A new set of cluster driven composite development indicators

Abstract

Composite development indicators used in policy making often subjectively aggregate a restricted set of indicators. We show, using dimensionality reduction techniques, including Principal Component Analysis (PCA) and for the first time information filtering and hierarchical clustering, that these composite indicators miss key information on the relationship between different indicators. In particular, the grouping of indicators via topics is not reflected in the data at a global and local level. We overcome these issues by using the clustering of indicators to build a new set of cluster driven composite development indicators that are objective, data driven, comparable between countries, and retain interpretabilty. We discuss their consequences on informing policy makers about country development, comparing them with the top PageRank indicators as a benchmark. Finally, we demonstrate that our new set of composite development indicators outperforms the benchmark on a dataset reconstruction task.

1 Introduction

Economic indicators are vital in understanding and tracking the macroeconomic state and development of a country [1], informing government policy makers about the health of the economy and also for citizens to evaluate and assess any improvement in their life [2]. However, with the ever expanding number of different indicators and digital records of this data, it becomes difficult to interpret the high dimensional data as a whole, spot overall trends and see how different indicators are related to each other. Often qualitative or obscure factors are used to explain development such as the need to have a good education and healthy citizens.

Additionally, it is not agreed what factors affect development [3, 4, 5, 6, 7, 8, 9, 10, 11], and so arbitrarily chosen indicators are often used, ignoring specific information by excluding other indicators. In some cases, a more educated assumption is made by taking only indicators of relevance e.g. those relating to infrastructure. Even in these cases, different classes of indicators are treated separately to each other. Links with other classes of indicators e.g. poverty and infrastructure [12] are disregarded. This is especially relevant when one combines them in some way into composite indicators[13], which aim to describe several development indicators with just one composite version. These can range from more general indicators such as the Human Development Index (HDI) [14], which is used to measure the progress in life expectancy, education and Gross National Income per capita (GNI)[15], to more specific indicators such as the Global Connectivity Index (GCI) [16]. Composite indicators are also often used to summarise the state of a country relating to the specific objective of combining the chosen set of indicators e.g. GCI is used to track the extent of digital infrastructure of a country, whilst HDI is used to track overall human development. In literature they have been used, for example, to relate cancer rates to development [17] or to produce a global rank of a country’s competitiveness.

Whilst aggregating indicators into composite ones seems to be a good solution to the problem of summarising information from many different indicators, we propose that the high number of possible ways to combine them calls for the developement of guiding principles on how this should be achieved. Moreover, some indicators are calculated differently for different regions [18], making comparisons based on them much more difficult. By knowing how indicators are inter-related to each other, we will be able to understand in a data-driven, objective way which indicators are most important in characterising a country and how they should be combined to produce economically meaningful composite indicators.

Dimensionality reduction can help here by providing a smaller but faithful version of the relationship between the vast number of available development indicators [19]. This paper proposes to study these relationships in an unbiased way, using these relationships as a basis to propose a new set of composite development indicators. Differently to previous work, we make no subjective restriction on the type of indicators we study, drawing from a large range of scope of indicators to study the relationship between the indicators emerging from the data itself. We test whether we can indeed separate the indicators into different pre defined groups based on the different factors proposed that affect development using PCA (Principal Component Analysis) and Random Matrix Theory (RMT) [20]. We find that the broad topic category they are assigned, e.g. health vs economic vs infrastructure, is not necessarily the best way to aggregate them. We also employ hierarchical clustering algorithms for the first time to analyse the structure of indicators rather than countries, finding that the indicator clusters are a mixture of topics but still retain an economic interpretation. We use these results to overcome traditional problems faced in making composite indicators such as how/what indicators to aggregate to derive a new set of objective, data driven, interpretable and country comparable composite indicators. Leveraging on these composite development indicators, we observe useful observations for policy makers, such as the ability of mobile phone adoption to be able to distinguish between underdeveloped countries. Next, we provide a new application of network filtering to find subsets of highly influential indicators based on PageRank [21]. Finally, we compare the performance of our composite indicators to a random benchmark, a subset of influential indicators and PCA, concluding that our proposed composite indicators outperform the others.

In the context of this problem, dimensionality reduction has been applied in [22], where Principal Component Analysis (PCA) was used on a set of restricted indicators to form infrastructure composite indicator. This indicator was then used to examine the direction of the causal relationship between infrastructure capability and economic growth. The authors of [23] compare the pre-set weights of the HDI to that derived from a PCA. Hierarchical clustering has been applied to analyse clusters of countries such as in [24, 25]. However, in either cases either a restricted set of indicators are used or the focus of the work is on countries, rather than the analysis and development of new indicators themselves. The problem of forming composite indicators using PCA and dimensionality reduction is emphasised in [26], where it has been shown this approach could overlook important information. In particular for PCA, this includes ignoring information from components other than the first and difficult to interpret weights.

Network filtering techniques [27, 28] and their related hierarchical clustering algorithms [29, 30, 31] have also proved to be useful when analysing data, with wide ranging applications from finance to biology [31, 30, 32]. Network filtering techniques view a similarity matrix as a network, each node being a feature and each link having a weight with the respective non-zero correlation. Within this framework, removing noisy entries in the correlation matrix can be translated into finding a sparse version of the similarity network. These techniques aim to extract the backbone of the structure between generic features by enforcing sparsity in a specific way to the particular technique. The induced sparsity of the network helps make hidden structures more visible. One successful example of this is the Minimum Spanning Tree (MST) [33, 27], which imposes that the correlation matrix is a tree that maximises the total weight of links, and has been applied in a diverse number of fields from electricity networks to taxonomy [32, 33]. A generalisation which includes the possibility of loops is the Planar Maximally Filtered Graph (PMFG) [34, 28], which instead imposes a weaker constraint that the network is planar i.e. it can be embedded on a sphere without any links crossing. Hierarchical algorithms are also highly related and aim to group features with similar properties into clusters that organised in a hierarchical fashion in the form of a dendrogram. An example of this is the Directed Bubble Hierarchical Tree (DBHT) algorithm that is based on the PMFG, having been used for finance [31, 35] and in gene expression data [30]. In particular, the DBHT algorithm has also been shown to outperform other hierarchical clustering algorithms.

This paper is organised as follows. The second section is a description of the dataset and how we amalgamate topics together. In the third section we apply a PCA analysis to our dataset, which we use to show the difference between the structure of the empirical correlation matrix and the preassigned topics. We then find the clustering using the DBHT algorithm in Section 4. Developing the clustering results further to form a novel set of composite indicators in Section 5, we observe some interesting features of our composite indicators in Section 6. For Section 7 we apply the PMFG to the empirical correlation matrix in order to derive some influential indicators via PageRank. In Section 8 we compare the performance of our composite indicators with a random benchmark and top indicators taken from the PageRank. Finally, we discuss the dynamic stability of our results in Section 9 and draw some conclusions in the final section.

2 WDI Dataset

The World Development Indicator (WDI) dataset is a vast collection of various yearly development indicators for countries (where is the number of countries) and are taken from official, internationally recognised agencies [36]. Note that we have applied the imputation scheme the distribution regularisation procedure detailed in the Supplementary Information Section 10.1 (to treat missing data) and in Section 10.2 (to standardise and normalise the indicators) respectively. Note that we have also checked that the amount of missing data does not change the results significantly - see Supplementary Information Section 10.1 for more information. We shall use a total of years, where represents the years from to . The number of indicators contained within the dataset is , and the objectives for collecting these indicators ranges from well known economic data such as Gross Domestic Product (GDP), education data such as the literacy rate and population health such as infant mortality rate. Hence both the large number of indicators and the diverse range of granularity and objectives makes this dataset a perfect candidate in order to study the relationships between different classes of indicators and to infer and derive conclusions that hold globally. Note that we also remove highly correlated indicators with a correlation coefficient of since some indicators can be trivially related together e.g. percentage of population that are males and the same but for females, which would bias the results. This reduces the number of indicators to .

2.1 Amalgamating Topics

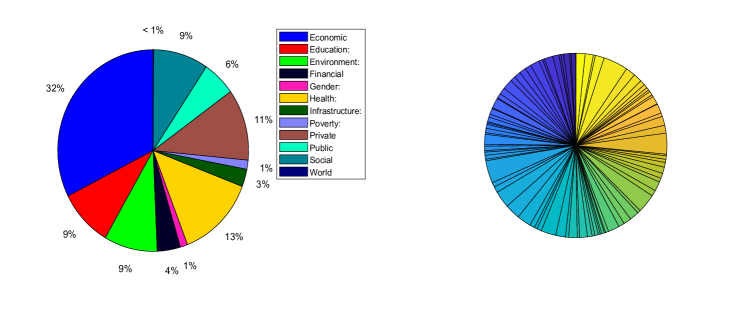

The indicators are also divided into different topics that include different classes of economic indicators such as Economic Policy and Debts: National Accounts: Growth Rates, which measures growth rates of agriculture, industry, manufacturing and services sectors, and Education: Participation, which measures participation rates across gender, age groups in various levels of education. We show the distribution of all such topics using this classification in Fig. 1a. We can see that most of the groups of indicators make up a very small fraction of the indicators, which would mean that any averaged statistic across within each group would be subject to significant noise. To counteract this, we aggregate the topics for each classification based on their root objective e.g. Education: Participation and Education: Efficiency are both classes of indicators relating to education and hence we combine these two groups into one group Education, similarly Health: Nutrition and Health: Disease Prevention are combined into Health. Applying this procedure to the entire dataset produces different topics for the indicators which we indicate in Fig. 1b. We can see that each topic has a larger number of indicators, which will increase the statistical reliability of any conclusions drawn from the data.

