A robust variable screening procedure

for ultra-high dimensional data

Abstract

Variable selection in ultra-high dimensional regression problems has become an important issue. In such situations, penalized regression models may face computational problems and some pre-screening of the variables may be necessary. A number of procedures for such pre-screening has been developed; among them the sure independence screening (SIS) enjoys some popularity. However, SIS is vulnerable to outliers in the data, and in particular in small samples this may lead to faulty inference. In this paper, we develop a new robust screening procedure. We build on the density power divergence (DPD) estimation approach and introduce DPD-SIS and its extension iterative DPD-SIS. We illustrate the behavior of the methods through extensive simulation studies and show that they are superior to both the original SIS and other robust methods when there are outliers in the data. We demonstrate the claimed robustness through use of influence functions, and we discuss appropriate choice of the tuning parameter . Finally, we illustrate its use on a small dataset from a study on regulation of lipid metabolism.

Keywords: Variable selection; NP dimensionality; Independence screening; Minimum density power divergence estimator; Influence Function; Gene selection.

1 Introduction

The introduction of the Omics technologies has led to a revolution in medical research, leading to an increased knowledge of the biological background of many diseases and paving the way for personalized therapies. A characteristic feature of data arising from the Omics technologies is its high dimensionality, which is a challenge for the statistical analysis. A typical example is gene expressions. The microarray technology enabled us to measure the expressions of thousands of genes simultaneously, while the number of subjects was typically rather low. More recently, sequencing technologies allow us to measure genetic features at an even finer resolution, often leading to dimensions in the millions. If we are to relate these high-dimensional features to some outcome variable in a regression set-up, we need to perform some sort of variable selection [34, 29, 38, 9, 23, 22, 25].

The most commonly used method for identifying important predictor variables in a high-dimensional regression model is to fit a penalized model. Consider the linear regression model with response variable and explanatory variables (e.g. gene expressions) as covariates, say , given by

| (1) |

where the model error is distributed as . Given the responses from independent samples and the corresponding covariate values, say , , for the -th covariate for , this model can be written in matrix form as

| (2) |

where , for . The model parameters and need to be estimated from the data. In the ultra-high dimensional case with , e.g., Omics data, we need to assume sparsity of the regression coefficient to achieve identifiability of the estimators, i.e., we assume that only a few of the components of are non-zero. Without loss of generality, we may assume that the true model parameter values are where with being the non-sparse part of size . Under sparsity assumptions, estimation of the parameters is performed through penalized estimation procedures with appropriate penalties which can successfully recover all and only the truly important variables (corresponding to non-zero ) asymptotically with probability tending to one. There are plenty of such penalized regression procedures available in recent literature, starting from the Least Absolute Shrinkage and Selection Operator (LASSO) method of Tibshirani [37] and its refinements [e.g., 42, 45] to more advanced procedures based on penalties like SCAD [6] or MCP [41], and many more, which work well in moderately high dimensions. However, a common problem with these methods in ultra-high dimensional set-ups is their computational cost and numerical issues, which has led to development of simpler variable screening methods at the initial stage to reduce the model size (e.g., number of genetic features) from the order of millions to an order of a few hundred (often lesser than the sample size as well) and then apply an appropriate penalization method to obtain final model estimates from the reduced set of covariates. The most popular method for such screening purposes is the Sure Independent Screening (SIS) proposed by Fan and Lv [7] which has a simple interpretation and theoretical guarantees along with fast computation. Even with its simple structure (the SIS ranks the covariates based on their correlation with the response), the method yet enjoys the model selection oracle property under ultra-high dimensional set-ups where for some . An iterative extension, ISIS, is also proposed in [7] to tackle the issue of collinearity among covariates. The SIS and ISIS is routinely being applied in ultra-high dimensional applications and has also been extended to more complex models [e.g., 8, 1, 43, 28]. However, one major drawback of the SIS or ISIS is its non-robust nature against data contamination as indicated already in the discussion of the original paper itself. This issue can be crucial when applying the method for screening of important genes from large scale Omics data, which are often prone to at least a few outliers. Here is our motivating data example.

Triglyceride Data:

Intake of marine omega-3 fatty acids may reduce the risk of cardiovascular disease (CVD), especially in high-risk individuals.

Elevated serum triglyceride (TG) levels are strongly associated with increased risk of CVD,

and the CVD risk reducing effect of marine omega-3 fatty acids is thought to be mainly mediated through reduction of serum TG levels.

However, it is well known that there is large individual variation with regard to TG response in relation to intake of fatty acids,

and an improved understanding of such individual variation would be beneficial.

We are analyzing data from a small randomized study () where the subjects received either fish oil,

oxidized fish oil or sunflower oil for a period of seven weeks, and serum TG levels were measured at baseline and after seven weeks.

Our goal is to relate TG response (the difference between two measurements of serum TG levels) to gene expressions measured at baseline.

Gene expressions were measured using microarray technology, and we have available data from in total probes.

Thus, an initial variable screening to reduce the model size is needed.

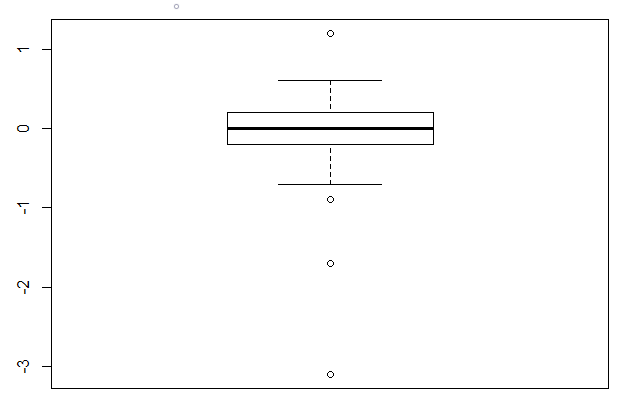

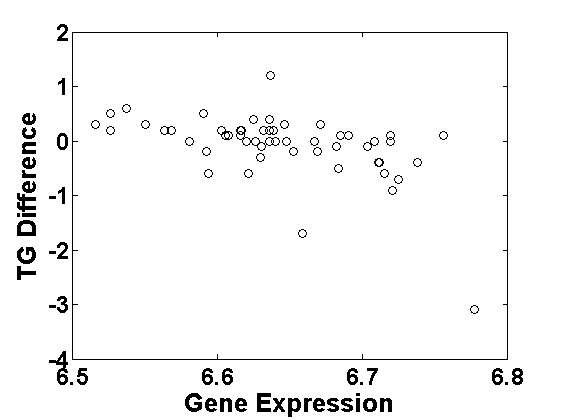

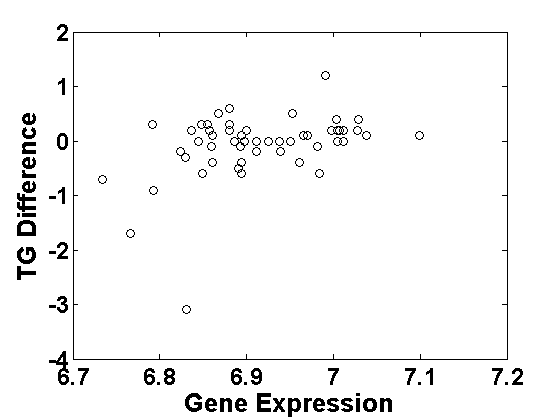

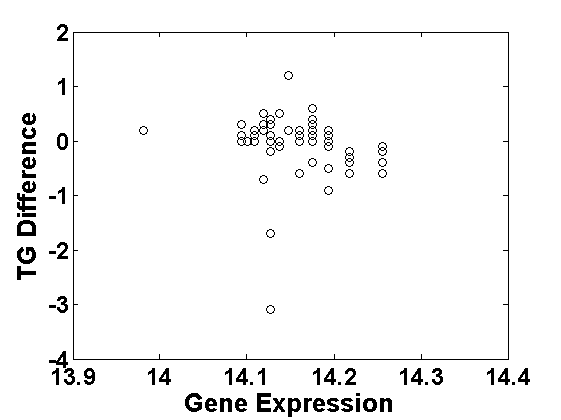

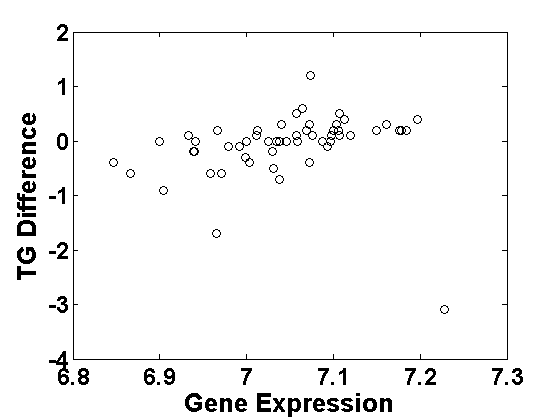

From the box-plot of the TG response (Fig 1a), it is clearly justified to fit a normal error distribution in the linear regression model (2) except for three outlying values. Now, if we are screening the genes via correlation with response in SIS or ISIS, these outliers will have an erroneous effects. Note that, it is not justified to remove these outliers at the start of the screening procedure, since they are outliers in the univariate distribution of response only but may or may not be outliers in the bivariate distribution of the response with any covariate. A few such examples are given in Fig 1b–1e; the outliers seem more legitimate in the bivariate space for the first case (Figure 1b), having no effect on the significance of the associated regression slope, but this is not true for the other cases. In Figure 1c, the outliers make the relation between the response and the corresponding gene look significant and hence it will come up towards the top of the selected gene list through usual SIS, although there is clearly no relation among these variables after removing the outliers. The situation is more serious in the last two cases (Figures 1d-1e); there are actually strong associations between the response variable and both these genes which get masked by the presence of outliers and hence, these genes will not be among the top selected genes in SIS or even through ISIS (we have checked up to three steps of ISIS). Further, Figure 1d also presents a new outlier in the covariate space (in the gene expressions) and the same outlier may be present in several other gene expressions as well; such a scrutiny for each gene is clearly not feasible with larger sets of Omics data with potentially millions of features. Even if performed (with a huge time effort), this might leave us with very few cases left for performing any reasonable (joint) inference. A robust screening method which would ignore the effect of such outliers would be of great help in such ultra-high dimensional problems.

In this paper, we will develop a new robust screening procedure, an extension of the usual SIS, using the popular density power divergence (DPD) based estimation approach (briefly described in Section 2). The DPD measure was originally proposed by Basu et al. [2] in the context of robust estimation in IID data. It has recently become very popular for robust inference in general and is widely applied on different types of data; see, e.g., [3]. The same approach has also been used for high-dimensional penalized linear regression and variable selection more recently [40, 17] and has been shown to be extremely useful under data contamination along with consistency of the resulting estimates and oracle model selection property. However, the computation is still a concern in ultra-high dimensional set-ups and a robust version of SIS along the same line would be a useful approach to analyze such data more robustly, with robust screening at an initial stage followed by the robust DPD based penalized regression method to the reduced low or moderately high dimensional set of covariates. In the current work we fill the gap in the literature for the first (screening) stage by proposing a robust screening method based on the DPD for ultra-high dimensional linear regression models and illustrate its claimed robustness property theoretically as well as numerically. A robust version of ISIS along the same line using DPD will also be discussed to tackle the correlations among covariates. The suggested method will be applied to our motivating data example.

We also compare our method with the existing state-of-the-art robust screening procedures for ultra-high dimensional linear models [19, 26, 27, 31, 39, etc.] through extensive simulation studies. The major advantages of our proposed DPD based SIS and ISIS methods can be summarized as follows.

-

•

Most (if not all) of the existing robust screening procedures are non-parametric in nature. We consider a more efficient parametric approach with robust parameter estimation to develop our robust sure screening procedure (in Section 3). Thus, when the assumed (parametric) linear regression model is even approximately correct, our proposed screening procedure enjoys a significantly improved performance over the existing non-parametric robust versions of SIS (as evident from simulations in Section 5).

-

•

As a consequence of the parametric approach, our proposed screening method indeed estimates the error variance () also from data in each step (see Sections 2-3.1), rather than just assuming it to be known (not possible in practice) or ignoring it as in most existing (non-parametric) approaches. This, in turn, provides better control of the signal-to-noise ratio in each step of the screening, eventually leading to improved variable selection behavior.

-

•

Through extensive simulation studies, we have illustrated the performance of the proposed DPD based screening procedures with suitably chosen tuning parameter value (). Under pure data, as expected with any robust procedure, the performance of the proposed screening procedures become slightly inferior compared to the usual SIS; however, the loss is small for smaller values of the underlying tuning parameter and additionally, they significantly outperform all the existing (non-parametric) robust procedures. Under contamination, our proposal performs the best, selecting the most stable set of variables even when the contamination is as heavy as 20%, whereas the usual SIS breaks down even in the presence of 5% contamination. A few existing non-parametric procedures like those based on ranks or G-K correlation [18] provide robust results under contaminations which are competitive to our proposal, but our proposed screening procedure even outperform them under more vulnerable cases like heavier contaminations, weak signal-to-noise ratios or smaller sample sizes. This makes our proposal even more advantageous over all the existing variable screening procedures.

In continuation with the last bullet point above, we would like to emphasize the size of our empirical experiments where we have considered covariates with a sample size as small as . Such an experimental set-up is more extreme compared to most (if not all) other existing work on SIS or its extensions for the linear regression model. However, they are clearly more realistic scenarios arising in medical sciences and hence provide more confidence about the performance of the proposed method in real data applications.

2 Background: The Minimum DPD Estimators

For completeness, we start with a brief description of the DPD measure and associated minimum divergence estimation process. Given two densities with respect to a common dominating measure , the DPD between them is defined, in terms of a tuning parameter , as [2]

Given IID samples from a true density to be modeled by a parametric family of densities , the minimum DPD estimator (MDPDE) of is obtained as a minimizer of with respect to , where is an empirical estimate of the true density . One of the reasons for the popularity of the DPD measure is that, unlike many other divergences, we can avoid the non-parametric density estimation (e.g., kernel for continuous models) in this estimation step. To see this, note that the third integral in is independent of , so we only need to empirically estimate the second integral where is the true distribution function. Therefore, we can just use the empirical distribution function to estimate to obtain the estimates of the second integral as . Hence, avoiding the complications of non-parametric smoothing, the MDPDE can be obtained by minimizing a simpler objective function, namely

The last term, , is added to ensure that

so that the MDPDE at coincides with the classical (but non-robust) MLE. It has been observed that the robustness of these MDPDEs increases with increasing but their asymptotic efficiency decreases slightly, although this loss in efficiency is not significant for smaller ; see [3] for more detailed theory and examples. Due to the simple interpretation as a robust generalization of the MLE, high robustness along with high efficiency and easy computation, the MDPDE has become an extremely popular estimator in parametric robust inference and has been extended to different types of more complex datasets; see, e.g., [12, 13, 14, 15, 11, 16] among many others.

In particular, Durio and Isaia [5] discussed the MDPDE for linear regression models and its theoretical properties are later established by Ghosh and Basu [12] in the context of more general independent non-homogeneous set-ups. In this set-up, we assume that the sample s () are independent but potentially have different densities which are then modeled by the family of densities , respectively. The most common example is the parametric regression model, where the distribution of the response depends of the given (-th) value of the covariates but they all share the same parameter sets – the regression coefficients (and error variance). For such set-up, Ghosh and Basu [12] proposed to obtain the MDPDE of by minimizing the average of the DPD measures over different possible densities () with respect to , which leads to the following simpler objective function (along the same lines as in the IID case)

| (3) |

Here, also the MDPDE at coincides with the corresponding MLE. Theoretical properties of the MDPDEs under this general non-homogeneous set-up is derived in [12], which are then applied to several types of regression models [14, 15, 11].

3 Proposed Robust Variable Screening Procedures

3.1 The DPD-SIS

We now consider the linear regression model (2) with ultra-high dimensional covariates and the true sparse regression coefficient as described in Section 1; let us denote the true sparse model as . Recall that the SIS method [7] can also be considered as ordering the absolute value of the slope in marginal regression models of the response with individual (standardized) covariates. Given values of the -th covariate for each , we consider the -th marginal model

| (4) |

where the s are IID for , each having distribution . We estimate the parameters by usual MLE or OLS based methods, say, . Note that, when all covariates are standardized, ranking them in order of (absolute) correlation with the response is equivalent to ordering the estimated slopes . However, this method is clearly non-robust since the estimates s are so for MLE/OLS.

Here, we will propose to use the same approach as in the usual SIS, but with robust estimates for in the marginal model using the DPD approach. Let us fix a and an . Since, given covariate values, , it belongs to the non-homogeneous set-up discussed in Section 2 and hence, we can define the MDPDE of the parameters via the objective function (3) there. For the marginal model (4), one can easily simplify the MDPDE objective function as to have the form , where

| (5) |

Then, we define the MDPDE of for the marginal model (4) as

| (6) |

This is a much simpler optimization problem with only three parameters (compared to any penalized estimation problem),

but we need to run it times (once for each ).

However, the overall computation time is still much lower than the penalized regression procedure with NP dimensional .

Based on these MDPDEs for a given , we can now choose the important variables

in order of the values of , which we refer to as the DPD-SIS procedure;

for given index we select the estimated model .

Once is obtained,

one can then apply any suitable penalized regression method

on the reduced set of covariates from

to obtain the final spares estimate of the parameters in the original model (2).

For this stage, to be consistent with the DPD-SIS,

we suggest to use the penalized DPD based estimation procedure with the same as used in the screening stage,

following Ghosh and Majumdar [17].

Therefore, our proposed robust screening procedure, the DPD-SIS, can be summarized in the following algorithm.

Algorithm 1: DPD-SIS()

-

1.

Input: -vector of responses ; matrix of covariates ; screening model size .

-

2.

For each , compute the marginal MDPDE via (6).

