2020 \setcopyrightacmlicensed\acmConference[EC ’20]Proceedings of the 21st ACM Conference on Economics and ComputationJuly 13–17, 2020Virtual Event, Hungary \acmBooktitleProceedings of the 21st ACM Conference on Economics and Computation (EC ’20), July 13–17, 2020, Virtual Event, Hungary \acmPrice15.00 \acmDOI10.1145/3391403.3399533 \acmISBN978-1-4503-7975-5/20/07 \settopmatterprintacmref=true \orcid0000-0003-3205-2457

Continuous Credit Networks and Layer 2 Blockchains: Monotonicity and Sampling

Abstract.

To improve transaction rates, many cryptocurrencies have implemented so-called “Layer-2” transaction protocols, where payments are routed across networks of private payment channels. However, for a given transaction, not every network state provides a feasible route to perform the payment; in this case, the transaction must be put on the public ledger. The payment channel network thus multiplies the transaction rate of the overall system; the less frequently it fails, the higher the multiplier.

We build on earlier work on credit networks and show that this network liquidity problem is connected to the combinatorics of graphical matroids. Earlier work could only analyze the (unnatural) scenario where transactions had discrete sizes. In this work, we give an analytical framework that removes this assumption. This enables meaningful liquidity analysis for real-world parameter regimes.

Superficially, it might seem like the continuous case would be harder to examine. However, removing this assumption lets us make progress in two important directions. First, we give a partial answer to the “monotonicity conjecture” that previous work left open. This conjecture asks that the network’s performance not degrade as capacity on any edge increases. And second, we construct here a network state sampling procedure with much faster asymptotic performance than off-the-shelf Markov chains (, where is the complexity of solving a linear program on constraints.)

We obtain our results by mapping the underlying graphs to convex bodies and then showing that the liquidity and sampling problems reduce to bounding and computing the volumes of these bodies. The transformation relies crucially on the combinatorial properties of the underlying graphic matroid, as do the proofs of monotonicity and fast sampling.

Key words and phrases:

Credit Networks; Monotonicity<ccs2012> <concept> <concept_id>10010405.10003550.10003554</concept_id> <concept_desc>Applied computing Electronic funds transfer</concept_desc> <concept_significance>500</concept_significance> </concept> <concept> <concept_id>10010405.10003550.10003551</concept_id> <concept_desc>Applied computing Digital cash</concept_desc> <concept_significance>300</concept_significance> </concept> <concept> <concept_id>10002950.10003624.10003633.10003644</concept_id> <concept_desc>Mathematics of computing Network flows</concept_desc> <concept_significance>100</concept_significance> </concept> </ccs2012> \ccsdesc[500]Applied computing Electronic funds transfer \ccsdesc[300]Applied computing Digital cash \ccsdesc[100]Mathematics of computing Network flows

1. Introduction

1.1. Problem Motivation

Recent years have witnessed a dramatic rise in the importance of cryptocurrencies such as Bitcoin nakamoto2008bitcoin and Ethereum buterin2014next as means of exchanging money and storing value coinbasebtcgrowth . Unfortunately, however, most blockchains can directly process only a small number of transactions per second. Most Bitcoin variants, for example, only support 4-5 transactions per second bitcoinscalinghackernoon . One method for improving data throughput is to settle transactions privately, using the blockchain as fallback security guarantor. This enables the construction of so-called “off-chain” or “Layer-2” networks. The most famous of these networks is the Lightning network on Bitcoinpoon2016bitcoin , but Layer 2 protocols have also been implemented in Ethereum and other cryptocurrencies raiden ; connext ; outpace .

The core idea of these networks is that if two parties frequently transact, they need not record every transaction on the global ledger, but rather, need only record the net total of their transactions at the end of a business relationship. Traditional commercial banks behave in a similar manner; instead of repeatedly transferring cash, they often have accounts with each other, and simply move money in and out of these accounts.

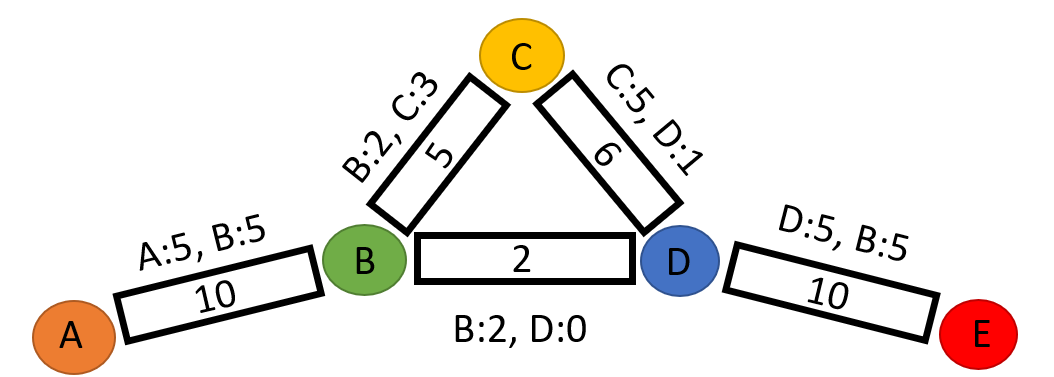

Traditional banks can go to court if a financial transfer never arrives. In an anonymous cryptocurrency network, or when blockchains span political jurisdictions, users may have no such recourse. Instead, to guarantee solvency, two parties can agree to put money into escrow. Transferring money then means privately updating shares of ownership of the escrowed funds. Such an escrow account is typically called a “payment channel.” Pairs of agents who lack a direct channel can route funds across a path in the payment channel graph. Figure 1 gives an example payment network on 5 nodes.

However, if one agent comes to own the entirety of the escrowed funds, it cannot accept additional money on that channel without opening itself to the risk of being cheated by its channel counterparty. More generally, no fixed network of payment channels can satisfy every possible sequence of transactions. We give a more detailed description of the network model, based on credit networks dandekar2011liquidity , in Section 2.

When a payment channel network cannot process a transaction, that transaction falls back to the underlying blockchain. The ratio of the number of transactions successfully settled privately to the number of transactions that a payment channel network cannot settle thus acts as a multiplier on a blockchain’s limited transaction rate. This ratio is our object of study; a higher ratio is clearly desirable for improving blockchain performance. Higher liquidity can also benefit individual agents directly, in that a higher transaction throughput capacity should mean lower fees per individual transaction, and higher liquidity means a higher chance of being able to purchase something online quickly.

Implementing a payment channel network in the real world is a complex systems design problem. For example, agents must have some way of discovering payment routes across the network. Some users might also like to keep their payment patterns private from network intermediaries. However, as we show here, even if a payment network operates perfectly – no hardware ever fails, every node has full information, transactions resolve instantaneously – no payment network can resolve every transaction (under a natural class of transaction models). Therefore, the baseline performance of e.g. a payment routing system is not 100% success, but rather, the transaction success rate in an ideal system. Our goal in this work is to study this baseline performance.

In real-world implementations of payment channel networks, off-chain transactions can settle in seconds, but putting data onto the blockchain or settling on-chain can take 10s of minutes. Because the network’s topology itself cannot change fast enough to respond to individual transactions, we study the performance of fixed network topologies.

