Statistical applications of random matrix theory:

comparison of two populations I

Abstract

This paper investigates a statistical procedure for testing the equality of two independent estimated covariance matrices when the number of potentially dependent data vectors is large and proportional to the size of the vectors, that is, the number of variables. Inspired by the spike models used in random matrix theory, we concentrate on the largest eigenvalues of the matrices in order to determine significance. To avoid false rejections we must guard against residual spikes and need a sufficiently precise description of the behaviour of the largest eigenvalues under the null hypothesis.

In this paper, we lay a foundation by treating alternatives based on perturbations of order , that is, a single large eigenvalue. Our statistic allows the user to test the equality of two populations. Future work will extend the result to perturbations of order and demonstrate conservativeness of the procedure for more general matrices.

keywords:

T1This paper is based on the PhD thesis of Rémy Mariétan that will be divided into three parts.

and

t1PhD Student at EPFL in mathematics department t2Professor at EPFL in mathematics department

1 Introduction

In the last two decades, random matrix theory (RMT) has produced numerous results that offer a better understanding of large random matrices. These advances have enabled interesting applications in communication theory and even though it can potentially contribute to many other data-rich domains such as brain imaging or genetic research, it has rarely been applied. The main barrier to the adoption of RMT may be the lack of concrete statistical results from the probability side. The straightforward adaptation of classical multivariate theory to high dimensions can sometimes be achieved, but such procedures are only valid under strict assumptions about the data such as normality or independence. Even minor differences between the model assumptions and the actual data lead to catastrophic results and such procedures also often do not have enough power.

This paper proposes a statistical procedure for testing the equality of two covariance matrices when the number of potentially dependent data vectors and the number of variables are large. RMT denotes the investigation of estimates of covariance matrices or more precisely their eigenvalues and eigenvectors when both and tend to infinity with . When is finite and tends to infinity the behaviour of the random matrix is well known and presented in the books of Mardia, Kent and Bibby (1979), Muirhead (2005) and Anderson (2003) (or its original version Anderson (1958)). In the RMT case, the behaviour is more complex, but many results of interest are known. Anderson, Guionnet and Zeitouni (2009), Tao (2012) and more recently Bose (2018) contain comprehensive introductions to RMT and Bai and Silverstein (2010) covers the case of empirical (estimated) covariance matrices.

Although the existing theory builds a good intuition of the behaviour of these matrices, it does not provide enough of a basis to construct a test with good power, which is robust with respect to the assumptions. Inspired by the spike models, we define the residual spikes and provide a description of the behaviour of this statistic under a null hypothesis when the perturbation is of order . These results enable the user to test the equality of two populations as well as other null hypotheses such as the independence of two sets of variables. Later papers will extend the results to perturbations of order and demonstrate the robustness of our test’s level for more general matrices.

The remainder of the paper is organized as follows. In the next section, we develop the test statistic and discuss the problems associated with high dimensions. Then we present the main theorem 2.1. Various results necessary for the proof are introduced in Section 3. The proofs themselves are technical and presented in the supplementary material Mariétan and Morgenthaler (2019) included in the second part of this paper. The last section contains case studies and a comparison with alternative tests.

2 Test statistic

We compare the spectral properties of two covariance estimators and of dimension which can be represented as

In this equation, and are of the form

with and being independent unit orthonormal random matrices whose distributions are invariant under rotations, while and are independent positive random diagonal matrices, independent of with trace equal to m and a bound on the diagonal elements. Note that the usual RMT assumption, is replaced by this bound! The (multiplicative) spike model of order 1 determines the form of and .

Our results will apply to any two centered data matrices and which are such that

and can be decomposed in the manner indicated. This is the basic assumption concerning the covariance matrices. We will assume throughout the paper that . Note that because and are independent and invariant by rotation we can assume without loss of generality that as in Benaych-Georges and Rao (2009). Under the null hypothesis, and we use the simplified notation for both matrices where and .

To test against it is natural to consider the extreme eigenvalues of

| (2.1) |

We could also swap the subscripts, but it turns our to be preferable to use the inversion on the matrix with larger sample size.

