∎

Große Scharrnstraße 59

15230 Frankfurt (Oder), Germany

Cross-validated covariance estimators for

high-dimensional minimum-variance portfolios

Abstract

The global minimum-variance portfolio is a typical choice for investors because of its simplicity and broad applicability. Although it requires only one input, namely the covariance matrix of asset returns, estimating the optimal solution remains a challenge. In the presence of high-dimensionality in the data, the sample covariance estimator becomes ill-conditioned and leads to suboptimal portfolios out-of-sample. To address this issue, we review recently proposed efficient estimation methods for the covariance matrix and extend the literature by suggesting a multi-fold cross-validation technique for selecting the necessary tuning parameters within each method. Conducting an extensive empirical analysis with four datasets based on the S&P 500, we show that the data-driven choice of specific tuning parameters with the proposed cross-validation improves the out-of-sample performance of the global minimum-variance portfolio. In addition, we identify estimators that are strongly influenced by the choice of the tuning parameter and detect a clear relationship between the selection criterion within the cross-validation and the evaluated performance measure.

JEL classification G10 G11 C13 C80

Keywords:

Covariance Estimation Portfolio Optimization High-dimensionality Cross-validation1 Introduction

Based on the simple but essential idea of diversification and optimal risk-return profile of an investment strategy, the mean-variance model by Markowitz (1952) still represents the groundwork for portfolio optimization. In its original design, Markowitz portfolio theory assumes perfect knowledge about the expected value and variance of returns. For practical implementations, however, these parameters have to be estimated from historical data. The misspecifications due to error in estimation can lead to strong deviations from optimality and therefore an inferior out-of-sample performance (Jobson and Korkie 1981, Frost and Savarino 1986, Michaud 1989, Broadie 1993). This major drawback has been tackled from different perspectives in the financial literature. Some focus on estimation errors in the portfolio weights directly (see, e.g., Brodie et al. 2009, DeMiguel et al. 2009a), whereas others work on the inputs by improving expected returns and the covariance matrix.

In particular, portfolio weights are extremely sensitive to changes in expected returns (Best and Grauer 1991b, a), which in turn are more difficult to estimate than the covariances of returns (Merton 1980). It is therefore not surprising that a considerable part of recent academic research focuses on the global minimum-variance portfolio (GMV), as this does not depend on expected returns.111DeMiguel et al. (2009b) additionally show that the mean-variance portfolio is outperformed out-of-sample by the minimum-variance portfolio not only in terms of risk, but as well in respect to the return-risk ratio. However, even if investors decide to use the global minimum-variance portfolio, the estimation errors associated with the covariances can still lead to significant estimation errors in the portfolio weights, especially in a high-dimensional scenario.

We cover several approaches that have been shown to overcome these estimation issues and perform well in terms of out-of-sample variance. For instance, we discuss the linear shrinkage estimators of Ledoit and Wolf (2004a, b) designed to offer an optimal bias-variance trade-off between the sample covariance matrix and a structured target matrix. Furthermore, we adopt the recent nonlinear shrinkage technique by Ledoit and Wolf (2017) that is proven to be optimal under a variety of financially relevant loss functions (Ledoit and Wolf 2018b). Since an underlying factor structure is considered a valid assumption for asset returns’ covariance estimators, we outline the elaborate principal orthogonal complement thresholding (POET) estimator by Fan et al. (2013). In addition, we follow the findings of the recent empirical studies by Goto and Xu (2015) and Torri et al. (2019) and include a sparse precision matrix estimator, namely the graphical least absolute shrinkage and selection operator (GLASSO), which has so far received little attention in portfolio optimization research. To the best of our knowledge, we are the first to compare state-of-the-art covariance estimators such as the nonlinear shrinkage and POET with the GLASSO and to prove its significant outperformance in a high-dimensional scenario.

More importantly, the selected covariance estimation methods share one thing in common: a regularization of the sample covariance is performed to optimize its out-of-sample performance. For example, linear shrinkage methods need an optimal shrinkage intensity to balance the included variance and bias, whereas the performance of the GLASSO depends on the level of sparsity, induced by a penalty parameter. The procedure for optimally identifying those tuning parameters often includes the choice of a specific loss function to be minimized. As often advocated, a loss function or measure of fit in the model estimation is best aligned with the evaluation framework (Christoffersen and Jacobs 2004, Ledoit and Wolf 2017, Engle et al. 2019). To exploit those effects in more detail, we apply a nonparametric cross-validation (CV) technique with different selection criteria to determine the optimal parameters, necessary for the calculation of all the considered covariance estimators.

Since we focus on enhancing the risk profile of the GMV portfolios, we choose two relevant risk-related measures for our data-driven estimation methodology and the corresponding out-of-sample performance evaluation, namely the mean squared forecasting error (MSFE), as in Zakamulin (2015), and the out-of-sample portfolio variance. We show empirically that in most cases there exists a strong positive relation between the selection criterion within the CV and the respective out-of-sample performance measure. For instance, when the overall goal is to reduce the out-of-sample risk, then using CV with the portfolio variance as a measure of fit leads to lower risk than the original method. Similar results are documented by Liu (2014), although he only considers the most straight-forward linear shrinkage as in Ledoit and Wolf (2003, 2004a, 2004b). Here, we examine more recent and efficient estimation methods and identify those that can actually profit from a data-driven methodology. In detail, estimators that depend strongly on the choice of a specific tuning parameter within their derivation are more prone to be positively influenced by replacing the original solution with a data-driven one.

Our contributions to the current literature on the subject of covariance and precision matrix estimation within the portfolio optimization framework can be summarized as follows. First, we show that recent advances in methods for high-dimensional covariance estimation lead to strong improvements in the risk profile of the GMV. In this context, we emphasize the distinct and often significant outperformance of the GLASSO, which estimates sparse precision matrices by identifying pairs of zero partial auto-correlations in asset returns data. In line with the main discussion, we show that a model’s outperformance in respect to out-of-sample portfolio variance does coincide with an identical objective within the CV. Although the elaborate method outlined in Ledoit and Wolf (2017) is not strongly influenced by applying the CV procedure, all the other considered data-driven estimators perform better than their original counterparts. This advantage becomes even greater as the high-dimensionality of the data increases. Considering the MSFE, the results are straightforward for all estimation methods. If an investor aims to minimize this measure, the respective data-driven estimation ought to be performed. Nonetheless, we analyze the inefficiency of the MSFE for high-dimensional asset returns’ data, in particular, because of a distorted calculation of the realized covariance matrix. Finally, to test the robustness of our results, we examine the effects of the suggested methods on the GMV without short sales. As argued by Jagannathan and Ma (2003), a constraint imposed on short sales is similar to the linear shrinkage technique since it reduces the impact of estimation errors on optimal portfolio weights. Nevertheless, we show that a CV with the portfolio variance as a selection criterion slightly improves the out-of-sample risk even in this scenario.

The rest of paper is organized as follows: In Section 2, we review the considered covariance estimation methods and their properties. Section 3 outlines the suggested data-driven methodology in respect to its main characteristics: the cross-validation procedure, the parameter set, and the selection criteria. We describe the empirical study in Section 4 with a strong focus on the chosen dataset, methodology and performance measures. In Section 5, we discuss the performance of classical and constrained GMV portfolios and analyze in detail the influence of data-driven estimation among all considered datasets and methods. Section 6 summarizes the results and concludes.

2 Overview of the Estimation Methods

2.1 Sample Covariance

The standard approach for estimating the covariance matrix of returns among researchers and practitioners is to use the sample estimator, defined as

| (1) |

where is the matrix of past asset returns with observations and number of stocks, is the vector of expected returns, here estimated with the sample mean, and is an -dimensional vector of ones. As shown by Merton (1980), the sample covariance matrix is an asymptotically unbiased and consistent estimator of the true covariance matrix in terms of the Frobenius norm ´when the concentration ratio . For a large number of assets a concentration ratio of such magnitude is practically infeasible due to limited data availability and illiquidity issues. With a high relation of the number of assets to the sample size, also called high-dimensionality, the sample covariance and its inverse exhibit higher amount of estimation error, mainly due to the over- and underestimation of the respective eigenvalues. Moreover, for , the sample covariance becomes singular and the inverse cannot be calculated.

The sample estimator’s instability and possible singularity in case of high-dimensionality are a problem within the optimization of global minimum-variance portfolios, where the covariance matrix and, specifically, its inverse capture the dependency between asset returns and allow for the effect of diversification as a way of reducing risk. It is then straightforward that the accuracy of optimally estimated portfolio weights is directly related to the estimator’s precision. As a solution, several alternative estimators have been proposed in the literature.

2.2 Linear Shrinkage

To produce more stable estimators of the covariance matrix, a linear shrinking procedure can be applied to the sample estimator towards a more structured target matrix ,

where the constant controls the shrinkage intensity, which is set higher the more ill-conditioned the sample estimator is and vice versa. In contrast to the unbiased, but unstable sample covariance, a structured target matrix has little estimation error but tends to be biased. As a compromise, the convex combination of both uses the bias-variance trade-off by accepting more bias in-sample in exchange for less variance out-of-sample. This idea is central to the shrinkage methodology of Stein (1956) and James and Stein (1961). More recently, Ledoit and Wolf (2004b) propose a set of asymptotically optimal shrinkage estimators and specify the identity matrix as a generic target matrix if no specific covariance structure is assumed. The respective linear shrinkage estimator is calculated as

| (2) |

where is the average of all individual sample variances and is an optimal shrinkage intensity parameter. However, in the context of financial time series, it is beneficial to consider target matrices with reference to the correlation structure of asset returns.

