Conservative Exploration in Reinforcement Learning

Evrard Garcelon Mohammad Ghavamzadeh Alessandro Lazaric Matteo Pirotta

Facebook AI Reasearch

Abstract

While learning in an unknown Markov Decision Process (MDP), an agent should trade off exploration to discover new information about the MDP, and exploitation of the current knowledge to maximize the reward. Although the agent will eventually learn a good or optimal policy, there is no guarantee on the quality of the intermediate policies. This lack of control is undesired in real-world applications where a minimum requirement is that the executed policies are guaranteed to perform at least as well as an existing baseline. In this paper, we introduce the notion of conservative exploration for average reward and finite horizon problems. We present two optimistic algorithms that guarantee (w.h.p.) that the conservative constraint is never violated during learning. We derive regret bounds showing that being conservative does not hinder the learning ability of these algorithms.

1 Introduction

While Reinforcement Learning (RL) has achieved tremendous successes in simulated domains, its use in real system is still rare. A major obstacle is the lack of guarantees on the learning process, that makes difficult its application in domains where hard constraints (e.g., on safety or performance) are present. Examples of such domains are digital marketing, healthcare, finance, and robotics. For a vast number of domains, it is common to have a known and reliable baseline policy that is potentially suboptimal but satisfactory. Therefore, for applications of RL algorithms, it is important that are guaranteed to perform at least as well as the existing baseline.

In the offline setting, this problem has been studied under the name of safety w.r.t. a baseline (Bottou et al., 2013; Thomas et al., 2015a, b; Swaminathan and Joachims, 2015; Petrik et al., 2016; Laroche et al., 2019; Simão and Spaan, 2019). Given a set of trajectories collected with the baseline policy, these approaches aim to learn a policy –without knowing or interacting with the MDP– that is guaranteed (e.g., w.h.p.) to perform at least as good as the baseline. This requires that the set of trajectories is sufficiently reach in order to allow to perform counterfactual reasoning with it. This often implies strong requirements on the ability of exploration of the baseline policy. These approaches can be extended to a semi-batch settings where phases of offline learning are alternated with the executing of the improved policy. This is the idea behind conservative policy iteration (e.g., Kakade and Langford, 2002; Pirotta et al., 2013b) where the goal is to guarantee a monotonic policy improvement in order to overcome the policy oscillation phenomena Bertsekas (2011). These approaches has been successively extended to function approximation preserving theoretical guarantees (e.g., Pirotta et al., 2013a; Achiam et al., 2017). A related problem studied in RL is the one of safety, where the algorithm is forced to satisfy a set of constraints, potentially not directly connected with the performance of a policy (e.g., Altman, 1999; Berkenkamp et al., 2017; Chow et al., 2018).

In the online setting, which is the focus of this paper, the learning agent needs to trade-off exploration and exploitation while interacting with the MDP. Opposite to offline learning, the agent has direct control over exploration. Exploration means that the agent is willing to give up rewards for policies improving his knowledge of the environment. Therefore, there is no guarantee on the performance of policies generated by the algorithm, especially in the initial phase where the uncertainty about the MDP is maximal and the algorithm has to explore multiple options (almost randomly). To increase the application of exploration algorithm, it is thus important that the policies selected by the algorithm are (cumulatively) guaranteed to perform as well as the baseline by making exploration more conservative. This setting has been studied in multi-armed bandits (Wu et al., 2016), contextual linear bandits (Kazerouni et al., 2017), and stochastic combinatorial semi-bandits (Katariya et al., 2019). These papers formulate the problem using a constraint defined based on the performance of the baseline policy (mean of the baseline arm in the multi-armed bandit case), and modify the corresponding UCB-type algorithm (Auer et al., 2002) to satisfy this constraint. Another algorithm in the online setting is by (Mansour et al., 2015) that balances exploration and exploitation such that the actions taken are compatible with the agent’s (customer’s) incentive formulated as a Bayesian prior.

While the conservative exploration problem is well-understood in bandits, little is known about this setting to RL, where the actions taken by the learning agent affect the system state. This dynamic component makes the definition of the conservative condition much less obvious in RL. While in the bandit case it is sufficient to look at (an estimate of) the immediate reward to perform a conservative decision, in MDPs acting greedily may not be sufficient since an action can be “safe” in a single step but lead to a potentially dangerous state space where it will not be possible to satisfy the conservative constraint. Moreover, after steps, the action followed by the learning agent may lead to a state that is possibly different from the one observed by following the baseline. This dynamical aspect is not captured by the bandit problem and should be explicitly taken into account by the learning agent in order to perform a meaningful decision. This, together with the problem of counterfactual reasoning in an unknown MDP, make the conservative exploration problem is much more difficult (and interesting) in RL than in bandits.

This paper aims to provide the first analysis of conservative exploration in RL. In Sec. 3 we explain the design choices that lead to the definition of the conservative condition for RL (both in average reward and finite horizon settings), and discuss all the issues introduced by the dynamical nature of the problem. Then, we provide the first algorithm for efficient conservative exploration in average reward and analyze its regret guarantees. The variant for finite-horizon problems is postponed to the appendix. We conclude the paper with synthetic experiments.

2 Preliminaries

We consider a Markov Decision Process (Puterman, 1994, Sec. 8.3) with state space and action space . Every state-action pair is characterized by a reward distribution with mean and support in , and a transition distribution over next states. We denote by and the number of states and action A stationary Markov randomized policy maps states to distributions over actions. The set of stationary randomized (resp. deterministic) policies is denoted by (resp. ). Any policy has an associated long-term average reward (or gain) and a bias function defined as

where denotes the expectation over trajectories generated starting from with . The bias measures the expected total difference between the reward and the stationary reward in Cesaro-limit (denoted by ). We denote by the span (or range) of the bias function.

Assumption 1.

The MDP is ergodic.x

In ergodic MDPs, any policy has constant gain, i.e., for all . There exists a policy for which satisfy the optimality equations,

where is the optimal Bellman operator. We use to denote the diameter of , where is the hitting time of starting from . We introduce the “worst-case” diameter

| (1) |

which defines the worst-case time it takes for any policy to move from any state to . Asm. 1 guarantees that .

Exploration in RL. Let be the true unknown MDP. We consider the learning problem where , and are known, while rewards and transition probabilities are unknown and need to be estimated online. We evaluate the performance of a learning algorithm after time steps by its cumulative regret

| (2) |

The exploration-exploitation dilemma is a well-known problem in RL and (nearly optimal) solutions have been proposed in the literature both base on optimism-in-the-face-of-uncertainty (OFU, e.g., Jaksch et al., 2010; Bartlett and Tewari, 2009; Fruit et al., 2018a) and Thompson sampling (TS, e.g., Gopalan and Mannor, 2015; Osband and Roy, 2016). Refer to (Lazaric et al., 2019) for more details.