Of course, placing capital into escrow to secure a link incurs a cost, in terms of the interest rate on the escrowed funds. When agents participate in a payment network, they implicitly choose to pay this cost in exchange for the ability to use the network directly. One goal of this work is to provide a framework for agents to understand the utility they would derive from participating in the network in a particular manner, and thus to evaluate whether this utility outweighs the costs they must pay. Agents must make a strategic choice about how to allocate their escrowed funds. One agent could choose to make one high-capacity link with a central node, or it could choose to make several lower-capacity links with different nodes. An agent might wish to avoid making a link with another agent whose internet connection is unreliable. Given some set of feasible options, agents must implicitly pick a preferred option. One goal of this work is to lay out a framework for agents to evaluate and compare their options.

1.2. Monotonicity

At a high level, a payment network appears similar to a single-commodity flow network when resolving a single transaction. The main difference is that transactions have side effects, and side effects of different transactions can cancel each other out or compound each other. Many network flow problems or queueing problems study the case where the flow across an edge in each direction is independently limited. In a payment network, flow in one direction cancels out flow in the other direction. At any point in time, on each link, the total flow sent since the start of network operation in one direction must be approximately equal to the total flow in the other direction (where approximately means the amount of funds in escrow on that link).

Many seemingly similar network flow problems are subject to what has become known as Braess’s paradox braess2005paradox . Famously, in car traffic networks, when drivers choose their routes selfishly, total traffic throughput in a road network can be decreased by adding roads. Example 4.6 of ramseyer2020liquidity gives a simple example of a credit network variant that violates monotonicity. Many network models display similar deleterious effects.

In cryptocurrency networks, where no central party exists to act as a coordinator, if selfishly routing payments had this deleterious effect, there would be no obvious way to coordinate a more efficient routing process. It could also be possible for an adversarial party to add edges to the network to decrease throughput (there might even be a financial incentive to do this – offchain transactions reduce demand for data on the blockchain, which lowers on-chain transaction fees). There naturally arises, then, a question about the “monotonicity” of payment networks – is the fraction of transactions that succeed monotonically non-decreasing as the number and capacity of edges increase?

A Layer-2 payment network closely corresponds to a distributed currency model known as a credit network, first formulated independently by ghosh2007mechanism ; defigueiredo2005trustdavis ; karlan2009trust . Dandekar et. al. and Goel et. al. dandekar2011liquidity ; goel2015connectivity developed the mathematical foundations for the model and analyze transaction success rates, which they call “liquidity”. In order to perform their analysis, these authors assume that transactions have discrete sizes. With this assumption, the monotonicity conjecture is equivalent to a conjecture that matroid theory’s “negative correlation” conjecture holds on the collection of independent sets of a graphical matroid. Feder and Mihail in as1992balanced showed that if a matroid has this property, one can sample in polynomial time an approximately random basis, but not all matroids have this property. More recently, Anari et. al. anari2018log gave a polynomial-time approximate sampling algorithm for general matroids.

1.3. Our Results

In this work, we give a general analytical framework for Layer-2 payment networks with arbitrarily sized transactions, eliminating a key assumption needed for goel2015connectivity ; dandekar2011liquidity , and use this toolkit to prove the monotonicity conjecture for the classes of transactions most relevant to cryptocurrency applications. We also give an efficient network state sampling algorithm.

The detailed results are more understandable with the following two pieces of context.

First, formally defining the “probability that a transaction is successful” requires a small amount of care. We will define it as the probability that a given transaction is feasible in configuration sampled according to some probability measure on the set of configurations. This, of course, raises the question of what measures arise from real-world behavior.

We model transactions as arising from an exogenous random process. E-commerce transactions, for example, arise largely from demand for consumer goods, not from anything related to the short-term status of a payment processing pipeline. For consistency with prior work goel2015connectivity ; dandekar2011liquidity , we also model transactions as arising in sequence in discrete time. At every timestep, a payment network simply executes the current transaction if it is able in its current escrow-configuration (where a network’s escrow-configuration is the ownership status of every edge; henceforth “configuration”). Every successful transaction changes the configuration of the network, so a random transaction model induces a Markov chain on the set of configurations of the network. In the rest of this work, we measure transaction success probability relative to the invariant measure of this Markov chain. There are other similar transaction models that would define natural, induced probability measures; results derived through our analytical framework depend on the probability measure, not the process through which a measure is induced.

Second, the state space of the induced Markov chain is most succinctly described not as a set of escrow-configurations but rather, as a set of classes of functionally-equivalent configurations. An agent can send money to itself along a cycle to change the network configuration – however, every transaction realizable in the network configuration prior to the cyclic flow is realizable in the network configuration after the cyclic flow. Sending flow along cycles gives a “cycle-equivalence” relation between configurations, and for the purpose of executing transactions, representatives of one equivalence class are all functionally equivalent. The induced Markov chain is thus most naturally viewed as acting on the equivalence classes of this equivalence relation.

Prior work primarily analyzed the case where transaction distributions are symmetric, which is to say, agent is as likely to pay agent as is likely to pay . Such transaction distributions induce uniform probability measures. This assumption may not be realistic in some real-world credit network use cases. For clarity, note that of the below results, result 1 (sections 2-4) does not rely on this assumption, while result 2 (section 5) does, as does Theorem 6.3 of result 3. We give a small comment on this assumption and related open problems in section 7.

Our results are the following:

-

(1)

In sections 2, 3, and 4, we construct a new toolset for analyzing the set of configurations of a credit network. Simply put, we construct a map (for “Direction” of a transaction) from the set of possible transactions to and a map from the set of configurations of a credit network to that together preserve how transactions and configurations interact. If a transaction executed from configuration sends the network into configuration , then . The stationary measure of the induced Markov chain is a probability measure on , and analyzing liquidity reduces to analyzing the measures of subsets of .

For comparison to prior work, we study a continuous extension of the credit network model of goel2015connectivity ; dandekar2011liquidity . Specifically, Goel et. al. and Dandekar et. al. goel2015connectivity ; dandekar2011liquidity measure performance with regard to transactions of size , where is some minimum transaction size, while we study transactions of arbitrary real-valued size.

If transactions all have the same size (or integral sizes), then configurations of the credit network can be mapped into forests (acyclic subsets of edges) of a related, undirected multigraph with the same vertex set. They show that the probability that a transaction of size succeeds from agent to agent is equal to the probability that a forest sampled uniformly at random puts and in the same connected component.

Unfortunately, this correspondence gives no clues as to how to analyze liquidity for transactions of larger size. In real-world blockchains like Bitcoin, one Satoshi – one “smallest unit of money” – is worth at the time of writing roughly 1/10000th of a US dollar, while Lightning channel capacities may run into the hundreds or thousands of dollars. In this kind of parameter regime, a transaction of size succeeds with probability very close to in any network topology, and most transactions sent have much larger sizes. An agent in the network would be interested primarily in transactions of larger, but variable, sizes.

We also study the rate at which transaction success rates decline as transaction sizes increase. Modeling transactions as taking on arbitrary real-valued sizes streamlines this analysis and requires a new set of analytical tools.

As an aside, these analytical frameworks are in fact related mathematically. From the point of view of prior work, we study the success rate of transactions of fixed real-world value, as discretization becomes arbitrarily fine. Informally, analyzing the discrete case compared to the continuous case is like studying the number of points of a lattice within a well-behaved convex body, instead of directly studying the volume of said convex set. Prior work of goel2015connectivity ; dandekar2011liquidity is able to measure liquidity using forests because of a correspondence between forests and these lattice points (stanley1980decompositions , Example 3.1). As a lattice becomes increasingly fine, a (weighted) count of the number of lattice points in a well-behaved convex set approximates the volume of said set; we note without proof that many of our arguments could be adapted to hold if the transaction granularity is sufficiently small using this principle.

-

(2)

In section 5, we prove theorems about the liquidity of general credit networks and a limited version of the monotonicity conjecture.

