Bu, Simchi-Levi, and Xu

Online Pricing with Offline Data

Online Pricing with Offline Data:

Phase Transition and Inverse Square Law

Jinzhi Bu \AFFDepartment of Logistics and Maritime Studies, Faculty of Business, The Hong Kong Polytechnic University, Hung Hom, Kowloon, Hong Kong, \EMAILjinzhi.bu@polyu.edu.hk \AUTHORDavid Simchi-Levi \AFFInstitute for Data, Systems, and Society, Massachusetts Institute of Technology, Cambridge, MA 02139, \EMAILdslevi@mit.edu \AUTHORYunzong Xu \AFFInstitute for Data, Systems, and Society, Massachusetts Institute of Technology, Cambridge, MA 02139, \EMAILyxu@mit.edu

This paper investigates the impact of pre-existing offline data on online learning, in the context of dynamic pricing. We study a single-product dynamic pricing problem over a selling horizon of periods. The demand in each period is determined by the price of the product according to a linear demand model with unknown parameters. We assume that before the start of the selling horizon, the seller already has some pre-existing offline data. The offline data set contains samples, each of which is an input-output pair consisting of a historical price and an associated demand observation. The seller wants to utilize both the pre-existing offline data and the sequentially-revealed online data to minimize the regret of the online learning process.

We characterize the joint effect of the size, location and dispersion of the offline data on the optimal regret of the online learning process. Specifically, the size, location and dispersion of the offline data are measured by the number of historical samples , the distance between the average historical price and the optimal price , and the standard deviation of the historical prices , respectively. For the single-historical-price setting where the historical prices are identical, we prove that the best achievable regret is . For the (more general) multiple-historical-price setting where the historical prices can be different, we show that the best achievable regret is . For both settings, we design a learning algorithm based on the “Optimism in the Face of Uncertainty” principle, which strikes a balance between exploration and exploitation, and achieves the optimal regret up to a logarithmic factor. Our results reveal surprising transformations of the optimal regret rate with respect to the size of the offline data, which we refer to as phase transitions. In addition, our results demonstrate that the location and dispersion of the offline data also have an intrinsic effect on the optimal regret, and we quantify this effect via the inverse-square law. \KEYWORDSdynamic pricing, online learning, offline data, phase transition, inverse-square law

1 Introduction

Classical statistical learning theory distinguishes between offline learning and online learning. Offline learning deals with the problem of finding a predictive function based on the entire training data set. The performance of an offline learning algorithm is typically measured by its generalization error (also known as the out-of-sample error) or sample complexity (see, e.g., Hastie et al. 2005). In contrast to the offline learning setting where the entire training data set is directly available before the offline learning algorithm is applied, online learning deals with a setting where data become available in a sequential manner that may depend on the actions taken by the online learning algorithm. The performance of online learning algorithms is typically measured by the regret111In this paper, when we discuss online learning, we focus more on the literature of stochastic online learning, where the online sequential data arrive in a stochastic manner. There is a vast literature of online learning focusing on the non-stochastic setting where the online sequential data arrive in an adversarial manner (see Cesa-Bianchi and Lugosi 2006), which is not the emphasis of this paper.. While offline learning assumes access to offline data (but not online data) and online learning assumes access to online data (but not offline data), in reality, a broad class of real-world problems incorporate both aspects: there is an offline historical data set (based on historical actions) at the time that the learner starts an online learning process.

Currently, there is no standard framework for the above type of learning problems, as classical offline learning theory and online learning theory have different settings and goals. While establishing a framework that bridges all aspects of offline learning and online learning is generally a very complicated task, in this paper, we propose a framework that bridges the gap between offline learning and online learning in a specific problem setting, which, however, already captures the essence of many dynamic pricing problems that sellers face in practice.

1.1 The Model: Online Pricing with Offline Data

In this paper, we study the Online Pricing with Offline Data (OPOD) problem. Consider a firm selling a single product with an infinite amount of inventory over a selling horizon of periods. In each period , the seller chooses a price from a given interval to offer to its customers, and then observes random demand . We assume that the demand in each period is a linear function of the price plus some random noise. Specifically, for each ,

| (1) |

where and are two unknown demand parameters in the known interval and respectively, and are i.i.d. random variables with zero mean and unknown distribution. We assume that is an -sub-Gaussian random variable, i.e., there exists a constant such that for any . For notational convenience, let and , and we use to denote any possible vector in parameter space .

The seller’s single-period expected revenue is the price offered to the customer multiplied by the associated expected demand. To emphasize the dependence on the parameter values, for any , we define the expected revenue function as . Let be the price that maximizes over the interval , i.e., , and use to denote the true optimal price, i.e., . Let be the optimal expected revenue under demand parameter , i.e., . Without loss of generality,222This is because for any , , and we can choose and such that , which guarantees that is an interior point of interval . we assume that for any , the optimal price is an interior point of price range , and therefore .

Historical prices and offline data. In reality, the seller does not know the true demand model, but has to learn such information from the historical data. In this paper, we assume that the seller has some pre-existing offline data before the start of the online learning process. The offline data set contains independent samples: , where are fixed prices, and each is a demand observation under historical price , drawn independently according to the underlying linear demand model (1). Therefore, for each , for some i.i.d. random variables with the same distribution as that of .

Pricing policies and performance metrics. For each , let be the vector of information available at the beginning of period , i.e., . A pricing policy is defined as a sequence of functions , where each is a measurable function which maps the realization of (and possibly some external randomness) to a feasible price in . Let be the set of all pricing policies. For any policy , the regret of , denoted by , is defined as the difference between the optimal expected revenue generated by the clairvoyant policy that knows the exact value of and the expected revenue generated by pricing policy , i.e.,

1.2 Research Question, Observations and Challenges

This paper is inspired by the objective of bridging the gap between offline learning and online learning. The following question naturally arises whenever the offline data are incorporated into the online decision making: how do the offline data affect the statistical complexity of online learning? To address this question, the first challenge is to identify the key characteristics of the offline data that intrinsically affect the complexity of the online learning task.

Intuitively, the size of the offline data, measured by the number of historical samples , and the dispersion of the offline data, measured by the standard deviation of historical prices , i.e., , provide two important metrics that enable quantifying the amount of information collected before the online learning process starts. As becomes larger, or increases, the seller can form a better estimation for the unknown demand parameters using offline regression, and the regret may decrease accordingly.

Another crucial, and more intriguing metric of the offline data, is the location of the offline data, which is measured by , i.e., the distance between the average historical price and the optimal price . We refer to as the generalized distance, as it intuitively quantifies how far the offline data set is “away” from the (unknown) optimal decision. This is a crucial metric that uniquely appears when offline data are incorporated into the online learning process. Indeed, if there are no offline data available before the start of the online learning process, then there is no at all. Also, if the offline data are only used for estimation or prediction, with no need of online decision making, i.e., the seller is purely interested in estimating the model parameters from the offline data and does not need to make any online pricing decisions, then does not affect her estimation accuracy. Surprisingly, as we prove in this paper, when the offline data are incorporated into online learning, this metric will play a fundamental role.

Besides identifying the above three characteristics of the offline data, a key challenge is to precisely quantify the effects of these offline data characteristics on the online learning task. Specifically, we seek to understand to what extent these three metrics of the offline data influence the behavior and growth rate of the best-achievable regret bound. On the algorithmic side, we also seek to design a simple, intuitive and easy-to-implement pricing policy that exploits the values of both the pre-existing offline data and sequentially-revealed online data, and achieves a tight regret bound with respect to the selling horizon , as well as the three metrics of the offline data, i.e., , , . Moreover, since the generalized distance is completely unknown to the seller, the algorithm itself cannot use any information about , which implies a more challenging task of designing a learning algorithm whose performance is as good as if were known.

1.3 Main Results and Technical Highlights

In this paper, we address the above challenges in two settings: (i) single-historical-price setting where all the historical prices are identical, i.e., , and (ii) multiple-historical-price setting where the historical prices can be different, i.e., . We next summarize our main results and technical highlights. Throughout this paper, we use and to present upper and lower bounds on the growth rate up to logarithmic factors, and to characterize the rate when the upper and lower bounds match (up to logarithmic factors). In addition, we use and to denote and respectively. More formal definitions of these notations are provided in §1.5. For any , and .