3 Conservative Exploration in RL

In conservative exploration, a learning agent is expected to perform as well as the optimal policy over time (i.e., regret minimization) under the constraint that at no point in time its performance is significantly worse than a known baseline policy . This problem has been studied in the bandit literature (Wu et al., 2016; Kazerouni et al., 2017), where the conservative constraint compares the cumulative expected reward obtained by the actions selected by the algorithm to the one of the baseline action ,

| (3) |

where is the expected reward of action . At any time , conservative exploration algorithms first query a standard regret minimization algorithm (e.g., UCB) and decide whether to play the proposed action or the baseline based on the accumulated budget (i.e., past rewards) and whether the estimated performance of is sufficient to guarantee that the conservative constraint is satisfied at after is executed. While (3) effectively formalizes the objective of constraining an algorithm to never perform much worse than the baseline, in RL it is less obvious how to define such constraint. In the following we review three possible directions, we point out their limitations, and we finally propose a conservative condition for RL for which we derive an algorithm in the next section.

Gain-based condition. Instead of actions, RL exploration algorithms (e.g., UCRL2), first select a policy and then execute the corresponding actions. As a result, a direct way to obtain a conservative condition is to translate the reward of each action in (3) to the gain associated to the policies selected over time, i.e.,

| (4) |

The main drawback of this formulation is that the gain is the expected asymptotic average reward of a policy and it may be very far from the actual reward accumulated while executing in the specific state achieved at time . The same reasoning applies to the baseline policy, whose cumulative reward up to time may significantly different from times its gain. As a result, an algorithm that is conservative in the sense of (4) may still perform quite poorly in practice depending on , the initial state, and the actual trajectories observed over time.

Reward-based condition. In order to address the concerns about the gain-based condition, we could define the stronger condition

| (5) |

where is the sequence of rewards obtained while executing the algorithm and is the reward obtained by the baseline. While this condition may be desirable in principle (the learning algorithm never performs worse than baseline), it is impossible to achieve. In fact, even if the optimal policy is executed for all steps, the condition may still be violated because of an unlucky realization of transitions and rewards. If we wanted to accounting for the effect of randomness, we would need to introduce an additional slack of order (i.e., the cumulative deviation due to the randomness in the environment), which would make the condition looser and looser over time.

Condition in expectation. The previous remarks could be solved by taking the expectation of both sides

| (6) | ||||

where denotes the expectation w.r.t. the trajectory of states and actions generated by the learning algorithm , while the RHS is simply the expected reward obtain by running the baseline for steps. Condition (6) effectively captures the nature of the RL problem w.r.t. the bandit case. In fact, after steps, the actions followed by the learning algorithm may lead to a state that is possibly very different from the one we would have reached by playing only the baseline policy from the beginning. This deviation in the state dynamics needs to be taken into account when deciding if an exploratory policy is safe to play in the future. In the bandit case, selecting the baseline action contributes to build a conservative budget that can be spent to play explorative actions later on (i.e., by selecting , the LHS of (3) in increased by , while only a fraction is added to the RHS, thus increasing the margin that may allow playing alternative actions later). In the RL case, selecting policy at time may not immediately contribute to increasing the conservative budget. In fact, the state where is applied may significantly differ from the state that would have achieved had we selected it from the beginning. As a result, a conservative RL algorithm should be extra-cautious when selecting policies different from since their execution may lead to unfavorable states, where it is difficult to recover good performance, even when selecting the baseline policy.

While this may seem a reasonable requirement, unfortunately it is impossible to build an empirical estimate of (6) that a conservative exploration algorithm could use to guide the choice of policies to execute. In fact, the LHS averages the performance of the algorithm over multiple executions, while in practice we have only access to a single realization of the algorithm’s process. This prevents from constructing accurate estimates of such expectation directly from the data observed up to time . A possible approach would be to construct an estimate of the MDP and use it to replay the algorithm itself for steps. Beside prohibitive computational complexity, the resulting estimate of the expected cumulative reward of would suffer from an error that increases with , thus making it a poor proxy for (6).111More precisely, let be an estimate of and be the largest error in estimating its dynamics at time . Estimating the expected cumulative reward by running (an infinite number of) simulations of in would suffer from an error scaling as . For any regret minimization algorithm, cannot decrease linearly with and thus the estimation of would have an error increasing with .

Condition with conditional expectation. Let be a generic time and , the non-stationary policy executed up to . We require the algorithm to satisfy the following conditional conservative condition

| (7) | ||||

where the expectations are taken w.r.t. the trajectories generated by a fixed non-stationary policy (i.e., we ignore how rewards affect ). Notice that this condition is now stochastic, as itself is a random variable and thus we require to satisfy (7) with high probability. This formulation can be seen as relying on a pseudo-performance evaluation of the algorithm instead of the actual expectation as in (6)222We use pseudo-performance to stress the link the pseudo-regret formulations used in bandit (e.g., Auer et al., 2002) and it is similar to (3), which takes the expected performance of each of the (random) actions, thus ignoring their correlation with the rewards. This formulation has several advantages w.r.t. the conditions proposed above: 1) it considers the sum of rewards rather than the gain as (4), thus capturing the dynamical nature of RL, 2) it contains expected values, so as to avoid penalizing the algorithm by unlucky noisy realizations as (5), 3) as shown in the next section, it can be verified using the samples observed by the algorithm unlike (6).

The finite-horizon case.

We conclude the section, by reformulating (7) in the finite-horizon case. In this setting, the learning agent interacts with the environment in episodes of fixed length . Let be the initial state, be the policy proposed at episode and let be beginning of the -th episode. Then is a sequence of policies , each executed for steps. In this case, condition (7) can be conveniently written as

| (8) | ||||

where is the step value function of at the first stage. In this formulation, the conservative condition has a direct interpretation, as it directly mimics the bandit case (3). In fact, the performance of the algorithm up to episode is simply measured by the sum of the value functions of the policies executed over time (each for steps) and it is compared to the value function of the baseline itself. Note that this definition is compatible with the regret: . Indeed, the regret defined in expectation w.r.t. the stochasticity of the model but not w.r.t. the algorithm, there is no expectation w.r.t. the possible sequence of policies generated by .

4 Conservative UCRL

In this section, we introduce conservative upper-confidence bound for reinforcement learning (CUCRL2), an efficient algorithm for exploration-exploitation in average reward that both minimize the regret (2) and satisfy condition (7).

