A mixture autoregressive model based on Gaussian and Student’s t-distributions

Savi Virolainen

University of Helsinki

We introduce a new mixture autoregressive model which combines Gaussian and Student’s mixture components. The model has very attractive properties analogous to the Gaussian and Student’s mixture autoregressive models, but it is more flexible as it enables to model series which consist of both conditionally homoscedastic Gaussian regimes and conditionally heteroscedastic Student’s regimes. The usefulness of our model is demonstrated in an empirical application to the monthly U.S. interest rate spread between the 3-month Treasury bill rate and the effective federal funds rate.

Keywords: nonlinear autoregression, mixture model, regime switching, interest rate spread

1 Introduction

Recently, Kalliovirta et al., (2015) introduced a mixture autoregressive model based on Gaussian distribution with very attractive features. The Gaussian mixture autoregressive (GMAR) model has linear Gaussian autoregressions as its component models and mixing weights that, for a th order model, depend on the full distribution of the past observations. The specific formulation of the mixing weights leads to ergodicity and full knowledge of the stationary distribution of consecutive observations. Moreover, it allows regime switches to depend on the level, variability, and temporal dependence of the past observations.

Meitz et al., 2018a proposed a mixture autoregressive model closely related to the GMAR model but based on Student’s -distribution. The Student’s mixture autoregressive (StMAR) model has linear Student’s autoregressions as its component models and mixing weights constructed analogously to the GMAR model, leading to similar theoretical and practical properties. The linear Student’s autoregressions have the same form for the conditional mean as the Gaussian autoregressions (a linear function of the past observations) but different conditional variance. In particular, the conditional variances of the Student’s autoregressions depend on quadratic forms of past observations, whereas in the Gaussian case the conditional variances of the component models are constants. Utilization of the -distribution does hence not only allow the StMAR model to account for larger kurtosis than the GMAR model but also stronger forms of conditional heteroskedasticity.

In this paper, we propose a generalization of the GMAR and StMAR models. The G-StMAR model accommodates both Gaussian autoregressions and Student’s autoregressions as its component models, and its mixing weights are constructed analogously to the GMAR and StMAR models, leading to similar attractive features. It thus enables to model series which consist of regimes with time varying conditional variance and excess kurtosis as well as regimes with constant conditional variance and zero excess kurtosis. It turns out that the G-StMAR model is a limiting case of a StMAR model with the -distributions of some regimes tending to normal distributions as the degrees of freedom parameters tend to infinity. As opposed to the limiting StMAR model, the advantage of the G-StMAR model is that it removes the redundant degrees of freedom parameters from the model and is free from numerical problems induced by weak identification of very large degrees of freedom parameters.

We demonstrate the usefulness of the G-StMAR model in an empirical application to the monthly U.S. interest rate spread between the 3-month Treasury bill (TB) rate and the effective federal funds (FF) rate. Our G-StMAR model identifies three regimes for the spread, with a GMAR type regime mainly appearing after the financial crisis in 2008 when the zero lower bound limits movements of the spread. The remaining regimes are of the StMAR type, one accommodating eras of low mean and high variability and the other high mean and moderate variability. The former StMAR type regime dominates often when the market possibly anticipates decreases in the FF rate or has increased preference for safety, whereas the latter one mostly prevails when the Fed is arguably not expected to significantly decrease the FF rate target. Our findings are consistent with Sarno and Thornton, (2003) who found that the FF rate seems to adjust to the TB rate, supporting the hypothesis that the market anticipates movements of the FF rate, moving the TB rate, and hence the spread, in advance.

The rest of this article is organized as follows. Section 2 first introduces the component processes of the G-StMAR model and then proceeds to define the G-StMAR model and discusses its theoretical properties. Section 3 discusses maximum likelihood (ML) estimation of the model parameters and establishes the asymptotic properties of the ML estimator. It is, in particular, discussed how the accompanying R package ”uGMAR” (Virolainen,, 2020) estimates the model parameters in practice with a two-phase procedure. Section 4 describes a simple model selection procedure and discusses numerical consequences of very large degrees of freedom parameter estimates. Section 5 presents the empirical application to the interest rate spread and Section 6 concludes. Details of the estimation procedure employed by uGMAR, as well as proofs for the stated theorems are given in an Appendix.

Throughout this paper, we use the following notation. We write for the column vector where the components may be either scalars or (column) vectors. The notation signifies that the random vector has a -dimensional Gaussian distribution with mean and (positive definite) covariance matrix . Similarly, signifies that has a -dimensional -distribution with mean , (positive definite) covariance matrix , and degrees of freedom (assumed to satisfy ). The density functions and some properties of the multivariate Gaussian and Student’s -distributions are given in an Appendix. The vectorization operator stacks columns of a matrix on top of each other and, is the dimensional vector , signifies the identity matrix of dimension , and denotes the Kronecker product. Moreover, and denote dimensional vectors of ones and zeros, respectively.

2 Models

We consider mixture autoregressive models in which each observation is generated by a mixture component that is randomly selected according to the probabilities pointed by the mixing weights. The mixture components are either (linear) conditionally homoscedastic Gaussian autoregressions as in the GMAR model (Kalliovirta et al.,, 2015) or conditionally heteroscedastic Student’s autoregressions as in the StMAR model (Meitz et al., 2018a, ). The mixing weights are functions of the past observations constructed in a way that, for a th order model, leads to ergodicity and full knowledge of the stationary distribution consecutive observations. Moreover, as the mixing weights depend on the full distribution of the past observations, they allow regime switches to depend on the level, variability, and temporal dependence of the past observations. In this section, we first introduce the component processes of the G-StMAR model and then proceed define of the G-StMAR model and discuss its properties.

2.1 Linear Gaussian and Student’s t autoregressions

To develop theory and notation, we first consider the component processes of the G-StMAR model. For a linear th order Gaussian or Student autoregression , we have

| (2.1) |

where , , and the autoregressive (AR) parameter satisfies the stationarity condition where

| (2.2) |

In the case of Gaussian autoregression, the distribution of the errors terms is standard normal and is a constant for all . Denoting and , , and , it is well know that the stationary solution to (2.1) for the Gaussian autoregression satisfies

| (2.3) | ||||

| (2.4) | ||||

| (2.5) |

where , and the covariance matrices and are Toeplitz matrices given as (see, e.g., Lütkepohl (2005), eq. (2.1.39))

| (2.6) |

Using the same notation as in (2.3)-(2.5) for , , and , the Student’s autoregressions utilized by Meitz et al., 2018a (which have also appeared at least in Spanos, (1994) and Heracleous and Spanos, (2006)) are obtained by letting with in (2.1) and defining

| (2.7) |

This definition (which requires the stationarity condition of the AR parameter) guarantees stationarity of the Student’s autoregressions. Distributional properties of such stationary Student’s autoregressions are similar to the Gaussian case, in particular (Meitz et al., 2018a, , Theorem 1),

| (2.8) | ||||

| (2.9) | ||||

| (2.10) |

The aforementioned properties of the component processes are essential in the following discussions and will be exploited implicitly. Gaussian component processes of the G-StMAR model are referred to as GMAR type and Student’s component processes as StMAR type since they are identical to the component processes of the GMAR model (Kalliovirta et al.,, 2015) and the StMAR model (Meitz et al., 2018a, ), respectively.

