Pakiman et al.

Self-guided Approximate Linear Programs

Self-guided Approximate Linear Programs

Parshan Pakiman, Selvaprabu Nadarajah, Negar Soheili

\AFFCollege of Business Administration, University of Illinois at Chicago, 601 South Morgan Street, Chicago, IL60607, USA \EMAIL{ppakim2@uic.edu,selvan@uic.edu,nazad@uic.edu} \AUTHORQihang Lin

\AFFTippie College of Business, The University of Iowa, 21 East Market Street, Iowa City, IA 52242, USA

\EMAILqihang-lin@uiowa.edu

Approximate linear programs (ALPs) are well-known models based on value function approximations (VFAs) to obtain policies and lower bounds on the optimal policy cost of discounted-cost Markov decision processes (MDPs). Formulating an ALP requires (i) basis functions, the linear combination of which defines the VFA, and (ii) a state-relevance distribution, which determines the relative importance of different states in the ALP objective for the purpose of minimizing VFA error. Both these choices are typically heuristic: basis function selection relies on domain knowledge while the state-relevance distribution is specified using the frequency of states visited by a heuristic policy. We propose a self-guided sequence of ALPs that embeds random basis functions obtained via inexpensive sampling and uses the known VFA from the previous iteration to guide VFA computation in the current iteration. Self-guided ALPs mitigate the need for domain knowledge during basis function selection as well as the impact of the initial choice of the state-relevance distribution, thus significantly reducing the ALP implementation burden. We establish high probability error bounds on the VFAs from this sequence and show that a worst-case measure of policy performance is improved. We find that these favorable implementation and theoretical properties translate to encouraging numerical results on perishable inventory control and options pricing applications, where self-guided ALP policies improve upon policies from problem-specific methods. More broadly, our research takes a meaningful step toward application-agnostic policies and bounds for MDPs.

approximate linear programming, Markov decision processes, reinforcement learning, random features, inventory control, options pricing \HISTORYDecember 2019 (initial version); October 2021 (this version).

1 Introduction

Computing high-quality control policies in sequential decision making problems is an important task across several application domains. Markov decision processes (MDPs; Puterman 1994) provide a powerful framework to find optimal policies in such problems but are often intractable to solve exactly due to their large state and action spaces or the presence of high-dimensional expectations (see §1.2 and §4.1 of Powell 2007). Therefore, a class of approximate dynamic programming (ADP) approaches instead approximate the value functions of MDPs and use the resulting approximations to obtain control policies in simulations (Bertsekas and Tsitsiklis 1996). Approximate linear programming (Schweitzer and Seidmann 1985, De Farias and Van Roy 2003) is a math-programming based ADP approach for computing value function approximations (VFAs) that has been applied to a wide variety of domains, including operations research, reinforcement learning, and artificial intelligence (Adelman 2003, Guestrin et al. 2003, Forsell and Sabbadin 2006, Desai et al. 2012a, Adelman and Mersereau 2013, Tong and Topaloglu 2013, Nadarajah et al. 2015, Mladenov et al. 2017, Balseiro et al. 2019, Blado and Toriello 2019). It solves a so called approximate linear program (ALP) to obtain a VFA, from which a control policy can be computed. This VFA can also be used to obtain a lower bound on the optimal policy cost, which facilitates the computation of an optimality gap for the ALP policy as well as other heuristic policies.

Formulating an ALP requires (i) basis functions, the linear combination of which defines the VFA over the MDP state space, and (ii) a state-relevance distribution, which determines the relative importance of different states in the ALP objective for the purpose of minimizing VFA error. It is well known that the choices of basis functions and the state-relevance distribution are challenging and are typically handled heuristically, the former using domain knowledge and the latter most commonly by considering the states visited by a heuristic policy (see §5 in Farias and Van Roy 2006 and §3.2.2 in Sun et al. 2014). Once an ALP is formulated, its solution provides the weights associated with basis functions defining a VFA but requires tackling a large-scale, potentially semi-infinite, linear program. Solving an ALP can be approached, for example, using techniques such as constraint generation, constraint sampling, and constraint-violation learning (see Lin et al. 2020 for a recent overview of ALP solution techniques). If the ALP VFA gives rise to a policy and a lower bound with a small optimality gap, the near-optimal policy is used; otherwise, the choice of basis functions and state-relevance distribution will need to be modified. The initial choice and possible modification of ALP parameters is of fundamental importance to ensure the quality of the ALP VFA but their choice has received limited attention in the literature (Klabjan and Adelman 2007, Adelman and Klabjan 2012, and Bhat et al. 2012). The goal of this paper is to broaden the applicability of ALP by reducing the burden of making these choices.

Our starting point is to provide a new reformulation of a discounted-cost MDP as a large-scale linear program. This linear program has infinitely many variables corresponding to a weighted integral of a continuum of basis functions, referred to as random basis functions (or random features in machine learning), and a large number of constraints (possibly infinite), one for each MDP state and action pair. Random Fourier basis functions defined using cosines are popular examples (Rahimi and Recht 2008a). A functional analogue of Monte Carlo sampling can be used to approximate the integral over random basis functions. The resulting model, dubbed feature-based approximate linear program (FALP), has variables corresponding to the VFA weights in a linear combination of randomly sampled basis functions. We establish high-probability bounds on the worst-case error between the FALP VFA and the MDP value function. In particular, this error bound converges at the dimension-free rate of one divided by the square root of the number of sampled random basis functions, analogous to the convergence rate of standard Monte Carlo sampling with respect to the number of samples.

While FALP does not rely on defining basis functions using domain knowledge, its formulation still requires choosing a state-relevance distribution. Misspecifying this distribution can lead to poor ALP policies (De Farias and Van Roy 2003, Sun et al. 2014). The literature documents an iterative approach to guide this choice using ALP policy information (De Farias and Van Roy 2003, Page 854 and Farias and Van Roy 2006). This approach first solves ALP formulated with fixed basis functions and a heuristic choice of the state-relevance distribution, then simulates the ALP policy to evaluate the probabilities of visiting states, then uses these probabilities as a state-relevance distribution in a subsequent solution of the ALP, and so on. While intuitive, this approach lacks conceptual backing and also requires simulating the policy after every iteration, which can be expensive. We consider this iterative approach with FALP and refer to it as policy-guided FALP.

We propose an alternative iterative approach that does not rely on policy simulation to update a state-relevance distribution. Instead, it leverages our ability to sample additional random basis functions inexpensively. To elaborate, we solve a sequence of FALP models with increasing numbers of random basis functions that include guiding constraints, which require the VFA being computed at a given iteration to be no smaller than the VFA available from the immediately preceding iteration. By dualizing the guiding constraints, we show that this sequence of models is equivalent to a series of FALP models with increasing numbers of random basis functions and adaptively updated state-relevance distributions. We thus label the model class as self-guided FALP because state-relevance distribution updates involve its own past VFA information. The sequence of VFAs associated with these models provides monotonically increasing lower bounds and a monotonically non-increasing worst-case measure of policy performance. These properties are not guaranteed for policy-guided FALP. The “price” of the aforementioned desirable properties is the larger number of constraints in self-guided FALP compared to FALP. We establish an error bound for self-guided FALP, highlight the effect of the guiding constraints on this bound, and discuss how solution approaches for FALP can be directly applied to solve self-guided FALP.

We validate the performance of the aforementioned ALP models on inventory control and options pricing applications, which give rise to discounted-cost MDPs with rather distinct properties.

The MDP for perishable inventory control has an infinite horizon, a non-convex cost structure, a continuous action space, and a continuous state space that is affected by decisions (i.e., controllable state space). MDPs that share similar properties also arise in lost-sales inventory control, healthcare screening, and dual sourcing, among other applications (Zipkin 2008, Steimle and Denton 2017, Hua et al. 2015). Policies for the perishable inventory control application with optimality gaps of not more than 12% have been found by Lin et al. (2020) for a three-dimensional state space using an ALP model with problem-specific basis functions. FALP with a uniform state-relevance distribution essentially closes the optimality gaps on these known instances, that is, no iterative versions of FALP are needed. In contrast, for new instances that we create with five- and ten-dimensional state spaces, FALP performs poorly with optimality gaps ranging from 5.9% to 27.7% and policy-guided FALP becomes unstable. Self-guided FALP instead obtains excellent policies in these high-dimensional instances with optimality gaps of less than 7.5%.