Relative to a uniform probability measure (i.e. transaction distributions that are symmetric), transaction success probability can be computed via effective resistance calculations.

Payment networks on cryptocurrencies are particularly beneficial for two kinds of transactions. First, they streamline transactions between parties that transact frequently, especially between parties with a direct connection. And second, by increasing transaction throughput, they put downward pressure on transaction fees, which helps make small transactions economically worthwhile. Again relative to a uniform probability measure (i.e. transaction distributions that are symmetric), our analytical toolkit enables a proof of the monotonicity conjecture for transactions of these types.

In real world terms, this means that bad actors cannot add edges to the graph and harm either of these payment network use cases.

-

(3)

Finally, in section 6, we also show that the problem of sampling a random network state reduces to the problem of sampling a random point from a zonotope (that depends on the payment network graph). Sampling from a distribution on a convex set is a well studied problem and can be done in practice with reasonably fast Markov chains, such as the well-studied Hit and Run process smith1984efficient .

Furthermore, relative to a uniform measure on network configurations, we give an algorithm (Theorem 6.3) for exact uniformly random sampling states of a payment network of agents and edges in time , where is the complexity of solving a linear program on constraints. For comparison, Hit and Run would require . Currently, cohen2019solving , for the matrix multiplication constant.

1.4. Related Work

The concept of the Credit Network that underlies the analysis here was developed independently by ghosh2007mechanism ; defigueiredo2005trustdavis ; karlan2009trust . These authors worked in the contexts of informal borrowing networks karlan2009trust , online reputation systems backed by social relationships defigueiredo2005trustdavis , and auction systems built on a credit network.

Recently, an analysis of the distribution of network states induced by a distribution on transactions was conducted in branzei2017charge . The stated goal of these authors is to understand transaction pricing models, but central to the pricing analysis is an understanding of transaction failure rates in the short term. By constrast, for scaling a network, the key metric is failure rate amortized in the long term. Their analysis, however, only looks at graphs consisting of isolated edges and of stars, and also assumes that the size of a transaction between pairs is fixed.

Most early implementations of payment networks discuss transactions as being routed along single paths (as in e.g. poon2016bitcoin ). But for the purpose of actually sending money, one successful $2 transaction along a single path is functionally equivalent to two separate successful $1 transactions along two different paths. More generally, a transaction in a payment network can be thought of as a flow through the network.

What we study is also similar to the study of “capacitated transportation networks,” as in doulliez1972transportation and hassin1988probabilistic . In this model, the capacity of each edge is drawn independently from some random distribution. These capacities are “successful” if they can satisfy some fixed set of flow sources/demands, and the reliability of the network is the chance of success. Similarly, Grimmett and Suen grimmett1982maximal studied the expected size of a maximum flow through a graph, if edge capacities are random. Efforts to approximately compute transportation network reliability include lin1995reliability .

A key difference from our model, however, stems from the fact that routing flow along a cycle does not change the ability of a payment network to satisfy a flow demand. The set of network states, therefore, is not the product of sets of states on individual edges (unless the network is acyclic).

2. The Network Model

In practice, a payment network consists of a set of agents and a set of edges between agents, where each edge has some associated amount of money in escrow. If an edge runs between two agents and , then and privately track how much of the escrow on the edge belongs to and how much belongs to . For example, Figure 1 gives a simple payment network between a few nodes.

Suppose that agent wishes to pay one unit of money to agent . Then the amount of money on the edge between and remains constant, but and privately decide that of this escrow, ’s ownership stake decreases by one, and ’s ownership increases by one. Of course, this transaction would fail if and only if ’s ownership stake were less than one.

Formally, then, we can model a payment network as the following. As transactions occur, the unchanging components of the system consist of a graph , representing nodes and edges, along with a map that records the capacity of each edge. An escrow configuration of the network, which changes as transactions happen, will be a map recording, for each edge, how much of the escrow each agent owns. Specifically, for some edge , if , then owns units of escrow on edge , and .

Before proceeding, we would like to note that an escrow configuration in the above sense is not the same as the network states discussed in the introduction. For the purpose of sending money, many escrow configurations can be functionally equivalent, and we will treat equivalent escrow configurations as a single network state.

A simple transaction along a single edge will consist of a sender , a receiver , and an amount , and we will say that the transaction succeeds if and only if . If this transaction succeeds, the network will be left in the state where is decreased by and is increased by .

To complete the model, a transaction consists of a sender , a receiver , and a transaction amount , and we will say that succeeds in a configuration if and only if there exists a commodity flow taking units of flow from to with . Such a transaction change an escrow configuration in the same way that simple transactions of size along each edge collectively change an escrow configuration.

2.1. Definitions and Basic Properties

First, note that if agents can successfully perform the same sequences of transactions starting from two different escrow configurations, then in terms of moving money, the configurations are identical. This motivates the following definition.

Definition 2.1 (Transaction Equivalence).

Two configurations and are transaction equivalent if, given any sequence of transactions , succeeds starting from if and only if succeeds starting from .

Unfortunately, this definition provides no obvious aid in understanding the space of configurations. For that, consider as an example a cycle graph where each edge has capacity , and pick one direction around the cycle to be “clockwise”. Let be the configuration where if and only if points in the clockwise direction, and let be the configuration where if and only if points in the counterclockwise direction. Then for any two vertices and , could send at most one unit of payment to along a counterclockwise path in configuration and could send at most one unit of payment along a clockwise path in configuration . In this sense, then, and are transaction-equivalent.

Observe that one could move from to by routing a payment from a vertex to itself in a counterclockwise direction. This motivates the following definition.

Definition 2.2 (Cycle Equivalence (Definition 2, dandekar2011liquidity )).

Two configurations are cycle-equivalent if and only if one is reachable from the other by routing a series of payments along cycles.

We will see later that these two definitions are equivalent (Corollary 3.8), and consequently, that the choice of route when making a transaction does not influence the resulting cycle-equivalence class.

Finally, the “liquidity” of the network is the probability that a transaction will succeed from a “random” cycle-equivalence class. We make this definition formal in 4, but intuitively, the distribution of interest is the one that is induced by real-world random processes. We model this as the stationary distribution of a Markov chain that sequentially attempting to execute randomly generated transactions; this Markov chain has a dimple description if it’s state space is thought of as cycle-equivalence classes, not as individual configurations.

3. From Networks to Continuous Representations

For the rest of the discussion, we will assume that a graph is connected, and let be the size of a spanning tree in .

At a high level, in this section, we will construct a map from the set of escrow configurations to a convex subset of , and show that sending money in the credit network is equivalent to moving in . That is to say, every transaction corresponds to some vector , and if executing from a configuration results in the configuration , then . Furthermore, the preimage of any point in is exactly one cycle-equivalence class of configurations.

This map relies on a representation of the graphic matroid in , subject to the additional constraint that the signed summation of the edges visited while walking in a cycle is . This condition lets us discuss the “direction” of money moving from a vertex to a vertex in a well-defined manner.

Fix some orientation on every edge.

Definition 3.1.

Let (for “direction”) be a map from to .

The direction of a path is simply the (signed) summation of along the path:

The direction of a flow is similarly defined to be

We will refer to the direction of a path as and the direction of a flow as .

Sending money in a credit network is akin to sending flow through the underlying residual graph. We want the direction of the flow to capture something about how a credit network configuration changes as money is sent. For that, it suffices for a direction map to satisfy the following conditions:

Definition 3.2.

A direction map is a spanning representation of the credit network if:

-

(1)

The direction (under ) of any path is if and only if is a cycle.

