Beta Rank Function: A Smooth Double-Pareto-Like Distribution

Deceased 9 May 2019.

Abstract

The Beta Rank Function (BRF), , where is the normalized and continuous rank of an observation , has wide applications in fitting real-world data from social science to biological phenomena. The probability density function (pdf) converted from the BRF, , does not usually have an analytic expression except for specific parameter values. We show however that it is approximately a unimodal skewed and asymmetric two-sided power law/double Pareto/log-Laplacian distribution. The pdf of the BRF has very simple properties when the independent variable is log-transformed: . At the peak it makes a smooth turn from one side to the other and it does not diverge, lacking the sharp angle observed in the double Pareto or the Laplace distribution. The mode of (peak position) is ; the probability is partitioned by the peak to the proportion of (left) and (right); the functional form near the peak is largely controlled by the cubic term in the Taylor expansion when ; the mean of is ; the decay on left and right sides of the peak is approximately exponential with the form and . These results are also confirmed by numerical simulations. As a comparison, properties of without a log-transformation of the variable, some of them were also derived analytically, are much more complex, though the approximate power-law behavior, or double Pareto, (for ) and (for ) is simple. Our results elucidate the relationship between BRF and log-normal distributions when , and explain why the BRF is ubiquitous and versatile. Based on the pdf, we also suggest a quick way to elucidate if a real data set follows a one-sided power-law, a log-normal or a two-sided power-law of BRF. We illustrate our results with a few examples: urban populations and returns of financial indexes.

Abbreviations: BRF: Beta rank function; cdf: cumulative density function; DGBD: Discrete Generalized Beta Distribution; DPLN: double-Pareto-lognormal distribution; pdf: probability density function;

1 Introduction

Since the introduction of the two-parameter Discrete Generalized Beta Distribution (DGBD) (or Beta-like Rank Function or Cocho Rank Function) [1, 2], a wide range of real-life data have been successfully fitted by this function [3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24, 25]. Two questions naturally arise: first, what’s the corresponding probability density function (pdf) of the DGBD? Second, why is this family of functions so ubiquitous? In order to fully address these questions, we will need to define a continuous-rank version of the DGBD, which is a function with discrete independent variable (rank).

These two questions are partially addressed in [26]: when the two parameters in the DGBD are equal, leading to the one-parameter rank function called Lavalette Rank Function [27, 28, 29, 30, 31], the corresponding pdf can be derived analytically [32, 26]. This pdf, which we called Lavalette distribution, is similar (but not identical) to the lognormal distribution [26]. But the nature of the difference between the Lavalette and lognormal distributions has not been addressed in depth. It is also shown in [26] that when one of the parameters in the DGBD is equal to zero, it reduces to a one-sided power-law distribution; when the other parameter is zero, it becomes a uniform distribution. Although there are other attempts to explain the widespread applications of the DGBD [33, 34], the spanning from uniform, approximately log-normal and one-sided power-law distribution by turning the parameters demonstrates the versatility of the family of functions defined by the DGBD.

In order to make a connection between DGBD and families of continuous probability distributions, we will introduce its continuous equivalent, which we will call Beta Rank Function (BRF). This coincides with a quantile function proposed in [35] (Hankin-Lee quantile function or Davies distribution), which accurately approximates some non-negative distributions such as lognormal, Weibull and generalized Tukey. This quantile function has also been proposed in [36], where it is called the power-Pareto distribution. Ideally, we would like to derive its corresponding pdf in an analytic form. However, the task is not straightforward except for a few specific points (or lines) in the parameter space. The apparent impossibility for a closed-form expression of the underlying distribution has been noticed in [37]. As mentioned above, these exceptions include , , and . We will show later that it also includes , where or sometimes other integer values.

In this paper we use a combination of analytic and simulation approaches to study the properties of pdfs derived from the BRF family. In particular, we will show that the pdf becomes much simpler when the independent variable is log-transformed. One of the most important results we obtained is that the fall off from the peak is exponential. In other words, the pdf is approximately log-Laplace, or double-Pareto, or double-power-law [38, 39]. Differing from the lognormal distribution, our pdf can be asymmetric around the peak and the cubic term, as well as the quadratic form, plays a role in the functional form. Our pdf also differs from lognormal in its decay form from the peak. The exponential fall off on the two sides of the peak can be different, with the left side controlled by parameter and the right side by parameter .

The results in this paper provide a comprehensive picture of the pdf associated to the BRF or Hankin-Lee-Davies function without the analytic expression of its functional form. This pdf is an approximate double Pareto/power-law function away from the peak, a different perspective from the typical practice to focus attention on one tail (e.g. in Zipf’s law). The function near the peak is smooth, not only different from the potential divergence of the distribution in one-sided power-laws, but also different from the divergence of the second derivative (sharp transition) for double-Pareto functions. The different decay rates on both sides of the peak also make our novel distribution flexible in data fittings.

The paper is organized as follows: first we describe the rank order representation of a random variable and its connection with the pdf; in this context we will define the Beta Rank Function, which is the continuous equivalent of the DGBD with normalized rank. For the sake of completeness, we analyze some particular cases of the BRF, which we had already studied in previous works. Next we will show that our analysis is greatly simplified after a logarithmic transformation, we will introduce the novel log-BRF family of distributions and analyze some of its main properties. Then we will introduce the novel BRF family of distributions, study some of its main properties and propose methods to produce pseudo-random numbers from this distributions and to numerically approximate its pdf. After that, we will illustrate the possible usefulness of these distributions in data analysis by means of two particular examples (distribution of financial log-returns and city population distribution). The paper ends with Discussion and Conclusion sections.

2 Rank-Ordering Statistics and the Beta Rank Function

2.1 Connection between rank-size function and probability density function

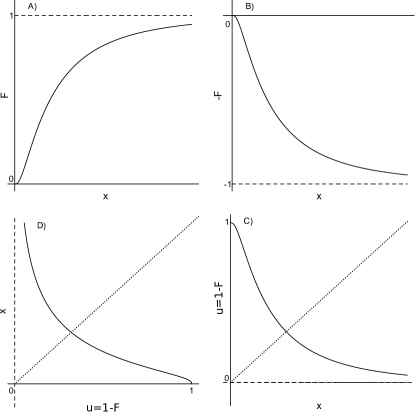

Let be a positive and continuous random variable with a probability density function . Let be a list of independent realizations of (a random sample). We define the rank of the observation within the list as the number of observations in the list that are greater or equal than . For instance, the rank of the largest observation in the sample will be , whereas for the lowest observation . Ranks are well defined if the probability of making two identical observations is equal to zero, which is here the case, since we assume the observations come from a density function. Consider now the list sorted in decreasing order, , where (observe that the k-th order statistic is ). We call the list of ranks of the ordered list the rank list, . A plot of against is called a rank-size plot of the observations. By construction, these plots are always decreasing.

