Metastability in a continuous mean-field model

at low temperature

and strong interaction

Abstract

We consider a system of mean-field interacting stochastic differential equations that are driven by Brownian noise and a single-site potential of the form . The strength of the noise is measured by a small parameter (which we interpret as the temperature), and we suppose that the strength of the interaction is given by . Choosing the empirical mean (, ) as the macroscopic order parameter for the system, we show that the resulting macroscopic Hamiltonian has two global minima, one at and one at . Following this observation, we are interested in the average transition time of the system to , when the initial configuration is drawn according to a probability measure (the so-called last-exit distribution), which is supported around the hyperplane . Under the assumption of strong interaction, , the main result is a formula for this transition time, which is reminiscent of the celebrated Eyring-Kramers formula (see [16]) up to a multiplicative error term that tends to as and . The proof is based on the potential-theoretic approach to metastability.

In the last chapter we add some estimates on the metastable transition time in the high-temperature regime, where , and for a large class of single-site potentials.

Key words and phrases. Metastability, Local Cramér theorem, Kramers’ law.

2010 Mathematics Subject Classification. 60F10; 60J60; 60K35; 82C22 00footnotetext: K.B. is partially supported by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) - Projektnummer 211504053 - SFB 1060 and by Germany’s Excellence Strategy – GZ 2047/1, projekt-id 390685813 – “Hausdorff Center for Mathematics” at Bonn University.

In memory of our dear friend and mentor Dmitry Ioffe.

Introduction

By now it is well-known that many stochastic systems exhibit a phenomenon called metastability. A typical situation for this is the following. First, for a relatively long time, the system is trapped in a state, (the metastable state), which is not the (sole) equilibrium state of the system. Second, after many unsuccessful attempts and due to local fluctuations, the system finally makes the transition to the (other) equilibrium state (the stable state). In many cases, this transition is triggered by the appearance of a critical state, and the metastable and the stable states are modelled through local minima of a free energy functional or Hamiltonian corresponding to the system. For a more detailed introduction to metastability, we refer to [13, Chapter 1].

In this paper, we are interested in the metastable behaviour of a system of stochastic differential equations given by

| (0.1) | ||||

where , is an -dimensional Brownian motion, and the single-site potential is given by We consider the strength of the Brownian noise as the temperature of the system.

We proceed as follows. First, in order to analyse the system for large , we choose the empirical mean, , as the macroscopic order parameter. That is, we consider the image of the system under the map . Then, as a result of an improvement of the well-known Cramér theorem for this setting, which we call local Cramér theorem (see Section 1.2), we obtain a function , which we interpret as the macroscopic Hamiltonian of the system. A simple analysis shows that admits exactly two global minima at and , and that admits a unique local maximum at . This fact indicates that our model exhibits metastable behaviour with the two metastable states being the hyperplanes and . The goal of this paper is to compute the average transition time to a region around , when the system is initially close to .

We tackle this goal in two different regimes, the first one being the low-temperature regime, where the strength of the Brownian noise tends to zero, and the second one being the high-temperature regime, where we set . We obtain the following results in this paper.

-

•

In Chapter 2 we show that in the low-temperature regime and under the assumption111The reason for this assumption is that, if , we are able to control the microscopic fluctuations via functional inequalities. We explain this in further detail in Remark 2.9. that , the average transition time is asymptotically given by a formula, which is of a similar form as the well-known Eyring-Kramers formula (see [16]) up to a multiplicative error term that tends to as and . Such a result is often known as Kramers’ law in the literature. See [7] for a review on such results.

-

•

In Chapter 3 we consider the high-temperature regime, where we only show that, as , the average transition time is confined to an interval , where , and are independent of . This result still holds true if we replace by a large class of single-site potentials.

Our proofs are based on the potential-theoretic approach to metastability, which was initiated in the seminal papers [14], [15] [16] and [23]. Here, one uses tools from potential theory to tackle metastability. In particular, one obtains that the average transition time to the (other) equilibrium state can be expressed in terms of quantities from electric networks. More precisely, in terms of capacities, for which powerful variational principles are known. Hence, the computation of sharp estimates basically reduces to an appropriate choice of test functions in those variational principles. The reader is referred to the monograph [13] for an extensive treatment of this approach.

We now provide some remarks on the historical background on metastability results in high-dimensional diffusion models. In the papers [3], [4], [8], and [10], Kramers’ law has been shown for systems of nearest-neighbour interacting stochastic differential equations in low temperature. These models are considered as -dimensional approximations of stochastic partial differential equations. A similar setting was studied in [9], where, instead of the potential-theoretic approach, the so-called path-wise approach to metastability was used. This approach, initiated in [17], first focused on the asymptotic exponential distribution of the transition time to the (other) equilibrium state, and then developed itself upon the Freidlin-Wentzell theory. In this approach, the asymptotic behaviour of the average transition time is computed up to logarithmic equivalence. We refer to the monograph [38] for a comprehensive introduction to this approach.

For high-dimensional mean-field interacting systems in the high-temperature regime (i.e. for the setting of Chapter 3 in this paper), the asymptotic behaviour, up to logarithmic equivalence, of the average transition time has been stated without proof in [18, Theorem 4]. The rough estimates from Chapter 3 provide a slightly improved version of this conjecture under different initial conditions. We explain the relation between the results of Chapter 3 and the conjecture formulated in [18, Theorem 4] in greater detail below Theorem II in Section 1.4. Up to the authors’ best knowledge, besides Chapter 3 of this paper, the only other result which is aimed to verify the conjecture formulated in [18, Theorem 4] is given in [30]. In this paper the system of Chapter 3 is considered but with more general interaction and by restricting the stochastic differential equations (0.1) to a finite torus. The main result in [30] is an estimate on the probability that a transition between the two metastable states occurs in a time interval which is independent of ; see [30, Theorem 1.4] for more details. The latter result provides a lower bound for the average transition time in the conjecture formulated in [18, Theorem 4] for the case that the stochastic differential equations are restricted to the torus.

Hence, only very few metastability results are known for high-dimensional mean-field interacting systems in the high-temperature regime. In contrast to that, the general behaviour of such systems is by now well-understood. For instance, a law of large numbers and a large deviation principle for a much broader class than the system (0.1) is shown in [27] and [19], respectively.

Also the case of high-dimensional mean-field interacting systems in the low-temperature regime (i.e. for the setting of Chapter 2 in this paper) has been studied before; see for instance [32] or [39] and the references therein. However, up to the authors’ best knowledge, the results of Chapter 2 are the first ones on the metastable behaviour of such systems.

We conclude this introduction with a comment on the fact that we consider the case of strong interaction. In the setting of Chapter 3 in this paper this assumption is essential and can not be removed. More precisely, we have to assume that the strength of the interaction is larger than some quantity (cf. Assumption 3.1) in order to ensure that the macroscopic Hamiltonian (recall that in Chapter 3) admits exactly the two global minima . That is, if is too small, the system does not admit metastable behaviour under the order parameter given by the empirical mean. However, the situation is different in Chapter 2. In this chapter we also assume that is larger than some quantity. Namely, we suppose that . But, and this is the crucial difference to Chapter 3, it can also be shown that if , then, for small enough, is a double-well function and consequently the system may admit metastable behaviour. The reason why we nevertheless make this assumption is that, if , we are able to control the microscopic fluctuations via functional inequalities. We explain this in further detail in Remark 2.9. To study the metastable behaviour also for the case is the content of future research. Up to the author’s best knowledge this is still an open problem, and there is no relevant literature on this problem yet.

Outline of the paper.

In Chapter 1, we introduce the model, formulate the main results, and sketch the main ideas of this paper. In Chapter 2, we provide the full details for the proof of Kramers’ law in the low-temperature regime and under the assumption that . In Chapter 3 we compute estimates on the average transition time in the high-temperature regime. Finally, in the appendix, we state some general properties of Legendre transforms, compute certain asymptotic integrals by using Laplace’s method, and provide the proofs of the local Cramér theorem and the equivalence of ensembles, which are the key ingredients in this paper.