2.2 Gaussian and Student’s t mixture autoregressive model

Let () be the real valued time series of interest, and let denote the -algebra generated by the random variables . For a G-StMAR model with mixture components and autoregressive order , we have

| (2.11) | ||||

| (2.12) |

where are -measurable, are independent of , , (the set is defined in (2.2)), and are unobservable regime variables such that for each , exactly one of them takes the value one and the others take the value zero. Given the past of , and are assumed to be conditionally independent, and the conditional probability for regime occurring at the time is expressed in terms of the mixing weights that satisfy (for all ). Each observation is thus generated by a linear autoregression corresponding to some (unobserved) mixture component which is selected randomly according to the probabilities determined by the mixing weights.

The first mixture components are (linear) Gaussian autoregressions and the rest are Student’s autoregressions. Regarding equation (2.11), this means that for , the terms have standard normal distributions and the variances are constants . For , the terms follow the -distribution and the variances are as in equation (2.7) except that is replaced with and the regime specific parameters are used to define and therein. The component specific conditional means are defined by equation (2.12) for all the components.

Based on the above specifications, the conditional density function of a G-StMAR model with autoregressive order is given as

| (2.13) |

where the conditional densities and are obtained from the properties of the component processes (using the regime specific parameters). The form of the Student’s density function in (2.13) is given in online Appendix. The G-StMAR model adds to the class of mixture models introduced by Le et al., (1996) and further developed by Wong and Li, (2000), Wong and Li, 2001a , Wong and Li, 2001b , Glasbey, (2001), Lanne and Saikkonen, (2003), and Wong et al., (2009), to name a few.

In order to specify the mixing weights in (2.13), we first define the following function for notational convenience. Let

| (2.14) |

where the -dimensional densities and correspond to the stationary distribution of the th component process (given in the equations (2.3) and (2.8)). Denoting , the mixing weights of the G-StMAR model are defined as

| (2.15) |

where the parameters satisfy . The mixing weights are thus weighted ratios of densities of the component processes corresponding to the previous observations. This specific definition of the mixing weights is appealing as it states that an observation is more likely to be generated from a regime with higher relative weighted likelihood. Moreover, it allows the probabilities of each regime occurring to depend on the level, variability, and temporal dependence of the past observations. This is not only convenient for forecasting but it also allows the researcher to associate specific characteristics to different regimes. It turns out that this formulation of the mixing weights also leads to attractive theoretical properties such as fully known stationary distribution of realizations , , and ergodicity of the process. These theoretical properties are formally stated in Theorem 1 below.

Before stating the theorem, a few notational conventions are provided. We collect the parameters of the G-StMAR model to a vector where , , , , and . The parameter is omitted because it is obtained from the restriction . The parameter space for the G-StMAR model is

| (2.16) |

where the restriction () is made to ensure existence of finite second moments and the set is as in (2.2). A G-StMAR model with autoregressive order , GMAR type regimes, and StMAR type regimes is referred to as the G-StMAR() model, whenever clarity of the presentation requires.

Theorem 1

The stationary distribution of is a mixture of -dimensional normal and -distributions with constant mixing weights . By the well known properties of the normal and the -distribution, all its moments lower than exist and are finite. Moreover, as shown in the proof of Theorem 1, for any , the marginal stationary distribution of the vector is also a mixture of normal and -distributions. This gives the parameters an interpretation as the unconditional probabilities for the observation being generated from the th component process. Similarly to the GMAR and the StMAR process, the mean, variance, and first autocovariances of are thus

| (2.18) |

where is the :th autocovariance of the :th component process.

The conditional mean and variance of the G-StMAR process are obtained from the definition of the model as and

| (2.19) |

The conditional mean shares a common form with the GMAR model and StMAR model but differs from them in the definition of the mixing weights. The conditional variance includes three components; the first one is related to the conditional variances of the GMAR type components and the second one to the StMAR type components, whereas the third term encapsulates heteroskedasticity caused by variations in the conditional mean.

Notice that the GMAR model (Kalliovirta et al.,, 2015) can be obtained as a special of the G-StMAR model by setting and , and similarly the StMAR model (Meitz et al., 2018a, ) is obtained by setting and . We simply need to drop the corresponding terms from the formulas, and all the definitions and results stated in this and in the next section also hold for to the GMAR and StMAR models individually. However, some theory developed for the GMAR model, such as geometric ergodicity (Kalliovirta et al.,, 2015, Theorem A.1), has not been established for the StMAR and G-StMAR models. The GMAR model also requires less (currently) unverified assumptions than the StMAR and G-StMAR models for concluding asymptotic normality of the maximum likelihood estimator (see Kalliovirta et al.,, 2015, Section 2, Meitz et al., 2018a, , Theorem 3, and Theorem 2 of this paper)

3 Estimation

Parameters of the G-StMAR model can be estimated with the method of maximum likelihood (ML). Because the stationary distribution of the process is known, the exact log-likelihood function can be used. Suppose the observed time series is and that the initial values are stationary. Then the log-likelihood function of the G-StMAR model takes the form

| (3.1) |

where

| (3.2) |

and the density functions and follow the notation described in Section 2.2. If stationarity of the initial values seems unreasonable, one can condition on the initial values by dropping the first term on the right hand side of (3.1) and base the estimation on the resulting conditional log-likelihood function.

In what follows, we assume estimation based on the conditional log-likelihood function , i.e., that the ML estimator maximizes . We have scaled the conditional log-likelihood function with the sample size so that the notation is consistent with the referred literature.

To investigate the asymptotic properties of the ML estimator , the parameter space given in (2.16) needs to be restricted in a way that guarantees identification of the parameters. This amounts to requiring that components of the G-StMAR model cannot be ”relabelled” so that one ends up with the same model with different parameter vector; that is,

| (3.3) |

The restrictions required to establish asymptotic properties of the ML estimator are summarized in the following assumption.

Assumption 1

The true parameter value is an interior point of which is a compact subset of .

Asymptotic properties of the ML estimator under the conventional high-level conditions are stated in the following theorem (which is similar to Theorem 3 in Meitz et al., 2018a on the ML estimator of the StMAR model). Denote and .

Theorem 2

Suppose that are generated by the stationary and ergodic G-StMAR process of Theorem 1 and that Assumption 1 holds. Then is strongly consistent, i.e., almost surely. Suppose further that (i) with finite and positive definite, (ii) , and (iii) for some , compact convex set contained in the interior of that has as an interior point. Then .

