∎

22email: yankai.cao@ubc.ca

33institutetext: Victor M. Zavala 44institutetext: Department of Chemical and Biological Engineering, University of Wisconsin-Madison, 1415 Engineering Dr, Madison, WI 53706, USA.

44email: victor.zavala@wisc.edu

A Sigmoidal Approximation for Chance-Constrained Nonlinear Programs††thanks: This work was partially supported by the U.S. Department of Energy grant DE-SC0014114.

Abstract

We propose a sigmoidal approximation for the value-at-risk (that we call SigVaR) and we use this approximation to tackle nonlinear programs (NLPs) with chance constraints. We prove that the approximation is conservative and that the level of conservatism can be made arbitrarily small for limiting parameter values. The SigVar approximation brings scalability benefits over exact mixed-integer reformulations because its sample average approximation can be cast as a standard NLP. We also establish explicit connections between SigVaR and other smooth sigmoidal approximations recently reported in the literature. We show that a key benefit of SigVaR over such approximations is that one can establish an explicit connection with the conditional value at risk (CVaR) approximation and exploit this connection to obtain initial guesses for the approximation parameters. We present small- and large-scale numerical studies to illustrate the developments.

Keywords:

Nonlinear optimization Chance constraints Large-scale Approximation1 Problem Definition and Setting

We study the chance-constrained nonlinear program (CC-P):

| (1a) | ||||

| (1b) | ||||

Here, are decision variables and the objective function is twice continuously differentiable and potentially nonconvex. The set is assumed to be compact and non-empty and is comprised of twice differentiable and potentially nonconvex constraints . We consider the probability space and we assume that is a measurable space equipped with -algebra of subsets of , and that is a linear space of -measurable functions (random variables). The probability measure function is given by and we use to denote realizations of . The scalar constraint function is also assumed to be twice continuously differentiable and potentially nonconvex. We define the scalar random variable with realizations . When appropriate, we use the notation to highlight the dependence of the random variable on the decision . We use to denote the probability of the event and to denote the cumulative distribution functions of .

The CC (1b) requires that the event occurs with probability of at least , where . Since , the CC can also be written as or . We recall that the -quantile of is (where VaR is known as the value-at-risk). Consequently, the CC can also be written as . Another important observation is that holds, where denotes the indicator function of set (i.e., if and if ). Consequently, (1b) can be written as or, equivalently, as . We define the feasible set of CC-P as , where and we assume to be compact for all . We denote an optimal solution and objective value of (1) as and , respectively. We also denote the solution set as . We focus our attention on NLPs with a single CC but the concepts discussed can also be applied to multiple CCs of the form .

A distinguishing and challenging feature of CC-P is that it cannot be solved exactly (except for certain simplified settings). Settings that admit exact solutions include those in which the quantile can be expressed in algebraic form (e.g., the constraint function is linear in both arguments and the random data vector is Gaussian bienstock ) or cases in which the cumulative distribution and its derivatives can be computed explicitly henrion . Exact reformulations to its sample average approximation (SAA) with integer variables, originally proposed in luedtkeahmed , use an indicator function representation of the CC. Unfortunately, in the context of CC-P, the integer reformulation would lead to large-scale and nonconvex mixed-integer nonlinear programs (MINLPs). Conservative and computationally more tractable approximations of CC-P can be used to avoid the need for solving MINLPs. A conservative approximation can be obtained by using the so-called scenario-based approach campi ; calafiore2006scenario ; nemirovski2006scenario . In this approach, we solve a stochastic NLP that enforces with probability one (almost surely). Such an approach leads to structured NLPs, which can in turn be solved using parallel interior-point solvers zavalalaird . A drawback of the scenario approach is that it can be overly conservative and does not offer direct control on the probability level of CC. Alternative conservative approximations include the conditional value-at-risk (CVaR) approximation and the Bernstein approximation, which use convex approximations of the indicator function nemirovski2006convex . The level of conservatism of both CVaR approximation and Bernstein approximation might be reduced, but not eliminated using the “tuning methods” nemirovski2006convex . The authors in hong2011sequential ; shan2014smoothing propose a difference of convex functions (DC) approximation for the indicator function and they show that the approximation can be made equivalent to CC-P for limiting parameters. This approach involves a difference of non-smooth max functions that cannot be handled with standard NLP modeling and solution tools. Instead, this approach requires specialized solution algorithms that are not guaranteed to work in a general nonconvex NLP setting.

The authors in geletu2017inner ; geletu2015tractable propose a smooth sigmoidal (SS) approximation for the indicator function. The solutions of this approximation are shown to be conservative and converge to the solutions of CC-P for limiting parameter values. This approach has the practical advantage that its sample average approximation can be handled using standard NLP tools. Unfortunately, no guidelines have been provided to select suitable approximation parameters. This is important, because, when the parameter values are far away from their limiting values, the approximation can be very conservative and lead to infeasible problems. On the other hand, when the parameter values are too close to their limiting values, the sigmoidal approximation becomes difficult to handle numerically.

In this work, we propose a tailored sigmoidal approximation to outer-approximate the indicator function. We use this sigmoidal function to construct a risk measure, that we call SigVaR, and show that this is a conservative approximation of the value at risk (VaR). We prove that the SigVaR approximation is always conservative and that it converges to CC-P for limiting parameter values. As with SS, a benefit of the SigVaR approximation is that it can be handled by using standard NLP solvers, thus offering parallel solution capabilities. We establish explicit relationships between the parameters of SigVaR with those of CVaR. This allows us to establish parameter values that guarantee that the approximation is as conservative as CVaR. Specifically, we show that we can directly relate the parameters of the SigVaR approximation to the value-at-risk (VaR) identified with CVaR. This connection provides a mechanism to obtain an initial feasible solution and an initial guess for the parameter values. We also establish explicit connections between the parameters of SigVaR and those of DC and SS approximations. As with SS, a drawback of SigVaR is that numerical stability is encountered as the approximation approaches the indicator function. To improve this issue, we propose a scheme that solves a sequence of conservative approximations of increasing quality. Another drawback of SigVaR is that solving SigVaR to global optimality is computationally intractable if the dimension of is large. Scenario-based approach, CvaR approximation, DC approximation, and and SS approximation all have the same drawback if nonconvex functions are involved. Actually Even solving the original large-scale NLP problem without chance constraints to global optimality is computationally intractable. However, solving SigVaR to local optimality also provides promising performance for many problems as shown in Section 5. Small and large case studies are used to illustrate the concepts and demonstrate performance.

