Bias-Optimal Vol-of-Vol Estimation: The Role of Window Overlapping

Abstract

The simplest and most natural vol-of-vol estimator, the pre-estimated spot variance based realized variance (PSRV), is typically plagued by a large finite-sample bias. In this paper, we analytically show that allowing for the overlap of consecutive local windows to pre-estimate the spot variance may correct for this bias. In particular, we provide a feasible rule for the bias-optimal selection of the length of local windows when the volatility is a CKLS process. The effectiveness of this rule for practical applications is supported by numerical and empirical analyses.

Keywords:

stochastic volatility of volatility, high-frequency data, bias optimization, CIR model, CKLS model.JEL codes: C13, C14, C58, G10

1 Introduction

Estimating the volatility of asset volatility (hereinafter vol-of-vol) is relevant in many areas of mathematical finance, such as the calibration of stochastic volatility of volatility models (Barndorff-Nielsen and Veraart, (2009), Sanfelici et al., (2015)), the hedging of portfolios against volatility of volatility risk (Huang et al., (2018)), the estimation of the leverage effect (Kalnina and Xiu, (2017), Aït-Sahalia et al., (2017)), and the inference of future returns (Bollerslev et al., (2009)), along with spot volatilities (Mykland and Zhang, (2009)).

The literature offers a number of consistent estimators for the integrated vol-of-vol. The first estimator to appear was the one proposed by Barndorff-Nielsen and Veraart, (2009), termed pre-estimated spot-variance based realized variance (PSRV), which is, in fact, simply the realized variance of the unobservable spot variance, computed using estimates of the latter. Later, Vetter, (2015) derived two sophisticated versions of the simple PSRV: one that allows for a central limit theorem with the optimal rate of convergence, but also for negative values, and another that preserves positivity at the expense of a slower rate of convergence. Note that the simple PSRV and its sophisticated versions are consistent when the price and volatility processes are continuous semimartingales, in the absence of microstructure noise contaminations. Further, Fourier-based estimators of the integrated vol-of-vol were introduced by Sanfelici et al., (2015) and Cuchiero and Teichmann, (2015). In particular, the estimator by Sanfelici et al., (2015) is asymptotically unbiased in the presence of market microstructure noise, while the estimator by Cuchiero and Teichmann, (2015) allows for a central limit theorem in the presence of jumps in the price and volatility processes.

The numerical studies in Aït-Sahalia et al., (2017) and Sanfelici et al., (2015) show that both realized and Fourier-based integrated vol-of-vol estimators may carry a substantial finite-sample bias unless the selection of the tuning parameters involved in their computation is carefully optimized. However, this is a rather unexplored issue, which we aim to explore. To do so, we focus on the simple PSRV, since it represents the most intuitive and easy-to-implement vol-of-vol estimator. Furthermore, asymptotically-optimal estimators do not necessarily guarantee the best finite-sample performance, as pointed out in the extensive study by Gatheral and Oomen, (2010) on integrated volatility estimators and confirmed for integrated vol-of-vol estimators by the numerical studies in Aït-Sahalia et al., (2017) and Sanfelici et al., (2015). Thus, there is no reason to expect a priori that the simple PSRV would show worse finite-sample performance than its sophisticated version with optimal rate of convergence.

As mentioned, the PSRV is the realized volatility of the unobservable spot volatility process, computed from discrete estimates of the latter. In other words, the PSRV is the sum of the squared increments of estimates of the unobservable spot volatility on a discrete grid. These estimates are obtained as local averages of the price realized volatility. Formally, the locally averaged realized variance and the PSRV are defined as follows.

Definition 1

Locally averaged realized variance

Suppose that the log-price process is observable on an equally-spaced grid of mesh size , with as . Also, let , be a sequence of positive integers such that and define the local window such that as . The locally averaged realized variance at time is defined as

where denotes the floor function.

Definition 2

Pre-estimated spot-variance based realized variance

Suppose that the log-price process is observable on an equally-spaced grid of mesh size , with as . The pre-estimated spot-variance based realized variance (PSRV) on the interval is defined as

where:

-

-

is the locally averaged realized variance in Definition 1, with , ;

-

-

, , is the locally averaged realized variance sampling frequency.

The following propositions summarize the asymptotic properties of the locally averaged realized variance and the PSRV. For further details, see Chapter 8 inAït-Sahalia and Jacod, (2014).

Proposition 1

Let the log-price process be a continuous semimartingale and let the process denote its instantaneous volatility. Then is a consistent local estimator of as .

Proof

See Chapter 8.1 in Aït-Sahalia and Jacod, (2014).

Proposition 2

Let the log-price process and the spot volatility process be continuous semimartingales. Then the PSRV is a consistent estimator of the quadratic variation of the volatility process if and .

Proof

See Proposition 8 in Barndorff-Nielsen and Veraart, (2009).

Remark 1

Note that the requirements for rates and that guarantee consistency imply that as . Indeed, as one can easily verify, and imply which, in turn, implies as .

In practical applications, when computing PSRV values, one has to select the spot volatility estimation grid. Moreover, since the spot volatility is estimated as an average of the price realized volatility over a local window, the length of the latter must also be selected. More specifically, the figure below details the different quantities involved in the computation of the PSRV: the time horizon ; the log-price sampling frequency ; the spot volatility sampling frequency , , ; the size of the local window to estimate the spot volatility , , , ; and the spot volatility estimates , , . Note that denotes the ceiling function.

As a consequence, for given values of the asymptotic rates and , the finite-sample performance of the PSRV (i.e., the performance of the PSRV for a fixed ) depends on the selection of two tuning parameters: , which determines the mesh of the spot volatility estimation grid and , which determines the length of the local window used to estimate the spot volatility.

With regard to the selection of , note that the efficient computation of the spot volatility in finite samples may require the selection of fairly long local windows (see, e.g., Lee and Mykland, (2008), Aït-Sahalia et al., (2013) and Zu and Boswijk, (2014)). This in turn suggests that the finite-sample efficient implementation of the PSRV over a given period (e.g., one day) may require the use of price observations from the previous period(s) (e.g., day(s)). At the same time, this might imply that it is optimal to allow consecutive local windows to overlap in finite samples, that is, for finite. This aspect is confirmed by the numerical study in Sanfelici et al., (2015), which shows that it is optimal to select such that in finite samples. The aim of this paper is to gain insight into the bias-reducing effect due to window-overlapping from an analytic perspective. To do so, we follow an approach inspired by the one used in Aït-Sahalia et al., (2013) to solve the “leverage effect puzzle”.

The “leverage effect puzzle” pertains to the absence of correlation between log-price and (estimated) volatility changes at high-frequencies, observed in empirical samples. Aït-Sahalia et al., (2013) solve this puzzle by showing analytically that a substantial bias masks the presence of correlation unless log-price and volatility estimates changes are computed on a suitably sparse grid. The aim is not to solve the problem of the efficient non-parametric estimation of the leverage at high-frequencies, but rather to obtain insight into the puzzle by solving it in a widely used parametric setting that allows for fully explicit computations. This paper is written in the same spirit. In fact, we do not address the general problem of the efficient non-parametric vol-of-vol estimation from high-frequency prices, but, rather, our aim is to obtain insight from an analytic perspective into why the PSRV, the simplest and most natural vol-of-vol estimator, is plagued by a large bias in finite samples and investigate the role of window-overlapping as a tool for reducing such large bias.

2 Outline of the paper

To achieve this aim, we proceed as follows. In Section 3 we perform a preliminary numerical exercise that uncovers the crucial role of the local-window parameter in determining the finite-sample performance of the PSRV and, at the same time, shows that the latter is basically insensitive to the selection of the grid parameter . In particular, it is evident from simulations that the PSRV finite-sample bias is optimized by selecting such that consecutive local windows to estimate the spot volatility overlap. Numerical results of Section 3 confirm those by Sanfelici et al., (2015) and motivate the analytic study of Section 4.

In Section 4, we address the problem of the optimal selection of PSRV tuning parameters in finite samples from an analytic perspective. To do so, in the spirit of Aït-Sahalia et al., (2013), we assume a widely-used parametric form for the data-generating process, which allows us to obtain the full explicit PSRV finite-sample bias expression. Specifically, we assume the price to be a continuous semimartingale and the volatility to be a CIR process (see Cox et al., (1985)). In general, independently of the parametric assumption on the data-generating process, the PSRV finite-sample bias expression differs in case window overlapping is allowed, i.e., when , or not, i.e., . Consequently, in Section 4 we study both cases.

In the no-overlapping case we adopt a conventional approach and isolate the dominant term of the bias as , thereby showing that a value of that annihilates the dominant term of the bias does not always exist and, even when it does exist, its computation would be basically unfeasible in practice, as it depends on the drift parameters of the volatility, which cannot be reliably estimated on a fixed time horizon, due to the fact that their consistent estimation is possible only in the classic long-sample asymptotics setting (see, e.g., Kanaya and Kristensen, (2016)). In addition, when the optimal value of exists, for typical orders of magnitude of the CIR parameters it actually satisfies the no-overlapping constraint only at ultra-high frequencies ( second).

