Optimal market making with persistent order flow

Abstract

We address the issue of market making on electronic markets when taking into account the clustering and long memory properties of market order flows. We consider a market model with one market maker and order flows driven by general Hawkes processes. We formulate the market maker’s objective as a stochastic control problem. We characterize an optimal control by proving existence and uniqueness of a viscosity solution to the associated Hamilton-Jacobi-Bellman equation. Finally we propose a fully consistent numerical method allowing to implement this optimal strategy in practice.

Keywords: Hawkes processes, market making, high frequency trading, stochastic control, partial differential equations, viscosity solutions.

1 Introduction

Most electronic exchanges are organized as anonymous continuous double auction systems. Market participants can send limit orders to a central limit order book (LOB for short) displaying the volume of shares and the price at which they stand ready to buy or sell those shares. Market participants can also use market orders specifying a volume to buy or sell instantaneously at the best available price. In a very stylized view we can consider that there are two types of market participants: market takers seeking to buy or sell shares for strategic purposes using market orders and market makers filling the LOB with limit orders. Market makers play the role of intermediaries between buyers and sellers market takers.

In practice one of the main risks faced by a market maker is the inventory risk. For example if he has a large positive inventory, price may decrease to his disadvantage. Market makers thus design their strategies in order to mitigate this risk. Basically we expect a market maker with a large positive inventory to set attractive ask prices and less competitive bid prices to attract more buy than sell market orders. More generally he must adapt his strategy to the main statistical features of order flows. Two key stylized facts market makers should take into account in their trading strategies are the clustering and long memory properties of market order flows. The clustering property refers to the fact that buy and sell market orders are not distributed homogeneously in time but tend to be clustered, see [14]. In practice it means that after a buy (for say) market order it is likely that a new one is going to be sent shortly. The long memory of market order flows means the autocorrelation function of trades signs ( for a buy order and for a sell order) has a power-law tail, see [19]. In this paper our goal is to propose a method to design market making strategies that take into account those two features of market order flows.

The issue of market making while managing inventory risk has been notably addressed in [3, 11] where market order flows are modeled using Poisson processes, see also the books [5, 10]. But Poisson processes neither reproduce the clustering nor the long memory property of market order flows. Dealing with the same topic the authors of [6, 27] use a refined model based on Hawkes processes with exponential kernels. The same modeling is also used in [2, 14] to design optimal liquidation strategies. With such kernels Hawkes processes reproduce the clustering property of market order flows but not its long memory. However when the kernel has a power law tail, both properties are reproduced, see [4, 18]. Hence in this paper we extend the works [3, 6, 11] to market order flows driven by Hawkes processes with general kernels.

We now make precise the market model we use. We consider a market with one market maker controlling the best bid and ask prices and with market takers sending only market orders of unit volume. We denote by (resp. ) the total number of buy (resp. sell) market orders sent between time and time and the market maker’s inventory, which is null at time . As in [3] the market maker controls the bid and ask spreads, denoted by and . The corresponding best ask and bid prices are and , where is the fundamental price of the underlying asset. The set of admissible controls is then

where predictability is relative to the natural filtration generated by , see Section 5.1 for more details. Since market takers are seeking for low transaction costs, their trading intensity is decreasing with the spreads. More precisely we know, from classical financial economics results, see [8, 20, 26], that the average number of trades per unit of time is a decreasing function of the ratio between spread and volatility. To model this we consider that market order intensities are given by

where is a positive constant, the price volatility and

where is a continuous function and a completely monotone function222In this paper we consider complete monotony on .. Note that if the spreads are null, the processes and are, as intended, generalized Hawkes processes with kernel . Regarding the dynamics of we assume it is given by

| (1) |

where is a Lipschitz function.

Inspired by [3, 6, 11] we consider that the market maker’s problem is equivalent to solve the following stochastic control problem:

| (2) |

where is a positive constant and and are two continuous functions with at most quadratic growth. The former represents a continuous reward received by the market maker (besides its P&L) and the latter is a final lump sum payment received at the end of the trading horizon. Typical choices would be and . The notation denotes the expectation under the law corresponding to the control (see Section 5.1 for details).

When the order flows are Poisson processes (corresponding to constant) the process is Markovian. Hence to solve the market maker’s optimization problem the authors of [3] study the associated Hamilton-Jacobi-Bellman equation (HJB for short). However when and are general Hawkes processes is not Markovian333In the exponential case the process is Markovian.. In order to circumvent this issue we need to consider auxiliary state variables enabling us to work in a Markovian setting. More precisely we consider the process where

Note444To define and we consider that is extended to with value on . that and are random functions from into and that the process is Markovian. Studying the HJB equation associated with this representation, we prove in Section 2 that the stochastic control problem (2) admits a solution of the form , where is a feedback control function.

The HJB equation associated with (2) and the representation is defined on a subset of an infinite dimensional vector space. So we cannot rely on classical numerical methods to approximate . To tackle this issue we propose the following strategy.

-

1.

We show that if converges towards in and uniformly on then converges almost surely towards .

-

2.

We show that when , there exists a Markovian representation of the model in dimension . Therefore in this case the feedback control can be approximated numerically.

-

3.

Inspired by [1], we prove that for any completely monotone kernel in , we can find a sequence , converging towards in and uniformly on , such that for any , is a linear combination of decreasing exponential functions.

Those three points show that if is close from then , which is related to a finite dimensional HJB equation, is good approximation of . However when is large we cannot rely on finite differences methods to compute the feedback control since the dimension of the associated HJB equation is too large. Hence for numerical experiments we use the probabilistic representation of semi-linear partial differential equations (PDEs for short) introduced in [13].

The paper is organized as follows. In Section 2 we prove existence of a solution to Problem (2) based on the study of its associated HJB equation. In Section 3 we explain how to approximate the optimal control obtained in Section 2. Finally in Section 4, we present some numerical experiments. Main proofs are relegated to Section 5.

