Ruin probability in a two-dimensional model with correlated Brownian motions

Abstract

We consider two insurance companies with endowment processes given by Brownian motions with drift. The firms can collaborate by transfer payments in order to maximize the probability that none of them goes bankrupt. We show that pushing maximally the company with less endowment is the optimal strategy for the collaboration if the Brownian motions are correlated and the transfer rate can exceed the drift rates. Moreover, we obtain an explicit formula for the minimal ruin probability in case of perfectly positively correlated Brownian motions where we also allow for different diffusion coefficients.

| 2020 MSC : | Primary 49J20, 35R35, Secondary 91B70. |

|---|---|

| Keywords : | Ruin probabilities, Optimal control problem, Collaboration, Two-dimensional Brownian motion, Correlated Brownian motions. |

Introduction

We focus on two insurance companies whose endowment processes are given by correlated Brownian motions with drift. The common aim of the firms is to minimize the probability that at least one of the endowment processes falls below zero and, thus, they collaborate by transfer payments. These payments are assumed to be absolutely continuous with respect to the Lebesgue measure and to be bounded, but they can exceed the drift rates so that a company can be faced with a negative drift rate. The problem can be interpreted as an optimal control problem which consists in minimizing the probability that the two-dimensional endowment process leaves the positive quadrant and in identifying the optimal transfer payments.

If at some point in time one firm has high endowment and the endowment of the other firm is close to zero then it seems reasonable that the latter is maximally supported and obtains the whole available drift rate. Using this so-called push-bottom strategy turns out to be optimal no matter how big the difference between the endowment processes is: The firm with less endowment receives the maximal drift. To show this result we use a comparison principle for stochastic differential equations (SDEs) from [16].

If the Brownian motions are perfectly positively correlated we derive a closed formula for the value function, because only one Brownian motion is involved and we can rewrite the ruin probability in terms for which explicit formulas are available. The arguments also apply to the case where the endowment processes have different diffusion coefficients and the Brownian motions are perfectly positively correlated. The value function turns out to be a classical solution of the corresponding Hamilton-Jacobi-Bellman equation.

This control problem was first studied by McKean and Shepp in [17] for independent Brownian motions and the value function was derived in the case that the transfer payments are at most as high as the drift rates.

In case that each company keeps a given minimal positive drift rate, the value function and the gain of collaboration for independent Brownian motions are obtained in [12] by constructing a classical solution of the associated Hamilton-Jacobi-Bellman equation.

Although the ruin probability is one of the most important evaluation criteria for insurance companies, there are only few articles dealing with two or more companies. For an overview of the one-dimensional case consult [2]. In [7] a two-dimensional model is analyzed and simple bounds for the ruin probability are obtained by using results from the one-dimensional case. The Laplace transform in the initial endowments of the probability that at least one of the two companies is ruined in finite time is derived in [3]. Collamore [8] investigates the probability that a -dimensional discrete process hits a -dimensional set and obtains some large deviation results. For specific choices of the set the hitting probability can be seen as a ruin probability. The asymptotic behavior of the ruin probability if the initial endowments both tend to infinity under a light-tails assumption on the claim size distribution is analyzed in [4].

Let us emphasize that also for the maximal expected aggregated dividend payments, which is another main evaluation criteria for insurance companies, the literature in the multidimensional setting is scarce. The optimal collaboration for maximizing the total dividend payments of two companies in different models is analyzed for example in [1, 11, 13, 15].

The paper is organized as follows. In Section 1 we introduce our model. We derive the optimal strategy for the transfer payments in order to minimize the ruin probability in Section 2. In Section 3.1 we focus on perfectly positively correlated Brownian motions and compute the value function explicitly. The same arguments are extended to a model with different diffusion coefficients in Section 3.2. Finally, we rewrite the minimal ruin probability for perfectly negatively correlated Brownian motions in terms of the hitting probability of a reflected Brownian motion with drift in Section 4.

1 Model

The endowment processes of the two companies are described by the stochastic processes

where denote the initial endowments, are constant cash rates, e.g. premium rates, , , with a two-dimensional Brownian motion. Here is the correlation coefficient of and . The drift rates can be interpreted as transfer payments from one company to the other one. More precisely, if , then the first company obtains payments from the second company at time and if it is vice versa. We say that the companies do not collaborate if for all . We assume that the transfer payments are bounded in such a way that the total drift rate of each company is bounded below by , thus,

for some .

Introducing the control process the endowment processes are given by

| (1.1) | ||||

where and .

