Nonparametric sequential change-point detection for multivariate time series based on empirical distribution functions

Abstract

The aim of sequential change-point detection is to issue an alarm when it is thought that certain probabilistic properties of the monitored observations have changed. This work is concerned with nonparametric, closed-end testing procedures based on differences of empirical distribution functions that are designed to be particularly sensitive to changes in the contemporary distribution of multivariate time series. The proposed detectors are adaptations of statistics used in a posteriori (offline) change-point testing and involve a weighting allowing to give more importance to recent observations. The resulting sequential change-point detection procedures are carried out by comparing the detectors to threshold functions estimated through resampling such that the probability of false alarm remains approximately constant over the monitoring period. A generic result on the asymptotic validity of such a way of estimating a threshold function is stated. As a corollary, the asymptotic validity of the studied sequential tests based on empirical distribution functions is proven when these are carried out using a dependent multiplier bootstrap for multivariate time series. Large-scale Monte Carlo experiments demonstrate the good finite-sample properties of the resulting procedures. The application of the derived sequential tests is illustrated on financial data.

keywords:

[class=MSC2010]keywords:

and

1 Introduction

Let , , be a stretch from a -dimensional stationary times series of continuous random vectors with unknown contemporary distribution function (d.f.) given by , . These available observations will be referred to as the learning sample as we continue. The context of this work is that of sequential change-point detection: new observations arrive sequentially and we wish to issue an alarm as soon as possible if the contemporary distribution of the most recent observations is not equal to anymore. If there is no evidence of a change in the contemporary distribution, the monitoring stops after the arrival of observation for some .

The theoretical framework of our investigations is that adopted in the seminal paper of Chu, Stinchcombe and White (1996). Unlike classical approaches in statistical process control (SPC) usually calibrated in terms of average run length (ARL) (see, e.g., Lai, 2001; Montgomery, 2007, for an overview) and leading in general to the rejection of the underlying null hypothesis of stationarity with probability one, the approach of Chu, Stinchcombe and White (1996) guarantees that, asymptotically (that is, as the size of the learning sample tends to infinity), stationarity, if it holds, will only be rejected with a small probability to be interpreted as a type I error and thus called the probability of false alarm. The latter paradigm is increasingly considered in the literature; see, e.g., Horváth et al. (2004), Aue et al. (2012a), Aue et al. (2012b), Fremdt (2015), Kirch and Weber (2018), Dette and Gösmann (2019) or Kirch and Stoehr (2019).

Among the approaches à la Chu, Stinchcombe and White (1996), one can distinguish between closed-end and open-end procedures. The latter can in principle continue indefinitely if no evidence against the null is observed. Our approach is of the former type in the sense that at most new observations will be considered before the monitoring stops.

As already mentioned, the null hypothesis of the procedure that we shall investigate is that of stationarity and can be more formally stated as follows:

| (1.1) |

Notice that, if one is additionally ready to assume the independence of the observations, simplifies to

| (1.2) |

The aim of this work is to derive nonparametric sequential change-point detection procedures particularly sensitive to the alternative hypothesis

| (1.3) |

In other words, unlike some of the approaches reported for instance in Kirch and Weber (2018), Dette and Gösmann (2019) or Kirch and Stoehr (2019), we are not solely interested in being sensitive to a change in a given parameter of the -dimensional time series such as the mean vector or the covariance matrix. We aim at deriving nonparametric monitoring procedures that, in principle, provided and are large enough, can detect all types of changes in the contemporary d.f.

In the considered context, the two main ingredients of a sequential change-point detection procedure are a sequence of positive statistics , , and a sequence of suitably chosen strictly positive thresholds , . For , the statistic (called a detector in the literature) is used to assess a possible departure from in (1.1) using only observations and is such that the larger , the more evidence against . After the arrival of observation , , the detector is computed and compared to the threshold . If , the available evidence against stationarity is considered to be large enough and an alarm is issued resulting in the monitoring to stop. If and , a new observation is collected and the previous iteration is repeated. This monitoring process can be naturally represented by a graph illustrating the evolution of the sequence of detectors against the sequence of thresholds; see, e.g., Figures 6.1 and 6.2. To ensure that the monitoring can be interpreted as a testing procedure, the sequence of thresholds , , needs to be chosen such that, under stationarity,

| (1.4) |

for some small significance level .

The detectors , , proposed in this work are defined from differences of empirical distribution functions. Specifically, as shall be explained in detail in Section 2, particularly powerful monitoring procedures can be obtained by defining as a maximized, suitably normalized difference of empirical distribution functions computed from and , respectively, where the maximum is taken over all . When sequentially investigating changes in real-valued parameters of multivariate time series, such an approach (related to what was called a Page-CUSUM procedure in Kirch and Weber (2018) as a consequence of the work of Fremdt (2015)) was recently suggested in Dette and Gösmann (2019) and justified through a likelihood ratio approach. The latter principle had actually already been considered in the SPC literature (to the best of our knowledge, without any asymptotic theory, however) since at least the work of Hawkins, Qiu and Kang (2003); see also Hawkins and Zamba (2005), Ross, Tasoulis and Adams (2011) and Ross and Adams (2012). As we shall see, our detectors can be cast into the framework of Dette and Gösmann (2019) with the difference that they involve a weighting allowing to give more or less importance to recent observations. In that sense, they could also be regarded as an adaptation of the statistics considered in Csörgő and Szyszkowicz (1994a) for a posteriori (offline) change-point detection to the sequential setting considered in this work.

As far as the thresholds , , are concerned, unlike in the recent literature in which these are calibrated through parametric functions defined up to a positive multiplicative constant such that (1.4) holds (see, e.g., Kirch and Weber, 2018; Dette and Gösmann, 2019; Kirch and Stoehr, 2019), we define them through simulations or resampling with the aim that, under in (1.1), the probability of rejection of be roughly the same at every step of the procedure. In the considered sequential testing framework à la Chu, Stinchcombe and White (1996), the latter requirement had actually already been proposed by Anatolyev and Kosenok (2018). Interestingly enough, as we shall see, it is strongly related to an approach appearing in SPC in Margavio et al. (1995); see also, for instance, Hawkins and Zamba (2005), Ross (2014), Ross and Adams (2012) and the R package cpm described in Ross (2015).

From the point of view of their main ingredients, the sequential change-point tests studied in this work are related to the approach put forward in SPC in Ross and Adams (2012) (without any asymptotic theory) and implemented in the R package cpm (Ross, 2015). However, unlike the latter, they are not restricted to univariate observations and they can deal with time series, among several other differences. To achieve this, as soon as the learning data set is multivariate () or serially dependent, resampling, under the form of a dependent multiplier bootstrap à la Bücher and Kojadinovic (2016), is used to carry out the monitoring procedures. By adapting the theoretical framework considered in Dette and Gösmann (2019), the asymptotic validity of the investigated procedures is proven under strong mixing both under in (1.1) and under sequences of alternatives related to in (1.3).

This paper is organized as follows. In the second section, we propose three classes of detectors based on differences of empirical d.f.s and study their asymptotics, both under and sequences of alternatives related to . A more general perspective is adopted in the third section: for an arbitrary detector in the considered closed-end setting, a procedure for estimating the threshold function such that the probability of false alarm remains approximately constant over the monitoring period is investigated and its asymptotic validity is proven under both and sequences of alternatives related to when the estimation is based on an asymptotically valid resampling scheme. The results of the third section are applied in the fourth section to the three proposed classes of detectors based on differences of empirical d.f.s. To do so, the consistency of a dependent multiplier bootstrap for the detectors is proven under strong mixing. The fifth section presents a summary of large-scale Monte-Carlo experiments demonstrating the good finite-sample properties of the resulting sequential testing procedures. An application on real financial data concludes the article.

2 The detectors and their asymptotics

After defining three classes of detectors based on empirical distribution functions and noticing that they are margin-free under in (1.1), we study their asymptotics under the null and sequences of alternatives related to in (1.3).

2.1 Detectors based on empirical distribution functions

Let be the empirical d.f. computed from the stretch of available observations. More formally, for any integers and , let

| (2.1) |

where the inequalities are to be understood componentwise and is equal to 1 (resp. 0) if all (resp. some) of the underlying inequalities are true (resp. false).

After the th observation has arrived, the available data take the form of the stretch . If we were in the context of a posteriori change-point detection, a prototypical test statistic would be the maximally selected Kolmogorov–Smirnov-type statistic

| (2.2) |

practically considered for instance in Gombay and Horváth (1999) or Holmes, Kojadinovic and Quessy (2013). The intuition behind is the following: every is treated as a potential break point in the sequence and the maximum in (2.2) implies that will be large as soon as the difference between and is large for some . The weighting ensures that converges in distribution under stationarity as . As explained for instance in Csörgő and Szyszkowicz (1994a) in the case of independent observations, replacing for instance these weights simply by would result in a statistic that diverges in probability to under stationarity. The part in the weighting favors however the detection of potential break points in the middle of the sequence. Test statistics that are more sensitive to changes at the beginning or at the end of the sequence but still converge in distribution under stationarity can be obtained by considering weights of the form for some suitable strictly positive function on ; see, e.g., Csörgő and Szyszkowicz (1994b, a), Csörgő, Horváth and Szyszkowicz (1997) and Csörgő and Horváth (1997).

Going back to the setting of sequential change-point detection considered in this work, a first meaningful modification of (2.2) is to restrict the maximum over to since a change cannot occur at the beginning of the sequence given that is the learning sample known to be a stretch from a stationary sequence. Another modification is a rescaling consisting of replacing by in the weighting. The latter is made solely for asymptotic reasons as shall become clear in Sections 2.3 and 2.4. These modifications essentially lead to the first detectors considered in this work:

| (2.3) |

In the previous display, is a strictly positive function whose role is to potentially give more weight to recent observations. In the sequel, we consider the parametric form

| (2.4) |

where is a small constant and is a parameter in . If , is the constant function and is then a straightforward adaptation of in (2.2) to sequential change-point detection. In that case, the general form of can also be heuristically justified through a likelihood ratio approach; see Section 2 in Dette and Gösmann (2019). When , as shall be discussed in Remark 2.6 using asymptotic arguments, can be regarded, under in (1.1), as a maximum of random variables with, approximately, the same mean and variance. This heuristically implies that all the potential break points are given roughly the same weight in the computation of unlike in the case in which potential break points closest to are given more weight. Hence, for certain types of alternatives to in (1.1), choosing might accelerate the detection of the corresponding change in the contemporary distribution of the underlying time series. Examples of such alternatives will be given in Section 5 in which the results of numerous Monte Carlo experiments are summarized.

