Sparse Covariance Estimation in Logit Mixture Models

Abstract

This paper introduces a new data-driven methodology for estimating sparse covariance matrices of the random coefficients in logit mixture models. Researchers typically specify covariance matrices in logit mixture models under one of two extreme assumptions: either an unrestricted full covariance matrix (allowing correlations between all random coefficients), or a restricted diagonal matrix (allowing no correlations at all). Our objective is to find optimal subsets of correlated coefficients for which we estimate covariances. We propose a new estimator, called MISC, that uses a mixed-integer optimization (MIO) program to find an optimal block diagonal structure specification for the covariance matrix, corresponding to subsets of correlated coefficients, for any desired sparsity level using Markov Chain Monte Carlo (MCMC) posterior draws from the unrestricted full covariance matrix. The optimal sparsity level of the covariance matrix is determined using out-of-sample validation. We demonstrate the ability of MISC to correctly recover the true covariance structure from synthetic data. In an empirical illustration using a stated preference survey on modes of transportation, we use MISC to obtain a sparse covariance matrix indicating how preferences for attributes are related to one another.

keywords:

Discrete Choice, Logit Mixture Models, Sparse Covariance Estimation, Algorithmic Model Selection, Machine LearningcaptionUnsupported document class

1 Introduction

The logit mixture model, also called the mixed logit model, is widely considered to be the most promising state of the art discrete choice model; see Hensher and Greene (2003). In a seminal paper, McFadden and Train (2000) show that under some mild regularity conditions any discrete choice model that is consistent with random utility maximization has choice probabilities that can be approximated, up to any desired precision, by a logit mixture model through a right choice of explanatory variables and distributions for the random coefficients. The logit mixture model enables the modelling of preference heterogeneity by allowing the model’s coefficients to be randomly distributed across the population under study; see Chapter 6 of Train (2009).

In specifying a logit mixture model, the researcher makes assumptions on the distribution of the model’s coefficients (called the mixing distribution) and on the structure of the covariance matrix. For example, for normally distributed coefficients , the researcher decides which, if any, covariance matrix elements to estimate and which ones to constrain to zero. Typically, the researcher compares goodness-of-fit statistics on a few competing hypotheses on the structure of the covariance matrix (usually full against diagonal covariance matrix). As the number of all possible covariance matrix specifications grows super-exponentially with the number of distributed coefficients, it is not practically feasible for the researcher to comprehensively compare all possible specifications of the covariance matrix in order to determine an optimal specification to use.111If there are random coefficients in a mixed logit model, the number of different covariance matrix specifications corresponding to mutually exclusive and collectively exhaustive subsets of correlated coefficients can be determined by counting the number of ways a set of elements can be partitioned into non-empty subsets. This is given by the Bell numbers (Aigner, 1999). The first few Bell numbers are .

In this paper, we introduce an algorithmic estimation procedure that discovers the best block diagonal covariance matrix specification, corresponding to subsets of correlated coefficients, directly from the data.

Parsimonious specifications of the covariance matrix are desirable since the number of covariance elements grows quadratically with the number of distributed coefficients. Consequently, sparser models provide efficiency gains in the estimation process compared to estimating a full covariance matrix. James (2018) demonstrates, on an empirical application, that sparser representations of the covariance matrix provide a better fit on the data than a fully unrestricted model as measured by BIC or AIC. James (2018) proposed a factor structured covariance approach to cast the covariances into a lower dimensional representation of latent factors. Keane and Wasi (2013) compared different logit mixture specifications with full, diagonal, and restricted covariance matrices and concluded that a full covariance matrix is not justified by the data in many cases, and that different specifications of the covariance matrix fit best on different datasets.

On the other hand, Hess et al. (2017) shows that ignoring statistically significant correlations between the distributed coefficients can distort the estimated distribution of ratios of coefficients, representing the values of willingness-to-pay (WTP) and marginal rates of substitution. Several studies including Hess and Train (2017), Kipperberg et al. (2008), Scarpa et al. (2008), Revelt and Train (1998), and Train (1998) have found statistically significant correlations between coefficients in logit mixture models on a number of empirical applications.

The conclusion is that, in general, researchers cannot know, without testing, which restrictions to impose.

In this paper, we propose a new methodology for learning the structure of the covariance matrix in logit mixture models with a normal mixing distribution (or transformations of the normal distribution such as the log-normal or Johnson SB distributions) from the data. In particular, we are interested in algorithmically identifying optimal subsets of correlated coefficients for which we estimate covariances. This corresponds to a block diagonal specification of the covariance matrix. We build on ideas from the mixed-integer optimization (MIO) framework for variable selection in linear regression models developed by Bertsimas et al. (2016), the Hierarchical Bayes (HB) estimator for logit mixture models, (see Allenby, 1997, Allenby and Rossi, 1998, and Train, 2009), and its extension to block diagonal covariance matrices by Becker (2016). We discuss practical extensions of our proposed methodology to cases where some of the coefficients are distributed while others are fixed, latent-class logit mixture models, and logit mixtures with inter- and intra-consumer heterogeneity.

The remainder of this paper is organised as follows. Section 2 presents a brief background on covariance estimation in logit mixture models, sparse covariance matrix estimation in statistics, and the use of mixed-integer programming in model selection. Section 3 presents the proposed methodology for learning the covariance structure in logit mixture models and forms the core methodological contribution of this paper. Section 4 presents Monte Carlo simulations to validate our proposed methodology, in addition to an empirical application. Section 5 discusses the extensions of our proposed methodology mentioned above. Section 6 concludes the paper.

2 Background

This section provides an overview of covariance matrix estimation in logit mixture models, the problem of estimating sparse covariance matrices in statistics, and the motivation for using a mixed-integer programming approach to select an optimal covariance matrix specification.

2.1 Covariance Matrix Estimation in Choice Models

We consider the logit mixture model with the utility specification shown in equation (2.1). The indices used are for individuals, for choice situations (or “menus”), and for alternatives.

| (2.1) |

is individual ’s unobserved utility of alternative in choice situation , is the systematic utility function, is a vector of explanatory variables (e.g. attributes of the alternatives and characteristics of the individual), is a vector of individual-specific coefficients, and is an error term following the extreme value distribution with zero mean and unit scale. The researcher specifies a distribution for the coefficients and estimates the parameters of that distribution. Typically, a normal or log-normal distribution is specified; see Ben-Akiva et al. (1997) and Revelt and Train (1998). We assume that is normally distributed in the population with mean and covariance matrix . The ’s represent the preferences or tastes of individual decision-makers.

| (2.2) |

Exponentiation of coefficients in the utility equations is used when a particular coefficient is known to have the same sign across the population of decision-makers (e.g. a negative sign for a price coefficient) – this is equivalent to specifying a log-normal distribution for said coefficient.

The researcher estimates and . The matrix represents the covariance structure of the individual-specific coefficients. The variances on the diagonal elements reflect the magnitude of heterogeneity in these coefficients in the population, and the off-diagonal elements represent covariances between these coefficients– indicating that preferences for one attribute are related to their preferences for another attribute; see Hess and Train (2017).

Conditional on , the probability of selecting alternative can be expressed as:

| (2.3) |

The individual-specific coefficients are random, and the unconditional probability of choice is obtained by integrating over the mixing distribution of these coefficients (which we assume to be normal).

| (2.4) |

The model’s parameters, and , can be estimated using Maximum Simulated Likelihood (MSL). This requires integration over a multidimensional distribution. Most applications using MSL for model estimation assume a diagonal covariance matrix specification, due to the computational constraints that manifest through the so-called “curse of dimensionality”: the number of draws required for simulation increases exponentially with the number of variables, making estimation highly intractable; see Guevara et al. (2009) and Cherchi and Guevara (2012).

Train and

Sonnier (2005) show that Bayesian methods for estimating the logit mixture model, such as Markov Chain Monte Carlo (MCMC), are less susceptible to the “curse of dimensionality”. The most commonly used estimation method of logit mixtures is an Hierarchical Bayes (HB) estimator; see Allenby (1997), Allenby and

Rossi (1998), and Train (2009). This estimator is based on a three-step Gibbs sampler with an embedded Metropolis-Hastings algorithm which we describe below:

Becker (2016) extended the three-step Gibbs-sampler (Algorithm 1) to allow for a block diagonal covariance structure specification. The covariance matrix is divided into mutually exclusive blocks, and each block is updated separately in step 2 of Algorithm 1. All of the off-diagonal elements that do not belong to any of the blocks are not estimated and constrained to zero.

Inferring a parsimonious covariance structure from the data has not yet been addressed in the literature on logit mixture models. On the other hand, several methods appear in the statistics literature dedicated to estimating sparse covariance matrices.