-

(2)

For any spanning tree , the set of vectors spans .

Theorem 3.3.

Spanning representations exist.

The proof is in the appendix, but informally, take the edges of a spanning tree, represent them as the standard basis, and represent the other edges so that cycles sum to . We will not mention the representation when the choice of representation is clear from context. The utility of a spanning representation is that it naturally induces a map from configurations to that has several useful properties.

Definition 3.4.

The represented score of a configuration with respect to a spanning representation is .111The analysis would work out the same if we simply summed over all directed edges. This definition makes later theorem statements cleaner.

The condition that means that the summation above is over edges pointed in their positive direction.

This should be thought of as a generalization of the “score vectors” as in e.g. kleitman1981forests . In fact, the represented score map exactly captures the transactional relationships between cycle-equivalence classes.

Theorem 3.5.

-

1

Two cycle-equivalent configurations have the same represented score.

-

2

If a transaction along path of size takes configuration to configuration , then .

-

3

If two paths and both go from vertex to vertex , then .

A transaction of size from to is a special case of a flow demand, and as a corollary of the above properties, any flow that satisfies a given demand will have the same direction. Given some spanning representation, then, it is reasonable to think of transactions not just as paths from to but also as flow demands or as vectors in . In particular, we make the following convention:

Definition 3.6.

A transaction sending units of flow from to corresponds to a vector if, for some path from to , .

In other words, if executing sends configuration to , then .

These definitions are sufficient to analyze the space of cycle-equivalence classes.

First, recall that the Minkowski Sum of vectors is the set .

Theorem 3.7.

The image of the set of cycle-equivalence classes, under a spanning representation, is exactly the Minkowski sum of the vectors .

As before, the requirement simply means that the summation is over all edges, viewed in their positive direction.

With these definitions, we can finally make the following useful characterization of transaction-equivalence.

Corollary 3.8.

Transaction-equivalence is equivalent to cycle-equivalence.

4. Induced Measures on the Configuration Space

As outlined in the introduction, we would like to understand success probability with respect to a “random” configuration drawn from the distribution induced by real-world transaction activity. For this work, we will think of transactions as arriving from some external process; most transactional contexts like online shopping are driven by forces entirely external to the payment network, such as demand for consumer goods.

Our analysis is one of an idealized payment network, so we will model transactions as happening one at a time, communication links never fail, and transaction fees are zero.222The question of how to optimally set transaction fees is a fascinating open problem for future study. In particular, we will model transactions as occuring in sequence, drawn from some distribution. At every timestep, we draw a new transaction by drawing a pair of vertices who will transact and then a transaction size. If the transaction is feasible in the current network configuration, we execute the transaction and move to the resulting state. Otherwise, we disregard the transaction.

Definition 4.1 (Transaction Model).

A transaction model for a set of vertices consists of the following:

-

(1)

The set of pairs of vertices that transact, .

-

(2)

A distribution on .

-

(3)

For each pair , a continuous probability distribution on the size of a transaction between and .

This transaction model generates a transaction by using to choose a sender and a receiver , and then using to choose a transaction size.

For technical convenience, we will allow to output negative values, and sending negative money from to will be considered sending money from to . It is without loss of generality, then, to assume that only one of or is in .

We would like to use a transaction model to induce a distribution on the set of cycle-equivalence classes. In the discrete credit network case of dandekar2011liquidity ; goel2015connectivity , the set of cycle-equivalence classes was finite, and so those authors could simply sum over all classes. However, in our continuous setting, the set of cycle-equivalence classes has infinite cardinality. We would like to analyze the probability mass of a subset of configurations, but it is not clear how to integrate over a set of cycle-equivalence classes without building a lot of measure-theoretic infrastructure. Instead, given a fixed spanning representation, it will be much easier to simply map the set of cycle-equivalence classes into and analyze subsets of . As a notational shorthand, we will say that the measure of a set of cycle-equivalence classes is simply the measure of the image of the set in (if said image is measurable).

Given this technical difficulty, when we define the following Markov Chain, we will use as its state space the image in of the set of all cycle-equivalence classes under a fixed spanning representation.

Definition 4.2 (Markov Chain 1).

Let be a payment network, let be a spanning representation, let be the image under of the set of cycle-equivalence classes of , and let be some transaction model. The induced Markov chain will be defined as follows:

Start at some point .

At each timestep, draw a transaction between vertices and of size from . If the transaction is feasible from the current state , then perform the transaction and update the state of the network accordingly (. Otherwise, remain in the same state ().

The induced distribution on is the stationary measure of this Markov chain (if a stationary measure exists and is unique).

Theorem 4.3.

The above Markov Chain has an invariant probability measure.

We are primarily interested in the case where a transaction model induces a unique stationary measure. The following condition is sufficient but not necessary; there are many similar sufficient conditions.

Theorem 4.4.

Let be a graph, and let be a transaction model on .

Suppose that for each pair , the support of contains the interval for some . Then Markov Chain 1 has a unique stationary distribution if the graph is connected.

Motivated by Theorem 4.4, we call a transaction model that satisfies these conditions a connected transaction model.

In the next section, we will primarily study the case where the unique stationary measure is uniform.

Theorem 4.5.

Let be a connected transaction model.

If each is symmetric about , then the induced stationary measure is uniform.

Motivated by Theorem 4.5, we call a transaction that satisfies these conditions a symmetric, connected transaction model.

When the stationary measure is unique, the natural definition of transaction success probability is well-defined.

Definition 4.6.

Given a spanning representation , let be the set of configurations represented in and let be some density measure over . Then the liquidity of the network with regard to a transaction is the relative measure of the image of the set of configurations where succeeds, .

Theorem 4.7.

The liquidity of a network with respect to a particular transaction does not depend on the choice of spanning representation.

These theorems show that under small assumptions on transaction distributions, the distribution on configurations of a payment network is a well-defined topic of discussion.

5. Liquidity Analysis and Monotonicity

One question that an agent operating in a payment network might ask is how adding escrow to one edge will affect transaction success rate across another edge. It would be bad for a payment network if bad actors could add escrow and in doing so decrease liquidity between well-behaved agents.

The authors of goel2015connectivity were concerned with this question, which they dubbed the “Monotonicity Conjecture.” In their work, they observe that this conjecture is equivalent to the well-studied “Negative Correlation” conjecture about the set of forests of a graph. To summarize, a matroid on a set of elements is said to be negatively correlated if, for any two elements , the probability that is in a random basis is greater than the probability that is in a random basis that also contains . as1992balanced showed that this conjecture implies a polynomial time random sampling algorithm for matroid bases.

Not all matroids are negatively correlated, however. And although the set of forests is not a matroid, much intellectual energy has been devoted to the negative correlation of forests question – for example, grimmett2004negative ; cocks2008correlated ; semple2008negative .

We show in this section that for the monotonicity conjecture on credit networks, relaxing the (somewhat unnatural) restriction that transactions must have discrete sizes can actually make the monotonicity question tractable. Below we reproduce this conjecture in the context of our network model.

Conjecture 5.1 (Monotonicity).

Let be a credit network with edge capacities , let be a transaction from a vertex to another vertex of size , and let be the uniform stationary measure induced by a symmetric, connected transaction model.

For any pair of vertices , increasing in should not decrease the liquidity of with respect to .

5.1. Liquidity Analysis

To move towards a study of the monotonicity conjecture, we first prove some theorems about general liquidity in credit networks in the continuous model.

As before, to avoid the need to set up measure-theoretic infrastructure on the set of cycle-equivalence classes, we will for the rest of this section measure the probability of a set of configurations as the relative measure of its image in under the map induced by a spanning representation. When the measure is uniform, the measure of a set in is simply its volume.