The options pricing application involves a finite-horizon, a non-convex reward, a finite action space, and a continuous state space that evolves in an exogenous manner (that is, it is not affected by decisions). This MDP structure is representative of many financial and real options problems (Smith and McCardle 1998, Haugh and Kogan 2004, Secomandi 2010, Glasserman 2013), and ALP has been shown to perform poorly relative to least-squares Monte Carlo for real options pricing (Nadarajah et al. 2015, Nadarajah and Secomandi 2017). For our experiments, we consider the Bermudan option instances from Desai et al. (2012b) with up to a sixteen-dimensional state space and add the least-squares Monte Carlo policy, which is near-optimal in these instances, to our set of ALP benchmarks. We find that the self-guided FALP policy value is higher than the least-squares Monte Carlo policy value by 2% on average and by upto 4%, a significant improvement for this application. In contrast, the average performance of an application-specific ALP model and FALP are worse than least-squares Monte Carlo by roughly .

Our results show that self-guided FALP promises to reduce the ALP implementation burden and improve the effectiveness of its policies in a broader class of applications. This approach, which does not directly exploit domain knowledge, may not always improve on application-specific methods. Regardless, it can still serve as a useful benchmark to assess the value of procedures that exploit application structures. To facilitate such benchmarking, we have made Python code implementing the approaches developed in this paper publicly available.

1.1 Novelty and Contributions

Research on ALPs predominantly assumes a fixed set of basis functions and a heuristic choice of the state-relevance distribution. Work relaxing these assumptions, as we do, is limited.

Klabjan and Adelman (2007) is a seminal paper that develops a convergent algorithm to generate basis functions for semi-Markov decision processes. It requires the solution of a challenging nonlinear program. Building on this work, Adelman and Klabjan (2012) considered an innovative algorithm for basis function generation in a generalized joint replenishment problem. Their algorithm leverages structure and numerical experience for this application. Our approach differs from this work because it uses low-cost sampling to generate basis functions, focuses on discounted-cost MDPs, and is application agnostic.

Bhat et al. (2012) side-stepped basis function selection when computing VFAs by applying the kernel trick (see, e.g., chapter 5 of Mohri et al. 2012) to replace the inner-products of such functions in the dual of a regularized ALP relaxation. Guarantees on the approximation quality of their VFAs depend on the kernel and an idealized sampling distribution that assumes knowledge of an optimal policy. Our approach instead works directly on the primal ALP formulation and samples over the parameters of a class of basis functions as opposed to state-action pairs. Moreover, the sampling distribution is readily available in our framework and the error bounds that we develop are not linked to the knowledge of an optimal policy.

The papers above do not address the choice of the state-relevance distribution. Parametric forms for the state-relevance distribution that are close to the steady-state distribution of an optimal policy can be obtained for some queuing applications but not in general (De Farias and Van Roy 2003). The use of policies to choose this distribution in policy-guided FALP is based on an approach discussed in De Farias and Van Roy (2003, page 854) and Farias and Van Roy (2006), a version of which is employed in Sun et al. (2014). Self-guided FALP, while iterative, is fundamentally different as it leverages the ability to cheaply sample new random basis functions and uses only past VFA information available from solving an ALP model to guide new VFAs; we demonstrate that this can be interpreted as modifying the state-relevance distribution. Along with the theoretical guarantees already discussed, one can view self-guided FALP as a conceptually sound mechanism for updating the state-relevance distribution.

Overall, the exact representation of an MDP based on random bases, the FALP and self-guided FALP models, and their associated theoretical guarantees are novel. A useful property of our results is that they apply to MDPs with state spaces containing continuous and discrete elements. The implementation guidelines and our numerical study highlight how these developments can ease the use of ALP, while providing effective policies on two challenging applications. On the perishable inventory control problem, we close the optimality gaps of the prior application-specific policies on known instances and obtain near-optimal policies on much larger instances. For options pricing, self-guided ALP improves on least-squares Monte Carlo with problem-specific basis functions in terms of policy performance, which is encouraging.

Our work builds on the seminal research on random bases by Rahimi and Recht (2008a, 2008) and Rahimi and Recht 2009. There is extant literature applying this idea to data mining and machine learning applications (Lu et al. 2013, McWilliams et al. 2013, Beevi et al. 2016, and Wu et al. 2018) and to a value iteration algorithm by Haskell et al. (2020). These papers embed random bases in what amounts to a regression setting, whereas we show that such bases can be effectively used in ALPs that have complicated constraints. We also added to this literature in terms of theory. Our approximation guarantees for FALP adapt the arguments in Rahimi and Recht (2008) to an ALP setting and also strengthen the error bounds. Similar analysis of self-guided FALP, unfortunately, does not lead to insightful bounds. In this case, we develop error bounds based on functional projections, which is new to this literature, and potentially of independent interest.

More broadly, our work adds to the rich literature on reinforcement learning that attempts to reduce the burden of feature engineering (Mnih et al. 2015, Silver et al. 2017). Here, neural networks and deep learning have received significant research attention as they facilitate the approximation of complex functions with limited domain knowledge (Fujimoto et al. 2018, Osband et al. 2019, Franke et al. 2021). They give rise to VFAs that depend nonlinearly on the parameters but involve the solution of non-convex optimization problems (Wang et al. 2020). Our use of random basis functions in ALP also mitigates domain knowledge but it retains linear programming structure and can thus be viewed as a complementary strategy.

1.2 Organization of Paper

In §2, we present the standard linear programming approach to solve MDPs and then introduce an alternative approach that employs random basis functions. In §3, we discuss FALP. In §4, we present iterative FALP-based approaches: policy-guided FALP and self-guided FALP. In §5, we present extensions to discrete-state MDPs and finite-horizon MDPs. The numerical studies on perishable inventory control and options pricing are in §6 and §7, respectively. We conclude in §8. All proofs can be found in an electronic companion. Python code accompanying this paper can be found at https://github.com/Self-guided-Approximate-Linear-Programs.

2 Exact Linear Programs

In §2.1, we provide background on infinite-horizon, discounted-cost MDPs and their known linear programming MDP reformulations. In §2.2, we propose an alternative linear programming reformulation for MDPs based on random basis functions, which plays a central role in the approximations we consider in later sections.

2.1 Background

Consider a decision maker controlling a system over an infinite horizon. A policy assigns an action to each state , where denotes the MDP state space and represents the feasible action space at state . An action taken at state results in an immediate cost of and the transition of the system to the next state according to the probability distribution .

The decision maker’s objective is to find a stationary and deterministic optimal policy that minimizes discounted expected costs. Starting from an initial state , the discounted expected cost of a policy is

where denotes the discount factor, expectation is with respect to the state-action probability distribution induced by the transition probability distribution and the policy , and is the state reached at stage when following this policy. The quality of a given policy is evaluated with respect to a distribution for the initial state. Specifically, we define the cost of policy as .

The policy-cost minimization problem is

| (1) |

An optimal policy that solves (1) exists and the MDP value function satisfies . The state space is a continuous, compact real-valued set and the action spaces for all either share this property or are finite. Moreover, the MDP value function is continuous. The existence of in the literature is guaranteed under different requirements, mainly over the cost function and state transition kernel . Informally, one such set of conditions requires the lower semi-continuity of the immediate cost and the strong continuity of state transitions. We present them formally in §9.1 and refer to Theorem 4.2.3 in Hernández-Lerma and Lasserre (1996) for a more elaborate discussion. Continuous state spaces and value functions arise in applications such as lost-sales inventory control (Zipkin 2008), healthcare screening (Steimle and Denton 2017), dual sourcing (Hua et al. 2015), robotics (Peters et al. 2003, Haarnoja et al. 2019), and flight simulators (McGrew et al. 2010, Yang et al. 2019). Our models and analysis in the remainder of this section and §§3–4 focus on MDPs satisfying Assumption 2.1. We discuss in §5 how they apply to a broader class of MDPs, for instance, where the state space can have discrete components.

