Machine Learning on Volatile Instances

Abstract

Due to the massive size of the neural network models and training datasets used in machine learning today, it is imperative to distribute stochastic gradient descent (SGD) by splitting up tasks such as gradient evaluation across multiple worker nodes. However, running distributed SGD can be prohibitively expensive because it may require specialized computing resources such as GPUs for extended periods of time. We propose cost-effective strategies to exploit volatile cloud instances that are cheaper than standard instances, but may be interrupted by higher priority workloads. To the best of our knowledge, this work is the first to quantify how variations in the number of active worker nodes (as a result of preemption) affects SGD convergence and the time to train the model. By understanding these trade-offs between preemption probability of the instances, accuracy, and training time, we are able to derive practical strategies for configuring distributed SGD jobs on volatile instances such as Amazon EC2 spot instances and other preemptible cloud instances. Experimental results show that our strategies achieve good training performance at substantially lower cost.

Index Terms:

Machine learning, Stochastic Gradient Descent, volatile cloud instances, bidding strategiesI Introduction

Stochastic gradient descent (SGD) is the core algorithm used by most state-of-the-art machine learning (ML) problems today [1, 2, 3]. Yet as ever more complex models are trained on ever larger amounts of data, most SGD implementations have been forced to distribute the task of computing gradients across multiple “worker” nodes, thus reducing the computational burden on any single node while speeding up the model training through parallelization. Currently, even distributed training jobs require high-performance computing infrastructure such as GPUs to finish in a reasonable amount of time. However, purchasing GPUs outright is expensive and requires intensive setup and maintenance. Renting such machines as on-demand instances from services like Amazon EC2 can reduce setup costs, but may still be prohibitively expensive since distributed training jobs can take hours or even days to complete.

A common way to save money on cloud instances is to utilize volatile, or transient, instances, which have lower prices but experience interruptions [4, 5, 6]. Examples of such instances include Google Cloud Platform’s preemptible instances [5] and Azure’s low-priority virtual machines [6]; both give users access to virtual machines that can be preempted at any time, but charge a significantly lower hourly price than on-demand instances with availability guarantees. Amazon EC2’s spot instances offer a similar service, but provide users additional flexibility by dynamically changing the price charged for using spot instances. Users can then specify the maximum price they are willing to pay, and they do not receive access to the instance when the prevailing spot price exceeds their specified maximum price [7]. Volatile computing resources may also be used to train ML jobs outside of traditional cloud contexts, e.g., in datacenters that run on “stranded power.” Such datacenters only activate instances when the energy network supplying power to the datacenter has excess energy that needs to be burned off [8, 9], leading to significant temporal volatility in resource availability. SGD variants are also commonly used to train machine learning models in edge computing contexts, where resource volatility is a significant practical challenge [10, 11].

SGD algorithms can be run on volatile instances by deploying each worker on a single instance, and deploying a parameter server on an on-demand or reserved instance that is never interrupted [12]. This deployment strategy, however, has drawbacks: since the workers may be interrupted throughout the training process, they cannot update the model parameters as frequently, increasing the error of the trained model compared to deploying workers on on-demand instances. Compensating for this increased error would require either training the model for a larger number of iterations or increasing the number of provisioned workers, both of which will increase the training cost. In this paper, we quantify the performance tradeoffs between error, cost, and training time for volatile instances. We then use our analysis to propose practical strategies for optimizing these tradeoffs in realistic preemption environments. We first consider Amazon spot instances, for which users can indirectly control their preemptions by setting maximum bids, and derive the resulting optimal bidding strategies. We then derive the optimal number of iterations and workers when users cannot control their instances’ preemptions, as in GCP’s preemptible instances and Azure’s low-priority VMs. More specifically, this work makes the following contributions:

-

1.

Quantifying training error convergence with dynamic numbers of workers (Section III). Using volatile instances that can be interrupted and may rejoin later presents a new research challenge: prior analyses of distributed SGD algorithms do not consider the possibility that the number of active workers will change over time. We derive new error bounds on the convergence of SGD methods when the number of workers varies over time and show that the bound is proportional to the expected reciprocal of the number of active workers.

-

2.

Deriving optimal spot bidding strategies (Section IV). To the best of our knowledge, no works have yet explored bidding strategies for distributed machine learning jobs that consider the bidding’s effect on error convergence and random iteration runtimes. We analyze a unique three-way trade-off between the cost, error, and training time, using which we can design optimal bidding strategies to control the preemptions of spot instances. For tractability, we focus on the case where each worker submits one of two distinct bids.

-

3.

Deriving the optimal number of workers (Section V). For scenarios where users cannot control the preemption probability, we propose a general model to relate the number of provisioned workers to the expected reciprocal of the number of active workers, which can capture practical preemption distributions. Using this model, we then provide mathematical expressions to jointly optimize the number of provisioned workers and iterations. We also propose a strategy to dynamically adjust the number of provisioned workers, which can further improve the error convergence.

-

4.

Experimental validation on Amazon EC2 (Section VI). We validate our results by running distributed SGD jobs analyzing the CIFAR-10 [13] dataset on Amazon EC2. We show that our derived optimal bid prices can reduce users’ cost by 65% on real, and 62% on synthetic, spot price traces while meeting the same error and completion time requirements, compared with bidding a high price to minimize interruptions as suggested in [14]. Moreover, we implement and validate two simple but effective dynamic strategies that reduce the cost and yield a better cost/completion time/error trade-off: (i) adding workers later in the job and re-optimizing the bids according to the realized error and training time so far, and (ii) exponentially increasing the number of provisioned workers and running for a logarithmic number of iterations.

II Related Work

Our work is broadly related to prior works on algorithm analysis for distributed machine learning, as well as exploiting spot instances to efficiently run computational jobs.

Distributed machine learning generally assumes that multiple workers send local computation results to be aggregated at a central server, which then sends them updated parameter values. The SGD algorithm [1], in which workers compute the gradients of a given objective function with respect to model parameters, is particularly popular. In SGD, workers individually compute the gradient over stochastic samples (usually a mini-batch [15]) chosen from data residing at each worker in each iteration. Recent work has attempted to limit device-server communication to reduce the training time of SGD and related models [10, 16, 17, 18], while others analyze the effect of the mini-batch size [15] or learning rate [19, 20] on SGD algorithms’ training error. Bottou et al. [20] analyze the convergence of training error in SGD but do not consider the runtime per iteration. Dutta et al. [19] analyze the trade-off between the training error and the (wall-clock) training time of distributed SGD, accounting for stochastic runtimes for the gradient computations at different workers [21]. Our work is similar in spirit but focuses on spot instances, which introduces cost as another performance metric. We also go beyond [20, 19] to derive error bounds when the number of active workers changes in different iterations.