(This is an optimization in three parameters only and can be performed either by a standard optimization function in some software or by standard numerical techniques). -

3.

Sort in decreasing order for .

Set , if has rank , for . -

4.

Construct the estimated model set , with indices corresponding to the top values of (absolute) marginal MDPDEs.

-

5.

Run a robust penalized regression model (low or moderate dimensional) with the covariates selected in to obtain an estimated coefficient vector, say .

(We suggest to use the DPD based method of Ghosh and Majumdar [17] with the same , which also gives an estimate of the overall model error variance .) -

6.

Output: The final estimated model along with the parameter estimates (and the estimate of , if available).

Note that, at (in a limiting sense), the marginal MDPDE of regression coefficients just coincides with the MLE and hence with the OLS as well. Thus the proposed DPD-SIS algorithm at becomes close to the usual SIS of Fan and Lv [7], but differ from it in that we are also estimating in DPD-SIS (even at ) rather than estimating only in the usual SIS. This makes DPD-SIS at to have slightly better performance than the usual SIS even under no data contamination (pure data) due to better control based on the signal-to-noise ratio in each step; these claims are supported by our simulations presented in Section 5 where this method is referred to as SIS-Reg. This improvement due to the estimation of the error variance in each step is also present in the DPD-SIS with any , another advantage of our proposed robust screening procedure over the existing ones. The extent of robustness of these DPD-SIS procedures further increases with increasing values of , as will be justified and illustrated further in Sections 4 and 5.

3.2 Iterative DPD-SIS

It has been noted that the usual SIS fails to pick up a variable having weak marginal correlation but significant joint relation with the response; on the other hand, it might pick up a variable having stronger marginal correlation but no joint relation with the response. Such cases occur mostly due to strong correlation between the important and unimportant predictor variables. To solve these issues, Fan and Lv [7] also proposed an iterative extension of SIS, namely the ISIS, which selects the truly important variables even under the above situations. Later, several extensions of the original ISIS have also been proposed [33]. As a robust extension of SIS, the DPD-SIS also suffers from the above issues, and fails to provide optimal results when covariates are strongly correlated (see Section 5) and an iterative extension in the line of ISIS is required.

The DPD-SIS can be easily extended through iterations to avoid the strong effects of correlation among predictors by considering, in subsequent iterations, the residuals from the fitted regression with predictors picked up in earlier stages. More explicitly, we start with DPD-SIS (Algorithm 1) in the first step to select variables with index set . Then, in the second step, we compute the residuals from the fitted regression model of the response on the selected covariates in . The DPD-SIS screening is again applied taking these residuals as our new response to select another variables from the pool of variables with index set ; let us denote the index set of these selected variables as . We further proceed repeating these steps to generate the index sets of selected variables in the subsequent stages till we reach our target model size, say , i.e., till the smallest for which . Considering its similarity with the ISIS, we refer to this robust iterative variable screening procedure as Iterative DPD-SIS or, in short, DPD-ISIS, which is presented schematically in the following algorithm.

Algorithm 2: DPD-ISIS()

-

1.

Input: -vector of responses ; matrix of covariates ; screening model size .

-

2.

Set , and index set of available covariates as

-

3.

DPD-SIS with model size :

-

(a)

For each , compute the marginal MDPDE via (6) with response and covariate .

-

(b)

Sort in decreasing order for and set , if has rank .

-

(c)

Construct the estimated model set , with indices corresponding to the top values of (absolute) marginal MDPDEs.

-

(a)

-

4.

Run any suitable (fast) robust penalized regression model (e.g., RLARS [24]) with the main response and the covariates selected in to get estimated coefficient vector .

Let us assume that, at this -th stage, the number of covariates selected in is and denote them as so that the estimated coefficient vector has the form . Denote . -

5.

If a specified stopping criterion (see discussion below) is satisfied, go to step 8. Otherwise go to Step 6.

-

6.

Compute the residuals .

-

7.

Set and the index set of available covariates as .

Change to and go to Step 3. -

8.

Run a robust penalized regression model (low or moderate dimensional) with the covariates selected in to get estimated coefficient vector, say .

-

9.

Output: The final estimated model along with the parameter estimates (and the estimate of , if available).

A few remarks related to the above algorithm is in order before further discussions. Firstly, the most straightforward stopping criterion (required in Step 5) could be . Step 8 assumes that the size of , at the end of the last iteration, is exactly , which may not always be the case. When , we may work with all those selected variables or remove the extra variables having lower values of the marginal MDPDEs at the last stage of iteration. Alternatively the DPD-ISIS can also be terminated after a pre-fixed number of iterations (say ) or when the size of the active set does not change from its value in the previous iteration .

Secondly, in step 4 of DPD-ISIS, any fast robust penalized regression method, like RLARS, may be used without hampering the basic structure of DPD-ISIS. However, we strongly suggest to use the DPD based penalized regression method of Ghosh and Majumdar [17] with the same in Step 8 to obtain the final model; as in DPD-SIS, it makes the whole procedure structurally consistent and also provides an estimate of the overall error (unexplained) variance in our final model.

Finally, it is worthwhile to note that our algorithm of DPD-ISIS is more similar to an extension of ISIS, namely Van-ISIS described in [33], rather than its original version proposed in [7]. The difference is mainly in Step 4 of the algorithm, where we consider all the covariates selected till the -th iteration in the penalized joint regression model in the -th stage, as in Van-ISIS; hence a variable which has been selected in an earlier stage could have been removed at the -th stage due to insertion of new variables in the model. The original version of Fan and Lv [7] considered the penalized regression to be run with only the variables selected in that -th iteration (and not the previously selected covariates) and hence a false positive selected at one iteration cannot be removed at any subsequent iteration. In this method the model size continue to increase whereas, in our approach, it may grow or shrink depending on the joint relationship of all the variables selected, reducing the number of false-positive covariates.

Although the DPD-SIS at is similar to the usual (non-robust) regression based SIS, the DPD-ISIS() is slightly different from its usual non-robust counterpart van-ISIS. Due to the use of RLARS within iterations, the DPD-ISIS() is slightly more robust than van-ISIS and additionally DPD-ISIS at any (including 0) estimates the error variance in a marginal regression setting whereas the usual van-ISIS uses marginal correlation based screening. However, the DPD-ISIS at is not yet acceptable as a robust method since the estimates of the marginal regression coefficients are still non-robust (MLE). As increases, the proposed DPD-ISIS becomes more robust, which is justified theoretically through the influence function of the underlying marginal MDPDE in the following section.

4 Robustness of the proposed DPD-SIS procedure

The proposed variable screening methods DPD-SIS and DPD-ISIS both depend crucially on the estimates from each marginal regression model and hence, the same is true for their robustness. If these marginal estimates are robust with respect to any outliers or noise contamination in either the response or the corresponding covariate, their ordering (in absolute value) is also expected to be robust under data contamination, leading to correct and stable variable screening.

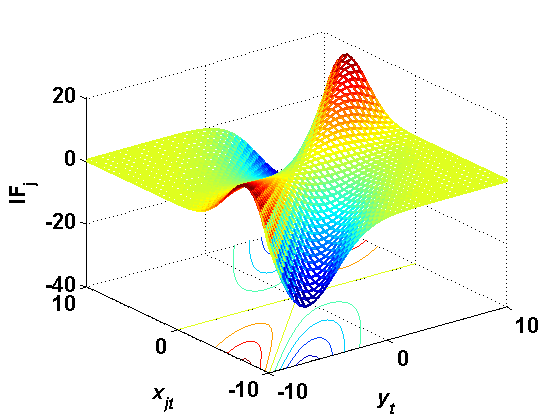

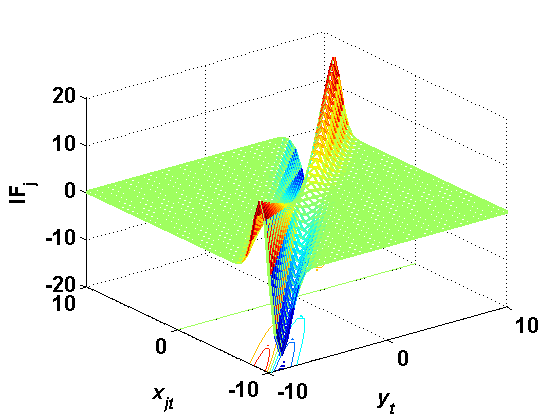

The robustness of the MDPDE under any parametric set-up, including the linear regression model, is well-studied in the literature [3, 12, 14]; it is known to crucially depend on the choice of . At the MDPDE coincides with the MLE and hence, it is extremely non-robust; its robustness increases with increasing values of . This can be examined theoretically through the concept of influence functions and gross error sensitivity [20]. The influence function indeed measures the asymptotic (standardized) bias of the estimator caused by an infinitesimal contamination through the degenerate distribution at a distant outlier point. For our -th marginal regression model (4), the influence function of the MDPDE estimator of the regression coefficients with respect to the contamination point, say , in the response for a given covariate value, say , can be obtained from the general results of Ghosh and Basu [12]. When the assumed linear model is true with parameter values , it has a simplified form given by

To study its nature, in Figure 2 we plot over the contamination point for different values of , by taking the true parameter values to be . We assume and . For the case , the above influence function simplifies to a linear function of , and hence, it is unbounded with respect to the contamination point , for all possible covariate values which justifies the well-known non-robust nature of the MLE (MDPDE at ). However, it can be clearly seen from Figure 2 that, for the proposed DPD-SIS at any , the influence function of the corresponding marginal estimator is bounded in the contamination point for all values of , indicating the claimed robust nature.

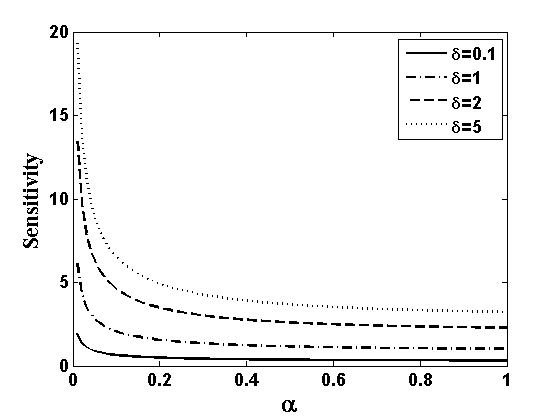

Further, we also study their self-standardized gross error sensitivity, which is the maximum of the -norm of the influence functions, standardized by the variance of the MDPDE, over all possible contamination points. It is clearly observed from Figure 3a that these sensitivity measures indeed decrease with increasing for any given value of ; thus the extent of robustness of the MDPDE increases with increasing values of . As a consequence, the same is also expected for the proposed DPD-SIS (or DPD-ISIS) with increasing .

Remark 4.1.

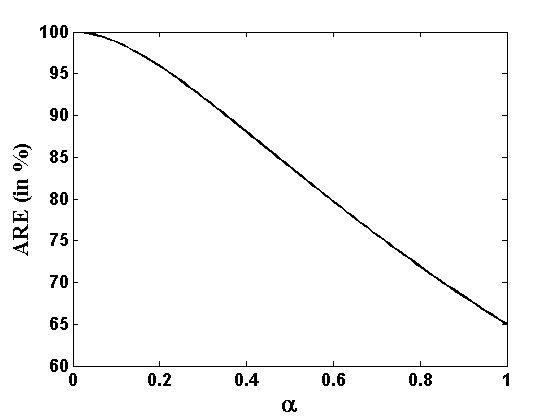

Although we have seen that the robustness increases as increases, we cannot use the larger values of in every cases. This is because, when there is no outlier (pure data) with respect to the assumed (marginal) regression model, the asymptotic variance of the MDPDE is known to increase with increasing values and hence their asymptotic relative efficiency (ARE) compared to the (most efficient but non-robust) OLS/MLE decreases as increases (see Figure 3b). Therefore, in summary, the tuning parameter provides a trade-off between efficiency of the MDPDE under pure data and its robustness under data contamination (which is the case with most common robust inference approaches) so that we need to choose carefully for any practical application, ideally depending on the amount of expected contamination in the data. In the following section (Section 5), we will empirically investigate the performance of the proposed MDPDE-based variables screening procedures, DPD-SIS and DPD-ISIS, under various situations and accordingly provide more insights and suggestions on the choice of in DPD-SIS (or DPD-ISIS) in the subsequent Section 5.5.

5 Simulation Studies

5.1 Experimental Plans

We have performed extensive simulation studies to study and illustrate the performance of our proposed DPD based screening procedures. For each set-up we have simulated a random sample of size from a linear regression model (2) of dimension where the covariates, except the intercept, are generated from a multivariate normal distribution having mean vector and some specified covariance matrix, say . After generating covariate values and error components for some fixed , the responses are computed based on specified true values of the regression coefficient ; these true values are taken to be sparse with only the first components being non-zero and the rest being zero. So, other than the intercept, only four covariates are significantly related with the response variable and the rest are noise covariates in all our simulation set-ups. Additionally, to study the robustness, a part (say, ) of the samples are contaminated through an appropriate contamination scheme. All the parameters in the simulations are considered as follows.

-

•

Two possible sample sizes are considered; and . For each case, the model dimension is taken as to mimic the common ultra-high dimensional set-ups appearing in real life. Recall . These set-ups are clearly more extreme with regard to dimensionality compared to the set-ups studied in the SIS literature, but we believe they are closer to the true scenarios in practical Omics data analysis.

-

•

The first non-zero coefficient values are all taken as 1. Three different values of the error variance are considered; given by , which yield three types of signal strengths having different signal-to-noise (SN) values. We refer to them, respectively, as strong (SN=5), moderate (SN=1) and weak (SN=0.5) signals.

-

•

Different correlation structures are considered among the covariates via different . In particular, we consider independent covariates with being identity, and two types of correlated cases with the -th elements of being , and . We will refer to these two cases, respectively, as the case of partially correlated and strongly correlated covariates. Several values of have been studied but the SIS performance results corresponding to only (in both cases) are reported in the paper for brevity.

-

•

We have also studied different types of contamination schemes which all yield similar (in spirit) results. Hence, for brevity, we present the results for one particular contamination scheme where the responses are contaminated by replacing its value (say) by . The contamination proportion is taken as , resulting in mild, moderate and heavy contaminations, respectively.

For each simulation set-up, we have applied the proposed DPD-SIS procedure to select the important variables and different performance measures are computed in order to study the results. The whole process is replicated 300 times to report some stable summary of the performance measures. In particular, the performance measures considered are

| (10) |

Note that the average IC over all 300 replications yields the percentage of times the full model is selected in a model of size (). This is reported in the tables. However, for a deeper understanding, resulting values of TP and MMS from 300 replications are presented in terms of box-plots and histograms, respectively. Additionally, a run-time comparison is provided towards the end of this section.

Along with studying our proposed DPD-SIS, the above performance measures are also used to compare our proposal with existing parametric and nonparametric competitive screening procedures. In this paper, we have considered the following competitive methods, where the first two are usual SIS approaches (non-robust) and the remaining four are robust non-parametric extensions of the SIS available in the literature.

-

•

SIS: The usual SIS of Fan and Lv [7] which use the Pearson correlation between the response and covariates for screening.

-

•

Reg-SIS: The version of the usual SIS obtained from a marginal regression model, as in [8], but considering the error variance as a parameter in the model and estimating it (along with the regression coefficients) using the maximum likelihood approach. This is indeed the same as DPD-SIS().

-

•

Rank-SIS: A robust extension of SIS obtained by using non-parametric rank correlation in place of Pearson correlation in SIS [26].

- •

- •

-

•

MCP-SIS: A robust extension of SIS based on a robust measure of association, namely the median of component-wise products (MCPs) introduced by Mu and Xiong [31], which is used to rank the covariate importance.

Another non-parametric robust screening procedure is available in the literature, based on the bivariate winsorized (BW) correlation estimator of Khan et al. [24] in place of the usual correlation in SIS; we have not considered this BW based SIS, since Mu and Xiong [31] have already shown it to have similar performance as the MCP-SIS considered here.

In the following two subsections, we give the results from our simulation studies with pure and contaminated data, respectively, for studying the performance of different SIS approaches. Another set of simulation results illustrating the performance of DPD-ISIS will be discussed later in Subsection 5.4.

5.2 Performance of the DPD-SIS without contamination

Let us first illustrate the performance of the DPD-SIS under pure data containing no outliers. For all the simulation set-ups without contamination as described in the previous subsection, the percentage of times the full (correct) model is selected (average IC) by different SIS approaches with target model size is reported in Table 1. One can immediately see that, as expected, all the SIS methods fails in case of strongly correlated covariates (except for large sample sizes and strong signal strength) and we need to use appropriate ISIS is such cases; we will illustrate the performance of our proposed DPD-ISIS later in Section 5.4. For the other two types of covariates, the performance of our proposed DPD-SIS under pure data deteriorate slightly with increasing values of (due to the loss in efficiency of MDPDE under pure data), but the DPD-SIS at are pretty much comparable with the usual SIS is most cases and also significantly better compared to the existing non-parametric robust SIS approaches. For all the partially correlated cases as well as independent cases with moderate to strong signals and , the DPD-SIS provides the correct full model in over 90% of the replications which decreases as the signal strength becomes weaker or sample size becomes smaller. Among the two types of covariates, the performance is far better when some amount of correlation is present compared to the fully independent covariates when we have weaker signal strength and/or smaller sample sizes. The good behavior of the methods in the case with partially correlated data is caused by the way we simulated our data, with a cluster of important variables at the start of the -sequence. When these important variables are randomly distributed in the sequence, the results are less good (as expected). This holds for all methods, but their relative behavior is again observed to be the same as in the present case. So, to keep our focus on comparison between the models, we have not presented the results for randomly distributed important covariates for brevity.