Therefore, as a notational shorthand, we take the “volume” of a set of cycle-equivalence classes to mean the volume in of the image of the set of cycle-equivalence classes under the map induced by a fixed spanning representation. As per Theorem 4.7, liquidity metrics are not affected by choice of spanning representation.

As mentioned in Theorem 3.7, the image of the set of configurations is the Minkowski sum of a particular set of vectors. It turns out that the volume of this Minkowski sum is closely related to the undirected graphical matroid of the payment network. The connection comes through the generating polynomial for the matroid, which we now define for completeness.

Definition 5.2.

Let be a graph, and let be the set of all spanning trees of . Associate with every a real variable .

The generating polynomial of is .

We will also denote as the summation over sets such that is a spanning tree, or equivalently, .

More generally, we will denote with the generating polynomial of the graph where vertex is identified with vertex . If , then .

Theorem 5.3.

Let be a payment network with edge capacities .

Suppose that a spanning representation maps some tree to the standard basis. Then the volume of the image of the set of cycle-equivalence classes of configurations is equal to .

The volume of a Minkowski sum of vectors is equal to a summation over subset of vectors of the determinant of the matrix whose columns are . The result follows from the fact that an edge can only appear once in a simple cycle and the multilinearity of the determinant.

For convenience, in the rest of this section, assume that we have fixed to be such a spanning representation. 333As per Theorem 4.7, choice of spanning representation does not affect liquidity results. This makes the presentation of results simpler.

To analyze liquidity, we also need a useful analytical description of the volume of set where a transaction succeeds.

Lemma 5.4.

Let be the vector in corresponding to some transaction If is the subset of corresponding to the entire set of cycle-equivalence classes, then (Minkowski subtraction) is the space where succeeds.

Proof 5.5.

Follows from the theorems of Section 3.

We start with the easy case for analysis. Theorems 3.7 and 5.3 shows that the image of the set of all cycle-equivalence classes is a zonotope with a convenient structure. When there is an edge already present in the graph between two agents and , the area where a transaction from to succeeds retains the same kind of structure.

In the language of the above lemma, for a transaction from to , the space corresponding to transactions where succeeds, , is a zonotope. In fact, this zonotope is identical to the zonotope generated by a credit network where the capacity of the edge from to is reduced by the size of the transaction.

Theorem 5.6.

If corresponds to a transaction between and of size , and , then the volume where succeeds is equal to where except that . The volume of the space where fails is equal to .

When this holds, then computing a transaction’s chance of success is straightforward.

Corollary 5.7.

Suppose that corresponds to a transaction between and of size , and that the graph contains an edge with .

-

1

The probability that fails is simply .

-

2

Let be the underlying graph, and let be a multigraph where is with duplicated to make edges and . Set , , and for all other edges , .

Then the probability that fails is equal to the probability that is in a random weighted tree sample from .

As an aside, the criterion that and have an edge of capacity at least does not mean that and must route all of their transactions explicitly along that edge. The model does not require any particular type of routing algorithm. The rest of the graph is still relevant for and when they share an edge, as many configurations will require and to use edges other than the one directly between them.

Now for the harder case for analysis. Namely, when and does not correspond to an edge in the underlying graph, the space where succeeds is not necessarily a Minkowski sum of a set of vectors and thus lacks a concise mathematical characterization. Such examples unfortunately occur in very simple graphs, such as the cycle on four vertices when nonadjacent vertices transact. Figure 6 of althoff2015computing gives a visual depiction of such an object.

Nevertheless, lower bounds on liquidity are derivable using the same analytical frameworks as Corollary 5.7.

Lemma 5.8.

Let and be any two vertices, and let be the direction of a path from to .

Let denote the probability that a transaction size from to fails. Then . Moreover, .

Corollary 5.9.

A lower bound of transaction success probability (i.e. ) is computable efficiently (via calculating effective resistance, similarly to Theorem 5.7).

Proof 5.10.

Let be the image of the set of all cycle-equivalence classes, let be the projection of onto some fixed hyperplane with normal , and let denote the volume of the projection in . For every , consider the line extending in direction from . Suppose a point is on this line. Let be the signed distance of from , namely, .

Then for the set of points on this line and also in , let and .

Note that because is convex, it can be represented as the space .

Then the volume of where a transaction in the direction of of size fails is:

The derivative of this quantity at is therefore

Clearly this quantity is bounded between and , achieves when , and is monotonically decreasing in .

Note that a projection of a Minkowski sum of a set of vectors is the Minkowski sum of the vectors individually projected. It follows that and that is .

lower bounds transaction success probability because the volume where a transaction of size in direction fails is upper bounded by , and thus transaction success probability is at least .

Corollary 5.11.

The lower bound of Lemma 5.8 is tight if and only if there is an edge of capacity at least in the direction of the transaction in the credit network graph.

Proof 5.12.

The lower bound is clearly tight if the credit network graph contains an edge in the direction of the transaction, by Theorem 5.7.

Now suppose that the edge does not exist. Specifically, let again be the image of the set of all cycle equivalence classes, and let be the direction of a transaction between vertices and . Suppose that the transaction has size , and that edge from to , if it exists, has capacity .

The proof of Lemma 5.8 shows that volume of the space in where a transaction in direction of size fails is equal to

with , , and defined as in the proof of Lemma 5.8.

The lower bound of Lemma 5.8 is tight if and only if

| (1) |

It suffices to find a point such that and . Given such a point , the point is a point from which . Because is closed, there is a point such that . Hence there exists such that for with , then , and thus the first equality of Equation 1 cannot hold.

Consider a credit network configuration defined as follows. Pick some vertex cut of the graph separating from . That is, a set of vertices such that all paths from to flow through (other than possibly a direct path from to ). Let be the number of edges such that and , and for every such edge , set such that . Let . Pick for every other edge arbitrarily.

Then from configuration , strictly less than money can move from to or from to . This means that the point that is the image of under our spanning representation has the property that and but .

5.2. Monotonicity

Although we conjecture monotonicity in the general case, the same technical difficulty (Minkowski subtraction does not always produce zonotopes) that obstructed liquidity analysis presents itself when studying monotonicity. Nevertheless, we show that monotonicity holds when transactions are small or between vertices that already share a direct connection in the credit network graph.

Theorem 5.13.

Suppose that is a transaction from to of size and that . Let and be any two vertices (not necessarily connected directly, possibly equal to or ).

Then increasing does not decrease the success probability of .

Proof 5.14.

If and are disconnected, connecting to with an edge of capacity does not change the liquidity of any transaction, so without loss of generality assume and are connected by an edge of possibly capacity.

Let be the image of the entire space of configurations before adding capacity on edge , and let be the image of the space where succeeds. Let be the image of the entire space of configurations after capacity is increased along , and let be the image of the space where succeeds after capacity is increased along .

For convenience, write and . Let denote the volume of a set in . Finally, let be the increase in capacity along .

It suffices to show that .

Note that is the Minkowski sum of the vectors and that is the Minkowski sum of the vectors .

Then and .

Moreover, adding to and to get and means that and , respectively, are the Minkowski sums of and with the the vector . Hence, and .

Rearranging terms shows that inequality holds if and only if , which holds because the tree matroid is Rayleigh choe2006rayleigh ; kirchhoff1847ueber .

More generally, we can prove the monotonicity conjecture if we bound transaction size.

Theorem 5.15.

For every credit network , there exists a constant such that is monotone with regard to transactions of size less than .

Proof 5.16.