Now consider the rank list normalized to the interval, . Unless specified we will consider only normalized ranks, so we will refer to them simply as the rank (to be made continuous) variable . A rank-size function is a function that quantifies the dependence of the size (or value) of an observation as a function of the rank it would have within an infinite list of observations. The rank-size function can be constructed from the pdf in the following way: notice that, according to our definition, the (normalized and continuous) rank of equals the probability of making a larger observation,

| (1) |

where is the cumulative distribution (cdf). Note that, after this construction, the function coincides with the well-known survival function. If the cdf is strictly increasing and continuous, then we can solve Eq.(1) for the pdf,

| (2) |

According to Eq.(1), we define the rank-size function as the inverse survival function, which can be computed if the pdf is known and the survival function is invertible. On the other hand, Eq.(2) allows us to compute the pdf of a random variable from its inverse survival function, or rank-size function.

Geometrically, it is possible to get the rank-size function from the cdf or vice versa in the following way: starting from the cumulative function , reflect it respect to the axis (getting ), make a shift in the direction (getting ) and reflect it respect to the line (getting ). Therefore, the rank-size plot of a collection of random observations serves as an attempt to approximate the cdf in a similar way that a histogram approximates the density function. This geometric procedure is illustrated in Fig.1. A similar illustration can also be found in [5].

Let’s summarize the contents in this subsection as they will be repeatedly used later: is the rank-size function; is the survival function and is the probability density function. Later on, we will also show that after is log-transformed, , the probability density function of is .

In the next paragraph we will recall the definition of the Discrete Generalized Beta Distribution and define the Beta Rank Function, which will be a normalized and continuous-rank version of the DGBD, whose underlying pdf we intend to investigate.

2.2 Definition of the Beta Rank Function

The Discrete Generalized Beta Distribution (DGBD) is a discrete, two-parameter rank-size function defined by

where is the size (value) of the observation, is the total number of observations, and are parameters, the rank spans , and is a scale normalization constant.

In order to establish a connection between this representation and the pdf, we need to define the continuous and normalized equivalent of the DGBD, which leads to the following definition. The Beta Rank Function (BRF) is a two-parameter rank-size function (inverse survival function) defined by

| (3) |

where and are free parameters. The parameter is related to the scale of the data: it can be estimated from the data or, if the data is re-scaled, can be simply set to 1. It is straightforward to see that implies , so the BRF is strictly decreasing over . Therefore, the inverse function exists within this interval. As we mentioned, the BRF coincides with the Hankin-Lee-Davies quantile function proposed in [35] or power-Pareto distribution introduced in [36]. The connection between BRF and the Hankin-Lee-Davies function has already been noticed in [40].

3 Particular cases of the BRF

In this section we review some of the known results concerning special cases of the Beta Rank Function in Eq.(3).

3.1 BRF yields a constant random variable when

When , is a constant function, meaning there is one single outcome with non-zero probability. In other words, the BRF corresponds to a degenerate random variable with a delta distribution at the position .

3.2 BRF yields a uniform distribution when and

If and , Eq.(3) is reduced to

This equation can be solved exactly for , , yielding the cdf . Differentiating we get the pdf

| (4) |

Notice that implies , hence the restriction . Direct integration shows that this random variable has expectation and its variance is given by . For this case, we can give a closed-form formula for the characteristic function,

Notice that Eq.(4) is the density of a uniform random variable over if . Also notice that the result in the previous subsection () can be re-created:

3.3 BRF yields a Pareto distribution when

If and , then the BRF reduces to

which can be exactly solved for , . Differentiating it leads to pdf

This is the (one-tail) Pareto distribution with shape parameter and scale parameter . If , the mean exists and it is equal to ; if , the variance exists and it is equal to . The characteristic function is given by the formula

where is the exponential integral function.

3.4 BRF yields a Lavalette distribution when

As discussed with detail in [26], can be solved analytically when : , and its negative derivative leads to the pdf

| (5) |

Detailed information about its expectation and variance, as well as applications, can be consulted in the reference cited above.

Before analyzing the properties of the pdf associated to the BRF, we will study the pdf of the random variable , where follows a BRF.

4 The log-BRF family of distributions

4.1 Logarithmic transformation of the independent variable is a key step to simplify the probability density function for the BRF

Following the results from the previous section, we would like to derive the general form of the pdf corresponding to the BRF in Eq.(3). However, we cannot hope to invert the rank-size function in order to write a general formula for this pdf in a closed-form. To see this, note that in order to obtain the pdf from the rank function we need to obtain the cdf first, which is the solution for . From Abel-Ruffini’s impossibility theorem, polynomial equations higher than 4th order do not have a general, explicit algebraic solution (e.g. [41]). However, we obtained multiple hints that log-transforming may simplify the characterization of the probability density function.

The first hint came from the Lavalette function, which is similar to the log-normal distribution [26]. Both from the analytic expression and by numerical validation, it is also known that the Lavalette is not equivalent to the lognormal distribution [26]. We can derive the pdf for from Eq.(3). Note that implies . We denote and define , then

| (6) |

This expression is already much simpler than Eq.(5): it is the reciprocal square of the catenary curve [42].

The expression in Eq.(6) makes the analysis of the Lavalette distribution easier. It is more obvious from this functional form that the distribution of the logarithm of a Lavalette random variable, just as the normal distribution, is symmetric around the peak in . Near the peak, Lavalette and log-normal distributions are similar because the linear term in the Taylor expansion is zero, leaving only the quadratic term:

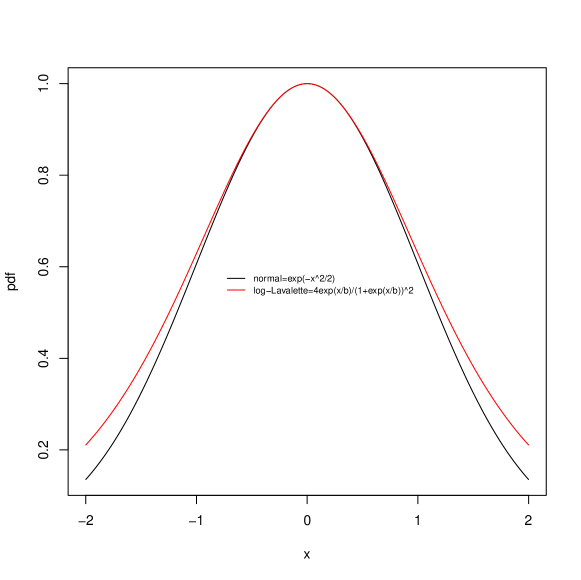

When this is compared to a similar Taylor expansion of a standard normal density near the peak, , we have .