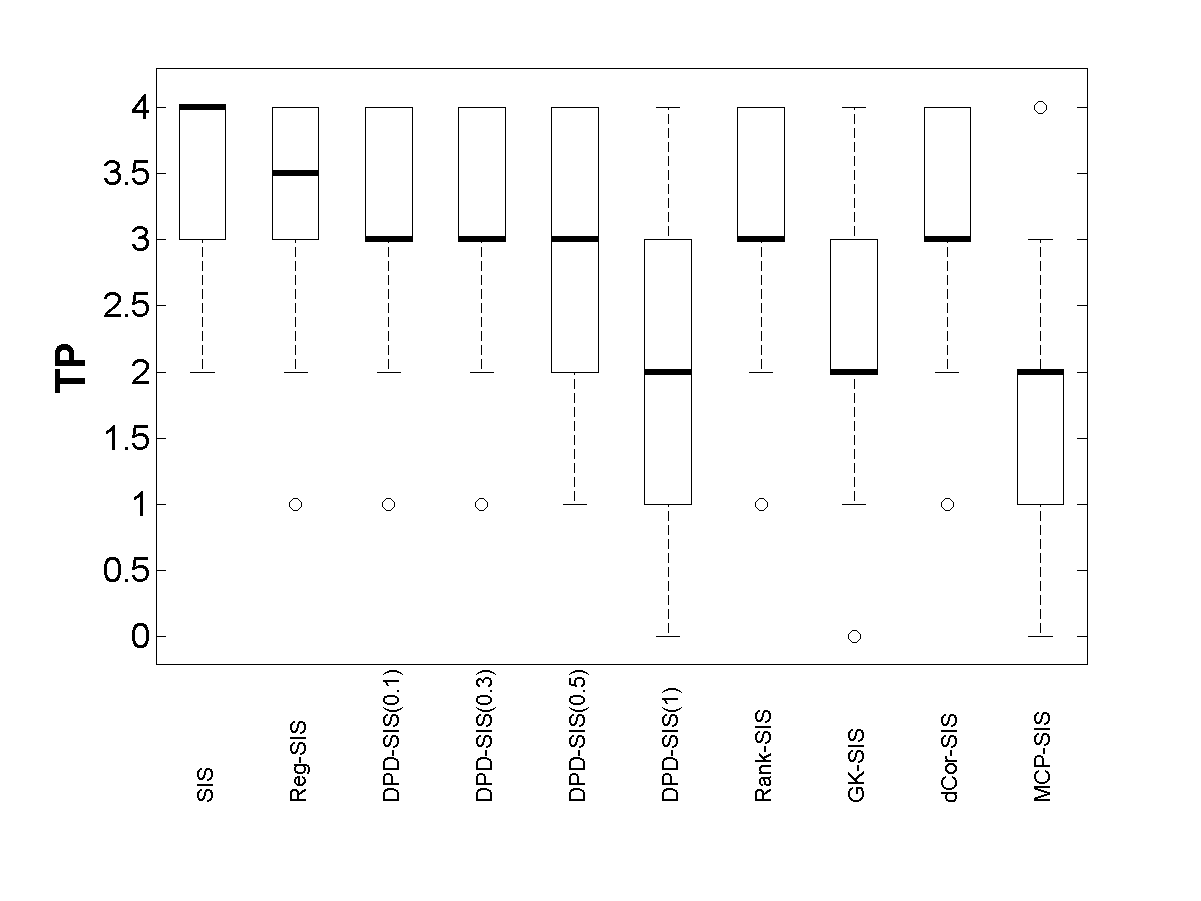

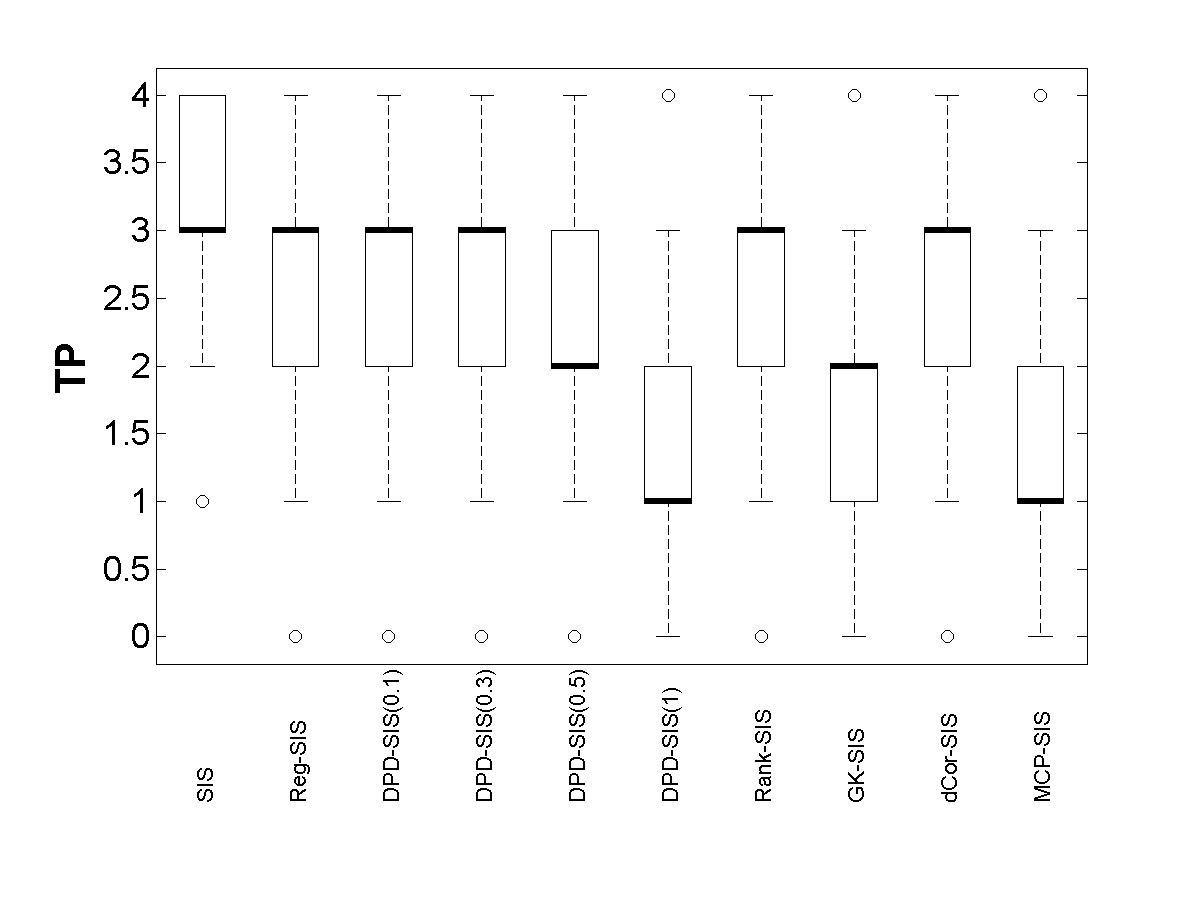

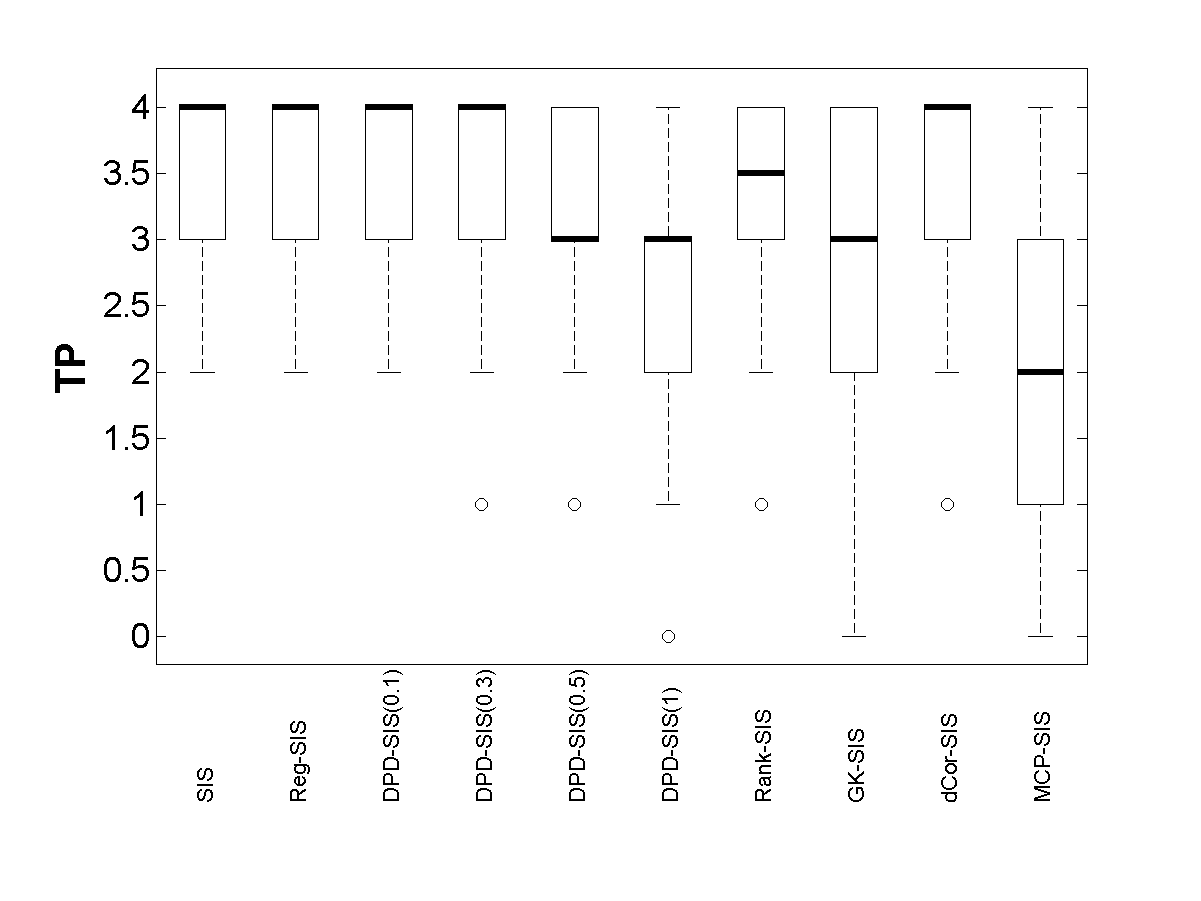

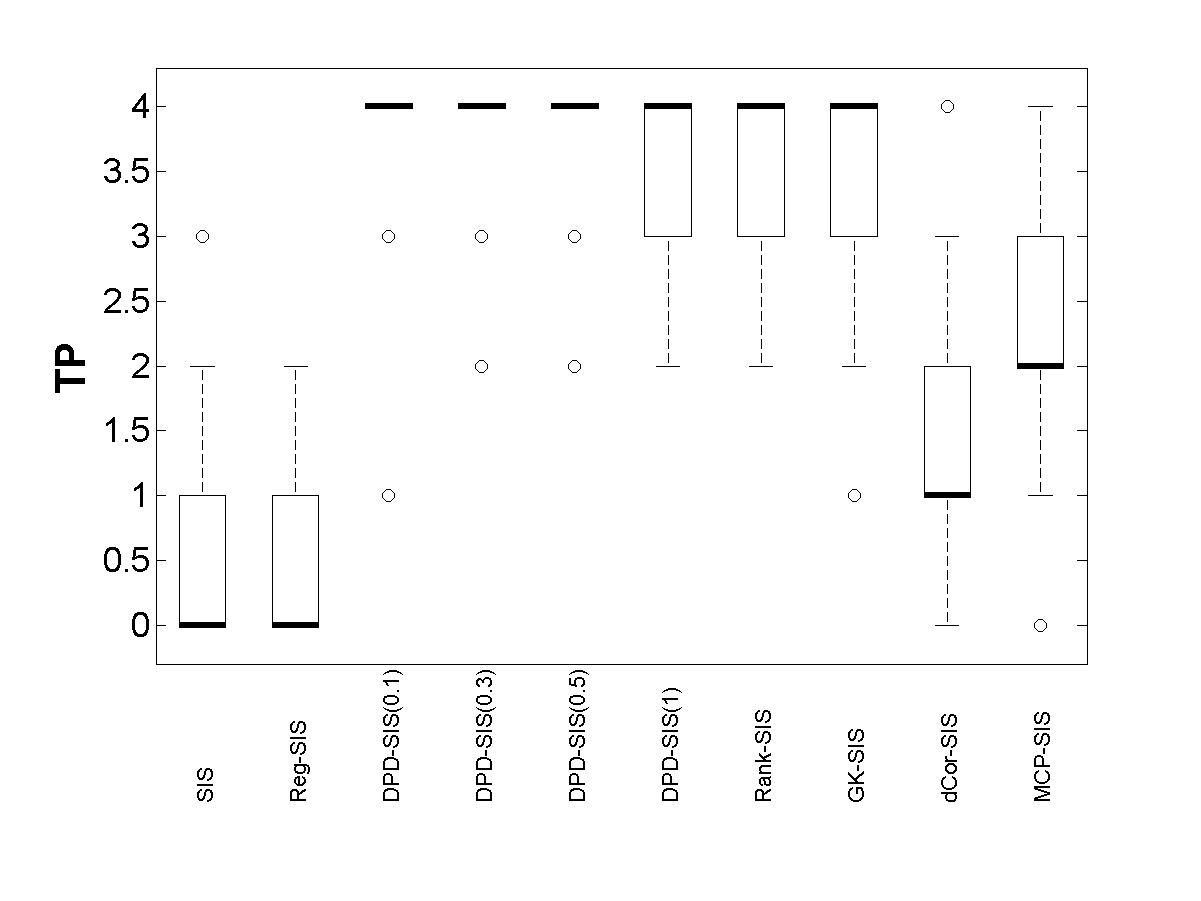

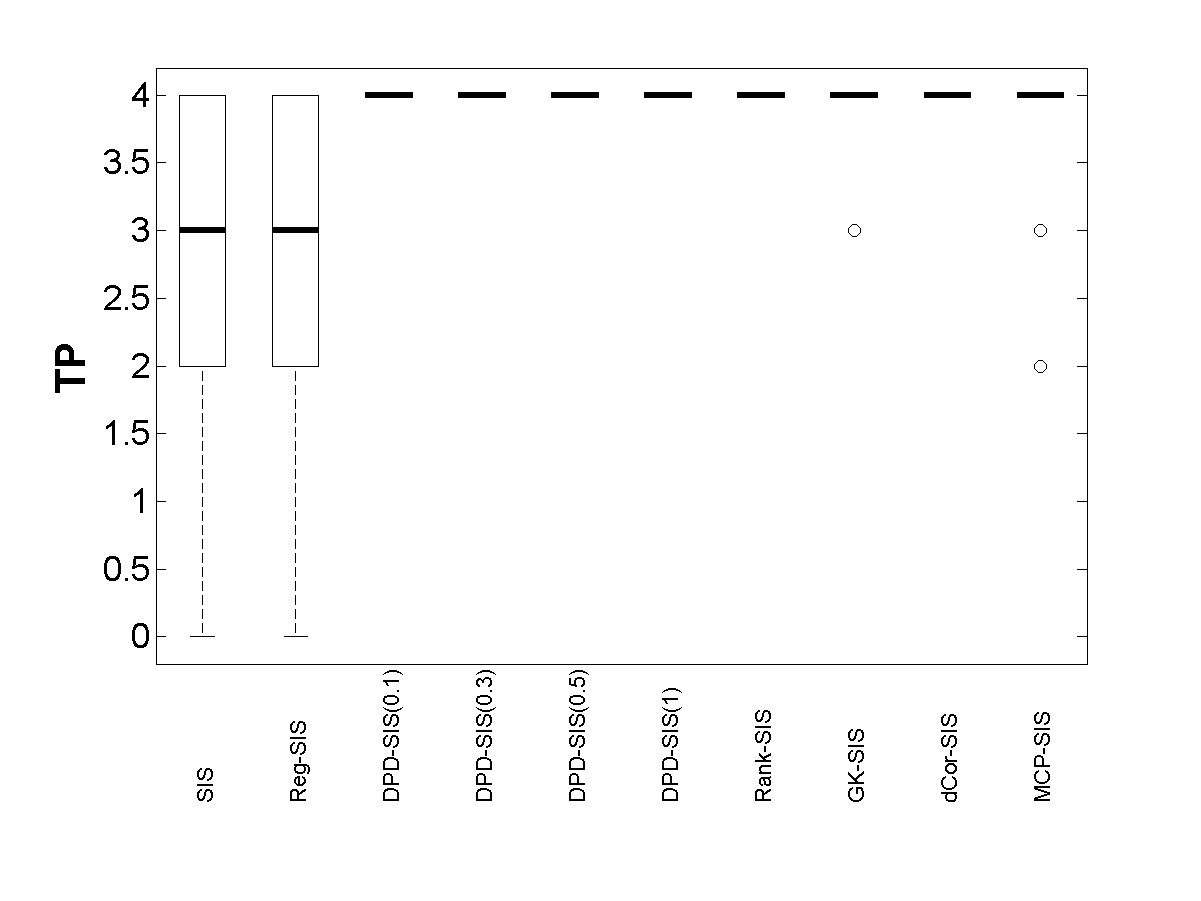

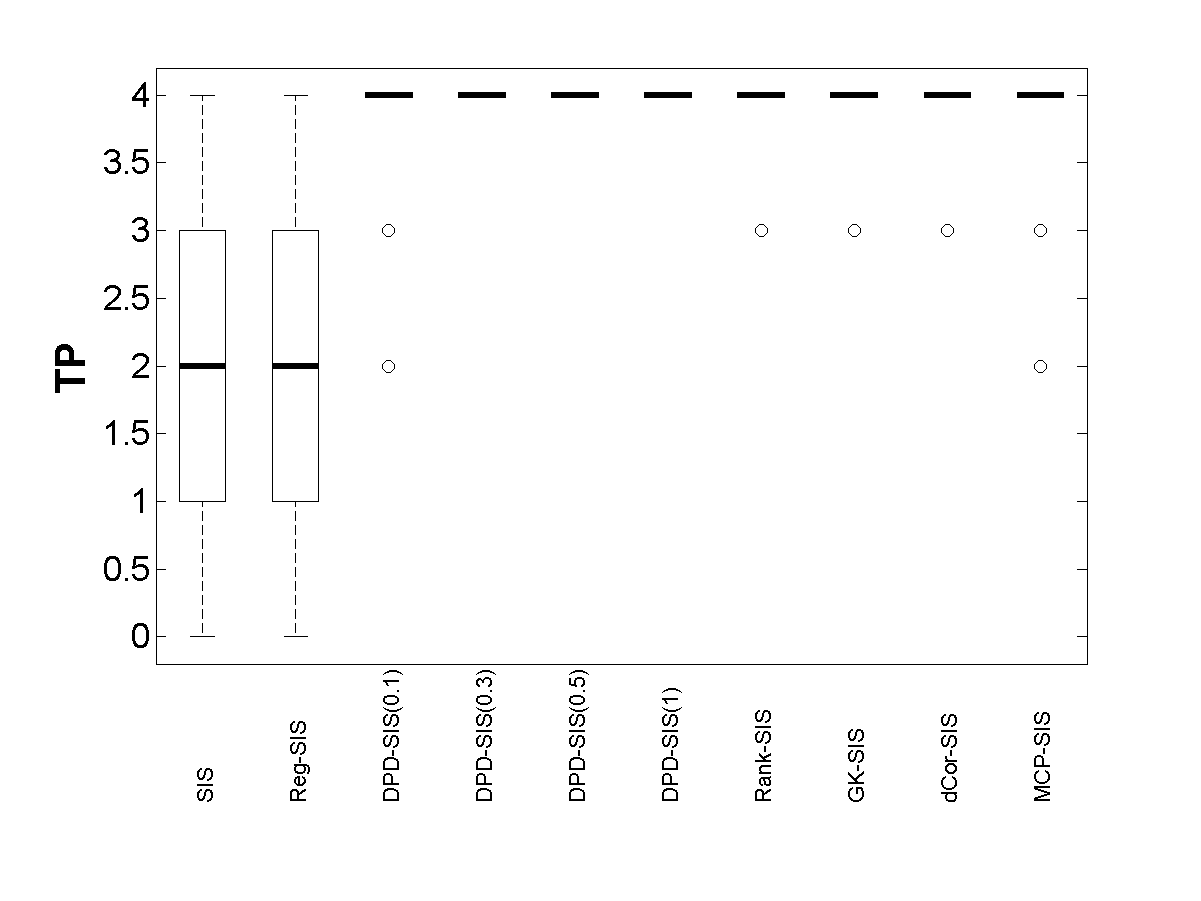

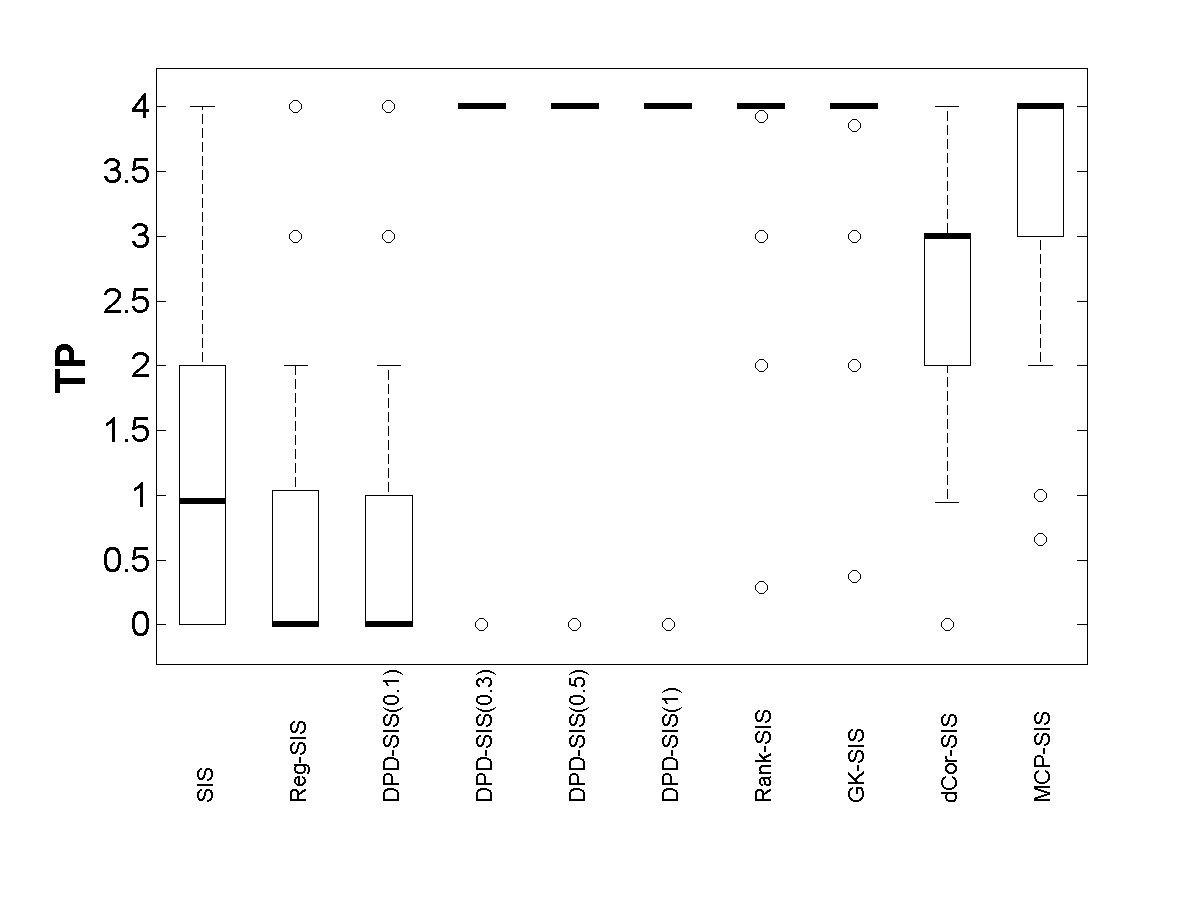

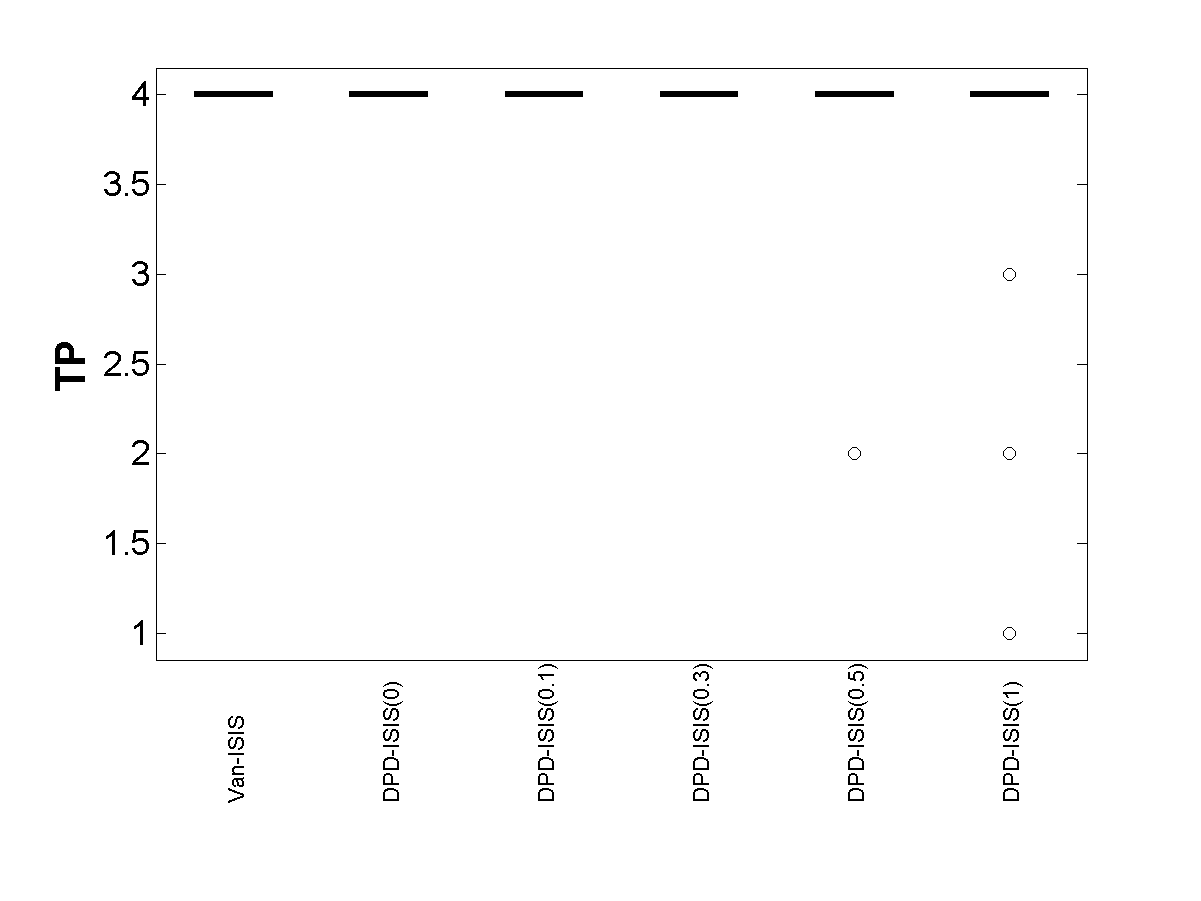

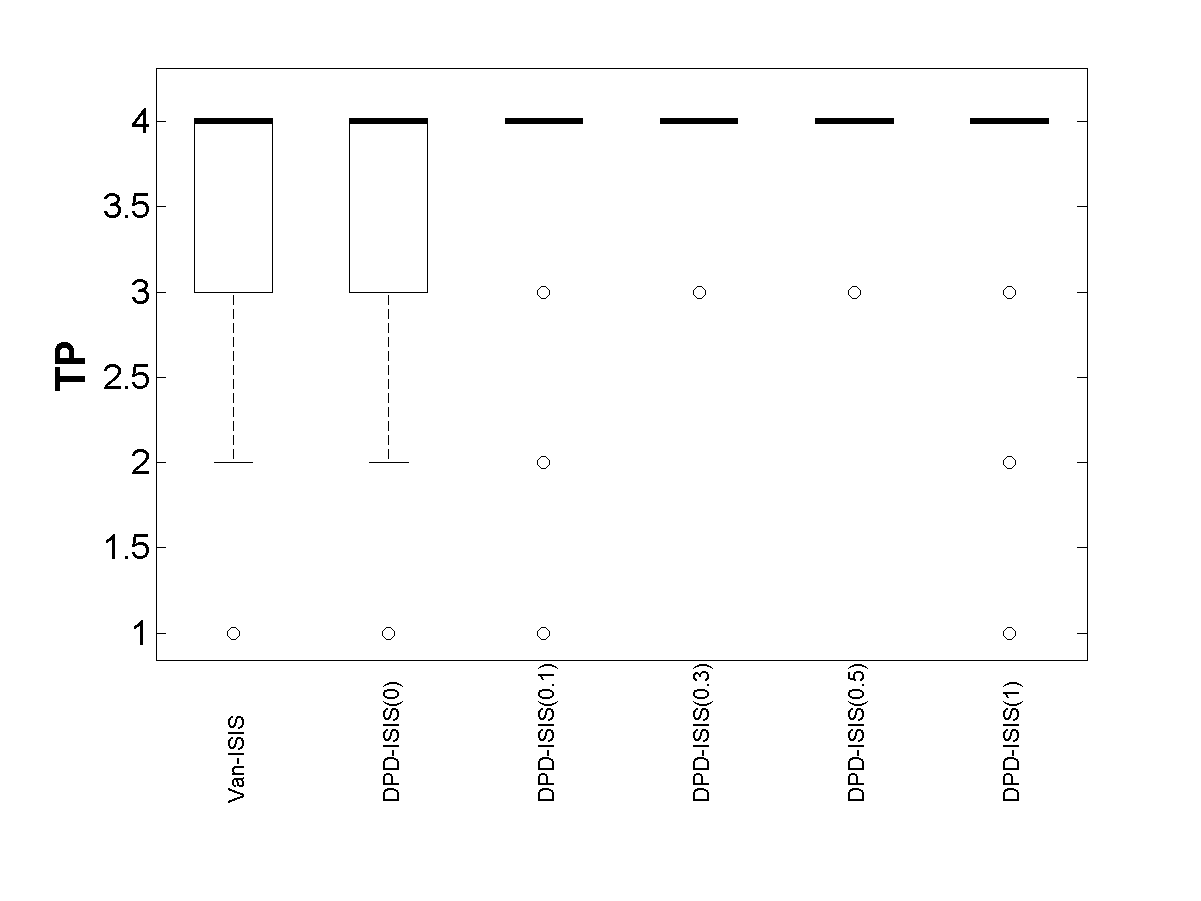

The methods can be compared further via the other performance measures, TP and MMS. With regard to TP, our simulations show that the median of the true positives selected by the usual SIS, Reg-SIS and our DPD-SIS at with a target model size of are all equal four (the true active set size) for the cases of partially correlated covariates under pure data and hence, they are extremely comparative in these cases (data not shown). For the independent covariate cases, the box-plots of the obtained true-positives are presented in Figure 4 where we can see that the results are again very similar for . For smaller sample size , however, the results are not that good; the usual SIS has median true-positive values of 4, 3 and 2, respectively, for strong, moderate and weak signals, whereas the median true positives obtained by DPD-SIS at are 3, 3, and 2, respectively. The values of true-positives generally seem to decrease with increasing in DPD-SIS under pure data scenarios but also gives very competitive results in most cases. As for the other (non-parametric) robust methods, the Rank-SIS and the dCor-SIS also perform reasonably well with regard to this measure.

