∎

200, Fujiagucho, Ohta, Gunma 169-8050 Japan

22email: gspddlnit45@toki.waseda.jp

Bayesian Matrix Completion Approach to Causal Inference with Panel Data

Abstract

This study proposes a new Bayesian approach to infer binary treatment effects. The approach treats counterfactual untreated outcomes as missing observations and infers them by completing a matrix composed of realized and potential untreated outcomes using a data augmentation technique. We also develop a tailored prior that helps in the identification of parameters and induces the matrix of untreated outcomes to be approximately low rank. Posterior draws are simulated using a Markov Chain Monte Carlo sampler. While the proposed approach is similar to synthetic control methods and other related methods, it has several notable advantages. First, unlike synthetic control methods, the proposed approach does not require stringent assumptions. Second, in contrast to non-Bayesian approaches, the proposed method can quantify uncertainty about inferences in a straightforward and consistent manner. By means of a series of simulation studies, we show that our proposal has a better finite sample performance than that of the existing approaches.

Keywords:

Causal inference Matrix completion Panel data Synthetic control method Treatment effect1 Introduction

Program/policy evaluations and comparative case studies using observational data are pervasive in social and natural sciences and in government and business practice. In particular, causal inference is an integral part of social sciences, where randomized experiments are usually infeasible. For instance, although Abadie et al. Abadie2015 analyzed the economic cost of the German reunification in 1990, we cannot repeat such a political event many times in a controlled fashion.

The primary interest of this study is inference of causal effects of a treatment, such as average treatment effect and average treatment effect on treated (ATET). Suppose we have panel data with units and time periods. An outcome of unit at period is denoted by , where when the unit is exposed to treatment and otherwise. Let and be sets of indices for treated and untreated observations, respectively. Then, for instance, ATET is defined as

where denotes the cardinality of set . Inference of causal effects amounts to inference of counterfactual untreated outcomes , , or the “potential outcome” in terms of Neyman–Rubin’s causal model Imbens2015 . Causal inference poses a serious challenge to statisticians, and numerous approaches have been proposed: the difference-in-difference estimator, regression discontinuity design, matching-based methods, etc.111See, e.g., Imbens2015 .

In this study, we propose a new Bayesian approach for inferring the causal effect of a binary treatment with panel data. We transform a statistical problem of causal inference into a matrix completion problem, an extensively studied issue in machine learning (e.g., Keshavan2010 ). Our approach implements in two steps. First, the potential outcomes are inferred via a Bayesian matrix completion method. Then, a causal effect is inferred based on the posterior draws of the potential outcomes.

We model the sum of a matrix of outcomes using two-component factorization and a matrix of covariate effects. The potential outcomes are treated as missing observations and simulated from the posterior predictive distribution,

where denotes a set of observations including untreated outcomes , and exogenous covariates and denotes a set of parameters and random variables to be sampled. The other unknown parameters, such as coefficients on the covariates and the variance of measurement error, are simulated from the conditional posterior distribution. Leaving aside the covariate effects, the proposed approach can be thought as treating inference of the potential outcomes as multiple imputation of a matrix of panel data that is probably rank deficient.

Given the posterior draws of potential outcomes, we can infer a causal effect of interest. For instance, when we have a total of posterior draws of potential outcomes, the posterior mean estimate of the ATET is given by

where denotes the th posterior draw of the potential outcome of unit at period .

To facilitate this task, we develop a tailored prior that induces the model to be lower rank, adapting a cumulative shrinkage process prior Legramanti2019 . With this prior specification, there is no need to specify the rank of the outcome matrix, because the priors pushes insignificant columns of one of the factorizations toward zero.

Our Bayesian approach has two notable advantages. First, it can provide credible intervals in a consistent and straightforward manner, while the existing non-Bayesian approaches have difficulty quantifying uncertainty. As hypothesis testing is an essential component of scientific research, this advantage is a strong reason to use a Bayesian method. Second, our approach has better finite sample performance than that of the existing approaches. By means of a series of simulation studies, we show that our proposal is competitive with the existing approaches in terms of the precision of the prediction of potential outcomes.

Three strands of the literature are particularly relevant to this study. First, the proposed approach is related to a class of synthetic control methods (SCMs) (e.g., Abadie2003 ; Abadie2010 ).222See Abadieforthcoming for a recent overview of the literature on SCMs. This class of methods is aimed at obtaining “synthetic” observations of untreated outcomes as weighted sums of the outcomes of the control units. Despite its increasing popularity, the original SCM Abadie2010 has two notable shortcomings. First, it imposes a strong assumption that the weights of synthetic observations are nonnegative and sum to one. This assumption implies that the treated unit falls in the convex hull of the control units and that synthetic observations are positively correlated with the control units, which is not plausible in many real situations. While some alternative approaches Doudchenko2017 ; Kim2019 ; Amjad2018 do not require these assumptions, our approach has better finite sample performance under various data generating processes, as shown in the simulation studies. Second, the original SCM does not have an effective method for assessing the uncertainty of the obtained estimates. Abadie et al. Abadie2010 conduct a series of placebo studies, but the approach incurs size distortion Hahn2017 . Recently, Li Liforthcoming proposes a subsampling method to obtain confidence intervals for SCMs, but our Bayesian approach can obtain credible intervals simply as a byproduct of posterior simulation.