The paper is organized as follows. Section 2 introduces basic nomenclature and reviews CVaR, Bernstein, and DC approximations. Section 3 introduces the SigVaR approximation and establishes properties. Section 4 outlines a numerical scheme to solve a sequence of SIgVaR approximations. Section 5 provides numerical studies. Final remarks are provided in Section 6.

2 Review on CC Approximations

We review approaches to deal with CC-P in order to introduce some necessary concepts and notation. Derivations follow the work of nemirovski2006convex ; pinter1989deterministic . We make the following blanket assumptions throughout the paper.

Assumption 1

There exists such that is Lipschitz continuous in for every .

Assumption 1 is slightly weaker than the Assumption 4 in hong2011sequential . We will discuss special cases violating Assumption 1, that is When is a discrete random variable, with for every , in Section 3.1 following Theorem 1.

Assumption 2

with .

This regularity assumption is Assumption 5 in hong2011sequential .

2.1 CVaR Approximation

Because , the CC can be expressed as , and we can use the equivalent formulation:

| (2) |

A computationally practical approach to approximate the CC is to find a conservative approximation. This is done by finding an approximating function satisfying for any . For such a function we have that for any parameter . Consequently,

| (3) |

We can thus conclude that the satisfaction of the constraint:

| (4) |

implies that is satisfied (and so does ). Because (4) is valid for all we also have, if is convex, that:

| (5) |

implies . The quality of the conservative approximation depends on the choice of the approximating function . The choice with leads to the approximation:

| (6) |

can be replaced with to obtain:

| (7) |

By redefining and recalling that , we see that (7) can be used to derive a conservative approximation of CC-P of the form:

| (8a) | ||||

| (8b) | ||||

We denote an optimal objective value and solution of this problem (which we call CVaR-P) as and , respectively. We define the feasible set of CVaR-P as and notice, because CVaR provides a conservative approximation, that . This also implies that for all .

A key advantage of the CVaR approximation is that its sample average approximation (SAA) can be cast as a standard NLP cao2017scalable ; rockafellar2000optimization . Moreover, if is convex in for given , CVaR is also convex in . One can also prove that the function is the tightest convex approximation of . Despite these benefits, the CVaR approximation can be quite conservative. Moreover, the CVaR approximation does not offer a mechanism to enforce convergence to a solution of CC-P.

2.2 Bernstein Approximation

If we use the function , (4) takes the form . For this is equivalent to,

| (9) |

Because this relationship is valid for all , we can also conclude that:

| (10) |

which is called Bernstein approximation. From the definition of entropic value-at-risk (EVaR) ahmadi2012entropic :

| (11) |

it is thus easy to see that (10) is equivalent to:

| (12) |

This conservative approximation can be handled using standard NLP techniques. Moreover, if is convex in for given , EVaR is also convex in . Unfortunately, one can prove that EVaR is even more conservative than CVaR. This follows from nemirovski2006convex .

2.3 DC Approximation

In hong2011sequential it is shown that the indicator function can be approximated by using a difference of convex functions (the authors in hong2011sequential assume assume that is convex). The DC approximation of has the form:

| (13) |

where , is an approximation parameter. By using approximation (13) instead of (1b), we obtain problem DC-P. In hong2011sequential it is shown that DC-P is equivalent to CC-P for . A practical limitation of DC-P is that its SAA cannot be cast as a standard NLP, due to the difference of max functions. Consequently, tailored algorithms are needed hong2011sequential .

2.4 Smooth Sigmoidal Approximation

The authors in geletu2015tractable approximate the indicator function by using a smooth sigmoidal function. The approximation has the form:

| (14) |

where , are approximation parameters satisfying and . The framework proposed in geletu2015tractable also consider the possibility of using functions and . The SS approximation is exact in the limit . We denote an optimal objective value and the feasible set of the approximation with (14) (which we call SS-P) as and . An important practical limitation of this approximation is that no guidelines exist to choose .

3 SigVaR Approximation

As noticed in geletu2015tractable , our work is motivated by the observation that the indicator function can be outer-approximated by using a standard sigmoid function of the form:

| (15) |

where are the approximation parameters. The associated CC approximation takes the form:

| (16) |

The sigmoid function (15) is equivalent to when , , and . The sigmoid function is also a special case of the generalized logistic function, which is a standard approximation function for the indicator function chen1995smoothing .

In this work, we consider a variant of the sigmoid function (15) of the form:

| (17) |

This gives the CC approximation:

| (18) |

Although is non-smooth, in Section 4 we show that the sample average approximation with constraint (18) can be cast as a standard NLP.

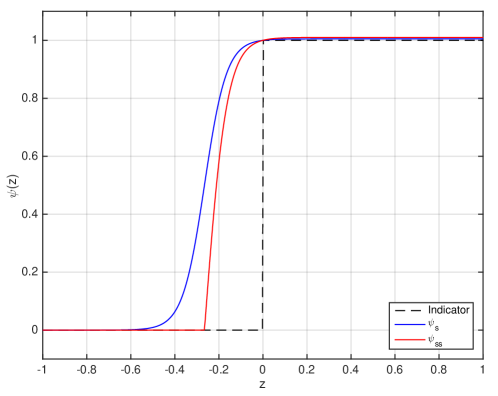

The motivation behind the tailored variant is illustrated in Figure 1, where we can see that the variant is more accurate than the standard counterpart because the max function sets for all where . Although (17) is not smooth, we show in Section 4 that it can still be cast as a standard NLP. In the following sections we prove that the structure of the proposed variant allows us to establish connections with CVaR and DC approximations.

We being by showing that sigmoid functions provide natural conservative approximations for CCs.

Lemma 1

Proof

Consider the random variable with realizations . Since holds for and holds for we have that for any and holds for . We thus have that holds for . Therefore, and for any . Consequently, and . The result follows.

