Calibration of the Pareto and related distributions—a reference-intrinsic approach

Abstract

We study two Bayesian (Reference Intrinsic and Jeffreys prior) and two frequentist (MLE and PWM) approaches to calibrating the Pareto and related distributions. Three of these approaches are compared in a simulation study and all four to investigate how much equity risk capital banks subject to Basel II banking regulations must hold. The Reference Intrinsic approach, which is invariant under one-to-one transformations of the data and parameter, performs better when fitting a generalised Pareto distribution to data simulated from a Pareto distribution and is competitive in the case study on equity capital requirements.

Keyowrds Generalised Pareto distribution, Intrinsic loss, invariance, Reference prior.

Correspondence details

J. Sharpe, Sharpe Actuarial ltd. London, UK. james@sharpeactuarial.co.uk

Miguel A. Juárez, School of Mathematics and Statistics, University of Sheffield, S3 7RH, Sheffield, UK. m.juarez@sheffield.ac.uk

1 The Generalised Pareto and related distributions

The Generalised Pareto distribution (GPD) is widely used in engineering, environmental science and finance to model low probability events. Typically the GPD is used to estimate extreme percentiles such as the 99th percentile for a specific event. This might be used for setting the height of flood wall defences or estimating how much capital banks might hold for specific market risks.

We say that the positive quantity follows a GPD if it has probability density function (PDF)

| (1) |

with . The support of the distribution if , while if ; thus is a shape and is scale parameter. The mean,

exist iff and , respectively.

The GPD is related to several distributions. It clearly has an exponential distribution with mean as a special case when . Further, follows a Pareto distribution, , if , where

| (2) |

and an inverted-Pareto, , if , where

| (3) |

In the latter case, , distributes uniformly on ; follows a Beta distribution, ; and follows a location (or shifted) Exponential distribution,

where . If the shape is fixed, follows an Exponential distribution with rate , . Similarly, if follows a , then follows a . If a sample, = , from the Pareto distribution is available, is sufficient, with and . No such sufficient statistics exist for the GPD.

One key feature of this family of distributions is their so-called lack of memory, a property at the core of their prominence in extreme value theory, related to peaks-over-threshold theory described in Section 1.1. Specifically let and consider , it is straightforward to prove that , with , hence , which is commonly used to graphically check model fit (davidson). It is immediate to check that if follows a then , provided , and thus a similar graphical model fit check can be carried out.

In this paper we consider the Bayesian Reference Intrinsic (BRI) approach (io; rueda; intint) for calibrating this family of distributions, and compare it with three alternative approaches, Maximum Likelihood (ML), Probability Weighted Moments (PWM) and a Bayesian approach using a Jeffreys prior, implemented using Markov chain Monte Carlo (MCMC). A simulation study is carried out comparing the average mean square error of three of the four approaches when calibrated to synthetic data from a Pareto distribution. These methods are then applied to some equity return data in a case study and the results compared.

1.1 The GPD and extremes

The GPD was first introduced by Pickands in the extreme value framework as a distribution of sample excesses over a sufficiently high threshold (zea1; zea2). Two key theories of the extreme value framework the GPD arose from are summarised below —we use the second theory in the case study in Section 5.

1.1.1 Extreme Value Theory 1

Let be a sequence of iid random variables. If these are divided into blocks of size , and (i.e. the largest value in each block), then the follow a Generalised Extreme Value (GEV) distribution, with cumulative distribution function (CDF)

with the scale parameter and the shape parameter (frey, p. 265). Thus, the distribution of the maxima of blocks of data from almost any probability distribution follows a GEV with some shape parameter .

1.1.2 Extreme Value Theory 2 (Picklands-Balkema-de Haan)

Let be a random quantity with CDF . The excess over threshold has CDF

for , where is the upper bound of the support of .

