Explaining black box decisions by Shapley cohort refinement

Abstract

We introduce a variable importance measure to quantify the impact of individual input variables to a black box function. Our measure is based on the Shapley value from cooperative game theory. Many measures of variable importance operate by changing some predictor values with others held fixed, potentially creating unlikely or even logically impossible combinations. Our cohort Shapley measure uses only observed data points. Instead of changing the value of a predictor we include or exclude subjects similar to the target subject on that predictor to form a similarity cohort. Then we apply Shapley value to the cohort averages. We connect variable importance measures from explainable AI to function decompositions from global sensitivity analysis. We introduce a squared cohort Shapley value that splits previously studied Shapley effects over subjects, consistent with a Shapley axiom.

1 Introduction

Black box prediction models used in statistics, machine learning and artificial intelligence have been able to make increasingly accurate predictions, but it remains hard to understand those predictions. Part of understanding predictions is understanding which variables are important. Variable importance in machine learning and AI has been studied recently in Štrumbelj and Kononenko, (2010, 2014), Ribeiro et al., (2016), Lundberg and Lee, (2017), Sundararajan and Najmi, (2020), Kumar et al., (2020) as well as the book of Molnar, (2018).

A variable could be important because changing it makes a causal difference, or because changing it makes a large change to our predictions or because leaving it out of a model reduces that model’s prediction accuracy (Jiang and Owen,, 2003). Importance by one of these criteria need not imply importance by another.

In order to explain a decision like somebody being admitted to the intensive care unit or turned down for a loan, we are not focused on causality. The variables that are predictive of somebody’s outcome ideally should have been the ones that were important to the decision, but they may not have been. Similarly, variables whose inclusion is necessary for a good model fit are not necessarily the ones that best explain an outcome. The explanation should use the model that was deployed, and not any others.

We are left with a problem of explaining the output of one specific fitted function applied to a vector of input variables, hereafter predictors. For a target subject with a -dimensional set of predictors we can change some subset of values of , perhaps to some baseline levels in . Then the variables that best explain why is different from are deemed important for the decision on the target subject. Given possible changes, there are strong reasons to favor Shapley value Shapley, (1952) to combine them into an importance measure as Sundararajan and Najmi, (2020) and others that they survey do. We note however, that concerns about using Shapley value have been raised by Kumar et al., (2020).

Mixing and matching the components of and presents some problems. The variables and may show a strong correlation over subjects . Putting and into a single hypothetical point may produce an input combination far from any that has ever been seen. Beyond being unusual, some combinations are physically or even logically impossible. The changes might produce a hybrid data point representing a patient whose systolic blood pressure is lower than their diastolic blood pressure. Somebody’s birth date could follow their graduation date. When hospital records show minimum, maximum and average levels of blood oxygen, the hybrid point could have mean below minimum , or it could have minimum and maximum that differ along with a variable saying they were only measured once (or never). There could be important reasons to understand effects of longitude and latitude separately, but some combinations will not make sense, perhaps by placing a dwelling within a body of water.

When the function that made a decision was trained, it would have seen few if any impossible or extremely unlikely inputs. As a result, its predictions there cannot have been regularized suitably. Investigators should be able to choose an importance measure that does not rely on any such values.

In this paper we work under the constraint that only possible values can be used. It is hard to define possible values and so operationally we only use actually observed values. For each predictor, every subject in the data set is either similar to the target subject or not similar. Ways to define similarity are discussed below. Given predictors, there are different sets of predictors on which subjects can be similar to the target. We form different cohorts of subjects, each consisting of subjects similar to the target on a subset of predictors, without regard to whether they are also similar on any of the other predictors. At one extreme is a set of all predictors, and a cohort that is similar to the target in every way. At the other extreme, the empty predictor set yields the set of all subjects. As usual, for large , Monte Carlo sampling is used to approximate the Shapley value.

We can refine the grand cohort of all subjects towards the target subject by removing subjects that mismatch the target on one or more predictors. The predictors that change the cohort mean the most when we restrict to similar subjects, are the ones that we take to be the most important in explaining why the target subject’s prediction is different from that of the other subjects.

We call this approach ‘cohort refinement Shapley’ or cohort Shapley for short. With baseline Shapley, taking account of variable is done by replacing by . Cohort Shapley doesn’t change the value. It refines what we know about . Variables whose knowledge moves the cohort mean the most are then the important ones.

This knowledge approach has some consequences. If one is studying redlining by an algorithm that simply does not use a protected variable then baseline Shapley can only give that variable zero importance. Cohort Shapley can give that variable a nonzero importance measure even if it was not in the data set at the time the model was trained. It is thus useful for the problem of auditing an algorithm for indirect inferences, a task described by Adler et al., (2018). Kumar et al., (2020) describe this issue as a catch-22. In their terms, cohort Shapley is a conditional method (changing knowledge) while baseline Shapley is an interventional method (changing values). The conditional approach has the problem of requiring a joint distribution for predictors, while the interventional approach can depend on impossible predictor combinations. The word ‘importance’ does not have a unique interpretation. Multiple ways to quantify it estimate different quantities and involve tradeoffs. We expect that multiple methods must be considered in practice.

Sundararajan and Najmi, (2020) and Kumar et al., (2020) mention a second problem with baseline Shapley. If two predictors are highly correlated then the algorithm might have used them very unequally, perhaps due to an regularization. It then becomes unpredictable which will be deemed important. The situation is more stable with cohort Shapley. In the extreme case of identical variables and identical similarity notions, cohort Shapley will give them equal importance.

As mentioned above, we define the impact of a variable through the Shapley value. Shapley value has been used in model explanation for machine learning (Štrumbelj and Kononenko,, 2010, 2014; Lundberg and Lee,, 2017; Sundararajan and Najmi,, 2020) and for computer experiments (Owen,, 2014; Song et al.,, 2016; Owen and Prieur,, 2017). KernelSHAP (Lundberg and Lee,, 2017) computes an approximation of baseline Shapley replacing by a kernel approximation. KernelSHAP provides an option to compute the average of Shapley values for multiple baseline vectors, and one very reasonable choice is to use every training point as a baseline point. We call that ‘all baseline Shapley’ (ABS), below.

Our contribution is to further investigate the differences between baseline and cohort Shapley and to connect them to the global sensitivity analysis literature which emphasizes Sobol’ indices (Sobol’,, 1993). For surveys, see Saltelli et al., (2008) and Gamboa et al., (2016). We show how both baseline Shapley value and cohort Shapley value are derived from functional decompositions. Variable importance for a single target subject is ‘local’ as distinct from ‘global’ prediction importance, taken over all subjects. We consider aggregation and disaggregation between local and global problems. While Shapley value is additive over games, some unwanted cancellations can arise during aggregation. For instance, the local importances can sum to a global importance of zero. We resolve this by using squared differences for local and global methods. We illustrate these measures on the well known Boston housing and Titanic data sets.

2 Notation and Background

The predictor vector for subject is where is the number of predictors in the model. Each belongs to a set which may consist of real or binary variables or some other types. There is a black box function that is used to predict an outcome for a subject with predictor vector . We write and . For local explanation we would like to quantify the importance of predictors on . We assume that is in the set of subjects with available data, although this subject might not have been used in training the model. A baseline point might not be one of the subjects. For instance if it will ordinarily not be a data point. For example, might be in for a binary variable .

The set of subjects is denoted by and the set of predictors is . We will need to manipulate subsets of . For we let be its cardinality. The complementary set is denoted by , especially in subscripts. Sometimes a point must be created by combining parts of two other points. The point has for and for . Furthermore, we sometimes use and in place of the more cumbersome and . For instance, is what we get by changing the ’th predictor of the target subject to the baseline level. We also use for .

2.1 Function Decompositions

Function decompositions, also called high dimensional model representations (HDMR), write a function of inputs as a sum of functions, each of which depend only on one of the subsets of inputs. Because and have other uses in this paper, we present the decomposition for . Let be a function of with . In these decompositions we write

where depends on only through . Many such decompositions are possible (Kuo et al.,, 2010).

The best known decomposition for this problem is the functional analysis of variance (ANOVA) decomposition (Hoeffding,, 1948; Sobol’,, 1969). It applies to random with independent components . If , then we write

for non-empty . The effects are orthogonal in that for subsets , we have Letting , it follows from this orthogonality that

We can recover effects from conditional expectations, via inclusion-exclusion,

| (1) |

See Owen, (2013) for history and derivations of this functional ANOVA.