2 Solving the market maker problem

In this section we prove existence of a solution to Problem (2). First we define an appropriate domain for the process . Then we show that the HJB equation associated to (2) has a unique viscosity solution with polynomial growth on this domain. Finally we prove existence and characterize an optimal control solving (2).

2.1 Appropriate set for the process

To study uniqueness of solution to a PDE in the sense of viscosity, it is convenient to work with locally compact domain. We have , but is not locally compact. Hence we need to make precise the set in which the processes and belong. Obviously for or we have

We naturally endow with the topology and prove in Appendix A that it has the following topological properties.

Lemma 2.1.

-

(i)

The set is a locally compact closed subset of .

-

(ii)

For any sequence with values in such that for any , , if converges towards then we have and when .

-

(iii)

Moreover if is a sum of exponential functions then we have for any

Points and are purely technical and are used in Section 3. We now define a locally compact domain for the process . More precisely for any we consider

According to Lemma 2.1 the set (resp. ) is a locally compact closed subset of (resp. ). We also define

which is a locally compact closed subset of . Obviously for any we have . Hence is the appropriate domain to use the theory of viscosity solutions.

Before going to the next section we give additional definitions that we use later on. For we define the norm

Then for any positive the following set is a compact subset of , as consequence of Lemma 2.1 ,

Finally in order to lighten the notations from now on when we consider (resp. , ) we implicitly assume that resp. , .

Now that we have defined an adapted domain for PDE analysis we derive in the next section the HJB equation related to the stochastic control problem (2).

2.2 Hamilton-Jacobi-Bellman equation associated to the control problem

We start by rewriting the stochastic control problem (2). We note that up to a -local martingale the integrals

are respectively equal to and . Hence as a consequence of Appendix B.3 for any we have

Thus (2) is equivalent to the stochastic control problem

| (3) |

In order to give intuition on the HJB equation related to this stochastic control problem we write the Ito formula related to for a fixed control . We consider a function defined on that is . We call any function with such regularity a test function. For any we have

where

are -uniformly integrable martingales, see Appendix B.1 for details. The operator is the infinitesimal generator related to the diffusion of and is defined for any test function and by

The operators and correspond to the infinitesimal generators related to the diffusion of and . They are defined for by

Hence the HJB equation associated to the control problem (3) is

with , and where the function is defined for by

A straightforward computation gives the maximizers

| (4) |

Note that the dependence in of lies in the operator .

For such general partial-integro differential equation (PIDE for short) it is a priori impossible to prove existence of a smooth solution. Therefore in the next section we look for viscosity solutions.

2.3 Viscosity solutions: definitions

Since we are dealing with a PIDE defined on an unusual domain and in order to make things precise we define the notion of viscosity solution in our framework. First we give the classical definition and then its counterparts based on semi jets.

Definition 2.1.

-

-

A locally bounded function (the set of upper semi-continuous functions on ) is a viscosity sub-solution of if for all and test function such that is a maximum of we have

-

-

A locally bounded function (the set of lower semi-continuous functions on ) is a viscosity super-solution of if for all and test function such that is a minimum of we have

-

-

A continuous function defined on is a viscosity solution of if it is a viscosity super-solution and a viscosity sub-solution.

Note that in the above definition it is equivalent to consider local (or local strict) extrema. Also note that we have not replaced by for the last operator . This is because only requires finiteness of to be defined. Of course it is equivalent to replace by in Definition 2.1. Indeed consider a sub-solution and a test function at point . Since is a non local operator we can always build a sequence of test functions satisfying with equality at point and such that

By continuity of we get the equivalence. This also holds for super-solution.

We now introduce the notions of semi super and sub-jets in our framework. For in and , the super-jet of at point is the set

and the semi super-jet of at point is

In the above definition the convergence of is taken in the sense of locally uniform convergence at point . By analogy we define the sub-jet and the semi sub-jet for in .

We can now give another characterization of viscosity sub and super-solutions relying on the notions of semi jets.

Definition 2.2.

-

-

A locally bounded function is a viscosity sub-solution of if for all , and we have

-

-

A locally bounded function is a viscosity super-solution of if for all , and we have

In the next section based on the study of we prove that the control problem (2) admits a solution.

2.4 Existence of an optimal control

In this section we prove existence of a solution to Problem (3), which is equivalent to (2). Before stating the result we give a sketch of the proof.

We start by proving uniqueness of a viscosity solution with polynomial growth to using a comparison result. The main difficulty is to adapt the Crandall-Ishi’s lemma to our framework, which is done in Appendix D. Using a verification argument we then check that the continuation utility function associated to Problem (3) is actually this unique solution. The maximizers of the Hamiltonian given in Equation (4) then naturally provide a control solving (3) and therefore Problem (2). Full proof is given in Section 5.2.

Theorem 2.1.

-

(i)

There exists a unique viscosity solution with polynomial growth to .

-

(ii)

This solution satisfies:

- (iii)

It is important to note that in order to obtain existence of an admissible optimal control we have benefited from the fact that we are dealing with counting processes, whose infinitesimal generators are defined for any finite functions independently of their regularity. From a practical point of view Theorem 2.1 implies that if we manage to compute we can implement the optimal control by monitoring the processes and . Note that this is equivalent to monitor the list of arrival times of buy and sell market orders. However is a subset of an infinite dimensional vector space. So we cannot compute using classic numerical methods. Therefore we need to find another way to approximate the control . We deal with this issue in the next section.

3 How to approximate the optimal control

In this section we explain how to approximate numerically the feedback control . We proceed in three steps:

-

1.

We show that if converges towards in and uniformly on then converges almost surely towards .

-

2.

We prove that when there exists a Markovian representation of the model in dimension .

-

3.

Inspired by [1], we show that for any completely monotone function in we can find a sequence converging towards in and uniformly on such that for any , is a linear combination of decreasing exponential functions.