Ledoit and Wolf (2004a) consider identical pairwise correlations between all assets. The target matrix is therefore derived under the constant correlation matrix model of Elton and Gruber (1973), so that . While the variances are kept as their original sample values, the off-diagonal entries of the target matrix are estimated by assuming a constant average sample correlation . This results in The corresponding estimator is defined as

| (3) |

The level of the shrinkage in Equations (2) and (3) can be obtained analytically. In particular, as shown by Ledoit and Wolf (2004a, b), asymptotically consistent estimators for the optimal linear shrinkage intensity are derived under the quadratic loss function

| (4) |

known as the Frobenius loss, where the covariance estimator is substituted with Equation (2) or (3). The finite sample solution is found at the minimum of the expected value of the Frobenius loss, namely the mean squared error (MSE),

| (5) |

The methodology behind this derivation can be applied to other shrinkage targets in a convex combination setting after an individually performed analysis and mathematical adaptation. Our data-driven implementation, however, can be implemented for any linear shrinkage without further modifications, since we do not rely on the theoretically derived shrinkage intensity; instead, we search for an optimal value using CV.

2.3 Nonlinear Shrinkage

The nonlinear shrinkage method, first proposed by Ledoit and Wolf (2012), shrinks covariance entries by increasing small (underestimated) sample eigenvalues and decreasing large (overestimated) ones in an individual fashion. Without any assumption about the true covariance matrix, the positive-definite rotationally equivariant222This class of estimators was first introduced by Stein (1986). nonlinear shrinkage is based on the spectral decomposition of the sample covariance matrix and defined as

| (6) |

where is the orthogonal matrix with the sample eigenvectors as columns and is the diagonal matrix of the sample eigenvalues , shrunk as shown in Ledoit and Wolf (2012, 2015, 2017, 2018a). To find the optimal nonlinear shrinkage to the eigenvalues, Ledoit and Wolf (2012) originally minimize the MSE in finite samples. Under the considered large-dimensional asymptotics from the field of Random Matrix Theory the Frobenius loss converges almost surely to a nonstochastic limit, guaranteeing the estimator’s optimality.

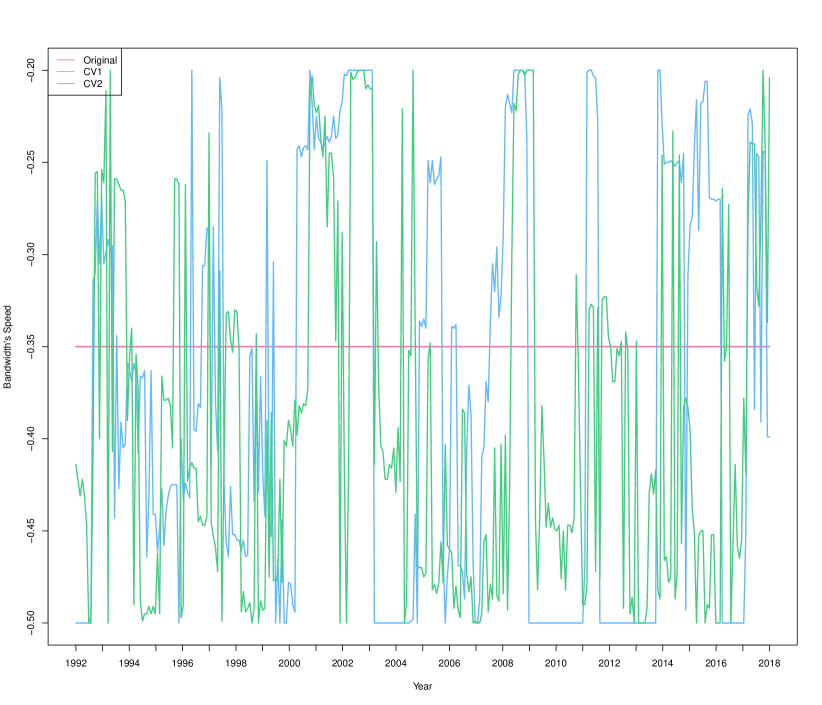

Without going into further details, we examine the practical implementation of the nonlinear shrinkage, as demonstrated by Ledoit and Wolf (2018a). The optimal solution is achieved using a nonparametric variable bandwidth kernel estimation of the limiting spectral density of the sample eigenvalues and its Hilbert transform. The speed at which the bandwidth vanishes in the number of assets can be set to according to standard kernel density estimation theory (Silverman 1986) or following the Arrow model of Ledoit and Wolf (2018b). As a compromise between those two approaches, Ledoit and Wolf (2018a) suggest the value of . Within the suggested data-driven methodology, we aim to verify whether this exact choice of the kernel bandwidth’s speed is crucial for the estimator’s efficiency and whether applying the suggested CV technique can improve the out-of-sample performance.

2.4 Approximate Factor Model

The previously outlined methods for improved high-dimensional covariance estimation do not assume any structural knowledge about the covariance matrix and regularize only the sample eigenvalues . An underlying structure could be established by regularizing the sample eigenvectors , for example if the covariance matrix itself is assumed to be sparse (see, e.g., Bickel and Levina 2008, Cai and Liu 2011). Unfortunately, this is not appropriate for financial time series because of the presence of common factors (Fan et al. 2013). However, if there is only conditional sparsity, the covariance matrix of investment returns can be estimated using factor models given by

where is the sample covariance matrix of the common factors and is the residuals covariance matrix.333Following this definition and assuming common factors with , a covariance matrix estimator based on factor models only needs to estimate covariance entries and is thus more stable. One disadvantage of such exact factor models is the strong assumption of no correlation in the error terms across assets; that is, the error covariance matrix is assumed to contain only the sample variances of the residuals. Therefore, possible cross-sectional correlations are neglected after separating the common present factors (Fan et al. 2013). Instead, approximate factor models allow for off-diagonal values within the error covariance matrix. The POET estimator is one of the most recent and efficient estimators from this branch of research. Using the close connection between factor models and the principal component analysis, Fan et al. (2013) infer the necessary factor loadings by running a singular value decomposition on the sample covariance matrix as

The covariance, formed by the first principal components, contains most of the information about the implied structure. The rest is assumed to be an approximately sparse matrix, estimated by applying an adaptive thresholding procedure (Cai and Liu 2011) with a threshold parameter .444For the operational use of POET, the threshold value needs to be determined, so that the positive-definiteness of is assured in finite samples. The choice of can therefore occur from a set, for which the respective minimal eigenvalue of the errors’ covariance matrix after thresholding is positive. The minimal constant that guarantees positive-definiteness is then chosen. For more details, see, Fan et al. (2013). As a result, the POET estimator becomes

| (7) |

As argued by Fan et al. (2013), for high-dimensional asset returns with a sufficiently large , the number of factors can be inferred from the data. A consistent data-driven estimator for is

| (8) |

where is the predefined maximum number of factors, is the matrix of asset returns with a sample covariance matrix , is a matrix with columns the eigenvectors, corresponding to the largest eigenvalues of , and is a penalty function of the type, introduced by Bai and Ng (2002). In this study we further examine whether the proposed CV approach can select optimal values for by considering the out-of-sample performance measure of interest as a selection criterion.

2.5 Graphical Model

A proper estimation of the covariance matrix of returns is crucial in a portfolio optimization context, since its inverse is the direct input parameter necessary for exploiting diversification effects upon optimization. Instead of imposing a factor structure on the covariance matrix with a sparse error covariance as in POET, sparsity in the precision matrix can be a valid approach for reducing estimation errors, especially in the case of conditional independence among asset pairs (Fan et al. 2016). In detail, the entry if and only if asset returns and are independent, conditional on the other assets in the investment universe. Since graphical models are used to describe both the conditional and unconditional dependence structures of a set of variables, the estimation of is closely related to graphs under a Gaussian model. The identification of zeros in the inverse can be performed with the Gaussian graphical model, since within the Markowitz portfolio optimization framework asset returns are assumed to follow a multivariate normal distribution.555This idea was first proposed by Dempster (1972) with the so-called covariance selection model.

One of the most commonly used methods for inducing sparsity on the precision matrix is by penalizing the maximum-likelihood. For i.i.d. with , the Gaussian log-likelihood function is given by

| (9) |

where denotes the determinant and the trace of a matrix. Maximizing Equation (9) alone yields the known maximum-likelihood estimator for the precision matrix , which suffers from high estimation error in case of high-dimensionality. To reduce such errors, the maximum log-likelihood function can be penalized by adding a lasso penalty (Tibshirani 1996) on the precision matrix entries as

| (10) |

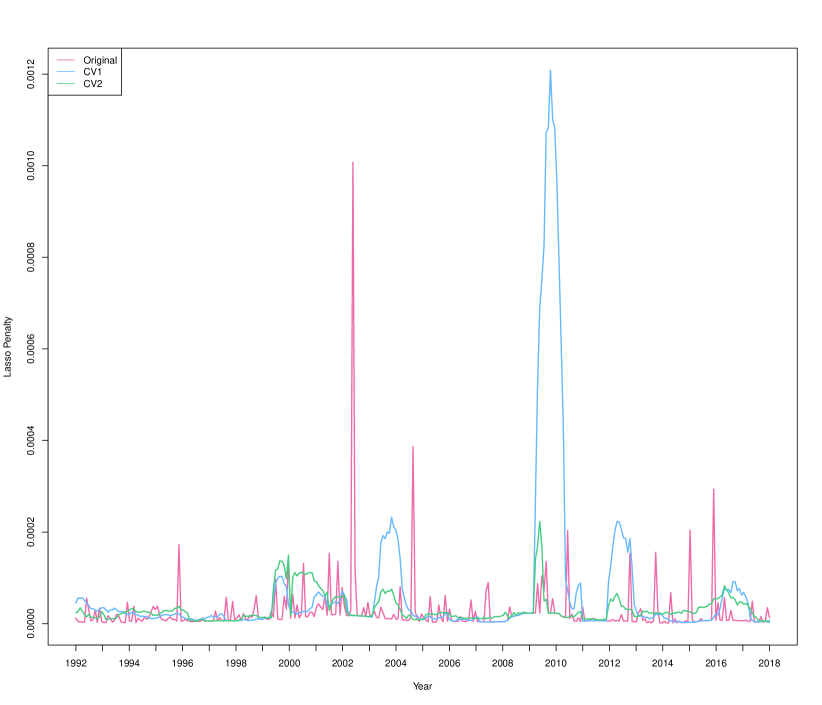

where is the -norm (the sum of the absolute values) of the matrix , an matrix with the off-diagonal elements, equal to the corresponding elements of the precision matrix and the diagonal elements equal to zero.666This insures that no penalty is applied to the asset returns’ sample variances. Furthermore, is a penalty parameter that controls the sparsity level, with higher values leading to a larger number of off-diagonal zero elements within the resulting estimator.