Fig.2 compares the pdfs of the standard normal distribution and the log-transformed Lavalette distribution for . Since the parameter is chosen to fit the two functions near the peak, the two indeed match very well. When the independent variable is far away from the peak, however, the log-transformed Lavalette decays not as fast as the normal distribution. The larger deviation between the two when the independent variable is away from the peak, despite the similarity near peak position, has already been observed in [26].

4.2 Definition of the log-BRF distribution

Informally, consider a continuous random variable such that its inverse survival function (the rank-size function) is given by

Recall that the inverse survival function at is equivalent to the quantile of the distribution. Consider the continuous random variable . We will see that we can compute the characteristic function of , which will provide us a way to give a formal definition of its distribution.

Let and be the densities of and . Because and , then , therefore

Here we have used the definition of the complex exponentiation and we are taking the principal branch of the logarithm.

We define that the continuous random variable follows a log-BRF distribution with parameters , and if its characteristic function is represented by the formula

It is possible to give a closed-form expression of the pdf of in terms of the Fox H-function,

See Appendix 9.3 for a detailed derivation of this density and for the definition and properties of the function.

4.3 Mean, variance, and median of

From the log-transformed BRF we can directly compute the first two moments of . We have

and

therefore,

Interestingly, the variance does not depend on and it increases with a product of and (assuming is similar to ).

The median of corresponds to the value where :

From these formula, it is clear that determine the location of the peak, but not the shape, of the distribution.

4.4 The probability partition by the peak and peak position (mode) in

We ask the question, for , what is the value where is the largest? And how is the probability being divided by the peak? In fact, the answer of the second question provides an answer of the first question.

At the peak position, the first derivative of is zero. Using an expression for in terms of (that we will derive in Section 4.5, Eq.(9)), we see that

which leads to

and the solution is

is the cdf accumulated up to the peak position and is the total probability on the right side of the peak. This result shows that the peak partitions the probability in by the ratio.

Since has a simple relation with (which we will derive in section 4.5, Eq.(8)), we can obtain the peak position in :

| (7) |

The second and the third terms above tend to cancel each other, so often is close to .

All the statistical properties of that we have computed are summarized in Table 1.

| properties of | |

|---|---|

| mean | |

| median | |

| mode | |

| variance | |

4.5 decays exponentially away from the peak

We first illustrate our conclusion by three special cases (uniform, Pareto and Lavalette), then we corroborate it by numerical simulation and finally we prove it analytically.

Recall that the identity implies that the pdf in is . For a uniform distribution, where , we have . For the Pareto distribution the pdf is , therefore . In both situations the decay from the peak () is exponential. For the uniform distribution the decay is towards the negative values, whereas for the Pareto distribution it is towards the positive axes. The transition between a power-law and an exponential distribution through a log-transformation (or exponential-transformation in the other direction) of the variable has been noticed before [43, 44, 45] (see section 14.2 of [46] for other possible transformations).

The Lavalette distribution is somewhat different from the uniform and Pareto distribution because it decays on both sides of the peak, and the decay near the peak is normal-like (). However, when is large, from Eq.(6):

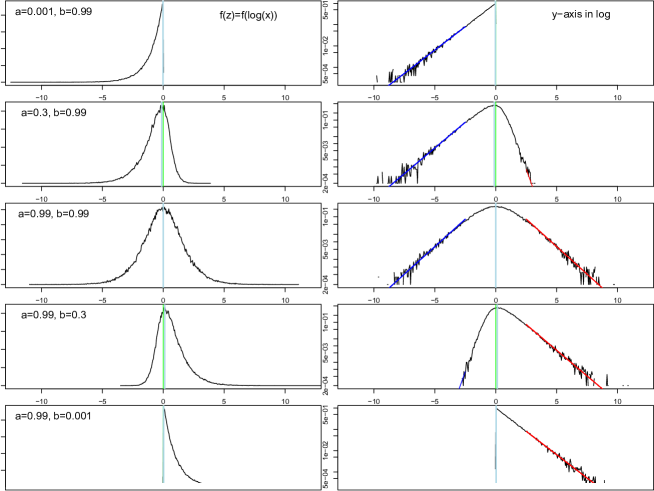

Numerically, we can either approximate the distribution with a histogram of the sampled values, or by the numerical approximation of the functional form. Fig.3 shows histograms of (log-transformed) randomly sampled values according to the procedure described in section 5.3 (with , and various , values). When the histogram which approximates is log-transformed, on the right panel of Fig.3, it is clear that the decay from the peak on both tails is exponential. We use the fittings on left and on the right and see that both fit the empirical perfectly.

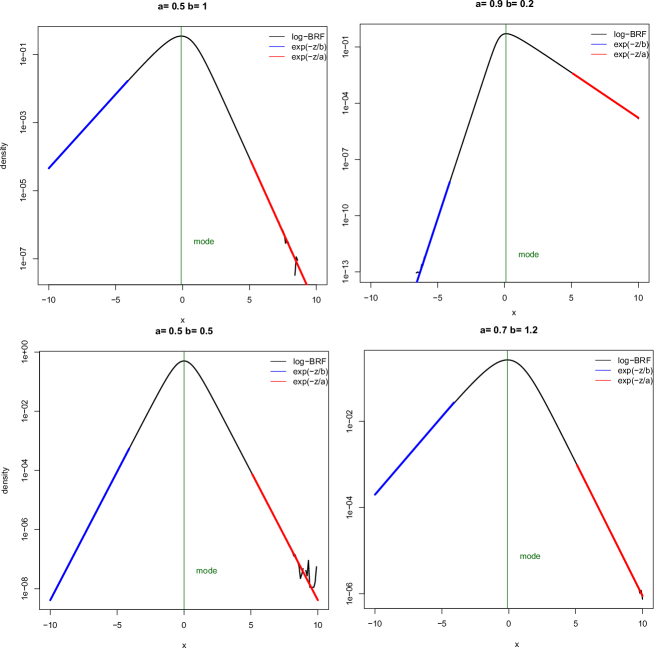

As an independent check, we use the numerical approximation procedure described in section 5.4 to generate the at several parameter values and the result is shown in Fig.4. Again, the blue line on the left side of the peak is and the red line on the right side of the peak is ; both fit perfectly with the numerical approximation of the .