The computation of the value function can be conceptually approached without knowing via the exact linear program (ELP; see, e.g., pages 131-143 in Hernández-Lerma and Lasserre 1996)

| s.t. | (2) |

where is a state-relevance distribution that specifies the relative importance of each state in the state space. ELP is well defined because Assumption 2.1 ensures that the MDP value function solves the optimality equations for every . Thus, is an optimal solution to ELP, which follows from its constraints holding as equalities at . Since is continuous over a compact domain (Assumption 2.1), it is bounded and the objective function of ELP, which is an expectation of , is also bounded. However, ELP is intractable to solve since it is a doubly infinite linear program. It has continua of decision variables and constraints, one for each state and state-action pair, respectively.

2.2 Feature-based Exact Linear Program

To be able to approximate ELP, we present a reformulation of it below that relies on a class of random basis functions defined by a vector and an associated sampling density , where integer denotes the dimension of the state space . Consider scalar mapping . This mapping can be used to represent a random basis function over the state space as using the inner product . In other words, for a given , we can define the basis function . These basis functions are referred to as random basis functions because is sampled using . Table 1 lists the components of three random basis functions: the mapping , the sampling density for the vector , and the parameters defining this density. Fourier basis functions are defined using a cosine mapping with sampled from a uniform distribution with support involving the Archimedes constant and the remaining elements of sampled from a normal distribution with mean zero and standard deviation , which is a tunable scalar parameter. ReLU basis functions employ a mapping that is a maximum with respect to zero. It samples from a uniform distribution over a unit sphere with no tunable parameters. Stump basis functions use a signum mapping that evaluates to a , , or , depending on whether the input is negative, zero, or positive, respectively. The element is sampled from a uniform distribution with support over an interval that depends on a tunable scalar parameter . The remaining elements of are sampled from a uniform distribution defined on the discrete set , where , is a -dimensional unit vector with 1 in the -th coordinate and zero elsewhere.

Parameters Fourier , for ReLU None Stump ;

To approximate ELP, we consider random bases with known “universal” approximation power; that is, they can approximate continuous functions with arbitrary accuracy. Given a class of random bases, we define the following function over the state space using the pair containing an intercept and an integrable weighting function :

| (3) |

A class of functions that can be covered by this construction is

where the -norm of is defined as

When the random bases are universal, the class contains a function that is arbitrarily close to any continuous function under an -norm. Definition 2.1 formalizes universality, a property satisfied by the examples in Table 1. For a continuous function , the -norm is . We also use the shorthand for a function .

Definition 2.1

A class of random basis functions with sampling density is called universal if for any continuous function and , there exists such that and .

Since the MDP value function is continuous (Assumption 2.1), replacing it with the integral form (3) with universal basis functions should intuitively not result in any significant error. Performing this replacement and requiring the weighting function to have a finite norm as in the definition of gives the following linear program:

| s.t. | ||||||

Unlike ELP, which directly optimizes a value function, the above linear program optimizes the weights associated with the feature based representation of the value function in the set . Hence, we refer to it as the feature-based exact linear program (FELP).

Proposition 2.2 states an easily verifiable relationship between an optimal FELP solution and :

Proposition 2.2

If , there is an optimal FELP solution such that for all .

When using universal random basis functions, the assumption is mild. Specifically, if is continuous but not in , then an optimal FELP solution defines a function that is arbitrarily close to under an -norm as we show formally in §10.1. Assumption 2.2, which holds for the rest of the paper, includes and additional conditions needed for our theoretical analysis, all of which are standard in the random basis functions literature (see, e.g., Rahimi and Recht 2008, Theorem 3.2). {assumption} The MDP value function belongs to . The class of random basis functions is universal, and its sampling distribution has a finite second moment. Moreover, has a Lipschitz constant and satisfies and . This assumption is satisfied by Fourier and ReLU basis functions in Table 1 but not by Stump basis functions as they are not continuous. While Assumption 2.2 is needed for analysis, the algorithms we present in §§3–4 can be applied even when this assumption fails to hold.

3 Feature-based Approximate Linear Program

In §3.1, we introduce and analyze FALP, which is an approximation of FELP using random basis functions. In §3.2, we provide guidelines for the formulation and solution of FALP.

3.1 Model and Theory

In the literature, an ALP is derived from ELP by substituting its decision variable by a linear combination of pre-specified basis functions. Our starting point is instead FELP. We replace the integral form (3) with a sampled VFA

where are iid samples of the basis function vector from and is the finite weight vector . The weight represents an intercept as in FELP and the remaining elements of are weights associated with the random basis functions. In other words, is the finite analogue of the weighting function in FELP and can be viewed as an approximation constructed using a functional extension of Monte Carlo sampling applied to . The resulting ALP with random basis functions, denoted by , is

| s.t. | ||||||

This model is a semi-infinite linear program with variables and an infinite number of constraints. We assume the existence of a solution to . This is mild because we can always bound the absolute value of the elements of by a large constant to ensure the existence of a finite optimal solution without affecting our results. We show this formally in §10.2. {assumption} A finite optimal solution to exists.

Theorem 3.1 establishes key properties of and relies on the constant

where denotes the 2-norm, , is the Lipschitz constant of random basis defined in Assumption 2.2, and is the expectation under the distribution . Let represent an optimal solution to .

Theorem 3.1

The following hold:

-

(i)

For a given , we have for all .

-

(ii)

Suppose for all . Given , we have that any finite optimal solution satisfies

with a probability of at least .

Part (i) of this theorem shows that is well defined and provides a lower bound on the MDP value function at all states. The latter is a known result in approximate linear programming (see, e.g., §2 in De Farias and Van Roy 2003). Part (ii) establishes a high probability -norm error bound for this VFA. This bound decreases at the dimension-independent rate of akin to Monte Carlo sampling, which is encouraging. The magnitude of the error increases only logarithmically as a more stringent probability guarantee is needed, that is, is decreased, and its growth with the dimension of the state space is captured in . As is the case with Monte Carlo sampling, this suggests that more random basis function samples are needed to approximate value functions over higher-dimensional state spaces. Indeed, the nature of the MDP value function also affects the error and this factor is signaled by the presence of the term in the error bound. When the representation of is not unique, one can select such that norm is minimized and this minimum can be viewed as the approximation difficulty associated with when using a class of random basis functions. The condition in Theorem 3.1(ii) of is needed to avoid a situation where random basis functions with a certain set of values are needed to approximate the value function well but are not sampled because is zero in this set. This requirement is fairly mild. Sampling distributions with bounded support (e.g., uniform) clearly satisfy it. Since is finite, distributions with support over an unbounded set, such as the normal distribution, satisfy it with high probability because the sampled vectors highly likely come from a truncated version of the distribution, which has bounded support.

The error bound in Theorem 3.1 extends to ALP the random basis function sampling results in Rahimi and Recht (2008), which proposes a functional form of Monte Carlo sampling in the regression setting and assumes knowledge of the function being approximated. First, we contend with the feasibility of VFA weights, which is possible because a given infeasible solution to ALP can be made feasible by appropriately scaling the intercept . Second, a guarantee on the -norm distance between and is intuitively possible without the knowledge of because is known (see Lemma 1 in De Farias and Van Roy 2003) to be equivalent to

| (4) | ||||

| s.t. |

Third, have a -norm involving in our error bound, which improves on an -norm variant of this term in the original bound of Rahimi and Recht (2008), because we employ a solution construction in the proofs that differs from the one used in that paper.

The utility of a VFA is that it can be used to obtain a policy. Given VFA weights , we can define a so-called greedy policy associated with (see, e.g., Powell 2007). The action taken by this policy at state solves

| (5) |

The cost of the greedy (feasible) policy, which we denote by , is an upper bound on the optimal policy cost.