Utilizing spot and other transient cloud resources for computing jobs has been extensively studied. Zheng et al. [12] design optimal bids to minimize the cost of completing jobs with a pre-determined execution time and no deadline. Other works derive cost-aware bidding strategies that consider jobs’ deadline constraints [22] or jointly optimize the use of spot and on-demand instances [23]. However, these frameworks cannot handle distributed SGD’s dependencies between workers. Another line of work instead optimizes the markets in which users bid for spot instances. Sharma et al. [14] advocate bidding the price of an on-demand instance and migrating to VM instances in other spot markets upon interruptions. The resulting migration overhead, however, requires complex checkpointing and migration strategies due to SGD’s substantial communication dependencies between workers, realizing limited savings [24]. Some software frameworks have been designed for running big data analytics on transient instances [25], but they do not include theoretical ML performance analyses.

III Error and Runtime Analysis of Distributed SGD with Volatile Workers

The number of active computing nodes used for distributed SGD training affects the convergence of the training error versus the number of SGD iterations as well as the runtime spent per iteration. Unlike most previous works in the optimization theory literature, which focus only on error-versus-iterations convergence, we consider both these factors and analyze the true convergence of SGD with respect to the wall-clock time. Moreover, to the best of our knowledge this is the first work that presents an error and runtime analysis for volatile computing instances, which can result in a changing number of active workers during training.

We formally introduce distributed SGD in Section III-A. In Section III-B, we quantify how the preemption probability adversely affects error convergence because having fewer active workers yields more noisy gradients. In Section III-C, we analyze the effect of worker volatility on the training runtime, which is affected in two opposing ways. A higher preemption probability results in longer dead time intervals where we have zero active workers. Although a lower preemption probability yields more active workers, it can increase synchronization delays in waiting for straggling nodes. This error and runtime analysis lays the foundation for subsequent results on bidding strategies that can dynamically control the probability of preemption and the number of active worker nodes.

In Sections IV and V, we use our results on the error and runtime analysis from this section to minimize the cost of training a job, subject to constraints on the maximum allowable error and runtime. Our goal is to solve the optimization:

| Expected total cost | (1) | |||

| st.: | (2) | |||

| (3) |

where and denote the maximum allowed error and the (wall-clock) job completion time respectively.

III-A Distributed SGD Primer

Most state-of-the-art machine learning systems employ Stochastic Gradient Descent (SGD) to train a neural network model so as to minimize the empirical risk function over a training dataset , which is defined as

| (4) |

where the vector denotes the model parameters (for example, the weights and biases of a neural network model), and the loss compares our model’s prediction to the true output , for each sample .

The mini-batch stochastic gradient descent (SGD) algorithm iteratively minimizes by computing gradients of over a small, randomly chosen subset of data samples in each iteration and updating as per the update rule . Here is the (pre-specified) step size and , the gradient computed using samples in the mini-batch .

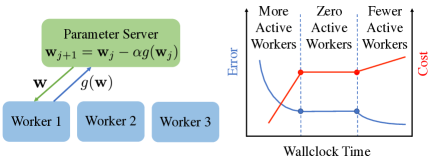

Synchronous Distributed SGD. To further speed up the training, many practical implementations parallelize gradient computation by using the parameter server framework shown in Fig. 1. In this framework, there is a central parameter server and worker nodes. Each worker has access to a subset of the data, and in each iteration each worker fetches the current parameters from the parameter server, computes the gradients of over one mini-batch of its data, and pushes them to the parameter server. The parameter server waits for gradients from all workers before updating the parameters to as per

| (5) |

where is the mini-batch gradient returned by the worker. The updated is then sent to all workers, and the process repeats. This gradient aggregation method is commonly referred to as synchronous SGD. Asynchronous gradient aggregation can reduce the delays in waiting for straggling workers, but causes staleness in the gradients returned by workers, which can give inferior SGD convergence [19]. While we focus on synchronous SGD in this paper, the insights could be extended to other distributed SGD variants.

Distributed SGD on Volatile Workers. In this work we consider that the parameter server is run on an on-demand instance, while the workers are run on volatile instances that can be interrupted or preempted during the training process, as illustrated in Fig. 1. Let denote the number of active (i.e., not preempted) workers in iteration , such that for all , where is the total number of iterations. The sequence can be considered as a random process. We do not count “iterations” where the number of active workers is , as there is then no gradient update. However, having zero workers will increase the total training runtime, which we will account for in the runtime analysis in Section III-C.

III-B SGD Error Convergence with Variable Number of Workers

Next we give an upper-bound on the expected training error in terms of for . For error convergence analysis we make the following assumptions on the objective function , which are common in most prior works on SGD convergence analysis [20, 19].

Assumption 1 (Lipschitz-smoothness).

The objective function is -Lipschitz smooth, i.e., it is continuously differentiable and there exists such that

| (6) |

Assumption 2 (First and second moments).

Let represent the expected gradient at iteration for a mini-batch of the training data. Then there exist scalars such that

| (7) |

and scalars and such that

| (8) |

for any given size of mini-batch on one worker.

Theorem 1 (SGD Error Bound).

The proof is given in the Appendix. The above convergence bound can be extended to handle non-convex objective function and a diminishing step size, where we analyze the convergence speed to a stationary point. We omit this extension for brevity.

Remark 1 (Penalty for Using Volatile Instances).

The error bound in Theorem 1 given the expected number of active workers is minimized when is not a random variable, i.e., SGD is run on on-demand instead of volatile instances. This result follows from the convexity of ; using Jensen’s inequality we can show that fixing the number of active workers to minimizes .

Remark 2 (Error and Preemption Probability).

Suppose that a worker is preempted with probability in each iteration. Then the bound in Theorem 1 increases with because increases with . Thus, more frequent preemption or interruption of workers reduces the effective number of active workers and yields worse error convergence.

III-C SGD Runtime Analysis with Volatile Workers

Now let us analyze how using volatile workers affects the training runtime. The runtime has two components: 1) the time required to complete the SGD iterations, and 2) the idle time when no workers are active and thus no iterations can be run.

Let denote the runtime of the iteration in which we have the set of active workers. Suppose each worker takes time to compute its gradient, where is a random variable. Fluctuations in computation time are common especially in cloud infrastructure due to background processes, node outages, network delays etc. [27]. Since the parameter server has to wait for all workers to finish their gradient computations, the runtime per iteration is,

| (10) |

where is the time taken by the parameter server to update and push it to the workers. The expected runtime increases with the number of active workers. For example, if , an exponential random variable that is i.i.d. across workers and mini-batches, then . Adding this per-iteration runtime to the idle time when no workers are active, we can show that the expected time required to complete SGD iterations is

For example, when each worker is preempted uniformly at random with probability in each iteration (as described in Remark 2), then the expected completion time becomes .

IV Optimizing Spot Instance Bids

In this section, we use the results of Section III to derive the bid prices and number of iterations that minimize the cost of running distributed SGD with workers placed on spot instances. We first consider the simple case in which we submit the same bid for each worker in Section IV-A and then consider the heterogeneous bid case in Section IV-B.

