Hybrid Quantile estimation for asymmetric power GARCH models

Abstract

Asymmetric power GARCH models have been widely used to study the higher order moments of financial returns, while their quantile estimation has been rarely investigated. This paper introduces a simple monotonic transformation on its conditional quantile function to make the quantile regression tractable. The asymptotic normality of the resulting quantile estimators is established under either stationarity or non-stationarity. Moreover, based on the estimation procedure, new tests for strict stationarity and asymmetry

are also constructed. This is the first try of the quantile estimation for non-stationary ARCH-type models in the literature. The usefulness of the proposed methodology is illustrated by simulation results and real data analysis.

keywords:

JEL classification: C01, C22, C58

, , and

1 Introduction

Since the seminal work in Engle (1982) and Bollerslev (1986), the generalized autoregressive conditional heteroskedasticity (GARCH) model has been widely used to capture the volatility clustering of financial data; see, e.g., Francq and Zakoïan (2010) for an overview. Financial data are well known to exhibit conditional asymmetric features, in the sense that large negative returns tend to have more impact on future volatilities than large positive returns of the same magnitude. This stylized fact, which is known as the leverage effect, was first documented by Black (1976), and leads to many variants of the classical GARCH model (see, e.g., Higgins and Bera, 1992; Li and Li, 1996; Zhu et al., 2017). Among the existing asymmetric ARCH-type models, the first order asymmetric power-transformed GARCH (PGARCH) model proposed by Pan et al. (2008) is often used in applications, and it is defined by

| (1.1) |

where is a given positive constant exponent, , , , and is a sequence of independent and identically distributed (i.i.d.) random variables. Here, the notations and are used. Model (1.1) is motivated by the Box-Cox transformation, and it covers the classical GARCH model in Engle (1982) and Bollerslev (1986), the absolute value GARCH in Taylor (1986), the GJR model in Glosten et al. (1993), the threshold GARCH model in Rabemananjara and Zakoïan (1993), the PARCH model in Hwang and Kim (2004), and many others.

Following Hörmann (2008), model (1.1) is stationary if and only if the top Lyapunov exponent , where

| (1.2) |

By assuming follows a standard normal distribution, the Gaussian quasi-maximum likelihood estimator (QMLE) of model (1.1) was studied in Pan et al. (2008) and Hamadeh and Zakoïan (2011) for , and Francq and Zakoïan (2013a) for . Although the Gaussian QMLE has some desired asymptotic properties, it overlooks a crucial practical feature that the quantile structure of the financial data actually varies in shape across the quantile levels (Engle and Manganelli, 2004). Nowadays, the estimation of the conditional quantile becomes increasingly important for the financial data, since it is related to the quantile-based risk measures such as Value-at-Risk (VaR) and Expected Shortfall (ES), which are implemented worldwide in financial market regulation and banking supervision. However, only few attempts have been made to study the quantile estimation for model (1.1), especially when .

This paper contributes to the literature in two aspects. First, we extend the idea of Zheng et al. (2018) to construct a hybrid conditional quantile estimator of in model (1.1). To elaborate this idea, we let and , where is the given quantile level, , is the th quantile of , and is a given monotonic transformation function. Then, the th quantile of the transformed data conditional on is

| (1.3) |

and the th quantile of the original data conditional on is

| (1.4) |

where , is the -field generated by , and . The result (1.3) implies that is linear in terms of , and hence if is observable, can be easily estimated by the regression quantile estimation. With this quantile estimator of , then can be estimated via (1.3), leading to an estimator of according to (1.4). However, contains an unobservable , which has a recursive form, adding difficulty to the theoretical derivation and numerical optimization. To circumvent this difficulty, we replace by some initial estimators to calculate the quantile estimator of ; see also Xiao and Koenker (2009), So and Chung (2015) and Zheng et al. (2018). Indeed, Zheng et al. (2018) estimated based on the Gaussian QMLE, which needs in theory. To relieve the moment condition of , we estimate by using the generalized QMLE (GQMLE) in Francq and Zakoïan (2013b), and our theory only requires , where is a user-chosen positive number, indicating the estimation method used. Note that there is a vast literature on the estimation of conditional quantile for financial data, and two leading examples are the filtered historical simulation (FHS) method (Barone-Adesi et al., 1998; Barone-Adesi and Giannopoulos, 2001; Kuester et al., 2006) and the conditional auto-regressive VaR-method called “CAViaR” (Engle and Manganelli, 2004). As argued in Zheng et al. (2018), the hybrid conditional quantile estimation method combines the advantages of both FHS and CAViaR approaches, since it can exploit the ARCH-type structure in both the global estimation of the volatility and the local estimation of quantiles.

Second, we study the asymptotic properties of the quantile estimator of . Denote , where and . Under some regularity conditions, the quantile estimator of is shown to be asymptotically normal for either or , while the quantile estimator of is asymptotically normal only for . Our findings are similar to those in Jensen and Rahbek (2004a, b) and Francq and Zakoïan (2012, 2013a), and our asymptotic results for are the first try of the quantile estimation for non-stationary ARCH-type models in the literature. Compared to the Gaussian QMLE in Francq and Zakoïan (2013a), our quantile estimator takes the quantile structure of into account through the transformation function , and it could be a more appealing tool to investigate the quantile-based measures such as VaR and ES (Engle and Manganelli, 2004; Francq and Zakoïan, 2015). Moreover, our quantile estimator only requires for its asymptotics, and hence it is more appropriate to study the heavy-tailed financial data than the Gaussian QMLE, which requires for its asymptotic normality. As a by-product, new tests for strict stationarity and asymmetry of model (1.1) are derived from our estimation procedure.

The remaining of this paper is organized as follows. Section 2 introduces our hybrid conditional quantile estimation procedure. Section 3 studies the asymptotic properties of our proposed quantile estimator. The strict stationarity tests and the asymmetry tests are provided in Section 4. Simulation results are reported in Section 5. Applications are presented in Section 6. The conclusions are offered in Section 7. The proofs are given in the Appendix.

Throughout the paper, denotes the absolute value, denotes the vector -norm, denotes -norm for a random variable, is the transpose of matrix , denotes the convergence in probability, denotes the convergence in distribution, (or ) denotes a sequence of random numbers converging to zero ( or bounded) in probability, is a generic constant, , , is the indicator function, and is the sign of any .

2 The hybrid conditional quantile estimation

Let be the unknown parameter vector of model (1.1), and be its true value, where is the parameter space, and it is a compact subset of . Moreover, let , and be its true value, where . Assume that are observations generated from model (1.1). By (1.3), the parametric th quantile of the transformed data is

| (2.1) |

If are observable, we are able to estimate by the linear quantile regression. However, are not observable, and we shall replace them by some initial estimates. To accomplish this, we define recursively by

Then, . In practice, we calculate by , where

with given initial values and .

Based on (2.1) and (1.4), our hybrid conditional quantile estimation procedure for has the following three steps.

Step 1 (Estimation of the global model structure). Using the generalized quasi-maximum likelihood estimator (GQMLE) in Francq and Zakoïan (2013b) to estimate the parameter in model (1.1),

| (2.2) |

where is a user-chosen positive number. Based on , compute the initial estimates of as .

Step 2 (Quantile regression at a specific level). Perform the weighted linear quantile regression of on at quantile level ,

| (2.3) |

where . Based on , estimate the th conditional quantile of by .

Step 3 (Transforming back to ). Estimate the th conditional quantile of the original observation by .

For the GQMLE in Step 1, Francq and Zakoïan (2013b) established its asymptotic normality under some regularity conditions. The non-negative user-chosen number involved in indicates the estimation method used. Particularly, when , reduces to the Gaussian QMLE; and when , reduces to the Laplacian QMLE. So far, how to choose an “optimal” (under certain criterion) is unclear, and simulation studies in Section 5 suggest that we could choose a small (or large) value of when is heavy-tailed (or light-tailed).

For the quantile estimator in Step 2, Zheng et al. (2018) studied its asymptotics for a special case that and with (i.e., the stationary classical GARCH model) and (i.e., the Gaussian QMLE). In the present paper, we will study the asymptotic properties of for the general case.

3 Asymptotic properties of the hybrid quantile estimator

In this section, we study the asymptotic properties of the hybrid conditional quantile estimator. First, we give some technical assumptions as follows:

Assumption 3.1.

(i) is an interior point of ; (ii) the random variable can not concentrate on at most two values, the positive line or the negative line, and ; (iii) .

Assumption 3.2.

The density of is positive and differentiable almost everywhere on .

Assumption 3.3.

When tends to infinity,

Assumption 3.1(i)-(ii) used by Francq and Zakoïan (2013a) are usually assumed for ARCH-type models. Assumption 3.1(iii) is the identification condition for the GQMLE; see Francq and Zakoïan (2013b). If , we have

by (1.1) and Assumption 3.1(iii), meaning that we can directly predict the th moment of by . If , the th moment of has to be predicted by in this general case.

Assumption 3.2 is standard for quantile estimation. Assumption 3.3 is needed only for , and it is used to prove that when , as in (see Francq and Zakoïan, 2012 and 2013a).

Theorem 3.1.

(i) [Stationary case] When , and for all ,

| (3.1) |

where

(ii) [Explosive case] When , and ,

| (3.2) |

where

Remark 1.

Similar to the Gaussian QMLE in Jensen and Rahbek (2004a, b) and Francq and Zakoïan (2012, 2013a), is always asymptotically normal distributed regardless of the sign of , and is shown to be asymptotically normal distributed only for .

Our results in Theorem 3.1 are also related to those in Zheng et al. (2018), but with three major differences. First, the results in Theorem 1 of Zheng et al. (2018) are nested by ours with , and . Second, the results in Zheng et al. (2018) need the assumption , while our results hold under a weaker assumption , which is applicable to the heavy-tailed . Third, the results of Zheng et al. (2018) are only for the stationary GARCH model, but our results cover both stationary and non-stationary asymmetric PGARCH models, leading to a much larger applicability scope than theirs.