Second, an approach developed by Athey et al. Athey2018 is particularly related to our proposal. They also treat potential outcomes as missing data and estimate them via matrix completion with the nuclear norm penalty Mazumder2010 . However, Athey et al.’s Athey2018 non-Bayesian approach does not have an estimator for confidence intervals. Finally, our proposal is conceptually similar to approaches proposed by Brodersen2015 ; Ning2019 in that all of them infer potential outcomes as missing observations in Bayesian manners. On the other hand, their approaches rely on the fit of a time-series model, while our approach exploits the factor structure of panel data. Therefore, our proposal is better suited for typical panel data covering short time periods where it is difficult to estimate a time-series model.

The remainder of this study is structured as follows. In Section 2, we introduce a new Bayesian approach to causal inference with panel data and compare it with the existing alternatives. In Section 3, we illustrate the proposed approach by applying it to simulated and real data. We conduct a simulation study and show that our proposed method is competitive with the existing approaches in terms of the precision of the predictions of potential outcomes. Then, the proposed approach is applied to the evaluation of the tobacco control program implemented in California in 1988. The last section concludes the study.

2 Proposed Approach

2.1 Framework

An individual outcome is modeled as follows: for ; ,

where is a unit- and time-specific intercept, is an -dimensional vector of covariates that may contain unit- and/or time-specific effects, is the corresponding coefficient vector, and is an error term that is distributed according to a normal distribution with precision . is a treatment indicator: if is untreated and if is treated. A set of the treatment indicators is denoted by =. The covariates are completely observed for all the units and periods.

and are sets of indices for treated and untreated observations, respectively. denotes a set of all the indices for the observations. Let be a -by- matrix composed of (actually) untreated outcomes, , , and counterfactual untreated outcomes that are actually treated, , . The latter elements are also called “potential outcomes” Imbens2015 . We define sets of observed and unobserved untreated outcomes respectively as

In this study, we treat as missing and infer it as a set of unknown parameters via matrix completion, using a Markov chain Monte Carlo (MCMC) method. In other words, we transform the inferential problem into a matrix completion problem, and infer the potential outcomes by imputing them via data augmentation Tanner1987 (or, more generally, Gibbs sampling).

Let be a set of covariates. Define a -by- matrix of the covariate effects as with . The model can be posed in a matrix representation as

where is a -by- matrix of the error terms.

We have several assumptions in the model. First, we make the standard stable unit treatment value assumption (STUVA) Imbens2015 : there is no interference between units, there is a single type of treatment, and each unit has two potential outcomes. In addition, the assignment mechanism is assumed to be unconfounded, i.e., ignorable, conditional on the covariates :

In contrast to the difference-in-difference estimator, the treated and untreated units are not supposed to have parallel trends in outcome.

A matrix of untreated outcomes can be structured flexibly. For instance, when only the th unit is affected by the treatment for the last periods as in the standard synthetic control method (SCM) Abadie2003 ; Abadie2010 , is specified as

where denotes a missing entry. It is possible to allow more than one treated unit:

Furthermore, it is possible to handle a more complex structure:

From a theoretical perspective, Bayesian inference of is specified as follows. Let denote the set of all unknown parameters. If , , and are given, the complete-data likelihood is represented as

where denotes the column-wise vectorization operator. The joint posterior distribution of the missing observations of the responses and the unknown parameters is written as

where denotes the prior density of . Given and , the conditional posterior distribution of the missing responses is given by

By the unconfoundedness assumption, the assignment mechanism and the covariate distribution are ignorable:

In turn, the conditional posterior of is proportional to the product of the complete-data likelihood and the prior of :

We can conduct a posterior simulation using a Gibbs sampler: and are alternately simulated from the corresponding conditional posterior distributions.

Once the approximation of the posterior distribution of is obtained, we can evaluate treatment effects straightforwardly. For instance, the posterior density of ATET can be represented as

Given the posterior draws of the potential outcomes, the posterior mean estimate of ATET is computed as

where denotes the th posterior draw of the potential outcome of unit at period and is the number of posterior draws used for the posterior analysis. The posterior estimates of the variance/quantiles of the posterior of are obtained analogously.

2.2 Priors

As the structure of the model indicates, unless some restrictions are imposed, we cannot identify and . We induce to be low rank and decompose it into two parts as

where . Although this decomposition is not unique, as and are not identified, exact parameter identification is not necessary for our purpose: we require the identification of the convolution, , not that of its factorization, and .

Nevertheless, when and are not identified, the posterior simulation can diverge, which is computationally inefficient. We use a prior motivated by singular value decomposition (SVD). When the SVD of is represented as , we interpret as the right orthonormal matrix and as the product of the left orthonormal matrix and the diagonal matrix having the eigenvalues in its principal diagonal . Two types of priors introduced in what follows correspond to the interpretation of and .