Single-historical-price setting. For the single-historical-price setting, we develop a learning algorithm called Online and Offline–OFU (O3FU) algorithm, where OFU refers to the principle of Optimism in the Face of Uncertainty, which arises from multi-armed bandits and is widely used in the literature on bandits (see, e.g., Dani et al. 2008, Abbasi-Yadkori et al. 2011). In general, this principle suggests taking actions based on an optimistic guess of the reward associated with each action in each period. We show that the regret of O3FU algorithm has an upper bound . Although this upper bound depends on the unknown quantity , the algorithm itself does not require any information about . In addition, we prove an information-theoretic lower bound which matches the upper bound, showing that the regret bound cannot be further improved by other algorithms (in a certain sense); we define such an unimprovable regret bound as the optimal (instance-dependent) regret for the OPOD problem in the single-historical-price setting. We summarize its rate in Table 1. In particular, when , or and is a constant independent of , the results in the leftmost and rightmost cases with in Table 1 recover those in Keskin and Zeevi (2014).

Multiple-historical-price setting. For the general setting that the historical prices may be different, we modify O3FU algorithm by adding a preliminary step that detects whether a corner case happens or not, and propose the Modified O3FU (M-O3FU) algorithm. We prove that M-O3FU algorithm achieves the regret upper bound , except for a corner case where the upper bound becomes .333This corner case rarely happens because it requires the generalized distance to be very small and the price variance to be very large, such that there is no need of online learning. See the discussion in §4.2. In addition, we prove an information-theoretic lower bound that matches the upper bound for both cases, showing that our regret bound cannot be further improved (in a certain sense); we define such an unimprovable regret bound as the optimal (instance-dependent) regret for the OPOD problem in the multiple-historical-price setting. We summarize its rate in Table 2.

Sufficient condition for self-exploration. As a byproduct, we provide a sufficient condition for the myopic (i.e., greedy) policy to self-explore in the online learning process. Specifically, if the variance of historical prices is sufficiently large, and the average historical price is found to be bounded away from the confidence interval for the optimal price constructed from offline regression, then the myopic policy, the one that always charges the optimal price associated with the least-square estimate obtained in each round, achieves the optimal regret under mild conditions. This result generates additional insights for the performance guarantee of the myopic policy with the help of offline data, and also provides analytical support for the wide use of such policies in practice.

Methodology contributions. From a technical perspective, the tight upper and lower bounds that we obtain in this paper are both instance-dependent regret bounds, which are much stronger and more challenging to prove than the traditional worst-case regret bounds. To prove the instance-dependent upper bound, we conduct a period-by-period trajectory analysis, and develop novel inductive arguments, integrated with the specific property guaranteed by OFU principle, to obtain a sharp characterization on the distance between the algorithm’s price and the average historical price. To prove the instance-dependent lower bound, we reduce the OPOD problem to a hybrid of estimation and hypothesis testing problems, which requires constructing an instance-dependent prior distribution and an instance-dependent hypothesis set, respectively. To the best of our knowledge, these are the first tight and general instance-dependent regret bounds obtained in (i) the linear-demand online pricing problem, and (ii) a continuous-armed bandit problem where the optimal action may not be an extremal point (in contrast to the extremal-point requirement in Dani et al. 2008 and Abbasi-Yadkori et al. 2011).

1.4 Key Insights: Phase Transitions and Inverse-Square Law

The characterization of the optimal instance-dependent regret also leads to two important implications on the value of offline data. First, when the offline sample size changes, the optimal regret rate exhibits significantly different decaying patterns, and we refer to such significant transitions between the regret-decaying patterns as phase transitions444We borrow this terminology from statistical physics, see Domb (2000). See also the discussion of phase transitions in the optimal stopping problem studied by Correa et al. (2018), and in the multi-armed bandit problem studied by Simchi-Levi and Xu (2019).. For example, when and (see Table 1), the optimal regret rate remains at the level of whenever , and then gradually decays according to when , and finally stays at the level of when . Second, in the regular case, the optimal regret is inversely proportional to the square of the standard deviation and generalized distance , which is referred to as the inverse-square law. The optimal regret’s dependence on is consistent with our intuition, as more dispersive historical prices indicate more information gained before the online learning process starts, and therefore a smaller regret. The optimal regret’s dependence on is more intriguing, as it suggests that the closer the historical prices are to the optimal price, the worse the optimal regret will be. In fact, this is a consequence of the tradeoff between exploration (i.e., experimenting to improve estimates of the unknown demand model) and exploitation (i.e., leveraging current estimates to maximize revenue). Specifically, whenever an algorithm tries to learn the true demand model, it has to make substantial efforts in charging various prices “far away” from the average historical price. Therefore, when is small, such a deviation will also lead to a significant gap with the optimal price, leading to greater revenue loss. These two findings contribute new insights to the fundamental problem of dynamic pricing with demand learning.

| offline sample size | |||

|---|---|---|---|

| optimal regret | |||

| offline sample size | |||

| optimal regret | |||

| and | ||||

|---|---|---|---|---|

| offline sample size | ||||

| optimal regret | ||||

| and | ||||

| offline sample size | ||||

| optimal regret | ||||

| offline sample size | ||||

| optimal regret | ||||

1.5 Structure and Notations

This paper is organized as follows. In §2, we review the relevant literature. In §3 and §4, we study the OPOD problem in the single-historical-price setting and multiple-historical-price setting respectively. We conduct a numerical study in §5, and discuss the self-exploration of the myopic policy in §6. In §7, we summarize our paper with extensions and future research directions. Most of the technical proofs are deferred to the appendix.

Throughout the paper, all the vectors are column vectors unless otherwise specified. For any , we use to denote the set . For any column vector and positive semi-definite matrix , , and . The notations , and are applied to hide constant factors, and , and are applied to hide both constant and logarithmic factors. That is, means that there exists a constant such that for any , and means that there exist constants and , such that for any . In addition, (resp. ) means (resp. ), and (resp. ) means and (resp. and ).

2 Related Literature

2.1 Dynamic Pricing with Online Learning

When there are no offline data, the OPOD problem becomes a pure online learning problem, i.e. dynamic pricing with an unknown linear demand model, and belongs to a broad category referred to as the online pricing problems. Online pricing problems have generated great interest in recent years in the operations research and management science (OR/MS) community, see den Boer (2015) for a comprehensive survey. In particular, there is a vast literature (e.g., den Boer and Zwart 2013, den Boer 2014, Keskin and Zeevi 2014, Wang et al. 2014, Keskin and Zeevi 2016, Qiang and Bayati 2016, den Boer and Keskin 2017, Nambiar et al. 2019, Ban and Keskin 2020) studying dynamic pricing problems with an unknown linear (or generalized linear) demand model, which is arguably one of the most fundamental demand models for pricing. All of the existing papers purely focus on online learning. In this paper, we take the fundamental problem of dynamic pricing with a linear demand model as our baseline, but significantly extend it by incorporating offline data into online decision making.

Keskin and Zeevi (2014) is the most relevant paper to this work. The authors consider dynamic pricing with an unknown linear demand model, studying an important question of how knowing an exact point at the demand curve (i.e., the exact expected demand under a single price) in advance helps reduce the optimal regret. Depending on whether the seller knows this exact point or not, they prove that the best achievable regret is and respectively. Compared with their work, the OPOD problem studied in this paper seems more relevant to practice, and is more general in theory. Practically, while firms will never know the true expected demand under a given price exactly (which requires infinitely many demand observations), they usually have some pre-existing offline data (which are finitely many) prior to the online learning process. Theoretically, the results in Keskin and Zeevi (2014) (for the single-product setting) can be viewed as two special cases of our results when (i) ; and (ii) , , and , with an additional assumption that is lower bounded by a known constant (as their algorithms for case (ii) rely on this knowledge). Since is completely unknown and can be small in our setting (and in reality), their algorithms and analysis do not apply here. In fact, the principle of our algorithm design and the approach of our regret analysis are very different from theirs.

There is also a stream of literature in Bayesian learning, where the decision maker is assumed to have a known prior distribution for the unknown parameter, and can update her belief on the prior distribution from online observations. For recent works on dynamic pricing with Bayesian learning, we refer the interested readers to Harrison et al. (2012) and Agrawal et al. (2017) that focus on the worst-case regret, and to Ferreira et al. (2018) and Miao and Chao (2020) that focus on the Bayesian regret. While the prior distribution in Bayesian learning can be estimated using offline data, the modeling approach and results of these papers are very different from this work. First, in Bayesian learning, it is usually assumed that the decision maker knows the exact prior distribution, which typically belongs to some specific parametric family. By contrast, in this work, we do not assume any prior distribution or impose any parametric assumption on the distribution of demand parameter, but directly incorporate offline data into online learning. Second, as a main contribution of this paper, we characterize the effects of the size, dispersion and location of the offline data on the statistical complexity of online learning, which are not discussed in and not the focus of the current literature on Bayesian learning.