Remark 2.

To prove the result in (iii), a technical condition is needed, and it poses an additional restriction on the parameter . Clearly, the boundary point is related to the constant , the distribution of , and the value of . Table 1 reports the values of for several choices of , , and , where the value of is fixed to be 0.9, the value of is set to be , and the value of is uniquely determined by the condition . From this table, we can find that (i) the value of always lies in the region ; (ii) the values of do not vary too much across or the distribution of , although they become slightly smaller as the values of become larger. In sum, based on our calculations, the technical condition seems mild, and it should not hinder the practical application of our proposed estimation.

| 0.01 | 0.04 | 0.07 | 0.10 | 0.13 | 0.16 | 0.19 | 0.22 | 0.25 | ||

| Panel A: | ||||||||||

| 2 | 0.97366 | 0.98019 | 0.98380 | 0.98524 | 0.98497 | 0.98325 | 0.98023 | 0.97599 | 0.97066 | |

| 4 | 0.95886 | 0.96792 | 0.97274 | 0.97465 | 0.97429 | 0.97201 | 0.96797 | 0.96215 | 0.95448 | |

| 6 | 0.94949 | 0.95953 | 0.96467 | 0.96667 | 0.96630 | 0.96391 | 0.95958 | 0.95320 | 0.94441 | |

| 2 | 0.96867 | 0.97439 | 0.97750 | 0.97894 | 0.97913 | 0.97831 | 0.97662 | 0.97410 | 0.97075 | |

| 4 | 0.95403 | 0.96143 | 0.96531 | 0.96708 | 0.96732 | 0.96631 | 0.96421 | 0.96106 | 0.95677 | |

| 6 | 0.94528 | 0.95323 | 0.95727 | 0.95909 | 0.95934 | 0.95831 | 0.95614 | 0.95284 | 0.94826 | |

| 2 | 0.96093 | 0.96276 | 0.95718 | 0.96282 | 0.97221 | 0.98027 | 0.98736 | 0.99368 | 0.99940 | |

| 4 | 0.94825 | 0.95038 | 0.94380 | 0.94596 | 0.95183 | 0.95670 | 0.96087 | 0.96450 | 0.96772 | |

| 6 | 0.94116 | 0.94335 | 0.93651 | 0.93704 | 0.94125 | 0.94468 | 0.94756 | 0.95003 | 0.95219 | |

| Panel B: | ||||||||||

| 2 | 0.98360 | 0.98868 | 0.99209 | 0.99401 | 0.99459 | 0.99397 | 0.99224 | 0.98952 | 0.98587 | |

| 4 | 0.97119 | 0.97972 | 0.98545 | 0.98867 | 0.98964 | 0.98859 | 0.98570 | 0.98113 | 0.97501 | |

| 6 | 0.96174 | 0.97257 | 0.97982 | 0.98389 | 0.98512 | 0.98379 | 0.98013 | 0.97435 | 0.96659 | |

| 2 | 0.98177 | 0.98659 | 0.98993 | 0.99198 | 0.99290 | 0.99279 | 0.99176 | 0.98987 | 0.98720 | |

| 4 | 0.96894 | 0.97679 | 0.98217 | 0.98547 | 0.98694 | 0.98676 | 0.98511 | 0.98208 | 0.97776 | |

| 6 | 0.95955 | 0.96931 | 0.97597 | 0.98002 | 0.98182 | 0.98161 | 0.97958 | 0.97585 | 0.97052 | |

| 2 | 0.96174 | 0.97257 | 0.97982 | 0.98389 | 0.98512 | 0.98379 | 0.98013 | 0.97435 | 0.96659 | |

| 4 | 0.96629 | 0.97588 | 0.97941 | 0.97865 | 0.97438 | 0.96686 | 0.96342 | 0.96892 | 0.97385 | |

| 6 | 0.95788 | 0.96930 | 0.97347 | 0.97258 | 0.96753 | 0.95856 | 0.95315 | 0.95703 | 0.96043 | |

Remark 3.

Our results in Theorem 3.1 are derived for a known exponent . When is unknown in general, we can include as an additional unknown parameter in our first estimation procedure, and the asymptotics of the resulting GQMLE can be established with some minor modifications (see also Section 6 in Francq and Zakoïan (2013a)). However, since the unknown exponent is involved in the transformation function , how to derive the asymptotics of the corresponding quantile estimator in the second step estimation procedure is challenging at this stage, and we leave this interesting topic for the future study.

Based on , we can calculate , , , , , , and , which are the sample counterparts of , , , , , , and , respectively111For , we follow Silverman (1986) to estimate by the Gaussian kernel density estimator with and the rule-of-thumb bandwidth , where , and and are the sample standard deviation and interquartile range of the transformed residuals , respectively.. Since is a martingale difference sequence, by (3.3) we can estimate by

where with . Under the conditions of Theorem 3.1(i), we can show that is a consistent estimator of for .

Partition , , and

Then, , , , and are the sample counterparts of , , , and , respectively. Since is a martingale difference sequence, by (3.4) we can estimate by

where with . Under the conditions of Theorem 3.1(ii)-(iii), we can show that and for , which implies that we can estimate by for either or .

4 Strict stationarity and asymmetry tests

4.1 Testing for strict stationarity

Since the stationarity of model (1.1) is determined by the sign of , it is interesting to consider the strict stationarity testing problems as follows:

| (4.1) |

and

| (4.2) |

In Francq and Zakoïan (2013a), a strict stationarity test based on the Gaussian QMLE is proposed. In this subsection, similar to Francq and Zakoïan (2013a), we construct a strict stationarity test based on the GQMLE.

For any , let and

Then, we can estimate by . The following result shows the asymptotic distribution of in both stationary and nonstationary cases.

Corollary 4.1.

The proof of Corollary 4.1 is omitted, since it is similar to the one in Francq and Zakoïan (2013a) except for some minor modifications. Let . Under the conditions of Corollary 4.1, can be consistently estimated by , where is the sample variance of . Then, the statistic

asymptotically converges to when . For the testing problem (4.1) [or (4.2)], this leads us to consider the critical region

| (4.4) |

at the asymptotic significance level of .

4.2 Testing for asymmetry

Testing for the existence of asymmetry (or leverage) effect is important in many financial applications. For model (1.1), this asymmetry testing problem is of the form

| (4.5) |

In this subsection, we propose two tests for the hypotheses in (4.5). Let and with , where defined before is a consistent estimator of the asymptotic variance of , and

By Lemmas .1-.4 and the similar argument as for Theorem 3.2 in Francq and Zakoïan (2013a), we can show that is a consistent estimator of the asymptotic variance of . With and , our test statistics for asymmetry are defined by

Note that is based on the GQMLE, and it aims to examine the asymmetric effect in model (1.1) globally, while does this locally at a specific quantile level by using the quantile estimator. Under the conditions of Theorem 3.1, it is straightforward that both and asymptotically converge to under in (4.5). Hence, the critical region based on [or ] is

| (4.6) |

for the testing problem (4.5), and it has the asymptotic significance level . Since , , or has the unified asymptotics for both and , the tests and can be used in both cases. This is also the situation for the asymmetry test in Francq and Zakoïan (2013a). We shall emphasize that unlike the Gaussian QMLE-based tests in Francq and Zakoïan (2013a), our tests , and only require , and they thus are valid for the very heavy-tailed .

5 Simulation studies

5.1 Simulation studies for the quantile estimators

In this section, we assess the finite-sample performance of . We generate 1000 replications from the following model:

| (5.1) |

where is taken as , the standardized Student’s () or the standardized Student’s () such that . Here, we fix , and , and choose as in Table 2, where the values of correspond to the cases of , , and , respectively. For the power index (or the estimation indicator ), we choose it to be 2 or 1. For the quantile level , we set it to be or . Since each GQMLE has a different identification condition, has to be re-scaled for in model (5.1), and it is defined as

where is the hybrid quantile estimator calculated from the data sample, and the true value of is used.

| 0.05 | -0.0104 | 0.05 | -0.0152 | 0.05 | -0.0226 | 0.05 | -0.0233 | 0.05 | -0.0261 | 0.05 | -0.0286 | |||||

| 0.07224697 | 0.0000 | 0.09206513 | 0.0000 | 0.1516561 | 0.0000 | 0.1083685 | 0.0000 | 0.1332366 | 0.0000 | 0.1830638 | 0.0000 | |||||

| 0.2 | 0.0517 | 0.2 | 0.0330 | 0.2 | 0.0091 | 0.2 | 0.0337 | 0.2 | 0.0192 | 0.2 | 0.0034 | |||||