The distributional approximations we will refer to are based on RMT, that is, they are derived by embedding a given data problem into a sequence of random matrices for which both and tend to infinity such that tends to a positive constant . The most celebrated results of RMT describe the almost sure weak convergence of the empirical distribution of the eigenvalues (spectral distribution) to a non-random compactly supported limit law. An extension of this theory to the ”Spike Model” suggests that we should modify because estimates of isolated eigenvalues derived from these estimates are asymptotically biased. The following corrections will be used.

Definition 2.1.

Suppose is of the form described at the start of the section. The unbiased estimator of is defined as

| (2.2) |

where is the eigenvalue of . When as above, it is asymptotically equivalent to replace by .

Suppose that is the eigenvector corresponding to , then the filtered estimated covariance matrix is defined as

| (2.3) |

The matrix (2.1) which serves as the basis for the test then becomes either

| (2.4) |

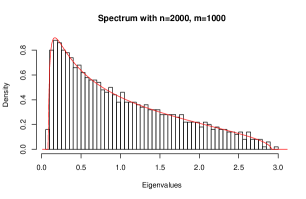

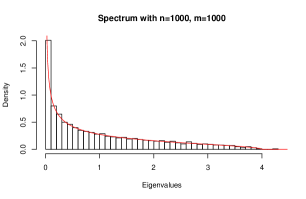

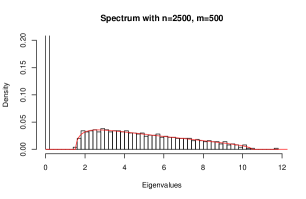

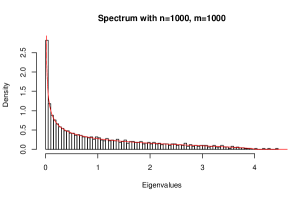

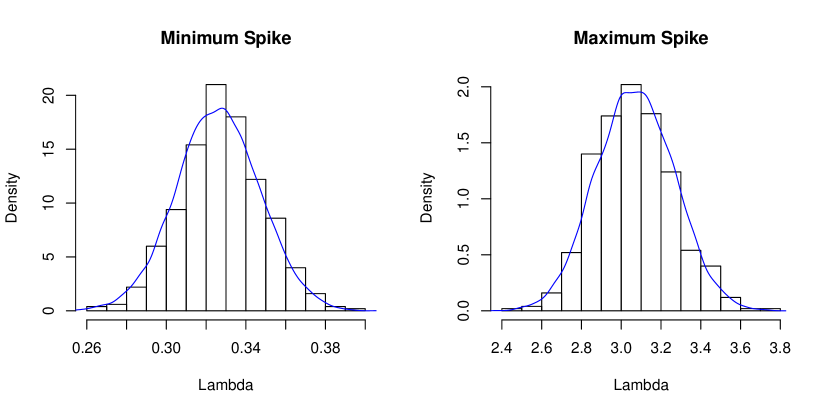

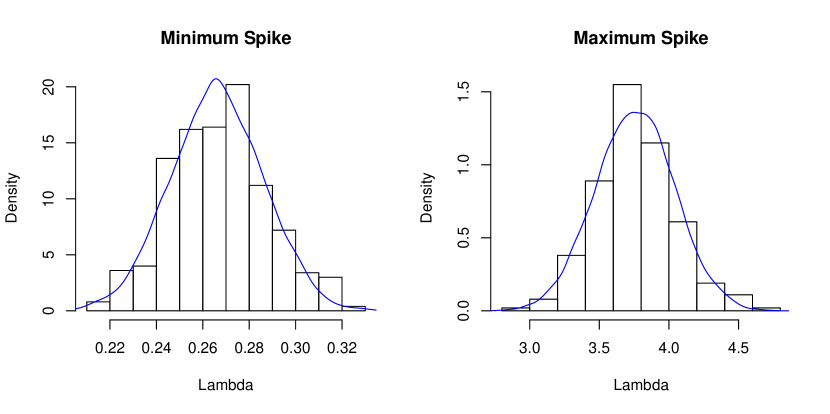

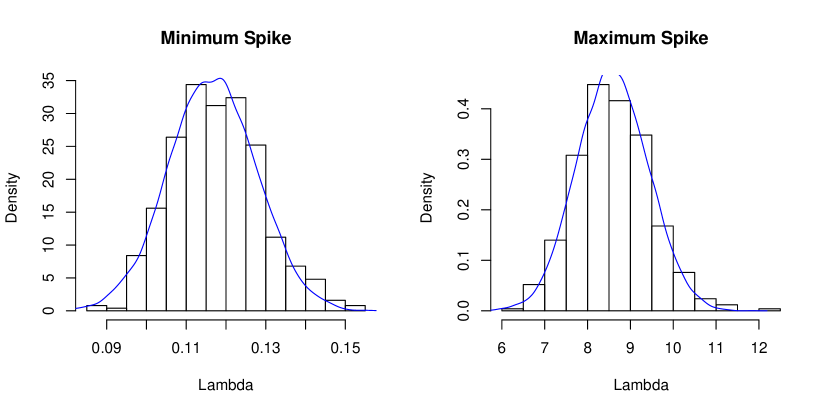

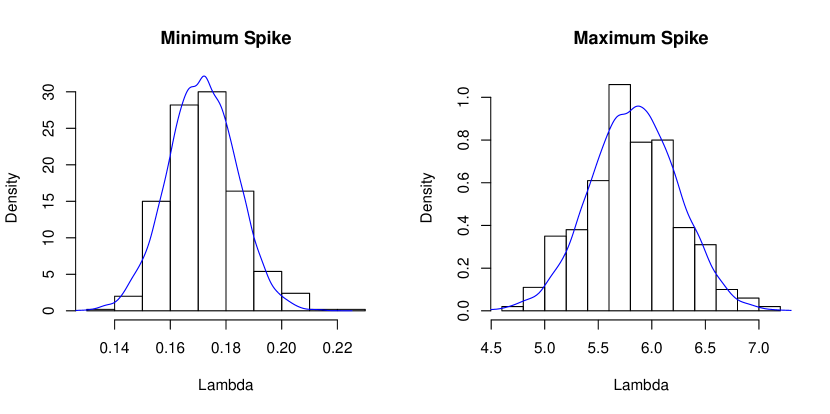

In the particular case where and have independent jointly normal columns vector with constant variance , the distribution of the spectrum of the second of the above matrices is approximately Marcenko-Pastur distributed (see Marchenko and Pastur (1967)). This follows because is a finite perturbation. However, because of the non-consistency of the eigenvectors presented in Benaych-Georges and Rao (2009), we may observe residual spikes in the spectra, as shown in Figure 1. Thus, even if the two random matrices are based on the same