The penalized likelihood framework for a sparse graphical model estimation was first proposed by Yuan and Lin (2007), who solve Equation (10) with an interior-point method. Banerjee et al. (2008) show that the problem is convex and solve it for with a box-constrained quadratic program. To date, the fastest available solution for the sparse graphical model in Equation (10) is reached with the GLASSO algorithm, developed by Friedman et al. (2008) and later improved by Witten et al. (2011). They demonstrate that the above formulation is equivalent to an N-coupled lasso problem and solve it using a coordinate descent procedure.

In addition to a well-performing algorithm, the value of is necessary for calculating the optimal GLASSO estimator. For this purpose, Yuan and Lin (2007) suggest using the Bayesian Information Criterion (BIC), defined for each as

| (11) |

where the indicator function counts the number of nonzero off-diagonal elements in the estimated precision matrix. The value of , corresponding to the lowest BIC, is chosen as the optimal lasso penalty parameter. The choice of the BIC as a selection criterion for is further justified by the relation between the penalized problem in Equation (10) and the model selection criteria (Goto and Xu 2015). Although Yuan and Lin (2007) argue that a CV procedure for an optimal lasso penalty can yield better out-of-sample results, the existing financial applications estimate only once in-sample.777Goto and Xu (2015) induce sparsity to enhance robustness and lower the estimation error within portfolio hedging strategies, Brownlees et al. (2018) develop a procedure called “realized network” by applying GLASSO as a regularization procedure for realized covariance estimators, and Torri et al. (2019) analyze the out-of-sample performance of a minimum-variance portfolio, estimated with GLASSO. By contrast, next to such conservative approach, we consider the superiority of data-driven methods in the context of lasso regularization and perform additionally a multi-fold CV with risk-related selection criteria. The exact methodology is described in the next section.

3 Data-Driven Methodology

Each of the outlined covariance estimators includes an exogenous or data-dependent parameter. The linear shrinkage estimators in Equations (2) and (3) are calculated with an optimal shrinkage intensity . For the more general nonlinear shrinkage Ledoit and Wolf (2017) set the kernel bandwidth’s speed at as the average of two recognized approaches. The approximate factor model, the POET estimator by Fan et al. (2013), deals with an unknown number of factors , which are identified by minimizing popular information criteria. Finally, the GLASSO estimator proposed by Friedman et al. (2008) needs an optimal choice for the penalty parameter , often estimated by minimizing the BIC in-sample. To clarify our analysis, we refer to these estimation methods as ‘original’. In addition, we adopt a nonparametric technique, a multi-fold CV, to identify the necessary parameter for each estimation method in a data-driven way. Instead of relying on pre-specified assumptions and deriving corresponding solutions individually, we perform a grid search over a domain of values and find the best possible parameter for two exemplary out-of-sample statistics.

3.1 Parameter Set

To employ a data-driven choice, we first need to specify a domain of possible values for the necessary parameters that should be selected within the CV procedure. For this purpose we create a sequence (or grid) of arbitrary parameters for each covariance model. Depending on the chosen length of the sequence, the CV can be computationally time-consuming. Since the choice of this sequence is crucial for the out-of-sample efficiency of the data-driven methodology, the domain of possible parameters has to be individually evaluated for each estimation method by considering the trade-off between desired precision and computing time. Subsection 4.2 outlines the examined sequences for the considered covariance estimation methods.

3.2 Cross-Validation Procedure

The CV is a model validation technique designed to assess how an estimated model would perform on an unknown dataset. To evaluate the model accuracy, the available dataset is repeatedly split into a training and a testing subset in a rolling-window fashion (see, e.g., Refaeilzadeh et al. 2009, Arlot et al. 2010). For instance, in the case of an -fold CV, a dataset with observations is split into equal parts. The first rolling-window then uses as a training dataset the first fold consisting of the first observations ordered by time. Upon this, the consecutive observations are used to validate the performed estimation as a test dataset. This is iteratively done times by shifting the training window by observations and, therefore, maintaining the chronological order within the data.

In our setting, for each of the pre-defined parameters we successively use the training data to calculate a covariance matrix estimator for a test dataset and a specific parameter .888For clarity in the notation, we do not differentiate between covariance estimators. The procedure is applied to all methods equally. During the following validation stage, we must set selection criteria, also referred to as measures of fit, to identify which parameter performs best. In this study, we investigate two common objectives within the field of portfolio risk minimization.

As often argued, the squared forecasting error (SFE) or, as defined in Section 2, the Frobenius loss, is minimized to find a covariance estimator with the least forecasting error (see, e.g., Zakamulin 2015). Specifically, we first calculate a realized covariance matrix for the test dataset with

where are the asset returns from the test dataset and is the vector of average returns for the testing period consisting of observations. Then, we find the corresponding SFE as

This procedure is repeated times, so that we end up with SFE values for each . From the parameter set we then choose this for which the average (over all iterations) SFE is minimized. In our empirical study, the data-driven estimation method with the SFE as a measure of fit is referred to as CV1.

Instead of the SFE, within a portfolio optimization framework, one is generally more interested in whether a covariance estimator leads to lower out-of-sample risk of the optimal portfolio (see, e.g., Liu 2014, Ledoit and Wolf 2017, Engle et al. 2019). To incorporate and later investigate this concept, as our second scenario (CV2), we minimize the out-of-sample portfolio variance. In detail, with the covariance matrix , previously estimated with the training data, we calculate the optimal weights for a portfolio of our choice (e.g., the GMV). This then allows us to calculate the respective portfolio returns throughout the testing period with observations as

This procedure is repeated times, so that we end up with portfolio return vectors for each . From the parameter set, we then choose this for which the empirical variance (over all iterations) of those portfolio out-of-sample returns is minimized.

By applying different measures of fit within the data-driven methodology we explicitly address the importance of aligned selection criteria for the out-of-sample performance of each covariance estimation method. Moreover, we aim to verify whether the estimation of covariance parameters with a multi-fold CV yields better results out-of-sample than the original models.

4 Empirical Study

To exploit the above considerations, we perform an extensive empirical study of the suggested covariance estimation methods within a high-dimensional portfolio optimization context. For this purpose, we create GMV portfolios with and without short sales and evaluate their out-of-sample performance for a range of commonly used measures. We additionally compare the theoretical covariance parameters with their calibrated equivalents. The exact empirical construct is elaborated on in the following subsections.

4.1 Model Setup

For the empirical study, we focus on the GMV portfolio. The optimal weights for an investment period are determined by minimizing the portfolio variance as

| (12) | ||||

| s.t. |

where is an n-dimensional vector of ones and is an arbitrary covariance matrix estimator for the investment period . This formulation has the analytical solution Furthermore, we consider a GMV portfolio with an imposed constraint on the weights (GMV-NOSHORT),

| (13) | ||||

| s.t. |

which is a quadratic optimization problem with linear constraints that can be solved with every popular quadratic optimization software.999The measure of fit within CV2, the portfolio variance, depends on the estimated optimal weights. When short sales are allowed, we use the solution of Equation (12) to calculate the portfolio variance as in Subsection 3.2. For the case of GMV-NOSHORT, we solve Equation (13) within the CV. As discussed by recent literature (see, e.g., Jagannathan and Ma 2003, DeMiguel et al. 2009b), the introduction of a short-sale constraint is not only practically relevant because of common fund rules or budget constraints for individual investors. It moreover limits the estimation error in the portfolio weights. As a consequence, we would expect a slightly reduced effect of the estimation methods’ efficiency in respect to the out-of-sample performance. The empirical analysis of GMV-NOSHORT portfolios thus aims to complement our study and to ensure the practical reproducibility and relevance of our results.

4.2 Data and Methodology

To test the performance of the proposed covariance matrix estimation methods, we utilize four S&P 500 related datasets, which differ only in the number of assets used: 50, 100, 200 and 250 stocks. Throughout our study the datasets are referred to as 50SP, 100SP, 200SP and 250SP, respectively. Choosing datasets with different quantities of assets, we aim to study the behavior of covariance estimators when the concentration ratio becomes increasingly large in-sample. As common within the research on such high-dimensional covariance estimation (see, e.g., Fan et al. 2013, Ledoit and Wolf 2017, Engle et al. 2019), we consider daily prices.101010The price history originates from the Thomson Reuters EIKON database. For our out-of-sample analysis we use daily returns, starting on 01/01/1990 and ending on 12/31/2018. Overall, our data include observations for months (or 7306 days) per asset.

To ensure the stability in our results, we randomly select the necessary number of stocks among all the companies that have survived throughout the investigated period and keep them as the investment universe for our empirical study. Since the chosen datasets consist of individual stocks, the adopted investment strategies can be recreated easily and cost efficiently in practice by simply buying or selling the respective amount of stocks.

To evaluate the out-of-sample performance of the constructed portfolios and, implicitly, the covariance estimation methods, we adopt a rolling-window study with an in-sample period of two years, months (or roughly 504 days), and an out-of-sample period from 01/01/1992 to 12/31/2018, resulting in months (or 6801 days) out-of-sample portfolio returns. Similarly to the original studies on the reviewed covariance estimation methods (Fan et al. 2013, Ledoit and Wolf 2017, Engle et al. 2019), we employ a monthly rebalancing strategy, since this is more cost efficient and common in practice. Within each rolling-window step, the covariance matrix of asset returns for the investment month is estimated at the end of month using approximately the most recent 504 daily in-sample observations.