Those three points give a simple method to compute an approximate version of the control : choose , a sum of decreasing exponential functions, close enough to . Use the finite dimensional representation to compute and implement instead of .

3.1 Convergence of solutions and optimal controls

Consider a completely monotone function in . We show that if a sequence of continuous functions converges towards in and uniformly on then the sequence converges almost surely towards .

From Theorem 5.8 in [25] we observe that the notion of viscosity solution is perfectly adapted to prove the convergence of solutions to a sequence of PIDEs. Hence we prove in Section 5.3 the following result which is an extension of Theorem 5.8 in [25] to our framework.

Proposition 3.1.

Consider a sequence of continuous functions converging towards a completely monotone function in and uniformly on , then for any we have

| (6) |

where

The main technical difficulty in the proof of Proposition 3.1, compared to Theorem 5.8 in [25], is that the functions are defined on different domains.

We now consider a fixed sequence of continuous functions converging towards in and uniformly on . We have that almost surely

From now on, when we consider a similar limit result we forget to write to lighten notations.

We first recall that with

where

Obviously we have the following almost sure convergences

So according to Proposition 3.1 we get that almost surely

Hence we obtain the following result.

Proposition 3.2.

Consider a sequence of continuous functions converging towards a completely monotone function in and uniformly on , then for any we have almost surely

Proposition 3.2 perfectly fits our purpose of approximating . Indeed suppose we manage to find a dense555Here dense is intended in the sense of convergence in , together with uniform convergence on . subset of the completely monotone functions such that for any in this subset, the control can be approximated numerically. Then Propositions 3.1 and 3.2 guarantee that for any completely monotone function in we can approximate numerically and .

We show in the next two sections that the set

satisfies those two conditions. Note that is simply the set of positive linear combinations of decreasing exponential functions. In the next two sections we study Problem (3) when the function is in and then show that is dense in the set of completely monotone functions in .

3.2 Solving the market maker’s problem when

In this section we explain how to solve Problem (3) when the kernel function is in .

We consider that the kernel of the Hawkes processes and is

where is a positive integer, and . For and or we define the process

Then is a Markovian process since for or

The domain associated with this representation is , which is locally compact. As for , when we have we implicitly consider that . Note that we can naturally go from the first representation to this one. More precisely we prove in Appendix E that there exists a continuous function from into such that for any we have . However notice that the second representation is somehow larger than the first one.

The infinitesimal generators associated to the processes and for the new representation are denoted by and . They are defined for any function on and by

The HJB equation related to Problem (3) in this new representation is therefore

with where for or , , ,

and where the function is defined for by

We easily adapt the proof of Theorem 2.1 to and prove the following result.

Theorem 3.1.

-

(i)

There exists a unique continuous viscosity solution with polynomial growth to .

-

(ii)

The solution satisfies

- (iii)

-

(iv)

We have .

The proof of the three first points is exactly the same as the proof of Theorem 2.1. We deal with point in Section 5.4. Points and of Theorem 3.1 imply that for any and in we can approximate numerically . We just need to approximate using any numerical method, which is possible because the domain of is a subset of a finite dimensional vector space. Then using the change of variable one gets

Note that this shows that the controls given in Theorem 2.1 (iii) and given in Theorem 3.1 (iii) are actually the same.

3.3 Density of in the set of completely monotone functions

In this section we show that is dense in the set of completely monotone functions in . Before giving the result we present a short sketch of the proof.

The key idea is that any completely monotone function can be written as the Laplace transform of a positive measure , see Lemma 2.3 in [21]:

| (7) |

Moreover if then is and if is in then . Hence using Riemann sums to approximate the integral (7) we get a natural way of approximating by a sequence of functions in . Based on this idea we prove the following result in Appendix F.

Lemma 3.1.

For any completely monotone function in there exists a sequence , such that:

-

For any , ,

-

converges towards in and uniformly on every compact set of ,

-

3.4 Conclusion on approximating the optimal control

For a completely monotone function in consider a sequence given by Lemma 3.1. We write instead of to lighten notations. According to Proposition 3.2, we have the following almost sure convergence for any

Hence to implement an approximated version of the optimal control we simply have to implement the control for large enough. This approximated control can be computed by solving numerically the finite dimensional PIDE .

In conclusion the recipee to implement an approximated version of the optimal control is the following:

-

1.

Fix positive and find such that is the closest possible from . See Appendix F for a method to choose such and .

-

2.

Approximate numerically , the solution of , which is equivalent to approximate numerically the feedback .

-

3.

Monitor and apply the control .

The only flaw of this method is that the set is a subset of a vector space of dimension . Hence when is larger than it is very unlikely that simple finite differences methods can be used to solve numerically . To tackle this issue we need to use other numerical methods such as neural networks, see [15] for example, or probabilistic method, see [13]. In this article we propose to use the later method for numerical applications.

4 Numerical applications

In this section we present some numerical experiments illustrating our results. We consider a simplified version of the market maker’s problem:

This corresponds to and . We take and . We note the unique viscosity solution (with polynomial growth) of the HJB equation associated to when the Hawkes processes’ kernel is . In this section we discard the price variable from the PIDEs since it does not appear in the optimization problem.

We first consider in Section 4.1 the cases of kernels in with and show the importance for market makers to take into account the clustering and long memory properties of market order flows in their trading strategies . Then in Section 4.2 we deal with more complex functions and illustrate the convergence of the method described in Section 3.4. In this last Section to solve the PIDEs we use the probabilistic representation introduced in [13] which is described in Appendix H.

4.1 The impact of taking into account the self exciting property of market order flows

In this section we consider that for a positive constant and that the kernel is of the form:

This means that for or

In order to illustrate the interest of taking into account the clustering and long memory properties of market order flows we are going to compare three trading strategies corresponding to three controls and . Each of those controls is computed in the following way:

-

is the optimal control of a market maker believing that buy and sell market order flows are Poisson processes with intensity .