2.2 Data Structure

We here start exploring the correlation structure across years as a measure to quantify the relationship between indicators. We aggregate values across years in order to average out correlations that might hold only for specific periods or groups of countries. This also helps to reduce the noise in the correlation matrix, since one-year matrices would be too shallow to reliably obtain correlation estimates.

With this mind, we organise the data matrix as follows. It consists of matrices of size matrices stacked vertically, with each cross sectional block representing the data for one specific country and each column reporting the data for indicator . For each cross section, the entries in the first row and column are the values of the indicator for and the last row are the same but for . In order to discard spurious correlations in the data, we remove trends by taking the first difference, that is for each block of data we calculate

| (1) |

with is the value of indicator for country at year . is similar but with . represents the first difference between and , with running from . Every has rows and columns. Stacking each of these vertically forms the matrix , which now contains all the differenced values for all countries and all time steps.

To encode the relationship between the indicators we use the empirical Pearson correlation matrix , which can be calculated from a zero mean, standardised as

| (2) |

where represents the transpose. Therefore, we aim to understand the multivariate dependence between development indicators through analysing the main driving factors of the structure of . However, using the raw correlation matrix would be unwise due to its large size ( by ) and noise present in the system, potentially leaving a certain amount of redundant information in . As mentioned earlier, we can distill the information given in to a smaller version using dimensionality reduction, which should also have the added benefit of making it easier to interpret the structure of .

3 PCA analysis

Within the class of dimensionality reduction methods, PCA is a popular and easy to apply technique used on correlation matrices [37]. This technique has been successfully applied in many diverse areas, ranging from finance [38] to molecular simulation [39]. PCA accomplishes the task of dimensionality reduction by taking a subset of the orthogonal basis for the correlation matrix [37]. The first principal component corresponds to the eigenvector with the highest eigenvalue, providing the direction where the data is maximally spread out i.e. explains the most variance of the system. Each subsequent principal component has a lower eigenvalue and thus explains a lower fraction of the total variation of the system. Therefore, we can reduce the dimensionality of the correlation matrix by taking a subset of principal components, hoping to encode most of the total variance of the data. This subset can be chosen with the help of Random Matrix Theory (RMT) [20], which studies the properties of matrices drawn from a probability distribution. In our specific context of forming composite indicators in a data-driven way, one could then use the chosen subset of components as a basis for composite indicators.

In this section, we apply PCA to the correlation matrix on the dataset of Section 2, finding the distribution of its eigenvalues, using results from RMT to help interpret it. We then analyse the contribution of each topic defined in Section 2.1 to the eigenvectors corresponding to the principal components.

3.1 Eigenvalue Spectrum

As is customary in Random Matrix Theory, we fitted the Marčenko-Pastur (MP) distribution [40] to the eigenvalue distribution of to discern what part of the eigenvalue spectrum is less likely to be a product of finite-sampling noise. We found that MP does not fit our eigenvalue distribution well, which suggests that there is structure in the whole distribution, as opposed to just its right tail. We shuffled the data to destroy all correlations between indicators, and obtained an eigenvalue distribution that fitted the MP near perfectly. These findings suggest that choosing only a subset of the principal components obtained by PCA is likely to discard relevant information. In other words, this is a clue that PCA might be unsuitable to reduce dimensionality on this dataset. For a more detailed discussion of the procedures in this subsection, we refer to the Supplementary Information Section 11.

3.2 Eigenvector Interpretation

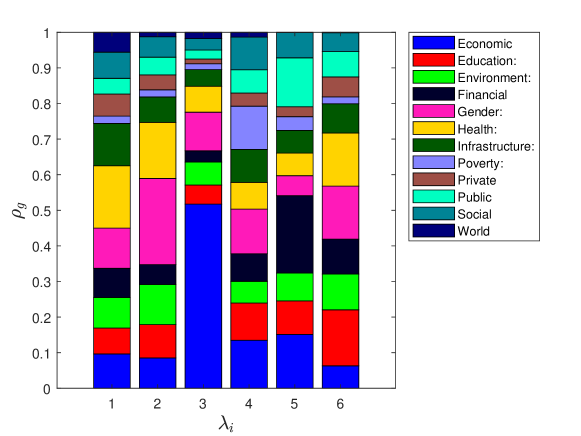

We investigate what the interpretation of the eigenvectors is by calculating the contribution of each of the topics from Section 2.1 that divide the indicators. This will reveal the structure with respect to topics of the principal components so we can see if they are dominated by one specific topic. The analysis will also be particularly relevant for the earlier principal components that are the main contributors to the variance of the system, which will bring to the surface any topics which are more significantly contributing to development.

Specifically, we project the eigenvectors of onto the topics which divide the indicators that we defined in Section 2 using the projection matrix with entries

where is the number of indicators that are part of topic . From this, for every we can define , which is -dim vector with entries , and is computed as

| (3) |

where is the normalisation constant . Each entry of gives the contribution of the -th topic to the -th eigenvector. As an example, we plot for the top principal components in Fig. 2.

In Table 1, we report the one-sided p values of for testing against the null hypothesis that the contribution from the topic to the principal component is random using the procedure detailed in Supplementary Information Section 12. The bolded values are those below the significance level where we reject the null hypothesis. By looking at Fig. 2 and Table 1, we see that for the first principal component although other topics contribute to the largest eigenvalue, the statistically significant contributions come from the Health and Infrastructure. Similarly for the second principal component the Environment, Health and Gender topics make a statistically significant contribution, and for the third principal component only the Economic related indicators make a significant contribution.

pval ’Economic’ 0.109263 0.503665 0 4.60E-07 0 0.965214 ’Education’ 0.818697 0.237016 0.987429 0.05904 0.224225 6.90E-07 ’Environment’ 0.447607 0.01599 0.932927 0.959271 0.689149 0.110319 ’Financial’ 0.543933 0.958713 0.999491 0.646416 0 0.200756 ’Gender’ 0.140525 3.68E-06 0.175278 0.07279 0.849132 0.016654 ’Health’ 0 0 0.838467 0.788524 0.952838 0 ’Infrastructure’ 0.043397 0.733465 0.983559 0.312448 0.854746 0.517028 ’Poverty’ 0.999458 0.999486 0.999633 0.079216 0.98248 0.999533 ’Private’ 0.958778 0.99881 0.999667 0.999483 0.999664 0.983491 ’Public’ 0.996577 0.990442 0.999663 0.896429 0.000541 0.812393 ’Social’ 0.80534 0.97684 0.999635 0.287871 0.853167 0.988461 ’World’ 0.41984 0.709084 0.656062 0.697268 0.923661 0.909286

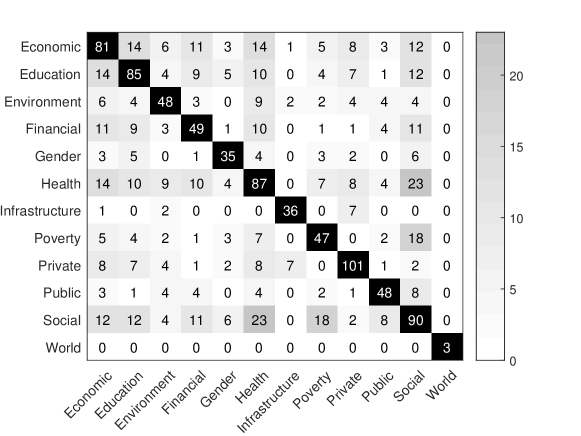

We have also plotted the number of times two topics are simultaneously significant across all principal components in Fig. 3, with a darker grey indicating a higher number of times this occurs. We use a p value with a Bonferroni correction of , giving the actual p value used to be . The black diagonal terms give the number of times a single topic is significant across all principal components using the same p value. If the indicators could be neatly divided into topics then we should see no interaction between them so that Fig. 3 will look almost like a diagonal matrix. In fact, we see that some of the off diagonal elements are quite large relative to the diagonal elements e.g. Education vs Economic and Social vs Health, which indicates that the topics are indeed interacting. We can therefore conclude from this analysis that there is not a clear, single topic that contributes more than others and that in fact statistically significant contributions can come from different topics that combine in different ways.

This has implications for composite indicators aiming to capture some particular aspect of development such as GCI and HDI since it suggests that the inclusion of certain indicators which focus on other aspects of development might improve the quality of the composite indicator. Conversely, some indicators may actually not be representative of the aim of the composite one, which means including it would add no information with respect to the aim of the composite indicator whilst also simultaneously increasing complexity. These problems have also been mentioned in [26] and [41], where it has been shown that potentially important indicators are ignored when forming composite indicators from PCA. Overall, we can conclude that whilst the principal components indicate that the correlations between indicators contains interesting structure, it is difficult to use PCA to form new composite indicators. This means we must turn to other methods to achieve both of these goals.

4 Interpretation of the clustering from the DBHT

This section analyses the relationships between indicators in a data driven way where we make as little assumptions about the structure of the data as possible. In this way, we can develop an interpretation and partition of the indicators which is consistent with the data. In the previous section, we showed that this is not possible with PCA and by dividing indicators based on their a priori topic given in Section 2.1.

Hierarchical clustering algorithms [42], which group together data with similar properties in a hierarchical fashion, and their associated network filtering techniques will help in this respect. This is because we can consider information from all indicators. Hierarchical clustering is advantage in our context since it has been shown with many other different kinds of data originating from complex systems that data is organised hierarchically [43, 44]. Therefore it seems natural to apply a hierarchical clustering algorithm to discover this structure. Once we apply the clustering algorithm on the correlation matrix, we have a natural way of accomplishing dimensionality reduction by using one variable to describe each cluster of nodes, with the collection of clusters forming the reduced correlation matrix. The ones associated to network filtering algorithms leverage on the topological properties of the filtered network.