2.2 Multi-Armed Bandits

Our paper is also related to the literature of multi-armed bandits (MAB). In the classical -armed bandit problem, the decision maker chooses one of the arms in each round and observes a random reward generated from some unknown distribution associated with the arm being played, with the goal of minimizing the regret, see Lattimore and Szepesvári (2018) for more references on this topic. In most of the literature on bandit problems (see, e.g., Auer et al. 2002, Dani et al. 2008, Rusmevichientong and Tsitsiklis 2010, Abbasi-Yadkori et al. 2011, Filippi et al. 2010), the decision maker has to start from scratch (i.e., with no historical information). By contrast, a few papers study bandit problems in settings where the algorithms may utilize different types of historical information, see, e.g., Shivaswamy and Joachims (2012), Bouneffouf et al. (2019), Bastani et al. (2019), Hsu et al. (2019), Gur and Momeni (2019), Ye et al. (2020), of which Shivaswamy and Joachims (2012) and Gur and Momeni (2019) are the most relevant to this paper.

Shivaswamy and Joachims (2012) study the MAB problem with offline observations of rewards collected before the online learning algorithm starts. While our idea of incorporating offline data into an online learning problem is similar to theirs, there are significant differences between the two papers in terms of model settings, main results and analytical techniques. First, Shivaswamy and Joachims (2012) study the MAB problem with discrete and finitely many arms, while our model builds on the literature of online pricing problems (see §2.1 for references), where the prices are continuous and infinitely many, and the rewards are nonlinear with respect to prices. The properties and results for these two classes of problems are very different. Second, under the well-separated condition, Shivaswamy and Joachims (2012) prove some regret upper bounds that change from to when the amount of offline observations of rewards for each arm exceeds , with no regret lower bound proven and hence no discussion of phase transitions. In comparison, we characterize the optimal regret via matching upper and lower bounds, and figure out surprising phase transitions of the optimal regret rate as the offline sample size changes. Moreover, we also discover the inverse square law, which does not appear in the previous literature. Third, while Shivaswamy and Joachims (2012) use a conventional approach in bandit literature to upper-bound the regret via the so-called sub-optimality gap, since we are bounding the regret via and , we present different regret analysis that may be of independent interest.

In a recent paper by Gur and Momeni (2019), a generalized MAB formulation is studied, where some additional information may become available before each online decision is made. Under the well-separated condition, the authors characterize the optimal regret as a function of the information arrival process, and study the effect of the characteristics of this process on the algorithm design and the best achievable regret bound. In particular, their results include the MAB with offline data as a special case. Although our paper shares similar spirits with Gur and Momeni (2019) in the focus of identifying key characteristics of some “additional” information that affect the optimal regret, and quantifying the magnitude of such effects, the model settings, results and insights in these two papers are very different.

Interestingly, although neither Shivaswamy and Joachims (2012) nor Gur and Momeni (2019) makes an attempt to characterize the optimal regret for the MAB with offline data under general case (i.e., when the well-separated condition does not necessarily hold), or discuss the phase transitions, combining the regret upper bound in Shivaswamy and Joachims (2012) with the regret lower bound in Gur and Momeni (2019) gives a characterization on the optimal regret for the MAB with offline data under some mild conditions, which also leads to phase transitions not discussed before. We provide more discussions on this finding in Appendix G.

3 Single Historical Price

In this section, we study the single-historical-price setting: where all the historical prices are identical to . As pointed out in Harrison et al. (2012) and Keskin and Zeevi (2014), in finance industry, for many consumer lending products, banks often keep a fixed interest rate over some periods of time before they conduct price experimentation. Similarly, in the retail industry, there are many scenarios where the seller charges a fixed price based on the manufacturer’s suggestion, branding or competitors’ price before using a dynamic pricing strategy. Thus, we start with this simple but important single-historical-price setting in this section. We first design a learning algorithm with a per-instance regret upper bound in §3.1, and then characterize the regret lower bound in §3.2. Some important implications are discussed in §3.3.

3.1 O3FU Algorithm and Regret Upper Bound

Our proposed algorithm Online and Offline–Optimism in the Face of Uncertainty (O3FU) is constructed based on the celebrated Optimism in the Face of Uncertainty (OFU) principle, which effectively addresses the exploration-exploitation dilemma inherent in many online learning problems (see, e.g., §7.1 of Lattimore and Szepesvári 2018 for a reference). For any , we define a confidence radius that will be used to construct a confidence ellipsoid for the demand parameter at the end of period , and the expression of is as follows:

| (2) |

where and will be specified in the description of the algorithm. The choice of is based on the high-probability confidence bound developed in Theorem 2 of Abbasi-Yadkori et al. (2011), which will also be used throughout our regret analysis. The pseudo-code of O3FU algorithm is provided in Algorithm 1.

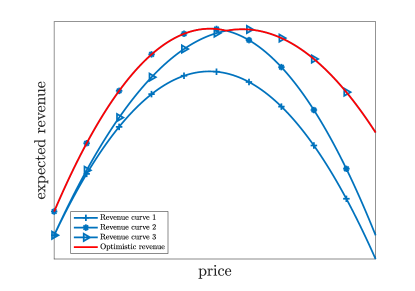

In O3FU algorithm, when , the price is chosen from boundary points , depending on which one has a larger distance from historical price . The choice of such an initial price is not unique, and any price that is bounded away from by a constant distance will also work. For each , we first maintain a confidence ellipsoid for the unknown parameter , and then O3FU algorithm selects an optimistic estimator , and charges price , which is optimal with respect to estimator . Note that when , as a function of , has multiple maximizers, can be set as any maximizer. Figure 1 shows how O3FU algorithm works, where the three blue curves depict the expected revenues with three different parameters belonging to set (we only draw three curves for illustration), and the red curve is the upper envelope of all the possible candidate revenue curves, which is also the revenue function associated with the demand parameter , i.e., .

Intuitively, if we knew that generalized distance would be large, then trying prices far away from is beneficial for both exploration and exploitation. By contrast, if we knew that would be small, then striking a balance between exploration and exploitation would be very important, because choosing prices close to is only effective for exploitation but not for exploration. Of course, the seller does not know the true value of , which makes designing a learning algorithm that achieves the right balance between exploration and exploitation a more challenging task. O3FU algorithm achieves this objective by maximizing the optimistic revenue, which is defined as , and can be treated as the estimated revenue plus a “bonus” of exploration. In fact, as implied from equation (19.8) in Lattimore and Szepesvári (2018), when , we have . Therefore, exploitation and exploration are both incorporated into the objective function through the first term and the second term, respectively.

It’s worth noting that our O3FU algorithm is parameter-free in the sense that it does not need to use any information about . In addition, while O3FU algorithm takes as input, one can easily extend the current algorithm to work with unknown using the standard doubling trick (see, e.g., Lattimore and Szepesvári 2018) and construct an anytime algorithm that does not need to know .

We now provide an upper bound on the regret of O3FU algorithm.

Theorem 3.1

Let be O3FU algorithm. Then there exists a finite constant such that for any , and , and for any possible value of ,

Theorem 3.1 provides a regret upper bound that depends on the problem instance through the value of , which is therefore called the instance-dependent upper bound. If is a constant, when or , i.e., there are no offline data or infinitely many offline data under price , the upper bound reduces to and respectively. If is not a constant, with an order shrinking to zero as grows, the regret upper bound is then inversely proportional to . We summarize the regret upper bound under different combinations in Table 3 of Appendix H.

We next outline the key ideas to prove Theorem 3.1 and leave the detailed analysis to Appendix A.1. From the statement of Theorem 3.1, it suffices to show an instance-independent upper bound and an instance-dependent upper bound . The instance-independent bound can be proved using similar arguments from stochastic linear bandits, e.g., Abbasi-Yadkori et al. (2011), by noting that the expected revenue is the inner product of the unknown parameter and the action vector . Showing the instance-dependent bound is the novel part in our proof, which relies on the following crucial lemma.

Lemma 3.2

Suppose , , and for each , then two sequences of events and also hold, where

and , , , .