Notation.

-

•

denotes the space of Borel probability measures on the topological space .

-

•

For and a Borel map , is the image measure of by .

-

•

In this paper, is always an element of for , and its components are denoted by . and are always elements of .

-

•

Let be a compact set, and let . In this paper, always stands for a function, whose absolute value is bounded by for small enough, for large enough and uniformly in . More precisely, this means that there exist constants , and such that for some function with

(0.2) If, in addition, we have that for all for some , and we write instead of .

-

•

Similarly, always stands for a function, whose absolute value is bounded by for small enough and for large enough. That is, there exist constants , and such that for some function with

(0.3) Finally, we define analogously as .

-

•

Let be a metric space, and . Then, define .

-

•

Let Y be an Euclidean space. Then we say that satisfies the Poincaré inequality with constant if for all ,

(0.4) where denotes the gradient determined by the Euclidean structure of .

1 The model and the results

This chapter is organized as follows. In Section 1.1 we define the microscopic model. Then, in Section 1.2 we introduce the macroscopic order parameter, and collect some result on the energy landscape of the model under this order parameter. In Section 1.3 and 1.4 we formulate the two main results of this paper. For the sake of comprehensibility, in this introductory chapter, we only provide rough formulations of the setting and the main results. For the full details, we refer to the Chapters 2 and 3.

1.1 The microscopic model

Recall the definition of the system given in (0.1). For , let . Recall that we have also introduced the single-site potential and the parameters and .

The Gibbs measure corresponding to this model has the form

| (1.1) |

where is a normalization constant, and, for , the microscopic Hamiltonian is defined by

| (1.2) |

It is well-known that is the unique stationary measure of the process .

1.2 The macroscopic variables and the macroscopic energy landscape

The empirical mean is defined by

| (1.3) |

This operator will act as the order parameter for our microscopic system. That is, in order to analyse the process for large , we study the image of this process under the map . Therefore, intuitively, describes the (long-time) macroscopic behaviour of our microscopic model, and it will be crucial to study the asymptotic behaviour of this measure.

In fact, in Proposition 2.1, we show that, for small enough and for any compact set ,

| (1.4) |

where is the so-called Cramér transform of the Gibbs measure with respect to the single-site potential (or more precisely with respect to the effective single-site potential defined in (2.2)) and is defined in (2.8) and (2.9), and the function is defined by222The second term in the definition of is due to the fact that the interaction part can be rewritten in terms of the square of the empirical mean; see (2.1) and (2.2). In order to fully understand the motivation behind the definition of we refer to Subsection 2.1.1.

| (1.5) |

Since is the law of the empirical mean of a sequence of random variables, (1.4) can be seen as an improvement of the well-known Cramér theorem (cf. [22, Theorem 6.1.3]) for this setting. This explains, why we call this result local Cramér theorem.

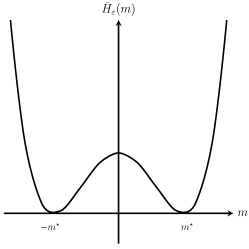

Equation (1.4) shows that, for large and for small enough, is very similar to a Gibbs measure with playing the role of the energy function. Therefore, we consider as the macroscopic Hamiltonian of the system. This suggests to study the analytic properties of the function . We do this in Lemma 2.2, where we show that, for small enough, is a symmetric double-well function with two global minima at and , and with a local maximum at . That is, is of the form given in Figure 1.

1.3 The Eyring-Kramers formula at low temperature

The fact that the macroscopic free energy has two global minima at and suggests that our system exhibits metastable behaviour and the hyperplanes and are the metastable states of the system. More precisely, provided that the initial condition of our system is concentrated in a small region around the hyperplane , we expect that the average transition time to hit a small region around fulfils Kramers’ law. This is the content of the main result of this paper, which is formulated in Theorem I. (For a more detailed explanation and motivation of the result, we refer to Section 2.2.) In this theorem, we suppose that

| (1.6) |

The reason for this assumption is that, in this regime, we are able to control the microscopic fluctuations via functional inequalities. We explain this in further detail in Remark 2.9. To show the metastable behaviour for the case is the content of future research.

Theorem I

Note that, since and is concentrated on , the initial condition of our system is initially close to the metastable state given by the hyperplane . However, the initial condition is random, which is a weakness of our results. As it is suggested by one of the anonymous referees, we believe that we can circumvent this issue by applying the techniques of the papers [1] and [28]. This is planned for future research.

We first collect in Section 2.1 three important ingredients. More precisely, in Subsection 2.1.1 we state the local Cramér theorem (i.e. (1.4)), which is the key tool in our proof to go from the microscopic variables to the macroscopic ones. Then, in Subsection 2.1.2 we study the analytic properties of the macroscopic Hamiltonian and show that its graph is of the form given in Figure 1. And as the third ingredient, we collect in Subsection 2.1.3 the key elements from potential theory that allow us to rewrite the average transition time, , in terms of quantities from electric networks. Namely, we show that is equal to the quotient of the mass of the equilibrium potential and the capacity (see Lemma 2.5).

After we collect these ingredients, we introduce all missing objects of Theorem I and provide the main steps of its proof in Section 2.2. This proof is divided into three steps. The first step consists of showing the correct upper bound for the capacity in Section 2.3. This is done by using the so-called Dirichlet principle (see Lemma 2.6). Here we have to choose an appropriate test function and compute the asymptotic value of the corresponding Dirichlet form. In the second step, we compute in Section 2.4 the lower bound on the capacity by an adaptation of the so-called two-scale approach, which was initiated in the paper [29]. This is the main point, where we use the assumption (1.6). We explain this in further detail in Remark 2.9. Finally, we compute in Section 2.5 the asymptotic value of the mass of the equilibrium potential. This follows from applying standard Laplace asymptotics, and by exploiting that the graph of has the form of a double-well function (cf. Figure 1).

1.4 Rough estimates at high temperature

We also consider in this paper the situation where the microscopic fluctuations in the system do not become negligible. That is, we study the system given by (0.1) with . It is not surprising that the methods that we use for the setting in Section 1.3 do not yield the precise Eyring-Kramers formula in the present case. The reason is that in this case, the entropy of the paths matters substantially, i.e. the microscopic fluctuations do not allow to restrict solely to the macroscopic variables determined by the map . We believe that, in order to obtain the Eyring-Kramers formula, we need to consider the empirical distribution ,

| (1.8) |

as the order parameter instead of the empirical mean determined by the map . A heuristic argument for that is the following.

For all and , let . Using [20, (1.8)], [6, Proposition 3.36] and the formal Riemannian setting on the Wasserstein space introduced in [40, Chapter 1] (or in [26, Section 9.4]), we know that the evolution of can be described by a diffusion-like equation of the form

| (1.9) |

where denotes the duality product on the space of smooth functions, is the free energy functional on the Wasserstein space corresponding to (see [6, Section 3.4]), is the formal gradient of in the Wasserstein space interpreted in the sense of distributions as in [26, Definition 9.36], and is a martingale for all such . Equation (1.9) suggests intuitively that the random perturbations of the process are of order ; see [20, (1.9)] and the comments afterwards for more details. Moreover, (1.9) shows that the potential landscape for this process is given by the free energy functional . This provides a heuristic justification that, in the limit as , one is in a weak noise setting analogously to the setting in [16, (1.1)] but in the infinite dimensional Wasserstein space. We therefore believe that, by adapting the strategy of the proof of [16, Theorem 3.2] to the Wasserstein setting, it should be possible to verify Kramers’ law for .