We shall use the PMFG network filtering technique because it is able to retain a higher amount of information about the system than the MST. This is because it preserves a greater number of links of the original network and in fact contains the MST as a subgraph [28]. This is important for us since the MST is a tree and thus contains no loops, whereas the PMFG contains and cliques, and we would like to avoid discarding relevant information about the relationship between indicators. For the PMFG, the associated clustering algorithm is the DBHT algorithm, which takes advantage of the clique structure of the PMFG. There has been objections to the use of cluster analysis due mainly to the distance between points as a metric [45, 46] since it does not measure the similarity between variables. Instead, the DBHT algorithm forms the clustering by measuring forming a distance matrix directly from the similarity matrix, which encodes the relationships between variables. In our case the similarity matrix is , with the entries of the distance matrix commonly defined as [27, 47, 31]

| (4) |

therefore measures how far two indicators are in terms of their correlation.

The main advantage of using the DBHT algorithm is that it does not need prior input into the number of clusters, making it preferable over other clustering algorithms so that we can make a-posteriori comparison with less assumptions [30, 31]. This is important for us since we want to uncover the structure of correlations between indicators, making as few assumptions as possible on this same structure. Furthermore, the DBHT algorithm has been shown to retrieve a higher amount of meaningful information[31].

In this section, we investigate whether the indicators can be divided into their topics by applying the DBHT algorithm to in Section 4.1. Then by analysing clusters individually, we look for their dominating topics and what their possible interpretation is in Section 4.2.

4.1 DBHT results and interpretation

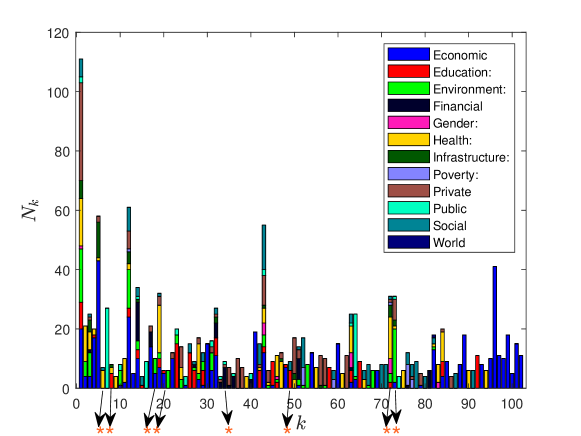

We apply DBHT to . It identifies a total of clusters which we label , significantly more than the preassigned topics, with an average cluster size of . In Fig. 4 we summarise the clustering labels obtained from DBHT and its topic composition, with the height of the bar representing the number of indicators in each cluster . Each bar is further divided by colours which represent how many indicators belong to that particular topic. Figure 4 shows that cluster sizes are highly heterogeneous - the biggest cluster has indicators versus the smallest with .

We can see that some clusters are dominated by certain topics - for example cluster is dominated by economic indicators and in particular indicators related to countries’ current account balance and external balance of trade. At the same time however, there are also some clusters which are instead a mixture of topics but still have an interpretation based on the indicators contained within them such as cluster , which contains indicator from disparate topics. A closer inspection reveals that this cluster is made of indicators about access to electricity, railways size, primary and secondary education expenditure, health-related indicator such as HIV incidence and hepatitis immunization, access to sanitation facilities, prevalence of underweight children, number of women who justify a husband’s beatings, and the Gini index. All these measurements can be easily used to characterize underdeveloped countries [48, 49, 50, 51, 52, 53, 54]

Another interesting fact that we can observe from the data is that the cluster contains very important economic indicators such as GDP per capita, value added contributions of agriculture, industry, manufacturing, services and trade, and also imports/exports of goods and services as a fraction of GDP. This same cluster also contains indicators directly related to measuring the innovation output of a country such as patent, trademark and industrial design applications, suggesting that innovation is an important factor in economic development. We can interpret this by realising that innovation led growth increases productivity through the accumulation of knowledge obtained via education, new products or better processes [55, 11].

Many other interesting clusters are found, such as number 11, which seems to relate to underdevelopement with it contents relating to life expectancy, foreign aid, drinking water availability, fertility rate, and percentage of women married before the age of 18. Cluster 21 puts together CO2 emissions, alternative and nuclear energy, combustible renewables and waste, hydroelectric sources prevalence and power distribution losses. Cluster 101 describes the distress status of a country’s debt, including indecators about how much of it has been rescheduled or forgiven.

4.2 Similarity of the DBHT clustering with the topics

Once we have established that each of the clusters has an economic meaning, we quantify how much the clustering outputted by the DBHT in Fig. 4 is similar to the clustering based on topics. Therefore, we will be able to see overall how close the two divisions of topics are in a quantitative way. We do so using the Adjusted Rand Index (ARI), which is if there is a perfect agreement, if there is an anti-agreement and if there is no agreement [56]. It has been successfully used in [31]. Computing the ARI to compare the output of the DBHT algorithm and the topics distribution, we find that this value is i.e. quite close to , which corroborates our previous conclusion that overall the clustering of the data is not in general linked to that based on topics.

The analysis can also be made at local level by seeing if any topics have a significant presence in each cluster. In this way, it allows us to also to see locally if more than one topic might be present in each cluster, which is important since whilst on a global level there may not be much similarity . Practically, this is achieved by using the procedure proposed in [57]. Specifically, we test statistically, using a one sided test, the null hypothesis that a cluster from the DBHT and the -th topic have common elements is random. Under the null hypothesis, this distribution is hyper geometric. If the null hypothesis is rejected, it means that statistically we say that the -th topic is overexpressed in cluster . We apply this procedure to each of the DBHT clusters and topics using the p value of (which is with a Bonferoni correction [58] of ), recording the number of overexpressed topics in each cluster. The results of this procedure reveals that whilst a majority of clusters have one or two topics overexpressed, there are a total of clusters which have no overexpressed topics. These particular clusters of indicators still have an economic meaning. For example, cluster contains indicators relating to tertiary education such as pupil to teacher ratio in tertiary education and completed education at a tertiary level, which belong the education topic. However, it also contains indicators such as scientific and technical journal articles, which is classed as relating to infrastructure. These indicators may be linked e.g. because scientific articles are usually always published by authors with at least a tertiary level education. This confirms our conclusions that overall at a system wide and local level, the clustering of the data does not reflect the information given by the topics, suggesting that indicators do not necessarily correlate with other indicators of the same type.

5 Deriving new composite development indicators from DBHT

In the previous section we showed that the distribution of topics amongst the indicators is not an accurate description of the data and may miss key information about the relationship between different classes of indicators. This means that composite indicators based on this premise such as the HDI or the WEF-GCI infrastructure pillar may not be the best way of combining indicators. We want to propose a new set of data driven composite development indicators which can encapsulate this new information based on the results given in Section 4.1. In doing so, we would overcome traditional problems faced when forming composite development indicators, mainly on how and which indicators we should aggregate. This section is dedicated to describing a way of using the results in section 4 to derive a novel set of cluster driven composite development indicators.

To define each composite indicator we shall use the set of clusters from DBHT given in Section 4.1. It provides a natural way to select the indicators to combine for our composite indicators since each cluster contains indicators which share similar properties, and also has an economic interpretation as highlighted in section 4. Hence, aggregating information for indicators which are members of the same cluster enables us to simply and efficiently summarise the economic information contained within them. In contrast with PCA [26, 41], since we rely on the DBHT clustering, we automatically include information coming from all the indicators since every indicator is a member of some cluster that defines its respective composite version. Condensing the complimentary insight offered by indicators in the same cluster also overcomes the need to make ’educated’ assumptions about which indicators are to be combined that other alternative composite indicators often use [14]. In this way, we can more clearly see the overall behaviour of each set of indicators in cluster by using the corresponding composite indicator value as a proxy. DBHT also is significantly advantageous in this respect since it requires no prior input of the number clusters (and thus number of composite indicators) needed to describe the properties of the data) [30, 31]. Potentially, opposite polarities of indicators in the same cluster could make the interpretation of the value of any composite indicator formed from the same cluster problematic [26]. However, an advantage of forming composite indicators from the DBHT is that the clusters from the sparse correlation network PMFG, which we calculated has only of its non negative entries as negative. Hence, the indicators in the same cluster have same polarity.

5.1 Method used to calculate the composite indicators

Here, we shall define the method used to calculate the new composite development indicators based on the results of Section 4.1. In the composite indicator we want to capture the average behaviour of all indicators in that cluster. Therefore, we aggregate the indicators in cluster by using the median value across all indicators within this cluster. We can do this because the indicators are standardised and normalised via the procedure in the Supplementary Information Section 10.2. This forms composite indicator , , defined as

| (5) |

where the notation indicates that we only take indicators that are members of cluster . An advantage of using the median over the arithmetic mean or even a weighted mean is that the median is more robust to outliers. The median is a valid measure across the different indicators because the entries of are also standardised, meaning that their scales are all the same. We highlight that we have chosen to use the median for every since this provides us with a consistent methodology so that the precise details of how is calculated do not change for every . This improves some existing methods used in the literature where for example the same indicator may be calculated in different ways for different regions [18] meaning that we can make valid comparisons between indicators. Furthermore, a PCA based approach would require the use of weights, which has been argued to be hard to interpret economically [26, 59]. Instead, the median used does not require weights as an input to form the composite indicators we propose. We use this method to calculate the set of , giving indicators in total and call this set of cluster driven composite indicators (CDCIs).