There is a positive measurable function such that

where is the shape parameter of the GPD and is the scale parameter, which is a function of the threshold (frey, p. 277). This means that whilst the scale parameter changes as the threshold changes, the shape parameter stays the same. The distributions for which the block maxima converge to a GEV distribution constitute a set of distributions for which the excess distribution converges to the GPD as the threshold is raised. The shape parameter of the GPD of the excesses is the same as the shape parameter of the GEV of block maxima. This means that the excess above a threshold can effectively be modelled by a GPD (almost) regardless of the distribution of the full data set as long as the threshold is high enough. This feature is used in a case study in Section 5.2, where the GPD is calibrated to just the tail of the data.

Characterising the GPD and deriving probabilistic and statistical results are extensively addressed in the literature (e.g. see gala2; leadbetter; beirlant; Embrechts; Coles; Kotz; Castillo; Haan, and references therein). Several approaches have been proposed to calibrate the GPD mainly focussing on the MLE, PWM or Method of Moments (MoM) (see e.g. zea1; zea2, and references therein). More recently, Bayesian approaches have been investigated (see e.g. Lima; Ragulina; Juarez; Tancredi; Turkman). Gilleland reviews available software for estimation. We refer the reader to zea1; zea2 which include summary tables of papers describing how the GPD is calibrated to a wide range of data sets, reproduced in Table LABEL:tab:paps in the Appendix to show some of the extensive literature covering calibration of the GPD.

1.2 The Pareto principle: the Lorenz curve and Gini index

The ‘80-20 rule’ or Pareto principle has reached popular culture through books such as Koch. It is a way of more easily explaining the calibration of a Pareto or GPD. An example of this is the 80-20 rule identified by V. Pareto in 1897 that 20% of the population had 80% of the wealth (Persky). It is possible to use the calibration of the GPD to identify the Pareto principle parameters through the Lorenz curve and Gini index. The Lorenz curve,

where is the CDF of the random quantity and its expected value, describes precisely this relationship. In case the distribution of the size is homogenous, i.e. ‘% of the population accumulates % of the income’, then . This motivates some measures of inequality, such as the Gini index,

which is the relative area under , respect to the straight line: the closer to 0(1), the more(less) egalitarian the distribution. For the GPD,

depend only on the shape parameter, thus inference on and/or is tantamount to inference on this parameter, which is explored in Section 5.

2 Intrinsic calibration

The Bayesian reference-intrinsic (BRI) approach (io; rueda) provides a non-subjective Bayesian alternative to point estimation, based on the reference prior (sun; sun2) and an intrinsic loss function (Robert). In short, Let be a probability model assumed to describe the probabilistic behaviour of the observables , and suppose that a point estimator, , of the parameter is required. From a Bayesian decision standpoint, the optimal estimate, , minimises the expected loss,

where is a loss function measuring the consequences of estimating by and is the decision maker posterior distribution. The BRI approach argues that in fact one is interested in using as a proxy of and thus the loss function should reflect this. It advocates the use of the Kullback–Leibler (KL) divergence as an appropriate measure of discrepancy between two distributions. The KL (or directed logarithmic) divergence,

is nonnegative and nought if and only if , and it is invariant under one-to-one transformations of either or . However, the KL divergence is not symmetric and it diverges if the support of is a strict subset of the support of . To simultaneously address these two unwelcome features io propose to use the intrinsic discrepancy,

| (4) |

a symmetrised version of the KL divergence. This is taken as the quantity of interest, for which a reference posterior is derived. The intrinsic estimator can then be obtained.

Definition 1 (Bayesian intrinsic estimator).

Let be a family of probability models for some observable data , where the sample space, may possibly depend on the parameter value. The BRI estimator,

| where | |||

is the intrinsic expected loss and is the reference posterior for the intrinsic discrepancy, , as defined in (4).

Within the same methodology one can also obtain interval estimates, i.e. credible regions.

Definition 2 (Bayesian intrinsic interval).

Let and be as in Definition 1. A BRI interval, , of probability , is a subset of the parameter space such that

for all and .