We aim at maximizing the probability that both firms survive forever. For this purpose denote by

the ruin times of the first and second company, respectively, when the control is used. Let

Our target functional is then given by

and the value function is

| (1.2) |

where denotes the set of all admissible controls. More precisely, is the set of all progressively measurable processes with respect to the filtration generated by satisfying , .

For and we obtain the same model as in the paper by McKean and Shepp [17]; for and we are in the setting of [12].

The Hamilton-Jacobi-Bellman equation and the boundary conditions for the optimal control problem (1.2) are given by

2 The Optimal Strategy for the Transfer Payments

For deriving the optimal strategy in the control problem (1.2) we use a comparison theorem for solutions of stochastic differential equations. We focus on the case because it is more involved and the arguments simplify for and, thus, are omitted.

First, consider the transformation

where and , . Observe that does not depend on the control . Furthermore, it holds that

and

We rescale the diffusion parts of the processes and and define

Hence, we conclude that , are independent Brownian motions and that

where . Here denotes the set of all progressively measurable processes with respect to the filtration , which is generated by and , and satisfies , . Note that and the filtration generated by coincide.

So far all arguments hold for . Now let . Then also coincides with the filtration generated by the Brownian motion . In particular, there exists a measurable function

such that for every

We rewrite in terms of and . More precisely,

Hence,

| (2.1) |

and for every optimal in (2.1) we obtain an optimal for (1.2) by setting .

To characterize an optimal control for (2.1) denote by the filtration generated by , i.e.

and observe that

Note that and are measurable with respect to and that is independent of . Now choose a realization of . In particular, and are fixed. Furthermore, let

If the optimal strategy for maximizing

| (2.2) |

is independent of and , it is also optimal for maximizing over all . To identify one can extend the arguments from Theorem 2.1 in [16] and its corollary to the case, where the control does not take values in but in and the diffusion coefficient equals instead of 1. Observe that the required filtration is given by and that is an -Brownian motion. Then for all we have

where satisfies

| (2.3) |

with

The existence of a strong solution of (2.3) which is strongly unique follows from Theorem 1 in [18]. In particular, there exists a measurable function such that

and, thus, the drift of is a measurable function of the Brownian motion up to time . Hence, the optimal control for maximizing (2.2) is given by

and, in particular, it is independent of and . Therefore,

is optimal for (2.1). By setting we obtain an optimal control for (1.2).

For one also uses the arguments from [16] and obtains the same optimal strategy.

Remark 2.1.

We now summarize the result in the following theorem.

Theorem 2.2.

Let . The optimal drift rate in (1.2) for minimizing the ruin probability is given by

Moreover, the optimal transfer rate is .

Theorem 2.2 implies that the company with less endowment is as much supported as possible, i.e. this company receives a drift of until the endowment processes of the two companies are equal: The push-bottom strategy is optimal.

Remark 2.3.

In [9] and [10] the authors analyze two diffusion processes where the drift and diffusion coefficients are rank-dependent and the Brownian motions are independent. The leader obtains a negative drift coefficient and the laggard a positive one. For the isotropic case, i.e. for the same diffusion coefficients, this corresponds to the optimal controlled processes and for in our setting.

3 Perfectly Positive Correlation:

In this section we consider perfectly positively correlated Brownian motions, i.e. , which implies , and derive an explicit formula for the value function (1.2). In Section 3.1 we deal with the simplest case where and . For the same arguments can be used for endowment processes and having different diffusion coefficients. Hence, we extend our model and state the value function for different diffusion coefficients and in Section 3.2. In both sections we also compute the gain of collaboration.

3.1 Deriving the Value Function for and

We now derive the value function for and . The same arguments extend to the case with but lead to more complicated terms. Therefore, we first focus on this simple case.

Let , . As in Section 2 consider the processes

where and , . Recall that does not depend on the control ,

and that

Here is the set of all progressively measurable processes with respect to the filtration generated by satisfying for all .

Since is a Brownian motion with drift and it is not controllable by and does not depend on the Brownian motion , the best strategy is to control in such a way that it is going to zero with the highest possible rate and then let stay zero. In particular,

is optimal. Note that the corresponding optimal strategy in (1.2) is given by , which we have already seen in Theorem 2.2; also recall Remark 2.1.

