Modeling Human Dynamics and Lifestyle using Digital Traces

2United States Military Academy, West Point, NY

3University of California, Berkeley, CA

March 2020 )

Abstract

Human behavior drives a range of complex social, urban, and economic systems, yet understanding its structure and dynamics at the individual level remains an open question. From credit card transactions to communications data, human behavior appears to exhibit bursts of activity driven by task prioritization and periodicity, however, current research does not offer generative models capturing these mechanisms. We propose a multivariate, periodic Hawkes process (MPHP) model that captures — at the individual level — the temporal clustering of human activity, the interdependence structure and co-excitation of different activities, and the periodic effects of weekly rhythms. We also propose a scalable parameter estimation technique for this model using maximum-aposteriori expectation-maximization that additionally provides estimation of latent variables revealing branching structure of an individual’s behavior patterns. We apply the model to a large dataset of credit card transactions, and demonstrate the MPHP outperforms a non-homogeneous Poisson model and LDA in both statistical fit for the distribution of inter-event times and an activity prediction task.

1 Introduction

Within the last decade, the digital age has sharply redefined the way we study human behavior. Electronic records now encompass a diverse spectrum of human activity, ranging from phone [13, 2, 23] and email communication data [21] to location records [30, 9] and household energy usage [16, 37]. The existence of these passively collected datasets supersedes the need to actively collect data through cumbersome and expensive surveys. With the rising ubiquity of passive data, we now have new opportunities to understand the individual dynamics at a higher level of granularity in time scale and behavioral detail. Models of human behavior have the potential to inform government policy, helping to optimize infrastructure, reduce congestion, and mitigate pollution.

In particular, the analysis of credit card records can give us a fine-grained understanding of spending patterns, lending valuable insight into the design of cities, the distribution of wealth, and the urban economy. The primary use of this emerging data source has centered around measuring similarity in purchases through affinity algorithms [27, 29]. However, recent work has started to link both mobility and socio-demographics with purchase behavior [7, 8], suggesting that models of the individual have broader implications. For example, although traditionally mobile phone data is the basis for models of human mobility, recent research has shown that credit card data enables similar applications. That is, through the preferred transitions between businesses, we can model movement resulting from shopping activity, observing the same imbalance in the spatial distribution as found in traditional mobility studies [40].

Despite the wide range of applications, current literature lacks temporal models of shopping patterns. Indeed, there are few urban models describing human dynamics at the individual level in present research. One exception is a recent framework for urban mobility, TimeGeo [11]. This framework learns a high resolution model from passive data containing sparse traces of individuals. It explicitly outlines the choice mechanisms each individual makes, delineating a procedure in which, for example, individuals start at home, then must choose whether to move, then choose whether to explore, and then choose whether to visit a previously unvisited location.

In this paper, we propose a unified statistical framework to describe multidimensional human dynamics. Applying our method to credit card transaction histories, we model the individual dynamics of shopping behavior for the first time. From massive amounts of passive data, the proposed framework extracts the key underlying mechanisms driving human behavior. The resulting model is simple and interpretable, but comprehensive enough to generate realistic trajectories. As a result, the method lends insight into periodic patterns and temporal transitions in urban areas. Unlike TimeGeo, we impose no explicit choice mechanisms on behavior, capturing a comprehensive representation of human dynamics through just two well-known behavioral characteristics: burstiness and periodic effects.

A pattern of temporal clustering — that is, long periods of low activity punctuated by short periods of high activity — seems to define many natural and human-centric phenomena, from earthquakes and neural impulses to social systems, technological advances, and economic markets. This so-called “burstiness” has been shown to be a fundamental property of human dynamics [21, 35, 22, 14]. Past work attributes the burstiness of human dynamics to two driving mechanisms: inherent correlations due to decision-making mechanisms like task-prioritization, and underlying temporal correlations like circadian rhythms (e.g. the home-work-home cycle).

There is a rich literature surrounding the hypothesis that task prioritization results in the bursty signals in human behavior [4]. This hypothesis stems from the idea that certain activities with shared prioritization will occur in bursts, resulting in short inter-event times, followed by long periods of inactivity. For example: a taxi ride may result in restaurant and department store transactions; regular payments for network, phone, and cable services may often be made together; a person running weekly errands may make many purchases in a short time period. Similar patterns occur in communication networks [24]: a call from mother to son may excite a call from son to father; an email from the manager may induce increased communication between team members. Capturing the structure of these excitation patterns gives important insight into individual priorities and behavioral patterns, extending current work, which only considers temporal behavior without the context of different activities.

Queuing process models are a primary example of models based on this task prioritization mechanism. These models attribute burstiness to the execution of tasks based on their priority [6, 4], describing the waiting time of a task, or in other words, the time period before a task is executed. This depends on the cumulative time needed to perform all tasks before it. The queuing mechanism and priority distribution are chosen to produce heavy tails in the waiting time distribution [1, 35], as this has been found to agree well with empirical observations [26].