In the overlapping case, instead, the natural expansion as is precluded, as the consistency of the PSRV requires that consecutive windows do not overlap as the number of price observations grows to infinity (see Remark 1). Therefore, in this case we adopt a novel approach and expand sequentially the bias expression as the tuning parameter and the time horizon go to zero, based on the fact that, in practical applications, and are typically very close to zero. This approach yields a dominant term of the bias which is independent of the tuning parameter and is annihilated by selecting the asymptotic rate of as , the asymptotic rate of as , and the local-window tuning parameter as , where and denote, respectively, the spot variance process at the initial time and the CIR diffusion parameter. This analytic result shows that, when overlapping is allowed, it is possible to select such that the bias is effectively optimized in practical applications and supports the numerical evidence on the bias-reducing effect due to window overlapping collected in Section 3 and in Sanfelici et al., (2015). However, this rule to select is unfeasible unless reliable estimates of and are available. Accordingly, in Appendix B we detail a simple procedure to estimate and .

In Section 4 we also address the problem of the bias-optimal implementation of the PSRV in the more realistic situation where the price process is contaminated by an i.i.d. microstructure noise process at high frequencies. Again, we distinguish between the overlapping and no-overlapping case and derive, for each case, the exact parametric expression of the extra bias term due to microstructure noise. However, in both cases it emerges that this extra term depends not only on some moments of the noise process but also on the drift parameters of the volatility process, which cannot be consistently estimated over a fixed time horizon (see, e.g., Kanaya and Kristensen, (2016)). This precludes the possibility of efficiently subtracting the bias due to noise in small samples. As a solution, we suggest sampling prices on a suitably sparse grid as in the seminal paper by Andersen et al., (2001), so that the presence of noise becomes negligible and the bias optimal rule to select the local-window parameter can still be applied. The efficiency of this solution is verified numerically in Section 6 for typical values of the noise-to-signal ratio. For completeness, we also analyze the noise bias expression in the no-overlapping case. In particular, we exploit this expression to derive the asymptotic rate of divergence of the PSRV bias as tends to infinity.

Additionally, as a byproduct of the PSRV bias analysis, in Section 4 we quantify the bias reduction following the assumption that the initial value of the volatility process is equal to the long-term volatility parameter, in the case of both the PSRV and the locally averaged realized variance. This is a very common assumption in the literature, typically made in simulation studies where a mean-reverting process drives the spot volatility (see, e.g., among many others, Aït-Sahalia et al., (2013), Sanfelici et al., (2015), Vetter, (2015)).

In Section 5 we use a heuristic approach based on dimensional analysis to generalize the rule for the selection of to the case of a volatility process belonging to the CKLS class (see Chan et al., (1992)). Specifically, we find that it is optimal, in terms of bias reduction, to select , where is the variance process and is the variance-of-variance process, while is the initial time of the estimation horizon. Note that in the absence of price and volatility jumps (a condition required for the PSRV to be consistent), the semi-parametric stochastic volatility model where the price is a semimartingale and the volatility is a CKLS process represents a fairly flexible model. In fact, the CKLS framework encompasses a number of widely-used models for financial applications. Indeed, besides the CIR model, which determines the volatility dynamics in the popular Heston model (Heston, (1993)) and its generalized version with stochastic leverage by Veraart and Veraart, (2012), the CKLS family includes, e.g., the model by Brennan and Schwartz, (1980) and the model by Cox et al., (1980), which appear, respectively, in the continuous-time GARCH stochastic volatility model by Nelson, (1990) and 3/2 stochastic volatility model by Platen, (1997).

In Section 6 we perform an extensive numerical study where we test the performance of the feasible rule to select derived in Section 4 and generalized in Section 5. The results confirm that this rule is effective in reducing the PSRV bias. We underline that this rule does not require the estimation of the drift parameters of the CIR process, which can not be consistently estimated on a fixed time horizon. Finally, in Section 7 we illustrate the results of an empirical study, in which we compute PSRV values from high-frequency S&P 500 prices, selecting based on the bias-optimal rule. Section 8 summarizes our conclusions. Finally, Appendix A contains the proofs and Appendix B illustrates the feasible procedure that we propose to select from sample prices.

3 Preliminary results

The finite-sample accuracy of the PSRV requires the careful selection of the tuning parameters and . In this section we gain some preliminary insight into this issue by performing a numerical study, whose result motivate the analytic investigation of Section 4. In particular, we simulate observations from the following data-generating process, where the volatility is a CIR process. Note that this data-generating process is also used for the analytic study in Section 4.

Assumption 1

Data-generating process

For , , the dynamics of the log-price process and the spot volatility process read:

where and are two Brownian motions on , is the initial price, and the strictly positive constants and denote, respectively, the initial volatility and the speed of mean reversion, long-term mean and vol-of-vol parameters. We also assume that to ensure that is a.s. positive .

In particular, we simulate one thousand 1-year trajectories of 1-second observations, with a year composed of 252 trading days of 6 hours each. We consider three scenarios determined by the following sets of model parameters: Set 1: ; Set 2: ; Set 3: .

The first set of parameters, Set 1, is taken from Sanfelici et al., (2015) and Vetter, (2015) and is used as the baseline scenario. The second, Set 2, represents the opposite scenario. In fact, the volatility generated by Set 2 is lower than the volatility generated by Set 1, since the long term mean, , and the speed of mean reversion, , are, respectively, much lower and much higher than in Set 1. The second scenario is also characterized by a lower volatility of the volatility, which is captured by the parameter and a more pronounced leverage effect, which is captured by the correlation parameter . The third set of parameters, Set 3, differs from the first only in that the initial value of the volatility, , is twice the long term volatility, . In this regard, note that if the initial volatility is equal to , the spot volatility has a constant unconditional mean over time under Assumption 1 (see Appendix A in Bollerslev and Zhou, (2002)). Setting is a simplifying assumption typically adopted in numerical studies where a mean-reverting volatility process is used (see, e.g., among many others, Aït-Sahalia et al., (2013), Sanfelici et al., (2015), Vetter, (2015)).

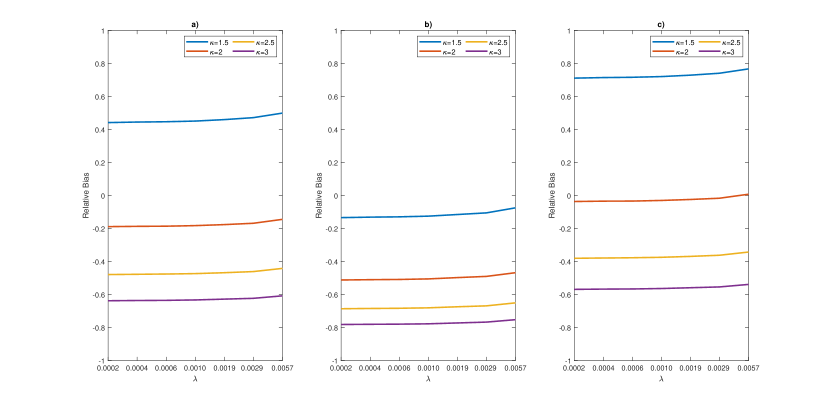

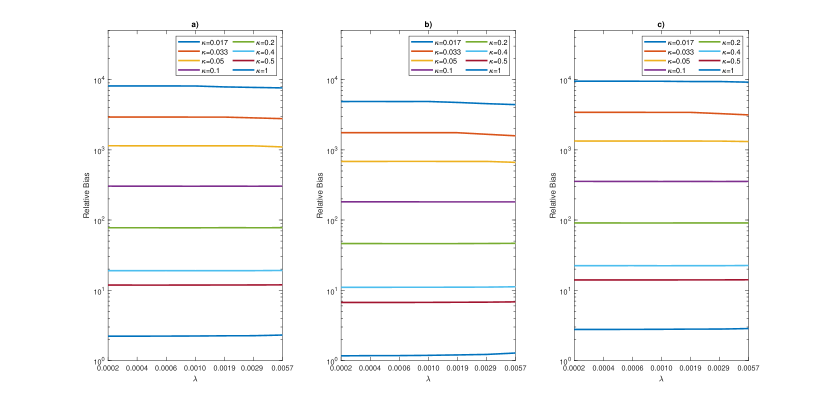

We estimate daily values of the PSRV in these three scenarios from simulated prices sampled with a 1-minute frequency. For the estimation, we set and 111This choice of and satisfies the constraints for asymptotic unbiasedness (see Theorem 4.2). Moreover, note that the selection is also performed in the numerical exercises of Aït-Sahalia et al., (2017) and Sanfelici et al., (2015). and study the sensitivity of the bias to different values of and . With respect to , we consider values in the set , which correspond to equal to minutes, respectively, thereby preserving the high-frequency nature of the estimator. As for , we consider values in the set , which correspond to equal to (approximately) minutes, respectively. Overall, these sets of values for and allow us to consider both cases when window overlapping occurs, that is when , and cases when it does not occur, that is when . Figure 2 summarizes the results of the numerical exercise for values of that lead to a relative bias smaller than an absolute value of . This happens for . Instead, for smaller than , the relative bias rapidly explodes for all values of considered, as shown in Figure 3.

As one can easily verify, the values of in Figure 2 imply that local windows for estimating the spot volatility overlap, for all values of considered. Consequently, Figure 2 tells us that window overlapping is crucial in order to optimize the relative bias of the PSRV even when . This confirms the numerical results in Sanfelici et al., (2015). Furthermore, one can also easily check that the combinations of and such that overlapping does not occur are all included in Figure 3, where the relative bias is larger than and rapidly increases as becomes smaller, for any considered, reaching the order magnitude when equals minutes.