Two similar Cramér–von Mises-like detectors are also considered in this work. They are defined, for , by

| (2.5) |

and

| (2.6) |

Remark 2.1.

The detectors in (2.3) and (2.5) are related to those used in Ross and Adams (2012, pp 104–106). The latter are also based on differences of empirical d.f.s but deal only with independent univariate observations. The analogue of (2.3) is apparently defined as a maximum of the quantities , , previously normalized using an empirical probability integral transformation, probably based on simulations. The analogue of (2.5) takes the form of a maximum of the quantities , , after centering and scaling. The asymptotics of these detectors were not studied. Given that the detectors of Ross and Adams (2012) are distribution-free (see also Section 2.2 hereafter), that their approach assumes serially independent observations and is based on simulations, the absence of asymptotic theory is not problematic.

Remark 2.2.

The detectors in (2.3), (2.5) and (2.6) are almost of the Page-CUSUM type considered initially in Fremdt (2015); see also Kirch and Weber (2018). For instance, in the case of (2.3), the adaption of the latter construction to the present setting would have instead involved a maximum of the quantities , . As explained in Dette and Gösmann (2019), the use of such detectors may result in a loss of power in the case of a small learning sample and a rather late change point. In the Monte Carlo experiments carried out in Dette and Gösmann (2019), Page-CUSUM detectors were always outperformed by their analogues of type (2.3), which is why we do not consider them in this work.

Remark 2.3.

In addition to the detectors (2.3), (2.5) and (2.6), we also considered in our Monte Carlo experiments the following natural competitors which are straightforward adaptions of the so-called CUSUM construction considered for instance in Horváth et al. (2004) and Aue et al. (2012b). Their Kolmogorov–Smirnov versions and Cramér–von Mises versions are respectively given, for any , by

| (2.7) | ||||

| (2.8) |

The asymptotic theory for these detectors being simpler than for the detectors (2.3), (2.5) and (2.6), it will not be stated in the forthcoming sections for the sake of readability.

2.2 The detectors are margin-free under the null

The detectors defined previously are actually margin-free under in (1.1), a property that shall be exploited in the forthcoming sections to carry out the corresponding sequential change-point detection procedures.

Recall that are assumed to be continuous random vectors. Saying that the detectors are margin-free under the null means that they do not depend on the univariate margins of (the unknown d.f. of ) or, equivalently, that they can alternatively be written in terms of the unobservable random vectors defined from through marginal probability integral transformations:

| (2.9) |

Notice that we can recover the from the by marginal quantile transformations:

| (2.10) |

where, for any univariate d.f. , denotes its associated quantile function defined by

| (2.11) |

with the convention that the infimum of the empty set is .

To verify that the detectors are margin-free under the null, for any integers and , let

| (2.12) |

be the analogue of in (2.1) based on the in (2.9). For any , by (right) continuity of , we have that for all and ; see, e.g., Proposition 1 (5) in Embrechts and Hofert (2013). The latter property combined with (2.10) implies that, under in (1.1), for any ,

| (2.13) |

where . Hence, for any ,

using again the continuity of . Similarly,

In the case of univariate independent observations, the margin-free property under the null implies that the detectors are distribution-free under the null. When , this is not true anymore as the null distribution of the detectors depends on the copula associated with . The latter is merely the d.f. of the random vector obtained through (2.9). Equivalently, is a -dimensional d.f. with standard uniform margins further uniquely defined (see Sklar, 1959) through the relationships

and

Remark 2.4.

To be able to handle both the univariate and the multivariate situations, in the rest of the paper, we adopt the convention that is the copula associated with when and merely the identity function when .

2.3 Asymptotics of the detectors under the null

As shall become clear in the forthcoming sections, the knowledge of the asymptotic behavior of the detectors under in (1.1) is instrumental in showing the asymptotic validity of the corresponding sequential change-point detection procedures. To study these asymptotics, we follow Dette and Gösmann (2019), among others, and set for some fixed real number . This will imply that, in the asymptotics, as the size of the learning sample goes to infinity, the maximum number of new observations considered in the monitoring increases proportionally.

Let and let

| (2.14) |

Then, for any and , let

| (2.15) |

where and are generically defined by (2.12), and let

| (2.16) |

where is defined in (2.4). Notice that, with the definitions adopted thus far, for all .

For any with and any , there exists such that and . We can thus write as

| (2.17) |

Similarly, it can be verified that

| (2.18) | ||||

| (2.19) |

As we continue, we adopt the convention that . Furthermore, given a set , the space of all bounded real-valued functions on equipped with the uniform metric is denoted by . The main purpose of this section is to study the asymptotics under the null of the elements , and of defined respectively, for any , by

| (2.20) |

Specifically, we will provide conditions under which they converge weakly in the sense of Definition 1.3.3 in van der Vaart and Wellner (2000) under in (1.1). Throughout the paper, this mode of convergence will be denoted by the arrow ‘’ and all convergences will be for unless mentioned otherwise.

From the expressions given in (2.17), (2.18) and (2.19), we see that, under the null, the detectors studied in this work are functionals of in (2.16), and thus of in (2.15). Under stationarity, the latter is in turn a functional of the sequential empirical process defined, for any and , by

| (2.21) |

Indeed, under in (1.1), for any and ,

| (2.22) |

In the forthcoming asymptotic results, we shall assume that the underlying stationary sequence (or, equivalently, the corresponding unobservable stationary sequence defined through (2.9)) is strongly mixing. Denote by the -field generated by , , and recall that the strong mixing coefficients corresponding to the stationary sequence are then defined by ,

and that the sequence is said to be strongly mixing if as . The following result is proven in Appendix A.

Proposition 2.5.

Assume that in (1.1) holds and that, additionally, is a stretch from a stationary sequence of continuous -dimensional random vectors whose strong mixing coefficients satisfy for some as . Then, in , where is a tight centered Gaussian process with covariance function

with the minimum operator and

| (2.23) |

As a consequence, and in , where and are defined in (2.15) and (2.16), respectively, and, for any and ,

| (2.24) |

It follows that , and in , where

| (2.25) |

Furthermore, for any interval such that , the distributions of , and are absolutely continuous with respect to the Lebesgue measure.

Combined with a generic result on the threshold estimation procedure to be stated in Section 3 and additional bootstrap consistency results to be stated in Section 4, the last claims of Proposition 2.5 constitute a first step in proving that the derived change-point detection procedures hold their level asymptotically.

Remark 2.6.

Proposition 2.5 can be used to heuristically justify the form of the weight function in (2.4) appearing in the expression of the detectors (2.3), (2.5) and (2.6). From (2.24), for any and , we obtain that

As a consequence, for any and ,

Under the conditions of the proposition, when and is large, we could then expect that, very roughly, does not depend on and thus regard the quantities , , appearing in the expression of in (2.17) as random variables with, approximately, the same mean and variance. The latter conveys the intuition that, when , all the potential break points are given roughly the same weight in the computation of . This is, of course, only approximately true because of the presence of the constant in the expression of the weight function in (2.4). In practice, the setting might accelerate the detection of certain types of changes.

2.4 Asymptotics of the detectors under alternatives related to

Under alternatives related to in (1.3), the detectors are not margin-free anymore. As we shall see in the forthcoming proposition, their asymptotic behavior is then a consequence of that of the process

where

| (2.26) |

the empirical d.f.s and are generically defined by (2.1), and is defined in (2.4).

The following result is proven in Appendix A. The arrow ‘’ in its statement denotes convergence in probability.

Proposition 2.7.

Assume that, for some , , denoted equivalently by , is a stretch from a stationary sequence of continuous -dimensional random vectors with contemporary d.f. whose strong mixing coefficients satisfy for some as , and that , denoted equivalently by , is a stretch from a stationary sequence of continuous -dimensional random vectors with contemporary d.f. whose strong mixing coefficients satisfy for some as . Then, in , where

| (2.27) |

Consequently, in , where , , , and

Combined with a generic result on the threshold estimation procedure to be stated in the forthcoming section and additional results on the asymptotic validity of adequate resampling methods to be stated in Section 4, the three last claims of the previous result will be instrumental in showing that the derived change-point detection procedures have asymptotic power one under sequences of alternatives related to .

3 A generic threshold estimation procedure

In the studied context, the second ingredient of a sequential change-point detection procedure is a set of strictly positive thresholds to which detectors will be compared. In this section, we consider a generic threshold estimation procedure that can be employed with any type of detector, and provide conditions under which it is asymptotically valid. The derived results will be applied in the next section to establish the asymptotic validity of sequential change-point detection procedures based on the detectors studied in Section 2.

3.1 A constant probability of false alarm at each step

Within the context of closed-end monitoring from time to time , let , , be arbitrary detectors. As discussed in the introduction, it seems natural to choose the corresponding thresholds , , so that, under in (1.1), the probability of rejection of is the same at every step of the procedure. Adapting the reasoning of Anatolyev and Kosenok (2018) to our context, the latter requirement consists of choosing the , , such that, under stationarity, for all ,

| (3.1) |

where is the desired significance level of the sequential testing procedure, or, equivalently, such that, under , for all ,

Notice that the previous display translates mathematically our requirement that the probability of false alarm be proportional to the number of monitoring steps.

Interestingly enough, the previous way of choosing the thresholds , , is strongly related to an approach used in SPC and possibly first appearing in Margavio et al. (1995) (see also, e.g., Hawkins and Zamba, 2005; Ross, 2014). It consists of choosing the , , such that, under stationarity, for some small ,

| (3.2) |

We then obtain that, under , for all ,

| (3.3) |

with the convention that .