6 Using the CDCIs to understand country development

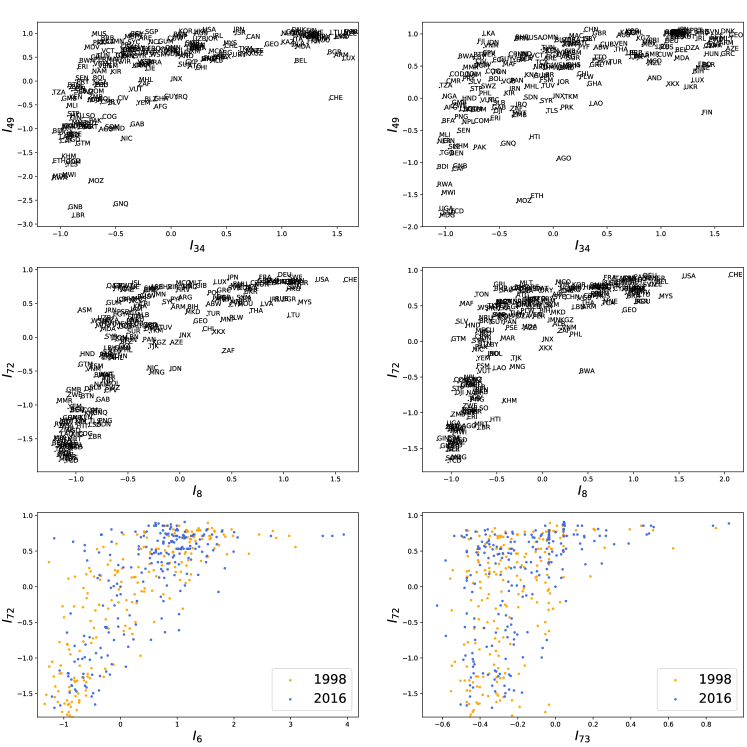

One of the main uses of indicators is to track the country development of a country to assess its progress. This is important since it gives an idea of what has been achieved in terms of country development and where to focus policy changes to affect country development positively. One can also use indicators to compare countries either pair wise or globally. On the last point, CDCIs can be useful because the methodology used to compute them is not reliant on subjective, country dependent criteria, which means we can make fair comparisons between different values of the CDCIs for different countries at different times. By comparing the CDCIs with each other for all countries, we can therefore investigate whether they can be used to assess the development of a country. The main CDCIs we shall concentrate on are , which are marked by orange asterisks in Fig. 4.

In Fig. 5, we provide some examples of comparisons between different indicators. Overall, we remark that all the plots have a ’hockey-stick’ shape. We can specifically see for the plots in the top two panels the vertical leg of the hockey-stick shape is made of developing countries, whilst the horizontal leg, indicating a saturation effect, is made of developed countries. This is interesting since it suggests a country level transition from a group consisting of developing nations to one with developed nations. In fact, this further supports the so called two regime hypothesis [60, 22], where countries below a barrier struggle to develop consistently, which corresponds to nations in the vertical leg of hockey-stick shape. Countries that overcome this barrier have or are experiencing high growth in development, which are represented by the horizontal leg of the hockey-stick shape. This transition can clearly be observed to be consistent across time from the bottom panel comparing and and and , with the years and overlayed.

As a consequence of the consistency of the observed hockey-stick shape, we can make interesting observations regarding the particular pair of CDCIs being plotted. Specifically in the top panel of Fig. 5, we plot against , where the former represents those who have use mobile and banking services and the latter come from primary school statistics, a key signature of development [61]. We see here that it seems that the vertical leg access to mobile phone technology can, for developing countries, characterise their development. Past a certain point however, the concavity changes, suggesting that access to mobile phones becomes less able to distinguish between countries’ development. In this region, we have already remarked that they are mostly developed nations, who have a saturation in mobile phone access due to their higher average income. Likewise, we see in the middle panel, which corresponds to (secondary school enrollment) and (recalling from Section 4.1 that this represents underdevelopment), that secondary school enrollment can initially also be used to characterise development. However after a certain level of development, secondary school enrollment saturates in these developed countries, meaning it can no longer be used in this way.

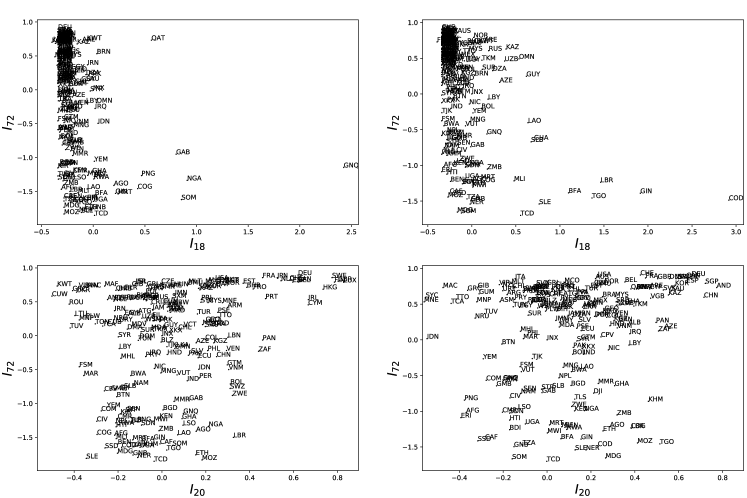

However, not all relationships between certain CDCIs are hockey-stick shaped. Indeed, we can see this from Fig. 6 which plots vs for on the left and on the right in the top panel and the same but for vs in the bottom panel. For the top panel, is a CDCI that represents natural resource abundance, whilst again we recall from Section 4.1 that corresponds to underdevelopment. We notice from the plots in the top panel that most of the countries with higher abundance of natural resources are underdeveloped countries. This reminds of the so called ’resource curse’ [62], where resource-rich nations with inefficient governments are often underdeveloped.

Additionally in the bottom panel of Fig. 6, we plot vs . corresponds to the amount of flow of foreign direct investment (FDI). Interestingly, we can observe an intriguing relationship between underdevelopment and FDI in the plots. All underdeveloped nations tend to have low FDI, which can be interpreted as being perceived with a low investment potential by foreign investors. However, countries which are not underdeveloped may have both high or low FDI, for example Poland, Kuwait and Uzbekistan are all more highly developed countries that have a low FDI. Attractiveness to foreign investments is not directly correlated to a country’s level of developement.

7 Deriving influential indicators by using PMFG

One can imagine that there could be nodes that are very important to the structure of the correlation network than others, implying that these same nodes could be highly influential in the analysis of the development of countries. This would be very interesting for our purposes since they could provide a direct way to form a reliable reduced set of development indicators that would automatically overcome any problems associated with calculating composite versions. More specifically, one could take a subset of the top most influential indicators since these indicators’ influence have an aggregate, over-arching influence on all other indicators, and thus the structure of interactions in the system.

In this section we shall apply the PMFG to and identify system wide important indicators. For this purpose, information filtering is useful because it neatly transfers the problem of identifying influential indicators as finding a ranking of important nodes in the network, for which there exist several so called network centrality measures. We choose to use PageRank [21], which has proven successful in ranking scientists and webpages [21, 63], to identify the most system wide influential indicators that affect the network. In PageRank, we rank nodes of networks on their importance based on the probability of a random walker landing on a particular node [21] with higher values indicating that the node has more importance.

We find the PMFG of . The output network of this visualisation can be seen in the Supplementary Information Section 13. Then we apply PageRank to the PMFG of , displaying an example of the top indicators in Table 2.

7.1 Interpretation of the PageRank identified indicators

From Table 2 we observe that there are some indicators which we would expect to be in this ranking: for example GDP measures the value of goods and services an economy produces, and is widely used as a primary development indicator [64]. Central government debt has also been linked to economic development since high levels of debt can drag growth rates down [65]. However, it is interesting to see that mobile cellular subscriptions to be the top ranking indicator, especially considering our comments in Section 6 that mobile banking can be used to track the development of countries. This is an interesting result since there are many papers in computational socioeconomics which use mobile data as metric of an average citizen’s socioeconomic status due to vast information it can encode [66, 67, 68, 69, 70]. In fact, it has been shown for example that mobile data is correlated with household expenditure [66] and poverty [71], and reveal gender inequality [68]. This may be because having a mobile cellular subscription requires a number of milestones in the development of a country e.g. a healthy enough population to make use of them, the education to know how to use them, the relevant infrastructure such as phone masts that can reach all parts of the population.

We have also investigated whether particular topics are overexpressed within the top (chosen because this is the number of clusters identified by the DBHT) PageRank indicators by applying the same hypothesis test used in Section 4.2. We find that no topic is overexpressed within this subset of indicators, which again corroborates our conclusion that no single topic is more influential than the other.

pagerank names 0.006764 Mobile cellular subscriptions 0.004666 Share of tariff lines with specific rates, manufactured products (%) 0.003717 Children in employment, wage workers, male (% of male children in employment, ages 7-14) 0.003706 Unemployment, male (% of male labor force) (national estimate) 0.003129 Mobile cellular subscriptions (per 100 people) 0.002939 Central government debt, total (% of GDP) 0.00276 Share of youth not in education, employment or training, female (% of female youth population) 0.002686 Population ages 30-34, female (% of female population) 0.002553 GDP (current US$)

8 Performance comparison

If we reduce all of the indicators in the dataset to the composite ones, we have boiled down the structure of the correlations between indicators to more essential constituents. Therefore, when the set of composite indicators are taken together, they should still be a faithful representation of the original since they are main driving factors behind the structure of correlations. We can use this principle to evaluate the performance of the CDCIs against any alternatives. This section is dedicated to comparing the performance of the CDCIs derived in Section 5 against some alternatives.