2.2 Sparse Covariance Matrix Estimation

In statistics, the covariance selection problem, introduced by Dempster (1972), involves setting some of the elements of the covariance matrix (or its inverse, the concentration matrix) to zero. Several approaches have been developed to achieve parsimonious specifications of the covariance matrix. These mainly fall into one of two categories. The first approach involves traditional multiple hypotheses testing. The relevant papers belonging to this approach include Knuiman (1978), Porteous (1985), Drton and Perlman (2004), Drton et al. (2007), and Drton and Perlman (2008). The second approach uses a LASSO penalty ( norm) to achieve model selection and estimation simultaneously. The implementation of the penalty methods, however, is nontrivial because of the positive definite constraint on the covariance (or concentration) matrix; see Yuan and Lin (2007).

Yuan and Lin (2007) proposed a penalized likelihood method for model selection and parameter estimation simultaneously using an penalty on the off-diagonal elements. The “maxdet” interior point algorithm from Vandenberghe et al. (1998) is used, and a BIC-type criterion is adopted for the selection of the tuning parameter. A similar approach was taken by Banerjee et al. (2008), and Dahl et al. (2008). Meinshausen et al. (2006) suggested fitting a LASSO model to each variable, using others as predictors. This was later enhanced by Friedman et al. (2008) who proposed a fast algorithm that cycles through the variables, and fits a modified lasso regression to each variable.

In the Bayesian context, Khondker et al. (2013) introduced the Bayesian Covariance Lasso (BCLASSO), which uses exponential priors on the diagonal elements and double exponential (Laplace) priors on the off-diagonal elements of the concentration matrix. The authors used Gibbs sampling to draw from the diagonal elements (since their full conditionals are available in closed form), and the standard Metropolis-Hastings algorithm for sampling from the off-diagonal elements.

Wang et al. (2012) proposed a similar Bayesian estimator with similar priors (exponential priors for the diagonal elements and double exponential priors for the off-diagonal elements). Data augmentation was used to develop a more efficient block Gibbs sampler, which updates one column and row of the concentration matrix at a time.

In both of the Bayesian covariance LASSO methods by Wang et al. (2012) and Khondker et al. (2013) described above, the estimator does not set any of the covariance matrix entries exactly to zero, instead it generates draws that are concentrated around zero. To distinguish between zero and non-zero elements, Wang et al. (2012) suggests using the thresholding approach recommended by Carvalho et al. (2010), which compares the relative magnitudes of the penalized and non-penalized estimates. Alternatively, Khondker et al. (2013) recommends using “credible regions” based on confidence intervals of the estimates. However, the choice of the significance level is somewhat arbitrary, and coupled with the choice of the penalty itself.

There are fundamental limitations associated with the direct application of the LASSO methods just described to the logit mixture context. First, LASSO penalties penalize larger coefficients more than smaller ones. This is not desirable when estimating behavioural models, as this might result in underestimating the magnitude of heterogeneity in the population. In addition, LASSO methods not only set some covariance elements to zero, but also shrink the non-zero covariances towards zero. The estimated non-zero variances and covariances will clearly be biased, and it is not clear how a post-LASSO type methodology, (e.g. Belloni et al., 2013), can be applied to the logit mixture context. In contrast, our proposed mixed-integer programming methodology finds the optimal locations of zeros in the covariance matrix without penalizing the non-zero covariances during the estimation process.

2.3 The Mixed-Integer Programming Approach

The problem of deciding which subsets of the distributed variables are potentially correlated (or equivalently specifying the structure of the covariance matrix to be estimated) naturally admits an integer programming formulation. A covariance element is either estimated or restricted to zero. Each of these decisions is represented by a binary decision variable in the formulation we introduce in Section 3. Making a decision on which covariances to estimate has an effect on information loss in the covariance matrix and on the likelihood, and deciding which covariances to estimate requires balancing information loss and sparsity. We solidify these ideas in the next section.

As described in Section 2.1, Algorithm 1 can be easily modified to draw from block diagonal matrices; see Becker (2016). Estimating general covariance matrix structures is technically possible through the Metropolis-Hastings algorithm, but with much added computational cost. We therefore restrict the decisions on which covariances to estimate and which to constrain to zero so that the resulting covariance matrix structure is block diagonal. The covariance elements restricted to zero are not estimated, all other elements of the covariance matrix are estimated without penalty. This is in contrast to the LASSO-type methodologies which also penalize all the covariance matrix elements leading to possible bias in the estimated values.

Mixed-integer optimization (MIO) problems are NP-hard, which means that, in general, finding a “certificate of optimality” in a reasonable amount of time cannot be guaranteed; see Bertsimas and Tsitsiklis (1997). However, massive developments in the state of the art solvers’ ability to solve large scale MIO problems has enabled recent successes in applying MIO methods to statistical problems such as best subset selection Bertsimas et al. (2016). Bertsimas et al. (2016) show that mixed-integer programming can be used to solve the best variable subset selection problem in linear regression for much larger problem sizes than what was thought possible. Bertsimas and Dunn (2017) find optimal classification trees using an MIO formulation. Aboutaleb (2019) used mixed-integer and non-convex programming techniques to find an optimal specification for nested logit models. We find that the MIO solution times in our proposed methodology take up only a small fraction of the total estimation time, with the Bayesian MCMC procedure taking up the bulk of the estimation time.

3 Methodology

This section develops our proposed methodology for estimating an optimal covariance structure in logit mixture models. Our goal is to algorithmically find optimal subsets of the distributed coefficients for which we estimate covariances.

3.1 Optimization Problem

Let be a set of MCMC posterior draws from an unrestricted (full) covariance matrix (i.e. all the covariances are estimated), and let be a sparse block-diagonal representation of the matrix . In representing by a sparse matrix , there is invariably some loss of information. This is represented by the following equation:

| (3.1) |

where the matrix is the loss matrix. The problem of interest is to find the optimal balance between information, as represented by , and loss as represented . In this section, we formulate this problem as a mixed-integer optimization problem with a quadratic objective and linear constraints. We first begin with some necessary definitions.

Definition 3.1

A square matrix M is block diagonal if its diagonal elements are square matrices of any size (possibly even ), and the off-diagonal terms are zero. Formally, M is block diagonal if there exists square matrices such that . Where the direct sum of any pair of matrices is given as a matrix of size defined as:

and the boldface zeros are blocks of zeros i.e., zero matrices.

Any square matrix can be trivially considered to be block diagonal with one block. Each of the square matrices on the diagonal elements of the matrix M represents the covariance matrix of a subset of correlated coefficients. There can be as many blocks as there are rows or columns in the original matrix M (if all the blocks are matrices).

Block diagonal matrices are restrictive in the sense that the property is dependent on the particular ordering or indices of the distributed coefficients– which is somewhat arbitrary. We would like to relax this restriction by introducing the notion of a permutation independent block diagonal matrix.

Definition 3.2

A square matrix M is pseudo block diagonal (PBD) if there exists a permutation of its indices such that the index-permuted matrix is block diagonal.

Note that this definition is not standard in the literature, but is necessary for our exposition. By this definition, any block diagonal matrix is trivially PBD.

We restrict our attention to PBD matrices, for two reasons. First, the three-step Gibbs-sampler (Algorithm 1) can be easily modified to draw from block diagonal matrices (Becker, 2016) and by trivial extension to PBD matrices through a simple permutation of indices. The second reason is that blocks in PBD matrices naturally correspond to a partition of the correlated coefficients which are arguably more interpretable than general covariance matrices.

At a high level, the problem of finding an optimal sparse representation of the matrix can be written as follows:

| (3.2) | ||||

| (3.3) | ||||

| (3.4) | ||||

| (3.5) |

where (the so-called norm) is the number of non-zero elements in the matrix .333Technically speaking, the norm is not a proper norm because it is not homogeneous. Nevertheless, this non-zero counting “norm” appears in the statistics literature. is a parameter that is determined through cross-validation.

Constraint (3.3) stipulates that at most elements of are nonzero and is, therefore, a sparsity constraint. (3.4) is a conservation of information constraint: what is not in the sparse representation of , , must be in the loss matrix . Constraint (3.5) restricts the class of to PBD matrices, and can be viewed as an interpretability constraint. This optimization problem can be described as follows: we want to find a PBD representation of the covariance matrix with at most non-zero elements with minimal square loss of information.