Moreover, focusing on Figure 2, it is worth noting that the bias-optimal selection of is strongly dependent on the parameters of the data-generating process. In fact, the same value of may lead to very different values of the bias in the three scenarios considered: for instance, the selection leads to a relative bias of approximately in scenario 1, in scenario 2 and in scenario 3. At the same time, Figure 2 also tells that the bias is not very sensitive to the selection of . Finally, Panel a) of Figure 2 suggests that, for all values of considered, the bias-optimal value of is close to 2 in scenario 1. This indication is in line with the numerical findings by Sanfelici et al., (2015), where, based on the same parameter set as in scenario 1, the optimal value of is found to be approximately equal to 2.

In sum, our preliminary numerical study shows not only that allowing for window overlapping is critical to avoid obtaining highly biased vol-of-vol estimates, but also that the selection of is crucial for optimizing the PSRV finite-sample bias and, in particular, it is critical to uncover the dependence between the bias-optimal value of and the parameters of the data-generating process. Gaining a more in-depth understanding of these numerical findings is what motivates our analytic study in the next section.

4 Analytic results

In this section we analyze the PSRV finite-sample bias in a parametric setting, namely assuming that the volatility is a CIR process, so that a fully explicit formula of the latter can be obtained. We treat the overlapping case (i.e., the case when ) and the no-overlapping case (i.e., ) separately as, in general, the finite-sample bias expression differs in the two cases, independently of the parametric model used. Lemma 1 details the explicit expression of the PSRV bias for fixed.

Lemma 1

Let Assumption 1 hold, with independent of . Further, let be fixed. If , the bias of the PSRV in Definition 2 reads

| (1) |

Instead, if , it reads

| (2) |

Proof

See Appendix A.

Remark 2

The bias in the case differs from that in the case for the presence of the extra term , which appears due to the fact that the parametric expression of differs in the two cases. See the proof of Lemma 1 for the definition of the quantity , which is only used in the Appendix, and further details.

Remark 3

The explicit bias expression in Lemma 1 is derived under the simplifying assumption that is independent of , which rules out leverage effects. The sensitivity of the PSRV bias to the presence of leverage effects is studied numerically in Section 6, where simulations suggest that such effects are a negligible source of finite-sample bias, thereby preserving the practical relevance of the results derived in this section. In the literature, numerical and empirical studies of the impact of leverage effects on analytical results derived under the no-leverage assumption are found, e.g., in Barndorff-Nielsen and Shepard, (2006), Mancino and Sanfelici, (2008) and references therein.

In the next subsections we investigate the existence of a rule to select the tuning parameters and in both the cases and . To do so, we first isolate the leading term of the bias in each case and then verify whether the latter can be canceled by an selection of tuning parameters. We address overlapping case first, as it is the one relevant for practical applications, based on the results of the simulation studies in Section 3 and in Sanfelici et al., (2015).

4.1 The relevant case for practical applications:

When , the natural expansion of the bias as the number of sampled price observations tends to infinity is precluded, because the consistency of the PSRV requires that as . Thus, we determine the leading term of the bias through an alternative asymptotic expansion, which exploits some natural, non-restrictive constraints on the magnitude of the tuning parameter and the time horizon . Specifically, we first regard the bias in equation (2) as a function of and we perform its Taylor expansion with base point . Then, regarding each term of this expansion as a function of , we perform their Taylor expansions with base point . The choice of the base point is supported by the fact that the largest feasible values of are very small, e.g., on the order of when and is equal to one minute (see Figure 2 for the case ). Note that a value of is feasible if it satisfies . The choice of base point is instead supported by the fact that in the literature on high-frequency econometrics, the typical time horizon used to estimate the integrated quantities is one trading day, i.e., . The order of this sequential expansion is rather natural: intuitively, we first take the limit 0 to approximate the integral of the vol-of-vol in an infill-asymptotics sense, then take the limit 0 to localize the estimate of the integral near the initial time . This approach leads to the following result.

Theorem 4.1

Let Assumption 1 hold, with independent of . Further, let . Then, for fixed, as

| (3) |

Moreover, let be the natural filtration associated with the process . Then, for fixed, as

| (4) |

Proof

See Appendix A.

Remark 4

Remark 5

The conditional bias expansion in equation (4) allows the dominant term of the bias to be expressed in terms of and , two quantities that can be consistently estimated over a fixed time horizon. This is crucial for the existence of a feasible procedure to select , as detailed below. Instead, the unconditional expression in equation (3) depends on , whose parametric expression in turn depends on the drift parameters of the volatility and thus cannot be consistently estimated over a fixed time horizon (see, e.g., Kanaya and Kristensen, (2016)). In particular, it holds (see equation (4) in Section 2.2.1 of Bollerslev and Zhou, (2002)).

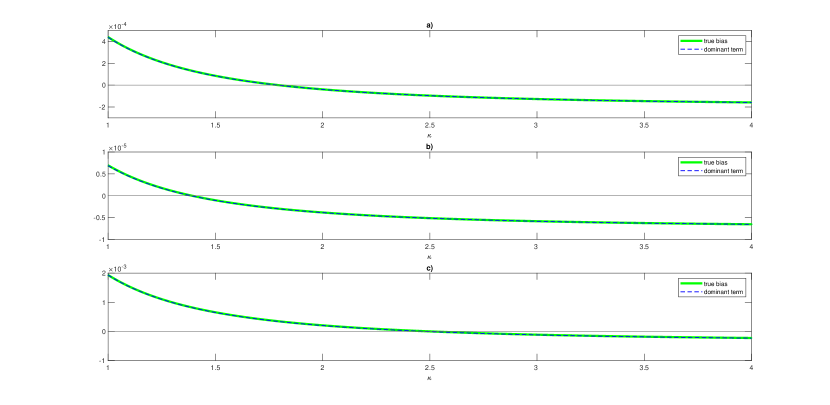

Figure 4 compares the true finite-sample bias of the daily PSRV in equation 2 with the dominant term of the expansion in equation 3 as functions of the tuning parameter . Specifically, the panels refer to the three parameter sets already used in Section 3, that is Set 1 (panel a)), Set 2 (panel b)), and Set 3 (panel c)). Note that we have set , , , , and . The corresponding and are equal to 1 minute and (approximately) 3 minutes, as we consider 6-hr trading days. The approximation of the true bias with the dominant term of the expansion is very accurate.

Based on the conditional bias expansion in equation (4), we make the following considerations on the optimal selection of tuning parameters in finite samples. First, we note that the dominant term of the bias can be annihilated simply by suitably selecting for any feasible value of when , . Instead, when , , the dominant term of the bias is independent of and . Specifically, when , , the suitable selection is

| (5) |

However, since is a tuning parameter, it is not allowed to depend on . Therefore, the only admissible choice is and , so that the suitable selection becomes

| (6) |

Further, if , then (see equation (4) in Section 2.2.1 of Bollerslev and Zhou, (2002)) and thus, based on equation (3), it is immediate to see that the bias-optimal value of reduces to Interestingly, this analytic result supports the optimal selections of and determined numerically in the literature. Indeed, for the first parameter set in the numerical exercise in Section 3, Set 1, which is also used in Sanfelici et al., (2015), is equal to , a value compatible with the numerical result in Sanfelici et al., (2015), where the optimal is said to be approximately equal to . Note also that the numerical studies in Aït-Sahalia et al., (2017), Sanfelici et al., (2015) both select . With regard to this selection of , the following remark is in order.

Remark 6

The selection does not satisfy the consistency constraint in Proposition 2. However, to achieve consistency, it is sufficient to select and , with strictly positive but arbitrarily small and, for such selection of , bearing in mind (5), the impact of on the optimal selection of will be negligible in finite-sample exercises. Therefore, in finite-sample exercises we can select as in (6).

Furthermore, the following remark regarding the selection is in order.

Remark 7

The overlapping condition implies a constraint on the price grid . In particular, if , for , , is equivalent to . The threshold is very small for typical orders of magnitude of and , corresponding to one trading day and any feasible value of . For example, for the values of the parameters in Set 1 (see Section 3), and (so that, if minute, then minutes), we have seconds and thus the constraint is largely satisfied at the most commonly available price sampling frequencies.

However, Equation (6) implies that the bias-optimal selection is unfeasible unless reliable estimates of and are available. In Appendix B we detail a simple feasible procedure to obtain . In a nutshell, the procedure is as follows. First, we estimate using the Fourier spot volatility estimator by Malliavin and Mancino, (2009). Then we estimate via a simple indirect inference method.

4.2 The case

The finite-sample bias expression for in equation (1) is the starting point to derive the asymptotic constraints on rates and that ensure the asymptotic unbiasedness of the PSRV. In this regard, we obtain the following result, which is based on the asymptotic expansion of the bias in the limit .

Theorem 4.2

Let Assumption 1 hold, with independent of . Then, if and or and , as and the PSRV as given in Definition 2 is asymptotically unbiased, i.e.,

In particular, as ,

| (7) |

where:

Proof

See Appendix A.

A bias-optimal rule for the selection of the tuning parameters and when is given in the following corollary to Theorem 4.2. Unfortunately, this bias-optimal rule is of little interest for practical applications, as explained in Remark 8.

