Some analytically solvable problems of the mean-field games theory

Abstract.

We study the mean field games equations [1], consisting of the coupled Kolmogorov-Fokker-Planck and Hamilton-Jacobi-Bellman equations. The equations are complemented by initial and terminal conditions. It is shown that with some specific choice of data, this problem can be reduced to solving a quadratically nonlinear system of ODEs. This situation occurs naturally in economic applications. As an example, the problem of forming an investor s opinion on an asset is considered.

1. Introduction

The theory of Mean field games (MFG) studies the models with a large number of small components (agents) that interact with each other achieving their individual objectives. The term ”mean field” means that the strategy of each agent to achieve the maximum of its individual utility directly depends on the average distribution of influences of other agents and does not depend on the initial configuration of the system. The mean field theory is well known in statistical physics, but similar concepts related to active objects [1], [2] were formulated only in the last decade. These concepts, together with the optimal control theory, have made it possible to study models in economics and sociology. Now MFG are widely used in areas requiring analysis of differential games with a large number of participants.

Here is a heuristic derivation of MFG equations, following [1]. More details can be found in [3]. Let us assume that averaged behavior of the agents is described by Ito stochastic process that is given as

| (1) |

where is a point in the space of the states, , is a standard Brownian motion, is a positive constant, is a parameter, choosing the value of which from a given Borel set at any time , one can control the process (the stochastic process is an admissible Markov control). Fixing , we mark trajectory for a specific agent.

The problem of control is to define maximum over all the admissible controls of the expresssion

where and are prescribed continuous functions and the process obeys (1).

Let us consider the payoff function as

The Hamilton-Jacobi-Bellman equation which allows to solve the problem above is (see [4] )

| (2) |

where

with the terminal condition

We denote the probability density of process (1) as .

In what follows, we consider a particular case

Thus, we assume that each agent receives a penalty for changing its position in the phase space and seeks to maximize its individual utility function, based on the fact that he knows only the distribution of the other agents. The choice of the function depends on the type of problem.

Based on the specific form of the quality function , we obtain from (2)

Thus, if initially the density function is known, we get the following initial-terminal problem for coupled Hamilton-Jacobi and Kolmogorov-Fokker-Planck equations (, ):

| (3) | ||||

| (4) | ||||

| (5) |

It is known that under certain natural assumptions (boundedness and Lipschitz continuity of and ) problem (3)–(5) has only one classical solution [5].

The aim of this work is

1. To show that for some choice of and the solution of problem (3)–(5) can be reduced to the solution of a system of Riccati equations.

2. To show that waiving the requirement of boundedness of and , we can construct an example of nonexistence of solution to (3)–(5).

3. To show that the position of the maximum of density can be analytically found even though it is impossible to find solution of (3)–(5) for all time interval .

4. To give an example of economic problem where and have a form that allows to find a solution using the Riccati equations.

2. Reduction to Riccati equations

First of all, we note that from a mathematical point of view, it is interesting to analyze the function , which depends on , because in this case the equations (3) and (4) turn out to be linked. However, from the point of view of applications, the presence of in the utility function of agents is not critical. Indeed, if increases then this means that it is beneficial for agents to stay closer to the maximum of . However, the presence of the term already means that agents tend to resemble each other, this creates movement in the same direction.

Therefore, we consider a simpler case when depends only on . We need it for applications below. We could, without prejudice to the method, add the term to (which was done in [6]), however, for the sake of simplicity, we refuse this.

We also could consider a multidimensional analog of the problem () via reducing the problem to the Riccati matrix equations. However, the analysis of the obtained equations is a separate difficult problem and we strive to get the simplest model.

2.1. Gaussian distribution

Let , where , and is the normalization constant. Let also , where are arbitrary constants. We look for a solution to system (3), (4) in the form

which imposes the terminal condition with constants .

Substitution into the system and equating the coefficients at the same powers of gives the following set of equations:

| (6) | ||||

| (7) | ||||

| (8) | ||||

| (9) | ||||

The initial-terminal conditions are the following:

First, we note that equation (6) which can be elementary solved under the terminal condition is separated from the system and determines its dynamics. Indeed, knowing , we find from (8). Then we can find all the remaining functions. It is easy to calculate that the solution is given by the following formulae:

-

•

at :

(10) -

•

at :

(11) -

•

at :

(12)

Analyzing (10) and (11), it is easy to see that for the solution with terminal condition exists for for all , while for the solution with any terminal condition can exist only for . When and the solution also does not exist for all .