3.2 Implementation Guidelines

The literature contains three general strategies to solve , which we overview. The most commonly used approaches are constraint generation and constraint sampling (Adelman and Klabjan 2012, De Farias and Van Roy 2004), which both rely on solving a relaxation of a , but differ in how they construct the relaxation. Constraint generation works in an iterative fashion and starts with a subset of constraints. Given an optimal solution of this relaxation, it identifies the most-violated ALP constraint, if any, adds this constraint, and repeats the procedure until no violated constraint is identified, at which point the incumbent solution is optimal to . In principle, constraint generation can be used to obtain a near-optimal ALP solution and a lower bound on the optimal policy cost. The computational feasibility of this approach depends on the separation problem. Examples of its success in the literature rely on formulating this separation problem as a linear, convex, or mixed integer program (Adelman 2004, Zhang and Adelman 2009, Adelman and Klabjan 2012). Constraint sampling instead constructs a random relaxation of by sampling a finite number of its constraints. It is easy to implement but its performance depends on the constraint sampling distribution and it does not directly provide a lower bound on the optimal policy cost. A more recent approach for tackling employs a saddle-point reformulation and applies a first order method to it. This approach is referred to as constraint violation learning (Lin et al. 2020).

We outline in more detail a hybrid approach that uses constraint sampling to solve , as it is the easiest to implement, and then relies on another approach to obtain a lower bound on the optimal policy for benchmarking. The key step is to replace the set of constraints in with a subset obtained by sampling iid state-action pairs from a probability distribution over the state-action space (Calafiore and Campi 2005). The result is the following linear program with random basis functions and constraint samples:

| (6) | ||||||

| s.t. | ||||||

Proposition 3.2 is an application of a key result in Calafiore and Campi (2006) and shows that the linear program (6) for large enough provides a good randomized approximation of .

Proposition 3.2 (Theorem 1 in Calafiore and Campi 2006)

Given , if is supported over , linear program (6) is bounded, and

then for every optimal solution to this program, the following inequality holds

with a probability of at least .

In particular, this proposition shows that as more samples are added the set of states where the FALP constraints are violated when measured using is at most and this holds with a probability of at least . Therefore, if one solves the constraint-sampled version of FALP (6) with a large number of samples , we expect the results in Theorem 3.1 to hold approximately.

A sharper constraint sampling result specific to ALP can be found in De Farias and Van Roy (2004, Theorem 3.1) when is chosen using information from the optimal policy, which is unknown. During implementation, can be a uniform distribution or based on states visited by a baseline policy. Expectations in (6) are typically replaced by sample average approximations. The number of constraint samples can be chosen so that the optimal objective function of (6) does not increase significantly as more samples are added. The optimal solution to (6) defines a VFA , which can be used to obtain a greedy policy. To obtain a lower bound for benchmarking, one could use as a starting point in an approach to solve to that does provide a bound, such as constraint generation or constraint violation learning (see 12). Alternatively, one could use the VFA defined by in the information relaxation and duality approach to generate lower bounds (see Brown and Smith 2021 for details).

The quality of the VFA obtained using the above procedure depends on how FALP is formulated, in particular, the number of basis function samples , the choice of random basis functions, and the state relevance distribution . We provide some guidance on these choices next.

Similar to standard Monte Carlo sampling, the value of depends on the computational budget. That is, one determines the largest for which the sampled version (6) of can be tackled within a reasonable time limit (and possibly memory limit) using an off-the-shelf commercial solver. The ability of getting good VFAs with a small number of basis functions is thus an important consideration in choosing random basis functions. While multiple universal random basis functions guarantee the same theoretical convergence rate, their empirical rates may differ. A good starting point is to consider Fourier random basis functions (see Table 1), as they are known to provide better approximations as the continuous function becomes smoother (please see §2.1.1 of Canuto et al. 2012 and Nersessian 2019 for recent examples). The non-smoothness of the MDP value function in several applications is localized, that is, even these value functions are smooth in most neighborhoods. Given a choice of random basis functions, the tunable parameters are a few and do not depend on the application. The random bases examples in Table 1 have at most one such parameter. Thus, we recommend using cross-validation with the goal of minimizing the objective function of FALP for small values of to determine the parameter values of random basis functions. Fourier basis functions, which depend on a single bandwidth parameter, tuned using the aforementioned simple cross-validation strategy, worked well in both applications in our numerical experiments. The second decision factor could be computational. For example, in some applications, choosing an appropriate random basis function may facilitate the use of constraint generation. This is the case in the generalized joint replenishment studied in Adelman and Klabjan (2012). The separation problem in this application can be formulated as a mixed-integer program when employing random stump basis functions, which are piecewise constant.

The state-relevance distribution plays an important role in linking the quality of the VFA to greedy policy performance (De Farias and Van Roy 2003, Desai et al. 2012a, Sun et al. 2014). Proposition 3.3 formalizes this link using the state-visit frequency of a greedy policy, which defines the following probability of visiting a subset of states (see, e.g., pages 132–133 in Hernández-Lerma and Lasserre 1996):

| (7) |

where state and transition probability distribution retain their definitions from §2, and is the probability of the initial state belonging to . The expectation is taken with respect to control policy and initial state distribution over initial state .

Proposition 3.3 (Theorem 1 in De Farias and Van Roy 2003)

For a VFA such that , we have

Proposition 3.3 shows that for a VFA that lower bounds (e.g., the FALP VFA), the additional cost incurred by using the greedy policy instead of the optimal policy is bounded above by the -norm difference between the VFA and the MDP value function . This result motivates the search for good VFAs.

If and are identical, Proposition 3.3 and the reformulation (4) imply that a FALP VFA with a small -norm error also guarantees good greedy policy performance. However, one does not know before solving FALP, which makes this choice challenging (De Farias and Van Roy 2003). Heuristics in the literature can be interpreted as approximating the expression (7) for . The first approach sets equal to the initial state distribution , which ignores the second term in (7) that captures the effect of states visited by the policy in the future. This observation motivates the second strategy, in which a baseline policy is simulated to approximate the aforementioned second term. That is, replaces the greedy policy in (7). The effectiveness of this approach depends on how close the states visited by the simulated heuristic policy overlap with those of good greedy policies. The third approach chooses to be a uniform distribution, which can be interpreted as acknowledging that we do not have any information about . The effectiveness of these approaches will need to be tested numerically.

4 Guided Feature-based Approximate Linear Programs

In this section, we discuss iterative strategies to mitigate the impact of the initial state-relevance distribution choice in FALP. In §4.1 and §4.2, we describe such existing and new strategies, respectively. We take Assumption 3.1 to hold in these subsections and then discuss implementation and solution guidelines in §4.3.

4.1 Policy-guided FALP

We summarize in Algorithm 1 a procedure described in De Farias and Van Roy (2003) and Farias and Van Roy (2006) that uses policies to guide the choice of the state-relevance distribution. To faciltate exposition, we make the dependence of on explicit by writing []. The procedure starts by solving [] based on an initial state-relevance distribution choice to obtain the VFA weights . Then, it simulates the greedy policy to obtain the state-visit distribution. This distribution is chosen as the new state-relevance distribution . Iteration 1 starts by solving [] and so on. A total of iterations are performed, after which the VFA weight vector is returned. We refer to Algorithm 1 as policy-guided FALP. As Algorithm 1 iterates, one hopes that the state-relevance distribution overlaps more with states visited by good greedy policies but there is no gurantee that this will happen.

4.2 Self-guided Approximate Linear Programs

We present a new iterative scheme that leverages our ability to inexpensively sample new random basis functions to guide the state-relevance distribution. Specifically, this scheme gradually increases the number of basis functions in FALP by sampling new batches of random basis functions of size and adds guiding constraints to FALP that link the VFAs across consecutive iterations. For a given , we refer to this modification of as . We first present the modified model and explain its interpretation as a mechanism to update the state-relevance distribution, before formalizing an algorithm and providing theoretical support.