| Signal | Sample | Non-robust SIS | Proposed DPD-SIS() | Existing Robust (Non-parametric) SIS | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Strength | size () | SIS | Reg-SIS | Rank-SIS | GK-SIS | dCor-SIS | MCP-SIS | ||||

| Independent Covariates | |||||||||||

| Strong | 50 | 55.0 | 50.0 | 48.3 | 41.7 | 27.7 | 8.0 | 41.7 | 12.7 | 43.7 | 1.7 |

| 100 | 99.0 | 99.7 | 99.7 | 98.7 | 98.3 | 90.7 | 97.7 | 93.7 | 97.7 | 49.3 | |

| Moderate | 50 | 25.3 | 20.7 | 18.7 | 15.7 | 10.0 | 1.0 | 14.7 | 5.3 | 15.3 | 0.3 |

| 100 | 94.3 | 95.7 | 94.7 | 93.3 | 91.3 | 72.0 | 91.0 | 77.3 | 91.3 | 26.3 | |

| Weak | 50 | 2.0 | 1.3 | 1.0 | 1.0 | 0.7 | 0.3 | 1.3 | 0.7 | 0.7 | 0.0 |

| 100 | 58.7 | 58.0 | 57.3 | 53.7 | 44.7 | 23.3 | 50.0 | 26.7 | 50.7 | 5.3 | |

| Partially Correlated Covariates with | |||||||||||

| Strong | 50 | 99.3 | 99.7 | 99.7 | 99.7 | 99.0 | 86.3 | 98.3 | 78.0 | 98.7 | 49.3 |

| 100 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 97.7 | |

| Moderate | 50 | 98.7 | 99.3 | 99.0 | 98.7 | 97.3 | 73.7 | 95.7 | 68.0 | 97.7 | 37.7 |

| 100 | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 95.4 | |

| Weak | 50 | 86.7 | 86.0 | 85.3 | 82.3 | 75.7 | 38.3 | 79.0 | 42.0 | 80.7 | 20.3 |

| 100 | 99.7 | 99.7 | 100.0 | 100.0 | 100.0 | 99.7 | 99.7 | 97.3 | 100.0 | 85.0 | |

| Strongly Correlated Covariates with | |||||||||||

| Strong | 50 | 14.7 | 1.7 | 1.7 | 1.0 | 0.7 | 0.0 | 5.7 | 0.0 | 9.0 | 0.0 |

| 100 | 82.3 | 49.0 | 48.0 | 39.0 | 25.7 | 7.3 | 59.7 | 2.7 | 66.3 | 1.0 | |

| Moderate | 50 | 5.0 | 1.0 | 1.0 | 0.7 | 0.7 | 0.0 | 2.3 | 0.0 | 2.7 | 0.0 |

| 100 | 31.7 | 24.4 | 17.4 | 4.4 | 64.6 | 64.6 | 43.0 | 1.0 | 50.0 | 0.4 | |

| Weak | 50 | 0.7 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.3 | 0.0 |