Let be the direction of a path from to , and let be the direction of a path from to . Let . Finally, let denote the probability that a transaction sending flow of size in direction fails in the graph where capacity has been added to an edge in direction .

First, note that by Lemma 5.8, at , .

Because the tree matroid is Rayleigh choe2006rayleigh , some computation shows that at for every . These two quantities are equal if and only if there are no cycles containing the edges and , in which case monotonicity holds trivially.

Then for any fixed , there exists some such that for all , .

Now, let denote the volume where the transaction succeeds before the capacity addition, and let denote the volume of the entire space before the capacity addition. Let denote the marginal volume where the transaction succeeds after the capacity addition, and let denote the marginal volume of the entire space after the capacity addition.

Importantly, because the space of configurations is a Minkowski sum, adding capacity simply adds an element to the Minkowski sum. The volume of any convex subset of the Minkowski sum, therefore, is increased simply by times its projection in the direction . Thus the ratio is constant with respect to .

Note that . Then for any , if for any , then for all .

Putting this all together, there exists some such that the credit network is monotone with respect to all transactions along paths with transaction size less than .

6. Efficient Sampling

In Theorem 5.6, we showed that for a narrow class of parameters, agents can compute the probability of transaction success. But this class of parameters was quite narrow, and likely not directly relevant to real-world networks. An agent in a payment network might like to be able to estimate this probability efficiently, so that they could measure the effects of behavior change under a wide variety of distributional assumptions.

In prior work on credit networks that assume that transactions have discrete sizes, estimating this probability is roughly equivalent to sampling a random forest of the underlying graph. A polynomial-time algorithm for this was recently discovered in anari2018log . This algorithm is quite interesting from a theoretical standpoint, but likely is still too slow to run on real-world graphs.

By contrast, we observe here that removing the discrete size requirement makes sampling a random network state quite efficient for a wide variety of parameter regimes. Where earlier work on credit networks invoked long lines of detailed mathematical machinery, sampling a random network state here simply requires sampling a uniformly random point from a convex body. This can be done with the well-studied hit-and-run sampling scheme smith1984efficient .

Theorem 6.1.

If is a log-concave distribution on the set of cycle-equivalence classes of a credit network, then the hit-and-run sampling algorithm samples a random cycle-equivalence class from .

The algorithm requires a preprocessing step of time complexity preprocessing and (amortized) per sample, where denotes the complexity of solving a linear program with constraints (hiding log factors and dependencies on ).

By the results of cohen2019solving , , for the current matrix multiplication constant.

Proof 6.2.

The zonotope is a convex body, and thus this statement is simply a special case of the results of lovasz2003hit and lovasz2007geometry . The algorithm, however, requires zonotope membership oracle calls. Checking membership in a zonotope can be solved with a linear program on variables.

When the distribution is uniform, we can improve our sample time complexity to the minimum of . The image under a spanning representation of the space of cycle-equivalence classes is not an arbitrary zonotope, but rather, has additional structure that we can exploit.

Theorem 6.3.

If is the uniform distribution on cycle-equivalence classes of a credit network, then there exists an exactly uniform sampling algorithm with time complexity .

This shaves a factor of off of the asymptotic sampling complexity. Note that real-world payment network graphs, like those deployed in Lightning, are typically quite sparse.

Our algorithm runs in steps, where each step involves solving a linear program on variables (taking time ) and computing the electrical resistance between two points in a graph (taking time ). We remark that using the linear program solver of cohen2019solving gives total complexity of . However, one could substitute a faster approximate resistance algorithm and get an approximately uniform sample with a faster complexity. Similarly, one could use any linear program solver in our algorithm, and the time complexity would change accordingly.

Proof 6.4.

Let be a credit network, and fix some ordering on the edges and some spanning representation . Furthermore, say that the first elements of the ordering form a spanning tree. Let the edge capacity of edge be , and let the Minkowski sum of the first edges be . Denote . It suffices to sample a uniformly random point within .

Let be any edge. Let denote the portion of the surface of that is “visible” from the direction of . (The surface of a zonotope is a collection of faces. A face forms part of if its normal vector has ). Note that can be decomposed into the almost disjoint union of two pieces. The first is , and the second is the remainder, which is the Minkowski sum of the set and the vector . Their intersection is a translation of .

As noted in Corollary 5.7, the ratio of the volume of the second part to the total volume of is computable via an effective resistance calculation.

Let be the projection of onto the hyperplane through the origin with normal . A random point in this second part can be sampled by taking a random point in , mapping back to the corresponding point in , and adding for drawn from uniformly at random.

The mapping from points in back to points in can be computed via a linear program. Specifically, given a point , maximize such that is a point within . This linear program has constraints and decision variables, so solving this takes time .

Conveniently, both and are zonotopes, so our sampling process naturally sets itself up for a recursive sampling algorithm.

An algorithm for sampling a random point from the Minkowski sum, therefore, could look as follows. Given as input vectors and capacities , will return a uniformly random point in the Minkowski sum of the input vectors. For notation, let this Minkowski sum again be and its surface in the direction be . First, check whether the input set of vectors is linearly independent. If they are, return a random list of values drawn uniformly at random from .

Next, compute the effective resistance along edge . Use this to choose between the spaces and randomly proportionally to their volumes.

If the algorithm chooses , the algorithm can invoke on the list of vectors , where is the component of perpendicular to . It can then find the corresponding point in via the above linear program.

Finally, the algorithm can sample uniformly at random from and return .

If we do not accept , simply return .

Computing a spanning representation takes time . Each step of this algorithm takes time for solving the linear program, computing effective resistance, and processing a list of vectors. Since the algorithm recurses times, the total time complexity is .

7. Future Work, and A Note on Symmetricity

Our arguments for the monotonicity conjecture require that the Markov-chain-induced probability measure on the set of configurations be uniform over cycle-equivalent classes of configurations. We showed that this occurs when the transaction distribution is symmetric. However, real-world transaction distributions may not be symmetric.

In the real world, transactions on a payment network do not necessarily happen in sequence. We chose to analyze a discrete-time transaction model for conceptual simplicity and to follow the pattern of prior work on credit networks; however, we could have analyzed a continuous-time transaction model where in some window of time, pairs of agents can transact many times. Within a fixed time window, the net transaction balance between every pair of agents and might be randomly distributed. We could then sum these biases, weighted by the direction of a transaction from to , to get an overall direction of bias .

With this motivation, we could also model transactions via a “Reflected Brownian Motion” with drift vector (and normal reflection). It follows directly from harrison1987multidimensional that the invariant distribution of an RBM with bias is proportional to .

Of course, in the symmetric distribution case, is and the distribution is again uniform. If is nonzero, then the invariant distribution is efficiently sampleable using an algorithm like Hit and Run. Some asymmetric transaction distributions still have a net bias of . Finding realistic real-world assumptions that would be sufficient to imply uniformity of the induced stationary measure, or analyzing monotonicity when the induced stationary measure is nonuniform, are interesting open research problems.

General models of Brownian motion in a bounded space have been studied in other contexts, such as network queuing theory. A credit network is not exactly a traditional queuing network, but nevertheless, understanding connections with results in queuing theory or the theory of diffusion processes might prove fruitful. A potential line of future work would be to study cases where agent behavior changes based on the current configuration of the network. Under mild technical conditions, the notion of an induced invariant measure when agent behavior varies with state is still well-defined, and analogous concepts have been studied in other literature (such as kang2014characterization ).

8. Conclusion

The Credit Network model forms an accurate representation of the combinatorics underlying modern “Layer-2” transaction protocols. The performance of these networks is an important piece of the process of scaling up cryptocurrency deployments.