Denoting by an optimal solution to , the model is

| s.t. | (8) | ||||

| (9) | |||||

The only difference between and is that the former linear program includes additional constraints (9) that require its VFA to be a state-wise upper bound on the VFA , which is computed in the previous iteration by solving . The VFA weights are feasible to . We assume for all when , which implies that the constraints (9) are redundant in the first iteration. Dualizing these additional constraints provides insight into . Let denote the optimal dual value associated with the constraint (9) at state . Define a state-relevance distribution that evaluates at this state to

If strong duality holds, then we have that an optimal solution of solves

The main takeway from this reformulation is that can be viewed as modifying the state-relevance distribution using its own past VFA information, that is, the VFA. Thus, we refer to the iterative scheme involving , which is summarized in Algorithm 2, as self-guided FALP. For brevity, we do not discuss the technical conditions for strong duality here (see, e.g., Shapiro 2009, Theorem 2.3, and Basu et al. 2017, Theorem 4.1) because the constraints will be sampled during implementation, in which case standard strong duality for finite linear programs will apply.

The inputs to Algorithm 2 are similar to Algorithm 1, except for the batch size , which replaces the apriori fixed number of basis functions across iterations. At each iteration, Algorithm 2 (i) samples a batch of vectors of size and includes them in the current set of such vectors and increases the basis function count by , and (ii) solves a revised model formulated with these additional random basis functions and the VFA computed in the previous iteration. After iterations, it returns the VFA weights , where .

Proposition 4.1

For any integer , it holds that

| (10) |

The equality in (10) follows from our assumption that . The relationship holds for all and by Part (i) of Theorem 3.1 because is feasible to ; thus, it is also feasible to . The inequalities of the type are directly implied by the self-guiding constraints (9).

An important consequence of Proposition 4.1 is that Algorithm 2 generates a sequence of VFAs that draws (weakly) closer to at all states. Therefore, two consecutive VFAs with and random basis functions satisfy

for any proper distribution defined over the state space and, in particular, when is the state-visit frequency associated with the greedy policy . As a result, for any fixed iteration index and its corresponding state-visit frequency , it follows that the sequence of VFAs generated by Algorithm 2 improves the worst-case performance bound of Proposition 3.3, that is, is non-increasing in . These results, together with our Lagrangian reformulation of , show that self-guided FALP embeds a mechanism to adaptively update the state-relevance distribution such that a worst-case performance of their greedy policies is (weakly) improving. To understand this mechanism, recall the regression reformulation of ALP in (4), which shows that considers a candidate set of VFAs that satisfy constraints (8) and chooses its VFA as the one in this set that minimizes the -norm with respect to . The guiding constraints (9) impose the additional condition that the so computed VFA cannot worsen the -norm distance to of the most recently computed VFA. Thus, from a VFA error minimization perspective, self-guiding FALP can be seen as using iteration to guard against -norm improvements leading to a worsening of the -norm distance to .

Studying the quality of the sequence of VFAs generated by Algorithm 2 is challenging because consecutive VFAs in this sequence are coupled by the guiding constraints (9). Given the VFA generated by solving , we bound the -norm error of a VFA that is constructed with additional random basis functions, is feasible to constraints (8), and near feasible to (9). The techniques used to obtain a sampling bound for in Theorem 3.1 (understandably) do not factor in the effect of and, thus, do not provide a useful error bound of the type we require here (please see Online Supplement §11 for details). Therefore, we develop a new projection-based analysis.

Consider the set of functions spanned by an intercept plus a linear combination of random basis functions in set :

A strategy to account for the impact of on is to ask if is a part of the functional space containing . If , then it would not be possible to improve the incumbent VFA via additional sampling. If , then intuitively has a (projected) component in the functional space , as well as a nonzero (projected) component in the orthogonal complement of this space. We then bound the approximation error pertaining to this orthogonal component as increases, which allows us to bound the error of a VFA in that is feasible to .

Formally, we decompose into a component that belongs to and a residual in an orthogonal complement space. Such decomposition is possible because the closure of is a Hilbert space (by Proposition 4.1 in Rahimi and Recht 2008), where an orthogonal decomposition is well defined (by Theorem 5.24 in Folland 1999). Because by Assumption 2.2, we can decompose it into and , that is, , where and are projections of on to and its orthogonal complement (to be precise, the projections are performed on to the closures of these sets). Based on this construction, we have the below theorem. For given positive integers and , define the constant

Theorem 4.2

Theorem 4.2 establishes that with a high level of probability the set will contain a VFA satisfying the FALP constraints that simultaneously approaches at all states (i.e., -norm) and becomes more feasible to the guiding constraints at the dimension-free rate of . This rate is analogous to the one associated with FALP in Theorem 3.1, and so is the structure of the error bound. There are two distinct features of the bound in Theorem 4.2 worth noting. First, it contains the norm in lieu of . It is easy to verify that if the projection of onto is nonzero. The difference between these norms signals the quality of the most recently computed VFA . This suggests that the number of additional samples needed to obtain a good approximation of decreases with , that is, when is itself closer to . Second, Theorem 4.2 provides a rate at which the infeasibility of the guiding constraints decreases with . This is because of the worst-case nature of the analysis. Specifically, it is possible for the reference VFA in the guiding constraints to be very close to , in which case, satisfying the guiding constraints determines the worst-case distance of the new VFA from . In practice, this is unlikely to happen, and the key insight from Theorem 4.2 is that good -norm solutions will likely be a part of the feasible set as increases, which is corroborated by our numerical experience.

4.3 Implementation Guidelines

We discuss the implementation guidelines for algorithms 1 and 2, focusing on parameter choices and solution issues that were not already discussed in §3.2.

The additional parameters needed for the implementation of policy-guided FALP are the numbers of the basis functions and iterations and , respectively. As becomes larger, the time for a single iteration of Algorithm 1 increases, which includes solving and simulating the greedy policy. This is because will have more variables, so we need to evaluate expectations of a larger number of random basis functions during policy simulation. A sequential strategy is to first select such that the per iteration cost allows for choosing such that a few iterations can be performed within an acceptable time limit.

For self-guided FALP, we need to choose the batch size and the number of iterations . These choices become easier if we fix a target number of basis functions following the logic discussed for FALP in §3.2. Then, smaller values of entail solving linear programs with fewer decision variables and doing so more often. In other words, the per iteration cost is lower with smaller , but more iterations are needed and the improvement between iterations will likely be smaller. Therefore, the value of can be selected to balance improvement in the self-guided FALP objective function value and the per-iteration cost. Solving self-guided FALP requires handling the guiding constraints (9). We suggest replacing these constraints with a sampled subset, as done for FALP in §3.2. Under such replacement, analogues of Proposition 4.1 and the discussion following it hold over the sampled states. Similar to the implementation of FALP in §3.2, if we also replace constraints (8) with sampled constraints, we expect the results in Theorem 4.2 to hold approximately as is sufficiently large.

Although we consider an iteration limit as the stopping criterion in algorithms 1 and 2, several alternatives are possible. For instance, the iteration limit can be replaced by a time limit, or both types of limits can be imposed together. Another strategy is to look at the improvement of consecutive policies and stop when these improvements are smaller than a certain threshold. If a lower bound on the optimal policy cost is available, these improvements can be converted to optimality gaps, and a termination gap can be set.

5 Extensions

Although we have assumed continuous state spaces and value functions thus far, the random basis function sampling approach underpinning our models can be readily extend to handle discounted cost MDPs with finite state spaces. A special structure that arises in important applications is a state space with a low dimensional discrete component and a high dimensional continuous component (e.g., financial and real options pricing). In this case, it is common to define a separate continuous VFA for each discrete state value, and our results directly apply. Next, we handle the more general case when such a strategy may not be computationally feasible.

Consider the analgoue of the MDP in §2.1 with a discrete state space , where is a finite index set and each state is a bounded real value. We denote by the MDP value function. Proposition 5.1 provides a bound on the -norm error between the VFA and , which decreases at a rate of as more random basis functions are sampled. Such a bound is possible because we can construct a continuous extension of , as discussed next. Let be the smallest continuous and compact set containing . It is easy to verify that the following continuous function defined for each coincides with at all the discrete states:

where is a positive constant. We assume , in which case, we have for some (the results extend to the case when , as explained in §2 and in 10.1). Compared with Theorem 3.1 in the continuous state space case, the weighting function is replaced by , and the constant is instead

where . Here, we will continue to use the notation related to from §3.1 and define to denote the -norm distance over the discrete state space, which is .

