Abstract

Consider a random vector , where is -dimensional and is one-dimensional. We suppose that the random variable is subject to random right censoring and satisfies the -mixing property. The aim of this paper is to study the behavior of the kernel estimator of the relative error regression and to establish its uniform almost sure consistency with rate. Furthermore, we have highlighted the covariance term which measures the dependency. The simulation study shows that the proposed estimator performs well for a finite sample size in different cases.

Keywords:

Censored data and Kernel estimate and Relative error regression and Strong mixing condition and Uniform almost sure consistency.∎

On the strong uniform consistency for relative error of the regression function estimator for censoring times series model

BOUHADJERA Feriel. 1, 2

1 Université Badji-Mokhtar, Lab. de Probabilités et Statistique. BP 12, 23000 Annaba, Algérie.

OULD SAÏD Elias. Corresponding author.

2 Université du Littoral Côte d’Opale. Lab. de Math. Pures et Appliquées. IUT de Calais. 19, rue Louis David. Calais, 62228, France.

1 Introduction

Let be a strictly positive random variable (r.v.) representing the survival time of an individual taking part to an experimental study and let be a vector of covariate taking values in that gives us information about the individuals (age, sex, …). This paper is concerned with the nonparametric regression model: where is a regression function and is a r.v. (corresponding to the residual) such that . Recall that, is usually modeled by the following minimization problem . However this loss function is unsuitable when the data contains some outliers, which is a relatively common case in practice. To avoid this drawback, another approach is to build an efficient estimator of given by the minimization of the mean squared relative error given by

| (1.1) |

This kind of model is called relative error regression (RER) which has been studied by many authors. We can refer to Narula and Wellington (1977), Makridakis et al. (1984) in the parametric case. Recall that Park and Stefanski (1998) showed that the solution of (1.1) satisfies, for ,

| (1.2) |

In the nonparametric analysis, there exist some papers dealing with the estimation of the RER. Without pretending to exhaustivity, we quote

Jones et al. (2008) considered kernel and local linear approach to estimate the regression function, Attouch et al. (2015) regarded the problem of estimating the regression function for spatial data and Demongeot et al. (2016) considered the case where the explanatory variable are of functional type of data. Shen and Xie (2013) obtained the strong consistency of the regression estimator under -mixing data. Their result has been generalized to dependent case by Li et al. (2016).

In the case of incomplete data, for independent and identically distributed (i.i.d.) random variables under random right censoring, Guessoum and Ould Said (2008) studied the consistency and asymptotic normality of the kernel estimator of the regression function.

Many statistical results have been established by considering independent samples. It is then interesting to consider the more realistic situation when the observation are no longer i.i.d. This is for exemple the case, in clinical trials studies, not infrequently, patients from the same hospital have correlated survival times, due to unmeasured variables such as the skill or training of the staff or the quality of the hospital equipment (for more details, see : Lipsitz and Ibrahim, 2000).

Few papers deal with the regression function under censoring in the dependent case. We can cite Cai (1998) who studied the asymptotic properties of Kaplan-Meier’s estimator of censored dependent data and Cai (2001) who addressed the estimation of the distribution function for censored time series data. El Ghouch and Van Keilegom (2008, 2009) estimated the regression and conditional quantile functions by applying local linear method. Guessoum and Ould Said (2010, 2012) studied the consistency and the asymptotic normality of the kernel estimator for the regression function for censored dependent data.

Here we derive the uniform consistency result over a compact set with rate of the RER estimator for dependent case and censored data by highlighting the covariance term which does not appear in many papers. This paper is organized as follows. In Section 2, we recall some notations and definitions needed in our model. The hypotheses and main result are given in Section 3. Simulations study are drawn in Section 4. Finally, the proofs are relegated to Section 5 with some auxiliary results.

2 Presentation of the model

Consider a randomly right-censored model given by two non-negative stationary sequences, which represents the survival time with common unknown absolutely continuous distribution function (d.f.) and the censoring time with common unknown d.f. . In this context, we observe the pairs , where

and denotes the indicator function of the set . Let be a sequence of copies of the random vector and denote by the components of . The study we perform below is then on the set of observations . Having in mind this kind of model, we define a pseudo-estimator of the relative error for the regression function, for all , by

| (2.1) |

with and , where is a density function defined on and is a sequence of positive numbers.

In this kind of model, it is well known that the empirical distribution is not a consistent estimator for the df . Therefore, Kaplan-Meier (1958) proposed a consistent estimator for survival function which is defined as

| (2.2) |

where are the order statistics of the ’s and is the indicator of non-censoring. The properties of the K-M estimator for dependent variables can be found in Cai (1998, 2001). Then a calculable estimator of is given by

where for

and is the kernel estimator of the marginal density function .

In order to define the -mixing notion, we will use the following notations. Denote by the algebra generated by .

- Definition

-

Let denote a sequence of rv’s. Given a positive integer n, set

The sequence is said to be -mixing (strong mixing) if the mixing coefficient as

Many processes fulfill the strong mixing property. We quote

here, the usual ARMA processes which are geometrically strongly mixing,

i.e., there exist and such that, for any , (see, e.g., Jones (1978).

The threshold models, the EXPAR models (see, Ozaki (1979), the simple ARCH

models (see Engle (1982), their GARCH extension (see Bollerslev (1986) and

the bilinear Markovian models are geometrically strongly mixing under some

general ergodicity conditions.

We suppose that the sequences and

are -mixing with coefficients and , respectively. Cai (2001) Lemma 2

showed that is then strongly mixing, with

coefficient

From now on, we suppose that is strongly mixing with mixing’s coefficient such that for some .

3 Hypotheses and main results

Let be a compact set in . We define the endpoint of by and we assume that and .

All along the paper, we denote by

where is the joint density of . For any generic strictly positive constant , we assume

| (3.1) |

In order to present our result, we have to introduce the following notations and hypotheses.

-

H1.

The bandwidth satisfy

-

H2.

-

H3.

, , such that

-

K1.

The kernel is bounded and

-

K2.

with

-

K3.

and

-

D1.

The function defined in (2.1) is continuously differentiable and for

-

D2.

The function is continuously differentiable and for and .

-

D3.

The joint density of exists and satisfies for

where is a positive constant.

3.1 Some comments on the hypotheses

Hypotheses H1 and H2 are very common in both independent and dependent cases. Furthermore, H3 permits to estimate the covariance term. The hypotheses concerning the kernel K are technicals and it is well-known that it does not improve the quality of the estimation. The D1 intervenes in Lemma 1, however hypotheses D2 and D3 intervene in Lemma 4 to deal with the covariance term.

3.2 Bandwidth selection

Note that: It is well-known that the choice of the kernel does not affect the quality of the estimation. In contrast, the bandwidth parameter has a great influence on the quality of the estimator. A parameter that is too small causes the appearance of artificial details in the graph of the estimator, and for a large enough value of the bandwidth , the majority of the features is on the contrary erased. The choice of the bandwidth is therefore a central question in nonparametric estimation. Recall that in the literature, there are mainly three methods, the ”rule of thumb”, ”plug-in” and ”cross-validation”. Each method has its merits and drawbacks. We point out that the latter is very popular and its main idea is to minimize the following criterion

where is the estimator of obtained by raising the observation in the sense of practical point of view. Even if the latter has the drawbacks that it is very variable and can give an underestimation of , it remains the most common used method. In our entire simulation study, we adopt the cross-validation method (see: Sect. 4). The following theorem establishes the almost sure uniform convergence of towards .

Remark 1

We point out that in our result we highlight the covariance term which give us how the dependency intervenes. This point is rarely given in the dependent case of many papers. In the latter the authors made an additional hypotheses to vanish the covariance term to get an analogous result as in the independent case.

4 Simulation study

The aim of this part is to examine the performance of our estimator by considering some fixed size particular cases. We do it by varying the dependency rate and the censoring percentage (C.P.). We compare the efficiency of the implemented method to the classical regression (CR) estimator defined in Guessoum and Ould Saïd (2010).

In the next paragraph, we recall a result of Port (1994) which permits to calculate the theoretical regression function that will be used throughout this section (see formula (4.1) below).

Proposition 1

Let and be two random variables with means: and and variances: and respectively, and covariance . Let be an i.i.d. sequence of r.v. and defined by

and then the second order approximation of is

- Step 1 :

-

We consider the strong mixing two-dimensional process generated by

- Step 2 :

-

Given , we have . Using Port property (see proposition 1) the theoretical function becomes

(4.1) - Step 3 :

-

Determine and which gives the observed sample .

- Step 4 :

-

The K-M estimator of is calculated from (2.2).

- Step 5 :

-

The Gaussian kernel is used as kernel function for the estimator and we choose the optimal bandwidth by the cross validation method (see Subsection 3.2) from by step of and satisfying H3.

Output: Calculate the RER estimator given by (2) for and .

4.1 Linear case

In this subsection, we observe the finite sample performance of our estimator (RER) for weak and strong dependency when the theoretical function is of linear form.

