Asymptotic Consistency of Loss-Calibrated Variational Bayes

†{varao@purdue.edu} Department of Statistics, Purdue University.)

Abstract

This paper establishes the asymptotic consistency of the loss-calibrated variational Bayes (LCVB) method. LCVB was proposed in LaSiGh2011 as a method for approximately computing Bayesian posteriors in a ‘loss aware’ manner. This methodology is also highly relevant in general data-driven decision-making contexts. Here, we not only establish the asymptotic consistency of the calibrated approximate posterior, but also the asymptotic consistency of decision rules. We also establish the asymptotic consistency of decision rules obtained from a ‘naive’ variational Bayesian procedure.

1 Introduction

In this paper we establish the asymptotic consistency of loss-calibrated variational Bayes (LCVB). Consider a loss function , where is a decision/design variable and is a model parameter space. Given a set of observations drawn from a distribution with unknown parameter , , our goal is to compute the Bayes optimal decision rule

| (1) |

where is the posterior distribution. The latter results when a Bayesian decision-maker places a prior distribution over the parameter space , capturing a priori information about such as location or spread. Given , the prior and likelihood together define a posterior distribution , the conditional distribution over given observations. The posterior distribution represents uncertainty over the unknown parameter , and contains all information required for further inferences or optimization.

In general, under most realistic modeling assumptions, closed-form analytic expressions are unavailable for , making the subsequent integration and optimization problems intractable. In practice, therefore, one uses an approximation to the posterior in the integration in (1). It is easy to see that posterior computation can be expressed as a convex optimization problem:

| (2) | ||||

where KL is the Kullback-Leibler divergence and is the space of all distributions that are absolutely continuous with respect to the posterior (or, equivalently, the prior). This problem can be immediately recognized as minimizing the ‘variational free energy’ neal1998view . Variational Bayesian (VB) procedures BlJo2006 , in standard form, restrict the optimization in (2) to a fixed subset . Here, we are interested in a generalized version of this procedure where the posterior computation is calibrated by the loss function for each :

| (3) | ||||

| (4) |

Observe that the set need not be convex. Consequently, this optimization problem is non-convex, in full generality, and practical algorithms for solving (3) can only guarantee convergence to local minima. We leave the analysis of these optimization-related issues for future work, and focus instead on the global solution and its associated asymptotics. As we show later in Section 2.2 that the optimal value of this loss-calibrated VB objective turns out to be a lower bound to , the logarithm of the loss in (1).

Loss-calibration was introduced in LaSiGh2011 as a method for approximately computing a generalized Bayesian posterior, where the likelihood is re-weighted or calibrated by a loss function over the parameter space . As with most VB methods, theoretical properties of the approximations present largely unanswered questions. Recently, the theoretical properties of the variational Bayesian methods have been studied extensively in (alquier2017concentration, ; abdellatif2018, ; jaiswal2019b, ; WaBl2017, ; yang2017alpha, ; ZhGa2017, ). WaBl2017 established the asymptotic consistency of the VB approximate posterior and also proved a Bernstein-von Mises’ type result for the same. Whereas, the authors in ZhGa2017 studied the convergence rate of the VB approximate posterior. jaiswal2019b presented a general framework for computing a risk-sensitive VB approximation and also studies the statistical performance of the inferred decision rules using these methods. Furthermore campbell2019universal ; cherief2019gen ; huggins2018practical ; jaiswal2019a studied theoretical properties of variational Bayesian methods defined using Hellinger distance, Wasserstein distance, and Rényi divergence respectively instead of Kullback-Liebler (KL) divergence. In this paper, we study the asymptotic consistency of the loss-calibrated approximate posterior and the optimal decisions computed using the this approximate posterior, as the number of samples .

More precisely, in Proposition 3.1, we show (for fixed and an appropriate subset of distributions ) that as the optimizer of (3) weakly converges to a Dirac delta distribution concentrated on the true parameter for almost every sequence generated from the true data generating process. This result shows that the posterior concentrates for any . The reason for this is manifest: observe that . Thus, the loss function can be seen as only changing the prior distribution in the posterior computation. As the number of samples increases, we should anticipate that any calibration effect is diminished. Extending this result, in Proposition 4.3 we show that the optimizers of the approximate decision making problem, computed using the loss calibrated VB posterior, are asymptotically consistent, in the sense that this set of optimizers will necessarily be included in the optimizers of the ‘true’ objective .