We use the proposed function to define the Sigmoidal Value-at-Risk (SigVaR):

| (19) |

and we use this to formulate the problem:

| (20a) | ||||

| (20b) | ||||

We define an optimal objective and solution of (20) as and . We also denote the set of optimal solutions as and define the feasible set of (20) as . From Lemma 1, it is clear that for all . This implies that for all and .

The definition of SigVaR is motivated by the observation that can also be expressed in terms of the indicator function:

| (21) |

Because we have established that the sigmoid function is a conservative approximation of , we have that . Consequently, SigVaR can be interpreted as an approximate quantile and (20) is a conservative representation of CC-P. As in the case of the VaR representation of CC-P, problem (20) is not particularly attractive for computation. However, this problem also has the following equivalent representation (that we call SigVaR-P):

| (22a) | ||||

| (22b) | ||||

In Section 4 we will show that the SAA approximation of SigVaR-P can be cast as a standard NLP.

To show that (22) and (20) are equivalent, we make the following observations. If is satisfied then it implies that satisfies , and since is the smallest satisfying , then . On the other hand, if is satisfied, according to the definition, satisfies . Since is a decreasing function of , then also satisfies and thus .

3.1 Relationship with CC-P

We now show that SigVaR-P becomes an exact approximation of CC-P in the limit of its parameter values. For the random variable with , we define the SigVaR-CC approximation error:

| (23) |

From Lemma 1 we have that for all .

We proceed to establish a bound for the SigVaR-CC approximation error. Under Assumption 1 we can establish that there exists a positive constant satisfying for all , and any . The reasoning is the following: when , from Lipschitz continuity of , we get , where is set to be the Lipschitz constant. When , we have and we have . A special case satisfying Assumption 1 is when is a continuous random variable with bounded probability density . In this case, we have that constant exists and satisfies for all .

Lemma 2

The SigVaR-CC error is bounded as for all .

Proof

We establish the result by following sequence of implications:

Here, the first inequality follows since for , for and for . The last inequality follows from .

Theorem 1

Let with . Then .

Proof

From Lemma 2 we can establish the bound with . The result follows.

Remark: When is a discrete random variable, we can establish the error bound of Lemma 2 if has finite outcomes and we have that . Here, we assume that has finite possible outcomes with corresponding probabilities as . A bounding constant can be found in this case by noticing that if , , if , and if . We thus have that satisfies . Consequently, the results of Theorem 1 hold. This is relevant because we are often interested in solving discrete approximations of SigVar-P (e.g., by using SAA).

The following result shows that we can construct a sequence of SigVaR approximations of increasing quality by progressively increasing .

Lemma 3

Let with . We have that and for and for all .

Proof

We show that for any (for , we have for any ). To proceed, it suffices to show that the kernel function is a strictly decreasing function of for all . We establish this by showing that the derivative of of the kernel function is negative:

The last step follows from , for any (from Taylor’s theorem and from the convexity of the exponential function).

The following result establishes convergence of the feasible set of SigVaR-P to that of CC-P.

Theorem 2

Let with . We have .

Proof

Take an arbitrary increasing sequence with . From Lemma 3 and Exercise 4.3 (a) of rockafellar2009variational , exist and . Since , from Theorem 7.43 of shapiro2009lectures , is a continuous function of and thus is a closed set. Lemma 1 implies .

The following is our main result, which establishes convergence of the solution set and optimal objective value.

Theorem 3

Let with . We have and .

Proof

Let and , where if and if . By Proposition 7.4(f) of rockafellar2009variational , we have epi-converges to as . Since is continuous, by Exercise 7.8(a) in rockafellar2009variational , epi-converges to as . Because is bounded, by Exercise 7.32 (a) of rockafellar2009variational , is eventually level bounded. Because and are lower semi-continuous and proper, by Theorem 7.33 of rockafellar2009variational , we have and .

3.2 Relationship with CVaR-P

We define and recall that rockafellar2000optimization :

| (24) |

and thus . This observation also highlights that CVaR provides a conservative approximation for the CC.

Crucial to our results is the constant:

| (25) |

with .

We now argue that we can always find a (equivalently ) at any . Since (8b) is satisfied at and , we have that either or . In the first case, it follows that with . In the latter case, from , we have , thus and . We have both and (from ), which violates the Assumption 1. Thus the later case is not valid. Even if Assumption 1 does not hold (e.g. is a discrete random variable with finite outcomes, as long as , we cannot have that both and hold.

We now show that the parameters of SigVaR-P can be selected in such a way that they provide an approximation of CC-P that is at least as good as that of CVaR-P.

Proposition 1

Assume a fixed and that satisfy (where is the positive solution of ), , and defined in (25). We have that .

Proof

For simplicity, we omit dependency on for , , and (we simply write ). We proceed by proving that any solution of CVaR-P is a feasible point for SigVaR-P provided that satisfy the conditions of the proposition. This would imply that we can always find such that . We define the random variable with realizations ; the constraint (8b) evaluated at can be written as . It suffices to show that holds for any . If , where , we have that and, consequently, . For we have that,

| (26) |

The last inequality follows because is a monotonically decreasing function for . We also observe that, for ,

| (27) |

We now define and proceed to show that holds for . This is established from the following sequence of implications:

| (28a) | ||||

| (28b) | ||||

| (28c) | ||||

| (28d) | ||||

| (28e) | ||||

| (28f) | ||||

| (28g) | ||||

Here, (28c) follows because and . (28e) follows since . (28f) follows since . (28g) follows because is a monotonically increasing function for and . For we have,

| (29) |

This follows because (), , and . Since we have that for . We thus have that holds for satisfying the conditions of the proposition.

Proposition 1 is of practical computational relevance because it indicates that we can use the solution of CVaR-P (which is a computationally attractive formulation) to find an initial guess for SigVar-P. We also note that Proposition 1 implies that SigVaR provides an approximation that is at least as good as that of EVaR.

3.3 Relationship with DC-P

The following results compare the solutions of SigVaR-P and DC-P. To establish these results, we define the SigVaR-DC error:

| (30) |

In addition, we define for all . Consequently, .

We now establish a lower bound for the SigVar-DC error.

Proposition 2

Assume that satisfies . We have that for any .