Lemma 3.2 is interpreted as follows. When the optimal price has a certain distance from historical price , i.e., , given that the demand parameter belongs to the confidence ellipsoid in each period , the algorithm’s pricing sequence is also uniformly bounded away from proportional to the unknown quantity (as implied by events ), and will gradually approach the true optimal price in a rate of (as implied by events ). This implies that the algorithm can “adaptively” explore to a suitable degree, to create an efficient “collaboration” between the online prices and the historical price, while concurrently approaching the unknown optimal price. This property is nontrivial and cannot be implied from the existing analysis of the OFU-type algorithms. To prove this lemma, we conduct a period-by-period trajectory analysis of the random pricing sequence generated by our algorithm. Specifically, we find that the occurrence of relies on the joint occurrence of , while the occurrence of (combined with the specific structure of the optimistic revenue curve) in turn leads to the occurrence of . We thus introduce novel induction-based arguments to prove Lemma 3.2, see details in Appendix A.2. The induction-based arguments also explain why we set the initial price in the algorithm to be a boundary point (or any price that has a constant distance from ), since this enables to occur.

We remark that for the stochastic linear bandit problem with a polytope action set, Abbasi-Yadkori et al. (2011) prove an instance-dependent upper bound of , where is defined as the sub-optimality gap between the rewards of the best and second best extremal points of the action set. We emphasize that their result and analysis cannot be applied to prove our instance-dependent upper bound due to the following reasons. First, the instance-dependent upper bound in our problem is developed to capture the effect of the generalized distance on the regret bound, which does not exist in the stochastic linear bandit problem. Second, the instance-dependent upper bound in Abbasi-Yadkori et al. (2011) relies on two strong conditions: (i) their algorithm only selects actions among the extremal points of the action set, and (ii) every sub-optimal action taken by their algorithm is bounded away from the optimal action by a reward gap . Such conditions only hold under their setting and assumptions. Our problem, however, has a quadratic objective function, with the optimal price being an interior point of the interval , which requires the algorithm’s actions to converge to the optimal action. As a result, the sub-optimality gap becomes zero, and standard arguments based on do not work.

3.2 Lower Bound on Regret

In this subsection, we establish a lower bound on the performance of any algorithm for the OPOD problem with a single historical price. We first introduce the following set of admissible policies denoted by , which includes all the policies whose regret is guaranteed to be for any possible value of demand parameter , i.e.,

| (3) |

where and are arbitrary constants. Intuitively, excludes those “bad” policies that are not robust and suffer from large worst-case regret, e.g., a policy that never explores and always chooses , incurring zero regret when but linear regret when . Restricting our attention to (which O3FU and many existing algorithms obviously belong to) ensures that the considered policies are reasonable enough. Note that is specified by a pair of , but for simplicity, when there is no ambiguity, we drop the dependence on in the notation. To facilitate our discussion, let be defined as the regret for admissible policy when the demand parameter is , i.e., . We also denote as the generic distribution of and , and as the class of sub-Gaussian distributions with parameter .

The following theorem provides a regret lower bound for any admissible policy in terms of the generalized distance . For any generalized distance , we define an instance-dependent environment class , which is the set of all possible values of the demand parameter whose associated optimal prices are -distance away from (here can be any fixed constant in ). This environment class highlights the role of as a key instance-dependent quantity, and enables us to establish an instance-dependent regret lower bound that holds for all possible values of ; see Theorem 3.3 (note that the environment class appears under the operator in the LHS of (6)).

Theorem 3.3

There exists a positive constant such that for any admissible policy , for any , and , and for any ,

| (6) |

Remark 3.4

We emphasize that finding a “right” definition of the instance-dependent environment class is important for capturing the true role of in determining the instance-dependent regret. While there may be other ways to specify the environment class, they may fail to accurately reflect the instance-dependent complexity of the OPOD problem. For example, if one sets the environment class to be the entire parameter space , then one can obtain a single lower bound for the worst-case regret (independent of ); however, such a definition is too conservative and does not fully capture the value of offline data. Another seemingly natural way to specify the environment class is to consider , which is the set of all possible values of the demand parameter whose associated optimal price has a distance from exactly equal to . However, this definition cannot preclude certain speculative behavior of algorithms, and would result in an unrealistic regret bound that cannot be attained by any single algorithm. We refer to Appendix D for more details regarding the limitations of the above two definitions of the environment class.

We explain Theorem 3.3 as follows. First, when , the regret lower bound is , and in particular, if is a constant and , the regret lower bound reduces to , which recovers Theorem 3 in Keskin and Zeevi (2014) for their incumbent-price setting. Second, when , the regret lower bound is always , regardless of offline sample size . The intuition is as follows. When restricting attention to , we exclude those “unreasonable” policies that seldom explore but make pricing decisions in a naive way, e.g., the one that always chooses price , because the regret of such policies cannot always be upper bounded by for any possible value of . In this case, any admissible policy should be able to make sufficient exploration to distinguish between different demand curves. However, to achieve this, the policy must deviate from , which is less informative since the seller already has collected some data under this price, to gain more information about the true demand curve. When is very small, charging prices away from leads to a significant gap relative to the optimal price, and therefore a large regret bound. We summarize the regret lower bound under different combinations in Table 4 of Appendix H.

We next highlight the key steps in proving Theorem 3.3 and leave the detailed analysis to Appendix A.3. The proof idea is to reduce the OPOD problem to a hybrid of an estimation problem (see Step 1) and a hypothesis testing problem (see Step 2).

Step 1. In this step, we prove that when follows a normal distribution, for any pricing policy (not necessarily in ),

| (7) |

To prove (7), we consider an “auxiliary” estimation problem for the optimal price , and appeal to the multivariate van Trees inequality (cf. Gill and Levit 2001) to construct a lower bound for the Bayesian regret. In particular, when applying the van Trees inequality, we need to carefully choose a suitable instance-dependent prior distribution whose Fisher information grows at an appropriate rate with respect to , and upper-bound the resulting Fisher information of the sequential estimators in different cases. Then we can rightly control the growth rate of the Bayesian regret.

Step 2. In the second step, we show that when follows a normal distribution and , for any admissible policy , there exists satisfying such that

| (8) |

The proof of (8) is based on arguments using Kullback-Leibler divergence and Bretagnolle-Huber inequality (Theorem 2.2 in Tsybakov 2009), whose key idea is as follows. We construct two problem instances with parameters and such that (i) the two demand curves under and intersect at price ; (ii) the optimal prices under and are and respectively, with . For any pricing policy , it has to perform well under both constructed problem instances, i.e., the regret upper bound is under either instance, and therefore should be able to distinguish between the demand environments under and . Moreover, any policy with the goal of separating and should charge prices significantly different from the intersected price , i.e., the KL-divergence between the two probability measures under and induced by policy is large. Nevertheless, since the optimal price associated with is , which is extremely close to , the policy will incur large regret when the underlying parameter is in fact . Therefore, the regret under is always lower bounded by no matter how large is.

3.3 Phase Transitions and Inverse-Square Law

In this subsection, we discuss two important implications. By comparing Theorems 3.1 and 3.3, one can easily verify that the regret upper bound achieved by O3FU algorithm, after ignoring the logarithm factor, is unimprovable within the class of all admissible policies under the instance-dependent environment class considered in Theorem 3.3. Motivated by this result, for with , we define the optimal (instance-dependent) regret as

| (9) |

Thus, characterizes the statistical complexity of the OPOD problem in the sense that no algorithm in the admissible policy class can perform better than this rate when the true optimal price is allowed to center around within . We state this result in the following corollary.

Corollary 3.5

The optimal regret defined in (9) for the single-historical-price setting is

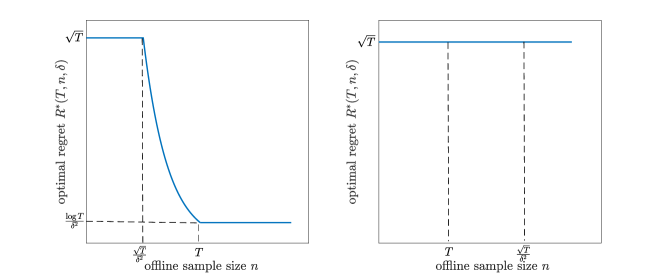

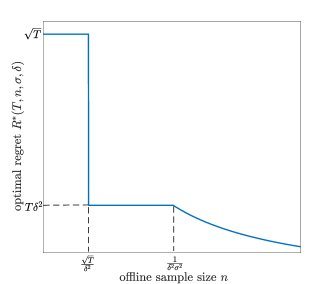

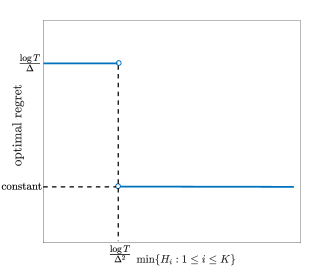

The characterization of the optimal regret leads to two important implications. First, the decaying patterns of the optimal regret rate are different when offline sample size belongs to different ranges. To better illustrate this phenomenon, we first consider the well-separated case where is a constant independent of . This case frequently happens in reality as it suggests that the seller’s historical price is suboptimal and quite different from the true optimal price. In this case, as increases, the optimal regret rate first remains at the level of when , then gradually decays according to when , and finally reaches when . This is depicted in Figure 2, from which we can clearly see that there are three ranges of , i.e., , and , referred to as the first, second and third phase respectively, and the optimal regret shows different properties in different phases. We refer to the significant transitions between the regret-decaying patterns of different phases as phase transitions.