Spot Price and Bidding Model. Let denote the spot price of each instance at time . We assume is i.i.d. and is bounded between a lower-bound and an upper-bound , similar to prior works on optimal bidding in spot markets [12]. Let and denote the probability density function (PDF) [28] and the cumulative density function (CDF) [29] of the random variable . When a bid is placed for an instance, we consider that the provider assigns available spot capacity to users in descending order of their bids, stopping at users with bids below the prevailing spot price. Thus, a worker is active only if its bid price exceeds the current spot price. Hence, without loss of generality the range of the bid price can also be assumed to be . Whenever a worker is active (), the per-time cost incurred for running it is equal to the prevailing spot price (not the bid price).

IV-A Identical Worker Bids

Suppose we choose bid price for each of the workers. We first simplify the error and runtime in Section III for this case, and then solve the cost minimization problem (1)-(3).

Observe that the workers are either all available or all interrupted depending on the bid price . This insight implies that , and thus that the error bound in Theorem 1 is independent of the bid : this bid affects only the frequency with which iterations are executed, not the number of active workers in an iteration. We can thus rewrite the error bound as a function of , the number of iterations required to reach error . Formally, we set to be the right-hand side of (1) and , where is the number of iterations required to ensure that the expected error is no larger than .

We further observe that, the number of active workers always equals when the job is running. Thus, the expected runtime per iteration can be rewritten as . Accounting for the idle time we can show that the expected completion time is monotonic with :

Lemma 1 (Completion Time in Terms of Bid Price).

Using the same bid price for all workers, the expected completion time to complete iterations of synchronous SGD is

| (11) |

which increases with and is non-increasing in the bid price . The function is the CDF of the spot price.

We can further show the expected cost (defined in (1)) is monotonically non-decreasing with and .

Lemma 2 (Cost in Terms of Bid Price).

Using one bid price for all workers, the expected cost of finishing a synchronous SGD job is given by

| (12) |

which is non-decreasing in the bid price and . The function is the CDF of the spot price.

Since both and increase with , we should set to be equal to in order to reach the target error in minimum time and cost of the volatile workers.

Optimizing the Bid Price. Having shown that , we now find the optimal bid that minimizes the expected cost (12) to solve the optimization problem (1)–(3).

According to Amazon’s policy [4], is determined upon the job submission without knowing the future spot prices and will be fixed for the job’s lifetime. Although the user can effectively change the bid price by terminating the original request and re-bidding for a new VM, doing so induces significant migration overhead. Thus, we assume that users employ persistent spot requests: a worker with a persistent request will be resumed once the spot price falls below its bid price, exiting the system once its job completes. Using Lemma 1 and Lemma 2, we can show the following theorem for the optimal bid price .

Theorem 2 (Optimal Uniform Bid).

When we make an identical bid for workers and use them to perform distributed synchronous SGD to reach error within time , the optimal bid price that minimizes the cost is .

Theorem 2 provides a general form of the optimal bid price, given the number of workers per iteration, , the deadline , and the target error bound , for any distributions of the spot price and training runtime per iteration.

IV-B Optimal Heterogeneous Bids

We next extend our results from Section IV-A to find the optimal bidding strategy with two distinct bid prices and for two groups of workers. This strategy is motivated by the observation that bidding lower prices for some workers yields a larger number of active workers when the spot price is relatively low, which improves the training error but will not cost much. Formally, we place bids of for workers and () for workers . We define the random variable as the number of active workers when the bid prices are . Note that the times when workers are active are not considered into an SGD ‘iteration’. Thus, can only be either (with probability ) or (with probability ) in each iteration.

Optimized Bids. We initially assume that , the number of workers in the first group, and , the required number of iterations, are fixed; thus, we optimize the trade-off between the expected cost, expected completion time, and the expected training error using only the bid prices . After deriving the closed-form optimal solutions of and in Theorem 3, we discuss co-optimizing and with the bids . The expected cost minimization problem (1)–(3) then becomes:

| (13) | ||||

| subject to: | (14) | |||

| (15) | ||||

| (16) |

To derive the cost and completion time expressions in (13) and (15), we express the expected runtime of iteration as , a function of the bids and price; depends on and thus is re-written as . For simplicity, we assume that the spot prices do not change within each iteration. In practice, the spot price changes at most once per hour [30], compared to a runtime of several minutes per iteration, and thus this assumption usually holds. Note that we did not need this assumption for the identical bid case in Section IV-A since all workers become active/inactive at the same time.

To derive the optimal bid prices, we first relate the distribution of the spot price and our bid prices to the training error through the number of active workers, i.e., . From Theorem 1, the expected error is at most if satisfies:

| (17) |

Further, we simplify to be a function of the number of active workers: is the expected runtime per iteration given workers are active. We then provide closed-form expressions for the optimal bid prices through Theorem 3.

Theorem 3 (Optimal-Two Bids with a Fixed ).

Suppose the objective function satisfies Assumptions 1–2. Given a number of iterations () that can guarantee ( is defined as the right-hand side of (17)), a fixed step size , and a feasible deadline (), we have the optimal bid prices and :

| (18) |

for any i.i.d. spot price and any i.i.d. running time per mini-batch, i.e., and (or ) do not change during the training process.

