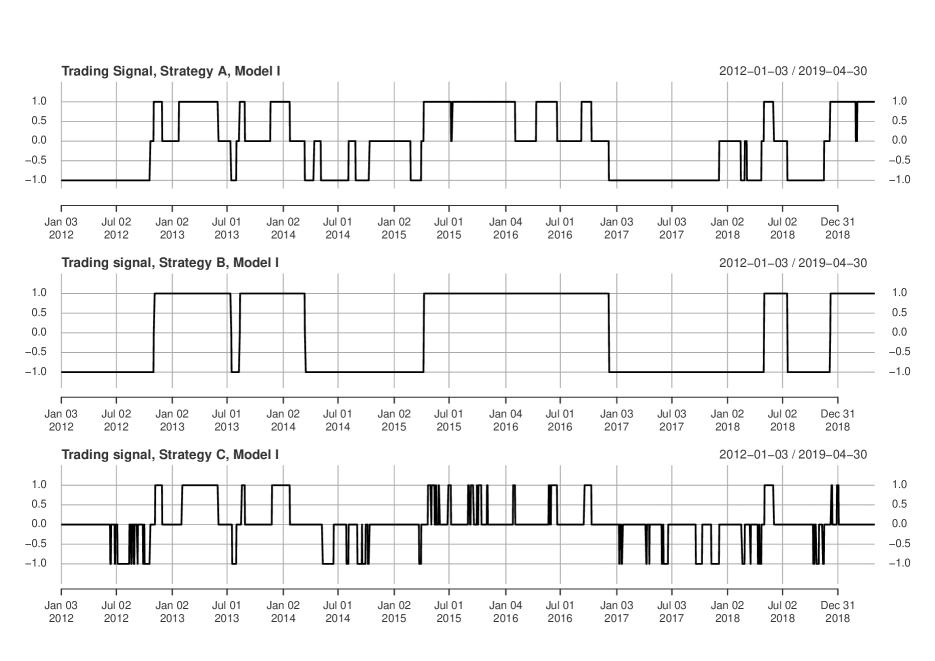

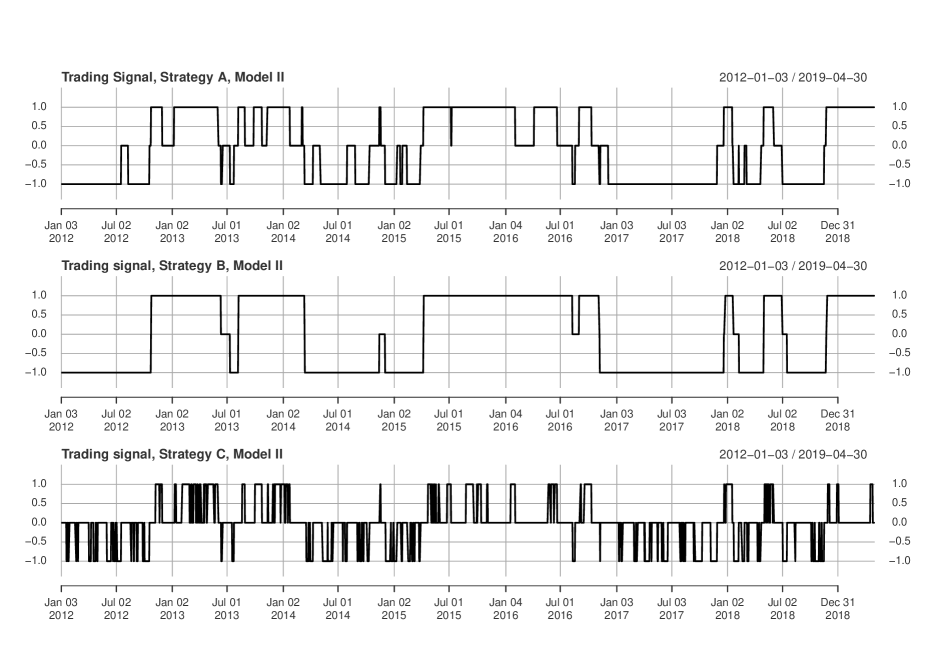

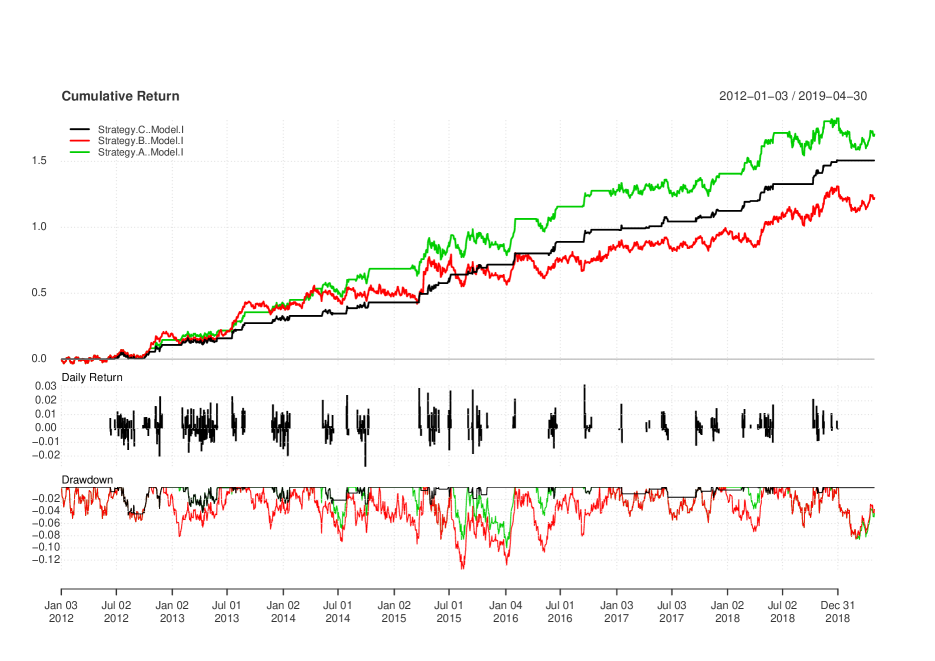

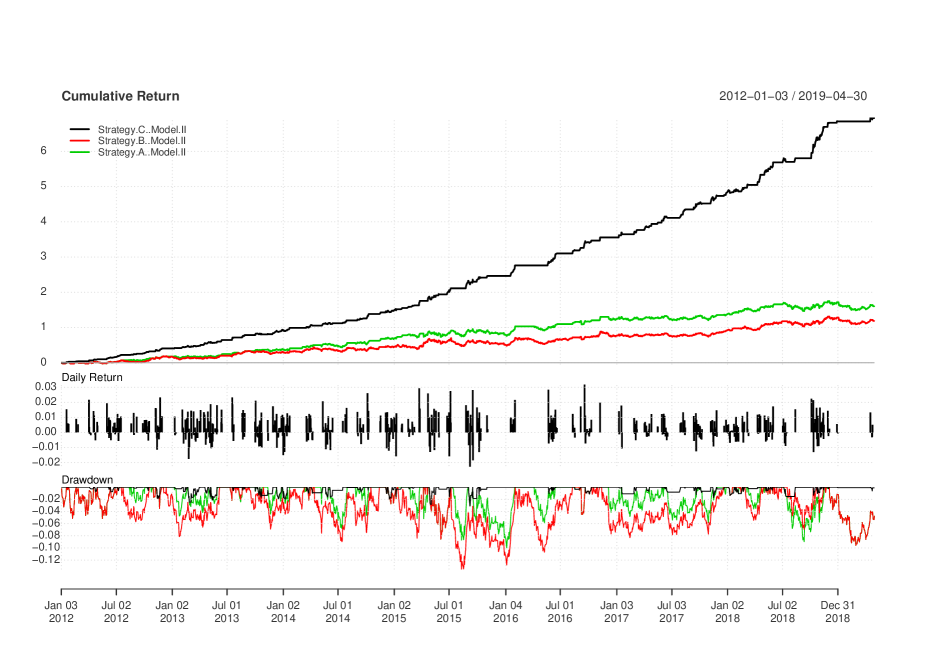

Table 2 reports the parameter estimation of both Model I and Model II for this pair. The trading signal for Model I is given in Figure A5 and that for Model II is given in Figure A6, and the annualized performance (annualized return, annualized Std Dev, annualized Sharpe ratio and Calmar ratio, and annualized Pain index) is given in Table 3. The plot of the cumulative return and drawdown of every strategy through the whole trading period for both models are given in Figure A7 and A8. It’s easy to find that in Model II, the annualized return of Strategy C is almost 50% higher than those of Strategy A and B, while Strategy C keeps the risk (measured by Annualized Std Dev) almost half of Strategy A or B. By comparing the Sharpe ratio, Calmar ratio and Pain index, we can find this improvement is significant. While the difference of performances of Strategy A and Strategy B across the two models is limited. This implies the effect of heteroskedasticity modelling to the performances of Strategy A and B is not significant. This is because in Strategy A and B, the hedging portfolio will be held until the spread is around the mean, so the frequency of changing positions is low in Strategy A or B than that in Strategy C. This can be easily confirmed by counting the trading numbers based on Figure A5 and Figure A6.

| Model I | Model II | |

|---|---|---|

| 1.98 | 2.03 | |

| 0.012 | 0.011 | |

| -0.0001 | -0.001 | |

| 0.9572 | 0.9330 | |

| 0.029 | 0.0003 | |

| - | 0.1283 |

| Return | Std Dev | Sharpe | Calmar | Pain index | |

|---|---|---|---|---|---|

| Strategy A, Model I | 0.1311 | 0.0988 | 1.1003 | 1.3742 | 0.0195 |

| Strategy B, Model I | 0.1385 | 0.1153 | 1.0052 | 1.2204 | 0.0334 |

| Strategy C, Model I | 0.0618 | 0.0534 | 0.7649 | 0.8243 | 0.0087 |

| Strategy A, Model II | 0.1340 | 0.1038 | 1.0751 | 1.4040 | 0.0200 |

| Strategy B, Model II | 0.1407 | 0.1139 | 1.0366 | 1.2398 | 0.0258 |