-

is the optimal control of a market maker believing buy and sell market order flows are Hawkes processes with kernel and that the value of is .

-

is the optimal control .

The first and second market makers are misleading on the dynamics of the market order flows so their strategies are suboptimal.

To compute the controls and the associated value functions we solve the corresponding HJB equations using finite differences methods. We use the following parameters settings:

-

,

-

, and ,

-

, and .

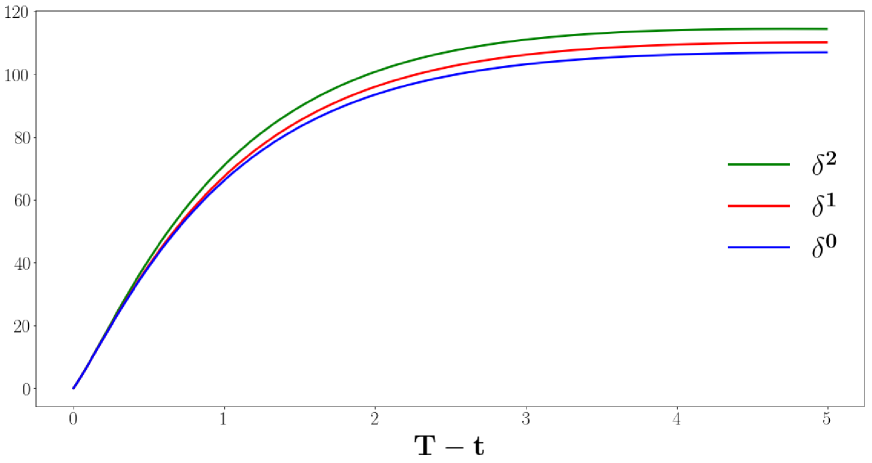

We compare the different value functions associated to each controls in Figures 1, 2 and 3. As expected the control is optimal and is sub-optimal compared . Moreover we observe in Figure 1 that considering an exponential kernel Hawkes model for the order flows leads to a gain compared with a strategy considering that market order flows is a Poisson process. Using two exponentials leads to another gain. This shows the large gain that can arise from taking into account the clustering and long memory properties of market order flows when designing a market making strategy.

4.2 Numerical illustration of Section 3.4

In this section we use the method presented in Section 3.4 to estimate at several points when the function is the following completely monotone function:

for , , and is a small shift used for numerical purposes.

We explain in Appendix G how to build in this case the sequence given by Lemma 3.1. As in Section 3.4 we note .

For any we consider the following elements of

and the following elements of

According to Proposition 3.1 we have

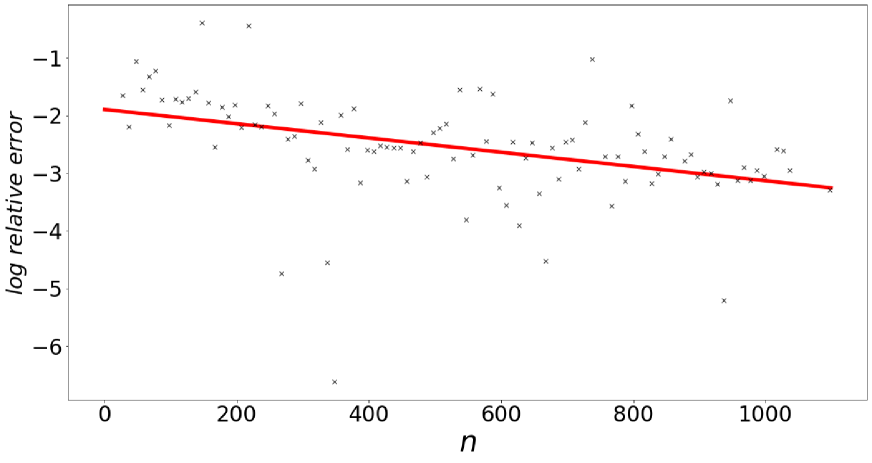

This convergence is illustrated in Figure 4. We used the probabilistic representation of [13] to compute the and , see Appendix H for more details. This proves the tractability of the method presented in Section 3.4.

.

Acknowledgments

We thank Thibaut Mastrolia, Mathieu Rosenbaum and Nizar Touzi for many interesting discussions. The author gratefully acknowledges the financial support of the ERC Grant 679836 Staqamof and of the chair Analytics and Models for Regulation.

5 Proofs

In this section we drop the superscript for the processes , and to lighten the notations.

5.1 Formal definition of the probability space

In this section we make precise the probability space we are working on. In particular we give a proper definition to . First we define the canonical process and the probability space associated to our stochastic control problem.

-

-

Consider the set of increasing piecewise constant càdlàg functions from into with jumps equal to and the set of continuous functions from into . We define .

-

-

We let be the canonical process on .

-

-

The associated filtration is where (resp. ) is the right continuous completed filtration associated with (or ) (resp. ).

-

-

We denote by the probability measure on such that , for , are local martingales and is a Brownian motion .

We now introduce some processes we use later in this paper. For a fixed we define that is the state of the system after time when starting from point . The dynamics of is given on by

Using those processes we explicit the change of measure associated to each control process. For this we consider the functions

that represent the ask and bid intensity in the state when the control is . For any we define by

where is the Doléans-Dade exponential of

Since and , by the Corrolary 2.6 in [24], for any , is a true martingale. Moreover by Theorem III-3.11 in [17] the processes

are -local martingales on . Actually they are true martingales, see Appendix B.1.

For and we note the expectation under the law and note instead of .

Finally, for any bounded continuous function, and stopping time with values in we have:

| (8) |

where, is the restriction to of . This prove that for any the process is Markovian.

5.2 Proof of Theorem 2.1

We proceed in 5 steps.

-

1.

Section 5.2.1: Using a comparison result we show that admits a unique viscosity solution with polynomial growth.

- 2.

-

3.

