Reactive Global Minimum Variance Portfolios with BAHC covariance cleaning

Abstract

We introduce a covariance cleaning method which works well in the very high dimensional regime, i.e., when there are many more assets than data points per asset. This opens the way to unconditional reactive portfolio optimization when there are not enough points to calibrate dynamical conditional covariance models, which happens for example when new assets appear in a market. The method is a -fold boosted version of the Bootstrapped Average Hierarchical Clustering cleaning procedure for correlation and covariance matrices. We apply this method to global minimum variance portfolios and find that should increase with the calibration window length. We compare the performance of BAHC with other state-of-the-art covariance cleaning methods, including dynamical conditional covariance (DCC) with non-linear shrinkage. Generally, we find that our method yields better Sharpe ratios after transaction costs than competing unconditional covariance filtering methods, despite requiring a larger turnover Finally, BAHC yields better Global Minimum Variance portfolios with long-short positions than DCC in a non-stationary investment universe.

JEL classification: G11; G17; C02; C13; C38.

1 Introduction

Portfolio optimization requires trustworthy estimation of covariance matrices, or equivalently, of correlation matrices and asset price volatility. In a dynamical investment context, several problems arise. First, because the dependence between asset prices is not constant in financial markets, correlations matrices are not constant either, and thus estimation should be dynamical. Investment universes evolve as well and thus it may be worth including in a newly-introduced asset in one’s portfolio. A naive idea consists in using as few data points as possible, but this gives rise to very large estimation noise of covariance matrices when the number of data points is comparable to the number of assets (the so-called curse of dimensionality); even worse, correlation and covariance matrices are non-invertible when . This explains the need to use an efficient filtering method to reduce one-shot estimation noise of covariance or correlation matrices and to regularize them (see Bun et al. ((2017)) for a review and the literature overview section below). A more palatable econometric approach is provided by the dynamical conditional correlation (DCC) approach ((Engle, 2002)) and its corrected version ((Aielli, 2013)), which adds a dynamical component to correlation estimation, and its latest variation which includes the filtering of the target matrix ((Engle et al., 2019)).

The second ingredient to improve covariance matrix estimation is to account for stochastic volatility itself by using dynamical methods such as GARCH and its numerous variants. Combining both correlation filtering and conditional volatility estimation with DCC was introduced recently ((Engle et al., 2019)) and is considered state of the art.

Our contribution is to improve the BAHC correlation matrix filtering method ((Bongiorno and Challet, 2021)) and to test it against other filtering methods such as non-linear shrinkage (NLS) and other types of Rotationally Invariant Estimators. Remarkably, our method works well even when (for example with data points and assets) as it produces invertible matrices. The first aim of this paper is to establish how and when the improved BAHC unconditional covariance cleaning method performs better than any other competitive unconditional method. We then compare DCC+NLS with the new BAHC in non-stationary investment universes.

2 Literature overview

We focus here on the global minimum variance portfolio optimization problem (GMV) because it provides the best test of the covariance forecast abilities of each filtering method, as indeed the optimal asset weights only depend on the inverse of the estimated covariance matrix. GMV itself is a special case of minimum variance portfolios, themselves a subset of relevant risk/reward cost functions ((Markowitz, 1959, Black and Litterman, 1990, Duffie and Pan, 1997, Hull and White, 1998, Krokhmal et al., 2002, Roncalli, 2013, Meucci et al., 2015)).

The necessity to filter covariance (and correlation) matrices was recognized a long time ago in this context ((Michaud, 1989)). This is due for example to the fact that mean-variance optimization places more weight on the smallest eigenvalues of the covariance matrix, which, all other things being equal, are more likely to be purely caused by estimation noise (see e.g. the discussion in Potters et al. ((2005)) and subsection 4.2). According to the Marčenko-Pastur distribution of random correlation matrices, the eigenvalues of correlation matrices are themselves systematically noisy when the ratio is too small. Thus, filtering the eigenvalues (without modifying the eigenvectors) also filters the correlation matrix itself. This yields so-called rotationally invariant estimators of correlation matrices (RIE). Remarkably, how to filter only eigenvalues optimally is known: if , if the system is stationary, and if the distribution of price returns is gentle enough, the optimal RIE converges to the Oracle estimator (which knows the future realized correlation matrix) at fixed ratio and in the large system limit and ((Bun et al., 2016)). In practice, computing the optimal RIE is far from trivial for finite , i.e., for sparse eigenvalue densities; several numerical methods address this problem, such as QuEST ((Ledoit et al., 2012)), Inverse Wishart regularisation ((Bun et al., 2017)), or the cross-validated approach (CV hereafter) ((Bartz, 2016)).

The optimal RIE is optimal with two important restrictions: first that only the eigenvalues are filtered, and second that the system is stationary. In other words, an estimator that is more reactive, for example by allowing , or that captures more of the stable structure of the true correlation matrix by also filtering the eigenvectors may be better than the optimal RIE.

A second kind of correlation (or covariance) matrix filtering rests on a well-chosen ansatz, or equivalently on a structure family of the dependence matrix. For example, linear shrinkage uses a target covariance (or correlation) matrix (it also has an eigenvalue filtering interpretation ((Potters et al., 2005))). Factor models belong to the structure-based approach. A particular case is hierarchical factor models, which have been shown to yield remarkably good GMV portfolios ((Tumminello et al., 2007a, b, Pantaleo et al., 2011)).

A problem of the hierarchical ansatz is its sensitivity to the relatively small changes of the input data. For example, bootstrapping the original data does not yield many statistically validated hierarchical clusters in correlation matrices of equity returns ((Bongiorno et al., 2019)). Very recently, this sensitivity was leveraged to build a more flexible estimator, which consists in averaging filtered hierarchical clustering correlation or covariance matrices over bootstraps of the input data (BAHC) ((Bongiorno and Challet, 2021)). BAHC not only allows an imperfect hierarchical structure, i.e., a moderate overlapping among clusters, but also a probabilistic superposition of quite distinct hierarchical structures. When applied to GMV portfolios, BAHC yields similar or better realized risk than the optimal eigenvalues filtering methods but for a much smaller than its competitors, which leads to portfolios that are much more reactive to changing market conditions. It can be further improved, as shown below.

The RIE literature, beyond one-shot volatility estimation, can be generalized to exponentially moving averages of correlation/covariance matrices ((Potters et al., 2005, WC Tan and Zohren, 2021)). The latter are a special case of dynamic conditional correlations (DCC), which is the equivalent of GARCH for correlation matrices ((Engle, 2002)) where the baseline correlation matrix is computed over a long time horizon and mixed with exponentially averaged point-wise estimates of correlations. This method requires points without further regularization. Convergence problems were fixed in Aielli ((2013)).

Finally, volatility estimation and prediction are needed to obtain covariance matrices such as GARCH (or one of its variations) or rough volatility ((Gatheral et al., 2018)) . Engle et al. ((2019)) propose a way to combine both DCC, RIE, and GARCH estimation in an efficient way, which is regarded as the state of the art.

3 Methods

This paper extends BAHC to account for the structure of the correlation matrix that is not described by BAHC, i.e., the residuals. The rationale is that the latter may also contain structures that persist in the out-of-sample window, hence that they should not be left out by the filtering method. The idea to filter the residuals recursively and to average the filtered matrices of bootstrapped data.

The order of recursion, denoted by , is a parameter of the method, which we thus propose to call BAHC. This new method is equivalent to BAHC when by convention. The higher , the finer the details kept by BAHC, which, as shown below, improves the out-of-sample GMV portfolios up to a point. When tends to infinity, the filtered correlation matrix converges to the unfiltered correlation matrix averaged over many bootstrap copies. This matrix is almost surely positive definite in the high-dimensional regime , despite the fact that the empirical unfiltered correlation matrix is not positive definite, a by-product of bootstraps, as shown by ((Bongiorno, 2020)).

As shown below, the optimal average depends on the size of the in-sample window in a data set of US equities. It is generally an increasing function of the in-sample window length: when the latter is small, most of the variations of the empirical correlation matrices are due to estimation noise, which is best filtered by a small ; as calibration window length increases, the relative importance of estimation noise decreases and thus a higher should be preferred.

3.1 Notations

Let us start with some notations of standard quantities: let be a matrix of price returns. Its covariance matrix, denoted by , has elements , where

| (1) |

and where is the sample mean of vector . The Pearson correlation matrix has elements

| (2) |

As BAHC is an extension of BAHC, itself is a bootstrapped version of the strictly hierarchical filtering method of Tumminello et al. ((2007a)), let us start with hierarchical clustering.