Corollary 1

The leading term of the PSRV finite-sample bias expansion in Eq. (7) can be canceled in the case and , provided that there exists a solution to the following system:

If a solution exists, the corresponding bias-optimal selection of and reads

Proof

See Appendix A.

Remark 8

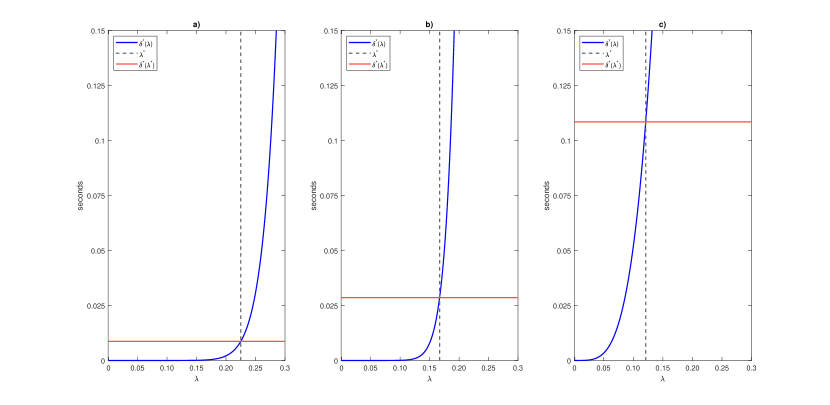

For and , the no-overlapping condition is equivalent to . Assuming that a positive solution to exists for some , we define the “no-overlapping” threshold for as . For the three sets of CIR parameters used in the numerical study in Section 3, Figure 5 plots the threshold as a function of , where is the largest admissible value of such that , i.e., such that when is equal to the “no-overlapping” threshold. Specifically, Figure 5 shows that the sampling frequency corresponding to is bounded by a value smaller than, respectively, (see Panel a)), (see Panel b)) and seconds (see Panel c)). This suggests that for typical values of the CIR parameters, the system in Corollary 1 may be solved only for ultra-high frequencies. Also, note that the solution (if it exists) depends on , and , which in turn depend on the expected initial volatility and all CIR parameters, including the drift parameters, which can not be consistently estimated over a fixed time horizon.

4.3 The impact of noise on the bias

In empirical applications one can only observe the noisy price , that is, the efficient price contaminated by a noise component that originates from market microstructure frictions, such as bid-ask bounce effects and price rounding. Here, we assume that the noise component is an i.i.d. process independent of the efficient price process, as in the seminal paper by Roll, (1984). For a general discussion of the statistical models of microstructure noise, see Jacod et al., (2017).

Assumption 2

Data-generating process in the presence of market microstructure noise

The observable price process is given by

where represents the efficient price process and evolves according to Assumption 1 while is a sequence of i.i.d. random variables independent of , such that , and .

The presence of noise clearly changes the PSRV bias expression, introducing an extra term, as illustrated in the following lemma. Note that the parametric form of the extra bias term due to the presence of noise is different in the overlapping and no-overlapping cases.

Lemma 2

Let Assumption 2 hold, with independent of , and let be fixed. Moreover, let denote the PSRV in Definition 2, computed from noisy price observations. If , then

| (8) |

Instead, if , then

| (9) |

The parametric expressions of , , and are as in Lemma 1, while that of the extra term due to the presence of noise (resp., ) in the no-overlapping case (resp., overlapping case) is as follows:

| (10) |

| (11) |

Proof

See Appendix A.

Remark 9

Ideally, in the overlapping case, if one could efficiently estimate the extra bias due to noise and subtract it, then the bias-optimal rule to select could still be applied effectively. Unfortunately, can not be consistently estimated over a fixed time horizon, as it depends on the drift parameters of the volatility and , whose consistent estimation can not be achieved on a fixed time horizon222Note that and can, instead, be estimated consistently for fixed, see for instance Zhang et al., (2005). As a solution, we suggest to sample prices on a suitably sparse grid, as done for the realized variance in the seminal paper by Andersen et al., (2001), so that the extra bias term induced by the presence of noise becomes negligible and the bias optimal rule to select the local-window parameter can still be applied. The efficiency of this solution is verified numerically in Section 6.

Finally, for completeness, we also study the asymptotic behavior of the additional bias due to noise in the no-overlapping case, . More precisely, in the next theorem we derive its rate of divergence as .

Theorem 4.3

Let Assumption 2 hold, with independent of . Moreover, let denote the PSRV in Definition 2, computed from noisy price observations. Then, if either and or and , as and is asymptotically biased, i.e.,

Proof

See Appendix A.

4.4 The bias-reducing effect of the assumption

As mentioned in Section 4.1, if , then . Lemmas 1 and 2 quantify the bias reduction ensuing from assuming that . Indeed, this assumption cuts off the entire source of bias and part of the sources of bias (see equation (10)) or (see equation (11)). The finite-sample bias reduction ensuing from the assumption is not peculiar to the PSRV, though. In fact, this simplifying assumption is also beneficial for reducing the finite-sample bias of the locally averaged realized variance, as shown in the next theorem.

Theorem 4.4

Let Assumption 1 hold. Moreover, let denote the locally averaged realized variance in Definition 1 at time . Then, if , is asymptotically unbiased, i.e.,

and, as , we have

Let Assumption 2 hold. Moreover, let denote the locally averaged realized variance in Definition 1 at time computed from noisy price observations. Then, , is asymptotically biased, i.e.,

and, as , we have

Proof

See Appendix A.

This theorem has two interesting implications. First, under Assumption 1, the locally averaged realized variance is unbiased in finite samples if and only if . Second, under Assumption 2, if , the presence of noise could actually compensate for the negative bias originating from the first term of the bias expression. This also holds for the PSRV finite-sample bias, provided that the term (resp., ) in Lemma 2 is of opposite sign with respect to the sum of the other terms in the bias expression.

5 Generalization via dimensional analysis

In this section we propose a heuristic approach, based on dimensional analysis, to generalize the rule for the bias-optimal selection of in equation (6), derived under the assumption that the volatility is a CIR process, to the more general case where the volatility follows a process in the CKLS class (see Chan et al., (1992)). Specifically, the stochastic volatility model we assume as the data-generating process is now as follows.

Assumption 3

Data-generating process

For , , the dynamics of the log-price process and the spot volatility process follow

where and are two correlated Brownian motions on , is a continuous adapted process, , , and if .

The stochastic volatility model in Assumption 3 is quite flexible to reproduce empirical prices behaviour in the absence of price and volatility jumps. In fact it incorporates a number of widely-used stochastic volatility models with continuous price and volatility paths as special cases. For example, if , one obtains the model by Heston, (1993); if one finds the continuous-time Garch model by Nelson, (1990); if , one gets the 3/2 model by Platen, (1997). Further, by allowing for a stochastic correlation between and , Assumption 3 includes also the generalized Heston model with stochastic leverage introduced by Veraart and Veraart, (2012). Finally, note that Assumption 3 also includes a price drift. The numerical study in Section 6 confirms that the impact of the latter on the PSRV finite-sample bias is negligible.

We now use dimensional analysis to heuristically derive a rule for the bias-optimal selection of under Assumption 3. We test the efficacy of this rule in the numerical study of Section 6, with overwhelming results. Note that dimensional analysis is typically used in physics and engineering to make an educated guess about the solution to a problem without performing a full analytic study (see, e.g., Kyle and Obizhaeva, (2017), Smith et al., (2003)).

The basic concept of dimensional analysis is that one can only add quantities with the same units333Dimensional analysis is also called a unit-factor method or a factor-label method, since a conversion factor is used to evaluate the units.. Accordingly, when applying dimensional analysis, the first step entails identifying the units of the quantities appearing in the equations being studied. In this specific analysis, we start with the units of the quantities appearing in the model given in Assumption 3. Let denote the unit/dimension of the quantity . The log-return , , is a dimensionless quantity (i.e., a pure number) since it is the logarithm of a ratio of prices (the ratio of quantities with the same units is dimensionless). Instead, the quadratic variation of the Wiener processes and has the dimension of since and are continuous random walks. As a consequence, we have (see, for example, Wilmott, (2000) or the square-root-of-time rule in Danielsson and Zigrand, (2006)). Now consider the dynamics of the log-price, bearing in mind that we cannot add or subtract quantities with different measurement units. The dimension of the left-hand side must then be equal to those of the addenda on the right-hand side, thereby implying that and . Thus, from the dynamics of , we have , and . The latter implies . Therefore, bearing in mind that , we obtain .

Now, without loss of generality, let and consider the dominant term in the expansion of Theorem 4.1, i.e., the term

Since the dominant term of the PSRV bias must clearly have the same dimension as the expected quadratic variation of over any generic interval of length , i.e., , we have

and, as one can easily verify, this implies (alternatively, one can show that by simply noting that is dimensionless and ).

Now observe that the leading term of any expansion of the PSRV finite-sample bias must have dimension equal to . Based on this observation, we conjecture that the leading term of the expansion in Theorem 4.1 under Assumption 3 is

whose dimension is , as one can easily check by recalling that , and . Accordingly, if one conditions the bias to the natural filtration of up to time , the generalized bias-optimal value of , for and , reads

| (12) |

Note that equation (12) can be rewritten in non-parametric form as

where is the vol-of-vol process. This result, while offering insight into the non-parametric solution to the problem of the bias-optimal selection of , is problematic in terms of feasibility as it requires the estimation of the spot vol-of-vol at , a challenging issue which has not been addressed so far in the literature to the best of our knowledge and goes beyond the scope of this paper.