Section 5.2.3: We prove a dynamic programming principle for .

-

4.

Section 5.2.4: Using a verification argument we show that is the unique viscosity solution (with polynomial growth) of .

- 5.

5.2.1 Comparison result for

We start by proving a comparison result for bounded solutions, then we extend it to functions with polynomial growth.

Proposition 5.1.

Let be a bounded from above viscosity sub-solution of and be a bounded from below viscosity super-solution of such that then

Proof.

We suppose that there exists some such that

By hypothesis, necessarily . We show that this implies a contradiction. We consider the following quantities

and

The functions and being bounded from above we have

uniformly in . Thus we can restrict the supremums to bounded sets that depends only on . More precisely

| (9) | |||||

| (10) |

where only depends on . Since the set is compact the supremum is achieved at some . We show at the end of the proof that when , up to a subsequence, we have

| (11) |

where achieves the supremum . We also prove that

| (12) |

and that

| (13) |

A consequence of Equation (13) is that

| (14) |

We use the notations .

With respect to Lemma D.1, which is an adaptation of the Crandall-Ishi’s lemma to our framework, for any there exists and such that

with

Remark that for small enough

We now walk towards a contradiction by showing that

According to the definition of sub-solution and super-solution we have

and

By definition of :

thus

where

Note that the function is Lipschitz continuous. Taking we get

The RHS can be taken arbitrarly small when and by Equation (12). Using the Lipschitz property of we have

Here the RHS goes to zero when and due to Equation (12). Finally, by Equation (14) and since (resp. ) is a USC (resp. LSC) function and is continuous and decreasing with respect to its last variable we have

Remark that for any such that we have by definition of

Consequently we have

and so

The monotony and Lipschitz regularity of implies

Notice that for any

thus there exists such that . Consequently we get

that goes to zero when taking the limit . Finally we have shown that

which is a contradiction.

We finally prove the statements (11), (12) and (13). We consider that exists since is compact. Since then necessarily . We now prove the first limit of (12) and that corresponds to a point where the supremum is achieved. Passing to the lower limit we get

Hence by definition of we necessarily have that and that

To conclude we show that and that . For consider that is -optimal in the definition of :

For small enough is lower than , and we get

Therefore we get convergence of towards and as consequence

Since for any we have

we get that . This concludes the proof.

∎

We now extend Proposition 5.1 to the case of functions with polynomial growth.

Proposition 5.2.

Let with polynomial growth be a viscosity sub-solution of Equation and with polynomial growth be a viscosity super-solution of Equation such that . Then

Proof.

There exists such that

We introduce the following function

where is a positive constant. We have

with polynomials with degree . Consequently for some

We have

and

where and are two polynomials with respective degree and . Consequently for any constant

which is positive for large enough. Hence for any the function is a bounded from above viscosity sub-solution of Equation . Indeed if then consequently

We have for large enough

It implies that

We show in the same way that is a bounded from below viscosity super-solution. Then from Proposition 5.1 we have

and taking to we get the stated result. ∎

An immediate consequence from Proposition 5.2 is that there exists a unique viscosity solution with polynomial growth to . We now prove the existence of such solution using a verification argument.

5.2.2 Definition of the continuation utility function

For and we define

where

We also define

| (15) |

that is the maximal utility than can expect a market maker starting its trading from time with initial market condition given by . By Lemma B.1 we get that has polynomial growth. More precisely there exists a positive constant such that

We also define

the set of controls starting from and independent from the past. Since under the processes and have independent increments, using the same arguments than in Remark 2.2- in [25] we get

In the next sections we show that the function is the unique viscosity solution with polynomial growth to . For this we prove a dynamic programming principle for and then conclude using a verification argument.

5.2.3 Dynamic programming principle

Consider the lower and upper semi-continuous version of :

Inspired by [25] we prove the following dynamic programming principle.

Theorem 5.1.

Let be fixed and be a family of finite stopping times with values in . Assume that for any , is -bounded. Then we have

and

The proof of Theorem 5.1 is the same as the one of Theorem 2.3 in [25]. However since we are working on non-standard domains we write the proof for the sake of completeness.

Proof.

We first show the first inequality. We consider a continuous function such that . By definition of for any there is an admissible control that is optimal:

Using Fatou’s lemma and the fact that and are lower semi-continuous we get that is a lower semi-continuous function. Then being upper semi continuous we can find a family of positive real such that for any we have

where

The system forms an open covering of . With the topology it is endowed is second countable since is second countable. Hence by the Lindelöf covering Theorem we can extract from a countable subfamily that covers . Thus we have such that

Set . Consider and define the sequence

Now fix . With the above construction, we have and for , we have

We define the control process by

The control is in . By Equation (8) we have

Thus we get

Since is a true martingale and for we have

By dominated convergence letting we get

Since is any positive real we have

We now explain how to pass from dominated by to . By hypothesis, for any we can find such that almost surely for any . Then we can find an increasing sequence of continuous functions on , such that and such that converges pointwise towards on (see Lemma 3.5. in [22]), where

Consequently from monotone convergence Theorem we have

Then we can pass to the supremum in to get the result.

Now we show the first inequality. Take and consider the controlled process obtained after freezing the trajectory of up to time . By definition of we have

Using Equation (8) this gives

Now taking the average, by arbitrariness of we get the second inequality

∎

In the next section we show that is a viscosity solution of using a verification argument based on Theorem 5.1.

5.2.4 Verification

In this section using the dynamic programming principle proved previously we prove that (resp. ) is a viscosity super (resp. sub)-solution of . The proof is inspired from the proof of Propositions 6.2 and 6.3 in [25].

Proposition 5.3.

The function (resp. ) is a viscosity sub (resp. super)-solution of .

Proof.

We first show that is a viscosity super-solution and then that is a viscosity sub-solution.