Given a desired significance level , a simple way to ensure that (1.4) holds under is to choose such that , that is, . As one can see from (3.2), is then a quantile of order of under stationarity and, for any , is a quantile of order of conditionally on under stationarity. When as is typically the case, the first-order approximation turns out to be precise up to at least two decimals. Similarly, for all ,

where it can be verified that the resulting approximation is precise up to at least two decimals. In other words, for typical values of , choosing the thresholds , such that (3.2) holds with is almost equivalent to choosing the thresholds such that (3.1) holds (some thought reveals that the latter equivalence could be made to hold exactly by allowing in (3.2) to change with ).

Given the precision of the aforementioned first-order approximations for typical values of , for the sake of a simplicity, we shall base our threshold estimation procedure on (3.2). Before we discuss the estimation of the thresholds and its validity, let us give an alternative view of (3.2). In Sections 2.3 and 2.4 in which was taken equal to , we saw that the asymptotic results for the detectors are given in terms of elements of . With the convention that , another equivalent way of looking at sequential change-point detection procedures of the considered type is then to consider that the piecewise constant detector function defined by , , is compared to the piecewise constant threshold function defined by , . Let , and define the intervals , , and . Some thought reveals that (3.2) is then equivalent to choosing the threshold function such that, under in (1.1), for any ,

| (3.4) |

3.2 A formulation compatible with asymptotic validity results

With , the threshold setting procedure as given in (3.2) or (3.4) makes no sense asymptotically since the number of (conditional) probabilities tends to infinity as . A natural solution consists of keeping the number of probabilities fixed, or, equivalently, of considering a time grid that does not depend on . Let and let be a fixed uniformly spaced time grid such that (a condition that will always be satisfied for large enough). Let be a piecewise constant threshold function taking the value on the interval , , and on the interval . Mimicking (3.4), the aim is then to choose such that, under in (1.1), for any ,

| (3.5) |

with the convention that . Some thought reveals that the formulation in (3.5) is equivalent to choosing such that, under in (1.1),

| (3.6) |

In other words, is a quantile of order of under stationarity and , , is a quantile of order of given that under stationarity. Notice that the suprema in (3.6) are actually maxima since is a piecewise constant function.

Remark 3.1.

A further generalization of (3.5) or, equivalently (3.6), would be to consider that is not necessarily piecewise constant but only defined up to a multiplicative constant on each of the intervals , . For instance, it could have one of the parametric forms considered in Dette and Gösmann (2019, Section 5), among others. For the sake of simplicity, we shall not however consider such an extension in this work.

3.3 Estimation of the threshold function

As we continue, we shall focus on the threshold setting procedure as formulated in (3.5) or, equivalently, (3.6), mostly because its asymptotic validity can be studied. To estimate the threshold function in (3.5), or, equivalently, the , , in (3.6), it is thus necessary to be able to compute, at least approximately, the distribution of the -dimensional random vector

| (3.7) |

3.3.1 Monte Carlo estimation and asymptotic validity

Assume that the observations to be monitored are univariate and independent, and that is distribution-free under in (1.2). Notice that the latter implies that so is the random vector (3.7). To obtain a Monte Carlo estimate of the distribution of (3.7), it then suffices to consider a large integer , generate independent samples , , of size from the standard uniform distribution and compute the corresponding realizations , , of . The latter can be used to obtain a Monte Carlo estimate of the threshold function . More formally, let

where is the empirical d.f. of the sample , for any and ,

and , , are the associated quantile functions generically defined by (2.11). Notice that, in this particular case, the resulting estimate of the threshold function does not at all depend on the learning sample.

By taking a sufficiently large , the Monte Carlo estimates , , can be made arbitrarily close to the quantiles , , where is the d.f. of , and , , is the d.f. of given that for all . Interestingly enough more can be said as a consequence of the fact that Monte Carlo simulation can be regarded as a particular resampling scheme. As shall become clear in the next section, the general result stated in Theorem 3.3 hereafter can actually be used to show the asymptotic validity of the Monte Carlo based threshold estimation procedure when both and tend to infinity, under both in (1.2) and sequences of alternatives related to in (1.3). This is discussed in more detail in Remark 3.4 below.

3.3.2 Bootstrap-based estimation and asymptotic validity

In settings in which is not distribution-free anymore, a natural alternative is to rely on a resampling scheme making use of the available learning sample known to be under in (1.1). Specifically, let be a large integer and suppose that we have available bootstrap replicates , , of computed from and depending on additional sources of randomness involved in the resampling scheme. Mimicking the previous situation in which was distribution-free, let

where is the empirical d.f. of the sample , and, for any and ,

As we shall see below, the main result of this section is that, essentially, as soon as the underlying resampling scheme for is consistent, the above bootstrap-based version of the threshold setting procedure (3.6) is asymptotically valid in the sense that, under , as , where is the estimated bootstrap-based piecewise constant threshold function taking the value on the interval , , and on the interval .

Remark 3.2.

Following for instance van der Vaart and Wellner (2000, Section 3.6) or Kosorok (2008, Section 2.2.3), a resampling scheme for is typically considered consistent, if, informally, “ converges weakly to the weak limit of in conditionally on in probability”. A rigorous definition of the underlying mode of convergence is more subtle than that of weak convergence. From Lemma 3.1 of Bücher and Kojadinovic (2019), the aforementioned validity statement is actually equivalent to the joint unconditional weak convergence of and two bootstrap replicates to independent copies of the same limit. Throughout the paper, all our bootstrap asymptotic validity results will take that form.

The following general result is proved in Appendix C.

Theorem 3.3.

Remark 3.4.

Consider the Monte Carlo estimation setting of Section 3.3.1 in which the observations to be monitored are univariate independent and is distribution-free. Then, the weak convergence in under immediately implies (3.8), where and are (independent) Monte Carlo replicates of . Hence, as a consequence of Theorem 3.3, the asymptotic validity under in (1.2) of the sequential change-point detection procedure based on and the Monte Carlo estimated threshold function defined in Section 3.3.1 is an immediate corollary of the weak convergence under the null of if has a continuous d.f.

4 Threshold function estimation for the detectors based on empirical d.f.s

The aim of this section is to apply the generic results of the previous section to estimate the threshold functions for the empirical d.f.-based detector functions , and defined in (2.20). We distinguish two situations for the observations to be monitored: the independent univariate case and the possibly multivariate, time series case.

4.1 Monte Carlo estimation in the independent univariate case

As verified in Section 2.2, the detector functions , and defined in (2.20) are margin-free under in (1.1). In the univariate case, they are thus distribution-free. When dealing with independent univariate observations, one can therefore proceed exactly as explained in Section 3.3.1 to estimate the corresponding threshold functions. Furthermore, from Proposition 2.5, Remark 3.4 and Proposition 2.7, we know that the assumptions of Theorem 3.3 are satisfied. The latter then implies that the corresponding sequential change-point detection procedures are asymptotically valid both under in (1.2) and sequences of alternatives related to in (1.3).

4.2 A dependent multiplier bootstrap in the time series case

When the monitored observations are multivariate or exhibit serial dependence, the approach considered in Section 4.1 is not meaningful anymore. Having the asymptotic results of Sections 2.3 and 3.3.2 in mind, our aim in the considered time series context is to define suitable bootstrap replicates of in (2.21) such that, following Remark 3.2, and two of its replicates jointly weakly converge to independent copies of the process defined in Proposition 2.5. Subsequently defining corresponding bootstrap replicates of the detectors functions , and defined in (2.20) will lead to asymptotically valid corresponding sequential change-point detection procedures.

Following Bühlmann (1993, Section 3.3) and Bücher and Kojadinovic (2016), we opted for a dependent multiplier bootstrap in the considered time series context. In the rest of the paper, we say that a sequence of random variables is a dependent multiplier sequence if:

-

(M1)

The sequence is stationary, independent of the available learning sample and satisfies , and for all .

-

(M2)

There exists a sequence of strictly positive constants such that and the sequence is -dependent, i.e., is independent of for all and .

-

(M3)

There exists a function , symmetric around 0, continuous at , satisfying and for all such that for all .

Let , , be independent copies of the same dependent multiplier sequence. If we had a learning sample of size , following Bücher and Kojadinovic (2016), a natural definition of a dependent multiplier replicate of in (2.21) would be

| (4.1) |

where is generically defined by (2.12). Since threshold functions need to be estimated prior to the beginning of the monitoring and the learning sample is only of size , we consider a time-rescaled version of in which, roughly, and play the role of and , respectively. Hence, in the considered context, our definition of a dependent multiplier replicate of is

| (4.2) |

thereby translating the fact that we can only rely on functionals computed from the learning sample to approximate the variability of the detector functions under the null.

From the two previous displays, we see that the multipliers act as random weights and that the bandwidth defined in Assumption (M2) plays a role somehow similar to that of the block length in the block bootstrap of Künsch (1989). Note that, in our Monte Carlo experiments to be presented in Section 5, was estimated from the learning sample as explained in detail in Section 5.1 of Bücher and Kojadinovic (2016) while corresponding dependent multiplier sequences were generated using the so-called moving average approach based on an initial standard normal random sample and Parzen’s kernel as precisely described in Section 5.2 of the same reference.

The latter construction based on a time-rescaling suggests to form a dependent multiplier replicate of in (2.22) as

with its weighted version being

where is defined as in (2.14). Finally, for any and , let

| (4.3) |

be dependent multiplier replicates of , and , respectively, defined in (2.20), where is defined generically by (2.12).

The definitions given in (4.3) hide the fact that the proposed dependent multipliers replicates of the detector functions , and actually depend on the learning sample . To verify that this is the case, for any , and , let , where ,

and

Since (2.13) always holds for all , we immediately obtain that, for any ,

where is generically defined by (2.1), and furthermore that, for any ,

The following result is proven in Appendix D.

Proposition 4.1.

Assume that in (1.1) holds and that, additionally, is a stretch from a stationary sequence of continuous -dimensional random vectors whose strong mixing coefficients satisfy for some as . If for some , then

in , where is defined in (2.21), and are defined in (4.2), is the weak limit of defined in Proposition 2.5, and and are independent copies of .