Input: , , , , , For episodes do 1. Set and episode counters . 2. Compute estimates , and a confidence set . 3. Compute an -approximation of the optimistic planning problem . 4. Compute , see Eq. 11. 5. if Eq. 4.1 is true then else 6. Sample action . 7. While do (a) Execute , obtain reward , and observe . (b) Set . (c) Sample action and set . 8. Set , and

CUCRL2 builds on UCRL2 in order to perform efficient conservative exploration. At each episode , CUCRL2 builds a bounded parameter MDP , where and are high-probability confidence intervals on the rewards and transition probabilities such that w.h.p. and is the -dimensional simplex. This confidence intervals can be built using Hoeffding or empirical Bernstein inequalities by using the samples available at episode (e.g., Jaksch et al., 2010; Fruit et al., 2018b). CUCRL2 computes an optimistic policy in the same way as UCRL2: . This problem can be solved using EVI (see Fig. 3 in appendix) on the optimistic optimal Bellman operator of (Jaksch et al., 2010).333. Then, it needs to decide whether policy is “safe” to play by checking a conservative condition (see Sec. 4.1) where contains all the information (samples and chosen policies) available at the beginning of episode , including the optimistic policy . If , the UCRL2 policy is “safe” to play and CUCRL2 plays until the end of the episode. Otherwise, CUCRL2 executes the baseline , i.e., . We denote by the set of episodes ( included) where UCRL2 executed an optimistic policy and by its complement. Formally, if we set else . The pseudocode of CUCRL2 is reported in Fig. 1.

Note that, contrary to what happens in conservative (linear) bandits, the statistics of the algorithm are updated continuously, i.e., using also the samples collected by running the baseline policy. This is possible since UCRL2 is a model-based algorithm and any off-policy sample can be used to update the estimates of the model. To have a better estimate of the conservative condition, it is possible to use the model available at episode to re-evaluate the policies at previuous episodes (change line 3 in Fig. 1). This will improve the empirical performance of CUCRL2 but breaks the regret analysis.

4.1 Algorithmic Conservative Condition

We now derive a checkable conservative condition that can be incorporated in the UCRL2 structure illustrated in the previous section. In the bandit setting, it is relatively straightforward to turn (3) into a condition that can be checked at any time using estimates and confidence intervals build from the data collected so far. On the other hand, while condition (7) effectively formalizes the requirement that the learning algorithm should constantly perform almost as well as the baseline policy, we need to consider the specific RL structure to obtain a condition that can be verified during the execution of the algorithm itself. In order to simplify the derivation, we rely on the following assumption.

Assumption 2.

The gain and bias function of the baseline policy are known.

As explained in (Kazerouni et al., 2017), this is a reasonable assumption since the baseline policy is assumed to be the policy currently executed by the company and for which historical data are available. We will mention how to relax this assumption in Sec. 4.1.

We follow two main steps in deriving a checkable condition. 1) We need to estimate the cumulative reward obtained by each of the policies played by the learning algorithm directly from the samples observed so far. We do this by relating the cumulative reward to the gain and bias of each policy and then building their estimates. 2) It is necessary to evaluate whether the policy proposed by UCRL2 is safe to play w.r.t. the conservative condition, before actually executing it. While this is simple in bandit, as each action is executed for only one step. In RL, policies cannot be switched at each step and need to be played for a whole episode. Nonetheless, the length of a UCRL2 episode is not known in advance and this requires predicting for how long the explorative policy could be executed in order to check its performance.

Step 1: Estimating the conditional conservative condition from data. In order to evaluate (7) from data, one may be tempted to first replace the sum of rewards obtained by each policy in on the lhs side by its gain , similar to the gain-based condition in (4). Indeed, under Asm. 1 any stationary policy receives asymptotically an expected reward at each step. Unfortunately, in our case . In fact, when evaluating a policy for a finite number of steps, we need to account for the time required to reach the steady regime (i.e., mixing time) and, as such, the influence of the state at which the policy is started. The notion of reward collected during the transient regime is captured by the bias function.444Puterman (1994, Sec. 8.2.1) refers to the gain as “stationary” reward while to the bias as “transient” reward. In particular, for any stationary (unichain) policy with gain and gain function executed for steps, we have that:

| (9) |

As a result, we have the bounds

Leveraging prior knowledge of the gain and bias of the baseline, we can use the second inequality to directly upper bound the baseline performance as

| (10) |

On the other hand, for a generic policy , the gain and bias cannot be directly computed since is unknown. To estimate the cumulative reward of the algorithm we resort to the estimate of the true MDP build by UCRL2 to construct a pessimistic estimate of the cumulative reward for any policy (i.e., to perform counterfactual reasoning).

Given a policy and the bounded-parameter MDP , we are intersted in finding such that: Define the Bellman operator associated to as:

| (11) |

Then, there exists such that, , where (see Lem. 5.1 in App. A). Similarly to what is done by UCRL2, we can use EVI with to build an -approximate solution of the Bellman equations. Let , then . The values computed by the pessimistic policy evaluation can be then used to bound the cumulative reward of any stationary policy.

Lemma 1.

Consider a bounded parameter MDP such that w.h.p., a policy and let . Then, under Asm. 1 for any state :

Step 2: Test safety of optimistic policy. Let be the time when episode starts. Policies have been executed until and UCRL2 computed an optimistic policy . In order to guarantee that (7) is verified the algorithm needs to anticipate how well may perform if executed for the next episode. For any policy , we first compute .555The subscript in the operator denotes the fact that it is computed using the samples observed up to . For each episode, we need to compute the estimate only for the new UCRL2 policy. In order to have a tighter estimate of the conservative condition it possible to recompute the gain and bias of the past policies at every episode (or periodically) by using all the available samples (i.e., using ). However, this will break the current regret proof. If (i.e., the baseline was executed at episode ), we let and . Then

| (12) | ||||

where is time at which episode started, is the probability of reaching state after steps starting from state following policy . The inequality follows from Lem. 1. By lower bounding the LHS of (7) by (12) and upper bounding the RHS by (10), the conservative condition becomes:

| (13) | ||||

Note that the algorithm should check this condition at the beginning of episode in order to understand if the policy is safe or if it should resort to playing policy . In many OFU algorithms, including UCRL2, the length of episode (i.e., ) is not known at the beginning of the episode. As a consequence, condition (13) is not directly computable. To overcome this limitation, we consider the dynamic episode condition introduced by (Ouyang et al., 2017). This stopping condition provides an upper-bound on the length of each episode as , without affecting the regret bound of UCRL2 (up to constants). This condition can be used to further lower-bound the last term in (13) by

| (14) | ||||

Plugging this lower bound into (13) gives the final conservative condition

| (15) |

tested by CUCRL2 at the beginning of each episode. Unknown . If the gain and bias of the baseline are unknown, we can use EVI on (Eq. 11 with instead of ) to compute an optimistic estimate of the cumulative reward of the baseline up to time . While this account for the RHS of Eq. 7, we simply define for every episode to compute a lower bound to the cumulative reward obtained by the algorithm by playing the baseline in episode before . Clearly, this approach is very pessimistic and it may be possible to design better strategies for this case.