Tables 3 and 4 report the bias, the empirical standard deviation (ESD) and the asymptotic standard deviation (ASD) of for the cases of and , respectively. In this section, since the results for are similar, they are not reported here for saving space. From Tables 3 and 4, our findings are as follows:

| Panel A: | |||||||||||||||||||||||||||||||

| 1000 | Bias | -1.36 | -0.68 | -0.36 | 0.62 | -1.29 | -0.55 | -0.28 | 0.40 | -1.17 | -0.51 | -0.37 | 0.36 | -0.72 | -0.52 | -0.34 | 0.48 | -1.74 | -0.41 | -0.24 | 0.22 | -0.93 | -0.16 | -0.32 | 0.16 | ||||||

| ESD | 5.63 | 1.81 | 2.72 | 2.33 | 6.20 | 1.82 | 2.88 | 2.49 | 5.45 | 1.99 | 2.74 | 2.23 | 5.66 | 2.11 | 2.88 | 2.42 | 6.33 | 3.14 | 2.65 | 2.35 | 6.10 | 3.13 | 2.80 | 2.45 | |||||||

| ASD | 3.99 | 2.11 | 2.78 | 2.43 | 4.30 | 2.14 | 2.80 | 2.54 | 3.88 | 2.25 | 2.75 | 2.34 | 4.26 | 2.32 | 2.84 | 2.45 | 5.34 | 3.09 | 2.77 | 2.41 | 4.76 | 3.18 | 2.85 | 2.53 | |||||||

| 2000 | Bias | -1.08 | -0.37 | -0.12 | 0.29 | -1.35 | -0.24 | -0.14 | 0.25 | -1.32 | -0.24 | -0.13 | 0.14 | -0.66 | -0.21 | -0.05 | -0.15 | -1.65 | -0.22 | -0.11 | -0.07 | -1.41 | -0.09 | -0.10 | 0.03 | ||||||

| ESD | 4.76 | 1.31 | 2.01 | 1.69 | 5.33 | 1.35 | 2.08 | 1.81 | 5.96 | 1.48 | 1.95 | 1.63 | 4.94 | 1.55 | 1.98 | 1.67 | 6.01 | 2.27 | 2.01 | 1.70 | 6.47 | 2.20 | 2.01 | 1.69 | |||||||

| ASD | 3.97 | 1.56 | 2.02 | 1.76 | 4.24 | 1.55 | 2.04 | 1.83 | 4.55 | 1.67 | 2.03 | 1.70 | 4.40 | 1.65 | 1.99 | 1.72 | 5.05 | 2.27 | 2.02 | 1.73 | 5.21 | 2.28 | 2.04 | 1.79 | |||||||

| 1000 | Bias | -1.72 | -0.84 | -0.70 | 0.60 | -1.57 | -0.88 | -0.35 | 0.53 | -3.28 | -0.85 | -0.82 | 0.17 | -8.57 | -0.26 | -0.56 | 0.11 | -4.70 | -0.75 | -0.63 | 0.08 | -3.32 | -0.43 | -0.58 | 0.15 | ||||||

| ESD | 7.72 | 2.26 | 3.53 | 3.18 | 6.92 | 2.43 | 3.40 | 2.78 | 10.9 | 2.92 | 3.34 | 2.72 | 4.77 | 8.98 | 3.52 | 2.96 | 21.9 | 3.96 | 3.18 | 2.89 | 18.6 | 4.12 | 3.31 | 2.64 | |||||||

| ASD | 5.75 | 2.18 | 3.34 | 3.15 | 5.05 | 2.20 | 3.17 | 2.89 | 6.51 | 2.69 | 3.23 | 2.84 | 15.9 | 8.34 | 3.19 | 2.91 | 7.35 | 3.60 | 3.18 | 2.83 | 6.47 | 3.55 | 3.17 | 2.63 | |||||||

| 2000 | Bias | -1.35 | -0.46 | -0.33 | 0.39 | -1.71 | -0.40 | -0.18 | 0.35 | -3.12 | -0.57 | -0.35 | 0.12 | -1.99 | -0.39 | -0.19 | 0.15 | -5.37 | -0.56 | -0.44 | 0.07 | -3.24 | -0.35 | -0.29 | 0.04 | ||||||

| ESD | 6.03 | 1.51 | 2.40 | 2.27 | 5.79 | 1.64 | 2.37 | 2.05 | 13.2 | 2.05 | 2.27 | 1.96 | 10.7 | 2.06 | 2.28 | 1.81 | 28.1 | 2.81 | 2.51 | 2.03 | 13.8 | 2.83 | 2.36 | 1.82 | |||||||

| ASD | 5.56 | 1.59 | 2.36 | 2.29 | 4.75 | 1.59 | 2.34 | 2.11 | 6.11 | 1.97 | 2.35 | 2.02 | 5.19 | 1.95 | 2.36 | 1.89 | 7.54 | 2.70 | 2.35 | 2.04 | 6.74 | 2.70 | 2.39 | 1.93 | |||||||

| Panel B: | |||||||||||||||||||||||||||||||

| 1000 | Bias | -0.84 | -0.45 | -0.25 | 0.36 | -0.62 | -0.38 | -0.18 | 0.32 | -1.10 | -0.47 | -0.35 | 0.28 | -0.87 | -0.40 | -0.25 | 0.26 | -1.18 | -0.25 | -0.18 | 0.12 | -0.86 | -0.17 | -0.09 | -0.10 | ||||||

| ESD | 3.42 | 1.15 | 1.67 | 1.56 | 3.29 | 1.17 | 1.69 | 1.57 | 3.71 | 1.31 | 1.72 | 1.40 | 3.68 | 1.33 | 1.75 | 1.41 | 3.79 | 1.97 | 1.71 | 1.53 | 3.69 | 2.00 | 1.73 | 1.53 | |||||||

| ASD | 3.05 | 1.38 | 1.80 | 1.58 | 3.03 | 1.38 | 1.80 | 1.58 | 3.32 | 1.51 | 1.82 | 1.54 | 3.35 | 1.50 | 1.81 | 1.54 | 3.91 | 2.00 | 1.79 | 1.55 | 3.95 | 2.00 | 1.79 | 1.55 | |||||||

| 2000 | Bias | -0.85 | -0.25 | -0.16 | 0.28 | -0.64 | -0.21 | -0.11 | 0.25 | -0.87 | -0.16 | -0.14 | 0.09 | -0.62 | -0.12 | -0.10 | 0.07 | -1.34 | -0.14 | -0.08 | 0.07 | -0.97 | -0.11 | -0.04 | 0.06 | ||||||

| ESD | 3.10 | 0.87 | 1.27 | 1.08 | 3.04 | 0.87 | 1.27 | 1.07 | 3.36 | 0.95 | 1.30 | 1.05 | 3.19 | 0.95 | 1.30 | 1.06 | 3.96 | 1.39 | 1.21 | 1.09 | 3.86 | 1.41 | 1.22 | 1.11 | |||||||

| ASD | 2.83 | 0.10 | 1.30 | 1.13 | 2.83 | 0.99 | 1.30 | 1.13 | 3.05 | 1.06 | 1.29 | 1.08 | 3.04 | 1.06 | 1.29 | 1.08 | 3.94 | 1.42 | 1.28 | 1.10 | 3.94 | 1.42 | 1.28 | 1.10 | |||||||

| 1000 | Bias | -1.62 | -0.43 | -0.29 | 0.31 | -1.36 | -0.33 | -0.16 | 0.34 | -1.65 | -0.50 | -0.36 | 0.06 | -1.32 | -0.39 | -0.22 | 0.12 | -2.66 | -0.34 | -0.39 | -0.05 | -1.96 | -0.24 | -0.23 | 0.04 | ||||||

| ESD | 4.42 | 1.03 | 1.55 | 1.68 | 4.38 | 1.00 | 1.54 | 1.52 | 4.57 | 1.41 | 1.56 | 1.47 | 4.60 | 1.38 | 1.55 | 1.31 | 8.28 | 1.95 | 1.67 | 1.56 | 7.47 | 1.93 | 1.63 | 1.40 | |||||||

| ASD | 3.21 | 1.15 | 1.67 | 1.62 | 2.95 | 1.13 | 1.65 | 1.47 | 3.56 | 1.41 | 1.67 | 1.49 | 3.31 | 1.40 | 1.66 | 1.35 | 4.27 | 1.90 | 1.67 | 1.51 | 4.14 | 1.88 | 1.64 | 1.35 | |||||||

| 2000 | Bias | -1.09 | -0.23 | -0.20 | 0.19 | -0.85 | -0.18 | -0.11 | 0.19 | -1.72 | -0.19 | -0.17 | 0.05 | -1.20 | -0.12 | -0.21 | 0.06 | -2.86 | -0.22 | -0.19 | 0.03 | 2.13 | -0.03 | -0.11 | -0.01 | ||||||

| ESD | 3.05 | 0.75 | 1.23 | 1.19 | 3.02 | 0.79 | 1.26 | 1.05 | 6.24 | 0.98 | 1.17 | 1.07 | 4.19 | 0.94 | 1.19 | 0.98 | 8.59 | 1.35 | 1.14 | 1.06 | 7.76 | 1.33 | 1.19 | 0.10 | |||||||

| ASD | 2.94 | 0.82 | 1.22 | 1.20 | 2.70 | 0.82 | 1.21 | 1.09 | 3.70 | 0.10 | 1.21 | 1.07 | 3.29 | 0.99 | 1.21 | 0.96 | 4.25 | 1.37 | 1.20 | 1.08 | 4.39 | 1.35 | 1.20 | 0.97 | |||||||

| Panel A: | |||||||||||||||||||||||||||||||

| 1000 | Bias | -0.32 | -0.67 | -0.56 | 0.55 | -0.11 | -0.59 | -0.44 | 0.45 | -0.38 | -0.55 | -0.51 | 0.41 | -0.31 | -0.44 | -0.39 | 0.35 | -0.85 | -0.40 | -0.41 | 0.29 | -0.57 | -0.25 | -0.23 | 0.23 | ||||||

| ESD | 1.53 | 0.93 | 1.23 | 0.96 | 1.51 | 0.93 | 1.25 | 0.95 | 1.53 | 1.08 | 1.29 | 0.87 | 1.63 | 1.12 | 1.24 | 0.91 | 1.87 | 1.38 | 1.26 | 0.95 | 1.93 | 1.39 | 1.22 | 0.96 | |||||||

| ASD | 1.28 | 1.23 | 1.36 | 1.00 | 1.33 | 1.22 | 1.36 | 1.02 | 1.49 | 1.30 | 1.35 | 0.97 | 1.60 | 1.29 | 1.36 | 0.99 | 2.01 | 1.43 | 1.36 | 1.00 | 1.97 | 1.41 | 1.35 | 1.01 | |||||||