| 100 | 25.0 | 10.3 | 8.7 | 8.3 | 5.3 | 1.3 | 14.0 | 0.7 | 16.0 | 0.3 | |

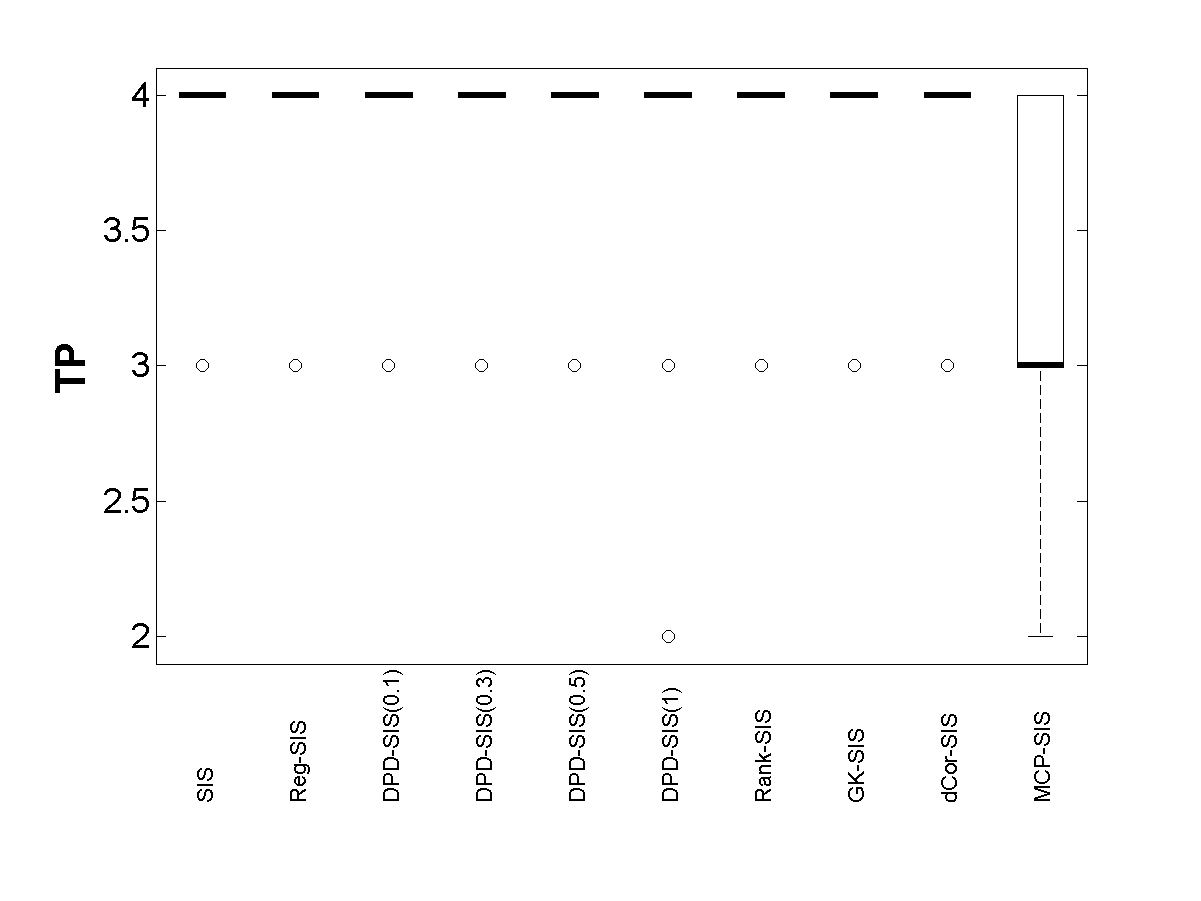

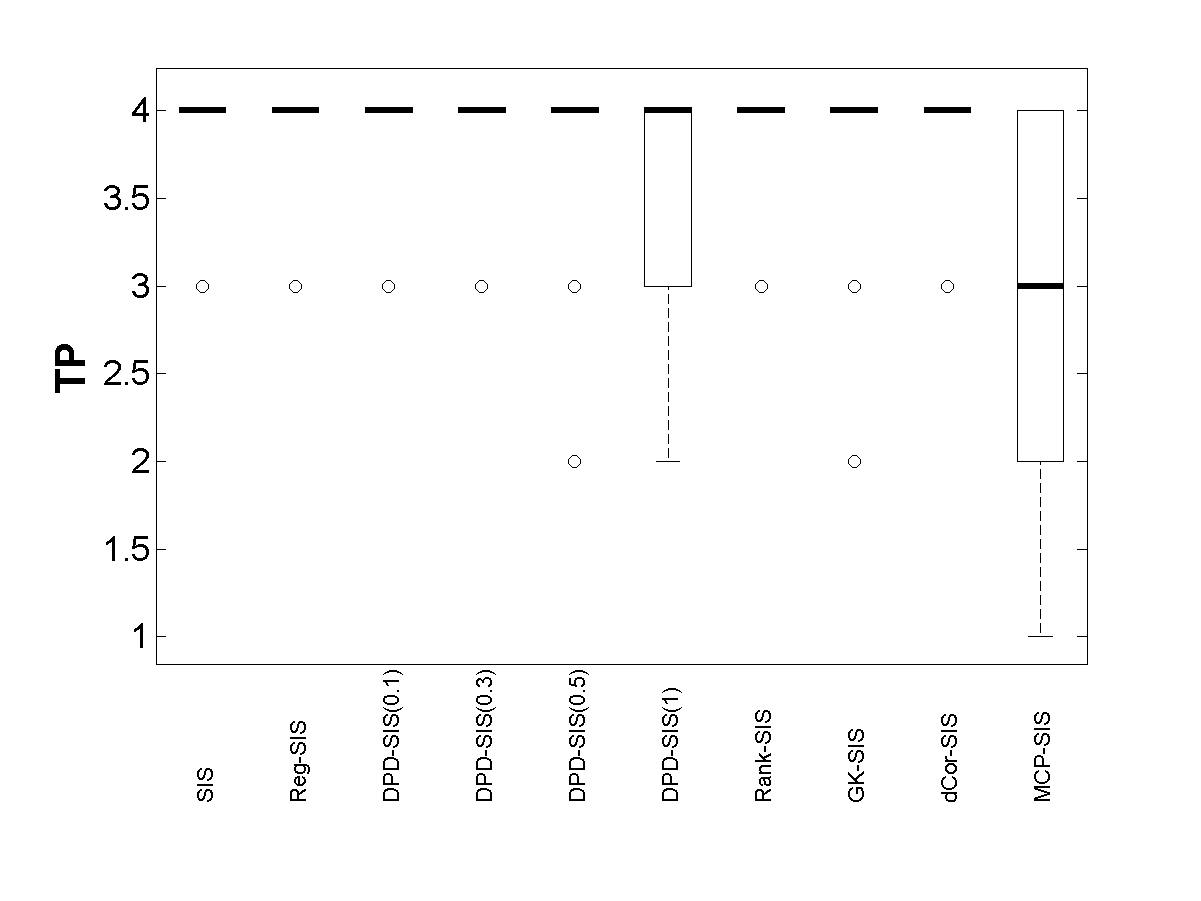

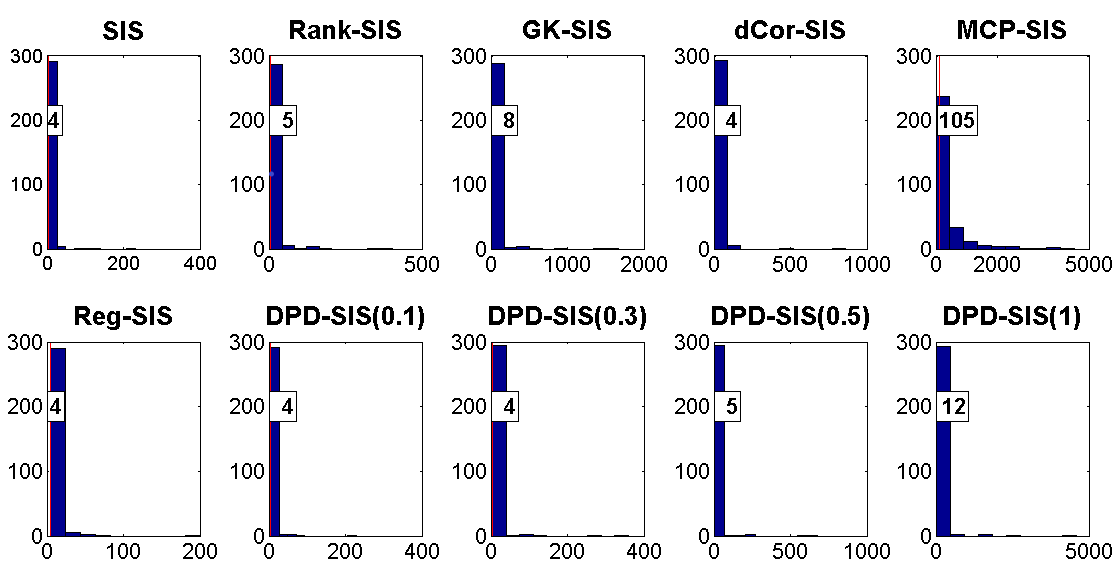

We have further investigated MMS, the minimum target model size required to select all the four true positives by different SIS approaches. Whenever SIS performs well, e.g., partially correlated covariates and/or strong signals, the MMS values are pretty low, often less than 10 with a median of about 4-6. For brevity, we only present the results (histogram) on MMS for two extreme cases with independent covariates in Figure 5, namely for strong signal with (one of the best performing cases) and weak signal with (one of the worst performing cases). The range (and median) of MMS differ widely in both cases but the general trend is the same (which is also the same in all other cases not reported here). The the median MMS for DPD-SIS increases with increasing values of and are generally higher than the usual SIS in pure data; but those obtained by DPD-SIS at are very close to the values obtained by the usual SIS and often significantly better than the other existing non-parametric SIS approaches.

In summary, under pure data, usual SIS performs the best as expected, but there is only a slight loss in performance by the proposed DPD-SIS with smaller values of . We will see next that, with this small price in case of pure data, we gain significant improvement over the usual SIS by using DPD-SIS under data contamination. Having a parametric nature, the proposed DPD-SIS naturally performs better than the existing non-parametric SIS approaches.

5.3 Performance of the DPD-SIS under data contamination

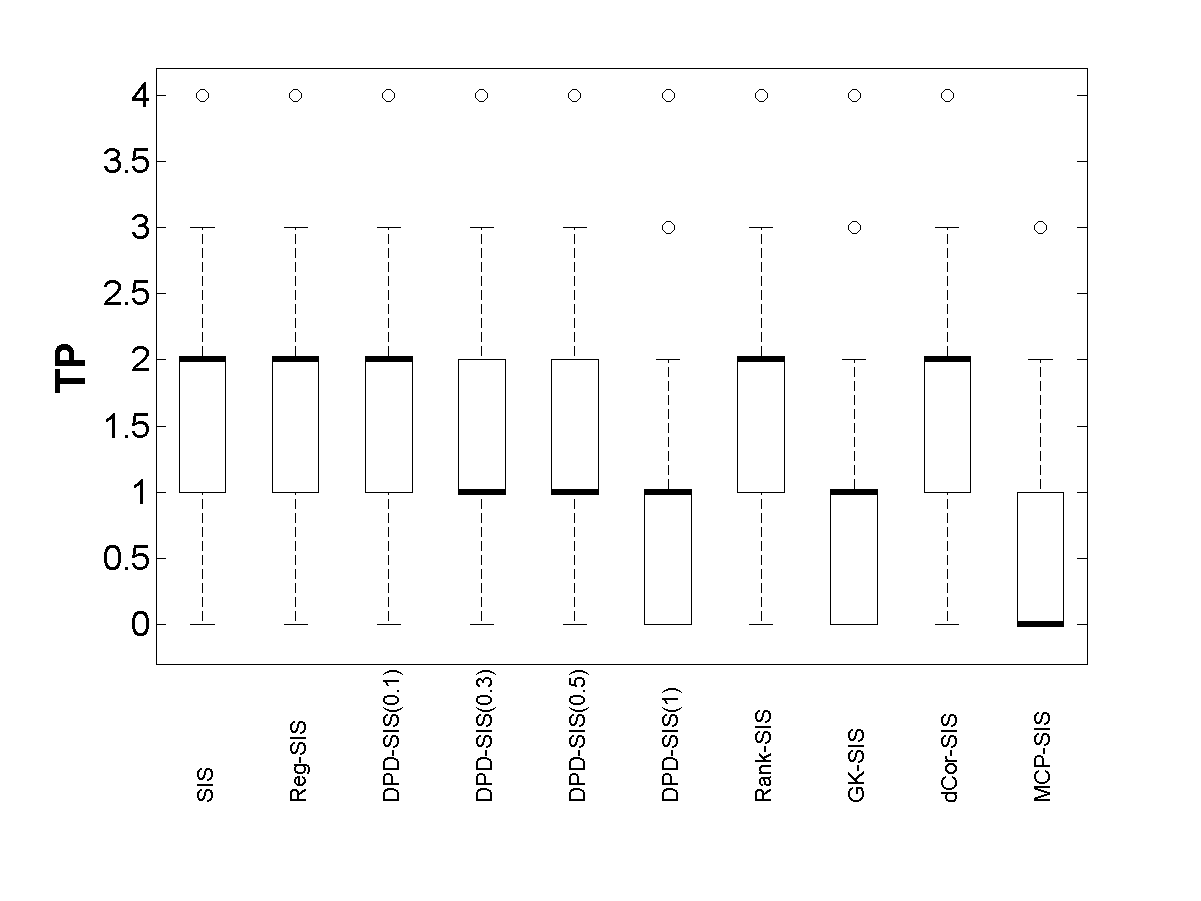

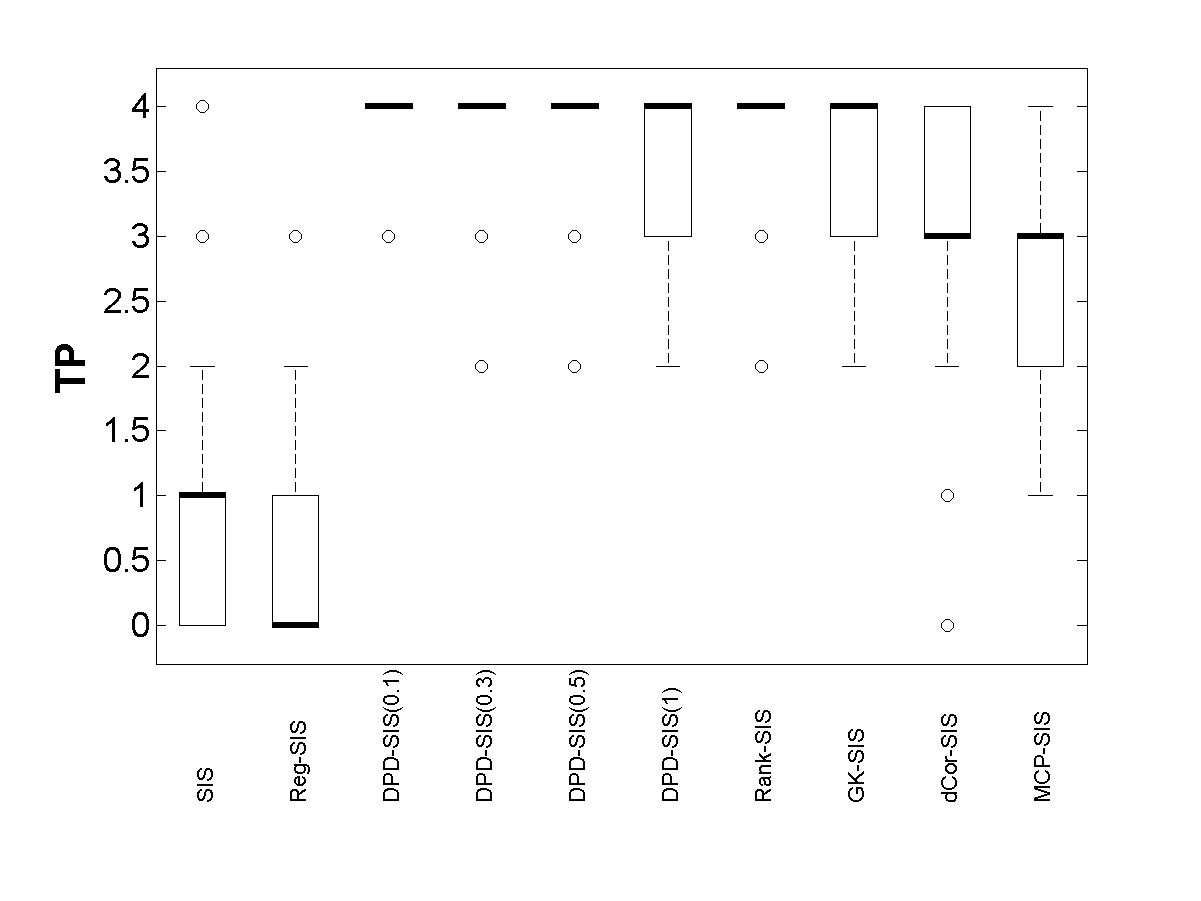

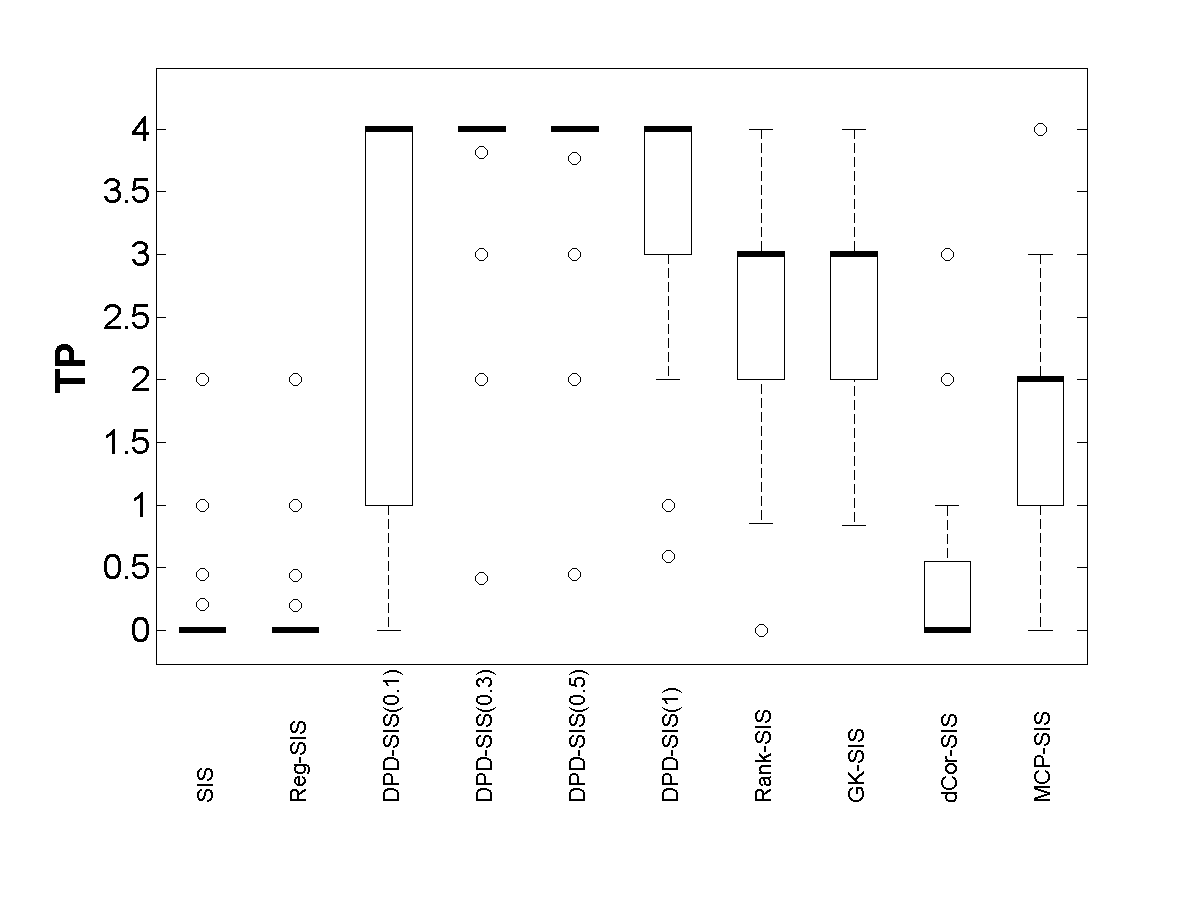

Let us now illustrate the performance of our DPD-SIS under data contamination and investigate the claimed improvements over the existing SIS and non-parametric robust SIS approaches. Due to the similarity in the patterns of results across all the cases considered (the only difference being in the magnitude of the performance measures, as in the pure data cases), we here only present the results for a representative case of and moderate signal strength for both the independent and partially correlated covariates. For these representative cases, the percentage of times the full model is selected and the box-plots of the actual numbers of true-positives selected by different SIS approaches with target model size are presented in Table 2 and Figure 6, respectively.