We will need the anchored decomposition, which goes back at least to Sobol’, (1969). It is also called cut-HDMR (Aliş and Rabitz,, 2001) in chemistry, and finite differences-HDMR in global sensitivity analysis (Sobol’,, 2003). We begin by picking a reference point called the anchor, with for . The anchored decomposition is

We have replaced averaging over by plugging in the anchor value via . If and , then . We do not need independence of the , or even randomness for them and we do not need mean squares. What we need is that when is defined, so is for any .

2.2 Shapley Value

Shapley value (Shapley,, 1952) is used in game theory to define a fair allocation of rewards to a team that has cooperated to produce something of value. Suppose that a team of people produce a value , and that we have at our disposal the value that would have been produced by the team , for all teams . Let be the reward for player .

Shapley introduced quite reasonable criteria:

-

1)

Efficiency: .

-

2)

Symmetry: If for all , then .

-

3)

Dummy: if for all , then .

-

4)

Additivity: if and lead to values and then the game producing has values .

He found that the unique valuation that satisfies all four of these criteria is

| (2) |

Formula (2) is not very intuitive. Another way to explain Shapley value is as follows. We could build a team from to in steps, adding one member at a time. There are different orders in which to add team members. The Shapley value is the increase in value coming from the addition of member , averaged over all different orders. For large , random permutations can be sampled to estimate . From equation (2) we see that Shapley value does not change if we add or subtract the same quantity from all . It can be convenient to make .

2.3 Shapley Value for Local Explanation

When we apply Shapley value to the black box function of the target data subject , we define a player as an input predictor . The presence of the player means that the value of is known to the black box function . Shapley additive explanation (SHAP) of Lundberg and Lee, (2017) uses the value function

The value of depends on the data distribution that is implicitly or explicitly assumed. Sundararajan and Najmi, (2020) and Kumar et al., (2020) give various definitions.

Interventional Shapley values assume that all combinations of input predictors are possible. That is, the inputs are functionally independent. Baseline Shapley (BS) (Sundararajan and Najmi,, 2020) defines the value function for a predictor set as

It replaces predictors one by one from baseline to subject value. KernelSHAP (Lundberg and Lee,, 2017) computes baseline Shapley value for a kernel regression approximation to , for computational efficiency. It also supports ABS, which like the quantitative input influence (QII) measure of Datta et al., (2016) assumes statistically independent predictors, using the empirical margins.

Conditional Shapley values such as cohort Shapley allow for predictor variable dependence. When the similarity measures are all identity, then cohort Shapley, defined below, is equivalent to the Conditional Expectation Shapley of Sundararajan and Najmi, (2020) on the empirical distribution of the data, denoted . Cohort Shapley extends with similarity measures to better handle continuous variables. CondKernelSHAP (Aas et al.,, 2019) implements conditioning using kernel weights derived from the Mahalanobis distance and optionally restricted to -nearest neighbor points only.

3 Cohort Shapley

The cohort Shapley measure designates subjects as similar or not similar to the target subject for each of predictors. Then for each subset of predictors, there is a set of subjects similar to the target for all of those predictors. We call these subsets cohorts. The cohorts are not empty because they all include subject . Cohort Shapley value is Shapley value applied to cohort means. First we describe similarity.

3.1 Similarity

For each predictor , we define a target-specific similarity function . If , then subject is considered to be similar to subject as measured by predictor . Otherwise means that subject is dissimilar to subject for predictor . We always have . The simplest similarity is identity:

which is reasonable for binary predictors or those taking a small number of levels. For real-valued predictors, there may be no with and then we might instead take

where subject matter experts have chosen . Taking recovers the identity measure of similarity. The two similarity measures above generate an equivalence relation on , if does not depend on . In general, we do not need to be an equivalence. For instance, we do not need and would not necessarily have that if we used relative distance to define similarity, via

In some settings equivalence is a useful simplification.

3.2 Cohorts of

We use to define our set of subjects. Let

with by convention. Then is the cohort of subjects that are similar to the target subject for all predictors but not necessarily similar for any predictors . These cohorts are never empty, because we always have . We write for the cardinality of the cohort. As the cardinality of increases, the cohort focuses in on the target subject.

Given a set of cohorts, we define cohort averages

Then the value of set is

where . The last equality follows because the cohort with is the whole data set. The total value to be explained is

It may happen that is the singleton . In that case, the total value to be explained is . In this and other settings, some of the value may be the average of a very small number of subjects’ predictions, and potentially poorly determined but much better determined than points that are extreme extrapolations or are even impossible.

3.3 Importance Measures

Equation (2) yields cohort Shapley values

Here is the difference that refining on predictor makes when we have already refined on the predictor set .

4 Disaggregation of Global Importance

We use Shapley value for local explanation because it uses no impossible data combinations. Here we show that the Shapley effects of Song et al., (2016) can be disaggregated into a local squared cohort Shapley effect, when the predictors are given their empirical distribution.

Shapley effects arise from a value function . When has independent components, then Owen, (2014) shows that the Shapley value for is

| (3) |

but the dependent data case is much harder.

We may write the value function as

where is the probability density function of and we retain the same notation for discrete . We take to be the empirical distribution of the data set coarsened by a similarity function. Then represents the discrete distribution on obtained by choosing subject uniformly at random from the cohort . Then under ,

We also have for this . Finally, places equal probability on the data and so

Next, in addition to ordinary cohort Shapley with value function we introduce a squared version with

Then,

| (4) |

From the additivity axiom of Shapley value, the variance explained Shapley value is the average of the squared version of cohort Shapley value ,

| (5) |

The point of equations (4) and (5) is that squared values give an aggregation/disaggregation between local and global measures that satisfies the Shapley axioms. Unsquared Shapley values, whether baseline or cohort, give uninteresting aggregate Shapley values of zero.

5 Comparison of Shapley Value Importance

Here we compare importances of three Shapley values, BS, ABS, and CS. For BS, the baseline is . For ABS, all subjects are used for the baselines. We also define squared versions. Here, for simplicity, we assume no other subject matches the target on all predictors. Then the total value function of CS and its squared version are

The value functions of BS and its squared difference version are

Now if , as for instance it would be for linear and equal to the average of , then both and .

The value function of ABS and its squared difference version are defined as

We see that . We can also show that with equality when and only when for all , a very unlikely possibility. Thus, while ABS decomposes the same value that CS does, their squared counterparts decompose quite different quantities.

6 Derivation from Function Decomposition

Štrumbelj and Kononenko, (2010) derived a Shapley value under independent predictors uniformly distributed over finite discrete sets but they could as well be countable or continuous and non-uniform, so long as they are independent (see the appendix). We give a proof of this different from theirs, and show how both baseline Shapley value and cohort Shapley value are derived from functional decompositions.

6.1 Importance Measures

For Shapley value, every variable is either ‘in’ or ‘out’, and so binary variables underlie the approach. Here we compute Shapley values based on function decompositions of a function defined on . The values of that function might themselves be expectations, like the cohort mean in cohort Shapley or the quantity Štrumbelj and Kononenko, (2010) use (see the appendix), but for our purposes here they are just numbers.

We use to represent the binary vector of length with a one in position and zeroes elsewhere. This is the ’th standard basis vector. We then generalize it to for . An arbitrary point in is denoted by .

Let be a function on . In our applications, the total value to be explained is , with corresponding to matching the target in all ways and corresponding to no matches at all. The value contributed by is .

6.2 Shapley Value via Anchored Decomposition

Because we use the anchored decomposition for functions on instead of the ANOVA, we do not need to define a distribution for . The anchored decomposition on with anchor has a simple structure.

Lemma 1.

For integer , let have the anchored decomposition with anchor . Then , where .

Proof.

See the appendix. ∎

Now we find the Shapley value for a function on in an anchored decomposition. Štrumbelj and Kononenko, (2010) proved this earlier using different methods.

Theorem 1.

Let have the anchored decomposition with terms for . Let the set contribute value . Then the total value is , and the Shapley value for variable is

| (6) |

Proof.

We give a purely combinatorial proof of this result, using the hockey-stick identity, in our appendix. ∎

6.3 Baseline, Cohort and Variance Shapley

For and the function for baseline Shapley is

The corresponding function for cohort Shapley is

In variance Shapley . It is Shapley value applied to the anchored decomposition of where the values are in turn defined through an ANOVA decomposition.