perturbation, we see some spikes outside the bulk. This observation is worse in the last plot because four spikes fall outside the bulk even if there is actually no difference! This poses a fundamental problem for our test, because we must be able to distinguish the spikes indicative of a true difference from the residual spikes. These remarks lead to the following definition.

Definition 2.2.

The residual spikes are the isolated eigenvalues of

when (under the null hypothesis). The residual zone is the interval where a residual spike can fall asymptotically.

|

|

|

|

This paper studies these residual spikes by deriving the distribution of the extreme residual spikes under the null hypothesis. The philosophy is explained in Figure 2 with illustrations inspired by the i.i.d. normal case. All the eigenvalues lying in what we call the residual zone are potentially not indicative of real differences. However, when an eigenvalue is larger, we declare that this spike expresses a true difference.

Most of our plots feature the seemingly more natural matrix

But, although this choice simplifies the study in terms of convergence in probability when the perturbation is of order , this is no longer the case in more complex situations. In addition, the eigenvectors associated with the residual spikes are more accessible for the matrix in which all estimates are filtered.

Let and be isolated eigenvalues and construct the asymptotic unbiased estimators as in Equation (2.2)

Here and are the eigenvalues of and , respectively. In practice we do of course not observe and , but a simple argument using Cauchy’s interlacing law shows that we can replace the previous estimators by

where and are the ith ordered eigenvalue of and , respectively. The test statistic is then

where the filtered matrices are constructed as in (2.3). These two statistics provide a basis for a powerful and robust test for the equality of (detectable) perturbations and .