3.2 Hierarchical Clustering

Hierarchical clustering agglomerates groups of objects recursively according to a distance matrix taken here as with elements ; D respects all the axioms of a proper distance. Accordingly, the distance between clusters and , denoted by is defined as the average distance between their elements

| (3) |

where and denote the , respectively , elements of clusters and respectively.

Hierarchical agglomeration works as follows: initially, each element is a cluster.. Then, the two clusters with the smallest distance are merged into a new cluster which contains the elements . This algorithm is applied until all the nodes form a single cluster. This defines a tree, called a dendrogram, which uniquely identifies the genealogy of cluster merges, denoted by .

3.3 Hierarchical Clustering Average Linkage Filtering (HCAL)

Defining a merging tree is not enough to clean correlation matrices. Tumminello et al. ((2007a)) propose to average all the elements of the sub-correlation matrix defined from the indices , i.e., to replace by

| (4) |

where is the average distance between clusters and (see Eq. (3)), with set to 1. This defines the HCAL-cleaned correlation matrix , which corresponds to a hierarchical factor model ((Tumminello et al., 2007a)).

HCAL-filtered matrices have two interesting properties: by construction, is positive definite when the correlation matrix is dominated by a global mode, i.e., when the average correlation is large, as in equity correlation matrices ((Tumminello et al., 2007a)). In addition, is the simplest matrix that has the same dendrogram as the empirical correlation matrix ; this means that by applying the HCAL to both and , the resulting dendrograms will be identical. This, however, is also one of the main limitations of this approach as it prevents any overlap among clusters; in addition, the dendrogram of may not be the true one.

3.4 BAHC

Bongiorno and Challet ((2021)), noting that a single hierarchical structure may be too inflexible to describe the dependence structure of financial correlation matrices faithfully, introduced a bootstrapped version of HCAL, where each bootstrap may be associated to a new hierarchical structure. The recipe prescribes to create a set of bootstrap copies of the data matrix , denoted by . A single bootstrap copy of the data matrix is defined entry-wise as , where is a vector of dimension obtained with random sampling by replacement of the elements of the vector . The vectors , are sampled independently.

We compute the Pearson correlation matrix of each bootstrap of the data matrix, from which we derive the HCAL-filtered matrix . Finally, the filtered Pearson correlation matrix is defined as the average over the filtered bootstrap copies, i.e.,

| (5) |

Finally, BAHC filtered covariance is obtained from the sample univariate variance according to

| (6) |

Bootstraps introduce perturbations to the original data. Whenever the hierarchical structure describes the dependence structure of data well, bootstraps essentially lead to the same dendrogram. On the other hand, whenever a single dendrogram fails to account for the full dependence structure, bootstraps lead to several candidate dendrograms. This is why BAHC is a more flexible filtering method than HCAL.

3.5 k-BAHC

Let us write

| (7) |

where is the residual matrix of the HCAL filtering, which contains the dependence structure of not included in . The central idea behind BAHC is to apply HCAL filtering further to , which yields the second order approximation of the residuals.

More generally, one write

| (8) |

where is obtained by applying HCAL filtering to the residual matrix

| (9) |

with the conventions that and . When , . For example, correspond to HCAL-filtered matrix. The recursive application of Eqs (8) and (9) allows us to compute the filtered matrix at any order . It is worth noticing that by iterating Eqs (8) and (9),

| (10) |

as the residues become smaller and smaller. It is important to point out that is not in general a semi-positive definite matrix for , and in most cases, some small negative eigenvalues have been observed in our numerical experiments. These eigenvalues, according to Eq.(10), shrink to non-negative values when approaches infinity. For any order , we set the possibly negative eigenvalues to 0.

As for BAHC, the filtered Pearson correlation matrix is defined as the average over the filtered bootstrap copies, i.e.,

| (11) |

While is a semi-positive definite matrix, the average of these filtered matrices rapidly becomes positive-definite, as shown in Bongiorno ((2020)): it is essentially a by-product of data bootstrapping. This convergence is fast, and it is guaranteed almost surely if the number of bootstraps , but in most of the cases, it is reached for . Finally, -BAHC filtered covariance is obtained from the sample univariate variance according to

| (12) |

The main advantage of BAHC over HCAL is not to force to be embedded in a purely recursive hierarchical structure.

4 Results

4.1 Data

We consider the daily close-to-close returns from 1999-01-04 to 2020-03-31 of US equities, adjusted for dividends, splits, and other corporate events. More precisely, the data set consists of 1295 assets taken from the union of all the components of the Russell 1000 from 2010-06 to 2020-03. The number of stocks with data varies over time: it ranges from 497 in 1999-02-18 to 1172 in 2018-01-17.

4.2 Spectral Properties

Spectral properties explain why the original BAHC filtering achieves a similar or better realized variance than its competitors that focus on filtering the eigenvalues of the correlation matrix only: BAHC eigenvectors have a larger overlap with the out-of-sample eigenvectors than the unfiltered empirical eigenvectors while still filtering eigenvalues nearly as well as the optimal methods ((Bongiorno and Challet, 2021)). This sub-section is devoted to investigate how the eigenvector components change as is increased. It turns out that the localization of eigenvector components is crucial in understanding the role of .

To understand why localization matters to portfolio optimization, in particular the localization of the eigenvectors associated to the smallest eigenvalues, it is worth recalling that Global Minimum Portfolios correspond to the optimal weights

| (13) |

which is a sum by rows (or columns) of the inverse covariance matrix, normalized to one. The inverted covariance matrix can be expressed in terms of the spectral decomposition of as

| (14) |

where and are respectively the th eigenvalue of and its associated eigenvector. This equation means that the composition of the eigenvectors related to the highest eigenvalues is irrelevant and the portfolio allocation is dominated by the eigenvectors of the smallest eigenvalues. Let us assume that the eigenvalue are ordered, i.e., that . If the smallest eigenvalue is much smaller than all the others ones, i.e., , the largest part of investment will be on the -stocks such that . Therefore, the localization of the non-zero elements of the eigenvectors associated to the smallest eigenvalues is crucial to understand the portfolio allocation.

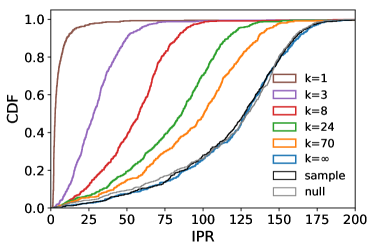

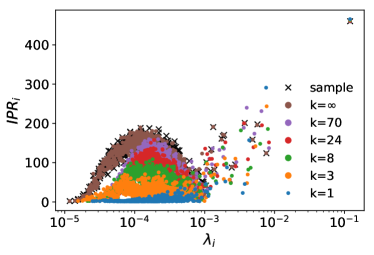

Eigenvector localization can be summarized by the Inverse Participation Ratio (IPR), defined as

| (15) |

where the index refers to the -th eigenvalue. The smaller the value of , the more localized its associated eigenvector. The most localized case corresponding to IPR.

Figure 1a reports the cumulative distribution function of IPR of the eigenvectors for different values of the recursion order . The dependence on is obvious: BACH has the most localized eigenvectors; the larger the value of , the less localized the components of the eigenvectors. In the limit , one recovers the empirical, unfiltered, covariance matrix. In addition, the IPR of the latter two are hardly different from the random matrix null expectation obtained by shuffling price returns asset by asset in the data matrix.

Figure 1b gives more details about the IPRs associated with the eigenvalues. It makes it obvious that IPRs are different for small eigenvalues, while no clear pattern emerges for the outliers . Since the lowest eigenvalues are the ones that affect mainly GVM portfolio optimization, a filtering procedure that modifies the IPR of such eigenvalues will produce a substantial difference in the portfolio allocation.

4.3 Global Minimum Variance portfolios

This part explores how the realized risk of GMV portfolios depends on the recursion order and compares it with the performance obtained from sample covariance and the Cross-Validated (CV) eigenvalue shrinkage ((Bartz, 2016)), which is a strong contender for the best realized risk ((Bongiorno and Challet, 2021)). Two types of tests are carried out: because our data covers many different market regimes and a variable number of assets, we first ask what is the average realized risk of each covariance cleaning method over random collections of assets in randomly chosen periods of fixed length. This allows us to assess the performance of each cleaning scheme in a fair way and to control the effect of the calibration window length. In the second part, we compare the performance of these optimal portfolios with all available stocks at any given time. We also differentiate between portfolios restricted to long-only positions and those without this constraint. In both cases, there is no asset selection from the chosen universe other than that coming from the minimization of the variance.