BRI credible regions are typically unique and, since they are based in the invariant intrinsic discrepancy loss, they are also invariant under one-to-one transformations (intint).

2.1 Calibration for the Pareto family of distributions

In Section 1.1 we highlighted the relationship between the GPD and the Pareto and Inverse Pareto distributions. The main characteristic we will exploit here is that the GPD shape parameter remains invariant to any of those transformations, whilst the GPD scale parameter is linearly transformed. Given that the support of the inverted Pareto is bounded, it is easier to calibrate directly than the Pareto or the GPD. For this reason we choose to work with this parameterisation and apply the results to the GPD parameters by the above simple transformations.

Let be a random sample from an , using (3), the likelihood is

are jointly sufficient, with . Moreover, given the MLE,

are conditionally independent, with sampling distributions and , where the latter is an inverted Gamma distribution (malik).

The conjugate prior is a Pareto-Gamma distribution,

| (5) |

which yields a Gamma marginal posterior , where and . For any choice of prior parameters, the posterior is asymptotically Gaussian and will converge to a mass point at a.s. as .

From (4), the intrinsic discrepancy for the inverted Pareto distribution, , when the parameter of interest is the shape, can be written as

| (6) |

with , which does not depend on . Following Juarez, given that (6) is a (piecewise) one-to-one function of , we can use the reference prior , a liming case of (5), which yields the marginal posterior , for . The intrinsic expected loss,

is defined for all and can be calculated numerically. Due to the asymptotic Gaussianity of the posterior, the approximations and , work well even for moderate sample sizes.

The intrinsic discrepancy when the scale is the parameter of interest is

where . The reference prior is , or in terms of the original parameterisation, ; which is not a limiting case of the Pareto-Gamma family.

In this case the loss function depends on both parameters and thus

| (7) | |||

| with | |||

| (8) | |||

| and | |||

The corresponding Bayes rule can be calculated numerically. An analytical approximation, which works well even for moderate sample sizes, can be obtained by substituting the shape parameter with a consistent estimator in (8), carrying out the one dimensional integration and then solving (7). Using the MLE, , yields .

The Uniform and location-Exponential models are particular cases of the inverted Pareto (see Section 1). For the former, we have = and in this case the intrinsic discrepancy is

and the corresponding reference prior is , which yields a posterior, with the MLE. The expected intrinsic discrepancy has a simple analytical form,

where . It is immediate to prove that the BRI estimator, , is the median of the posterior, highlighting its invariance under one-to-one transformations. Indeed, the BRI estimator of the parameter in the location-Exponential model, , where , i.e. the distribution obtained by letting , is .

3 Alternative approaches

We briefly describe two alternative frequentist approaches, maximum likelihood estimate (MLE) and probability weighted moments (PWM). We also describe a Bayesian approach that uses a Jeffreys prior which yields a proper posterior for any sample size. The posterior has no analytical form, so we implement an MCMC strategy to sample from it.

3.1 Jeffreys prior

For an alternative Bayesian approach, we use the independent Jeffreys prior,

which, despite being improper, yields a proper posterior for any sample size (castellanos). The posterior, , is not analytical, so we implement an MCMC scheme to carry out inference. Our strategy is a Metropolis-within-Gibbs algorithm with full conditionals

To set the proposal distributions, one must bear in mind the parameter space depends on the sample space; specifically, if . Hence, for the shape parameter, , we propose from a truncated Gaussian with mode at the MLE, and upper bound at , where is the current state of the shape; we use the free parameter to control the acceptance rate. For the scale, , if the current state of the shape, , we use a Gamma proposal with mode at the and use the free parameter to control the acceptance rate; otherwise, we propose from a truncated Gaussian with lower bound at , mode at , and use the free parameter to control the acceptance rate. Our R code is available under request from the corresponding author.