Prior work was only able to analyze the scenario where transactions have discrete sizes, and could only give meaningful liquidity bounds when transactions had a single fixed size that was not too small relative to edge capacities. Not only is this not a natural assumption, but the resulting analysis left open the important question of monotonicity and the problem of sampling efficiently random network configurations. In this work, we show that not only is the analogous continuous model analytically tractable, but that removing the assumption of discrete transaction sizes actually enables efficient sampling and progress on the monotonicity conjecture.

The results are obtained by exploiting a relationship between the graphs underlying payment networks and particular convex sets in . The problems of monotonicity and sampling thereby transform into problems of analyzing the volume of convex sets. This transformation relies crucially on the combinatorial properties of the underlying graphic matroid.

The authors hope that connections to other branches of mathematics, such as diffusion processes, that the continuous relaxation facilitates could prove fruitful areas of research, such as when studying state-dependent agent behavior or transaction pricing.

This research was supported by the Stanford Center for Blockchain Research and by the Office of Naval Research, award number N000141912268.

References

- (1) Connext network, https://connext.network/

- (2) Introducing outpace: Off-chain unidirectional trustless payment channels, https://medium.com/the-adex-blog/introducing-outpace-off-chain-unidirectional-trustless-payment-channels-243a08e152a

- (3) Raiden network, https://raiden.network/

- (4) Althoff, M.: On computing the minkowski difference of zonotopes. arXiv preprint arXiv:1512.02794 (2015)

- (5) Anari, N., Liu, K., Gharan, S.O., Vinzant, C.: Log-concave polynomials ii: High-dimensional walks and an fpras for counting bases of a matroid. arXiv preprint arXiv:1811.01816 (2018)

- (6) Braess, D., Nagurney, A., Wakolbinger, T.: On a paradox of traffic planning. Transportation science 39(4), 446–450 (2005)

- (7) Brânzei, S., Segal-Halevi, E., Zohar, A.: How to charge lightning. arXiv preprint arXiv:1712.10222 (2017)

- (8) Buterin, V., et al.: A next-generation smart contract and decentralized application platform

- (9) Choe, Y., Wagner, D.G.: Rayleigh matroids. Combinatorics, Probability and Computing 15(5), 765–781 (2006)

- (10) Cocks, C.C.: Correlated matroids. Combinatorics, Probability and Computing 17(4), 511–518 (2008)

- (11) Cohen, M.B., Lee, Y.T., Song, Z.: Solving linear programs in the current matrix multiplication time. In: Proceedings of the 51st Annual ACM SIGACT Symposium on Theory of Computing. pp. 938–942. ACM (2019)

- (12) Coinbase: Charting the course of bitcoin, 11 years and counting, https://blog.coinbase.com/charting-the-course-of-bitcoin-11-years-and-counting-b4e17969d4e1

- (13) Dandekar, P., Goel, A., Govindan, R., Post, I.: Liquidity in credit networks: A little trust goes a long way. In: Proceedings of the 12th ACM conference on Electronic commerce. pp. 147–156. ACM (2011)

- (14) DeFigueiredo, D.B., Barr, E.T.: Trustdavis: A non-exploitable online reputation system. In: E-Commerce Technology, 2005. CEC 2005. Seventh IEEE International Conference on. pp. 274–283. IEEE (2005)

- (15) Doulliez, P., Jamoulle, E.: Transportation networks with random arc capacities. Revue française d’automatique, informatique, recherche opérationnelle. Recherche opérationnelle 6(V3), 45–59 (1972)

- (16) Eberle, A.: Markov processes. Lecture Notes at University of Bonn (2017)

- (17) as Feder, T., Mihail, M.: Balanced matroids. Citeseer

- (18) Ghosh, A., Mahdian, M., Reeves, D.M., Pennock, D.M., Fugger, R.: Mechanism design on trust networks. In: International Workshop on Web and Internet Economics. pp. 257–268. Springer (2007)

- (19) Goel, A., Khanna, S., Raghvendra, S., Zhang, H.: Connectivity in random forests and credit networks. In: Proceedings of the twenty-sixth annual ACM-SIAM symposium on Discrete algorithms. pp. 2037–2048. Society for Industrial and Applied Mathematics (2015)

- (20) Grimmett, G.R., Winkler, S.: Negative association in uniform forests and connected graphs. Random Structures & Algorithms 24(4), 444–460 (2004)

- (21) Grimmett, G., Suen, W.S.: The maximal flow through a directed graph with random capacities. Stochastics: An International Journal of Probability and Stochastic Processes 8(2), 153–159 (1982)

- (22) Harris, T.E.: The existence of stationary measures for certain markov processes

- (23) Harrison, J.M., Williams, R.J.: Multidimensional reflected brownian motions having exponential stationary distributions. The Annals of Probability pp. 115–137 (1987)

- (24) Hassin, R., Zemel, E.: Probabilistic analysis of the capacitated transportation problem. Mathematics of operations research 13(1), 80–89 (1988)

- (25) Kang, W., Ramanan, K., et al.: Characterization of stationary distributions of reflected diffusions. The Annals of Applied Probability 24(4), 1329–1374 (2014)

- (26) Karlan, D., Mobius, M., Rosenblat, T., Szeidl, A.: Trust and social collateral. The Quarterly Journal of Economics 124(3), 1307–1361 (2009)

- (27) Kirchhoff, G.: Ueber die auflösung der gleichungen, auf welche man bei der untersuchung der linearen vertheilung galvanischer ströme geführt wird. Annalen der Physik 148(12), 497–508 (1847)

- (28) Kleitman, D.J., Winston, K.J.: Forests and score vectors. Combinatorica 1(1), 49–54 (1981)

- (29) Li, K.: The blockchain scalability problem & the race for visa-like transaction speed, https://hackernoon.com/the-blockchain-scalability-problem-the-race-for-visa-like-transaction-speed-5cce48f9d44

- (30) Lin, J.S., Jane, C.C., Yuan, J.: On reliability evaluation of a capacitated-flow network in terms of minimal pathsets. Networks 25(3), 131–138 (1995)

- (31) Lovász, L., Vempala, S.: Hit-and-run is fast and fun. preprint, Microsoft Research (2003)

- (32) Lovász, L., Vempala, S.: The geometry of logconcave functions and sampling algorithms. Random Structures & Algorithms 30(3), 307–358 (2007)

- (33) Nakamoto, S., et al.: Bitcoin: A peer-to-peer electronic cash system (2008)

- (34) Poon, J., Dryja, T.: The bitcoin lightning network: Scalable off-chain instant payments (2016)

- (35) Ramseyer, G., Goel, A., Mazières, D.: Liquidity in credit networks with constrained agents. In: Proceedings of The Web Conference 2020. pp. 2099–2108 (2020)

- (36) Semple, C., Welsh, D.: Negative correlation in graphs and matroids. Combinatorics, Probability and Computing 17(3), 423–435 (2008)

- (37) Shephard, G.C.: Combinatorial properties of associated zonotopes. Canadian Journal of Mathematics 26(2), 302–321 (1974)

- (38) Smith, R.L.: Efficient monte carlo procedures for generating points uniformly distributed over bounded regions. Operations Research 32(6), 1296–1308 (1984)

- (39) Stanley, R.P.: Decompositions of rational convex polytopes. Ann. Discrete Math 6(6), 333–342 (1980)

Appendix A Section 3 Omitted Proofs

A.1. Proof of Theorem 3.3

Proof A.1.