Finally, we illustrate our results on the so-called newsvendor problem, studied extensively in the operations research literature as a prototypical decision-making problem. In this problem, a newsvendor must decide on the number of newspapers to stack up before selling any over a given day. We operate under the assumption that the newsvendor can observe realizations of the demand, but does not know the precise data generation process. The goal is to find the optimal number of newspapers to stack that minimizes losses. We conduct numerical studies to show that both the loss calibrated and naive VB methods on this problem are consistent.

The remainder of the paper is organized as follows. In Section 2 we formally introduce decision-theoretic variational Bayesian methods. In Section 3 we prove that the LCVB approximate posterior is asymptotically consistent. We build on this result and prove the consistency of the optimal decisions, using both the LCVB and NVB methods, in Section 4. Finally, we present our numerical results in Section 5.

2 Decision-theoretic Variational Bayes

2.1 The Naive Variational Bayes (NVB) Algorithm

The idea behind standard VB is to approximate the intractable posterior with an element of a simpler class of distributions known as variational family. Popular examples of include the family of Gaussian distributions, or the family of factorized ‘mean-field’ distributions that discard correlations between components of . A natural caveat to the choice of is that these distributions should be absolutely continuous with respect to the posterior (or equivalently, the prior). The variational solution is the element of that is ‘closest’ to in the sense of the Kullback-Leibler (KL) divergence:

| (5) | ||||

VB approaches allow practitioners to bring tools from optimization to the challenging problem of Bayesian inference, with expectation-maximization (neal1998view, ) and gradient-based (kingma2013auto, ) methods being used to minimize equation (5). Note that this optimization problem is non-convex, since the constraint set is non-convex in general. Also, observe that the objective in (5) only requires the knowledge of posterior distribution up to the proportionality constant, since the normalizing term does not depend on .

The natural variational approximation to the optimization in (1) is to calculate the variational approximate expected posterior loss of taking an action , and then perform the following optimization

| (6) |

We call this the naive variational Bayes (NVB) decision rule. This algorithm involves two optimization steps in sequence, separating the approximation of the posterior in (5) from the decision optimization (6). This sequential procedure, in general, involves a loss in performance compared to (1). This creates the desideratum for a calibrated approach that takes the loss function into consideration in computing an appropriate posterior.

2.2 Loss-Calibrated Variational Bayes (LCVB) Algorithm

A more sophisticated approach is to jointly optimize and ; one would expect this to outperform the naive two-stage NVB algorithm. Assuming that the objective , a loss-calibrated lower bound can be derived by applying Jensen’s inequality to the logarithm of the objective in (1), obtaining

In particular, it can be seen that

| (7) |

We call (7) the loss-calibrated (LC) variational objective. Since is a monotone transformation, minimizing the logarithmic objective on the left hand side above is equivalent to (1). Now, for any given we denote the (globally maximal) LCVB approximate posterior as

| (8) |

If the risk function is constant then , for every , is the same as . Akin to in (5), computing only requires knowledge of the posterior distribution up to a proportionality constant. The corresponding LCVB decision-rule is defined as

| (9) |

Observe that the lower bound achieves the log posterior value precisely for such that is proportional to the posterior . Furthermore, (7) shows that the maximization in the lower bound computes a ‘regularized’ approximate posterior. Regularized Bayesian inference (zhu2014bayesian, ) views posterior computation as a variational inference problem with constraints on the posterior space represented as bounds on certain expectations with respect to the approximate posterior. The loss-calibrated VB methodology can be viewed as a regularized Bayesian inference procedure where the regularization constraints are imposed through the logarithmic risk term . Observe, however, that our setting also involves a minimization over the decisions (which does not exist in the regularized Bayesian inference procedure).

3 Consistency of the LCVB Approximate Posterior

Recall the definition of the LCVB approximate posterior in (8) for any . In this section, we show regularity conditions on the prior distribution, the risk function, the likelihood model, and the variational family, under which , for any , converges weakly to a Dirac-delta distribution at the true parameter . We first assume that the prior distribution satisfies

Assumption 3.1.

The prior density function is continuous with non-zero measure in the neighborhood of the true parameter and it is bounded by a positive constant , that is .

The prior distribution with bounded density can be chosen from a large class of distribution, like the exponential-family distributions. The first condition, that the prior has positive density at is a common assumption in Bayesian consistency analysis, otherwise the posterior will not have any measure in the ball around the true parameter .

We also assume the expected loss, or risk function, satisfies the following

Assumption 3.2.