For this purpose we propose, as a first approximation, that each indicator can be written as a linear factor model [72] of composite indicators. The general linear model is

| (6) |

where is the th indicator i.e. the th column . is the -th composite indicator of either the CDCIs or the other alternative schemes of composite indicators. is the loading of for indicator , which measures the sensitivity of to changes in . Finally, are white noise terms. Eq. 6 is an appropriate approximation to use since firstly, we are using the linear correlation matrix, which means it is intimately related to linear factor models. Note we also have that the number of composite indicators in each of the alternatives used in our comparison must be the same as the number of CDCIs . This is because the size of the indicator set will inevitably affect its ability to describe the correlations, so fair comparison must involve fixing the number of indicators used. We then use elastic net regression (for details see Supplementary Information Section 14), which is able to take into consideration the potential correlation between composite indicators, to find and for every . The performance can then be evaluated on the basis of the error between the linear model and the real indicator values. For this, we define the usual mean squared error of the regression as

| (7) |

where are the predicted values of using the from the elastic regression. The final metric we use the evaluate the performance of the cluster driven composite indicators is

| (8) |

where is called the error reduction ratio, is the calculated in Eq. 7 for the CDCIs. Similarly, is the same but for any of the alternative schemes of composite indicators used as a comparison. If is below (above ) then this means that the CDCIs perform better (worse). Also note that of course is bounded below by .

The choice of alternative schemes of composite indicator, is as follows. We take the top PageRank indicators that were identified in Section 7.1. We choose these particular schemes since they offer the best feasible alternative in forming a basis of composite indicators that have the most influence on correlations system wide. A fourth comparison is also made by randomly selecting indicators from the columns of that provides a benchmark of the performance of the other composite indicator schemes since a set of randomly selected indicators should not be able to reliably incorporate anything from the real correlation network.

We carry out the elastic regression and compute for all alternative schemes of indicators used. For the random benchmark, we repeat and average the results for different random subsets of indicators. The results are shown in Table 3. We see that in both cases is much less than , indicating that the CDCIs are able to outperform the random benchmark and the PageRank alternative. We can therefore conclude that the CDCIs are more effective at reducing the dimensionality of the dataset the random benchmark and the PageRank alternative.

| random | PageRank |

|---|---|

| 0.66 | 0.71 |

9 Dynamical Analysis

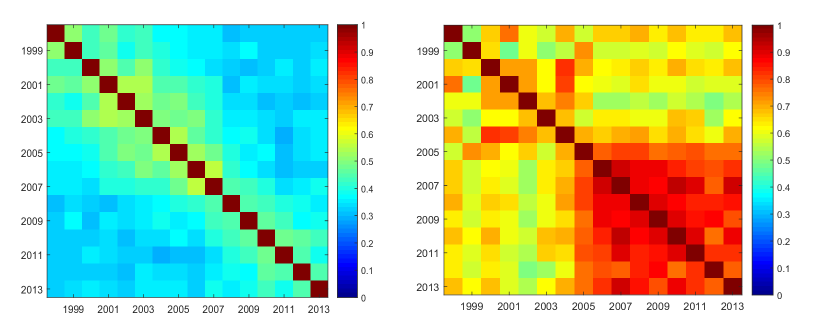

Since in the analysis so far we have used the static correlation matrix computed over the whole time period, we should also investigate the dynamic stability of the clusters. We start by splitting the whole time period into rolling time window of length , with a time shift of year. For each time window , we calculate the corresponding correlation matrix and its DBHT clustering. The similarity between each pair of time windows and is then measured by calculating the ARI between their respective DBHT clusterings. The results are shown in the heat map of Fig. 7a. We can see that overall the DBHT clusterings display a high similarity with each other, with a median ARI value of , which is high considering that the static clustering does not reflect the topics as argued through the ARI computed in Section 4.2. This also confirms to some extent our choice for the length of the sliding window since we see that the clusters are stable through time.

We also used the same procedure and parameters to investigate the dynamic stability of the relationship between CDCIs (except using the correlation matrix and DBHT clustering between the CDCIs). A heat map of the results can be seen in Fig. 7b. Again, we see that overall there is a high likeness between the clusterings of the CDCIs in each time window. In fact, the median ARI is even higher at . Interestingly, we see that starting from the window covering to , which is the year corresponding to the financial crisis, there is a markedly higher similarity between the clusterings of the CDCIs. This could be explored further.

10 Conclusion

In this paper, we have investigated whether the collection of development indicators given by the WDI database can be divided using their fundamental topic description. Leveraging on PCA and a novel application of information filtering and hierarchical clustering techniques, we showed that the structure of the topics does not mirror the actual structure between the indicators. This suggests that composite development indicators that are aggregated from restricted sets may ignore key information. Instead, we propose a new set of cluster driven composite development indicators that overcomes these problems. They are objective, data driven, interpretable and are able to make valid comparisons between countries. We have used the composite indicators and some highly influential PageRank indicators to give new insights into the development of countries. Some of these may support decisions for policy makers. Lastly, we showed that our proposed composite indicators can outperform schemes of indicators based on a random benchmark and PageRank. We mention that it has been pointed out by [26] that using the correlation matrix to form composite indicators may ignore the presence of causality relationships. We mainly use the CDCIs to group countries to understand how they can be classified in terms of their development so that there is no implicit reliance on there being a different causal relationship between indicators. It would, however, be interesting to develop combining the methodology proposed here with an analysis of the causal relationships in a future work.

Declarations

Availability of data and materials

The WDI dataset analysed during the current study is available at the following link https://datacatalog.worldbank.org/dataset/world-development-indicators.

Competing interests

The authors declare that they have no competing interests.

Funding

A.V wishes to thank EPSRC for providing funding during his PhD studies under grant EP/M50788X/1. We also wish to thank the ESRC Network Plus project ’Rebuilding macroeconomics’. We acknowledge support from Economic and Physical Science Research Council (EPSRC) grant EP/P031730/1. We are grateful to the NVIDIA corporation for supporting our research in this area with the donation of a GPU.

Author’s contributions

A.V, O.A and T.D.M conceived the experiment(s), A.V. and O.A. conducted the experiment(s) and A.V, O.A and T.D.M authors analysed the results. A.V, O.A and T.D.M reviewed the manuscript.

Acknowledgments

We acknowledge the input of Giuseppe Brandi in this article. We thank the two anonymous reviewers, whose contributions have greatly improved the manuscript.

References

- [1] Stock, J. H. & Watson, M. W. New indexes of coincident and leading economic indicators. \JournalTitleNBER macroeconomics annual 4, 351–394 (1989).

- [2] Mügge, D. Studying macroeconomic indicators as powerful ideas. \JournalTitleJournal of European Public Policy 23, 410–427 (2016).

- [3] Ricardo, D. Principles of political economy and taxation (G. Bell, London, 1891).

- [4] Leontief, W. Factor proportions and the structure of american trade: further theoretical and empirical analysis. \JournalTitleReview of Economics and Statistics 38, 386–407 (1956).

- [5] Bowen, H. P., Leamer, E. E. & Sveikauskas, L. a. Multicountry, multifactor tests of the factor abundance theory (1986).

- [6] Aghion, P. & Howitt, P. A model of growth through creative destruction. Tech. Rep., National Bureau of Economic Research (1990).

- [7] Heckscher, E. F. & Ohlin, B. G. Heckscher-Ohlin trade theory (The MIT Press, Cambridge, 1991).

- [8] Kremer, M. The o-ring theory of economic development. \JournalTitleThe Quarterly Journal of Economics 108, 551–575 (1993).

- [9] Krueger, A. B. & Lindahl, M. Education for growth: why and for whom? \JournalTitleJournal of economic literature 39, 1101–1136 (2001).

- [10] Egert, B., Kozluk, T. J. & Sutherland, D. Infrastructure and growth: empirical evidence. \JournalTitleCESifo Working Paper Series (2009).

- [11] Aghion, P., Howitt, P. & Murtin, F. The relationship between health and growth: when lucas meets nelson-phelps. Tech. Rep., National Bureau of Economic Research (2010).

- [12] (Ghana), U. N. D. P. Ghana Human Development Report (United Nations Development Programme, Accra, 1997).

- [13] Salzman, J. Methodological choices encountered in the construction of composite indices of economic and social well-being (Centre for the study of living standards, Ottawa, 2003).

- [14] Sagar, A. D. & Najam, A. The human development index: a critical review. \JournalTitleEcological economics 25, 249–264 (1998).

- [15] Todaro, M. P. & Smith, S. C. Economic development (Pearson, New Jersey, 2015).

- [16] Huawei. Global connectivity index 2018 (2018).

- [17] Bray, F., Jemal, A., Grey, N., Ferlay, J. & Forman, D. Global cancer transitions according to the human development index (2008–2030): a population-based study. \JournalTitleThe lancet oncology 13, 790–801 (2012).

- [18] Huggins, R. Creating a uk competitiveness index: regional and local benchmarking. \JournalTitleRegional Studies 37, 89–96 (2003).

- [19] Van Der Maaten, L., Postma, E. & Van den Herik, J. Dimensionality reduction: a comparative. \JournalTitleJ Mach Learn Res 10, 66–71 (2009).

- [20] Bun, J., Bouchaud, J.-P. & Potters, M. Cleaning large correlation matrices: tools from random matrix theory. \JournalTitlePhysics Reports 666, 1–109 (2017).

- [21] Page, L., Brin, S., Motwani, R. & Winograd, T. The pagerank citation ranking: Bringing order to the web. Tech. Rep., Stanford InfoLab (1999).