| 2000 | Bias | -0.46 | -0.40 | -0.32 | -0.39 | -0.28 | -0.39 | -0.29 | 0.34 | -0.45 | -0.26 | -0.21 | 0.21 | -0.37 | -0.20 | -0.19 | 0.16 | -0.75 | -0.20 | -0.20 | 0.16 | -0.50 | -0.12 | -0.16 | 0.14 | ||||||

| ESD | 1.76 | 0.69 | 0.91 | 0.78 | 1.65 | 0.74 | 0.94 | 0.79 | 1.52 | 0.84 | 0.89 | 0.64 | 1.66 | 0.82 | 0.93 | 0.68 | 1.94 | 1.04 | 0.93 | 0.69 | 1.76 | 1.02 | 0.93 | 0.72 | |||||||

| ASD | 1.28 | 0.88 | 0.98 | 0.76 | 1.29 | 0.88 | 0.98 | 0.77 | 1.51 | 0.93 | 0.97 | 0.70 | 1.50 | 0.93 | 0.97 | 0.71 | 1.82 | 1.02 | 0.97 | 0.71 | 1.84 | 1.01 | 0.97 | 0.72 | |||||||

| 1000 | Bias | -0.69 | -0.87 | -0.66 | 0.62 | -0.47 | -0.64 | -0.50 | 0.51 | -1.14 | -0.60 | -0.61 | 0.31 | -0.74 | -0.56 | -0.55 | 0.34 | -1.23 | -0.55 | -0.52 | 0.23 | -1.00 | -0.24 | -0.40 | 0.21 | ||||||

| ESD | 2.34 | 1.14 | 1.55 | 1.32 | 2.46 | 1.20 | 1.56 | 1.34 | 2.76 | 1.51 | 1.54 | 1.09 | 2.79 | 1.57 | 1.53 | 1.07 | 2.82 | 1.66 | 1.56 | 1.08 | 3.05 | 1.65 | 1.48 | 1.09 | |||||||

| ASD | 1.71 | 1.46 | 1.67 | 1.24 | 1.73 | 1.43 | 1.66 | 1.22 | 2.09 | 1.61 | 1.65 | 1.16 | 2.06 | 1.61 | 1.65 | 1.12 | 2.53 | 1.78 | 1.66 | 1.18 | 2.27 | 1.71 | 1.63 | 1.12 | |||||||

| 2000 | Bias | -0.81 | -0.49 | -0.38 | 0.48 | -0.61 | -0.40 | -0.29 | 0.42 | -0.97 | -0.28 | -0.34 | 0.16 | -0.83 | -0.22 | -0.24 | 0.17 | -1.37 | -0.23 | -0.27 | 0.12 | -0.88 | -0.23 | -0.26 | 0.14 | ||||||

| ESD | 2.24 | 0.84 | 1.14 | 1.11 | 2.25 | 0.86 | 1.14 | 1.03 | 2.42 | 1.09 | 1.14 | 0.82 | 2.79 | 1.13 | 1.19 | 0.77 | 2.85 | 1.21 | 1.11 | 0.82 | 2.85 | 1.25 | 1.16 | 0.81 | |||||||

| ASD | 1.70 | 1.04 | 1.20 | 0.97 | 1.68 | 1.04 | 1.19 | 0.94 | 2.17 | 1.16 | 1.19 | 0.84 | 2.10 | 1.16 | 1.19 | 0.80 | 2.64 | 1.26 | 1.19 | 0.84 | 2.25 | 1.26 | 1.19 | 0.81 | |||||||

| Panel B: | |||||||||||||||||||||||||||||||

| 1000 | Bias | -0.17 | -0.48 | -0.43 | 0.37 | -0.07 | -0.40 | -0.29 | 0.28 | -0.33 | -0.37 | -0.32 | 0.30 | -0.17 | 0.25 | -0.24 | 0.18 | -0.59 | -0.29 | -0.29 | 0.20 | -0.45 | -0.18 | -0.25 | 0.19 | ||||||

| ESD | 1.31 | 0.78 | 1.05 | 0.81 | 1.26 | 0.74 | 1.05 | 0.79 | 1.24 | 0.92 | 1.00 | 0.71 | 1.20 | 0.90 | 1.00 | 0.72 | 1.40 | 1.07 | 1.04 | 0.76 | 1.47 | 1.12 | 1.01 | 0.79 | |||||||

| ASD | 1.28 | 1.02 | 1.14 | 0.86 | 1.23 | 1.02 | 1.13 | 0.85 | 1.44 | 1.07 | 1.13 | 0.81 | 1.42 | 1.08 | 1.13 | 0.82 | 1.82 | 1.19 | 1.13 | 0.83 | 1.77 | 1.18 | 1.13 | 0.83 | |||||||

| 2000 | Bias | -0.26 | -0.26 | -0.21 | 0.24 | -0.11 | -0.22 | -0.21 | 0.17 | -0.40 | -0.20 | -0.22 | 0.16 | -0.33 | -0.14 | -0.11 | 0.11 | -0.58 | -0.12 | -0.11 | 0.08 | -0.41 | -0.09 | -0.07 | 0.06 | ||||||

| ESD | 1.30 | 0.57 | 0.76 | 0.63 | 1.19 | 0.57 | 0.78 | 0.62 | 1.27 | 0.69 | 0.74 | 0.53 | 1.27 | 0.70 | 0.72 | 0.54 | 1.43 | 0.82 | 0.76 | 0.57 | 1.43 | 0.81 | 0.76 | 0.57 | |||||||

| ASD | 1.25 | 0.73 | 0.81 | 0.65 | 1.22 | 0.73 | 0.81 | 0.65 | 1.52 | 0.77 | 0.81 | 0.58 | 1.43 | 0.77 | 0.80 | 0.58 | 1.83 | 0.84 | 0.81 | 0.59 | 1.74 | 0.84 | 0.81 | 0.59 | |||||||

| 1000 | Bias | -0.44 | -0.49 | -0.46 | 0.36 | -0.21 | -0.42 | -0.30 | 0.31 | -0.57 | -0.41 | -0.41 | 0.24 | -0.51 | -0.27 | -0.30 | 0.19 | -0.87 | -0.35 | -0.38 | 0.16 | -0.72 | -0.19 | -0.27 | 0.13 | ||||||

| ESD | 1.59 | 0.78 | 1.09 | 0.96 | 1.40 | 0.81 | 1.07 | 0.86 | 1.61 | 1.03 | 1.09 | 0.80 | 1.62 | 1.01 | 1.06 | 0.72 | 1.81 | 1.15 | 1.07 | 0.80 | 2.18 | 1.17 | 1.08 | 0.76 | |||||||

| ASD | 1.43 | 1.02 | 1.18 | 0.92 | 1.34 | 1.01 | 1.17 | 0.86 | 1.66 | 1.14 | 1.16 | 0.83 | 1.63 | 1.12 | 1.16 | 0.78 | 2.03 | 1.23 | 1.17 | 0.84 | 1.86 | 1.22 | 1.16 | 0.79 | |||||||

| 2000 | Bias | -0.43 | -0.24 | -0.20 | 0.23 | -0.33 | -0.27 | -0.21 | 0.23 | -0.63 | -0.17 | -0.20 | 0.08 | -0.48 | -0.16 | -0.15 | 0.10 | -0.79 | -0.19 | -0.17 | 0.07 | -0.52 | -0.13 | -0.11 | 0.07 | ||||||

| ESD | 1.45 | 0.57 | 0.81 | 0.75 | 1.48 | 0.63 | 0.84 | 0.72 | 1.67 | 0.75 | 0.82 | 0.58 | 1.53 | 0.79 | 0.79 | 0.53 | 1.69 | 0.88 | 0.75 | 0.60 | 1.65 | 0.83 | 0.81 | 0.53 | |||||||

| ASD | 1.43 | 0.73 | 0.84 | 0.74 | 1.30 | 0.73 | 0.83 | 0.68 | 1.64 | 0.81 | 0.83 | 0.59 | 1.61 | 0.81 | 0.83 | 0.56 | 1.96 | 0.88 | 0.83 | 0.60 | 1.81 | 0.88 | 0.83 | 0.56 | |||||||

(a1) The biases of all parameters become small as the sample size increases, except when , the estimators of have relatively large biases as expected. For each distribution of , the biases of with (or ) are generally smaller than those of with (or ). For each estimator, its biases (in absolute value) in the case of tend to be smaller than those in the case of .

(a2) The ESDs and ASDs of the parameter are close in all cases, while the ESDs and ASDs of the parameter have a relatively large disparity as expected. As the sample size increases, the ESDs and ASDs of all parameters become small. For each distribution of , the ASDs of seem robust to the choices of , and they become large as the value of decreases. For each estimator, its ASDs in the case of are generally larger than those in the case of , except for and .

Note that all of the aforementioned findings are invariant, regardless of the power index and the sign of . In summary, our quantile estimator has a good finite sample performance, which is robust to the choice of . Particulary, its performance tends to be even better, when is more light-tailed or the value of is larger.

5.2 Simulation studies for the tests

In this subsection, we first assess the performance of the strict stationarity test . We generate 1000 replications from model (5.1) with the same settings for and , except that the values of are chosen as in Table 5. We apply with and to both testing problems (4.1) and (4.2) at the significance level of 5%, and obtain the following findings:

(b1) The size of is controlled by the level of 5% in general, though there is some over-sized risk for the testing problem (4.2) when the sample size is not large enough. This is also observed in Francq and Zakoïan (2012, 2013a).

(b2) The power of is satisfactory, and it increases with the sample size . Also, is more powerful when the tail of is thinner. But the choice of has a negligible effect on the power of . This may be because the asymptotic variance of in (4.3) does not depend on .