4.3.1 Random assets, random periods

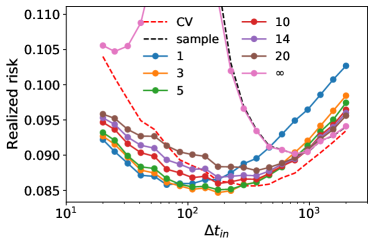

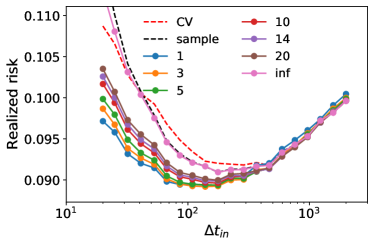

The experiments of this part are carried out in the following way: for each calibration window length we randomly choose a time between 2000-01-03 and 2020-03-30 that defines a calibration window , and a test window with days. We then sample stocks over the available assets in the calibration and test windows. Finally, we compute the GMV portfolios with and without short positions using BAHC, the state-of-art Cross-Validated (CV) eigenvalue shrinkage ((Bartz, 2016)) and the unfiltered empirical covariance matrix.

Figure 2 shows the realized risk of GMV portfolios obtained with the chosen filtering schemes and with the empirical (sample) covariance matrix. The BACH estimators outperform both CV and the sample covariance estimators for in the long-short case and for every for the long-only case (Figures 2a and 2c). The highest performance of CV is obtained for ; however, the highest absolute minimum is obtained for BAHC with , which requires much shorter calibration times and thus yields more reactive portfolios.

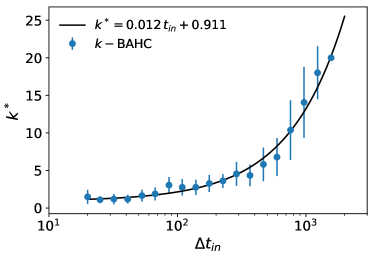

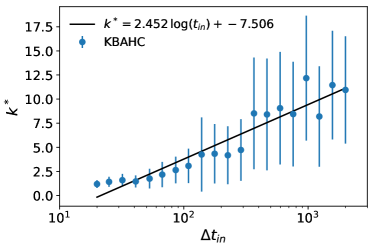

What values to take for (and for this data set) depends on . In the high-dimensional regime (), i.e. for , the best results are obtained for ; however, when increases, the performance of becomes even worse than the sample covariance. From this analysis, it is clear that the larger the calibration window size, the larger the approximation order must be. Figures 2b and 2d show the average optimal that minimizes the realized risk as a function of for the long-short and long-only case. They confirm that a longer calibration window requires a higher approximation order both for the long-short and long-only cases; however, whereas for the long-short setting, seems to have a linear dependence on , this dependence is sub-linear (and much noisier) in the long-only case. It is worth remarking that the fits of the right plots of Figure 2 are obtained with : larger values of might further improve the performance for larger ; however, they would require a comparatively greater computational effort.

4.3.2 Dynamic Conditional Covariance Estimation

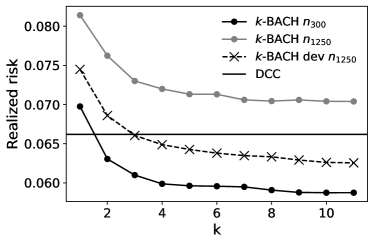

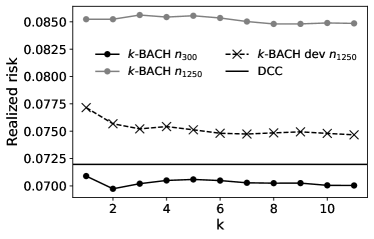

This section is devoted to a comparison between BAHC and DCC-NLS, the state-of-the-art method to clean covariance matrices in a dynamical way ((Engle et al., 2019)): the idea behind DCC-NLS is to have a punctual estimation of the correlation matrix defined as a linear combination of a time-varying correlation matrix with a target matrix (DCC, see ((Engle, 2002))) that comes from a non-linear shrinkage (NLS) of the sample correlation matrix. The estimation of the importance of the time-varying part is obtained by likelihood maximization. Since the former approach is dynamical, although it requires a long calibration window, the final estimator is strongly influenced by the most recent history, also leading to reactive portfolios. The DCC is computed over devolatized returns, which are defined as the ratio between the returns and the conditional volatility, both obtained from a GARCH(1,1). The last estimation of the conditional volatility are joined into the last dynamical estimation of the correlation matrix, producing the DCC covariance matrix. However, since both the GARCH fitting and the likelihood estimation for the dynamical correlation matrices require typically a long time-series, e.g. days (about 5 years), as suggested in Engle et al. ((2019)), the available pool of stock is necessarily limited to the ones which are simultaneously listed over the whole calibration period. This a quite important restriction since the average lifetime of an asset is about 7 years for US equities. We stress that -BAHC does not have this limitation, since its reactivity comes from using very short calibration windows. In particular, as reported in the previous section, -BACH performs very well also in the regime, which raises the question of the respective performance of both methods, each having distinct advantages.

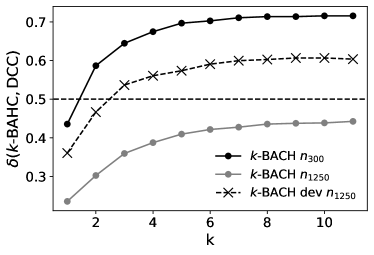

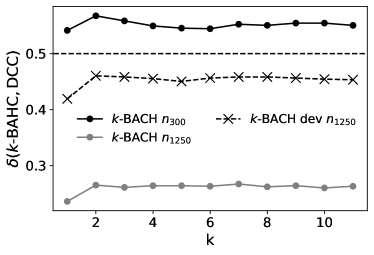

In order to perform this comparison, we used the R implementation of DCC from Nakagawa and Imamura ((2018)). For each simulation we randomly selected the first day of the out-of-sample period in the [2000-01-02,2020-03-31] period and we selected all the stocks were listed in the previous 1250 days for DCC and all the stocks that were listed in the previous 300 days for -BACH, denoted respectively by and . The larger pool of stocks for gives more diversification opportunities, which leads in general to lower realized risk of GMV portfolios. In Fig. 3, we show that -BAHC outperforms DCC when , reaching its optimal performance in the long-short case for . In the long-only case, the gain of -BAHC is approximately constant for all the values of explored here. In particular, in Fig. 3b and Fig. 3d, we show the fraction of times -BACH obtains a lower risk than DCC, which reaches 72% and 57% for the long-short and long-only respectively (Fig 3b).

In order to have a fair comparison and to show that this gain mainly comes from the larger pool of available assets, we include also a set of simulations where the available pool of assets for -BAHC is restricted to the ones used by DCC, i.e., , in this case, DCC outperforms -BAHC for small values of in the long-short case, although -BAHC reaches similar performances for large . On the other hand, the long-only portfolios are totally dominated by DCC. To understand better the respective role of GARCH and DCC, we also apply BAHC to the devolatized returns of the set of assets used by DCC, i.e., . This time, BAHC outperforms DCC in the long-short case for (Fig. 3c). For the long-only case, even if the performance of BAHC significantly increases, DCC is still better (Fig. 3d).

4.3.3 Full-universe, full period backtest

In this section we performed a set of portfolio optimizations with monthly computations of new portfolio weights (and rebalancing) over the full time-period [2000-01-02, 2020-03-31] for all the considered covariance estimators and equally weighted portfolios (EW hence after), and for different in-sample window lengths. The backtests include transaction costs set to 2 bps. A slight complication comes from the variable number of available assets. Thus, as any time, varies and generally increases with time at fixed calibration window length. In any case, it is worth keeping in mind that is relatively large, i.e., between 497 and 1172.

In particular, at each rebalancing time-step we considered all the available stocks listed in both the in-sample and out-of-sample periods. The present work investigates in detail short calibration windows: we chose a sequence of days by steps of days, i.e., about months. We emphasize that this corresponds to . In addition, for sake of completeness we also included longer calibration windows . For each method and calibration window, we computed the realized annualized volatility, the realized annualized return, the Sharpe ratio, the gross-leverage, the concentration of the portfolio, and the average turnover.