| Strategy C, Model II | 0.2186 | 0.0659 | 2.9518 | 8.2384 | 0.0030 |

-

•

Note: The data is from 01/03/2012-06/28/2019. The return is displayed in number, instead of in percentage.

4.2 EWT vs EWH

In this example, we examine the performance of Pairs Trading for EWT and EWH. The data is the daily observation of adjusted closing prices of EWT and EWH from 01/01/2012-05/01/2019. EWT is the iShares MSCI Taiwan ETF managed by BlackRock, which seeks to track the investment results of an index composed of Taiwanese equities, and EWH is that for Hong Kong equities. Following the example of PEP vs KO, we will test the performance of Strategy A, B and C for Model I and Model II. We report the parameter estimation in Table 4 and the trading signal in Figure A9 and Figure A10. By comparing the annualized performance in Table 5, we can find the heteroskedasticity modeling can improve the performance of Strategy C significantly, while has no effect on Strategy A or B. Also, the riskiness of Strategy B (small Sharpe ratio and Calmar ratio and high annualized standard variance) is confirmed again in this example. We also plot the cumulative return and drawdown of every strategy through the whole trading period for both models in Figure A11 and A12.

| Model I | Model II | |

|---|---|---|

| 1.40 | 1.42 | |

| 0.0007 | 0.0006 | |

| -0.0004 | -0.0015 | |

| 0.9898 | 0.9589 | |

| 0.0337 | 0.0016 | |

| - | 0.1136 |

| Return | Std Dev | Sharpe | Calmar | Pain index | |

|---|---|---|---|---|---|

| Strategy A, Model I | 0.1480 | 0.1111 | 1.1277 | 1.3042 | 0.0156 |

| Strategy B, Model I | 0.1109 | 0.1362 | 0.6531 | 0.7836 | 0.0328 |

| Strategy C, Model I | 0.1294 | 0.0740 | 1.4458 | 3.0926 | 0.0080 |

| Strategy A, Model II | 0.1402 | 0.1223 | 0.9622 | 1.2354 | 0.0196 |

| Strategy B, Model II | 0.1093 | 0.1349 | 0.6473 | 0.7717 | 0.0306 |

| Strategy C, Model II | 0.3184 | 0.0752 | 3.8892 | 10.3005 | 0.0032 |

-

•

Note: The data is from 01/03/2012-06/28/2019. The return is displayed in number, instead of in percentage.