More precisely, the latter should be done as follows. First, one uses standard results from potential theory in order to represent expected transition times between the metastable states associated to in terms of Dirichlet forms on the Wasserstein space. Second, one has to derive sharp asymptotics of these Dirichlet forms in the limit as . At this point one should benefit from the results obtained in [21] and [43], where a Malliavin calculus is constructed on the Wasserstein space. The rigorous implementation of these thoughts is left for future research.

We note that, in order to show Kramers’ law for , there are also three other approaches to metastability which seem to be applicable. The first one is based on the characterization of Markov processes as unique solutions of martingale problems (see [34] for an introduction), the second one is based on the analysis of the corresponding Poisson equation (see [42]), and the third one is based on an application of the so-called Sandier-Serfaty approach (see [41] for the Sandier-Serfaty approach and [2] for its application to show Kramer’s law).

However, we can still obtain estimates for the mean transition time if the order parameter is given by the empirical mean, i.e. if the macroscopic variables are determined by the map . Here we replace by single-site potentials of the form , where is a symmetric and bounded perturbation of a strictly convex function (cf. Assumption 3.1). Moreover, we have to assume that . This condition is necessary for to be of the form of a double-well function. (Note that the objects are defined as in Theorem I but with replaced by and with .) That is, in the case , we do not have a metastable behaviour for the system under the order parameter given by the empirical mean. This is different than in Theorem I, where we can show that is a double-well function also in the case (see Lemma 2.2). The main result is the following statement.

Theorem II

Suppose Assumption 3.1. Let be the two global minimisers of the macroscopic Hamiltonian . Then, for all large enough and for some , which is independent of ,

| (1.10) | ||||

| (1.11) |

The proof of this result is organized in the same way as the proof of Theorem I, and is given in Chapter 3.

Finally, we compare the results of Theorem II with the conjecture given in [18, Theorem 4]. The authors of [18] expect that for all , there exists such that for the average transition time is confined to the interval , where . Here we have used the simple fact that can be written in terms of the free energy functional from (1.9); see [5, Lemma 2.4] or [37, Section IV.2] for more details on this relation. In contrast to this, Theorem II states that, for large enough, the average transition time is confined to an interval , where are independent of . Hence, in terms of asymptotic precision, our result is an improvement of the conjecture stated in [18].

However, we note that the initial condition in our setting is very different than in the conjecture formulated in [18, Theorem 4]. The initial configuration in Theorem II is randomly drawn according to the last-exit distribution , which is concentrated on (which, similarly as it is explained after Theorem I, is close to the metastable state , since ). In contrast to this, the initial condition in the conjecture formulated in [18, Theorem 4] is given by a sequence of deterministic points such that the corresponding sequence of empirical measures converges (in a topology which is slightly stronger than the weak topology) to a measure from the basin of attraction associated to the metastable state . More explanations and details on the basin of attraction and the energy landscape in this point of view are given in [5, Proposition 1.4 and Lemma 2.4].

2 The Eyring-Kramers formula at low temperature

In order to simplify the notation, we omit in this chapter the superscripts and . For example, we abbreviate and . Moreover, we rewrite the microscopic Hamiltonian (see (1.2)) as

| (2.1) |

where the (effective) single-site potential is defined by

| (2.2) |

Recall that, for the strength of the interaction part in this model, we assume that

| (2.3) |

The outline of this chapter is given after Theorem I in Section 1.3.

2.1 Preliminaries

2.1.1 Local Cramér theorem

This subsection extends the results from [29, Proposition 31] or [35, Section 3]. The goal is to find an asymptotic representation for the measure .

The first observation is that we can disintegrate with respect to explicitly using the coarea formula ([25, Section 3.4.2]). Indeed, as in [29, p. 306], we obtain that

| (2.4) |

for all bounded and measurable , where the conditional measures (or fluctuation measures) are given by

| (2.5) |

Here, denotes the -dimensional Hausdorff measure and is defined by

| (2.6) |

Moreover, for , we obtain the representation

| (2.7) |

for some normalization constant .

It turns out that the asymptotic behaviour of will be determined by the Cramér transform of the measure , which is defined as the Legendre transform of the function

| (2.8) |

That is,

| (2.9) |

Moreover, for , we define the probability measure by

| (2.10) |

is closely related to and . This can be seen in Section A.4 in the appendix, where we list several properties of the Cramér transform that are used in this paper. In particular, we have that and are strictly convex and smooth, and hence, is well defined for all .

In the following proposition we state the local Cramér theorem. (Recall that in Section 1.2 we explain why this result is called like that.) Very similar versions of this result are already known in the literature; see for instance [29, Proposition 31] or [35, Section 3]. The main novelty here is that the result is uniform in .

Proposition 2.1 (Local Cramér theorem)

Suppose (2.3). Let be compact. Then, there exist and such that, for all , and ,

| (2.11) |

In particular, this implies that

| (2.12) |

where

| (2.13) |

Proof. The proof is postponed to Section A.7 in the appendix.

2.1.2 Analysis of the energy landscape

Proposition 2.1 indicates that the graph of determines the macroscopic energy landscape of our system if the order parameter is given by the empirical mean (see also Section 1.2 for more comments). This suggests to study the analytic properties of , which is the content of the following lemma.

Lemma 2.2

Suppose that . Then, for all small enough,

-

(i)

, , and

-

(ii)

has exactly three critical points located at , and for some333Recall the definition of the -,-,-,-notation which is given in the introduction of this paper; in this particular case, this means that there exists a constant such that for all small enough. . Moreover, , and . That is, has a local maximum at , and the two global minima of are located at .

Proof. Part (i) follows from a simple argument, which is based on the fact that is super-quadratic at infinity and on Hölder’s inequality. For instance, a proof can be found in [37, Lemma III.2.6] for a slightly more general setting.

To show part (ii), first note that the condition is equivalent to

| (2.14) |

where we used (A.4.4) to get the first equality, and (A.4.6) and (2.10) to get the second equality. Then, we know from [31, Proposition 3.1 and Theorem 3.2] that, for small enough, there exist exactly three solutions and for (2.14), where .

We now show that in the case . Using (A.4.5) and that we have that for small enough,

| (2.15) |

where we have applied Corollary A.5.2 in the second equality with (and hence ). In order to show that in the case , note that here the function admits exactly two minima at . Hence, by standard Laplace asymptotics we have that for small enough

| (2.16) | |||

The same result holds also for the case , since depends continuously on (cf. Step 5.3 in the proof of [31, Theorem 3.2]).

By the symmetry of , it only remains to show that . First note that, since , for all , the function admits a unique global minimum at some point . Indeed, in the case , this follows by simply observing that is invertible, and in the case , we have to apply Cardano’s formula (see [11, Chapters 1 and 2]). (We omit the details in the latter case, since we do not use the claim of this lemma for the case in the remaining part of this paper.) Then, as above, using (A.4.5) and that implies that for small enough,

| (2.17) | ||||

where we have used Corollary A.5.3 with the function and . This concludes the proof.

Remark 2.3

In the remaining part of this paper, we suppose that is small enough such that .

2.1.3 Potential-theoretic approach to metastability

In this subsection, we quickly review the key ingredients form the potential-theoretic approach to metastability that we need in our setting. We follow [16, Chapter 2], where all the omitted details can be found.

The generator of the stochastic process introduced in Section 1.1 is given by

| (2.18) |

where is the microscopic Hamiltonian (recall (2.1)). We need the following definitions.

Definition 2.4

Let be open and regular and such that and is connected. For any , we write .

-

(i)

The equilibrium potential between and , , is defined as the unique solution to the Dirichlet problem

(2.19) For , we have the probabilistic interpretation that .

-

(ii)

The equilibrium measure, , is defined as the unique measure on such that

(2.20) where is the Green function corresponding to on (cf. [16, (2.2) and (2.3)]).

-

(iii)

The capacity, , of the capacitor is defined by

(2.21) -

(iv)

The last-exit biased distribution on , , is the probability measure on defined by

(2.22)

Before we proceed and collect the other ingredients from potential theory that we need in this paper, we would like to provide a brief intuitive description of the equilibrium measure, , and the last-exit biased distribution on , .