4.1.1 Weak dependency

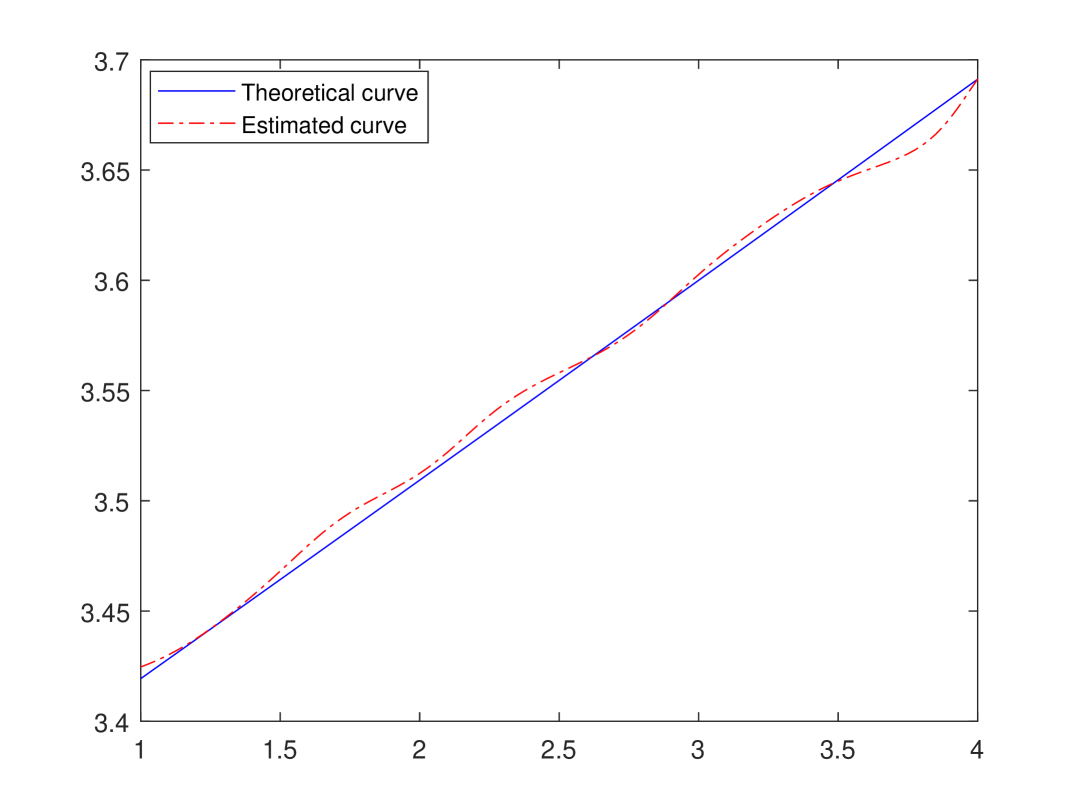

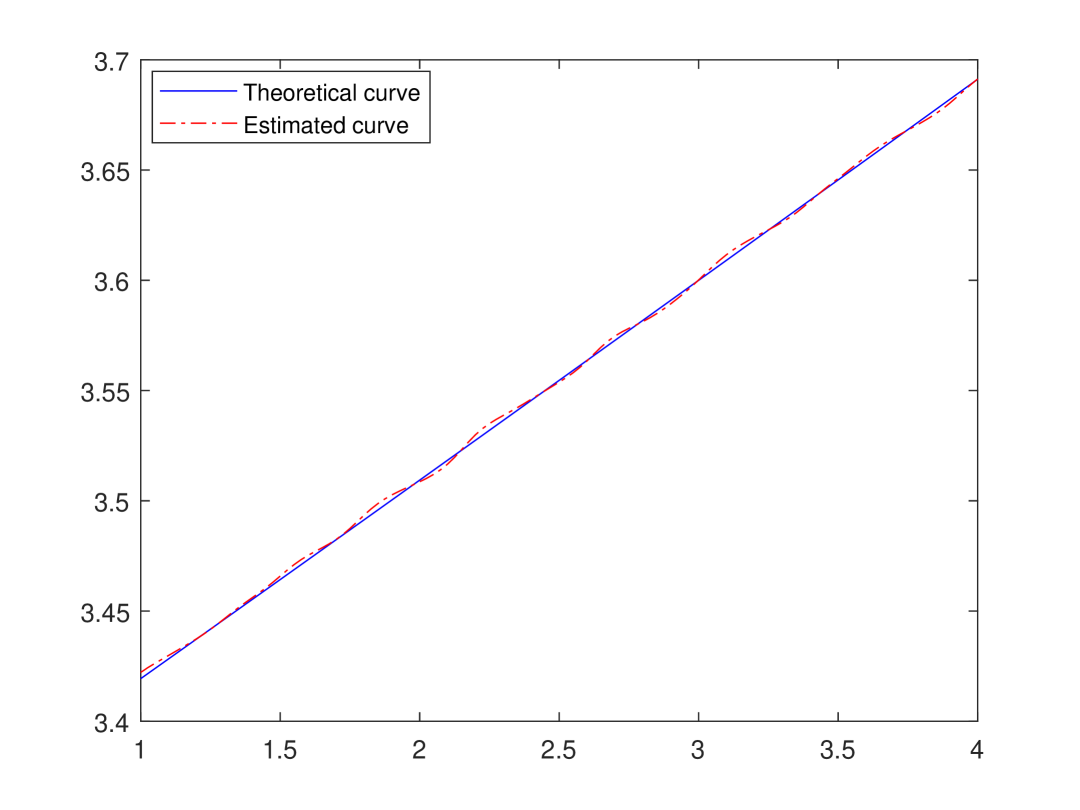

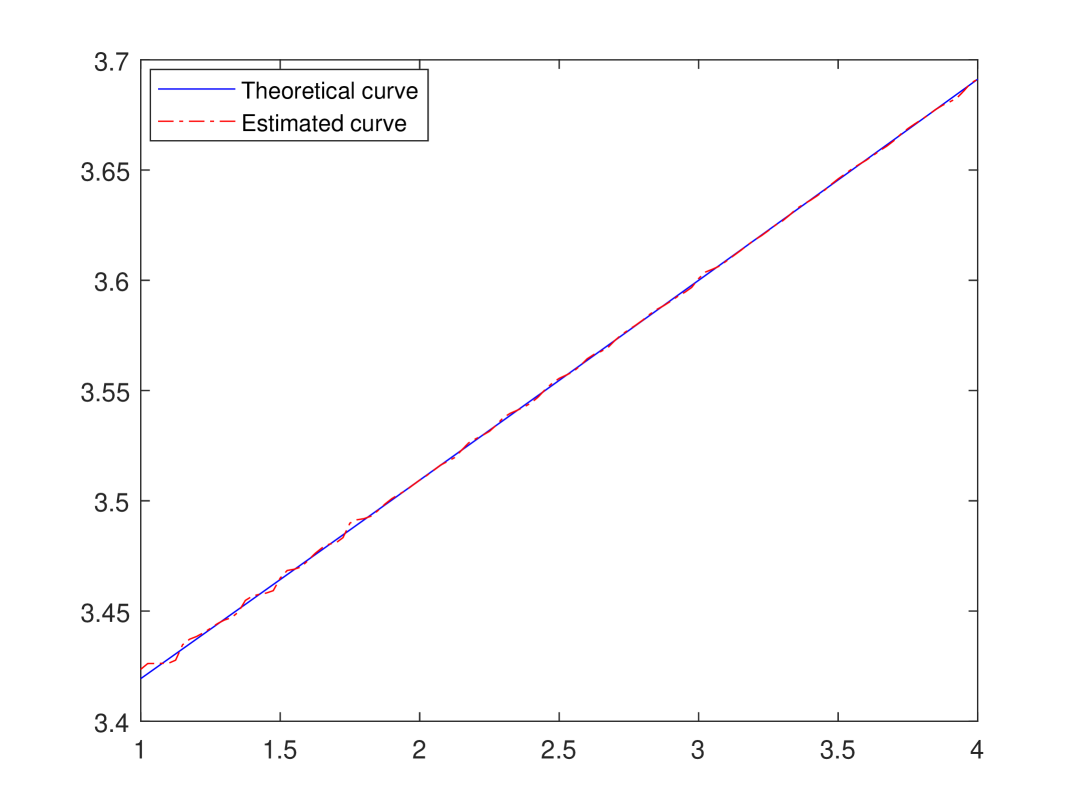

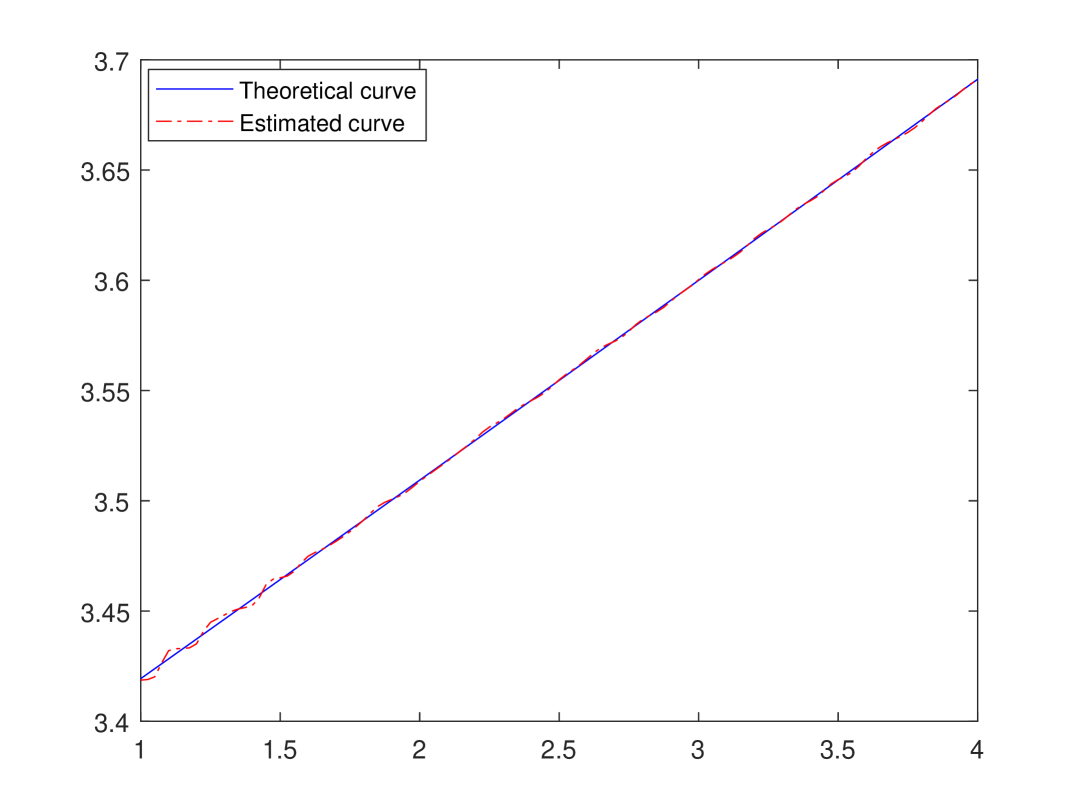

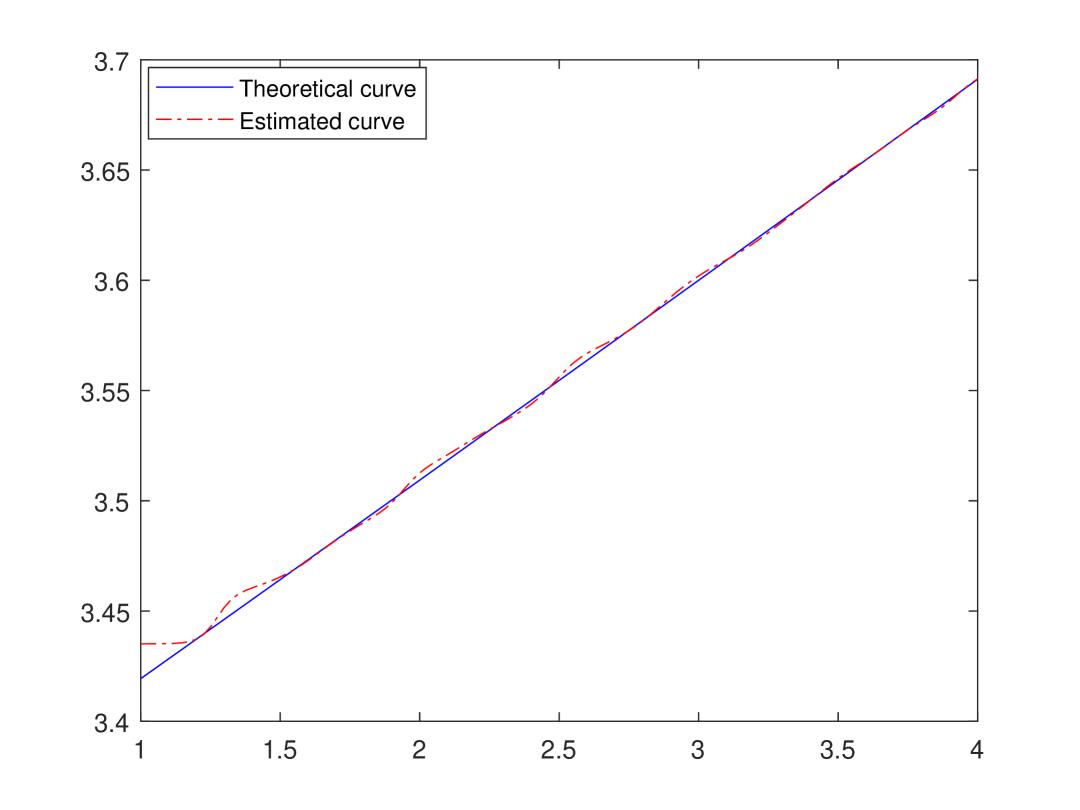

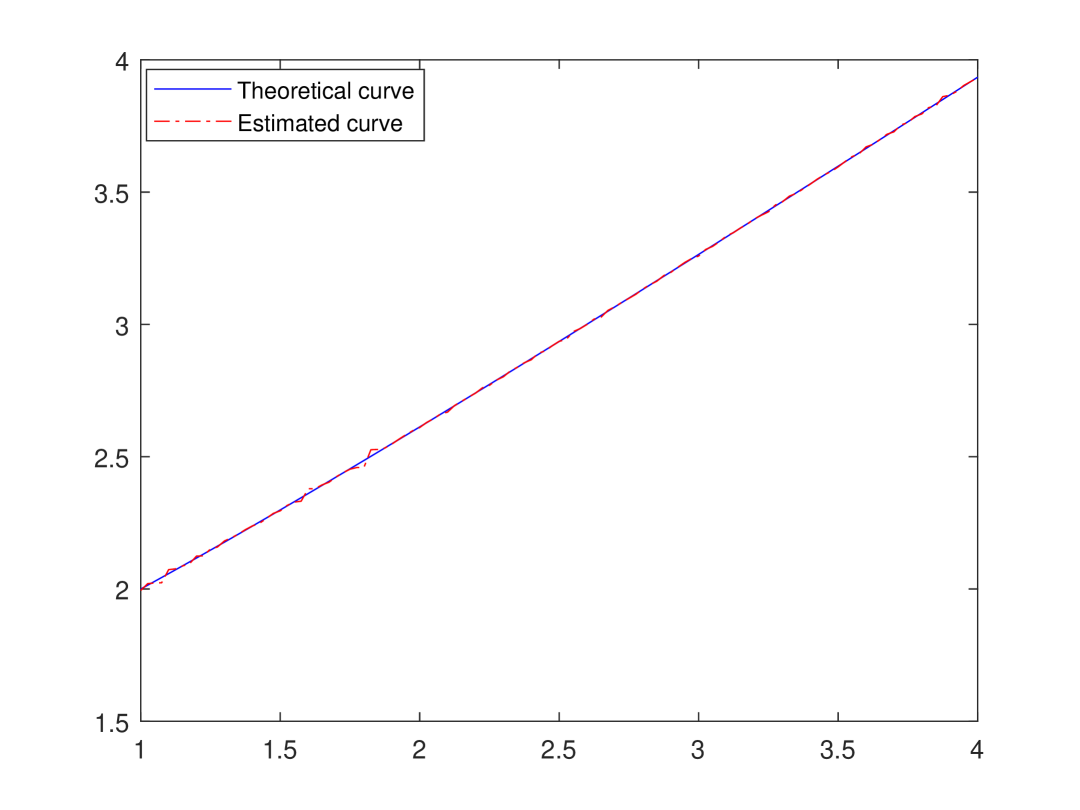