The risk function is

-

1.

continuous in decision variable and locally Lipschitz in the parameter , that is and for every compact set

such that is the Lipschitz constant for any .

-

2.

uniformly integrable in with respect to any and for any .

In order to analyze the consistency of the decisions in this case, we make a further assumption on the log-likelihood function (which follows WaBl2017 ):

Assumption 3.3.

The likelihood satisfies the local asymptotic normality (LAN) condition. In particular, fix . The sequence of log-likelihood functions (where ) satisfies the LAN condition, if there exist matrices and , and random vectors such that as , and for every compact set

This LAN condition is typical in asymptotic analyses, holding for a wide variety of models and allowing the likelihood to be asymptotically approximated by a scaled Gaussian centered around (vdV00, ). We use in the proofs of our results, where is the maximum likelihood estimate of .

Next, we define the rate of convergence of a sequence of distributions to a Dirac delta distribution.

Definition 3.1 (Rate of convergence).

A sequence of distributions converges weakly to , at the rate of if

-

(1)

the sequence of means converges to as , and

-

(2)

the variance of satisfies

We also define rescaled density functions as follows.

Definition 3.2 (Rescaled density).

For a random variable distributed as with expectation , for any sequence of matrices , the density of the rescaled random variable is

where represents the determinant of the matrix.

Next, we place a restriction on the variational family :

Assumption 3.4.

-

1.

The variational family must contain distributions that are absolutely continuous with respect to the posterior distribution .

-

2.

There exists a sequence of distributions in the variational family that converges to a Dirac delta distribution at the rate of and with mean , the maximum likelihood estimate.

-

3.

The differential entropy of the rescaled density of such sequence of distributions is positive and finite.

The first condition is necessary, since the KL divergence in (5) and (7) is undefined for any distribution , that is not absolutely continuous with respect to the posterior distribution. The Bernstein von-Mises theorem shows that under mild regularity conditions, the posterior converges to a Dirac delta distribution at the true parameter at the rate of , and the second condition is just to ensure that the KL divergence is well defined for all large enough . This condition does not, by any means, imply that the LCVB and NVB approximate posterior converges to Dirac delta distribution at the true parameter as .

The primary result in this section shows that the loss-calibrated approximate posterior for any is consistent and converges to the Dirac-delta distribution at . We establish the frequentist consistency of LCVB approximate posterior, extending and building on the results in WaBl2017 .

Some comments are in order for this result. Recall that loss-calibration of the posterior distribution ‘weights’ it by the risk of taking decision , . The optimization then finds the closest density functions in the family to this re-weighted posterior distribution. The posterior re-weighting has the effect of ‘directing’ the VB optimization to the most informative regions of the parameter sample space for the decision problem of interest. However, , which does not involve the data , effectively serves to change the prior distribution, and in the limit, modulo our regularity assumptions, the consistency of the approximate posterior is to be anticipated. The proof of the proposition is presented in the appendix.

Since for a constant risk function , the LCVB approximate posterior is same as NVB approximate posterior , we recover the result obtained in Theorem 5(1) of WaBl2017 . We rewrite the result as a corollary for completeness.

4 Consistency of Decisions

In this section we prove that the optimal decision estimated by the LCVB and NVB algorithms are consistent, in the sense that for almost every infinite sequence, the optimal decision rules and concentrate on the set of ‘true’ optimizers

For brevity, we define for any distribution on and We place a typical, but relatively strong condition on the decision space that

Assumption 4.1.

The decision space is compact.

Coupled with Assumption 3.2, this implies that the risk function is uniformly bounded in the decision space.

Now, suppose that the true posterior is in the set . Then, the NVB approximate posterior in (5) equals , so that the empirical decision-rule coincides exactly with the Bayes optimal decision rule . The consistency of the true posterior has been well-studied, and under Assumption 3.1 it is well known (Sc1965, ; Gh1997, ) that for any neighborhood of the true parameter

| (12) |

where represents the true data-generation distribution. Then, it follows from Assumption 3.2 that

| (13) |

It is straightforward to see that the limit result follows pointwise, and the uniform convergence result follows from the uniform boundedness of the loss functions. In the following section, we consider the typical case when the posterior .

4.1 Analysis of the NVB Decision Rule

The first result of this section proves that the Bayes predictive loss, is (uniformly) asymptotically consistent as the sample size grows. We relegate the proof to the appendix.

Proposition 4.1.