Further, we note that the position of maximum of , ), which can be found as , can be described by equation

| (13) |

and

Thus, the position of maximum either experiences fluctuations (at ), or tends to reach a certain constant value outside boundary layers near and . We know the initial condition , while to determine the second constant of integration it is necessary to use explicit expressions for and .

Note that the function can be found as a solution to the corresponding linear equations and written in elementary functions, but in a very cumbersome way, while the dynamics of is very simple.

Let us analyze the qualitative behavior of the solution of (6), (7), (13) with boundary conditions

First, we note that for the solution of system (6), (7), has a stable equilibrium , to which the solution converges exponentially under any terminal conditions ensuring the continuation of the solution on the entire semi-axis . Therefore, if is large enough, then the solution of (13) outside the boundary layers near and differs little from . We will give pictures for specific data in the next section when we analyze an economical problem.

Let us note that the function can be found for all , although it satisfies a linear first-order equation, the coefficients of which can become unbounded. For , the form is the simplest:

We can see that the formula is also defined for positive , the only restriction is the condition . In this case, the position of the maximum has no limit as and with an increase in , the maximum of deviates unboundedly from its initial position.

If , the position of maximum is described as follows:

where

The position of the maximum of density varies periodically around .

For the solution is

where , are functions which do not have singularities, specifically,

2.2. Distribution on the semi-axis .

Let , where , and is the normalization constant. For the solution of (3) to be symmetric about zero along the entire axis, we require

where are arbitrary constants. We find a solution to system (3), (4) in the form

| (14) |

with the terminal condition with constants . In fact, we are looking for a solution to (3), (4) with the boundary condition .

Substituting (14) in (3), (4) gives the following system:

| (15) | ||||

The initial-terminal conditions have the following form

The maximum of density is at the point . It is easy to calculate that the position of the maximum satisfies the following Bernoulli equation:

| (16) |

where can be found according (10), (11) and (12). The system (15), (16) has the first integral

which allows to express from , specifically:

| (17) |

where . From (17) we can find that, as in Sec.2.1, the function does not have singularities inside the interval , even if goes to infinity. In these points tends to zero. If , then for large the maximum of density is close to the equilibrium .

3. An example of application of the mean field game theory: forming the opinion of investors about the asset

We give an example showing that the solutions found in the previous section have natural applications in the field of financial mathematics. To do this, consider a market in which a large number of investors operate, managing their own portfolio of securities, consisting of a risky asset and a deposit, by solving the Merton problem [7].

3.1. Individual strategy

Let us retell the statement of the problem, which each investor solves individually, following [6], Example 11.2.5.

The price of the risky asset is described by the stochastic differential equation

| (18) |

where is the standard Wiener process , . In the economic context, these values are commonly called the drift parameter and the volatility parameter, respectively. The price of the risk-free asset is determined only by a constant interest rate :

Suppose that the investor operates the portfolio , which consists of risky and risk-free assets, with and being the shares of capital invested in risk and risk-free assets, respectively, . Then

Let us denote , . The change in the value of the portfolio has the following form::

| (19) |

Assume that starting with capital at the time , the investor wants to maximize the expected return on capital at some subsequent point of time . If we set the utility function , which is usually assumed to be increasing and convex upward, then the problem reduces to finding the function and the Markov control , such that

where is the Markov control, . In order to solve this problem we should define a differential operator

and solve the Hamilton-Jacobi-Bellman equation:

| (20) | |||

If and , then the solution is . Substituting this expression in (20) gives the following boundary value problem for :

| (21) | |||

As a utility function we take , , , or . The latter function formally corresponds to the limit . All these functions belong to the class HARA (hyperbolic absolute risk aversion) [8]. In addition, the case corresponds to the strategy of the investor who prefers the least risky investments, corresponds to risk-neutral strategies, corresponds to the risk-prone investor [9], Sec.2.