First, we restrict to be unitary, i.e., , and assign a uniform Haar prior to , , where denotes a Stiefel manifold with dimensions of and denotes the indicator function. This restriction implies that the covariance of the rows of is . Then, can be regarded as being generated from a static factor model as

Second, we arrange the relative magnitudes of the columns of in descending order. For this purpose, we adapt a cumulative shrinkage process prior Legramanti2019 to our context. A prior of is specified by the following hierarchy:

where is an inverse gamma distribution with shape parameter and rate parameter , and is a beta distribution (of the first kind) with scale parameters and . The prior of is a scale mixture of normal distributions. The prior distribution of the variances belongs to a class of spike-and-slab priors (e.g., Ishwaran2005 ), in that the prior consists of spike and slab . Although can be zero, we set it to a small nonzero value for the ease of posterior simulation Ishwaran2005 ; Legramanti2019 . The prior distribution of the weights exploits the stick-breaking construction of the Dirichlet process Ishwaran2001 . As grows, the distribution of concentrates around since almost surely.

In turn, for the remaining parameters, we employ standard priors. For , we use an independent normal prior with mean zero and precision , . The prior distribution of is specified by a gamma distribution with shape parameter and rate parameter , .

Although we do not consider them in this study, many alternative priors can be used for . Bhattacharya and Dunson Bhattacharya2011 consider a prior similar to the cumulative shrinkage process prior, called the multiplicative gamma process prior. This prior cannot simultaneously control the rate of shrinkage and the prior for the active elements; thus, it readily overshrinks the model. See Durante2017 and Legramanti2019 for further discussion. In addition, many fully Bayesian approaches exist for estimating or completing low-rank matrices (e.g., Salakhutdinov2008 ; Ding2011 ). However, these approaches do not consider the parameter identification. The only exception is Tang et al. Tang2019 . They factorize a possibly rank-deficient matrix into three parts as in SVD, , where is diagonal. While they suppose and to be unitary as in this study, the diagonal elements of are not restricted: the ordering of rows of and and the diagonal elements of are freely permuted along the posterior simulation.

2.3 Posterior simulation

For posterior simulation, we develop an MCMC sampler. We conduct posterior simulations using a hybrid of two algorithms. To address the unitary constraint, we sample using the geodesic Monte Carlo on embedded manifolds Byrne2013 . As the conditionals of the remaining parameters are standard, the remaining parameters are updated via Gibbs steps. See the Appendix for the computational details.

While Legramanti et al. Legramanti2019 adaptively tune the rank of a matrix of interest, we prefix the rank of , , for several reasons. First, the unitary constraint on makes it difficult to change adaptively. Second, as our prior pushes to be low rank, it is unnecessary to exactly specify the true rank of : if the th eigenvalue of is negligible, the prior standard deviation of the th row of is inclined to be (spike part). Therefore, we recommend choosing a conservative value for or tuning based on test runs.

2.4 Extensions

We mention some simple extensions. First, we can make the model more robust to outliers by modeling the measurement errors using a distribution with heavier tails than those of a normal distribution. For instance, following Geweke1993 , the generalized Student’s t error is modeled as

where is an auxiliary random variable, is the degrees of freedom of , and is a prior distribution of .

Second, to allow serial correlations in the error terms, their distribution can be modeled as

where is a correlation matrix whose generic element is specified as a function of an autocorrelation parameter . As the conditional posterior of is not standard, is sampled using, e.g., the random-walk Metropolis-Hastings algorithm.

2.5 Comparison with existing approaches

The class of SCMs Abadie2003 ; Abadie2010 is closely related to the proposed approach. In SCMs, “synthetic” untreated outcomes are estimated as weighted sums of the untreated units. This approach imposes three strong assumptions: no intercept, nonnegativity of the weights, and weights that sum to one. However, none of these assumptions appears plausible in many real cases. The proposed approach is free from such restrictions. Doudchenko and Imbens Doudchenko2017 propose an approach that does not impose any of these restrictions on the weights and use a penalty similar to the elastic net estimator Zou2005 . Amjad et al. Amjad2018 propose a robust synthetic control method (RSCM). The difference between RSCM and the abovementioned SCMs is that RSCM constructs a design matrix using the SVD of a matrix composed of the outcomes of untreated units: SVD is used for dimension reduction and denoising. Xu Xu2017 also considers a similar modeling strategy.

All the existing non-Bayesian approaches, including Abadie2010 , Doudchenko2017 , Amjad2018 , and Xu2017 share the same caveat: they cannot evaluate confidence intervals straightforwardly. Abadie et al. Abadie2010 conduct a series of placebo studies, which can be interpreted as permutation tests, to quantify the uncertainty of an inference, but the size of the permutation tests may be distorted as shown by Hahn2017 . No statistically sound method has been developed to estimate confidence intervals of synthetic control methods. Recently, Li Liforthcoming proposes a subsampling method to obtain confidence intervals. In contrast, our Bayesian approach can estimate credible intervals as a byproduct of posterior simulation.

Kim et al. Kim2019 develop a Bayesian version of Doudchenko and Imbens’s Doudchenko2017 approach. Instead of the elastic net penalty, they propose the use of a shrinkage prior, e.g., the horseshoe prior Carvalho2010 . As with Bayesian inference, their approach can obtain credible intervals consistently. Our fully Bayesian approach also enjoys the same advantage. Amjad et al. Amjad2018 also mention a Bayesian version of RSCM, but the method is not fully Bayesian in that the SVD of an outcome matrix is treated as given and uncertainty about the decomposition is ignored.