The finite-horizon case.

We conclude this section with a remark on the finite horizon case. This case is much simpler and resemble the bandit setting. We can directly build a lower bound to the value function by using the model estimate and its uncertainty at episode . This estimate can be computed via extended backward induction –see (Azar et al., 2017, Alg. 2)– simply subtracting the exploration bonus, see Lem. 10 in App. C. The same approach can be used to construct an optimistic and pessimistic estimate of when it is unknown. This values can be directly plugged in (8) to define a checkable condition for the algorithm.

4.2 Regret Guarantees

We start providing an upper-bound to the regret of CUCRL2 showing the dependence on UCRL2 and on the baseline . Since the set is updated at the end of the episode, we denote by the set containing all the episodes where CUCRL2 played an optimistic policy. The set is its complement.

Lemma 2.

Under Asm. 1 and 2, for any and any conservative level , there exists a numerical constant such that the regret of CUCRL2 is upper-bounded as

and the conservative condition (7) is met at every step with probability at least .666The probability refers to both events: the regret bound and the conservative condition.

denotes the regret of UCRL2 over an horizon conditioned on the fact that the UCRL2 policy is executed only at episodes . During the other episodes, the internal statistics of UCRL2 are updated using the samples collected by the baseline policy . This does not pose any major technical challenge and, as shown in App. B, the UCRL2 regret can be bounded as follows.

Lemma 3 ((Jaksch et al., 2010)).

Let , for any , there exists a numerical constant such that, with probability at least ,

The second term in Lem. 2 represents the regret incurred by the algorithm when playing the baseline policy . The following lemma shows that the total time spent executing conservative actions is sublinear in time (see Lem. 8 in App. B for details).

Lemma 4.

For any and any conservative level , with probability at least , the total number of play of conservative actions is bounded by:

where and as in Eq. 1

Proof.

Let be the last episode played conservatively: . This means that at the beginning of episode the conservative condition was not verified. By rearranging the terms in Eq. 4.1 and using simple bounds, we can write that:

where and are optimistic and pessimistic gain of policy . Note that both satisfies the Bellman equation: (see footnote 3) and (see Eq. 11). At this point, the important terms in upper-bounding are similar to the one analysed in UCRL2. In particular, we have a term depending on the confidence intervals and one depending on the transitions . Let . By using the definition of the confidence intervals, it is easy to show that Define the -algebra based on past history at : . The sequence is an MDS. Thus, using Azuma inequality we have that . Putting everything together we have a quadratic form in and solving it we can write that where (see App. B). The result follows noticing that . ∎

Combining the results of Lem. 3 and Lem. 4 into Lem. 2 leads to an overall regret of order , which matches the regret of UCRL2. This shows that CUCRL2 is able to satisfy the conservative condition without compromising the learning performance. Nonetheless, the bound in Lem. 4 shows how conservative exploration is more challenging in RL compared to the bandit setting. While the dependency on the conservative level is the same, the number of steps the baseline policy is executed can be as large as instead of constant as in CUCB (Wu et al., 2016). Furthermore, Lem. 2 relies on an ergodicity assumption instead of the much milder communicating assumption needed by UCRL2 to satisfy Lem. 3. Asm. 1 translates into the bound through the “worst-case” diameter , which in general is much larger than the diameter . This dependency is due to the need of computing a lower bound to the reward accumulated by policies in the past (see Lem. 1). In fact, UCRL2 only needs to compute upper bounds on the gain and the value function returned by EVI by applying the optimistic Bellman operator has span bounded by the diameter . This is no longer the case for computing pessimistic estimates of the value of a policy. Whether Asm. 1 and the worst-case diameter are the unavoidable price to pay for conservative exploration in infinite horizon RL remains as an open question.

The finite-horizon case.

App. C shows how to modify UCB-VI (Azar et al., 2017) to satisfy the conservative condition in Eq. 8. In this setting, it is possible to show (see Prop. 1 in appendix) that the number of conservative episodes is simply logarithmic in . Formally, where , for all , and is the optimality gap. This problem dependent terms resemble the one in the bandit analysis. The regret of conservative UCB-VI is bounded by .

5 Experiments

In this section, we report results in the inventory control problem to illustrate the performance of CUCRL2 compared to unconstrained UCRL2 and how it varies with the conservative level. See App. D for additional experiments for both average reward and finite horizon. In order to have a better estimate of the budget, we re-evaluate past policies at each episode. We start considering the stochastic inventory control problem (Puterman, 1994, Sec. 3.2.1) with capacity and uniform demand. At the beginning of a month , the manager has to decide the number of items to order in order to satisfy the random demand, taking into account the cost of ordering and maintainance of the inventory (see App. D). Since the optimal policy is a threshold policy, as baseline we consider a policy (Puterman, 1994, Sec. 3.2.1) with target stock and capacity threshold . Note that and . We use this domain to perform an ablation study w.r.t. the conservative level . We have taken and the results are averaged over realizations.

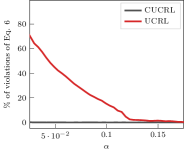

Fig. 2(left) shows that the regret of CUCRL2 grows at the same speed as the one of the baseline policy at the beginning (the conservative phase), because during this phase CUCRL2 is constrained to follow to make sure that constraint (7) is satisfied. Clearly, the duration of this conservative phase is proportional to the conservative level . As soon as CUCRL2 has built margin, it starts interleaving exploratory (optimistic) policies with the baseline. After this phase, CUCRL2 has learn enough about the system and has a sufficient margin to behave as UCRL2. As expected, Fig. 2(left) confirms that the convergence to the UCRL2 behavior happens more quickly for larger values of , i.e., when the conservative condition is relaxed and CUCRL2 can explore more freely. On the other hand, UCRL2 converges faster since it is agnostic to the safety constraint and may explore very poor policies in the initial phase. To better understand this condition, Fig. 2(right) shows the percentage of time the constraint was violated in the first steps (about of the overall time ). CUCRL2 always satisfies the constraint for all values of while UCRL2 fails a significant number of times, especially when the conditions is tight (small values of ).

6 Conclusion

We presented algorithms for conservative exploration for both finite horizon and average reward problems with regret. We have shown that the non-episodic nature of average reward problems makes the definition of the conservative condition much harder than in finite horizon problems. In both cases, we used a model-based approach to perform counterfactual reasoning required by the conservative condition. Recent papers have focused on model-free exploration in tabular settings or linear function approximation (Jin et al., 2018; Yang and Wang, 2019; Jin et al., 2019), thus a question is if it is possible for model-free algorithms to be conservative and still achieve regret.

References

- Achiam et al. (2017) Joshua Achiam, David Held, Aviv Tamar, and Pieter Abbeel. Constrained policy optimization. In ICML, volume 70 of Proceedings of Machine Learning Research, pages 22–31. PMLR, 2017.