First, heuristically, the equilibrium measure describes the escape probability from towards . That is, it describes the probability to enter without returning to . The reason why this is true can be understood best in the discrete case, i.e. in the case when and are discrete sets. Indeed, in this case, for ; see [13, (7.1.19), (7.1.20) and below (7.1.23)] for more details.

Second, heuristically, the last-exit biased distribution on , , can be seen as the Gibbs measure of the system restricted to and weighted by the escape probability from towards . Intuitively, it describes the Gibbs measure of the system “conditioned” on the event that the next exit from is the final (or last) exit from and leads to the transition towards . In order to explain this more precisely, note that, by (2.22), is given by the measure restricted to and weighted by . Moreover, note that can be seen as the Gibbs measure of the system444 can be seen as the Gibbs measure of the system, since it is the unique stationary measure of the stochastic process and has the form of a Gibbs measure with respect to the microscopic Hamiltonian . and that, as we have explained before, describes the escape probability from towards . In this picture, the capacity, , serves as the normalization constant of the restricted measure .

Using the notions from Definition 2.4 one can rewrite the average hitting time of in the case that the initial condition is randomly chosen according to the last-exit distribution. This is the content of the following lemma.

Lemma 2.5

Consider the same setting as in Definition 2.4. Then,

| (2.23) |

As we already mentioned, the main advantage to use Lemma 2.5 is the availability of variational principles for the capacity. In this paper, we use the so-called Dirichlet principle, which is stated in the following lemma.

Lemma 2.6 (Dirichlet principle)

Consider the same setting as in Definition 2.4. Let

| (2.24) |

and define the Dirichlet form on , , by

| (2.25) |

Then,

| (2.26) |

2.2 The proof of Theorem I

In this section we first introduce all missing ingredients of Theorem I. Afterwards we provide the proof of this theorem. However, as we explained after the formulation of Theorem I in Section 1.3, the main three steps of this proof are moved to Section 2.3, Section 2.4 and Section 2.5, respectively.

Recall that, under (2.3) and for small enough, the macroscopic Hamiltonian admits exactly two global minima . We therefore consider the hyperplanes and as the metastable sets in our system.

The goal in this paper is to use the potential-theoretic setting from Subsection 2.1.3 to compute the average transition time from to for the stochastic process introduced in Section 1.1. However, due to technical reasons, we have to modify this goal in two ways.

First, instead of considering and as the metastable sets, we rather consider and , where

| (2.27) |

Note that, by using the arguments from Step 3 of the proof of Proposition 2.7, we have that

| (2.28) |

Heuristically, the reason for this shift is the following. In the proof of Theorem I we have to compute the integral in the numerator on the right-hand side of (2.23). Using the disintegration (2.4), Proposition 2.1 and the fact that has its global minima at and , we see that this integral is concentrated on the sets . Hence, in order to apply Laplace’s method, we need that the equilibrium potential is equal to or equal to on these sets, respectively.

Second, instead of running the system from some specific point in , we rather have to initialise our system randomly according to the last-exit biased distribution , where are defined by

| (2.29) | ||||

Note that is a probability measure supported on . The main reason for the choice of this initial distribution is that we can exploit the formula (2.23). However, in a finite-dimensional setting, such as in [16], we could also obtain an asymptotic expression for for . This is done by using Harnack inequalities. But since these inequalities depend on the dimension of the base space, we are not able to transfer the strategy used in [16] to our high-dimensional setting.

We are now in the position to prove Theorem I.

2.3 Upper bound on the capacity

Proposition 2.7

Consider the same setting as in Theorem I. Then, for large enough and small enough,

| (2.31) |

Proof. We will obtain the upper bound by using the Dirichlet principle (Lemma 2.6). That is, we introduce a suitable test function and show that the corresponding Dirichlet form is asymptotically given by the right-hand side of (2.31).

Step 1. [Choice of the test function .]

Let and the function be defined by

| (2.32) |

which is well-defined, since is strictly convex. Then, is the equilibrium potential between and corresponding to the invariant measure . That is, is the unique solution to the Dirichlet problem (cf. Definition 2.4, [13, Section 7.2.5] or [13, (11.2.18) and (11.2.19)])

| (2.33) | ||||

The test function that we use in this proof is given by

| (2.34) |

Step 2. [Estimation of the Dirichlet form of .]

Using the Dirichlet principle (Lemma 2.6) we have that

| (2.35) | ||||

where, in the first inequality, we use Lemma 2.6 and the definition of the test function , in the first equality, we use the definition of , and in the second equality, we use the disintegration (2.4).

Applying Proposition 2.1 for and the definition of yields that

| (2.36) |

In Step 4 and 5 of this proof we show that for ,

| (2.37) | ||||

| (2.38) |

And since, by the coarea formula, , (2.37) and (2.38) imply that

| (2.39) | ||||

The integral on the right-hand side of (2.39) can be estimated from below as follows.

| (2.40) |

Step 3. [Some a priori estimates.]

Before we show (2.37) and (2.38), we collect some a priori estimates.

First, we note that there exists such that for all and small enough,

| (2.41) |

where we used (A.4.5) in the second equality, and then applied Lemma A.6.1 (iii). Moreover, recall that in the proof of Lemma 2.2, we have seen that . Therefore, for small enough, .

Next, we note that it is shown in Lemma A.6.1 that there exists and a function such that and for all and . Then, we see that there exists such that for all and for small enough,

| (2.42) | ||||

where we used the second equation in (A.4.5) in the first step, the first equation in (A.4.5) and the third equation in (A.4.6) in the second step, the first equation in (A.4.6) in the third step, and (2.10), (2.41) and Corollary A.5.3 for the function in the last step.

Step 4. [Proof of (2.37).]

By Taylor’s formula, we have for some ,

| (2.43) |

Then, by the estimates from Step 3,

| (2.44) | ||||

2.4 Lower bound on the capacity

In this section, we prove the lower bound on the capacity. The proof is inspired by the two-scale approach, which was initiated in [29]. To apply this approach, we use that by the Bakry-Émery theorem (see for instance [29, p. 305] and [36, Remark 1.2]), satisfies the Poincaré inequality (recall (0.4) from the introduction) with constant . That is, for all , and ,

| (2.47) |

where for .

Proposition 2.8

Consider the same setting as in Theorem I. Then, for large enough and small enough,

| (2.48) |

As in [29, Section 2.1], we split the gradient into its fluctuation part and its macroscopic part . Note that

| (2.50) |

and by [29, Lemma 21],

| (2.51) |

where is the microscopic Hamiltonian defined in (2.1), and, for two functions ,

| (2.52) |

Using (2.4), the fact that for all , Jensen’s inequality and (2.51), we obtain that

| (2.53) | ||||

Then, using Young’s inequality, we have that for all ,

| (2.54) | ||||

Later in this proof we show that

| (2.55) |

and that for some constant , which is independent of and ,

| (2.56) | ||||

By combining (2.54), (2.55) and (2.56) and by choosing

| (2.57) |

we infer that

| (2.58) |

Together with (2.50) this yields that

Applying now Lemma 2.6 implies (2.48). It only remains to show (2.55) and (2.56).

Proof of (2.55). Note that by Proposition 2.1,

| (2.59) | ||||

Then, by the fact that and by our knowledge on one-dimensional capacities (see for instance [13, Section 7.2.5]),

| (2.60) | ||||

Recalling that and by the coarea formula, we conclude (2.55) from standard Laplace asymptotics.

Proof of (2.56). Since is supported on , we have that

| (2.61) |

Then, using Hölder’s inequality and (2.47),

| (2.62) | ||||

It remains to show that the second integral on the right-hand side of (2.62) is bounded from above by for some constant which is independent of and .