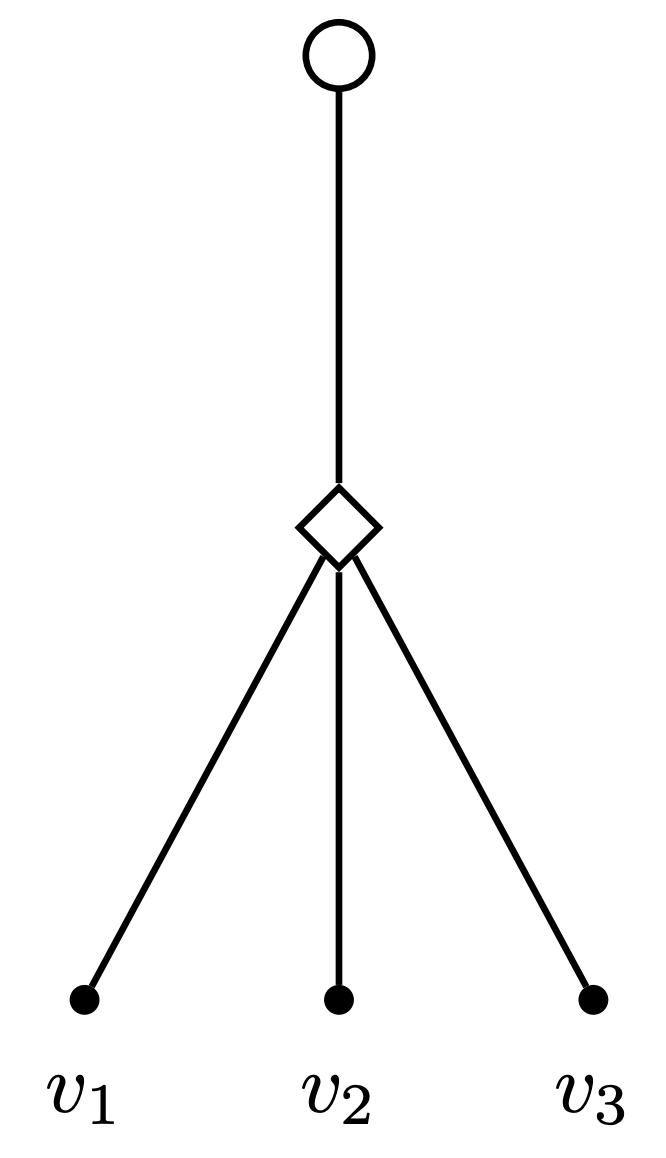

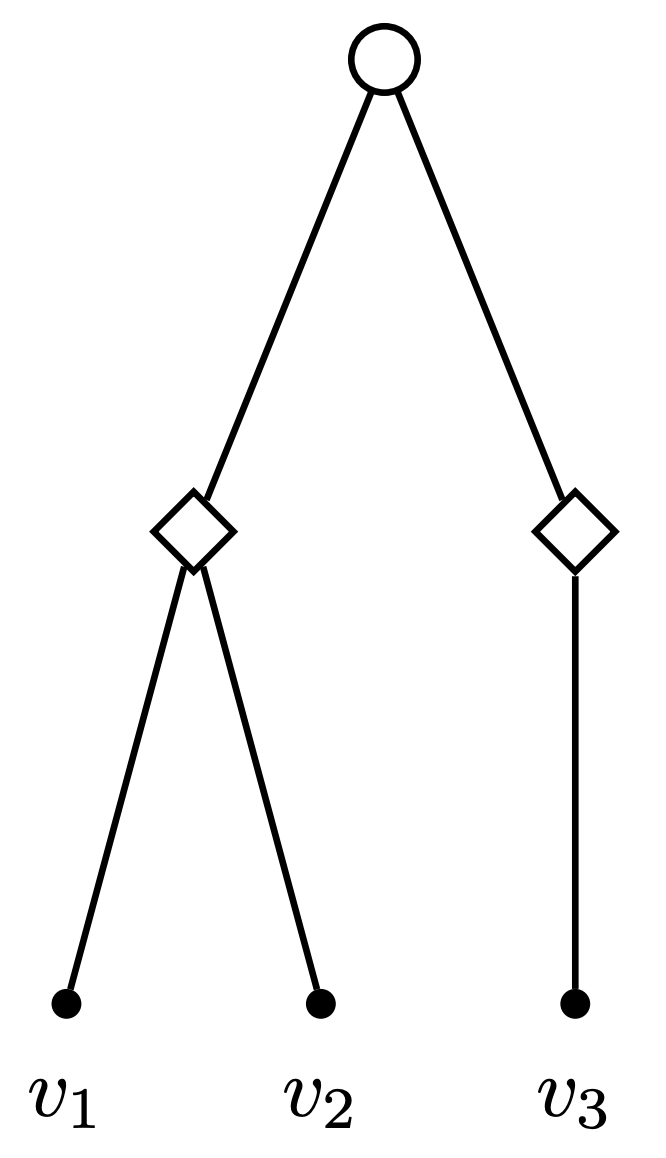

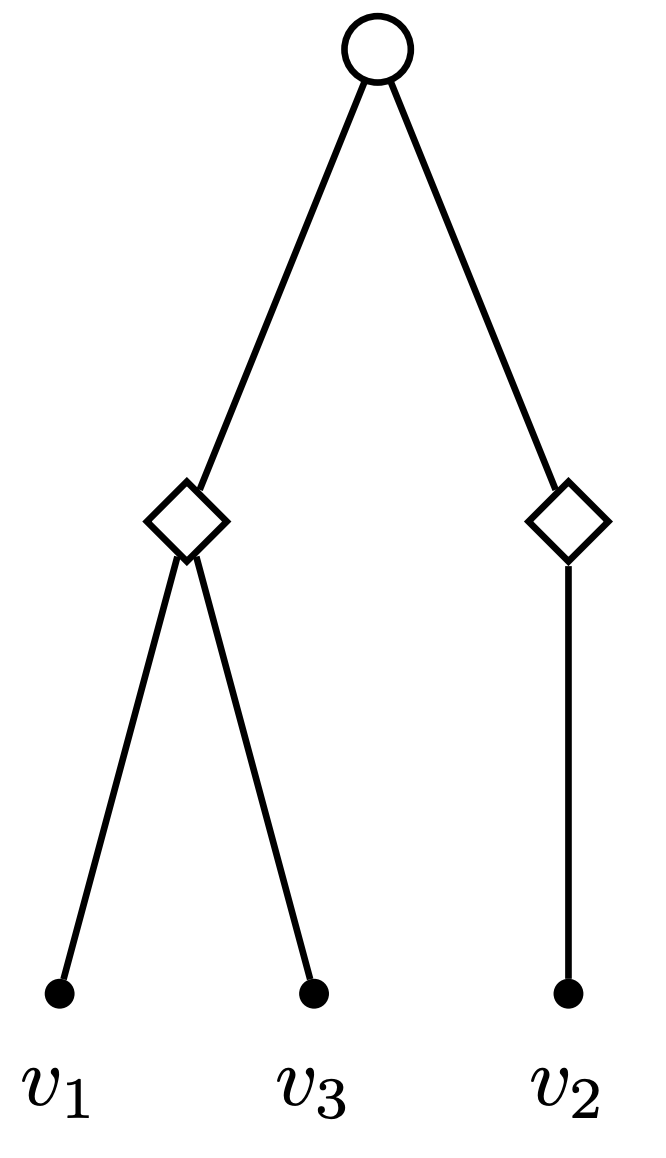

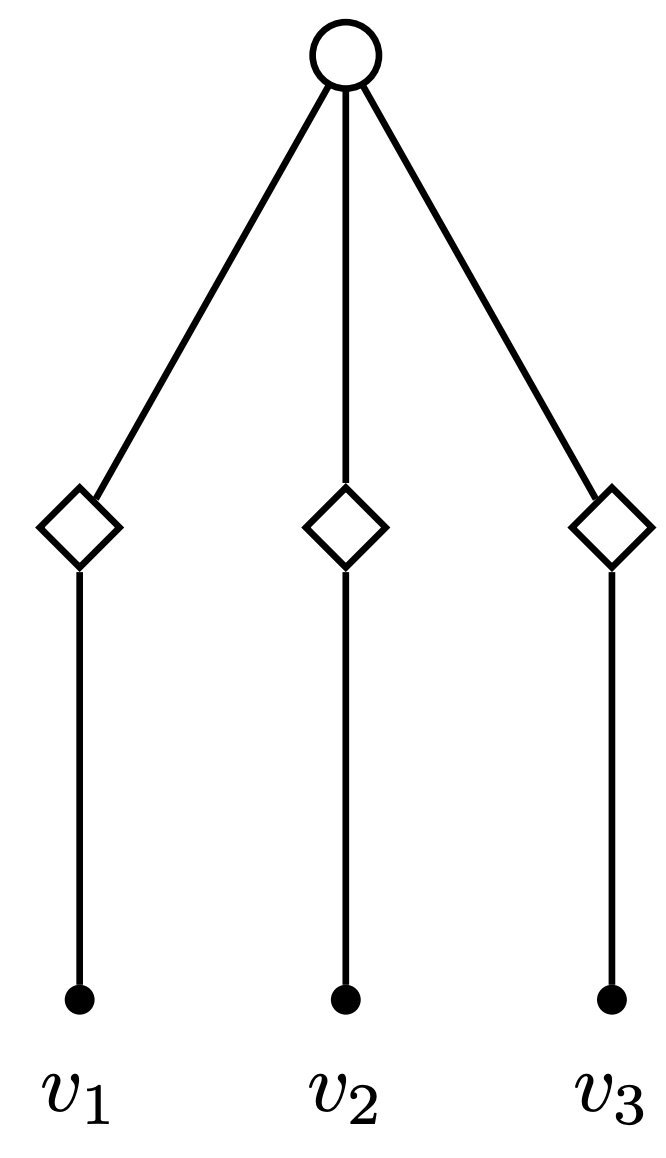

To mathematically formulate constraint (3.5), we first establish an association between trees and PBD matrices. Establishing such a one-to-one correspondence enables us to use the machinery of graph theory to enforce these PBD constraints. As we will find, such a representation will enable us to write constraint (3.5) as a set of linear constraints. We discuss how to construct such a graphical representation of PBD matrices and the linear constraint representation next.