The solution (21) can be found in the form , the corresponding optimal strategy at all is

| (22) |

3.2. Collective strategy

Now let us describe the collective behavior of investors. We assume that they all manage the portfolio based on their own ideas about the parameters (drift and volatility parameters) of the risk asset. In other words, each fixed investor carries out control based on the equation (18) with its own choice of and . The true values of these parameters (we denote them by and ) are unknown to investors. These true values may differ from those accepted in the market, and they manifest themselves only in that the investor receives a penalty for their incorrect choice.

It is believed that the opinions of investors about the correct value of the drift parameter are distributed normally along the entire axis, the maximum is initially at .

The volatility obeys some positive distribution and its density initially has a maximum at some point . At the same time, investors receive a penalty both for deviating from the ”true” values of the drift and volatility parameters, and for deviating from the majority opinion. A significant simplification that stems from the desire to obtain an analytical solution to the problem is the assumption that all investors treat risk the same way, guided by the same utility function .

During the control process, the initial distributions of drift and volatility parameters change with the desire to maximize capital growth rate.

We will be interested in how the position of the distribution maximum changes in response to the control method, that is, how the market is forming an opinion about the parameters of a risky asset.

We obtain a typical optimization problem of the theory of mean-field games (1), when the random variables or play the role of , subordinate to (1), , and

, , , , is some smooth function of volatility, is a function simulating penalty for an investor who incorrectly guesses the parameters of the risky asset. It is chosen for reasons of convenience, for example, . The presence of the function , where is the value of the maximum of density at a fixed time models a penalty for deviating the opinion of a investor about a risky asset from the majority opinion. As we have already noted, the first term under the integral in (1) serves the same purpose. Moreover, it can be analytically shown that the equation describing the position of the distribution maximum does not change if we assume , the presence of this term will only lead to a more pronounced maximum, which is also confirmed by numerical analysis. Therefore, below we assume . The coefficients and can be considered equal to zero or not, depending on what problems we are studying.

As application of the results of the previous sections, we consider two separate cases. In the first of them, we suppose that the volatility of a risky asset is known and an opinion is formed regarding its drift. In the second, on the contrary, the drift parameter is considered known, and an opinion is formed about volatility.

3.3. The opinion about the parameter of drift

So, we assume that the volatility is fixed, . The system of equations (3)–(5) has the following form:

| (23) | ||||

| (24) |

where .

Thus, in the notation of Sec.2.1

According to the results of Sec.2.1, the solution of (23)–(3.4) exists for all , if and only if and . However, the position of the maximum of can always be determined. Namely, if (), then for large the position of maximum is close to

In other words, in this case, investors form an opinion about the asset. If (), then the maximum of oscillates periodically, sometimes deviating significantly from its average value. The frequency of these oscillations increases with . In this case, we say that investors cannot agree on the parameters of asset.

Let us analyze this result from the point of view of the agent’s behavior when investing for a long period of time.

-

•

If , that is, investors adhere to a rather risky strategy (), then the market forms the opinion about the correct value of , even if . In the threshold case most investors believe that the correct return on a risky asset is close to the risk-free rate of the asset and avoid investing in a risky asset. If , then, otherwise, the opinion tends to the ”true” value of .

-

•

If , that is, the investors are rather cautious (), then

-

–

without the presence of a penalty for the wrong choice of an opinion on the return of the asset does not form.

-

–

If or is sufficiently large, then is close to the ”true” value .

-

–

The similar effect has an unlimited increase of or , since .

In other words, very cautious investors quickly form the correct opinion about the asset, and this the faster, the greater the volatility.

-

–

-

•

Since , the smaller the randomness component in the value of the risky asset, the more difficult it is for investors to come to a common opinion about it. Indeed, to ensure the condition for a fixed , so we should choose a large value of . This situation seems paradoxical, but can be explained as follows: if the investor is dealing with a low-risk asset, then he is inclined to adhere to a more risky strategy, that is, choose a larger . It is easy to see that if , then tends to zero, which helps to determine the correct value of .