2.1 Null distribution

Obviously under , is a function of . The suspected worst case occurs in the limit as and it is this limit which will determine the critical values of the test. This can be checked by Criterion 2.3 which we discuss later. Let

Because of our focus on the worst case scenario under , we will investigate the asymptotics as . Our test rejects the null hypothesis of equal populations if either or is small, where and are the observed extreme residual spikes.

In the investigation of the extremal eigenvalues under multiplicative perturbations, we make use of the following random variables

In particular, when , we use . When we only study one group, we use the simpler notation when no confusion is possible. Note that is the empirical T-transform. Moreover, for an applied perspective, all these variables can be estimated by M_s_1,s_2,X(ρ_X)=^M_s_1,s_2,X(ρ_X)=1m-1 ∑_i=2^m ^λ^ΣX,is1(ρX-^λ^ΣX,i)2.

The following result describes the asymptotic behavior of the extreme eigenvalues and thus of and . .

Theorem 2.1.

Suppose are as described at the start of Section 2 and with with regard to large . Let

and , as described above (see, 2.1).

Then, conditional on the spectra and of and ,

where

Moreover,

where

The error in the approximation is with regard to large values of .

Special case

If the spectra are Marcenko-Pastur distributed, then:

If tends to , then

(Proof in supplement material Mariétan and Morgenthaler (2019).)

2.2 Discussion and simulation

The above theorem gives the limiting distribution of and . In this subsection, we first check the quality of the approximations in Theorem 2.1, then we investigate the worst case with regard to .

2.2.1 Some simulations

Assume and with and . The components of the random vectors are independent and the covariance between the vectors is as follows:

Let and be two perturbations in . Then,

We assume a common and large value for and .

Distribution

Figure 1 presents empirical distributions of the extreme residual spikes in different scenarios together with the normal densities from our theorem.

|

|

||||||||||||||||||

|

|

||||||||||||||||||

|

|

||||||||||||||||||

|

|

2.2.2 Increasing residual spike

In the four scenarios used in the simulations, we can estimate the expectation of the residual spike. Figure 3 shows that the expectations of the largest residual spikes are always strictly increasing as a function of and the expectations of the smallest residual spikes are always strictly decreasing. This is, however, not universally true. To address this issue, the following criterion can be used.

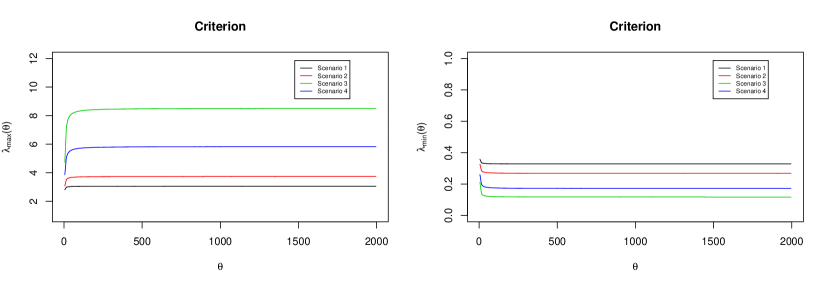

Definition 2.3.

Suppose and are two independent random estimated covariance matrices of the form described at the start of Section 2. Let

|

|

(2.5) |

where and and

|

|

We say that the criterion is satisfied, if this estimate of the expectation of the residual spike is a monotone increasing function of .

Remark 2.1.

The above estimate of the expectation of a residual spike fails when is large compared to and we should then use an asymptotic estimator of based on:

Using this approximation, the estimated curve of the equation (2.5) makes an error of .

3 Further Results

The proof of the main distributional result (Theorem 2.1) is based on three results and a lemma that are worthwhile on their own right and will be presented and discussed in this section. Future papers will also use this result for extensions.

3.1 Unit invariant vector statistic

Theorem 3.1.

Let be a random matrix with spectrum and trace equal to . We denote by and , two orthonormal invariant random vectors of size and independent of the eigenvalues of . We set

where , and with indices and . If ,

|

|

where . Moreover, for ,

|

|

In particular, with the notation ,

|

|

and

|

|

Finally if we look at bivariate normal random variables :

|

|

where if . Then, conditioning on the spectrum , tends to a multivariate Normal. Moreover, all the bivariate elements are asymptotically independent.