3.2 Two frequentist approaches

3.2.1 Maximum likelihood

For a sample = from a , the log-likelihood can be expressed as

The MLE exist only for and is typically found using numerical methods. If , its sampling distribution is asymptotically Gaussian with covariance matrix (zea1)

3.2.2 Probability weighted moments

Probability weighted moments (PWM), or L-moments,

characterise the distribution function of a random quantity and are exploited as a robust alternative to the method of moments for point estimation Greenwood. Particularly for the GPD, Diebolt, suggest using

from which

The corresponding PWM estimators are obtained by substituting and by the estimators , with the -th order statistic. Various expressions are available for , in the sequel we use , with and as in zea1. For large sample sizes and if , the PWM estimators are asymptotically Gaussian (Diebolt) with covariance matrix

land have a different angle, exploiting the lack of memory to find a threshold and then estimate the shape parameter for the tail distribution of the size of agricultural land by county in the USA.

4 Synthetic data and comparison

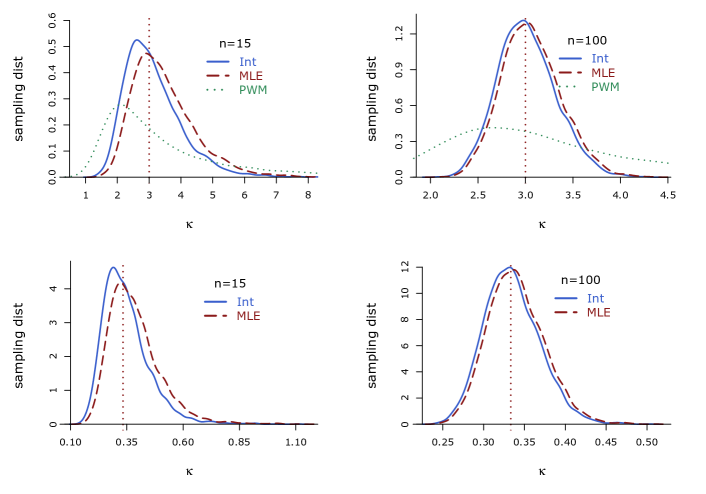

We carry out a simulation study to compare the calibration efficiency of the BRI, the ML and PWM estimators and present results on the shape parameter only for brevity. As the MHA is itself a time consuming simulation process it has been left out of this comparison. We generate 10,000 samples of size , from a Pareto distribution, —which is linked to the GPD as described in Section 1—, with and . The parameters are calibrated using the BRI, ML and PWM approaches, their sampling distribution are estimated and their bias and mean squared error (MSE) used as efficiency measures, illustrated in Table 1.

| BRI | MLE | PWM | |||||

|---|---|---|---|---|---|---|---|

| Bias | MSE | Bias | MSE | Bias | MSE | ||

| 1/3 | 15 | 0.135 | 0.865 | 0.475 | 1.365 | 0.691 | 16932 |

| 50 | 0.036 | 0.191 | 0.129 | 0.218 | 11.75 | 6282 | |

| 100 | 0.018 | 0.095 | 0.063 | 0.102 | 1.096 | 1039 | |

| 3 | 15 | 0.014 | 0.011 | 0.052 | 0.016 | 0.802 | 13.88 |

| 50 | 0.003 | 0.002 | 0.013 | 0.003 | 0.711 | 0.508 | |

| 100 | 0.002 | 0.001 | 0.007 | 0.001 | 0.688 | 0.474 | |

| 7 | 15 | 0.007 | 0.002 | -0.009 | 0.001 | -0.131 | 0.128 |

| 50 | 0.002 | 0.0005 | -0.003 | 0.0004 | -0.039 | 0.030 | |

| 100 | 0.0009 | 0.0002 | -0.0015 | 0.0002 | -0.019 | 0.014 | |

Given that PWM works well only if (at least) the first two moments of the distribution exist it is not striking to confirm its poor performance for values of (Hosking), regardless of the sample size. In contrast, both MLE and BRI estimators yield relatively low bias and MSE, even for moderate sample sizes, with their sampling distributions becoming increasingly similar as the sample size grows (Figure 1). Both estimators are invariant under one-to-one transformations, while PWM is not; further, BRI credible intervals are invariant, a feature we will exploit in the sequel.