Our conjecture is based on the origin of the two addenda in the leading term of the bias (see Theorem 4.1) in the CIR framework. In fact, bearing in mind the the leading term is

we note that the second addendum, i.e., , comes from the expected quadratic variation of the volatility process. More specifically, it originates from the leading term of the following expansion:

Instead, the first addendum, i.e., , is due to the drift of the volatility process.

Thus in the case of the CKLS model, the first addendum remains unchanged since the drift of the process is the same for any , while the second addendum changes according to the expected quadratic variation of the volatility process, which, for small , reads

since .

6 Numerical results

6.1 Numerical results in the CIR setting

As detailed in Section 4, in the absence of microstructure noise and assuming to be observable and to be known, the finite-sample bias of the PSRV is optimized, under Assumption 1 and for any , by selecting , and . In this subsection, we give numerical confirmation of the optimality of this rule for the selection of in three progressively more realistic scenarios, where incremental sources of biases are added.

In the first scenario, we simulate log-price paths under Assumption 1 and compute daily PSRV values from noise-free price observations assuming that the CIR parameters are known and the initial volatility value is observable. In this scenario, we use two price sampling frequencies, that is, minute and minutes. Results show that the bias generated by the price discrete sampling is relatively small, e.g., less than if minute when (see Table 1).

In the second scenario, we simulate log-price paths under Assumption 2 and compute PSRV values from noisy prices while assuming that the CIR parameters are known and the initial volatility value is observable. As the PSRV is not robust to the presence of noise contaminations in the price process, here we only consider the sampling frequency minutes, as recommended in the seminal paper by Andersen et al., (2001), where the authors suggest that this sampling frequency reduces the impact of noise on returns while still falling within a high-frequency framework. Indeed, a comparison of the numerical results obtained in these first two scenarios shows that the impact of the price noise on the PSRV estimates is relatively small at the 5-minute sampling frequency, when is used.

In the third scenario, we still simulate the log-price path under Assumption 2, but the value of the initial volatility, , is now unobservable and the model parameter is unknown. Thus, we compute PSRV values from noisy prices by selecting . Here, and are obtained through the estimation procedure detailed in Appendix B.

A comparison of the results obtained in these different scenarios shows that

the PSRV finite-sample bias reduction obtained with the feasible selection is very similar to the reduction obtained with the unfeasible selection . For the simulation of each scenario, we use the three realistic sets of parameters from Section 3. For each parameter set, we simulate one thousand 1-year trajectories of 1-second observations.

The noise component in Assumption 2 is simulated as an i.i.d. Gaussian process, with noise-to-signal ratio ranging from 0.5 to 3.5, as in the numerical exercise proposed in Sanfelici et al., (2015). We define the noise-to-signal ratio as in Sanfelici et al., (2015), i.e., , where denotes a generic increment of the i.i.d. process under Assumption 2 and denotes the noise-free log-return at the maximum sampling frequency available, which is equal to 1 second in our numerical exercise. From the simulated prices, we compute daily PSRV values, that is, we set a small time horizon , i.e., . Recall that the bias-optimal rule for the selection of is valid when and . Accordingly, we set and in our numerical study.

Tables 1–3 summarize the results of our numerical exercises and, to make the results of the three parameter sets comparable, we report the values of the relative bias. Since we simulate 6-hr days, is equal to when minute and when minutes. Note that the overlapping condition is always satisfied for the values of in Table 1. In particular, the average length of is approximately equal to: 530 minutes for Set 1, 410 minutes for Set 2 and 580 for Set 3, when minute; 1200 minutes for Set 1, 930 minutes for Set 2 and 1310 minutes for Set 3, when minutes. These averages are computed over all simulated days and are stable across the three scenarios. Recall that the length of varies by day, as it depends on , which in turn depends on the volatility value at the beginning of each day, i.e., (in scenarios 1 and 2), or its estimate, i.e., (in scenario 3).

| noise-to-signal ratio | rel. bias 1(Set 1) | rel. bias (Set 2) | rel. bias (Set 3) | |||

|---|---|---|---|---|---|---|

| 1 min. | (1 min.) | 0.003 | 0.004 | 0.032 | ||

| (2 min.) | 0.006 | 0.006 | 0.033 | |||

| (3 min.) | 0.008 | 0.009 | 0.034 | |||

| (5 min.) | 0.011 | 0.013 | 0.036 | |||

| (10 min.) | 0.021 | 0.025 | 0.041 | |||

| (15 min.) | 0.031 | 0.037 | 0.047 | |||

| 5 min. | (5 min.) | 0.024 | 0.024 | 0.060 | ||

| (10 min.) | 0.029 | 0.029 | 0.061 | |||

| (15 min.) | 0.031 | 0.033 | 0.061 | |||

| (30 min.) | 0.046 | 0.049 | 0.063 |

| noise-to-signal ratio | rel. bias (Set 1) | rel. bias (Set 2) | rel. bias (Set 3) | |||

|---|---|---|---|---|---|---|

| 5 min. | (5 min.) | 0.025 | 0.024 | 0.062 | ||

| (10 min.) | 0.030 | 0.029 | 0.062 | |||

| (15 min.) | 0.032 | 0.036 | 0.064 | |||

| (30 min.) | 0.047 | 0.052 | 0.065 | |||

| 5 min. | (5 min.) | 0.039 | 0.037 | 0.075 | ||

| (10 min.) | 0.044 | 0.043 | 0.076 | |||

| (15 min.) | 0.046 | 0.049 | 0.078 | |||

| (30 min.) | 0.061 | 0.065 | 0.079 | |||

| 5 min. | (5 min.) | 0.064 | 0.064 | 0.102 | ||

| (10 min.) | 0.069 | 0.070 | 0.103 | |||

| (15 min.) | 0.075 | 0.075 | 0.105 | |||

| (30 min.) | 0.091 | 0.091 | 0.107 | |||

| 5 min. | (5 min.) | 0.108 | 0.105 | 0.143 | ||

| (10 min.) | 0.113 | 0.111 | 0.145 | |||

| (15 min.) | 0.115 | 0.117 | 0.146 | |||

| (30 min.) | 0.130 | 0.132 | 0.149 |

| noise-to-signal ratio | rel. bias (Set 1) | rel. bias (Set 2) | rel. bias (Set 3) | |||

|---|---|---|---|---|---|---|

| 5 min. | (5 min.) | 0.059 | 0.011 | 0.046 | ||

| (10 min.) | 0.059 | 0.011 | 0.047 | |||

| (15 min.) | 0.060 | 0.013 | 0.047 | |||

| (30 min.) | 0.060 | 0.017 | 0.047 | |||

| 5 min. | (5 min.) | 0.068 | 0.022 | 0.049 | ||

| (10 min.) | 0.068 | 0.023 | 0.049 | |||

| (15 min.) | 0.069 | 0.024 | 0.049 | |||

| (30 min.) | 0.070 | 0.027 | 0.050 | |||

| 5 min. | (5 min.) | 0.085 | 0.047 | 0.053 | ||

| (10 min.) | 0.088 | 0.049 | 0.053 | |||

| (15 min.) | 0.088 | 0.049 | 0.054 | |||

| (30 min.) | 0.088 | 0.051 | 0.054 | |||

| 5 min. | (5 min) | 0.112 | 0.083 | 0.058 | ||

| (10 min.) | 0.115 | 0.083 | 0.058 | |||

| (15 min.) | 0.117 | 0.084 | 0.059 | |||

| (30 min.) | 0.118 | 0.088 | 0.061 |

Table 1 shows that for minute and minutes, the bias is almost negligible (i.e., less than ) when , while it is slightly larger but still acceptable (i.e., between and ) when . This is in line with equation 2 in Lemma 1, where it is evident that the source of bias is eliminated when , which implies . With a price sampling frequency of five minutes, the bias is still acceptable, around at worst. Additionally, Table 3 shows that in the presence of noise, price sampling at five-minute intervals to avoid microstructure frictions represents an acceptable compromise, as the bias is less than even in the presence of very intense microstructure effects. Finally, Table 3 shows that the statistical error related to the estimation of and could actually partially compensate for the bias due to the presence of noise, especially when the common assumption is violated.