Now assume that . Then the optimal controlled process is given by

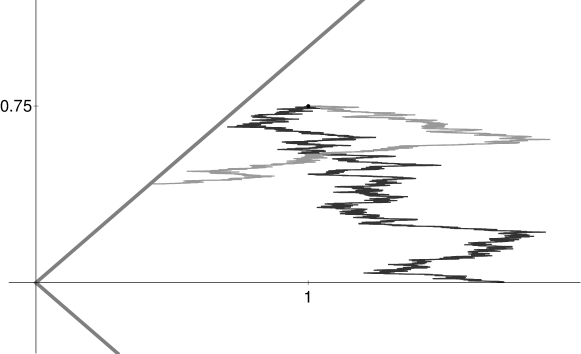

For computing the value function, we focus on . On the set the stopping time either occurs before the process becomes zero or afterwards. For two possible trajectories see Figure 1.

Hence,

We compute the two summands separately.

| (3.1) | ||||

where denotes the cumulative distribution function of a standard normal distribution. The last equality follows from Formula 1.2.4 in Part II, Chapter 2 of [6].

For the second summand we obtain

| (3.2) |

where the last equality follows from Formula 1.2.4 (1) in Part II, Chapter 2 of [6]. For the remaining probability we have

| (3.3) |

where we used Formula 1.2.8 in Part II, Chapter 2 of [6] in the last equality. Hence, combining (3.2) and (3.3) yields

| (3.4) |

Therefore, we conclude from (3.1) and (3.4) that for it holds that

For we have that for all . Therefore,

For we use the symmetry of the problem and conclude that .

To summarize, we have shown the following result.

Theorem 3.1.

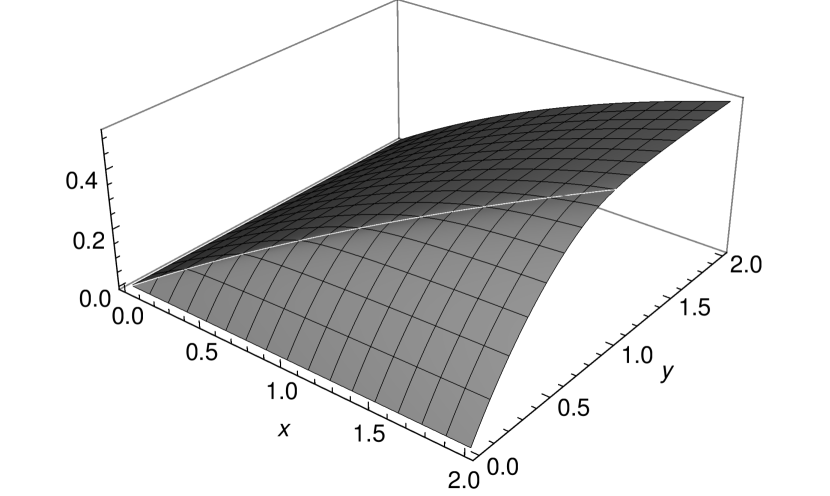

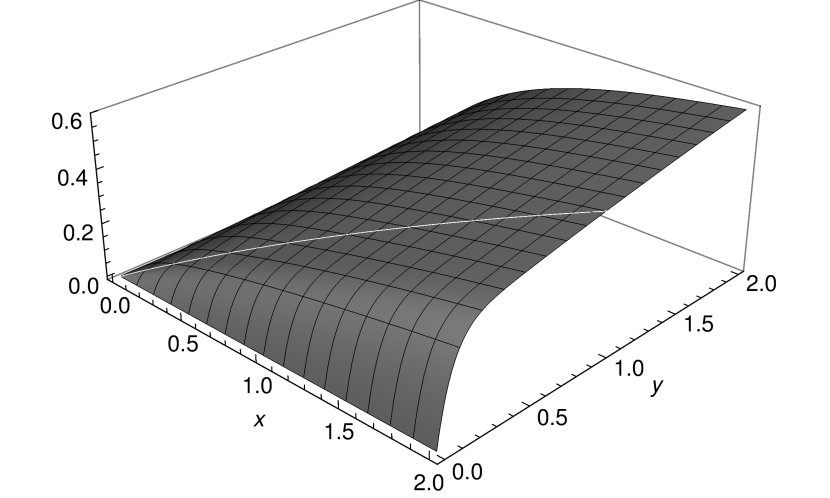

For , and the value function (1.2) is given by

Remark 3.2.

Hence, another possibility for proving Theorem 3.1 is to use a classical verification theorem. For applying this standard method the explicit formula of the value function has to be known in advance. The advantage of our approach is that it allows to compute the optimal strategy and the value function directly.