In our empirical study, the sample covariance estimator serves as a benchmark to the high-dimensional estimation methods and considered data-driven adjustments in terms of out-of-sample risk. For the application of the nonlinear shrinkage, we use the MATLAB-code provided by Ledoit and Wolf.111111https://www.econ.uzh.ch/en/people/faculty/wolf/publications.html.. The POET estimator is calculated using the R-package POET provided by Fan et al. (2013). As suggested by the authors, we adopt a soft-thresholding rule as well as a data-driven derivation of the number of factors and the thresholding constant for the original version of the method. Finally, the GLASSO estimator is calculated with the algorithm provided by Friedman et al. (2008) within the R-package glasso with no penalty on the diagonal elements.

In addition to the models in Section 2, we calculate the data-driven estimators as in Section 3 by applying an -fold CV. To calculate the selection criteria for the respective CV methods, we choose and therefore divide the in-sample observations into a training sample of 12 months (or 252 days) and a testing sample of one month (or 21 days). With this construction, we replicate the proposed monthly rebalancing strategy inside the performed CV. As introduced in Subsection 3.1, we additionally need to define a set of parameters for each covariance estimation method.

Since both linear shrinkage methods in Equation (2) (LW1) and Equation (3) (LWCC) represent the weighted average between the sample and a target covariance matrix, we define a parameter set of G shrinkage intensities, such that . Considering the reasoning in Subsection 2.3, for the nonlinear shrinkage estimator in Equation (6) (LWNL), we set the kernel bandwidth’s speed to lie between and with . Since the accuracy of a data-driven estimation depends on the number of examined parameters, with more parameters allowing for finer results, we consider a linear grid of equidistant values in the above cases. Furthermore, for the POET estimator, we consider . For the GLASSO estimator, we follow Friedman et al. (2008) and choose a sequence of penalty parameters , derived from the training data. Specifically, we define a logarithmic sequence as our -generating function, where with number of parameters in the sequence, being the maximal absolute value of the sample covariance matrix, estimated with the training dataset, and .

After calculating all the possible combinations of original and data-driven estimators within the validation subset, we choose an optimal parameter for each covariance estimation method, as outlined in Subsection 3.2, and use all the in-sample data to estimate the covariance matrix for the next investment month. Since the reviewed estimation methods and our data-driven methodology do not model time-dependency in the covariance matrix, we set . We use to find the optimal weights , as in Equations (12) and (13). With these weights, we calculate the out-of-sample portfolio returns for each model in . This procedure is repeated multiple times until the end of our investment horizon.

Overall, our study covers 17 different portfolios for each scenario with and without short sales. First, we include the equally-weighted portfolio, hereafter also referred to as the Naive portfolio. This strategy implies an identity covariance matrix and hence, does not include any estimation risk (DeMiguel et al. 2009b). In addition to the Naive strategy, which is a standard benchmark when comparing induced transaction costs, we build a GMV portfolio with the sample covariance matrix estimator, which serves as a benchmark for the out-of-sample risk. For each of the five high-dimensional covariance estimation methods discussed in Section 2, we construct portfolios with the original and calibrated parameters, resulting in three versions for each estimation methodology. All these portfolios are evaluated with the performance measures, presented in the following subsection.

4.3 Performance Measures

To evaluate the out-of-sample performance of each covariance matrix estimation method, we report different performance measures for the estimator’s efficiency and the risk profile as well as the allocation properties of the corresponding GMV and GMV-NOSHORT portfolios. First, we calculate the MSFE as

| (14) |

where is the covariance matrix estimator and is the realized covariance for month . The MSFE is frequently used to measure the forecasting power of an estimation method. To avoid double accounting for forecasting errors, we exclude the lower triangular part of both matrices from the calculation.

Considering the nature of minimum-variance portfolios as risk-reduction strategies, we are especially interested in the out-of-sample SD as a performance indicator. We calculate the standard deviation (SD) of the 6801 out-of-sample portfolio returns and multiply by to annualize it. For a more detailed analysis of the out-of-sample risk of the constructed portfolios and therefore, implicitly, covariance estimation methods, we perform the two-sided Parzen Kernel HAC-test for differences in variances, as described by Ledoit and Wolf (2008) and Ledoit and Wolf (2011), and report the corresponding significance levels. Since we utilize daily returns, a sufficient number of observations is available and a bootstrap technique is not essential.121212For the sake of completeness, we have also performed a block bootstrap as in Ledoit and Wolf (2011). The corresponding significant values are comparable to those from the HAC test and are therefore not reported. Since the MSFE is closely related to the SFE optimality criterion, as within the CV1 method, we expect the respectively optimized covariance estimators to exhibit a lower MSFE than their original versions. Moreover, a data-driven estimation with the CV2 approach, based on minimizing the portfolio variance, is expected to result in a lower out-of-sample SD.

In practice investors need to additionally address the problem of high transaction costs; hence, they prefer a more stable allocation for an optimal portfolio strategy. Therefore, as a proxy for occurring transaction costs, we analyze the average monthly turnover, defined as

| (15) |

where denotes the -norm of a vector as the sum of its absolute values and denotes the portfolio weights at the end of the investment month , scaled back to one. The turnover rate is calculated as the averaged sum of absolute values of the monthly rebalancing trades across all assets and over all investment dates . The next section reports the detailed out-of-sample performance analysis and empirical results.

5 Empirical Results

In the empirical part to this paper we compare how the original and data-driven methods for estimating the covariance matrix of returns affect the out-of-sample performance of GMV portfolios with and without short positions. This section examines the out-of-sample properties of the three estimation methodologies (original, CV1 and CV2).