In contrast to the well-separated case where the phase transitions do not depend on the value of , in the general case where may be very small, we cannot simply ignore the effect of in the optimal regret, and as a result, the number of phases and the thresholds of the offline sample size that define different phases are closely related to the magnitude of . As illustrated in Figure 3, when , similar to the well-separated case, there are three phases defined by two thresholds of : the optimal regret remains at the level of in the first phase, and gradually decays according to in the second phase, and stays at the level of in the third phase. When , there is no phase transition, and the optimal regret rate is always .

Second, Corollary 3.5 also characterizes the impact of the location of offline data relative to the optimal price on the optimal regret, which can be stated in the following inverse-square law: whenever offline data take effect, i.e., , and is in the second phase or the third phase, the optimal regret is inversely proportional to the square of generalized distance . Therefore, the factor is intrinsic in the regret bound. Seemingly counter-intuitive, the inverse-square law indicates that the closer the historical price is to the optimal price, the more difficult it is to learn the demand parameter, and the larger the optimal regret will be. In fact, this is a consequence of the exploration-exploitation trade-off. In the presence of offline data, a “good” learning algorithm needs to deviate from historical price to conduct price experimentation. However, when is extremely small, such a deviation will also lead to a significant gap with the optimal price, and therefore incurs greater revenue loss to the seller. In an extreme case when the historical price happens to be the optimal price, i.e., , even if , the optimal regret is always .

4 Multiple Historical Prices

In this section, we consider the multiple-historical-price setting, where the historical prices can be different. In this case, can be strictly positive and will play an important role to further reducing the complexity of the online learning task.

4.1 M-O3FU Algorithm and Regret Upper Bound

In this subsection, we develop a learning algorithm for the multiple-historical-price setting. We first make the following observations.

-

(i)

If and , then the offline data provide so much information that there is no need for online learning. In fact, by simply running linear regression on the offline data, we can obtain the estimate for the true demand parameter with the squared estimation error of , i.e., , which means that by simply charging price in each online period, we achieve the regret of . Note that this -type estimation error cannot be further improved in the online process by policies within , since when , we have

(10) where for any sequence and . This suggests that in the online process, exploration is “useless” in the sense that it cannot bring any theoretical improvement (in terms of reducing the order of estimation error) beyond offline regression. Therefore, if the algorithm knew that conditions and hold, then there is no exploration-exploitation trade-off at all.

-

(ii)

If in addition to the conditions in (i), a further extreme condition occurs, then even the above offline-regression-based approach may still be conservative: if an algorithm knew that , then by simply charging in every online period, it achieves the regret of , which is even better than . We refer to as the corner case, and its complement as the regular case.

-

(iii)

However, since the algorithm does not know the value of in advance, it does not know whether it is in the corner case (i.e., whether is true) in advance. If the conditions in (i) do not hold, then the algorithm still needs online exploration; if the condition in (ii) does not hold, then the algorithm still needs offline regression.

Motivated by the above observations, we design the following Modified O3FU (M-O3FU) algorithm. With an abuse of terminology, we refer to O3FU algorithm in this section as the one proposed in §3.1 after natural modification to the multiple-historical-price setting by letting , , and .

We next make several highlights about M-O3FU algorithm. First, in comparison with O3FU algorithm, before the start of the online learning process, M-O3FU algorithm takes a preliminary step that tests whether the distance between and interval is smaller than a constant times the length of interval . The goal of this step is to test whether condition holds or not. If this condition is inferred to hold based on the empirical observation, and in addition, , the algorithm keeps using for each online period. Otherwise, the algorithm simply runs O3FU algorithm. Second, parameter defined in is modified from (used in O3FU) to , which guarantees that belongs to each confidence ellipsoid with sufficiently high probability, and the revenue loss incurred when does not belong to some confidence ellipsoid can be bounded by .

The following theorem provides an upper bound on the regret of M-O3FU algorithm.

Theorem 4.1

Let be M-O3FU algorithm. Then there exists a finite constant such that for any , , and , and for any possible value of , we have

Theorem 4.1 shows that the regret upper bound has different forms in two different cases. When , M-O3FU algorithm achieves the regret upper bound , which matches the ideal regret bound in the above item (ii) discussed at the beginning of this subsection. Otherwise, the regret upper bound becomes . Compared with the upper bound in Theorem 3.1, there is an additional term in the denominator capturing the effect of the dispersion of offline data. We summarize the regret upper bound under different combinations in Table 5 of Appendix H.

The proof of Theorem 4.1 can be found in Appendix B.1. Similar to the proof of Theorem 3.1, we also need an important technical lemma stated as follows.

Lemma 4.2

Suppose we run O3FU algorithm from with given input offline data , , , and for each , then two sequences of events and also hold, where

and and are defined in Lemma 3.2, and

Similar to Lemma 3.2, Lemma 4.2 is also proved based on induction arguments. Besides, we need to use the following lower bound on the sum of squared price deviations:

| (11) |

where for any sequence and . We can interpret as the information metric capturing the variation for a sequence . Then inequality (11) bounds the information accumulated up to period from below, through the pre-existing offline information, plus the information due to the deviation of the algorithm’s prices from the average historical price. The proof of Lemma 4.2 is provided in Appendix B.2.

4.2 Lower Bound on Regret

In this subsection, we establish a lower bound on the best-achievable regret for the OPOD problem among the class of admissible policies defined in a similar way to (3). Again, we denote as the regret incurred by policy under the demand parameter .

Theorem 4.3

There exists a positive constant such that for any admissible policy , for any , , and , and for any ,

Similar to Theorem 3.3, the instance-dependent environment class is defined as the set of instances whose associated optimal prices are away from by a distance . Since M-O3FU algorithm achieves the regret upper bound for any value of (thus belongs to the admissible policy class with ), Theorem 4.3 demonstrates that for both the corner and regular cases, the regret rate achieved by M-O3FU algorithm in Theorem 4.1 cannot be further improved by any policy in . The proof of Theorem 4.3 is provided in Appendix B.4, which is a generalization to that of Theorem 3.3. We also summarize the regret lower bound under different combinations in Table 6 of Appendix H.

4.3 Phase Transitions and Generalized Inverse-Square Law

Motivated from the matching upper and lower bounds (after ignoring logarithm factors) in Theorems 4.1 and 4.3 respectively, we define the optimal instance-dependent regret for the OPOD problem in the multiple-historical-price setting as follows:

| (12) |

where a slight difference compared with (9) is the modification from the single historical price to the average historical price .

Combining Theorem 4.1 and Theorem 4.3, we are able to characterize the optimal regret of the OPOD problem for the multiple-historical-price setting.

Corollary 4.4

The optimal regret defined in (12) for the multiple-historical-price setting is

Recall that in the single-historical-price setting, the threshold of plays an important role in characterizing the behavior of the optimal regret rate. This threshold also plays a role in the optimal regret rate of the multiple-historical-price setting.

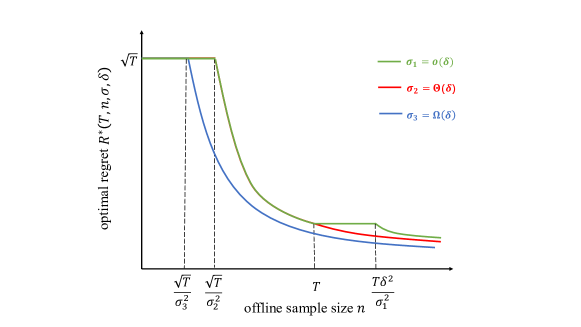

When , there are significant differences for the behaviors of the optimal regret rate, depending on whether is less than, equal to or greater than . This is illustrated in Figure 4, where the green, red and blue curves depict the above three cases respectively. If , as shown in the green curve, the optimal regret rate exhibits four decaying patterns as changes between different ranges. Specifically, the optimal regret rate first remains at when , and then decreases according to when . After that, the optimal regret rate stays at when , and finally, it decreases according to when . If or as shown in the red or blue curve, the optimal regret rate exhibits two phases: it remains at the level of when , and decays according to when . Therefore, when gradually increases, depending on its magnitude compared with , the number of phases of the optimal regret rate also experiences the change from four phases to two phases, and the entire patterns of the phase transitions of the optimal regret rate also change accordingly.