4.3 Pairs Trading on US Banks Listed on NYSE

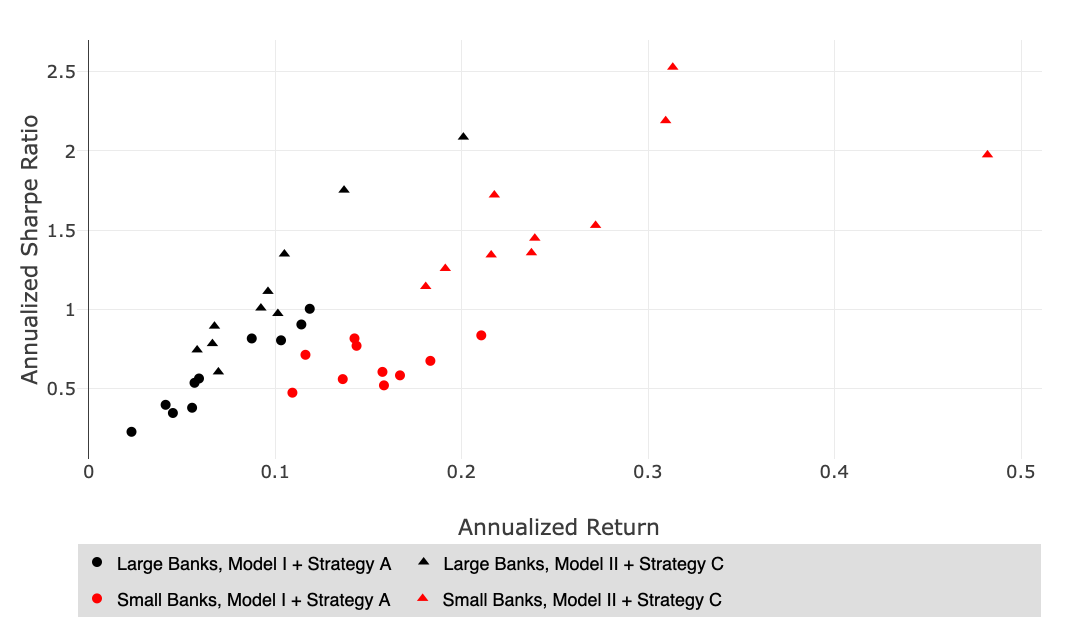

We use this example to illustrate the improvement of our new modelling and strategy by implementing pairs trading on US banks listed on NYSE during 01/01/2013-01/10/2019. To avoid data snooping and make our results more concrete, we use a simple way to choose assets and construct pairs. More precisely, based on the market capacity, we select the 5 largest banks to construct the group of large banks and the 5 smallest banks to construct the group of small banks. The large bank group includes: JPM, BAC, WFC, C and USB555JPM is for J P Morgan Chase & Co; BAC is for Bank of America Corporation; WFC is for Wells Fargo & Company; C is for Citigroup Inc.; USB is for U.S. Bancorp. , and the small bank group includes: CPF, BANC, CUBI, NBHC, FCF666CPF is for CPB Inc.; BANC is for Banc of California, Inc.; CUBI is for Customers Bancorp, Inc.; NBHC is for National Bank Holdings Corporation; FCF is for First Commonwealth Financial Corporation.. We compare the performance between Model I combined with Strategy A and Model II combined with Strategy C. Model I combined with Strategy A is a popular approach in the existing literature on pairs trading, and it can be a good benchmark for comparison.

In Table A1, we report the performance of these two approaches on 10 pairs among the large banks. The performance on 10 pairs among the small banks is given in Table A2. It’s easy to find that Model II combined with Strategy C outperforms Model I combined with Strategy A through almost all of the pairs, either in the sense of annualized return or annualized Sharpe ratio. And the improvement of Model II combined with Strategy C in Sharpe ratio is much more significant than that in return. For example, when trading is implemented on pairs among large banks, the improvement on return is 41.29%, and the improvement on Sharpe ratio is 89.23%; and if trading is implemented on pairs among small banks, the improvement on return is 74.41%, and the improvement on Sharpe ratio is 151.8%.

Also, by comparing the results in Table A1 and A2, we can find that the performance of pairs among small banks would be better than that among large banks, either Model I combined with Strategy A or Model II combined with Strategy C is applied for trading. For example, if we exercise Model I combined with Strategy A, the mean of returns of all pairs among large banks would be 0.0703, that among small banks can be improved to 0.1524; and if Model II combined with Strategy C is exercised, we could get an improvement of 0.1664 (from 0.0994 to 0.2658) by switching from trading on large banks to trading on small banks. This is because the movement of prices of small banks is more volatile than that of large banks, and thus the volatility of the spread between small banks is bigger than that between large banks.

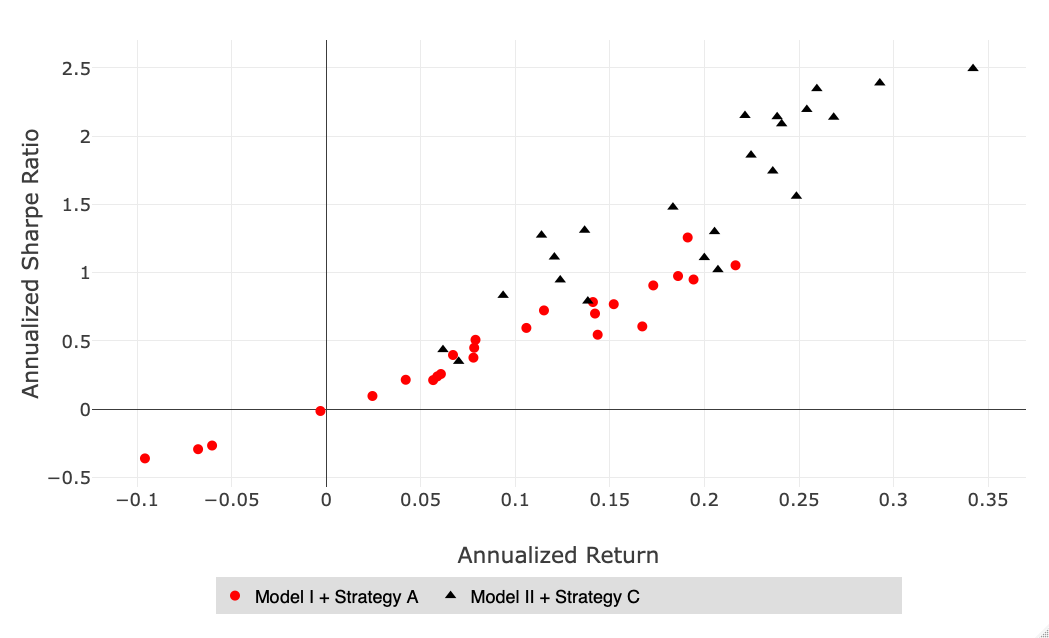

In Table A3, we report the performance of the two approaches of pairs trading on all possible pairs between large banks and small banks, that is, we pair one large bank with one small bank. For some pairs, such as JPM/CUBI and BAC/CUBI, the resulting spread is far from mean-reverting, thus the performance of pairs trading is poor for these pairs. Similiar to our findings from Table A1 and A2, in this exercise, we can also find that the improvement of Model II combined with Strategy C with respect to Model I combined with Strategy A on Sharpe ratio would be more significant than return (208.4% on Sharpe ratio, and 103.6% on return).