If one is willing to assume validity of the conditions (i)-(iii) of Theorem 2, the ML estimator has the conventional limiting distribution, implying that approximative standard errors for the estimates are obtained as usual. Moreover, standard likelihood based tests are applicable as long as the orders and are correctly specified. If or is chosen too large, some of the parameters are not identified causing the result of Theorem 2 to break down. This particularly happens when one tests for the number of regimes as the null hypothesis would imply that some regime is reduced from the model111Meitz and Saikkonen, (2017) have, however, recently developed such tests for mixture models with Gaussian conditional densities. (see the related discussion in Kalliovirta et al.,, 2015, Section 3.3.2). Similar caution also applies for testing whether a regime is of the GMAR type against the alternative that it is of the StMAR type, as under the null hypothesis for the StMAR type regime being tested, violating Assumption 1. Numerical consequences of the weak identification of very large degrees of freedom parameters are briefly discussed in Section 4.

3.1 Two-phase maximum likelihood estimation

Finding the ML estimates amounts to maximizing the log-likelihood function (3.1) over the high dimensional parameter space (2.16) satisfying several constraints. Due to the complexity of the log-likelihood function, finding an analytical solution is infeasible, so numerical optimization methods are required. The EM algorithm (Redner and Walker,, 1984) has been a popular choice for estimating mixture models (e.g. Wong and Li,, 2000, Wong and Li, 2001a, , Wong and Li, 2001b, , and Wong et al.,, 2009) as it is suitable for problems where all the data relevant to estimation is not observed (for mixture models that is the origin of each observation; in our case, the random variables in (2.11)). For the G-StMAR model the EM algorithm is not, however, particularly useful because in each maximization step one faces a new optimization problem that is not much simpler than the original one. This is because in the G-StMAR model the mixing weights also depend on the AR parameters (in a complex way). Conventional gradient based algorithms, on the other hand, tend to converge to some local maximum near the starting point, making them generally insufficient for maximizing multimodal objective functions such as (3.1) that require thorough exploration of the parameter space.

Several optimization algorithms capable of escaping from local maxima have been proposed for maximization of complicated multimodal objective functions. Such robust methods, which include simulated annealing and the genetic algorithm (see, e.g., Goffe et al.,, 1994 and Dorsey and Mayer,, 1995), often perform well but they are computationally heavy and tend to converge slowly when near the global maximum point (see the discussion in Dorsey and Mayer,, 1995, Section 3). Following Dorsey and Mayer, (1995) (and Meitz et al., 2018a, , Meitz et al., 2018b, ), we hence suggest employing a hybrid estimation procedure where a genetic algorithm is used to find starting values for a gradient based method which then accurately converges to a nearby local maximum or saddle point.

Even with the two-phase estimation procedure, parameters of the G-StMAR model can be challenging to estimate. We have therefore accompanied this paper with the CRAN distributed R package ”uGMAR” (Virolainen,, 2020) in which the genetic algorithm has been modified to improve its performance.222In addition to the G-StMAR model, uGMAR also accomodates the GMAR and StMAR models. Brief descriptions of the employed genetic algorithm and its modifications are given in an Appendix. After running the genetic algorithm, the estimation is finalized with a variable metric algorithm (Nash,, 1990, algorithm 21, implemented by R Core Team,, 2020) using central difference approximation for the gradient of the log-likelihood function. Because of the presence of multiple local maxima, a (sometimes large) number of estimation rounds should be performed to obtain reliable results, for which uGMAR makes use of parallel computing to shorten the estimation time.

4 Building a G-StMAR Model

In empirical applications, building a G-StMAR model amounts to finding a suitable autoregressive order , the number of GMAR type regimes , and the number of StMAR type regimes . Different strategies for choosing the number of each type of regimes may be considered depending on the application. We propose a simple model selection procedure which takes advantage of the observation that the G-StMAR model is a limiting case of the StMAR model333The definition of the StMAR() model is technically the same as of the G-StMAR() model..

It is easy to see that the linear Gaussian autoregression defined in Section 2.1 is obtained as a limiting case of the Student’s autoregression with the degrees of freedom parameter tending to infinity. As the mixing weights (2.15) are weighted ratios of the component process densities, it then follows that the G-StMAR() model is obtained as a limiting case of a StMAR() model with the parameters limiting to infinity. Consequently, if a StMAR() model is fitted to data generated by a G-StMAR() process, then asymptotically, the regimes of the fitted StMAR model are expected to get large degrees of freedom estimates. We therefore suggest building a G-StMAR model by first finding a suitable StMAR model, and then estimating the appropriate G-StMAR model if the fitted StMAR model contains large degrees of freedom estimates. A StMAR model can be specified, for example, by using information criteria together with quantile residual diagnostics (see, e.g., Kalliovirta,, 2012).

Overly large degrees of freedom estimates in a StMAR model are redundant but their weak identification also causes several inconveniences in numerical analysis of the model. They lead to nearly numerically singular Hessian matrix of the log-likelihood function when evaluated at the estimate, making the approximate standard errors often unavailable. Weakly identified degrees of freedom parameters also cause inconvenience in quantile residual based model diagnostics. In particular, the quantile residual tests proposed by Kalliovirta, (2012) require a positive definite approximation of the Hessian matrix (evaluated the ML estimate). The tests are thus not applicable for StMAR models with too large degrees of freedom estimates, whereas they are for the corresponding G-StMAR models. Applicability of Kalliovirta,’s (2012) tests, which take into account the uncertainty caused by estimation of the parameters, might have consequences in model selection when sheer graphical analysis of the quantile residuals fails to reveal inadequacies. We demonstrate such a case in the empirical application.

5 Empirical application

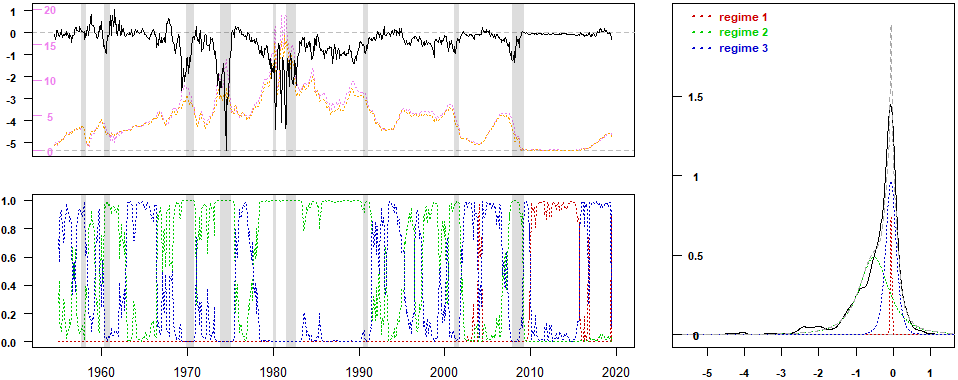

We consider the monthly U.S. interest rate spread between the 3-month Treasury bill (TB) secondary market rate and the effective federal funds (FF) rate, covering the period from 1954VII to 2019VII (781 observations). The series is plotted in Figure 1 (top left) along with the 3-month TB and FF rates, and with the shaded areas indicating the periods of (NBER based) U.S. recessions. All the data were taken from the Federal Reserve Bank of St. Louis database.