A related modeling paradigm to capture the temporal clustering observed in human behavior uses stochastic (point) processes with non-homogeneous rates. For example, one may engineer the probability of an event occurrence to depend on the occurrence of other, recent events — this is the so-called “self-exciting” property of models like the Hawkes process [22, 14]. Alternatively, one may modify the process’s intensity to fluctuate according to some observed seasonal, weekly, or daily rhythm. This pattern is evident in activity ranging from location data [30, 9], phone [13, 2] and email communication [21] to Twitter activity [31] and open-source contributions on Wikipedia and OpenStreetMap [39, 38]. A number of factors contribute to this periodicity, including the day-night cycle, employment status, work schedules and commuting patterns [19, 20], and the activity of one’s social contacts [33].

Perhaps surprisingly, this periodicity appears to provide sufficient explanatory power to model the temporal correlation observed in human behavior, even using memoryless models. For example, [10] shows that the observed power law scaling on inter-event time distributions can be achieved using Poissonian agents with varying rates. Extending upon this line of work, [21] argues that such distinctly non-homogeneous event sequences are solely due to circadian rhythms, proposing a non-homogeneous Poissonian model using “cascades” of processes corresponding to the hour and day of week. Extensions of this model uses a Markov process with multiple states to modulate transitions between Poisson models with different rates, thus reflecting periods of high and low activity seen in human communications [12, 28]. However, while these methods give a close approximation to observed data, they require a large number of parameters to specify the start and end points for distinct time intervals that represent active periods. Thus the result is not only computationally expensive, but is also not descriptive and gives no generative explanation for diversity in human dynamics [15]. In addition, research [13, 43] has shown that even after removing periodic effects, signals remain bursty.

In this paper, we propose a stochastic model called the multivariate periodic Hawkes process (MPHP) that explicitly captures both the structure of interdependency between multiple types of human activity and the fluctuations in activity rates due to circadian rhythms. We demonstrate, using a large dataset of credit card transactions, that the MPHP model reveals an inherent branching structure to the observed human behavior which allows interpretation of activity ordering and prioritization. We show the MPHP provides more predictive power than a periodic Poisson process or a latent Dirichlet allocation model. We also present a maximum-aposteriori (MAP) expectation-maximization (EM) method for parameter estimation of the MPHP that scales to large datasets and allows use of priors to provide the necessary regularization.

2 Model

We propose a multivariate periodic Hawkes process (MPHP) model that captures the rates of different activities, the branching structure of ordering and interdependence of one activity on another, and the periodicity due to weekly circadian rhythms. We give a brief exposition of the model here, with technical details focused on parameter estimation and simulation to be found in Methods.

The Hawkes process [17] is a point process that is conditionally Poisson, with the conditional rate or intensity depending on the history of events up to time . The intensity consists of a background rate and additive contributions from previous events which decay over time. This allows the model to capture self-excitation and interdependence between events of different types. We may further incorporate periodicity into the model by scaling the background rate.

Specifically, consider a sequence of events where the th event occurs at time over an interval and is of event type , out of total types. We then define the conditional intensity for each dimension as

| (1) |

where is the background intensity for occurrences of type , adjusted by global parameters capturing daily and hourly periodicity. Each scales the background rate depending on the day of the week corresponding to time . We let and ensure these parameters are normalized so that . We use , but one may choose more or less granularity to capture, for example, seasonal or hourly effects.

The function is a triggering kernel which represents the excitation effects of an event from at time on the intensity in . We decompose the triggering kernel into an excitation parameter and decay function:

| (2) |

We use the common choice of an exponential decay, and set as a single global parameter governing the speed of decay for an individual. The excitation parameters capture the level of effect an event in has on the probability of an event occurrence in , and we may consider the entire excitation matrix .