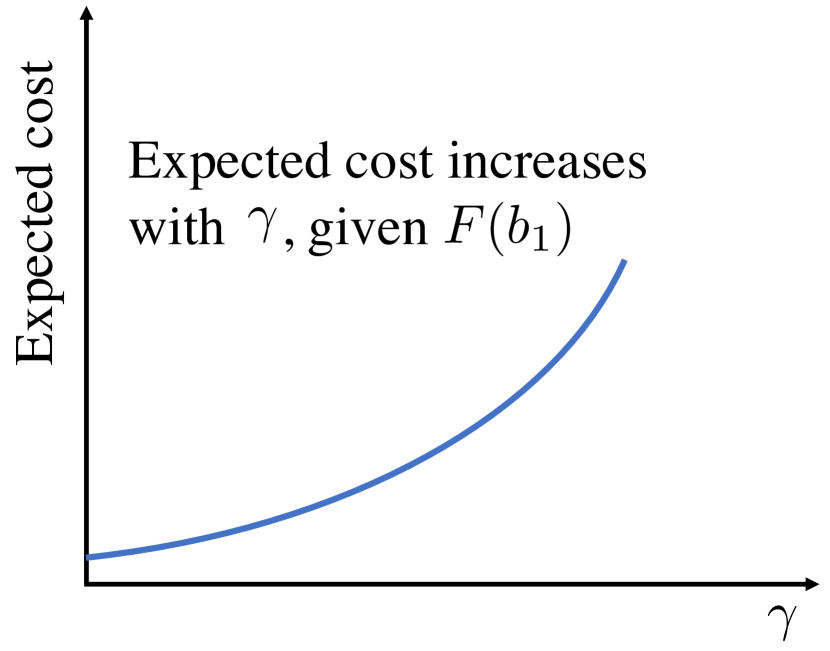

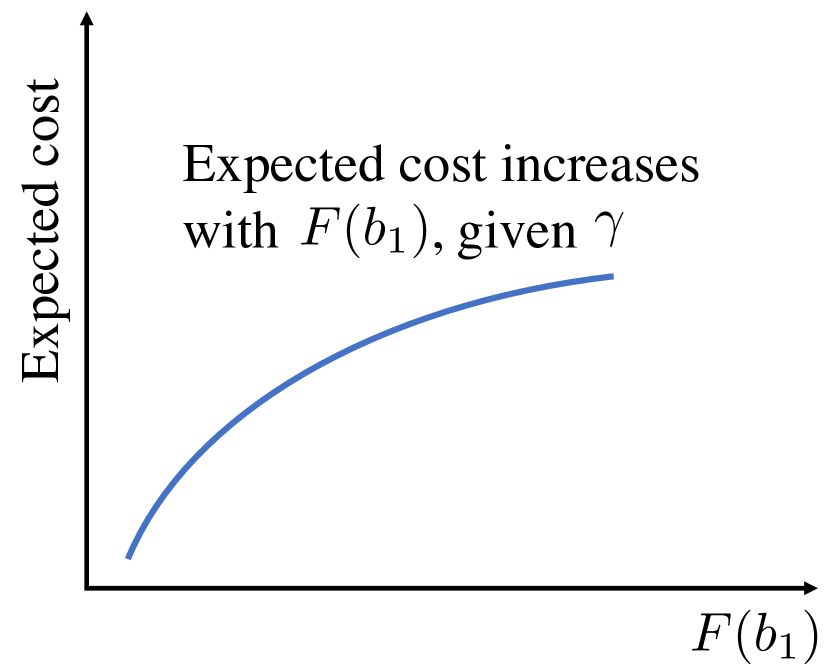

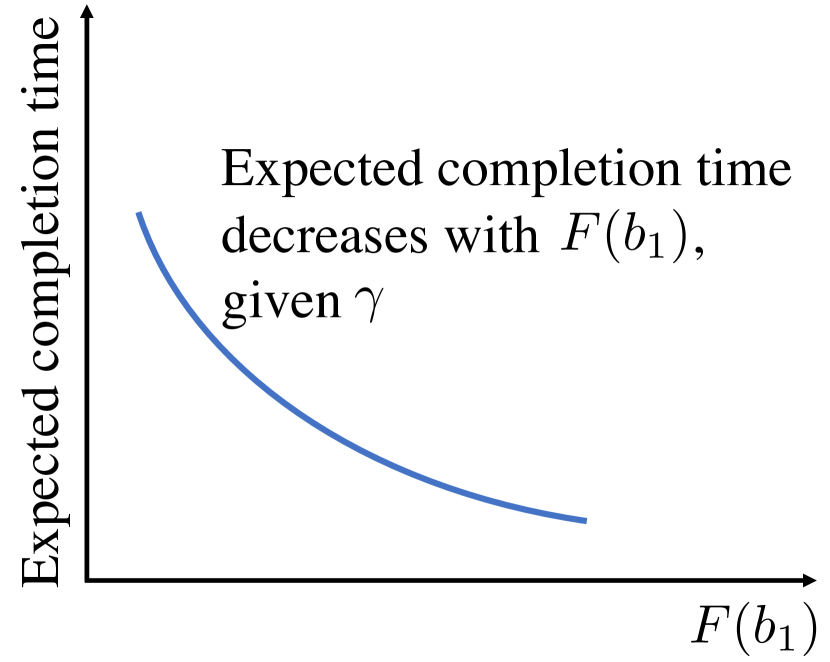

For brevity, we use Figure 2 to illustrate our proof of Theorem 3. The key steps are: (i) change the variables of the optimization problem (13) to be and ; (ii) show that the expected cost, completion time, and error are monotonic w.r.t. to and . Intuitively, the expected error should depend only on the number of active workers given that some workers are active, which is controlled by the relative difference between and : . Formally, the error bound decreases with . Applying to (17) gives us the optimal , since the expected cost increases with both and . We then choose to the one that yields (tight (15)). Intuitively, should be high enough to guarantee that some workers are active often enough that the job completes before the deadline.

Co-optimizing and . If is not a known input but a variable to be co-optimized with , we can write and in terms of according to (18) and plug them into (13)-(16) to solve for first, and then derive and the optimal .

Co-optimizing and . Taking as an optimization variable may allow us to further reduce the job’s cost. For instance, allowing the job to run for more iterations, i.e., increasing , increases (the right-hand side of (17)). We can then increase by submitting lower bids , making it less likely that workers will be active, while still satisfying (17). A lower may decrease the expected cost by making workers less expensive, though this may be offset by the increased number of iterations. To co-optimize , we show it is a function of and :

Corollary 1 (Relationship of and ).

To guarantee a training error , the number of iterations should be at least

| (19) |

V Optimal Number of Preemptible Instances

In this section, we consider preemptible instances offered by other cloud platforms, e.g., low priority VMs from Microsoft Azure [6] and preemptible instances from Google Cloud Platform [5]. Unlike spot instances where users can specify the maximum prices they are willing to pay, on these platforms users can only decide the number of provisioned instances to request in each iteration, as well as the number of iterations. Therefore, in this section, we choose to optimize the number of instances (workers) and assume the instance price is stable during the entire training time [5]. To better quantify the relationship between the number of active workers and the number of provisioned workers , we consider the two preemption distributions in Lemma 3. We will make use of the fact that for both distributions, there exists a parameter such that . The problem of minimizing the job cost is then equivalent to minimizing , subject to the completion time and error constraints.

Lemma 3 (Example Distributions of ).

If the number of active workers follows a uniform distribution , we have ; if each worker is preempted with probability each iteration, we have , where there exists a .

We find closed-form solutions for the optimal number of workers and iterations when in Theorem 4. Theorem 5 provides an optimization strategy for any .

Theorem 4 (Co-optimizing and ).

Suppose and , the probability of no active workers does not depend on , and the runtime per iteration is deterministic. Then the completion time constraint (3) is simply where is a constant, and the optimal and (denoted by and ) satisfy:

where , , and .

A Strategy with Dynamic Numbers of Workers. While Theorem 4 gives us the exact optimal expression for when the provisioned number of workers is fixed over iterations, ML practitioners often increase the number of workers over time [31, 32, 33]. Intuitively, in the later stages of the model training the parameter values are closer to convergence, and thus it is crucial that the gradient updates are accurate, i.e., averaged over a larger number of worker mini-batches. More formally, we observe in Theorem 1 that ’s contribution to the error bound increases exponentially with by .

Inspired by these observations, we propose to decrease over iterations by controlling the provisioned number of workers: we dynamically set the number of workers to be for each iteration and some ; we show how to optimize the value of below. One can similarly exponentially increase the batch size of each worker while using the same number of workers over iterations [34], but doing so will exponentially increase the runtime of each iteration. We prove in Theorem 5 that our dynamic strategy achieves the same error convergence rate and a better asymptotic error bound with a significantly smaller number of iterations than using a static number of workers during the entire training.

Theorem 5 (Error with Dynamic Workers).

Suppose the number of active workers satisfies for some . Then for any and sufficiently large, provisioning workers in iteration and running SGD for iterations achieves an error bound no larger than provisioning workers for iterations.