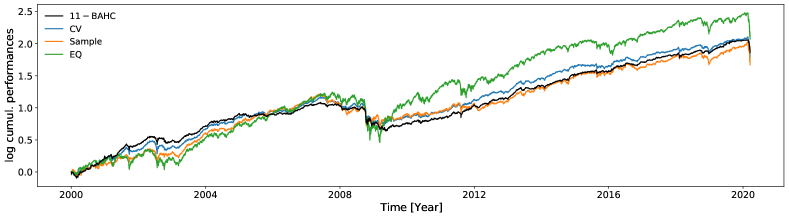

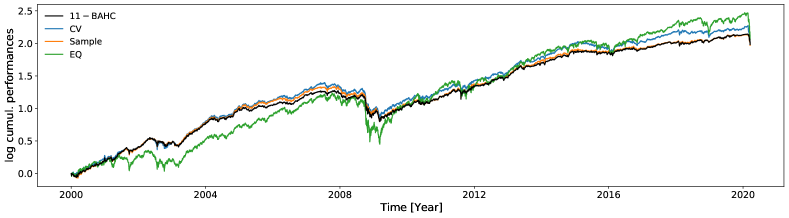

Figure 4 shows the behavior of equally weighted portfolios and GMV portfolios obtained by BAHC, the globally best value for the data set that we used. As expected, GMV reduces the realized risk with respect to EW portfolios, and cleaning the covariance matrix is clearly beneficial as well.

Let us start with realized risk, the focus of this paper. The realized risk of EQ portfolios is much larger than that resulting from the other methods, which is hardly surprising as the latter account for the covariance matrix (Tables 2 and 3); BACH achieves the smallest realized risk, and the best value for increases as increases.

Although GMV does not guarantee a positive return, we also report the Sharpe ratios of the various filtering methods. Because computing Sharpe ratios with moments is not efficient for heavy-tailed variables, we use the efficient and unbiased moment-free SR estimator introduced in Challet ((2017a)) and implemented in Challet ((2017b)). Sharpe ratios paint a picture similar to realized risk (see Tables 4 and 5): BAHC outperforms all the other methods for medium to large values of for almost every both in the long-only and long-short cases, especially when the calibration window is smaller than a year, which corresponds to , i.e., quite deep in the high-dimensional regime. In particular, in the long-short case, the highest SR equals for in the remarkably short calibration window days (about 5 months), and is significantly higher than the best performance of CV (SR) obtained for a much higher calibration window . This shows that reactive portfolio optimization is invaluable. In the long-only case, the improvement of BAHC is smaller: the best SR (1.13) is that of BAHC, whereas the highest SR of CV is .

However, as shown from the cumulative performances in Figure 4, the relative performance changes over time. To overcome this limitation, we evaluated the SR every year, and we performed a dense ranking of all the methods after having rounded the related SRs to the second decimal (to ensure some equal ranks). Finally we associated a score, denoted by , to every method defined as the average dense rank over the years. The results for the long-short and long-only cases are summarized in Table 1. It is worth noting that medium to large values of for BACH outperform all the other methods and that the optimal performance is achieved with a calibration window length shorter than for CV by a factor of about four.

We checked that the portfolios obtained with BAHC are more concentrated than the other ones, which is consistent with the fact that the IPR of the relevant eigenvectors is smaller. The concentration of a portfolio can be measured with

| (16) |

as proposed in Bouchaud and Potters ((2003)); However, as noticed in Pantaleo et al. ((2011)), this quantity does not have a clear interpretation when short selling is allowed. To overcome this issue, Pantaleo et al. ((2011)) introduced the metrics which measures the smallest number of stocks that amount for at least 90% of the invested capital. Accordingly, we used is for the long-short case and for the long-only one. Looking at Tables 6 and 7, the number of stocks selected is systematically smaller for every and calibration window for BAHC for both long-only and long-short portfolios.

That said, BAHC has two drawbacks. First, the gross leverage is generally larger than for CV in the long-short case (see Table 8). However, if we compare the values of gross leverage corresponding to the larger SR for CV and BAHC for within one year, they differ only by ( for CV and for BAHC). On the other hand, without constraining the calibration window, the highest SR for CV is achieved for and the gross leverage reaches , which is larger than for other methods.

The other drawback of BAHC is that it requires a larger turnover for long-short portfolios. A natural turnover metrics, denoted by , was defined in Reigneron et al. ((2020)) as

| (17) |

where is the number of rebalancing operations and is the initial time; measures the average changes in the portfolio allocation between two consecutive portfolio allocations. Table 9 shows that BAHC has a typically twice as large as CV, except for and large for long-short portfolios. For the long-only case (Table 10) CV still outperforms BAHC in that respect, although not by much. All performance measures take into account into account the rebalancing costs. Note that the larger turnover comes from the fact that portfolios are more concentrated, i.e., select fewer assets. It is therefore more likely that the set of selected assets changes at every weight updates.

5 Discussion

By combining recursive hierarchical clustering average linkage and bootstrapping of the data matrix yields a globally better way to filtering asset price covariance matrices. We have shown that this method filters the eigenvectors associated with small eigenvalues of the covariance matrix by making them more concentrated, which in turn yields portfolios with fewer assets. Because BACH captures more of the persistent structure of covariance matrices with shorter calibration windows, it produces Global Minimum Variance portfolios with smaller realized volatility than even the optimal Rotationally Invariant Estimators. Furthermore, because it works well for very short calibration windows, it is well suited to evolving investment universes and changing market conditions, and thus can profit from more diversification opportunities than conditional methods that require much longer timeseries. This is why an unconditional covariance approach with BAHC filtering outperforms state-of-the-art conditional volatility methods for long-short portfolios.

The main drawback of BAHC is that it requires a larger turnover. This is due, in part, to the fact that resulting portfolios are more concentrated, hence that the fraction of capital in which to invest change more rapidly than less specific methods. Whether this reflects a genuine change of market structure or a by-product of the specific assumptions of BACH is an interesting open question.

Future work will investigate how BAHC may improve other kinds of portfolio optimization schemes and other financial applications of covariance matrices. A detailed exploration of the performances of -BAHC on devolatized returns with the DCC approach will be also addressed in future works.

Acknowledgement(s)

This work was performed using HPC resources from the “Mésocentre” computing center of CentraleSupélec and École Normale Supérieure Paris-Saclay supported by CNRS and Région Île-de-France (http://mesocentre.centralesupelec.fr/)

Funding

This publication stems from a partnership between CentraleSupélec and BNP Paribas.

References

- Aielli ((2013)) G. P. Aielli. Dynamic conditional correlation: on properties and estimation. Journal of Business & Economic Statistics, 31(3):282–299, 2013.

- Bartz ((2016)) D. Bartz. Cross-validation based nonlinear shrinkage. arXiv preprint arXiv:1611.00798, 2016.

- Black and Litterman ((1990)) F. Black and R. Litterman. Asset allocation: combining investor views with market equilibrium. Goldman Sachs Fixed Income Research, 115, 1990.

- Bongiorno ((2020)) C. Bongiorno. Bootstraps regularize singular correlation matrices. arXiv preprint arXiv:2004.03165, 2020.

- Bongiorno and Challet ((2021)) C. Bongiorno and D. Challet. Covariance matrix filtering with bootstrapped hierarchies. PloS one, 16(1):e0245092, 2021.

- Bongiorno et al. ((2019)) C. Bongiorno, S. Miccichè, and R. N. Mantegna. Nested partitions from hierarchical clustering statistical validation. arXiv preprint arXiv:1906.06908, 2019.

- Bouchaud and Potters ((2003)) J.-P. Bouchaud and M. Potters. Theory of financial risk and derivative pricing: from statistical physics to risk management. Cambridge university press, 2003.

- Bun et al. ((2016)) J. Bun, R. Allez, J.-P. Bouchaud, and M. Potters. Rotational invariant estimator for general noisy matrices. IEEE Transactions on Information Theory, 62(12):7475–7490, 2016.

- Bun et al. ((2017)) J. Bun, J.-P. Bouchaud, and M. Potters. Cleaning large correlation matrices: tools from random matrix theory. Physics Reports, 666:1–109, 2017.

- Challet ((2017a)) D. Challet. Sharper asset ranking from total drawdown durations. Applied Mathematical Finance, 24(1):1–22, 2017a.

- Challet ((2017b)) D. Challet. sharpeRratio: Moment-Free Estimation of Sharpe Ratios, 2017b. URL https://CRAN.R-project.org/package=sharpeRratio. R package version 1.4.1.

- Duffie and Pan ((1997)) D. Duffie and J. Pan. An overview of value at risk. Journal of Derivatives, 4(3):7–49, 1997.

- Engle ((2002)) R. Engle. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics, 20(3):339–350, 2002.

- Engle et al. ((2019)) R. F. Engle, O. Ledoit, and M. Wolf. Large dynamic covariance matrices. Journal of Business & Economic Statistics, 37(2):363–375, 2019. doi: 10.1080/07350015.2017.1345683. URL https://doi.org/10.1080/07350015.2017.1345683.

- Gatheral et al. ((2018)) J. Gatheral, T. Jaisson, and M. Rosenbaum. Volatility is rough. Quantitative Finance, 18(6):933–949, 2018.