The last claims of the previous proposition along with the last claim of Proposition 2.5 and Proposition 2.7 are the assumptions of Theorem 3.3 for . It follows that the sequential change-point detection procedures based on these detector functions carried out as explained in Section 3.3.2 using the above dependent multiplier replicates are asymptotically valid under in (1.1) and sequences of alternatives related to in (1.3). Note that, in practice, since in the considered approach and play the role of and , respectively, the largest possible value for , the number of steps of the estimated threshold function , is and, in this case, each of the estimated thresholds covers approximately time steps in the monitoring.

5 Monte Carlo experiments

Large-scale Monte Carlo experiments were carried out to investigate the finite-sample properties of the studied sequential change-point detection procedures. The aim was in particular to try to answer the following questions:

-

•

How well do the procedures hold their level, in particular, when the threshold functions are estimated using the dependent multiplier bootstrap of Section 4.2?

- •

-

•

What is the effect of on the power and the mean detection delay (the latter is the expectation under of the difference between the time at which the change was detected and the time at which the change really occurred)?

-

•

What is the effect of the parameter appearing in the expression of the weight function defined in (2.4) on the power and mean detection delay?

- •

-

•

How do the derived procedures compare with similar, more specialized procedures in terms of power and mean detection delay?

We tried to answer these questions in detail in the univariate independent case when the estimation of the threshold functions of the sequential change-point detection procedures can be rightfully so based on the Monte Carlo approach described in Sections 3.3.1 and 4.1. When the observations to be monitored are not univariate or independent so that resampling as described in Section 4.2 is needed for the estimation of the threshold functions, we essentially investigated how well the procedures hold their level depending on the underlying data generating mechanism. Although many other questions could be formulated given the complexity of the problem, the following experiments should allow the reader to grasp the main finite-sample properties of the studied procedures.

5.1 Monte Carlo estimation in the independent univariate case

As already discussed in Section 3.3.1, the estimation of the threshold functions when monitoring independent univariate observations can be made arbitrarily precise by increasing the number of Monte Carlo samples. We used the setting in our experiments and estimated all the rejection percentages from samples. The change-point detection procedures were always carried out at the nominal level.

| =0 | =0.25 | =0.5 | =0 | =0.25 | =0.5 | =0 | =0.25 | =0.5 | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 50 | 5.2 | 5.2 | 5.1 | 4.9 | 5.0 | 4.9 | 4.7 | 4.9 | 4.7 | 5.2 | 5.2 |

| 100 | 4.9 | 4.9 | 4.6 | 4.8 | 4.8 | 5.0 | 4.9 | 4.8 | 4.7 | 5.1 | 5.0 | |

| 2 | 50 | 4.9 | 5.1 | 5.0 | 4.8 | 5.2 | 5.1 | 4.9 | 4.9 | 4.9 | 5.1 | 4.4 |

| 100 | 4.9 | 4.8 | 4.9 | 4.9 | 4.7 | 4.9 | 4.9 | 4.8 | 5.1 | 5.0 | 4.6 | |

| 4 | 50 | 4.9 | 4.9 | 5.1 | 4.6 | 4.9 | 5.3 | 4.6 | 4.9 | 5.0 | 5.1 | 5.2 |

| 100 | 5.0 | 5.0 | 5.0 | 4.8 | 4.9 | 5.3 | 4.9 | 4.9 | 4.9 | 5.0 | 4.9 | |

| 10 | 50 | 5.2 | 5.1 | 5.0 | 4.9 | 4.9 | 5.2 | 4.6 | 4.7 | 5.0 | 5.0 | 4.8 |

| 100 | 5.0 | 5.1 | 5.1 | 4.9 | 4.9 | 5.1 | 5.0 | 5.1 | 5.0 | 4.9 | 4.6 | |

| 50 | 50 | 5.0 | 5.1 | 5.1 | 4.8 | 4.9 | 5.1 | 4.3 | 4.6 | 4.9 | 4.9 | 4.5 |

| 100 | 5.0 | 4.9 | 5.1 | 4.8 | 4.9 | 5.0 | 5.0 | 4.9 | 4.8 | 4.9 | 4.7 | |

5.1.1 Under the null

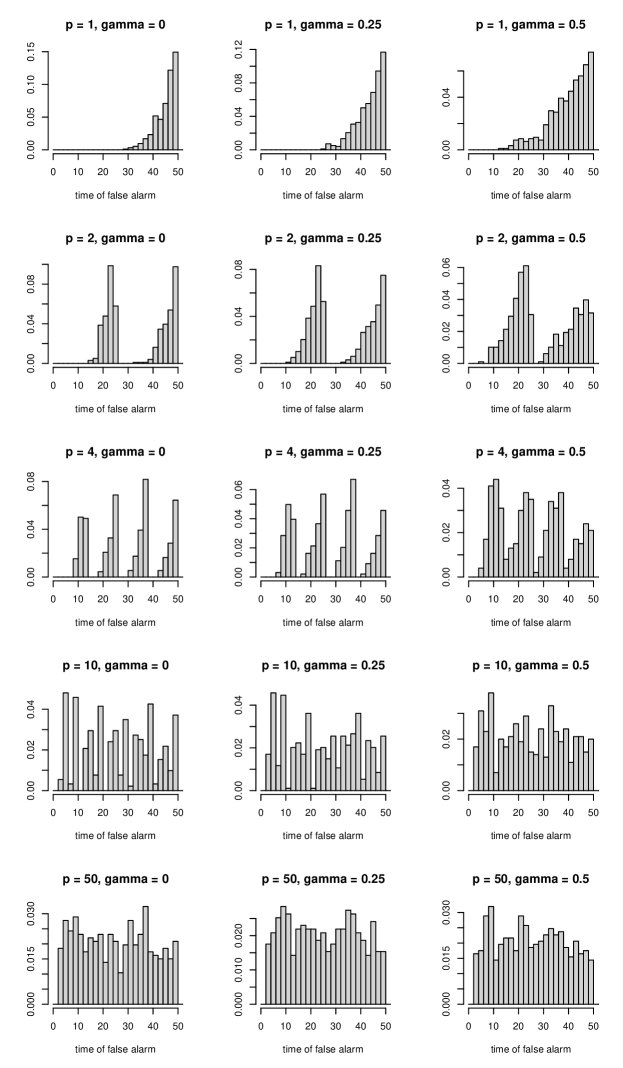

Unsurprisingly, all the studied tests were found to hold their level very well as can for instance be seen by inspecting the rejection percentages reported in Table 5.1. Furthermore, as could have been expected given the fact that the studied detector functions have a tendency to be increasing on average, it was observed that the setting resulted in a concentration of false alarms at the end of the monitoring period, while the larger , the more uniform the distribution of the false alarms over the monitoring period. These unsurprising findings are for instance illustrated in Figure 5.1 for the procedure based on in (2.3).

5.1.2 Change in mean

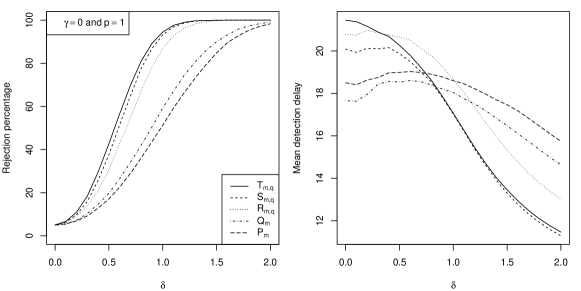

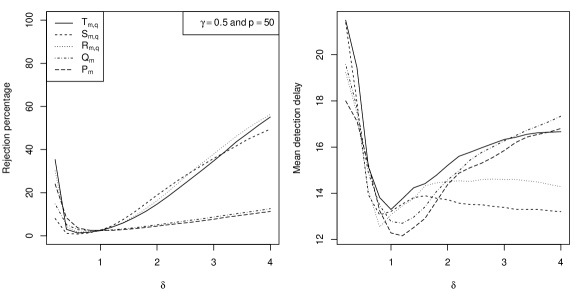

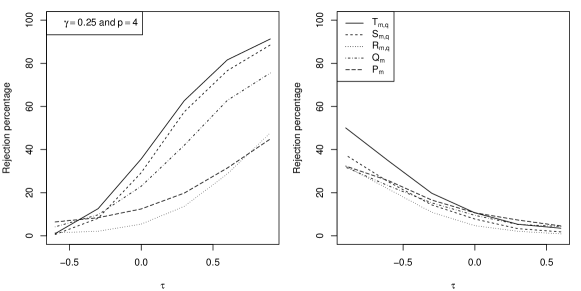

To answer the aforementioned questions related to the behavior of the procedures under in (1.3), we first considered a simple experiment consisting of a change in the expectation of a normal distribution. Specifically, , , , and in were taken equal to 50, 75, 100, the d.f. of the standard normal and the d.f. of the , respectively. The left graph in Figure 5.2 displays the estimated rejection percentages for the five detectors , , , and with in (2.4) set to zero and . The right graph represents the corresponding mean detection delays which were estimated only from the samples for which neither a false alarm was obtained (which occurs when the detector function becomes larger than the threshold function before the time of change ) nor the change was undetected (which occurs when the detector function remains below the threshold function during the entire monitoring period). Because the number of steps in the threshold function was set to , the left graph of Figure 5.2 is directly comparable with the top left graph given in Figure 1 of Dette and Gösmann (2019). An inspection of the latter seems to indicate that the powers of the procedures based on , and are not substantially different from those of the mean-specialized procedures considered in Section 5.1 of Dette and Gösmann (2019), even though the detectors , and are not specifically designed to be sensitive to changes in the expectation. The graphs are not substantially different for other values of and . Overall, the procedures based on , and were always observed to be more powerful and superior in terms of mean detection delay than those based on and . The latter is in full accordance with the empirical observations of Dette and Gösmann (2019) for more specialized procedures. Note that the procedure based on seems the most powerful for the alternative under consideration.