Our proposal is closely related to Athey et al. Athey2018 , where an estimation problem is treated as a matrix completion problem with a nuclear norm penalty. Athey et al. Athey2018 call their estimator the matrix completion with a nuclear norm minimization estimator (MC-NNM). The prior of used in our approach plays a similar role to the nuclear norm penalty because the nuclear norm is a convex relaxation of the rank constraint Fazel2001 . This family of approaches involving matrix completion has two notable advantages over SCMs. First, treatment is allowed to occur arbitrarily, not consecutively. Second, while SCMs use only pretreatment observations for estimation, this family exploits all the observations including the treated periods (except treated outcomes). Therefore, this class is likely to be statistically more efficient than SCMs, as shown in the simulation study below. Similar to Amjad et al.’s Amjad2018 approach, the matrix completion approaches intend to capture the underlying factor structure of panel data. While in Amjad et al.’s Amjad2018 approach, a threshold for truncating the eigenvalues of an outcome matrix must be specified (hard thresholding), our approach and Amjad et al.’s Amjad2018 approach do not because the cumulative shrinkage process prior and the nuclear norm penalty automatically push the model to be low rank (soft thresholding). As with other non-Bayesian approaches, Athey et al.’s Athey2018 approach provides only a point estimation, while our proposal readily estimates credible intervals.

Finally, Brodersen et al. Brodersen2015 and Ning et al. Ning2019 also develop Bayesian approaches to causal inference that use structural time series models, more specifically, state-space models. Brodersen et al.’s Brodersen2015 approach relies on a univariate state-space model, while Ning et al.’s Ning2019 approach uses a multivariate state-space model that allows spatial correlations between units. These two approaches are similar to ours in that both tend to obtain potential outcomes using Bayesian methods. On the other hand, there is a notable difference between their approaches and ours: their approaches rely on the fit of a state-space model, while our approach exploits the factor structure of panel data. As a consequence, our proposal is better suited for typical panel data where due to the short sample, it is difficult to recover the dynamics of the potential outcomes from the observations.

3 Application

3.1 Simulated data

We conduct a simulation study to demonstrate the proposed approach. In our experimental setting, only the th unit is treated, and it is exposed to the treatment during the last periods of . Let denote the number of untreated periods; thus, . The realized treated outcomes are specified by the sums of hypothetical untreated outcomes and the average treatment effect on treated :

is generated from a factor model: for ; ,

We do not include any covariates.

We consider three types of data-generating processes (DGPs). The first two types differ only in how is generated. In the first case, called DGP-independent, latent factors are independently distributed according to a normal distribution specified as

The second case is called DGP-dependent, where the row of motion of is specified by the following process:

Entries in the factor loading are generated independently from a standard normal distribution:

The third case, DGP-weighted, is motivated by a simulation study in Kim2019 . In this setting, outcomes of untreated units are generated from a multivariate normal distribution, and outcomes of treated units are constructed as weighted sums of untreated units:

is specified as follows:

and

We compare six alternative approaches.

-

1.

The first is the original synthetic control method described in Abadie2010 (SCM-ABD).

-

2.

The second is a method proposed by Doudchenko2017 (SCM-DI).

-

3.

The third is a Bayesian approach developed by Kim et al. Kim2019 . According to their simulation study, specifications with the horseshoe Carvalho2010 and spike-and-slab Ishwaran2005 priors outperform other alternatives. While the performances of these two priors are comparable, posterior simulation using the horseshoe prior is faster. Thus, we consider the horseshoe prior for Kim et al.’s Kim2019 approach and refer to this specific approach as BSCM. We sample weighting parameters in the observation model using the elliptical slice sampler Hahn2019 and obtain the remaining parameters (noise variance and shrinkage parameters) using a Gibbs sampler, as in Makalic2016 .

-

4.

The fourth is the robust synthetic control method introduced by Amjad2018 (RSCM). Specifically, we consider their primary choice described in Algorithm 1 of the original paper (p. 8).

-

5.

The fifth is the matrix completion with a nuclear norm minimization estimator Athey2018 (MC-NNM).

-

6.

The seventh is the proposed approach, Bayesian matrix completion with cumulative shrinkage process prior (BMC-CSP). The prefixed hyperparameters for the cumulative shrinkage process prior are chosen following Legramanti2019 as and . While Legramanti et al. Legramanti2019 use , we use a smaller value, . The maximum rank of is set to , where denotes the ceiling function.

To ensure a fair comparison, we use the same prior for the error variance in BSCM as in the proposed approach. We choose the hyperparameters as , inducing the prior of to be fairly noninformative. For MC-NNM, we choose tuning parameters via five-fold cross-validation, where the training samples are randomly chosen without replacement. For SCM-DI and RSCM, the tuning parameters are determined by forward chaining: the tuning parameters are chosen by minimizing the mean squared errors of one-step-ahead out-of-sample predictions, and the training sample is initially set to five and expanded sequentially to . For BSCM and BMC-CSP, we obtain 40,000 draws after discarding the initial 10,000. All the posterior simulations pass Geweke’s Geweke1992 convergence test at a significance level of 5%.