Remark 3.1.1.

-

1.

The trace of equal to can easily be obtained by rescaling the matrix.

-

2.

Although the condition of independence between eigenvectors and eigenvalues of appears to be restrictive, it is an automatic consequence if the eigenvectors are Haar distributed.

-

3.

If is a rescaled standard Wishart, then

where are the eigenvectors of .

(Proof in supplement material Mariétan and Morgenthaler (2019).)

3.2 Characterisation and convergence of eigenvalues and angles

In this section, we study the convergence of the random variable and the angle between the eigenvectors. The proof for the parts and are given in Benaych-Georges and Rao (2009), which also provides the main idea for the proof. We only show convergence results for perturbations of order , although we express eigenvectors and eigenvalues of a matrix as a function of the eigenstructure of in general and can already be perturbed.

Theorem 3.2.

In this theorem, is a finite perturbation of order .

-

1.

Suppose is a symmetric matrix with eigenvalues and eigenvectors for . The perturbation of by leads to .

For , we define and such that W P ~u_^Σ,i = ^λ_^Σ,i ~u_^Σ,i, and the usual such that if , then ^Σ ^u_^Σ,i = P^1/2 W P^1/2 ^u_^Σ,i = ^λ_^Σ,i ^u_^Σ,i. Under these conditions, the following results hold:

-

•

The eigenvalues are such that for ,

-

•

The eigenvectors are such that

In particular if ,

Moreover,

Therefore, for and such that ,

where is a weighted empirical T-transform.

Suppose that , and satisfy the conditions described at the start of Section 2. Moreover, suppose that is large enough to create detectable spikes, and , in the matrices and . Then,

where

Note that and are empirical T-transform and its estimation.

Remark 3.2.1.

If the spectra of and are Wishart random matrices of size and degree of freedom , respectively, then by setting and

(Proof in supplement material Mariétan and Morgenthaler (2019).)

The second part of Theorem 3.2 is very surprising! We already knew that the eigenvectors are not consistent. We show in the proof that the dot product of and is smaller than that of and and that of and . Among the consequences of this theorem is the fact that there is always an asymptotic bias between two eigenvectors, even if they are equal.

3.3 Asymptotic distribution of the eigenvalues and the angle

Suppose that you observe a perturbation of order applied to two random matrices and . We investigate the distribution of , , and .

Theorem 3.3.

Suppose and satisfy the conditions described at the start of Section 2 with , a detectable perturbation of order . Moreover, we assume and , the eigenvalues of and as known. We defined

We construct the unbiased estimators of , and via the relationship

where and are the largest eigenvalues of and corresponding to the eigenvectors and .

-

1.

If , we define

where we assume

and a convergence rate of to in . Then

where

If , then we can simplify the formulas. We define

| and |

Using this notation,

Moreover, the asymptotic distributions of and are the same.

If , a finite constant, then a mixture of the two first scenarios describes the first two moments of the joint distribution. The formula of the second moment is asymptotically the same as the variance formula when . The formula of the first moment is asymptotically the same as the expectation formula when .

The random variables can be expressed as functions of invariant unit random statistics of the form:

(Assuming a canonical perturbation leads to a simpler formula) Knowing and we have

-

•

Exact distributions:

Moreover,

where is independent of , , and . In order to get the exact distribution, we should replace by where and are independent unit invariant random vectors.

-

•

Approximations:

We provide three methods of estimation of the angle in order to estimate it for all .

Finally, the double angle is such that

Remark 3.3.1.

If the spectra of and are rescaled Wishart matrices of size with degree of freedom. By setting

and

If tends to infinity, then (^^θX⟨^uX,u ⟩2) Asy∼ N((θ1-c(θ-1)21+cθ-1) , 1m(2 c θ22c22c22 c2(c+1)θ2)). Moreover, (^^θX^^θY⟨^uX,^uX⟩2) Asy∼ N((θθ1-c(θ-1)21+cθ-1), 1m(2c θ20 2c20 2c θ22c22c22c24 c2(c+2)θ2) ).

(Proof in supplement material Mariétan and Morgenthaler (2019).)