7 Examples

In this section we include some numerical examples of cohort Shapley. First we look at variables that predict survival in the Titanic data set. Then we look at the variables that predict value in the Boston housing data set.

7.1 Titanic Data

Here we consider a subset of the Titanic passenger data set (from http://biostat.mc.vanderbilt.edu/wiki/pub/Main/DataSets/titanic3.csv) containing 1045 individuals with complete records. This data was collected from Encyclopedia Titanica (https://www.encyclopedia-titanica.org/) and has been used by Kaggle (see https://www.kaggle.com/c/titanic/data) to illustrate machine learning. As the function of interest, we construct a logistic regression model which predicts ‘survival’ based on the predictors ‘pclass’, ‘sex’, ‘age’, ‘sibsp’, ’parch’, and ‘fare’ (defined at the Vanderbilt web site). Our logistic model outputs an estimated probability of survival, . To calculate the cohort Shapley values, we define similarity as exact for the discrete predictors ‘pclass’, ‘sex’, ‘sibsp’, and ‘parch’ and within a distance of less than 1/10 of the variable range on the continuous predictors ‘age’ and ‘fare’.

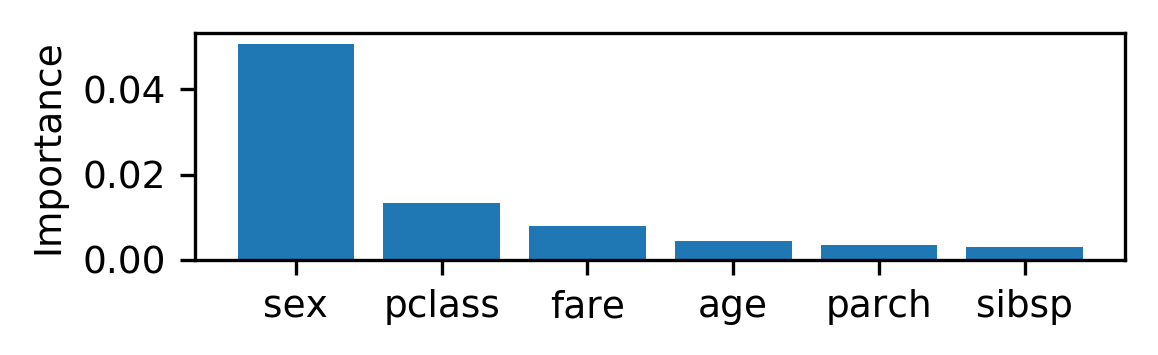

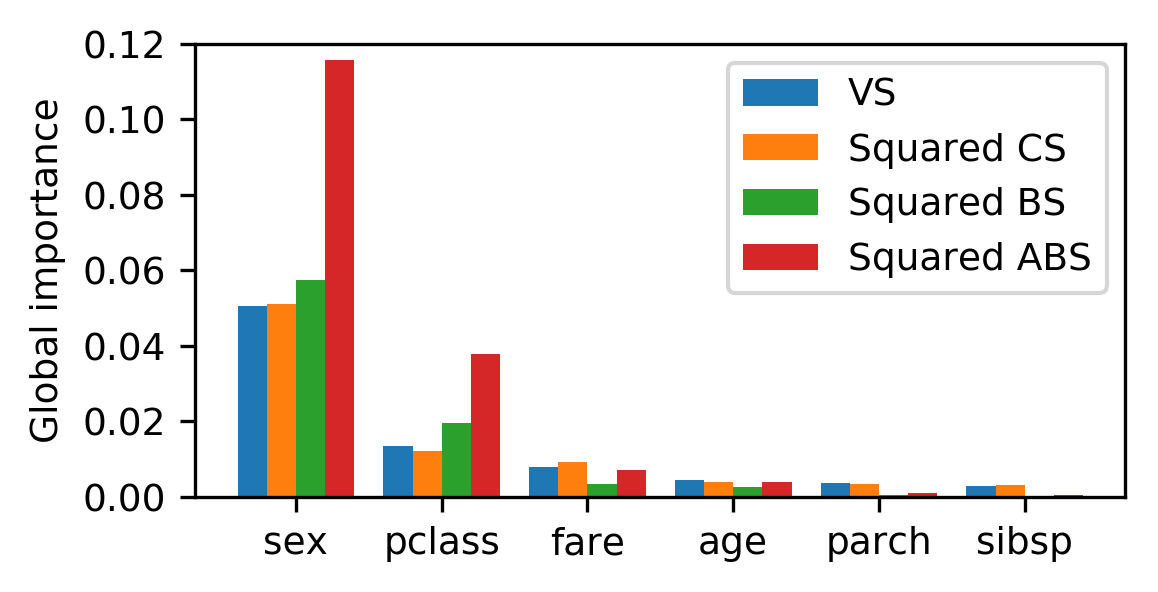

Figure 1 shows the variance Shapley values, known as ‘Shapley effects’ (Song et al.,, 2016). They decompose the total variance into importance of predictor variables. The results indicate that ‘sex’ is the most important followed by ‘pclass’, and ‘fare’.

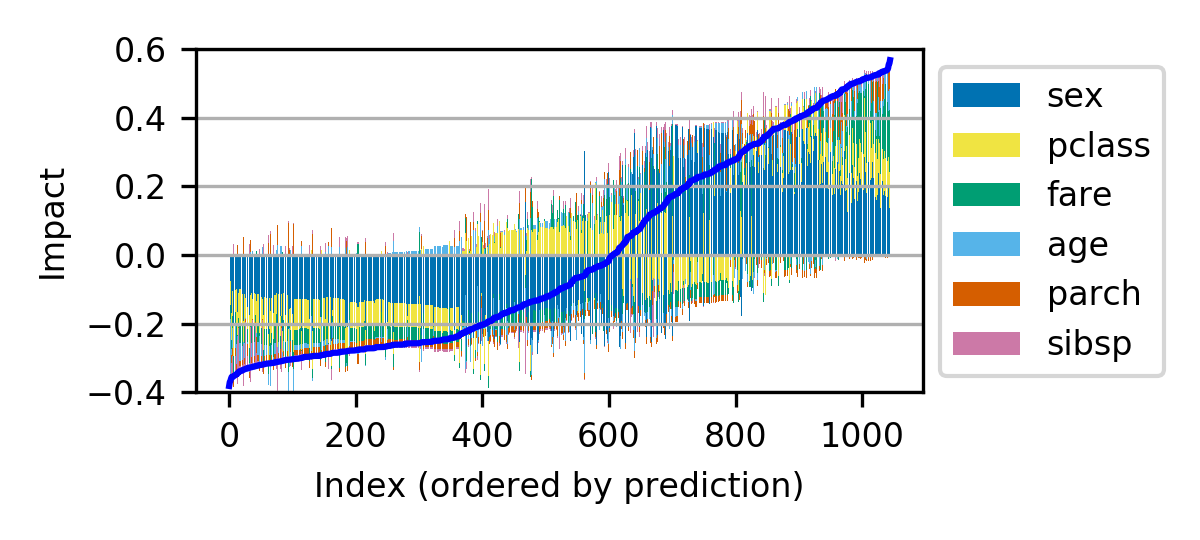

Figure 2 shows the cohort Shapley values for each predictor stacked vertically for every individual. The individuals are ordered by their predicted survival probability. Starting at zero, we plot a blue bar up or down according to the cohort Shapley value for the ‘sex’ variable. Then comes a yellow bar for ‘pclass’ and so on. The squared version of the cohort Shapley is a decomposition of Variance Shapley in Figure 1. For a comparison of cohort, baseline, all baseline Shapley values, and for their squared versions, see the appendix.

A visual inspection of Figure 2 reveals clusters of individuals with similar Shapley values for which we could potentially develop a narrative. As just one example, we see passengers with indices between roughly 400 and 600 who have negative Shapley values for ‘sex’ but positive Shapley values for ‘pclass’ while their predicted value is below the mean. Many of the these passengers are men who are not in the lowest class.

7.2 Boston Housing Data

The Boston housing dataset has 506 data points with 13 predictors and the median house value as a response (Harrison and Rubinfeld,, 1978). Each data point corresponds to a vicinity in the Boston area. We fit a regression model to predict the house price from the predictors using XGBoost (Chen and Guestrin,, 2016).