We now compare the gain of collaboration. If the two firms do not collaborate, i.e. for all , then the survival probability of both firms is given by

| (3.5) |

For the cases , with and with the endowment of one company is for all lower than the other company’s endowment. Thus, (3.5) is just the survival probability of the firm with lower endowment and we have

For with and with the company with lower initial endowment has less endowment until time and afterwards its endowment process is always larger than the process of the company with higher initial endowment. Therefore, it becomes more involved to compute (3.5). We apply similar arguments as in the derivation of the value function in Theorem 3.1, in particular, we use Formulas 1.2.4, 1.2.4 (1) and 1.2.8 in Part II, Chapter 2 of [6].

Assume that and . Then it holds that

For with change the role of and and the role of and .

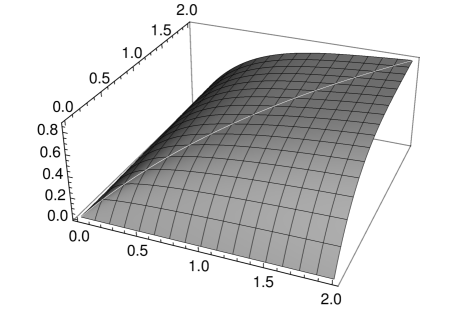

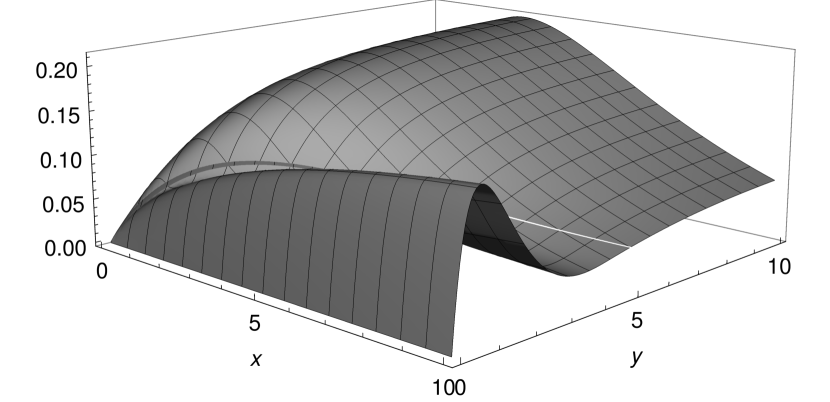

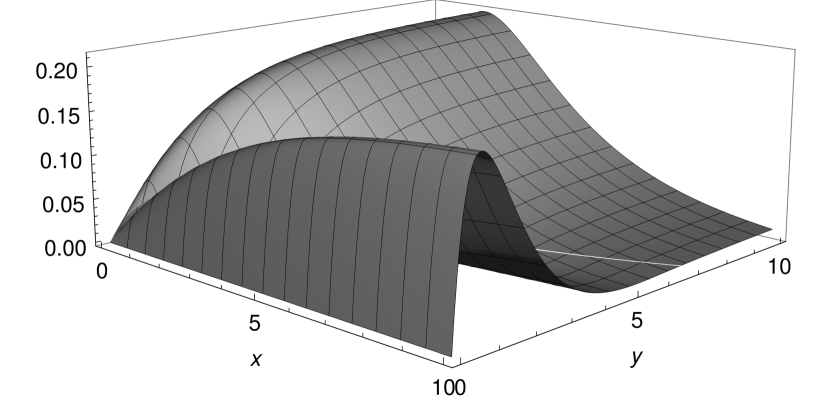

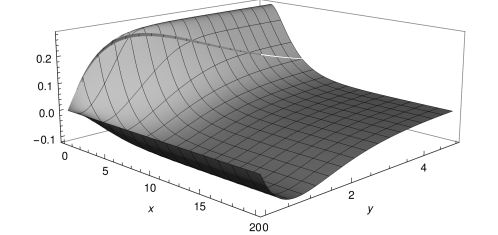

The gain of collaboration is then given by . See Figure 3 for the gain of collaboration for different drift rates and .

3.2 Different Diffusion Coefficients

We now extend the model (1.1) and allow for different diffusion coefficients for and . More precisely, for let

| (3.6) | ||||

where , , . Thus, the relative drift rates and are bounded below by .

Define and denote by

the value function in the extended model (3.6). Here denotes the set of progressively measurable processes with respect to the filtration generated by such that for all . Consider the transformation

where and , with . Observe that also in the extended model does not depend on the control and does not depend on the Brownian motion .