Proof

We proceed by proving that holds for any . If we have that and, consequently, . For we have that,

| (31) |

We also observe that, for ,

| (32) |

We proceed to show that holds for . This is established from the following sequence of implications:

| (33) |

Here, the first inequality follows since and the second inequality follows because of the condition . Since , we have that for. For we have, .

This result shows that as , the range of feasible that make SigVaR-P more conservative increases. We now establish an upper bound for the SigVar-DC error.

Proposition 3

Assume satisfy where is the positive solution of and . We have that .

Proof

We proceed by proving that holds for any if satisfy the conditions of the proposition. If , where , we have that and, consequently, . For , we can follow the derivation of Proposition 1 to prove that . For we have that . The result follows.

This result shows that improving the quality of the DC-P approximation (by setting ) corresponds to setting for SigVaR-P (e.g., by using with ).

3.4 Relationship with SS-P

The following results compare the solutions of SigVaR-P and SS-P. We show that there exist parameters of SigVaR-P that provide an approximation of CC-P that is at least as good as that of SS-P.

Proposition 4

Assume that satisfy , . We have that and .

Proof

We proceed by proving that any feasible point of SS-P is a feasible point for SigVaR-P provided that satisfy the conditions of the proposition. This would imply that we can always find such that and . It suffices to show that holds for any . If , where , we have that and, consequently, . For we have

| (34a) | ||||

| (34b) | ||||

| (34c) | ||||

| (34d) | ||||

| (34e) | ||||

where the first equality holds since , the second equality follows by substituting and , and the inequality holds since .

Corollary 1

Assume that satisfy , , and , we have that and .

4 Computational Implementation

We use SAA to convert SigVar-P into a finite-dimensional NLP kleywegt2002sample . We generate a set of realizations from . The total number of realizations is . The SAA approximation is given by:

| (35a) | ||||

| (35b) | ||||

| (35c) | ||||

| (35d) | ||||

Large values of will cause difficulty for the NLP solver due to the high nonlinearity of the sigmoid function. For example, the first derivative of with respect to is and thus becomes increasingly steep as is increased. Moreover, the second derivative is . Consequently, we propose a scheme to solve a sequence of SigVaR approximations of increasing quality and with this achieve more robustness. The scheme (called SigVaR-Alg) begins by finding a solution of the SAA approximation of the CVaR-P. The SAA approximation of CVaR-P is:

| (36a) | ||||

| (36b) | ||||

| (36c) | ||||

| (36d) | ||||

From Proposition 1, we have that holds and from Lemma 3 we have that holds for all (provided that the NLPs are solved to global optimality). However, for the numerical studies in Section 5, the SigVaR approximation at each iteration is solved to local optimality because solving a large-scale NLP to global optimality is computationally intractable.

5 Numerical Studies

The first two case studies are small-scale linear problem; consequently, exact and tractable MILP reformulations can be used and provide best performance. We use two small-scale studies to illustrate the theoretical properties of SigVaR. The next two case studies include a wind turbine optimization study and a flare system optimization study, which are large-scale and highly nonlinear. For these two case studies, exact mixed integer reformulations are intractable. We use the large-scale studies to illustrate the practical benefits of SigVaR.

5.1 Analytical Example

Consider the following CC-P:

| (37a) | ||||

| (37b) | ||||

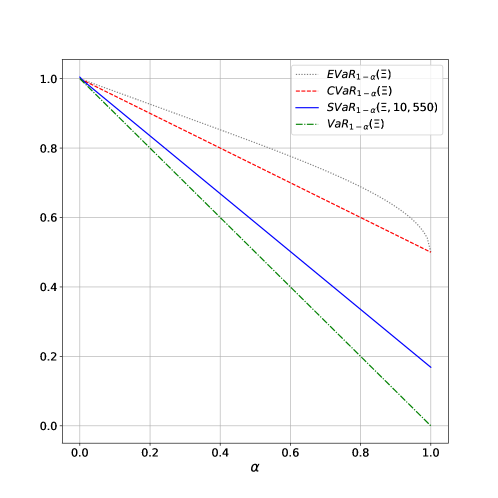

with . The optimal objective value and solution are and we note that . This implies . We handle the CC (37b) using the VaR (exact), the CVaR approximation (8b), the EVaR approximation (12), and the SigVaR approximation (20b).The optimal solution and objective values obtained with these approaches are, respectively, , , , and . Moreover, , , and . For the case of SigVar we have that, for ,

| (38) |

where . Otherwise, we have that

| (39) |

The optimal objective values for all approaches as a function of are shown in Figure 2. As predicted by the properties of SigVaR, we have that for all .

We have that for . Consequently, the constant satisfies for all . From Lemma 2, the approximation error of the SigVaR function is bounded as . We note that this is an upper bound of the empirical error observed in Figure 2 and computed by (vertical distance at each ).

From the solution of the CVaR approximation we obtain that and thus . Proposition 1 predicts that for and , . This prediction is verified in Figure 2, which shows that empirically for , . The extreme conservatism of CVaR and EVaR becomes obvious at large values of . In particular, at we see that and =0.5, which illustrates that the quality of the approximation can be substantially improved.

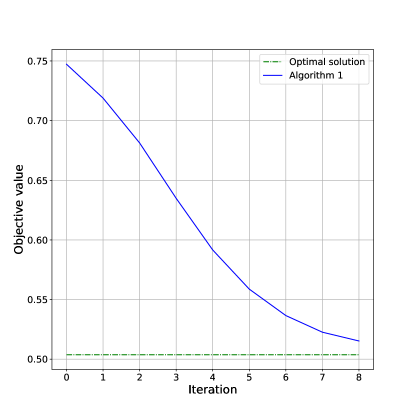

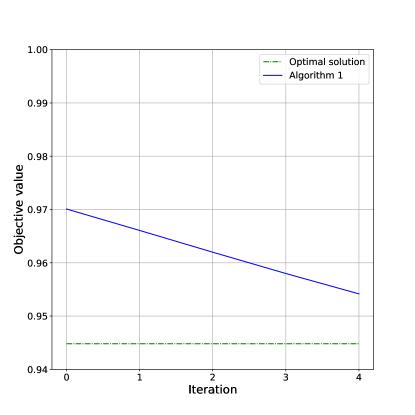

In practice, it is very rare that analytical solutions can be obtained. Therefore, We now illustrate numerical behavior of SigVar-Alg (in our experiments we use SAA with 1,000 scenarios). The CC-P in this case can be cast exactly as an MILP, CVaR-P is cast as an LP, and SigVaR-P and as NLP. The MILPs are solved with the solver SCIP and the LPs and NLPs are solved with IPOPT. Lemma 3 shows that becomes less conservative for increasing , which is verified in Figure 3 for and . For , the solution of the MILP formulation is 0.504, which is close to the analytical solution of 0.5. SigVaR-Alg first finds the solution of CVaR approximation, which is 0.747. At iteration 1, we solve with SigVaR approximation with and , and find a solution of 0.719. After 8 iterations, we solve a SigVaR approximation with and and find a a solution of 0.515. The gap between MILP formulation and SigVaR is only 4% of the gap between CC-P and CVaR-P. For , the gap is 36% but we also see that the gap is more difficult to close with SigVaR.