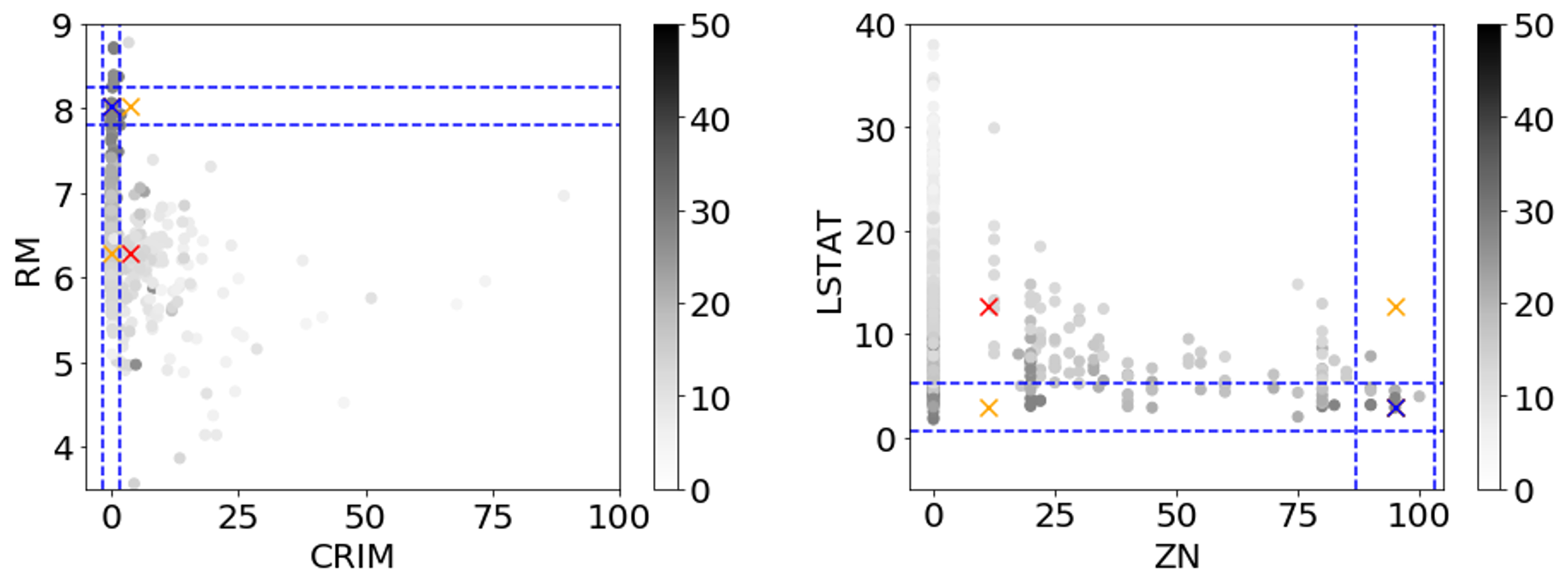

This dataset is of interest to us because it includes some striking examples of dependence in the predictors. For instance, the variables ‘CRIM’ (a measure of per capita crime) and ‘ZN’ (the proportion of lots zoned over 25,000 square feet) can be either near zero or large, but none of the 506 data points have both of them large and similar phenomena can be seen in some other scatterplots.

We will compute baseline Shapley and cohort Shapley for one target point. That one is the 205’th case in the sklearn python library and also in the mlbench R package. This target was chosen to be one for which some synthetic points in baseline Shapley would be far from any real data, but we did not optimize any criterion measuring that distance, and many of the other 506 points share that property. For Shapley values of all subjects, see the appendix. For cohort Shapley, we consider predictor values to be similar if their distance is less than 1/10 of the difference between the 95’th and 5’th percentiles of the predictor distribution.

Figure 3 shows two scatterplots of the Boston housing data. It marks the target and baseline points, depicts the cohort boundaries and it shows housing value in gray scale. The baseline point is , the sample average, and it is not any individual subject’s point partly because it averages some integer valued predictors. Here, the predicted house prices are 28.38 for the subject and 13.43 for the baseline. The figure also shows some of the synthetic points used by baseline Shapley. Some of those points are far from any real data points even in these two dimensional projections. Model fits at such points are questionable.

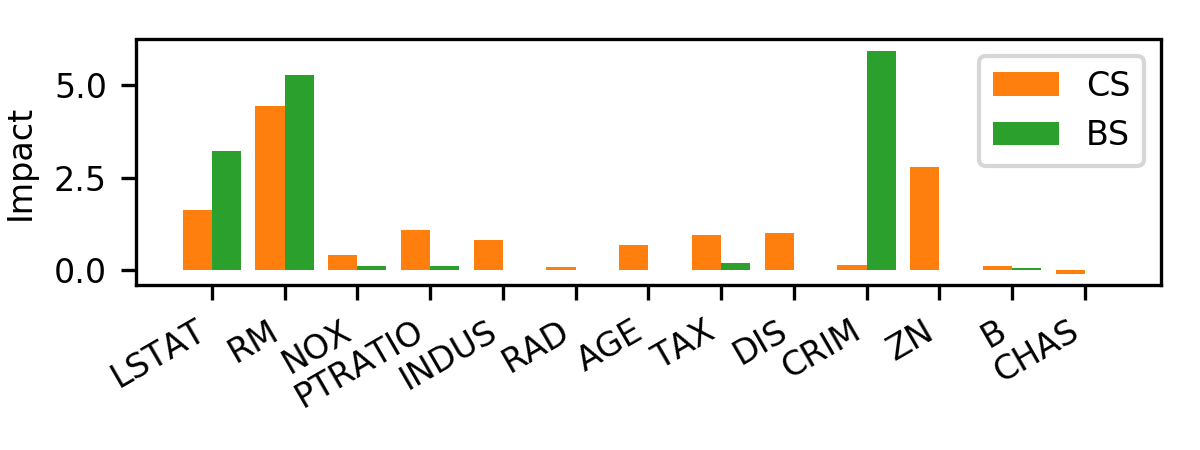

Figure 4 shows cohort Shapley and baseline Shapley values for this target subject. On baseline Shapley, we see that ‘CRIM’, ‘RM’, and ‘LSTAT’ have very large impact and the other variables do not. For cohort Shapley, the most impactful predictors are ‘RM’, ‘ZN’ and ‘LSTAT’ followed by a very gradual decline.

In baseline Shapley ‘CRIM’ was the most important variable, while in cohort Shapley it is one of the least important variables. We think that the explanation is from the way that baseline Shapley uses the data values at the upper orange cross in the left plot of Figure 3. The predicted price for a house at the synthetic point given by the upper orange cross is 14.17, which is much smaller than that of the subject, and even quite close to the baseline mean. This leads to the impact of ‘CRIM’ being very high. Data like that synthetic point were not present in the training set and so that value represents an extrapolation where we do not expect a good prediction. We believe that an unreliable prediction there gave the extreme baseline Shapley value that we see for ‘CRIM’.

Related to the prior point, refining the cohort on ‘RM’ reduces its cardinality much more than refining the cohort on ‘CRIM’ does. Because cohort Shapley uses averages of actual subject values, refining the target on ‘CRIM’ removes fewer subjects and in this case makes a lesser change.

The right panel in Figure 3 serves to illustrate the effect of dependent predictors on cohort Shapley value. The model for price hardly uses ‘ZN’, if at all, and the baseline Shapley value for it is zero. Baseline Shapley atributes a large impact to ‘LSTAT’ and nearly none to ‘ZN’. For either of those predictors, the cohort mean is higher than the global average, and both ‘LSTAT’ and ‘ZN’ have high impact in cohort Shapley.

We can explain the difference as follows. As ‘ZN’ increases, the range of ‘LSTAT’ values narrows, primarily by the largest ‘LSTAT’ values decreasing as ‘ZN’ increases. Refining on ‘ZN’ has the side effect of lowering ‘LSTAT’. Even if ‘ZN’ itself is not in the model, the cohort Shapley value captures this effect. Baseline Shapley cannot impute a nonzero impact for a variable that the model does not use.