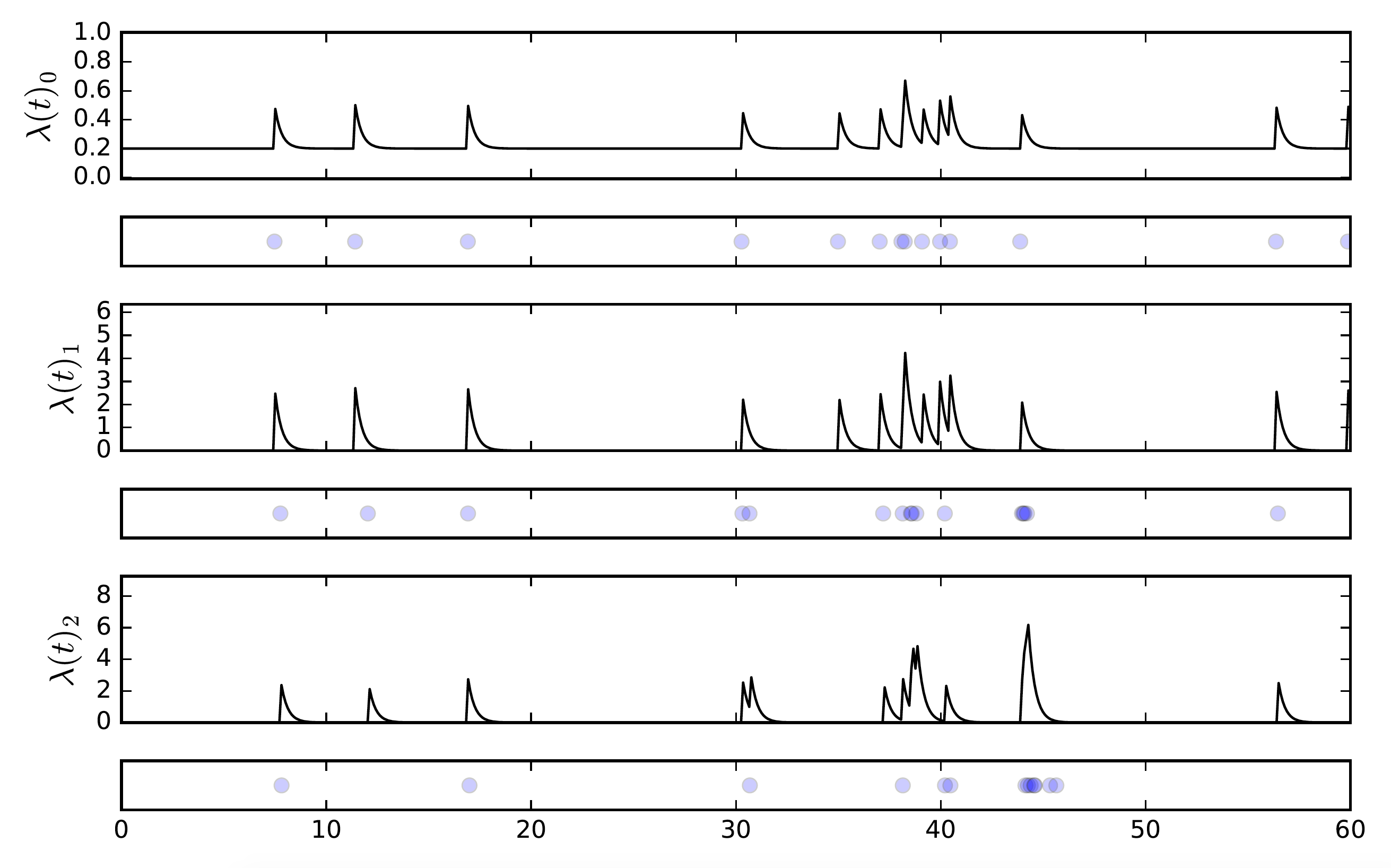

As an example of the Hawkes process with a small () number of activities, consider Fig. 2. Here Activity 0 has intensity with base rate , while Activities 1 and 2 have base rate 0. We set , , , and all other , so that Activity 0 has some self-excitation effect, and there is a cascading effect from occurrences of Activity 0 to occurrences of Activity 1 and then 2. The figure depicts one sample from such a process.

In order to frame both our results and our parameter estimation methodology, it is also important to understand an interpretation of the Hawkes process as a branching process [17]. Note that when the intensity , we can consider any arrivals as parent events. But any immediately subsequent event (where now due to the contribution of ) is either another parent event, or (more likely) an offspring that was a result of a previous parent event’s increase in the intensity function. Under this interpretation, controls the branching ratio, or likelihood of an arrival causing another arrival. (Indeed, in order for the process to be stationary we must ensure the largest eigenvalue of the excitation matrix is .)

We may represent this branching structure with a matrix such that if the th event is a child of the th event, and otherwise (note only if is a parent event). This provides a natural latent variable for the expectation-maximization procedure we outline in Methods, and it also provides a source of information about the structure of an individual’s day-to-day activity.

The multivariate periodic Hawkes process (MPHP) provides a powerful framework to model the activity of an individual, capturing both interdependence of event types and periodicity. The parameter may be fine tuned to represent different granularities of periodicity as the question requires or data permits. For this study, we retain simplicity by assuming and are global parameters for an individual governing all activity types, but this could be fairly straightforwardly extended if appropriate. Treating as a global parameter has precedent and significantly reduces the burden of parameter estimation.