5 Bank equity capital requirements

We apply the calibration approaches described above to equity risk capital that banks are required to hold in the banking Basel II regulations. In the Basel II regulations in pghs.700 and 718 (LXXVI)111http://www.bis.org/publ/bcbs128b.pdf a value-at-risk () approach is required for a 99th percentile one sided confidence interval on 10 day equity returns. This means a bank will estimate what it thinks the 99th percentile 10 day equity returns can fall by (for example it might estimate this as a 10% fall in its equities market value) and it is then required to hold at least this amount as a monetary capital amount on its balance sheet to demonstrate the bank can withstand a 99th percentile fall in the value of its equities.

The regulations mention a number of approaches are possible to calculate this VAR and in this case study a GPD is fitted to an historic time series of an equity index of 10 day returns. The equity index used here is the FTSE 100 index taken from yahoo finance 2/4/1984-–26/7/2013222Available from http://uk.finance.yahoo.com/q/hp?s=5EFTSE.

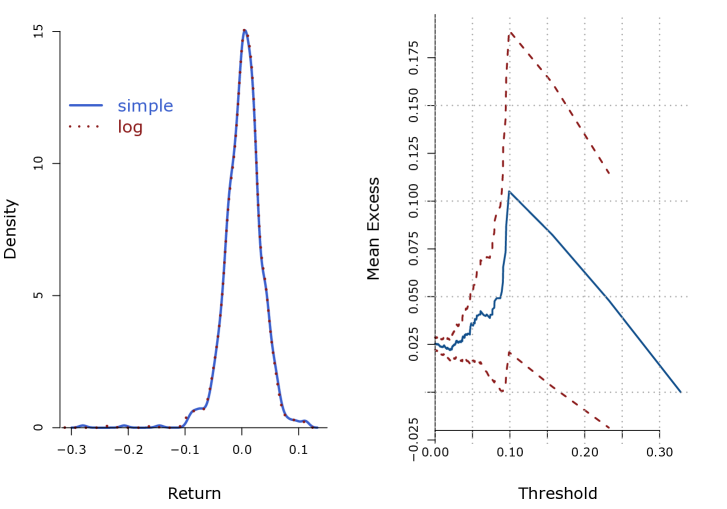

The raw data have been pre-processed to convert the daily index values into 10 day returns, (i.e. the percentage change in value of the index over non overlapping 10 day periods). A common question is either to use simple returns, where is the index value at time , or log-returns, . Whilst the difference between these two definitions is not crucial for a 10 day period, the log returns have been used in this case study. This is because the left tail is of interest and is unbounded for the log return, but bounded at -100% for the simple return. An unbounded domain is potentially more appropriate for the GPD calibration. When the 99th percentile has been calibrated in log returns, this needs to be converted back to a simple return for the VAR value. For example if an -11% fall in equity values is the log return 99th percentile, this is a simple return fall in equity market value.

5.1 Exploratory data analysis

We explore some basic features of the data, presented for both simple and log returns on the left panel of Figure 2.