8 Discussion

Cohort Shapley resolves two conceptual problems in baseline Shapley and other interventional methods. First, it does not use any impossible or even unseen predictor combinations. Second, if two predictors are identical then it is perfectly predictable that their importances will be equal rather than subject to details of which black box model was chosen or what random seed if any was used in fitting that model. Cohort Shapley also allows the user to study indirect influence which is impossible via baseline Shapley.

It does not escape the catch-22 that Kumar et al., (2020) mention. Cohort Shapley requires the user to specify a distribution on predictors. That distribution is the empirical distribution coarsened by a similarity definition. The importance measure will depend on the chosen similarity measure which can be an advantage but may also be a burden. Baseline Shapley and cohort Shapley have different counterfactuals and they address different problems.

There is a related literature on how finely a continuous variable should be broken into categories. Gelman and Park, (2009) suggest as few as three levels for the related problem of choosing a discretization prior to fitting a model. We have used more levels but this remains an area for future research.

Cohort Shapley supports another choice not possible with baseline Shapley. We can replace the function values by the original response values in the cohort averages. The resulting sensitivity measures are for a similarity-based nearest neighbor rule.

In our appendix we investigate numerically the proportion of unrealistic data points created when sampling independently from marginal distributions. Using a working definition of ‘realistic’ we find that marginal sampling produces many more unrealistic values than one gets in hold out data sets.

Ethics Statement

Our cohort Shapley method can be used to detect unethical practices such as redlining, even when the protected variable or variables were not used in the prediction model. We take care to point out that a large cohort Shapley value for a protected variable is not in itself proof of redlining. Followup investigations would be required to reach that conclusion.

Acknowledgments

We thank Masashi Egi of Hitachi for valuable comments. This work was supported by the U.S. National Science Foundation under grant IIS-1837931.

References

- Aas et al., (2019) Aas, K., Jullum, M., and Løland, A. (2019). Explaining individual predictions when features are dependent: More accurate approximations to shapley values. arXiv preprint arXiv:1903.10464.

- Adler et al., (2018) Adler, P., Falk, C., Friedler, S. A., Nix, T., Rybeck, G., Scheidegger, C., Smith, B., and Venkatasubramanian, S. (2018). Auditing black-box models for indirect influence. Knowledge and Information Systems, 54(1):95–122.

- Aliş and Rabitz, (2001) Aliş, Ö. F. and Rabitz, H. (2001). Efficient implementation of high dimensional model representations. Journal of Mathematical Chemistry, 29(2):127–142.

- Chen and Guestrin, (2016) Chen, T. and Guestrin, C. (2016). Xgboost: A scalable tree boosting system. In Proceedings of the 22Nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, KDD ’16, pages 785–794, New York, NY, USA. ACM.

- Datta et al., (2016) Datta, A., Sen, S., and Zick, Y. (2016). Algorithmic transparency via quantitative input influence: Theory and experiments with learning systems. In 2016 IEEE symposium on security and privacy (SP), pages 598–617. IEEE.

- Gamboa et al., (2016) Gamboa, F., Janon, A., Klein, T., Lagnoux, A., and Prieur, C. (2016). Statistical inference for Sobol’ pick-freeze Monte Carlo method. Statistics, 50(4):881–902.

- Gelman and Park, (2009) Gelman, A. and Park, D. K. (2009). Splitting a predictor at the upper quarter or third and the lower quarter or third. The American Statistician, 63(1):1–8.

- Harrison and Rubinfeld, (1978) Harrison, D. and Rubinfeld, D. L. (1978). Hedonic prices and the demand for clean air. Journal of Environmental Economics and Management, 5:81–102.

- Hoeffding, (1948) Hoeffding, W. (1948). A class of statistics with asymptotically normal distribution. Annals of Mathematical Statistics, 19:293–325.

- Jiang and Owen, (2003) Jiang, T. and Owen, A. B. (2003). Quasi-regression with shrinkage. Mathematics and Computers in Simulation, 62(3-6):231–241.

- Kumar et al., (2020) Kumar, I. E., Venkatasubramanian, S., Scheidegger, C., and Friedler, S. (2020). Problems with Shapley-value-based explanations as feature importance measures. In The 37th International Conference on Machine Learning (ICML 2020).

- Kuo et al., (2010) Kuo, F., Sloan, I., Wasilkowski, G., and Woźniakowski, H. (2010). On decompositions of multivariate functions. Mathematics of computation, 79(270):953–966.

- Lundberg and Lee, (2017) Lundberg, S. M. and Lee, S.-I. (2017). A unified approach to interpreting model predictions. In Advances in Neural Information Processing Systems, pages 4765–4774.

- Molnar, (2018) Molnar, C. (2018). Interpretable machine learning: A Guide for Making Black Box Models Explainable. Leanpub.

- Owen, (2013) Owen, A. B. (2013). Variance components and generalized Sobol’ indices. Journal of Uncertainty Quantification, 1(1):19–41.

- Owen, (2014) Owen, A. B. (2014). Sobol’ indices and Shapley value. Journal on Uncertainty Quantification, 2:245–251.

- Owen and Prieur, (2017) Owen, A. B. and Prieur, C. (2017). On Shapley value for measuring importance of dependent inputs. SIAM/ASA Journal on Uncertainty Quantification, 5(1):986–1002.

- Ribeiro et al., (2016) Ribeiro, M. T., Singh, S., and Guestrin, C. (2016). Why should I trust you?: Explaining the predictions of any classifier. In Proceedings of the 22nd ACM SIGKDD international conference on knowledge discovery and data mining, pages 1135–1144, New York. ACM.

- Saltelli et al., (2008) Saltelli, A., Ratto, M., Andres, T., Campolongo, F., Cariboni, J., Gatelli, D., Saisana, M., and Tarantola, S. (2008). Global Sensitivity Analysis. The Primer. John Wiley & Sons, Ltd, New York.

- Shapley, (1952) Shapley, L. S. (1952). A value for n-person games. Technical report, DTIC Document.

- Sobol’, (1969) Sobol’, I. M. (1969). Multidimensional Quadrature Formulas and Haar Functions. Nauka, Moscow. (In Russian).

- Sobol’, (1993) Sobol’, I. M. (1993). Sensitivity estimates for nonlinear mathematical models. Mathematical Modeling and Computational Experiment, 1:407–414.

- Sobol’, (2003) Sobol’, I. M. (2003). Theorems and examples on high dimensional model representation. Reliability Engineering & System Safety, 79(2):187–193.

- Song et al., (2016) Song, E., Nelson, B. L., and Staum, J. (2016). Shapley effects for global sensitivity analysis: Theory and computation. SIAM/ASA Journal on Uncertainty Quantification, 4(1):1060–1083.

- Štrumbelj and Kononenko, (2010) Štrumbelj, E. and Kononenko, I. (2010). An efficient explanation of individual classifications using game theory. Journal of machine learning research, 11:1–18.

- Štrumbelj and Kononenko, (2014) Štrumbelj, E. and Kononenko, I. (2014). Explaining prediction models and individual predictions with feature contributions. Knowledge and information systems, 41(3):647–665.

- Sundararajan and Najmi, (2020) Sundararajan, M. and Najmi, A. (2020). The many Shapley values for model explanation. In The 37th International Conference on Machine Learning (ICML 2020).

Appendix 1 Approach of Štrumbelj and Kononenko, (2010)

To get a Shapley value for predictor variables, we must first define the value produced by a subset of them. The approach of Štrumbelj and Kononenko, (2010) begins with a vector of independent random predictors from some distribution . They used independent predictors uniformly distributed over finite discrete sets but they could as well be countable or continuous and non-uniform, so long as they are independent. For a target subject , let be the prediction for that subject. They define the value of the predictor set by

with expectations taken under a random baseline . The distribution has independent components. In words, is the expected change in our predictions at a random point that comes from specifying that for , while leaving for .

In their formulation, the total value to be explained is

the extent to which differs from a hypothetical average prediction over independent predictors. The subset explains , and from that they derive Shapley value. They define quantities via and

They prove that the Shapley value for predictor is

We give a proof of this, different from theirs, making use of the anchored decomposition. While their is defined via expectations of independent random variables, their Shapley value comes via the anchored decomposition, applied to those expectations, not an ANOVA.

Appendix 2 Proof of Lemma 1

Proof.

The inclusion-exclusion formula for the binary anchored decomposition, using is

Suppose that for . Then, splitting up the alternating sum

because and are the same point when . It follows that if does not hold.