First we observe that by symmetry,

| (2.63) | ||||

Then, applying Proposition 2.10, the right-hand side of (2.63) is lower or equal to

| (2.64) |

It remains to show that

| (2.65) |

In order to show (2.65), we again apply the Bakry-Émery theorem (see e.g. [29, p. 305] and [36, Remark 1.2]) to observe that the measure satisfies the Poincaré inequality (see (0.4)) with constant . Hence,

| (2.66) |

Then, using Lemma A.4.1 and Lemma A.6.1 we obtain that for all ,

| (2.67) | ||||

for some constant which is independent of and . Combining (2.66) and (2.67) yields (2.65). This concludes the proof of (2.56).

Remark 2.9

The proof of (2.56) is the main reason for the assumption (2.3). Indeed, in this step, we use that, under (2.3), the (effective) single-site potential defined in (2.2) is strictly convex so that we can apply the Bakry-Émery theorem, which in turn yields that we have a good control on the covariance term in (2.56) for small . Note that, intuitively, the quantity describes the microscopic fluctuation of the system around the hyperplane .

In (2.64) we use that we can pass from expectations with respect to to expectations with respect to . Such a statement is known in the literature as the equivalence of observables (see [33]). The result in our setting is formulated in the following proposition. The proof is postponed to the appendix.

Proposition 2.10 (Equivalence of observables)

Let be compact. Let , and let be such that

| (2.68) |

where . Then, there exist , such that for all ,

| (2.69) |

Proof. The proof is postponed to Section A.8.

2.5 The mass of the equilibrium potential

Proposition 2.11

Consider the same setting as in Theorem I. Then, for small enough,

| (2.70) |

Proof. In this proof, denotes a varying positive constant, which is independent of and .

Step 1. [Splitting into four regions.]

Recall the definition of in (2.27).

Let be a positive number, which is independent of , and , and whose precise value is chosen later in Step 3.

Using that for , we split the left-hand side of (2.70) according to this in the following way.

| (2.71) | ||||

In Step 2 we compute the asymptotic value of the term , and in Step 3 and 4 we show that the terms and are of lower order than .

Step 2. [Estimation of the term .]

Note that, using the same arguments as in Step 4 and Step 5 of the proof of Proposition 2.7, for all ,

| (2.72) | ||||

Then, using the coarea formula in the same way that we did in Subsection 2.1.1 and applying Proposition 2.1 for the compact set , we observe that

| (2.73) | ||||

Using (2.72) and arguing as in the proof of Proposition 2.7, we have that for small enough,

| (2.74) |

Step 2. [Estimation of the terms and .]

We only consider the term . The term can be estimated in the same way.

By using that and by applying the coarea formula and Proposition 2.1 as in Step 1, we have that

| (2.75) | ||||

Note that, similarly as in Step 3 of the proof of Proposition 2.7, we have that . Together with (2.41), this shows that . In the following we prove that , which shows that is of lower order than . Since is symmetric and has its two global minima at , we have that

| (2.76) |

Then, by (2.41), (2.72) and the definition of (see (2.27)),

| (2.77) |

Step 3. [Estimation of the term .]

Using Jensen’s inequality, we have that . Then, via the coarea formula,

| (2.78) | ||||

In Lemma A.7.1, we show that for all ,

| (2.79) |

Therefore, by [12, Lemma 1.1], we have that for small enough,

| (2.80) |

Note that for some . Indeed, by Lemma A.6.1 (ii), we have that for some bounded function ,

| (2.81) | ||||

| (2.82) |

Combining (2.81) and (2.82) with the definition of , shows that for some . Then, choosing large enough, (2.80) implies that

| (2.83) | ||||

This shows that the term is of lower order than , and concludes the proof.

3 Rough estimates at high temperature

In this chapter, we consider the same system as in Chapter 2, but with two key differences. First, we do not consider the low-temperature regime here, that is, throughout this chapter, we suppose that . The second difference is that, instead of , we consider here a class of single-site potentials given by functions of the form , where satisfies Assumption 3.1.

Hence, the microscopic Hamiltonian in this chapter is given by

| (3.1) |

where . We make the following assumptions on the single-site potential .

Assumption 3.1

-

(1)

There is a splitting for some , and there are constants such that

-

(2)

for all .

-

(3)

is convex on .

-

(4)

If is a quadratic function of the form for some , then we suppose that .

-

(5)

.

-

(6)

is locally bounded on .

Remark 3.2

If is a quadratic function, then Assumption 3.1 is not fulfilled for any choice of . However, we do not expect that Kramers’ law holds true in this case, since the macroscopic Hamiltonian is not of double-well form, where is defined as in (2.13) with being replaced by the function and with . Indeed, from (A.7.22), we see that is a quadratic function and hence not of double-well form.

This chapter is organized similarly as Chapter 2. That is, in Section 3.1 we introduce the local Cramér theorem and show that the macroscopic Hamiltonian has a double-well structure. In Section 3.2 we provide the proof of Theorem II. The main part here is the proof of the lower bound on the capacity. This is done in Section 3.3.

3.1 Preliminaries

3.1.1 Local Cramér Theorem.

Replacing by the function and setting , we define the Gibbs measure by (1.1), and introduce a disintegration of as as in and Subsection 2.1.1. Analogously, we define the quantities , , and by (2.6), (2.8), (2.9) and (2.10), respectively, by replacing by the function and setting . Then, the local Cramér theorem in this chapter is given as follows.

Proposition 3.3 (Local Cramér theorem)

3.1.2 Analysis of the energy landscape.

In the following lemma we show that the macroscopic Hamiltonian has the form of a double-well function with at least quadratic growth at infinity.

Lemma 3.4

Suppose Assumption 3.1. If is a quadratic function, then let denote the leading order coefficient. Otherwise, let . Then, we have that

-

(i)

, ,

-

(ii)

there exists and such that for all and for all , and

-

(iii)

has exactly three critical points located at , and for some . Moreover, , and . That is, has a local maximum at , and the two global minima of are located at .

Proof. Since for all , it suffices to prove all claims only on .

(ii). From part (i) and Assumption 3.1 (4), we know that there exist and such that for all . Using that is increasing (since is strictly convex) we obtain that for all ,

| (3.5) |

which concludes the claim.

(iii). Before we show the claims, note that the function is convex on . Indeed, from [24, Theorem 1.2 c)], we know that Assumption 3.1 yields that is concave on (cf. [37, Remark IV.0.4]). Hence, for , we have that , since, due to the convexity of , we have that . Therefore,

| (3.6) |

which shows that is convex.

To show that admits a local maximum at , we observe that, since , we have that . Moreover, Assumption 3.1 implies that . Therefore, and .

It remains to show that there exists a unique point such that and . Using again that , we infer that for small enough,

| (3.7) |

Moreover, by part (ii), we know that there exists such that

| (3.8) |

However, the mean value theorem implies that there exists such that . Together with the fact that is non-decreasing, this implies that for all . This in turn yields that

| (3.9) |

Combining (3.8) and (3.9) shows that, at , there is the unique global minimum of on .

3.2 Proof of Theorem II

In this section we provide the proof of Theorem II. The bulk part of the proof is a straightforward adaptation from the proof of Theorem I. However, the proof of the lower bound on the capacity is modified, since the (effective) single-site potential is not convex in this chapter. The new proof of the lower bound is moved to Section 3.3.

Proof of Theorem II. Let be the two global minimisers of the macroscopic Hamiltonian . Let and be defined by (2.27) and (2.29) with . As in the proof of Theorem I, the starting point is the formula (2.23). Then, proceeding exactly as in the proofs of Proposition 2.7 and Proposition 2.11, we can show that

| (3.10) | ||||

| (3.11) |

which yields (1.10). Finally, (1.11) follows from combining (3.11) with Proposition 3.5. This concludes the proof of this theorem.