- [22] Cristelli, M., Tacchella, A. & Cader, M. The virtuous interplay of infrastructure development and the complexity of nations. \JournalTitleEntropy 20, 761 (2018).

- [23] Lai, D. Principal component analysis on human development indicators of china. \JournalTitleSocial indicators research 61, 319–330 (2003).

- [24] Nardo, M., Saisana, M., Saltelli, A. & Tarantola, S. Tools for composite indicators building. \JournalTitleEuropean Comission, Ispra 15, 19–20 (2005).

- [25] Castellacci, F. Closing the technology gap? \JournalTitleReview of Development Economics 15, 180–197 (2011).

- [26] Mazziotta, M. & Pareto, A. Use and misuse of pca for measuring well-being. \JournalTitleSocial Indicators Research 142, 451–476 (2019).

- [27] Mantegna, R. N. Hierarchical structure in financial markets. \JournalTitleThe European Physical Journal B-Condensed Matter and Complex Systems 11, 193–197 (1999).

- [28] Tumminello, M., Aste, T., Di Matteo, T. & Mantegna, R. N. A tool for filtering information in complex systems. \JournalTitleProceedings of the National Academy of Sciences 102, 10421–10426 (2005).

- [29] Anderberg, M. R. Cluster analysis for applications: probability and mathematical statistics: a series of monographs and textbooks, vol. 19 (Academic press, Cambridge, 2014).

- [30] Song, W.-M., Di Matteo, T. & Aste, T. Hierarchical information clustering by means of topologically embedded graphs. \JournalTitlePloS one 7, e31929 (2012).

- [31] Musmeci, N., Aste, T. & Di Matteo, T. Relation between financial market structure and the real economy: comparison between clustering methods. \JournalTitlePloS one 10, e0116201 (2015).

- [32] Sneath, P. H. The application of computers to taxonomy. \JournalTitleMicrobiology 17, 201–226 (1957).

- [33] Graham, R. L. & Hell, P. On the history of the minimum spanning tree problem. \JournalTitleAnnals of the History of Computing 7, 43–57 (1985).

- [34] Aste, T., Di Matteo, T. & Hyde, S. Complex networks on hyperbolic surfaces. \JournalTitlePhysica A: Statistical Mechanics and its Applications 346, 20–26 (2005).

- [35] Musmeci, N., Aste, T. & Di Matteo, T. Risk diversification: a study of persistence with a filtered correlation-network approach. \JournalTitleJournal of Network Theory in Finance 1, 77–98 (2015).

- [36] Group, W. B. I. E. D. D. D. World development indicators (World Bank, Washington D.C., 2018).

- [37] Jolliffe, I. Principal component analysis (Wiley Online Library, Hoboken, 2002).

- [38] Plerou, V. et al. Random matrix approach to cross correlations in financial data. \JournalTitlePhysical Review E 65, 066126 (2002).

- [39] Stein, S. A. M., Loccisano, A. E., Firestine, S. M. & Evanseck, J. D. Principal components analysis: a review of its application on molecular dynamics data. \JournalTitleAnnual Reports in Computational Chemistry 2, 233–261 (2006).

- [40] Marčenko, V. A. & Pastur, L. A. Distribution of eigenvalues for some sets of random matrices. \JournalTitleSbornik: Mathematics 1, 457–483 (1967).

- [41] Mishra, S. K. On construction of robust composite indices by linear aggregation. \JournalTitleAvailable at SSRN 1147964 (2008).

- [42] Bishop, C. M. Pattern recognition and machine learning (springer, Berlin, 2006).

- [43] Ravasz, E. & Barabási, A.-L. Hierarchical organization in complex networks. \JournalTitlePhysical review E 67, 026112 (2003).

- [44] Corominas-Murtra, B., Goñi, J., Solé, R. V. & Rodríguez-Caso, C. On the origins of hierarchy in complex networks. \JournalTitleProceedings of the National Academy of Sciences 110, 13316–13321 (2013).

- [45] Jain, A. K., Murty, M. N. & Flynn, P. J. Data clustering: a review. \JournalTitleACM computing surveys (CSUR) 31, 264–323 (1999).

- [46] Wang, H., Wang, W., Yang, J. & Yu, P. S. Clustering by pattern similarity in large data sets. In Proceedings of the 2002 ACM SIGMOD international conference on Management of data, 394–405 (2002).

- [47] Mantegna, R. N. & Stanley, H. E. Introduction to econophysics: correlations and complexity in finance (Cambridge university press, 1999).

- [48] Winkler, H. et al. Access and affordability of electricity in developing countries. \JournalTitleWorld development 39, 1037–1050 (2011).

- [49] Garcia-Moreno, C. et al. Prevalence of intimate partner violence: findings from the who multi-country study on women’s health and domestic violence. \JournalTitleThe lancet 368, 1260–1269 (2006).

- [50] Smith, L. C. & Haddad, L. J. Explaining child malnutrition in developing countries: A cross-country analysis, vol. 111 (Intl Food Policy Res Inst, Washington D.C., 2000).

- [51] Ravallion, M. Can high-inequality developing countries escape absolute poverty? \JournalTitleEconomics letters 56, 51–57 (1997).

- [52] Bose, N., Haque, M. E. & Osborn, D. R. Public expenditure and economic growth: A disaggregated analysis for developing countries. \JournalTitleThe Manchester School 75, 533–556 (2007).

- [53] Gupta, G. R., Parkhurst, J. O., Ogden, J. A., Aggleton, P. & Mahal, A. Structural approaches to hiv prevention. \JournalTitleThe Lancet 372, 764–775 (2008).

- [54] Montgomery, M. A. & Elimelech, M. Water and sanitation in developing countries: including health in the equation (2007).

- [55] Romer, P. M. Endogenous technological change. \JournalTitleJournal of political Economy 98, S71–S102 (1990).

- [56] Rand, W. M. Objective criteria for the evaluation of clustering methods. \JournalTitleJournal of the American Statistical association 66, 846–850 (1971).

- [57] Tumminello, M., Micciche, S., Lillo, F., Piilo, J. & Mantegna, R. N. Statistically validated networks in bipartite complex systems. \JournalTitlePloS one 6, e17994 (2011).

- [58] Feller, W. An introduction to probability theory and its applications, vol. 2 (John Wiley & Sons, Hoboken, 2008).

- [59] Somarriba, N. & Pena, B. Synthetic indicators of quality of life in europe. \JournalTitleSocial Indicators Research 94, 115–133 (2009).

- [60] Pugliese, E., Chiarotti, G. L., Zaccaria, A. & Pietronero, L. Complex economies have a lateral escape from the poverty trap. \JournalTitlePloS one 12, e0168540 (2017).

- [61] Keller, K. R. Investment in primary, secondary, and higher education and the effects on economic growth. \JournalTitleContemporary Economic Policy 24, 18–34 (2006).

- [62] Ross, M. L. The political economy of the resource curse. \JournalTitleWorld politics 51, 297–322 (1999).

- [63] Liu, X., Bollen, J., Nelson, M. L. & Van de Sompel, H. Co-authorship networks in the digital library research community. \JournalTitleInformation processing & management 41, 1462–1480 (2005).

- [64] Lepenies, P. The power of a single number: a political history of GDP (Columbia University Press, New York, 2016).

- [65] Checherita-Westphal, C. & Rother, P. The impact of high government debt on economic growth and its channels: An empirical investigation for the euro area. \JournalTitleEuropean economic review 56, 1392–1405 (2012).

- [66] Blumenstock, J., Shen, Y. & Eagle, N. A method for estimating the relationship between phone use and wealth. In QualMeetsQuant Workshop at the 4th International Conference on Information and Communication Technologies and Development, vol. 13, 114–125 (2010).

- [67] Blumenstock, J. E. & Eagle, N. Divided we call: disparities in access and use of mobile phones in rwanda. \JournalTitleInformation Technologies & International Development 8, pp–1 (2012).

- [68] Mehrotra, A., Nguyen, A., Blumenstock, J. & Mohan, V. Differences in phone use between men and women: quantitative evidence from rwanda. In Proceedings of the fifth international conference on information and communication technologies and development, 297–306 (ACM, 2012).

- [69] Gutierrez, T., Krings, G. & Blondel, V. D. Evaluating socio-economic state of a country analyzing airtime credit and mobile phone datasets. \JournalTitlearXiv preprint arXiv:1309.4496 (2013).

- [70] Gao, J., Zhang, Y.-C. & Zhou, T. Computational socioeconomics. \JournalTitlearXiv preprint arXiv:1905.06166 (2019).

- [71] Smith, C., Mashhadi, A. & Capra, L. Ubiquitous sensing for mapping poverty in developing countries. \JournalTitlePaper submitted to the Orange D4D Challenge (2013).

- [72] Thompson, B. Exploratory and confirmatory factor analysis: Understanding concepts and applications. (American Psychological Association, Washington D.C., 2004).

- [73] Rubinsteyn, A., Feldman, S., O’Donnell, T. & Beaulieu-Jones, B. hammerlab/fancyimpute: Version 0.2.0, DOI: 10.5281/zenodo.886614 (2017).

- [74] Mazumder, R., Hastie, T. & Tibshirani, R. Spectral regularization algorithms for learning large incomplete matrices. \JournalTitleJournal of machine learning research 11, 2287–2322 (2010).

- [75] Troyanskaya, O. et al. Missing value estimation methods for dna microarrays. \JournalTitleBioinformatics 17, 520–525 (2001).

- [76] Hastie, T., Tibshirani, R., Friedman, J. & Franklin, J. The elements of statistical learning: data mining, inference and prediction. \JournalTitleThe Mathematical Intelligencer 27, 83–85 (2005).