5.1 Optimal Parameters

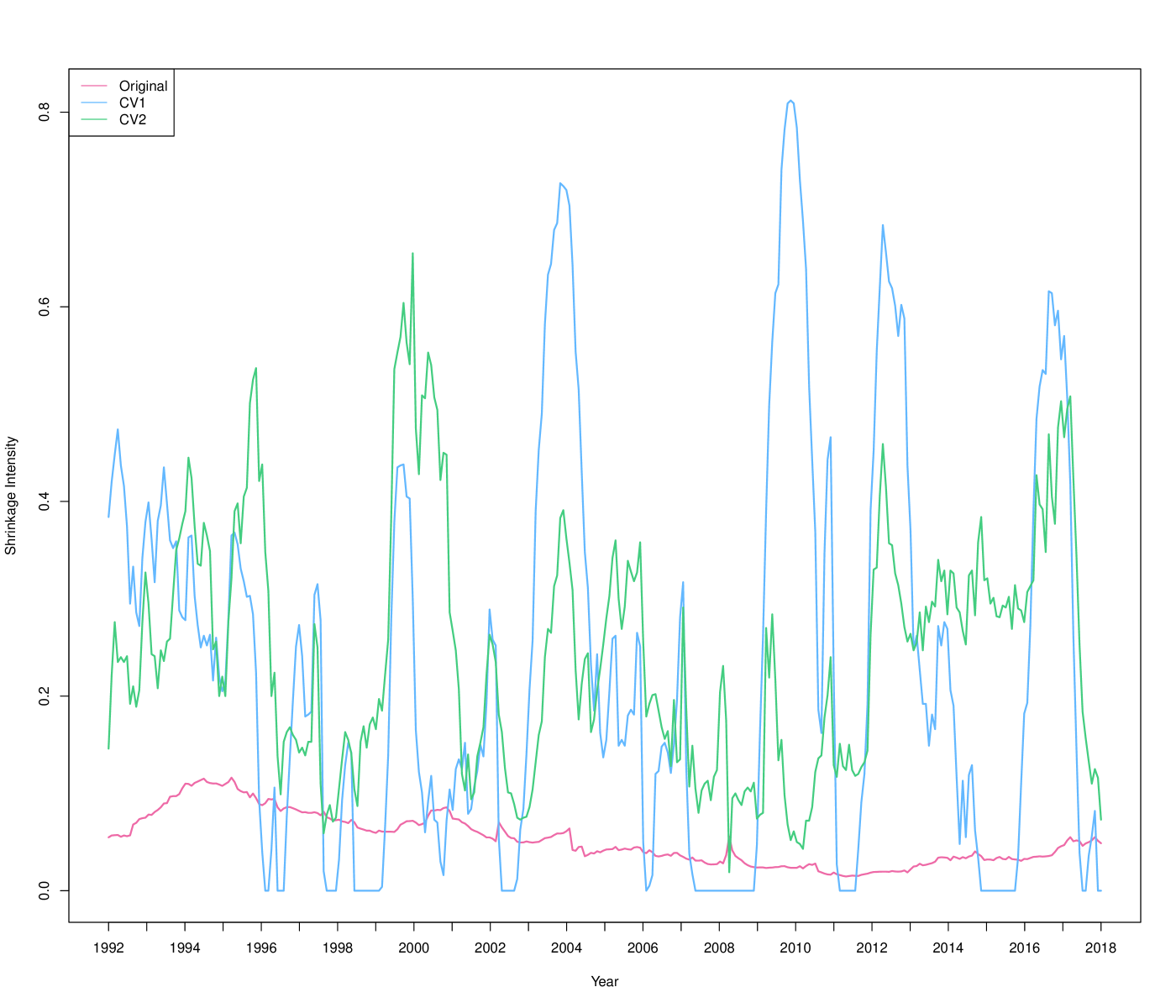

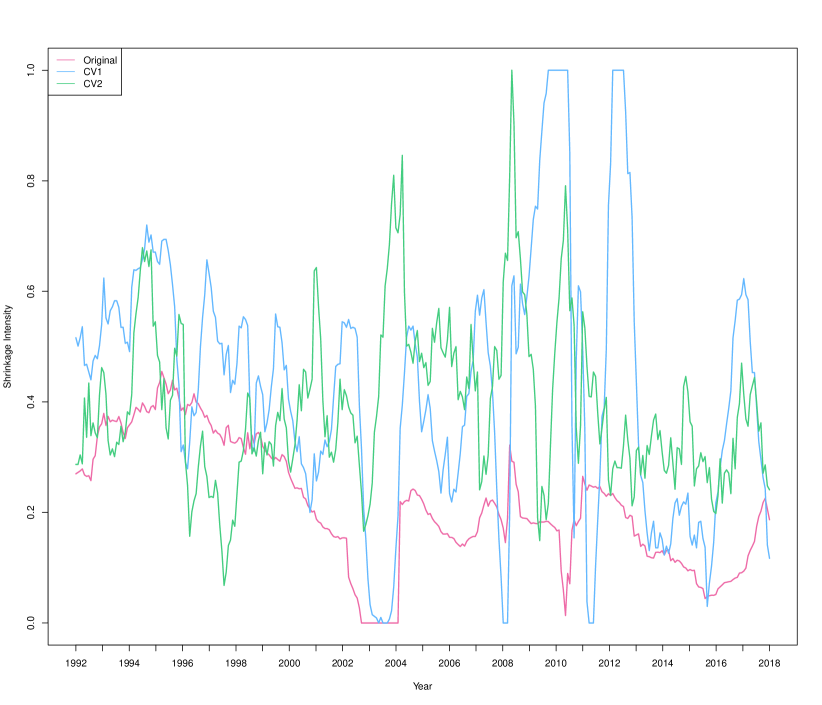

Figure 1 exemplary displays the selected linear shrinkage intensities for the original as well as CV1- and CV2-based LW1 estimation methods in the case of 50 stocks.131313Figure 2 shows the evolution of the selected parameters for the remaining covariance estimation methods in the case of the 50 considered stocks. The other three datasets produce similar results. To our surprise, the code for the POET estimator provided by Fan et al. (2013) produces a consistent number of factors throughout the observation period and for all four datasets. The trend of the optimal linear shrinkage intensities shows that the original approach of Ledoit and Wolf (2004b) is less reactive to changes in asset returns than our CV methodologies. The strong fluctuation in the selected shrinkage intensity for CV1 and CV2 results from their data-driven nature which implies fast adaptation to potentially changing market conditions. Nevertheless, such volatility in the parameter estimation could have negative effects on the out-of-sample properties of the corresponding estimators and thus, the estimated portfolios (e.g., in terms of turnover or an overall risk level). Therefore, the sole observation of the chosen parameters cannot lead to a clear conclusion on whether the CV technique enhances the covariance matrix estimator and the respective portfolio performance. In the following subsections we examine this behavior for the GMV portfolios with short sales.

5.2 GMV with short sales

Table 1 presents the central results of our empirical analysis on the GMV portfolio. The columns show the investment universes with 50, 100, 200 and 250 randomly chosen S&P 500 stocks as well as the three performance measures MSFE, SD and average monthly turnover rate (TO). The rows indicate the portfolio strategies based on the covariance estimation. While the original estimators are noted only by the respective name of the estimation method, the endings CV1 and CV2 represent the data-driven approaches, as explained in the previous sections.

| 50SP | 100SP | 200SP | 250SP | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| MSFE | SD | TO | MSFE | SD | TO | MSFE | SD | TO | MSFE | SD | TO | |

| Naive | 0.1887 | 0.0596 | 0.1811 | 0.0587 | 0.1852 | 0.0601 | 0.1858 | 0.0592 | ||||

| Sample | 0.0974 | 0.1265 | 0.3426 | 0.3224 | 0.1163 | 0.6578 | 1.3344 | 0.1180 | 1.5118 | 1.9834 | 0.1216 | 2.0891 |

| LW1 | 0.0970 | 0.1250 | 0.2945 | 0.3211 | 0.1132 | 0.5229 | 1.3297 | 0.1092 | 0.9742 | 1.9768 | 0.1074 | 1.2052 |

| LW1-CV1 | 0.0887 | 0.1263 | 0.2623 | 0.2911 | 0.1145 | 0.4527 | 1.1980 | 0.1112 | 0.8662 | 1.7720 | 0.1120 | 1.3532 |

| LW1-CV2 | 0.0953 | 0.1248 | 0.2236 | 0.3074 | 0.1112 | 0.3017 | 1.2621 | 0.1053 | 0.4229 | 1.8644 | 0.1019 | 0.4998 |

| LWCC | 0.0972 | 0.1244 | 0.2773 | 0.3218 | 0.1130 | 0.5097 | 1.3336 | 0.1092 | 1.0257 | 1.9819 | 0.1060 | 1.2435 |

| LWCC-CV1 | 0.0967 | 0.1261 | 0.2469 | 0.3214 | 0.1146 | 0.4365 | 1.3333 | 0.1098 | 0.8360 | 1.9825 | 0.1083 | 1.4716 |

| LWCC-CV2 | 0.0971 | 0.1244 | 0.2474 | 0.3218 | 0.1120 | 0.3699 | 1.3508 | 0.1076 | 0.5502 | 2.0050 | 0.1025 | 0.6201 |

| LWNL | 0.0974 | 0.1246 | 0.2753 | 0.3222 | 0.1118 | 0.4336 | 1.3329 | 0.1053 | 0.6712 | 1.9811 | 0.1020 | 0.7307 |

| LWNL-CV1 | 0.0973 | 0.1247 | 0.2817 | 0.3221 | 0.1118 | 0.4406 | 1.3322 | 0.1053 | 0.6798 | 1.9810 | 0.1020 | 0.7396 |

| LWNL-CV2 | 0.0974 | 0.1246 | 0.2817 | 0.3221 | 0.1118 | 0.4393 | 1.3329 | 0.1053 | 0.6774 | 1.9811 | 0.1021 | 0.7397 |

| POET | 0.0975 | 0.1238 | 0.2855 | 0.3225 | 0.1119 | 0.5233 | 1.3336 | 0.1070 | 1.1009 | 1.9843 | 0.1041 | 1.4242 |

| POET-CV1 | 0.0974 | 0.1240 | 0.2974 | 0.3223 | 0.1115 | 0.5457 | 1.3333 | 0.1072 | 1.1384 | 1.9831 | 0.1054 | 1.5588 |

| POET-CV2 | 0.0974 | 0.1239 | 0.3062 | 0.3224 | 0.1114 | 0.5456 | 1.3343 | 0.1072 | 1.1879 | 1.9836 | 0.1044 | 1.5188 |

| GLASSO | 0.0974 | 0.1242 | 0.4552 | 0.3222 | 0.1105 | 0.5522 | 1.3303 | 0.1054 | 0.5385 | 1.9668 | 0.1017 | 0.6117 |

| GLASSO-CV1 | 0.0941 | 0.1263 | 0.2299 | 0.3072 | 0.1147 | 0.3148 | 1.2591 | 0.1124 | 0.3410 | 1.8577 | 0.1099 | 0.3603 |

| GLASSO-CV2 | 0.0967 | 0.1221 | 0.2178 | 0.3180 | 0.1088 | 0.3164 | 1.3159 | 0.1046 | 0.4042 | 1.9579 | 0.1008 | 0.4150 |

-

•

This table reports the annualized out-of-sample SD and average monthly turnover (TO) of the GMV portfolios as well as the monthly MSFE of the respective covariance estimators across all the considered datasets with 50, 100, 200 and 250 stocks, respectively. Since the Naive portfolio strategy does not require a covariance estimator per definition, no values are reported for the MSFE. We report the lowest MSFE, SD, and TO for each estimation method in bold. The best results in terms of the MSFE and SD for each dataset are underlined. We additionally underline the lowest TO, excluding the Naive portfolio.

The compact representation of the results allows us to observe that in the case of enhanced covariance estimators the annualized SD declines as more assets are included in the GMV portfolio. This is easily explained by the known power of diversification – the desirable effect of including more stocks in a portfolio. Not surprisingly however, the estimation error with the sample covariance estimator diminishes the positive diversification effect, as shown by the increase in out-of-sample risk for the scenarios with 200 and 250 stocks. All the efficient covariance estimation methods perform better than the sample estimator in terms of out-of-sample risk for all the datasets, with larger deviations for a higher concentration ratios.141414Figure 3 provides a more visually attractive summary of the results for the GMV portfolios in terms of out-of-sample risk. For those estimation methods more susceptible to the tuning parameter, the differences in SD between the original, CV1, and CV2 methods are more pronounced.

More importantly, we can clearly detect the positive effect of the appropriate choice of selection criterion for determining the necessary covariance parameters. For all the datasets, minimizing the portfolio variance with the CV2 approach indeed leads to lower out-of-sample SD for the linear shrinkage methods LW1 and LWCC and the GLASSO estimator. Especially noteworthy is the continuous and strong risk-reduction property of the GLASSO model alone and in combination with CV2. First, among the original models, the GLASSO estimation produces the best results for the 100SP and 250SP datasets. Second, when the sparsity parameter for the GLASSO estimation is selected with the CV2 approach, outperformance is superior for all the datasets. Hence, in respect to out-of-sample risk, applying graph models to induce sparsity within the precision matrix seems to be a valid approach, even in comparison to highly sophisticated methods such as the nonlinear shrinkage and approximate factor models. Interestingly, for the latter, the CV2 method does not lead to consistent outperformance in terms of risk. The original version of POET performs better than POET-CV2 in all cases but the 100SP dataset. In the case of GMV portfolios with short sales this result implies that the application of the CV with selection criteria such as SFE (CV1) and out-of-sample portfolio variance (CV2) does not result in a more optimal number of factors than the originally established function in Equation (8). Moreover, for LWNL, there is almost no relevant difference in annualized out-of-sample SD. We can therefore argue that the efficiency of LWNL does not strongly depend on the choice of the kernel bandwidth’s speed and hence, a data-driven specification cannot lead to an improvement in the performance out-of-sample.