Proposition 5.1

When the action space is finite for all states, we can drop Assumption 3.1 and establish the existence of a finite optimal solution, although as discussed in §3.1, this assumption is already mild. We highlight that the construction of does not change based on the structure of the state space since the sampling distribution does not depend on this structure. Therefore, the same procedures for generating basis functions apply in the discrete state space case. Using the arguments here, we can also handle state spaces with a mixture of discrete and continuous elements.

Our results also extend to handle MDPs with a finite horizon by considering time to be in the state; that is, we can define the state as . Because the options pricing application in §7 gives rise to a finite-horizon MDP, we formulate next in the more familiar notation of such MDPs. Let the index set of stages in the horizon be . The MDP value function at stage is , and we assume without a loss of generality that . At stage , the state space is , and the action space at this stage and state is . Then, the finite horizon analogue of computes VFAs that approximate at each stage by sampling :

where are the stage VFA weights. Because the sampling distribution does not depend on the stages or state space, the set of random basis functions can be the same across stages, which also provides the flexibility to use the same basis function weights across stages if needed. Assuming that the state-relevance distribution is defined over the stage state space (it could easily be defined over the state spaces at all stages), in the finite horizon setting is s.t. where and , respectively, are the stage cost function and expectation under the state transition function from stage to . We omit the terminal condition for brevity. Theoretical guarantees that are analogous to the infinite horizon case for FALP and self-guided FALP can be derived in the finite horizon setting as well.

6 Perishable Inventory Control

We perform a numerical study on the perishable inventory control problem considered in Lin et al. (2020, henceforth abbreviated LNS). We discuss the infinite-horizon discounted cost MDP formulation of the problem and instances in §6.1, the experimental setup in §6.2, and numerical findings in §6.3.

6.1 MDP Formulation and Instances

Managing the inventory of a perishable commodity is a fundamental and challenging problem in operations management (Karaesmen et al. 2011, Chen et al. 2014, Sun et al. 2014, and LNS). We study a variant of this problem with partial backlogging and lead time from §7.3 in LNS.

Consider a perishable commodity with and periods of life time and ordering lead time, respectively. Ordering decisions are made over an infinite planning horizon. At each decision epoch, the state vector is of size . The state element for is the previously ordered quantity that will be received periods from now. If , for is the amount of available commodity with periods of life remaining. If , the values of these state elements are notional quantities to compute the total on hand inventory, which is . Inventories and take values in the interval for all and , respectively, where denotes the maximum ordering level. If , then the onhand inventory is non-negative. Instead, if , then the on-hand inventory is negative and represents the amount of backlogged orders.

The demand for the commodity is governed by a random variable. In each period, we assume that the demand is realized before order arrival and is satisfied in a first in-first out manner. Given a demand realization , taking an ordering decision (i.e., action) from a state results in the system transitioning to a new state

where and is a maximum limit on the amount of backlogged orders, beyond which we treat unsatisfied orders as lost sales. The updating logic in the first element of ensures that the backlogging limit is enforced. This can be understood as follows: If there was no backlogging limit, then the on-hand inventory after demand realization and before order arrival would be ; instead, in the presence of the maximum backlog limit , this total on-hand inventory of is greater than or equal to if and only if . The remaining elements of are shifted elements of , with the last element accounting for the latest order .

The immediate cost associated with a transition from a state-action pair is

|

|

where expectation is given with respect to the demand distribution. The per-unit ordering cost is discounted by because we assume payments for orders are made only upon receipt. The holding cost penalizes leftover inventory , while the per-unit disposal and backlogging costs and factor in, respectively, the costs associated with disposing units and backlogging units. Finally, each unit of lost sales is charged .

We consider 24 perishable inventory control instances – twelve from LNS with (three-dimensional state space) and twelve new higher-dimensional instances. Six of the new instances have and (five-dimensional state space), and the remaining six instances have and (ten-dimensional state space). Similar to LNS, across all instances, we fix the demand distribution to a truncated normal distribution with a mean of and support in the range . We require the maximum limit on the amount of backlogged orders to equal the maximum ordering level, that is, . We vary the cost function parameters, the discount factor , the maximum ordering level , and the demand standard deviation . Their specific values are shown in tables 2–4.

6.2 Computational Setup

We formulate using the guidelines in §3.2. We use Fourier basis functions, with its bandwidth parameter chosen via cross validation over the candidate set . For , we considered both the initial MDP state of (i.e., a degenerate initial distribution ) and a uniform distribution over the hyper-cube . The latter choice leads to substantially better policies, so we report the results only for this choice. We use constraint sampling to solve and choose state-action pairs sampled from a uniform distribution over the hyper-cube . The number of basis functions was set to , , and for the three-, five-, and ten-dimensional instances, respectively. We approximate expectations in using sample average approximations constructed using iid samples.

We formulate policy-guided FALP and self-guided FALP using the guidelines in §4.3. For the former model, we set equals 5, and for the latter one, we set equal to , , and on the three-, five-, and ten-dimensional instances, respectively. We keep the samples of the basis functions and constraints in these models the same as for each instance. In particular, the guiding constraint in self-guided FALP are added for the states that appear in the state-action pair samples used to construct . We use the notation and when reporting the results for policy-guided FALP and self-guided FALP, respectively.

We use the Gurobi commercial solver to solve linear programs. We simulate greedy policies using sample paths to estimate their value. Similar to LNS, we replace the action space by equally spaced points and find the best action by using enumeration. We estimate the lower bounds using an approximate version of the constraint violation learning approach that only performs dual updates involving Markov Chain Monte Carlo samples, for which we use the Metropolis–Hastings algorithm with independent Markov chain trajectories with a length of and a burn-in size of . Please see 12 for details. The maximum standard errors of all estimates were less than . In addition, to understand the variation caused by solving sampled models, for each instance and method, we repeat the solution of the models and simulations to estimate bounds ten times, that is, we perform ten trials.

LNS LNS 2 5 10 10 0.0 0.1 2.3 0.0 2 5 10 50 6.5 2.4 1.2 2.2 5 10 8 10 3.6 0.0 3.7 0.0 5 10 8 50 13.0 2.2 12.7 3.3 2 10 10 10 0.8 0.0 1.8 0.1 2 10 10 30 5.1 1.6 2.3 2.1 Average 4.8 1.0 4.0 1.2

6.3 Results

Table 2 reports the optimality gaps of and the LNS method, which solves an ALP model that embeds a fix set of 19 application-specific basis functions that involve hinges (i.e., ) to mirror the structure of the cost function presented in §6. Optimality gaps are computed using the lower bound. For each instance, the reported values are averaged over the 10 trials. For a discount factor of , the LNS and optimality gap ranges are – and –, respectively. The behavior is similar for the larger discount factor of . The variation of the optimality gaps across 10 trials is less than 1% across instances; that is, the policy cost is robust to the resampling of random bases and constraints. The significant improvement of over the LNS method highlights the value of using sampled random basis functions, which are not designed based on application structure. The policy and lower bound of the former model are near-optimal and close the gap on almost all the three-dimensional instances. In addition, these results show that more advanced iterative methods to guide state-relevance choice, such as policy-guided FALP and self-guided FALP, are not needed on these instances. In fact, we confirmed that the performance of the policy-guided FALP and self-guided FALP policies are comparable to the ones from FALP on these instances.