Let and be a test function such that

and a sequence in such that

Since is continuous we have

Let and consider the constant control process equal to . We use the notation and . Finally, for all we define the stopping time:

where the ball for , centered in with radius positive and small enough such that if a jump occurs then the stopping time is immediatly reached. We take

Notice that almost surely.

From the first inequality in the dynamic programming principle, we have

Now using that we get

We can use the Ito formula since is smooth. Thus we get

where

and with

The function being continuous, the integrands in the term are all bounded so the expectation of under is . Consequently we have

Taking using dominated convergence and arbitrariness of we get

The control being arbitrary we finally have that

Thus is a viscosity supersolution of .

Now we suppose that is not a viscosity subsolution of and exhibit a contradiction. According to the definition of viscosity subsolution we can find a test function and such that

and that

| (16) |

By continuity of and we have existence of a small enough such that on we have

Moreover we can find some (up to a change of ), such that

where is the set of all values that can be reached if a jump occurs inside . Note that it is a compact set. We consider a sequence such that

Since we can assume that

For a fixed control We define the stopping time

At the stopping time, either the process has not jumped and so is on or has jumped and is in . Thus

We derive from the Ito formula

Hence using Equation (16) we get

Since is any control and is positive this contradict the second equation of Theorem 5.1. Thus is a viscosity sub-solution of .

∎

5.2.5 Proof of Theorem 2.1

To prove Theorem 2.1 we must show that .

As we did previously we can show that is the unique viscosity solution with polynomial growth of

But since is a viscosity solution of and by definition of , is also a viscosity solution with polynomial growth of . This gives the result.

5.3 Proof of Proposition 3.1.

We define the following functions on :

We show that and are respectively a viscosity super-solution and a viscosity sub-solution of .

Consider a test function and a strict minimizer of . We have existence of a sequence in such that

Consider the closed ball of with radius centered in . Then we can always suppose that . Let be a minimizer of the difference on (exists because is locally compact). We note . We show at the end of the proof that there exists such that is the limit of a subsequence of and that for and . Hence we can write

Thus by definition of we get that converges towards and that

As a consequence when is large enough is a local minimizer of (because it is in the interior of ) hence by definition of viscosity solutions

Then by definition of and since :

Finally since is decreasing with respect to the last variable and since converges towards for and we have

So by Definition 2.1 is a viscosity super-solution of . In the same way we can show that is a viscosity sub-solution of . Moreover since the a priori inequalities on can be chosen uniform in (because ) they are true for and . Therefore Proposition 5.2 implies that . Because we have the other inequality by definition we get , the unique viscosity solution with polynomial growth of .

To complete the proof we show that admits a subsequence converging towards some and that for and , converges .

We have with

where and are non-negative integers, and are in . We recall that is bounded. Hence up to a subsequence converges towards some . Since we have assumed that is positive the convergence of and imply those of and . Consequently those sequences are eventually constant and equal to and for large enough. Then up to a subsequence we have convergence of and since they take their values in and which are compact sets. We consider and their limits. We now show that converges in towards

We show that converges in towards to conclude. We write

The first term goes to by hypothesis, the second by dominated convergence. Same results holds for and . Consequently we have proved the convergence of towards

We finally show that converges towards , the same methodology holds for . We have for large enough

The uniform convergence of towards implies that converges towards . This concludes the proof.

5.4 Proof of point of Theorem 3.1

We recall that the proof of Theorem 3.1 is exactly the same of Theorem 2.1. Hence for any we define for the process by analogy with the process defined in Section 5.2.2. Note that by construction for any and for any we have for

| (17) |

Then as in Section 5.2.4 we prove that the function

is the unique viscosity solution with polynomial growth of . Moreover for any and by Equation (17) we have:

Therefore for any we have . This concludes on the proof of point of Theorem 3.1.

Appendix A Proof of Lemma 2.1

We first prove (i). Consider a sequence with values in that converges towards some in . We have

The convergence of towards gives that is constant and equal to some up to a certain rank. Finally for any subsequence converging to some we have :

so is closed. Now with the same notation we consider a bounded sequence . We can find a subsequence such that is constant and equal to some and such that for , . This implies that

This shows that that is locally compact.

Now we prove (ii). Consider a converging sequence such that for any and let be the limit of . Then necessarily converges towards . Moreover by comparison we have and by continuity of that

Finally consider now that , for we have

The convergence of thus imply that .

Appendix B A priori inequalities

In this section we prove some a priori inequalities.

B.1 Hawkes processes

Consider a Hawkes process with kernel and exogenous intensity . The intensity of is given by

The existence of such process is proved in [16]. Consider , by to [16], . To lighten the notations we write . We have for any

thus using a Grönwall’s lemma we get . The RHS being independent of and using monotone convergence we get

We also have

Using again a Gronwall lemma we deduce that with independent of , so

Now consider a Hawkes process with kernel bounded and intensity given by

with non decreasing in its last variable and such that for some . By the thinning property we can see as dominated by some Hawkes process with kernel and exogenous intensity . Remark that as a consequence dominates . Hence we get

then consequently

This ensures that the function defined in Equation (15) is well defined. This also implies that the martingales and are uniformly integrable martingales.

B.2 A priori estimates on

We prove here that the value function defined in Equation (15) has polynomial growth in . For this we show some inequalities on the norm of . More precisely we prove the following result:

Lemma B.1.

There exists some positive constant depending only on and on the regularity constants of and such that for any

and

To prove Lemma B.1, consider and with . We show different a priori estimates on the subprocesses composing under the probability measure .

A priori estimates on and :

We have

since and we have

Taking the expected value over the probability measure using the fact that is a true martingale and a Grönwall lemma we get

| (18) |

where only depends on and on the model constants. Consequently we have for some positive constant

We now give an a priori estimate for the second order moment.

The average of the last term of the right hand side is as consequence of Appendix B.1. Thus taking the average and using a Grönwall lemma we get

| (19) |

A priori estimates on :

We have

By assumption there exists such that :. We have the classic apriori estimates (see for example Theorem 1.2 in [25]).

| (20) |

Where only depends only on the Lipshitz constant and on .