Finally, an important remark is in order. The three realistic parameter sets that we have used all imply the presence of leverage effects, as each includes a negative . To meet the simplifying no-leverage assumption under which the results in Section 4 are derived, for each scenario we have also performed additional simulations under the hypothesis of the independence between the Brownian motion driving the price and the volatility, keeping the same values of the variance parameters , and that characterize the scenario. However, the numerical results obtained in the absence of leverage are basically indistinguishable from those illustrated in Tables 1–3, thereby suggesting that the leverage is a negligible source of bias. Such additional numerical results are not reported here for brevity, but are available from authors.

| Model | rel. bias (Set 1) | rel. bias (Set 2) | rel. bias (Set 3) | |||

|---|---|---|---|---|---|---|

| 1 min. | (1 min.) | 0.014 | 0.012 | 0.027 | ||

| (2 min.) | 0.017 | 0.015 | 0.029 | |||

| (3 min.) | 0.020 | 0.016 | 0.029 | |||

| (5 min.) | 0.024 | 0.022 | 0.031 | |||

| (10 min.) | 0.034 | 0.033 | 0.036 | |||

| (15 min.) | 0.042 | 0.044 | 0.039 |

| Model | rel. bias (Set 1) | rel. bias (Set 2) | rel. bias (Set 3) | |||

|---|---|---|---|---|---|---|

| 1 min. | (1 min.) | 0.003 | 0.002 | 0.011 | ||

| (2 min.) | 0.004 | 0.002 | 0.012 | |||

| (3 min.) | 0.005 | 0.002 | 0.014 | |||

| (5 min.) | 0.006 | 0.003 | 0.015 | |||

| (10 min.) | 0.008 | 0.005 | 0.017 | |||

| (15 min.) | 0.012 | 0.006 | 0.021 |

6.2 Numerical results in the more general CKLS setting

We conclude this section by testing the efficacy of the generalized, conjecture-based, criterion for the bias-optimal selection of under Assumption 3, i.e., under the assumption that the volatility evolves as a CKLS model. In this case, the feasible version of the bias-optimal rule to select is given by , for , .

To test the efficacy of this criterion, we repeat the numerical exercise previously performed in scenario 1 under Assumption 1, considering three different values of : , corresponding to the model by Heston, (1993), which differs from the model of Assumption 1 only in the presence of a price drift; , corresponding to the continuous-time GARCH model by Nelson, (1990); and , corresponding to the 3/2 model by Platen, (1997). For all parameter sets, is set equal to 0.05. Tables 4,5 and 6 show that our general criterion for the bias-optimal selection of under Assumption 3 is effective, as it gives satisfactory results in terms of relative bias. Note that the case is of interest only in that it confirms that the criterion for the bias-optimal selection of derived analytically under Assumption 1, i.e., , is also effective in the presence of a price drift.

| Model | rel. bias (Set 1) | rel. bias (Set 2) | rel. bias (Set 3) | |||

|---|---|---|---|---|---|---|

| 1 min. | (1 min.) | 0.004 | 0.001 | 0.029 | ||

| (2 min.) | 0.004 | 0.002 | 0.031 | |||

| (3 min.) | 0.005 | 0.003 | 0.031 | |||

| (5 min.) | 0.006 | 0.006 | 0.037 | |||

| (10 min.) | 0.006 | 0.007 | 0.038 | |||

| (15 min.) | 0.008 | 0.009 | 0.041 |

7 Empirical study

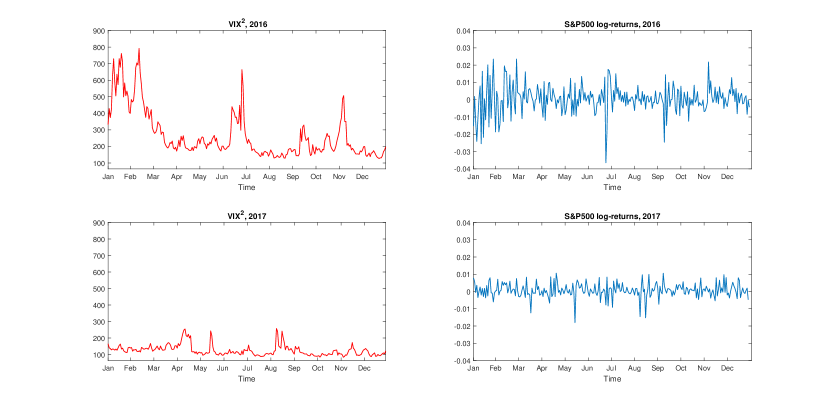

We conclude the paper with an empirical analysis, where we apply the bias-optimal criterion for selecting in equation (12) to compute daily PSRV estimates. The dataset is composed of two 1-year samples of S&P 500 1-minute prices relative to the years 2016 and 2017, respectively. The two samples are analyzed separately since the volatility of these two time series behaves very differently. In fact, the year 2016 is characterized by volatility spikes (due, e.g., to uncertainty pertaining to the so-called Brexit in the month of June or the U.S. presidential election in the month of November), while the year 2017 is characterized by low volatility, as one can see in Figure 6. Analyzing the two series separately allows for validation of the feasible rule for the selection of in two very different scenarios.

We proceed as follows. First, through the method detailed in Appendix B, we obtain non-parametric estimates of the process at the beginning of each day and estimates of under Assumption 3, for the three different values of considered in the numerical exercise of Section 6. The results of the estimation of are shown in Table 7444The estimates of the process at the beginning of each day are not reported for the sake of brevity. See Chapter 4 in Mancino et al., (2017) for a detailed study which demonstrates the finite-sample accuracy of the Fourier estimator of the spot volatility suggested in Appendix B..

| Model | Sample year | ||

|---|---|---|---|

| 2016 | 0.7127 | 0.1383 | |

| 2017 | 0.4250 | 0.1736 | |

| 2016 | 6.1682 | 0.0725 | |

| 2017 | 5.9973 | 0.0901 | |

| 2016 | 72.0358 | 0.1141 | |

| 2017 | 65.1084 | 0.0866 |

Then, based on values, we assume the Heston model () as the data generating process for both samples. Consequently, we select , , and compute daily PSRV values from empirical prices sampled at the frequency minutes. The resulting selection of is approximately equal, on average, to minutes in 2016 and minutes in 2018. Note that the selection minutes is justified by the fact that we assume the impact of microstructure contaminations to be negligible at that sampling frequency, based on the application of the Hausman test by Aït-Sahalia and Xiu, (2019) for the presence of noise, which tells that the impact of noise at the 5-minute frequency is negligible in our samples, confirming a well-known stylized fact (see Andersen et al., (2001)).

Additionally, we have performed the jump-detection test by Corsi et al., (2010). Precisely, we have performed this test on 5-minute returns, as it is not robust to the presence of noise. Based on the results of the jump test, we have computed daily PSRV values from 5-minute prices according to the following procedure for the removal of days with jumps555Note that the analytical results in Section 4 are derived under the assumption of absence of jumps in the price and volatility. The literature on non-parametric jump tests provides large and robust empirical evidence, mainly based on US markets, that volatility jumps are accompanied by price jumps (see, e.g., Jacod and Todorov, (2010); Bandi and Renò, (2016); Bibinger and Winkelmann, (2018)). Thus removing days with price jumps from the estimation basically also takes care of jumps in the volatility. In the absence of jumps, a model in the CKLS class for the volatility could provide a reasonable trade-off between accuracy in reproducing empirical features of prices and parsimony in terms of parameters to be estimated, as pointed out, e.g., in Christoffersen et al., (2010) and Goard and Mazur, (2013).. Assume that time is measured in days and that we are interested in computing the daily PSRV on . Further, without loss of generality, assume that the bias-optimal value of is equal to 2.5 days for equal to 5 minutes. If jumps have occurred within the interval , i.e., on the day of interest or the day before, we do not compute the PSRV on ; if jumps have occurred in , but not in at any instant , , we select to pre-estimate the spot volatility; instead, if jumps have occurred in , but not in , at any instant , we select ; finally, if no jump has occurred within the period , at any instant , we select Overall, based on this procedure, the days for which we do not compute the PSRV amount to of the sample in 2016 and of the sample in 2017.

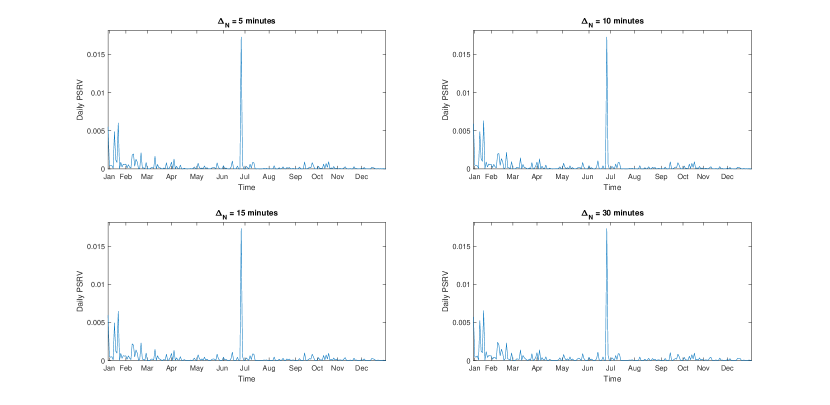

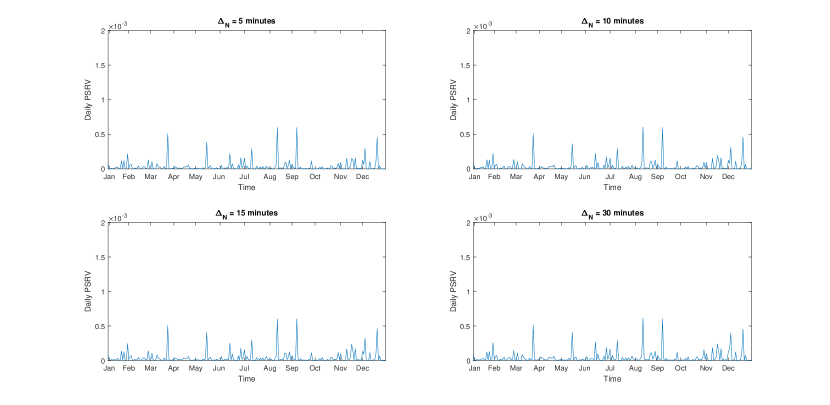

Figures 7 and 8 show the daily PSRV values obtained for four different values of corresponding to a spot volatility estimation frequency equal to 5, 10, 15, and 30 minutes, respectively.