Now we show analytically that both tails of are approximately exponential without knowing the analytic form of . First, we derive the relationship between and :

| (8) |

The pdf is the negative derivative of :

Then (note that the cdf is ):

| (9) |

Near the right tail (from Eq.(8), at the limit, ):

| (10) |

Near the left tail (similarly from Eq.(8), at the limit, ):

| (11) |

Now we not only know that decays exponentially on both tails (and log-exponentially, thus algebraically for ), but also we know the parameters and control the left and right side of the exponential decay rate respectively. When , the two decay rates are equal. When , the decay on the right side of the peak decays slower and vice versa. This result is consistent with the probability partition by the peak discussed in the previous subsection: when , the decay on the right side of the peak is slower, thus occupying more probability area underneath and the other way around. The same result for is also obtained in [35].

4.6 Cubic term and asymmetry near the peak of

We have just shown that decays exponentially on both sides of the peak with (usually) different decay rates. This leads to an asymmetry around the peak, which requires higher order terms beyond the quadratic term in a Taylor expansion. Our previous results on quadratic approximation of Lavalette function can not be applied.

Using Taylor expansion, we have

| (12) |

near the peak . From the relationship , we also have that near ,

which we can solve for ,

Substituting this in Eq.(12) and rearranging terms we get a polynomial expansion for near the mode ,

where

Since the quadratic term is symmetric around the peak, whereas the cubic term is not, we expect will increase if and are more different. Fig.5 shows as a function of . Indeed, the cubic term dominates the quadratic term when and are very different.

5 The BRF family of distributions

Once we have defined the log-BRF distribution, we can formally define that the continuous random variable follows a BRF distribution with parameters and if the random variable follows a log-BRF distribution. According to this definition, the pdf of must have non-negative support (because is always a non-negative number).

The pdf of can be written in terms of the Fox function, with the formula

See Appendix 9.3 for a detailed derivation of this expression and for the characteristic function of this distribution. This makes the BRF a particular case of the Fox-H distribution, defined as the family of non-negative distributions whose pdf can be expressed by a function of this class. The Fox-H family of distributions is closed under products and quotients, thus suggesting possible generating mechanisms of the BRF distribution [47].

5.1 Moments of are given by a Beta function

Recall the special function called Euler integral (or Beta function):

The moments of can be represented by this special function:

which is finite if .

5.2 Median and peak position (mode) for

The aim here is to find the solution for . First, the first derivative of is the second derivative of : . Secondly, there is a relation between the second derivative of a function and that of its inverse function:

so we now can solve instead. Take the second derivative of Eq.(3), we have

whose solution is:

An equivalent solution can be derived by using :

When , setting the second derivative to zero is to solve a linear equation:

which leads to the solution

5.3 Randomly sampling variables from the BRF distribution

Because is the cdf, randomly sampling values from a (0,1) uniform distribution also randomly samples cdf values. Since is a simple function of , the corresponding values thus obtained represent a random sampling from the BRF distribution. The general idea on this procedure can be found in [48]. A simple R (https://www.r-project.org/) code can be (e.g.) the following:

Ψa <- 0.5 Ψb <- 1.2 ΨA <- 1 Ψnump <- 1E6 Ψu <- runit(nump) Ψx <- A*(1-u)^b/u^a

5.4 Numerical approximation of the pdf

Getting the pdf of the BRF distribution requires inverting the rank-size function , which can be seen as a root-finding step, then differentiating the function . The first step is a problem we cannot analytically solve, but there are several algorithms to do it numerically. Thus, we can combine a numeric root-finding procedure with some numerical differentiation rule to establish an algorithm to numerically approximate the pdf of a BRF. For the sake of illustration, we propose the following algorithm: (i) Choose a tolerance interval for root finding and a step size for numerical differentiation; (ii) use a root-finding method to solve Eq.(3) for , i.e., find the root of , then ; (iii) use finite-difference coefficients to compute .

There are several combinations of root finding (step (ii)) and numerical differentiation techniques (step-(iii)) that can be used. Consider, for instance, bisection method for step (ii), which guarantees convergence, and one-dimensional five-point stencil for step (iii). The error of this algorithm with these two numerical methods are discussed below; from one side, we have the finite difference approximation for the derivative,

where . Let be the numerically determined cdf from step (ii), implying that this differs from the real value of in less than the tolerance interval, . Consequently, , and we can compute the total error:

meaning that the error of the algorithm is of order We show some examples of this procedure in Fig.6.

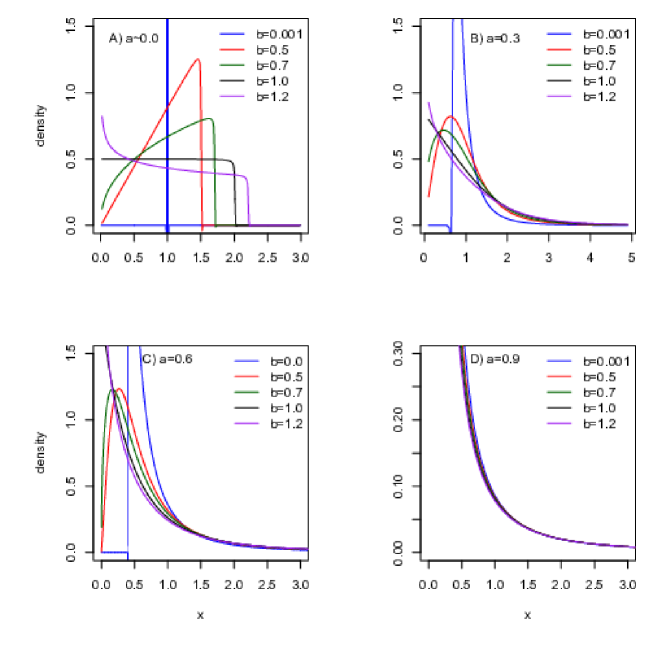

Notice in Fig.6A that, when , the pdfs are defined over a finite interval, as expected from section 3.2. We can see the constant random variable with its delta pdf (blue line), as well as the uniform distribution (black line). At , the pdfs shift from being increasing to decreasing. The pdfs are always unimodal, but for the peak can be either at or to the right, depending on the value of , as can be seen in Fig.6B and C. When , the location of the maximum shifts from a positive to a zero value. Notice also that, when , the pdf exhibits a typical power-law behavior with a cut-off, as expected from section 3.3. Interestingly, the parameter completely dominates the behavior of the pdf when it is close to : as can be seen in Fig.6D, pdfs with different values for become hard to distinguish from one another.

6 Using the properties of the BRF and log-BRF distributions in data analysis

6.1 Modeling log-returns of financial indexes with log-BRF distribution

Understanding the properties of provides us with very simple approaches to distinguish the distribution type in real data. In order to analyze data that may be well described by a log-BRF distribution (unimodal, support on the entire real axis, exponential decay on both tails) we propose the following pipeline: (1) plot the histogram of a set of observations with the -axis in log scale; (2) examine the shape of the histogram with in log scale to infer the type of the distribution that produced the observations.