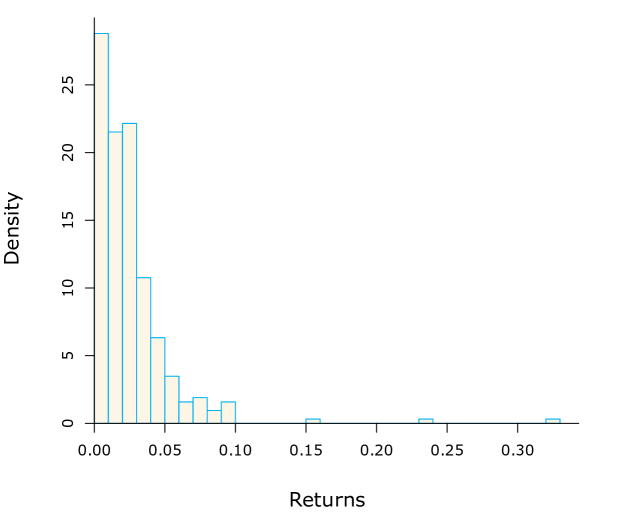

We would like to highlight that the distribution of the returns is fat tailed—it has a higher frequency of extreme events compared to a Gaussian distribution—as measured by its kurtosis (that of a Gaussian distribution is 3). It is also negatively skewed—a higher proportion on events are on the left hand side of the mean, which emphasises the underlying financial risks. Plotting the Mean Excess (ME) function, , is often used to explore whether the data has power tails (Ghosh). A characteristic of a fat tailed GPD type distribution with negative shape parameter is an increasing straight line, while a decreasing line indicates thin tails; a horizontal line suggests exponential tails. The right panel in Figure 2 shows the mean excess plot of the absolute value of the negative log returns, which displays a positive slope (up to losses of about 10%) suggesting a power distribution is appropriate for this data. Combining this features with Figure 3 suggest a GPD with a negative shape parameter may be appropriate to model the negative returns of this data set.

5.2 Peaks over threshold

We now apply the calibration approaches described in Section 2.1 and 3 to the left tail of the 10-day FTSE100 log-returns, using the peaks over threshold approach (frey, with theory as in Section 1.1.2), which allows the focus to be on the percentiles of interest.

We do not discuss how to set the threshold, but refer the reader to zea2. frey suggest using the ME plot as a guide to threshold setting. We subjectively pick -5% as the approximate point on the mean excess plot beyond which the slope appears to increase faster and end up with . It is noted there are still enough points beyond this level for reasonable calibration and the threshold is expected to be sufficiently high for the Picklands-Balkema-de Haan theorem to apply.

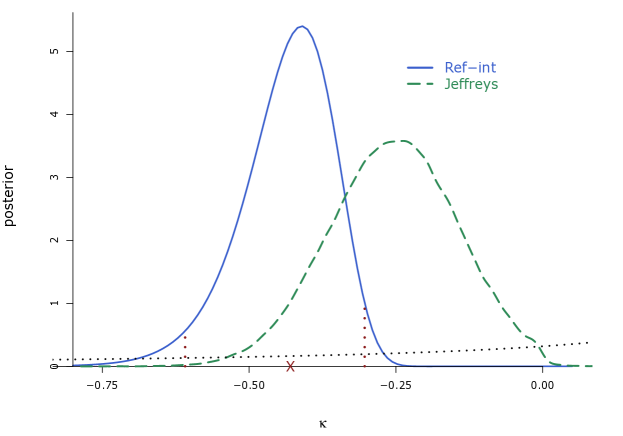

Relying on the fact that if then , we use the methods in Section 2.1 to obtain point and interval estimates of the shape parameter. The MLE is straightforward to obtain, , where , is the geometric mean and is the MLE of the shape. The marginal posterior distribution of the shape parameter is , the BRI point estimate and interval are illustrated in Figure 4. In particular, notice the intrinsic interval is different from the HPD, , highlight the fact that HPDs are not invariant under transformations, while the intrinsic is. Given that the scale parameter typically is a nuisance parameter, we use the analytical approximation to the BRI estimator,

We use quasi-Newton (Fletcher) to maximise the likelihood for the GPD, yielding MLEs and . The confidence intervals are found from the observed covariance matrix, which gives a standard errors for of 0.228, thus an approximate 95% confidence intervals for the shape is . Using PWM, one gets and , with a CI of approximate 95% for . Exploiting the invariance of the BRI estimator, and the BRI interval of probability 0.95. To fit the Bayesian model with Jeffreys prior, we generated chains of length , dropped the first as burn-in and thinned every fifth draw, ending up with samples of size 198,000 for inference, the marginal posterior distributions are illustrated in Figure 4. The posterior mean and median of the shape are and , respectively and the equally tailed interval of posterior probability 0.95 is . Note both frequentist CIs include 0, suggesting an exponential tail behaviour, while the Bayesian alternatives strongly support heavy tails; also notice the intrinsic posterior has a smaller variance, hence the BRI interval is shorter than the equally tailed from Jeffreys prior.