1 8 2 5 16.3 9.9 8.7 1 8 2 2 18.7 12.4 9.1 1 2 8 5 13.6 21.3 7.3 1 2 8 2 10.6 6.2 4.2 2 8 5 5 13.2 7.6 9.6 2 8 5 2 13.6 10.0 7.1 Average 14.3 11.2 7.6

Table 3 compares the (average) optimality gaps of the , , and policies on the five-dimensional instances. The optimality-gap ranges for these respective policies are 10.6%–18.7%, 6.2%–21.3%, and 4.2%–9.6%. Across the 10 trials in each instance, the optimality gaps vary by at most 1% for and and by at most 10% for . Policy-guided FALP exhibits somewhat unstable behavior as witnessed by the larger optimality gap range and performance variance across trials. In contrast to the three-dimensional instances, we see here that without state-relevance distribution (guiding) updates, can lead to highly suboptimal policies. Despite the weak policies, the lower bound used to compute the optimality gap is excellent as witnessed by the results. This observation is consistent with the discussion in §3.2 and §4.2, suggesting that ALP VFAs providing good lower bounds may not provide good policies because of a poor state-relevance distribution choice. The policy-guided FALP policy improves on the FALP policy on almost all instances, except for one instance, where it has a substantially worse optimality gap. Self-guided FALP leads to consistent and large improvements over FALP across all the instances, as well as a significant benefit over policy-guided FALP, again with the exception of one instance. This underscores the value of the guiding mechanism underpinning self-guided FALP.

1 8 2 5 11.9 26.4 7.3 1 8 2 2 5.9 10.4 4.7 1 2 8 5 10.9 23.8 7.4 1 2 8 2 7.4 10.6 5.9 2 8 5 5 12.4 27.7 7.3 2 8 5 2 9.2 13.2 7.2 Average 9.6 18.6 6.6

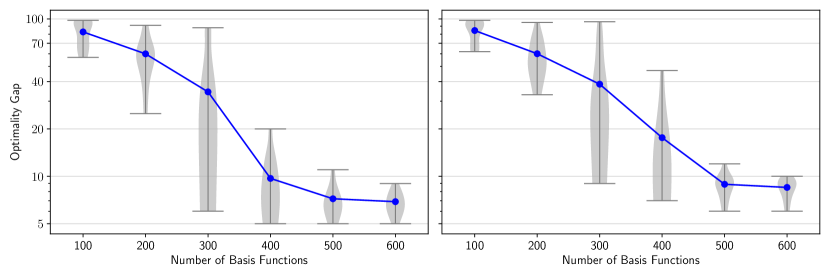

Table 3 reports the (average) optimality gaps of the and policies on the ten-dimensional instances computed using the lower bound. We were unable to obtain reliable results with because it results in very erratic behavior as we iterated the steps in Algorithm 1. This observation is consistent with the behavior reported by Farias and Van Roy (2006) on a Tetris application when using policy guided state-relevance distribution updates. In particular, they observe improvement in policy performance for the first few iterations and then an unexplainable dropoff. We also added as a benchmark to see if additional random basis functions in FALP help. The optimality gap ranges for , , and are 5.9%–12.4%, 10.4%–27.7%, and 4.7%–7.3%, respectively. The optimality gap variation across trials is at most 2.3%. Once again, policies based on adhoc state-relevance distribution choices can perform poorly, even if they have a sufficient number of basis functions, as shown by the substantially worse performance of compared with . The optimality gaps of show that the lower bounds from are very good. The mechanism in self-guided FALP to guide the state-relevance distribution adds significant value relative to the benchmarks and leads to excellent policies. It improves on the policy by an average of 3% and by as much as 5%. To gain some insight into how the self-guiding mechanism in helps, we display the average optimality gap of the policy on two representative ten-dimensional instances as basis functions are iteratively added in batches of 100, as well as, a violin plot for each iteration showing the variation of the optimality gaps. At the beginning (100 basis functions), the policies are bad across all trials. After a few iterations (200 and 300 basis functions), the variation of optimality gaps increases, and we find very good policies in some trials and poor policies in others. In subsequent iterations, the variance of policy performance quickly decreases, and at 600 basis functions, the worst case optimality gap across trials is less than 10%. Our results on the ten-dimensional instances when compared to those on the three- and five-dimensional instances suggest that the importance of the state-relevance distribution becomes more critical for higher dimensional problems. Intuitively, this would happen if near-optimal policies visit smaller and smaller regions of the state space as its dimension becomes larger, in which case, there is a greater need for having a good state-relevance distribution that aligns the ALP VFA error minimization objective with policy performance. The guiding mechanism in helps with such alignment.

Finally, as expected, the average run times increase as we employ more basis functions and move to higher dimensional instances. On the three-dimensional instances, these run times for and the LNS method were six and three minutes, respectively. For instances with a five-dimensional state space, , , and take on average 12, 108, and 32 minutes, respectively. The average run times of , , and were 23, 86, and 54 minutes, respectively, on the ten-dimensional instances. Thus, the computational times of self-guided FALP to obtain the policy improvements discussed earlier are encouraging.

7 Bermudan Options Pricing

We perform a numerical study on the Bermudan option pricing problem in Desai et al. (2012b, henceforth abbreviated DFM). In §7.1, we present the finite-horizon discounted MDP formulation. In §7.2, we describe our computational setup. In §7.3, we discuss the results and findings.

7.1 MDP Formulation

We consider the pricing of a knocked-out Bermudan call option with assets over a finite time horizon. The components of the finite-horizon MDP formulation will be presented following the notation in §5, but with one exception: instead of a cost function , we use a reward function . The option has exercise opportunities over years; that is, exercise is possible at times , where . The asset prices at stage are , where is the price of the -th asset at this time. Prices evolve according to a multi-asset geometric Brownian motion. The option becomes worthless any time the maximum of the asset prices exceeds a pre-specified barrier price . We use the binary variable to indicate if the option is knocked out at time . It takes a value of one in this case and is zero otherwise. The transition equations governing are and for , where {a} equals one if is true and zero otherwise. At time , the MDP state is given by the vector that belongs to the state space . The MDP action is binary, with values of one and zero corresponding to “stop” and “continue,” respectively. Stopping at stage yields the reward , where the discount factor , is the risk-free interest rate, and the payoff function with respect to a pre-specified strike price is

A continue decision at state has zero reward, that is, . The objective is to find an exercise policy that maximizes the discounted expected reward.

Our experiments use nine instances from DFM, for which , , , , and are 3, 54, 100, 170, and 5%, respectively. The geometric Brownian motion driving the prices has zero correlation and volatilities equal to . All assets share the same initial price , that is, . This price is varied between , and , and the number of assets takes on the values , and . Although the asset prices can take values greater than the barrier price , they need not be included in the state space because the option becomes worthless at all such prices. Thus, the range of each price relevant to the MDP belongs to the interval .

7.2 Computational Setup and Benchmarks

Our setup of models mirrors §6. We formulate the finite-horizon version of given in §5 using Fourier random bases, with its bandwidth parameter chosen via cross-validation over the candidate set . The strategy of using a policy to obtain a state-relevance distribution in §3.2 is simplified because the exercise decisions do not affect prices. Therefore, the price-portion of the state evolves according to the geometric Brownian motion model, regardless of the policy used. Motivated by this property, we use a lognormal state-relevance distribution of prices. We find that performs much better with this choice than a uniform distribution. We do not consider policy-guided FALP given its unstable behavior. For self-guided FALP, we choose equal to ; that is, we consider . We sample the constraints of both and by generating trajectories of prices from the geometric Brownian motion model. We approximate the expected values by sampling 500 transitions from this model.

We consider two application-specific benchmarks. The first is a least squares Monte Carlo (LSM), which is popular for financial and real option valuation (Carriere 1996, Longstaff and Schwartz 2001, Glasserman and Yu 2004, and see Nadarajah and Secomandi 2021 for a recent review) and provides very good policies on the instances we consider. LSM approximates the optimal continuation function with the boundary condition using a backward recursive scheme that uses a regression. To construct the continuation function approximation, we use the same application-specific basis functions considered in DFM, which are , , and for . We use 100,000 sample paths to estimate the weights of these basis functions at each time . Our second benchmark is an ALP with the same basis functions as LSM. We denote this model by ALP. We construct the constraints of this model using the same price trajectories and transitions used in the construction of .