We consider four types of sample size, namely, combinations of and , and the length of the treated periods is fixed to . A total of 200 experiments are conducted for each case. As noted earlier, an estimation of ATE amounts to an estimation of potential outcomes. Therefore, we evaluate the alternatives based on the precision of the estimates of , , measured by the mean of the sum of the squared errors (MSE) and the mean of the sum of absolute errors (MAE). For the Bayesian approaches, we compute posterior means of predicted potential outcomes. We also report the mean computation time measured in seconds (Time).333We wrote all the programs in Matlab R2019b (64 bit) and executed them on an Ubuntu Desktop 18.04 LTS (64 bit), running on AMD Ryzen Threadripper 1950X (4.2GHz). For each experiment, the MSE and MAE are normalized by the corresponding values for SCM-ABD, (i.e., the smaller the values are, the better).

Table 1 summarizes the results of the simulation study for DGP-independent. In terms of MSE and MAE, irrespective of the combination of , the proposed approach consistently outperforms the others. The recently proposed alternatives are comparable with or worse than SCM-ABD. In this setting, RSCM is consistently inferior to the original SCM-ABD. In terms of computational time, as expected, the Bayesian approaches are slower than the non-Bayesian options. Indeed, BMC-CSP is computationally heavy, but the computational cost is not prohibitive. In our simulation study, SCM-DI is slow to converge, possibly due to nonsmooth objective functions. The simulation results for DGP-dependent are reported in Table 2. In terms of MSE and MAE, RSCM, MC-NNM, and BMC-SCP perform best. Table 3 summarizes the results for DGP-weighted. SCM-DI and BSCM perform very well because this DGP is exactly consistent with the DGPs of the models. In contrast to the other DGPs, the predictive accuracy of RSCM and MC-NNM is much worse than that of the others, including SCM-ABD. Although BMC-SCP performs worse than SCM-DI and BSCM, it consistently outperforms the remaining approaches. In summary, while the relative finite-sample performance of the alternative approaches depends on the DGP, the proposed approach, BMC-SCP, is fairly competitive under various circumstances.

| Approach | MSE | MAE | Time | ||||

|---|---|---|---|---|---|---|---|

| (1) SCM-ABD | 1. | 00 | 1. | 00 | 0. | 1 | |

| (2) SCM-DI | 1. | 48 | 1. | 17 | 24. | 7 | |

| (3) BSCM | 1. | 60 | 1. | 23 | 11. | 3 | |

| (4) RSCM | 1. | 22 | 1. | 08 | 6. | 5 | |

| (5) MC-NNM | 0. | 99 | 0. | 98 | 0. | 8 | |

| (6) BMC-CSP | 0. | 95 | 0. | 96 | 92. | 7 | |

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 1. | 54 | 1. | 21 | 96. | 0 | |

| (3) BSCM | 1. | 53 | 1. | 21 | 28. | 3 | |

| (4) RSCM | 1. | 27 | 1. | 11 | 8. | 1 | |

| (5) MC-NNM | 1. | 09 | 1. | 04 | 1. | 6 | |

| (6) BMC-CSP | 0. | 90 | 0. | 95 | 507. | 8 | |

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 0. | 96 | 0. | 97 | 175. | 5 | |

| (3) BSCM | 0. | 97 | 0. | 97 | 14. | 9 | |

| (4) RSCM | 1. | 29 | 1. | 10 | 53. | 2 | |

| (5) MC-NNM | 1. | 00 | 0. | 98 | 0. | 8 | |

| (6) BMC-CSP | 0. | 90 | 0. | 93 | 96. | 1 | |

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 1. | 16 | 1. | 06 | 728. | 6 | |

| (3) BSCM | 1. | 68 | 1. | 27 | 46. | 1 | |

| (4) RSCM | 1. | 59 | 1. | 24 | 74. | 3 | |

| (5) MC-NNM | 1. | 09 | 1. | 04 | 2. | 1 | |

| (6) BMC-CSP | 0. | 94 | 0. | 97 | 514. | 5 | |

| Approach | MSE | MAE | Time | ||||

|---|---|---|---|---|---|---|---|

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 1. | 44 | 1. | 15 | 23. | 9 | |

| (3) BSCM | 1. | 57 | 1. | 21 | 10. | 3 | |

| (4) RSCM | 0. | 71 | 0. | 84 | 6. | 1 | |

| (5) MC-NNM | 0. | 73 | 0. | 85 | 0. | 6 | |

| (6) BMC-CSP | 0. | 71 | 0. | 84 | 93. | 8 | |

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 1. | 53 | 1. | 22 | 97. | 9 | |

| (3) BSCM | 1. | 42 | 1. | 18 | 26. | 0 | |

| (4) RSCM | 0. | 81 | 0. | 89 | 7. | 6 | |

| (5) MC-NNM | 0. | 88 | 0. | 93 | 1. | 1 | |

| (6) BMC-CSP | 0. | 79 | 0. | 89 | 508. | 7 | |

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 0. | 86 | 0. | 92 | 170. | 6 | |

| (3) BSCM | 0. | 87 | 0. | 92 | 14. | 0 | |

| (4) RSCM | 0. | 75 | 0. | 86 | 52. | 0 | |

| (5) MC-NNM | 0. | 76 | 0. | 86 | 0. | 5 | |

| (6) BMC-CSP | 0. | 75 | 0. | 86 | 97. | 0 | |

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 1. | 47 | 1. | 19 | 698. | 4 | |