A priori estimates on :

A priori estimates on the value function:

B.3 Rewriting of the utility

We show that for any we have

To conclude it is enough to show that

is a true martingale. We have

and since we get

The last term of the RHS is integrable by Lemma B.1. By the monotone convergence is also integrable so is a uniformly integrable martingale. As consequence we get

Using the sames arguments we get We show that for any we have

Appendix C Equivalence between the two definitions of viscosity solutions

Proof.

We show it for sub-solutions, the demonstration is the same for super-solutions.

Consider a USC sub-solution of in the sense of Definition 2.2. Now consider a test function such that for a neighborhood of in . We show that

Writing we have where is a modulus of continuity of . Thus we have

Consequently

So is a viscocity sub-solution of in the sense of Definition 2.1.

Now we show the opposite implication. Consider a USC function sub-solution of in the sense of Definition 2.1. Consider , we built a test function dominating with equality at point and such that

We will then get the expected inequality that will extend directly to by continuity of .

Using the notation we have

hence

We take the supremum on over a compact neighborhood of , and consider

Since we get

We prove at the end that is a USC function and assume this is true. The last equation means that . Then by an argument developped for the analysis of viscosity solutions on (see for example [9] Lemma 4.1.) we have existence of a function such that

So finally we have on a compact neighborhood of :

This local domination can then be extended to the whole domain .

Finally we show that is a USC function. Fix and . Since is USC and continuous, for any we can find such that on we have

The collection forms an open covering of which is a compact set by Lemma 2.1. Thus we may find a finite sequence that covers . Consider . Now take any , then fo any there is some such that . Hence we get

so and consequently

Passing to the supremum in in the LHS we get that is USC. ∎

Appendix D Crandall Ishi’s lemma

The most crucial point to prove comparison result for viscosity solutions is the Crandall-Ishi’s lemma that allows to deal with the second order terms. In the general case the Crandall Ishi’s lemma is proved for subset of , see [7]. Hence our particular domain requires an adaptation of the classic version of the Lemma.

Lemma D.1.

Let , and , and . Suppose we have such that

| (22) |

Then for any there is and in such that

and that

| (23) |

where is the Hessian operator and denotes the spectral radius of the matrix .

Note that even thought this extension is not straightforward we benefit from the fact that in the second order derivative concerns a real variable. Therefore to prove this result we are going to benefit from the usual Crandall Ishi’s lemma.

Proof.

Suppose there exists a compact neighborhood of in such that on we have

where is any modulus of continuity of the function and a positive constant. For consider for or . Hence on we have:

| (24) |

with equality at and with .

We can always assume that there exists so that is of the form

where denotes the closed ball with center and radius . We define the following functions

where the supremums above are taken for such that . The functions and are respectively USC and LSC functions since the supremums are taken over compact subsets (see the proof of Lemma C.1). And we have

Thus by the Crandall Ishi’s lemma (see for example Theorem 6.1. in [9]) there exists satisfying (23) such that

Consequently there exist a sequence such that

So for any we have

Consider and such that

such maximizers exist by compacity. We show that converges towards , we assume it for now. Equation (24) implies that for any we have

Consider the function such that and

Since converges towards the sequence converges uniformly towards because is continuous and because we are working on compact neighborhood. Consider that converges towards

Thus we have

hence and

Finally we show that which will imply the conclusion that

We have for any :

Consider any . Since , by upper semi-continuity of and by the definition of we get

Which implies that since everywhere else the above inequality is false because of Equation (24). Hence we get

and so

Similarly we get

This concludes the proof. ∎

Appendix E Existence of

Appendix F Proof of Lemma 3.1

We are going to approximate the integral in Equation (7) by Riemann sum. We take and a regular grid of with mesh . We set

For , we have

Hence for any and :

which goes to when goes to infinity, uniformly on . Hence the sequence converges uniformly towards and is dominated by so converges in towards .

Set and and consider , we have for any

and in . Thus the sequence gives the result.

Appendix G Choice of an approximating sequence for Section 4.2

Consider the Mittag-Leffler density function, see [12] for details, and the Laplace transform operator we have

Moreover for any we have

where is the fractional derivative operator, see [23] for details. Hence we have

Therefore to build the we simply use Riemman sums. More precisely for any we set

where . Hence we have

Finally we rescale the to obtain equality of the norm.

Appendix H Probabilistic representation of PIDE in high dimension

We are going to use a probabilistic representation based on branching processes. This method is insensitive to the dimension of the domain of the PIDE. Theoretically the method works for any semi-linear PIDE admitting a strong solution and with a generator that can be written as a power serie. Thought this is not the case for , in order to implement this method we approximate the generator of the PIDE by a second order polynomial and assume that the approximated PIDE have a strong solution. Thus we are left with an PIDE of the form

where

The operator is defined by .

Consider a process starting at time with initial state such that and whose dynamics is driven by the infinitesimal generator . The Feynman-Kac formula gives

| (26) |

where is a positive random variable with density .

We show in Appendix H.1 that there exists an appropriate probability measure on the set

and a set of functions from such that for any random variable with law we have

| (27) |

The set is defined by

and

where (resp. ) is the jump corresponding to an ask (resp. bid) market order, namely (We recall that the price variable is no longer part of the domain).

We now define a branching process in the following way: any particle is noted by where and the ’s belong in . The variable denotes the initial position of the particle and its birth time, is the label of the particle, the label of its parent, and so on. The lifetime of the particles are i.i.d random variables with density

We now describe the evolution of the particle. Consider a particle born at time at the state with lifetime . During its lifetime the particle state is described by its position: in . The dynamics of the particle position is given by

The other components are constants. Note that this dynamics corresponds to the infinitesimal generator . When the particle dies it gave birth to independent particles. The number and type of children particles depend on the label of the particle:

-

•

if : child

-

•

if : child

-

•

if : children

-

–

if the initial state of the child particle is

-

–

if the initial state of the child particle is

-

–

The labels of the children particles are i.i.d. random variables with law . We note the set of the children particles.