We simulate 20,000 price trajectories to evaluate the value of greedy policies, which provide a lower bound on the optimal policy value (because we are maximizing reward). The maximum standard error of these estimates is 0.4%. We benchmark the performance of all policies using the essentially optimal upper bound for these instances from the pathwise optimization approach of DFM. For each instance and method, we perform ten trials.

LSM ALP 4 90 6.8 5.1 2.8 2.8 4 100 6.1 5.9 3.7 3.6 4 110 5.0 6.2 5.7 3.5 8 90 5.9 5.5 3.4 3.3 8 100 4.3 5.8 8.5 1.8 8 110 3.0 5.5 16.0 1.4 16 90 3.9 5.4 2.3 2.3 16 100 2.6 5.0 1.8 1.6 16 110 1.9 4.4 1.7 1.2 Average 4.4 5.4 5.1 2.4

7.3 Results

Table 5 reports the optimality gaps of LSM, ALP, , and on the nine DFM instances averaged across 10 trials. The respective optimality gap ranges for each method are 1.9%–6.8%, 4.4%–6.2%, 1.7%–16%, and 1.4%–3.6%, which shows that the policy is near optimal and improves on the remaining benchmarks. The performance of the policy is within 1% of the one from on six of the nine instances but 2.2%, 6.7%, and 14.6% worse on the remaining instances. Once again, we see significant value in updating the state-relevance distribution using the logic in . There is no clear ordering between the policies of ALP and LSM – the average optimality gap of the LSM method across all the instances is 1% smaller than ALP. The policy is significantly better than the LSM policy, with improvements of less than 2% on 5 instances and greater than 2% on the remaining four. The largest such improvement is 4%.

The policy improvements obtained using over LSM are comparable to or larger than those reported in DFM with a pathwise optimization policy. The superior self-guided FALP policies come at a computational cost. The average runtime of LSM, ALP, and across trials and instances are, respectively, 2.42, 5.1, 99.5, and 117.9 minutes. There is thus an additional, albeit manageable, computational overhead to obtain the improved policies.

A broader takeaway from these experiments is that an application-agnostic ALP model with random basis functions and a guided state-relevance distribution can provide near-optimal policies for a challenging option pricing problem, also improving on application-specific benchmarks.

8 Conclusions

We revisit the approximate linear programming approach for computing value function approximations (VFAs) for Markov decision processes (MDPs). We focus on the key choices needed to formulate an approximate linear program (ALP) that affects the quality of the VFA and its associated policy. The first is the selection of the basis functions defining the ALP VFA, and the second is the choice of a state-relevance distribution in the ALP objective. These choices are typically made in an ad-hoc manner based on domain knowledge, which limits the applicability of ALP. We embed VFAs based on cheaply sampled random basis functions in ALP, hence sidestepping the need for ad-hoc basis function engineering. We refer to this model as feature-based ALP (FALP). We also propose an iterative scheme to guide the state-relevance distribution in FALP using its past VFA information, which leverages the ability to add new random basis functions in an inexpensive manner. We develop error bounds for the VFAs from these models and also show that self-guided FALP has desirable theoretical properties not shared by an existing iterative scheme for updating the state-relevance distribution. We test FALP and self-guided FALP on challenging perishable inventory control and option pricing applications. Self-guided FALP outperforms FALP and application-specific benchmarks. Our findings showcase the potential for our procedure to (i) significantly reduce the implementation burden of using ALP and (ii) provide an application-agnostic policy and lower bound for MDPs that can be used to benchmark other methods.

Our research suggests several interesting directions for future work, of which we state two. The first is to study the possibility and value of a guided sampling mechanism for ALP where the new samples of random basis functions leverage information from past VFAs. Approaches for the data-dependent sampling of random basis functions in machine learning (see, e.g, Sinha and Duchi 2016, Shahrampour et al. 2018) can query the function being approximated, which is the unknown MDP value function in our setting. It is unclear how to develop inexpensive and approximate queries of the MDP value function that still provide useful information, which would be needed to obtain an effective and efficient sampling approach. The second is to investigate the value of random basis functions in other approximate dynamic programming methods and compare against neural networks and deep learning that also attempt to mitigate tuning but lead to nonlinearly parametrized VFAs, which are typically harder to train.

References

- Adelman (2003) Adelman D (2003) Price-directed replenishment of subsets: methodology and its application to inventory routing. Manufacturing & Service Operations Management 5(4):348–371.

- Adelman (2004) Adelman D (2004) A price-directed approach to stochastic inventory/routing. Operations Research 52(4):499–514.

- Adelman and Klabjan (2012) Adelman D, Klabjan D (2012) Computing near-optimal policies in generalized joint replenishment. INFORMS Journal on Computing 24(1):148–164.

- Adelman and Mersereau (2013) Adelman D, Mersereau AJ (2013) Dynamic capacity allocation to customers who remember past service. Management Science 59(3):592–612.

- Balseiro et al. (2019) Balseiro SR, Gurkan H, Sun P (2019) Multiagent mechanism design without money. Operations Research 67(5):1417–1436.

- Basu et al. (2017) Basu A, Martin K, Ryan CT (2017) Strong duality and sensitivity analysis in semi-infinite linear programming. Mathematical Programming 161(1-2):451–485.

- Beevi et al. (2016) Beevi KS, Nair MS, Bindu GR (2016) Detection of mitotic nuclei in breast histopathology images using localized ACM and Random Kitchen Sink based classifier. 2016 38th Annual International Conference of the IEEE Engineering in Medicine and Biology Society (EMBC), 2435–2439.

- Bertsekas and Tsitsiklis (1996) Bertsekas DP, Tsitsiklis JN (1996) Neuro-dynamic Programming, volume 5 (Belmont, MA: Athena Scientific).

- Bhat et al. (2012) Bhat N, Farias V, Moallemi CC (2012) Non-parametric approximate dynamic programming via the kernel method. Advances in Neural Information Processing Systems, 386–394.

- Blado and Toriello (2019) Blado D, Toriello A (2019) Relaxation analysis for the dynamic knapsack problem with stochastic item sizes. SIAM Journal on Optimization 29(1):1–30.

- Brown and Smith (2021) Brown DB, Smith JE (2021) Information relaxations and duality in stochastic dynamic programs: A review and tutorial. Working paper .

- Calafiore and Campi (2005) Calafiore G, Campi MC (2005) Uncertain convex programs: randomized solutions and confidence levels. Mathematical Programming 102(1):25–46.

- Calafiore and Campi (2006) Calafiore GC, Campi MC (2006) The scenario approach to robust control design. IEEE Transactions on automatic control 51(5):742–753.

- Canuto et al. (2012) Canuto C, Hussaini MY, Quarteroni A, Thomas Jr A, et al. (2012) Spectral methods in fluid dynamics (Springer Science & Business Media).

- Carriere (1996) Carriere JF (1996) Valuation of the early-exercise price for options using simulations and nonparametric regression. Insurance: Mathematics and Economics 19(1):19–30.

- Chen et al. (2014) Chen X, Pang Z, Pan L (2014) Coordinating inventory control and pricing strategies for perishable products. Operations Research 62(2):284–300.

- De Farias and Van Roy (2003) De Farias DP, Van Roy B (2003) The linear programming approach to approximate dynamic programming. Operations Research 51(6):850–865.

- De Farias and Van Roy (2004) De Farias DP, Van Roy B (2004) On constraint sampling in the linear programming approach to approximate dynamic programming. Mathematics of Operations Research 29(3):462–478.

- Desai et al. (2012a) Desai VV, Farias VF, Moallemi CC (2012a) Approximate dynamic programming via a smoothed linear program. Operations Research 60(3):655–674.

- Desai et al. (2012b) Desai VV, Farias VF, Moallemi CC (2012b) Pathwise optimization for optimal stopping problems. Management Science 58(12):2292–2308.

- Farias and Van Roy (2006) Farias VF, Van Roy B (2006) Tetris: A Study of Randomized Constraint Sampling, 189–201 (London: Springer London).

- Folland (1999) Folland GB (1999) Real Analysis: Modern Techniques and Their Applications (New York, NY: John Wiley & Sons).