| (3) BSCM | 1. | 75 | 1. | 30 | 42. | 3 | |

| (4) RSCM | 0. | 87 | 0. | 93 | 65. | 9 | |

| (5) MC-NNM | 0. | 90 | 0. | 95 | 1. | 5 | |

| (6) BMC-CSP | 0. | 88 | 0. | 94 | 518. | 6 | |

| Approach | MSE | MAE | Time | ||||

|---|---|---|---|---|---|---|---|

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 0. | 03 | 0. | 17 | 25. | 4 | |

| (3) BSCM | 0. | 03 | 0. | 17 | 17. | 3 | |

| (4) RSCM | 23. | 28 | 5. | 70 | 12. | 7 | |

| (5) MC-NNM | 15. | 18 | 4. | 62 | 3. | 2 | |

| (6) BMC-CSP | 0. | 63 | 0. | 78 | 90. | 4 | |

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 0. | 39 | 0. | 60 | 70. | 1 | |

| (3) BSCM | 0. | 43 | 0. | 63 | 54. | 1 | |

| (4) RSCM | 14. | 67 | 4. | 60 | 23. | 9 | |

| (5) MC-NNM | 13. | 88 | 4. | 44 | 6. | 3 | |

| (6) BMC-CSP | 0. | 71 | 0. | 83 | 507. | 3 | |

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 0. | 02 | 0. | 13 | 211. | 2 | |

| (3) BSCM | 0. | 02 | 0. | 13 | 21. | 0 | |

| (4) RSCM | 26. | 56 | 6. | 17 | 86. | 7 | |

| (5) MC-NNM | 11. | 74 | 3. | 96 | 3. | 5 | |

| (6) BMC-CSP | 0. | 05 | 0. | 19 | 92. | 2 | |

| (1) SCM-ABD | 1. | 00 | 1. | 00 | <0. | 1 | |

| (2) SCM-DI | 0. | 03 | 0. | 17 | 622. | 1 | |

| (3) BSCM | 0. | 03 | 0. | 17 | 84. | 1 | |

| (4) RSCM | 22. | 77 | 5. | 74 | 185. | 6 | |

| (5) MC-NNM | 9. | 70 | 3. | 63 | 7. | 4 | |

| (6) BMC-CSP | 0. | 41 | 0. | 63 | 511. | 9 | |

3.2 Real data

As an illustration, we apply the proposed approach to evaluate California’s tobacco control program implemented in 1988. We replicate Abadiet et al.’s Abadie2010 study using the same data, annual state-level panel data spanning 1970 to 2000.444The data and the Matlab program were downloaded from Jens Hainmueller’s personal website. (https://web.stanford.edu/~jhain/synthpage.html) The first 19 years are the pretreatment period. Only California is treated, while the other 38 states are used as control units. We include seven time-invariant covariates: log of gross domestic product per capita, percentage share of 15–24–year–old people in the population, retail price, beer consumption per capita, and cigarette sales per capita in 1980 and 1975; see Abadie2010 for further details. We use the same hyperparameters as in the simulation study. We draw 100,000 posterior samples and use the last 80,000 samples for posterior analysis.555We also conduct a posterior simulation where the unitary constraint on is removed and is sampled via a standard Gibbs step, but this approach is unsuccessful because the Markov chains diverge, resulting in numerical error.

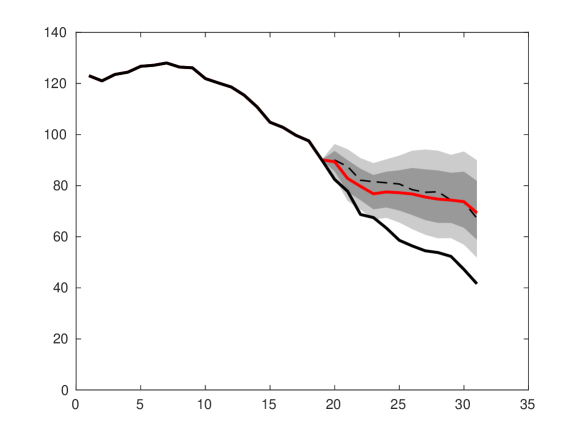

Figure 1 compares the realized per capita cigarette sales in California (solid black line), the potential per capita cigarette sales in “synthetic California” obtained using the original SCM Abadie2010 (dashed black line), and the posterior mean estimates of the corresponding potential outcomes obtained by the proposed method (solid red line). The estimates obtained using the proposed method are in line with the estimates obtained using the original SCM. Posterior estimates of 90% and 70% credible sets are also reported (shaded areas). As the credible sets do not include the realized California, the program has statistically significant effects on tobacco consumption in California, confirming the conclusion in the original paper.