Under the assumptions stated above, we have

| (14) |

This proposition builds on (WaBl2017, , Theorem 5), which shows that modulo Assumptions 3.1, 3.3, and 3.4, the NVB approximate posterior distribution is asymptotically consistent(see Corollary 3.1). Using the consistency of and Assumption 3.2(1), we first establish the pointwise convergence of to . Then we argue, using continuity of the risk function in and the compactness of set , that uniform convergence follows.

A straightforward corollary of Proposition 4.1 implies that the optimal value is asymptotically consistent as well; the proof is in the appendix.

The primary question of interest is the asymptotic consistency of the optimal decision-rule . Our main result proves that in the large sample limit is a subset of the true optimal decisions for almost all samples .

Proposition 4.2.

We have

| (15) |

We use the uniform convergence of to and argue that any decision which is not in the true optimal decision set , must not exist in NVB approximate optimal decision set for large enough . Once again, we relegate the proof to the appendix. Consequently, it follows that NVB optimal actions are asymptotically oracle regret minimizing:

Corollary 4.2.

For any and ,

The result above is a straightforward implication of the continuity of in and Proposition 4.2 and therefore the proof is omitted.

4.2 Analysis of the LC decision rule

Now, recall from (7) that the LC decision-rule is

The next proposition shows that is a subset of the true optimal decision set in the large sample limit for almost all sample sequences. We use similar ideas as used in Section 4.1.

Proposition 4.3.

We have

| (16) |

The proof is in the appendix. This result naturally implies that the loss-calibrated VB optimal decisions are also oracle regret minimizing

Corollary 4.3.

For any and ,

5 Numerical Example

In this section we present a simulation study of a canonical optimal decision making problem called the newsvendor problem. This problem has been extensively studied in the inventory management literature bertsimas2005data ; levi2015data ; Sc1960 . Recall that the newsvendor loss function is defined as

where is the random demand, is the inventory or decision variable, and and are given positive constants. We assume that the decision variable take values in a compact decision space . We also assume that the the random demand is exponentially distributed with unknown rate parameter . The model risk can easily be derived as

| (17) |

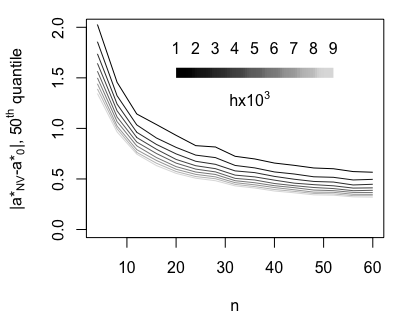

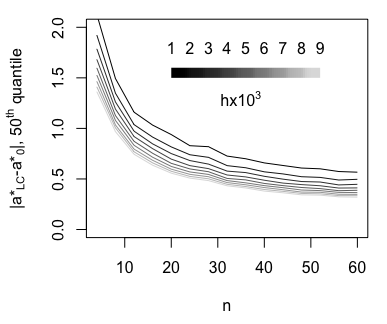

which is convex in . Let be observations of the random demand, assumed to be independent and identically distributed. Next, we posit a non-conjugate inverse-gamma prior distribution over the rate parameter with shape and rate parameter and respectively. Finally, we run a simulation experiment using the newsvendor model described above for a fix , . We use naive VB and LCVB algorithms to obtain the respective optimal decision and for 9 different values of and repeat the experiment over 1000 sample paths. In Figure 1, we plot the quantile of the , where for this model. Observe that the optimality gap decreases quite rapidly for both the naive VB (left) and the loss-calibrated VB (right) methods.

References

- [1] Pierre Alquier and James Ridgway. Concentration of tempered posteriors and of their variational approximations. arXiv preprint arXiv:1706.09293, 2017.

- [2] Dimitris Bertsimas and Aurélie Thiele. A data-driven approach to newsvendor problems. Working Paper, Massachusetts Institute of Technology, 2005.

- [3] David M Blei and Michael I Jordan. Variational inference for dirichlet process mixtures. Bayesian analysis, 1(1):121–143, 2006.

- [4] Trevor Campbell and Xinglong Li. Universal boosting variational inference. arXiv preprint arXiv:1906.01235, 2019.

- [5] Badr-Eddine Chérief-Abdellatif. Generalization error bounds for deep variational inference. arXiv preprint arXiv:1908.04847, 2019.