Figure 5.3 highlights the influence of the parameter in (2.4) on the rejection percentages and the mean detection delays of the procedure based on with . The graphs are very similar for other values of or for the procedures based on and . The conclusion is the same for all three procedures. For a change in expectation, while the parameter does not seem to affect the power of the procedures much, it has a clear influence on the mean detection delay: the greater , the shorter the mean detection delay. As we shall see, this behavior is not true for all types of alternatives.

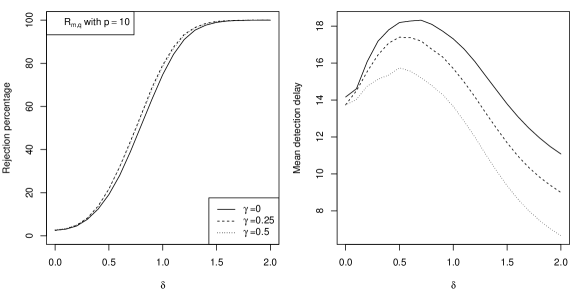

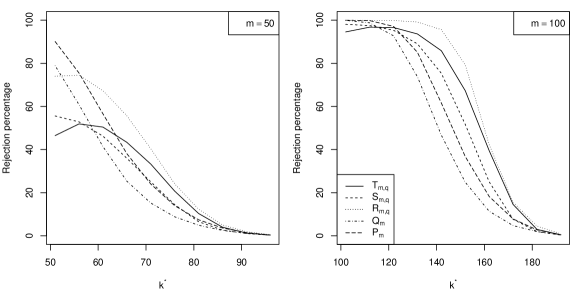

Figure 5.4 displays the influence of the number of steps of the threshold function on the rejection percentages and the mean detection delays of the procedure based on with . The graphs are not qualitatively different for other values of or for the procedures based on and . Overall, the procedures with have the highest rejection percentages. The latter is due to the fact that, because , detections occur mostly at the end of the monitoring period, and, at the end of the monitoring interval, by construction, the threshold functions for are below the corresponding threshold functions obtained for larger values of .

5.1.3 Change in variance

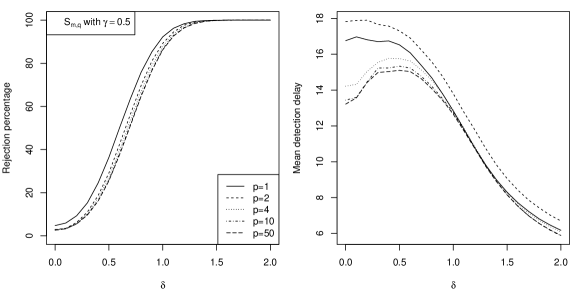

The setting is similar to that of the previous experiment except that, this time, it is the variance of the normal distribution that changes from 1 to . The left graph in Figure 5.5 displays the estimated rejection percentages for the procedures based on , , , and with and . The graph on the right represents the corresponding mean detection delays. Again, the procedures based on , and appear to be substantially more powerful and superior in terms of mean detection delay than those based on and . The conclusion remains true for all values of and . The influence of and is of the same nature as in the case of a change in mean: the greater , the shorter the mean detection delay and the lower , the higher the power.

5.1.4 Change in distribution

As a final experiment for independent univariate observations, we considered a change in distribution that keeps the expectation and the variance constant. Specifically, and in were taken equal to the d.f. of the and the d.f. of the Gamma distribution whose shape and rate parameters are both equal to 1/2, respectively. The parameter was taken to be in , was set to and the parameter to with .

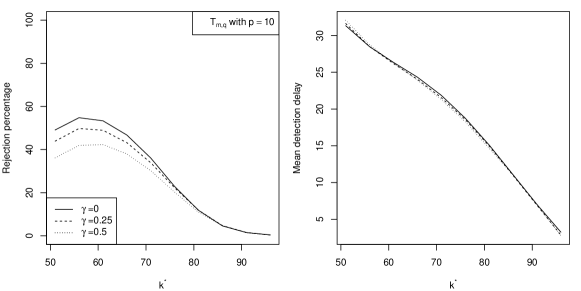

Figure 5.6 shows the rejection percentages of in (1.2) against for the procedures based on , , , and with and . The graphs for other values of and are very similar. As one can see, the procedures based on and appear to be the most powerful when the change occurs at the beginning of the monitoring period. The latter could have been expected from the definition of the underlying detectors and the simulation results of Dette and Gösmann (2019). As increases, the procedures based on and become more powerful.

Figure 5.7 displays the influence of the parameter on the rejection percentages of the procedure based on with . The graphs are not qualitatively different for other values of and or for the procedures based on and . As one can see, unlike for a change in expectation, has hardly no influence on the mean detection delay and it is the setting that leads to the highest rejection percentages.

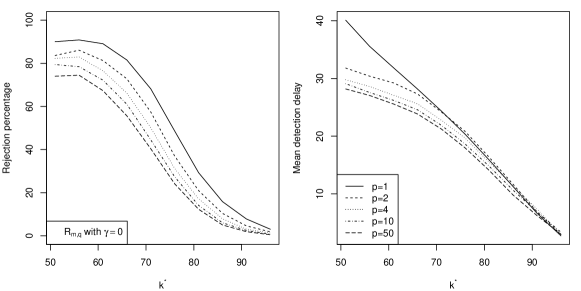

Finally, Figure 5.8 shows the influence of for the procedure based on with . The graphs are not qualitatively different for other values of or for the procedures based on and . As in previous experiments, the setting leads in the highest rejection percentages. However, when the change occurs in the first third of the monitoring period, the mean detection delay for is clearly substantially larger than for . Additional simulations show that the larger the monitoring period, the more pronounced this phenomenon.

5.2 Dependent multiplier bootstrap-based estimation in the time series case

The threshold function estimation approach based on the dependent multiplier bootstrap described in Section 4.2 can in principle be used as soon as the observations to be monitored are either multivariate or serially dependent. We used the setting in our experiments and estimated all the rejection percentages from 1000 samples at the nominal level.

| () | () | () | () | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| =1 | =2 | =4 | =1 | =2 | =4 | =1 | =2 | =4 | =1 | =2 | =4 | |||

| 0.0 | 0.00 | 50 | 4.4 | 6.0 | 5.4 | 6.6 | 5.9 | 5.8 | 3.6 | 3.7 | 2.9 | 5.2 | 4.9 | 4.4 |

| 100 | 5.6 | 5.2 | 4.9 | 7.3 | 7.6 | 6.4 | 6.2 | 6.1 | 6.1 | 6.2 | 5.8 | 7.2 | ||

| 200 | 6.1 | 5.2 | 5.5 | 5.1 | 5.1 | 6.1 | 5.1 | 5.3 | 6.2 | 6.9 | 6.2 | 5.2 | ||

| 400 | 5.5 | 5.9 | 5.3 | 7.5 | 6.9 | 7.1 | ||||||||

| 0.25 | 50 | 4.1 | 5.0 | 4.6 | 5.5 | 4.9 | 4.9 | 3.4 | 4.1 | 3.0 | 6.1 | 5.1 | 4.2 | |

| 100 | 5.0 | 4.6 | 4.3 | 6.5 | 6.2 | 6.1 | 6.2 | 5.6 | 5.8 | 6.2 | 5.8 | 6.7 | ||

| 200 | 5.5 | 5.5 | 5.0 | 5.0 | 4.3 | 5.4 | 5.0 | 5.3 | 5.9 | 6.7 | 5.9 | 5.3 | ||

| 400 | 4.8 | 5.9 | 4.9 | 7.3 | 6.7 | 6.2 | ||||||||

| 0.50 | 50 | 2.8 | 3.1 | 2.7 | 3.6 | 2.5 | 2.9 | 2.9 | 2.5 | 3.0 | 5.1 | 3.2 | 3.3 | |

| 100 | 3.7 | 2.7 | 3.2 | 4.6 | 4.3 | 4.6 | 5.3 | 4.2 | 4.3 | 5.1 | 4.9 | 4.9 | ||

| 200 | 3.9 | 3.0 | 3.1 | 3.6 | 2.6 | 3.4 | 4.2 | 4.7 | 4.6 | 5.9 | 4.8 | 3.6 | ||

| 400 | 3.7 | 3.6 | 3.2 | 6.2 | 5.7 | 4.6 | ||||||||

| 0.1 | 0.00 | 50 | 4.3 | 4.8 | 6.7 | 7.3 | 8.1 | 9.2 | 4.3 | 4.9 | 3.8 | 4.6 | 5.6 | 4.3 |

| 100 | 5.4 | 6.2 | 7.4 | 6.5 | 7.8 | 7.6 | 6.2 | 5.8 | 6.1 | 7.9 | 6.1 | 7.5 | ||

| 200 | 6.5 | 7.0 | 7.5 | 6.2 | 6.9 | 7.9 | 6.3 | 6.7 | 6.4 | 7.4 | 8.4 | 8.6 | ||

| 400 | 6.1 | 5.7 | 7.1 | 5.3 | 5.7 | 6.4 | ||||||||

| 0.25 | 50 | 3.6 | 4.0 | 4.7 | 7.2 | 7.1 | 7.2 | 4.4 | 5.4 | 4.3 | 5.0 | 5.9 | 4.4 | |

| 100 | 5.4 | 5.6 | 6.1 | 5.5 | 6.9 | 6.5 | 6.0 | 5.2 | 4.9 | 7.7 | 5.8 | 7.0 | ||

| 200 | 5.9 | 6.0 | 6.5 | 5.7 | 7.2 | 7.2 | 6.4 | 6.9 | 6.6 | 7.5 | 8.2 | 8.6 | ||

| 400 | 5.8 | 6.0 | 6.6 | 5.6 | 5.0 | 6.3 | ||||||||

| 0.50 | 50 | 2.7 | 2.5 | 2.9 | 5.0 | 5.0 | 4.9 | 4.0 | 4.4 | 4.5 | 4.1 | 4.6 | 3.5 | |

| 100 | 3.6 | 3.4 | 3.8 | 4.9 | 4.9 | 4.6 | 4.9 | 3.9 | 3.5 | 6.6 | 4.7 | 5.5 | ||