Proposition 3.1

Any pseudo block diagonal matrix can be represented by a tree.

Proof 3.1.

Suppose M is a PBD matrix, then by Definition 3.2 there exists some index permuted matrix of M, such that is block diagonal. By Definition 3.1, we can write as the direct sum of square matrices, i.e., there exists matrices such that . To construct a tree representation of :

-

Step 1.

Represent each of the distributed coefficients in the model by a leaf node ().

-

Step 2.

Represent each of the square matrices by an internal node ().

-

Step 3.

Create a root node () and connect it to each of the internal nodes.

-

Step 4.

Connect each leaf node to the internal node representing the square matrix corresponding to its index.

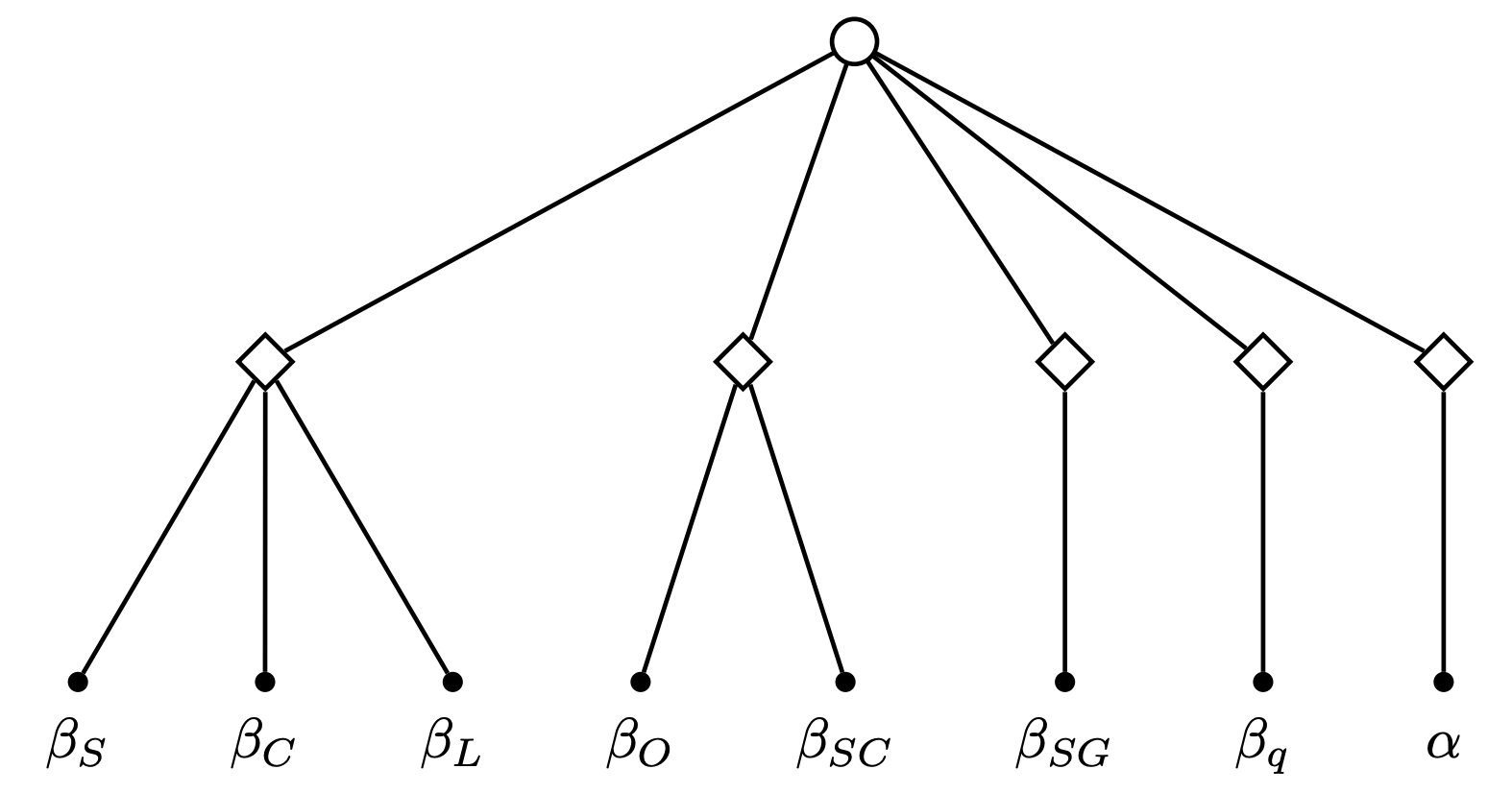

This procedure is illustrated by an example in Figure 1.

Let denote the index set of distributed coefficients in the model and let denote a set of intermediate nodes representing abstract blocks. These abstract blocks correspond to the constituent block matrices of the sparse PBD representation of the covariance matrix of the distributed coefficients .

To find an optimal PBD matrix , we need to determine:

-

1.

The number of blocks in .

-

2.

How to form the blocks corresponding to subsets of distributed coefficients.

From the preceding discussion on representing PBD matrices as trees, we can instead consider the induced graph , where the set of nodes consists of a root node , a set of leaf nodes representing the distributed variables, and a set of abstract intermediate nodes representing the constituent blocks. Formally, . Under this framework, the two optimization decisions posed above can be re-framed as follows:

-

1.

Which internal nodes to include in the graph ?

-

2.

How to form edges such that the resulting is a tree?

To this end, we define a binary variable for to denote whether or not the node representing abstract block is included in the tree representation of . Furthermore, let be a binary variable equal to one if there is a directed edge between nodes , and zero otherwise.

We now look at representing constraints (3.3) and (3.5) as linear constraints. The sparsity constraint (3.3) allows up to non-zero elements in the matrix . To enforce this constraint, we first define a binary variable for , and consider the following set of constraints:

| (3.6) |

Where and are lower and upper bounds on the size of the entries of the matrix and are determined from the MCMC posterior draws of the full covariance matrix . The sparsity constraint (3.3) can now be represented as:

| (3.7) |

Since covariance matrices are symmetric, we require that:

| (3.8) |

To enforce constraint (3.5), we first define the following binary auxiliary variables to denote if variables share a common block , that is:

| (3.9) |

This can be represented by the following linear constraints:

| (3.10) | |||

| (3.11) | |||

| (3.12) |

(3.10) and (3.11) represent the forward implication of (3.9), and (3.12) represents the backward implication of (3.9).

The covariance between is estimated if and only if and share a common block. Formally,

| (3.13) |

To represent this constraint, first note that the negation of the forward implication of (3.13) is the statement: (i.e., if and do not share a common block, then the corresponding covariance element is not estimated and constrained to zero). This can be written as the following linear constraint:

| (3.14) |

Likewise, the negation of the backward implication in (3.13) is which can be written as a set of either-or constraints:

| (3.15) |

Finally, we need to impose a number of structural constraints as follows: First, each of the nodes representing the distributed variables must belong to one block only:

| (3.16) |

Second, the edges must be selected such that the resulting graph is a tree. Recall that a tree with nodes must exactly have edges (otherwise the addition of an edge results in a cycle and the removal of an edge results in a disconnected graph). This condition can be enforced through the following equality constraint:

| (3.17) |

Third, block nodes can not have connections unless included in the graph:

| (3.18) |

Fourth, if a block node is included, it must have an incoming connection from the root node:

| (3.19) |

Finally, we always allow the diagonal elements (representing the variances) to be nonzero, i.e., for all , we permit no incoming edges to the root node: , no outgoing edges from the leaf nodes , and disallow self-arcs: .

Putting it all together, we arrive at the following optimization problem: Pseudo Block Diagonal Optimization Problem (P)

| subject to: | |||

Given a set of draws from the full covariance matrix and a sparsity level parameter , optimization problem (P) returns – a sparse PBD representation of with at most non-zeros. The sparse representation is optimal in the sense that it constructed with minimal square loss of information across draws .

This mixed-integer optimization problem has a quadratic objective and linear constraints and can be solved efficiently to optimality for relatively large problem sizes using standard conic quadratic programming techniques (Bertsekas, 1997 and Boyd and Vandenberghe, 2004) implemented in state of the art solvers such as GUROBI (Gurobi Optimization, 2015) and CPLEX (CPLEX, 2009).