In the proof of Theorem 5, we also show that our dynamic strategy achieves an error bound that converges to asymptotically with , while when using a static number of workers the error bound in Theorem 1 converges to a positive constant.

We then optimize to minimize the expected cost, subject to the error and completion time constraints. If we ignore straggler effects, we can define . Suppose denotes the number of active workers including the case , and follows a binomial distribution with parameter and probability (the probability that each instance is inactive), namely, the probability that equals . Assuming and , our cost minimization problem can be modified as follows.

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) |

where , , and . For any given , both the objective function and constraints are convex functions of (refer to the operations that preserve convexity in [26]). Therefore, we can use standard algorithms for convex optimization to solve for the optimal .

We can capture the effect of straggling workers by replacing the constant per-iteration runtime in (3) with in the completion time constraint (3). This constraint accounts for the fact that as we have more active workers in each iteration, the per-iteration runtime will likely increase because we need to wait for the slowest worker to finish. As in the case without stragglers, we then observe that our optimization problem is convex in for each fixed , and moreover that there exists a finite maximum number of iterations for which (3) is feasible. Thus, we can jointly optimize the optimal rate of increase in the number of workers, , and by iterating over all possible values of .

VI Experimental Validation

We evaluate our bidding strategies from Section IV on the CIFAR-10 image classification benchmark dataset, using iterations on ResNet-50 [35] and on a small Convolutional Neural Network (CNN) [36] with two convolutional layers and three fully connected layers; the distributed SGD algorithms under both datasets are implemented based on Ray [37] and Tensorflow [38]. We run the former experiments on a local cluster with GPU servers and the latter on Amazon EC2’s c5.xlarge spot instances.

Choosing the Experiment Parameters. We set the deadline () to be twice the estimated runtime of using workers to process iterations without interruptions. We estimate that for our choices of and ( for ResNet-50 and for the small CNN), demonstrating the robustness of our optimized strategies to mis-estimations. To estimate the probability distribution of the spot prices, we first consider two synthetic spot price distributions for the ResNet-50 experiments: a uniform distribution in the range and a Gaussian distribution with mean and variance equal to and ; we draw the spot price when each iteration starts and re-draw it every seconds after the job is interrupted. We then download the historical price traces of c5.xlarge spot instances using Amazon EC2’s DescribeSpotPriceHistory API for the small CNN experiments, demonstrating that our bidding strategy is robust to non-i.i.d spot prices.

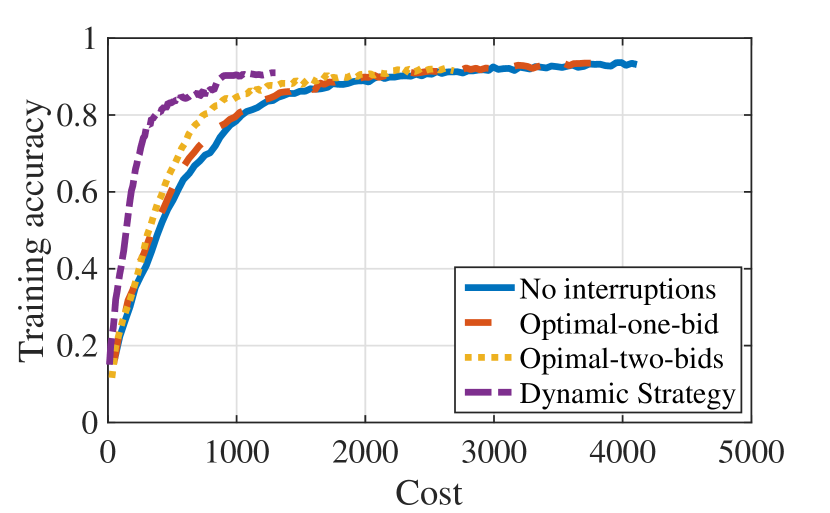

Superiority of our Bidding Strategies. We evaluate the bidding strategies with both the optimal single bid price for all workers (Optimal-one-bid) and the optimal bid prices for two groups of workers derived in Theorem 3 (Optimal-two-bids) against an aggressive No-interruptions strategy that chooses a bid price larger than the maximum spot price. To further minimize the expected total cost while guaranteeing a low training/test error, we propose a Dynamic strategy, which updates the optimal two bid prices when increasing the total number of workers. More specifically, we initially launch four workers (, ) and apply our optimal two bid prices. After completing 4000 iterations, we add four more workers () and re-compute the optimal bids by subtracting the consumed time from the original deadline and taking to be the number of remaining iterations. One could further divide the training and re-optimization into more stages. Frequent re-optimizing will likely incur significant interruption overheads, but infrequent optimization may reduce the cost with tolerable overhead.