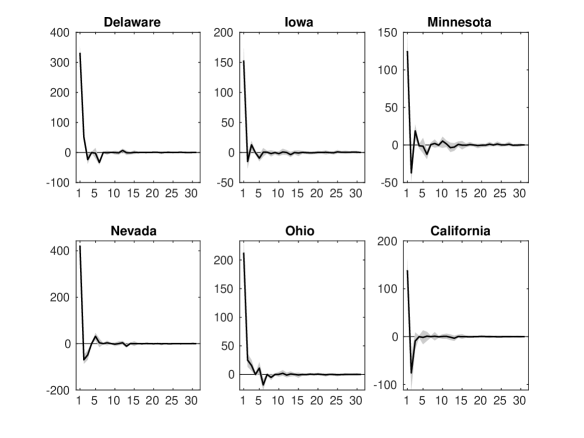

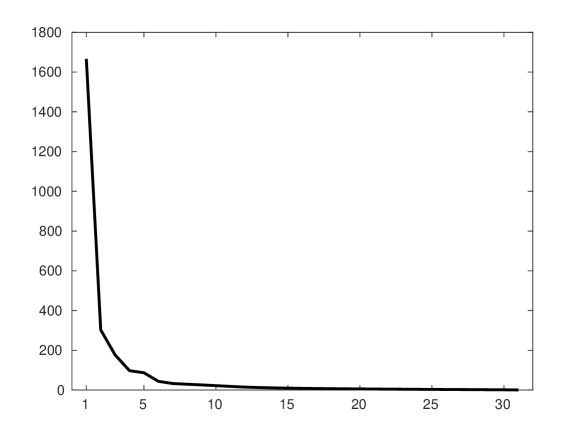

Figure 2 depicts the posterior estimates of some rows of , which can be interpreted as state-specific loadings. While the estimates have different patterns, reflecting heterogeneity in US states, their magnitude is roughly decreasing with as intended by the prior. Figure 3 plots the posterior mean estimates of the eigenvalues of , which suggests that approximately half of the eigenvalues are not essential.

4 Concluding Remarks

This study develops a novel Bayesian approach to causal analysis using panel data. We treat the problem of inferring a treatment effect as a matrix completion problem: counterfactual untreated outcomes that are actually treated are inferred using a data augmentation technique. We also propose a prior structured to help identification and to obtain a low-rank approximation of the panel data. In contrast to existing non-Bayesian methods, the proposed Bayesian approach can estimate credible intervals straightforwardly. By means of a series of simulation studies, we show that the proposed approach outperforms the existing ones in terms of the prediction of hypothetical untreated outcomes, that is, the accuracy of the treatment effect estimates.

While asymptotic argument is not absolutely necessary for Bayesian analysis, there is a need to investigate frequentist (asymptotic) properties of the proposed approach, such as posterior consistency and Bernstein-von-Mises theorem. However, up to the author’s knowledge, there is no published work on frequentist properties of Bayesian matrix factorization/completion, except Mai2015 .666Mai and Alquier Mai2015 propose a Bayesian estimator for the matrix completion method and provide an oracle inequality for this estimator. However, they employ a uniform prior, and the proof critically depends on this prior choice; thus, their discussion is not easily extended to other environments. The author hopes that this paper stimulates further theoretical studies in the related research horizons.

Appendix: Computational Details

This appendix describes the computational details of the posterior simulation of the proposed approach. The joint posterior is specified as

where and . Each sampling block is specified in what follows.

Sampling

Each row of is sampled from a multivariate normal distribution. For ,

Sampling the shrinkage parameters

The conditional of is specified as

where is the PDF of a multivariate normal distribution with mean and covariance evaluated at and is the PDF of a multivariate t distribution with location parameter , scale parameter , and degrees of freedom. The sampling distributions of and are

Sampling

To sample , we employ the geodesic Monte Carlo on embedded manifolds developed by Byrne2013 . The algorithm for sampling is summarized in Algorithm 1. Let be the posterior density of conditional on the other parameters. Then the gradient with respect to is derived as

The step size is adaptively tuned to maintain the average acceptance rate near a target value . In the th iteration, is updated as follows:

where is the average acceptance rate in the th iteration and is a tuning parameter. We choose and .777The target acceptance rate is chosen based on a multivariate effective sample size Vats2019 . The number of steps is fixed to five, .

Sampling

is simulated from a multivariate normal distribution:

Sampling

is updated via the following gamma distribution:

Sampling

The conditional posterior distribution of a missing observation of unit in time period is a normal distribution,

Acknowledgements.

The author would like to thank Hideki Konishi, Yasuhiro Omori, and Hisatoshi Tanaka for their helpful discussions.Conflict of interest

The author declares that there is no conflict of interest.

References

- (1) Abadie, A.: Using synthetic controls: Feasibility, data requirements, and methodological aspects. Journal of Economic Literature (forthcoming)

- (2) Abadie, A., Diamond, A., Hainmueller, J.: Synthetic control methods for comparative case studies: Estimating the effect of california’s tobacco control program. Journal of the American Statistical Association 105(490), 493–505 (2010)

- (3) Abadie, A., Diamond, A., Hainmueller, J.: Comparative politics and the synthetic control method. American Journal of Political Science 59(2), 495–510 (2015)

- (4) Abadie, A., Gardeazabal, J.: The economic costs of conflict: A case study of the basque country. American economic review 93(1), 113–132 (2003)

- (5) Amjad, M., Shah, D., Shen, D.: Robust synthetic control. Journal of Machine Learning Research 19(1), 802–852 (2018)