| 200 | 3.7 | 3.7 | 3.9 | 5.3 | 5.2 | 5.1 | 5.8 | 5.8 | 5.8 | 7.0 | 6.9 | 6.5 | ||

| 400 | 4.8 | 4.7 | 4.2 | 4.5 | 4.0 | 4.7 | ||||||||

| 0.3 | 0.00 | 50 | 9.3 | 9.3 | 10.0 | 10.8 | 11.7 | 12.9 | 6.4 | 6.5 | 6.5 | 5.9 | 6.9 | 6.2 |

| 100 | 8.4 | 10.1 | 10.2 | 8.3 | 9.5 | 11.1 | 7.4 | 7.6 | 8.3 | 7.7 | 8.8 | 10.2 | ||

| 200 | 7.4 | 7.7 | 8.5 | 7.0 | 8.0 | 10.1 | 7.2 | 6.8 | 8.9 | 7.1 | 8.6 | 8.9 | ||

| 400 | 5.7 | 7.7 | 8.4 | 7.0 | 8.1 | 8.5 | ||||||||

| 0.25 | 50 | 8.9 | 8.4 | 9.0 | 10.2 | 11.0 | 12.0 | 7.1 | 7.2 | 7.1 | 6.3 | 7.1 | 7.8 | |

| 100 | 8.3 | 9.3 | 9.8 | 8.3 | 9.5 | 10.3 | 7.5 | 7.7 | 8.1 | 7.8 | 9.2 | 10.3 | ||

| 200 | 7.1 | 6.7 | 7.6 | 7.3 | 8.0 | 10.2 | 7.3 | 6.6 | 9.0 | 7.2 | 8.8 | 9.6 | ||

| 400 | 5.9 | 6.8 | 7.6 | 7.1 | 7.9 | 7.8 | ||||||||

| 0.50 | 50 | 5.7 | 6.0 | 6.5 | 9.3 | 9.1 | 10.2 | 7.4 | 6.5 | 6.6 | 6.5 | 7.6 | 8.0 | |

| 100 | 6.1 | 6.4 | 8.4 | 7.7 | 6.2 | 7.7 | 6.7 | 7.5 | 7.2 | 6.6 | 7.8 | 8.1 | ||

| 200 | 5.0 | 4.9 | 5.1 | 6.3 | 6.4 | 8.1 | 6.4 | 5.3 | 6.9 | 6.0 | 6.2 | 7.9 | ||

| 400 | 4.2 | 5.3 | 4.6 | 5.9 | 5.9 | 5.5 | ||||||||

| 0.5 | 0.00 | 50 | 9.6 | 11.7 | 13.5 | 12.8 | 13.2 | 17.3 | 9.8 | 9.8 | 9.1 | 8.5 | 11.7 | 11.7 |

| 100 | 9.6 | 12.2 | 13.4 | 11.5 | 14.0 | 14.7 | 9.7 | 9.8 | 13.4 | 11.4 | 12.3 | 14.0 | ||

| 200 | 8.6 | 10.0 | 12.4 | 7.5 | 8.7 | 10.9 | 8.2 | 10.5 | 11.1 | 8.4 | 9.1 | 10.5 | ||

| 400 | 7.5 | 8.9 | 11.3 | 5.7 | 7.5 | 9.4 | ||||||||

| 0.25 | 50 | 9.6 | 11.5 | 12.4 | 12.5 | 13.3 | 16.6 | 10.3 | 10.8 | 10.7 | 9.6 | 12.7 | 13.1 | |

| 100 | 9.2 | 11.0 | 12.2 | 11.3 | 13.4 | 14.0 | 10.2 | 10.2 | 13.4 | 11.5 | 12.3 | 14.3 | ||

| 200 | 7.9 | 9.7 | 11.1 | 6.8 | 7.8 | 10.1 | 8.7 | 10.4 | 11.5 | 8.4 | 9.4 | 10.8 | ||

| 400 | 6.7 | 8.0 | 10.6 | 5.6 | 7.7 | 8.8 | ||||||||

| 0.50 | 50 | 7.7 | 9.6 | 10.2 | 10.9 | 10.9 | 15.1 | 9.7 | 10.3 | 10.5 | 9.7 | 12.3 | 13.5 | |

| 100 | 6.8 | 7.6 | 9.8 | 9.5 | 9.8 | 11.4 | 8.2 | 9.7 | 12.4 | 10.2 | 11.1 | 12.0 | ||

| 200 | 5.8 | 6.8 | 8.7 | 6.1 | 5.8 | 7.1 | 7.5 | 8.5 | 9.7 | 7.6 | 8.6 | 9.7 | ||

| 400 | 5.2 | 6.2 | 7.4 | 4.8 | 5.3 | 6.5 | ||||||||

5.2.1 Under the null

One of the most important practical aspects is to assess how well the procedures hold their level when based on the dependent multiplier bootstrap. To attempt to answer this question, we conducted extensive simulations in the univariate case. For and , we generated samples of size from an AR(1) model with normal innovations and autoregressive parameter , and estimated the levels of the procedures based on , and with and . The rejection percentages of in (1.1) for are given in Table 5.2 (the missing entries in the table correspond to parameter settings for which computations took too long given our computer cluster resources). As one can see, unsurprisingly, the larger , the more liberal the procedure based on tends to be. This phenomenon is particularly visible for . Reassuringly however, for a given , , and , the estimated levels seem to get closer to the 5% nominal level as increases. Hence, unsurprisingly, the stronger the serial dependence, the larger needs to be so that the procedure can be expected to hold its nominal level. For in particular and keeping , and fixed, we also see that the larger , the more liberal the procedure based on tends to be. The latter could be explained by the fact that, as increases, more thresholds need to be estimated, and that, except for the first, all the estimated thresholds are conditional empirical quantiles: the precision of the estimation of a threshold thus critically depends on the precision of the previously estimated thresholds with respect to which conditioning is performed. In other words, the fact that the empirical levels tend to become higher when increases could be explained by an error propagation effect. Finally, for , , and fixed, we also see that the larger , the lower the rejection percentages tend to be. Overall, for , the procedure based on holds its level best for .

The conclusions for the procedures based on and are very similar, with the exception that the effect of seems “stronger”: while the empirical levels are better for than for , the procedures become way too conservative for . The latter effect might be due to the fact the detectors and involve maxima (unlike which involves means) and to our too low setting of the constant in the definition of the weight function (2.4). The latter was arbitrarily set to (and had de facto no effect in our Monte Carlo experiments given the values of that we considered).

| () | () | () | () | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| =1 | =2 | =4 | =1 | =2 | =4 | =1 | =2 | =4 | =1 | =2 | =4 | ||

| 0.00 | 50 | 5.4 | 5.4 | 4.9 | 9.1 | 7.6 | 7.6 | 4.8 | 4.7 | 4.0 | 5.4 | 6.3 | 5.3 |

| 100 | 6.6 | 7.5 | 7.6 | 7.9 | 8.6 | 7.2 | 9.6 | 8.4 | 9.2 | 10.5 | 10.3 | 10.0 | |

| 200 | 7.4 | 7.2 | 8.6 | 8.3 | 8.4 | 8.5 | 6.6 | 7.7 | 6.1 | 8.7 | 8.0 | 8.2 | |

| 400 | 6.7 | 7.5 | 8.4 | 7.0 | 7.0 | 8.4 | |||||||

| 0.25 | 50 | 4.7 | 4.2 | 4.3 | 7.5 | 5.9 | 5.6 | 4.8 | 4.5 | 4.2 | 5.8 | 6.4 | 5.9 |

| 100 | 5.9 | 6.3 | 6.3 | 7.2 | 6.9 | 6.7 | 9.6 | 8.8 | 8.4 | 10.2 | 9.8 | 9.2 | |

| 200 | 7.0 | 6.9 | 7.8 | 7.2 | 7.3 | 8.2 | 6.4 | 6.9 | 5.9 | 8.3 | 7.6 | 8.4 | |

| 400 | 6.2 | 7.9 | 7.9 | 6.9 | 6.7 | 8.4 | |||||||

| 0.50 | 50 | 2.4 | 2.5 | 2.6 | 4.4 | 3.9 | 4.2 | 4.0 | 3.9 | 3.5 | 5.0 | 4.7 | 4.6 |

| 100 | 4.1 | 4.2 | 4.5 | 5.0 | 4.1 | 3.9 | 6.6 | 5.9 | 6.0 | 7.9 | 7.5 | 7.0 | |

| 200 | 4.9 | 5.0 | 5.2 | 5.7 | 4.8 | 5.7 | 5.8 | 5.1 | 4.9 | 6.8 | 6.6 | 7.1 | |

| 400 | 5.1 | 5.4 | 5.1 | 6.3 | 5.9 | 5.9 | |||||||

A similar experiment was conducted by generating samples from a GARCH(1,1) model with parameters , and to mimic SP500 daily log-returns following Jondeau, Poon and Rockinger (2007). The empirical levels for the procedure based on are reported in Table 5.3 and appear to be closest to the 5% nominal overall when .