The results of Table A1-A3 are also plotted in Figure A13 and A14 to give a more straightforward comparison of the performances.

To further investigate the performance of pairs trading, we check the out-of-sample performance of the two approaches on the 10 bank stocks. More precisely, we separate 01/10/2012-01/12/2019 into two periods: 01/10/2012-01/01/2018 as in-sample period and 01/01/2018-01/12/2019 as out-of-sample period. We use the in-sample data to train the model, estimate the parameter of the model, and determine the optimal trading rules. In out-of-sample period, we use the parameters and optimal trading rules based on in-sample data to generate the trading signal. The results are given in Table A4-A9. We can confirm our earlier findings through these tables also: (1) Model II combined with Strategy C outperforms Model I combined with Strategy A in both return and Sharpe ratio, and the improvement is more significant in Sharpe ratio. (2) The performance of pairs trading on small banks would be better than large banks. Also, by comparing the performance through in-sample period to out-of-sample period, we can find that pairing large bank with small bank would be more robust than pairing large banks only or small banks only.

5 Conclusion

Pairs trading is a statistical arbitrage involves the long/short position of overpriced and underpriced assets. Our result in this paper shows that digging into the modeling and trading strategy can improve the performance of pairs trading significantly and implies the great potential of pairs trading on financial market. This can help the empirical research on the general profitability of pairs trading and discussion on the tests of market efficiency, and we leave this for future research.

References

- 1 Agnès Tourin and Raphael Yan, 2013, Dynamic pairs trading using the stochastic control approach, Journal of Economic Dynamics and Control, 37 (2013) 1972-1981.

- 2 Ait-Sahalia, Y., 1996, Testing Continuous-Time Models of the Spot Interest Rate, Review of Financial Studies, 9, 385-426

- 3 Avellaneda, M., and J.-H. Lee. 2010. Statistical arbitrage in the US equities market. Quantitative Finance 10:761–782.

- 4 Benoit B. Mandelbrot, 1971, When Can Price be Arbitraged Efficiently? A Limit to the Validity of the Random Walk and Martingale Models, The Review of Economics and Statistics, Vol. 53, No. 3 (Aug., 1971), pp. 225-236

- 5 Bogomolov, T. 2013. Pairs trading based on statistical variability of the spread process, Quantitative Finance 13:1411–1430.

- 6 Carlos Eduardo de Moura, Adrian Pizzinga and Jorge Zubelli (2016), A pairs trading strategy based on linear state space models and the Kalman filter, Quantitative Finance

- 7 Clegg, Matthew and Krauss, Christopher. 2018, Pairs trading with partial cointegration, Quantitative Finance 18 (1), 121–138.

- 8 Cummins, Mark and Bucca, Andrea, 2012, Quantitative spread trading on crude oil and refined products markets, Quantitative Finance. Dec2012, Vol. 12 Issue 12, p1857-1875.

- 9 David A. Hsieh, 1989, Testing for Nonlinear Dependence in Daily Foreign Exchange Rates, The Journal of Business, Vol. 62, No. 3 (Jul., 1989), pp. 339-368

- 10 Ding, Z., Granger, C.W.J. Modeling volatility persistence of speculative returns: A new approach, Journal of Econometrics, 1996, vol. 73, issue 1, 185-215

- 11 E. F. Fama and James D. MacBeth. Risk, return, and equilibrium, The Journal of Political Economy 791.1 (1971), pp. 30–55

- 12 Elliott, R. J., J. Van Der Hoek, and W. P. Malcolm. 2005. Pairs trading. Quantitative Finance 5:271–276

- 13 Elliott, R. J. ; Bradrania, R, 2018, Estimating a regime switching pairs trading model, Quantitative Finance, 2018, Vol.18(5), pp.877-883

- 14 Eugene F. Fama, 1970, Efficient Capital Markets: A Review of Theory and Empirical Work, The Journal of Finance, Vol. 25, No. 2, Papers and Proceedings of the TwentyEighth Annual Meeting of the American Finance Association New York, N.Y. December, 28-30, 1969 (May, 1970), pp. 383-417

- 15 Gatev, E.G., Goetzmann, W.N. and Rouwenhorst, K.G. (2006). Pairs Trading: Performance of a Relative Value Arbitrage Rule. The Review of Financial Studies, 19, 797-827.

- 16 Jose A. Scheinkman and Blake LeBaron, 1989, Nonlinear dynamics and stock returns, The Journal of Business, Vol. 62, No. 3 (Jul., 1989), pp. 311-337

- 17 Kiyoshi Suzuki, 2018, Optimal pair-trading strategy over long/short/square positions—empirical study, Quantitative Finance, Volume 18, 2018 - Issue 1

- 18 Kon S, 1984, Models of stock returns: a comparison, J. Finance XXXIX 147–65

- 19 Mandelbrot B, 1963, The variation of certain speculative prices, J. Business XXXVI 392–417

- 20 Ole E. Barndorff-Nielsen, and Neil Shephard, 2001, Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics, J. R. Statist. Soc. B (2001) 63, Part 2, pp. 167-241

- 21 Rad, H., R. K. Y. Low, and R. Faff. 2016. The profitability of pairs trading strategies: distance, cointegration and copula methods. Quantitative Finance 16:1541–1558.

- 22 Rama Cont, 2001, Empirical properties of asset returns: stylized facts and statistical issues, Quantitative Finance VOL 1 (2001) 223–236

- 23 Sergio M. Focardi, Frank J. Fabozzic, Ivan K. Mitov, 2016, A new approach to statistical arbitrage: Strategies based on dynamic factor models of prices and their performance. Journal of Banking & Finance, 65 (2016) 134-155

- 24 Stübinger, Johannes and Endres, Sylvia, 2018, Pairs trading with a mean-reverting jump-diffusion model on high-frequency data, Quantitative Finance Volume 18, 2018 - Issue 10

- 25 Tim Bollerslev, Ray Y. Chou and Kenneth F. Kroner, 1992, ARCH modeling in finance: A review of the theory and empirical evidence, Journal of Econometrics 52 (1992) 5-59.

- 26 Vidyamurthy, G., 2004. Pairs trading: Quantitative methods and analysis. J. Wiley, Hoboken, N.J.

- 27 Yang Bai and Lan Wu, 2018, Analytic value function for optimal regime-switching pairs trading rules, Quantitative Finance, 2018, Vol.18(4)

- 28 Yang, S. Y., Qiao, Q., Beling, P. A., Scherer, W. T., Kirilenko, A. A., 2015. Gaussian process-based algorithmic trading strategy identification. Quantitative Finance 0 (0), 1–21.