Comparing the dynamics of the VIX2 index in Figure 6 with those of the PSRV, one notices that when the VIX2 spikes, the vol-of-vol also spikes (see, e.g., the behavior of the plots at the end of June 2016) and, viceversa, when the VIX2 is low and stable (e.g., in 2017) the vol-of-vol is also low and stable. This evidence corroborates the goodness of our vol-of-vol estimates. Finally, note that for either of the two samples, the plots for different values of are basically indistinguishable. With respect to the bias-optimal selection of (i.e., ), this evidence confirms what emerges from the analytic study in Section 4: the impact of the selection of (i.e., ) on PSRV values is marginal, if not negligible.

8 Conclusions

The pre-estimated spot-variance based realized variance (PSRV) by Barndorff-Nielsen and Veraart, (2009), the simplest and most natural consistent estimator of the integrated vol-of-vol, is typically affected by a substantial finite-sample bias. The main contribution of this paper is to show, analytically, that local-window overlapping in finite samples effectively reduces this bias. This result confirms the findings of Sanfelici et al., (2015), based on simulations.

The paper is written in the spirit of Aït-Sahalia et al., (2013). In Aït-Sahalia et al., (2013), a parametric data-generating process, namely the Heston model, is used to obtain a fully explicit bias expression for the price-volatility correlation, the most natural leverage estimator, which is very biased at high frequencies. Based on the full explicit knowledge of the bias, the authors are able to isolate the sources of bias that affect the simple leverage estimator and derive a feasible strategy to correct for them. In this paper we follow a similar approach. Assuming that the volatility is a CIR process, we obtain the full explicit expression of the PSRV finite-sample bias. Crucially, we show that this expression differs in the overlapping case and the no-overlapping case and, most importantly, that a feasible bias-correction strategy for finite samples can be derived only in the overlapping case.

Further, using dimensional analysis, we generalize the feasible bias-correction strategy to hold under the assumption that the volatility process belongs to the more general CKLS class, which encompasses a number of widely-used parametric models. Numerical results corroborate the validity of the generalized rule in that nearly unbiased vol-of-vol estimates are obtained for two other models in the CKLS class, namely, the continuous-time GARCH model and the 3/2 model.

In the paper, the impact of microstructure noise on the PSRV bias is also investigated. First, we derive the exact analytic expression of the extra bias due to noise, which differs in the overlapping and no-overlapping cases. This extra bias can not be consistently estimated over a fixed time horizon and then subtracted, as it depends, other than on some moments of the noise process, on the drift of the volatility. As a solution, we propose to apply the feasible rule for the bias-optimal selection of the local-window parameter on sparsely-sampled prices, following Andersen et al., (2001). Numerical evidence of the efficacy of this solution is provided.

Finally, as a byproduct of this analysis, we quantify, for both the PSRV and the locally averaged realized variance, the bias reduction ensuing from the assumption that the initial value of the volatility is equal to its long-term mean, which is very common in simulation studies found in the literature.

Declarations

Funding: Not applicable.

Conflicts of interest: The authors have no conflicts of interests to declare.

Availability of data and material: Not applicable.

Code availability: See supplementary file.

References

- Aït-Sahalia et al., (2017) Aït-Sahalia, Y., Fan, J., Laeven, R., Wang, C. D., and Yang, X. (2017). Estimation of the continuous and discontinuous leverage effects. Journal of the American Statistical Association, 112(520):1744–1758.

- Aït-Sahalia et al., (2013) Aït-Sahalia, Y., Fan, J., and Li, Y. (2013). The leverage effect puzzle: disentangling sources of bias at high frequency. Journal of Financial Economics, 109:224–249.

- Aït-Sahalia and Jacod, (2014) Aït-Sahalia, Y. and Jacod, J. (2014). High-frequency financial econometrics. Princeton University Press.

- Aït-Sahalia and Xiu, (2019) Aït-Sahalia, Y. and Xiu, D. (2019). A hausman test for the presence of noise in high frequency data. Journal of Econometrics, 211:176–205.

- Andersen et al., (2001) Andersen, T., Bollerslev, T., Diebold, F., and Ebens, H. (2001). The distribution of realized stock return volatility. Journal of Financial Economics, 61:43–76.

- Bandi and Renò, (2016) Bandi, F. and Renò, R. (2016). Price and volatility co-jumps. Journal of Financial Economics, 119(1):107–146.

- Barndorff-Nielsen and Shepard, (2006) Barndorff-Nielsen, O. and Shepard, N. (2006). Econometrics of testing for jumps in financial economics using bipower variation. Journal of Financial Econometrics, 4(1):1–30.

- Barndorff-Nielsen and Veraart, (2009) Barndorff-Nielsen, O. and Veraart, A. (2009). Stochastic volatility of volatility in continuous time. CREATES Research Paper, No. 2009-25.

- Bibinger and Winkelmann, (2018) Bibinger, M. and Winkelmann, L. (2018). Common price and volatility jumps in noisy high-frequency data. Electronic Journal of Statistics, 12(1):2018–2073.

- Bollerslev et al., (2009) Bollerslev, T., Tauchen, G., and Zhou, H. (2009). Expected stock returns and variance risk premia. The Review of Financial Studies, 22(11):4463–4492.

- Bollerslev and Zhou, (2002) Bollerslev, T. and Zhou, H. (2002). Estimating stochastic volatility diffusion using conditional moments of integrated volatility. Journal of Econometrics, 109:33–65.

- Brennan and Schwartz, (1980) Brennan, M. and Schwartz, E. (1980). Analyzing convertible securities. Journal of Financial and Quantitative Analysis, 15(4):907–929.

- Chan et al., (1992) Chan, K., Karolyi, G., Longstaff, F., and Sanders, A. (1992). An empirical comparison of alternative models of the short-term interest rate. The Journal of Finance, 47(3):1209–1227.

- Christoffersen et al., (2010) Christoffersen, P., Jakobs, K., and Mimouni, K. (2010). Volatility dynamics for the s&p500: evidence from realized volatility, daily returns and option prices. The Review of Financial Studies, 23(8):3141–3189.

- Corsi et al., (2010) Corsi, F., Pirino, D., and Renò, R. (2010). Threshold bipower variation and the impact of jumps on volatility forecasting. Journal of Econometrics, 159(2):276–288.

- Cox et al., (1980) Cox, J., Ingersoll, J., and Ross, S. (1980). An analysis of variable rate loan contracts. The Journal of Finance, 35:389–403.

- Cox et al., (1985) Cox, J., Ingersoll, J., and Ross, S. (1985). An intertemporal general equilibrium model of asset prices. Econometrica, 53(2):363–384.

- Cuchiero and Teichmann, (2015) Cuchiero, C. and Teichmann, J. (2015). Fourier transform methods for pathwise covariance estimation in the presence of jumps. Stochastic Processes and Their Applications, 125(1):116–160.

- Danielsson and Zigrand, (2006) Danielsson, J. and Zigrand, J. P. (2006). On time-scaling of risk and the square-root-of-time rule. Journal of Banking and Finance, 30:2701–2713.

- Gatheral and Oomen, (2010) Gatheral, J. and Oomen, R. (2010). Zero-intelligence realized variance estimation. Finance and Stochastics, 14(2):249–283.

- Goard and Mazur, (2013) Goard, J. and Mazur, M. (2013). Stochastic volatility models and the pricing of vix options. Mathematical Finance, 23(3):439–458.

- Heston, (1993) Heston, S. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies, 6(2):327–343.

- Huang et al., (2018) Huang, D., Schlag, C., Shaliastovich, I., and Thimme, J. (2018). Volatility-of-volatility risk. Journal of Financial and Quantitative Analysis, page 1–63.

- Jacod et al., (2017) Jacod, J., Li, Y., and Zheng, X. (2017). Statistical properties of microstructure noise. Econometrica, 85:1133–1174.

- Jacod and Todorov, (2010) Jacod, J. and Todorov, V. (2010). Do price and volatility jump together? Annals of Applied Probability, 20(4):1425–1469.

- Kalnina and Xiu, (2017) Kalnina, I. and Xiu, D. (2017). Nonparametric estimation of the leverage effect: a trade-off between robustness and efficiency. Journal of the American Statistical Association, 112(517):384–399.

- Kanaya and Kristensen, (2016) Kanaya, S. and Kristensen, D. (2016). Estimation of stochastic volatility models by nonparametric filtering. Econometric Theory, 32(4):861–916.

- Kyle and Obizhaeva, (2017) Kyle, A. and Obizhaeva, A. (2017). Dimensional analysis and market microstructure invariance. Working Paper w0234, New Economic School (NES).

- Lee and Mykland, (2008) Lee, S. and Mykland, P. (2008). Jumps in financial markets: a new nonparametric test and jump dynamics. The Review of Financial Studies, 21(6):2535–2563.