For the CV1 approach, the investigation of the MSFE is mandatory. The values reported in Table 1 indicate the distinct effect of the CV1 approach on the minimization of the MSFE out-of-sample. For all the estimation methods and datasets, except the isolated case of LWCC for 250SP, the MSFE is the lowest for the CV1 version of every estimator. Even robust estimators such as LWNL and POET exhibit higher forecasting power, measured by the MSFE, when the corresponding parameters are estimated with the CV1 approach. Nevertheless, it is noteworthy that the MSFE measure does not seem to proxy for the out-of-sample portfolio risk level. Within the financial literature including Zakamulin (2015), the MSFE is studied in reference to datasets with low concentration ratios. Within a high-dimensional setting, however, a lower MSFE does not coincide with lower SD out-of-sample for any of the datasets or estimation methods.151515Only the LWNL estimator for the 200SP and 250SP datasets yields the lowest risk levels and lowest MSFE for the CV1 approach. This result is merely based on a negligible difference and can thus be ignored. Under the CV1 method, the SFE is computed as an estimator’s squared distance to the monthly realized covariance matrix, calculated on the basis of daily returns (roughly 21 days) for assets. The implied concentration ratios, ranging from for the 50SP dataset to for the 250SP dataset, lead to ill-conditioned realized covariance matrices and a noisy SFE calculation.161616To solve this problem, recent financial studies have focused on improving the estimation of large realized covariance matrices (see, e.g., Hautsch et al. 2012, Callot et al. 2017, Bollerslev et al. 2018). Therefore, we focus our further analysis on the CV2 approach.

To understand the magnitude of improvements in the CV2-based estimation methods as well as the superiority of the GLASSO method, Table 3 presents the differences in annualized SDs and the respective pairwise significance levels across all the original covariance estimators and their CV2-based counterparts for the high-dimensional case of the 250SP dataset.171717Appendix B compares further datasets. Overall, the results are similar in tendency, but are less pronounced due to a lower dimensionality in the data. Table 3 is to be read column-wise; that is, the difference in SD for the LW1 and Sample estimator is listed under the second column for the first row. For completeness, we construct the table symmetrically. Still, we focus our attention on the elements above the diagonal only.

| Sample | LW1 | LW1-CV2 | LWCC | LWCC-CV2 | LWNL | LWNL-CV2 | POET | POET-CV2 | GLASSO | GLASSO-CV2 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Sample | |||||||||||

| LW1 | |||||||||||

| LW1-CV2 | |||||||||||

| LWCC | |||||||||||

| LWCC-CV2 | |||||||||||

| LWNL | |||||||||||

| LWNL-CV2 | |||||||||||

| POET | |||||||||||

| POET-CV2 | |||||||||||

| GLASSO | |||||||||||

| GLASSO-CV2 | |||||||||||

| better than % of models |

-

•

This table shows the differences in the annualized out-of-sample SD of the GMV-250SP portfolios across the main covariance estimation methods and their CV2-based counterparts. The table is constructed in a symmetrical way with an applied color scheme from red (higher SD than the other model) to green (lower SD than the other model). In addition, on the elements above the diagonal, the significant pairwise outperformance in terms of variance is denoted by asterisks: *** denotes significance at the 0.001 level; ** denotes significance at the 0.01 level; and * denotes significance at the 0.05 level. Finally, for each model, we report the percentage of the other models that exhibit higher variance as a qualitative measure.

| Sample | LW1 | LW1-CV2 | LWCC | LWCC-CV2 | LWNL | LWNL-CV2 | POET | POET-CV2 | GLASSO | GLASSO-CV2 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Sample | |||||||||||

| LW1 | |||||||||||

| LW1-CV2 | |||||||||||

| LWCC | |||||||||||

| LWCC-CV2 | |||||||||||

| LWNL | |||||||||||

| LWNL-CV2 | |||||||||||

| POET | |||||||||||

| POET-CV2 | |||||||||||

| GLASSO | |||||||||||

| GLASSO-CV2 | |||||||||||

| better than % of models |

-

•

This table shows the differences in the annualized out-of-sample SD of the GMV-NOSHORT-250SP portfolios across the main covariance estimation methods and their CV2-based counterparts. The table is constructed in a symmetrical way with an applied color scheme from red (higher SD than the other model) to green (lower SD than the other model). In addition, on the elements above the diagonal, the significant pairwise outperformance in terms of variance is denoted by asterisks: *** denotes significance at the 0.001 level; ** denotes significance at the 0.01 level; and * denotes significance at the 0.05 level. Finally, for each model, we report the percentage of the other models that exhibit higher variance as a qualitative measure.

At first glance, we can once more distinguish the weak performance of the sample covariance estimator. All the other estimators lead to significantly less out-of-sample risk with a p-value of roughly 0.001 or lower. The second worst estimation method for this asset universe is the original LW1, followed by LWCC. On the contrary, when the linear shrinkage intensity is optimized for with respect to the out-of-sample portfolio variance with CV2, we observe an astonishing improvement for those estimators. Both LW1-CV2 and LWCC-CV2 result in a significantly lower out-of-sample SD than their original counterparts. Comparing LWCC-CV2 with LW1-CV2, we can conclude that linear shrinkage toward the identity matrix yields more stable and efficient portfolio allocation than the same technique applied to a constant correlation model. It seems, therefore, that within the data-driven approach it is better to assume less than assume the wrong structure. Another surprising insight emerges from the comparison of LW1-CV2 with LWNL. Although especially designed to overcome the high-dimensionality problem, both the original and CV2-based nonlinear shrinkage methods lead to higher out-of-sample risk than the data-driven linear shrinkage estimators. This effect is observable for the 100SP dataset as well (see, for reference, Table 6). As the difference is not statistically significant in any of the cases, we can only draw a qualitative conclusion that a methodologically easy-to-understand and simple-to-implement method can perform as well as a complex state-of-the-art estimator when the necessary tuning parameter (here, the shrinkage intensity) is identified in a data-driven way. With respect to the GLASSO estimation method, we find that GLASSO with CV2 results in a significantly lower out-of-sample SD than the original estimator (p-value of 0.01). This finding reveals that a suitable selection criterion for the sparsity parameter is of utmost importance. Furthermore, GLASSO-CV2 yields significantly lower out-of-sample portfolio variance than the sample, LW1, LWCC, and POET estimators. LWNL is significantly outperformed by GLASSO-CV2 for the 50SP and 100SP datasets with a p-value of 0.001 (see, for reference, the significant levels in Table 6 and Table 6). Overall, these results confirm that GLASSO in combination with CV2 is the most efficient covariance estimator among the estimators considered in our study.

Table 1 additionally reports the average monthly turnover rate as a proxy for the arising transaction costs induced by monthly rebalancing. The Naive portfolio, being long only and equally-weighted by construction, naturally has the lowest turnover (approximately 0.06 on average across all the datasets). As expected, the GMV portfolios estimated with the sample covariance matrix are characterized by extreme exposures for all the datasets. With higher dimensionality the ill-conditioned sample estimator induces even stronger dispersion in the portfolio weights. On the other hand, an estimation with GLASSO or its CV-based equivalents has the most pronounced positive effect on the allocation characteristics of the GMV portfolio. In particular, the GLASSO-CV1 estimation methodology results in GMV portfolios with the lowest turnover for the 200SP and 250SP datasets. For the least high-dimensional dataset, 50SP, GLASSO-CV2 leads to the lowest turnover. An interesting case is the 100SP dataset, where clear outperformance in terms of turnover rate occurs for the estimator LW1-CV2, followed closely by GLASSO-CV1. It seems that when the concentration ratio is tolerable, as for the case of 100SP, the linear shrinkage methodology, as a convex combination between the sample covariance and an identity matrix, produces satisfactory results. This can be explained by the fact that the underlying model in LW1 is equivalent to the introduction of a ridge type penalty in the estimation (Warton 2008), which has been proven to induce stability. However, when the sample covariance matrix becomes ill-conditioned, as for the 200SP and 250SP datasets, even a sophisticated data-driven choice of the linear shrinkage intensity cannot outperform the GLASSO estimation in terms of turnover. While LW1 shrinks the sample covariance matrix toward the identity matrix, GLASSO shrinks the precision matrix toward the identity matrix. Since the Naive portfolio corresponds to a GMV portfolio estimated with an identity covariance and hence, precision matrix, one may suggest that both estimation methods result in an implicit shrinkage of the sample GMV portfolio weights toward an equally-weighted portfolio, as in Tu and Zhou (2011), and therefore perform well in terms of turnover. Surprisingly, the estimator LWNL is strongly outperformed by all the data-driven estimators except POET with CV1 and CV2. For example, while GLASSO achieves a turnover rate of 0.61 for 250SP, estimation with LWNL leads to 0.73 average monthly turnover. The application of CV1 and CV2 for determining the sparsity parameter within the GLASSO model amplifies this result. More importantly, when a covariance estimator is susceptible to an improvement by the data-driven estimation of the necessary parameters, as LW1, LWCC, and GLASSO are, the implementation of CV leads to a strong positive impact on the stability of optimal weights.