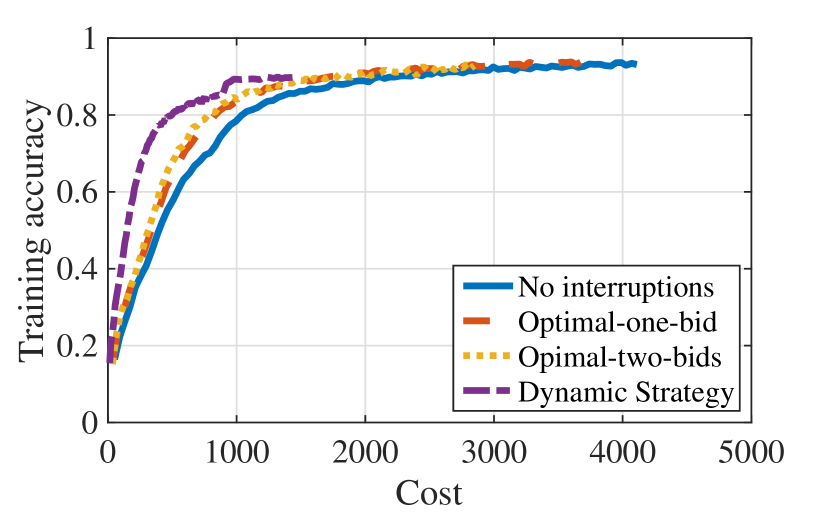

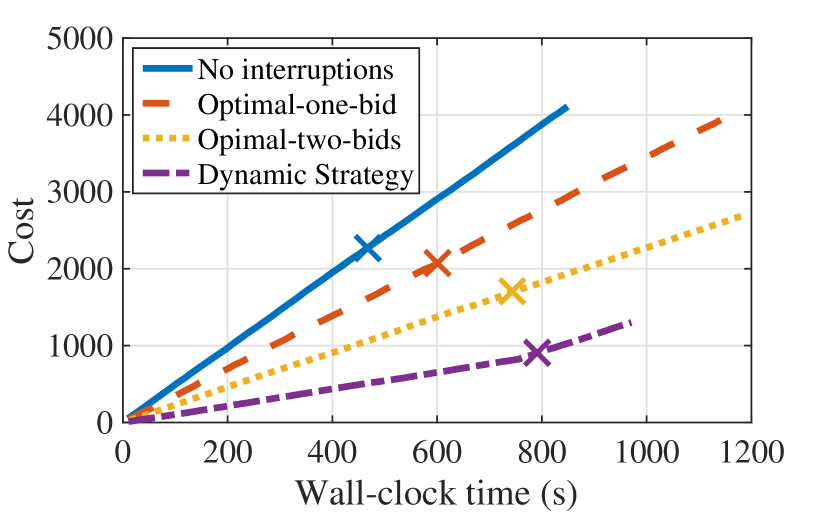

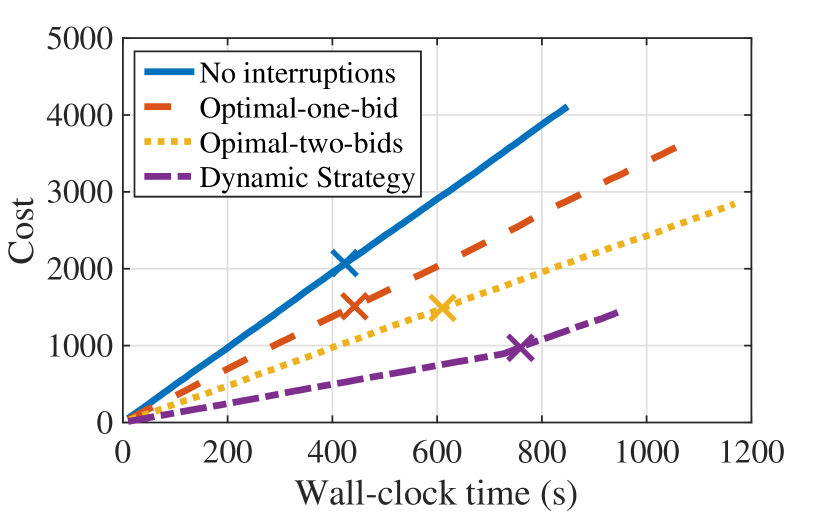

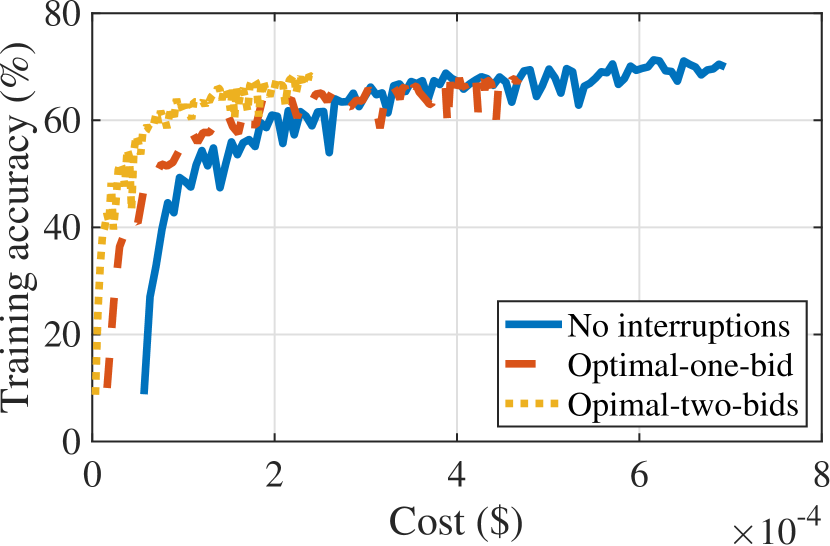

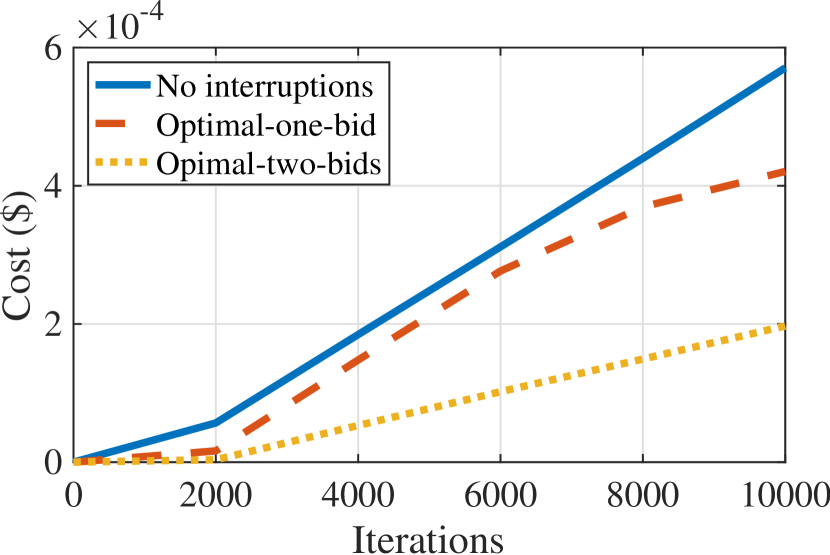

Figures 3 and 4 compare the performance of our strategies on synthetic and real spot prices, respectively. Figures 3(a) and 3(b) show that our dynamic strategy leads to a lower cost and the no interruptions benchmark to a higher cost for any given accuracy, compared to the optimal-one-bid and optimal-two-bids strategies. In Figures 3(c) and 3(d), we indicate the cumulative cost as we run the jobs. The markers indicate the costs where we achieve 98% accuracy; while the no interruptions benchmark achieves this accuracy much faster, it costs nearly three times as much as our dynamic strategy and twice as much as our optimal-two-bids strategy. Figures 4(a) and 4(b) show that our optimal-one-bid and optimal-two-bids strategies can significantly save cost under the real spot prices while achieving almost the same training accuracy as the no interruptions benchmark.