As an illustration of this pipeline, consider the analysis of logarithmic returns of financial assets or indexes. Recall that if denotes the price of a certain financial asset at time , then is called the gross one-period simple return and is called the logarithmic gross simple return of the asset (which we simply call the log-return of the asset). Classical models such as the Black-Scholes-Merton model imply that log-returns are normally distributed; however, several observations point to the presence of a fatter than normal tail on these distributions ([49, 50]). This seems like a good candidate to test our suggested pipeline.

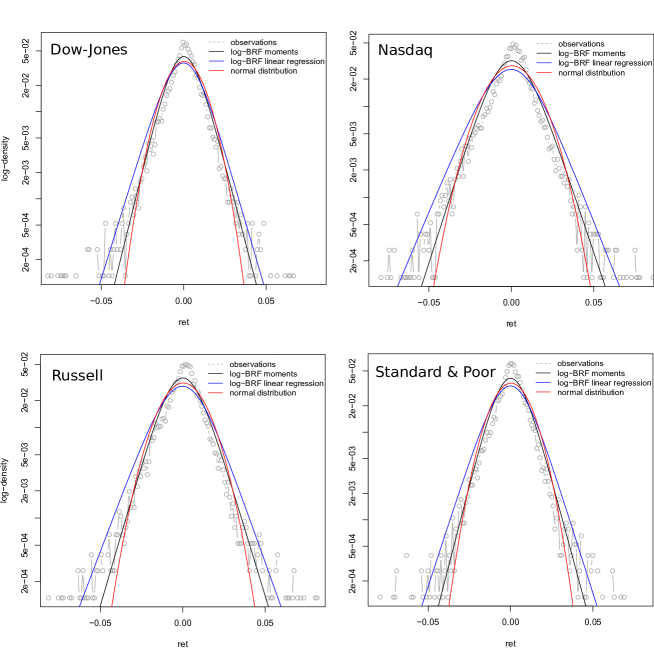

We analyzed daily log-returns over a 30 year period (from April 24 1989 to April 18 2019) of four different financial indexes: Dow Jones Industrial Average, NASDAQ Composite, Standard and Poor 500 and Russell 2000. Data were downloaded from https://finance.yahoo.com/.

We propose two different methods to estimate the parameters and of the BRF-density from the data (we do not know the exact form of the pdf, so more common methods, such as maximum likelihood, are not available). First we utilize the method of moments, by equating the first two sample central moments to the known expressions of and . The estimator we get from this method are

where and are sample mean and variance respectively. In order to reduce the bias of these estimators, we utilize the Jackknife re-sampling technique, by aggregating the estimates of reduced samples.

The second method we propose considers the fact that, in semi-log scale, a log-BRF decays linearly on both tales, with gradient on the left tail and on the right. Thus, we can restrict to one of these two domains, approximate the density from the histogram and and fit the linear models and .

We show in Fig.7 the results of these analysis. For each of the four financial index that we modeled, we show in semi-log scale the histogram of the observations (gray), the fitted log-BRF distribution with parameters estimated by the moments method (black) and the linear regression technique (blue); we also show the fitted normal distribution (red). In all four cases we observe a similar behavior: neither log-BRF nor the normal/log-normal fits the data satisfactorily at the peak of the distribution, but the normal/lognormal model tends to sub-estimate the tails, which log-BRF does not. We also note that, apparently, the linear regression technique yields better estimations than the Jackknife-moments method; this is no surprise, since for the former we are censoring the data, restring the observations to a different domain for each parameter.

6.2 Modeling urban population with a BRF distribution

There are several examples in the literature that utilize the BRF distribution (or DGBD rank-size function) to fit data that looks like a power-law, but with a break at the upper tail ( high rank / small size regime). In addition to these numerous examples, we propose here the following pipeline, that takes advantage of the properties of the log-BRF distribution: (1) log-transform the data to ; (2) plot the histogram of with the -axis in log scale; (3) examine the shape of histogram with in log scale to infer the type of the distribution may follow.

For example, if the histogram with in log scale falls from the peak only on the right side as a straight line, the distribution should be approximately a one-sided power-law. If the histogram falls from both sides with roughly equal slope, the distribution is approximately lognormal, or lognormal-like. If the histogram falls from both sides linearly with different slopes, the distribution is a BRF (). If there are not much data on one sides of the peak, we do not have enough evidence to claim the distribution to be a BRF.

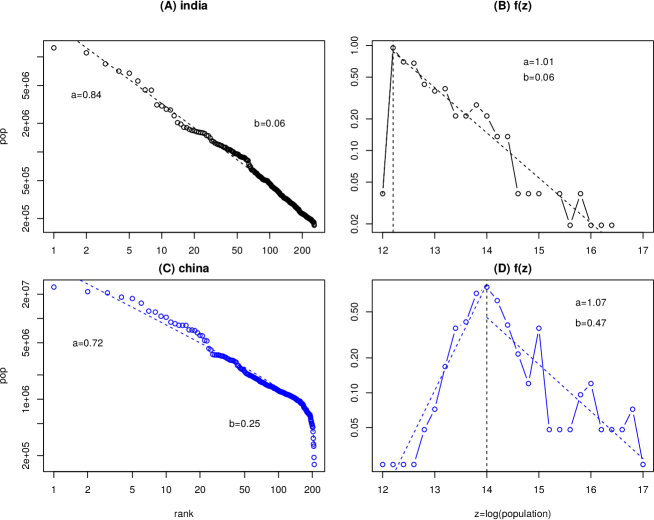

Fig.8 shows the India city population (2011 census) and China urban population (2010 census) represented in two different plots: the rank-population plot (Fig.8A,C), and the histogram of log-population (Fig.8A,C). The BRF in the rank-population plot can be fitted directly by the linear regression where is the population data, is the rank ( for the largest city), and .

In the histogram of , Fig.8B,D already provides some essential information without fitting. For example, Fig.8B indicates that India city population is mostly a one-sided power-law, as the peak is close to the left and the fall off from the peak on the left is very steep (indicating a small value). On the other hand, China urban population follows BRF better as the peak is closer to the middle, and the decay rate from both sides are different. Fitting the two sides by exponential decay leads to a qualitatively similar estimation of as the direct fitting in rank-population plot. The differences of the fitting values between the two approaches may be due to several factors: the choice of bin size in the histogram, the skipping of zero frequency in the histogram (as the logarithmic value diverges), etc.