- 29 Yaoting Lei and Jing Xu, 2015, Costly arbitrage through pairs trading, Journal of Economic Dynamics & Control, 56 (2015) 1-19

- 30 Zeng, Z., Lee, C. G., 2014. Pairs trading: optimal thresholds and profitability. Quantitative Finance 14 (11), 1881–1893.

- 31 Zhuanxin Ding, Clive W.J. Granger, Robert F. Engle (1993) A long memory property of stock market returns and a new model,Journal of Empirical Finance, Volume 1, Issue 1, 1993, Pages 83-106

| Pair | Stock #1 | Stock #2 | Model I + Strategy A | Model II + Strategy C | Improvement (in %) | |||

|---|---|---|---|---|---|---|---|---|

| Return | Sharpe | Return | Sharpe | Return | Sharpe | |||

| 1 | JPM | BAC | 0.1185 | 1.0030 | 0.0961 | 1.1126 | -18.90 | 10.93 |

| 2 | JPM | WFC | 0.0229 | 0.2268 | 0.0581 | 0.7434 | 153.7 | 227.8 |

| 3 | JPM | C | 0.0567 | 0.5359 | 0.1049 | 1.3486 | 85.01 | 151.7 |

| 4 | JPM | USB | 0.0412 | 0.3971 | 0.0663 | 0.7832 | 60.92 | 97.23 |

| 5 | BAC | WFC | 0.0451 | 0.3455 | 0.0695 | 0.6046 | 54.10 | 74.99 |

| 6 | BAC | C | 0.0874 | 0.8158 | 0.1369 | 1.7516 | 56.64 | 114.7 |

| 7 | BAC | USB | 0.0554 | 0.3786 | 0.0923 | 1.0077 | 66.61 | 166.2 |

| 8 | WFC | C | 0.1031 | 0.8041 | 0.1014 | 0.9731 | -1.649 | 21.02 |

| 9 | WFC | USB | 0.0591 | 0.5631 | 0.0674 | 0.8934 | 14.04 | 58.66 |

| 10 | C | USB | 0.1140 | 0.9040 | 0.2009 | 2.0862 | 76.23 | 130.8 |

| Mean | 0.0703 | 0.5974 | 0.0994 | 1.1304 | 41.29 | 89.23 | ||

| Min | 0.0229 | 0.2268 | 0.0581 | 0.6046 | 153.7 | 166.6 | ||

| Max | 0.1185 | 1.0030 | 0.2009 | 2.0862 | 69.54 | 108.0 | ||

| Median | 0.0579 | 0.5495 | 0.0942 | 0.9904 | 62.69 | 80.24 | ||

-

•

Note: Return is the annualized return, displayed in number, not in percentage. Sharpe is the annualized Sharpe ratio. Improvement is defined as for return and Sharpe ratio respectively, measured in percentage.

| Pair | Stock #1 | Stock #2 | Model I + Strategy A | Model II + Strategy C | Improvement (in %) | |||

|---|---|---|---|---|---|---|---|---|

| Return | Sharpe | Return | Sharpe | Return | Sharpe | |||

| 1 | CPF | BANC | 0.1832 | 0.6745 | 0.2158 | 1.3428 | 17.79 | 99.08 |

| 2 | CPF | CUBI | 0.1092 | 0.4736 | 0.2374 | 1.3563 | 117.4 | 186.4 |

| 3 | CPF | NBHC | 0.1436 | 0.7694 | 0.1912 | 1.2573 | 33.15 | 63.41 |

| 4 | CPF | FCF | 0.1162 | 0.7127 | 0.2175 | 1.7210 | 87.18 | 141.5 |

| 5 | BANC | CUBI | 0.1583 | 0.5199 | 0.4820 | 1.9742 | 204.5 | 279.7 |

| 6 | BANC | NBHC | 0.2105 | 0.8353 | 0.1807 | 1.1435 | -14.16 | 36.90 |

| 7 | BANC | FCF | 0.1669 | 0.5830 | 0.3094 | 2.1898 | 85.38 | 275.6 |

| 8 | CUBI | NBHC | 0.1575 | 0.6049 | 0.2392 | 1.4485 | 51.87 | 139.5 |

| 9 | CUBI | FCF | 0.1362 | 0.5593 | 0.2718 | 1.5292 | 99.56 | 173.4 |

| 10 | NBHC | FCF | 0.1425 | 0.8161 | 0.3132 | 2.5273 | 119.8 | 209.7 |

| Mean | 0.1524 | 0.6549 | 0.2658 | 1.6490 | 74.41 | 151.8 | ||

| Min | 0.1092 | 0.4736 | 0.1807 | 1.1435 | 65.48 | 141.4 | ||

| Max | 0.2105 | 0.8353 | 0.4820 | 2.5273 | 129.0 | 202.6 | ||

| Median | 0.1506 | 0.6397 | 0.2383 | 1.4889 | 58.29 | 132.7 | ||

-

•

Note: Return is the annualized return, displayed in number, not in percentage. Sharpe is the annualized Sharpe ratio. Improvement is defined as that in Table A1

| Pair | Stock #1 | Stock #2 | Model I + Strategy A | Model II + Strategy C | Improvement (in %) | |||