5.2 Farmer Problem

We consider modified version of the classical farmer problem birge2011introduction . In this problem, the farmer needs to decide how much land to allocate to grow wheat, corn, and beets while considering the uncertainty on crop yields. The farmer has the option to buy/sell crops to satisfy contracts and maximize revenue (minimize cost). The formulation is given by:

| (40a) | ||||

| s.t. | (40b) | |||

| (40c) | ||||

| (40d) | ||||

| (40e) | ||||

| (40f) | ||||

where denotes the land allocated to each crop at cost , represents the crops bought at price , denotes the crops sold at price , denotes the set of crops , is the yield of crops, denotes demand contracts and represents capacities. Constraint (40e) requires that the cost is lower than the threshold with probability at least . We assume that the yield of wheat and corn is constant, while the yield of beets follows a normal distribution . We generate 1,000 scenarios from this distribution and we set and .

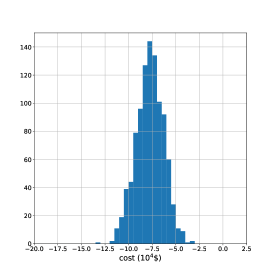

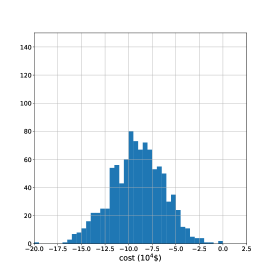

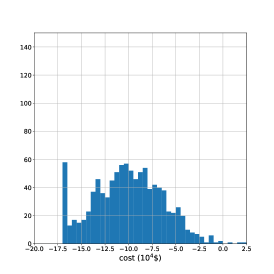

The performance of SigVaR-Alg is summarized in Table 1. The solution of CC-P is obtained using the MILP formulation. As can be seen, the expected cost of the MILP formulation is $-86431. The expected cost of CVaR approximation is $-76455 (which is around 11.5% higher than the optimal MILP cost). This is because, although (40e) only requires the cost to be lower than the threshold with probability equal to larger than 0.95, the solution of CVaR formulation satisfies the constraint with probability 0.978. Figure 4 shows the histogram of the cost obtained with CVaR, SigVaR, and MILP formulations. Here, it becomes obvious that CVaR can significantly distort the cost distribution due to high conservatism. From the solution of the CVaR approximation we obtain and . After 6 iterations, SigVaR-Alg solves the SigVaR approximation with and and finds a solution with an expected cost of $-85472 (which is is around 1.1% higher than the optimal MILP cost). The gap between the MILP and SigVaR formulations is only 9.6% of the gap between the MILP and CVaR formulations. We also observe that, as the iterations proceed, the objective value of SigVaR-P decreases monotonically, decreases, and increases. We can thus see that the SigVaR formulation can significantly reduce the conservatism of the CVaR solution. We acknowledge, however, that we are unable to close the gap further due to numerical instability of the NLP solver.

| CVaR-P() | - | - | -76455 | -55601 | 0.978 |

|---|---|---|---|---|---|

| 1 | 2.5 | 0.00031 | -78396 | -54511 | 0.974 |

| 2 | 5.0 | 0.00054 | -80225 | -53484 | 0.969 |

| 3 | 10.0 | 0.00098 | -82141 | -52408 | 0.965 |

| 4 | 20.0 | 0.00188 | -83659 | -51556 | 0.959 |

| 5 | 40.0 | 0.00367 | -84746 | -50945 | 0.957 |

| 6 | 80.0 | 0.00725 | -85472 | 50538 | 0.953 |

| CC-P | - | - | -86431 | -50000 | 0.95 |

5.3 Wind Turbine Optimization

We now solve a large-scale CC-P that seeks to find optimal pitch and torque control policies for a wind turbine given uncertainty in wind speed conditions. The formulation seeks to maximize expected power and to satisfy a CC on the maximum mechanical load experienced by the wind turbine. We represent this problem in the following abstract form:

| (41a) | ||||

| s.t. | (41b) | |||

| (41c) | ||||

| (41d) | ||||

| (41e) | ||||

where , is the wind speed, is the wind turbine power, is the mechanical load with associated threshold . For a time horizon of ten minutes, we set the control actions for the first 10 seconds to be first stage variables (the implemented control actions) and the rest to be second stage variables (the recourse control actions). Equation (41b) is an abstract representation of a wind turbine model (which comprises nonlinear differential and algebraic equations). The model details are presented in windpaper . A Julia model implementation along with all necessary data is available at https://github.com/zavalab/JuliaBox/tree/master/WindSigVaR.

An important practical problem is that power maximization conflicts with the mechanical load experienced by the turbine (i.e., the higher the power extracted the higher the load). Consequently, it is important to carefully trade-off these metrics so as to prevent putting the turbine at extreme mechanical risk. The probabilistic constraint (41c) enforces that the probability that the peak load exceeds the threshold is no more than . Constraint (41e) enforces that the peak load never exceeds another (less conservative) threshold . In our experiments we set MNm, and MNm.