| Non-robust SIS | Proposed DPD-SIS() | Existing Robust (Non-parametric) SIS | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| SIS | Reg-SIS | Rank-SIS | GK-SIS | dCor-SIS | MCP-SIS | |||||

| Independent Covariates | ||||||||||

| 0% | 94.3 | 95.7 | 94.7 | 93.3 | 91.3 | 72.0 | 91.0 | 77.3 | 91.3 | 26.3 |

| 5% | 0.3 | 0.0 | 94.3 | 91.0 | 89.0 | 73.7 | 77.3 | 63.0 | 32.7 | 18.0 |

| 10% | 0.0 | 0.0 | 91.3 | 89.0 | 85.7 | 70.3 | 55.3 | 51.3 | 2.7 | 12.3 |

| 20% | 0.0 | 0.0 | 59.3 | 82.5 | 77.5 | 64.6 | 25.1 | 23.1 | 0.0 | 3.7 |

| Partially Correlated Covariates with | ||||||||||

| 0% | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 99.7 | 95.4 |

| 5% | 31.0 | 29.7 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 99.7 | 100.0 | 94.3 |

| 10% | 6.3 | 5.7 | 93.3 | 100.0 | 100.0 | 100.0 | 99.7 | 97.3 | 96.7 | 85.7 |

| 20% | 2.0 | 1.4 | 1.7 | 99.7 | 99.7 | 99.7 | 92.8 | 85.8 | 21.7 | 60.3 |

It can be noted that the usual SIS as well as its modification, the Reg-SIS, performs extremely poorly under any amount of contamination. Even at only 5% contamination, they select all the true positives in only about 30% of the cases with partially correlated data and almost never for the independent covariates, although these numbers were 99.7% and about 94-96%, respectively, under no contamination. As the contamination proportion increases, their performance becomes even worse and the same poor performance can also be seen in terms of the median number of true positives selected by these methods in Figure 6. Our proposed DPD-SIS with shows a much more stable performance under data contamination. In terms of percentages of full model selection, DPD-SIS with yields the best performance under heavy contamination (20%) and are quite competitive to the choice of also at milder contamination of 5%. A similar improved performance of our DPD-SIS is observed over the usual SIS or Reg-SIS in terms of selected true positives as well. More interestingly, our DPD-SIS with often outperforms the existing non-parametric robust SIS approaches and the improvement becomes more significant at higher contamination level and for the cases of independent samples (or weaker signals). For the partially correlated covariates, the non-parametric Rank-SIS and GK-SIS performs quite good with a median true positive equal to four (the actual active set size) but have an overall worse performance (more outlying cases with lower number of true-positives selected) compared to DPD-SIS with moderate values.

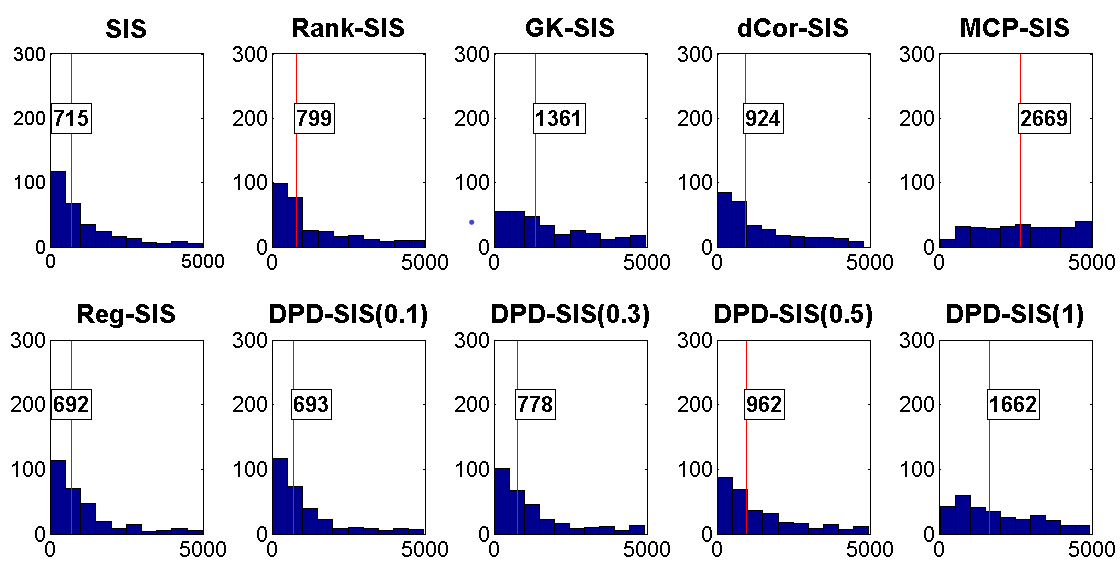

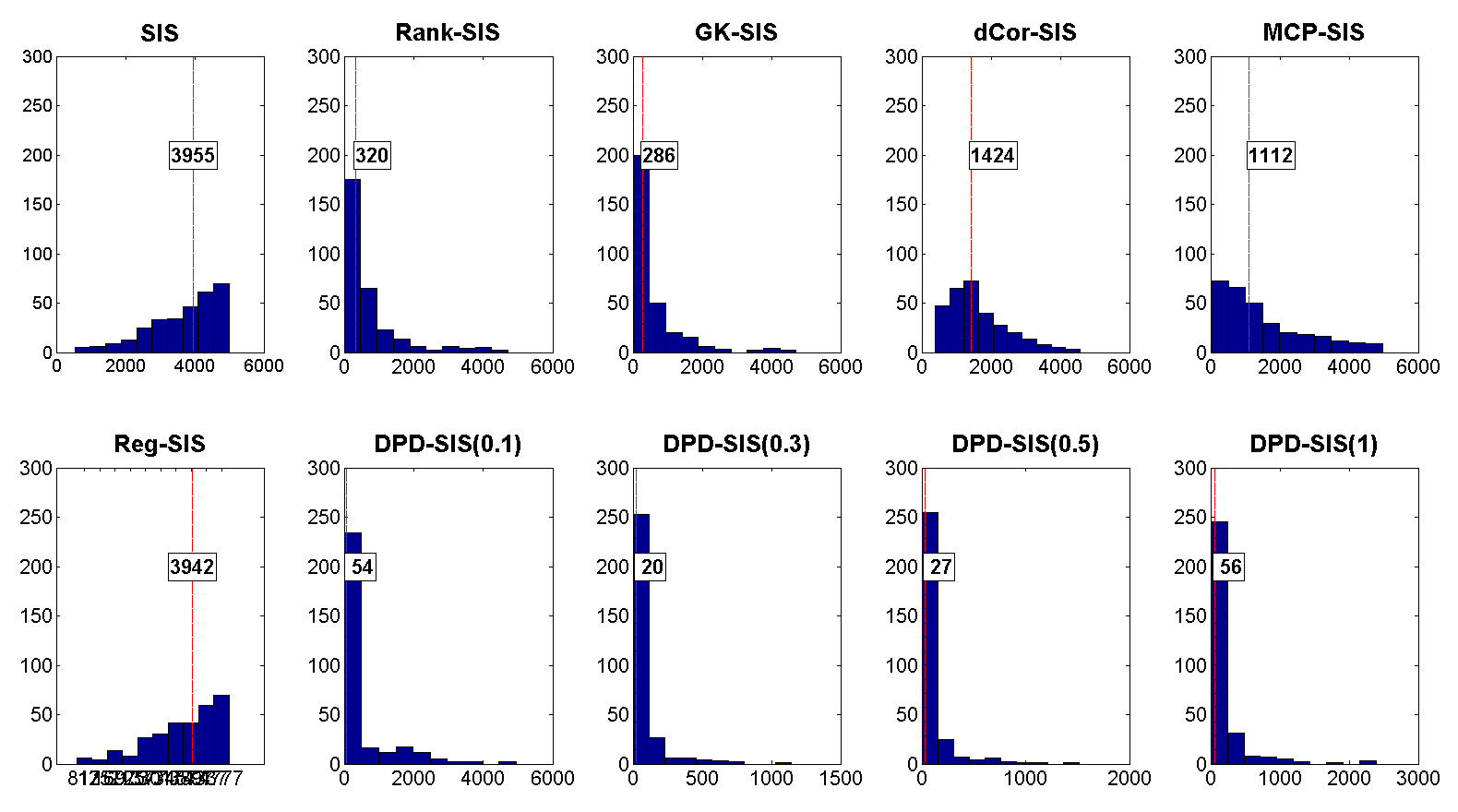

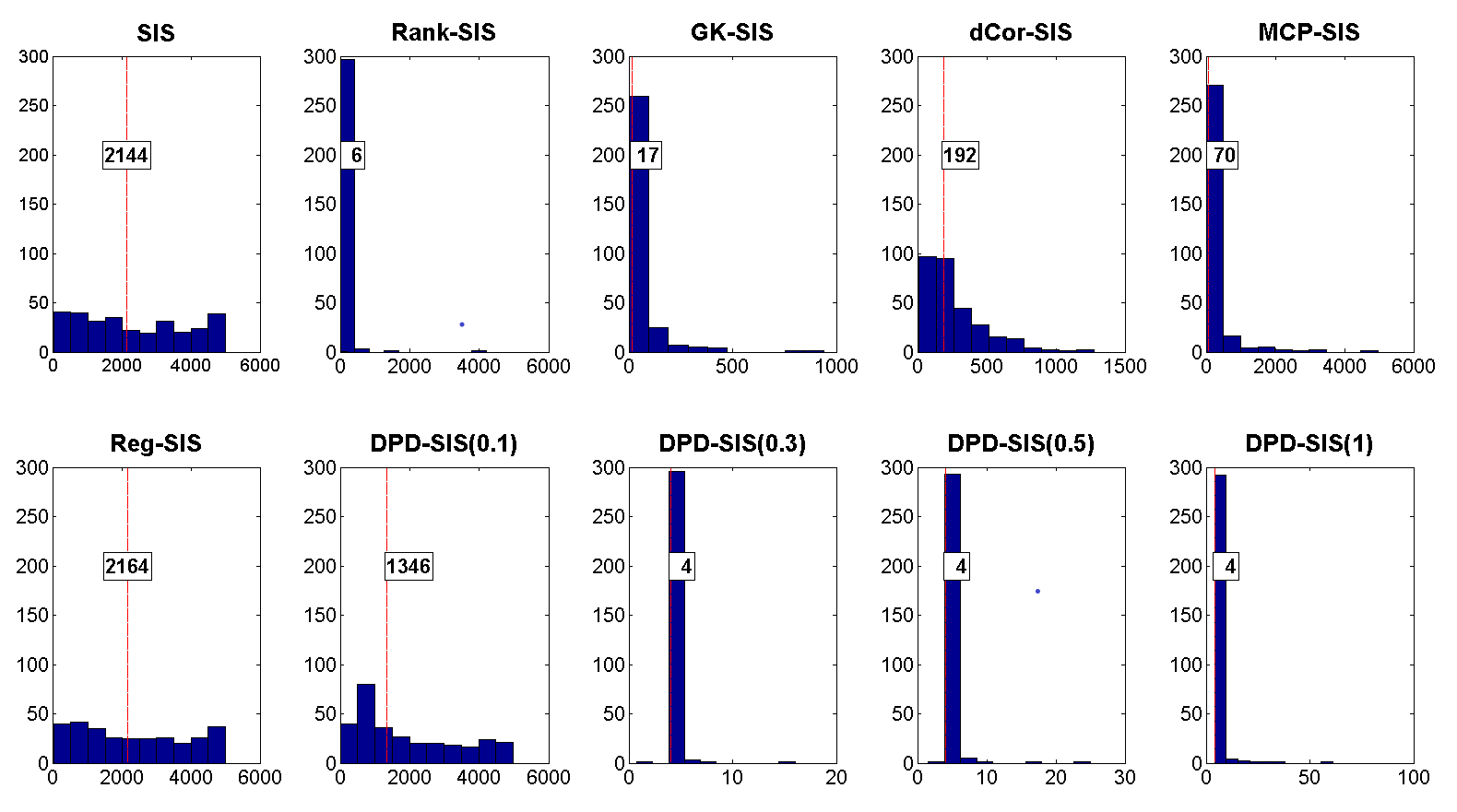

We have also studied the minimum target model size (MMS) required to select all four true positives under contamination which further illustrates the huge advantage of the proposed DPD-SIS over existing SIS approaches. For brevity, the results for 20% contamination under the representative cases are shown in Figure 7. Note that the median values of the MMS required by the usual SIS and Reg-SIS are of the order 3950 and 2150, respectively, for the independent and partially correlated covariates. These become heavily improved by the existing non-parametric robust SIS approaches with Rank-SIS and GK-SIS yielding better performance compared to the other two. But, still for these two cases of independent or partially correlated covariates, they reach the minimum median MMS of 286 (by GK-SIS) and six (by Rank-SIS), respectively. Our proposed DPD-SIS with clearly outperforms all these existing methods yielding even lower values of MMS with a median of four (the minimum possible value) for the partially correlated case. For the independent covariates the improvement is even more significant with the best performance of DPD-SIS at which provides a median MMS of 20 only (in comparison with the minimum value of 286 obtained by existing approaches). The results for all other simulation experiments, not presented here for brevity, have indicated the similar advantages of our proposed DPD-SIS under different types and amounts of data contamination with the improvements being larger for the more vulnerable cases of heavy contamination or weaker signal strength or smaller sample sizes.

Remark 5.1 (Runtime Comparison).

One important advantage of SIS in the context of ultra-high dimensional data is its high computational speed. Although MDPD is generally computationally intensive in large regression models, our DPD-SIS is pretty fast since it involves the computation of the MDPDE of three parameters only in each marginal regression model. Across our simulation studies, performed on a laptop having 32GB RAM and using parallel processing with 7 cores, the DPD-SIS for each sample with variables is seen to have a median runtime of 5-6 seconds, whereas the median runtime for the usual SIS (and Reg-SIS) for the same set-up is about 3 (and 5.5) seconds. The median runtime for the existing non-parametric SIS approaches are about 3-3.5 seconds for Rank-SIS, GK-SIS and MCP-SIS whereas for dCor-SIS it is approximately 5.2 seconds. So, we can clearly see that, on average, our DPD-SIS takes slightly more time than the other existing SIS approaches but it is still pretty fast, and fast enough to be useful for ultra-high dimensional set-ups considering its significantly improved robustness advantages as seen above.

5.4 Performances of the DPD-ISIS for strongly correlated covariates

Let us now study the performance of the DPD-ISIS for the case of strongly correlated covariates where the variance of each covariate is taken as 1 and the correlations between any pair of covariates are taken to be equal (). Since we have already seen significantly better performance of the DPD based (non-iterative) screening over the existing non-parametric screening approaches, the iterative approach is only examined for DPD-ISIS described in Section 3.2 along with the Van-ISIS [33] as the benchmark of comparison. As before, we take different sampel sizes , and the first non-zero coefficients to be and contaminate a certain percentage of the responses by replacing its value (say ) by . It is to be noted that, under such strongly correlated case, certain restrictions are required even for the usual ISIS to select all the important variables in terms of high signal-to-noise and ratios for given values of [6, 7]. So, we have investigated the performance of DPD-ISIS for different values of , and by fixing the error variance . Considering the similarity in the pattern of the simulation results, for brevity, we only present the results for the case , and (corresponding to SNR being 1 and 5, respectively).