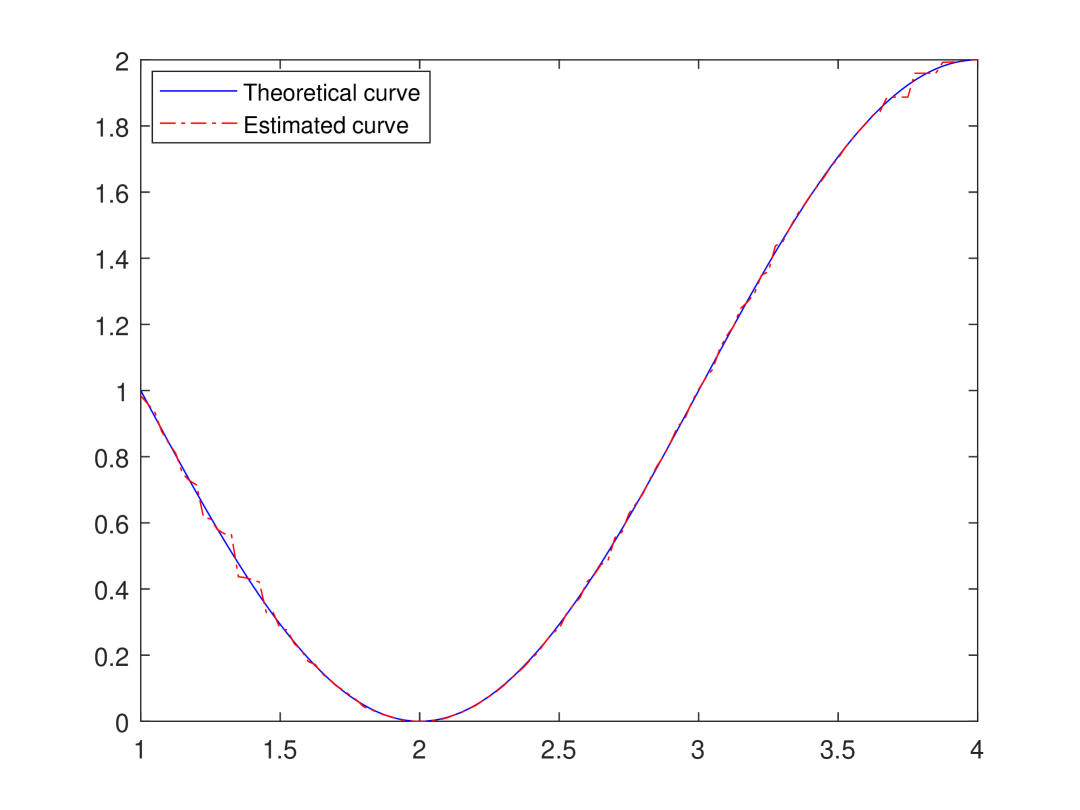

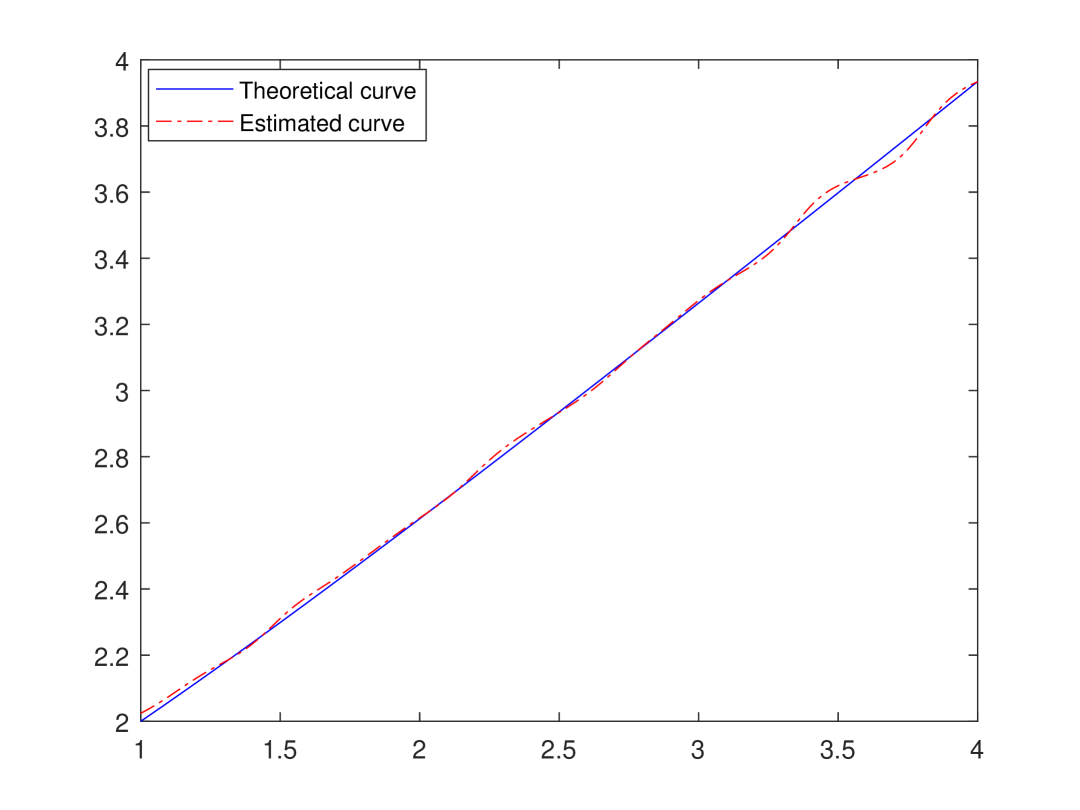

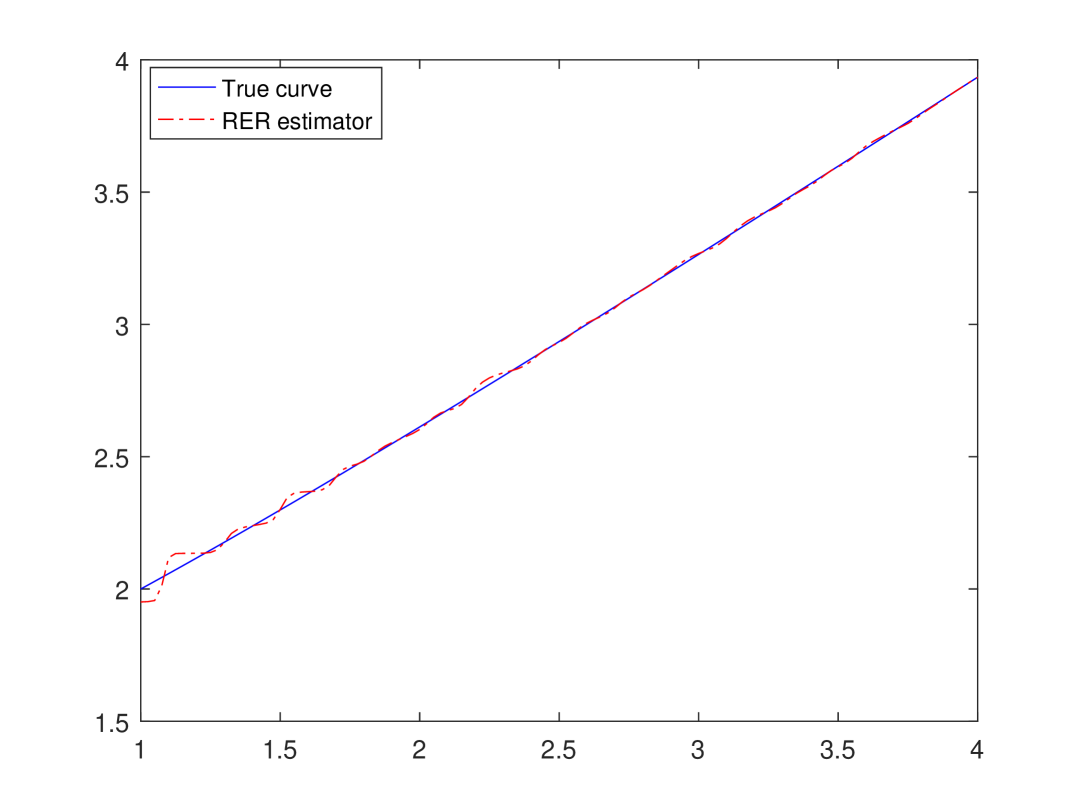

Effect of sample size:

It is easy to see from Figure 1 that the quality of fit is better when increases for a fixed C.P. and .