- (6) Athey, S., Bayati, M., Doudchenko, N., Imbens, G., Khosravi, K.: Matrix completion methods for causal panel data models. Tech. rep., arXiv:1710.10251 (2018)

- (7) Bhattacharya, A., Dunson, D.B.: Sparse bayesian infinite factor models. Biometrika pp. 291–306 (2011)

- (8) Brodersen, K.H., Gallusser, F., Koehler, J., Remy, N., Scott, S.L.: Inferring causal impact using bayesian structural time-series models. Annals of Applied Statistics 9(1), 247–274 (2015)

- (9) Byrne, S., Girolami, M.: Geodesic monte carlo on embedded manifolds. Scandinavian Journal of Statistics 40(4), 825–845 (2013)

- (10) Carvalho, C.M., Polson, N.G., Scott, J.G.: The horseshoe estimator for sparse signals. Biometrika 97(2), 465–480 (2010)

- (11) Ding, X., He, L., Carin, L.: Bayesian robust principal component analysis. IEEE Transactions on Image Processing 20(12), 3419–3430 (2011)

- (12) Doudchenko, N., Imbens, G.W.: Balancing, regression, difference-in-differences and synthetic control methods: A synthesis. Tech. rep., arXiv:1610.07748 (2017)

- (13) Durante, D.: A note on the multiplicative gamma process. Statistics and Probability Letters 122, 198–204 (2017)

- (14) Fazel, M., Hindi, H., Boyd, S.P.: A rank minimization heuristic with application to minimum order system approximation. In: Proceedings of the American Control Conference, vol. 6, pp. 4734–4739. Citeseer (2001)

- (15) Geweke, J.: Evaluating the accuracy of sampling-based approaches to the calculations of posterior moments. Bayesian Statistics 4, 641–649 (1992)

- (16) Geweke, J.: Bayesian treatment of the independent student-t linear model. Journal Of Applied Econometrics 8(S1), S19–S40 (1993)

- (17) Hahn, J., Shi, R.: Synthetic control and inference. Econometrics 5(4), 52 (2017)

- (18) Hahn, P.R., He, J., Lopes, H.F.: Efficient sampling for gaussian linear regression with arbitrary priors. Journal of Computational and Graphical Statistics 28(1), 142–154 (2019)

- (19) Imbens, G.W., Rubin, D.B.: Causal Inference in Statistics, Social, and Biomedical Sciences. Cambridge University Press, New York (2015)

- (20) Ishwaran, H., James, L.F.: Gibbs sampling methods for stick-breaking priors. Journal of the American Statistical Association 96(453), 161–173 (2001)

- (21) Ishwaran, H., Rao, J.S., et al.: Spike and slab variable selection: Frequentist and bayesian strategies. Annals of Statistics 33(2), 730–773 (2005)

- (22) Keshavan, R.H., Montanari, A., Oh, S.: Matrix completion from noisy entries. Journal of Machine Learning Research 11(Jul), 2057–2078 (2010)

- (23) Kim, S., Lee, C., Gupta, S.: Bayesian synthetic control methods. Tech. rep., Cornell University (2019)

- (24) Legramanti, S., Durante, D., Dunson, D.B.: Bayesian cumulative shrinkage for infinite factorizations. Biometrika (forthcoming)

- (25) Li, K.T.: Statistical inference for average treatment effects estimated by synthetic control methods. Journal of the American Statistical Association (forthcoming)

- (26) Mai, T.T., Alquier, P.: A bayesian approach for noisy matrix completion: Optimal rate under general sampling distribution. Electronic Journal of Statistics 9(1), 823–841 (2015)

- (27) Makalic, E., Schmidt, D.F.: A simple sampler for the horseshoe estimator. IEEE Signal Processing Letters 23(1), 179–182 (2016)

- (28) Mazumder, R., Hastie, T., Tibshirani, R.: Spectral regularization algorithms for learning large incomplete matrices. Journal of Machine Learning Research 11(Aug), 2287–2322 (2010)

- (29) Ning, B., Ghosal, S., Thomas, J.: Bayesian method for causal inference in spatially-correlated multivariate time series. Bayesian Analysis 14(1), 1–28 (2019)

- (30) Salakhutdinov, R., Mnih, A.: Bayesian probabilistic matrix factorization using markov chain monte carlo. In: Proceedings of the 25th international Conference on Machine learning, pp. 880–887. ACM (2008)

- (31) Tang, K., Su, Z., Zhang, J., Cui, L., Jiang, W., Luo, X., Sun, X.: Bayesian rank penalization. Neural Networks 116, 246–256 (2019)

- (32) Tanner, M.A., Wong, W.H.: The calculation of posterior distributions by data augmentation. Journal of the American Statistical Association 82(398), 528–540 (1987)

- (33) Vats, D., Flegal, J.M., Jones, G.L.: Multivariate output analysis for markov chain monte carlo. Biometrika 106(2), 321–337 (2019)

- (34) Xu, Y.: Generalized synthetic control method: Causal inference with interactive fixed effects models. Political Analysis 25(1), 57–76 (2017)

- (35) Zou, H., Hastie, T.: Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B 67(2), 301–320 (2005)