3.4 Residual spike as a function of the statistics

Finally we present a simple result of linear algebra that express the residual spike as a function of the statistics.

Lemma 3.1.

Suppose

|

|

The eigenvalues of are and

where . Moreover, if

|

|

The eigenvalues of are and

where . (Proof in supplement material Mariétan and Morgenthaler (2019).)

4 Comparison with existing tests

In the classical multivariate theory, Anderson (1958) proposes a log-ratio test for the equality of two covariance matrices. Suppose

We want to test

The log-likelihood ratio test look at the statistic

Under and if is finite, . Some other interesting tests propose to observe the determinant and the trace of . In this section we show that any test statistics using or have difficulties to test

when and are finite perturbations. We compare the performance of these tests with our procedure defined in Section 2.1 in the table 2.

- 1.

-

2.

When , the table show

where gives the quantiles of under and is found empirically.

-

3.

When , the table show

where gives the quantiles of under is are found empirically.

Remark 4.1.

In order to generalise the test to degenerated matrices, the determinant is defined as the product of the non-null eigenvalues of the matrix and the inverse is the generalised inverse.

| 0.81 | 1 | 0.98 | 0.99 | ||

|---|---|---|---|---|---|

| 0.15 | 0.05 | 0.11 | 0.05 | ||

| 0.11 | 1 | 0.13 | 0.1 | ||

| 1 | 1 | 0.99 | 1 | ||

| 0.09 | 0.31 | 0.04 | 0.11 | ||

| 0.47 | 1 | 0.15 | 0.12 | ||

| 1 | 1 | 1 | 1 | ||

| 0.07 | 0.12 | 0.07 | 0.02 | ||

| 0.41 | 1 | 0.08 | 0.05 |

In the particular case of finite perturbation, the trace and the determinant have difficulties to catch the alternative. On the other hand, our procedure detects easily some small differences. The statistic and would be interesting to detect perturbation of large order such as a global change of the variance.

Remark 4.2.

Assuming and are as described at the start of Section 2, the procedure proposed in this paper required the estimation of and for in order to compute the quantile under of the residual spikes, and . By Cauchy-Interlacing law and bounded eigenvalues and we can use the following estimator

4.1 Conclusion

By studying perturbation of order , this work highlights the particular behaviour of residual spikes. A future work will present the behaviours of residual spikes when the perturbations are of order . Nevertheless, this task requires many intermediary results. Therefore an other future work will present only the joint distribution of some statistics as the eigenvalues and the eigenvectors.

Appendix A Table

We extend the simulations of Section 2.2. We test our Main Theorem 2.1 under different hypotheses on and (recall that and ):

-

1.

The matrices and contain independent standard normal entries.

-

2.

The columns of the matrices and are i.i.d. Multivariate Student with degrees of freedom. For and , X_⋅,i i.i.d.∼ N(→0,Im)χ288 and Y_⋅,j i.i.d.∼ N(→0,Im)χ288

-

3.

The rows of and are i.i.d. ARMA entries of parameters and . Moreover, the traces of the matrices are standardised by the estimated variance.

1. Normal entries. 100 500 1000 2000 100 1000 100 1000 100 1000 100 1000 100 500 1000 2000 2. Multivariate Student. 100 500 1000 2000 100 1000 100 1000 100 1000 100 1000 100 500 1000 2000 3. ARMA . 100 500 1000 2000 100 1000 100 1000 100 1000 100 1000 100 500 1000 2000 1. Normal entries. 100 500 1000 2000 100 1000 100 1000 100 1000 100 1000 100 500 1000 2000 2. Multivariate Student. 100 500 1000 2000 100 1000 100 1000 100 1000 100 1000 100 1 500 1000 2000 3. ARMA . 100 500 1000 2000 100 1000 100 1000 100 1000 100 1000 100 500 1000 2000 Table 3: Simulations of the extreme residual spikes. The values and are respectively the estimations of the mean and the standard error of the residual spikes obtained by respectively the Main Theorem 2.1 and empirical methods using 500 replicates and .

The Table 3 compares the estimations of the mean and the standard error of the residual spikes to their empirical values . The simulations are computed for the three scenarios described above. The perturbation is without loss of generality assumed canonical and the eigenvalue is fixed to 5000.