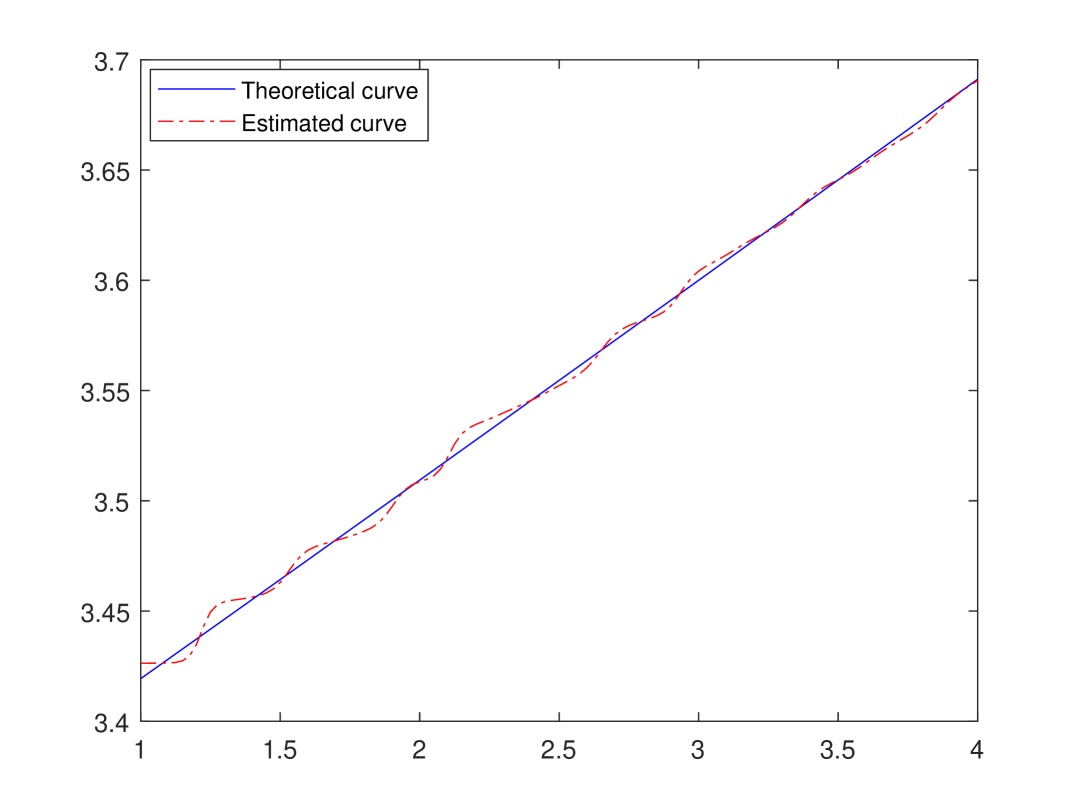

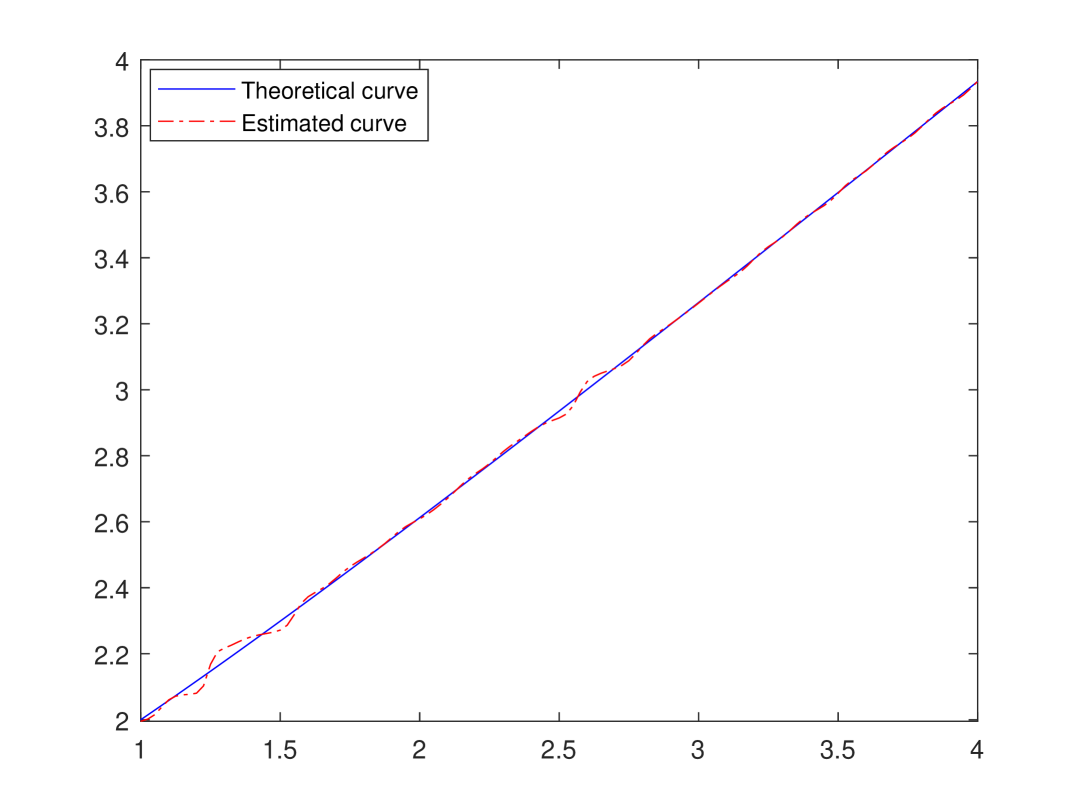

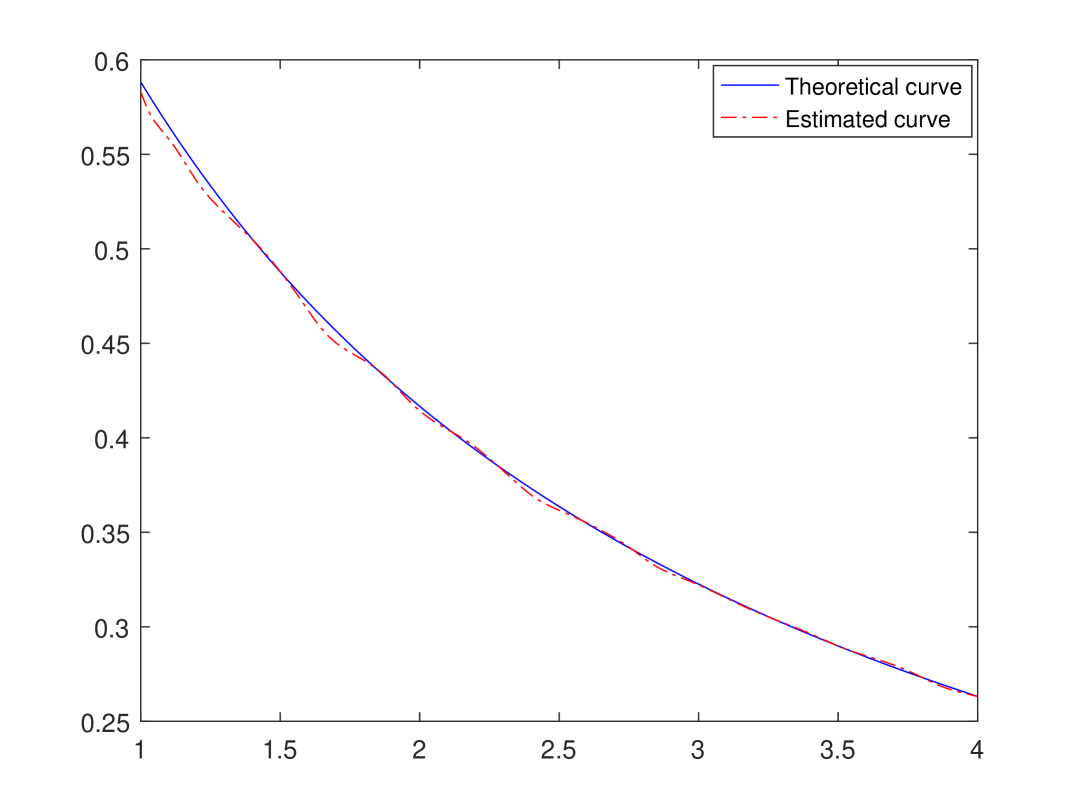

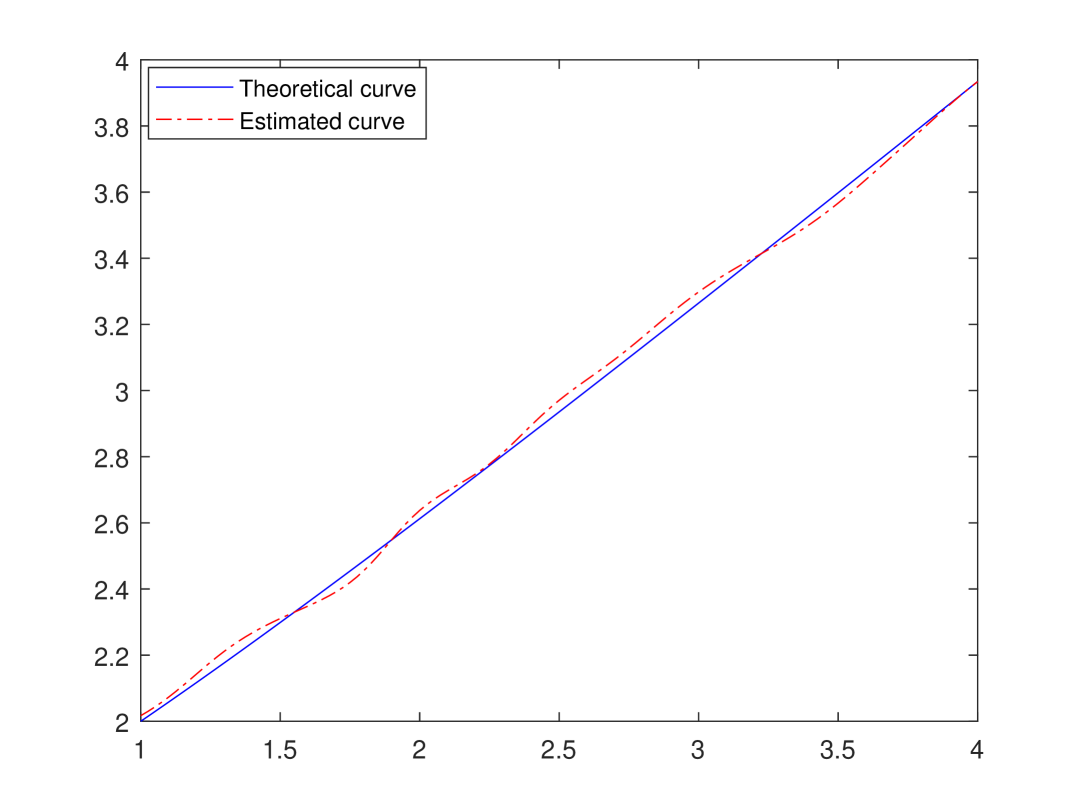

Effect of C.P.:

To visualize the global performance of the RER estimator under censorship, we set and vary the C.P. In this case, there is more variation in the resulting estimator, but generally remains close to the theoretical curve even for a high C.P. (Figure 2 displays the results). In conclusion, our estimator is still resistant to the effect of censorship when dependency is weak.

4.1.2 Strong dependency

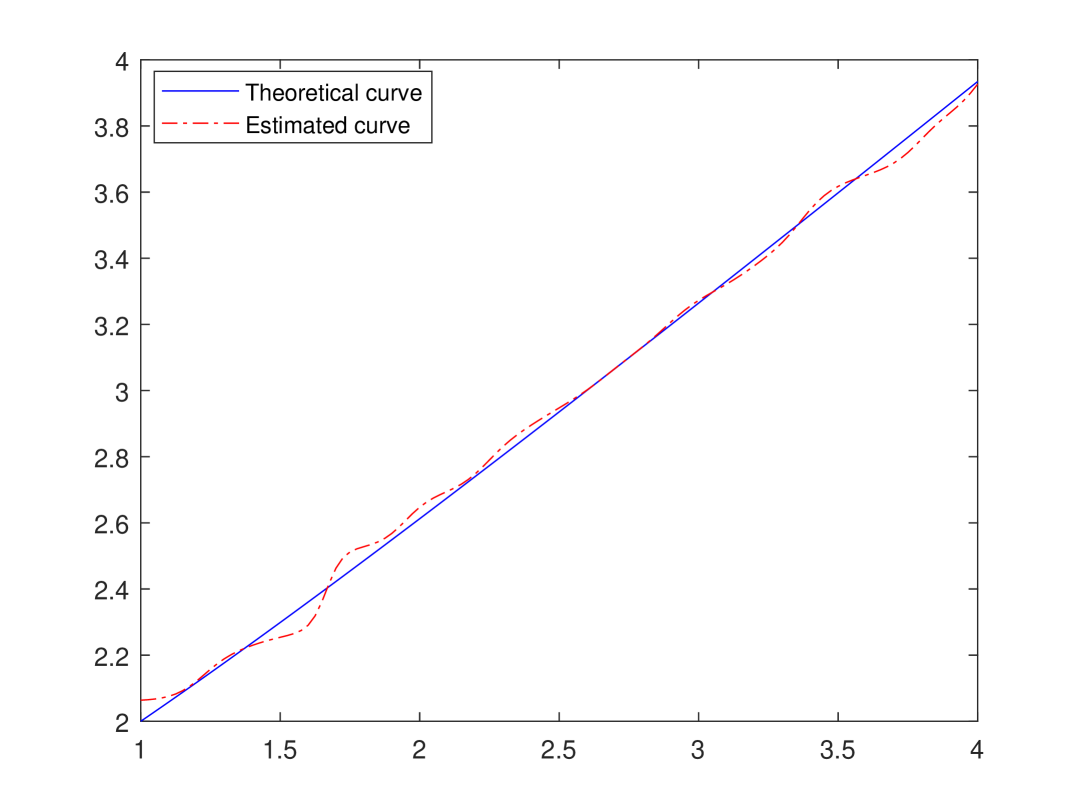

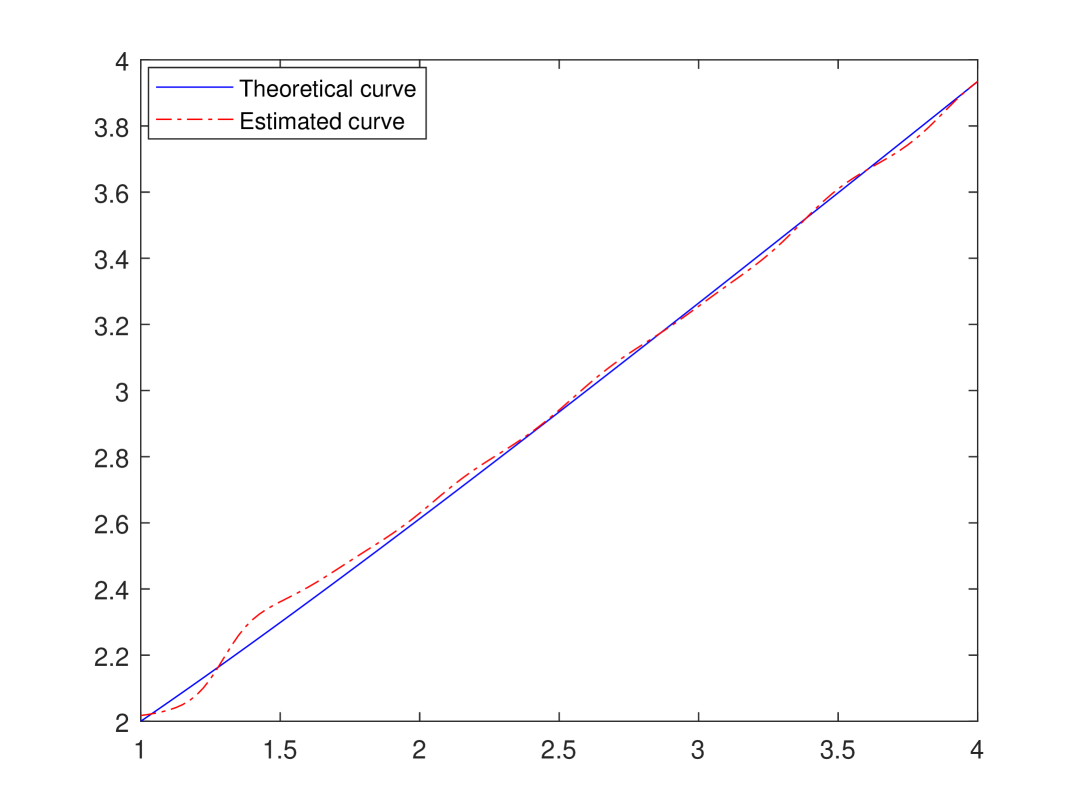

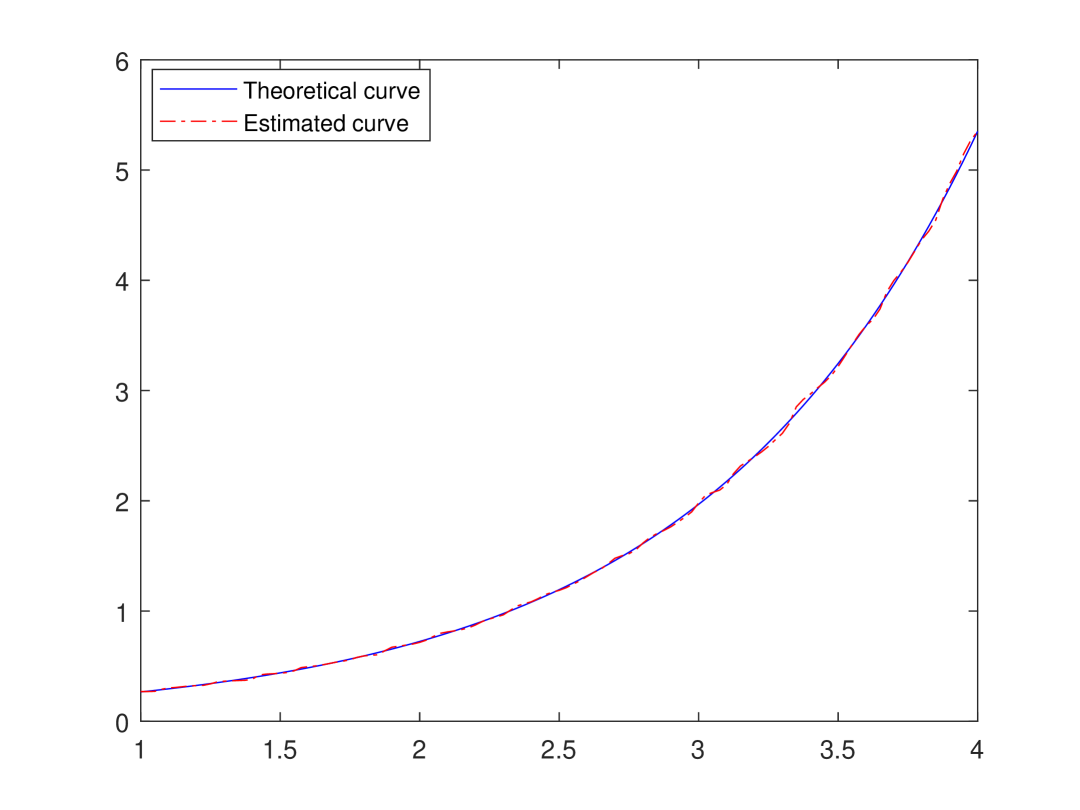

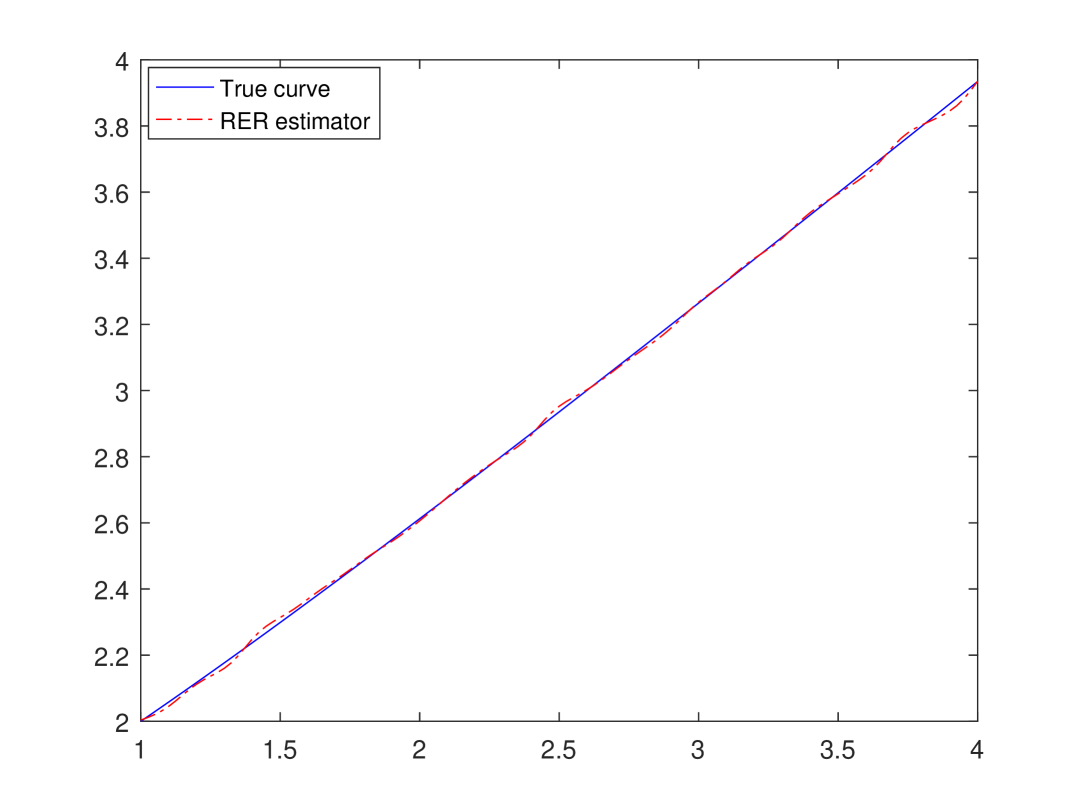

Effect of sample size:

For the case of highly dependent data and for a fixed C.P., we can observe from Figure 3 that the RER estimator is adjusted to the theoretical curve when rises.