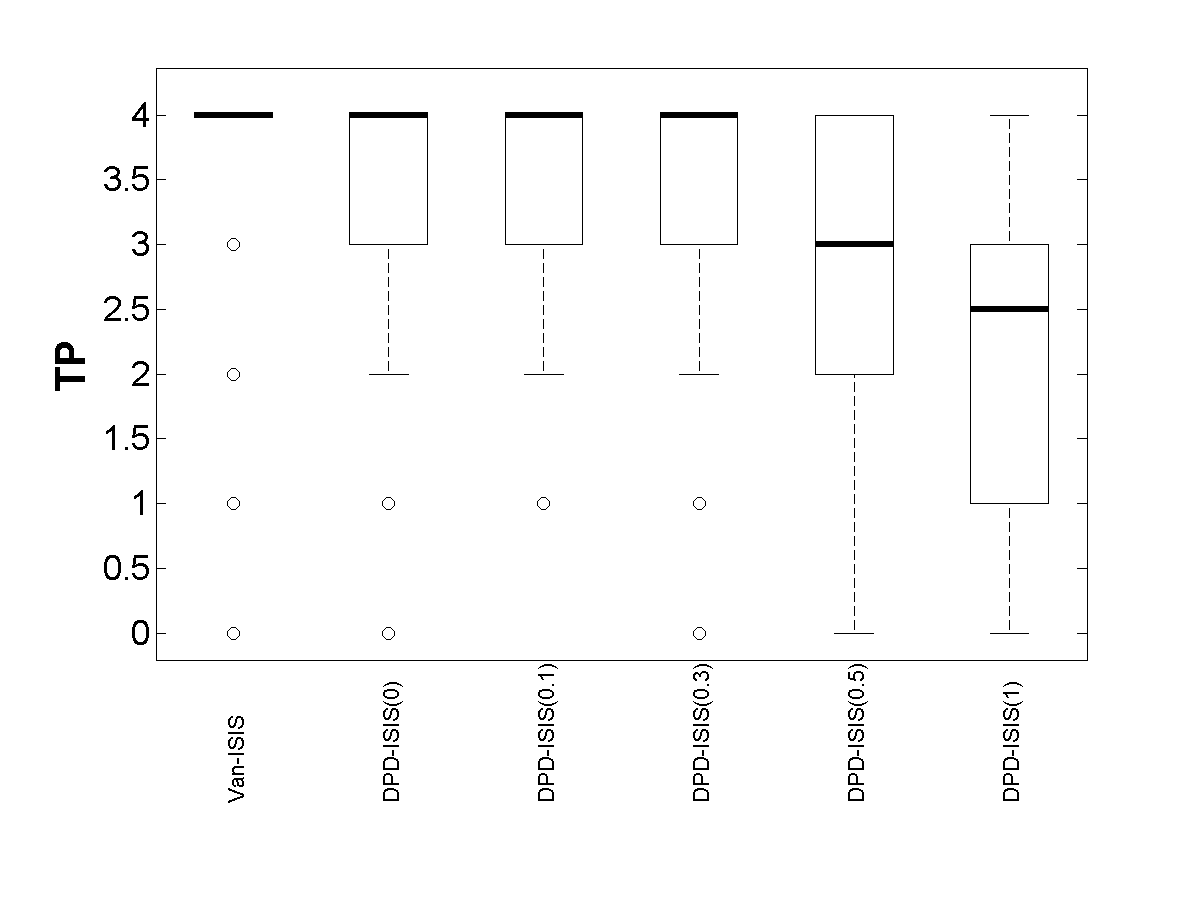

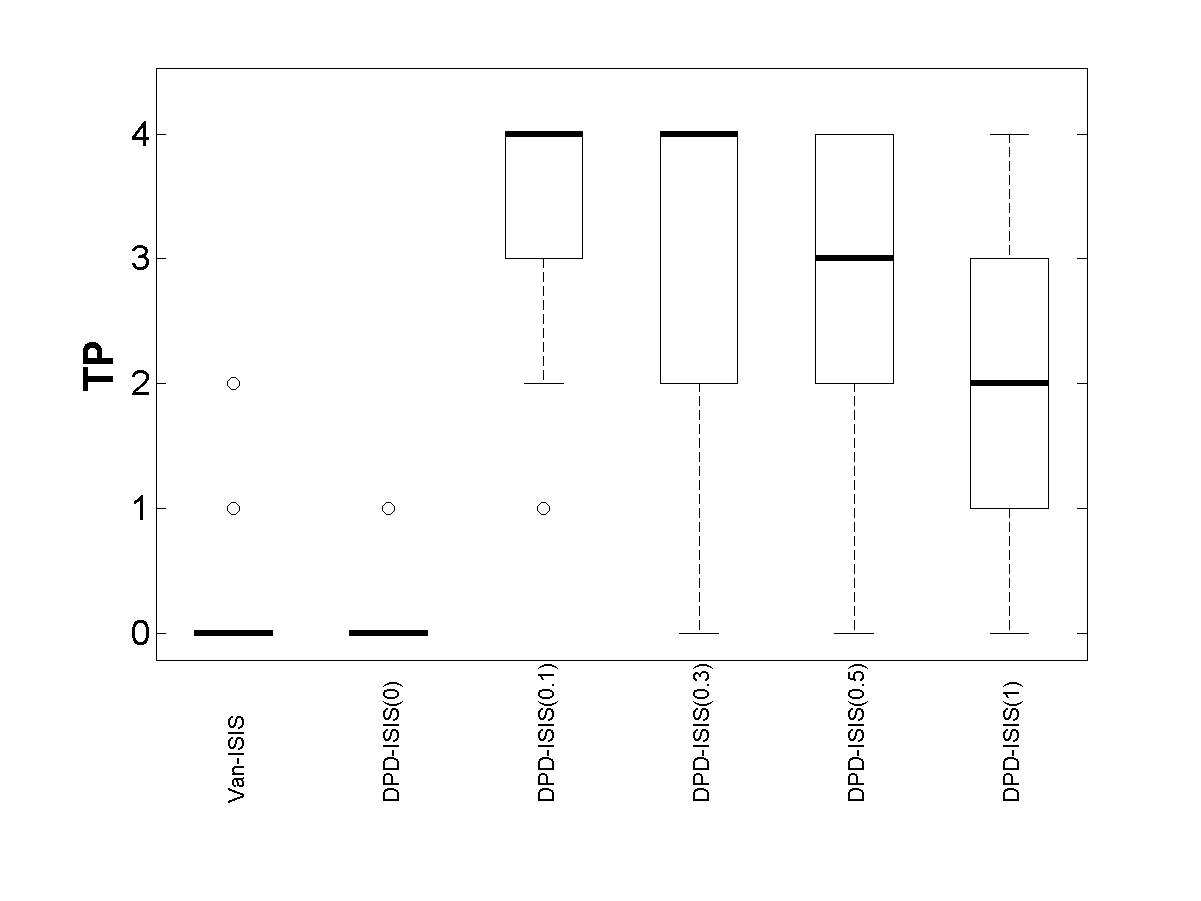

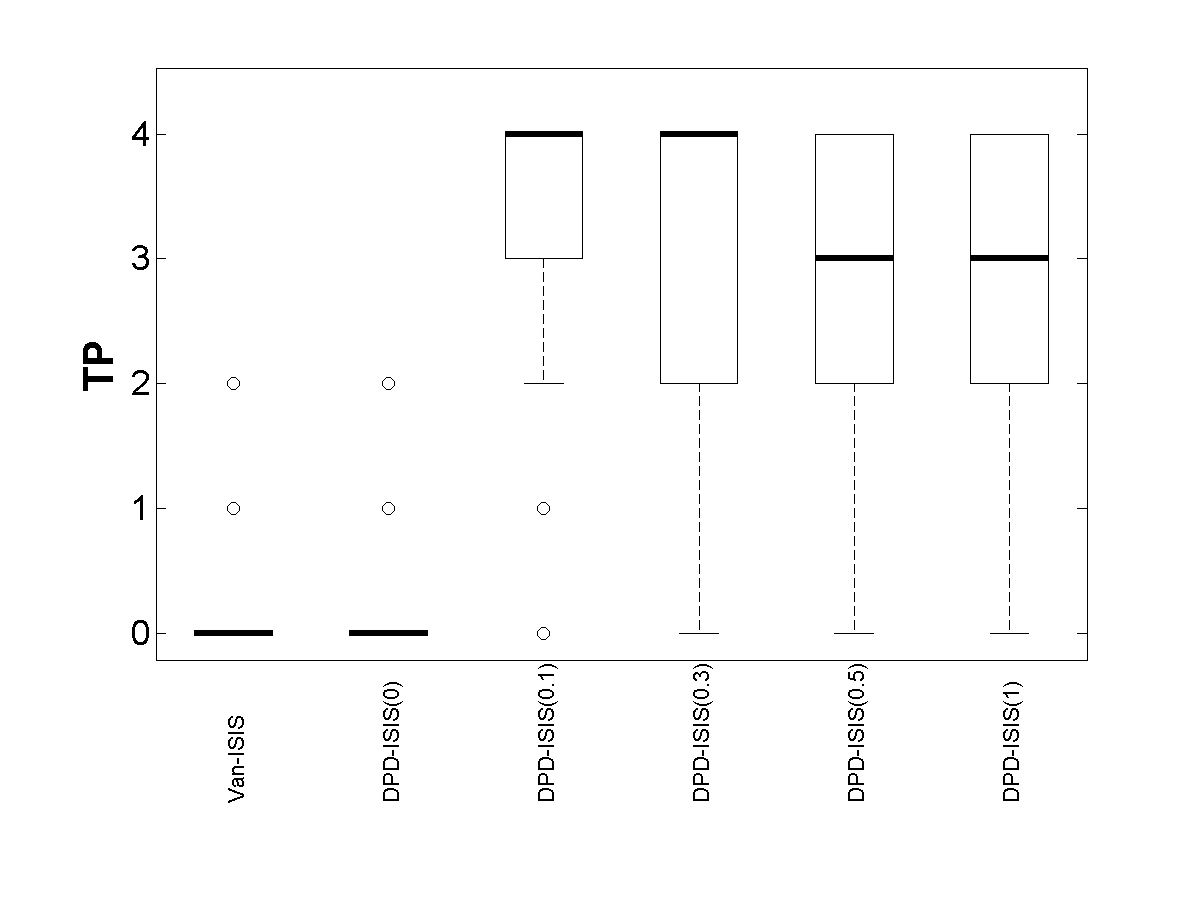

We present the average IC values obtained by different DPD-ISIS and Van-ISIS over 100 replications of the above-mentioned simulation under pure data as well as under contaminated data in Table 3; recall that it gives us the number of times the correct full model (all the 4 true positives) is selected by the DPD-ISIS approach. In each replication, as suggested in Section 3.2, we use the stopping criterion based on the selected active set-size and the screening is stopped when this active set in a given iteration does not change its size from the previous iteration. Since the full model is not always selected correctly, we also report the individual numbers of true positives selected (TP) via box-plots in Figure 8.

| Usual | Proposed DPD-ISIS() | |||||

|---|---|---|---|---|---|---|

| Van-ISIS | ||||||

| Moderate Signal (; SNR=1) | ||||||

| 0% | 79 | 68 | 65 | 58 | 48 | 22 |

| 5% | 0 | 0 | 63 | 55 | 45 | 20 |

| 10% | 0 | 0 | 51 | 55 | 48 | 31 |

| Moderate Signal (; SNR=5) | ||||||

| 0% | 100 | 100 | 100 | 100 | 99 | 93 |

| 5% | 61 | 63 | 93 | 98 | 99 | 89 |

| 10% | 28 | 25 | 68 | 92 | 94 | 92 |

From these results along with numerous other simulation studies not presented here, it is evident that for any fixed , the DPD-ISIS performs better in identifying more true positives as the SNR and ratio increase or the covariate correlation decreases; after some limiting values of SNR or , the DPD-ISIS always can correctly select all the true positives for any amount of correlation among covariates. This provides an indication that the DPD-ISIS also have similar sure screening property as the usual ISIS under suitably modified conditions. For any particular case with no contamination (pure data), in consistence with the DPD-SIS, the performance of DPD-ISIS also deteriorates with increasing values of but such a loss is not significant for smaller values of ; under appropriate set-up they all select the correct full model in all the replications yielding 100% correct results.

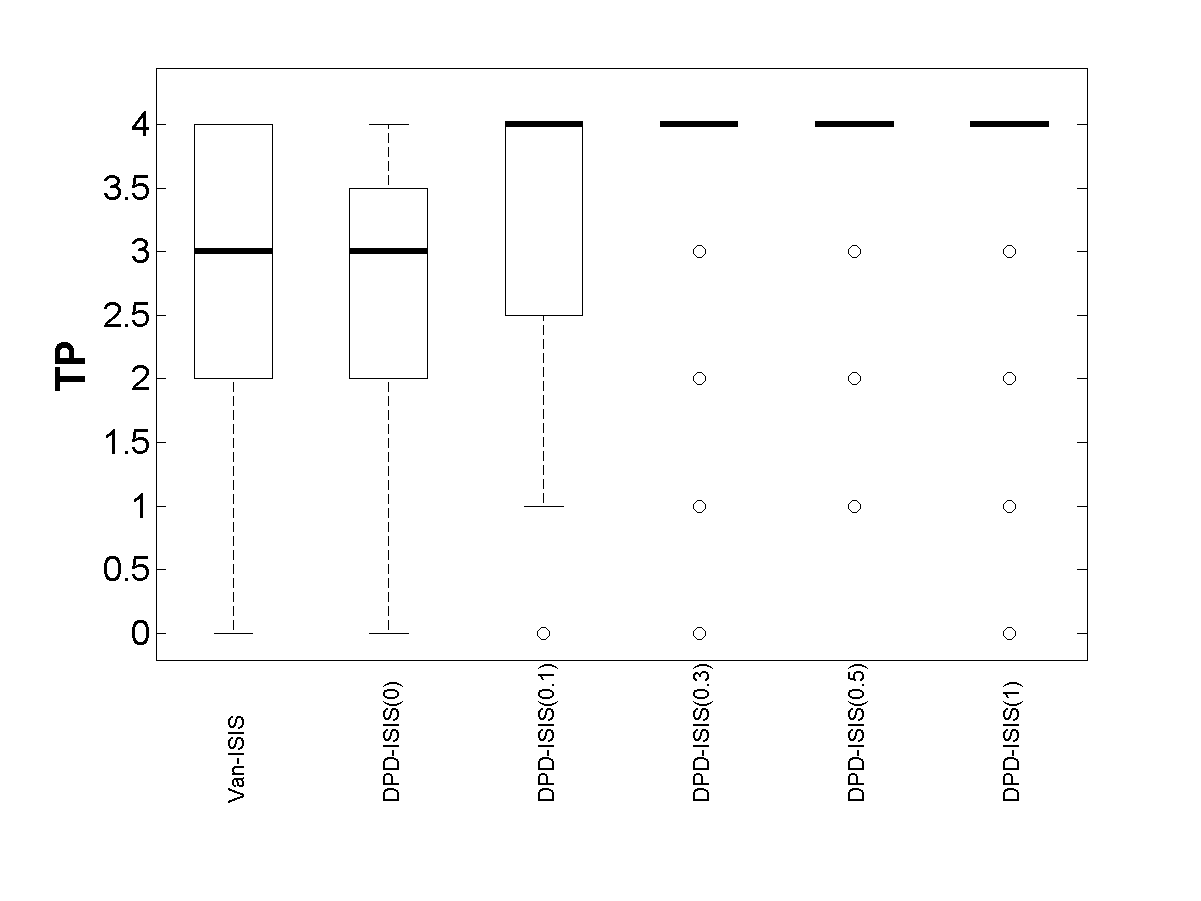

However, under contamination, the performance of the usual Van-ISIS (as well as DPD-ISIS at ) becomes significantly worse; under some weaker set-ups, they even fail to select the correct model at all in any replication! The proposed DPD-ISIS with larger values of yield extremely stable results with very little loss in their performance compared to the pure data case. It is also evident that provides the best trade-off in the cases considered here; it always yield the median TP values as the correct active set size (4) with some fluctuations depending on the signal strength or amount of contamination in the data.

5.5 On the Choice of robustness parameter in DPD-SIS or DPD-ISIS

Our proposed DPD-SIS (and also the DPD-ISIS) depends on a tuning parameter which is seen to control the trade-off between the asymptotic efficiency of the underlying MDPDE under pure data and its robustness under contamination. In terms of variable screening as well, similar trade-offs are observed through our extensive empirical experiments. When there is no contamination in the data, the usual SIS or Reg-SIS (which is DPD-SIS at ) has the best performance, which deteriorates for DPD-SIS() as increases although the loss is seen to be acceptable for smaller values of . On the other hand, under contamination, the performance of the DPD-SIS becomes more and more stable with increasing values of while the performance of the usual SIS or Reg-SIS breaks down completely even in presence of small amounts of contamination. Considering these trade-offs, it has been observed from our extensive simulation studies that DPD-SIS with performs the best under data contamination in all the scenarios considered and it also clearly outperforms all the existing non-parametric methods. Based on these experiments, we recommend to be a good empirical suggestion to use in most practical applications of DPD-SIS (or DPD-ISIS).