|---|---|---|---|---|---|---|---|---|

| Return | Sharpe | Return | Sharpe | Return | Sharpe | |||

| 1 | JPM | CPF | 0.0670 | 0.3965 | 0.1833 | 1.4799 | 173.6 | 273.2 |

| 2 | JPM | BANC | 0.0587 | 0.2396 | 0.0935 | 0.8334 | 59.28 | 247.8 |

| 3 | JPM | CUBI | -0.0604 | -0.2669 | 0.0423 | 0.3536 | 170.0 | 232.5 |

| 4 | JPM | NBHC | 0.1860 | 0.9750 | 0.2683 | 2.1385 | 44.25 | 119.3 |

| 5 | JPM | FCF | 0.1151 | 0.7230 | 0.2594 | 2.3479 | 125.4 | 224.7 |

| 6 | BAC | CPF | 0.0778 | 0.3770 | 0.2486 | 1.5596 | 219.5 | 313.7 |

| 7 | BAC | BANC | 0.0565 | 0.2124 | 0.1383 | 0.7916 | 144.8 | 272.7 |

| 8 | BAC | CUBI | -0.0959 | -0.3612 | 0.0473 | 0.5852 | 149.4 | 262.0 |

| 9 | BAC | NBHC | 0.1942 | 0.9496 | 0.3420 | 2.4948 | 76.11 | 162.7 |

| 10 | BAC | FCF | 0.1729 | 0.9061 | 0.2541 | 2.1954 | 46.96 | 142.3 |

| 11 | WFC | CPF | 0.0420 | 0.2149 | 0.1138 | 1.2746 | 171.0 | 493.1 |

| 12 | WFC | BANC | 0.1671 | 0.6058 | 0.2071 | 1.0214 | 23.94 | 68.60 |

| 13 | WFC | CUBI | 0.0606 | 0.2572 | 0.2053 | 1.3002 | 238.8 | 405.5 |

| 14 | WFC | NBHC | 0.1410 | 0.7844 | 0.1237 | 0.9464 | -12.27 | 20.65 |

| 15 | WFC | FCF | 0.1058 | 0.5948 | 0.1366 | 1.3104 | 29.11 | 120.3 |

| 16 | C | CPF | 0.1421 | 0.7000 | 0.2214 | 2.1513 | 55.81 | 207.3 |

| 17 | C | BANC | 0.0244 | 0.0961 | 0.1999 | 1.1101 | 719.3 | 1055 |

| 18 | C | CUBI | -0.0031 | -0.0138 | 0.0617 | 0.4357 | 2090 | 3257 |

| 19 | C | NBHC | 0.2164 | 1.0536 | 0.2927 | 2.3896 | 35.26 | 126.8 |

| 20 | C | FCF | 0.1520 | 0.7687 | 0.2246 | 1.8611 | 47.76 | 142.1 |

| 21 | USB | CPF | 0.0782 | 0.4494 | 0.2408 | 2.0902 | 207.9 | 365.1 |

| 22 | USB | BANC | 0.1435 | 0.5450 | 0.2361 | 1.7444 | 64.53 | 220.1 |

| 23 | USB | CUBI | -0.0678 | -0.2938 | 0.0700 | 0.3497 | 203.2 | 219.0 |

| 24 | USB | NBHC | 0.1911 | 1.2574 | 0.2384 | 2.1422 | 24.74 | 70.37 |

| 25 | USB | FCF | 0.0789 | 0.5077 | 0.1206 | 1.1142 | 52.85 | 119.5 |

| Mean | 0.0898 | 0.4671 | 0.1828 | 1.4409 | 103.6 | 208.4 | ||

| Min | -0.0959 | -0.3612 | 0.0423 | 0.3497 | 144.1 | 196.8 | ||

| Max | 0.2164 | 1.2574 | 0.3420 | 2.4948 | 58.04 | 98.41 | ||

| Median | 0.0789 | 0.5077 | 0.2053 | 1.3104 | 160.2 | 158.1 | ||

-

•

Note: Return is the annualized return, displayed in number, not in percentage. Sharpe is the annualized Sharpe ratio. Improvement is defined as that in Table A1

| Pair | Stock #1 | Stock #2 | Model I + Strategy A | Model II + Strategy C | Improvement (in %) | |||

| Return | Sharpe | Return | Sharpe | Return | Sharpe | |||

| 1 | JPM | BAC | 0.1145 | 0.8864 | 0.1501 | 1.8003 | 31.09 | 103.1 |

| 2 | JPM | WFC | 0.0160 | 0.1461 | 0.0795 | 0.9451 | 396.9 | 546.9 |

| 3 | JPM | C | 0.0664 | 0.5686 | 0.1013 | 1.5193 | 52.56 | 167.2 |

| 4 | JPM | USB | 0.0186 | 0.2172 | 0.0629 | 1.4293 | 238.2 | 558.1 |

| 5 | BAC | WFC | 0.0027 | 0.0179 | 0.0568 | 0.4748 | 2004 | 2553 |

| 6 | BAC | C | 0.0920 | 0.7252 | 0.1193 | 1.5417 | 29.67 | 112.6 |

| 7 | BAC | USB | 0.0603 | 0.3936 | 0.1535 | 1.5144 | 154.6 | 284.8 |

| 8 | WFC | C | 0.0827 | 0.5918 | 0.1219 | 1.2283 | 47.40 | 107.6 |

| 9 | WFC | USB | 0.0600 | 0.6432 | 0.0739 | 0.9603 | 23.17 | 49.30 |

| 10 | C | USB | 0.1146 | 0.8553 | 0.1695 | 1.7648 | 47.91 | 106.3 |

| Mean | 0.0628 | 0.5045 | 0.1089 | 1.3178 | 73.42 | 161.2 | ||

| Min | 0.0027 | 0.0179 | 0.0568 | 0.4748 | 2004 | 2553 | ||

| Max | 0.1146 | 0.8864 | 0.1695 | 1.8003 | 47.91 | 103.1 | ||

| Median | 0.0634 | 0.5802 | 0.1103 | 1.4719 | 74.11 | 153.7 | ||

-

•

Note: The data is from 01/10/2012 to 01/01/2018. Return is the annualized return, displayed in number, not in percentage. Sharpe is the annualized Sharpe ratio. Improvement is defined as that in Table A1.

| Pair | Stock #1 | Stock #2 | Model I + Strategy A | Model II + Strategy C | Improvement (in %) | |||

| Return | Sharpe | Return | Sharpe | Return | Sharpe | |||

| 1 | JPM | BAC | -0.0503 | -0.4730 | -0.0500 | -0.4760 | 0.5964 | -0.6342 |

| 2 | JPM | WFC | -0.0809 | -0.5693 | -0.0361 | -0.3281 | 55.38 | 42.37 |

| 3 | JPM | C | -0.0841 | -0.6845 | 0.0299 | 0.3228 | 135.6 | 147.2 |

| 4 | JPM | USB | 0.0867 | 0.9267 | 0.1297 | 1.6816 | 49.60 | 81.46 |

| 5 | BAC | WFC | 0.0364 | 0.4593 | 0.0464 | 0.4636 | 27.47 | 0.9362 |

| 6 | BAC | C | -0.0512 | -0.3766 | 0.0149 | 0.2612 | 129.1 | 169.4 |

| 7 | BAC | USB | -0.0037 | -0.0252 | 0.0587 | 0.5169 | 1686 | 2151 |

| 8 | WFC | C | -0.0586 | -0.3472 | 0.0698 | 0.7619 | 219.1 | 319.5 |

| 9 | WFC | USB | -0.1029 | -0.6961 | 0.0269 | 0.3591 | 126.4 | 151.6 |

| 10 | C | USB | -0.0486 | -0.2948 | 0.0942 | 0.7796 | 293.8 | 364.5 |

| Mean | -0.0357 | -0.2081 | 0.0384 | 0.4343 | 207.6 | 308.7 | ||

| Min | -0.1029 | -0.6961 | 0.0500 | -0.4760 | 51.41 | 31.62 | ||

| Max | 0.0867 | 0.9267 | 0.1297 | 1.6816 | 49.60 | 81.46 | ||

| Median | -0.0508 | -0.3619 | 0.0382 | 0.4114 | 175 2 | 213.7 | ||

-

•

Note: The data is from 01/01/2018 to 01/12/2019. Return is the annualized return, displayed in number, not in percentage. Sharpe is the annualized Sharpe ratio. Improvement is defined as that in Table A1.