Considering a particle starting at point , Equations (27) and (26) give

where denotes the initial position of the child particle and where is defined by

By iterating the above equality to the descendents of the particle and assuming that the number of descendent particles born before the time horizon is almost surely finite we can evaluate using Monte Carlo simulation. For more details on this method we refer to [13].

H.1 Existence of a measure for the particle method

We have

where is a random variable with values in , and

where is a random variable with values in and

Finally we have

with i.i.d. random variables with law . Thus finally

with is a random variable whose law is the uniform probability measure on the set and where

References

- [1] Eduardo Abi Jaber. Lifting the Heston model. Quantitative Finance, 19(12):1995–2013, 2019.

- [2] Aurélien Alfonsi and Pierre Blanc. Dynamic optimal execution in a mixed-market-impact Hawkes price model. Finance and Stochastics, 20(1):183–218, 2016.

- [3] Marco Avellaneda and Sasha Stoikov. High-frequency trading in a limit order book. Quantitative Finance, 8(3):217–224, 2008.

- [4] Emmanuel Bacry, Thibault Jaisson, and Jean-François Muzy. Estimation of slowly decreasing Hawkes kernels: application to high-frequency order book dynamics. Quantitative Finance, 16(8):1179–1201, 2016.

- [5] Álvaro Cartea, Sebastian Jaimungal, and José Penalva. Algorithmic and high-frequency trading. Cambridge University Press, 2015.

- [6] Álvaro Cartea, Sebastian Jaimungal, and Jason Ricci. Buy low, sell high: A high frequency trading perspective. SIAM Journal on Financial Mathematics, 5(1):415–444, 2014.

- [7] Michael G Crandall, Hitoshi Ishii, and Pierre-Louis Lions. User’s guide to viscosity solutions of second order partial differential equations. Bulletin of the American mathematical society, 27(1):1–67, 1992.

- [8] Khalil Dayri and Mathieu Rosenbaum. Large tick assets: implicit spread and optimal tick size. Market Microstructure and Liquidity, 1(01):1550003, 2015.

- [9] Wendell H Fleming and Halil Mete Soner. Controlled Markov processes and viscosity solutions, volume 25. Springer Science & Business Media, 2006.

- [10] Olivier Guéant. The Financial Mathematics of Market Liquidity: From optimal execution to market making, volume 33. CRC Press, 2016.

- [11] Olivier Guéant, Charles-Albert Lehalle, and Joaquin Fernandez-Tapia. Dealing with the inventory risk: a solution to the market making problem. Mathematics and financial economics, 7(4):477–507, 2013.

- [12] Hans J Haubold, Arak M Mathai, and Ram K Saxena. Mittag-Leffler functions and their applications. Journal of Applied Mathematics, 2011, 2011.

- [13] Pierre Henry-Labordere, Nadia Oudjane, Xiaolu Tan, Nizar Touzi, Xavier Warin, et al. Branching diffusion representation of semilinear PDEs and Monte Carlo approximation. In Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, volume 55, pages 184–210. Institut Henri Poincaré, 2019.

- [14] Patrick Hewlett. Clustering of order arrivals, price impact and trade path optimisation. In Workshop on Financial Modeling with Jump processes, Ecole Polytechnique, pages 6–8, 2006.

- [15] Côme Huré, Huyên Pham, Achref Bachouch, and Nicolas Langrené. Deep neural networks algorithms for stochastic control problems on finite horizon, part i: convergence analysis. arXiv preprint arXiv:1812.04300, 2018.

- [16] Jean Jacod. Multivariate point processes: predictable projection, Radon-Nikodym derivatives, representation of martingales. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 31(3):235–253, 1975.

- [17] Jean Jacod and Albert Shiryaev. Limit theorems for stochastic processes, volume 288. Springer Science & Business Media, 2013.

- [18] Thibault Jaisson, Mathieu Rosenbaum, et al. Rough fractional diffusions as scaling limits of nearly unstable heavy tailed Hawkes processes. The Annals of Applied Probability, 26(5):2860–2882, 2016.

- [19] Fabrizio Lillo and J Doyne Farmer. The long memory of the efficient market. Studies in nonlinear dynamics & econometrics, 8(3), 2004.

- [20] Ananth Madhavan, Matthew Richardson, and Mark Roomans. Why do security prices change? a transaction-level analysis of NYSE stocks. The Review of Financial Studies, 10(4):1035–1064, 1997.

- [21] Milan Merkle. Completely monotone functions: A digest. In Analytic Number Theory, Approximation Theory, and Special Functions, pages 347–364. Springer, 2014.

- [22] Philip J Reny. On the existence of pure and mixed strategy Nash equilibria in discontinuous games. Econometrica, 67(5):1029–1056, 1999.

- [23] Stefan G Samko, Anatoly A Kilbas, Oleg I Marichev, et al. Fractional integrals and derivatives, volume 1. Gordon and Breach Science Publishers, Yverdon Yverdon-les-Bains, Switzerland, 1993.

- [24] Alexander Sokol et al. Optimal Novikov-type criteria for local martingales with jumps. Electronic Communications in Probability, 18, 2013.

- [25] Nizar Touzi. Optimal stochastic control, stochastic target problems, and backward SDE, volume 29. Springer Science & Business Media, 2012.

- [26] Matthieu Wyart, Jean-Philippe Bouchaud, Julien Kockelkoren, Marc Potters, and Michele Vettorazzo. Relation between bid–ask spread, impact and volatility in order-driven markets. Quantitative finance, 8(1):41–57, 2008.

- [27] Ge Zhang Ying Chen, Zexin Wang and Chao Zhou. Optimal high frequency trading with thinned Hawkes process. Working paper.