Note that the left end of Fig.8A,C becomes right tail in Fig.8B,D, and vice versa. Fig.8B,D) also shows that the most likely India city population is 0.2 millions, and the most likely China urban population is 1.2 millions, in this particular data set.

7 Discussion and Conclusions

The Discrete Generalized Beta Distribution (DGBD) [1, 2], is developed mainly in the camp of Zipf’s law study [51, 26], which focus on one-sided power-law. Little attention was paid to the fact that, since DGBD is actually a two-sided power law, the better representation should be the pdf showing the peak and fall-off from the peak on both sides. We show in this paper that the crucial step in doing so is to log-transform the measured variable , , then the shape of the pdf becomes more clear.

By recognizing the peak in the middle of the distribution, we also recognize a fact that BRF, unlike the Pareto distribution, does not diverge at the peak, which is a problem for many other usage of one-sided power law functions. That divergence in one-sided power law is usually dealt with by adding a cutoff (truncation) [52].

The two approximate expressions of the log-BRF pdf on two sides of the peak (Eq.(10) and Eq.(11)) can be rewritten as (for ) and (for ), where . Using and (for simplicity, let us assume ), the BRF pdf in space is approximately (for ), and (for ). It illustrates again the importance of using the log-transformed variable, as the left size of the “peak” may not decay in if .

The functional form above appears in the literature recurrently with different names: log-Laplace distribution [53, 39], skewed log-Laplace distribution [54], and double Pareto distribution [38, 55]. These are exponential functions for log-transformed variables with a sharp angle at the peak. In 2004, Reed and Jorgensen proposed a new distribution which combines the double Pareto and the normal distribution, called “double-Pareto-lognormal” (DPLN) distribution [56], which has seen many applications [57, 58, 59, 60, 61] . This function, like BRF, has a smooth transition between the two sides at the peak. However, DPLN has four fitting parameters, two for the double Pareto and two for the normal distribution, whereas the BRF distribution only has two, without the need to use another normal distribution to smooth the function. The lesser number of parameters also makes BRF a flexible function to be utilized in data analysis, as we demonstrated in this paper through several examples.

With a better understanding of the pdf of BRF, we now can clarify confusions with the Beta distribution whose pdf is [62]. The range of is (0, ) for BRF, but is (0,1) in Beta distribution. BRF is unimodal, whereas Beta distribution may have two peaks (or two singularity points). When both BRF and Beta distribution are symmetric. However, BRF falls from the peak as inverse power-law, whereas Beta distribution as a concave quadratic function or its power. Needless to say, BRF and Beta distribution are not the same.

It is interesting that DGBD or BRF has been independently discovered multiple times in other fields. We are aware of at least two publications, one by Gilchrist in section 1.6 of [36], and another by Hankin and Lee (but attributed to Davies through private communication) in [35], in the context of quantile functions [63]. In a quantile function, the quantile value of a random variable is expressed as a function of the cumulative probability . This framework to represent a probability distribution is exactly in parallel to the rank-size plot, one of the two versions used to illustrate Zipf’s law [64, 65, 66], if we convert to the normalized rank . Neither [36] nor [35] explored the possibility of using the log-transformed variable and its impact on functional form of the probability distribution. This is however the trick that allowed us to derive many analytic results not available in [36, 35].

BRF is an example of a distribution where the closed-form analytic expression of the pdf or cdf is not generally available (i.e., it is not expressed by a finite number of “well-known” functions). However, its pdf is expressible as a function of its cdf or rank variable [35]. Here we further show that BRF’s pdf can be expressed in terms of Fox-H functions, which provides a rigorous definition of both functions (with and without log transformation of the variable). This task is accomplished by using the characteristic functions.

In conclusion, we provide a most comprehensive analysis of the continuous-rank version of DGBD or BRF, pointing out the key step in log-transforming the variable. We have obtained expressions for the mean, median, mode, variance and other quantities of the log-BRF. We have established the basic shape of the distribution. The parallelism between BRF and double-Pareto distribution, skewed log-Laplace distribution, and double-Pareto-lognormal distribution makes it one more useful function to fit real-world data with an appropriate statistical feature.

8 Acknowledgments

This work was partially supported by UNAM-PAPIIT grant IN108318. OF is a grant holder of the UNAM-DGAPA Postdoctoral Scholarships Program at CEIICH, UNAM. WL acknowledges the support from Robert S Boas Center for Genomics and Human Genetics.

References

- [1] R. Mansilla, E. Köppen, G. Cocho, and P. Miramontes, “On the behavior of journal impact factor rank-order distribution,” Journal of Informetrics, vol. 1, no. 2, pp. 155–160, 2007.

- [2] G. Martínez-Mekler, R. Alvarez-Martínez, M. del Río, R. Mansilla, P. Miramontes, and G. Cocho, “Universality of rank-ordering distributions in the arts and sciences,” PLoS One, vol. 4, no. 3, p. e4791, 2009.

- [3] L. Egghe, “Mathematical derivation of the impact factor distribution,” Journal of Informetrics, vol. 3, no. 4, pp. 290–295, 2009.

- [4] J. Campanario, “Distribution of ranks of articles and citations in journals,” Journal of the American Society for Information Science and Technology, vol. 61, no. 2, pp. 419–423, 2010.

- [5] W. Li, P. Miramontes, and G. Cocho, “Fitting ranked linguistic data with two-parameter functions,” Entropy, vol. 12, no. 7, pp. 1743–1764, 2010.

- [6] A. Petersen, H. Stanley, and S. Succi, “Statistical regularities in the rank-citation profile of scientists,” Scientific reports, vol. 1, p. 181, 2011.

- [7] R. Alvarez-Martinez, G. Martinez-Mekler, and G. Cocho, “Order–disorder transition in conflicting dynamics leading to rank–frequency generalized beta distributions,” Physica A: Statistical Mechanics and its Applications, vol. 390, no. 1, pp. 120–130, 2011.

- [8] W. Li and P. Miramontes, “Fitting ranked english and spanish letter frequency distribution in us and mexican presidential speeches,” Journal of Quantitative Linguistics, vol. 18, no. 4, pp. 359–380, 2011.

- [9] W. Li, “Analyses of baby name popularity distribution in us for the last 131 years,” Complexity, vol. 18, no. 1, pp. 44–50, 2012.

- [10] W. Li, “Fitting chinese syllable-to-character mapping spectrum by the beta rank function,” Physica A: Statistical Mechanics and its Applications, vol. 391, no. 4, pp. 1515–1518, 2012.

- [11] W. Li, “Characterizing ranked chinese syllable-to-character mapping spectrum: A bridge between the spoken and written chinese language,” Journal of Quantitative Linguistics, vol. 20, no. 2, pp. 153–167, 2013.