| Pair | Stock #1 | Stock #2 | Model I + Strategy A | Model II + Strategy C | Improvement (in %) | |||

|---|---|---|---|---|---|---|---|---|

| Return | Sharpe | Return | Sharpe | Return | Sharpe | |||

| 1 | CPF | BANC | 0.2713 | 0.9758 | 0.3513 | 2.0574 | 29.56 | 110.8 |

| 2 | CPF | CUBI | 0.1226 | 0.4404 | 0.4457 | 1.9114 | 263.5 | 334.0 |

| 3 | CPF | NBHC | 0.1905 | 0.9823 | 0.2559 | 1.7188 | 34.33 | 74.98 |

| 4 | CPF | FCF | 0.1855 | 1.2385 | 0.2453 | 2.5505 | 32.24 | 105.9 |

| 5 | BANC | CUBI | 0.2500 | 0.6928 | 0.4076 | 1.9505 | 63.04 | 181.5 |

| 6 | BANC | NBHC | 0.2406 | 0.8926 | 0.1699 | 1.4127 | -29.38 | 58.27 |

| 7 | BANC | FCF | 0.2056 | 0.7819 | 0.3308 | 1.8279 | 60.89 | 133.8 |

| 8 | CUBI | NBHC | 0.1130 | 0.3808 | 0.2164 | 1.8059 | 91.50 | 374.2 |

| 9 | CUBI | FCF | 0.1125 | 0.4133 | 0.1886 | 1.1579 | 67.64 | 180.2 |

| 10 | NBHC | FCF | 0.1026 | 0.5723 | 0.2523 | 1.8035 | 145.9 | 215.1 |

| Mean | 0.1794 | 0.7371 | 0.2864 | 1.8197 | 59.63 | 146.9 | ||

| Min | 0.1026 | 0.3808 | 0.1699 | 1.1579 | 65.59 | 204.1 | ||

| Max | 0.2713 | 1.2385 | 0.4457 | 2.5505 | 64.28 | 105.9 | ||

| Median | 0.1880 | 0.7374 | 0.2541 | 1.8169 | 35.16 | 146.4 | ||

-

•

Note: The data is from 01/10/2012 to 01/01/2018. Return is the annualized return, displayed in number, not in percentage. Sharpe is the annualized Sharpe ratio. Improvement is defined as that in Table A1.

| Pair | Stock #1 | Stock #2 | Model I + Strategy A | Model II + Strategy C | Improvement (in %) | |||

| Return | Sharpe | Return | Sharpe | Return | Sharpe | |||

| 1 | CPF | BANC | 0.1856 | 0.7541 | 0.1649 | 0.8297 | -11.15 | 10.03 |

| 2 | CPF | CUBI | -0.0924 | -0.3528 | 0.2424 | 1.8467 | 362.3 | 623.4 |

| 3 | CPF | NBHC | -0.0769 | -0.3944 | 0.1621 | 1.0216 | 310.8 | 359.0 |

| 4 | CPF | FCF | -0.0373 | -0.1906 | 0.2094 | 1.4249 | 661.4 | 847.6 |

| 5 | BANC | CUBI | 0.1266 | 0.7454 | 0.4109 | 2.5902 | 224.6 | 247.5 |

| 6 | BANC | NBHC | -0.1577 | -0.6720 | -0.0797 | -0.3926 | 49.46 | 41.58 |

| 7 | BANC | FCF | 0.0107 | 0.0821 | 0.1601 | 1.3930 | 1396 | 1596 |

| 8 | CUBI | NBHC | -0.1475 | -0.5514 | 0 | - | 100 | 100 |

| 9 | CUBI | FCF | -0.1137 | -0.4079 | 0 | - | 100 | 100 |

| 10 | NBHC | FCF | -0.0578 | -0.3088 | 0.1520 | 1.0421 | 363.0 | 437.4 |

| Mean | -0.0360 | -0.1296 | 0.1422 | 0.9756 | 494.6 | 852.6 | ||

| Min | -0.1577 | -0.6720 | -0.0797 | -0.3926 | 49.46 | 41.58 | ||

| Max | 0.1856 | 0.7541 | 0.4109 | 2.5902 | 121.4 | 243.5 | ||

| Median | -0.0674 | -0.3308 | 0.1611 | 1.0319 | 339.2 | 411.9 | ||

-

•

Note: The data is from 01/01/2018 to 01/12/2019. Return is the annualized return, displayed in number, not in percentage. Sharpe is the annualized Sharpe ratio. Improvement is defined as that in Table A1. The returns for CUBI/NBHC and CUBI/FCF are 0 because no trading is opened for these two pairs during the out-of-sample period, and the Sharpe ratios are undefined.

| Pair | Stock #1 | Stock #2 | Model I + Strategy A | Model II + Strategy C | Improvement (in %) | |||