Corollary 4.4 also reveals a generalized inverse-square law. Specifically, the optimal regret is inversely proportional to the square of both and , which quantifies the effect of the location and dispersion of the offline data on the optimal regret. The intuition for the dependence of the optimal regret on is similar to the single-historical-price setting. For the dependence of the optimal regret on , as the historical prices become more dispersive, i.e., increases, the seller can obtain a more accurate estimate for the unknown demand parameter from offline regression, which helps to further reduce the optimal regret of the online learning process.

It’s also worth noting that the thresholds of the offline sample size that define different phases of the optimal regret depend on both and . When and , the first threshold of that defines the first and second phases, i.e., , decreases in . When and , the threshold of that defines the first and second phases, i.e., , decreases in the standard deviation . This implies that more offline data will be required to overcome the challenges caused by a shorter generalized distance or a smaller standard deviation .

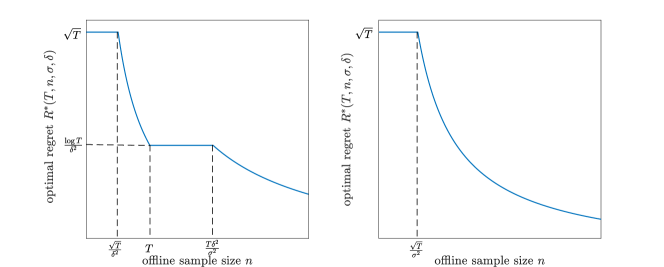

When , Corollary 4.4 indicates that there are three phases of the optimal regret rate as changes. When , the optimal regret remains at . When , the optimal regret experiences a sudden drop from to . When , the optimal regret decays according to . Such transitions of the optimal regret with different are illustrated in Figure 6. In particular, the second phase corresponds to the corner case defined in §4.1. In this case, smaller leads to lower optimal regret, which is in contrast to the inverse-square law in the regular case. This is because in the corner case, as discussed in §4.1, there is no need for online learning and therefore no exploration-exploitation trade-off, and the policy that always charges incurs very small regret. In this case, the closer the average historical price is to the optimal price, the smaller the optimal regret will be. By contrast, the inverse-square law in the regular case is a consequence of the exploration-exploitation trade-off.

5 Numerical Study

In this section, we test the performance of our algorithm on a synthetic data set. We define the relative regret for a given learning algorithm as , and the following three problem instances are tested:

-

(1)

, , , , ;

-

(2)

, , , , ;

-

(3)

, , , , .

and follows a normal distribution with standard deviation . For each of the above instance, we repeat the experiments for 500 times, and the results are computed after averaging over the 500 experiments. Under the multiple-historical-price setting, we test a simplified version of M-O3FU algorithm by directly running O3FU, without checking the preliminary condition. Thus, throughout this section, we simply call our algorithm “O3FU algorithm.”

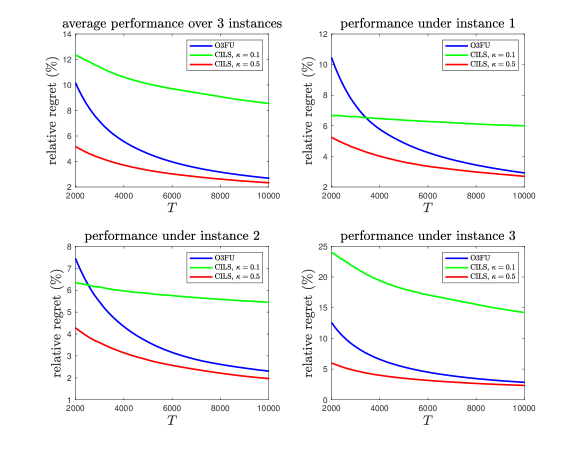

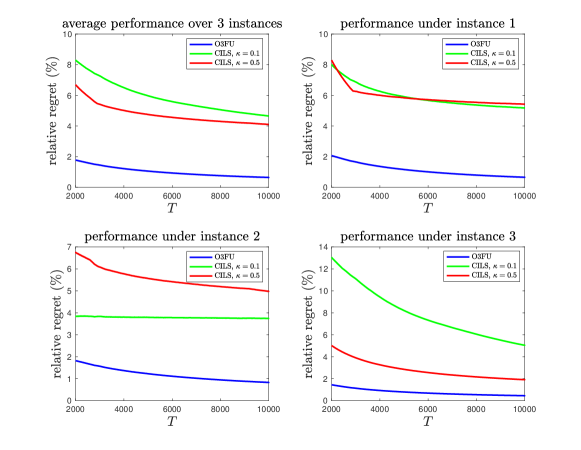

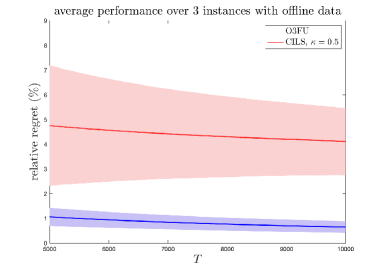

First, we compare our O3FU algorithm with the modified Constrained Iterated Least Squares (CILS) algorithm. When there are no offline data, we adopt CILS algorithm directly from Keskin and Zeevi (2014). When there are offline data, no existing learning algorithm in prior literature is directly suitable for this setting, so we make a natural modification to the original CILS by incorporating offline data into the least-square estimation. In both cases, we set the tuning parameter in CILS to be following Keskin and Zeevi (2014), and also which seems to lead to the best performance of CILS. Figures 8 and 8 show the performances of O3FU and CILS algorithms for the settings when there are no offline data, and when there are offline demand data under a single historical price (specifically, we set for instances (1)-(3) respectively). As seen from Figure 8, without offline data, O3FU performs better than CILS with and comparably to CILS with as becomes larger. Figure 8 reveals that with the help of offline data, the regret of O3FU algorithm is significantly reduced for all under all instances. By contrast, for CILS algorithms, the impact of offline data on the empirical regret is not obvious and heavily relies on the tuning parameter and specific problem instance. For CILS with , the improvement of the relative regret is clear under instance (3), but rather minimal under instances (1) and (2). For CILS with , the regret only decreases a little under instance (3), and even becomes larger under instances (1) and (2). Therefore, compared with CILS algorithms, O3FU algorithm better exploits the value of offline data and is more robust to different problem instances.

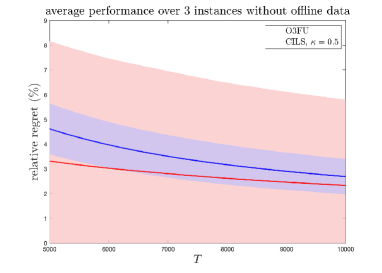

Second, Figure 9 plots the 95% confidence region of O3FU algorithm and CILS algorithm with , for both cases when there are no offline data and when there are offline data. The left figure shows that while CILS with properly tuned parameter performs slightly better than O3FU on average when there are no offline data, the standard deviation of CILS among the 500 simulations is much larger than O3FU. This implies that O3FU is more stable than CILS. The right figure shows that with offline data, O3FU always outperforms CILS, in terms of both the average regret and standard deviation. Since O3FU algorithm has highly stable performance, we believe that it should be preferable in many real-life business settings.

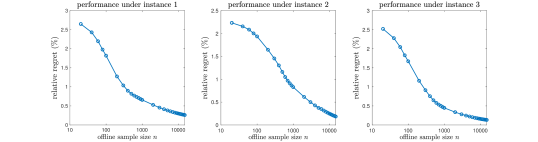

Third, we investigate the effect of offline sample size on the empirical regret of O3FU algorithm. In Figure 12, we plot the relative regret of O3FU algorithm given different amount of offline data (with ranging from 20 to 12000), under the single-historical-price setting (with for instances (1)-(3) respectively). The x-axis is depicted on a log scale. We can see clearly that for each problem instance, as the offline sample size increases, the relative regret decreases, which is consistent with the phase transitions implied from our theoretical results.