- Altman (1999) Eitan Altman. Constrained Markov decision processes, volume 7. CRC Press, 1999.

- Auer et al. (2002) Peter Auer, Nicolo Cesa-Bianchi, and Paul Fischer. Finite-time analysis of the multiarmed bandit problem. Machine learning, 47(2-3):235–256, 2002.

- Azar et al. (2017) Mohammad Gheshlaghi Azar, Ian Osband, and Rémi Munos. Minimax regret bounds for reinforcement learning. In ICML, volume 70 of Proceedings of Machine Learning Research, pages 263–272. PMLR, 2017.

- Bartlett and Tewari (2009) Peter L. Bartlett and Ambuj Tewari. REGAL: A regularization based algorithm for reinforcement learning in weakly communicating MDPs. In UAI, pages 35–42. AUAI Press, 2009.

- Berkenkamp et al. (2017) Felix Berkenkamp, Matteo Turchetta, Angela P. Schoellig, and Andreas Krause. Safe model-based reinforcement learning with stability guarantees. In NIPS, pages 908–918, 2017.

- Bertsekas (1995) Dimitri P Bertsekas. Dynamic programming and optimal control. Vol II. Number 2. Athena scientific Belmont, MA, 1995.

- Bertsekas (2011) Dimitri P Bertsekas. Approximate policy iteration: A survey and some new methods. Journal of Control Theory and Applications, 9(3):310–335, 2011.

- Bottou et al. (2013) L. Bottou, J. Peters, J. Quinonero-Candela, D. Charles, D. Chickering, E. Portugaly, D. Ray, P. Simard, and E. Snelson. Counterfactual reasoning and learning systems: The example of computational advertising. Journal of Machine Learning Research, 14:3207–3260, 2013.

- Chow et al. (2018) Yinlam Chow, Ofir Nachum, Edgar A. Duéñez-Guzmán, and Mohammad Ghavamzadeh. A lyapunov-based approach to safe reinforcement learning. In NeurIPS, pages 8103–8112, 2018.

- Fruit et al. (2018a) Ronan Fruit, Matteo Pirotta, and Alessandro Lazaric. Near optimal exploration-exploitation in non-communicating markov decision processes. In NIPS, 2018a.

- Fruit et al. (2018b) Ronan Fruit, Matteo Pirotta, Alessandro Lazaric, and Ronald Ortner. Efficient bias-span-constrained exploration-exploitation in reinforcement learning. In ICML, Proceedings of Machine Learning Research. PMLR, 2018b.

- Gopalan and Mannor (2015) Aditya Gopalan and Shie Mannor. Thompson sampling for learning parameterized markov decision processes. In COLT, volume 40 of JMLR Workshop and Conference Proceedings, pages 861–898. JMLR.org, 2015.

- Jaksch et al. (2010) Thomas Jaksch, Ronald Ortner, and Peter Auer. Near-optimal regret bounds for reinforcement learning. Journal of Machine Learning Research, 11:1563–1600, 2010.

- Jin et al. (2018) Chi Jin, Zeyuan Allen-Zhu, Sébastien Bubeck, and Michael I. Jordan. Is q-learning provably efficient? CoRR, abs/1807.03765, 2018.

- Jin et al. (2019) Chi Jin, Zhuoran Yang, Zhaoran Wang, and Michael I. Jordan. Provably efficient reinforcement learning with linear function approximation. CoRR, abs/1907.05388, 2019.

- Kakade and Langford (2002) Sham M. Kakade and John Langford. Approximately optimal approximate reinforcement learning. In ICML, pages 267–274. Morgan Kaufmann, 2002.

- Katariya et al. (2019) Sumeet Katariya, Branislav Kveton, Zheng Wen, and Vamsi K. Potluru. Conservative exploration using interleaving. In AISTATS, volume 89 of Proceedings of Machine Learning Research, pages 954–963. PMLR, 2019.

- Kazerouni et al. (2017) Abbas Kazerouni, Mohammad Ghavamzadeh, Yasin Abbasi, and Benjamin Van Roy. Conservative contextual linear bandits. In NIPS, pages 3910–3919, 2017.

- Laroche et al. (2019) Romain Laroche, Paul Trichelair, and Remi Tachet des Combes. Safe policy improvement with baseline bootstrapping. In ICML, volume 97 of Proceedings of Machine Learning Research, pages 3652–3661. PMLR, 2019.

- Lazaric et al. (2019) Alessandro Lazaric, Matteo Pirotta, and Ronan Fruit. Regret minimization in infinite-horizon finite markov decision processes. Tutorial at ALT’19, 2019. URL https://rlgammazero.github.io/.

- Mansour et al. (2015) Yishay Mansour, Aleksandrs Slivkins, and Vasilis Syrgkanis. Bayesian incentive-compatible bandit exploration. In Proceedings of the Sixteenth ACM Conference on Economics and Computation, pages 565–582. ACM, 2015.

- Olde Keizer (2016) Minou Catharina Anselma Olde Keizer. Condition-based maintenance for complex systems: Coordinating maintenance and logistics planning for the process industries. PhD thesis, University of Groningen, 2016.

- Osband and Roy (2016) Ian Osband and Benjamin Van Roy. Posterior sampling for reinforcement learning without episodes. CoRR, abs/1608.02731, 2016.

- Ouyang et al. (2017) Yi Ouyang, Mukul Gagrani, Ashutosh Nayyar, and Rahul Jain. Learning unknown markov decision processes: A thompson sampling approach. In NIPS, pages 1333–1342, 2017.

- Petrik et al. (2016) M. Petrik, M. Ghavamzadeh, and Y. Chow. Safe policy improvement by minimizing robust baseline regret. In Advances in Neural Information Processing Systems, pages 2298–2306, 2016.

- Pirotta et al. (2013a) Matteo Pirotta, Marcello Restelli, and Luca Bascetta. Adaptive step-size for policy gradient methods. In NIPS, pages 1394–1402, 2013a.

- Pirotta et al. (2013b) Matteo Pirotta, Marcello Restelli, Alessio Pecorino, and Daniele Calandriello. Safe policy iteration. In ICML (3), volume 28 of JMLR Workshop and Conference Proceedings, pages 307–315. JMLR.org, 2013b.

- Puterman (1994) Martin L. Puterman. Markov Decision Processes: Discrete Stochastic Dynamic Programming. John Wiley & Sons, Inc., New York, NY, USA, 1994. ISBN 0471619779.

- Simão and Spaan (2019) Thiago D. Simão and Matthijs T. J. Spaan. Safe policy improvement with baseline bootstrapping in factored environments. In AAAI, pages 4967–4974. AAAI Press, 2019.

- Swaminathan and Joachims (2015) A. Swaminathan and T. Joachims. Counterfactual risk minimization: Learning from logged bandit feedback. In Proceedings of The 32nd International Conference on Machine Learning, 2015.