5.3 GMV without short sales

Focusing on more practically relevant portfolio strategies, we construct a second set of GMV portfolios that do not exhibit negative weights (GMV-NOSHORT). The exclusion of short sales is a common regulatory constraint that strongly influences the optimal performance in respect to the out-of-sample risk and the allocation of weights. To investigate those, Table 4 reports the main out-of-sample measures for GMV-NOSHORT. Since the examined short-sale constraint does not play any role in the CV1-based estimation of the covariance matrix, we do not report the MSFE values. The table is structured similarly to Table 1 with the columns representing the investment universes (50SP, 100SP, 200SP and 250SP), and performance measures, while the rows indicate the portfolio strategies based on the considered covariance estimation methods.

| 50SP | 100SP | 200SP | 250SP | |||||

|---|---|---|---|---|---|---|---|---|

| SD | TO | SD | TO | SD | TO | SD | TO | |

| Naive | 0.1887 | 0.0596 | 0.1811 | 0.0587 | 0.1852 | 0.0601 | 0.1858 | 0.0592 |

| Sample | 0.1295 | 0.1473 | 0.1168 | 0.1810 | 0.1137 | 0.2158 | 0.1105 | 0.2227 |

| LW1 | 0.1296 | 0.1382 | 0.1167 | 0.1708 | 0.1135 | 0.1974 | 0.1105 | 0.2055 |

| LW1-CV1 | 0.1308 | 0.1486 | 0.1180 | 0.1712 | 0.1151 | 0.1999 | 0.1122 | 0.2310 |

| LW1-CV2 | 0.1294 | 0.1578 | 0.1169 | 0.1896 | 0.1136 | 0.2287 | 0.1103 | 0.2640 |

| LWCC | 0.1291 | 0.1347 | 0.1167 | 0.1655 | 0.1134 | 0.1941 | 0.1100 | 0.2011 |

| LWCC-CV1 | 0.1297 | 0.1310 | 0.1179 | 0.1607 | 0.1145 | 0.1863 | 0.1110 | 0.2246 |

| LWCC-CV2 | 0.1286 | 0.1484 | 0.1169 | 0.1857 | 0.1134 | 0.2228 | 0.1105 | 0.2749 |

| LWNL | 0.1296 | 0.1351 | 0.1166 | 0.1589 | 0.1136 | 0.1770 | 0.1110 | 0.1806 |

| LWNL-CV1 | 0.1296 | 0.1360 | 0.1166 | 0.1602 | 0.1136 | 0.1779 | 0.1110 | 0.1815 |

| LWNL-CV2 | 0.1295 | 0.1361 | 0.1166 | 0.1600 | 0.1135 | 0.1776 | 0.1110 | 0.1817 |

| POET | 0.1291 | 0.1392 | 0.1165 | 0.1711 | 0.1135 | 0.2034 | 0.1101 | 0.2125 |

| POET-CV1 | 0.1290 | 0.1418 | 0.1164 | 0.1752 | 0.1134 | 0.2038 | 0.1101 | 0.2167 |

| POET-CV2 | 0.1291 | 0.1452 | 0.1164 | 0.1759 | 0.1134 | 0.2069 | 0.1100 | 0.2283 |

| GLASSO | 0.1302 | 0.2828 | 0.1165 | 0.2622 | 0.1134 | 0.2368 | 0.1107 | 0.2704 |

| GLASSO-CV1 | 0.1314 | 0.1468 | 0.1196 | 0.1752 | 0.1182 | 0.1934 | 0.1158 | 0.2000 |

| GLASSO-CV2 | 0.1285 | 0.1348 | 0.1158 | 0.1693 | 0.1132 | 0.1690 | 0.1099 | 0.1778 |

-

•

This table reports the annualized out-of-sample SD and average monthly turnover rate (TO) of the GMV-NOSHORT portfolios across all the considered datasets with 50, 100, 200 and 250 stocks, respectively. We report the lowest SD and TO for each estimation method in bold. The best results in terms of SD for each dataset are underlined. We additionally underline the lowest TO, excluding the Naive portfolio.

First, the sample covariance estimator leads to better results in comparison to Table 1, verifying the impact of constraints on the minimization of estimation errors in portfolio weights, as shown by Jagannathan and Ma (2003). In contrast to the previous results, the differences in out-of-sample performance in terms of portfolio risk are generally less distinctive among the estimation methods. While GLASSO-CV2 continues to achieve the lowest out-of-sample annualized SD for all the datasets, a data-driven approach only inconsistently enhances the performance of the other original estimation methods. For instance, both LW1 and LWCC perform better than their CV2-based counterparts for the 100SP and 200SP datasets. Although both the nonlinear shrinkage and POET with CV2-estimated parameters seem to produce lower out-of-sample risk, the effect is negligible.181818The relative differences in SD among all the original and cross-validated estimators are presented in Figure 4. Moreover, Table 3 presents the differences in annualized SDs and the respective pairwise significance levels across all the main covariance estimation methods and their CV2-based counterparts for the high-dimensional case of the 250SP dataset.191919Appendix C compares further datasets. The table is constructed similarly to Table 3.

The first notable consequence of the short-sale constraint is the improvement in portfolio performance for the case of the sample covariance matrix. Table 3 shows that only the POET estimators with and without CV2 yield a statistically lower out-of-sample SD than the sample covariance matrix with a p-value of 0.001. Both the original and the CV2-based POET estimation methods result in a lower out-of-sample portfolio variance than all the other methods except LWCC and GLASSO-CV2. However, although GLASSO-CV2 outperforms all the other estimators qualitatively, the results are significant only compared to the original GLASSO estimator with a p-value of 0.001. This once more confirms that, first, the sparsity parameter for GLASSO is best determined with a CV and, second, the selection criterion within the CV should match the performance measure. In general, when no short sales are allowed, POET-CV2 and GLASSO-CV2 consistently outperform the rest of the methods (see, for reference, Tables 9 and 10 for the other datasets). For a less high-dimensional dataset, such as 100SP, the out-of-sample SD generated with GLASSO-CV2 is even significantly lower than the out-of-sample SD induced by POET. Although less pronounced, the positive effects of a CV methodology with an adequate selection criterion, namely the variance of a short sales constrained GMV, are noticeable here as well. In particular, the usage of GLASSO-CV2 significantly improves the out-of-sample risk of a GMV without short sales for the 50SP, 100SP, and 250SP datasets.202020For 200SP, GLASSO-CV2 outperforms all the other methods in terms of SD; however, the results are not significant.

Finally, we examine the average monthly turnover rates, reported in Table 4. Since the portfolios are optimized with the additional no short-sale constraint, we expect the optimal weights to be much less dispersed across the rebalancing periods. Such behavior in turn results in lower turnover rates and transaction costs. In comparison to the GMV portfolios from Subsection 5.2, the turnover reduction is present even for the case of the ill-conditioned sample covariance estimator. The latter still performs worst, compared to the other methods with more dispersion in the weights for high-dimensional datasets such as 200SP and 250SP. In addition, for those datasets, we observe the lowest turnover rates when GLASSO-CV2 is used, followed by LWNL with a difference of one percent. We therefore continue to observe the positive effects of a data-driven estimation with the portfolio variance as a measure of fit not only on the out-of-sample risk but as well on the turnover rates.

6 Conclusion

In this study, we review some of the most recent and efficient estimation methods for high-dimensional minimum-variance portfolios. We extend the current research by proposing a data-driven methodology to determine the corresponding tuning parameters such as the linear shrinkage intensity and the sparsity penalty term.

In a detailed empirical analysis with four datasets, we identify the characteristics of our data-driven methodology. First, we establish that the selection criterion within the CV should correspond to the performance measure of interest. We show that the lowest overall out-of-sample portfolio risk is indeed generated when we select the optimal tuning parameters by minimizing the portfolio variance with the proposed CV. In particular, the application of this procedure to each of the considered estimators with the exception of the nonlinear shrinkage leads to superior GMV or GMV-NOSHORT portfolios in terms of out-of-sample SD and average turnover rates. The performance of the nonlinear shrinkage estimator is only slightly affected by the speed of the kernel bandwidth and a data-driven selection of this speed does not lead to a significantly lower risk. Moreover, the POET estimator in combination with a CV technique seems to perform generally better under the scenario of short sales constraints. On the other hand, the GLASSO estimator clearly outperforms the other high-dimensional estimation methods for all data scenarios considered when calibrated accordingly. This not only provides new insights into the application of GLASSO in the portfolio context, but also confirms the relationship between lasso regulation and the power of CV in a covariance estimation context. We additionally demonstrate that a data-driven methodology is beneficial to estimators whose performance depends strongly on the embedded tuning parameters, as is the case with linear shrinkage and GLASSO estimation methods. Even complex and highly efficient estimators can be surpassed by simpler approaches if a sophisticated data-driven technique is used. One of the reasons for this observation is the rapid adaptation of the CV toward ever-changing market situations.

Within our analysis we investigate only high-dimensional covariance estimation methods that assume homoscedasticity in the returns. Since we observe a time-variable parameter selection with the CV approach and a resulting improvement in the out-of-sample performance, we argue that the combination of data-driven parameter evaluation and time-dependent high-dimensional variance estimators, as recently proposed by Halbleib and Voev (2014) and Engle et al. (2019), is an important topic for future research.

Acknowledgements.

This is a pre-print of the article submitted to Financial Markets and Portfolio Management. You can find the accepted version online at: 10.1007/s11408-020-00370-4.References

- Arlot et al. (2010) S. Arlot, A. Celisse, et al. A survey of cross-validation procedures for model selection. Statistics surveys, 4:40–79, 2010.

- Bai and Ng (2002) J. Bai and S. Ng. Determining the number of factors in approximate factor models. Econometrica, 70(1):191–221, 2002.

- Banerjee et al. (2008) O. Banerjee, L. E. Ghaoui, and A. d’Aspremont. Model selection through sparse maximum likelihood estimation for multivariate gaussian or binary data. Journal of Machine learning research, 9(Mar):485–516, 2008.

- Best and Grauer (1991a) M. J. Best and R. R. Grauer. Sensitivity analysis for mean-variance portfolio problems. Management Science, 37(8):980–989, 1991a. doi: 10.1287/mnsc.37.8.980.

- Best and Grauer (1991b) M. J. Best and R. R. Grauer. On the sensitivity of mean-variance-efficient portfolios to changes in asset means some analytical and computational results. Review of Financial Studies, 4(2):315–342, 1991b. doi: 10.1093/rfs/4.2.315.

- Bickel and Levina (2008) P. J. Bickel and E. Levina. Covariance regularization by thresholding. Annals of Statistics, 36(6):2577–2604, 2008. doi: 10.1214/08-AOS600.

- Bollerslev et al. (2018) T. Bollerslev, A. J. Patton, and R. Quaedvlieg. Modeling and forecasting (un)reliable realized covariances for more reliable financial decisions. Journal of Econometrics, 207(1):71–91, 2018. doi: 10.1016/j.jeconom.2018.05.004.

- Broadie (1993) M. Broadie. Computing efficient frontiers using estimated parameters. Annals of Operations Research, 45(1):21–58, 1993. doi: 10.1007/BF02282040.

- Brodie et al. (2009) J. Brodie, I. Daubechies, C. de Mol, D. Giannone, and I. Loris. Sparse and stable markowitz portfolios. PNAS, 106(30):12267–12272, 2009. doi: 10.1073/pnas.0904287106.