Treasury bills are short-term pure discount bonds which are backed by the U.S. government and therefore generally considered to be almost free from default-risk. The effective federal funds rate is the averaged rate at which depository institutes loan federal funds to each other overnight. The overnight FF lending agreements are one of the most liquid financial asset, but unlike TBs, they are subject to a notable default-risk. The relationship between TB and FF rates has been studied, among others, by Simon, (1990) and Sarno and Thornton, (2003), while Kishor and Marfatia, (2013) examine the relationship between TB and FF futures rate.

According to term structure theory, a long-term interest rate should reflect the current and expected future short-term rates, and also perceptions of risk and liquidity in the form of (possibly time varying) premium. Simon, (1990) studied the predictive power of the weekly spread between the 3-month TB and FF rates on the future levels of the FF rate in 1972-1987. He argued that the current and expected future FF rates affect the spread between the TB and FF rates through the repurchase agreement (repo) market444In a repo, the borrower sells a security to the lender and agrees to repurchase it in the future (often in the next day). Effectively, repos function similarly to collateralized loans. See Baklanova et al., (2015) for an overview of the U.S. repo market. because repos are closely linked to the FF rate, and corporations with funds to invest can buy TBs alternatively to investing in consecutive overnight repos. TB rates are linked to the FF rates also because security dealers finance the bulk of their TB inventories in the repo market, which is closely tied to the FF market. Furthermore, when trust in solidity of the banking system weakens, the increased demand for safety lowers TB rates relatively to FF rates. Simon, (1990) accounted for this by employing the spread between the 3-month Eurodollar time deposit555Eurodollar time deposit is a U.S. dollar-denominated deposit at a bank outside the U.S. with a fixed maturity. and TB rates as a risk premium for bank safety. He found that the spread between the 3-month TB and FF rate had significant predictive power on future levels of the FF rate in the volatile nonborrowed reserves operating period (late 1979 - late 1982) but less or none in the other subperiods.

Sarno and Thornton, (2003) identified an error correction model (ECM) between the daily 3-month TB and effective FF rate (covering the period from 1974 to 1999) and showed that their ECM, which allows for asymmetries and nonlinearities, outperforms the alternative of a linear ECM. One of their main findings was that the FF rate (which is controlled by the Fed) seems to adjust to the TB rate and not vice versa, supporting the hypothesis that the market anticipates changes in the FF rate, moving the TB rate in advance. Moreover, it appears that the adjustment speed depends on the sign and size of the deviation from the long-run equilibrium. Sarno and Thornton, (2003) argued that although there has been a number of procedural changes affecting predictability of the FF rate, their results implicate that the changes have been statistically unimportant. Furthermore, their robustness checks indicate that their findings on the adjustments from disequilibria also hold for monthly data. Variations and asymmetries in the adjustment speed, on the other hand, indicate that the dynamics of the spread between the TB and FF rates might fluctuate along with the level of the spread. This suggests that a mixture model, such as the G-StMAR model, which is able encapsulate such behaviour could be an appropriate choice of model.

Kishor and Marfatia, (2013) argued that the results in Sarno and Thornton, (2003) are not very surprising since the effective FF rate always tends to revert back to the FF target rate, and it does not incorporate markets expectations of the changes in the future FF rate. To get around that, they studied the relationship between the 3-month TB rate and the 1-month FF futures rate which does incorporate information about market’s anticipations on the future FF rate. They fitted a linear ECM to a daily series from 1989 to 2008, and found that the TB rate and the FF futures rate both seem to move to correct a short-run disequilibrium.

Interestingly, the spread between the 3-month TB rate and the effective FF rate is most of the time (covered in our sample period) negative. Sarno and Thornton, (2003) made a similar observation for their daily series and suggested that only a small fraction of the negative difference could be attributed to the low default-risk of TBs, but that a more plausible explanation is that the interest on TBs is exempt from some local and state taxes. As the smaller taxes have larger effect on paid net interest (relative to interest paid on federal funds) when the interest rates are higher, some movements of the spread could be partially caused by the differences in taxation.

5.1 Estimation and model selection

We employ the method of maximum likelihood based on the exact log-likelihood function for estimating the parameters of the considered models. Adequacy of the estimated models is examined using quantile residual diagnostics in the framework presented in Kalliovirta, (2012). The quantile residuals of a correctly specified G-StMAR model are asymptotically independent with standard normal distributions (Kalliovirta,, 2012, Lemma 2.1), so they can be used for graphical analysis in a similar fashion to conventional Pearson’s residuals. In addition to graphical analysis of the quantile residuals, we perform Kalliovirta,’s (2012) asymptotic tests (which take into account the uncertainty caused by estimation of the parameters) for testing normality, autocorrelation, and conditional heteroskedasticity of the quantile residuals. The estimation, quantile residual diagnostics, and other numerical analysis of the models is conducted using the R package uGMAR (Virolainen,, 2020) which is available through the CRAN repository.666There is also Matlab code available for the StMAR model in the form of StMAR MATLAB Toolbox by Meitz et al., 2018b . uGMAR estimates the model parameters using the two-phase procedure described in Section 3.1.

Following the model selection procedure described in Section 4, we started by finding a suitable StMAR model. First, we estimated the StMAR() model with one mixture component, , and autoregressive orders and found that the order yields the largest likelihood. Adequacy of the StMAR() model was clearly rejected by the quantile residual tests (see Table 2), so we estimated the StMAR() models with orders and . The order minimized the Schwarz-Bayesian (BIC) and the Hannan-Quinn (HQIC) information criteria, whereas the Akaike’s information criterion (AIC) was minimized by the order . Inappropriate estimates extremely near the border of the stationarity region were discarded as they are not solutions of interest (but maximize the likelihood for rather a technical reason), so in such cases the next-best local maximum of the log-likelihood function was considered instead. In both the StMAR() and the StMAR() model, a very large degrees of freedom estimate for one regime was obtained (approximately and , respectively), so we estimated the corresponding G-StMAR() and G-StMAR() models. Removing the weakly identified degrees of freedom parameters by switching to the G-StMAR models enabled us to compute approximate standard errors of the estimates and to calculate Kalliovirta,’s (2012) test statistics (see Section 4). The values of the information criteria are reported in Table 2 and the parameter estimates of the G-StMAR models are reported in Table 1 with the approximate standard errors for the estimates in brackets.

Estimates regarding the GMAR type regime are quite similar for the two G-StMAR models, and their standard errors are relatively large. This is because for both of the models the GMAR type regime mainly occurs in the period of near-zero interest rates after 2008 and there are hence only few observations from that regime (regime 1 in Figure 1, bottom left, which displays the mixing weights of the G-StMAR() model; the mixing weights of the G-StMAR() model are not shown). The three zeros in the variance parameter estimates (and in their standard errors) signify that the estimates (and their standard errors) round to zero in three digits accuracy777More accurate values for the ML estimate of and its standard error are and for the G-StMAR() model, and for the G-StMAR() model, and and for the G-StMAR( model, respectively., implying that the GMAR type regime exhibits very low variability (conditionally and unconditionally). The small mixing weight parameter estimates, interpreted as the unconditional probability for the GMAR type regime occurring, reflect the observation that eras of such a low variability have been rare in the sample period. Also, a remarkably large standard error for the second regime’s variance parameter sticks out for both of the models. Examination of the profile log-likelihood functions (not shown) does not, however, reveal anything notable.