The Pareto Principle and Gini index discussed in Section 1.2 depend only on the shape parameter, so we can use the invariance of the BRI and MLE approaches to calculate point and interval estimates shown in Table 2. As the calibration of the GPD is based on the tail of the data, we exploit its lack of memory to calculate

where is the threshold and is empirically estimated as the proportion of data points above the threshold relative to total number of data points (frey, p. 283); in our case .

| Gini index | |||

|---|---|---|---|

| BRI | |||

| Jeffreys | |||

| ML | |||

| PWM |

It is worth noticing both frequentist approaches not rule out , while the Bayesian alternatives suggest , but all point estimates are negative. The posterior distribution from the intrinsic approach is shifted to the right, compared to the Jeffreys alternative and has a smaller variance. Frequentist confidence intervals are wider than the Bayesian credible counterparts.

6 Final remarks

We have illustrated how the BRI approach can be used to calibrate the GPD by using a transformation from the inverted-Pareto distribution. Four different approaches to calibrating the GPD have been presented. Three of the approaches were compared in a simulation study of some simulated data from a Pareto distribution. All four approaches were then compared for similarities and differences in a case study.

From the simulation study it is apparent that the repeated sampling behaviour of the PWM estimator is poor in general and some modification is needed if it is to work in practice (see e.g. Chen). The results also indicate the BRI estimator has a lower MSE than the MLE even for moderated sample size, and also displays asymptotic Gaussianity (Figure 1 and Table 1). Combined with its invariance under one-to-one transformations make it a competitive alternative for calibration. One limitation of this simulation study was that it only simulated data from a Pareto distribution. An extension might be to compare the calibration approaches for data simulated from other distributions.

The case study shows a practical example of how all four approaches can be used to calibrate the GPD. Whilst there are some differences between the parameters for each of the four approaches, the point estimates of are roughly similar, suggesting a level between 9% and 10% for regulatory equity capital might appropriately meet the Basel II regulations. Point estimates of the shape and scale (not shown) parameters are roughly similar for each calibration approach, barring Jeffreys, which shrinks the estimate towards the origin; however, the length of the interval Bayesian estimates are shorter than their frequentist counterparts. Moreover, frequentist interval estimates for are difficult to get, while those from Jeffreys prior are straightforward from the MCMC output.

The BRI approach has produced lower mean squared errors in the simulation studies, suggesting it to be more accurate for parameter estimation when the data is indeed from a Pareto distribution. The MLE is relatively simple to understand and implement however there are questions over the convergence of the numerical optimisation methods, especially with fewer data points (zea1). The PWM is likewise simple to understand and implement, but is efficient only for a subset of the parameter space and it could produce estimates with a likelihood of zero.

The MHA was left out of the simulation study as it is computationally intense. The results in Section 5.2 were obtained by running one million simulations. It would not be possible to run to this level of accuracy and carry out an outer layer 1000 simulation analysis in a reasonable time period or without much greater computer power. Also, implementing the sampler has a number of practical issues that are different for each data set, which may take time to resolve and ensure the MHA converges in a reasonable time period. However, our implementation is robust and may be used as an off-the-shelf option.

One area of interest that could be the subject of further work is how sensitive the results are to the threshold used for each calibration method. A study might repeat the analysis looking at various different thresholds and how that impacts the shape, scale and for each threshold.

Another area of potential interest is how the time period of each data point impacts the shape parameter and GPD calibrations. For example if the case study looked at equity returns over 1 day, 5 days, 1 year, etc. What would the impact be on the GPD calibration? Clearly a large time step for each data point would be expected to give higher values for the 99th percentile, but would the Gini index remain invariant to other size time steps as for the 10 day period investigated in this case study?