3.3 Rough lower bound on the capacity

In this section we prove the rough lower bound on the capacity. We proceed as in the proof of Proposition 2.8. Recall that the critical estimate in the proof of Proposition 2.8 is given by (2.56), where we apply the Poincaré inequality for the fluctuation measure with a constant which is of order (see (2.47)). By using the strict convexity of the (effective) single-site potential, (2.47) is a consequence of the Bakry-Émery theorem. Since the (effective) single-site potential is not assumed to be strictly convex in this chapter, the Bakry-Émery theorem is not applicable here. However, instead, we can apply [35, Theorem 1.6], where it is shown that for all and , satisfies the Poincaré inequality with a constant , which is independent of and . That is, for all and and for all ,

| (3.12) |

where for . This is the main ingredient of the proof of the following proposition.

Proposition 3.5

Proof. Let . We proceed exactly as in the proof of Proposition 2.8, and obtain that for all ,

| (3.15) | ||||

Therefore, choosing it remains to show that

| (3.16) |

In order to show (3.16), note that as in (2.62),

| (3.17) | ||||

Then, we proceed analogously to (2.63) to observe that by the equivalence of ensembles (Proposition 3.6),

| (3.18) | ||||

This concludes the proof of (3.16).

It remains to show the equivalence of observables, which was used in (3.18). This is done in the following proposition.

Proposition 3.6 (Equivalence of observables)

Let , and let be such that

| (3.19) |

where . Then there exists such that for large enough,

| (3.20) |

Proof. Proceeding exactly as in the proof of Proposition 2.10, we observe that the claim is proven once we show that

-

(i)

the local Cramér theorem holds true in this setting,

-

(ii)

, where , and

-

(iii)

there exists such that for all .

Claim (i) is shown in Proposition 3.3, and claim (ii) and (iii) are shown in [35, Lemma 3.2]. This concludes the proof of this proposition.

Appendix

This appendix is organized as follows. In Section A.4 we collect several properties of Cramér transforms and the cumulant generating functions. In Section A.5 we derive asymptotic expressions for certain integrals by using standard Laplace asymptotics. Then, in Section 3.3 we apply these results to estimate the moments and the Fourier transforms of the measure (see (2.10)) for small . Finally, in Section A.7 and Section A.8 we state and prove the local Cramér theorem and the equivalence of observables, respectively.

We note that the proofs in Section A.7 and Section A.8 remain true if we replace the effective single-site potentials by some general strictly convex function .

A.4 Properties of the Cramér transform

Lemma A.4.1

Let be such that Let

| (A.4.1) |

and let denote its Legendre transform, i.e.

| (A.4.2) |

For all , define by

| (A.4.3) |

Then, the following statements hold true.

-

(i)

and are strictly convex and smooth. If is even, then and are also even.

-

(ii)

For , we have that

(A.4.4) In particular,

(A.4.5) -

(iii)

For all ,

(A.4.6)

A.5 Some asymptotic integrals

The main result in this section is the following lemma, which is based on Laplace asymptotics. In the proof we use the same strategy as in [31, Lemma A.3].

Lemma A.5.1

Let be a compact set. Let , and for , let . Suppose that there exist and such that, for all , admits a unique global minimum at some point with and such that for all . Furthermore, we assume that the map is bounded on . Then, for each , and ,

| (A.5.1) |

where for , denotes the double factorial, and we make the convention that . Moreover,

| (A.5.2) | ||||

Proof. Fix . In this proof, let denote a varying positive constant, which is independent of and .

Step 1. [Proof of (A.5.1).]

Let and .

Let be such that, for some , for all .

Then,

| (A.5.3) | ||||

In the following we show that provides the main contribution and that and are negligible.

Step 1.1. [Estimation of the term .]

Note that by Taylor’s formula, for some ,

| (A.5.4) |

By using that is locally bounded (uniformly in ), we see that there exists some such that for all . Therefore,

| (A.5.5) |

Thus, by using the definition of and by some standard Gaussian computations applied to the denominator in (A.5.5), we infer that

| (A.5.6) |

Step 1.2. [Estimation of the term .]

We know that and for all .

Hence, by [12, Lemma 1.1],

| (A.5.7) |

Since , this shows that

| (A.5.8) |

Step 1.3. [Estimation of the term .]

Since

has its unique minimum in ,

we have that for small enough,

.

Without restriction, we suppose that .

Then, by using (A.5.4) and the arguments from Step 1.1,

| (A.5.9) |

Using the definition of , we have shown that

| (A.5.10) |

Step 2. [Proof of (A.5.2).]

To show (A.5.2) we proceed exactly as in Step 1 (with replacing ) but with the only difference

that here we estimate the leading order term in the following way.

The idea is based on Step 2.3 of the proof of [31, Lemma A.3].

First, by adding one more term in the Taylor expansion in (A.5.4), we have that for some ,

| (A.5.11) |

where for , we abbreviate . Then,

| (A.5.12) | ||||

We now show that the term provides the dominant contribution and that and are of lower order than . Concerning , simple Gaussian computations as in Step 1.1 yield that

| (A.5.13) |

For we use that is locally bounded to obtain that

| (A.5.14) |

Finally, to estimate the term , note that and are locally bounded, and that . Then, by using the inequality ,

| (A.5.15) | ||||

This concludes the proof of (A.5.2).

Corollary A.5.2

Proof. To show (A.5.16), similarly as in Step 5 in the proof of [31, Lemma A.3], we apply (A.5.1) both to the numerator and to the denominator on the left-hand side of (A.5.16). Analogously, we apply (A.5.2) to the numerator and (A.5.1) to the denominator to show (A.5.17).

To show (A.5.18), we first introduce the measure . Then, the left-hand side of (A.5.18) is equal to

| (A.5.20) | ||||

Using (A.5.16) and (A.5.17), it is easy to see that for each ,

| (A.5.21) | ||||

It remains to show (A.5.19). Similarly as in (A.5.20), we have that the left-hand side of (A.5.19) is equal to

| (A.5.22) | ||||

| (A.5.23) |

As above, we observe that all the summands in (A.5.23) are of lower order. Then, using (A.5.16) and (A.5.17) for the two terms in (A.5.22), we infer (A.5.19).

Finally in this section, we note that Lemma A.5.1 and Corollary A.5.2 remain true if the function is allowed to slightly depend on . This is the content of the following corollary.

Corollary A.5.3

Let be a compact set and let . Let and let be such that

| (A.5.24) |

Let be defined by

| (A.5.25) |

For each , we write for all . Suppose that there exists and such that, for all , admits a unique global minimum at some point with and such that for all . Furthermore, we assume that the map is bounded on . Then, the statements (A.5.16)–(A.5.19) hold true if is replaced by and by .

A.6 A priori estimates for the measure

For the proof of the local Cramér theorem and the equivalence of observables we need some estimates on certain moments and Fourier transforms of (see (2.10)).

Lemma A.6.1

Recall the definition of , , and given in (2.2), (2.8), (2.9) and (2.10). Notice that the inverse of exists.

-

(i)

Let be compact. Then, for all , .

-

(ii)

For all compact intervals there exists and a function such that and for all and .

-

(iii)

For , let

(A.6.1) Note that is well-defined, since is strictly convex (see Lemma A.4.1). Then, for each compact interval , there exist and such that for all and for all ,

(A.6.2)

Proof. (i). Note that for all , the function satisfies the same conditions as the function from Corollary A.5.2. In particular, admits a unique global minimum at . Thus, part (i) follows immediately from Lemma A.4.1 and (A.5.17).

(ii). Let for some with . Set . From part (i), we know that for small enough,

| (A.6.3) | ||||

Therefore, by the continuity of and the mean value theorem, . We also know that is bijective, since is strictly increasing. Setting now for yields that

| (A.6.4) |

Since (cf. (A.4.4)), this concludes the proof of part (ii).