It is worthwhile to note that, in usual practice with statistical procedure depending on a tuning parameter, an adaptive data-driven choice of the underlying tuning parameter is expected and seems to provide the best results in each cases. For the underlying MDPDE used in our DPD-SIS, such data-driven selection procedures for the robustness tuning parameter are available. In the context of linear regression, one such algorithm for selecting the optimal is explored by Ghosh and Basu [13]. However, in the present case of DPD-SIS, we are using MDPDE for each marginal regression model and a data-based algorithm will often produce different values of for each such marginal model, since the amount of contamination is often different across covariates. Working with different values in one application of DPD-SIS is not useful and would break the coherence of the analysis – one should use the same across all the steps of DPD-SIS in one application to get consistent inference. Additionally, data-driven selection of would also increase the computation time, which is not an attractive feature in variable screening situations. We believe our empirical suggestion should work well in most applications.

6 Analysis of Triglyceride Data

In this section, we will apply our suggested variable screening method to our motivating example described in the Introduction, and show how this helps us in the variable selection process. As described in the Introduction, we have data from 54 individuals who underwent an intervention with intake of capsules of either fish oil, oxidized fish oil or sunflower oil for a period of seven weeks. The study is presented in Ottestad et al. [32]. Fasting triglyceride (TG) levels were measured at baseline and after seven weeks of intervention. In addition, we have gene expression measured in Peripheral blood mononuclear cells (PBMC). These are immune system cells and because they are circulating cells, they are exposed to nutrients, metabolites and peripheral tissues and may therefore reflect whole-body health. We are interested in relating TG change (seven weeks minus baseline) to gene expressions at baseline and our main goal is to identify genes that may be associated with TG response. Thus, we are primarily interested in variable selection.

As we have relatively few subjects, outliers might have a profound effect on the result, and hence, we are interested in performing a robust variable screening. Our analysis strategy is as follows: We will perform three iterations of the proposed robust DPD-ISIS (Algorithm 2) with RLARS in each iteration (Step 4), followed by a robust -penalized regression, the DPD-LASSO method of Ghosh and Majumdar [17] to be consistent (in Step 8), to produce our list of selected genes. In each iteration of DPD-ISIS we select the 13 top variables, while we use penalization parameter in the final DPD-LASSO. A penalization parameter of this order has been shown to have certain optimality properties, see e.g. page 296, Hastie et al. [21] We will do this for (which is not the usual ISIS as discussed in Section 3.2), 0.1, 0.3 and 0.5 and compare the lists of selected genes. We have also performed the usual correlation based Van-ISIS [33] described in Section 3.2 as our benchmark of comparison for the proposed procedures. When applying Van-ISIS, we observe that the estimated active set size (number of selected genes) does not change after three iterations, and we have used this as our stopping criterion. For the sake of comparison, we have also performed exactly three iterations of our proposed DPD-ISIS for each . In the final penalized regression model, we also include treatment group and body mass index. However, this does not change the results significantly for any of the procedures. We present the results on the number of genes selected in the final model obtained by each procedure in Table 4; the detailed gene list and estimated regression coefficients in the final model are only presented, for brevity, in case of the usual non-robust ISIS (benchmark) and our recommended choice in Table 5.

| Usual | DPD-ISIS with | ||||

|---|---|---|---|---|---|

| van-ISIS | 0 | 0.1 | 0.3 | 0.5 | |

| Genes selected by ISIS | 21 | 18 | 26 | 23 | 30 |

| Genes selected in the final joint model | 7 | 9 | 18 | 21 | 20 |

| Usual van-ISIS | Proposed DPD-SIS() | ||||

|---|---|---|---|---|---|

| Genes | Prob id | Genes | Prob id | ||

| HNRNPK | ILMN3260017 | 0.004 | FOXF2 | ILMN1674934 | 0.081 |

| NA | ILMN1896699 | 0 | HNRNPK | ILMN3260017 | 0.051 |

| NA | ILMN1910805 | 0.042 | HYAL1 | ILMN1739813 | 0.399 |

| NA | ILMN1712784 | 0.063 | UTY | ILMN3233091 | 0.309 |

| NA | ILMN1679106 | 0 | NA | ILMN1772136 | 0.227 |

| NA | ILMN1687707 | 0.025 | RPS27 | ILMN1660498 | 0.088 |

| MORC4 | ILMN1795463 | 0 | SCARA3 | ILMN1723358 | 0.058 |

| RPS16 | ILMN1651850 | 0 | SLITRK5 | ILMN1789040 | 0.060 |

| ZP3 | ILMN1672378 | 0.006 | ZP3 | ILMN1672378 | 0.427 |

| FOXF2 | ILMN1674934 | 0.006 | ZSCAN12 | ILMN1786281 | 0.738 |

| PKLR | ILMN1725172 | 0 | SEZ6L2 | ILMN2413780 | 0.224 |

| NA | ILMN1881212 | 0 | FAM161A | ILMN3238106 | 0.332 |

| NA | ILMN3242572 | 0 | EEF1A1 | ILMN3201843 | 0.091 |

| TTC8 | ILMN2401927 | 0 | ABCD1 | ILMN3237161 | 0.264 |

| XCR1 | ILMN1764034 | 0 | ALG1 | ILMN1787954 | 0.197 |

| TBX1 | ILMN2248112 | 0 | AASS | ILMN1678323 | 0.248 |

| PPT2 | ILMN1750664 | 0 | EML1 | ILMN1729455 | 0.152 |

| KLHL26 | ILMN1805330 | 0 | NA | ILMN1839740 | 0.313 |

| SCARA3 | ILMN1723358 | 0 | CDCA2 | ILMN1660654 | 0.163 |

| NA | ILMN1880704 | 0.037 | NA | ILMN1698246 | 0.459 |

| FGB | ILMN2114972 | 0 | EPB41L4A | ILMN1791867 | 0.096 |

| SLC7A11 | ILMN1655229 | 0 | |||

| TMEM47 | ILMN2129234 | 0 | |||

Two observations are worth discussing. First, three times as many genes are selected with the robust procedure (21 vs. 7) as with the non-robust ISIS. Second, there is very little overlap between the two gene sets (only three of the genes selected with are selected by van-ISIS). If we have a look at the number of genes selected as a function of (not shown), we observe that the numbers are increasing with increasing , more or less. This is somewhat counterintuitive, as the efficiency of the procedure is reduced with increasing . However, as pointed out earlier, the stability (in terms of robustness) is increasing. We see this as a strong indication of problems with outliers in this rather small dataset, as illustrated in the Introduction. The fact that there is very little overlap between the two gene sets in Table 5 can also be seen as an illustration of this problem; with small sample size, outliers are dominating the analysis to a rather large extent. It is worth pointing out that the single gene with the strongest effect by DPD-ISIS (ZSCAN12, illustrated in Fig. 1e) is not even on the list of selected genes for van-ISIS.

If we think in direction of biological interpretation of the findings, we observe that a clear majority of the genes have an estimated coefficient with a negative sign, indicating a down-regulation of TG. It should also be commented that three of the identified probes do not map to a known gene, and hence, their function is unclear.

7 Conclusions

In this paper, we have proposed a new robust variable screening procedure for ultra-high dimensional data using the marginal linear regression approach and the minimum density power divergence estimator for the regression parameter. This is extremely important in modern statistical analyses of large scale data from medical, biological and other applied sciences. We have also proposed an iterative version of our DPD based sure independence screening procedure in line with ISIS that is helpful for robust variable screening in the presence of correlated covariates. In this paper we have concentrated on linear relationships between the response and all the available covariates and hence, our proposed procedure is robust against data contamination (e.g., outliers, or leverage points) whenever the assumed linear regression model is approximately correct. The robustness of the proposed DPD-SIS is justified theoretically through use of influence functions and sensitivity analyses and also empirically through an extensive simulation study. It has been empirically shown that the proposed DPD-SIS at suitably chosen robustness tuning parameter provides the best performance under data contamination and is superior compared to the usual SIS as well as several existing robust non-parametric screening procedures under most critical scenarios. We have applied our proposal for the robust analyses of data on triglyceride response to identify the important genes that may cause the variation in triglyceride response between different subjects.

We have implemented the proposed DPD-based procedure in R for all the simulations and real data analyses. The relevant codes are available from the authors upon request, and can be used by any practitioner for robust analyses of their experimental datasets from real-life studies.

For the practical example it is worth noting that, in order to ensure stability of the final solution, it would make sense to apply some relevant additional procedure, e.g. stability selection [30, 35] on top of the final penalized regression. With the promising and encouraging performance of the proposed DPD based robust variable screening procedure, this paper opens up several important directions of future research. The first and foremost work would be to prove the theoretical properties of our proposed methodologies, including its claimed sure screening properties. Also, we have restricted ourselves to linear regression only in this work and hence, it would be practically important to extend this robust variable screening procedure to more general parametric regression settings, like generalized linear models. We hope to pursue these important research extensions in our future works.

Acknowledgment

The authors wish to thank Prof. Stine Ulven, Department of Nutrition, University of Oslo, for providing the Triglyceride dataset and guiding us in biological interpretation of the results. A major part of this research work has been done while the first author (AG) was visiting University of Oslo, Norway The research of AG is also partially supported by the INSPIRE Faculty Research Grant from Department of Science and Technology, Govt. of India.

References

- Barut et al. [2016] Barut, E., Fan, J., and Verhasselt, A. (2016). Conditional sure independence screening. J Amer Stat Assoc, 111(515), 1266-1277.

- Basu et al. [1998] Basu, A., Harris, I. R., Hjort, N. L., and Jones, M. C. (1998). Robust and efficient estimation by minimising a density power divergence. Biometrika, 85, 549–559.

- Basu et al. [2011] Basu, A., Shioya, H. and Park, C. (2011). Statistical Inference: The Minimum Distance Approach. Chapman Hall/CRC, Boca de Raton.

- Basu et al. [2019] Basu, A., Ghosh, A., Mandal, A., Martin, N. and Pardo, L. (2019) Robust Wald-type tests in GLM with random design based on minimum density power divergence estimators. ArXiv Pre-print, arXiv:1804.00160 [stat.ME].

- Durio and Isaia [2011] Durio, A., and Isaia, E. D. (2011). The minimum density power divergence approach in building robust regression models. Informatica, 22(1), 43-56.

- Fan and Li [2001] Fan, J. and Li, R. (2001). Variable Selection via Nonconcave Penalized Likelihood and its Oracle Properties. J Amer Statist Assoc, 96:1348–1360.

- Fan and Lv [2008] Fan, J., and Lv, J. (2008). Sure independence screening for ultrahigh dimensional feature space. J Royal Stat Soc B , 70(5), 849–911.

- Fan and Song [2010] Fan, J., and Song, R. (2010). Sure independence screening in generalized linear models with NP-dimensionality. Ann Stat, 38(6), 3567-3604.

- Fu and Wang [2018] Fu, L., and Wang, Y. G. (2018). Variable selection in rank regression for analyzing longitudinal data. Stat Methods Med Res, 27(8), 2447-2458.

- Gather and Guddat [2008] Gather, U., and Guddat, C. (2008). Comment on “Sure Independence Screening for Ultrahigh Dimensional Feature Space” by Fan, JQ and Lv, J. J Royal Stat Soc B, 70, 893-895.

- Ghosh [2019] Ghosh, A. (2019). Robust inference under the beta regression model with application to health care studies. Stat Methods Med Res, 28(3), 871–888.

- Ghosh and Basu [2013] Ghosh, A., and Basu, A. (2013). Robust estimation for independent non-homogeneous observations using density power divergence with applications to linear regression. Electron J Stat, 7, 2420–2456.

- Ghosh and Basu [2015] Ghosh, A., and Basu, A. (2015). Robust Estimation for Non-Homogeneous Data and the Selection of the Optimal Tuning Parameter: The DPD Approach J Appl Stat, 42(9), 2056–2072.

- Ghosh and Basu [2016] Ghosh, A., and Basu, A. (2016). Robust Estimation in Generalized Linear Models : The Density Power Divergence Approach. Test, 25(2), 269–290.

- Ghosh and Basu [2019] Ghosh, A., and Basu, A. (2019). Robust and efficient estimation in the parametric proportional hazards model under random censoring. Stat Med, 38(27), 5283–5299.

- Ghosh et al. [2018] Ghosh, A., Martin, N., Basu, A., and Pardo, L. (2018). A new class of robust two-sample Wald-type tests. Int J Biostat, 14(2).

- Ghosh and Majumdar [2019] Ghosh, A. and Majumdar, S. (2019). Ultrahigh-dimensional Robust and Efficient Sparse Regression using Non-Concave Penalized Density Power Divergence. ArXiv pre-print, arXiv:1802.04906v3.

- Gnanadesikan and Kettenring [1972] Gnanadesikan, R., and Kettenring, J. R. (1972). Robust estimates, residuals, and outlier detection with multiresponse data. Biometrics, 81-124.

- Hall and Miller [2009] Hall, P., and Miller, H. (2009). Using generalized correlation to effect variable selection in very high dimensional problems. J Comput Graphical Stat, 18(3), 533-550.

- Hampel et al. [1986] Hampel, F. R., Ronchetti, E., Rousseeuw, P. J., and Stahel W.(1986). Robust Statistics: The Approach Based on Influence Functions. New York, USA: John Wiley & Sons.

- Hastie et al. [2015] Hastie, T., Tibshirani, R., and Wainwright, M. (2015). Statistical learning with sparsity: the lasso and generalizations. CRC press.

- Jacobs et al. [2019] Jacobs, R., Lesaffre, E., Teunis, P. F., Hohle, M., and van de Kassteele, J. (2019). Identifying the source of food-borne disease outbreaks: An application of Bayesian variable selection. Stat Methods Med Res, 28(4), 1126–1140.

- Jung et al. [2019] Jung, Y., Zhang, H., and Hu, J. (2019). Transformed low-rank ANOVA models for high-dimensional variable selection. Stat Methods Med Res, 28(4), 1230-1246.

- Khan et al. [2007] Khan, J. A., Van Aelst, S., and Zamar, R. H. (2007). Robust linear model selection based on least angle regression. J Amer Statist Assoc, 102, 1289–1299.

- Krzykalla et al. [2020] Krzykalla, J., Benner, A., and Kopp‐Schneider, A. (2020). Exploratory identification of predictive biomarkers in randomized trials with normal endpoints. Stat Med, 39, 923–939.

- Li et al. [2012a] Li, G., Peng, H., Zhang, J., and Zhu, L. (2012a). Robust rank correlation based screening. Ann Stat, 40(3), 1846-1877.

- Li et al. [2012b] Li, R., Zhong, W., and Zhu, L. (2012b). Feature screening via distance correlation learning. J Amer Statist Assoc, 107(499), 1129-1139.

- Luo et al. [2014] Luo, S., Song, R., and Witten, D. (2014). Sure Screening for Gaussian Graphical Models. Stat, 1050, 29.4

- Lusa et al. [2008] Lusa, L., Korn, E. L., and McShane, L. M. (2008). A class comparison method with filtering‐enhanced variable selection for high‐dimensional data sets. Stat Med, 27(28), 5834–5849.

- Meinshausen and Buhlmann [2010] Meinshausen, N., and Buhlmann, P. (2010). Stability selection. J Royal Stat Soc B, 72(4), 417–473.

- Mu and Xiong [2014] Mu, W., and Xiong, S. (2014). Some notes on robust sure independence screening. J App Stat, 41(10), 2092–2102.

- Ottestad et al. [2012] Ottestad I, Vogt G, Retterstøl K, Myhrstad MC, Haugen JE, Nilsson A, Ravn-Haren G, Nordvi B, Brønner KW, Andersen LF, Holven KB. (2012). Oxidised fish oil does not influence established markers of oxidative stress in healthy human subjects: a randomised controlled trial. British Journal of Nutrition, 108(2), 315–26.

- Saldana and Feng [2018] Saldana, D. F., and Feng, Y. (2018). SIS: An R package for sure independence screening in ultrahigh-dimensional statistical models. J Stat Software, 83(2), 1–25.

- Segal et al. [2003] Segal, M. R., Dahlquist, K. D., and Conklin, B. R. (2003). Regression approaches for microarray data analysis. J Comput Bio, 10(6), 961-980.

- Shah and Samworth [2013] Shah, R. D., and Samworth, R. J. (2013). Variable selection with error control: another look at stability selection. J Royal Stat Soc B, 75(1), 55–80.

- Szekely et al. [2007] Székely, G. J., Rizzo, M. L., and Bakirov, N. K. (2007). Measuring and testing dependence by correlation of distances. Ann Stat, 35, 2769–2794.

- Tibshirani [1996] Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. J Royal Statist Soc B, 58, 267–288.

- Xue et al. [2018] Xue, H., Wu, S., Wu, Y., Ramirez Idarraga, J. C., and Wu, H. (2018). Independence screening for high dimensional nonlinear additive ODE models with applications to dynamic gene regulatory networks. Stat Med, 37(17), 2630-2644.

- Wang et al. [2017] Wang, T., Zheng, L., Li, Z., and Liu, H. (2017). A robust variable screening method for high-dimensional data. J App Stat, 44(10), 1839-1855.

- Zang et al. [2017] Zang, Y., Zhao, Q., Zhang, Q., et al. (2017). Inferring gene regulatory relationships with a high-dimensional robust approach. Genet Epidemiol, 41(5), 437–454.

- Zhang [2010] Zhang, C. H. (2010). Nearly Unbiased Variable Selection under Minimax Concave Penalty. Ann Statist, 38, 894–942.

- Zhang and Huang [2008] Zhang, C. H. and Huang, J. (2008). The sparsity and bias of the Lasso selection in high-dimensional linear regression. Ann Statist, 36(4), 1567–1594.

- Zhao and Li [2012] Zhao, S. D., and Li, Y. (2012). Principled sure independence screening for Cox models with ultra-high-dimensional covariates. J Mult Anal, 105(1), 397-411.

- Zhong [2014] Zhong, W. (2014). Robust sure independence screening for ultrahigh dimensional non-normal data. Acta Mathematica Sinica, English Series, 30(11), 1885–1896.

- Zou [2006] Zou, H. (2006). The Adaptive Lasso and Its Oracle Properties. J Amer Statist Assoc, 101, 1418–1429.