Finally, we investigate the effects of generalized distance and price dispersion on the empirical regret of our algorithm. Figure 12 shows the relative regret of O3FU algorithm given offline demand observations under historical price with different , and Figure 12 shows the relative regret of O3FU algorithm given 250 offline demand observations under historical price , and 250 offline demand observations under historical price with different , where for instances (1)-(3) respectively. As seen from Figure 12 and 12, when or increases, the empirical regret of our algorithm decays, which also matches the inverse-square law.

Remark 5.1

We remark that the empirical evidence for the phase transitions and inverse-square law is not always observed under every problem instance. This is because according to its definition through the supremum over some instance-dependent environment class, the optimal regret should be attained at some “hard” instances, and so do its implications of the phase transitions and inverse-square law. Besides, when discussing the optimal regret rate and its implications, we require to be sufficiently large, and ignore all the constant factors. Our choices of instances (1)-(3) capture the aforementioned hard instances, and also avoid that the problem falls into the regimes where constant factors significantly affect the overall regret rate.

6 Further Discussion: Offline Data and Self-Exploration

In M-O3FU algorithm proposed in §4.1, there is a preliminary step testing whether holds or not. We find that this step also has an important implication in practice: is actually a sufficient condition for self-exploration in our OPOD problem. That is, with high probability, when this condition holds, the myopic (i.e., greedy) policy can achieve the optimal regret without any active exploration.

The myopic policy is defined as follows. Let , where , , and . Let be the sequence of prices charged by the myopic policy. For , , and for each , we first compute the least-square estimator based on offline data and all the available online data within confidence ellipsoid :

and then let . The next proposition shows that the myopic policy is guaranteed to be optimal if certain condition holds.

Proposition 6.1

Suppose . Then with probability at least , the following event holds: if for some , then the myopic policy ensures that the regret is .

The intuition of Proposition 6.1 is as follows. Note that the key step to prove the instance-dependent upper bound in Theorem 4.1 is to show events and in Lemma 4.2 hold. Since the myopic policy charges prices based on estimator in each period , and contains with high probability, under the condition in Proposition 6.1, we can easily verify that the myopic price is bounded away from by a distance proportional to . In other words, event in Lemma 4.2 is automatically satisfied for each period , and in this case, when , we can further show that event also holds. Therefore, the myopic policy ensures that the regret is .

We also make several remarks about Proposition 6.1. First, the interpretation of probability “” is similar to the interpretation of “95%” in a 95% confidence interval. Such a probabilistic statement is common in frequentist statistics, when one wants to make some inference (e.g., myopic policy is optimal or not) based on some empirical observations (e.g., ). Second, if the regular case happens, i.e., and , one can easily verify that the empirical condition described in Proposition 6.1 always holds. In this case, the myopic algorithm always ensures regret. Nevertheless, verifying the condition requires knowing the true parameter in advance, which is not practical in reality. Thus, we make a probabilistic statement in Proposition 6.1 about the regret bound under an empirical condition that can be directly verified by the algorithm. Third, the choice of is not essential in Proposition 6.1. In fact, one can achieve any higher probability bound that is arbitrarily close to 1 by defining a larger confidence ellipsoid , although in that case, the condition will be more difficult to be satisfied.

In reality, myopic policies are commonly adopted in many industries, since they are quite easy to explain to managers, and relatively simple to implement in practice. See the discussion of myopic policies in, e.g. Harrison et al. (2012), Keskin and Zeevi (2014), Qiang and Bayati (2016). However, due to the lack of active exploration, myopic policies typically suffer from incomplete learning, thus usually have poor theoretical performance in dynamic pricing. Proposition 6.1 shows how offline data may help myopic policies to achieve self-exploration in dynamic pricing: when there are enough dispersive offline data, then with high probability, as long as is bounded away from offline confidence interval of , the issue of incomplete learning could be resolved, and the myopic policy could achieve self-exploration.

7 Conclusion

In this paper, we investigate the impact of offline data on online learning in the context of dynamic pricing. In contrast to previous literature that involves only offline data or only online data, we consider a more practical problem involving both offline data and online data, aiming to understand whether and how the pre-existence of offline data would benefit the online learning process. For both single-historical-price and multiple-historical-price settings, we design a learning algorithm based on the OFU principle with a provable instance-dependent regret upper bound, and establish a regret lower bound that matches the upper bound up to logarithmic factors. Two important and nontrivial implications implied by our results are phase transitions and the inverse-square law, characterizing the joint effect of the size, location, and dispersion of the offline data on the optimal regret. The numerical experiments demonstrate the effectiveness, robustness and stability of our algorithm, and reveal the empirical evidence for phase transitions and the inverse-square law. Besides, we also develop a sufficient condition for the myopic policy to achieve the optimal regret in the regular case.

We discuss two extensions of this paper. First, while we focus on the linear demand model in this paper, the regret upper bounds developed in Theorems 3.1 and 4.1 can be extended to the generalized linear model for some link function , under certain smoothness conditions. In particular, these conditions guarantee that the regret in each single period for any given policy is of the same order as the quadratic estimation error , and that Lemmas 3.2 and 4.2 continue to hold. We refer the interested readers to online Appendix E for more details. Second, we assume that historical prices are fixed constants in this paper. In reality, offline pricing decisions can also be made based on the previous prices and sales observations according to some offline pricing policy, in which case offline data will be generated in an adaptive way. By modifying the performance metric to the expected regret conditioned on the observed offline price trajectory, we can extend our results to the setting with adaptive offline data. This extension is discussed in online Appendix F.

This paper also suggests various directions for future research. First, with the development of information technology, firms have access to more detailed data that record customer information and product characteristics. It will be interesting to incorporate such contextual information into the model, and study context-based dynamic pricing with online learning and offline data. In this case, it’s important to understand how the definition of the location metric of offline data should be modified accordingly. Second, we believe that the framework of online learning with offline data is quite general and widely applicable, and it will be also interesting to explore how to extend such a framework to derive new results and insights for other data-driven operational problems, e.g., pricing under substitutable products, bandit with knapsack constraints, inventory control with demand learning, etc. Third, by leveraging the location metric of offline data, this paper develops the instance-dependent regret bound, which goes beyond the traditional worst-case regret and is new to the literature on dynamic pricing with demand learning. It will be valuable to explore whether other types of instance-dependent bounds can be developed for dynamic pricing and revenue management problems by utilizing certain historical information.

References

- Abbasi-Yadkori et al. (2011) Abbasi-Yadkori Y, Pál D, Szepesvári C (2011) Improved algorithms for linear stochastic bandits. Advances in Neural Information Processing Systems, 2312–2320.

- Agrawal et al. (2017) Agrawal S, Avadhanula V, Goyal V, Zeevi A (2017) Thompson sampling for the mnl-bandit. arXiv preprint arXiv:1706.00977 .

- Auer et al. (2002) Auer P, Cesa-Bianchi N, Fischer P (2002) Finite-time analysis of the multiarmed bandit problem. Machine learning 47(2-3):235–256.

- Ban and Keskin (2020) Ban GY, Keskin NB (2020) Personalized dynamic pricing with machine learning: High dimensional features and heterogeneous elasticity. Forthcoming, Management Science .

- Bastani et al. (2019) Bastani H, Simchi-Levi D, Zhu R (2019) Meta dynamic pricing: Learning across experiments. Available at SSRN 3334629 .

- Bouneffouf et al. (2019) Bouneffouf D, Parthasarathy S, Samulowitz H, Wistub M (2019) Optimal exploitation of clustering and history information in multi-armed bandit. arXiv preprint arXiv:1906.03979 .

- Broder and Rusmevichientong (2012) Broder J, Rusmevichientong P (2012) Dynamic pricing under a general parametric choice model. Operations Research 60(4):965–980.

- Cesa-Bianchi and Lugosi (2006) Cesa-Bianchi N, Lugosi G (2006) Prediction, learning, and games (Cambridge university press).

- Correa et al. (2018) Correa JR, Dütting P, Fischer F, Schewior K (2018) Prophet inequalities for independent random variables from an unknown distribution. arXiv preprint arXiv:1811.06114 .

- Dani et al. (2008) Dani V, Hayes TP, Kakade SM (2008) Stochastic linear optimization under bandit feedback. Proceedings of the 21st Conference on Learning Theory.

- den Boer and Keskin (2017) den Boer A, Keskin NB (2017) Dynamic pricing with demand learning and reference effects. Available at SSRN 3092745 .

- den Boer (2014) den Boer AV (2014) Dynamic pricing with multiple products and partially specified demand distribution. Mathematics of operations research 39(3):863–888.

- den Boer (2015) den Boer AV (2015) Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science 20(1):1–18.