Since the AR parameter estimates for the G-StMAR() model are somewhat similar in all regimes, we estimated a StMAR() model with the AR parameters restricted to be the same in all regimes, allowing for changes in the level, variability, and kurtosis only. The degrees of freedom estimate for one regime was very large (approximately ), so we estimated the corresponding restricted G-StMAR model which we refer to as the G-StMAR( model. The parameter estimates of this model are also presented in Table 1 with the related statistics, and the values of the information criteria in Table 2. The standard errors of the AR parameters are notably smaller than in the non-restricted models because the AR parameters are common for all the regimes.

| G-StMAR() | G-StMAR() | G-StMAR( | ||||

|---|---|---|---|---|---|---|

| (0.010) | (0.009) | (0.002) | ||||

| (0.129) | (0.124) | (0.037) | ||||

| (0.168) | (0.163) | (0.050) | ||||

| (0.140) | (0.136) | (0.050) | ||||

| (0.142) | (0.141) | (0.052) | ||||

| (0.128) | (0.132) | (0.042) | ||||

| (0.000) | (0.000) | (0.000) | ||||

| (0.021) | (0.035) | (0.025) | ||||

| (0.005) | (0.025) | (0.025) | ||||

| (0.040) | (0.055) | |||||

| (0.053) | (0.076) | |||||

| (0.053) | (0.075) | |||||

| (0.055) | (0.077) | |||||

| (0.042) | (0.058) | |||||

| (18.779) | (2.052) | (0.374) | ||||

| (0.026) | (0.801) | (0.872) | ||||

| (0.132) | (0.141) | |||||

| (0.005) | (0.005) | |||||

| (0.069) | ||||||

| (0.090) | ||||||

| (0.090) | ||||||

| (0.098) | ||||||

| (0.085) | ||||||

| (0.011) | (0.013) | |||||

| (2.951) | (4.511) | |||||

| Normality | Autocorrelation | Cond. h.skedasticity | AIC | HQIC | BIC | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Number of lags | ||||||||||||

| StMAR(6,1) | ||||||||||||

| G-StMAR() | ||||||||||||

| G-StMAR() | ||||||||||||

| G-StMAR( | ||||||||||||

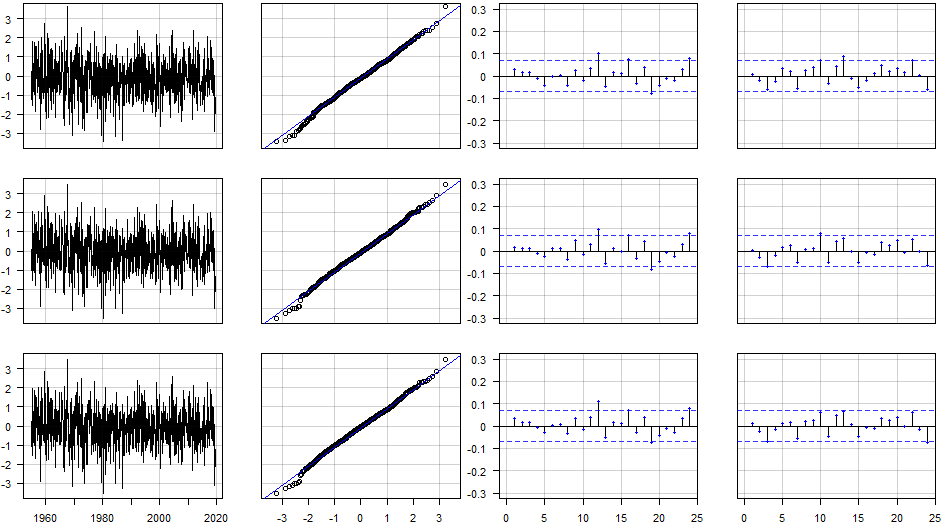

Figure 2 presents the time series, normal quantile plot, and the sample autocorrelation function of the quantile residuals, and the sample autocorrelation function of the squared quantile residuals for the G-StMAR models presented in Table 1. Graphical analysis of the quantile residuals does not show significant signs of inadequacy for any of the models. A slightly too fat lower tail in the quantile residuals’ distributions and somewhat large, approximately , sample autocorrelation at lag sticks out for each of the three models, however.

In order to further study adequacy of the models, we employed Kalliovirta,’s (2012) tests, and tested for normality, autocorrelation, and conditional heteroskedasticity of the quantile residuals, taking into account , and lags in the autocorrelation and heteroskedasticity tests. The -values obtained from the tests are reported in Table 2. The normality test rejects for all the three models at level of significance, possibly because of the fat lower tails in the quantile residuals’ distributions. More interestingly, despite the similarities in the graphical analysis, the autocorrelation tests unambiguously reject adequacy of the G-StMAR() model, whereas the -values are reasonable for the G-StMAR() model which also passes the heteroskedasticity tests. The -values for the autocorrelation tests are rather small also for the restricted G-StMAR( model, which is preferred by the information criteria, showing some evidence of inadequacy. We therefore prefer the unrestricted G-StMAR() model whose overall adequacy seems quite satisfactory. The fact that the restricted model has information criteria values superior to the unrestricted models, however, suggests that imposing the autocorrelation structure to be the same for all regimes would also be a reasonable modelling choice.888For comparison, we also estimated the GMAR() model with orders and . The values of the information criteria were, however, found inferior to our G-StMAR models, with the GMAR() model minimizing BIC () and the GMAR() model minimizing HQIC () and AIC ().

5.2 Discussion

Our model selection procedure led to the (unrestricted) G-StMAR() model which identifies three statistical regimes for the spread between the 3-month TB secondary market rate and the effective FF rate. The mixing weights of the model are presented in Figure 1 (bottom left) along with the interest rate spread series (top left). The GMAR type regime (red) dominates the period of near-zero interest rates occurring after 2008, where also the spread stays close to zero and exhibits very low variability. The second regime (green) identifies periods of high variability and low mean, spanning through most of the recessions, whereas the third regime (blue) often occurs999By a regime occurring at a point of time we mean that according to the estimated mixing weights, the process generated an observation from that regime with a probability close to one. after the recessions when the spread moderately varies around zero. These characteristics of the regimes are also highlighted in Figure 1 (right) where a kernel density estimate of the spread (black solid line) is presented with the model implied density (grey dashed line) and the regime densities (red, green, and blue dotted lines; regime densities are multiplied by the mixing weight parameter estimates , ). The model implied density matches fairly well to the skewed distribution of the observations, but peakiness of the distribution seems a bit exaggerated and the lower tail is not fat enough.