To solve this problem, we discretize the dynamic model by using a Radau collocation scheme zavalathesis . To accurately capture extreme loads we have found that it is necessary to discretize the model using a resolution of 0.5 seconds over 10 minutes, giving rise to 1,200 time steps. For an NLP with 230 scenarios (collected from real implementations), the total number of variables is 5.5 million. The NLPs arising in this application were implemented in Plasmo.jl plasmo and solved with the parallel interior-point solver PIPS-NLP pipsnlp (which exploits the structure of the stochastic program at the linear algebra level) and with the off-the-shelf serial solver IPOPTipopt (which treats the problem as a general NLP). Because of the size of the problem and because the wind turbine model is nonconvex, MINLP formulations of CC-P are computationally intractable. A conservative approach to solve this problem is to enforce the load constraint for all scenarios (almost surely). The expected power using this approach is 3.5 MW.

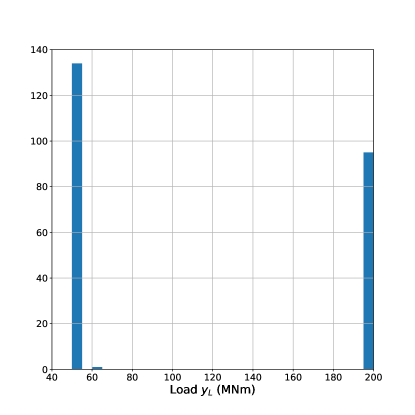

Table 2 summarizes the performance of SigVaR-Alg. The serial solver Ipopt takes 0.8 hours to solve the CVaR-P while the parallel solver PIPS-NLP requires 30 minutes using 23 computing cores. The expected power obtained with CVaR-P is 3.548 MW and we have found this performance to be too conservative. In particular, although the CC (41c) only requires to hold with a probability of 0.5, the CVaR-P solution satisfies it with probability 0.748. From the solution CVaR-P we obtain . From Table 2 we also see that the SigVaR approximation becomes less conservative as we increase and that the objective value is progressively improved (power is maximized). After three iterations, SigVaR-Alg solves SigVaR-P with and and achieves an expected power of 3.865 MW (an improvement of 8.9% over CVaR-P). The probability of satisfying the maximum load threshold is reduced to 0.583. At a price of electricity of 30 $/MWh, these cost savings obtained with SigVaR-P translate to around $83,000 per year (for a single 5 MW wind turbine). We can thus see that the economic benefits of reducing conservatism can be quite significant.

| Time | Ipopt | ||||||

|---|---|---|---|---|---|---|---|

| (Hour) | Iter | ||||||

| CVaR-P | - | - | 3.548 | 47.85 | 0.748 | 0.8 | 160 |

| 1 | 2.5 | 1.44 | 3.766 | 49.56 | 0.726 | 2.9 | 603 |

| 2 | 5.0 | 2.47 | 3.835 | 52.12 | 0.643 | 1.2 | 238 |

| 3 | 10.0 | 4.52 | 3.865 | 54.52 | 0.583 | 1.3 | 256 |

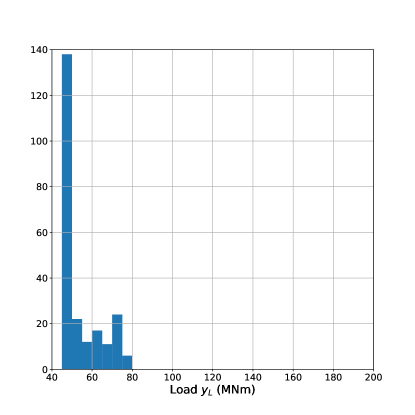

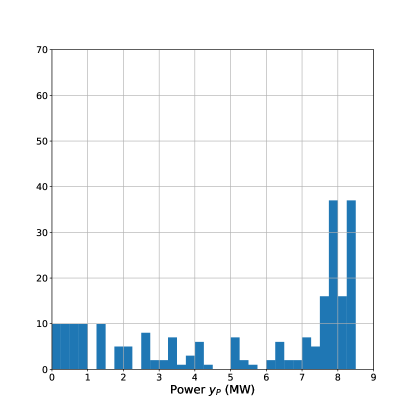

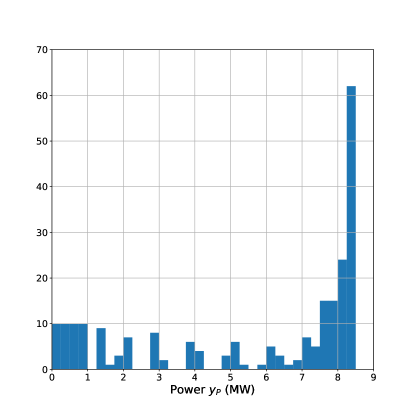

Figure 5 shows the cost distribution for the maximum load obtained with the CVaR-P and SigVaR-P. It is clear that CVaR is significantly more conservative and pushes the mechanical load towards small values. SigVaR, on the other hand, allows for an equal proportion of load violations and with this it can extract more power. This is illustrated in Figure 6, where we show that SigVaR achieves a larger proportion of scenarios with a large power output.

Table 3 summarizes the performance of smooth sigmoidal approximation SS-P. Here we set and , the same as the Figure 1 in geletu2015tractable . We tried 10 different values of . When , the approximation is too conservative and there is no feasible solution. When , IPOPT has numerical difficulty in solving the problem. The best expected power obtained with smooth approximation is better than the solution from CVaR-P, but worse than the solution from SigVaR-Alg. These results highlight the importance of having an explicit connection between SigVaR-P and CVaR-P and with this obtain an initial guess for the parameter values.