Now suppose that . First because only depends on through . From we have . Then , completing the proof. ∎

Appendix 3 Proof of Theorem 1

Proof.

The proof in Štrumbelj and Kononenko, (2010) proceeds by substituting the inclusion-exclusion identity into the first expression for in (6) and then showing that it is equal to the definition of Shapley value. They also need to explain some of their steps in prose and the version above provides a more ‘mechanical’ alternative approach.

Appendix 4 Comparison of Shapley Values

Here we compare local and global versions of several Shapley value measures for the Titanic and Boston housing data sets. We include baseline, all baseline and cohort Shapley values as well as their squared versions. We also calculate variance Shapley values and squared local Shapley values aggregated over all subjects for global sensitivity analysis.

Titanic Data

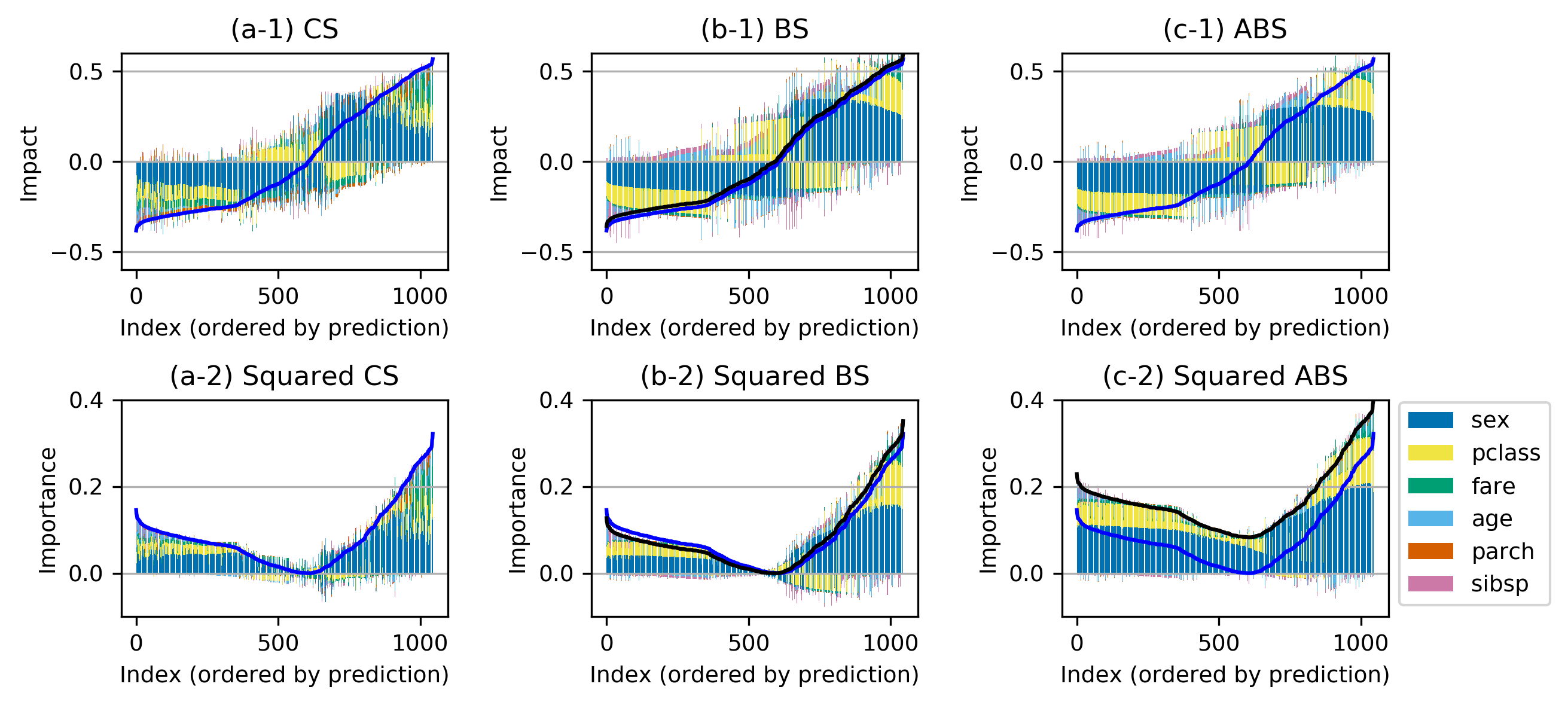

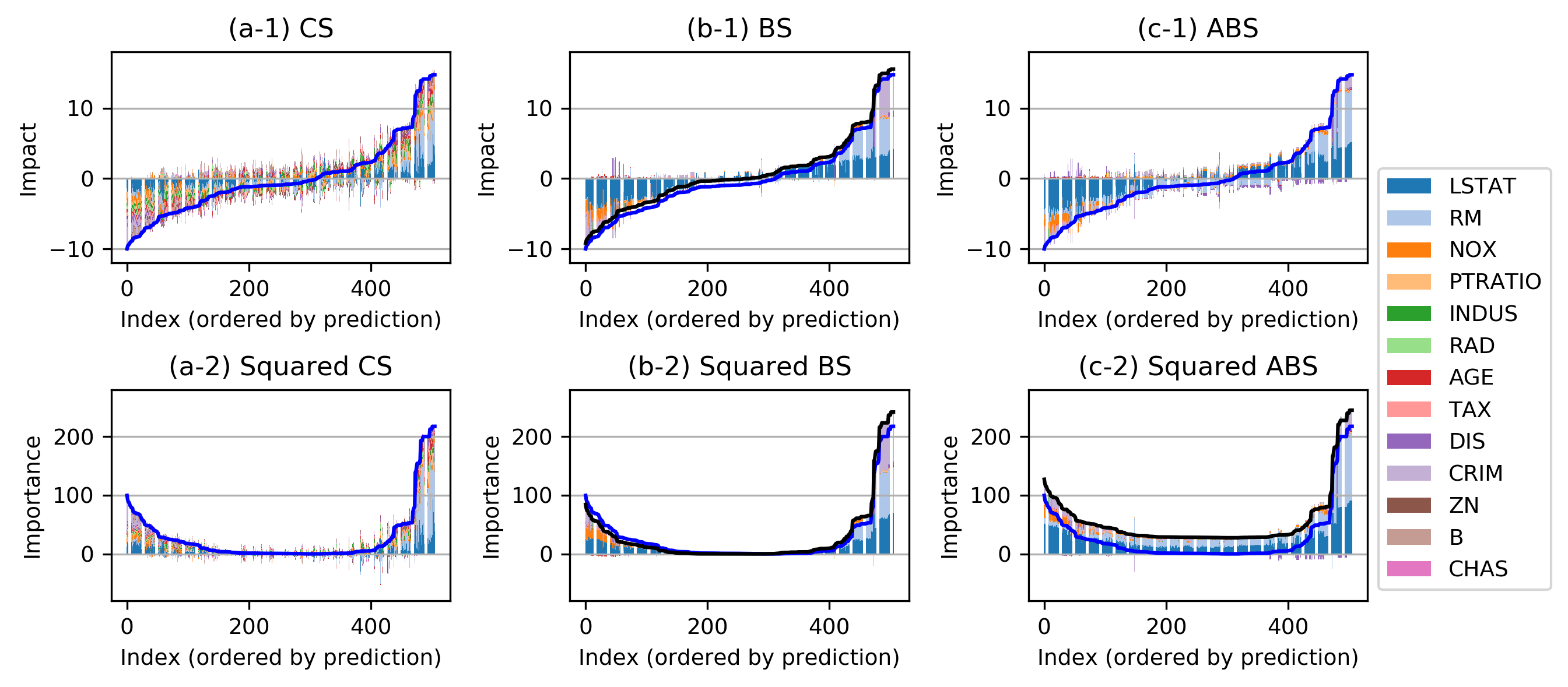

Figure 5 shows the comparison of local Shapley values including cohort Shapley (CS), baseline Shapley (BS), and all baseline Shapley (ABS) and their squared versions. Each figure shows the Shapley value for each predictor stacked vertically for individual subjects arranged along the horizontal axis. The subjects are ordered by their predicted values. The black overlay is the sum of predictor contributions for each individual subject. The blue overlay represents the sum of cohort Shapley values for comparison.

For computation of Shapley values on all 1045 data subjects using a desktop PC with an Intel Core i7-8700 CPU, it spent for CS, for BS, and for ABS, respectively.