- [12] A. Petersen, S. Fortunato, R. Pan, K. Kaski, O. Penner, A. Rungi, M. Riccaboni, H. Stanley, and F. Pammolli, “Reputation and impact in academic careers,” Proceedings of the National Academy of Sciences, vol. 111, no. 43, pp. 15316–15321, 2014.

- [13] M. Ausloos, “Two-exponent lavalette function: A generalization for the case of adherents to a religious movement,” Physical Review E, vol. 89, no. 6, p. 062803, 2014.

- [14] M. Ausloos, “Intrinsic classes in the union of european football associations soccer team ranking,” Open Physics, vol. 12, no. 11, pp. 773–779, 2014.

- [15] B. Finley and K. Kilkki, “Exploring empirical rank-frequency distributions longitudinally through a simple stochastic process,” PloS one, vol. 9, no. 4, p. e94920, 2014.

- [16] W. Li, J. Freudenberg, and P. Miramontes, “Diminishing return for increased mappability with longer sequencing reads: implications of the k-mer distributions in the human genome,” BMC bioinformatics, vol. 15, no. 1, p. 2, 2014.

- [17] S. Valverde and R. Solé, “A cultural diffusion model for the rise and fall of programming languages,” Human biology, vol. 87, no. 3, pp. 224–234, 2015.

- [18] J. Morales, S. Sánchez, J. Flores, C. Pineda, C. Gershenson, G. Cocho, J. Zizumbo, R. F. Rodríguez, and G. Iñiguez, “Generic temporal features of performance rankings in sports and games,” EPJ Data Science, vol. 5, no. 1, p. 33, 2016.

- [19] W. Li, O. Fontanelli, and P. Miramontes, “Size distribution of function-based human gene sets and the split–merge model,” Royal Society open science, vol. 3, no. 8, p. 160275, 2016.

- [20] O. Fontanelli, P. Miramontes, G. Cocho, and W. Li, “Population patterns in world’s administrative units,” Royal Society open science, vol. 4, no. 7, p. 170281, 2017.

- [21] T. Fenner, E. Kaufmann, M. Levene, and G. Loizou, “A multiplicative process for generating a beta-like survival function with application to the uk 2016 eu referendum results,” International Journal of Modern Physics C, vol. 28, no. 11, p. 1750132, 2017.

- [22] R. Alvarez-Martinez, G. Cocho, and G. Martinez-Mekler, “Rank ordered beta distributions of nonlinear map symbolic dynamics families with a first-order transition between dynamical regimes,” Chaos: An Interdisciplinary Journal of Nonlinear Science, vol. 28, no. 7, p. 075515, 2018.

- [23] V. Nguyen, O. Markelov, A. Serdyuk, A. Vasenev, and M. Bogachev, “Universal rank-size statistics in network traffic: Modeling collective access patterns by zipf’s law with long-term correlations,” EPL (Europhysics Letters), vol. 123, no. 5, p. 50001, 2018.

- [24] D. López, P. Camus, N. Valdivia, and S. Estay, “Food webs over time: evaluating structural differences and variability of degree distributions in food webs,” Ecosphere, vol. 9, no. 12, p. e02539, 2018.

- [25] A. Ghosh and B. Basu, “Universal city-size distributions through rank ordering,” Physica A: Statistical Mechanics and its Applications, vol. 528, p. 121094, 2019.

- [26] O. Fontanelli, P. Miramontes, Y. Yang, G. Cocho, and W. Li, “Beyond zipf’s law: the lavalette rank function and its properties,” PloS one, vol. 11, no. 9, p. e0163241, 2016.

- [27] D. Lavalette, “Facteur d’impact: impartialité ou impuissance,” Orsay (France): Institut Curie—Recherche, Bât, vol. 112, 1996.

- [28] I.-I. Popescu, M. Ganciu, M.-C. Penache, and D. Penache, “On the lavalette ranking law,” Romanian Reports in Physics, vol. 49, pp. 003–028, 1997.

- [29] I.-I. Popescu, “On a zipf’s law extension to impact factors.,” Glottometrics, vol. 6, pp. 83–93, 2003.

- [30] I. Voloshynovska, “Characteristic features of rank-probability word distribution in scientific and belletristic literature,” Journal of Quantitative Linguistics, vol. 18, no. 3, pp. 274–289, 2011.

- [31] D. Lavalette, “A general purpose ranking variable with applications to various ranking laws,” Exact Methods in the Study of Language and Text, pp. 371–382, 2011.

- [32] E. Chlebus and G. Divgi, “A novel probability distribution for modeling internet traffic and its parameter estimation,” in IEEE GLOBECOM 2007-IEEE Global Telecommunications Conference, pp. 4670–4675, IEEE, 2007.

- [33] G. Naumis and G. Cocho, “Tail universalities in rank distributions as an algebraic problem: The beta-like function,” Physica A: Statistical Mechanics and its Applications, vol. 387, no. 1, pp. 84–96, 2008.

- [34] M. Beltrán del Río, G. Cocho, and R. Mansilla, “General model of subtraction of stochastic variables. attractor and stability analysis,” Physica A: Statistical Mechanics and its Applications, vol. 390, no. 2, pp. 154–160, 2011.

- [35] R. Hankin and A. Lee, “A new family of non-negative distributions,” Australian & New Zealand Journal of Statistics, vol. 48, no. 1, pp. 67–78, 2006.

- [36] W. Gilchrist, Statistical modelling with quantile functions. Chapman and Hall/CRC, 2000.

- [37] M. Brzezinski, “Empirical modeling of the impact factor distribution,” Journal of Informetrics, vol. 8, no. 2, pp. 362–368, 2014.

- [38] W. Reed, “The pareto, zipf and other power laws,” Economics letters, vol. 74, no. 1, pp. 15–19, 2001.

- [39] S. Kotz, T. Kozubowski, and K. Podgorski, The Laplace distribution and generalizations: a revisit with applications to communications, economics, engineering, and finance. Springer Science & Business Media, 2012.

- [40] J. Sarabia, F. Prieto, and C. Trueba, “Modeling the probabilistic distribution of the impact factor,” Journal of Informetrics, vol. 6, no. 1, pp. 66–79, 2012.

- [41] H. Żoła̧dek et al., “The topological proof of abel-ruffini theorem,” Topological Methods in Nonlinear Analysis, vol. 16, no. 2, pp. 253–265, 2000.

- [42] D. Huang, “Impact factor distribution revisited,” Physica A: Statistical Mechanics and its Applications, vol. 482, pp. 173–180, 2017.