- [77] Tacchella, A., Mazzilli, D. & Pietronero, L. A dynamical systems approach to gross domestic product forecasting. \JournalTitleNature Physics 14, 861 (2018).

- [78] Webber, J. B. W. A bi-symmetric log transformation for wide-range data. \JournalTitleMeasurement Science and Technology 24, 027001 (2012).

- [79] Verma, A., Vivo, P. & Di Matteo, T. A memory-based method to select the number of relevant components in principal component analysis. \JournalTitleJournal of Statistical Mechanics: Theory and Experiment 2019, 093408 (2019).

- [80] Guhr, T. & Kälber, B. A new method to estimate the noise in financial correlation matrices. \JournalTitleJournal of Physics A: Mathematical and General 36, 3009 (2003).

- [81] Livan, G., Alfarano, S. & Scalas, E. Fine structure of spectral properties for random correlation matrices: An application to financial markets. \JournalTitlePhysical Review E 84, 016113 (2011).

- [82] Wilinski, M., Ikeda, Y. & Aoyama, H. Complex correlation approach for high frequency financial data. \JournalTitleJournal of Statistical Mechanics: Theory and Experiment 2018, 023405 (2018).

- [83] Van der Vaart, A. W. Asymptotic statistics, vol. 3 (Cambridge university press, 2000).

- [84] Zou, H. & Hastie, T. Regularization and variable selection via the elastic net. \JournalTitleJournal of the Royal Statistical Society: Series B (Statistical Methodology) 67, 301–320 (2005).

Appendix

10.1 Imputation

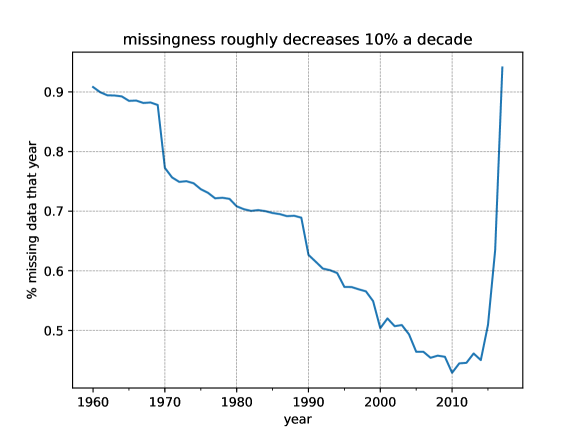

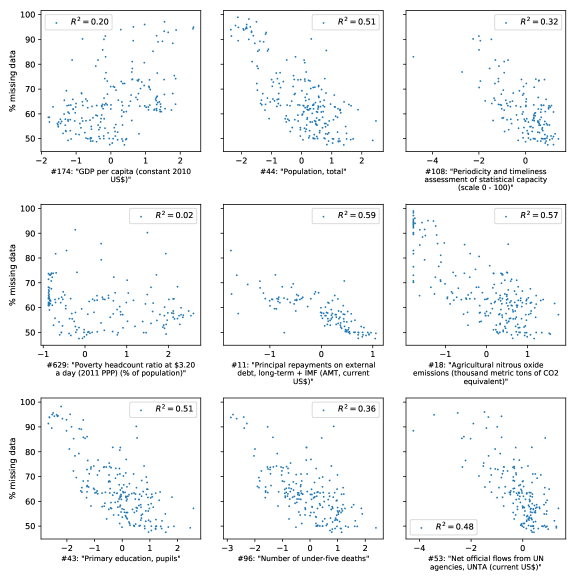

The WDI dataset suffers from high levels of missing data. We solved this problem with a combination of removal and imputation of datapoints. For starters, the amount of missing data decreases in time, as can be seen in Fig. 8. We decided to use the last 20 years of data, which have the least amount of missing datapoints in the dataset, so to not have to deal with missingness values above 50%.

We considered the possible bias of the dataset due to the fact that data is not missing at random. In fact, it can be seen from Fig. 9 that the amount of missing data a country has is correlated, sometimes strongly, with the values of some of its indicators. It seems that the dataset is biased towards industrialized and more developed countries. While this might cause problems when one tries to make predictions out of the data, we believe the results about the existence of a correlation structure in the data are affected little by this.

The remaining data still has a high amount of missingness. We therefore proceded to impute it. We tested several algorithms on the dataset, readily available from the Fancyimpute python package [73]. They cover mostly matrix factorization approaches to imputation: SoftImpute [74], IterativeSVD [75] and MatrixFactorization [73] are all based on this principle. SimpleFill consists in replacing missing entries with the median, and KNN is K-Nearest Neighbours [76]. In Table 4 we report the Mean Average Error (MAE) and Mean Square Error (MSE) for the techniques adopted (obtained by holding out 0.5% of the data to test the quality of the results). Interestingly, the best performing technique is K-Nearest Neighbours (KNN). This is in line with the result of [77], which predicts GDP change over time for a country by averaging the past GDP changes of similar countries, where similarity is measured as an euclidean distance on a space defined by two macroeconomic indicators. This agreement might point to the fact that the most reliable way to model a country is by its similarity to similar countries already observed. The only metaparameter for the KNN algorithm (, the number of neighbours to average) has been chosen by means of grid searching on logarithmically separated values of and testing on a holdout set of size 0.5%. Table 5 shows that the best value for is either 2 or 4, depending on whether one minimizes MAE or MSE. We chose the average, . We have checked that the results do not change qualitatively if or is chosen.

imputer MAE MSE KNN 0.032636 0.088496 SoftImpute 0.061094 0.112322 IterativeSVD 0.112888 0.181256 MatrixFactorization 0.130820 0.200824 SimpleFill 0.238268 0.321349

| D | MAE | MSE |

|---|---|---|

| 1 | 0.033483 | 0.102603 |

| 2 | 0.030785 | 0.091696 |

| 3 | 0.031161 | 0.090172 |

| 4 | 0.031588 | 0.087745 |

| 5 | 0.032636 | 0.088496 |

| 6 | 0.033698 | 0.089346 |

| 8 | 0.036122 | 0.091546 |

| 11 | 0.039479 | 0.094866 |

| 14 | 0.042721 | 0.097449 |

| 18 | 0.046539 | 0.100678 |

| 23 | 0.050710 | 0.104088 |

| 29 | 0.055189 | 0.108290 |

| 37 | 0.060167 | 0.113266 |

| 48 | 0.065573 | 0.119146 |

| 61 | 0.070659 | 0.124860 |

| 78 | 0.075911 | 0.131326 |

| 100 | 0.081211 | 0.137930 |

We have investigated the influence of missing data on the results by adding a random white noise, with the value of the variance given by the Mean Square Error (MSE) when (the parameter of the KNN which optimises the MSE). We then recalculated the correlation matrix and reapplied the Directed Bubble Hierarchical Tree (DBHT) algorithm. Comparing the two different set of clusters tests whether the value imputed by the KNN is accurate. Practically, this comparison is achieved by applying a similar procedure that is detailed in section for comparing the DBHT clustering to the topics to see if the clusters in the imputed data are overexpressed. This overexpression indicates statistically whether our imputed data clusters are indeed present in the random data clusters. With a p-value of , which is the p-value of modified by Bonferoni correction, that all of the clusters in the imputed data are overexpressed and thus also present into the random data. We also tested whether the KNN algorithm for imputation is appropriate and does not significantly affect the results. This is accomplished by instead replacing the missing data with random white noise with mean and variance (since the indicator data are standardised before being imputed). Like before, we recalculate the correlation matrix, apply the DBHT algorithm and compare the two sets of clusters through the same procedure with a p-value of . Here, we find of the original clusters are overexpressed and thus present in this new random data. This is quite high considering that the assumption tested and total replacement of missing data (rather than just adding noise with a lower standard deviation) here is stronger than before.

Since the formation of the CDCIs relies on the clusters present in the data, we can therefore safely conclude that missing data does not change the final results significantly.

10.2 Distribution regularisation

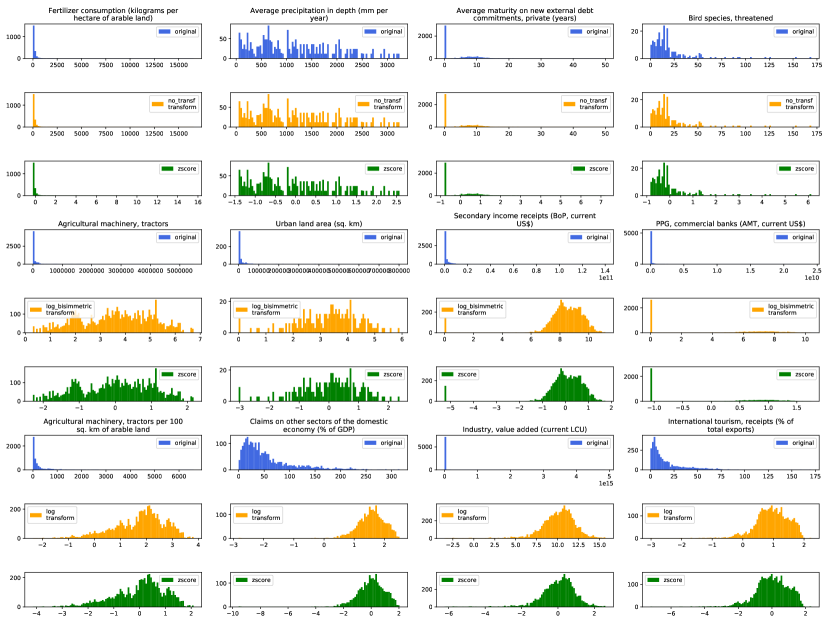

Another characteristic of the WDI dataset is the heterogeneity of the value distributions across different indicators. For example, many indicators are percentages, and as such are bounded between the values 0 and 100. Long-tailed distributions are very common, as well as some that might remind Gaussian distributions. A sample of these distributions can be seen in Fig. 10. We applied mathematical transformations to some of the indicators, in order to change their distribution and have a more homogeneous and tractable dataset.