3 Results

3.1 Data

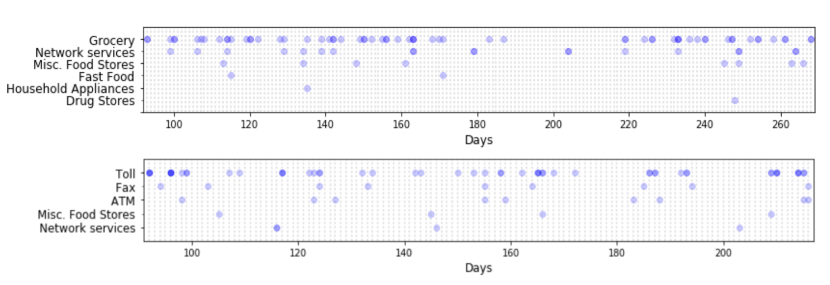

We apply our model to six months of credit card records in Mexico City. In this dataset, the activity types are purchase categories (e.g. tolls, fast food restaurants, drug stores). Our results focus on the 23,317 individual users within the dataset with at least 90 transactions. The granularity of time stamps is one day, and thus we model periodicity depending on the day of week only. Examining this data in Fig. 1, we see that empirical patterns in credit card transaction history show clear burstiness for two sample users.

3.2 Interdependence and Branching Structure

We begin with some qualitative observations about interdependence and branching structure of individuals’ activity patterns encoded in the excitation matrix and branching matrix revealed by the MPHP parameter estimation approach outlined in Methods.

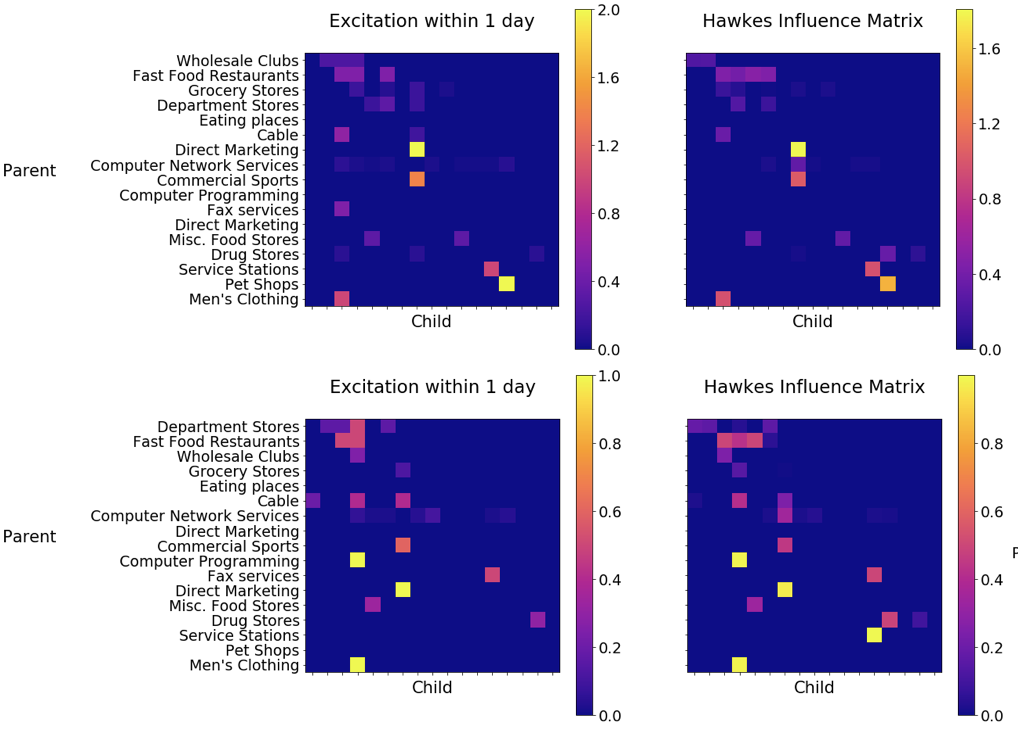

Recall each excitation parameter in scales the additive contribution of previous event on the rate of arrival for event , and thus describes the dependence of activity on activity — for this reason, one may refer to as the “influence matrix” although we are careful to note we are making no claims of causality. Fig. 3 compares, for two sample individuals, the same-day co-occurrence of pairs of transaction behavior in the empirical data (left) with the estimated excitation matrix of the MPHP model (right). We note a close correspondence between quantities, indicating primarily captures simple co-occurrence relationships. We also, however, note important exceptions: (i) where the Hawkes model identifies high co-occurrence behavior as spurious, assigning a low excitation parameter, and (ii) where despite low same-day co-occurrence, the Hawkes model detects important co-excitation.

Also recall the latent variable represents whether event was a parent of a child event , and our EM methodology provides an estimate such that , as described in Methods. This reveals additional, branching structure in a sequence of transactions, depicted in Fig. 4. While the credit card records provide only a “flat” timeline of events, the MPHP learns tendencies of certain event types to act as “parent events” of others. For example, for this individual, we observe frequent self-excitation among tolls, and a tendency for fast food purchases to act as parent events for other purchase activity.