When , the expected power obtained with CVaR-P is 3.5 MW, which is the same as the expected power obtained by forcing the inequality constraint to hold for all scenarios. Both SigVaR-P and SS-P cannot further improve the performance.

| Time | Ipopt | |||||

| (hr) | Iter | |||||

| 1 | 100 | - | - | - | - | - |

| 2 | 50 | - | - | - | - | - |

| 3 | 25 | - | - | - | - | - |

| 4 | 12.5 | - | - | - | - | - |

| 5 | 6.25 | - | - | - | - | - |

| 6 | 3.125 | 1.538 | 5.53 | 1.0 | 2.1 | 461 |

| 7 | 1.563 | 2.909 | 30.79 | 1.0 | 2.5 | 553 |

| 8 | 0.781 | 3.427 | 34.02 | 0.778 | 5.2 | 1138 |

| 9 | 0.390 | 3.749 | 42.55 | 0.669 | 2.2 | 464 |

| 10 | 0.195 | - | - | - | - | - |

5.4 Flare System Optimization

We consider the design of a flare stack system that combusts a random waste fuel gas flow. Gas flares are used as safety (relief) devices to manage abnormal situations in infrastructure systems (natural gas and oil processing plants and pipelines), manufacturing facilities (chemical plants, offshore rigs), and power generation facilities. Abnormal situations include equipment failures, off-specification products, and excess materials in start-up/shutdown procedures. In particular, flares prevent over-pressuring of equipment and use combustion to convert flammable, toxic or corrosive vapors to less dangerous compounds epa2017 . Flare design is influenced by several uncertain factors such as the amount and composition of the waste flow stream to be combusted and the ambient conditions. These systems are currently designed based on typical historical values for waste fuel gases and ambient conditions api1997521 ; epa2017 . Consequently, an improperly designed flare can be susceptible to extreme events not experienced before. The design goals are to minimize capital cost while controlling the radiation level at ground level (which is a function of the input waste flow to be combusted).

The heat released by combustion (BTU/h) is a function of the random input waste flow (lb/h) and the heat of combustion (BTU/lb):

| (42) |

The flame length (ft) can be calculated as a function of the released heat using an approximation of the form:

| (43) |

The flare stack diameter (ft) is sized on a velocity basis. This is done by relating this to the Mach number and the waste flow as:

| (44) |

The flare tip exit velocity (ft/s) is function of the flow and the diameter:

| (45) |

The wind speed (ft/s) is an important environmental factor that affects the tilting of the flame and the distance from the centre of the flame. The following correlations capture the flame distortion as a result of the wind speed and the exit velocity:

| (46) |

| (47) |

Here, and (ft) are the horizontal and vertical distortions. The distortions are used to compute the horizontal , vertical , and total distance (ft) to a given ground-level safe point as:

| (48) | ||||

| (49) | ||||

| (50) |

Here, (ft) is the flare height. The flame radiation (BTU/h ft is a function of the heat released and the total distance:

| (51) |

A primary safety goal in the flare stack design problem is to control the risk that the radiation exceeds a certain threshold value (BTU/h ft2) at the ground-level reference point . This is modeled using the CC:

| (52) |

The objective function is the cost (USD), which is a function of height and diameter:

| (53) |

The height and the diameter are key design parameters that control the radiation experienced at the reference point (i.e., a higher and wider flare reduces the radiation intensity). As a result, there is an inherent trade-off between capital cost and safety that needs to be carefully handled. The overall goal of the optimization problem is to determine the optimal value of the height and diameter. We assume that the random input waste flow follows an exponential distribution (with a rate parameter 21, 000 lb/h). We generate 2000 scenarios from this distribution and we set . The total number of variables in the NLPs is on the order of 18,000. A Julia model implementation along with all necessary data and parameters (e.g. ) is available at https://github.com/zavalab/JuliaBox/tree/master/FlareDesignSigVaR.

A conservative solution is first obtained by enforcing radiation constraint for all scenarios. The cost associated with this approach is $ 149,284. Table 4 summarizes the performance of SigVaR-Alg. The cost obtained with CVaR-P is $ 121,170. Although this approximation has reduced the cost by 18.8% compared with the scenario approach, this performance is still too conservative. In particular, although the CC only requires to hold with a probability of 0.95, the CVaR-P solution satisfies it with probability 0.979. From the solution CVaR-P we obtain . From Table 4 we also see that the SigVaR approximation becomes less conservative as we increase and that the objective value is progressively improved. After eight iterations, SigVaR-Alg solves SigVaR-P with and and reduced the cost to $ 109,488, which is of 9.6% lower than the cost of CVaR-P. The probability of satisfying chance constraint is reduced to 0.951. We can thus see that the economic benefits of reducing conservatism can be quite significant.

Table 3 summarizes the performance of the smooth SS-P approximation. For the first 4 iterations, the cost does not monotonically decrease as we increase the value of . This might be due to the fact that there are multiple local optimal solutions. When , IPOPT has numerical difficulty in solving the problem. The cost obtained with this approximation is 3.8% lower than the solution obtained with CVaR-P, but 6.4% higher than the cost of SigVaR-Alg.