Based on our G-StMAR() model, the regime specific unconditional mean of the spread varies from the %-units of the first (GMAR type) and third regime to the %-units of the second regime, with each regime regularly occurring for several consecutive months. As the second regime dominates during most of the recessions, and also often occurs before the recessions when the interest rates are relatively high, it seems plausible that part of the larger negative mean is explained by expectations of a decrease in the near-future FF rate. The third regime, on the other hand, mostly occurs after the recessions when the interest rates seem relatively low, possibly indicating that the larger mean of the regime could be related to the lack of expected decreases in the FF rate. These findings are consistent with Sarno and Thornton, (2003) who found that the FF rate corrects disequilibriums from the long-run relationship, supporting the hypothesis that market’s anticipations in the future movements of the FF rate are reflected in the TB rate.

Sarno and Thornton, (2003) also found that the adjustment speed of FF rate towards the long-run equilibrium depends on the sign and size of the deviation. Specifically, FF rate below the long-run trend or larger deviation implies faster adjustment, suggesting that too high values of the spread would be corrected faster than too low values. This might partially explain why the low mean second regime usually occurs when the interest rates are declining, but a rise in the FF rate is not always accompanied with a switch to the higher mean third regime. Another possibility is that market’s predictions on the future movements of the FF rate are sometimes rather poor or a premium has an increased effect on the opposite direction. During the savings and loan crisis in 80’s and 90’s, increased preference for the safety of TBs would seem like a plausible partial explanation for the moderately negative spread despite of the mainly increasing FF rate from late 1986 to early 1989.

Overall, the three statistical regimes of our G-StMAR model identify three economic regimes, with the first regime dominating the period in which the movements of the interest rates are limited by the zero lower bound. The second regime arguably occurs often when the market anticipates decreases in the FF rate or possibly has increased preferences for the safety of the almost default-risk free TBs. The third regime seems to mostly occur at times when the Fed is arguably not expected to significantly decrease the FF rate target (because the recession has already passed and the interest rates are relatively low).

6 Conclusions

This article introduced a mixture autoregressive model which is a combination of the Gaussian mixture autoregressive (GMAR) model (Kalliovirta et al.,, 2015) and the Student’s mixture autoregressive (StMAR) model (Meitz et al., 2018a, ). This model, referred to as the G-StMAR model, has several attractive theoretical and practical properties that are analogous to those of the GMAR and StMAR model. In addition to discussing the properties, it was noted that estimating the parameters of the G-StMAR model can be challenging in practice. Following Dorsey and Mayer, (1995) (and Meitz et al., 2018a, , Meitz et al., 2018b, ), we suggested using a two-phase estimation procedure where a genetic algorithm is used to find starting values for a gradient based method and accompied the paper with the R package uGMAR (Virolainen,, 2020) which implements the two-phase estimation procedure with a modified version of a genetic algorithm.

We stated that the G-StMAR model is a limiting case of a StMAR model with some degrees of freedom parameters tending to infinity, and found that large degrees of freedom estimates in a StMAR model are not only redundant but also cause several inconveniences in numerical analysis of the model. In particular, weak identification of large degrees of freedom parameters was found to lead to numerically nearly singular approximation of the observed information matrix when evaluated at the estimate, making the approximate standard errors for the estimates and Kalliovirta,’s (2012) diagnostic tests often unavailable. Removing the redundant degrees of freedom parameters by switching to a G-StMAR model was concluded to obviate the problems.

As an empirical application, we considered the monthly U.S. interest rate spread between the 3-month Treasury bill rate and the effective federal funds rate. Our G-StMAR model identified three regimes for the spread, with a switch from a StMAR type regime to a GMAR type regime arising from a switch in the economic regime, namely, to a regime where the zero lower bound limits the movements of the interest rates. The two StMAR type regimes accommodate eras of low mean and high variability and high mean and moderate variability. The first StMAR type regime arguably occurs often when the market anticipates decreases in the FF rate or possibly has increased preferences for safety, whereas the second one mostly occurs when the Fed is arguably not expected to significantly decrease the FF rate target. As opposed to modelling the series with a StMAR model containing an overly large degrees of freedom estimate, switching to the more parsimonious G-StMAR model allowed us to numerically compute approximate standard errors for the estimates, and moreover, to perform the Kalliovirta,’s (2012) quantile residual tests which turned out to have significance in the model selection.

Acknowledgements

The author thanks Markku Lanne, Mika Meitz, and Pentti Saikkonen who commented the work and gave insightful suggestions that helped to improve the paper substantially. The author also thanks the Academy of Finland for financing the project.

References

- Baklanova et al., (2015) Baklanova, V., Copeland, A., and McCaughrin, R. (2015). Reference guide to u.s. repo and securities lending markets, staff report no. 740. Technical report, Federal Reserve Bank of New York.

- Ding, (2016) Ding, P. (2016). On the conditional distribution of the multivariate distribution. The American Statistician, 70(3):293–295.

- Dorsey and Mayer, (1995) Dorsey, R. and Mayer, W. (1995). Genetic algorithms for estimation problems with multiple optima, nondifferentiability, and other irregular features. Journal of Business and Economic Statistics, 13(1):53–66.

- Glasbey, (2001) Glasbey, C. (2001). Non-linear autoregressive time series with multivariate gaussian mixtures as marginal distributions. Journal of Royal Statistical Society: Series C, 50(2):143–154.

- Goffe et al., (1994) Goffe, W., Ferrier, G., and Rogers, J. (1994). Global optimization of statistical functions with simulated annealing. Journal of Econometrics, 60(1-2):65–99.

- Heracleous and Spanos, (2006) Heracleous, M. and Spanos, A. (2006). Student’s dynamic linear regression: re-examining volatility modeling. In Terrel, D. and T.B, F., editors, Econometric Analysis of Financial Time Series (Advances in Econometrics), volume 20, chapter 1, pages 289–319. Emerald Group Publishing Limited, Bingley.

- Holzmann et al., (2006) Holzmann, H., Munk, A., and Gneiting, T. (2006). Identifiability of finite mixtures of elliptical distributions. Scandinavian Journal of Statistics, 33(4):753–763.

- Kalliovirta, (2012) Kalliovirta, L. (2012). Misspecification tests based on quantile residuals. The Econometrics Journal, 15(2):358–393.

- Kalliovirta et al., (2015) Kalliovirta, L., Meitz, M., and Saikkonen, P. (2015). A gaussian mixture autoregressive model for univariate time series. Journal of Time Series Analysis, 36(2):247–266.

- Kalliovirta et al., (2016) Kalliovirta, L., Meitz, M., and Saikkonen, P. (2016). Gaussian mixture vector autoregression. Journal of Econometrics, 192(2):465–498.

- Kishor and Marfatia, (2013) Kishor, N. and Marfatia, H. (2013). Does federal funds futures rate contain information about the treasury bill rate? Applied Financial Economics, 23(16):1311–1324.