3.3 Monte Carlo Hypothesis Testing

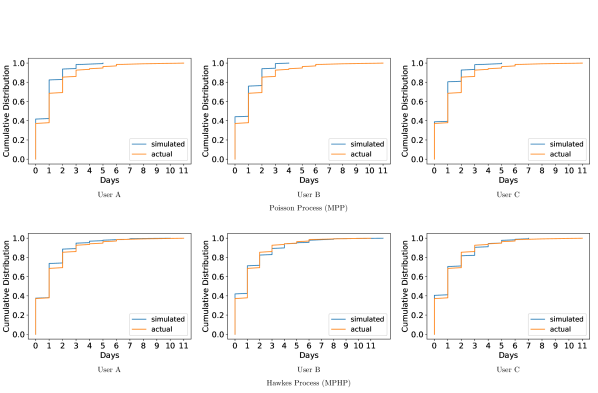

We next test the MPHP’s ability to capture an individual’s distribution of interevent times, in comparison with a non-homogeneous (periodic) Poissonian baseline. For each user, we learn a MPHP model and compare the model’s predictions with the empirical cumulative distribution of inter-event times (see Methods). Due to the inherent burstiness of human activity, we expect heavy tails in each distribution. The proposed MPHP better captures bursty inter-event time distributions than a multivariate periodic Poisson process (MPP), as shown by the empirical distributions for several example shoppers in Fig. 5.

Because the estimated parameters depend on the empirical data, we use Monte Carlo hypothesis testing to assess the significance of the agreement for each user. At the 5% significance level, our model can only be rejected for 29.8% of users. For this minority, the probability of a one day inter-event time was comparable to that of a same day inter-event time, indicating that their excitation function is not exponential decaying. For these cases, a better fit may be achieved with the substitution of a triggering kernel that does not start decaying until after one day. A nonparametric triggering kernel [42, 3] could result in a closer fit for all users, but would result in losses in both interpretability and scalability.

In comparison to the Hawkes model, a Poisson model, even with periodic intensity, is rejected for 100% of users. We see that the proposed model is complex enough to capture a wide range of human behavior, while remaining simple enough to lend insight into patterns within individual activity.

3.4 Prediction

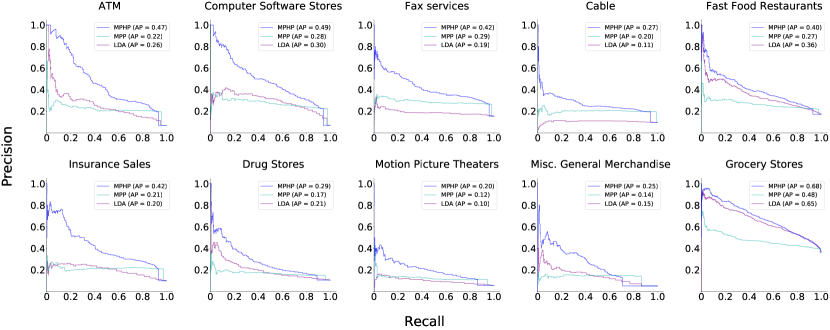

Lastly, we compare the predictive ability of the Hawkes model with a periodic Poisson process and latent Dirichlet allocation (LDA) [5]. LDA is a generative statistical model commonly used in the context of natural language processing. It is able to identify shared patterns across users, without the temporal dimension.

To evaluate the predictive ability of our model, we consider a binary classification task: given all purchases of a user until time , will the user make a new purchase type in the next time period, ? For each user, is a randomly chosen day within the last 10% of the user’s total history. We choose a small time window of days to measure each model’s ability to capture self-exciting behavior in addition to general patterns in activity.

For almost all activity types, an overwhelming majority of users will not make a purchase of that type (90% - 97%). Due to the imbalanced nature of the data, we use precision and recall as metrics to evaluate prediction performance. Denote as the number of positives (where a positive indicates that the corresponding individual made a purchase of the specified activity type within the time window), as the number of true positives (individuals correctly classified as making a purchase of the specified activity type), and as those the algorithm classifies positive, correctly or incorrectly. Then we have and .

For each model, we first estimate parameters for an individual using the time interval , then repeatedly generate sequences from the model in the time window . We record the percent of sequences containing a purchase of the specified type and compare with the data. For a discussion of our sampling procedure for the MPHP, see Methods. MPP and LDA are standard techniques and we refer the interested reader to more detailed texts.

As we can see from Fig. 6, the multivariate periodic Hawkes process (MPHP) outperforms both the multivariate periodic Poisson process (MPP) and LDA in predicting a range of event types. This shows that the temporal dimension is necessary to describe human behavior, and further, that more than periodicity is needed.