- [6] Badr-Eddine Chérief-Abdellatif and Pierre Alquier. Consistency of variational bayes inference for estimation and model selection in mixtures. Electron. J. Statist., 12(2):2995–3035, 2018.

- [7] Subhashis Ghosal. A review of consistency and convergence of posterior distribution. In Varanashi Symposium in Bayesian Inference, Banaras Hindu University, 1997.

- [8] Jonathan H Huggins, Trevor Campbell, Mikolaj Kasprzak, and Tamara Broderick. Practical bounds on the error of bayesian posterior approximations: A nonasymptotic approach. arXiv preprint arXiv:1809.09505, 2018.

- [9] Prateek Jaiswal, Harsha Honnappa, and Vinayak A Rao. Risk-sensitive variational bayes: Formulations and bounds. arXiv preprint arXiv:1903.05220v3, 2019.

- [10] Prateek Jaiswal, Vinayak A Rao, and Harsha Honnappa. Asymptotic consistency of rényi-approximate posteriors. arXiv preprint arXiv:1902.01902, 2019.

- [11] Diederik P Kingma and Max Welling. Auto-encoding variational bayes. arXiv preprint arXiv:1312.6114, 2013.

- [12] Simon Lacoste-Julien, Ferenc Huszár, and Zoubin Ghahramani. Approximate inference for the loss-calibrated bayesian. In International Conference on Artificial Intelligence and Statistics, pages 416–424, 2011.

- [13] Retsef Levi, Georgia Perakis, and Joline Uichanco. The data-driven newsvendor problem: new bounds and insights. Oper. Res., 63(6):1294–1306, 2015.

- [14] Radford M Neal and Geoffrey E Hinton. A view of the em algorithm that justifies incremental, sparse, and other variants. In Learning in graphical models, pages 355–368. Springer, 1998.

- [15] E. Posner. Random coding strategies for minimum entropy. Information Theory, IEEE Transactions on, 21(4):388–391, 1975.

- [16] Herbert E Scarf. Some remarks on bayes solutions to the inventory problem. Naval Research Logistics (NRL), 7(4):591–596, 1960.

- [17] Lorraine Schwartz. On bayes procedures. Probability Theory and Related Fields, 4(1):10–26, 1965.

- [18] A. W. van der Vaart. Asymptotic statistics. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, 1998.

- [19] Yixin Wang and David M. Blei. Frequentist consistency of variational bayes. Journal of the American Statistical Association, 0(0):1–15, 2018.

- [20] Yun Yang, Debdeep Pati, and Anirban Bhattacharya. -variational inference with statistical guarantees. arXiv preprint arXiv:1710.03266, 2017.

- [21] Fengshuo Zhang and Chao Gao. Convergence rates of variational posterior distributions. arXiv preprint arXiv:1712.02519, 2017.

- [22] Jun Zhu, Ning Chen, and Eric P Xing. Bayesian inference with posterior regularization and applications to infinite latent svms. Journal of Machine Learning Research, 15:1799, 2014.

Appendix A Proof of Proposition 3.1

Lemma A.1.

For any risk function that satisfies Assumption 3.2 and a given sequence of distributions that converges weakly to any distribution other than the Dirac-delta distribution at , the is undefined in the limit as .

Proof.

Using the definition of the posterior distribution , first observe that

| KL | ||||

| (18) |

where the last inequality uses the fact that . Now taking the on either side, we have

| (19) |

Recall that the posterior distribution converges weakly to . Due to [15, Theorem 16] we know that is a lower semi-continuous function of the pair in the weak topology on the space of probability measures. Using lower semi-continuity, it follows that the first term in (19) satisfies

| (20) |

where the last equality is by definition of the KL divergence, since (as does not weakly converge to ) and therefore it is not absolutely continuous with respect to . Since the last two terms are finite due to Assumption 3.2, we have shown that for any sequence of distribution that converges weakly to any distribution , the diverges in the limit as . ∎

Lemma A.2.

Let be a sequence of compact balls such that for all , and as . Then, under Assumption 4.1 and for any , the sequence of random variables is of order ; that is

Proof.

Using Markov’s inequality, it follows that,

| (21) |

Next, using Fubini’s Theorem in the RHS above and then the fact that , observe that

| (22) |

Since for all and as , is monotonic, and therefore using the monotone convergence theorem, as . Hence, taking limits on either side of (22) the result follows. ∎

Next, we show that for fixed , the KL divergence between the LC approximate posterior and the rescaled posterior is finite in the limit. Also, the following lemma uses similar proof techniques as used in [19].