- Thomas et al. (2015a) P. Thomas, G. Theocharous, and M. Ghavamzadeh. High confidence off-policy evaluation. In Proceedings of the Twenty-Ninth Conference on Artificial Intelligence, 2015a.

- Thomas et al. (2015b) P. Thomas, G. Theocharous, and M. Ghavamzadeh. High confidence policy improvement. In Proceedings of the Thirty-Second International Conference on Machine Learning, pages 2380–2388, 2015b.

- Wu et al. (2016) Yifan Wu, Roshan Shariff, Tor Lattimore, and Csaba Szepesvári. Conservative bandits. In ICML, volume 48 of JMLR Workshop and Conference Proceedings, pages 1254–1262. JMLR.org, 2016.

- Yang and Wang (2019) Lin F. Yang and Mengdi Wang. Reinforcement leaning in feature space: Matrix bandit, kernels, and regret bound. CoRR, abs/1905.10389, 2019.

- Zanette and Brunskill (2019) Andrea Zanette and Emma Brunskill. Tighter problem-dependent regret bounds in reinforcement learning without domain knowledge using value function bounds. In ICML, volume 97 of Proceedings of Machine Learning Research, pages 7304–7312. PMLR, 2019.

Appendix A Policy Evaluation with Uncertainties

Input: Operator and accuracy Set , , 1. While do (a) (b) 2. Return: and

Consider a bounded parameter MDP defined by a compact set and :

| (16) |

In this paper, we consider confidence sets and that are polytopes. We are interested in building a pessimistic (robust) estimate of the performance of a policy in . This robust optimization problem can be written as:

| (17) |

where is the gain of policy in the MDP . Lemma 5 shows that there exists a solution to this problem that can be computed using EVI when the set contains an ergodic MDP.

We recall that any bounded parameter MDP admits an equivalent representation as an extended MDP (Jaksch et al., 2010) with identical state space but compact action space. For a deterministic policy , the extended (pessimistic) Bellman operator is defined as:

| (18) |

Lemma 5.

Let be a bounded-parameter MDP defined as in Eq. 16 such that exists an ergodic MDP w.h.p. Consider a policy , then:

-

1.

There exists a tuple such that:

where is the Bellman operator of the extended MDP associated to (see Eq. 18).

-

2.

In addition, we have the following inequalities on the pair :

where is the expectation of using policy in the MDP and is the minimal number of steps to reach state .

Proof.

Point 1. We show that this policy evaluation problem is equivalent to a planning problem in an extended MDP with negative reward. Consider the extended MDP such that . For any state and action ,

Denote by the optimal Bellman operator of . Since and are polytopes, can be interpreted as an optimal Bellman operator with finite number of actions. A sufficient condition for the existence of a solution of the optimality equations is that the MDP is weakly communicating (Puterman, 1994, Chap. 8-9). Note that contains the model defined by , i.e., the Markov chain induced by in .777We abuse of language since is not formally a set. We should formally refer to the bounded parameter MDP associated to , i.e., built considering and . Note that w.h.p. Since is ergodic, is at least communicating and thus converges to a solution of the optimality equations. Extended value iteration (Jaksch et al., 2010) on converges toward a gain and bias such that:

By rearranging, we have that:

Thus follows that and . This shows the relationship between maximizing over policies in the extended MDP and minimizing over the set of models induced by .

Point 2. Let’s begin by bounding the span of the bias . Thanks to Theorem of Bartlett and Tewari (2009), we have that the span of is upper-bounded by the diameter of the extended MDP , i.e:

where is the expectation of using policy in the extended MDP and is the hitting time of state . But let’s define the policy in the extended MDP such that for a state , it chooses the action:

with and the true parameter of the MDP , this is possible because w.h.p the MDP with the Markov chain induced by using policy in the MDP . Thus for any pair of states :

with the expectation of using policy in the MDP . Therefore:

And because is assumed to be ergodic.

Let’s show that the gain is a lower bound on the gain of the policy in the MDP . Indeed, because the operator converges toward solution of the optimality equations for negative rewards, we have that, see (Puterman, 1994, Th. 8.4.1):

because reversing the sign of the rewards in the MDP changes the sign of the gain of a policy. Thus, . ∎

As a consequence, we can use EVI on to compute a solution for problem 17. EVI generates a sequence of vectors such that and . If the algorithm is stopped when we have (Puterman, 1994, Sec. 8.3.1) that:

| (19) |

where and . The following lemma shows how we can use the value produced by EVI to lower bound the expected sum of rewards under a policy .

Lemma 6.

Let the values computed by EVI using and an accuracy . Then, the cumulative reward collected by policy in after steps can be lower bounded by:

In addition,

Proof.

Using the inequalities in (19) we can write that:

since and w.h.p. By iterating this inequality, we get that for all and state :

The statement follows by noticing that

The last statement is a direct consequence of the argument developed in section of Jaksch et al. (2010). This reasoning relies on the fact that the initial vector used in EVI is a zero span vector. ∎

Appendix B Regret Bound for CUCRL

Lemma 7.

The regret of CUCRL2 can be upper-bounded for some , with probability at least , by:

Proof.

Recall that is the episode at time and that the regret is defined as .

Since the baseline policy may be stochastic, as a first step we replace the observed reward by its expectation. As done in (Fruit et al., 2018b) we use Azuma’s inequality that gives, with probability at least :

| (20) |

We denote by the set of episodes where the algorithm played an UCRL policy. Note that we cannot directly consider since the set is updated at the end of the episode and the last episode may not have ended at . Similarly we denote by . Then, the regret of CUCRL2 can be decomposed as follow:

| (21) | ||||

Moreover, note that the UCRL2 policy is deterministic so we hate that when . The second term, denoted , is the regret suffered by UCRL2 over steps. The only difference with the orginal analysis (Jaksch et al., 2010) is that the confidence intervals used by UCRL are updated when using the baseline policy, however it does not affect the regret of UCRL because it only means the confidence intervals used shrinks faster for some state-action pairs. We will analyze this term in Lem. 9. To decompose we can use the Bellman equations ():

But, can be bounded using a telescopic sum argument and the number of episodes:

Then it is easy to see that is a Martingale Difference Sequence with respect to the filtration which is generated by all the randomness in the environment and in the algorithm up until time : and . Thus with probability :

Therefore putting all the above together, we have that with probability at least :

As shown in (Ouyang et al., 2017, Lem. 1), thus we can simply write that . ∎

In the next lemma, we bound the total number of steps where CUCRL2 used the baseline policy.

Lemma 8.

For any, , the total length of episodes where the baseline policy is played by CUCRL after steps is upper-bounded with probability by:

with a logarithmic term in .

Proof.