- Malliavin and Mancino, (2009) Malliavin, P. and Mancino, M. (2009). A fourier transform method for nonparametric estimation of multivariate volatility. Annals of Statistics, 37(4):1983–2010.

- Mancino et al., (2017) Mancino, M., Recchioni, C., and Sanfelici, S. (2017). Fourier-malliavin volatility estimation. theory and practice. Spinger.

- Mancino and Sanfelici, (2008) Mancino, M. and Sanfelici, S. (2008). Robustness of fourier estimator of integrated volatility. Computational Statistics and Data Analysis, 52(6):2966–2989.

- Mykland and Zhang, (2009) Mykland, P. A. and Zhang, L. (2009). Inference for continuous semimartingales observed at high frequency. Econometrica, 77(5):1403–1445.

- Nelson, (1990) Nelson, D. (1990). Arch models as diffusion approximations. Journal of Econometrics, 45(2):7–38.

- Platen, (1997) Platen, E. (1997). A non-linear stochastic volatility model. Financial Mathematics Research Report No.FMRR005-97, Center for Financial Mathematics, Australian National University.

- Roll, (1984) Roll, R. (1984). A simple implicit measure of the effective bid‐ask spread in an efficient market. The Journal of Finance, 39:1127–1139.

- Sanfelici et al., (2015) Sanfelici, S., Curato, I., and Mancino, M. (2015). High frequency volatility of volatility estimation free from spot volatility estimates. Quantitative Finance, 15(8):1331–1345.

- Smith et al., (2003) Smith, E., Farmer, D., Gillemot, L., and Krishnamurthy, S. (2003). Statistical theory of the continuous double auction. Quantitative Finance, 3(6):481–514.

- Veraart and Veraart, (2012) Veraart, A. and Veraart, L. (2012). Stochastic volatility and stochastic leverage. Annals of Finance, 8(2):205–233.

- Vetter, (2015) Vetter, M. (2015). Estimation of integrated volatility of volatility with applications to goodness-of-fit testing. Bernoulli, 21(4):2393–2418.

- Wilmott, (2000) Wilmott, P. (2000). Derivatives. John Wiley and Sons.

- Zhang et al., (2005) Zhang, L., Mykland, P. A., and Aït-Sahalia, Y. (2005). A tale of two time scales: determining integrated volatility with noisy high-frequency data. Journal of the American Statistical Association, 100:1394–1411.

- Zu and Boswijk, (2014) Zu, Y. and Boswijk, H. P. (2014). Estimating spot volatility with high-frequency financial data. Journal of Econometrics, 181(2):117–135.

Appendix A Proofs

Lemma 1

Proof

-

-

-

-

-

-

Note that can be rewritten as

| (13) |

Therefore, under Assumption 1, the explicit formula for can be obtained by deriving the analytic expression for , and

. Note that the expression of the last term differs in the no-overlapping case and the overlapping case .

We derive the exact expression of these terms separately as follows.

I) Analytic expression of

To simplify the notation, let denote the quantity . Also, let be the natural filtration associated with the process . We have

where:

-

since is assumed to be independent of (see Sections 3.1.3 and 3.1.4 of Aït-Sahalia and Jacod, (2014)); this in turn implies

-

for and ,

-

-

for and ,

.

Finally, putting everything together, we obtain the following expression for :

.

II) Analytic expression of E[RV^2 (τ+iΔ_N-Δ_N, k_Nδ_N)] i i-1 E[RV^2 (τ+iΔ_N, k_Nδ_N)] E[RV (τ+iΔ_N, k_Nδ_N)RV (τ+ iΔ_N-Δ_NΔ_N, k_Nδ_N)] for

Assume that we are in the no-overlapping case . Then

IIIb) Analytic expression of for

Assume now that we are in the overlapping case . Then the parametric expression of can be decomposed into the sum of four components, that is

.

We then obtain the parametric expressions of these four components, which we term , , and , respectively (we omit the intermediate steps, as are they are analogous to those followed in I) and IIIa)):

-

-

-

-

-

-

-

-

The contribution to the PSRV finite-sample bias due to the overlapping of consecutive local windows to estimate the spot volatility (i.e., due to assuming that ) is mainly due to the terms , , and . In fact, when (i.e., ), the terms , , and are equal to zero.

Interestingly, the terms , , and are functions of the quantity (i.e., ) and, in particular,

are as as , as one can check focusing on the terms and .

After plugging the explicit expressions obtained in I), II) and IIIa) (resp., IIIb)) into Eq. (A), simple but tedious calculations yield the parametric expression of under Assumption 1, which can be expressed in the following compact form:

where:

| (14) |

| (15) |

| (16) |

| (17) | ||||

The proof is complete.

Theorem 4.1

Proof

Consider the exact parametric expression for the PSRV bias under Assumption 1 in the case , given in Lemma 1. By expanding it sequentially, first as , and then as , we obtain:

as , .

The sequential expansions as , are performed using the software Mathematica. The code is available as supplementary material.

Furthermore, let denote the natural filtration associated with the process . It is straightforward to see that

as , .

Theorem 4.2

Proof

Consider the exact parametric expression for the PSRV bias under Assumption 1 in the case , given in Lemma 1. Then recall that for , , and , . Moreover, note that for and or and , we have

and

Expanding , , and as , one obtains

from which we get Eq.(7).

Based on the corresponding asymptotic expansions, one can easily check that as , if and or, alternatively, and , then , and . This implies that as , if and or, alternatively, and , then converges to , where the equivalence is obtained from Appendix A in Bollerslev and Zhou, (2002).

In particular, one can easily verify that, as :

-

•

for and ,

(18) (19) -

•

for and ,

(20) (21) -

•

for and ,

(23) (24)

The proof is complete.

Corollary 1

Proof

Based on Eq. and the asymptotic rates of , and (see Eqs. , we observe that:

-

-

for or or ,

-

-

for

-

-

for

-

-

for , ,

-

-

for

-

-

for

-

-

for , ,

Thus, it is possible to select and such that the dominant term of the bias expansion is canceled only when and or and , provided that the selected values of and verify the condition , which is equivalent to .

The case and is of particular interest, as it may allow to cancel the dominant term under the usual assumption , which is equivalent to . In fact, if , then and it is not possible to cancel the leading term of the bias expansion through the selection of and when and or and .

Specifically, the leading term of the bias expansion in Eq. (7) can be canceled in the case and if there exists a solution to the following system

where and . If a solution exists, the corresponding bias-optimal selection of and reads

Lemma 2

Proof

Let Assumption 2 hold and consider the estimator:

where, for taking values on the time grid of mesh-size :

-

-

-

-

-

-

We observe that

To simplify the notation, we replace with and with and rewrite:

Based on the previous expression, we can split the expected value of into the sum of the following six components:

-

i)

-

ii)

-

iii)

-

iv)

-

v)

-

vi)

Note that under Assumption 2, is zero-mean and is a zero-mean stationary process independent of . Therefore components iv), v) and vi) are equal to zero. Moreover, note that the analytic expression of i) was already obtained in Theorem 4.2. Thus, in order to obtain the analytic expression of under Assumption 2, we only have to compute the analytic expressions of ii) and iii).

We start with ii). We have:

since is an i.i.d. process such that and , as one can easily check.

Then we move on to iii). First, we rewrite:

Then we note that:

-

-

is zero-mean and independent of , therefore:

-

-

;

-

-

-

-

-

-

is stationary and independent of , therefore:

where .

Therefore, simple calculations allow rewriting component iii) as:

Finally, putting everything together, we have

where

Analogous calculations in the overlapping case lead to

Theorem 4.3

Theorem 4.4

Proof

Recall from Definition 1 that for with values on the price-sampling grid of mesh size :

and

Therefore, under Assumption 1,

Expanding this as , we can rewrite Furthermore, recall that and . Therefore, under Assumption 1, converges to zero as , with rate .

Now let Assumption 2 hold and replace with in the definition of the locally averaged realized variance, i.e., consider the estimator Simple calculations lead to:

Therefore, under Assumption 2, diverges as , with rate . The proof is complete.

Appendix B Indirect inference method for the feasible bias-optimal selection of local-window tuning parameter

The feasible selection of in equation (12) requires, for a given , the knowledge of the volatility process at the instant and the vol-of-vol parameter . A simple and computationally-efficient indirect inference method to obtain estimates of those quantities is as follows.

First, one estimates the spot volatility path using the fast Fourier transform algorithm, following the procedure detailed in Appendix B.5 of Mancino et al., (2017). In particular, from a given sample of log-price observations, one obtains estimates of the spot volatility on the grid of mesh size , where denotes the sample size, while and denote, resp., the cutting frequencies for the computation of Fourier coefficients of the volatility and the reconstruction of the spot volatility path. See Chapter 4 in Mancino et al., (2017) for the consistency of the estimator and guidance on the efficient selection of the cutting frequencies and for a given .

Then, using the reconstructed volatility path , , one infers the value of the parameter by applying the following zero-intercept multivariate regression, based on the discretization of the CKLS process in Assumption 3:

| (25) |

where is a vector of independent standard normal random variables, while the dependent variable and independent variables are defined as

Denoting by the estimate of the standard deviation of the disturbance term, obtained from the regression residuals, we have .

An estimate of is simply given by the Fourier estimate of volatility in correspondence of the beginning of the period of interest.