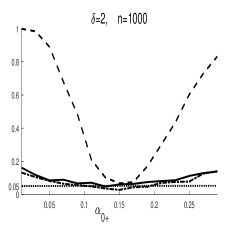

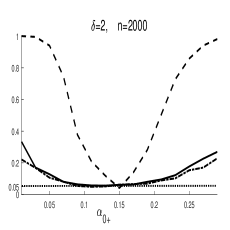

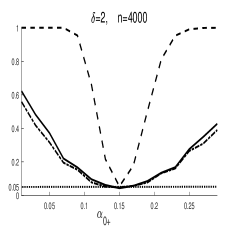

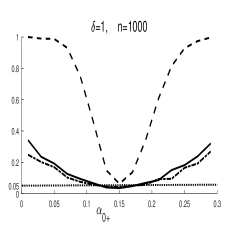

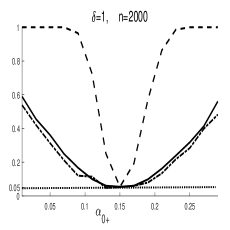

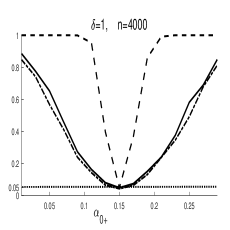

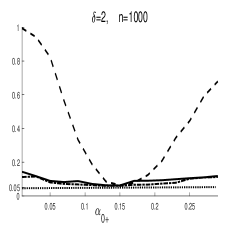

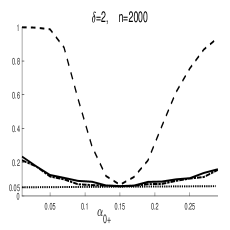

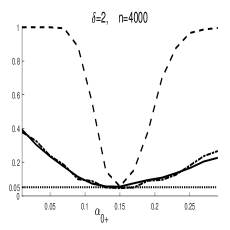

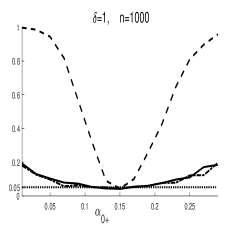

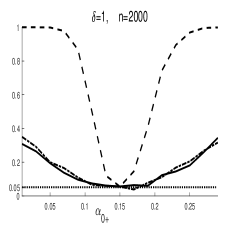

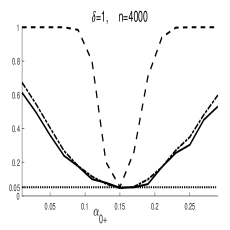

Next, we assess the performance of asymmetry tests and . As before, we generate 1000 replications from model (5.1) with the same settings for and , except that the values of are chosen to be . We apply and (with and ) to the testing problem (4.5) at the significance level of 5%. Figs. 1 and 2 plot the power of and for with and , respectively. Since the results for are similar, we do not show them here for saving the space. Our findings are as follows:

(c1) All three tests have precise sizes even when is not large.

(c2) The power of all three tests increases when the value of moves away from , and the global test is more powerful than the two local tests . Both local tests are more powerful for than for . When , with is more powerful than with , while when , the opposite conclusion is obtained.

Overall, all our proposed tests have a good performance especially for large .

| Panel A: | |||||||||||

| 0.01 | 0.03 | 0.05 | 0.07224697 | 0.09 | 0.11 | 0.13 | |||||

| 2 | 1000 | 0.0 | 0.0 | 0.0 | 7.6 | 53.7 | 96.8 | 99.8 | |||

| 2000 | 0.0 | 0.0 | 0.0 | 6.3 | 80.4 | 100 | 100 | ||||

| 4000 | 0.0 | 0.0 | 0.0 | 5.8 | 97.3 | 100 | 100 | ||||

| 1 | 1000 | 0.0 | 0.0 | 0.0 | 6.4 | 54.0 | 96.2 | 100 | |||

| 2000 | 0.0 | 0.0 | 0.0 | 5.4 | 79.3 | 100 | 100 | ||||

| 4000 | 0.0 | 0.0 | 0.0 | 5.0 | 96.9 | 100 | 100 | ||||

| 2 | 1000 | 100 | 99.3 | 78.1 | 14.1 | 0.6 | 0.0 | 0.6 | |||

| 2000 | 100 | 100 | 93.7 | 11.5 | 9.4 | 0.0 | 0.0 | ||||

| 4000 | 100 | 100 | 99.8 | 10.2 | 0.0 | 0.0 | 0.0 | ||||

| 1 | 1000 | 100 | 98.5 | 77.3 | 16.7 | 0.5 | 0.0 | 0.0 | |||

| 2000 | 100 | 100 | 93.7 | 13.8 | 0.0 | 0.0 | 0.0 | ||||

| 4000 | 100 | 100 | 99.6 | 8.4 | 0.0 | 0.0 | 0.0 | ||||

| 0.03 | 0.05 | 0.07 | 0.09206513 | 0.11 | 0.13 | 0.15 | |||||

| 2 | 1000 | 0.0 | 0.0 | 0.5 | 6.3 | 35.0 | 76.9 | 96.3 | |||

| 2000 | 0.0 | 0.0 | 0.0 | 5.6 | 52.9 | 95.1 | 99.9 | ||||

| 4000 | 0.0 | 0.0 | 0.0 | 5.3 | 78.2 | 99.0 | 100 | ||||

| 1 | 1000 | 0.0 | 0.0 | 0.1 | 6.3 | 34.6 | 74.5 | 95.4 | |||

| 2000 | 0.0 | 0.0 | 0.0 | 5.8 | 54.8 | 95.3 | 100 | ||||

| 4000 | 0.0 | 0.0 | 0.0 | 5.1 | 73.5 | 99.8 | 100 | ||||

| 2 | 1000 | 98.8 | 90.7 | 58.5 | 17.9 | 3.6 | 0.5 | 0.0 | |||

| 2000 | 100 | 98.3 | 75.4 | 13.7 | 0.8 | 0.0 | 0.0 | ||||

| 4000 | 100 | 100 | 92.3 | 12.7 | 0.1 | 0.0 | 0.0 | ||||

| 1 | 1000 | 99.6 | 99.3 | 60.9 | 16.7 | 1.9 | 0.1 | 0.0 | |||

| 2000 | 100 | 99.5 | 79.1 | 13.9 | 0.4 | 0.0 | 0.0 | ||||

| 4000 | 100 | 99.9 | 94.3 | 10.0 | 0.0 | 0.0 | 0.0 | ||||

| Panel B: | |||||||||||

| 0.05 | 0.07 | 0.09 | 0.1083685 | 0.13 | 0.15 | 0.17 | |||||

| 2 | 1000 | 0.0 | 0.0 | 0.0 | 6.8 | 94.1 | 100 | 100 | |||

| 2000 | 0.0 | 0.0 | 0.0 | 5.5 | 99.6 | 100 | 100 | ||||

| 4000 | 0.0 | 0.0 | 0.0 | 4.8 | 100 | 100 | 100 | ||||

| 1 | 1000 | 0.0 | 0.0 | 0.0 | 7.2 | 93.8 | 100 | 100 | |||

| 2000 | 0.0 | 0.0 | 0.0 | 5.8 | 99.8 | 100 | 100 | ||||

| 4000 | 0.0 | 0.0 | 0.0 | 5.1 | 100 | 100 | 100 | ||||

| 2 | 1000 | 100 | 99.9 | 89.5 | 10.8 | 0.1 | 0.0 | 0.0 | |||

| 2000 | 100 | 100 | 99.0 | 9.9 | 0.0 | 0.0 | 0.0 | ||||

| 4000 | 100 | 100 | 100 | 7.7 | 0.0 | 0.0 | 0.0 | ||||

| 1 | 1000 | 100 | 100 | 90.5 | 11.9 | 0.0 | 0.0 | 0.0 | |||

| 2000 | 100 | 100 | 99.2 | 10.2 | 0.0 | 0.0 | 0.0 | ||||

| 4000 | 100 | 100 | 100 | 7.9 | 0.0 | 0.0 | 0.0 | ||||

| 0.07 | 0.09 | 0.11 | 0.1332366 | 0.15 | 0.17 | 0.19 | |||||

| 2 | 1000 | 0.0 | 0.0 | 0.0 | 8.3 | 62.9 | 98.6 | 100 | |||

| 2000 | 0.0 | 0.0 | 0.0 | 7.4 | 84.4 | 100 | 100 | ||||

| 4000 | 0.0 | 0.0 | 0.0 | 5.6 | 99.0 | 100 | 100 | ||||

| 1 | 1000 | 0.0 | 0.0 | 0.0 | 7.4 | 63.5 | 98.8 | 100 | |||

| 2000 | 0.0 | 0.0 | 0.0 | 6.3 | 86.8 | 100 | 100 | ||||

| 4000 | 0.0 | 0.0 | 0.0 | 4.5 | 99.2 | 100 | 100 | ||||

| 2 | 1000 | 99.9 | 99.5 | 83.9 | 12.6 | 0.4 | 0.0 | 0.0 | |||

| 2000 | 100 | 100 | 97.9 | 11.1 | 0.0 | 0.0 | 0.0 | ||||

| 4000 | 100 | 100 | 100 | 10.1 | 0.0 | 0.0 | 0.0 | ||||

| 1 | 1000 | 100 | 99.7 | 88.0 | 14.9 | 0.4 | 0.0 | 0.0 | |||

| 2000 | 100 | 100 | 98.7 | 11.8 | 0.0 | 0.0 | 0.0 | ||||

| 4000 | 100 | 100 | 99.9 | 9.0 | 0.0 | 0.0 | 0.0 | ||||

-

•

The size of is in boldface.