- den Boer and Zwart (2013) den Boer AV, Zwart B (2013) Simultaneously learning and optimizing using controlled variance pricing. Management science 60(3):770–783.

- Domb (2000) Domb C (2000) Phase transitions and critical phenomena, volume 19 (Elsevier).

- Ferreira et al. (2018) Ferreira KJ, Simchi-Levi D, Wang H (2018) Online network revenue management using thompson sampling. Operations research 66(6):1586–1602.

- Filippi et al. (2010) Filippi S, Cappe O, Garivier A, Szepesvári C (2010) Parametric bandits: The generalized linear case. Advances in Neural Information Processing Systems, 586–594.

- Gill and Levit (2001) Gill R, Levit B (2001) Applications of the van trees inequality: a bayesian cramér-rao bound. Bernoulli 1:59.

- Gur and Momeni (2019) Gur Y, Momeni A (2019) Adaptive sequential experiments with unknown information flows. arXiv preprint arXiv:1907.00107 .

- Harrison et al. (2012) Harrison JM, Keskin NB, Zeevi A (2012) Bayesian dynamic pricing policies: Learning and earning under a binary prior distribution. Management Science 58(3):570–586.

- Hastie et al. (2005) Hastie T, Tibshirani R, Friedman J, Franklin J (2005) The elements of statistical learning: data mining, inference and prediction. The Mathematical Intelligencer 27(2):83–85.

- Hsu et al. (2019) Hsu CW, Kveton B, Meshi O, Martin M, Szepesvari C (2019) Empirical bayes regret minimization. arXiv preprint arXiv:1904.02664 .

- Keskin and Zeevi (2014) Keskin N, Zeevi A (2014) Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies. Operations Research 62(5):1142–1167.

- Keskin and Zeevi (2016) Keskin NB, Zeevi A (2016) Chasing demand: Learning and earning in a changing environment. Mathematics of Operations Research 42(2):277–307.

- Lattimore and Szepesvári (2018) Lattimore T, Szepesvári C (2018) Bandit algorithms. preprint .

- Li et al. (2017) Li L, Lu Y, Zhou D (2017) Provably optimal algorithms for generalized linear contextual bandits. Proceedings of the 34th International Conference on Machine Learning-Volume 70, 2071–2080 (JMLR. org).

- Miao and Chao (2020) Miao S, Chao X (2020) Dynamic joint assortment and pricing optimization with demand learning. Manufacturing & Service Operations Management .

- Nambiar et al. (2019) Nambiar M, Simchi-Levi D, Wang H (2019) Dynamic learning and pricing with model misspecification. Management Science .

- Qiang and Bayati (2016) Qiang S, Bayati M (2016) Dynamic pricing with demand covariates. Available at SSRN 2765257 .

- Rusmevichientong and Tsitsiklis (2010) Rusmevichientong P, Tsitsiklis JN (2010) Linearly parameterized bandits. Mathematics of Operations Research 35(2):395–411.

- Shivaswamy and Joachims (2012) Shivaswamy P, Joachims T (2012) Multi-armed bandit problems with history. Artificial Intelligence and Statistics, 1046–1054.

- Simchi-Levi and Xu (2019) Simchi-Levi D, Xu Y (2019) Phase transitions in bandits with switching constraints. arXiv preprint arXiv:1905.10825 .

- Tsybakov (2009) Tsybakov A (2009) Introduction to Nonparametric Estimation (Springer, New York).

- Wang et al. (2014) Wang Z, Deng S, Ye Y (2014) Close the gaps: A learning-while-doing algorithm for single-product revenue management problems. Operations Research 62(2):318–331.

- Ye et al. (2020) Ye L, Lin Y, Xie H, Lui J (2020) Combining offline causal inference and online bandit learning for data driven decisions. arXiv preprint arXiv:2001.05699 .

Online Appendix for “Online Pricing with Offline Data: Phase Transition and Inverse Square Law”

Appendix A. Proofs of Statements in Section 3

A.1. Proof of Theorem 3.1

As preparations, we introduce two results from Abbasi-Yadkori et al. 2011, which will be used in the analysis.

Lemma 7.1 (Lemma 11 in Abbasi-Yadkori et al. 2011)

Let be a sequence in , be a positive definite matrix and define . If for all and , then

Lemma 7.2 (Theorem 2 in Abbasi-Yadkori et al. 2011)

For any , any ,

We now divide the proof for Theorem 3.1 into two steps by proving the instance-independent upper bound and the instance-dependent upper bound .

Step 1. In this step, we prove that the regret of O3FU algorithm is . Let for each . For any , suppose (note that in this case, , and thus, is well-defined), then we have

| (13) |

where the first inequality follows from the definition of in O3FU algorithm, the second inequality follows from Cauchy-Schwarz inequality, and the last inequality follows from . Therefore,

| (14) |

where the first inequality follows from Cauchy-Schwarz inequality, and the second inequality follows from inequality (A.1. Proof of Theorem 3.1) and the fact that increases in .

Then we use Lemma 7.1 to bound the term . To apply Lemma 7.1, let , , ,

Then we have

which, combined with inequality (A.1. Proof of Theorem 3.1), the definition of , implies that when for any ,

| (15) |

Then the regret of O3FU algorithm is upper bounded as follows:

where the second identity follows from inequality (15) and Lemma 7.2 with for any .

Step 2. In this step, we prove that the regret of O3FU algorithm is also . It suffices to show the case when , since otherwise, , and the upper bound in Theorem 3.1 becomes , which is already proven in Step 1.

Note that it suffices to bound the term . Since defined in Lemma 3.2 is an absolute constant, the result is trivial when . We then consider .

where the first inequality follows from the proof of Lemma 3.2 and the concentration inequality in Lemma 7.2 with for any . It is easy to verify that when ,

and when ,

Combining both cases of and , we have , which completes the proof. ∎

A.2. Proof of Lemma 3.2

When , since , then . Thus, when , holds.

We next prove the following result: under the assumptions of Lemma 3.2, suppose for each (for a fixed ), the event holds, then and also hold. To this end, let , , and (when ). Since and , we have , which is equivalent to

| (16) |

We next divide the proof into three cases.

Case 1: . In this case, (16) becomes and

| (17) |

Therefore, (17) implies that

and

where the second inequality follows from (17) and Lipschitz continuity of the function : , and the third inequality holds since the assumption implies

| (18) |

Case 2: , . In this case, we have

| (19) |

where the first inequality holds since , and from (16), we have

and the last inequality follows from , which is easily verified by noting . Then, (19) implies that

and

where the second inequality follows from Lipschitz continuity of and (19), and the third inequality follows from (18).

Case 3: , . Recall the following definitions of , and in Lemma 3.2:

Subcase 3.1: . In this subcase, since

then we have

In addition, since , it follows that

where in the third inequality, we utilize the fact that , and the last inequality follows from and the definition of .

Subcase 3.2: . In this subcase, we have

where the second inequality holds since , and the last inequality follows from , and the inductive assumption: for each , . Now, it suffices to bound the term . If we can prove the following inequality:

| (20) |

then can be bounded as follows:

where the second inequality follows from (20), the fourth inequality follows from the assumption of Subcase 3.2, i.e., and , and the last inequality follows from the definition of .

Finally, we prove inequality (20). We define

Recall that and are the maximizers of the following maximization problem:

then we have the following relationships for , :

| (21) | |||

| (22) |

To show inequality (20), we consider the following two cases when and . If , then we have

| (23) |

where the first inequality follows from . Without loss of generality, we assume that , since otherwise, we can redefine and as and respectively, and the proof will be similar. Therefore, by dividing on both sides of (23), we get inequality (20). If ,

| (24) |

where the second identity and the second inequality follow from the property of quadratic functions. By dividing ( by assumption) on both sides of (A.2. Proof of Lemma 3.2), inequality (20) holds. It is also worth noting that from the above arguments, inequality (20) holds universally due to the specific property of OFU principle and quadratic structure of the objective function, and does not depend on any inductive assumption.

Combining Cases 1–3, we conclude that

i.e., and hold, which completes the inductive arguments. ∎

A.3. Proof of Theorem 3.3

As preparation, we first present the multivariate van Trees inequality, which will be used in Step 1 of the proof for Theorem 3.3. For simplicity, we focus on the estimation problem for a real-valued function when stating the multivariate van Trees inequality, which is sufficient for our use, and we refer the interested readers to Gill and Levit (2001) for the more general version on estimating a vector-valued function.

Lemma 7.3 (Multivariate van Trees Inequality, Theorem 1, Gill and Levit (2001))