|---|---|---|---|---|---|---|---|---|

| Return | Sharpe | Return | Sharpe | Return | Sharpe | |||

| 1 | JPM | CPF | 0.1668 | 0.9415 | 0.2866 | 3.0567 | 71.82 | 224.7 |

| 2 | JPM | BANC | 0.2067 | 0.7134 | 0.2581 | 1.5501 | 24.87 | 117.3 |

| 3 | JPM | CUBI | 0.0649 | 0.9832 | 0.2576 | 1.6633 | 296.9 | 69.17 |

| 4 | JPM | NBHC | 0.1505 | 0.8387 | 0.2735 | 2.2745 | 81.73 | 171.2 |

| 5 | JPM | FCF | 0.2083 | 1.3273 | 0.3281 | 2.9235 | 57.51 | 120.3 |

| 6 | BAC | CPF | 0.1572 | 0.7484 | 0.2099 | 1.7310 | 33.52 | 131.3 |

| 7 | BAC | BANC | 0.2361 | 0.7452 | 0.1708 | 1.0044 | -27.66 | 34.78 |

| 8 | BAC | CUBI | 0.0789 | 0.2755 | 0.1669 | 1.4519 | 111.5 | 427.0 |

| 9 | BAC | NBHC | 0.2608 | 1.2323 | 0.3354 | 2.5663 | 28.60 | 108.3 |

| 10 | BAC | FCF | 0.1918 | 1.0401 | 0.2653 | 2.3337 | 38.32 | 124.4 |

| 11 | WFC | CPF | 0.0376 | 0.1924 | 0.0988 | 0.6388 | 162.8 | 232.0 |

| 12 | WFC | BANC | 0.2371 | 0.8323 | 0.2165 | 1.0599 | -8.690 | 27.53 |

| 13 | WFC | CUBI | 0.0729 | 0.2682 | 0.2307 | 1.9597 | 216.5 | 630.7 |

| 14 | WFC | NBHC | 0.0974 | 0.5548 | 0.0917 | 0.6167 | -5.850 | 11.16 |

| 15 | WFC | FCF | 0.0656 | 0.3971 | 0.1413 | 1.1406 | 115.4 | 187.2 |

| 16 | C | CPF | 0.0571 | 0.2873 | 0.1766 | 1.4015 | 206.3 | 387.8 |

| 17 | C | BANC | 0.2454 | 0.8899 | 0.2154 | 1.9512 | -12.22 | 119.3 |

| 18 | C | CUBI | 0.0715 | 0.2696 | 0.1589 | 1.0954 | 122.2 | 306.3 |

| 19 | C | NBHC | 0.1279 | 0.6511 | 0.2125 | 1.5321 | 66.15 | 135.3 |

| 20 | C | FCF | 0.1160 | 0.6154 | 0.1790 | 1.3736 | 54.31 | 123.2 |

| 21 | USB | CPF | 0.0654 | 0.4915 | 0.2126 | 1.9990 | 225.1 | 306.7 |

| 22 | USB | BANC | 0.2164 | 0.7529 | 0.3389 | 1.9118 | 56.61 | 153.9 |

| 23 | USB | CUBI | 0.0565 | 0.2443 | 0.2826 | 1.9450 | 400.2 | 696.2 |

| 24 | USB | NBHC | 0.1340 | 0.9289 | 0.1947 | 1.5321 | 45.30 | 64.94 |

| 25 | USB | FCF | 0.0922 | 0.6221 | 0.2167 | 2.1579 | 135.0 | 246.9 |

| Mean | 0.1366 | 0.6737 | 0.2208 | 1.7148 | 61.61 | 154.5 | ||

| Min | 0.0376 | 0.1924 | 0.0917 | 0.6167 | 143.9 | 220.5 | ||

| Max | 0.2608 | 1.3273 | 0.3389 | 3.0567 | 29.95 | 130.3 | ||

| Median | 0.1279 | 0.7134 | 0.2154 | 1.6633 | 68.41 | 133.2 | ||

-

•

Note: The data is from 01/10/2012 to 01/01/2018. Return is the annualized return, displayed in number, not in percentage. Sharpe is the annualized Sharpe ratio. Improvement is defined as that in Table A1.

| Pair | Stock #1 | Stock #2 | Model I + Strategy A | Model II + Strategy C | Improvement (in %) | |||

|---|---|---|---|---|---|---|---|---|

| Return | Sharpe | Return | Sharpe | Return | Sharpe | |||

| 1 | JPM | CPF | 0.1514 | 0.8997 | 0.2731 | 2.3058 | 80.38 | 156.3 |

| 2 | JPM | BANC | 0.2190 | 0.9752 | 0.2023 | 1.1630 | -7.626 | 19.26 |

| 3 | JPM | CUBI | 0.0965 | 1.1227 | 0.1610 | 1.0135 | 66.84 | -9.727 |

| 4 | JPM | NBHC | 0.0303 | 0.1492 | 0.1799 | 1.8165 | 493.7 | 1117 |

| 5 | JPM | FCF | 0.0878 | 0.4209 | 0.1682 | 1.0338 | 91.57 | 145.6 |

| 6 | BAC | CPF | 0.0379 | 0.1702 | 0.1592 | 1.3579 | 320.1 | 697.8 |

| 7 | BAC | BANC | 0.1763 | 0.6913 | 0.1693 | 0.8830 | -3.971 | 27.73 |

| 8 | BAC | CUBI | 0.0926 | 0.3435 | 0.1014 | 0.4298 | 9.503 | 25.12 |

| 9 | BAC | NBHC | -0.0212 | -0.0999 | 0.0144 | 0.7148 | 167.9 | 815.5 |

| 10 | BAC | FCF | 0.0196 | 0.0899 | 0.1117 | 0.8152 | 469.9 | 8.6.8 |

| 11 | WFC | CPF | -0.0625 | -0.2981 | -0.0061 | 0.6388 | 90.24 | 314.3 |

| 12 | WFC | BANC | 0.0583 | 0.2249 | 0.1282 | 0.6058 | 119.9 | 169.4 |

| 13 | WFC | CUBI | -0.0181 | -0.0652 | 0.2826 | 1.5870 | 1661 | 2534 |

| 14 | WFC | NBHC | -0.1181 | -0.5631 | 0.0447 | 0.2594 | 137.8 | 146.1 |

| 15 | WFC | FCF | -0.0821 | -0.3725 | 0.1225 | 0.8413 | 249.2 | 325.9 |

| 16 | C | CPF | -0.0072 | -0.0314 | 0.1433 | 1.1894 | 2090 | 3888 |

| 17 | C | BANC | 0.1238 | 0.4691 | 0.0839 | 0.6480 | -32.23 | 38.13 |

| 18 | C | CUBI | 0.0459 | 0.1692 | 0.2568 | 1.2778 | 459.5 | 655.2 |

| 19 | C | NBHC | -0.0648 | -0.2911 | 0.2108 | 2.1138 | 425.3 | 826.1 |

| 20 | C | FCF | -0.0265 | -0.1143 | 0.2174 | 1.2651 | 920.4 | 1207 |

| 21 | USB | CPF | 0.2108 | 2.2429 | 0.2652 | 2.4946 | 25.81 | 11.22 |

| 22 | USB | BANC | 0.1951 | 0.8939 | 0.1909 | 1.3332 | -2.153 | 49.14 |

| 23 | USB | CUBI | 0.1516 | 0.7685 | 0.2356 | 1.5712 | 55.41 | 104.5 |

| 24 | USB | NBHC | -0.0242 | -0.1258 | 0.1514 | 0.9637 | 725.6 | 866.1 |

| 25 | USB | FCF | 0.0037 | 0.0192 | 0.1979 | 1.2151 | 5249 | 6229 |

| Mean | 0.0510 | 0.3076 | 0.1626 | 1.1815 | 218.6 | 284.2 | ||

| Min | -0.1181 | -0.5631 | -0.0061 | 0.2594 | 94.84 | 146.4 | ||

| Max | 0.2190 | 2.2429 | 0.2826 | 2.4946 | 29.04 | 11.22 | ||

| Median | 0.0379 | 0.1692 | 0.1682 | 1.1630 | 343.8 | 587.4 | ||

-

•

Note: The data is from 01/01/2018 to 01/12/2019. Return is the annualized return, displayed in number, not in percentage. Sharpe is the annualized Sharpe ratio. Improvement is defined as that in Table A1.