Let be the last episode played conservatively: . At the beginning of episode the conservative condition is not verified that is to say:

| (22) |

Let’s proceeding by analysing each term on the RHS of Eq. B. First, we have that , thus:

| (23) |

On the other hand, thanks to Lem. 6, we have:

| (24) |

Before analysing , let’s bound the contribution of episode :

| (25) |

where we used the fact that for all episode , we have . Indeed the dynamic episode condition is such that for an episode , thus by iterating this inequality, . At this point using equations B, 24 and 25 we have:

Let’s finish by analysing . Let’s define the event, , by definition of and , , see (Lazaric et al., 2019, App. B.2) for a complete proof. We have that on the event , for any , is such that (see App. A) where is the true gain: . Thus, since :

where is the optimistic gain at episode (see Lazaric et al. (2019)) thus the last inequality comes from for every episode . We can also define the optimistic bias at episode , , the pair is such that:

Recall that is the optimistic policy at episode and when , . Then, by using Bellman equations:

where is the transition probability of the true MDP, . By a simple telescopic sum argument, we have:

At this point we need to explicitly define the concentration inequality used to construct the confidence sets and . For every , we define such that:

where is the empirical average of the reward received when visiting the state-action pairs at the beginning of episode . For every , we define as:

with is the empirical average of the observed transitions. Choosing those and is done thanks to concentration inequalities such that event holds with high enough probability. In the following, we use:

where . For other choices of and refer to (Lazaric et al., 2019). Similarly to what done in (Jaksch et al., 2010, Sec. 4.3.1 and 4.3.2), by using Holder’s inequality and recentering the bias functions, we write:

To finish, the proof of this lemma, we need to bound the term and . In the following, we use the fact that (see Lem. 6) and again that . Let’s begin with , by definition of the radius of the confidence sets, we have:

and,

The second term is easy to bound because it is a Martingale Difference Sequence with respect to the filtration generated by all the randomness in the algorithm and the environment before the current step. For any time , the -algebra generated by the history up to time included is . Define with . Since is measurable, and . Then is an MDS and nothing change compared to the analysis of UCRL2. Therefore using Azuma-Hoeffding inequality, we have, with probability that:

Algorithmically, it is possible to evaluate the gain of the policies played in the past episodes at the beginning of the current episode. While this will provide a better estimate for the conservative condition, it will break the MDS structure in (b) since will be not measurable w.r.t. since it is computed with samples collected after episode . Thus putting the bound for and together, we have:

That is to say,

Rearranging the terms and calling , we have:

We have a quadratic equation and thus:

Therefore, as is the last episode where CUCRL2 played the policy , we have . Also, because of the condition on the length of an episode for every , therefore:

∎

The following lemma states the regret of the UCRL2 algorithm conditioned on running only the episodes in the set .

Lemma 9.

For any , we have that after , the regret of UCRL2 is upper bounded with probability at least by:

with a numerical constant.

Proof.

The same type of bound has been shown in numerous work before Jaksch et al. (2010); Lazaric et al. (2019), however the proof presented in those works can not be readily applied to our setting. Indeed, when the algorithm chooses to play the baseline policy for an episode, then the confidence sets used in CUCRL2 are updated for the state-action pairs encountered during this episode. However, in the classic proof for the UCRL2 algorithm the confidence sets are the same between the end of one episode and the beginning of the next one are the same. This may not be the case for CUCRL2.

Fortunately, when using the baseline policy during an episode, the confidence sets for every state-action pairs are either the same as the previous episode or are becoming tighter around the true parameters of the MDP . Thus, proving Lemma 9 is similar to the proof presented in Lazaric et al. (2019), the only difference resides in bounding the sum, , which is bounded by the square root of the total number of samples in the proof of Lazaric et al. (2019) whereas in the case CUCRL2 it is bounded by the square root of the total number of samples gathered while exploring the set of policies plus the number of samples collected while playing the baseline policies. Therefore, at the end of the day both quantities are bounded by a constant times the square root of .

A doubt someone could have is on controlling the term

For any time , the -algebra generated by the history up to time included is . Define . Since is measurable, and . Then is an MDS and nothing change compared to the analysis of UCRL2.

∎

Appendix C Conservative Exploration in Finite Horizon Markov Decision Processes

In this section, we show how the conservative setting can be applied to finite horizon MDPs. Let’s consider a finite-horizon MDP (Puterman, 1994, Chp. 4) with state space and action space . Every state-action pair is characterized by a reward distribution with mean and support in and a transition distribution over next state. We denote by and the number of states and actions, and by the horizon of an episode. A Markov randomized decision rule maps states to distributions over actions. A policy is a sequence of decision rules, i.e., . We denote by (resp. ) the set of Markov randomized (resp. deterministic) policies. The value of a policy is measured trough the value function

where the expectation is defined w.r.t. the model and policy (i.e., ). This function gives the expected total reward that one could get by following policy starting in state , at time . There exists an optimal policy (Puterman, 1994, Sec. 4.4) for which satisfies the optimality equations:

| (26) |

where for any state . The value function can be computed using backward induction (e.g., Puterman, 1994; Bertsekas, 1995) when the reward and transitions are known. Given a policy , the associated value function satisfies the evaluation equations . The optimal policy is thus defined as , .

In the following we assume that the learning agent known , and , while the reward and dynamics are unknown and need to be estimated online. Given a finite number of episode , we evaluate the performance of a learning algorithm by its cumulative regret

where is the policy executed by the algorithm at episode .

Conservative Condition

Designing a conservative condition, in this setting is much easier than in the average reward case as evaluating a policy can be done through the value function which gives an estimation of the expected reward over an episode. Thus, we can use this evaluation of a policy to use in place of rewards in the bandits condition. Formally, denote by the baseline policy and assume that is known. In general, this assumption is not restrictive since the baseline performance can be estimated from historical data. Given a conservative level , we define the conservative condition as:

| (27) |

where is the policy executed by the algorithm at episode and is the starting state of episode before policy is chosen. The initial state can be chosen arbitrarily but should be revealed at the beginning of each episode. Note that this condition is random due the choice of the policies and also because of the starting states thus the condition is required to hold with high probability.

Note that Eq. 27 requires to evaluated the performance of policy on the true (unknown) MDP. In order derive a practical condition, we need to construct an estimate of . In order to be conservative, we are interesting in deriving a lower bound on the value function of a generic policy which can be used in Eq. 27.

Pessimistic value function estimate.

We recall that OFU algorithms (e.g., UCB-VI and EULER) builds uncertainties around the rewards and dynamics that are used to perform an optimistic planning. Formally, denote by and the empirical transitions and rewards at episode . Then, with high probability

for all and . This uncertainties are used to compute an exploration bonus that can be used to compute an optimistic estimate of the optimal value function. Formally, at episode , optimistic backward induction (e.g., Azar et al., 2017, Alg. 2) computes an estimate value function such that for any state . The same approach can be used to compute a pessimistic estimate of the optimal value function by subtracting the exploration bonus to the reward (e.g., Zanette and Brunskill, 2019).