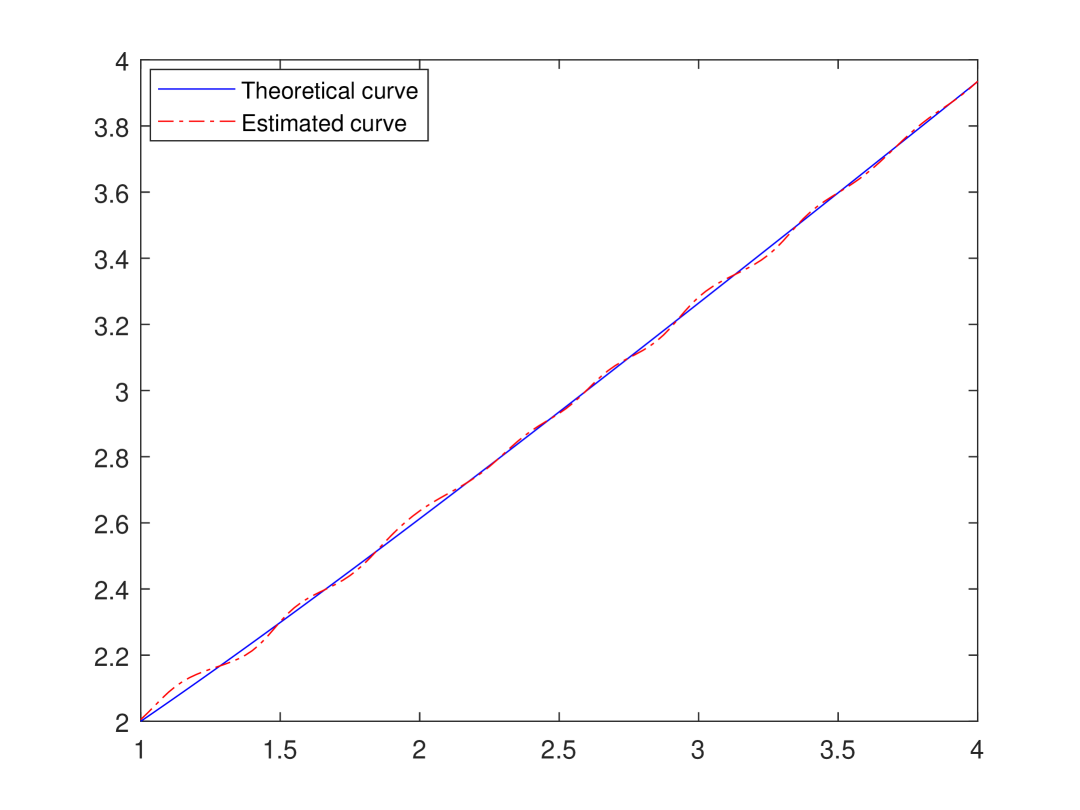

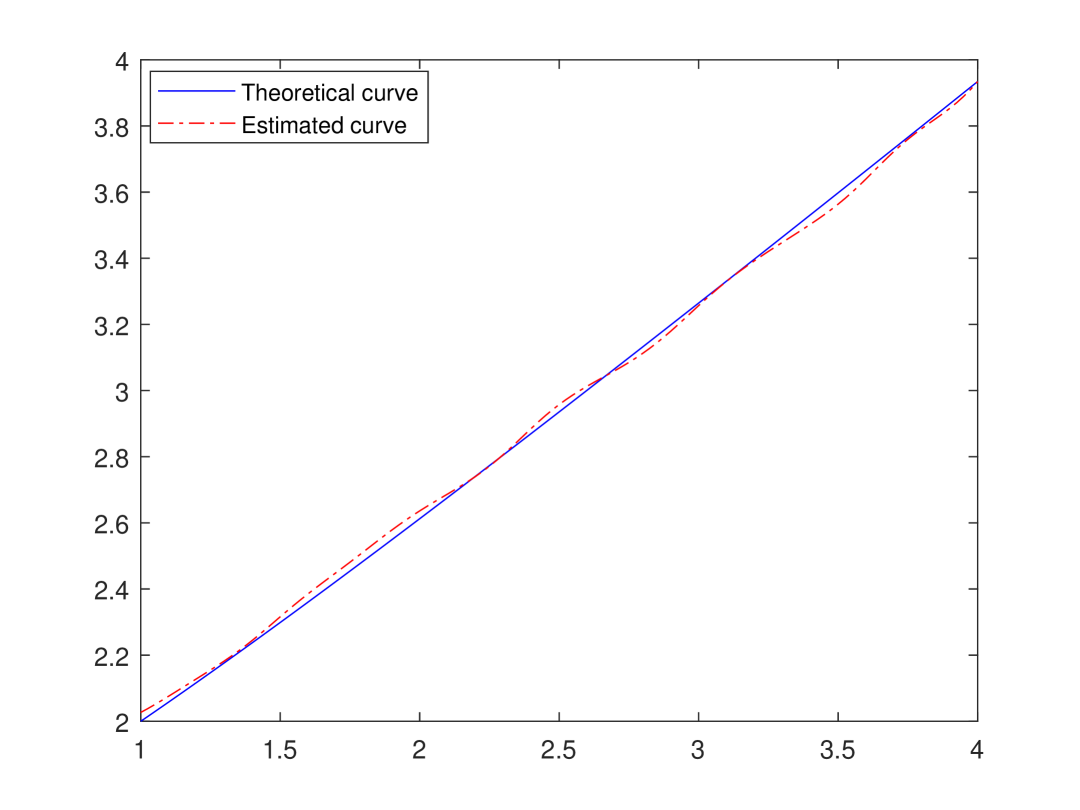

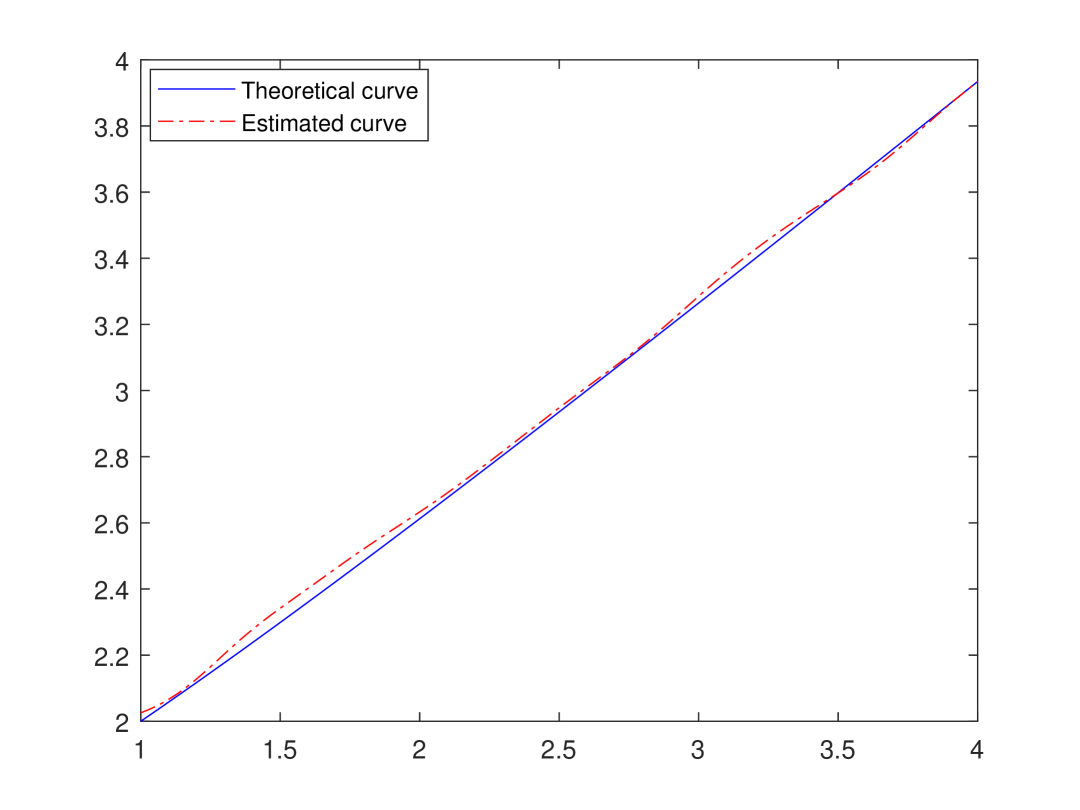

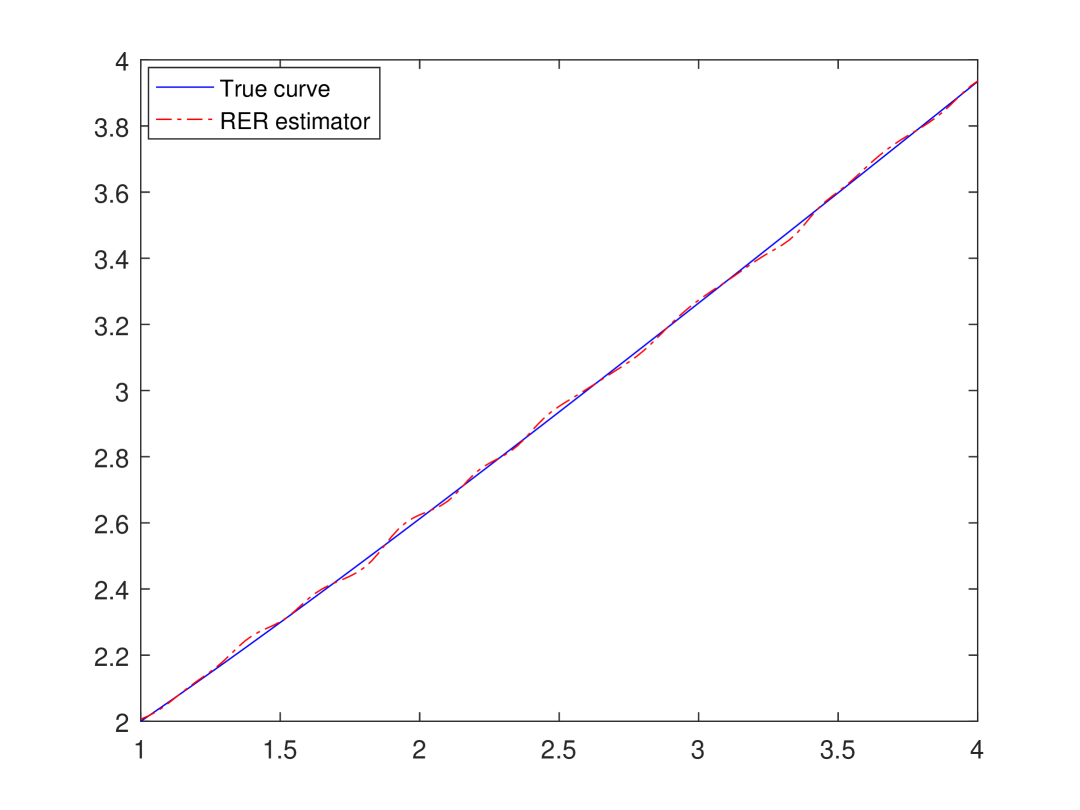

Effect of C.P.:

We see clearly that the quality of fit is better for large sample size and low percentage of censoring (see Figure 4).

4.2 Nonlinear case

We consider now, three nonlinear functions:

Figure 5 shows that the quality of the fit is good as in linear model. Clearly, we see that the adjustment improves when increases.

4.3 Effect of outliers

To show the robustness of our approach, we generate the case where the data contains outliers. To create this outlier effect, values of this sample are multiplied by a factor called M.F.. From Figure 6, we can see that our estimator is close to the theoretical curve knowing that we observe only of the trues values. Then, it is absolutely clear that our estimator is resistant in the presence of outliers.

4.4 Effect of contamination of the random error :

We take the same algorithm as before by changing step 1 which becomes :

-

Step 1’. where and . We choose the level of contamination and the magnitude of contamination generally.

We observe from (Figure 7) that the quality of the adjustment to the theoretical function deteriorates when the level of contamination becomes higher.

4.5 Comparaison study

To show the efficiency of the RER estimator, we carry out a comparative study in which we consider the classical regression (CR) estimator defined in Guessoum and Ould Saïd (2010) by

| (4.2) |

for weak and strong dependency.