| =1 | =2 | =4 | =1 | =2 | =4 | =1 | =2 | =4 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| -0.6 | 50 | 3.1 | 1.9 | 1.5 | 2.4 | 1.1 | 1.1 | 0.7 | 0.3 | 0.8 |

| 100 | 3.5 | 2.9 | 2.2 | 2.5 | 2.1 | 1.7 | 1.2 | 1.0 | 0.9 | |

| 200 | 4.0 | 3.2 | 3.1 | 3.0 | 2.4 | 2.1 | 0.9 | 1.0 | 1.0 | |

| -0.3 | 50 | 4.5 | 2.9 | 2.7 | 3.4 | 2.5 | 2.5 | 1.8 | 1.5 | 1.2 |

| 100 | 4.0 | 4.0 | 3.8 | 3.1 | 3.0 | 2.9 | 1.5 | 0.9 | 1.4 | |

| 200 | 4.8 | 4.1 | 4.0 | 4.1 | 3.3 | 2.9 | 1.6 | 1.6 | 1.6 | |

| 0.0 | 50 | 5.1 | 4.3 | 4.7 | 4.2 | 3.9 | 3.6 | 2.7 | 2.0 | 2.3 |

| 100 | 7.0 | 5.8 | 4.7 | 5.7 | 4.7 | 3.7 | 2.6 | 2.2 | 2.0 | |

| 200 | 6.0 | 6.2 | 5.8 | 5.3 | 5.0 | 5.2 | 3.3 | 2.4 | 2.3 | |

| 0.3 | 50 | 6.1 | 4.5 | 4.5 | 4.7 | 3.8 | 3.3 | 2.5 | 2.4 | 2.6 |

| 100 | 5.0 | 5.5 | 4.9 | 4.4 | 4.8 | 3.9 | 2.3 | 2.5 | 2.5 | |

| 200 | 6.2 | 6.3 | 7.8 | 6.0 | 4.8 | 6.3 | 3.4 | 2.6 | 3.8 | |

| 0.6 | 50 | 6.7 | 5.5 | 5.8 | 5.8 | 3.9 | 4.2 | 3.2 | 2.6 | 2.5 |

| 100 | 7.7 | 7.6 | 7.8 | 7.0 | 6.6 | 7.0 | 4.3 | 4.0 | 4.8 | |

| 200 | 5.4 | 6.2 | 7.2 | 5.1 | 5.6 | 6.1 | 3.4 | 3.5 | 3.2 | |

Finally, a bivariate experiment with independent observations consisting of generating samples of size for from a normal copula with a Kendall’s tau of was carried out. The empirical levels for the procedure based on are reported in Table 5.4. The effect of appears as in the previous experiments. For fixed and , it can also be observed that the procedure has a tendency of being too conservative in the case of strong negative dependence but, reassuringly, the agreement with the 5% nominal level seems to improve as increases.

5.2.2 Change in the copula parameter

To grasp further the finite-sample behavior of the procedures in the case of bivariate independent observations, we simulated a change in the parameter of a normal copula. The left (resp. right) graph in Figure 5.9 displays the estimated rejection probabilities of in (1.2) for the procedures based on , , , and with and under in (1.3) with , , , the bivariate normal copula with a Kendall’s tau of -0.6 (resp. 0.6) and the bivariate normal copula with a Kendall’s tau of (resp. ). As one can notice, the procedure based on (resp. ) is always among the most (resp. least) powerful ones. Graphs for other values of and are not qualitatively different. As for all previous experiments, we observed that the smaller , the more powerful the procedures. For this experiment, the parameter appeared to have a rather small impact on the rejection percentages of .

6 Data examples

To illustrate the use of the proposed sequential change-point detection tests, we considered two fictitious scenarios, the first (resp. second) of a univariate (resp. bivariate) nature based on closing quotes of the NASDAQ composite index (resp. Microsoft and Intel stocks) for the period 2019-01-02 – 2020-04-11. The latter were obtained using the get.hist.quote() function of the tseries R package (Trapletti and Hornik, 2019). In both scenarios, it was assumed that, on the last day of 2019, one wished to monitor the (univariate or bivariate) daily log-returns for a change in contemporary distribution possibly using the stretch of (univariate of bivariate) log-returns of 2019 as learning sample. The latter decision was confirmed after the tests of Bücher, Fermanian and Kojadinovic (2019) implemented in the functions stDistAutocop() and cpDist() of the npcp R package (Kojadinovic, 2020) provided no evidence against stationarity for the two candidate learning samples. Notice that, unsurprisingly, the rank-based test of serial independence of Genest and Rémillard (2004) implemented in the function serialIndepTest() of the copula R package (Hofert et al., 2018) provided weak evidence against the serial independence of the squared component time series.

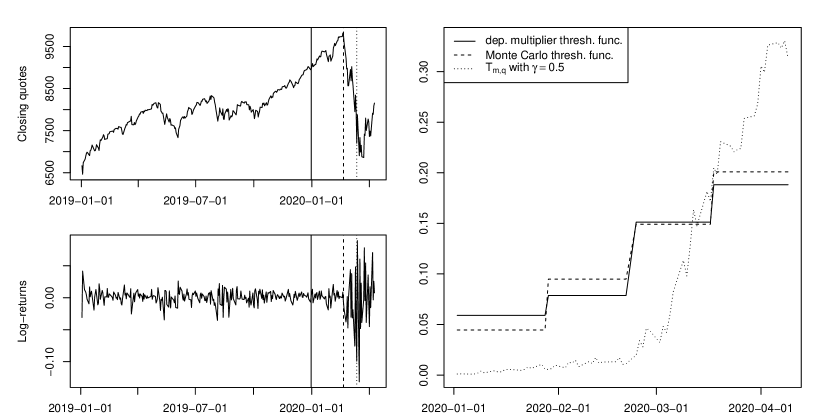

The closing quotes and corresponding daily log-returns of the NASDAQ composite index are represented in the left panel of Figure 6.1. The solid vertical lines mark the beginning of the monitoring. The dotted line in the right panel represents the detector function based on with . The latter was chosen given its overall good performance in our Monte Carlo experiments, both in terms of empirical level, power and mean detection delay. In the right panel, the solid line represents the threshold function with steps estimated using the dependent multiplier bootstrap with , while the dashed line represents the threshold function with steps estimated using Monte Carlo with . Note that the latter did not at all use the learning sample as it is computed under the assumption that the observations are serially independent. The relative proximity of the two threshold functions could be explained by the fact that, although present, serial dependence in the learning sample is probably very weak. The detector function exceeded the two threshold functions at the same date (2020-03-12), which is marked by the dotted vertical line in the left panel of Figure 6.1 and corresponds to the 49th daily log-return of 2020. Given the definition of in (2.6) and having that of in (2.5) in mind, a possible estimate of a point of change for an exceedance at position is given by

| (6.1) |

which returned 286 and corresponds to the date 2020-02-21. The latter is marked by a dashed vertical line in the left panel of Figure 6.1 and corresponds to the beginning of the sharp decrease of the NASDAQ composite index as a consequence of the Covid-19 pandemic.

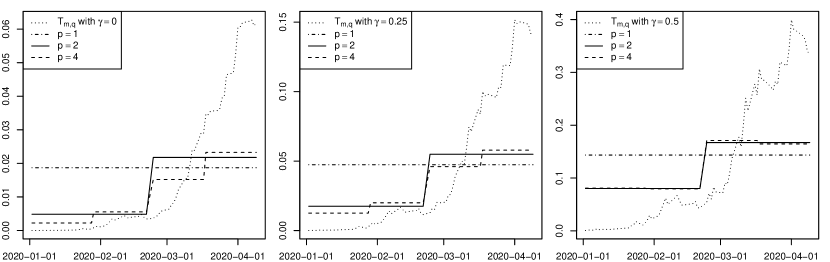

Figure 6.2 describes the monitoring of the bivariate daily log-returns of the Microsoft and Intel stocks using the procedure based on with and a threshold function with steps estimated using the dependent multiplier bootstrap. All the dates of exceedance are between the 2020-03-12 ( and ) and the 2020-03-09 ( and ). The estimated dates of change turn out not to depend on and are the 2020-01-25 for , the 2020-02-15 for and the 2020-02-20 for . This effect of on (6.1) was to be expected: larger values of give more weight to potential break points close to .

7 Concluding remarks

In the context of closed-end sequential change-point detection, it can be argued (see Anatolyev and Kosenok, 2018) that it is desirable that the underlying threshold function is such that the probability of false alarm remains approximately constant over the monitoring period. In this work, the asymptotic validity of the bootstrap-based estimation of such a threshold function was established for generic detectors. The latter was applied to sequential change-point tests involving detectors based on differences of empirical d.f.s that can be either simulated or resampled using a dependent multiplier bootstrap depending on whether univariate independent or multivariate serially dependent observations are monitored. The proposed detectors are adaptations of statistics used in a posteriori change-point testing and include a weight function in the spirit of Csörgő and Szyszkowicz (1994a) that can be used to give more importance to recent observations.

Extensive Monte Carlo experiments were used to investigate the finite-sample properties of the resulting sequential change-point tests. Among the proposed detectors, none led to a uniformly better testing procedure. When based on the dependent multiplier bootstrap, the procedure based on in (2.6) was observed to have the best behavior, overall, in terms of empirical level, power and mean detection delay. In the case of univariate independent observations, when the threshold function can be estimated using Monte Carlo simulation, the number of step of the threshold function can be chosen as large as the number of monitoring steps. However, in the time series case, when the estimation of the threshold function is based on the dependent multiplier bootstrap, should not be taken too large because of an error propagation effect.

As already hinted at in Section 3, a straightforward extension of the generic results on the estimation of the threshold function consists of allowing the conditional probability in (3.5) to change with the underlying monitoring sub-interval (or, equivalently, to have monitoring sub-intervals of different lengths). The choice of the conditional probabilities (or, equivalently, of the monitoring sub-intervals) could for instance be carried out according to the user’s prior knowledge. In future work, we also plan to investigate the validity of additional bootstraps for monitoring multivariate time series. The current and future theoretical results would further need to be complemented by additional Monte Carlo simulations, involving in particular multivariate experiments. Such finite-sample investigations are however a real computational challenge given the complexity and cost of execution of such change-point detection procedures.

Appendix A Proofs of Propositions 2.5 and 2.7

Proof of Proposition 2.5.

From Theorem 1 of Bücher (2015), we have that in , where . Let be the map from to defined, for any , by

| (A.1) |

It is straightforward to verify that is a continuous map which immediately implies by the continuous mapping theorem that in . Furthermore, it is easy to check that and that is a tight centered Gaussian process such that, for any and ,

where is defined in (2.23). It follows that in .

It remains to show the subsequent claims. Under , (2.22) holds and the continuous mapping theorem immediately implies that in and, then, that in since , the function in (2.4) is continuous on and . The continuous mapping theorem further straightforwardly implies that in .

Let for any . In order to prove that and in , we shall first prove that in , where for any .