3.2 Overall Algorithm

There are two critical components to our algorithm. The first component is the optimization problem (P) described in the previous section. Given draws from the full covariance matrix, and a regularization parameter , (P) outputs an optimal block structure as represented by the matrix . The second crucial component is a procedure that can estimate variance and covariance elements of pseduo block diagonal matrices from the data. This can be accomplished by applying step 2 of the three-step Gibbs sampling procedure (Algorithm 1) to each block separately as suggested by Becker (2016). Tying these two components together, we arrive at the following algorithm:

The number of non-zero covariances in can vary between to . Consequently, step 5 has to be repeated for

by varying in increments of 2 (since the covariance matrix is symmetric) for a total of runs. Note that these runs are embarrassingly parallel– meaning they can be run simultaneously.

We end this section by suggesting a more practical alternative to controlling sparsity than restricting the number of zero elements . Consider instead a modified optimization problem where Constraint (3.7) that restricts the number of non-zeros in the matrix , , in (P) is replaced by . This modified constraint now stipulates that the total number of blocks in is at least . Increasing the number of blocks increases the sparsity level of the matrix since each added block constraints the covariances between the coefficients that are in the added block and those that are not to zero. If consists of one only block, then it is a full matrix and all covariances are estimated. With as many blocks as there are rows or columns of , becomes a diagonal matrix will all the covariance elements restricted to zero. The benefit of using the number of blocks to control sparsity is that under this regime, step 5 is now to be repeated for by varying in increments of one for a total of runs only. The downside being the loss in granularity in how the sparsity is specified.

3.3 Implementation

The MISC algorithm consisting of the mixed-integer optimization problem (P) and the block-wise three-step Gibbs sampler (Algorithm 1) has been implemented in the Julia programming language (Bezanson et al., 2017) through the JuMP mathematical optimization interface (Dunning et al., 2017) and the GUROBI mixed-integer solver (Gurobi Optimization, 2015). The authors make the source code accessible under an MIT licence through https://github.com/ymedhat95/MISC.

4 Computational Experiments

In this section we validate the MISC algorithm introduced in Section 3. In Section 4.1, we demonstrate, through a Monte Carlo experiment that MISC can correctly recover the true covariance matrix structure. In Section 4.2, we apply our algorithm to the Apollo mode choice dataset from Hess and Palma (2019).

4.1 Monte Carlo Experiments

4.1.1 Dataset Description

The MISC algorithm introduced in Section 3 is applied to the synthetic choice-based-conjoint (CBC) Grapes dataset from Ben-Akiva et al. (2019). The setup is as follows: individuals are presented with eight menus, each including three different alternatives which are bunches of grapes with varying prices and attributes in addition to an opt-out alternative. The dependent variable is the choice between the three different bunches or not buying grapes at all (opting-out). The attributes and attribute levels are the same as in Ben-Akiva et al. (2019), and are presented in Table 1. The attributes of the different alternatives are drawn uniformly from their corresponding distributions.

| Attribute | Symbol | Levels |

|---|---|---|

| Price | P | $1 to $4 |

| Sweetness | S | Sweet (1) or Tart (0) |

| Crispness | C | Crisp (1) or Soft (0) |

| Size | L | Large (1) or Small (0) |

| Organic | O | Organic (1) or Non-organic (0) |

The utility equations (normalized to the opt-out alternative) are presented in equations (4.1)-(4.2). All coefficients are distributed with inter-consumer heterogeneity, as denoted by the subscripts .

| (4.1) | ||||

| (4.2) |

represents the utility of alternative in menu presented to individual . is a scale parameter. Exponentiation is used to ensure that it is always positive. is the price of grapes bunch in menu faced by individual . Its coefficient normalized to -1. , , , and represent sweetness, crispness, size, and organic dummies of bunch as indicated in Table 1, with coefficients , , , and respectively. and represent interaction terms between sweetness and crispness, and sweetness and a gender dummy with coefficients , respectively. is a constant for choosing one of the three bunches of grapes compared to opting-out. is an independently and identically distributed error term following the extreme value distribution with mean zero and unit scale.

The model is specified in the willingness-to-pay (WTP) space (i.e., the price coefficient is fixed to -1 and the scale parameter is estimated). Therefore, all the coefficients represent the willingness-to-pay for their corresponding attributes.

The population means and covariances of the coefficients of the synthetic population are shown Table 2. The covariance matrix is block diagonal and admits the tree representation shown in Figure 2 (cf. Proposition 3.1). Let the coefficients in Table 2 correspond to indices respectively. The structure of the population covariance can be compactly represented as . We will henceforth use this representation.

| Coefficient | Mean | Covariance | |||||||

| 1 | .9 | .4 | .2 | 0 | 0 | 0 | 0 | 0 | |

| .3 | .4 | .2 | .05 | 0 | 0 | 0 | 0 | 0 | |

| .2 | .2 | .05 | .15 | 0 | 0 | 0 | 0 | 0 | |

| .1 | 0 | 0 | 0 | .4 | .2 | 0 | 0 | 0 | |

| 0 | 0 | 0 | 0 | .2 | .3 | 0 | 0 | 0 | |

| .1 | 0 | 0 | 0 | 0 | 0 | .4 | 0 | 0 | |

| 2 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | |

| -1.5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | .25 | |

4.1.2 Block Structure Recovery and the Effect of Sample Size

The goal is here to use the MISC algorithm to recover the true covariance structure shown in Table 2 from the data. Out-of-sample validation is performed, to determine the optimal sparsity level, using a similar dataset, but with different individuals whose preferences follow the same multivariate normal distribution with the coefficients shown in Table 2.

The results of the experiment are presented in Table 3 and Table 4. Table 3 shows values of the training and validation log-likelihoods for various values of the regularizer , the maximum number of non-zero elements in the sparse representation of the matrix, and the corresponding optimal block structure output of the optimization problem (P). The experiment is repeated for various sample sizes. Notice that the training log-likelihood increases with decreasing sparsity level. This is expected as estimating additional covariance matrix elements cannot worsen the log-likelihood on the training sample. On the hold-out validation sample, however, denser covariance matrices do not necessarily perform better. This is akin to the machine learning concept of over-fitting: a more complicated model does not necessarily generalize better. Table 4 shows the estimated means and covariances for the specifications corresponding to the optimal sparsity levels for each of the three experiments determined from Table 3.

For sample sizes of and individuals, the block diagonal structure with the best validation log-likelihood is the true structure . For the sample size of 500 individuals, a block diagonal structure where an extra covariance term is estimated is recovered: .

![[Uncaptioned image]](/html/2001.05034/assets/MC_a.png)

![[Uncaptioned image]](/html/2001.05034/assets/MC_b.png)

![[Uncaptioned image]](/html/2001.05034/assets/MC_c.png)

Note: is the maximum number of non-zero elements in the covariance matrix. The Optimal Blocks column shows the optimal covariance structure at regularization level – the output of optimization problem (P). The colouring shown is proportional to the log-likelihood. The best validation log-likelihood for each experiment is underlined.

| Coefficient | Mean | Covariance | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 1.000 | .905 | .394 | .195 | 0 | 0 | 0 | 0 | 0 | |