- Lanne and Saikkonen, (2003) Lanne, M. and Saikkonen, P. (2003). Modeling the u.s. short-term interest rate by mixture autoregressive processes. Journal of Financial Econometrics, 1(1):96–125.

- Le et al., (1996) Le, N., Martin, R., and Raftery, A. (1996). Modeling flat stretches, bursts, and outliers in time series using mixture transition distribution models. Journal of the American Statistical Association, 91(436):1504–1515.

- (14) Meitz, M., Preve, D., and Saikkonen, P. (2018a). A mixture autoregressive model based on student’s -distribution. Unpublished working paper, available as arXiv:1805.04010.

- (15) Meitz, M., Preve, D., and Saikkonen, P. (2018b). StMAR Toolbox: A MATLAB Toolbox for Student’s t Mixture Autoregressive Models.

- Meitz and Saikkonen, (2017) Meitz, M. and Saikkonen, P. (2017). Testing for observation-dependent regime switching in mixture autoregressive models. Unpublished working paper, available as arXiv:1711.03959.

- Meyn and Tweedie, (2009) Meyn, S. and Tweedie, R. (2009). Markov Chains and Stochastic Stability. Cambridge University Press, Cambridge, 2nd edition.

- Monahan, (1984) Monahan, J. (1984). A note on enforcing stationarity in autoregressive-moving average models. Biometrika, 71(2):403–404.

- Nash, (1990) Nash, J. (1990). Compact Numerical Methods for Computers. Linear algebra and Function Minimization. Adam Hilger, Bristol and New York, 2nd edition.

- Newey and McFadden, (1994) Newey, W. and McFadden, D. (1994). Large sample estimation and hyphothesis testing. In Eagle, R. and MacFadden, D., editors, Handbook of Econometrics, volume 4, chapter 36. Elsevier Science B.V.

- Patnaik and Srinivas, (1994) Patnaik, L. and Srinivas, M. (1994). Adaptive probabilities of crossover and mutation in genetic algorithms. Transactions on Systems, Man and Cybernetics, 24(4):656–667.

- R Core Team, (2020) R Core Team (2020). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Rao, (1962) Rao, R. (1962). Relations between weak and uniform convergence of measures with applications. The Annals of Mathematical Statistics, 33(2):659–680.

- Redner and Walker, (1984) Redner, R. and Walker, H. (1984). Mixture densities, maximum likelihood and the em algorithm. Society for Industrial and Applied Mathematics, 26(2):195–239.

- Sarno and Thornton, (2003) Sarno, L. and Thornton, D. (2003). The dynamic relationship between the federal funds rate and the treasury bill rate: An empirical investigation. Journal of Banking & Finance, 27(6):1079–1110.

- Simon, (1990) Simon, D. (1990). Expectations and the treasury bill-federal funds rate spread over recent monetary policy regimes. Journal of Finance, 45(2):567–577.

- Smith et al., (1995) Smith, R., Dike, B., and Stegmann, S. (1995). Fitness inheritance in genetic algorithms. Proceedings of the 1995 ACM symbosium on Applied Computing, pages 345–350.

- Spanos, (1994) Spanos, A. (1994). On modeling heteroskedasticity: the student’s and elliptical linear regression models. Econometric Theory, 10(2):286–315.

- Virolainen, (2020) Virolainen, S. (2020). uGMAR: Estimate Univariate Gaussian or Student’s Mixture Autoregressive Model. R package version 3.2.3, availabe at CRAN: https://CRAN.R-project.org/package=uGMAR.

- Wong et al., (2009) Wong, C., Chan, W., and Kam, P. (2009). A student’s -mixture autoregressive model with applications to heavy-tailed financial data. Biometrika, 96(3):751–760.

- Wong and Li, (2000) Wong, C. and Li, W. (2000). On mixture autoregressive model. Journal of the Royal Statistical Society, 62(1):95–115.

- (32) Wong, C. and Li, W. (2001a). On a mixture autoregressive conditional heteroskedastic model. Journal of the American Statistical Association, 96(455):982–995.

- (33) Wong, C. and Li, W. (2001b). On logistic mixture autoregressive model. Biometrika, 88(3):833–846.

Appendix A Modified genetic algorithm

As discussed in Section 3.1, the accompanied R package uGMAR (Virolainen,, 2020) employs a two-phase producedure for estimating the parameters of the G-StMAR model (and also of the GMAR (Kalliovirta et al.,, 2015) and the StMAR (Meitz et al., 2018a, ) model). In the first phase, a genetic algorithm is used to find starting values for a gradient based variable metric algorithm (Nash,, 1990, algorithm 21) which then, in the second phase, accurately converges to a nearby local maximum or saddle point. In this appendix, it is first briefly described how our version of the genetic algorithm functions in general, and then the specific modifications made to enhance estimation of the G-StMAR model are discussed (for more detailed description of the genetic algorithm, see, e.g., Dorsey and Mayer,, 1995).

In a genetic algorithm, an initial population that consists of different parameter vectors (that are often drawn at random) is first constructed. Then the genetic algorithm operates iteratively so that in each iteration, referred to as generation, the current population consisting of candidate solutions goes through the phases of selection, crossover, and mutation. In the selection phase, parameter vectors are sampled with replacement from the current population to the reproduction pool according to probabilities that are based on their fitness, that is, on the related log-likelihoods. In the crossover phase, some of the parameter vectors in the reproduction pool are crossed over with each other, with the probabilities of experiencing crossover given by the crossover rate. Finally, some of the parameter vectors are mutated in the mutation phase, with the mutation probabilities given by the mutation rate. In our version of the genetic algorithm, mutation means that the mutating parameter vector is fully replaced with another parameter vector that is drawn at random (in Dorsey and Mayer,, 1995, mutations are drawn for each scalar component of parameter vectors individually). The reproduction pool that has experienced crossovers and mutations is the new population, and the algorithm proceeds to the next generation, evolving towards the global maximum one generation after another.

Because the G-StMAR model can be challenging to estimate even with a robust estimation algorithm such as the genetic algorithm, we have made modifications to improve its performance. In particular, a slightly modified version101010We modified it to enforce a 40% minimum crossover rate for all individuals in the population of the individually adaptive crossover rate and mutation rate introduced by Patnaik and Srinivas, (1994) is employed in order to force the subaverage solutions to disrupt while protecting the better ones. The fitness inheritance proposed by Smith et al., (1995) is deployed to shorten the estimation time by cutting down the number computationally costly evaluations of the log-likelihood function. In order to enhance thorough exploration of the parameter space, the algorithm proposed by Monahan, (1984) is used in some random mutations to generate parameter vectors near the boundary of the stationarity region. In the case of a premature convergence, most of the population is mutated so that exploration of the parameter space continues. Moreover, after a large number generations have been run, for faster convergence the random mutations will be targeted to a neighbourhood of the best-so-far parameter vector; we call these smart mutations.