4 Discussion

Our results demonstrate that the excitation structure between events, when coupled with weekly cycles, is able to generate realistic and predictive trajectories of shopping activity. In addition to accurately describing heavy tails in inter-event time distributions, the proposed model solidly outperforms baseline models in difficult prediction tasks. In general, our results demonstrate the effectiveness of task prioritization and periodicity in explaining activity involving credit card transactions, however, the model is readily applicable to a broader range of individual human activity (for example, making phone calls, doing chores) which we hope to pursue in future work.

Furthermore, the model is highly interpretable, in contrast with many state-of-the-art generative and predictive models. The excitation matrix gives a direct encoding of the interdependence of activity types. The branching matrix revealed through our proposed EM technique provides more than a convenient latent variable to aid in parameter estimation, it gives important information about the relationships between specific events in an individual’s activity history. This provides an interesting direction for future research: in past work [7], communities have been found that display consistent behavioral trends in terms of spending and demographics. We can further characterize the behavior of these communities by including the temporal dimension, thus describing temporal lifestyles at urban scale.

Lastly, due to its generality and flexibility, the Hawkes model is well-suited to describe a wide range of phenomena, with applications in diverse fields as noted in the Introduction. The addition of periodic effects, and the tractability of our proposed MAP EM parameter estimation technique, provide valuable extensions in this already expansive realm of applications.

5 Methods

In this section we present our methodologies for parameter estimation, simulation, and hypothesis testing of the multivariate periodic Hawkes process (MPHP)

5.1 MAP Expectation-Maximization

Consider again a sequence of events over a time period , where is the time of the th event and is the event type, out of possible types. Also, recall the conditional intensity of the MPHP as described in Eq. 1, with parameters .

The form of actually allows us to work out the likelihood function in closed form. This fact permits direct parameter estimation of via maximum likelihood estimation methodologies. However, in practice, such methods pose many challenges due to the objective function’s low curvature and large parameter space, requiring the invocation of strong regularization schemes and sophisticated optimization techniques [41]. Alternatively, the additive nature of the intensity permits hierarchical Bayesian approaches with priors achieving the necessary regularization, but which then require variational or sampling-based approaches [18].

We introduce a simpler approach that still incorporates some regularization in the form of a prior on and . We propose an extension of the expectation-maximization (EM) scheme presented in [44, 36] to the multivariate periodic case, and we incorporate a prior on the parameters governing interaction and periodicity through maximum aposteriori (MAP) EM.111See https://github.com/stmorse/hawkes (MHP) and https://github.com/sharonxu/hawkes (MPHP) for implementations of this methodology.

First, recall the interpretation of the Hawkes model as a branching process as in Fig. 4. We introduce latent variables over the data , called the branching matrix, defined such that if the event at was caused by the event at (0 otherwise), and note implies the event at was a background event. We will estimate these latent variables by computing their expected value .

We may now define the (expected) complete data log-likelihood as

| (3) |

where . See [36, 44, 41] for a more thorough treatment of the derivation of Eq. (3).

The complete data log-posterior is

| (4) |

We seek to maximize this posterior, subject to the periodicity constraints and , using the expectation-maximization (EM) algorithm.

By using a MAP estimate, we have the opportunity to place a prior on the excitation matrix entries and the periodicity scaling parameters . A Gamma prior is conjugate with the Poisson distributions of the complete data likelihood,

| (5) | ||||

| (6) |

Using Gamma priors also provides a nice interpretation of the hyperparameters as “pseudocounts” — for example, in the case of , they represent already observed counts of parent and child events between the pair .

The EM algorithm alternates between finding the expected value of of in the expectation step (E-step), and maximizing the posterior with respect to in the maximization step (M-step). More formally, the E-step computes ,

| (7) | ||||

| (8) |

where both formulas follow directly from the additive property of Poisson processes.

For the M-step, we may obtain update formulas by explicitly solving the stationarity condition on 4:

| (9) | ||||

| (10) | ||||

| (11) |

These formulas also have accessible interpretations; for example, the estimate for the background rate is the number of background events in divided by total time . Also note the role of the Gamma hyperparameters as pseudocounts for child and parent events. Finally, note we may take advantage of the fact that to simplify calculation of .

5.2 Simulation

In order to sample event sequences from the process, we use the thinning method due to Ogata [25]. We make two important modifications to this algorithm that increase efficiency; our method is described fully in 1.

As typically described [32, 17], the thinning method requires operations to draw samples over dimensions, which is prohibitive for large processes. Instead, we modify an approach mentioned in [34]. Namely, given the rates at the last event we can calculate for by

| (12) |

which we can do in , and only requires saving the rates at the most recent event. Secondly, we improve the typical attribution/rejection framework [32, 17] for each activity type by instead viewing the procedure as a weighted random sample over activity types, that is, the integers . This allows us to forgo for-loops and instead use optimized functions for weighted random samples.