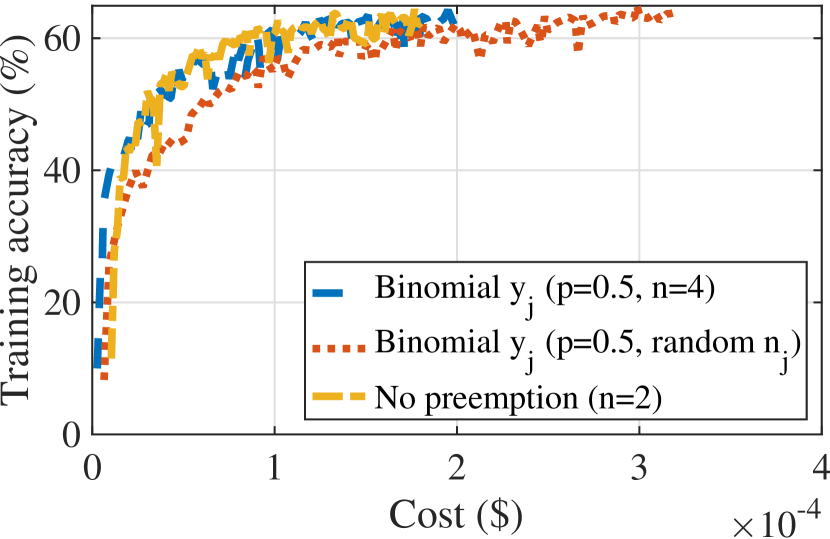

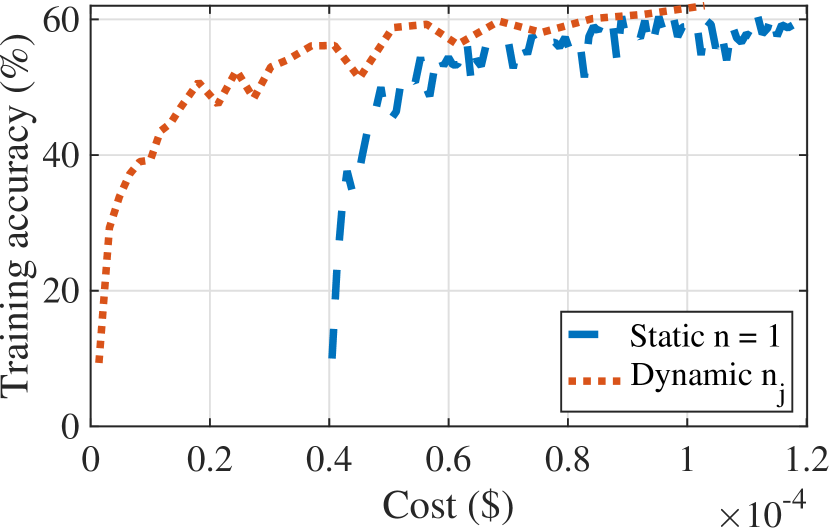

Superiority of Our Choices of the Number of Workers. To verify our results in Section V, we simulate No preemption by running 2 workers for 10000 iterations without preemption and observe that the final accuracy can approach . We then suppose instances are preempted with probability and provision workers for iterations, using the fact that the optimal for each fixed is proportional to and aiming to achieve the same accuracy . Co-optimizing and (Theorem 4) may yield further cost improvements. Figure 5(a) shows that using our estimated achieves a better accuracy per dollar than randomly choosing . We further show in Figure 5(b) that our strategy Dynamic , which exponentially increases by a fixed rate and runs for a much smaller number of iterations set according to Theorem 5, achieves a better accuracy per dollar, compared with using 1 worker for iterations (Static ).

VII Discussion and Conclusion

In this work, we consider the use of volatile workers that run distributed SGD algorithms to train machine learning models. We first focus on Amazon EC2 spot instances, which allow users to reduce job cost at the expense of a longer training time to achieve the same model accuracy. Spot instances allow users to choose how much they are willing to pay for computing resources, thus allowing them to control the trade off between a higher cost and a longer completion time or higher training error. We quantify these tradeoffs and derive new bounds on the training error when using time-variant numbers of workers. We finally use these results to derive optimized bidding strategies for users on spot instances and propose practical strategies for scenarios without controlling the preemption of the instances by submitting bids. We validate these strategies by comparing them to heuristics when training neural network models on the CIFAR-10 image dataset.

Our proposed strategies are an initial step towards a more comprehensive set of methods that allow distributed ML algorithms to exploit the benefits of volatile instances. As a simple extension, one might adapt the bids over time as we obtain better estimates of the iteration running time. Our bidding strategies might also be generalized to allow different bids for each worker. Even more generally, one can envision dividing a resource budget across workers, with the budget controlling each worker’s availability. This budget might be a monetary budget when workers are run on cloud instances, but if the workers are instead run on mobile devices, it might instead represent a power budget that controls how often these devices can afford to process data.

VIII Acknowledgments

This work was supported by NSF grants CNS-1751075, CNS-1909306, CCF-1850029, and a 2018 IBM Faculty Research Award. We also thank Fangjing Wu for her assistance.

Proof of Theorem 1.

is at most:

| (24) |

due to Assumption 1. Combining (5), Assumption 2, and (24),

| (25) | |||

| (26) |

where (26) follows from our choice of . If is -strong convex with , then it satisfies the Polyak-Lojasiewicz condition (Appendix B of [39]). Substituting this into (26) and subtracting on both sides, we have:

Applying the above inequality recursively over all iterations leads to (1), and the theorem follows. ∎

Proof of Lemma 2.

The objective function (1) takes the sum of price multipled by the runtime over all iterations with at least one active worker. Therefore, we have , which equals and thus . The lemma follows as . ∎

Proof of Theorem 2.

Note that is non-increasing with , the optimal number of iterations equals , and the expected cost in non-decreasing with , the optimal bid price has . Setting the right-hand side of (11) to be equal to and taking , we can conclude that the optimal should be equal to . ∎

Proof of Theorem 4.

Given that is i.i.d. across all iterations with , it suffices to minimize subject to . Suppose the is a feasible solution that is not least integer that makes the error constraint tight, i.e., satisfying , there exists a feasible solution such that the objective value is strictly smaller than , a contradiction. Therefore, we can replace the objective function by . Letting its derivative to be zero leads to where can be fractional. One can verify that monotonically decreases with and the objective function is smooth. Thus, should be among: the least integer no smaller than , the largest integer no larger than , and , whichever that yields the smallest objective value, the theorem follows. ∎

Proof of Theorem 5.

Based on our Theorem 1, the error bound of using workers in iteration and running the SGD for iterations is at most:

| (27) |

where we define and is a constant linear with . Given our choice of , the error bound will exponentially decrease with . In comparison, if using workers for iterations, the error is at most:

| (28) |

Based on (VIII), (28), and our choice of , the error decay rate is no smaller than in the dynamic strategy (bound (VIII)) and equals in the static strategy. Moreover, when , the error bound of the dynamic strategy approaches , where , while that of the static strategy (28) approaches . Putting into the former, it becomes which is smaller than (error bound of the static strategy) when is sufficiently large due to , the theorem follows. ∎

References

- [1] H. Robbins and S. Monro, “A stochastic approximation method,” The Annals of Mathematical Statistics, vol. 22, no. 3, pp. 400–407, 1951.

- [2] L. Bottou, “Large-scale machine learning with stochastic gradient descent,” in Proceedings of COMPSTAT, 2010.

- [3] J. D. et al., “Large scale distributed deep networks,” in International Conference on Neural Information Processing Systems (NIPS), vol. 1, 2012, pp. 1223–1231.

- [4] Amazon EC2, “Amazon ec2 spot instances,” https://aws.amazon.com/ec2/spot/, 2019.

- [5] Google Cloud Platform, “Preemptible virtual machines,” https://cloud.google.com/preemptible-vms/, 2019.

- [6] Microsoft Azure, “Announcing low-priority vms on scale sets now in public preview,” https://azure.microsoft.com/en-us/blog/low-priority-scale-sets/, 2018.

- [7] Amazon EC2, “Spot price overrides,” https://docs.aws.amazon.com/AWSEC2/latest/UserGuide/spot-fleet.html#spot-price-overrides, 2019.

- [8] F. Yang and A. A. Chien, “Zccloud: Exploring wasted green power for high-performance computing,” in 2016 IEEE International Parallel and Distributed Processing Symposium (IPDPS). IEEE, 2016, pp. 1051–1060.