- Hull and White ((1998)) J. Hull and A. White. Value at risk when daily changes in market variables are not normally distributed. Journal of derivatives, 5:9–19, 1998.

- Krokhmal et al. ((2002)) P. Krokhmal, J. Palmquist, and S. Uryasev. Portfolio optimization with conditional value-at-risk objective and constraints. Journal of Risk, 4:43–68, 2002.

- Ledoit et al. ((2012)) O. Ledoit, M. Wolf, et al. Nonlinear shrinkage estimation of large-dimensional covariance matrices. The Annals of Statistics, 40(2):1024–1060, 2012.

- Markowitz ((1959)) H. Markowitz. Portfolio selection: Efficient diversification of investments, volume 16. John Wiley New York, 1959.

- Meucci et al. ((2015)) A. Meucci, A. Santangelo, and R. Deguest. Risk budgeting and diversification based on optimized uncorrelated factors. Available at SSRN 2276632, 2015.

- Michaud ((1989)) R. O. Michaud. The Markowitz optimization enigma: Is “optimized ” optimal? Financial Analysts Journal, 45(1):31–42, 1989.

- Nakagawa and Imamura ((2018)) K. Nakagawa and M. Imamura. Estimating a (c)DCC-GARCH Model in Large Dimensions, 2018. URL https://cran.r-project.org/package=xdcclarge. R package version 0.1.0.

- Pantaleo et al. ((2011)) E. Pantaleo, M. Tumminello, F. Lillo, and R. N. Mantegna. When do improved covariance matrix estimators enhance portfolio optimization? an empirical comparative study of nine estimators. Quantitative Finance, 11(7):1067–1080, 2011.

- Potters et al. ((2005)) M. Potters, J.-P. Bouchaud, and L. Laloux. Financial applications of random matrix theory: Old laces and new pieces. Acta Physica Polonica B, 36:2767, 2005.

- Reigneron et al. ((2020)) P.-A. Reigneron, V. Nguyen, S. Ciliberti, P. Seager, and J.-P. Bouchaud. Agnostic allocation portfolios: A sweet spot in the risk-based jungle? The Journal of Portfolio Management, 46(4):22–38, 2020.

- Roncalli ((2013)) T. Roncalli. Introduction to risk parity and budgeting. CRC Press, 2013.

- Tumminello et al. ((2007a)) M. Tumminello, F. Lillo, and R. N. Mantegna. Hierarchically nested factor model from multivariate data. EPL (Europhysics Letters), 78(3):30006, 2007a.

- Tumminello et al. ((2007b)) M. Tumminello, F. Lillo, and R. N. Mantegna. Kullback-leibler distance as a measure of the information filtered from multivariate data. Physical Review E, 76(3):031123, 2007b.

- WC Tan and Zohren ((2021)) V. WC Tan and S. Zohren. Large non-stationary noisy covariance matrices: A cross-validation approach. Available at SSRN 3745692, 2021.

| Long-short | |||

| rank | rank | Method | |

| 1 | 39.00 | BAHC | 105 |

| 2 | 39.48 | BAHC | 84 |

| 3 | 39.76 | BAHC | 63 |

| 4 | 40.10 | BAHC | 105 |

| 5 | 40.14 | BAHC | 84 |

| 6 | 40.57 | BAHC | 63 |

| 7 | 41.00 | BAHC | 84 |

| 8 | 41.38 | BAHC | 63 |

| 9 | 42.14 | BAHC | 84 |

| 10 | 42.57 | BAHC | 105 |

| 31 | 47.62 | CV | 400 |

| 143 | 65.24 | Sample | 1500 |

| 192 | 81.57 | EQ | - |

| Long-only | |||

| rank | rank | Method | |

| 1 | 36.57 | BAHC | 63 |

| 2 | 38.43 | BAHC | 63 |

| 3 | 39.62 | BAHC | 63 |

| 4 | 40.90 | BAHC | 63 |

| 5 | 42.29 | BAHC | 84 |

| 6 | 42.67 | BAHC | 126 |

| 7 | 42.86 | BAHC | 63 |

| 8 | 43.57 | BAHC | 126 |

| 9 | 43.95 | BAHC | 63 |

| 10 | 44.19 | BAHC | 105 |

| 20 | 46.76 | CV | 126 |

| 29 | 48.52 | Sample | 400 |

| 168 | 73.86 | EQ | - |

| Covariance matrix estimators | |||||||||||

| EQ | Sample | CV | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | |

| 21 | 0.202 | NaN | 0.123 | 0.101 | 0.101 | 0.100 | 0.100 | 0.101 | 0.102 | 0.102 | 0.103 |

| 42 | 0.203 | NaN | 0.113 | 0.098 | 0.097 | 0.096 | 0.096 | 0.096 | 0.096 | 0.096 | 0.097 |

| 63 | 0.204 | 0.146 | 0.107 | 0.091 | 0.088 | 0.087 | 0.087 | 0.087 | 0.087 | 0.088 | 0.088 |

| 84 | 0.204 | 0.134 | 0.103 | 0.091 | 0.086 | 0.085 | 0.085 | 0.084 | 0.084 | 0.085 | 0.085 |

| 105 | 0.204 | 0.129 | 0.100 | 0.091 | 0.086 | 0.084 | 0.084 | 0.083 | 0.084 | 0.084 | 0.084 |

| 126 | 0.204 | 0.124 | 0.099 | 0.092 | 0.086 | 0.084 | 0.083 | 0.083 | 0.083 | 0.083 | 0.083 |

| 147 | 0.204 | 0.120 | 0.098 | 0.092 | 0.085 | 0.083 | 0.083 | 0.082 | 0.082 | 0.082 | 0.083 |

| 168 | 0.204 | 0.118 | 0.097 | 0.093 | 0.086 | 0.083 | 0.083 | 0.082 | 0.082 | 0.082 | 0.082 |

| 189 | 0.204 | 0.116 | 0.096 | 0.094 | 0.086 | 0.083 | 0.082 | 0.082 | 0.081 | 0.082 | 0.082 |

| 210 | 0.203 | 0.116 | 0.095 | 0.095 | 0.087 | 0.084 | 0.083 | 0.082 | 0.082 | 0.082 | 0.082 |

| 231 | 0.203 | 0.114 | 0.095 | 0.100 | 0.091 | 0.088 | 0.087 | 0.087 | 0.087 | 0.087 | 0.087 |

| 252 | 0.203 | 0.113 | 0.094 | 0.101 | 0.092 | 0.089 | 0.088 | 0.087 | 0.087 | 0.087 | 0.087 |

| 300 | 0.203 | NaN | 0.092 | 0.101 | 0.092 | 0.088 | 0.087 | 0.086 | 0.086 | 0.086 | 0.086 |

| 350 | 0.203 | NaN | 0.091 | 0.103 | 0.093 | 0.089 | 0.088 | 0.086 | 0.086 | 0.086 | 0.086 |

| 400 | 0.203 | NaN | 0.092 | 0.105 | 0.094 | 0.091 | 0.089 | 0.088 | 0.087 | 0.087 | 0.088 |

| 500 | 0.202 | NaN | 0.091 | 0.107 | 0.096 | 0.092 | 0.090 | 0.088 | 0.088 | 0.088 | 0.088 |

| 750 | 0.201 | NaN | 0.092 | 0.110 | 0.099 | 0.095 | 0.093 | 0.091 | 0.091 | 0.091 | 0.091 |

| 1000 | 0.200 | 0.207 | 0.093 | 0.113 | 0.103 | 0.099 | 0.097 | 0.095 | 0.094 | 0.093 | 0.093 |

| 1500 | 0.197 | 0.102 | 0.096 | 0.119 | 0.109 | 0.104 | 0.102 | 0.099 | 0.098 | 0.098 | 0.098 |

| 2000 | 0.196 | 0.105 | 0.102 | 0.125 | 0.115 | 0.110 | 0.109 | 0.107 | 0.106 | 0.105 | 0.104 |

| Covariance matrix estimators | |||||||||||

| EQ | Sample | CV | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | |

| 21 | 0.202 | 0.151 | 0.133 | 0.110 | 0.110 | 0.111 | 0.111 | 0.112 | 0.113 | 0.114 | 0.115 |

| 42 | 0.203 | 0.127 | 0.122 | 0.108 | 0.107 | 0.108 | 0.108 | 0.108 | 0.109 | 0.110 | 0.111 |

| 63 | 0.204 | 0.113 | 0.117 | 0.101 | 0.100 | 0.100 | 0.101 | 0.101 | 0.102 | 0.103 | 0.103 |

| 84 | 0.204 | 0.107 | 0.115 | 0.100 | 0.099 | 0.099 | 0.100 | 0.100 | 0.101 | 0.101 | 0.102 |