Using the same arguments as in Section 3.1 (but with more lengthy computations) we obtain the following result.

Theorem 3.3.

Let . Then the value function for the extended model (3.6) is given by

where

For it holds that

For we have

The optimal strategy for is given by

Remark 3.4.

Observe that the Hamilton-Jacobi-Bellman equation in the extended model (3.6) is given by

| (3.7) |

for with boundary conditions

| (3.8) | ||||

| (3.9) | ||||

| (3.10) |

One can prove that and that solves (3.7) with boundary conditions (3.8), (3.9) and (3.10). Furthermore,

| (3.11) | ||||

| (3.12) | ||||

To see that (3.11) holds true, note that for we have

If , then one can directly conclude that for all . If , then observe that

and

for . Hence, also in this case we have .

Similarly, one derives (3.12).

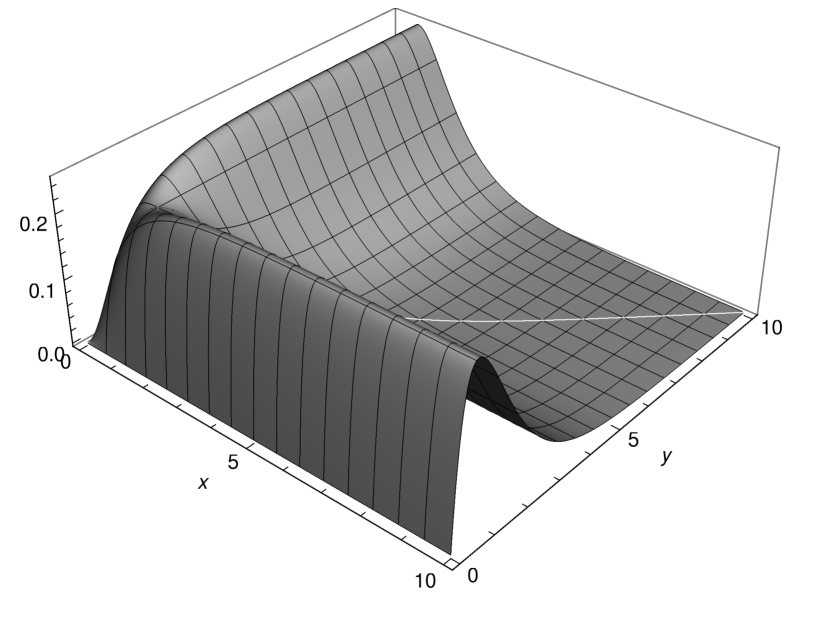

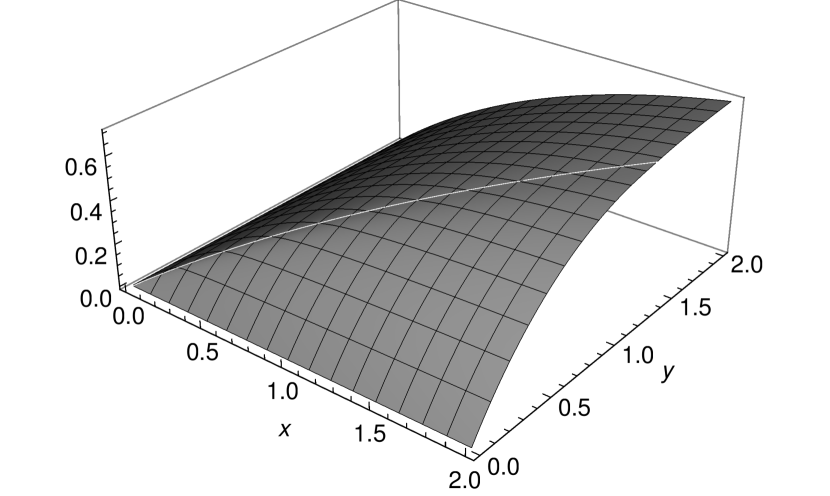

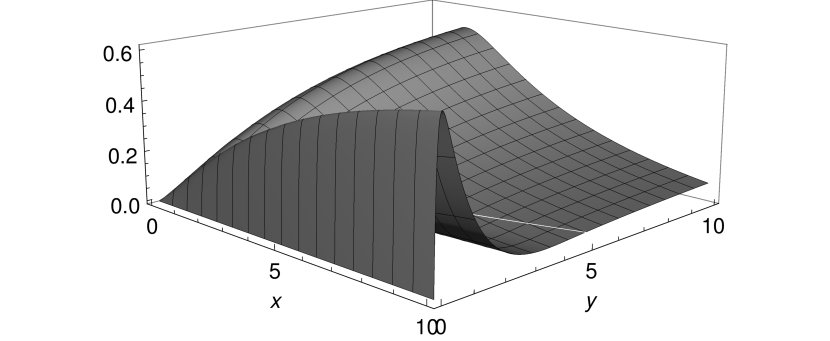

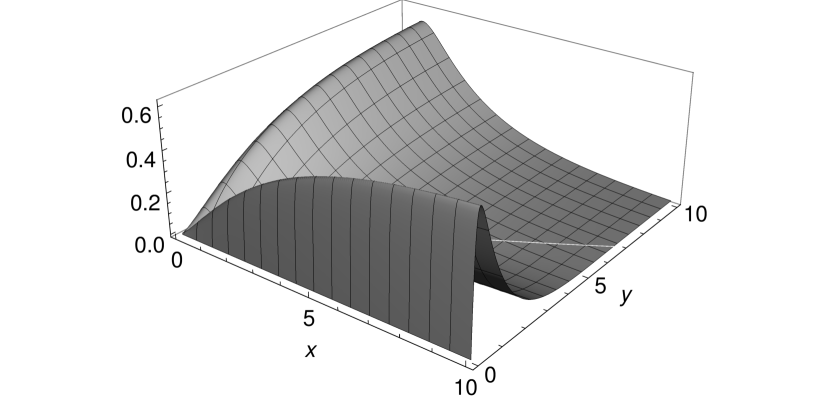

Figure 4 depicts the value function for different diffusion rates and different .

If we consider two insurance companies whose endowment processes are Brownian motions with drift , diffusion coefficients , , and initial endowments , respectively, then the survival probability can be derived similarly to the case and is given by