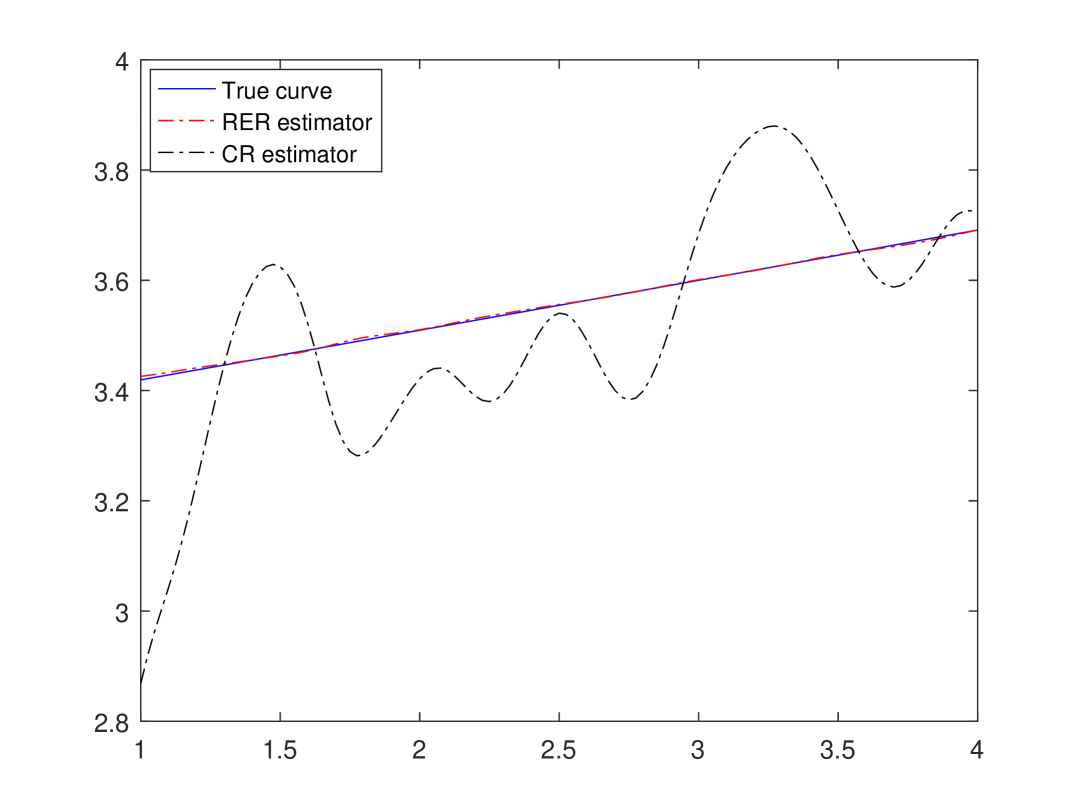

4.5.1 Weak dependency

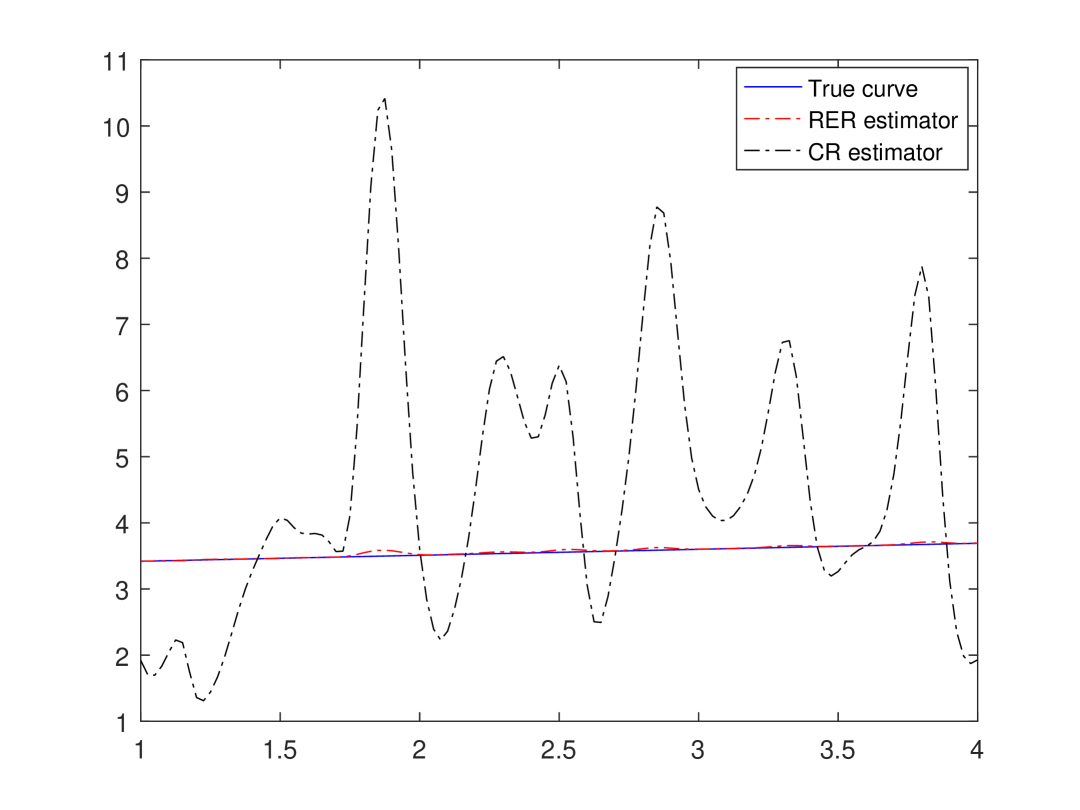

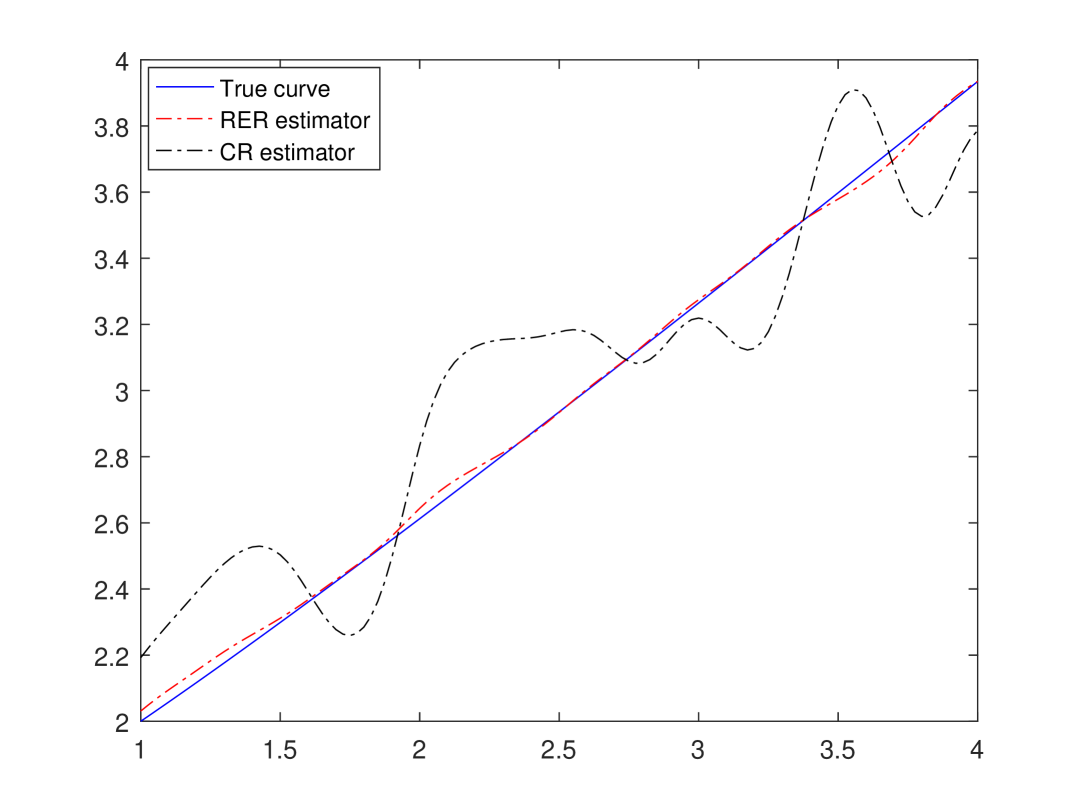

Effect of C.P.:

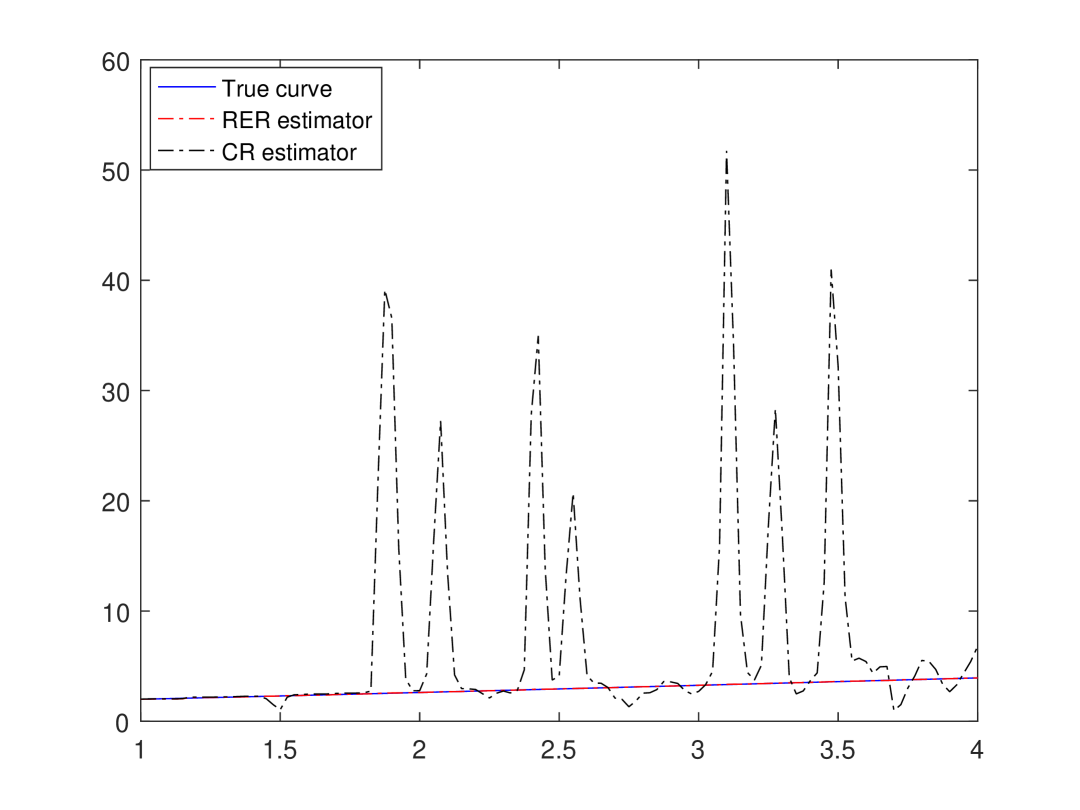

We fix and we vary the censoring rate. We can notice clearly (from Figure 8) that the RER estimator is near to the theoretical curve whereas the CR curve is distant from the true curve when C.P. increases.