| (.0147) | (.0241) | (.0116) | (.0086) | - | - | - | - | - | |

| .297 | .394 | .204 | .046 | 0 | 0 | 0 | 0 | 0 | |

| (.0097) | (.0116) | (.0074) | (.0050) | - | - | - | - | - | |

| .198 | .195 | .046 | .154 | 0 | 0 | 0 | 0 | 0 | |

| (.0070) | (.0086) | (.0050) | (.0063) | - | - | - | - | - | |

| .106 | 0 | 0 | 0 | .407 | .190 | 0 | 0 | 0 | |

| (.0091) | - | - | - | (.0113) | (.0010) | - | - | - | |

| 0.014 | 0 | 0 | 0 | .190 | .291 | 0 | 0 | 0 | |

| (.0132) | - | - | - | (.0010) | (.0020) | - | - | - | |

| .0910 | 0 | 0 | 0 | 0 | 0 | .375 | 0 | 0 | |

| (.0102) | - | - | - | - | - | (.0131) | - | - | |

| 2.031 | 0 | 0 | 0 | 0 | 0 | 0 | 1.051 | 0 | |

| (.0159) | - | - | - | - | - | - | (.0347) | - | |

| -1.507 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | .258 | |

| (.0167) | - | - | - | - | - | - | - | (.0178) | |

| Coefficient | Mean | Covariance | |||||||

|---|---|---|---|---|---|---|---|---|---|

| .931 | .875 | .350 | .187 | 0 | 0 | 0 | 0 | 0 | |

| (.0408) | (.0757) | (.0390) | (.0284) | - | - | - | - | - | |

| .241 | .350 | .178 | .058 | 0 | 0 | 0 | 0 | 0 | |

| (.0263) | (.0390) | (.0266) | (.0145) | - | - | - | - | - | |

| .168 | .187 | .058 | .152 | 0 | 0 | 0 | 0 | 0 | |

| (.0215) | (.0284) | (.0145) | (.0226) | - | - | - | - | - | |

| .011 | 0 | 0 | 0 | .3607 | .151 | 0 | 0 | 0 | |

| (.0273) | - | - | - | (.0327) | (.0268) | - | - | - | |

| .013 | 0 | 0 | 0 | .151 | .314 | 0 | 0 | 0 | |

| (.0350) | - | - | - | (.0268) | (.0494) | - | - | - | |

| .063 | 0 | 0 | 0 | 0 | 0 | .379 | 0 | 0 | |

| (.0312) | - | - | - | - | - | (.0429) | - | - | |

| 2.067 | 0 | 0 | 0 | 0 | 0 | 0 | 1.259 | 0 | |

| (.0506) | - | - | - | - | - | - | (.1220) | - | |

| -1.590 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | .381 | |

| (.0661) | - | - | - | - | - | - | - | (.0855) | |

| Coefficient | Mean | Covariance | |||||||

|---|---|---|---|---|---|---|---|---|---|

| .940 | .898 | .468 | .170 | 0 | 0 | 0 | 0 | 0 | |

| (.0618) | (.1086) | (.0607) | (.0382) | - | - | - | - | - | |

| .293 | .468 | .283 | .075 | 0 | 0 | 0 | 0 | 0 | |

| (.0475) | (.0607) | (.0518) | (.0212) | - | - | - | - | - | |

| .205 | .170 | .075 | .125 | 0 | 0 | 0 | 0 | 0 | |

| (.0296) | (.0382) | (.0212) | (.0266) | - | - | - | - | - | |

| .153 | 0 | 0 | 0 | .361 | .153 | 0 | 0 | 0 | |

| (.0385) | - | - | - | (.0475) | (.0372) | - | - | - | |

| -.068 | 0 | 0 | 0 | .153 | .224 | 0 | 0 | ||

| (.0572) | - | - | - | (.0372) | (.0685) | - | - | - | |

| .174 | 0 | 0 | 0 | 0 | 0 | .375 | 0 | 0 | |

| (.0451) | - | - | - | - | - | (.0600) | - | - | |

| 2.005 | 0 | 0 | 0 | 0 | 0 | 0 | 1.131 | .121 | |

| (.0744) | - | - | - | - | - | - | (.1647) | (.0788) | |

| -1.375 | 0 | 0 | 0 | 0 | 0 | 0 | .121 | .254 | |

| (.0783) | - | - | - | - | - | - | (.0788) | (.0878) | |

Note: Parameter means and covariances were calculated from draws from convergent MCMC posterior draws from the mean vector and covariance matrix respectively. Standard errors are shown in brackets below the corresponding estimate.

4.1.3 Edge Cases: Full and Diagonal Matrices

In this section, we demonstrate the ability of MISC to recover the correct covariance structure when the true covariance structure is a full matrix and when it is a diagonal matrix. For variety, we regularize using the number of blocks, , instead of the number of non-zero elements (as discussed at the end of Section 3.2). For the full matrix experiment, a random normally distributed matrix with mean zero and standard deviation 0.1 was added to the covariance matrix in Table 2. For the diagonal experiment, only the variances in Table 2 were preserved. In both experiments the means of the coefficients were unchanged. Data for 15000 individuals (10000 training, and 5000 validation) were generated according to these two schemes (full covariance and diagonal covariance matrices). The results are shown in Table 5. The MISC algorithm correctly recovers the structure for the full matrix experiment, and the structure for the diagonal matrix experiment.

![[Uncaptioned image]](/html/2001.05034/assets/MC_full.png)

![[Uncaptioned image]](/html/2001.05034/assets/MC_diag.png)

Note: is the number of blocks in the covariance matrix. Sparsity increases with increasing number of blocks. The Optimal Blocks column shows the optimal covariance structure at regularization level . The best validation log-likelihood for each experiment is underlined.

4.2 Empirical Application

In this section we apply the MISC algorithm to the Apollo mode choice dataset from Hess and Palma (2019). individuals were presented with choices between four modes of transportation: car, bus, air and rail. The options were described on the basis of travel times (hours), travel costs (£), and access times (for the bus, air and rail options). Additionally for the air and bus modes, a categorical quality of service attribute was added. The quality of service attribute takes one of three levels: no frills, wifi available, or food available. Each individual was presented with 14 stated preference tasks and each task had at least two of these four modes available.

A mixed logit model for the choice setup just described is specified according to utility equations (4.3)-(4.6). There is one equation for each alternative (four in total). and index individuals and stated preference tasks respectively. The dependent variable is the individual’s choice of transportation mode.

| (4.3) | ||||

| (4.4) | ||||

| (4.5) | ||||

| (4.6) |

The specification shown includes alternative-specific travel time coefficients and constants. The cost, access time, and level of service coefficients are shared across the alternatives. The coefficients of the model are assumed to be randomly distributed according to a normal distribution for which we estimate its mean and covariance matrix. The epsilon errors are extreme-valued with mean zero and unit scale. is normalized to zero for identification. The other alternative specific constants represent base preferences over the car alternative. Similarly, is normalized to zero and and measure the effects of additional quality of service over the no frills option. Negation and exponentiation are used to ensure that the effects of time and cost on the utility are negative (e.g. the coefficient enters the utility equations as . This is equivalent to specifying a log-normal distribution for ).

Table 6 shows the estimated parameters (mean and covariance matrix) corresponding to the optimal structure as determined by the MISC algorithm. Table 7 shows the output of the MISC algorithm for various levels of regularization. The specification corresponding to the best validation log-likelihood was chosen, and the corresponding estimated parameters are shown in Table 6. The optimal structure has four blocks, and allows covariances between the four alternative-specific travel time coefficients, the access time coefficient, the travel cost coefficient and the bus and rail modes alternative-specific constants. All other covariances are constrained to zero.

| Coefficient | Mean | Covariance | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| -1.23 | 5.54 | 0 | -1.89 | 4.97 | 5.30 | 6.82 | 6.35 | 2.79 | 0 | 0 | 3.74 | |

| (.419) | (1.35) | - | (.333) | (.730) | (.799) | (1.11) | (.947) | (.598) | - | - | (.514) | |

| .386 | 0 | .550 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| (.153) | - | (.092) | - | - | - | - | - | - | - | - | - | |

| -.428 | -1.89 | 0 | 1.04 | -2.02 | -2.11 | -2.71 | -2.54 | -1.11 | 0 | 0 | -1.45 | |

| (.110) | (.333) | - | (.156) | (.243) | (.250) | (.330) | (.332) | (.202) | - | - | (.197) | |

| -1.01 | 4.97 | 0 | -2.02 | 5.44 | 5.46 | 7.19 | 6.70 | 2.93 | 0 | 0 | 4.05 | |

| (.143) | (.730) | - | (.243) | (.470) | (.497) | (.694) | (.568) | (.439) | - | - | (.354) | |

| -.365 | 5.30 | 0 | -2.11 | 5.46 | 5.98 | 7.50 | 6.98 | 2.95 | 0 | 0 | 4.05 | |

| (.185) | (.799) | - | (.250) | (.497) | (.674) | (.741) | (.601) | (.449) | - | - | (.414) | |

| -1.97 | 6.82 | 0 | -2.71 | 7.19 | 7.50 | 10.7 | 9.27 | 3.83 | 0 | 0 | 5.36 | |

| (.242) | (1.11) | - | (.330) | (.694) | (.741) | (1.38) | (.915) | (.656) | - | - | (.468) | |

| -1.97 | 6.35 | 0 | -2.54 | 6.70 | 6.98 | 9.27 | 8.87 | 3.71 | 0 | 0 | 4.94 | |

| (.224) | (.947) | - | (.332) | (.568) | (.601) | (.915) | (.823) | (.520) | - | - | (.443) | |

| -.032 | 2.79 | 0 | -1.11 | 2.93 | 2.95 | 3.83 | 3.71 | 2.16 | 0 | 0 | 2.13 | |

| (.149) | (.598) | - | (.202) | (.439) | (.449) | (.656) | (.520) | (.487) | - | - | (.303) | |

| .908 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | .491 | 0 | 0 | |

| (.077) | - | - | - | - | - | - | - | - | (.086) | - | - | |

| .436 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | .431 | 0 | |

| (.072) | - | - | - | - | - | - | - | - | - | (.086) | - | |

| -2.63 | 3.74 | 0 | -1.45 | 4.05 | 4.05 | 5.36 | 4.94 | 2.13 | 0 | 0 | 3.44 | |

| (.096) | (.514) | - | (.197) | (.354) | (.414) | (.468) | (.443) | (.303) | - | - | (.339) | |

Note: The mixed logit model was reestimated on the full dataset after MISC model selection procedure. Parameter means and covariances were calculated from draws from convergent MCMC posterior draws from the mean vector and covariance matrix respectively. Standard errors are shown in brackets below the corresponding estimate.