In addition to the modifications described above, we have made further adjustments to care for the special structure of the log-likelihood function. Specifically, the definition of the mixing weights (2.15) implies that if a regime has parameter values that fit poorly relative to the other regimes, the mixing weights drop to near zero. The surface of the log-likelihood function thus flattens in the related directions, meaning that the algorithm is unable to converge properly if the proposed parameter vectors don’t pose a reasonable fit for all regimes. This problem of unidentified (or redundant) regimes often occurs when the number of mixture components is chosen too large, but it can be present even when the number of mixture components is chosen correctly. In uGMAR, we try to resolve this problem by penalizing parameter vectors containing redundant regimes with smaller probabilities to get chosen to the reproduction pool. Moreover, smart mutations are targeted only to the neighbourhood of parameter values that identify all regimes. If such parameter vectors have not been found (after a large number of generations have been run), combining regimes from different parameter vectors is attempted along with random search.

Appendix B Properties of multivariate Gaussian and Student’s -distribution

Denote a -dimensional real valued vector by . It’s well known that the density function of the -dimensional multivariate Gaussian distribution with mean and covariance matrix is

| (B.1) |

Similarly to Meitz et al., 2018a but differing from the standard form, we parametrize the Student’s -distribution using its covariance matrix as a parameter together with the mean and degrees of freedom. The density function of such a -dimensional -distribution with mean , covariance matrix , and degrees of freedom is

| (B.2) |

where

| (B.3) |

and is the gamma function. We assume that the covariance matrix is positive definite for both distributions.

Consider a partition of either a normally or -distributed (with degrees of freedom) random vector such that has dimension and has dimension . Consider also a corresponding partition of the mean vector and the covariance matrix

| (B.4) |

where, for example, the dimension of is . Then in the case of normally distributed , has the marginal distribution and has the marginal distribution . In the -distributed case, the marginal distributions are and respectively (see, e.g., Ding, (2016), also in what follows).

In the normally distributed case, the conditional distribution of the random vector given is

| (B.5) |

where

| (B.6) | ||||

| (B.7) |

In the -distributed case, the analogous conditional distribution is

| (B.8) |

where

In particular, we have

| (B.9) | ||||

| (B.10) |

Appendix C Proofs

C.1 Proof of Theorem 1

Suppose is a G-StMAR process. Then the process is clearly a Markov chain on . Let be a random vector whose distribution is characterized by the density function . According to equations (2.3)-(2.5), (2.8)-(2.10), (2.13), and (2.15), the density of the conditional distribution of given is

| (C.1) | |||

| (C.2) |

The random vector therefore has the density function

| (C.3) |

Using properties of marginal densities of multivariate normal and -distributions, by integrating out we obtain the density of as .111111Because the covariance matrices () have the Toepliz form and , the marginal densities for random vectors shorter than are obtained by integrating the desired random variables out, and their distributions are mixtures of normal and -distributions. Thus, the random vectors and are identically distributed. As the process is a (time homogeneous) Markov chain, it follows that has a stationary distribution characterized by the density (Meyn and Tweedie,, 2009, pp. 230-231).

For ergodicity, let signify the -step transition probability measure of the process . Using the th order Markov property of , it’s easy to check that has the density

| (C.4) |

Clearly for all and all , so we can conclude that is ergodic in the sense of Meyn and Tweedie, (2009, Ch. 13) by using arguments identical to those used in the proof of Theorem 1 in Kalliovirta et al., (2015).

C.2 Proof of Theorem 2

First note that is continuous, and that together with Assumption 1 of the main paper it implies existence of a measurable maximizer . In order to conclude strong consistency of , it needs to be shown that (see, e.g., Newey and McFadden,, 1994, Theorem 2.1 and the discussion on page 2122)

-

(i)

the uniform strong law of large numbers holds for the log-likelihood function; that is,

almost surely as , -

(ii)

and that the limit of is uniquely maximized at .

Proof of (i). Because the initial values are assumed to be from the stationary distribution, the process , and hence also , is stationary and ergodic, and . To conclude (i), it thus suffices to show that (see Rao,, 1962). This is done by using compactness of the parameter space to derive finite lower and upper bounds for which is given by

| (C.5) |

We know from the structure of the parameter space that and for all , and for all , for some , and . Because the exponential function is bounded from above by one on the non-positive real axis, and in addition , there exists a constant such that

| (C.6) |

for all .

We also have for all . Combined with the fact that the Gamma function is continuous on the positive real axis, this implies that there exist constants and such that

| (C.7) |

for all . Because and hence is positive definite, and , we can find some such that

| (C.8) |

for all . Combined with (C.7) and (C.8), the inequality implies that there exists a constant for which

| (C.9) |

for all . According to (C.6), (C.9) and the restriction , there exists a constant such that

| (C.10) |

We know from compactness of the parameter space that

| (C.11) |

implying

| (C.12) |

for all , and for some finite constant . By it also holds that , so

| (C.13) |

for all .

Accordingly, since and , it holds for some that

| (C.14) |

Thus, because and the inner functions below take values larger than one, we have

| (C.15) |

As Meitz et al., 2018a state in the proof of Theorem 3, the quadratic form on the right-hand-side of (C.8) satisfies

| (C.16) |

for all , and for some . Since also and , we have for some finite constant . Combining the former inequality with (C.7) and (C.15) yields a lower bound

| (C.17) |

Finally, the restriction together with (C.13) and (C.17) implies

| (C.18) |

As (because is stationary and has finite second moments), it follows from Jensen’s inequality that

| (C.19) |

The upper bound (C.10) together with (C.18) and finiteness of the aforementioned expectations shows that .

Proof of (ii). Given that condition (3.3) of the main paper sets a unique order for the mixture components, proving that this identification condition is satisfied amounts to showing that , and that the equality implies

| (C.20) |

for some permutations and . For notational clarity, we omit the subscripts from and , and write , , for the expressions in (C.5) making clear their dependence on the parameter value. We leave the dependence of on and unmarked and denote by mixing weights based on the true parameter value.

Making use of the fact that the density function of has the form (see proof of Theorem 1) and reasoning based on Kullback-Leibler divergence, one can use arguments analogous to those in Kalliovirta et al., (2015, p. 265) to conclude with equality if and only if for almost all

| (C.21) |

For each fixed at a time, the mixing weights, conditional means and variances in (C.21) are constants, so we may apply the result on identification of finite mixtures of normal and -distributions in Holzmann et al., (2006, Example 1) (their parametrization of the -distribution slightly differs from ours, but identification with their parametrization implies identification with our parametrization). For each fixed , there thus exists a permutation (that may depend on ) of the index set such that

| (C.22) |

for almost all (). Analogously, for each fixed there exists a permutation (that may depend on ) of the index set such that

| (C.23) |

for almost all ().

As argued by Kalliovirta et al., (2015, pp. 265-266) for the GMAR type components, it follows from (C.22) that and for . Accordingly, Meitz et al., 2018a showed that (C.23) implies , and for , completing the proof of strong consistency.

Given consistency and assumptions of the theorem, asymptotic normality of the ML estimator can now be concluded using standard arguments. The required steps can be found, for example, in Kalliovirta et al., (2016, proof of Theorem 3). We omit the details for brevity.