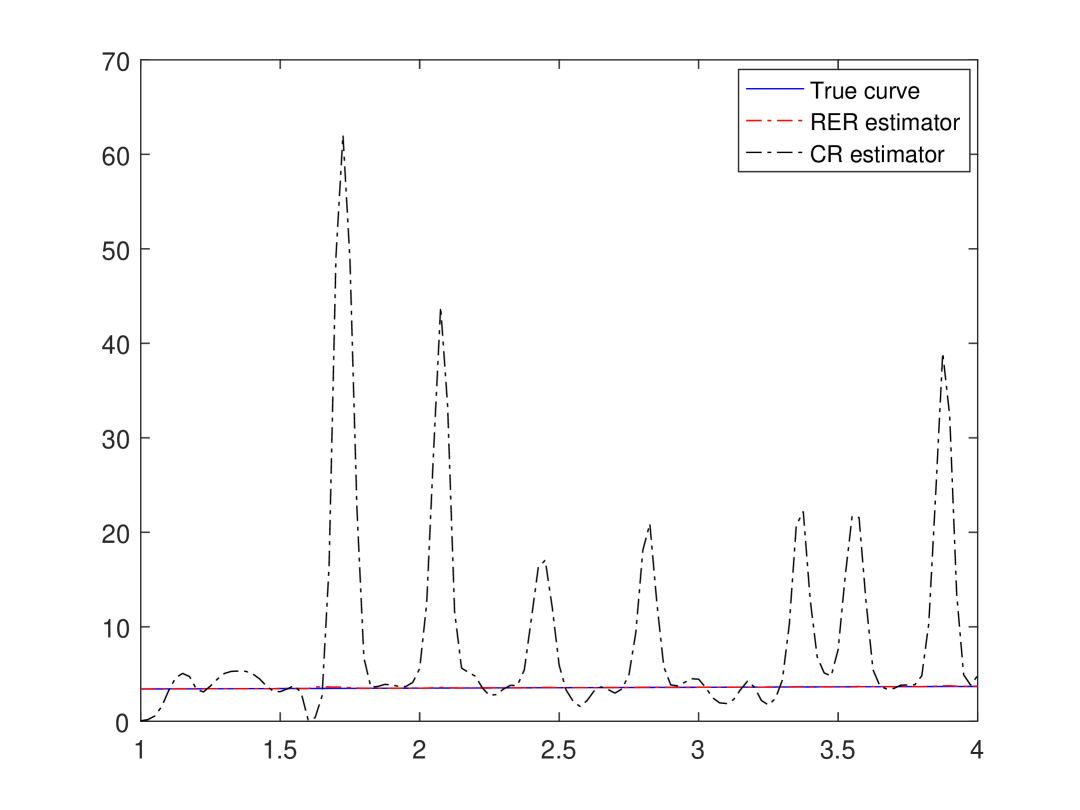

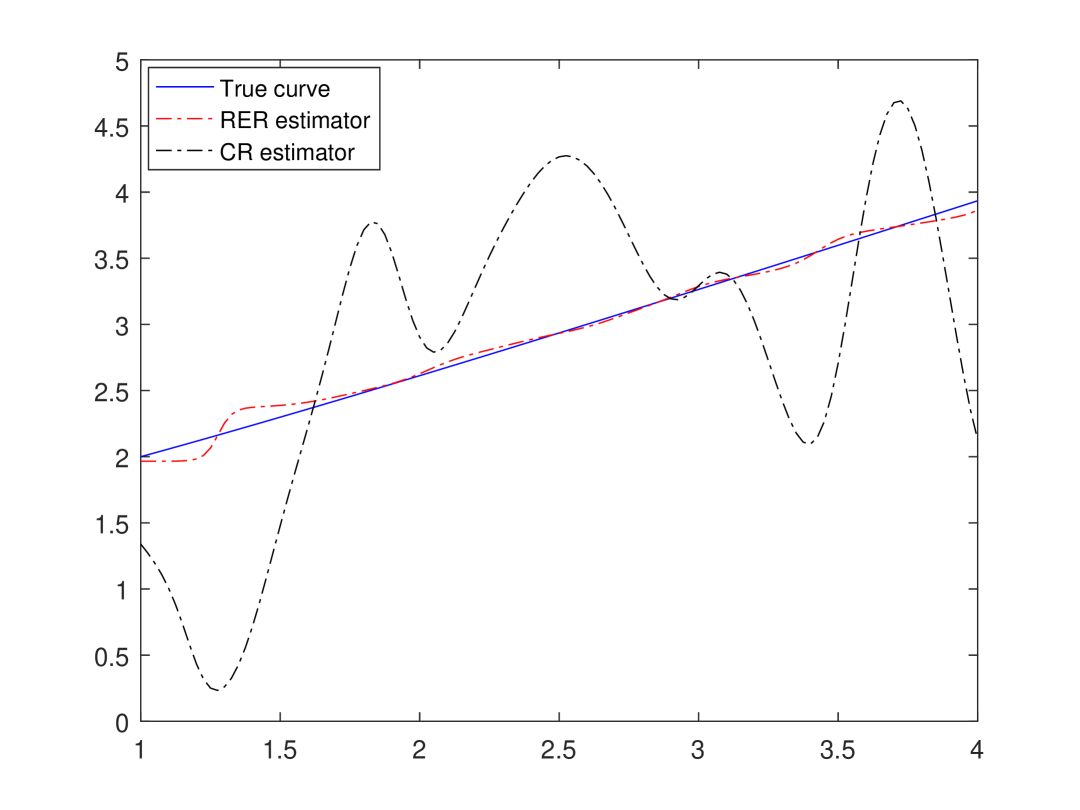

Effect of outliers:

We fix , C.P. and we vary the M.F. It can be reported from Figure 9 that the RER estimator is overlapped on the true curve in contrast with the CR estimator which is significantly affected by the M.F. when the dependency is weak.

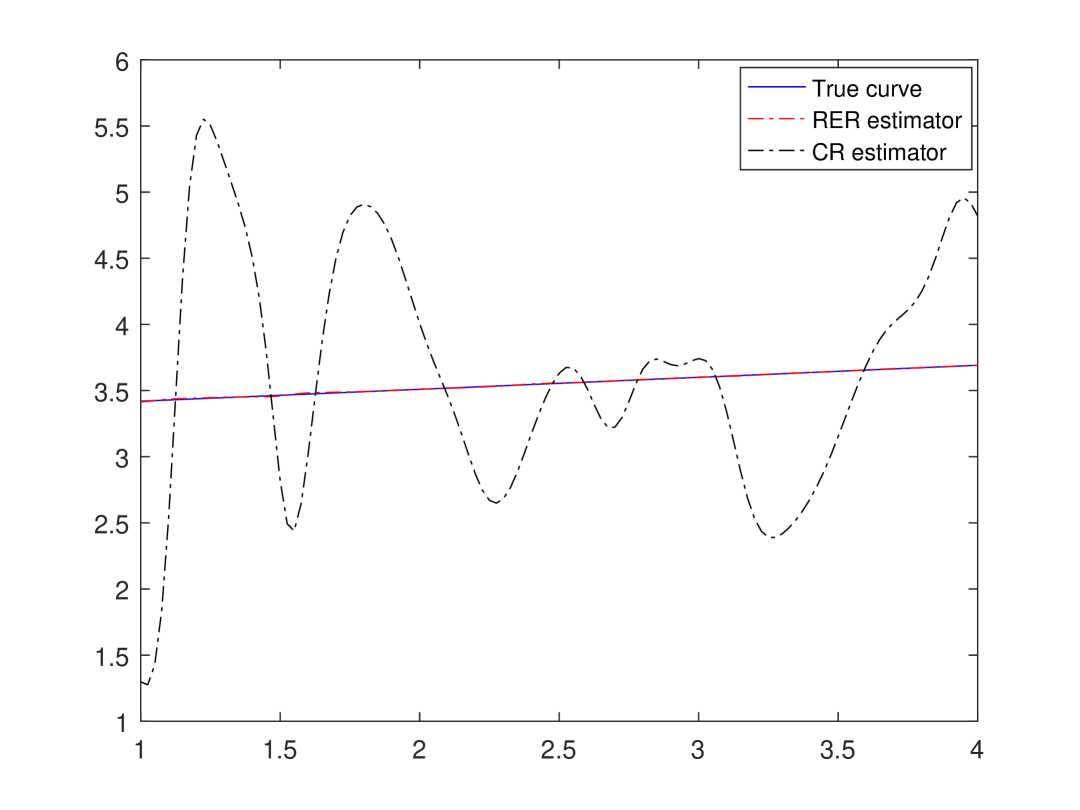

4.5.2 Strong dependency

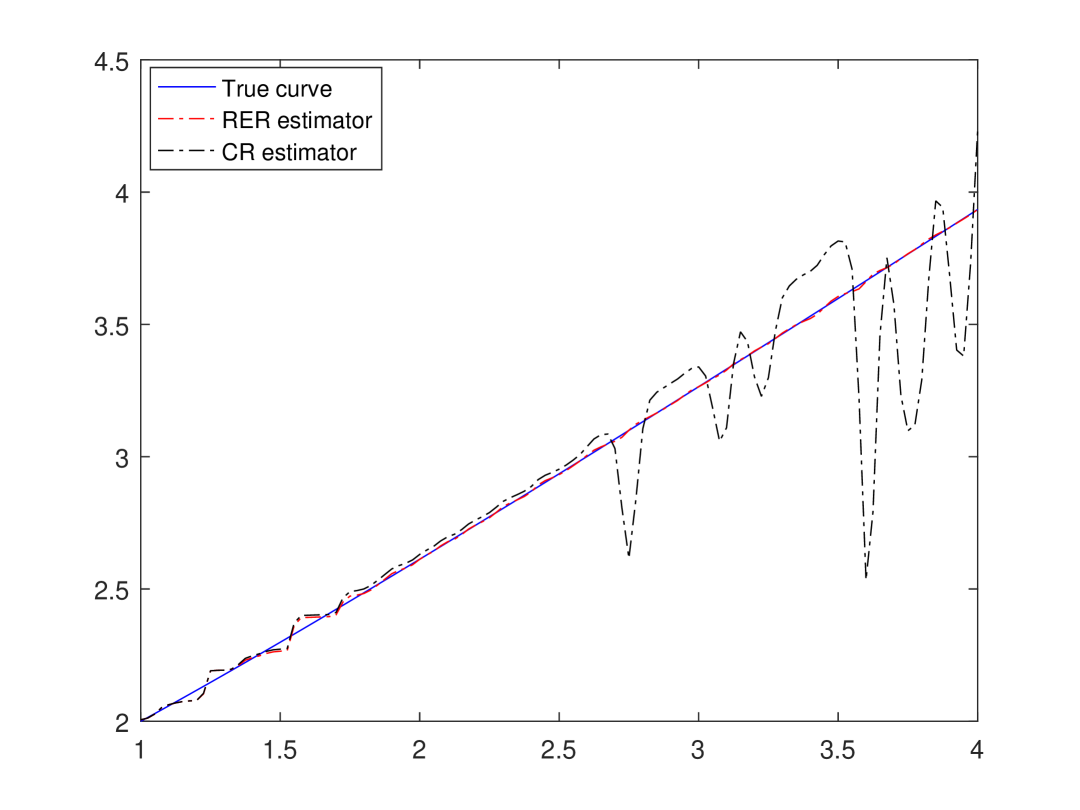

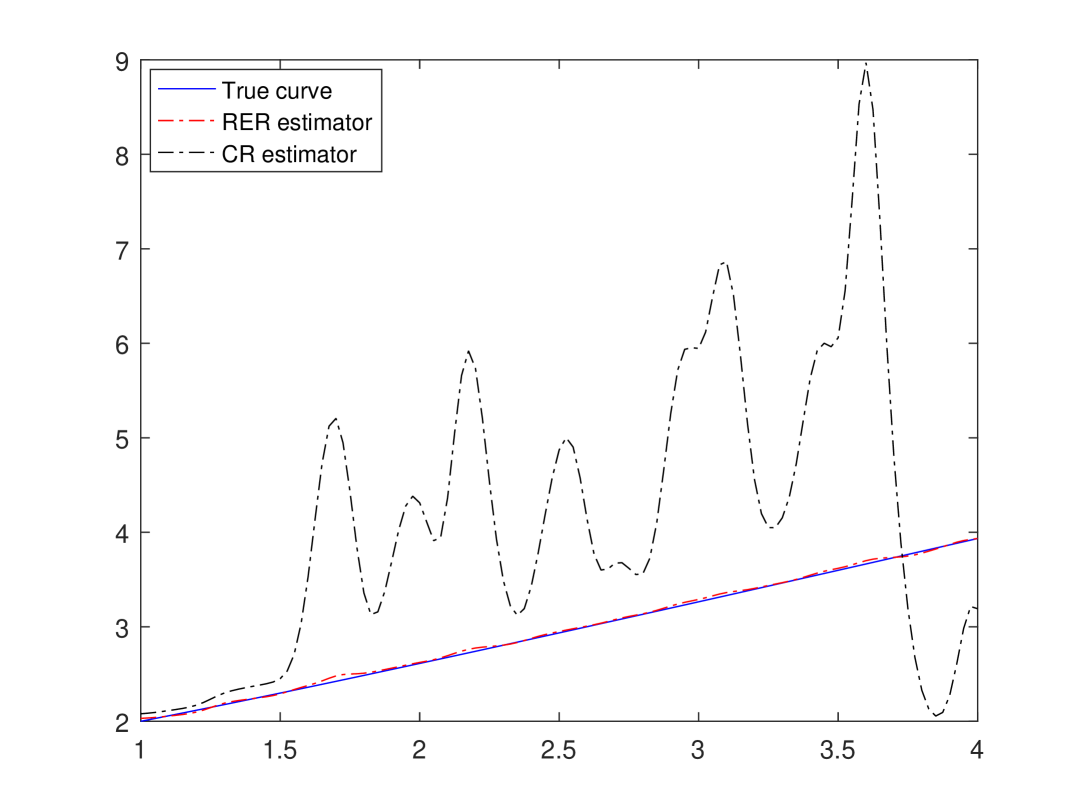

Effect of C.P.:

We fix , and we vary the C.P. to examine the effect of censorship on both RER and CR estimators when the dependency is strong. We can observe from Figure 10 that the RER estimator