![[Uncaptioned image]](/html/2001.05034/assets/Apollo.png)

Note: The indices shown correspond the coefficients column in Table 6. The dataset was randomly spliy into 300 individuals for training and 100 for validation. is a sparsity parameter corresponding to the minimum number of blocks in the covariance matrix. The best validation log-likelihood is underlined. The optimal block diagonal structure is obtained with blocks.

The estimated means of the alternative-specific constants show that, ceteris paribus, air and bus are the most and least preferred modes of transportation respectively. Travellers are also more sensitive to travel time by bus than by any other mode. The access time sensitivities outweighs, on average, the travel time sensitivities. Furthermore, the negative correlation between the alternative-specific constants of the bus and rail modes indicate that travellers who prefer to travel by rail tend to dislike travel by bus. The effects of increasing quality of service are positive, as expected, since we control for travel costs.

The estimated covariances indicate that the travel time sensitives for the different travel modes are positively correlated both among one another and with access time sensitivities, travel costs, and the preference for the bus travel mode. It appears that travellers who prefer the bus mode of travel are more sensitive to travel time and travel costs. We observe an opposite trend for travellers who prefer rail. These travellers tend to be less sensitive to travel times and travel costs. This is also reflected by the average travel time sensitivity for the rail travel mode being the lowest among the four travel modes.

Table 8 shows the calculated values of time. Travellers are more willing to spend to reduce their bus travel times than the travel times of the other available modes of transportation. Travellers are, however, most willing to spend to reduce the access times.

| Value of time (£/hour) | ||

|---|---|---|

| Median | Mean | |

| Car Travel Time | 5.05 | 7.49 |

| Bus Travel Time | 9.63 | 18.63 |

| Air Travel Time | 1.93 | 10.70 |

| Rail Travel Time | 1.93 | 6.52 |

| Access Time | 13.44 | 26.26 |

Note: The value of time is the extra amount of money, in £, that a traveller would be willing to pay to reduce their journey times by one hour. For an in depth demonstration of how values of time are calculated in logit mixture models see Xie et al. (2019).

5 Extensions

In this section, we propose adaptations to the MISC algorithm to handle common extensions of the logit mixture model: random and fixed coefficients (Section 5.1), inter- and intra-individual heterogeneity (Section 5.2) and flexible mixing distributions (Section 5.3).

5.1 Random and Fixed Parameters

A simple extension to our procedure can be made to allow optimization problem (P) to choose which variances to estimate i.e., which coefficients are random and which are fixed. This can be done by eliminating the following set of constraints from (P):

| (5.1) |

and by adjusting the equality constraint in constraint (3.16) to a less than or equal to constraint:

| (5.2) |

Any distributed coefficients that the modified optimization problem decides not to estimate variances for, are not included in step 1 or step 2 of the 3-step Gibbs sample (Algorithm 1), but are instead estimated through a separate Metropolis-Hastings algorithm step as in Khondker et al. (2013). This extension is particularly useful when working with small datasets where a much more parsimonious specification is required for maximal efficiency.

5.2 Inter- and Intra-Individual Heterogeneity

When multiple observations are available for each individual, it is possible to identify inter- as well as intra-individual heterogeneity, representing random taste variations among different individuals and among different choice situations of the same individual respectively. Becker et al. (2018) proposed an extension to the three-step Gibbs-sampler (Algorithm 1) of logit mixture models to account for both sources of heterogeneity. The underlying model assumes that the utility equation is given by the following:

| (5.3) |

represents a vector of choice-specific coefficients that follow the distribution:

| (5.4) |

and the individual-specific means are distributed as:

| (5.5) |

and are the inter- and intra-individual covariance matrices respectively. In such applications, the proposed methodology can be extended in two different ways to account for the two types of heterogeneity:

-

1.

Estimating sparse covariances the inter- and intra-individual covariance matrices. The MISC algorithm can be applied separately to the two covariance matrices.

-

2.

The modeler might be interested in estimating three different types of coefficients: (1) fixed coefficients, (2) coefficients with inter-individual heterogeneity only, and (3) coefficients with inter- and intra-individual heterogeneity as in Becker et al. (2018). The extension presented in Section 5.1 can be used to distinguish between the three types of coefficients.

5.3 Flexible Mixing Distributions

The logit mixture model with normally distributed random coefficients can be extended to account for semi-parametric flexible mixing distributions. These distributions are specified as a finite mixture of normals; see Rossi et al. (2012), Bujosa et al. (2010), Greene and Hensher (2013), Keane and Wasi (2013), and Krueger et al. (2018). Semi-parametric distributions can overcome the major limitation of normal or lognormal mixing distributions, which is the assumption of uni-modality, as they can asymptotically mimic any shape; see Vij and Krueger (2017).

The main limitation of this method is that the number of estimated coefficients is proportional to the number of “classes” in the normal mixture. For example, a mixture of three normals entails the estimation of three covariance matrices. Our methodology can be applied to these models to enforce sparsity and reduce the number of estimated coefficients. Let denote draw for class , the fraction of the population in class in draw , and the sparse representation of the covariance matrix for class . We suggest an extension of the representation (3.2)-(3.5) to the multi-class case as follows:

| (5.6) | ||||

| (5.7) | ||||

| (5.8) | ||||

| (5.9) |

controls the sparsity level across all . Greater sparsity control can be achieved through an -dimensional parameter by replacing (5.7) with . The clear downside being the much greater number of required runs of the MISC algorithm.

6 Concluding Remarks

This paper presents a new method of finding an optimal pseudo block diagonal (PBD) specification of the covariance matrix of the distributed coefficients in logit mixture models. The proposed algorithm, which we call MISC, marks a significant methodological improvement over the current modus operandi of estimating either a full covariance matrix or a diagonal matrix. By working on PBD matrices, our method is permutation invariant in that it does not depend on the particular ordering of the distributed coefficients in the problem. The algorithm presented is an interplay between a mixed-integer optimization program and the standard MCMC three-step Gibbs-sampling procedure typically used to estimate logit mixture models. A mixed-integer program is used to find an optimal PBD covariance matrix structure for any desired sparsity level using MCMC posterior draws from the full covariance matrix. The optimal sparsity level of the covariance matrix is determined using out-of-sample validation.

The proposed methodology is practical in that the main computational step can be completely parallelized. Furthermore, by controlling sparsity using the number of blocks in the matrix, the algorithm requires as many of the traditional MCMC runs used in logit mixture estimation as there are distributed coefficients.

Unlike the Bayesian LASSO-based sparsity methods in the statistics literature, our method does not penalize the non-zero elements of the covariance matrix. This is desirable, in the logit mixture context, since penalizing the non-zero covariances may lead to underestimating the heterogeneity in the population under study.

We have demonstrated the efficacy of our algorithm by applying it to a synthetic dataset where the correct block structure specification was successfully recovered. The algorithm was shown to be robust with respect to sample size. We demonstrated an empirical application to the Apollo mode choice dataset and presented a few practical extensions to our framework that are relevant for logit mixture models.

References

- Aboutaleb (2019) Aboutaleb, Y. M. (2019). Learning structure in nested logit models. Master’s thesis, Massachusetts Institute of Technology.

- Aigner (1999) Aigner, M. (1999). A characterization of the bell numbers. Discrete mathematics 205(1-3), 207–210.

- Akinc and Vandebroek (2018) Akinc, D. and M. Vandebroek (2018). Bayesian estimation of mixed logit models: Selecting an appropriate prior for the covariance matrix. Journal of choice modelling 29, 133–151.

- Allenby (1997) Allenby, G. (1997). An introduction to hierarchical bayesian modeling. In Tutorial notes, Advanced Research Techniques Forum, American Marketing Association.

- Allenby and Rossi (1998) Allenby, G. M. and P. E. Rossi (1998). Marketing models of consumer heterogeneity. Journal of econometrics 89(1-2), 57–78.

- Banerjee et al. (2008) Banerjee, O., L. E. Ghaoui, and A. d’Aspremont (2008). Model selection through sparse maximum likelihood estimation for multivariate gaussian or binary data. Journal of Machine learning research 9(Mar), 485–516.

- Becker (2016) Becker, F. (2016). Bayesian estimation of mixed logit models with inter-and intra-personal heterogeneity. Master’s thesis, Freie Universitaet Berlin, Berlin.

- Becker et al. (2018) Becker, F., M. Danaf, X. Song, B. Atasoy, and M. Ben-Akiva (2018). Bayesian estimator for logit mixtures with inter-and intra-consumer heterogeneity. Transportation Research Part B: Methodological 117, 1–17.

- Belloni et al. (2013) Belloni, A., V. Chernozhukov, et al. (2013). Least squares after model selection in high-dimensional sparse models. Bernoulli 19(2), 521–547.