We start by showing that the finite-dimensional distributions of converge weakly to those of . Let , , and be arbitrary. The result is proven if we show that

| (A.2) |

From the already proven weak convergence of to in , we obtain that

since and . From the fact that in , we then have that

in . The latter can be combined with the fact that is continuous, has continuous sample paths with probability one, Lemma 1 in Kojadinovic, Segers and Yan (2011) and the continuous mapping theorem to obtain (A.2).

It remains to show that the process is asymptotically tight (see, e.g., van der Vaart and Wellner, 2000, Section 1.5). From Section 2.1.2 and Problem 2.1.5 in the same reference, the latter is shown if, for every sequence ,

| (A.3) |

The supremum on the left-hand side of the previous display is smaller than , where

Now,

by the asymptotic uniform equicontinuity in probability of . Concerning , we have

since for all ,

and the fact that converges weakly by the continuous mapping theorem. Hence, (A.3) holds and therefore in . The fact that and in is finally and again an immediate consequence of the continuous mapping theorem.

Finally, we have to show that, for any such that , the distributions of , and are absolutely continuous with respect to the Lebesgue measure. To show the latter, we adapt the proof of Proposition 3.3 of Bücher, Fermanian and Kojadinovic (2019) to the current setting. Let denote the space of all continuous real-valued functions on equipped with the uniform metric. Since the sample paths of are elements of with probability one and in (2.4) is continuous, the sample paths of are elements of with probability one. Fix such that and let , and be the maps from to defined, for any , by

Then, we have that , and and, to show the desired result, it suffices to prove that the distributions of , and , denoted respectively by , and , are absolutely continuous with respect to the Lebesgue measure. Since the maps , and are continuous and convex, from Theorem 7.1 in Davydov and Lifshits (1984), we obtain that, for any , is concentrated on and absolutely continuous on , where

By Lemma 1.2 (e) in Dereich et al. (2003), we have that, for any , . Hence, for any ,

It follows that, for any and any , there exists functions in the support of such that , which implies that .

To conclude, it remains to show that , and have no atom at 0. For any , we have that if and only if for all and all in the support of the distribution induced by . Let be an arbitrary point in the latter support such that , where is defined in (2.23), and let such that . Then, , which implies that . The proof is complete since

∎

Proof of Proposition 2.7.

Let , , . The first claim is proven if

| (A.4) |

The supremum on the left-hand side of the previous display is equal to

| (A.5) |

To prove (A.4), we shall show that each of the three suprema in the previous display converge in probability to zero. Notice first that

| (A.6) |

Furthermore, for any , and , let

where , is defined in (2.14) and is generically defined by (2.1). By proceeding as in Section 2.2, it can be verified that, under in (1.1), for all and , where is defined in (2.21) and . By the continuous mapping theorem, it thus immediately follows that, under , converges weakly in to a tight limit. Some thought then reveals that, under the conditions of the proposition, (resp. ) converges weakly in (resp. in ) to a tight limit.

From the expression of given in (A.6), for the first supremum in (A.5), we obtain that

since converges weakly in to a tight limit as a consequence of the fact that, for any and , and the continuous mapping theorem.

Regarding the second supremum, for any and , we have that

Thus, on one hand,

On the other hand, from (A.6) and using the fact that ,

By the triangle inequality and using the fact that , it then follows that

Similarly, for the third supremum, for any and ,

and, hence, on one hand, for any and ,

while, on the other hand,

Finally, by the triangle inequality,

which completes the proof of (A.4).

Using the fact that , the function in (2.4) is continuous on and , we obtain, from the continuous mapping theorem, that in . From (2.3) and (2.26), and proceeding as in (2.17), it is easy to verify that , . Hence, again by the continuous mapping theorem, in , where , and, thus, . Since

we immediately obtain that .

To show the two last remaining claims, we shall first prove that

| (A.7) |

where, for any and ,

| (A.8) |

By the triangle inequality, the supremum on the left hand-side of (A.7) is smaller than , where

and

On one hand, some thought reveals that

as a consequence of the continuous mapping theorem. On the other hand, from (2.27), we have that

Using (A.8), the second supremum on the right-hand side of the previous display is smaller than , where

From the assumptions on the strong mixing coefficients and Theorem 1.2 in Berbee (1987) (see also Rio, 2017, Chapter 3), the strong law of large numbers implies that, as ,

where the arrow ‘’ denotes almost sure convergence. Since the previous convergence is equivalent to the fact that almost surely, we obtain that . Using the fact that, for any and ,

and that , we obtain that

The first term on the right-hand side of the previous display is equal to and thus converges to zero almost surely. The second term can be written as

| (A.9) |

Letting

and decomposing the sum in (A.9), by the triangle inequality, (A.9) is smaller than

since as .

Hence, . It follows that (A.7) is proven and, from the continuous mapping theorem, we immediately obtain that and in , where

and then that

Let and . Since and are continuous and , and . As a consequence, for all ,

Furthermore, since for all and since, for all ,

we have, from the continuity of , and , that

and

∎

Appendix B Auxiliary lemmas for the proof of Theorem 3.3

This section, which is, to a large extent, notationally independent of the rest of the paper, provides the proofs of two lemmas, possibly of independent interest, necessary for showing Theorem 3.3.

Let denote available data. No assumptions are made on apart from measurability. To fix ideas, one can think of as a sequence of multivariate serially dependent random vectors. Let be a -valued statistic such that as , where the random vector is assumed to have a continuous d.f. We additionally suppose that we have available bootstrap replicates of , where the , , are -dimensional independent and identically distributed random vectors representing the additional sources of randomness involved in the underlying bootstrap mechanism. We shall further assume that, as ,

| (B.1) |

in , where and are independent copies of . Note that, from Lemma 2.2 of Bücher and Kojadinovic (2019), (B.1) is equivalent to the usual conditional bootstrap consistency statement, that is,

Before stating and proving the two lemmas, we introduce some additional notation and list useful results. For any , , and , let

Since in as and has a continuous d.f., we have from Lemma 2.11 of van der Vaart (1998) that, for any and , as ,

| (B.2) |

Proceeding as in the proof of the aforementioned lemma, it can actually also be shown that, for any and , as ,

| (B.3) |

Combining (B.1) with Assertion (f) of Lemma 2.2 in Bücher and Kojadinovic (2019) and (B.2), we further obtain that, for any and , as ,

| (B.4) |

Let be arbitrary. The following notation will also be used in the lemmas. Let

and, recursively, for successively equal to ,

| (B.5) |

Similarly, let

and, recursively, for successively equal to ,

| (B.6) |

The following two lemmas are instrumental for proving Theorem 3.3.

Lemma B.1.

Lemma B.2.

Let be a -valued statistic such that as . Then

Proof of Lemma B.1.

The claims in (B.7) and (B.8) are immediate consequences of (B.4) and Lemma 4.2 in Bücher and Kojadinovic (2019), respectively. The claim (B.9) follows from the fact that , the triangle inequality, (B.2) and (B.8).

Proof of (B.10), (B.11) and (B.12) for j=2: By the triangle inequality, is smaller than

The first term converges in probability to zero by (B.4) as . The second term converges to zero by (B.2) as . The third term converges to zero as a consequence of (B.8) since . Hence, as . From (B.5) and (B.6), the latter implies that to prove that as , it suffices to prove that

as . From the triangle inequality, (B.2) and (B.4), the latter will hold if

| (B.13) |

as . For any , we have

| (B.14) |

Hence, by the triangle inequality,

| (B.15) |

From the triangle inequality, (B.2) and (B.3), we obtain that the last supremum on the right-hand side of the previous display converges to zero a since has a continuous d.f. Hence, to show (B.13), it remains to show that the first supremum on the right converges to zero in probability as . From the right-continuity of and , we obtain that, for any ,

Furthermore, using the fact that, for any and ,

| (B.16) |

we obtain that, for any ,

| (B.17) |

By the continuous mapping theorem and the Portmanteau theorem, the first probability on the right converges to as and can be made arbitrarily small by decreasing . The second probability converges to zero as by (B.7) for any . Hence, (B.13) holds and so does (B.10) for .

Let us now prove (B.11) for . Since, from (B.8), , as , it remains to show that

as . From the triangle inequality and (B.2), if suffices to prove that, as ,

The term on the left-hand side of the previous display is smaller than

The first difference between absolute values is smaller than (B.15), which was already shown to converge to zero as . Proceeding as in (B.14), to show that the second difference between absolute values converges to zero as , it suffices to prove that

as . Using again (B.16) and proceeding as in (B.17), the probability on the left can be shown to be smaller than

for any . Using the continuity of and the Portmanteau theorem, the first probability converges as to a probability that can be made arbitrarily small by decreasing . The second probability converges to zero as for any by (B.10) for , which was proven previously.

It remains to prove (B.12) for . From the triangle inequality, (B.2) and (B.13), we have that, as ,

Starting from (B.11) for , the desired result follows from the convergence in the previous display and (B.8).

Proof of (B.10), (B.11) and (B.12) for all : As mentioned previously, we proceed by induction. Let , assume that (B.10), (B.11) and (B.12) hold for all and let us show that they also hold for .

For any , let , and, for successively equal to , let

Then, from the induction hypothesis for (B.11), as ,

| (B.18) |

Thus, from (B.4), as , . Hence, to show (B.10) for , it suffices to prove that, as ,

From the triangle inequality, (B.2) and (B.4), the latter will hold if, as ,

| (B.19) |

For any , is smaller than the following sum of terms:

Proceeding as in (B.14), (B.15) and (B.17), the th term, , can be shown to converge to zero as as a consequence of the fact that

converges to zero as followed by using the continuity of and the induction hypothesis. Hence, (B.19) holds.

Let us now show (B.11) for . From (B.18), it suffices to prove that, as ,

From the triangle inequality and (B.2), the latter will hold if, as ,

The difference between absolute values on the left of the previous display is smaller than

The first term converges to zero in probability as as a consequence of (B.19). Proceeding as in (B.14), (B.15) and (B.17), the second term can be shown to converge to zero as as a consequence of the fact that

converges to zero as followed by using the continuity of and the already proven claim (B.10) for .

Proof of Lemma B.2.

Let . Then,