| 105 | 0.204 | 0.107 | 0.113 | 0.101 | 0.100 | 0.100 | 0.100 | 0.101 | 0.101 | 0.102 | 0.102 |

| 126 | 0.204 | 0.103 | 0.110 | 0.099 | 0.098 | 0.098 | 0.098 | 0.099 | 0.099 | 0.099 | 0.099 |

| 147 | 0.204 | 0.101 | 0.109 | 0.097 | 0.096 | 0.096 | 0.096 | 0.097 | 0.097 | 0.097 | 0.098 |

| 168 | 0.204 | 0.100 | 0.109 | 0.097 | 0.096 | 0.097 | 0.097 | 0.097 | 0.097 | 0.098 | 0.098 |

| 189 | 0.204 | 0.100 | 0.109 | 0.097 | 0.096 | 0.097 | 0.097 | 0.097 | 0.098 | 0.098 | 0.098 |

| 210 | 0.203 | 0.101 | 0.109 | 0.098 | 0.098 | 0.098 | 0.098 | 0.098 | 0.099 | 0.099 | 0.099 |

| 231 | 0.203 | 0.105 | 0.109 | 0.104 | 0.103 | 0.103 | 0.103 | 0.103 | 0.103 | 0.104 | 0.104 |

| 252 | 0.203 | 0.106 | 0.109 | 0.105 | 0.103 | 0.103 | 0.103 | 0.104 | 0.104 | 0.104 | 0.104 |

| 300 | 0.203 | 0.105 | 0.108 | 0.105 | 0.103 | 0.103 | 0.103 | 0.104 | 0.104 | 0.104 | 0.104 |

| 350 | 0.203 | 0.106 | 0.109 | 0.105 | 0.104 | 0.104 | 0.104 | 0.104 | 0.104 | 0.105 | 0.105 |

| 400 | 0.203 | 0.107 | 0.110 | 0.107 | 0.105 | 0.105 | 0.105 | 0.106 | 0.106 | 0.106 | 0.106 |

| 500 | 0.202 | 0.109 | 0.111 | 0.109 | 0.107 | 0.107 | 0.107 | 0.107 | 0.107 | 0.108 | 0.108 |

| 750 | 0.201 | 0.114 | 0.115 | 0.114 | 0.113 | 0.113 | 0.113 | 0.113 | 0.113 | 0.113 | 0.113 |

| 1000 | 0.200 | 0.118 | 0.119 | 0.119 | 0.118 | 0.118 | 0.118 | 0.118 | 0.118 | 0.118 | 0.117 |

| 1500 | 0.197 | 0.121 | 0.123 | 0.123 | 0.122 | 0.121 | 0.121 | 0.121 | 0.121 | 0.121 | 0.120 |

| 2000 | 0.196 | 0.124 | 0.126 | 0.128 | 0.125 | 0.124 | 0.124 | 0.124 | 0.124 | 0.124 | 0.124 |

| Covariance matrix estimators | |||||||||||

| EQ | Sample | CV | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | |

| 21 | 0.57 | NaN | 0.76 | 0.76 | 0.73 | 0.78 | 0.81 | 0.82 | 0.83 | 0.83 | 0.84 |

| 42 | 0.61 | NaN | 0.80 | 0.81 | 0.81 | 0.86 | 0.86 | 0.92 | 0.93 | 0.94 | 0.91 |

| 63 | 0.55 | 0.75 | 0.95 | 0.91 | 1.02 | 1.09 | 1.13 | 1.19 | 1.20 | 1.19 | 1.17 |

| 84 | 0.55 | 0.75 | 0.98 | 0.94 | 1.10 | 1.15 | 1.18 | 1.22 | 1.24 | 1.22 | 1.23 |

| 105 | 0.54 | 0.75 | 1.06 | 0.99 | 1.10 | 1.17 | 1.19 | 1.25 | 1.25 | 1.25 | 1.23 |

| 126 | 0.54 | 0.81 | 1.06 | 0.90 | 1.00 | 1.07 | 1.08 | 1.16 | 1.15 | 1.16 | 1.16 |

| 147 | 0.55 | 0.84 | 1.07 | 0.89 | 0.99 | 1.04 | 1.10 | 1.19 | 1.20 | 1.19 | 1.19 |

| 168 | 0.53 | 0.84 | 1.02 | 0.86 | 0.96 | 1.02 | 1.04 | 1.11 | 1.12 | 1.11 | 1.10 |

| 189 | 0.53 | 0.78 | 1.06 | 0.85 | 1.01 | 1.01 | 1.07 | 1.10 | 1.16 | 1.16 | 1.17 |

| 210 | 0.55 | 0.77 | 1.02 | 0.88 | 1.01 | 1.06 | 1.09 | 1.15 | 1.14 | 1.16 | 1.15 |

| 231 | 0.52 | 0.71 | 1.08 | 0.82 | 0.97 | 1.03 | 1.05 | 1.09 | 1.10 | 1.10 | 1.09 |

| 252 | 0.52 | 0.57 | 1.07 | 0.82 | 0.93 | 0.99 | 0.97 | 1.04 | 1.07 | 1.09 | 1.07 |

| 300 | 0.52 | NaN | 1.16 | 0.83 | 0.99 | 1.02 | 1.05 | 1.08 | 1.08 | 1.12 | 1.10 |

| 350 | 0.51 | NaN | 1.15 | 0.86 | 0.97 | 1.01 | 1.05 | 1.11 | 1.12 | 1.11 | 1.16 |

| 400 | 0.52 | NaN | 1.18 | 0.87 | 0.96 | 1.05 | 1.09 | 1.12 | 1.13 | 1.15 | 1.13 |

| 500 | 0.50 | NaN | 1.14 | 0.84 | 1.01 | 1.06 | 1.09 | 1.13 | 1.14 | 1.13 | 1.12 |

| 750 | 0.51 | NaN | 1.08 | 0.86 | 1.01 | 1.03 | 1.08 | 1.08 | 1.07 | 1.07 | 1.04 |

| 1000 | 0.50 | 0.10 | 1.06 | 0.87 | 0.96 | 1.05 | 1.09 | 1.14 | 1.13 | 1.12 | 1.08 |

| 1500 | 0.46 | 1.00 | 1.21 | 0.90 | 1.07 | 1.13 | 1.17 | 1.22 | 1.21 | 1.21 | 1.21 |

| 2000 | 0.45 | 1.06 | 1.10 | 0.86 | 0.98 | 0.97 | 0.99 | 1.04 | 1.06 | 1.09 | 1.10 |

| Covariance matrix estimators | |||||||||||

| EQ | Sample | CV | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | |

| 21 | 0.60 | 0.53 | 0.74 | 0.73 | 0.76 | 0.77 | 0.79 | 0.80 | 0.78 | 0.78 | 0.81 |

| 42 | 0.58 | 0.84 | 0.81 | 0.77 | 0.84 | 0.91 | 0.91 | 0.93 | 0.95 | 0.96 | 0.97 |

| 63 | 0.54 | 1.00 | 0.89 | 0.97 | 1.00 | 1.05 | 1.06 | 1.09 | 1.12 | 1.11 | 1.09 |

| 84 | 0.57 | 1.05 | 0.92 | 0.94 | 0.95 | 0.98 | 1.00 | 1.02 | 1.02 | 1.02 | 1.04 |

| 105 | 0.54 | 0.95 | 0.93 | 0.90 | 0.93 | 0.97 | 1.01 | 1.03 | 1.04 | 1.07 | 1.06 |

| 126 | 0.57 | 1.05 | 1.01 | 0.98 | 1.01 | 1.08 | 1.09 | 1.10 | 1.11 | 1.13 | 1.12 |

| 147 | 0.55 | 1.06 | 0.98 | 0.97 | 1.00 | 1.04 | 1.03 | 1.06 | 1.06 | 1.09 | 1.07 |

| 168 | 0.53 | 0.99 | 0.94 | 0.98 | 1.02 | 1.03 | 1.06 | 1.07 | 1.06 | 1.03 | 1.07 |

| 189 | 0.54 | 1.07 | 0.96 | 1.05 | 1.08 | 1.08 | 1.08 | 1.08 | 1.08 | 1.09 | 1.11 |

| 210 | 0.51 | 1.05 | 0.94 | 1.06 | 1.05 | 1.08 | 1.07 | 1.06 | 1.08 | 1.03 | 1.05 |

| 231 | 0.54 | 0.97 | 0.92 | 0.99 | 0.97 | 0.97 | 0.98 | 0.97 | 0.97 | 0.96 | 0.96 |