- Ben-Akiva et al. (1997) Ben-Akiva, M., D. McFadden, M. Abe, U. Böckenholt, D. Bolduc, D. Gopinath, T. Morikawa, V. Ramaswamy, V. Rao, D. Revelt, et al. (1997). Modeling methods for discrete choice analysis. Marketing Letters 8(3), 273–286.

- Ben-Akiva et al. (2019) Ben-Akiva, M., D. McFadden, and K. Train (2019). Foundations of stated preference elicitation: Consumer behavior and choice-based conjoint analysis. Foundations and Trends® in Econometrics 10(1-2), 1–144.

- Bertsekas (1997) Bertsekas, D. P. (1997). Nonlinear programming. Journal of the Operational Research Society 48(3), 334–334.

- Bertsimas and Dunn (2017) Bertsimas, D. and J. Dunn (2017). Optimal classification trees. Machine Learning 106(7), 1039–1082.

- Bertsimas et al. (2016) Bertsimas, D., A. King, R. Mazumder, et al. (2016). Best subset selection via a modern optimization lens. The annals of statistics 44(2), 813–852.

- Bertsimas and Tsitsiklis (1997) Bertsimas, D. and J. N. Tsitsiklis (1997). Introduction to linear optimization, Volume 6. Athena Scientific Belmont, MA.

- Bezanson et al. (2017) Bezanson, J., A. Edelman, S. Karpinski, and V. B. Shah (2017). Julia: A fresh approach to numerical computing. SIAM review 59(1), 65–98.

- Boyd and Vandenberghe (2004) Boyd, S. and L. Vandenberghe (2004). Convex optimization. Cambridge university press.

- Bujosa et al. (2010) Bujosa, A., A. Riera, and R. L. Hicks (2010). Combining discrete and continuous representations of preference heterogeneity: a latent class approach. Environmental and Resource Economics 47(4), 477–493.

- Carvalho et al. (2010) Carvalho, C. M., N. G. Polson, and J. G. Scott (2010). The horseshoe estimator for sparse signals. Biometrika 97(2), 465–480.

- Cherchi and Guevara (2012) Cherchi, E. and C. A. Guevara (2012). A monte carlo experiment to analyze the curse of dimensionality in estimating random coefficients models with a full variance–covariance matrix. Transportation Research Part B: Methodological 46(2), 321–332.

- CPLEX (2009) CPLEX, I. I. (2009). V12. 1: User’s manual for cplex. International Business Machines Corporation 46(53), 157.

- Dahl et al. (2008) Dahl, J., L. Vandenberghe, and V. Roychowdhury (2008). Covariance selection for nonchordal graphs via chordal embedding. Optimization Methods & Software 23(4), 501–520.

- Dempster (1972) Dempster, A. P. (1972). Covariance selection. Biometrics, 157–175.

- Drton and Perlman (2004) Drton, M. and M. D. Perlman (2004). Model selection for gaussian concentration graphs. Biometrika 91(3), 591–602.

- Drton and Perlman (2008) Drton, M. and M. D. Perlman (2008). A sinful approach to gaussian graphical model selection. Journal of Statistical Planning and Inference 138(4), 1179–1200.

- Drton et al. (2007) Drton, M., M. D. Perlman, et al. (2007). Multiple testing and error control in gaussian graphical model selection. Statistical Science 22(3), 430–449.

- Dunning et al. (2017) Dunning, I., J. Huchette, and M. Lubin (2017). Jump: A modeling language for mathematical optimization. SIAM Review 59(2), 295–320.

- Friedman et al. (2008) Friedman, J., T. Hastie, and R. Tibshirani (2008). Sparse inverse covariance estimation with the graphical lasso. Biostatistics 9(3), 432–441.

- Greene and Hensher (2013) Greene, W. H. and D. A. Hensher (2013). Revealing additional dimensions of preference heterogeneity in a latent class mixed multinomial logit model. Applied Economics 45(14), 1897–1902.

- Guevara et al. (2009) Guevara, C. A., E. Cherchi, and M. Moreno (2009). Estimating random coefficient logit models with full covariance matrix: comparing performance of mixed logit and laplace approximation methods. Transportation Research Record 2132(1), 87–94.

- Gurobi Optimization (2015) Gurobi Optimization, I. (2015). Gurobi optimizer reference manual. URL http://www. gurobi. com.

- Hensher and Greene (2003) Hensher, D. A. and W. H. Greene (2003). The mixed logit model: the state of practice. Transportation 30(2), 133–176.

- Hess et al. (2017) Hess, S., P. Murphy, H. Le, and W. Y. Leong (2017). Estimation of new monetary valuations of travel time, quality of travel, and safety for singapore. Transportation Research Record 2664(1), 79–90.

- Hess and Palma (2019) Hess, S. and D. Palma (2019). Apollo: a flexible, powerful and customisable freeware package for choice model estimation and application. Journal of Choice Modelling, 100170.

- Hess and Train (2017) Hess, S. and K. Train (2017). Correlation and scale in mixed logit models. Journal of choice modelling 23, 1–8.

- Huang et al. (2013) Huang, A., M. P. Wand, et al. (2013). Simple marginally noninformative prior distributions for covariance matrices. Bayesian Analysis 8(2), 439–452.

- James (2018) James, J. (2018). Estimation of factor structured covariance mixed logit models. Journal of choice modelling 28, 41–55.

- Keane and Wasi (2013) Keane, M. and N. Wasi (2013). Comparing alternative models of heterogeneity in consumer choice behavior. Journal of Applied Econometrics 28(6), 1018–1045.

- Khondker et al. (2013) Khondker, Z. S., H. Zhu, H. Chu, W. Lin, and J. G. Ibrahim (2013). The bayesian covariance lasso. Statistics and its Interface 6(2), 243.

- Kipperberg et al. (2008) Kipperberg, G., C. A. Bond, and D. L. Hoag (2008). An application of mixed logit estimation in the analysis of producers’ stated preferences. Technical report.

- Knuiman (1978) Knuiman, M. (1978). Covariance selection. Advances in Applied Probability 10, 123–130.

- Krueger et al. (2018) Krueger, R., A. Vij, and T. H. Rashidi (2018). A dirichlet process mixture model of discrete choice. arXiv preprint arXiv:1801.06296.

- McFadden and Train (2000) McFadden, D. and K. Train (2000). Mixed mnl models for discrete response. Journal of applied Econometrics 15(5), 447–470.

- Meinshausen et al. (2006) Meinshausen, N., P. Bühlmann, et al. (2006). High-dimensional graphs and variable selection with the lasso. The annals of statistics 34(3), 1436–1462.

- Porteous (1985) Porteous, B. (1985). Improved likelihood ratio statistics for covariance selection models. Biometrika 72(1), 97–101.

- Revelt and Train (1998) Revelt, D. and K. Train (1998). Mixed logit with repeated choices: households’ choices of appliance efficiency level. Review of economics and statistics 80(4), 647–657.

- Rossi et al. (2012) Rossi, P. E., G. M. Allenby, and R. McCulloch (2012). Bayesian statistics and marketing. John Wiley & Sons.

- Scarpa et al. (2008) Scarpa, R., M. Thiene, and K. Train (2008). Utility in willingness to pay space: a tool to address confounding random scale effects in destination choice to the alps. American Journal of Agricultural Economics 90(4), 994–1010.

- Train and Sonnier (2005) Train, K. and G. Sonnier (2005). Mixed logit with bounded distributions of correlated partworths. In Applications of simulation methods in environmental and resource economics, pp. 117–134. Springer.

- Train (1998) Train, K. E. (1998). Recreation demand models with taste differences over people. Land economics, 230–239.

- Train (2009) Train, K. E. (2009). Discrete choice methods with simulation. Cambridge university press.

- Vandenberghe et al. (1998) Vandenberghe, L., S. Boyd, and S.-P. Wu (1998). Determinant maximization with linear matrix inequality constraints. SIAM journal on matrix analysis and applications 19(2), 499–533.

- Vij and Krueger (2017) Vij, A. and R. Krueger (2017). Random taste heterogeneity in discrete choice models: Flexible nonparametric finite mixture distributions. Transportation Research Part B: Methodological 106, 76–101.

- Wang et al. (2012) Wang, H. et al. (2012). Bayesian graphical lasso models and efficient posterior computation. Bayesian Analysis 7(4), 867–886.

- Xie et al. (2019) Xie, Y., M. Danaf, C. Lima Azevedo, A. P. Akkinepally, B. Atasoy, K. Jeong, R. Seshadri, and M. Ben-Akiva (2019, Dec). Behavioral modeling of on-demand mobility services: general framework and application to sustainable travel incentives. Transportation 46(6), 2017–2039.

- Yuan and Lin (2007) Yuan, M. and Y. Lin (2007). Model selection and estimation in the gaussian graphical model. Biometrika 94(1), 19–35.