Comparing CS (a-1) and squared CS (a-2), the sign of each predictor is flipped whenever the total impact in CS is negative. The negative importance in squared CS is counter-intuitive but it indicates the predictor negatively affects the prediction outcome for each individual level the same as in the non-squared version of CS.

BS (b-1) and squared BS (b-2) sum to different values than CS (a-1) and squared CS (a-2), respectively, due to the difference between and . Comparing BS and CS, CS attributes significant importance to ‘fare’ for subjects with high and low prediction, but BS does not and the contribution of ‘sex’ is reduced for these subjects.

Squared ABS (b-2) sums to much larger values for each subject compared with cohort Shapley and baseline Shapley while non-squared ABS (c-1) looks nearly equivalent to BS (b-1).

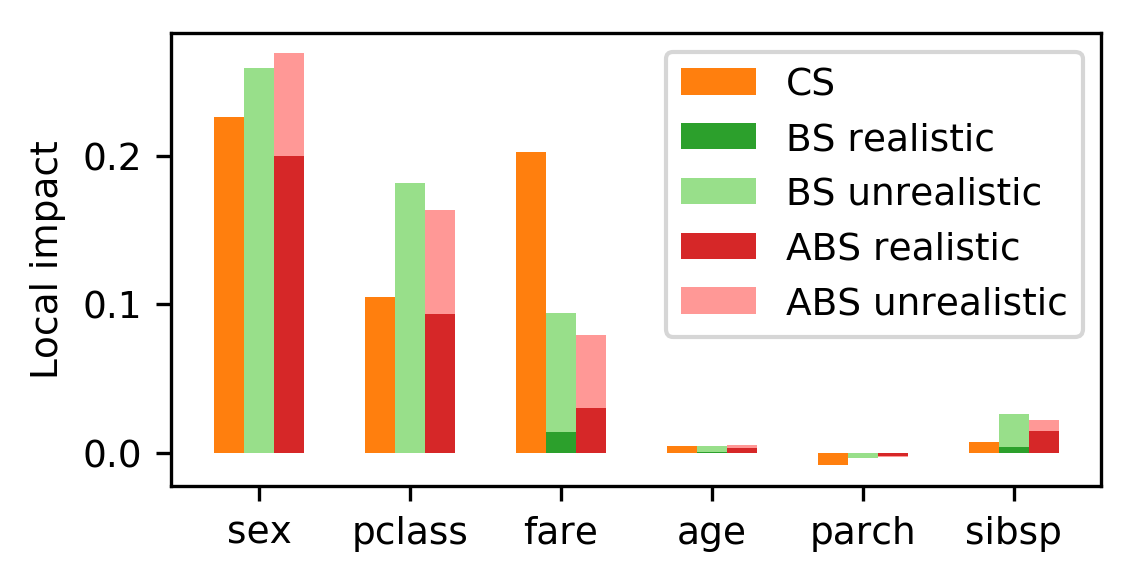

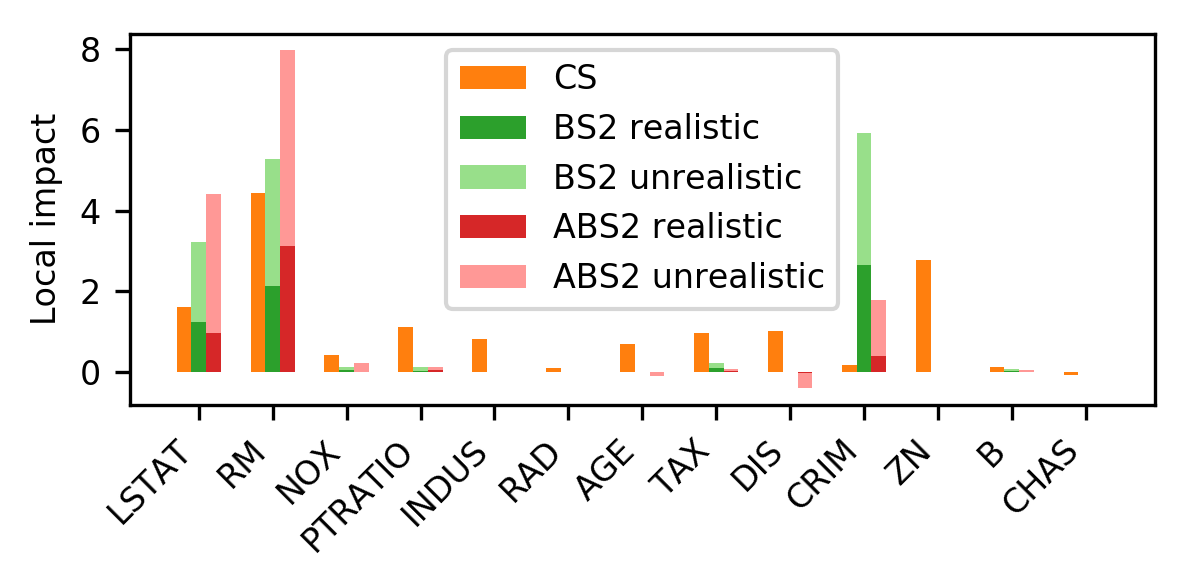

Figure 6 decomposes the importance measures into their contributions from ‘realistic’ and ‘unrealistic’ differences among synthetic data points. It is a local comparison for the first point in the data set, i.e., . Our working definition of what makes a feature combination unrealistic is discussed later. The figure indicates that a substantial proportion of the BS value is derived from unrealistic data values. The baseline point is the average of predictors, taken over all subjects. Note that some components of the average are already not realistic; for instance the averages of the binary variable ‘sex’ and categorical variable ‘pclass’. In addition to unrealistic levels there are also unrealistic combinations. The ABS by comparison has a much lower impact from unrealistic sampling because it makes comparisons to actual points. Even if the unrealistic contributions are distributed to other predictors, the top two predictors ‘sex’ and ‘pclass’ will not change. ABS samples only existing values in each predictor. Through replacing predictor from one subject to another subject, it sometimes goes to unrealistic combination, but that was rare in the Titanic data set.

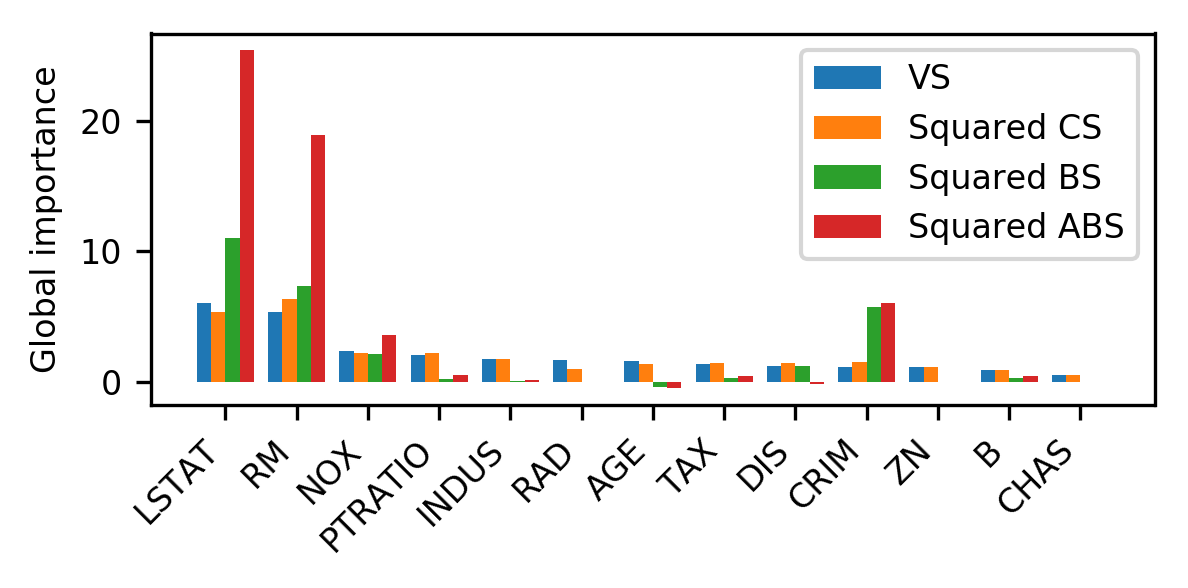

Figure 7 shows the comparison of aggregated squared Shapley values. Squared CS is theoretically equivalent to variance Shapley (VS), though we see small numerical differences. Compared to VS, BS overestimates the impact of ‘pclass’ and ‘sex’, and underestimates that of ‘sibsp’ and ‘parch’. ABS exaggerates this tendency and the importance estimate becomes nearly double that of CS.