6 Applications

6.1 Stationary data

In this subsection, we re-analyze the daily log returns of two stock market indexes: the S&P 500 index and the Dow 30 index in Zheng et al. (2018). The data are observed on a daily basis from January 2, 2008 to June 30, 2016, with a sample size . Zheng et al. (2018) studied these two datasets by using the classical GARCH() model, whose conditional quantile was estimated by the hybrid quantile estimator with the Guassian QMLE as its first step estimator. They found that the resulting method can produce better interval forecast than many existing ones. Since their GARCH() model overlooks the often observed asymmetry effect in financial data, it is of interest to re-fit these two sequences by model (1.1).

Based on model (1.1) with and , Table 6 gives the estimation results for both sequences. Here, we use the GQMLE with and in the first step estimation, and we consider the hybrid quantile estimators with and in the second step estimation. From this table, the estimates of are always much smaller than those of in magnitude, indicating that there is a strong asymmetric effect for both sequences. To look for more evidence, we apply the asymmetry tests and to both sequences, and their corresponding p-values given in Table 6 confirm the asymmetric phenomenon. We also consider the strict stationarity test for the testing problem (4.2) in Table 6, and its p-values show strong evidence that both time series are strictly stationary.

Next, we calculate the interval forecast of each sequence by the following expanding window procedure: first conduct the estimation using the data from January 2, 2008 to December 31, 2010 and compute the conditional quantile forecast for the next trading day, i.e., the forecast of ; then, advance the forecasting origin by one to include one more observation in the estimation subsample, and repeat the foregoing procedure until the end of the sample is reached.

| Panel A: S&P 500 | |||||||

| 4e-6 (9e-7) | 2e-6 (4e-7) | 7e-4 (1e-4) | 3e-4 (5e-5) | ||||

| 1e-7 (0.021) | 4e-6 (0.011) | 7e-6 (0.035) | 1e-4 (0.017) | ||||

| 0.261 (0.036) | 0.156 (0.018) | 0.302 (0.043) | 0.205 (0.019) | ||||

| 0.848 (0.025) | 0.850 (0.018) | 0.835 (0.031) | 0.862 (0.018) | ||||

| -1e-5 (2e-5) | -1e-5 (2e-5) | -1e-3 (1e-3) | -9e-4 (1e-3) | ||||

| -4e-7 (0.214) | -2e-5 (0.182) | -1e-5 (0.111) | -4e-4 (0.113) | ||||

| -0.812 (0.357) | -0.872 (0.308) | -0.517 (0.111) | -0.476 (0.113) | ||||

| -2.641 (0.004) | -4.689 (0.003) | -1.428 (0.172) | -2.002 (0.230) | ||||

| -6e-6 (7e-6) | -5e-6 (8e-6) | -8e-4 (9e-4) | 0.001 (9e-4) | ||||

| -2e-7 (0.089) | -1e-5 (0.098) | -9e-6 (0.086) | -0.002 (0.082) | ||||

| -0.431 (0.143) | -0.456 (0.160) | -0.388 (0.093) | -0.175 (0.088) | ||||

| -1.403 (0.002) | -2.454 (0.002) | -1.072 (0.130) | -1.486 (0.154) | ||||

| 1e-21 | 8e-14 | 7e-83 | 3e-51 | ||||

| 1e-13 | 1e-10 | 6e-15 | 7e-13 | ||||

| 0.023 | 0.006 | 5e-6 | 4e-5 | ||||

| 0.004 | 0.006 | 2e-5 | 0.030 | ||||

| Panel B: Dow 30 | |||||||

| 3e-6 (7e-7) | 2e-6 (3e-7) | 6e-4 (1e-4) | 3e-4 (5e-5) | ||||

| 4e-10 (0.019) | 1e-8 (0.010) | 2e-5 (0.029) | 1e-5 (0.016) | ||||

| 0.258 (0.035) | 0.160 (0.018) | 0.203 (0.037) | 0.205(0.019) | ||||

| 0.852 (0.021) | 0.852 (0.018) | 0.839 (0.027) | 0.863 (0.017) | ||||

| -1e-5 (9e-6) | -8e-6 (9e-6) | -1e-3 (0.001) | -9e-4 (1e-3) | ||||

| -1e-9 (0.156) | -5e-8 (0.158) | -4e-5 (0.114) | -2e-4 (0.122) | ||||

| -0.784 (0.232) | -0.862 (0.218) | -0.501 (0.114) | -0.474 (0.119) | ||||

| -2.590 (0.002) | -4.599 (0.002) | -1.447 (0.172) | -2.015 (0.230) | ||||

| -5e-6 (6e-6) | -4e-6 (6e-6) | -8e-4 (9e-4) | -9e-4 (8e-4) | ||||

| -7e-10 (0.095) | -3e-8 (0.099) | -3e-5 (0.090) | -5e-3 (0.088) | ||||

| -0.427 (0.154) | -0.462 (0.166) | -0.377 (0.098) | -0.141 (0.095) | ||||

| -1.411 (0.002) | -2.465 (0.002) | -1.087 (0.133) | -1.504 (0.159) | ||||

| 5e-20 | 8e-14 | 1e-83 | 2e-51 | ||||

| 1e-15 | 2e-10 | 5e-15 | 7e-13 | ||||

| 0.002 | 5e-4 | 7e-6 | 8e-5 | ||||

| 0.008 | 0.007 | 1e-4 | 0.087 | ||||

-

•

Note that and .

The standard deviations of all estimators are given in parentheses, and the p-values of all tests are given.

Moreover, we evaluate the forecasting performance of the aforementioned interval forecasts by using the following two measures:

(i) the minimum of the p-values of the two VaR backtests, the likelihood ratio test for correct conditional converge (CC) in Christoffersen (1998) and the dynamic quantile (DQ) test222As in Zheng et al. (2008), the regression matrix contains four lagged hits and the contemporaneous VaR estimate for DQ test. in Engle and Manganelli (2004);

(ii) the empirical coverage error is defined as the proportion of observations that exceed the corresponding VaR forecast minus the corresponding nominal level .

The reason for selecting the smaller of the two p-values is that the CC and DQ tests have different null hypotheses and hence are complementary to each other. Note that a larger p-value of either CC or DQ test gives a stronger evidence of good interval forecasts.

| Minimum p-value of VaR backtests | Empirical coverage error | |||||||||||||||

| S&P 500 | L1.0 | 0.000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | -0.0002 | -0.0069 | -0.0069 | -0.0088 | -0.0076 | |||||

| L2.5 | 0.001 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | -0.0048 | -0.0226 | -0.0195 | -0.0183 | -0.0183 | ||||||

| L5.0 | 0.017 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | -0.0090 | -0.0427 | -0.0378 | -0.0323 | -0.0255 | ||||||

| U5.0 | 0.245 | 0.6996 | 0.6304 | 0.4846 | 0.2401 | 0.0054 | 0.0041 | 0.0023 | 0.0047 | 0.0011 | ||||||

| U2.5 | 0.356 | 0.7142 | 0.7616 | 0.1476 | 0.2807 | 0.0030 | 0.0030 | 0.0011 | 0.0060 | 0.0048 | ||||||

| U1.0 | 0.275 | 0.8504 | 0.2956 | 0.8213 | 0.6206 | 0.0008 | 0.0002 | -0.0028 | 0.0008 | 0.0020 | ||||||

| Dow 30 | L1.0 | 0.063 | 0.0000 | 0.0000 | 0.000 | 0.0000 | -0.0014 | -0.0076 | -0.0027 | -0.0088 | -0.0076 | |||||

| L2.5 | 0.000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | -0.0054 | -0.0249 | -0.0201 | -0.0213 | -0.213 | ||||||

| L5.0 | 0.000 | 0.0000 | 0.0000 | 0.000 | 0.0000 | -0.0072 | -0.0433 | -0.0420 | -0.0329 | -0.0286 | ||||||

| U5.0 | 0.273 | 0.1678 | 0.2304 | 0.1842 | 0.2798 | 0.0084 | 0.0072 | 0.0035 | 0.0060 | 0.0023 | ||||||

| U2.5 | 0.568 | 0.3493 | 0.3723 | 0.6350 | 0.3723 | 0.0011 | 0.0024 | 0.0005 | 0.0011 | 0.0001 | ||||||

| U1.0 | 0.418 | 0.8256 | 0.8256 | 0.1296 | 0.0002 | -0.0028 | -0.0004 | -0.0004 | 0.0045 | 0.0020 | ||||||

-

•

Among the models with p-values , the largest p-value and the smallest empirical coverage error (in absolute value) are in boldface.

Based on model (1.1) with and 1, Table 7 reports the results of two measures at the lower (L) (or upper(U)) 0.01th, 0.025th and 0.05th conditional quantiles. Here, the GQMLE with and is used in the first step estimation. As a comparison, the results for the benchmark method (i.e., and ) in Zheng et al. (2018) are also included in Table 7. It can be seen that all methods have a poor performance for the lower conditional quantiles, while our proposed methods, based on the asymmetric model (1.1) together with the hybrid quantile estimation, have a significantly better interval forecasting performance for the upper conditional quantiles than the benchmark method in Zheng et al. (2018). The poor performance of the lower conditional quantiles from our method may be because our GQMLE does not account for the asymmetry of . We may expect to improve our forecasting performance particularly for the lower conditional quantiles by using a skewed distribution of to form our first estimation, and we leave this desired direction for future study. In terms of the minimum of the p-values of the two VaR backtests, our proposed methods with are better than those with in four out of six cases333Only consider the cases that the minimum of the p-values of two backtests is larger than 5%, while the choice of seems irrelevant to the forecasting performance. In terms of the empirical coverage error, our proposed methods with (or ) are better than those with (or ) in general. Overall, our method with , and has the best interval forecasting performance for both data.