5.3 Monte Carlo Hypothesis Testing

Following [21], we assess statistical goodness of fit of a model using the area statistic, or the area between two cumulative distribution functions. We use the area statistic to compare the interevent-time distributions of the empirical data and event sequences simulated from the model.

We estimate the parameters of a stochastic process from some dataset , use these to simulate data , and record the area between interevent CDFs of the real and simulated datasets. We then estimate parameters from , simulate data , and record the area between interevent CDFs of and . We repeat this times and compute the test statistic between the groups and .

References

- [1] Joseph Abate and Ward Whitt. Asymptotics for m/g/1 low-priority waiting-time tail probabilities. Queueing Systems, 25(1-4):173–233, 1997.

- [2] Talayeh Aledavood, Eduardo López, Sam GB Roberts, Felix Reed-Tsochas, Esteban Moro, Robin IM Dunbar, and Jari Saramäki. Daily rhythms in mobile telephone communication. PloS one, 10(9):e0138098, 2015.

- [3] Emmanuel Bacry, Khalil Dayri, and Jean-François Muzy. Non-parametric kernel estimation for symmetric hawkes processes. application to high frequency financial data. The European Physical Journal B, 85(5):157, 2012.

- [4] Albert-Laszlo Barabasi. The origin of bursts and heavy tails in human dynamics. Nature, 435(7039):207, 2005.

- [5] David M Blei, Andrew Y Ng, and Michael I Jordan. Latent dirichlet allocation. Journal of machine Learning research, 3(Jan):993–1022, 2003.

- [6] Alan Cobham. Priority assignment in waiting line problems. Journal of the Operations Research Society of America, 2(1):70–76, 1954.

- [7] Riccardo Di Clemente, Miguel Luengo-Oroz, Matias Travizano, Bapu Vaitla, and Marta C Gonzalez. Sequence of purchases in credit card data reveal life styles in urban populations. arXiv preprint arXiv:1703.00409, 2017.

- [8] Xiaowen Dong, Yoshihiko Suhara, Burçin Bozkaya, Vivek K Singh, Bruno Lepri, and Alex‘Sandy’ Pentland. Social bridges in urban purchase behavior. ACM Transactions on Intelligent Systems and Technology (TIST), 9(3):33, 2018.

- [9] Samiul Hasan, Christian M Schneider, Satish V Ukkusuri, and Marta C González. Spatiotemporal patterns of urban human mobility. Journal of Statistical Physics, 151(1-2):304–318, 2013.

- [10] César A Hidalgo R. Conditions for the emergence of scaling in the inter-event time of uncorrelated and seasonal systems. Physica A: Statistical Mechanics and its Applications, 369(2):877–883, 2006.

- [11] Shan Jiang, Yingxiang Yang, Siddharth Gupta, Daniele Veneziano, Shounak Athavale, and Marta C González. The timegeo modeling framework for urban mobility without travel surveys. Proceedings of the National Academy of Sciences, 113(37):E5370–E5378, 2016.

- [12] Zhi-Qiang Jiang, Wen-Jie Xie, Ming-Xia Li, Wei-Xing Zhou, and Didier Sornette. Two-state markov-chain poisson nature of individual cellphone call statistics. Journal of Statistical Mechanics: Theory and Experiment, 2016(7):073210, 2016.

- [13] Hang-Hyun Jo, Márton Karsai, János Kertész, and Kimmo Kaski. Circadian pattern and burstiness in mobile phone communication. New Journal of Physics, 14(1):013055, 2012.

- [14] Hang-Hyun Jo, Juan I Perotti, Kimmo Kaski, and János Kertész. Correlated bursts and the role of memory range. Physical Review E, 92(2):022814, 2015.

- [15] Márton Karsai, Hang-Hyun Jo, and Kimmo Kaski. Bursty human dynamics. Springer.

- [16] Jungsuk Kwac, June Flora, and Ram Rajagopal. Household energy consumption segmentation using hourly data. IEEE Transactions on Smart Grid, 5(1):420–430, 2014.

- [17] Patrick J Laub, Thomas Taimre, and Philip K Pollett. Hawkes processes. arXiv preprint arXiv:1507.02822, 2015.

- [18] Scott W Linderman, Yixin Wang, and David M Blei. Bayesian inference for latent hawkes processes. Advances in Neural Information Processing Systems, 2017.

- [19] Alejandro Llorente, Manuel Garcia-Herranz, Manuel Cebrian, and Esteban Moro. Social media fingerprints of unemployment. PloS one, 10(5):e0128692, 2015.

- [20] Thomas Louail, Maxime Lenormand, Oliva G Cantu Ros, Miguel Picornell, Ricardo Herranz, Enrique Frias-Martinez, José J Ramasco, and Marc Barthelemy. From mobile phone data to the spatial structure of cities. Scientific reports, 4:5276, 2014.