- [9] A. A. Chien, F. Yang, and C. Zhang, “Characterizing curtailed and uneconomic renewable power in the mid-continent independent system operator,” arXiv preprint arXiv:1702.05403, 2016.

- [10] J. Konečnỳ, H. B. McMahan, F. X. Yu, P. Richtárik, A. T. Suresh, and D. Bacon, “Federated learning: Strategies for improving communication efficiency,” arXiv preprint arXiv:1610.05492, 2016.

- [11] Z. Tao and Q. Li, “esgd: Communication efficient distributed deep learning on the edge,” in USENIX Workshop on Hot Topics in Edge Computing (HotEdge 18), 2018.

- [12] L. Zheng, C. Joe-Wong, C. W. Tan, M. Chiang, and X. Wang, “How to bid the cloud,” in Proc. ACM SIGCOMM, 2015.

- [13] A. Krizhevsky, V. Nair, and G. Hinton, “The cifar-10 dataset,” https://www.cs.toronto.edu/~kriz/cifar.html.

- [14] P. Sharma, D. Irwin, and P. Shenoy, “How not to bid the cloud,” in Proc. USENIX Conference on Hot Topics in Cloud Computing (HotCloud), 2016.

- [15] O. S. Ofer Dekel, Ran Gilad-Bachrach and L. Xiao., “Optimal distributed online prediction using mini-batches.” Journal of Machine Learning Research, vol. 13, no. 1, pp. 165–202, 2012.

- [16] O. Shamir, N. Srebro, and T. Zhang, “Communication-efficient distributed optimization using an approximate newton-type method,” in International conference on machine learning, 2014, pp. 1000–1008.

- [17] M. Kamp, L. Adilova, J. Sicking, F. Hüger, P. Schlicht, T. Wirtz, and S. Wrobel, “Efficient decentralized deep learning by dynamic model averaging,” arXiv preprint arXiv:1807.03210, 2018.

- [18] H. B. McMahan, E. Moore, D. Ramage, S. Hampson, and B. A. y Arcas, “Communication-efficient learning of deep networks from decentralized data,” in Proceedings of AISTATS, 2017. [Online]. Available: http://arxiv.org/abs/1602.05629

- [19] S. Dutta, G. Joshi, S. Ghosh, P. Dube, and P. Nagpurkar, “Slow and stale gradients can win the race: Error-runtime trade-offs in distributed sgd,” in Proceedings of AISTATS, 2018.

- [20] L. Bottou, F. E. Curtis, and J. Nocedal, “Optimization methods for large-scale machine learning,” SIAM Review, vol. 60, no. 2, pp. 223–311, 2018.

- [21] D. Wang, G. Joshi, and G. W. Wornell, “Efficient straggler replication in large-scale parallel computing,” ACM Trans. Model. Perform. Eval. Comput. Syst., vol. 4, no. 2, Apr. 2019. [Online]. Available: https://doi.org/10.1145/3310336

- [22] M. Zafer, Y. Song, and K.-W. Lee, “Optimal bids for spot vms in a cloud for deadline constrained jobs,” in Proc. of IEEE CLOUD, 2012.

- [23] A. Harlap, A. Tumanov, A. Chung, G. R. Ganger, and P. B. Gibbons, “Proteus: Agile ml elasticity through tiered reliability in dynamic resource markets,” in Proc. of European Conference on Computer Systems, 2017.

- [24] K. Lee and M. Son, “Deepspotcloud: leveraging cross-region gpu spot instances for deep learning,” in Proceedings of IEEE CLOUD. IEEE, 2017, pp. 98–105.

- [25] Y. Yan, Y. Gao, Y. Chen, Z. Guo, B. Chen, and T. Moscibroda, “Tr-spark: Transient computing for big data analytics,” in Proceedings of the Seventh ACM Symposium on Cloud Computing. ACM, 2016, pp. 484–496.

- [26] S. Boyd and L. Vandenberghe, “Convex optimization,” Cambridge university press, 2014.

- [27] J. Dean and L. A. Barroso, “The tail at scale,” Communications of the ACM, vol. 56, no. 2, pp. 74–80, 2013.

- [28] “Probability density function.” [Online]. Available: https://en.wikipedia.org/wiki/Probability_density_function

- [29] “Cumulative distribution function.” [Online]. Available: https://en.wikipedia.org/wiki/Cumulative_distribution_function

- [30] “How spot instances work,” https://docs.aws.amazon.com/aws-technical-content/latest/cost-optimization-leveraging-ec2-spot-instances/how-spot-instances-work.html.

- [31] J. Wang and G. Joshi, “Adaptive communication strategies to achieve the best error-runtime trade-off in local-update SGD,” in Proc. of SysML Conference, 2019. [Online]. Available: "https://arxiv.org/pdf/1810.08313.pdf"

- [32] H. Yun, H.-F. Yu, C.-J. Hsieh, S. V. N. Vishwanathan, and I. Dhillon, “Nomad: Non-locking, stochastic multi-machine algorithm for asynchronous and decentralized matrix completion,” in Proc. of VLDB Endowment, 2014.

- [33] J. Chen, X. Pan, R. Monga, and S. Bengio, “Revisiting distributed synchronous sgd,” in Proc. of ICLR Workshop Track, 2016.

- [34] H. Yu and R. Jin, “On the computation and communication complexity of parallel sgd with dynamic batch sizes for stochastic non-convex optimization,” in Proc. of ICML, 2019.

- [35] K. He, X. Zhang, S. Ren, and J. Sun, “Deep residual learning for image recognition,” 2015. [Online]. Available: https://arxiv.org/abs/1512.03385

- [36] G. E. H. Alex Krizhevsky, IIya Sutskever, “Imagenet classification with deep convolutional neural networks,” in Proceedings of NIPS, 2012.

- [37] P. Moritz, R. Nishihara, S. Wang, A. Tumanov, R. Liaw, E. Liang, M. Elibol, Z. Yang, W. Paul, M. I. Jordan, and I. Stoica, “Ray: A distributed framework for emerging ai applications,” in In Proceedings of USENIX OSDI, 2018.

- [38] M. Abadi, P. Barham, J. Chen, Z. Chen, A. Davis, J. Dean, M. Devin, S. Ghemawat, G. Irving, M. Isard, M. Kudlur, J. Levenberg, R. Monga, S. Moore, D. G. Murray, B. Steiner, P. Tucker, V. Vasudevan, P. Warden, M. Wicke, Y. Yu, , and X. Zheng., “Tensorflow: A system for large-scale machine learning.” in In Proceedings of USENIX OSDI, 2016.

- [39] H. Karimi, J. Nutini, and M. Schmidt, “Linear convergence of gradient and proximal-gradient methods under the polyak-Łojasiewicz condition,” in Proc. of ECML PKDD, 2016.

- [40] M. T. Chao and W. E. Strawderman, “Negative moments of positive random variables,” Journal of the American Statistical Association, vol. 67, no. 338, pp. 429–431, 1972.