6.2 Non-stationary data

In this subsection, we re-visit three daily stock return data sequences of Community Bankers Trust (BTC), China MediaExpress (CCME) and Monarch Community Bancorp (MCBF) in Francq and Zakoïan (2012, 2013a). These three sequences are shown to be non-stationary in Francq and Zakoïan (2012), while their conditional quantile estimators have not been investigated. Motivated by this, we study their conditional quantiles by our hybrid quantile estimation method. To compute our hybrid quantile estimator, we choose the GQMLE with in the first estimation step. Here, we do not consider the GQMLE with , since Li et al. (2018) demonstrated the innovations of the fitted GARCH() model for each sequence only have a finite second moment but not an infinite fourth moment. In the second step of quantile estimation, we consider the hybrid quantile estimators at levels and . Table 8 reports the results of and for each sequence, together with the results of for the testing problem (4.2). From the results of , we can reach the same conclusion as in Francq and Zakoïan (2012) that all three data are non-stationary, and hence the estimates for the drift term or may not be consistent. Meanwhile, Table 8 reports the results of , and for the testing problem (4.5). It is interesting to observe that the global asymmetry test as the one in Francq and Zakoïan (2013a) indicates that all three datasets do not have the asymmetric effect, while the local asymmetry tests and detect some strong asymmetric effects in model (1.1) with or for the CCME and MCBF data. Although none of the considered tests can find the asymmetric evidence for the BTC data, we think the examined BTC data still have the asymmetric effect, since our forecasting comparison below indicates that the asymmetric PGARCH model can perform better than its symmetric counterpart.

| Panel A: BTC | Panel B: CCME | Panel C: MCBF | |||||||||

| 8e-7 (7e-8) | 1e-4 (1e-4) | 2e-8 (2e-8) | 1e-4 (2e-5) | 8e-6 (4e-6) | 8e-4 (3e-4) | ||||||

| 0.089 (0.035) | 0.130 (0.040) | 0.107 (0.047) | 0.148 (0.048) | 0.033 (0.016) | 0.078 (0.003) | ||||||

| 0.119 (0.038) | 0.172 (0.041) | 0.125 (0.063) | 0.161 (0.056) | 0.029 (0.014) | 0.078 (0.028) | ||||||

| 0.840 (0.031) | 0.854 (0.027) | 0.838 (0.043) | 0.860 (0.033) | 0.931 (0.019) | 0.902 (0.024) | ||||||

| -5e-7 (1e-6) | -9e-4 (4e-4) | -1e-9 (6e-7) | -1e-7 (3e-4) | -2e-7 (1e-4) | -9e-4 (0.005) | ||||||

| -0.448 (0.229) | -0.320 (0.211) | -0.639 (0.421) | -0.498 (0.295) | -1.515 (0.221) | -0.479 (0.346) | ||||||

| -0.661 (0.215) | -0.423 (0.182) | -1.879 (0.504) | -0.846 (0.298) | -1e-4 (0.086) | -0.009 (0.144) | ||||||

| -4.660 (1e-4) | -2.097 (0.060) | -3.190 (1e-4) | -1.772 (0.032) | -4.625 (0.009) | -2.037 (0.263) | ||||||

| -8e-8 (7e-7) | -2e-7 (3e-4) | -4e-13 (2e-7) | -3e-8 (2e-4) | -1e-8 (9e-5) | -1e-4 (0.003) | ||||||

| -0.348 (0.211) | -0.153 (0.140) | -0.364 (0.268) | -0.404 (0.191) | -0.596 (0.229) | -0.314 (0.173) | ||||||

| -0.198 (0.178) | -0.113 (0.106) | -0.741 (0.267) | -0.792 (0.182) | -2e-5 (0.088) | 0.005 (0.095) | ||||||

| -2.232 (1e-4) | -1.522 (0.004) | -1.450 (1e-4) | -0.948 (0.021) | -2.438 (0.008) | -1.534 (0.151) | ||||||

| 0.397 | 0.966 | 0.145 | 0.577 | 0.894 | 0.143 | ||||||

| 0.222 | 0.208 | 0.409 | 0.424 | 0.429 | 0.499 | ||||||

| 0.257 | 0.359 | 0.032 | 0.210 | 1e-4 | 0.063 | ||||||

| 0.298 | 0.411 | 0.164 | 0.076 | 0.008 | 0.035 | ||||||

-

•

Note that , and .

The standard deviations of all estimators are given in parentheses, and the p-values of all tests are given.

| Minimum p-value of VaR backtests | Empirical coverage error | |||||||||||

| BTC | L1.0 | 0.0025 | 0.3999 | 0.9329 | -0.0100 | -0.0056 | -0.0012 | |||||

| L2.5 | 0.0000 | 0.0025 | 0.3335 | -0.0250 | -0.0206 | -0.0096 | ||||||

| L5.0 | 0.0000 | 0.0000 | 0.0031 | -0.0302 | -0.0478 | -0.0302 | ||||||

| U5.0 | 0.0299 | 0.1265 | 0.0182 | 0.0500 | 0.0170 | 0.0192 | ||||||

| U2.5 | 0.0003 | 0.6372 | 0.0877 | 0.0228 | 0.0052 | 0.0008 | ||||||

| U1.0 | 0.1296 | 0.8130 | 0.2569 | 0.0038 | -0.0010 | -0.0032 | ||||||

| CCME | L1.0 | 0.0301 | 0.9574 | 0.9574 | -0.0100 | -0.0015 | -0.0015 | |||||

| L2.5 | 0.0006 | 0.0001 | 0.0000 | -0.0250 | -0.0165 | -0.0165 | ||||||

| L5.0 | 0.0000 | 0.0000 | 0.0000 | -0.0500 | -0.0415 | -0.0415 | ||||||

| U5.0 | 0.0002 | 0.0000 | 0.0080 | 0.0457 | 0.0457 | 0.0372 | ||||||

| U2.5 | 0.0433 | 0.0006 | 0.0006 | 0.0207 | 0.0250 | 0.0250 | ||||||

| U1.0 | 0.6077 | 0.6077 | 0.0301 | 0.0057 | 0.0057 | 0.0100 | ||||||

| MCBF | L1.0 | 0.0031 | 0.0031 | 0.0031 | -0.0100 | -0.0100 | -0.0100 | |||||

| L2.5 | 0.0038 | 0.2131 | 0.4400 | -0.0204 | -0.0112 | 0.0050 | ||||||

| L5.0 | 0.0023 | 0.1220 | 0.1682 | -0.0316 | -0.0177 | -0.0131 | ||||||

| U5.0 | 0.0067 | 0.0023 | 0.0001 | 0.0200 | 0.0316 | -0.0030 | ||||||

| U2.5 | 0.0005 | 0.7622 | 0.0001 | 0.0227 | 0.0020 | -0.0188 | ||||||

| U1.0 | 0.0031 | 0.0000 | 0.7747 | 0.0100 | 0.0008 | 0.0031 | ||||||

-

•

Among the models with p-values , the largest p-value and the smallest empirical coverage error (in absolute value) are in boldface.

Next, we compute the interval forecasts for each sequence by using the same procedure as in Subsection 6.1, except that the first interval forecast is calculated based on the first half of sample. Again, we follow the measurements as in Subsection 6.1 to evaluate the interval forecasting performance of our methods, based on model (1.1) with the hybrid quantile estimators. Table 9 reports the corresponding results for all three datasets. As a comparison, the forecasting performance of the benchmark GARCH() model (i.e., and ) estimated by the Laplacian QMLE is also given in Table 9. It can be seen that, in terms of minimum p-values of two VaR backtests, model (1.1) with (or and ) can provide us with a good interval forecast in 6 cases, while the benchmark GARCH() model can only do this in one case. Similar conclusions can be obtained in terms of empirical coverage error. Particularly, our forecasting results indicate that the BTC data have the asymmetric effect, which, however, has not been detected by our considered tests in Table 8. Note that there are 7 cases (most of them are for the CCME data) in which none of the methods can deliver a satisfactory interval forecast, and these cases may require some new methods for their interval forecast.

7 Conclusion

In this paper, the hybrid quantile estimators are proposed for the asymmetric PGARCH models via the transformation . Asymptotic normality for the quantile estimators is established under both stationarity and non-stationarity. As a result, tests for strict stationarity and asymmetry are obtained. It is hoped these results will add to the tool kits of time series analysis.

Acknowledgement

The authors greatly appreciate the very helpful comments and suggestions of two anonymous reviewers and the editor. The first author’s work is supported by the Fundamental Research Funds for the Center University (12619624). The second author’s work is supported by RGC of Hong Kong (Nos. 17306818 and 17305619), NSFC (Nos. 11571348, 11690014, 11731015 and 71532013), Seed Fund for Basic Research (No. 201811159049), and the Fundamental Research Funds for the Central University (19JNYH08). The third author’s work is supported by RGC of Hong Kong (Nos. 17304417 and 17304617). The fourth author’s work is supported by RGC of Hong Kong (No. 17304417).

Appendix: Proofs

To facilitate our proofs, we first introduce some notations. Let and . Define four -valued processes

with the convention when . As shown in Francq and Zakoïan (2013a), , , , and have moments of any order.

Second, we give six technical lemmas. Lemmas .1-.2 from Francq and Zakoïan (2013a) show that, after being normalized by , the nonstationary process and its first derivatives can be well approximated by some stationary processes. Lemma .3 gives the asymptotic properties of the GQMLE , and its proof is similar to that of Theorem 3.1 in Francq and Zakoïan (2013a). Lemma .4 proves the consistency of for . Lemmas .5-.6 are used to for the proof of Theorem 3.1.

Lemma .1.

Suppose that Assumption 3.1(ii) holds.