(iii). Let . Then, using part (ii), Lemma A.4.1 and Corollary A.5.3, we know that for and for all ,

| (A.6.5) | ||||

Then, for , the left-hand side of (A.6.5) equals (cf. Lemma A.4.1). Thus, (A.6.5) proves the first claim in (A.6.2), since the map is locally bounded. Moreover, due to Hölder’s inequality, to show the second claim in (A.6.2), it suffices to show that there exists such that

| (A.6.6) |

However, combining (A.6.5) for and the first claim in (A.6.2), implies (A.6.6). This conclude the proof of part (iii).

Lemma A.6.2

Consider the same setting as in Lemma A.6.1. Let be compact, and abbreviate . Then, there exists such that for all ,

| (A.6.7) |

Proof. Fix . In this proof denotes a constant, which is independent of and , and may change every time it appears.

Let , where is introduced in Lemma A.6.1. Then, by partial integration (as in [35, p. 37]) and by (A.6.2),

| (A.6.8) | ||||

Let be the unique global minimum of , and let for some large enough. Then, using the same arguments as in the proof of Lemma A.5.1, we see that the integral in the numerator on the right-hand side of (A.6.8) is concentrated around , i.e.

| (A.6.9) | ||||

Moreover, by Taylor’s formula for some (cf. (A.5.4)),

| (A.6.10) | ||||

Combining (A.6.8), (A.6.9) and (A.6.10) and applying (A.5.1) to the denominator in the right-hand side of (A.6.8) yields (A.6.7). This concludes the proof.

A.7 Proof of the local Cramér theorem

In this section we prove the local Cramér theorem (Proposition 2.1). The main ideas of the proof are the same as in [29, Proposition 31] or [35, Section 3]. The main difficulty here is to show that the estimates are uniform in .

Proof of Proposition 2.1. Fix . In this proof denotes a varying constant, which is independent of , and , but may depend on .

Let be defined by (A.6.1). In order to simplify the presentation here, for any function and for all , we abbreviate

| (A.7.1) |

Step 1. [New representation of .]

Let be a sequence of random variables that are independent and identically distributed with common law . Let

| (A.7.2) |

and let denote the Lebesgue density of the distribution of . As in [35, (31)], using the coarea formula, we have that

| (A.7.3) |

Moreover, let be the Lebesgue density of the distribution of

| (A.7.4) |

Then, by Lemma A.4.1,

| (A.7.5) |

Therefore, it suffices to show that for small enough,

| (A.7.6) |

We show (A.7.6) by mimicking the arguments of the proof of [35, Proposition 3.1]. Therefore, as in [35, (44)], we apply the inverse Fourier transform to obtain that

| (A.7.7) |

and we split this integral according to some (which is chosen in Step 2) as

| (A.7.8) | ||||

In the following we compute the asymptotic value of , and show that is of lower order than .

Step 2. [Estimation of the term .]

From Lemma A.6.1 we know that there exists such that

| (A.7.9) |

Then, as in [35, (46)], the estimate (A.7.9) yields that there exist and a complex-valued function such that for all and all ,

| (A.7.10) |

Indeed, applying Taylor’s formula yields that for all ,

| (A.7.11) |

Notice that by (A.7.9). Therefore, by applying Taylor’s formula for the function for with small enough, we obtain (A.7.10).

As a consequence of (A.7.10), by choosing , we have that

| (A.7.12) |

Moreover, by arguing similarly as in [35, (69)], (A.7.10) yields that for small enough,

| (A.7.13) |

This in turn implies that, by proceeding as in [35, p. 32],

| (A.7.14) |

which yields, as in [35, p. 32], to the estimate

| (A.7.15) | ||||

Step 3. [Estimation of the term .]

It remains to show that the term is negligible.

Recall from Lemma A.6.1 and Lemma A.6.2 that there exist such that for all ,

| (A.7.16) |

Then, following the proof of [35, Lemma 3.4], the estimates in (A.7.16) (which are the analogues of [35, (52)] and [35, (53)]) imply that for all there exists (which depends only on and ) such that

| (A.7.17) |

Finally, applying the same arguments as in [35, p. 32] shows that

| (A.7.18) |

Hence, for large enough. This concludes the proof.

As a simple consequence of the ideas from the proof of Proposition 2.1, we can state the result in a more precise way in the trivial case that the (effective) single-site potential is a quadratic function. The result is given in the following lemma.

Lemma A.7.1

Proof. Using the same notation and the same arguments as in Step 1 of the proof of Proposition 2.1, we see that it suffices to show that

| (A.7.21) |

Note that by a simple computation, for all ,

| (A.7.22) | ||||

In particular, is a Gaussian measure. Therefore, the claim (A.7.21) is a simple consequence of the stability of Gaussian measures under convolution.

A.8 Proof of the equivalence of observables

In this section we prove the equivalence of observables, which is stated in Proposition 2.10. The proof is similar to the proof of Proposition 2.1 and combines the ideas from [33] and [35].

Proof of Proposition 2.10. For simplicity, we only consider the case . A straightforward modification of the following proof yields the claim also in the case .

Fix . In this proof, let denote a varying positive constant, which does not depend on and , but may depend on and .

Step 1. [Cramér’s representation.]

Proceeding as in [33], we use the so-called Cramér representation in order to rewrite the left-hand side of (2.69) in terms of the density of a certain random variable.

Let , and let, for , the measure be defined by

| (A.8.1) |

where denotes the normalization constant. Note that . Let be a random vector distributed according to , and let

| (A.8.2) |

Let denote the Lebesgue density of the distribution of . Note that , where is defined in Step 1 of the proof of Proposition 2.1. Using the same arguments as in [33, Lemma 5 and Lemma 6], we observe that

| (A.8.3) | ||||

Hence, in order to show (2.69), It suffices to show that there exist and such that for all , and ,

| (A.8.4) | ||||

| (A.8.5) |

where is defined in (A.6.1).

Step 2. [Proof of (A.8.5).]

Using the same arguments as in Step 1 of the proof of Proposition 2.1, we observe that

| (A.8.6) |

Step 3. [Proof of (A.8.4).]

Recall the abbreviations from (A.7.1).

Let be a random vector distributed according to , and let be a random variable distributed according to .

By [33, Lemma 7], we have that

| (A.8.7) | ||||

It remains to show that for large enough,

| (A.8.8) |

In order to show (A.8.8), we proceed as in the proof of [35, Proposition 3.1] and Proposition 2.1. Let and be given as in Step 2 of the proof of Proposition 2.1. We split the integral on the left-hand side in (A.8.8) according to some (which is chosen in Step 3.1) as

| (A.8.9) |

We now show that .

Step 3.1. [Estimation of the term .]

This step is very similar to Step 2 of the proof of Proposition 2.1.

Using (A.7.10), we have that there exists such that

| (A.8.10) |

Similarly as in (A.7.13), this inequality yields that for and for small enough,

| (A.8.11) |

and hence, as in (A.7.14),

| (A.8.12) |

This implies that

| (A.8.13) | ||||

since, in view of (2.68),

| (A.8.14) |

Moreover, by Taylor’s formula, for some ,

| (A.8.15) | ||||

Using (2.68) and that implies that .

Step 3.2. [Estimation of the term .]

First note that by using (A.8.14) it only remains to show that

| (A.8.16) |

Then, a straightforward adaptation of the arguments in Step 3 of the proof of Proposition 2.1 yields the claim.

Acknowledgement. The authors would like to give many thanks to Anton Bovier, Lorenzo Dello Schiavo, Dmitry Ioffe and André Schlichting for many useful discussions and suggestions. Moreover, the authors would like to thank the anonymous referees for numerous helpful comments and for having read the paper with great care.

References

- [1] I. Armendáriz, S. Grosskinsky, and M. Loulakis. Metastability in a condensing zero-range process in the thermodynamic limit. Probab. Theory Related Fields, 169(1-2):105–175, 10 2017.