where

The gain of collaboration is then given by the difference

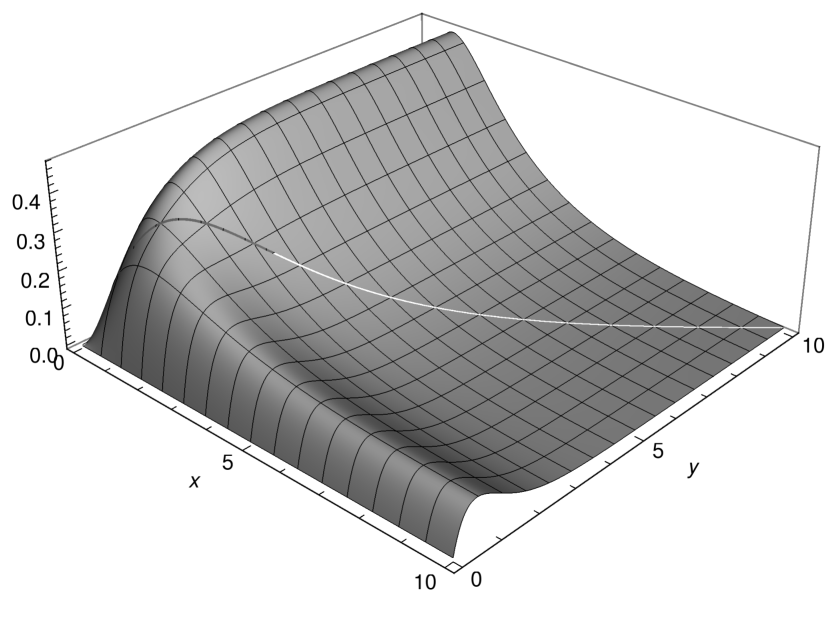

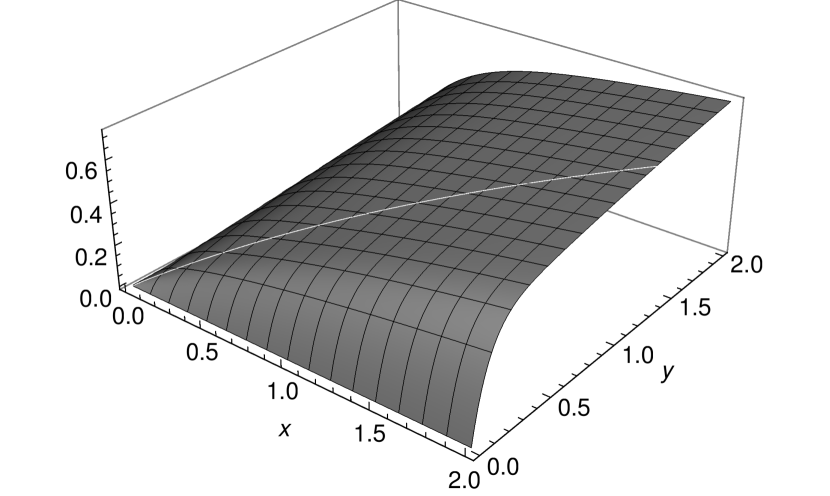

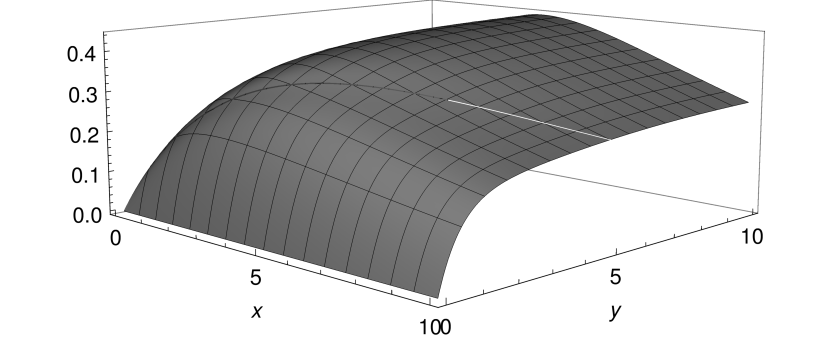

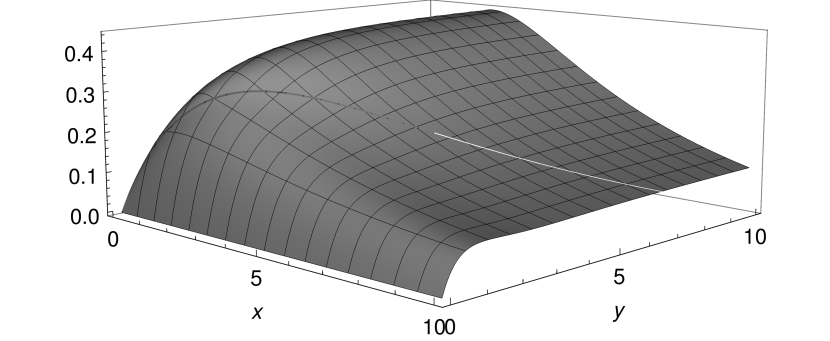

See Figure 5 for the gain of collaboration in case of different diffusion coefficients and drift rates.

Remark 3.5.