| 252 | 0.51 | 0.91 | 0.88 | 0.96 | 0.95 | 0.92 | 0.94 | 0.92 | 0.91 | 0.91 | 0.94 |

| 300 | 0.52 | 0.90 | 0.91 | 0.92 | 0.88 | 0.92 | 0.92 | 0.91 | 0.93 | 0.92 | 0.95 |

| 350 | 0.49 | 1.01 | 0.93 | 1.00 | 0.98 | 0.96 | 0.98 | 0.99 | 1.00 | 1.00 | 1.00 |

| 400 | 0.52 | 1.01 | 0.93 | 1.03 | 1.00 | 0.99 | 0.99 | 0.99 | 1.00 | 0.98 | 1.01 |

| 500 | 0.52 | 0.92 | 0.91 | 0.94 | 0.92 | 0.92 | 0.93 | 0.93 | 0.94 | 0.91 | 0.91 |

| 750 | 0.49 | 0.87 | 0.90 | 0.94 | 0.94 | 0.89 | 0.89 | 0.87 | 0.88 | 0.88 | 0.89 |

| 1000 | 0.51 | 0.92 | 0.95 | 0.94 | 0.92 | 0.91 | 0.91 | 0.89 | 0.89 | 0.90 | 0.91 |

| 1500 | 0.47 | 0.91 | 0.94 | 0.95 | 0.95 | 0.95 | 0.95 | 0.90 | 0.94 | 0.91 | 0.90 |

| 2000 | 0.43 | 0.87 | 0.88 | 0.86 | 0.90 | 0.91 | 0.86 | 0.89 | 0.88 | 0.89 | 0.89 |

| Covariance matrix estimators | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Sample | CV | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | |

| 21 | 558 | 566 | 474 | 475 | 473 | 473 | 470 | 468 | 467 | 465 |

| 42 | 556 | 560 | 494 | 492 | 492 | 492 | 491 | 491 | 490 | 490 |

| 63 | 551 | 554 | 501 | 496 | 497 | 498 | 498 | 498 | 497 | 498 |

| 84 | 546 | 549 | 502 | 495 | 497 | 498 | 498 | 498 | 498 | 499 |

| 105 | 544 | 543 | 502 | 494 | 496 | 497 | 498 | 498 | 499 | 499 |

| 126 | 540 | 540 | 501 | 493 | 494 | 496 | 497 | 497 | 498 | 498 |

| 147 | 536 | 536 | 499 | 490 | 493 | 495 | 496 | 497 | 497 | 498 |

| 168 | 533 | 532 | 498 | 489 | 491 | 493 | 495 | 496 | 496 | 497 |

| 189 | 530 | 529 | 497 | 486 | 488 | 489 | 492 | 493 | 493 | 494 |

| 210 | 527 | 525 | 495 | 484 | 485 | 487 | 490 | 490 | 491 | 492 |

| 231 | 524 | 521 | 493 | 481 | 483 | 485 | 487 | 488 | 489 | 490 |

| 252 | 521 | 518 | 491 | 479 | 479 | 482 | 484 | 486 | 487 | 487 |

| 300 | 512 | 511 | 486 | 473 | 473 | 475 | 479 | 481 | 481 | 482 |

| 350 | 504 | 503 | 480 | 467 | 467 | 468 | 472 | 474 | 475 | 476 |

| 400 | 496 | 496 | 474 | 461 | 460 | 463 | 466 | 468 | 470 | 470 |

| 500 | 479 | 482 | 462 | 449 | 448 | 450 | 454 | 456 | 458 | 459 |

| 750 | 441 | 449 | 434 | 421 | 420 | 421 | 425 | 428 | 429 | 430 |

| 1000 | 405 | 416 | 404 | 393 | 391 | 392 | 396 | 398 | 398 | 399 |

| 1500 | 340 | 353 | 347 | 337 | 337 | 337 | 339 | 341 | 341 | 341 |

| 2000 | 286 | 294 | 292 | 286 | 286 | 285 | 286 | 287 | 287 | 286 |

| Covariance matrix estimators | ||||||||||

| Sample | CV | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | |

| 21 | 27.5 | 155.2 | 10.3 | 14.8 | 18.8 | 21.7 | 27.3 | 31.3 | 34.5 | 36.5 |

| 42 | 14.8 | 92.4 | 10.3 | 13.1 | 15.6 | 17.5 | 21.2 | 23.8 | 25.8 | 26.8 |

| 63 | 13.6 | 73.9 | 10.8 | 13.0 | 14.8 | 16.3 | 19.1 | 21.2 | 22.8 | 23.5 |

| 84 | 13.2 | 64.3 | 11.2 | 13.2 | 14.7 | 15.8 | 18.1 | 19.8 | 21.2 | 21.8 |

| 105 | 13.5 | 56.9 | 11.7 | 13.5 | 14.9 | 15.9 | 17.9 | 19.4 | 20.5 | 21.1 |

| 126 | 13.6 | 53.7 | 12.2 | 13.9 | 15.1 | 15.9 | 17.6 | 18.9 | 20.0 | 20.5 |

| 147 | 13.8 | 50.5 | 12.4 | 14.0 | 15.0 | 15.8 | 17.3 | 18.4 | 19.3 | 19.8 |

| 168 | 13.9 | 48.2 | 12.6 | 14.1 | 15.0 | 15.7 | 17.0 | 18.0 | 18.9 | 19.3 |

| 189 | 14.0 | 46.4 | 12.7 | 14.1 | 14.9 | 15.6 | 16.7 | 17.6 | 18.4 | 18.8 |

| 210 | 14.1 | 44.6 | 12.9 | 14.1 | 14.9 | 15.5 | 16.5 | 17.3 | 18.0 | 18.5 |

| 231 | 14.1 | 43.5 | 13.0 | 14.1 | 14.9 | 15.4 | 16.3 | 17.0 | 17.7 | 18.1 |

| 252 | 14.0 | 42.4 | 13.0 | 14.1 | 14.7 | 15.2 | 16.1 | 16.8 | 17.4 | 17.7 |

| 300 | 14.0 | 40.0 | 13.1 | 13.9 | 14.4 | 14.8 | 15.5 | 16.1 | 16.7 | 17.0 |

| 350 | 14.2 | 38.3 | 13.3 | 14.1 | 14.5 | 14.9 | 15.5 | 16.0 | 16.5 | 16.8 |

| 400 | 14.2 | 36.7 | 13.4 | 14.0 | 14.4 | 14.7 | 15.2 | 15.7 | 16.1 | 16.4 |

| 500 | 14.2 | 34.2 | 13.5 | 14.1 | 14.5 | 14.7 | 15.0 | 15.3 | 15.7 | 15.9 |

| 750 | 14.5 | 30.3 | 14.1 | 14.5 | 14.4 | 14.5 | 14.8 | 15.0 | 15.2 | 15.5 |

| 1000 | 15.1 | 28.2 | 14.8 | 14.8 | 14.6 | 14.7 | 14.9 | 15.1 | 15.4 | 15.6 |

| 1500 | 15.9 | 25.5 | 15.3 | 15.3 | 15.0 | 15.2 | 15.4 | 15.6 | 15.8 | 16.0 |

| 2000 | 15.4 | 22.4 | 14.4 | 14.7 | 14.4 | 14.5 | 14.8 | 14.9 | 15.1 | 15.2 |

| Covariance matrix estimators | ||||||||||

| Sample | CV | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | |

| 21 | 2.53 | 1.65 | 2.43 | 2.45 | 2.34 | 2.26 | 2.12 | 2.03 | 1.95 | 1.91 |

| 42 | 2.50 | 1.97 | 2.69 | 2.81 | 2.71 | 2.64 | 2.51 | 2.42 | 2.36 | 2.33 |

| 63 | 2.44 | 2.17 | 2.85 | 3.04 | 2.96 | 2.89 | 2.77 | 2.69 | 2.63 | 2.61 |

| 84 | 2.70 | 2.33 | 2.96 | 3.20 | 3.13 | 3.07 | 2.95 | 2.88 | 2.83 | 2.82 |

| 105 | 2.98 | 2.47 | 3.04 | 3.32 | 3.28 | 3.22 | 3.11 | 3.04 | 3.00 | 3.00 |

| 126 | 3.25 | 2.55 | 3.11 | 3.42 | 3.39 | 3.34 | 3.24 | 3.17 | 3.13 | 3.14 |

| 147 | 3.52 | 2.64 | 3.16 | 3.51 | 3.51 | 3.46 | 3.36 | 3.30 | 3.26 | 3.27 |

| 168 | 3.78 | 2.72 | 3.21 | 3.58 | 3.59 | 3.56 | 3.46 | 3.40 | 3.37 | 3.39 |

| 189 | 4.04 | 2.79 | 3.24 | 3.63 | 3.66 | 3.63 | 3.55 | 3.49 | 3.46 | 3.48 |

| 210 | 4.31 | 2.87 | 3.27 | 3.68 | 3.73 | 3.70 | 3.62 | 3.57 | 3.54 | 3.56 |

| 231 | 4.59 | 2.92 | 3.29 | 3.72 | 3.78 | 3.76 | 3.69 | 3.64 | 3.61 | 3.64 |

| 252 | 4.87 | 2.98 | 3.31 | 3.76 | 3.83 | 3.82 | 3.75 | 3.70 | 3.68 | 3.71 |

| 300 | 498.38 | 3.11 | 3.34 | 3.83 | 3.93 | 3.93 | 3.87 | 3.83 | 3.81 | 3.85 |

| 350 | 327.54 | 3.21 | 3.38 | 3.88 | 4.01 | 4.02 | 3.98 | 3.94 | 3.93 | 3.97 |

| 400 | 740.75 | 3.31 | 3.40 | 3.93 | 4.08 | 4.10 | 4.07 | 4.03 | 4.03 | 4.07 |

| 500 | 380.61 | 3.47 | 3.43 | 4.00 | 4.19 | 4.22 | 4.22 | 4.19 | 4.19 | 4.24 |

| 750 | 207.73 | 3.75 | 3.48 | 4.11 | 4.36 | 4.42 | 4.45 | 4.45 | 4.46 | 4.51 |

| 1000 | 17.89 | 3.91 | 3.50 | 4.16 | 4.44 | 4.51 | 4.56 | 4.56 | 4.58 | 4.64 |

| 1500 | 7.10 | 3.97 | 3.47 | 4.08 | 4.36 | 4.44 | 4.52 | 4.54 | 4.56 | 4.62 |

| 2000 | 5.69 | 3.82 | 3.36 | 3.88 | 4.12 | 4.21 | 4.31 | 4.33 | 4.35 | 4.40 |

| Covariance matrix estimators | ||||||||||

| Sample | CV | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | |

| 21 | 3.75 | 1.54 | 2.93 | 3.03 | 2.89 | 2.79 | 2.61 | 2.50 | 2.41 | 2.36 |

| 42 | 3.01 | 1.36 | 2.27 | 2.58 | 2.52 | 2.47 | 2.35 | 2.27 | 2.22 | 2.19 |

| 63 | 2.24 | 1.25 | 1.81 | 2.23 | 2.23 | 2.20 | 2.12 | 2.07 | 2.03 | 2.02 |

| 84 | 2.24 | 1.18 | 1.59 | 2.05 | 2.09 | 2.07 | 2.02 | 1.97 | 1.95 | 1.94 |

| 105 | 2.35 | 1.19 | 1.40 | 1.89 | 1.96 | 1.96 | 1.92 | 1.88 | 1.86 | 1.87 |

| 126 | 2.45 | 1.06 | 1.25 | 1.76 | 1.85 | 1.86 | 1.84 | 1.81 | 1.79 | 1.80 |

| 147 | 2.62 | 1.02 | 1.15 | 1.67 | 1.78 | 1.79 | 1.78 | 1.75 | 1.73 | 1.74 |

| 168 | 2.79 | 0.98 | 1.05 | 1.59 | 1.71 | 1.73 | 1.72 | 1.69 | 1.68 | 1.69 |

| 189 | 2.93 | 0.96 | 0.96 | 1.50 | 1.64 | 1.68 | 1.67 | 1.65 | 1.64 | 1.65 |

| 210 | 3.10 | 0.97 | 0.91 | 1.46 | 1.60 | 1.64 | 1.64 | 1.62 | 1.61 | 1.62 |

| 231 | 3.28 | 0.92 | 0.86 | 1.41 | 1.56 | 1.61 | 1.61 | 1.59 | 1.57 | 1.58 |

| 252 | 3.46 | 0.89 | 0.80 | 1.36 | 1.52 | 1.56 | 1.57 | 1.56 | 1.54 | 1.55 |

| 300 | 916.40 | 0.86 | 0.73 | 1.29 | 1.46 | 1.51 | 1.53 | 1.51 | 1.50 | 1.51 |

| 350 | 567.25 | 0.82 | 0.66 | 1.23 | 1.41 | 1.46 | 1.49 | 1.47 | 1.45 | 1.46 |

| 400 | 1374.68 | 0.80 | 0.61 | 1.18 | 1.37 | 1.43 | 1.45 | 1.44 | 1.42 | 1.42 |

| 500 | 664.68 | 0.74 | 0.53 | 1.10 | 1.30 | 1.36 | 1.39 | 1.37 | 1.35 | 1.35 |

| 750 | 346.99 | 0.66 | 0.41 | 0.98 | 1.19 | 1.26 | 1.30 | 1.28 | 1.26 | 1.25 |

| 1000 | 13.92 | 0.60 | 0.35 | 0.89 | 1.11 | 1.18 | 1.22 | 1.20 | 1.18 | 1.17 |

| 1500 | 1.53 | 0.49 | 0.28 | 0.77 | 0.96 | 1.03 | 1.07 | 1.05 | 1.02 | 1.01 |

| 2000 | 0.88 | 0.40 | 0.24 | 0.64 | 0.82 | 0.88 | 0.91 | 0.90 | 0.88 | 0.86 |

| Covariance matrix estimators | ||||||||||

| Sample | CV | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | BAHC | |

| 21 | 1.61 | 1.37 | 1.51 | 1.53 | 1.53 | 1.53 | 1.53 | 1.53 | 1.53 | 1.53 |

| 42 | 1.47 | 1.04 | 1.13 | 1.14 | 1.14 | 1.14 | 1.14 | 1.14 | 1.15 | 1.15 |

| 63 | 1.19 | 0.82 | 0.87 | 0.89 | 0.89 | 0.89 | 0.89 | 0.89 | 0.90 | 0.91 |

| 84 | 1.00 | 0.69 | 0.76 | 0.77 | 0.77 | 0.78 | 0.78 | 0.78 | 0.79 | 0.79 |

| 105 | 0.85 | 0.60 | 0.66 | 0.66 | 0.67 | 0.67 | 0.67 | 0.68 | 0.68 | 0.69 |

| 126 | 0.76 | 0.52 | 0.58 | 0.59 | 0.60 | 0.60 | 0.61 | 0.61 | 0.61 | 0.62 |

| 147 | 0.66 | 0.46 | 0.51 | 0.52 | 0.53 | 0.54 | 0.54 | 0.54 | 0.54 | 0.55 |

| 168 | 0.59 | 0.42 | 0.45 | 0.46 | 0.47 | 0.48 | 0.48 | 0.48 | 0.48 | 0.49 |

| 189 | 0.55 | 0.38 | 0.41 | 0.43 | 0.44 | 0.44 | 0.44 | 0.45 | 0.45 | 0.45 |

| 210 | 0.51 | 0.36 | 0.39 | 0.40 | 0.42 | 0.42 | 0.43 | 0.43 | 0.43 | 0.43 |

| 231 | 0.47 | 0.34 | 0.36 | 0.38 | 0.39 | 0.39 | 0.39 | 0.39 | 0.40 | 0.40 |

| 252 | 0.43 | 0.31 | 0.33 | 0.35 | 0.36 | 0.36 | 0.37 | 0.37 | 0.37 | 0.37 |

| 300 | 0.38 | 0.28 | 0.30 | 0.32 | 0.33 | 0.33 | 0.33 | 0.33 | 0.33 | 0.34 |

| 350 | 0.34 | 0.25 | 0.27 | 0.29 | 0.30 | 0.30 | 0.30 | 0.30 | 0.30 | 0.31 |

| 400 | 0.30 | 0.23 | 0.24 | 0.26 | 0.28 | 0.28 | 0.28 | 0.28 | 0.28 | 0.28 |

| 500 | 0.25 | 0.20 | 0.21 | 0.23 | 0.24 | 0.24 | 0.24 | 0.24 | 0.24 | 0.24 |

| 750 | 0.19 | 0.15 | 0.16 | 0.19 | 0.19 | 0.20 | 0.20 | 0.20 | 0.20 | 0.20 |

| 1000 | 0.16 | 0.13 | 0.14 | 0.16 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 |

| 1500 | 0.11 | 0.09 | 0.10 | 0.13 | 0.13 | 0.13 | 0.13 | 0.13 | 0.13 | 0.13 |

| 2000 | 0.09 | 0.08 | 0.09 | 0.11 | 0.12 | 0.12 | 0.12 | 0.11 | 0.11 | 0.11 |