(i) When , for any , the process is stationary and ergodic. Moreover, for any compact set ,

and

Finally, for any , it holds that as .

(ii) When , for any with , the process is stationary and ergodic. Moreover, for any compact set ,

and

Lemma .2.

Suppose that Assumption 3.1(ii) holds.

(i) When , for any , the processes , , and are stationary and ergodic. Moreover, for any compact set ,

where

| (.1) |

(ii) When , for any with , the processes , , and are stationary and ergodic. Moreover, for any compact set ,

Lemma .3.

Suppose that Assumption 3.1 holds and .

(i) When , and for all , then a.s. as , and

| (.2) |

(ii) When , and , then a.s. as , and

| (.3) |

Lemma .4.

(i) When , and , then in probability as .

(ii) When , , and for any and some , then in probability as .

Proof.

We only show the proof of (i), and the proof of (ii) is similar.

First, by (2), it is straightforward that , where with . By using the identity

with , it follows that

| (.4) |

Next, we consider . By Proposition 2.1 in Francq and Zakoïan (2013a), as , and hence

| (.5) |

By Lemma .1(i), it follows that

| (.6) |

Define and . Since and , by (.5)-(.6) we have

| (.7) |

Note that and . Then, it is not difficult to have

| (.8) |

where the second equality holds by Lemma .1(i), (.7) and the boundedness of , and the last equality holds by Taylor’s expansion, Lemma .3(ii), and the fact that

Furthermore, by the double expectation, Lemma .1(i), Assumption 3.2, and standard arguments for tightness, we can prove

| (.9) |

Hence, by (Proof.) and (Proof.), it follows that

| (.10) |

where the second equality holds by the uniform ergodic theorem, the third equality holds by the dominated convergence theorem and Lemma .3(ii), the fourth equality holds since and , and the last equality holds by the double expectation and the fact that the th quantile of is .

Third, we consider . As for (Proof.), we can show

| (.11) |

where lies between and , and the second equality holds by the double expectation, Taylor’s expansion, and the fact that .

Write , where . Define , where

Lemma .5.

(i) If , and , then

| (.12) | |||

| (.13) |

where

Proof.

We only show the proof of (i), and the proof of (ii) is similar.

First, we consider . Without loss of generality, we only show that , where is the first entry of . Note that

| (.14) |

By a similar argument for Lemma 7.5 in Francq and Zakoïan (2013a), we can show that . For , since by Lemma .3(ii), we have

| (.15) |

where the second equality holds by Lemmas .1(i) and .2(i) and the similar arguments as for (Proof.) and (Proof.).

Write , where . Since the th quantile of is , by the ergodic theorem we have

where

By Lemmas .1(i), .2(i), .3(ii) and .4(i), we know that for sufficient large . Hence, for any , there exits a such that

| (.16) |

for , and

| (.17) |

Note that and by the double expectation and dominated convergence theorem. Thus, by Markov’s inequality, for any , there exists a such that . By (.16), it follows that

Second, by Lemmas .1(i), .2(i), .3(ii) and .4(i), Proposition 2.1 in Francq and Zakoïan (2013a), and a similar argument as for Theorem 2.1 in Zheng et al. (2018), we can prove the result for .

Third, we consider . Let

Then, we can see that where . Since is an increasing function and for some constants and , we only need to show

| (.18) |

for any fixed . Rewrite

| (.19) |

where

By Assumptions 3.1-3.2, Lemmas .1(i) and .4(i), and Proposition 2.1 in Francq and Zakoïan (2013a) it is not difficult to show that . Meanwhile, by a similar argument as for Lemma 2.2 in Zhu and Ling (2011), we can show that for fixed and any , we have

which implies that by Lemma .4(i). Hence, by (.19) it follows that

i.e., (.18) holds. This completes all of the proofs. ∎

Lemma .6.

(i) If , and , then

| (.20) |

where

Proof.

The proof can be accomplished by following a similar argument as for Lemma 7.4 in Francq and Zakoïan (2013a). ∎

Proof Theorem 3.1. (i) Following the proofs in Zheng et al. (2018) and Hamadeh and Zakoïan (2011), we can show

| (.21) |

which entails (i) by Lemma .3(i) and standard arguments.

(ii) Following the same argument as for Theorem 2.1 in Francq and Zakoïan (2012), the subgradient derivative with respect to is asymptotically equal to zero at the minimum, since by Lemma .4(i), and belongs to the interior of . This implies

| (.22) |

Moreover, by Lemmas .5(i) and .6(i), we have

By (.22), it follows that

| (.23) |

which implies (ii) holds by Lemmas .3(ii) and .6(i), and standard arguments.

(iii) Its proof can be accomplished by following a similar argument as for (ii). This completes all of the proofs.

References

- [1] Barone-Adesi, G., Bourgoin, F., Giannopoulos, K., 1998. Don’t look back. Risk 11, 100–103.

- [2] Barone-Adesi, G., Giannopoulos, K., 2001. Non parametric var techniques. myths and realities. Economic Notes 30, 167–181.

- [3] Black, F., 1976. Studies of stock price volatility changes. In Proceedings from the American Statistical Association, Business and Economic Statistics Section 177–181. Amer. Statist. Assoc., Alexandria, VA.

- [4] Bollerslev, T., 1986. Generalized autoregressive conditional heteroscedasticity. Journal of Econometrics 31, 307–327.

- [5] Christoffersen, P., 1998. Evaluating interval forecasts. International Economic Review 39, 841–862.

- [6] Engle, R.F., 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50, 987–1007.

- [7] Engle, R.F., Manganelli, S., 2004. CAViaR: conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics 22, 367–381.

- [8] Francq, C., Zakoïan, J.M., 2010. GARCH Models: Structure, Statistical Inference and Financial Applications. Wiley, Chichester.

- [9] Francq, C., Zakoïan, J.M., 2012. Strict stationarity testing and estimation of explosive and stationary generalized autoregressive conditional heteroscedasticity models. Econometrica 80, 821–861.

- [10] Francq, C., Zakoïan, J.M., 2013a. Inference in nonstationary asymmetric GARCH models. Annals of Statistics 41, 1970–1998.

- [11] Francq, C., Zakoïan, J.M., 2013b. Optimal predictions of powers of conditionally heteroscedastic processes. Journal of the Royal Statistical Society: Series B 75, 345–367.

- [12] Francq, C., Zakoïan, J.M., 2015. Risk-parameter estimation in volatility models. Journal of Econometrics 184, 158–173.

- [13] Glosten, L.R., Jaganathan, R., Runkle, D., 1993. On the relation between the expected values and the volatility of the nominal excess return on stocks. Journal of Finance 48, 1779–1801.

- [14] Hamadeh, T., Zakoïan, J.M., 2011. Asymptotic properties of LS and QML estimators for a class of nonlinear GARCH processes. Journal of Statistical Planning and Inference 141, 488–507.

- [15] Higgins, M.L., Bera, A.K., 1992. A class of nonlinear ARCH models. International Economic Review 33, 137–158.

- [16] Hwang, S.Y., Kim, T.Y., 2004. Power transformation and threshold modeling for ARCH innovations with applications to tests for ARCH structure. Stochastic Processes and their Applications 110, 295–314.

- [17] Hörmann, S., 2008. Augmented GARCH sequences: dependence structure and asymptotics. Bernoulli 14, 543–561.

- [18] Jensen, S.T., Rahbek, A., 2004a. Asymptotic normality of the QMLE estimator of ARCH in the nonstationary case. Econometrica 72, 641–646.

- [19] Jensen, S.T., Rahbek, A., 2004b. Asymptotic inference for nonstationary GARCH. Econometric Theory 20, 1203–1226.

- [20] Kuester, K., Mittnik, S., Paolella, M.S., 2006. Value-at-risk prediction: a comparison of alternative strategies. Journal of Financial Econometrics 4, 53–89.

- [21] Li, C.W., Li, W.K., 1996. On a double-threshold autoregressive heteroscedastic time series model. Journal of Applied Econometrics 11, 253–274.

- [22] Li, D., Zhang, X., Zhu, K., Ling, S., 2018. The ZD-GARCH model: A new way to study heteroscedasticity. Journal of Econometrics 202, 1–17.

- [23] Pan, J., Wang, H., Tong, H., 2008. Estimation and tests for power-transformed and threshold GARCH models. Journal of Econometrics 142, 352–378.

- [24] Silverman, B.W., 1986. Density Estimation for Statistics and Data Analysis. London: Chapman and Hall.

- [25] So, M.K., Chung, R.S., 2015. Statistical inference for conditional quantiles in nonlinear time series models. Journal of Econometrics 189, 457–472.

- [26] Rabemananjara, R., Zakoïan, J.M., 1993. Threshold ARCH models and asymmetries in volatility. Journal of Applied Econometrics 8, 31–49.

- [27] Taylor, S., 1986. Modelling Financial Time Series. New York: Wiley.

- [28] Xiao, Z., Koenker, R., 2009. Conditional quantile estimation for generalized autoregressive conditional heteroscedasticity models. Journal of the American Statistical Association 104, 1696–1712.

- [29] Zheng, Y., Zhu, Q., Li, G., Xiao, Z., 2018. Hybrid quantile regression estimation for time series models with conditional heteroscedasticity. Journal of the Royal Statistical Society: Series B 80, 975–993.

- [30] Zhu, K., Li, W.K., Yu, P.L.H., 2017. Buffered autoregressive models with conditional heteroscedasticity: An application to exchange rates. Journal of Business & Economic Statistics 35, 528–542.

- [31] Zhu, K., Ling, S., 2011. Global self-weighted and local quasi-maximum exponential likelihood estimators for ARMA-GARCH/IGARCH models. Annals of Statistics 39, 2131–2163.