There are, in fact, many spanning representations. This is unsurprising, given that graphical matroids are representable over , and the dimension of any basis of the graphical matroid is . It suffices to show that there exists a matroid representation such that summing along a cycle results in , not just that the set of vectors corresponding to a cycle forms a linearly dependent set.

As a concrete example, let be a spanning tree, and let be a basis for . Correspond the edges in with . For any other edge with , let be the path from to in , and set .

Then clearly the direction walking along the cycle formed by with is .

Note that the direction summation is clearly additive. In other words, if a path runs from to and a path runs from to , then the direction of plus the direction of is equal to the direction of the concatenation of and .

Observe that walking from to , and then back along the same path, gives a path whose sum is . In fact, any path from to that visits a vertex twice can be decomposed into a path directly from to plus a path from to itself. Sufficiently repeating this decomposition shows that the sum along every path in from to has the same summation. Note that because form a basis for , this summation is if and only if .

For any other path , if , then, by the construction, the summation of the path along is equal to the summation along the path , where is a path from to in . Repeating this process until all edges are in shows that has direction if and only if is a cycle.

A.2. Proof of Theorem 3.5

Proof A.2.

-

1

This follows from part 2. Assuming part 2, if transactions along cycles take to , then, because cycles have direction , .

-

2

Suppose that a path is feasible in configuration .

By rearranging the summations, we get that

-

3

Let be the reversal of . Then concatenated with forms a cycle, and concatenated with forms a cycle, so

A.3. Proof of Theorem 3.7

Proof A.3.

This theorem follows almost directly from the construction. If a vector is expressable as a Minkowski summation with coefficients , then the weight map , defined by if and otherwise, forms a feasible network configuration. Conversely, if , then , so is representable as a Minkowski sum of the vectors of interest.

A.4. Proof of Corollary 3.8

Proof A.4.

Let be the space of configurations under a spanning representation. Let and be in . Clearly, if , that is, and are cycle-equivalent, then for any transaction , if and only if .

Suppose that and are transaction-equivalent but not cycle-equivalent. Then the generalized transaction is feasible starting from and takes to . Let . Because is convex, the transaction is feasible starting from but not from , which gives a contradiction.

Appendix B Section 4 Omitted Proofs

B.1. Proof of Theorem 4.3

Proof B.1.

Let be a transaction model on , and let be some spanning representation.

Let be the transition kernel of Markov Chain 1 using transaction distribution , and let be any continuous, bounded function on the compact state space . By Theorem 1.10 of eberle2009markov , it suffices to show that if a sequence converges to , then goes to . But is the weighted sum of continuous, bounded functions, so this holds.

B.2. Proof of Theorem 4.4

Proof B.2.

Let be a transaction model on , let be the transition kernel of Markov Chain 1 using transaction distribution , and let be some spanning representation.

Let be the image under of the entire space of configurations, and let be some invariant distribution.

Note that it is equivalent to view the set of transacting pairs, , as a set of vectors . Moreover, is connected if and only if spans .

By Theorem 1 of harris1956existence , it suffices to show that if a set has nonzero measure, then from any starting point , the Markov Chain must visit infinitely many times in expectation.

Note that it suffices to show that for all , there is some such that . If this holds for all , then in expectation, the chain starting at will visit in a finite number of steps. After this, the chain could either stay in forever (in which case, the chain trivially visits infinitely many times), or it will leave to some .

Suppose that spans .

Because each is supported on , for any , the conditional distribution started at and running for steps has support on an ball (subset of ) of radius around . By the same argument, after steps, the conditional distribution started at has support on an ball (subset of ) of radius . Because is bounded, for sufficiently large , the support of the conditional distribution has measure equal to .

Suppose Markov Chain 1 only returns to some set finitely many times in expectation. Then is not in the support of the conditional distribution, and must have measure .

B.3. Proof of Theorem 4.5

Proof B.3.

Let be a transaction model on , let be the transition kernel of Markov Chain 1 using transaction distribution , and let be some spanning representation.

It suffices to show that for any measurable set , , where is a uniform measure on .

A transaction corresponding to a vector starting from point lands in if either – that is, the transaction succeeds and results in a state in – or if and – that is, the transaction fails and the initial state was already in . Note also that for any fixed , these events are mutually exclusive. Hence, the sets and are disjoint.

Note also that .

Translating by gives the set . Because is uniform on and both of these sets are fully contained in , we get that

Note also that the sets and form a disjoint partition of . Hence, , and thus

| (2) |

Expanding terms thus gives

Changing order of integration, we get

Because is symmetric, using equation 2, we can rearrange the integral above into

Hence, is stationary in Markov Chain 1.

B.4. Proof of Theorem 4.7

Proof B.4.

First, note that for a spanning tree , under any spanning representation, the vectors corresponding to form a basis for . Moreover, the behavior of a spanning representation on one spanning tree uniquely determines its behavior on all other edges. Thus, any spanning representation is the result of a linear transformation of another spanning representation.

Let and be two spanning representations, and let be the (nonsingular) matrix such that for all , . Let be the vector under corresponding to some transaction, and let be vector under for that same transaction. Let be the space of represented cycle-equivalent configurations under , and let be the space of represented cycle-equivalent configurations under . Finally, let be a density function on and let be the density function on such that for .

It suffices to show, therefore, that

The argument follows from a change of variables. We note that stretching the representation space should necessarily stretch the density function. Note that

and

Because is invertible and , the equality holds.

Appendix C Section 5 Omitted Proofs

C.1. Proof of Theorem 5.3

Proof C.1.

If is a set of vectors in , define as the determinant of the matrix where elements of are interpreted as column vectors.

By (57) of shephard1974combinatorial , the volume of the Minkowski sum of a set of vectors is equal to . The rest of this proof follows from basic facts about the determinant.

Let be the set of vectors corresponding to the directions under a spanning representation of edges in the underlying payment network . By assumption, maps some spanning tree to the standard basis .

For any linearly independent set of size , we would like to show that . Note that a set of vectors in is linearly independent if and only if the set is the set of directions under of a spanning tree in .

Suppose for induction that the set of vectors is the set of directions of a spanning tree in , contains , , and . Set .

If , then set to and the induction hypothesis holds. Otherwise, viewed as edges in , the set contains a single simple cycle. Say that the vectors corresponding to edges in this cycle are . Because is a spanning representation, for .

Set . Then by the linearity of the determinant, we can substitute the column corresponding to with the summation and expand to get that . Hence , and the induction hypothesis holds.

Since , the above induction shows that .

As such, the nonzero elements of the summation correspond exactly to the spanning trees of the underlying graph. This proves the theorem in the case where every edge has capacity . The general result follows from the multilinearity of the determinant.

C.2. Proof of Theorem 5.6

Proof C.2.

This is a general fact about Minkowski summation, but we include here a proof for completeness.

Let be the original credit network where , and let be a credit network where the capacity along has been reduced by (i.e. the capacities of edges in are ). Without loss of generality, assume corresponds to a transaction in the direction along that the spanning representation denotes as positive.

Let be the image of the set of configurations of , and let be the image of the set of configurations of from which transaction succeeds.

Let be the image of the set of configurations of (under the same spanning representation).

Clearly (directly as subsets of ). If is a configuration of , then , so the configuration except is a configuration of that maps to the same point in .

To show that , it suffices to show that each is the image of some configuration of where . Given such a configuration, we can construct a configuration as except that . Then is a configuration of .

Let be some configuration of from which transaction is successful. Then from configuration , can send at least units of money to . If , then there must be some other paths in that enable to send units of money to . But then is cycle-equivalent to a configuration constructed from by sending units of money from to through paths not using edge and then back to along edge .

Hence, .