- [21] R Dean Malmgren, Daniel B Stouffer, Adilson E Motter, and Luís AN Amaral. A poissonian explanation for heavy tails in e-mail communication. Proceedings of the National Academy of Sciences, 105(47):18153–18158, 2008.

- [22] Naoki Masuda, Taro Takaguchi, Nobuo Sato, and Kazuo Yano. Self-exciting point process modeling of conversation event sequences. In Temporal Networks, pages 245–264. Springer, 2013.

- [23] Steven Morse, Marta C González, and Natasha Markuzon. Persistent cascades: Measuring fundamental communication structure in social networks. In Big Data (Big Data), 2016 IEEE International Conference on, pages 969–975. IEEE, 2016.

- [24] Steven T Morse. Persistent cascades and the structure of influence in a communication network. PhD thesis, Massachusetts Institute of Technology, 2017.

- [25] Yosihiko Ogata. On lewis’ simulation method for point processes. IEEE Transactions on Information Theory, 27(1):23–31, 1981.

- [26] Joao Gama Oliveira and Albert-László Barabási. Human dynamics: Darwin and einstein correspondence patterns. Nature, 437(7063):1251, 2005.

- [27] Diego Pennacchioli, Michele Coscia, Salvatore Rinzivillo, Fosca Giannotti, and Dino Pedreschi. The retail market as a complex system. EPJ Data Science, 3(1):33, 2014.

- [28] Gordon J Ross and Tim Jones. Understanding the heavy-tailed dynamics in human behavior. Physical Review E, 91(6):062809, 2015.

- [29] Michael R Solomon, Dahren William Dahl, Katherine White, Judith L Zaichkowsky, and Rosemary Polegato. Consumer behavior: Buying, having, and being, volume 10. Pearson London, 2014.

- [30] Chaoming Song, Zehui Qu, Nicholas Blumm, and Albert-László Barabási. Limits of predictability in human mobility. Science, 327(5968):1018–1021, 2010.

- [31] Marijn Ten Thij, Sandjai Bhulai, and Peter Kampstra. Circadian patterns in twitter. Data Analytics, pages 12–17, 2014.

- [32] Ioane Muni Toke. An introduction to hawkes processes with applications to finance. 2011.

- [33] Jameson L Toole, Carlos Herrera-Yaqüe, Christian M Schneider, and Marta C González. Coupling human mobility and social ties. Journal of The Royal Society Interface, 12(105):20141128, 2015.

- [34] Isabel Valera and Manuel Gomez-Rodriguez. Modeling adoption and usage of competing products. In Data Mining (ICDM), 2015 IEEE International Conference on, pages 409–418. IEEE, 2015.

- [35] Alexei Vázquez, Joao Gama Oliveira, Zoltán Dezsö, Kwang-Il Goh, Imre Kondor, and Albert-László Barabási. Modeling bursts and heavy tails in human dynamics. Physical Review E, 73(3):036127, 2006.

- [36] Alejandro Veen and Frederic P Schoenberg. Estimation of space–time branching process models in seismology using an em–type algorithm. Journal of the American Statistical Association, 103(482):614–624, 2008.

- [37] Sharon Xu, Edward Barbour, and Marta C González. Household segmentation by load shape and daily consumption. 2017.

- [38] Taha Yasseri, Giovanni Quattrone, and Afra Mashhadi. Temporal analysis of activity patterns of editors in collaborative mapping project of openstreetmap. In Proceedings of the 9th International Symposium on Open Collaboration, page 13. ACM, 2013.

- [39] Taha Yasseri, Robert Sumi, and János Kertész. Circadian patterns of wikipedia editorial activity: A demographic analysis. PloS one, 7(1):e30091, 2012.

- [40] Yuji Yoshimura, Stanislav Sobolevsky, Juan N Bautista Hobin, Carlo Ratti, and Josep Blat. Urban association rules: uncovering linked trips for shopping behavior. Environment and Planning B: Urban Analytics and City Science, 45(2):367–385, 2018.

- [41] Ke Zhou, Hongyuan Zha, and Le Song. Learning social infectivity in sparse low-rank networks using multi-dimensional hawkes processes. In Artificial Intelligence and Statistics, pages 641–649, 2013.

- [42] Ke Zhou, Hongyuan Zha, and Le Song. Learning triggering kernels for multi-dimensional hawkes processes. In International Conference on Machine Learning, pages 1301–1309, 2013.

- [43] Tao Zhou, Zhi-Dan Zhao, Zimo Yang, and Changsong Zhou. Relative clock verifies endogenous bursts of human dynamics. EPL (Europhysics Letters), 97(1):18006, 2012.

- [44] Joseph R Zipkin, Frederic P Schoenberg, Kathryn Coronges, and Andrea L Bertozzi. Point-process models of social network interactions: Parameter estimation and missing data recovery. European journal of applied mathematics, 27(3):502–529, 2016.