The only difference in the conservative setting is that we are interesting to compute a pessimistic estimate for a policy different from the optimal one. We thus define the pessimistic evaluation equations for any episode , step , state and policy as:

| (28) |

with for all states . This value function is pessimistic (see Lem. 10) and can be computed using backward induction with .

Lemma 10.

Let and be the value function given by backward induction using Eq. 28 then with high probability:

Proof.

On the event that the concentration inequalities holds, let be the empirical reward at episode and the empirical distribution over the next state from at episode . We proceed with a backward induction. At time the statement is true. For :

where the first inequality is true because of the confidence intervals on the reward function and the penultimate inequality is true because of the backward induction hypothesis. ∎

Thanks to this result, we can formulate a condition that the algorithm can check, at the beginning of episode to decide if a policy is safe to play or not :

| (29) |

where is the set of episodes where the algorithm previously played non-conservatively, is the set of episodes played conservatively and is the policies that the OFU algorithm (e.g., UCB-VI) would execute without the conservative constraint.

Input: Policy , , , , , , Initialization: Set , and For episodes do 1. Compute optimistic policy using any OFU algorithm on history . 2. Compute pessimistic estimate as in Eq. 28. 3. if Equation (29) not verified: then (a) , and else: (a) and 4. for do (a) Execute , obtain reward , and observe . (b) if then: add to

Alg. 4 shows the generic structure of any conservative exploration algorithm for MDPs. First, it computes an optimistic policy by leveraging on an OFU algorithm and the collected history. Then it checks the conservative condition. When Eq. 29 is verified it plays the optimistic policy otherwise it plays conservatively by executing policy . This allows to build some budget for playing exploratory actions in the future.

Regret Guarantees

We analyse Alg. 4 with UCB-VI. Before to introduce the upper-bound to the regret of CUCB-VI we introduce the following assumption on the baseline policy.

Assumption 3.

The baseline policy is such that .

We can now state the main results:

Proposition 1.

For , the regret of conservative UCB-VI (CUCB-VI) is upper-bounded with probability at least by:

| (30) |

where and .

Proof.

Let’s define the high probability event, , that is such that in this event, all the concentration inequalities holds and the Martingale Difference Sequence concentration inequalities also holds :

and finally, , then holds with probability at least . Indeed,

Under this event, we have that for all episode :

where is a martingale difference sequence with respect to the filtration that is generated by all the randomness before step of episode . Indeed, for an episode , let , decomposing into successive decision rules.

Thus by defining, , we have :

But let’s define then is a Martingale Difference Sequence with respect to the filtration which is generated by all the randomness in the environment and the algorithm before step of episode . Then, by recursion, we have :

The regret of algorithm CUCB-VI can be decomposed as :

where . Therefore bounding the regret amounts to bound the number of episode played conservatively. To do so, let’s consider, the last episode played conservatively, then before the beginning of episode , the condition 29 is not verified and thus :

Thus, let’s finish this analysis by bounding for all . But:

where . Now, we need to bound the sum over all the non-conservative episodes of the difference between the optimistic and pessimistic value function. That is to say :

Also :

and, under the event , . On the other hand, for the episode , we can only bound the difference in value function by . Finally, we have that and thus if we assume that :

Thus, the function on the RHS in bounded and using lemma of Kazerouni et al. (2017), we have :

But by definition, . Hence the result. ∎

Experiments

Finally, we end this presentation of conservativeness in finite horizon MDPs with some experiments. We consider a classic gridworld problem with one goal state, a starting state and one trap state, we set , and the reward of any action in all the state to , the reward in the goal state to and the reward of falling in the trapping state to . We normalize the rewards to be in . The baseline policy is describing a path around the pit, see Fig 5.

On the two position adjacent to the goal the baseline policy is stochastic with a probability of reaching the goal of for the position on the right of the goal and below the goal, respectively. On the last line the probability of going up or right is also uniform. Figure 6 shows the impact of the conservative constraint on the regret of UCB-VI for a conservative coefficient . Fig 6 also shows the constraint as a function of the time for UCB-VI and CUCB-VI that is to say: as a function of episode with the starting state of the gridworld. In the first episodes (i.e until episode ) the condition was violated by UCB-VI of the time.

Appendix D Experiments

For average reward problems we consider “simplified” Bernstein confidence intervals given by:

where , is the empirical standard deviation and .

D.1 Single-Product Stochastic Inventory Control

Maintaining inventories is necessary for any company dealing with physical products. We consider the case of single product without backlogging. The state space is the amount of products in the inventory, where is the maximum capacity. Given the state at the beginning of the month, the manager (agent) has to decide the amount of units to order. We define to be the random demand of month and we assume a time-homogeneous probability distribution for the demand. The inventory at time is given by

The action space is . As in (Puterman, 1994), we assume a fixed cost for placing orders and a varible cost that increases with the quantity ordered: . The cost of maintaining an inventory of items is defined by the nondecreasing function . If the inventory is available to meet a demand , the agent receives a revenue of . The reward is thus defined as . In the experiments, we use , , and .

In all the experiments, we normalize rewards such that the support is in and we use noise proportional to the reward mean: where (we set ).

D.2 Cost-Based Maintenance

The system is composed by components in an active redundant, parallel setting, which are subject to economic and stochastic dependence through load sharing. Each component is described by its operational level . The level denotes that the component has failed. The deterioration process is modelled using a Poisson process. If all components have failed, the system is shut down and a penalty cost is paid. The replacement of a failed component cost , while the same operation on an active component cost (usually ). There is also a fixed cost for maintenance . At each time step, it is possible to replace simultaneously multiple components. Please refer to (Olde Keizer, 2016) for a complete description of dynamics and rewards.

We terminate the analysis of CUCRL2 with a more challenging test. We consider the condition-based maintenance problem (CBM, Olde Keizer, 2016) a multi-component system subject to structural, economic and stochastic dependences. We report a complete description of the problem in App. D. The resulting MDP has states and actions. The maintenance policy is often implemented as a threshold policy based on the deterioration level. Such a threshold policy is not necessarily optimal for a system with economic dependence and redundancy. We simulate this scenario by considering a strong (almost optimal) threshold policy for CBM without economic dependence as baseline. We make it stochastic by selecting with probability a random action. As a result we have that the optimal gain while the baseline gain is . Fig. 7 shows the cumulative regret for UCRL2 and CUCRL2 with . UCRL2 explores faster than CUCRL2 but violates the conservative condition of times in the initial phase (up to ), incurring in multiple complete system failures. On the other hand, CUCRL2 never violates the conservative condition.