| Cost | Time | Ipopt | |||||

|---|---|---|---|---|---|---|---|

| (USD) | (Btu/(hr )) | (sec) | Iter | ||||

| CVaR-P | - | - | 121,170 | 1612 | 0.979 | 20 | 143 |

| 1 | 2.5 | 0.0045 | 118,176 | 1687 | 0.975 | 3 | 37 |

| 2 | 5.0 | 0.0079 | 115,893 | 1767 | 0.971 | 4 | 52 |

| 3 | 10.0 | 0.0144 | 113,815 | 1833 | 0.965 | 4 | 49 |

| 4 | 20.0 | 0.0275 | 112,258 | 1885 | 0.962 | 6 | 65 |

| 5 | 40.1 | 0.0537 | 111,134 | 1923 | 0.957 | 9 | 97 |

| 6 | 80.2 | 0.1061 | 110,328 | 1952 | 0.954 | 15 | 121 |

| 7 | 160 | 0.211 | 109,780 | 1971 | 0.951 | 104 | 512 |

| 8 | 320 | 0.420 | 109,488 | 1982 | 0.951 | 45 | 439 |

| Cost | Time | Ipopt | ||||

| (USD) | (Btu/(hr )) | (sec) | Iter | |||

| 1 | 100 | 138,865 | 1214 | 0.997 | 119 | 708 |

| 2 | 50 | 141,880 | 1161 | 0.998 | 58 | 445 |

| 3 | 25 | 142,004 | 1159 | 0.998 | 106 | 698 |

| 4 | 12.5 | 135,526 | 1277 | 0.996 | 150 | 951 |

| 5 | 6.25 | 131,540 | 1359 | 0.993 | 80 | 723 |

| 6 | 3.125 | 126,018 | 1486 | 0.988 | 85 | 565 |

| 7 | 1.563 | 122,023 | 1589 | 0.981 | 9 | 78 |

| 8 | 0.781 | 116,472 | 1749 | 0.972 | 5 | 35 |

| 9 | 0.390 | - | - | - | - | - |

| 10 | 0.195 | - | - | - | - | - |

6 Concluding Remarks

We have proposed a sigmoidal approximation for chance constraints that we call SigVaR. We prove that SigVaR is conservative and that the level of conservatism can be made arbitrarily small for limiting values of the approximation parameters. We also provide conditions for the parameters guaranteeing that the SigVaR approximation is less conservative than the conditional value at risk (CVaR) approximation and other smooth sigmoidal approximations available in the literature. The SigVar approximation brings computational benefits over mixed-integer reformulations because its sample average approximation can be formulated as a standard nonlinear program. We also conduct numerical experiments to demonstrate that it can significantly reduce the conservatism of CVaR. A limitation of SigVaR, however, is that numerical instability is encountered for limiting parameter values. To ameliorate this issue, we proposed an algorithmic scheme that solves a sequence of approximations of increasing quality. This scheme exploits connections between the parameter values of SigVaR and the VaR detected with the CVaR approximation. As part of future work, we are interested in studying more closely the behavior of the sigmoidal approximation from numerical stand-point. In particular, while the proposed scheme does improve numerical performance, extreme sensitivity of the sigmoidal function for large parameter values remains an issue.

References

- (1) Ahmadi-Javid, A.: Entropic value-at-risk: A new coherent risk measure. Journal of Optimization Theory and Applications 155(3), 1105–1123 (2012)

- (2) API, R.: 521. Recommended practice 521(3) (1997)

- (3) Bienstock, D., Chertkov, M., Harnett, S.: Chance-constrained optimal power flow: Risk-aware network control under uncertainty. SIAM Review 56(3), 461–495 (2014)

- (4) Birge, J.R., Louveaux, F.: Introduction to stochastic programming. Springer Science & Business Media (2011)

- (5) Calafiore, G., Campi, M.C.: Uncertain convex programs: randomized solutions and confidence levels. Mathematical Programming 102(1), 25–46 (2005)

- (6) Calafiore, G.C., Campi, M.C.: The scenario approach to robust control design. IEEE Transactions on Automatic Control 51(5), 742–753 (2006)

- (7) Cao, Y., D’Amato, F., Zavala, V.M.: Stochastic optimization formulations for wind turbine power maximization and extreme load mitigation Under Review (2017)

- (8) Cao, Y., Fuentes-Cortes, L.F., Chen, S., Zavala, V.M.: Scalable modeling and solution of stochastic multiobjective optimization problems. Computers & Chemical Engineering 99, 185–197 (2017)

- (9) Chen, C., Mangasarian, O.L.: Smoothing methods for convex inequalities and linear complementarity problems. Mathematical programming 71(1), 51–69 (1995)

- (10) Chiang, N.Y., Zavala, V.M.: An inertia-free filter line-search algorithm for large-scale nonlinear programming. Computational Optimization and Applications 64(2), 327–354 (2016)

- (11) Geletu, A., Hoffmann, A., Kloppel, M., Li, P.: An inner-outer approximation approach to chance constrained optimization. SIAM Journal on Optimization 27(3), 1834–1857 (2017)

- (12) Geletu, A., Klöppel, M., Hoffmann, A., Li, P.: A tractable approximation of non-convex chance constrained optimization with non-gaussian uncertainties. Engineering Optimization 47(4), 495–520 (2015)

- (13) Hong, L.J., Yang, Y., Zhang, L.: Sequential convex approximations to joint chance constrained programs: A monte carlo approach. Operations Research 59(3), 617–630 (2011)

- (14) Jalving, J., Abhyankar, S., Kim, K., Hereld, M., Zavala, V.M.: A graph-based computational framework for simulation and optimization of coupled infrastructure networks. Undr Review (2016)

- (15) Kang, J., Chiang, N., Laird, C.D., Zavala, V.M.: Nonlinear programming strategies on high-performance computers. In: Decision and Control (CDC), 2015 IEEE 54th Annual Conference on, pp. 4612–4620. IEEE (2015)

- (16) Kleywegt, A.J., Shapiro, A., Homem-de Mello, T.: The sample average approximation method for stochastic discrete optimization. SIAM Journal on Optimization 12(2), 479–502 (2002)

- (17) Luedtke, J., Ahmed, S., Nemhauser, G.L.: An integer programming approach for linear programs with probabilistic constraints. Mathematical Programming 122(2), 247–272 (2010)

- (18) Nemirovski, A., Shapiro, A.: Convex approximations of chance constrained programs. SIAM Journal on Optimization 17(4), 969–996 (2006)

- (19) Nemirovski, A., Shapiro, A.: Scenario approximations of chance constraints. In: Probabilistic and randomized methods for design under uncertainty, pp. 3–47. Springer (2006)

- (20) Pintér, J.: Deterministic approximations of probability inequalities. Zeitschrift für Operations-Research 33(4), 219–239 (1989)

- (21) Rockafellar, R.T., Uryasev, S.: Optimization of conditional value-at-risk. Journal of risk 2, 21–42 (2000)

- (22) Rockafellar, R.T., Wets, R.J.B.: Variational analysis, vol. 317. Springer Science & Business Media (2009)

- (23) Shan, F., Zhang, L., Xiao, X.: A smoothing function approach to joint chance-constrained programs. Journal of Optimization Theory and Applications 163(1), 181–199 (2014)

- (24) Shapiro, A., Dentcheva, D., Ruszczyński, A.: Lectures on stochastic programming: modeling and theory. SIAM (2009)

- (25) Sorrels, J.L., Coburn, J., Bradley, K., Randall, D.: Chapter 1. flares. In: EPA Air Pollution Control Cost Manual. United States, Environmental Protection Agency (2017)

- (26) Van Ackooij, W., Henrion, R.: Gradient formulae for nonlinear probabilistic constraints with gaussian and gaussian-like distributions. SIAM Journal on Optimization 24(4), 1864–1889 (2014)

- (27) Wächter, A., Biegler, L.T.: On the implementation of a primal-dual interior point filter line search algorithm for large-scale nonlinear programming. Mathematical Programming 106, 25–57 (2006)

- (28) Zavala, V.M.: Computational strategies for the optimal operation of large-scale chemical processes. ProQuest (2008)