Lemma A.3.

Proof.

Following Assumption 3.4 there exists a sequence of distributions that converges to at the rate of . Specifically, we consider the sequence where has mean , the maximum likelihood estimate. It suffices to show that for such sequence ,

For brevity let us denote as KL. First, observe that for a compact set containing the true parameter , we have

| KL | ||||

| (23) |

Now we approximate using the LAN condition in Assumption 3.3. Let , and reparameterizing the expression with and denoting as the reparameterized set we have

| (24) | ||||

| (25) |

Now consider the last term in (23). Let be a compact sequence of balls such that for all , and as . Next, using the same re-parametrization we obtain,

| (26) |

Now, Lemma A.2 implies that

| (27) |

Hence, by the results in (26) and (27), the last term in (23) satisfies

| (28) |

where implies that . Now, by substituting (25) and (28) into (23) we obtain,

Since, the as and ,

implying that,

| (29) |

where represents the Gaussian density function. Since has mean and rate of convergence , then by a change of variable to

| (30) |

where is the rescaled density as defined in Definition 3.2. Substituting (30) into (29), we obtain

| (31) |

Since, , due to the specific choice of with variance (see Definition 3.1), it follows from (31) that for large ,

| (32) |

Now take limsup on either side of the above equation. Observe that the first term is finite by Assumption 3.4. The second term is finite since the prior distribution is bounded due to Assumption 3.1. For the third term, since

and the RHS above is bounded by Assumption 3.2. Since, , the fifth term is bounded by Laplace’s approximation,

Since the remaining terms are finite it follows that,

∎

Proof of Proposition 3.1.

Recall from the Lemma A.1 that for any risk function that satisfies Assumption 3.2 and for a given sequence of distributions that converges weakly to any distribution other than , diverges as . On the other hand, Lemma A.3 shows that for any ,

| (33) |

Therefore, Lemma A.1 and A.3 combined together imply that for any , and for any risk function that satisfies Assumption 3.2, the LC approximate posterior must converge weakly to as ; that is ∎

Appendix B Proof of Proposition 4.1

Proof.

Fix . Observe that for any .

| (34) |

Next, recall the fact that NV approximate posterior is consistent from [19], that is for every

| (35) |

Using the above result and the monotone convergence theorem, the first term in (34) converges to zero.

By Assumption 3.2 is locally Lipschitz continuous in . where is the Lipschitz constant for the compact set . Using this fact in the second term of (34), we obtain

| (36) |

Now taking limit on either side of (36), and Using (35) again, the second term in (36) tends to , but since can be arbitrarily small (and as ), we obtain

It follows straightforwardly that converges to -a.s. for any . That is,

| (37) |

Next, define , where is set of rationals on . Thus is a countable set containing the rational numbers (say ) in . Define a set . From (37) we know that . We also know that countable unions of sets of probability measure 0 are also of probability measure 0; that is, . By definition of , it follows that

This establishes the uniform convergence a.s.

By the continuity of in Assumption 3.2, and are continuous over the compact set , and by the Heine-Cantor theorem, and are uniformly continuous on the set . Since the set is dense in the compact set , we can find a sequence that converges to a point . Then, it follows that

From the above inequality, we can conclude that a.s., by using the uniform continuity of and on set and the uniform convergence of to 0a.s, thus completing the proof. ∎

Appendix C Proof of Corollary 4.1

Appendix D Proof of Proposition 4.2

Proof.

Equivalently, we can show that implies that a.s. as . Fix , then we have . Next define . Using Proposition 4.1, there exists an such that , Therefore we have, for all . We also know that for any and

which implies that . Therefore for any , for all . This implies that for all a.s. and hence the proposition follows. ∎

Appendix E Proof of Proposition 4.3

Proof.

Fix and recall from (7) that

Also recall that the LC approximate posterior converges weakly to a Dirac delta distribution at due to Propostion 3.1. It now follows that, due to Assumption 3.2 (2) on and application of dominated convergence theorem

| (40) |

Now since the set is compact, logarithm function is continuous, and is continuous in , it follows using similar arguments as used in Proposition 4.1 that for any ,

| (41) |

Now again using similar arguments as in Proposition 4.2 and monotonicity of logarithm function, we can show that the LC approximate decision rule for any , that is

is subset of the true decision set as . Since the result is true for any , it is true for any that lies in LC approximate decision set and therefore the proposition follows. ∎