Supplement A \stitleStatistical applications of Random matrix theory: comparison of two populations I, Supplement \slink[url]The supplement is in the second part of this paper. \sdescriptionProofs of Theorems

References

- Anderson (1958) {bbook}[author] \bauthor\bsnmAnderson, \bfnmT. W.\binitsT. W. (\byear1958). \btitleAn introduction to Multivariate Statistical Analysis. \bseriesWiley publications in statistics. \bpublisherWiley. \endbibitem

- Anderson (2003) {bbook}[author] \bauthor\bsnmAnderson, \bfnmT. W.\binitsT. W. (\byear2003). \btitleAn introduction to Multivariate Statistical Analysis. \bseriesWiley Series in Probability and Statistics. \bpublisherWiley. \endbibitem

- Anderson, Guionnet and Zeitouni (2009) {bbook}[author] \bauthor\bsnmAnderson, \bfnmGreg W.\binitsG. W., \bauthor\bsnmGuionnet, \bfnmAlice\binitsA. and \bauthor\bsnmZeitouni, \bfnmOfer\binitsO. (\byear2009). \btitleAn Introduction to Random Matrices. \bseriesCambridge Studies in Advanced Mathematics. \bpublisherCambridge University Press. \endbibitem

- Bai and Silverstein (2010) {bbook}[author] \bauthor\bsnmBai, \bfnmZhidong\binitsZ. and \bauthor\bsnmSilverstein, \bfnmJack W.\binitsJ. W. (\byear2010). \btitleSpectral Analysis of Large Dimensional Random Matrices. \bpublisherSpringer. \endbibitem

- Benaych-Georges and Rao (2009) {barticle}[author] \bauthor\bsnmBenaych-Georges, \bfnmFlorent\binitsF. and \bauthor\bsnmRao, \bfnmNadakuditi Raj\binitsN. R. (\byear2009). \btitleThe eigenvalues and eigenvectors of finite, low rank perturbations of large random matrices. \bjournalAdvances in Mathematics \bvolume227 \bpages494-521. \endbibitem

- Bose (2018) {bbook}[author] \bauthor\bsnmBose, \bfnmArup\binitsA. (\byear2018). \btitlePatterned Random matrices. \bpublisherChapman and Hall/CRC. \endbibitem

- Marchenko and Pastur (1967) {barticle}[author] \bauthor\bsnmMarchenko, \bfnmV. A.\binitsV. A. and \bauthor\bsnmPastur, \bfnmL. A.\binitsL. A. (\byear1967). \btitleDistribution of eigenvalues for some sets of random matrices. \bjournalMath. USSR \bvolume1 \bpages457-483. \endbibitem

- Mardia, Kent and Bibby (1979) {bbook}[author] \bauthor\bsnmMardia, \bfnmK. V.\binitsK. V., \bauthor\bsnmKent, \bfnmJ. T.\binitsJ. T. and \bauthor\bsnmBibby, \bfnmJ. M.\binitsJ. M. (\byear1979). \btitleMultivariate Analysis. \bseriesProbability and mathematical statistics. \bpublisherAcademic press. \endbibitem

- Mariétan and Morgenthaler (2019) {barticle}[author] \bauthor\bsnmMariétan, \bfnmRémy\binitsR. and \bauthor\bsnmMorgenthaler, \bfnmStephan\binitsS. (\byear2019). \btitleStatistical applications of Random matrix theory: comparison of two populations I, Supplement. \endbibitem

- Muirhead (2005) {bbook}[author] \bauthor\bsnmMuirhead, \bfnmRobb J.\binitsR. J. (\byear2005). \btitleAspect of Multivariate Statistical Theory. \bseriesWiley Series in Probability and Statistics. \bpublisherWiley-Interscience. \endbibitem

- Tao (2012) {bmisc}[author] \bauthor\bsnmTao, \bfnmTerence\binitsT. (\byear2012). \btitleTopics in random matrix theory. \bhowpublishedhttp://www.math.hkbu.edu.hk/~ttang/UsefulCollections/matrix-book-2011-08.pdf. \endbibitem