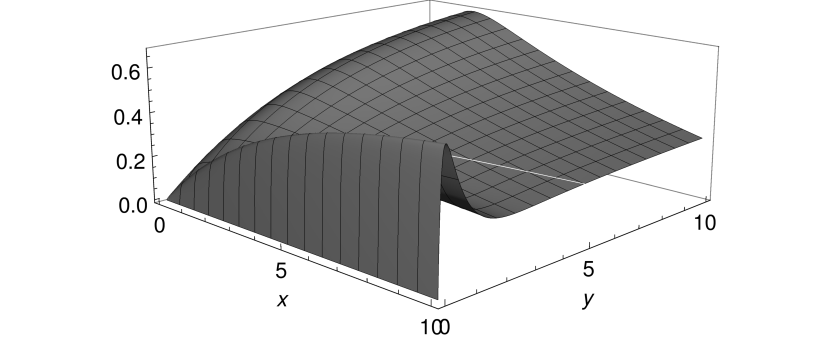

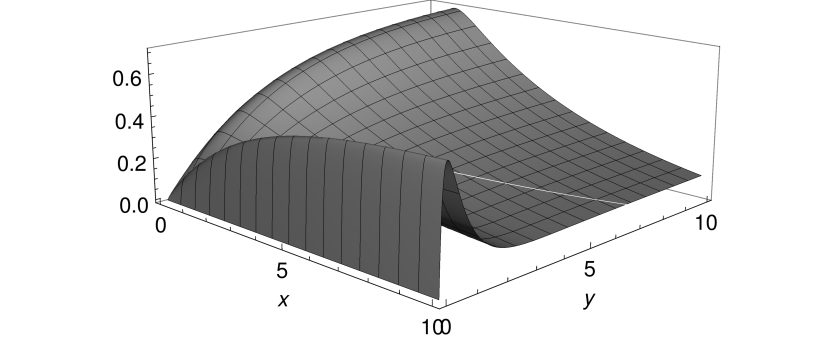

Observe that in the extended model we also relax the assumption on and do not assume that . For the companies are forced to collaborate, in particular firm with , , has to make payments to firm at every point in time. Thus, the gain of collaboration can be negative, see Figure 6.