- [2] S. Arnrich, A. Mielke, M. A. Peletier, G. Savaré, and M. Veneroni. Passing to the limit in a Wasserstein gradient flow: from diffusion to reaction. Calc. Var. Partial Differential Equations, 44(3-4):419–454, 2012.

- [3] F. Barret. Sharp asymptotics of metastable transition times for one dimensional SPDEs. Ann. Inst. Henri Poincaré Probab. Stat., 51(1):129–166, 2015.

- [4] F. Barret, A. Bovier, and S. Méléard. Uniform estimates for metastable transition times in a coupled bistable system. Electron. J. Probab., 15:no. 12, 323–345, 2010.

- [5] K. Bashiri. On the long-time behaviour of mckean-vlasov paths. Electron. Commun. Probab., 25:no. 52, 14, 2020.

- [6] K. Bashiri and A. Bovier. Gradient flow approach to local mean-field spin systems. Stochastic Process. Appl., 130(3):1461–1514, 2020.

- [7] N. Berglund. Kramers’ law: validity, derivations and generalisations. Markov Process. Related Fields, 19(3):459–490, 2013.

- [8] N. Berglund, G. Di Gesù, and H. Weber. An Eyring-Kramers law for the stochastic Allen-Cahn equation in dimension two. Electron. J. Probab., 22:Paper No. 41, 27, 2017.

- [9] N. Berglund, B. Fernandez, and B. Gentz. Metastability in interacting nonlinear stochastic differential equations. II. Large- behaviour. Nonlinearity, 20(11):2583–2614, 2007.

- [10] N. Berglund and B. Gentz. Sharp estimates for metastable lifetimes in parabolic SPDEs: Kramers’ law and beyond. Electron. J. Probab., 18:no. 24, 58, 2013.

- [11] J. Bewersdorff. Algebra für Einsteiger. Friedr. Vieweg & Sohn, Wiesbaden, second edition, 2004. Von der Gleichungsauflösung zur Galois-Theorie.

- [12] A. Bovier. Gaussian processes on trees, volume 163 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, 2017. From spin glasses to branching Brownian motion.

- [13] A. Bovier and F. den Hollander. Metastability, volume 351 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer, Cham, 2015. A potential-theoretic approach.

- [14] A. Bovier, M. Eckhoff, V. Gayrard, and M. Klein. Metastability in stochastic dynamics of disordered mean-field models. Probab. Theory Related Fields, 119(1):99–161, 2001.

- [15] A. Bovier, M. Eckhoff, V. Gayrard, and M. Klein. Metastability and low lying spectra in reversible Markov chains. Comm. Math. Phys., 228(2):219–255, 2002.

- [16] A. Bovier, M. Eckhoff, V. Gayrard, and M. Klein. Metastability in reversible diffusion processes. I. Sharp asymptotics for capacities and exit times. J. Eur. Math. Soc. (JEMS), 6(4):399–424, 2004.

- [17] M. Cassandro, A. Galves, E. Olivieri, and M. E. Vares. Metastable behavior of stochastic dynamics: a pathwise approach. J. Statist. Phys., 35(5-6):603–634, 1984.

- [18] D. A. Dawson and J. Gärtner. Large deviations and tunnelling for particle systems with mean field interaction. C. R. Math. Rep. Acad. Sci. Canada, 8(6):387–392, 1986.

- [19] D. A. Dawson and J. Gärtner. Large deviations from the McKean-Vlasov limit for weakly interacting diffusions. Stochastics, 20(4):247–308, 1987.

- [20] D. A. Dawson and J. Gärtner. Large deviations, free energy functional and quasi-potential for a mean field model of interacting diffusions. Mem. Amer. Math. Soc., 78(398):iv+94, 1989.

- [21] L. Dello Schiavo. The Dirichlet-Ferguson Diffusion on the Space of Probability Measures over a Closed Riemannian Manifold. Preprint, arXiv:1811.11598, 2019.

- [22] A. Dembo and O. Zeitouni. Large deviations techniques and applications, volume 38 of Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, 2010. Corrected reprint of the second (1998) edition.

- [23] M. Eckhoff. Precise asymptotics of small eigenvalues of reversible diffusions in the metastable regime. Ann. Probab., 33(1):244–299, 2005.

- [24] R. S. Ellis, J. L. Monroe, and C. M. Newman. The ghs and other correlation inequalities for a class of even ferromagnets. Comm. Math. Phys., 46(2):167–182, 1976.

- [25] L. C. Evans and R. F. Gariepy. Measure theory and fine properties of functions. Studies in Advanced Mathematics. CRC Press, Boca Raton, FL, 1992.

- [26] J. Feng and T. G. Kurtz. Large deviations for stochastic processes, volume 131 of Mathematical Surveys and Monographs. American Mathematical Society, Providence, RI, 2006.

- [27] J. Gärtner. On the McKean-Vlasov limit for interacting diffusions. Math. Nachr., 137:197–248, 1988.

- [28] A. Gaudillière, P. Milanesi, and M. E. E. Vares. Asymptotic exponential law for the transition time to equilibrium of the metastable kinetic Ising model with vanishing magnetic field. J. Statist. Phys., 179(2):263–308, Apr. 2020.

- [29] N. Grunewald, F. Otto, C. Villani, and M. G. Westdickenberg. A two-scale approach to logarithmic Sobolev inequalities and the hydrodynamic limit. Ann. Inst. Henri Poincaré Probab. Stat., 45(2):302–351, 2009.

- [30] R. S. Gvalani and A. Schlichting. Barriers of the mckean–vlasov energy via a mountain pass theorem in the space of probability measures. J. Funct. Anal., page 108720, 2020.

- [31] S. Herrmann and J. Tugaut. Non-uniqueness of stationary measures for self-stabilizing processes. Stochastic Process. Appl., 120(7):1215–1246, 2010.

- [32] S. Herrmann and J. Tugaut. Mean-field limit versus small-noise limit for some interacting particle systems. Commun. Stoch. Anal., 10(1):39–55, 2016.

- [33] Y. Kwon and G. Menz. Decay of correlations and uniqueness of the infinite-volume Gibbs measure of the canonical ensemble of 1d-lattice systems. J. Stat. Phys., 176(4):836–872, 2019.

- [34] C. Landim. Metastable Markov chains. Probab. Surv., 16:143–227, 2019.

- [35] G. Menz and F. Otto. Uniform logarithmic Sobolev inequalities for conservative spin systems with super-quadratic single-site potential. Ann. Probab., 41(3B):2182–2224, 2013.

- [36] G. Menz and A. Schlichting. Poincaré and logarithmic Sobolev inequalities by decomposition of the energy landscape. Ann. Probab., 42(5):1809–1884, 2014.

- [37] P. E. Müller. Limiting properties of a continuous local mean-field interacting spin system: Hydrodynamic limit, propagation of chaos, energy landscape and large deviations. PhD thesis, Rheinische Friedrich-Wilhelms-Universität Bonn, 2016.

- [38] E. Olivieri and M. E. Vares. Large deviations and metastability, volume 100 of Encyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, 2005.

- [39] C. Orrieri. Large deviations for interacting particle systems: joint mean-field and small-noise limit. Electron. J. Probab., 25:44 pp., 2020.

- [40] F. Otto. The geometry of dissipative evolution equations: the porous medium equation. Comm. Partial Differential Equations, 26(1-2):101–174, 2001.

- [41] E. Sandier and S. Serfaty. Gamma-convergence of gradient flows with applications to Ginzburg-Landau. Comm. Pure Appl. Math., 57(12):1627–1672, 2004.

- [42] I. Seo. Analysis of metastable behavior via solutions of poisson equations. Preprint. arXiv:1905.00743, 2019.

- [43] M.-K. von Renesse and K.-T. Sturm. Entropic measure and Wasserstein diffusion. Ann. Probab., 37(3):1114–1191, 2009.