We applied one of three possible transformations to each indicator. The first possibility is the identity function, i.e. we left the values unchanged. The second consists in taking the base-10 logarithm of the modulus of each indicator’s value. The third is the bisymmetric log transformation [78].

| (9) |

Given the high number of indicators and the need to avoid arbitrary decisions, the decision of what transformations to apply to each indicator has been made through an algorithm. To understand the criteria used, we will introduce first the definition of span of a set of numbers . We define span as:

| (10) |

In order to decide what transformation to apply to each indicator, we consider the set of all values for that indicator found in the dataset, . We then define two quantities. The first we will call in-span, which is the span for the subset of values found in such that . The second is the out-span, i.e. the span for all values of X that are outside the interval:

Then, the algorithm for assigning the transformation is this:

The rationale behind this algorithm is that frequently the values in X span a large number of orders of magnitude, and in this case we want to transform them so that their distribution is easier to manage with linear techniques such as PCA or factor models. If the numbers are all of the same sign and there is no zero in X, one can directly take the logarithm; otherwise we apply the log-bisymmetric transformation, which has no singularity on the zero and is defined for negative numbers.

After transforming the dataset with this algorithm, we z-score each indicator individually, so to set the mean to zero and the standard deviation to one. A sample of the results of this procedure can be seen in Fig. 10.

11 Eigenvalue Spectrum

Firstly, we should only extract components of that describe relevant interactions between indicators. The question then arises about how many principal components we keep [37]. This directly controls the size of the reduced correlation matrix - which we would like to be as small as possible - versus the fraction of the total variance of the indicator system that the reduced matrix can explain. It would also help us in identifying what economic indicators are responsible in driving the indicator system by analysing which are the main contributing indicators to the top eigenvalues.

The eigenvalues, however, could also be affected by noise from taking a finite sample [38]. We should therefore first study the empirical distribution of the eigenvalues, identifying those eigenvalues which are just noise and discarding them. To identify noisy eigenvalues, we will need a null distribution, produced from a Gaussian white noise process. The answer is provided by the well-known Marčenko-Pastur (MP) distribution [40], given by

| (11) |

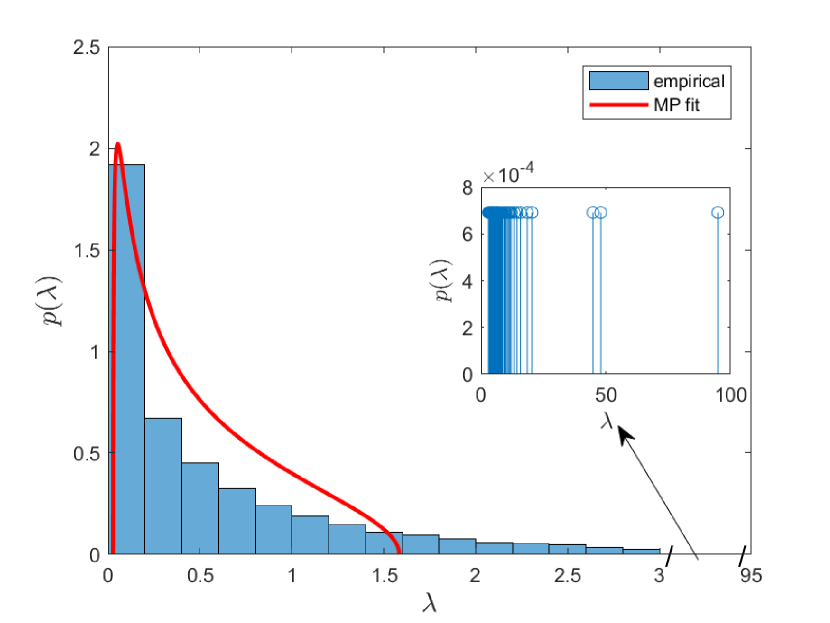

where is the probability density of eigenvalues having support in . The edge points , and is the standard deviation over all indicators. If we compare the distribution in Eq. 11 to the empirical eigenvalue distribution of , we will be able to see how many components are indistinguishable from noise, often called the ’bulk’ eigenvalues. These are then discarded. In practice, this is achieved by fitting Eq. Eq. 11 to the eigenvalues of , with and acting as free parameters. The results are shown in Fig. 11(a) which compares the empirical histogram of eigenvalues of and the best fit MP distribution in red, giving components beyond the upper limit of the MP distribution. Whilst this number appears large, it still means that we can reduce the size of the correlation matrix by before we start to include components which statistically can be seen as noise. Further methods can be used to reduce the number of components further e.g. cross validation or cumulative variance [37], and also [79].

However, by comparing the best fit MP distribution for our dataset in red in Fig. 11(a) we see that in fact there seems to be a noticeable deviation of the bulk eigenvalues from the MP distribution, so we can infer that the MP distribution may not be suitable in identifying noisy eigenvalues. We also notice that the best value of is noticeably different than the theoretical value for this dataset of indicating a significant difference in the predicted properties of the bulk using Eq. 11. Indeed, the use of the MP distribution in this respect has been questioned more recently [80, 81, 82] for financial data at least.

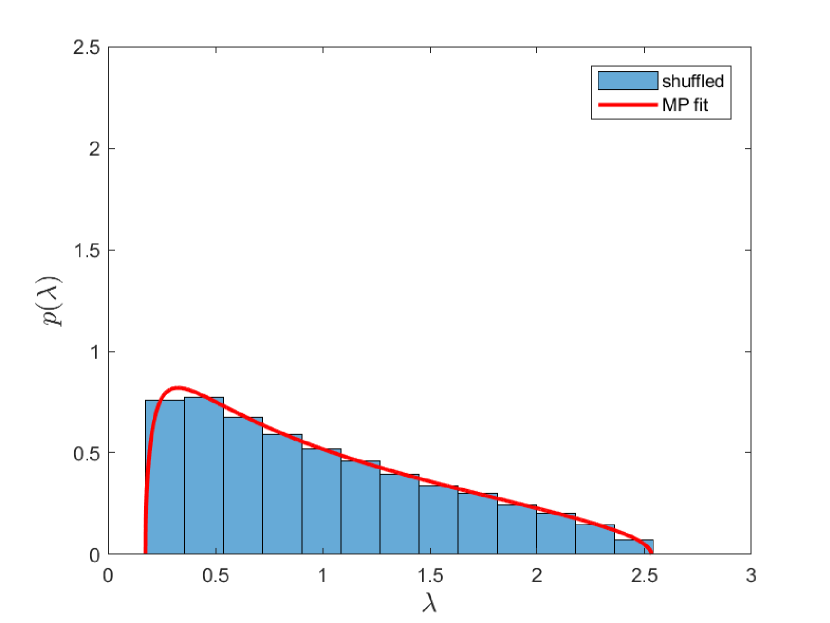

Moreover, it would also indicate that there could actually be some structure hidden within the bulk eigenvalues. We test this by shuffling our differenced indicator data, recalculating the correlation matrix and again finding the best MP fit to the eigenvalue distribution of this new correlation matrix. In doing so, we destroy the correlations between indicators, therefore testing whether these are the cause of the differences seen in the bulk in Fig. 11(a). The results are reported in Fig. 11(b), where the histogram of the eigenvalues coming from the new correlation matrix is in blue bars and the best MP fit for this given in red. We can clearly see an almost perfect fit in this case of the MP fit and much closer to theoretical value which Eq. 11 predicts, which suggests that indeed the earlier bulk eigenvalues are a result of non-trivial strucutre within , and are not just random fluctuations in the data. Overall, these two results together suggest that there is no natural way to a select a subset of principal components without loosing non-trivial information, which may make PCA an unsuitable method of dimensionality reduction for this dataset.

Nevertheless, as the inset plot in Fig. 11(a) shows, there are some eigenvalues whose magnitude is times greater than that of some of the smaller eigenvalues e.g. the first principal component has an eigenvalue of . These eigenvalues from the perspective of PCA are the most important eigenvalues since they make the biggest contributions to the overall variance of the system. They are also well separated from the bulk, which means that they are less affected by noise and will have a clearer, more discernible interpretation [20].

12 Procedure for calculating the p-values of

Here we detail the procedure used to calculate the p-values used to produce Table . Under the null hypothesis that is random, the entries of will be i.i.d normally distributed with mean and standard deviation of . We can therefore use the exact same definition given in Eq. (3) but with a randomly generated to produce an instance of under the null hypothesis. One can then estimate the empirical cumulative distribution function [83] of each entry by repeating this process many times and aggregating the results with the same . For Table , we repeat the process times.

13 PMFG network

Here, we report the visualisation of the PMFG network computed on in Fig. 12. From the PMFG, we can observe that there a few hubs of nodes which are connected to other less connected nodes, which is consistent with the observations from other complex networks in different contexts.

14 Elastic net regression

Elastic net regression is used to find the values of from Eq. (5). Further details of the use of this method is provided in this section. Elastic net regression [84] is a hybrid version of ridge regularisation and lasso regression, thus providing a way of dealing with correlated explanatory variables (in our case and ) and also performing feature selection, which takes into account non-interacting clusters that ridge regularisation would ignore. Elastic net regression solves the constrained minimisation problem

| (12) |

where is the vector of loadings given by , is the matrix consisting of columns and and are hyperparameters. is defined as

| (13) |