Boston Housing Data

Figure 8 shows the comparison of local Shapley values including cohort Shapley (CS), baseline Shapley (BS) and their squared versions. Each figure shows the Shapley value for each predictor stacked vertically for every individual in horizontal axis. The individuals are ordered by their prediction. The black overlay is the sum of predictor contributions for each individual subject. The blue overlay represents the sum of cohort Shapley values for comparison.

For computation of Shapley values on all 506 data subjects using a desktop PC with an Intel Core i7-8700 CPU, it spent for CS, for BS, and for ABS, respectively.

The variance Shapley later shown in Figure 10 is decomposed into squared CS for individual subjects in Figure 8(a-2). Comparing BS (b-1) and CS (a-1), BS attributes most importance to ‘STAT’, ‘RM’, ’CRIM’ and ‘NOX’ while CS attributes importance to more predictors.

Figure 9 decomposes the local importance measures for subject into their contributions from ‘realistic’ and ‘unrealistic’ differences among synthetic data points. The figure indicates that a substantial proportion of the BS value is derived from unrealistic data values. The baseline point is the average of predictors, taken over all subjects. In the Boston housing data, all predictors are continuous so that unrealistic samples are all due to unrealistic combinations.

Figure 10 shows the comparison of aggregated squared Shapley values. As we saw, squared CS is equivalent to variance Shapley (VS). But BS places much greater importance on ‘LSTAT’, ‘RM’, and ‘CRIM’ that is observed in visual inspection of Figure 8(b-1)(b-2).

Appendix 5 Calibration of Distance Threshold in Realistic Sampling Analysis

Baseline Shapley occasionally includes unrealistic input data where the model output is questionable. This arises because the underlying distribution is the product of empirical marginal distributions. Here, we study the prevalence of unrealistic data samples.

We generate data samples with independent components using the joint marginal distributions in a real world data set. A sample point is “realistic” if there is a subject to which it is similar in all predictors. Otherwise it is “unrealistic”. We used the similarity measure defined in the Similarity section in this paper. Then, we measure the proportion of “realistic” data samples to quantify the reliability. We used the distance based similarity function, varying the threshold in to explore the effect of the threshold choice.

A standard technique in machine learning is to hold out data and investigate how well predictions generalize. This motivates comparing the realism of sampling independently from marginal distributions to sampling held out data. We compare training to test set percentages using holdouts of 10%, 20% and 30% of the data.

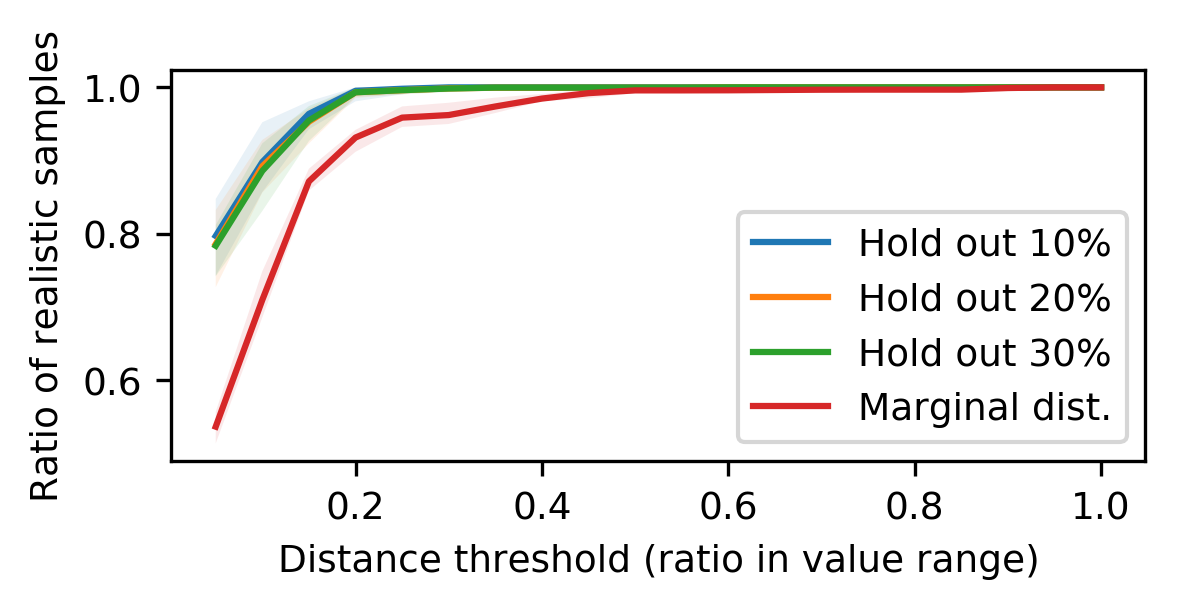

Figure 11 shows the resulting proportions of realistic samples when sampling from joint marginal distribution compared to held out data on the Titanic data set, averaged across runs. We see that held-out data score much higher realism rates than we get from independent sampling of the marginal distributions. There are only small differences as the hold-out fraction changes from % to 30%. At distance threshold held-out data are realistic 90 to 96 percent of the time, while marginal sampling generates only 86 percent realistic data.

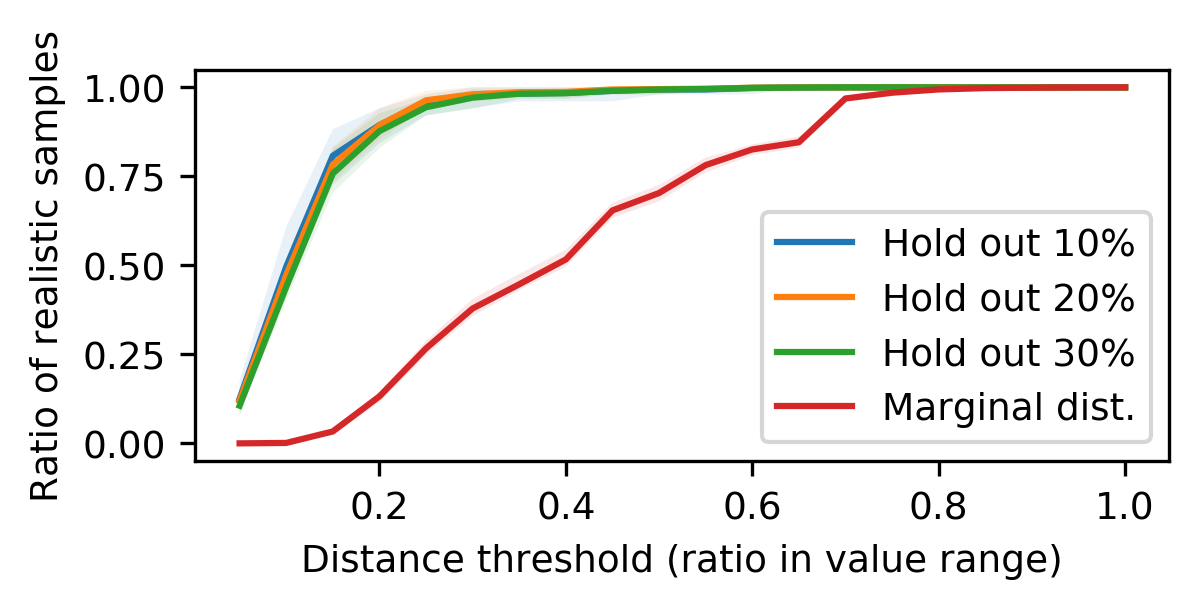

Figure 12 shows the evaluation results on Boston housing data set, averaged across runs. Once again, the proportion of realistic values does not depend strongly on the hold-out fraction and they are are over 90% at the distance threshold of 0.2. The gap between train-test splitting and marginal distribution sampling is much larger compared with the Titanic data. Only about 13% of the marginal distribution samples are realistic. This is partly to be expected because there are more predictor variables. Furthermore the strongly patterned bivariate distributions in this data serve to make for unrealistic combinations.