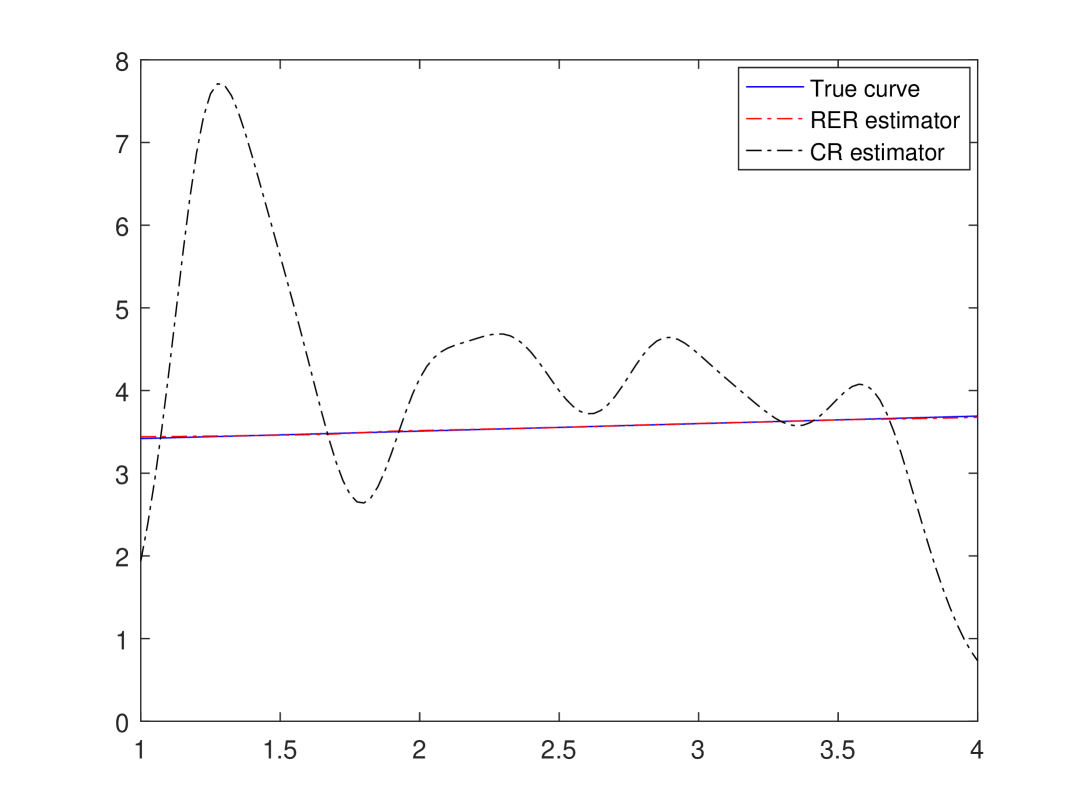

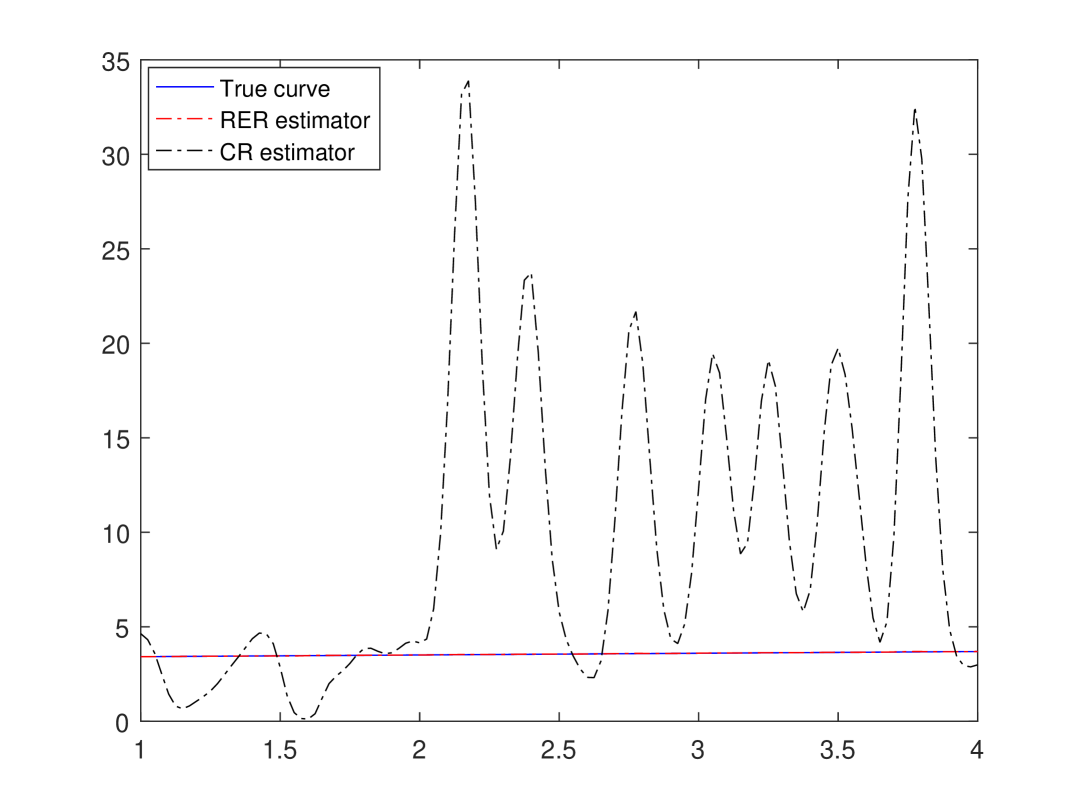

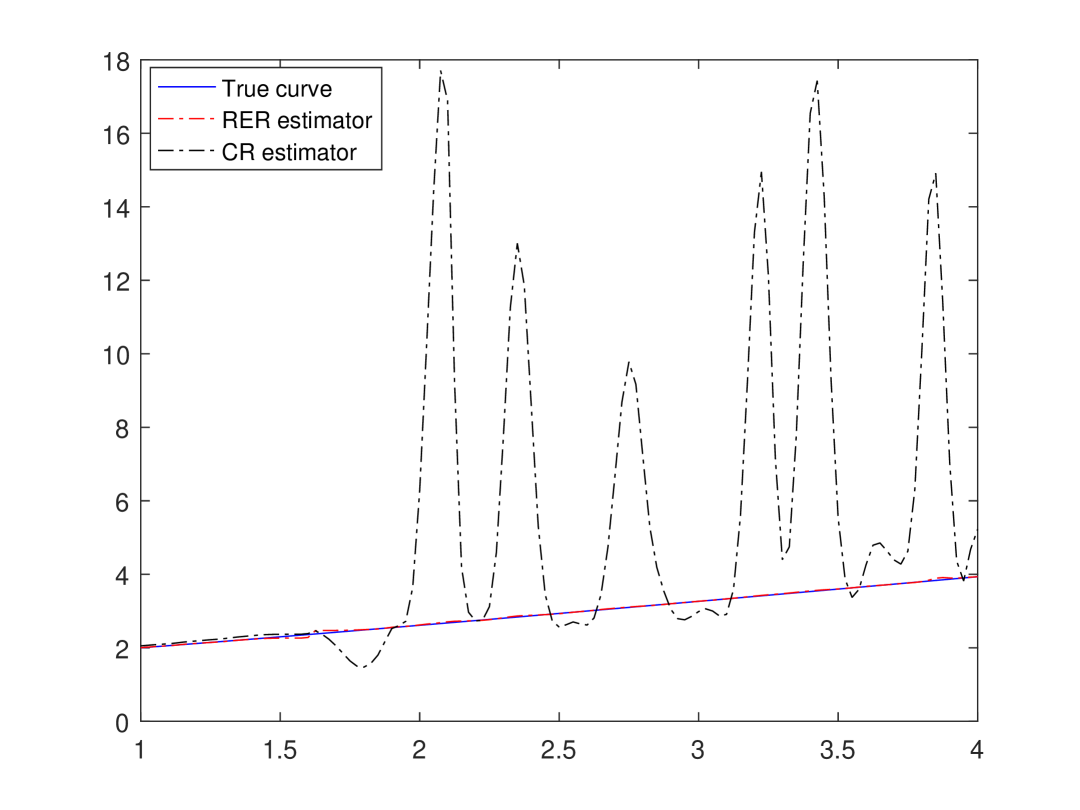

Effect of outliers:

We fix , , C.P. and we vary the M.F. to evaluate the effect of outliers on both estimators when the dependency is high. As expected, our estimator remains resistant to outliers under a high dependency unlike that of classical regression which is more distant when the M.F. becomes large se Figure 11.

4.6 Discussion

In this paper, an estimator for the relative error regression function on the multivariate case has been proposed, when the data are dependent and are subject to censoring.

After analyzing and comparing with the CR estimator, we have the following remarks. As expected, the asymptotic behavior of the RER estimator is better for a weak dependency (a small value of ) and a low censorship rate which is conforted by the numerical study in Sect. 4, where we show how the quality of the estimation is influenced by several parameters (C.P., , M.F., ).

Now, concerning the behavior of the RER estimator compared to the CR estimator, we can remark that the comportement of the RER remained almost unchanged in all our results in comparison with the CR estimator, which is significantly affected by the presence of outliers and censorship in the sample. Another interesting remark related to dependency is the fact that with small the estimator remains resistant.

5 Technical lemmas and proofs

We split the proof of Theorem 1 into following Lemmatas 1-4.

Proof

Lemma 2

Under hypotheses H1 and K1-K3, for , we have

Proof

To this step, we introduce the following lemma (Ferraty and Vieu (2006) Proposition A.11 ii), p.237).

Lemma 3 (Fuk-Nagaev)

Let be a sequence of real rv’s, with strong mixing coefficient , such that , , . Then for each and for each

where .

In the following lemma we establish the asymptotic expression for the variance and covariance of the estimator .

Proof

Recall that is a compact set, then it admits a covering by a finite number of balls centred at . Then for all there exists such that where verifies with is the Lipshitz condition in hypothesis K1. Since is bounded then there exist a constant such that .

Let for and the given set

then

that we decompose as follows

from where

We start by treating the first term

with

In the same manner, we have,

then

which allows to

| (5.1) |

To proceed to the determination of the second term , we will use Lemma 3. Let

To apply Lemme 4, we have to calculate first

| (5.2) | ||||

On the one hand, we have to start by considering

For , using the conditional expectation propreties and a change of variables, we get

by a Taylor expansion and from Hypotheses D2 and K3, we obtain

| (5.3) |

For , under hypothesis D1, we have

using again a change of variable and a Taylor expansion around , we have

| (5.4) |

Then from (5.3) and (5.4), we get

| (5.5) |

On the other hand,

which yeilds, under Hypothesis D3

| (5.6) |

uniformly on and .

Now to evaluate the asymptotic behaviour of following the decomposition of Marsy (1986), we define the sets :

where as at a slow rate, that is . Let and be the sums of covariances over and , respectively.

We then get, from (5.6)

For , we use the modified Davydov inequality for mixing processes (see Rio (2000)). This leads, for all , to

we then get,

Choosing permits to get,

| (5.7) |

Finally, from (5.2),(5.7) and (5.5) we obtain

Now, that all the calculus are done. It is convenient to apply the inequality in Lemma 4 with

Taking with , we get for the first part

| (5.8) |

By choosing with , (5.8) becomes

by taking logarithm and using a Taylor expansion of we get

which gives

| (5.9) |

For the same choice of and , we have

| (5.10) |

By taking again the inequality of Fuk-Nagaev and using , we can write

| (5.11) |

We have from hypothesis H3

Then, for an appropriate choice of , is the general term of a convergent series. In the same way, we can choose such that is the general term of convergent series. Finally, applying Borel-Cantelli’s lemma to (5) gives the result.

Remark 2

The parameter of the hypothesis H3 can be chosen such as :

| (5.13) |

This condition ensures the convergence of the series of Lemma 4.

Proof

of Theorem 1. For , we consider the following decomposition :

which by triangle inequality, we have

| (5.14) |

Then from the Lemmas 1-4 in conjunction with the inequality (5.14) conclude the proof.

References

- (1) Attouch M, Laksaci A, Messabihi N (2015), Nonparametric relative error regression for spacial random variables, Stat Papers, 58:987-1008

- (2) Bollerslev T (1986), General autoregressive conditional heteroscedasticity, J Econom , 31:307-327

- (3) Bosq, D (1998), Nonparametric statistics for stochastics processes Estimation and Prediction, Lecture Notes in Statistics, 110 Springer-Verlag New-York

- (4) Bradley RD (2007), Introduction to strong mixing conditions, Vol I-III Kendrick Pres Utah

- (5) Cai Z (1998), Asymptotic propreties of Kaplan-Meier estimator for censored dependent data, Stat Probab Lett, 37: 381-389

- (6) Cai Z (2001), Estimating a distribution function for censored time series data, J. Multiv. Analysis, 78: 299-318

- (7) Dabrowska M D (1987), Nonparametric regression with censored survival time data, Scand. J. Statist, 14: 181-197

- (8) Demongeot J, Hamie A, Laksaci A, Rachdi M (2016), Relative error prediction in nonparametric functional statistics: Theory and Practice, J. Multivariate Anal., 146: 261-268

- (9) El Ghouch A, Van Keilegom I, (2008), Nonparametric regression with dependent censored data, Scand. J. Statist., 35: 228-247

- (10) Engle, R F, (1982), Autoregressive conditional heteroskedasticity with estimates of the variance of U.K. inflation, Econometrica, 50:987-1007

- (11) Ferraty F, Vieu P, (2006), Non parametric functionnal data analysis, Theory and Practice, Springer-Verlag, New-York

- (12) Guessoum Z, Ould Said E, (2008), On the nonparametric estimation of the regression function under censorship model, Statist. and Decisions, 26: 159-177

- (13) Guessoum Z, Ould Said E, (2010), Kernel regression uniform rate estimation for censored data under -mixing condition. Elect. J. of statist., 4: 117-132.

- (14) Jones D A, (1978), Nonlinear autoregressive processes, Proc. Roy. Soc. London A, 360, 71-95

- (15) Kaplan E L, Meier P, (1958), Nonparametric estimation for incomplete observations, J. Amer. Statist. Assoc., 53: 457-481

- (16) Li X, Yang W, Hu S, (2016), Uniform convergence of estimator for nonparametric regression with dependent data, J. of inequal. and Appli. 142

- (17) Lipsitz S R, Ibrahim J G, (2000). Estimation with correlated censored survival data with missing covariates, Biostatistics, 19: 315-327

- (18) Makridakis S, (1984), The forecasting Accuracy of Major Time Series Methods, Wiley, New York, 1984

- (19) Masry E, (1986), Recursive probability density estimation for weakly dependent stationary processes, IEEE Trans. Inform. theory, 32: 254–267

- (20) Narula S C, Wellington, J F (1977), Prediction, linear regression and the minimum sum of relative errors, Technometrics, 19: 185-190

- (21) Ozaki, T (1979), Nonlinear time series models for nonlinear random vibrations, Technical report. Univ. of Manchester

- (22) Park H, Stefanski L A, (1998), Relative error prediction, Statistics and Probability Letters, 40: 227-236

- (23) Park H, Shin K I, Jones M C, Vines S K (2008), Relative error prediction via kernel regression smoothers, Journal of Stat. Plann. and Infer., 138, 2887-2898

- (24) Rio E, (2000) Theorie asymptotique des processus aléatoires faiblement dépendants, Math., 42: 43–47

- (25) Rosenblatt M, (1956), A central limit theorem and a strong mixing condition, Proc. Nat. Acad. Sci. USA, 42: 43–47

- (26) Shen J, Xie Y,(2013), Strong consistency of the internal estimator of the nonparametric regression with dependent data, Statistics and Probability Letters, 83, 1915-1925