- [43] W. Li, “Random texts exhibit zipf’s-law-like word frequency distribution,” IEEE Transactions on information theory, vol. 38, no. 6, pp. 1842–1845, 1992.

- [44] W. Li, “Comments on ‘bell curves and monkey languages’ (letter to the editor),” Complexity, vol. 1, no. 6, p. 6, 1996.

- [45] Z. Czechowski, “Transformation of random distributions into power-like distributions due to non-linearities: application to geophysical phenomena,” Geophysical Journal International, vol. 144, no. 1, pp. 197–205, 2001.

- [46] D. Sornette, Critical phenomena in natural sciences: chaos, fractals, selforganization and disorder: concepts and tools. Springer Science & Business Media, 2006.

- [47] B. Carter and M. Springer, “The distribution of products, quotients and powers of independent h-function variates,” SIAM Journal on Applied Mathematics, vol. 33, no. 4, pp. 542–558, 1977.

- [48] L. Devroye, Non-Uniform Random Variate Generation. Springer Science & Business Media, 2013.

- [49] H. Stanley and R. Mantegna, An introduction to econophysics. Cambridge University Press, Cambridge, 2000.

- [50] D. Sornette, Why stock markets crash: critical events in complex financial systems, vol. 49. Princeton University Press, 2017.

- [51] P. Miramontes, W. Li, and G. Cocho, “Some critical support for power laws and their variations,” arXiv preprint arXiv:1204.3124, 2012.

- [52] A. Clauset, C. Shalizi, and M. Newman, “Power-law distributions in empirical data,” SIAM review, vol. 51, no. 4, pp. 661–703, 2009.

- [53] C. Taillie, G. Patil, and B. Baldessari, Statistical Distribution in Scientific Work: Applications in Physical, Social and Life Sciences, vol. 6. Springer Science & Business Media, 1981.

- [54] T. Kozubowski and K. Podgórski, “Log-laplace distributions,” International Mathematical Journal, vol. 3, pp. 467–495, 2003.

- [55] F. Al-Athari, “Parameter estimation for the double-pareto distribution,” Journal of mathematics and statistics, vol. 7, no. 4, pp. 289–294, 2011.

- [56] W. Reed and M. Jorgensen, “The double pareto-lognormal distribution—a new parametric model for size distributions,” Communications in Statistics-Theory and Methods, vol. 33, no. 8, pp. 1733–1753, 2004.

- [57] W. Reed, “On the rank-size distribution for human settlements,” Journal of Regional Science, vol. 42, no. 1, pp. 1–17, 2002.

- [58] M. Csűrös, L. Noé, and G. Kucherov, “Reconsidering the significance of genomic word frequencies,” Trends in Genetics, vol. 23, no. 11, pp. 543–546, 2007.

- [59] K. Giesen, A. Zimmermann, and J. Suedekum, “The size distribution across all cities–double pareto lognormal strikes,” Journal of Urban Economics, vol. 68, no. 2, pp. 129–137, 2010.

- [60] G. Hajargasht and W. Griffiths, “Pareto–lognormal distributions: Inequality, poverty, and estimation from grouped income data,” Economic Modelling, vol. 33, pp. 593–604, 2013.

- [61] A. Toda, “A note on the size distribution of consumption: More double pareto than lognormal,” Macroeconomic Dynamics, vol. 21, no. 6, pp. 1508–1518, 2017.

- [62] M. Jambunathan, “Some properties of beta and gamma distributions,” The Annals of mathematical Statistics, vol. 25, no. 2, pp. 401–405, 1954.

- [63] E. Parzen, “Nonparametric statistical data modeling,” Journal of the American Statistical Association, vol. 74, no. 365, pp. 105–121, 1979.

- [64] C. Urzúa, “A simple and efficient test for zipf’s law,” Economics Letters, vol. 66, pp. 257–260, 2000.

- [65] W. Li, “Zipf’s law everywhere,” Glottometrics, vol. 5, pp. 14–21, 2002.

- [66] R. Rousseau, “George kingsley zipf: life, ideas, his law and informetrics,” Glottometrics, vol. 3, pp. 11–18, 2002.

- [67] F. Katscher, “How tartaglia solved the cubic equation,” Convergence (MAA). http://www. maa. org/press/periodicals/convergence/how-tartaglia-solved-the-cubic-equation, 2011.

- [68] A. Mathai and R. Saxena, The H function with applications in statistics and other disciplines. Wiley, 1978.

9 Appendixes

9.1 Appendix A - Analytic expression of when and

In the next few appendixes, we present a few analytic results without using the independent variable log-transformation. As will be seen, the derivation of these analytic formula is more tedious. The first example is the analytic expression of when is exactly twice the value of . The steps towards an analytic solution is: (i) obtain the inverse function from by solving an algebraic equation; (ii) since cdf is ,

or

The solution is:

Take the derivative:

The second example is when :

or

with solution

Take the derivative:

9.2 Appendix B - The probability density function when and

When , we have a relationship between and ( is the cumulative density function):

| (13) |

or

The left-hand-side term is negative () when , and positive ( ) when . Also, the first derivative (slope), , is always positive. Therefore, Eq.(13) has a single solution for when . Using Tartaglia’s trick [67] (for with ), the solution is:

where .

The pdf is the derivative (note ):

When , the procedure is very similar:

or

The solution is

where .

Take the derivative :

Exact pdf expressions for and are still possible to derive with this methodology, but they are extremely cumbersome to be included here.

9.3 Appendix C - Characteristic function and a closed-form representation of and

The pdf of Z is the inverse Fourier transform of the characteristic function. Hence we can get an integral formula for the pdf of Z,

With this formula and the relationship we can write an integral formula for the pdf of ,

We are taking again the principal branch of the logarithm. Recall the relationship between the Beta and the Gamma function,

| (14) |

Now, recall the definition of the Fox H-function. The H-function is defined by the Mellin-Barnes type contour integral

where the function is defined by

An empty product is considered as unit. Here, , ; , , and are integers such that and ; and are positive real numbers: and are real or complex numbers such that no pole of coincides with a pole of . Finally, is a contour on the complex plane running from to for some real constant such that the poles from lie to left of and all poles of lie to the right of . Conditions for the existence of the contour and for the existence and analyticity of the function are comprehensively enumerated in [68].

The following properties of the H-function can be deduced directly from the definition:

-

1.

-

2.

-

3.

By using (14) and making the substitution , we can write the pdf of as

Notice that we can write

by doing , , , , and . Therefore, we can write the pdf of the BRF random variable in terms of an function,

for . It is possible to write this pdf in another form by means of the properties of the function,

Finally, we can also write the pdf of in terms of the function,