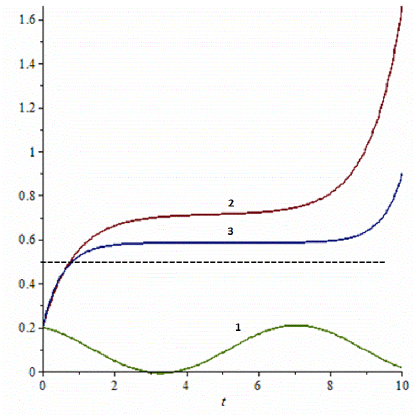

The typical behavior of the maximum of density is represented on Fig.1.

3.4. Opinion on volatility

Now suppose that the parameter of the asset is known, and the agents make their assumptions regarding volatility. Unlike the previous problem, we cannot assume that is distributed on the entire axis and we should consider some positive distribution of it. In order to be able to obtain an analytical solution, we consider instead of the quantity , which at the initial moment of time has the density with a maximum at and use the results of Sec.2.2. Due to the fact that the function must be even in , we cannot choose such as in Sec.3.3. Instead, we assume that , that is, the investor receives a penalty for choosing too large (or too small), formally . We emphasize that we change the problem for the sake of the ability to get an exact solution.

Let us make conclusions about the behavior of the maximum of , which which follow from the results of Sec.2.2.

-

•

If we assume that , then for large the maximum is close to a constant if and only if , that is . This constant is equal to . We associate this behavior with forming an opinion on the volatility of a risky asset. The solution reaches a constant, the faster, the greater the difference . If decreases, the value of tends to zero. This means that the maximum of tends to infinity, that is, the risky asset is perceived as more uncertain.

-

•

If and , then the opinion on volatility is formed under the condition . For large the maximum is close to a constant equal to .

-

•

If , then the position of the maximum of oscillates with a frequency that grows with .

At a qualitative level, the situation is identical to that described in Sec. 3.3.

4. Conclusion

We consider a simple application of the theory of mean field games to study the behavior of market agents managing a portfolio of securities which consist of risky and risk-free assets, based on a utility function that is common to all. We assume that the information on the market is incomplete, that is, agents are forced to independently decide on the parameters of the risky asset. When setting problems, we limit ourselves to the possibility of obtaining its analytical solution.

We deal with two separate situations. In the first one, agents know the exact value of volatility parameter, but decide on the correct value of the drift parameter. When agents manage their portfolio, they get a penalty for a false assumption of the ”true” value of the drift parameter. In the second case, on the contrary, the value of the drift parameter is known, however, agents receive a penalty for considering volatility too small. We study the question of whether, under the conditions described, the market formed an opinion about parameters of the asset, and if so, how far is it from the correct one.

The model that can be extended in different directions. In particular, it is natural to assume that agents have to choose three parameters at the same time: the drift and volatility of the asset, as well as risk attitude. Such problem can also be solved within the framework of the mean-field games theory, however, it is three-dimensional in space and does not allow an analytical solution. However, it can be investigated numerically.

References

- [1] Guéant O., Lasry J.M., Lions P.L., Mean Field Games and applications. Paris-Princeton lectures on mathematical finance, Springer, 2010, 205–266.

- [2] Lasry, J.-M., Lions, P.-L, Mean field games. Jpn. J. Math. 2 (1) 229–260, 2007.

- [3] Gomes, D. A., Saede, J., Mean Field Games Models-A Brief Survey// Dynamic Games and Applications, 4(2), 110–154, 2013.

- [4] Øksendal B., Stochastic differential equations. Introduction in theory and applications. Moscow: Mir, 2003.

- [5] Cardaliaguet, P., Notes on mean feld games from P.-L. Lions’ lectures at Collège de France, 2012

- [6] Guéant, O., A reference case for mean field games models// J. Math. Pures Appl. 92 (3), 276–294, 2009.

- [7] Merton R.C., Continuous Time Finance, Wiley-Blackwell, 1992.

- [8] Ingersoll, Jonathan E., Theory of Financial Decision Making. Totowa, NJ: Rowman and Littlefield, 1987.

- [9] Bielecki T., Pliska S., Sherris M., Risk sensitive asset allocation// Journal of Economic Dynamics and Control. 24. 1145–1177, 2000.