- Brownlees et al. (2018) C. Brownlees, E. Nualart, and Y. Sun. Realized networks. Journal of Applied Econometrics, 33(7):986–1006, 2018.

- Cai and Liu (2011) T. T. Cai and W. Liu. Adaptive thresholding for sparse covariance matrix estimation. Journal of the American Statistical Association, 106(494):672–684, 2011. doi: 10.1198/jasa.2011.tm10560.

- Callot et al. (2017) L. A. Callot, A. B. Kock, and M. C. Medeiros. Modeling and forecasting large realized covariance matrices and portfolio choice. Journal of Applied Econometrics, 32(1):140–158, 2017.

- Christoffersen and Jacobs (2004) P. Christoffersen and K. Jacobs. The importance of the loss function in option valuation. Journal of Financial Economics, 72(2):291–318, 2004.

- DeMiguel et al. (2009a) V. DeMiguel, L. Garlappi, F. J. Nogales, and R. Uppal. A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms. Management Science, 55(5):798–812, 2009a. doi: 10.1287/mnsc.1080.0986.

- DeMiguel et al. (2009b) V. DeMiguel, L. Garlappi, and R. Uppal. Optimal versus naive diversification: How inefficient is the 1/ n portfolio strategy? Review of Financial Studies, 22(5):1915–1953, 2009b. doi: 10.1093/rfs/hhm075.

- Dempster (1972) A. P. Dempster. Covariance selection. Biometrics, pages 157–175, 1972.

- Elton and Gruber (1973) E. J. Elton and M. J. Gruber. Estimating the dependence structure of share prices - implications for portfolio selection. Journal of Finance, 28(5):1203–1232, 1973. doi: 10.1111/j.1540-6261.1973.tb01451.x.

- Engle et al. (2019) R. F. Engle, O. Ledoit, and M. Wolf. Large dynamic covariance matrices. Journal of Business & Economic Statistics, 37(2):363–375, 2019.

- Fan et al. (2013) J. Fan, Y. Liao, and M. Mincheva. Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 75(4):603–680, 2013. doi: 10.1111/rssb.12016.

- Fan et al. (2016) J. Fan, Y. Liao, and H. Liu. An overview of the estimation of large covariance and precision matrices. The Econometrics Journal, 19(1):C1–C32, 2016.

- Friedman et al. (2008) J. Friedman, T. Hastie, and R. Tibshirani. Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9(3):432–441, 2008. doi: 10.1093/biostatistics/kxm045.

- Frost and Savarino (1986) P. A. Frost and J. E. Savarino. An empirical bayes approach to efficient portfolio selection. Journal of Financial and Quantitative Analysis, 21(3):293–305, 1986. doi: 10.2307/2331043.

- Goto and Xu (2015) S. Goto and Y. Xu. Improving mean variance optimization through sparse hedging restrictions. Journal of Financial and Quantitative Analysis, 50(6):1415–1441, 2015.

- Halbleib and Voev (2014) R. Halbleib and V. Voev. Forecasting covariance matrices: A mixed approach. Journal of Financial Econometrics, 14(2):383–417, 2014.

- Hautsch et al. (2012) N. Hautsch, L. M. Kyj, and R. C. Oomen. A blocking and regularization approach to high-dimensional realized covariance estimation. Journal of Applied Econometrics, 27(4):625–645, 2012.

- Jagannathan and Ma (2003) R. Jagannathan and T. Ma. Risk reduction in large portfolios: why imposing the wrong constraints helps. Journal of Finance, 58(4):1651–1683, 2003. doi: 10.1111/1540-6261.00580.

- James and Stein (1961) W. James and C. Stein. Estimation with quadratic loss. In J. Neyman, editor, Proceedings of the fourth Berkeley symposium on mathematical statistics and probability, pages 361–379. University of California Press, Berkeley, 1961.

- Jobson and Korkie (1981) J. D. Jobson and R. M. Korkie. Putting markowitz theory to work. Journal of Portfolio Management, 7(4):70–74, 1981. doi: 10.3905/jpm.1981.408816.

- Ledoit and Wolf (2003) O. Ledoit and M. Wolf. Improved estimation of the covariance matrix of stock returns with an application to portfolio selection. Journal of Empirical Finance, 10(5):603–621, 2003. doi: 10.1016/S0927-5398(03)00007-0.

- Ledoit and Wolf (2004a) O. Ledoit and M. Wolf. Honey, i shrunk the sample covariance matrix. Journal of Portfolio Management, 30(4):110–119, 2004a. doi: 10.3905/jpm.2004.110.

- Ledoit and Wolf (2004b) O. Ledoit and M. Wolf. A well-conditioned estimator for large-dimensional covariance matrices. Journal of Multivariate Analysis, 88(2):365–411, 2004b. doi: 10.1016/S0047-259X(03)00096-4.

- Ledoit and Wolf (2008) O. Ledoit and M. Wolf. Robust performance hypothesis testing with the sharpe ratio. Journal of Empirical Finance, 15(5):850–859, 2008. doi: 10.1016/j.jempfin.2008.03.002.

- Ledoit and Wolf (2011) O. Ledoit and M. Wolf. Robust performances hypothesis testing with the variance. Wilmott, 2011(55):86–89, 2011. doi: 10.1002/wilm.10036.

- Ledoit and Wolf (2012) O. Ledoit and M. Wolf. Nonlinear shrinkage estimation of large-dimensional covariance matrices. Annals of Statistics, 40(2):1024–1060, 2012. doi: 10.1214/12-AOS989.

- Ledoit and Wolf (2015) O. Ledoit and M. Wolf. Spectrum estimation: a unified framework for covariance matrix estimation and pca in large dimensions. Journal of Multivariate Analysis, 139:360–384, 2015. doi: 10.1016/j.jmva.2015.04.006.

- Ledoit and Wolf (2017) O. Ledoit and M. Wolf. Nonlinear shrinkage of the covariance matrix for portfolio selection: Markowitz meets goldilocks. Review of Financial Studies, 30(12):4349–4388, 2017. doi: 10.1093/rfs/hhx052.

- Ledoit and Wolf (2018a) O. Ledoit and M. Wolf. Analytical nonlinear shrinkage of large-dimensional covariance matrices, 2018a.

- Ledoit and Wolf (2018b) O. Ledoit and M. Wolf. Optimal estimation of a large-dimensional covariance matrix under stein’s loss. Bernoulli, 24(4B):3791–3832, 2018b. doi: 10.3150/17-BEJ979.

- Liu (2014) X. Liu. Portfolio selection via shrinkage by cross validation. Journal of Finance and Accounting, 2(4):74–81, 2014.

- Markowitz (1952) H. M. Markowitz. Portfolio selection. Journal of Finance, 7(1):77–91, 1952. doi: 10.1111/j.1540-6261.1952.tb01525.x.

- Merton (1980) R. C. Merton. On estimating the expected return on the market. Journal of Financial Economics, 8(4):323–361, 1980. doi: 10.1016/0304-405X(80)90007-0.

- Michaud (1989) R. O. Michaud. The markowitz optimization enigma: Is ‘optimized’ optimal? Financial Analysts Journal, 45(1):31–42, 1989. doi: 10.2469/faj.v45.n1.31.

- Refaeilzadeh et al. (2009) P. Refaeilzadeh, L. Tang, and H. Liu. Cross-validation. Encyclopedia of database systems, pages 532–538, 2009.

- Silverman (1986) B. W. Silverman. Density estimation for statistics and data analysis. Chapman & Hall, 1986.

- Stein (1956) C. Stein. Inadmissibility of the usual estimator for the mean of a multivariate normal distribution. In J. Neyman, editor, Proceedings of the third Berkeley symposium on mathematical statistics and probability, pages 197–206. University of California Press, Berkeley, 1956.

- Stein (1986) C. Stein. Lectures on the theory of estimation of many parameters. Journal of Soviet Mathematics, 34(1):1373–1403, 1986. doi: 10.1007/BF01085007.

- Tibshirani (1996) R. Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 58(1):267–288, 1996.

- Torri et al. (2019) G. Torri, R. Giacometti, and S. Paterlini. Sparse precision matrices for minimum variance portfolios. Computational Management Science, 16(3):375–400, 2019.

- Tu and Zhou (2011) J. Tu and G. Zhou. Markowitz meets talmud: A combination of sophisticated and naive diversification strategies. Journal of Financial Economics, 99(1):204–215, 2011. doi: 10.1016/j.jfineco.2010.08.013.

- Warton (2008) D. I. Warton. Penalized normal likelihood and ridge regularization of correlation and covariance matrices. Journal of the American Statistical Association, 103(481):340–349, 2008.

- Witten et al. (2011) D. M. Witten, J. H. Friedman, and N. Simon. New insights and faster computations for the graphical lasso. Journal of Computational and Graphical Statistics, 20(4):892–900, 2011.

- Yuan and Lin (2007) M. Yuan and Y. Lin. Model selection and estimation in the gaussian graphical model. Biometrika, 94(1):19–35, 2007.

- Zakamulin (2015) V. Zakamulin. A test of covariance-matrix forecasting methods. Journal of Portfolio Management, 41(3):97–108, 2015. doi: 10.3905/jpm.2015.41.3.097.

Appendix A Covariance Parameters

Appendix B GMV with short sales

| Sample | LW1 | LW1-CV2 | LWCC | LWCC-CV2 | LWNL | LWNL-CV2 | POET | POET-CV2 | GLASSO | GLASSO-CV2 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Sample | |||||||||||

| LW1 | |||||||||||

| LW1-CV2 | |||||||||||

| LWCC | |||||||||||

| LWCC-CV2 | |||||||||||

| LWNL | |||||||||||

| LWNL-CV2 | |||||||||||

| POET | |||||||||||

| POET-CV2 | |||||||||||

| GLASSO | |||||||||||

| GLASSO-CV2 | |||||||||||

| better than % of models |

-

•