4 Perfectly Negative Correlation:

In this section we focus on the case and obtain a different characterization of the value function in terms of the probability that a reflected Brownian motion with drift never hits a specific line. Unfortunately, we cannot use similar arguments as in the case to derive an explicit formula for the value function.

From Theorem 2.2 we already know that an optimal strategy for the transfer payments is given by

For perfectly negatively correlated Brownian motions and for the optimal strategy it holds that

Moreover,

and .

The process is a representation of a reflected Brownian motion with drift , see [14]. Therefore, the value function can be interpreted as the probability that a reflected Brownian motion with drift , never hits the linear barrier

To the best of our knowledge no closed formula for the hitting probability is available in the literature.

References

- [1] H. Albrecher, P. Azcue, and N. Muler. Optimal dividend strategies for two collaborating insurance companies. Adv. in Appl. Probab., 49(2):515–548, 2017.

- [2] S. Asmussen and H. Albrecher. Ruin Probabilities, volume 14 of Advanced Series on Statistical Science & Applied Probability. World Scientific Publishing, Hackensack, NJ, second edition, 2010.

- [3] F. Avram, Z. Palmowski, and M. Pistorius. A two-dimensional ruin problem on the positive quadrant. Insurance Math. Econom., 42(1):227–234, 2008.

- [4] F. Avram, Z. Palmowski, and M. R. Pistorius. Exit problem of a two-dimensional risk process from the quadrant: exact and asymptotic results. Ann. Appl. Probab., 18(6):2421–2449, 2008.

- [5] V. E. Beneš. Full “bang” to reduce predicted miss is optimal. SIAM J. Control Optim., 14(1):62–84, 1976.

- [6] A. N. Borodin and P. Salminen. Handbook of Brownian Motion – Facts and Formulae. Probability and its Applications. Birkhäuser Verlag, Basel, second edition, 2002.

- [7] W.-S. Chan, H. Yang, and L. Zhang. Some results on ruin probabilities in a two-dimensional risk model. Insurance Math. Econom., 32(3):345–358, 2003.

- [8] J. F. Collamore. Hitting probabilities and large deviations. Ann. Probab., 24(4):2065–2078, 1996.

- [9] E. R. Fernholz, T. Ichiba, and I. Karatzas. Two Brownian particles with rank-based characteristics and skew-elastic collisions. Stochastic Process. Appl., 123(8):2999–3026, 2013.

- [10] E. R. Fernholz, T. Ichiba, I. Karatzas, and V. Prokaj. Planar diffusions with rank-based characteristics and perturbed Tanaka equations. Probab. Theory Related Fields, 156(1-2):343–374, 2013.

- [11] H. U. Gerber and E. S. W. Shiu. On the merger of two companies. N. Am. Actuar. J., 10(3):60–67, 2006.

- [12] P. Grandits. On the gain of collaboration in a two dimensional ruin problem. Eur. Actuar. J., 9(2):635–644, 2019.

- [13] P. Grandits. A two-dimensional dividend problem for collaborating companies and an optimal stopping problem. Scand. Actuar. J., 2019(1):80–96, 2019.

- [14] S. E. Graversen and A. N. Shiryaev. An extension of P. Lévy’s distributional properties to the case of a Brownian motion with drift. Bernoulli, 6(4):615–620, 2000.

- [15] J.-W. Gu, M. Steffensen, and H. Zheng. Optimal dividend strategies of two collaborating businesses in the diffusion approximation model. Math. Oper. Res., 43(2):377–398, 2018.

- [16] N. Ikeda and S. Watanabe. A comparison theorem for solutions of stochastic differential equations and its applications. Osaka Math. J., 14(3):619–633, 1977.

- [17] H. P. McKean and L. A. Shepp. The advantage of capitalism vs. socialism depends on the criterion. J. Math. Sci., 139(3):6589–6594, 2006.

- [18] A. Y. Veretennikov. On the criteria for existence of a strong solution of a stochastic equation. Theory Probab. Appl., 27(3):441–449, 1983.