A varying terminal time mean-variance model 111 Keywords: finance; mean-variance; varying terminal time; stochastic control. MSC2010 subject classification: 91B28; 93E20; 49N10. OR/MS subject classification: Finance/portfolio; dynamic programming/optimal control.

Abstract: To improve the efficient frontier of the classical mean-variance model in continuous time, we propose a varying terminal time mean-variance model with a constraint on the mean value of the portfolio asset, which moves with the varying terminal time. Using the embedding technique from stochastic optimal control in continuous time and by varying the terminal time, we determine an optimal strategy and related deterministic terminal time for the model. Our results suggest that doing so for an investment plan requires minimizing the variance with a varying terminal time.

1 Introduction

Since the seminal works of Markowitz (1952, 1959), the mean-variance model has been used to balance the return (mean value) and risk (variance) in a single-period portfolio selection model, (refer to Markowitz (2014)). Based on mild assumptions, Merton (1972) solved this single-period problem analytically. More recently, multi-period and continuous time mean-variance portfolio selection models have been proposed. For example, Richardson (1989) studied a mean-variance model in a continuous-time setting for a single stock with a constant risk-free rate. Bajeux-Besnainou and Portait (1998) considered dynamic asset allocation in a mean-variance framework. For the multi-period case, Li and Ng (2000) embedded the discrete-time multi-period mean-variance problem within a multi-objective optimization framework. In the continuous time case, Zhou and Li (2000) formulated the continuous-time mean-variance problem as a stochastic linear-quadratic (LQ) optimal control problem. The solution to this problem is obtained by extending the embedding technique introduced in Li and Ng (2000) and using the results from the stochastic LQ control. Further extensions to the mean-variance problem include those with bankruptcy prohibition, transaction costs, and random parameters in complete and incomplete markets (Bielecki, Jin, Pliska and Zhou (2005); Dai, Xu and Zhou (2010); Lim (2004); Lim and Zhou (2002); Xia (2005)).

For the aforementioned multi-period and continuous time cases, we derive the pre-committed strategies that differ from that of the single-period case; for further details, see Kydland and Prescott (1997). Basak and Chabakauri (2010) adopted a dynamic method to study the mean-variance model and Björk, Murgoci and Zhou (2014) studied the mean-variance problem with state dependent risk aversion.

In the classical mean-variance model, for a given deterministic terminal time , we denote as the terminal value of a portfolio asset with strategy , and as the mean and variance, respectively. Note that we always want to minimize the variance for a given mean level in the single-period, multi-period, and continuous time cases, where is a constant. In the single-period case, can be viewed as the rate of return over one period. However, in multi-period and continuous time cases, can be viewed only as the return over the terminal time . We recognize this as an important difference between the single-period, multi-period case, and continuous time cases.

In the continuous time investment portfolio selection problem, we want to minimize the variance of for a given mean value of at some deterministic time . However, an investor always needs to determine the length of the holding time before investing, for example, equals to or years. A natural question is weather we can choose the holding time as a strategy for the mean variance model in continuous time. On the other hand, the investor would like to consider a short holding time within the same return. Note that the target of the mean value will move with the holding time but not a constant. For any given deterministic time , we can stop the investment at a deterministic time , where depends on both the mean value and time . The criteria used to decide when to stop the investment is as follows:

| (1.1) |

where and describes the target mean of the asset . From the definition of , we can see that and . Thus, the criterion (1.1) shows that can take value at the smallest time for the given time .

Therefore, the investor only need to minimize the variance at time , and the cost functional is given as follows:

| (1.2) |

Here, the terminal time depends on the control and time , unlike in the classical mean-variance problem. In this study, we will investigate an optimal strategy and a deterministic terminal time for the proposed model.

The work on the varying terminal time optimal control problem that most closely related to ours is that of Yang (2019), who established a stochastic maximum principle for a general state equation and cost functional. However, the result of Yang (2019) is a necessary condition for an optimal strategy and, thus cannot be used to solve the varying terminal time mean-variance model in this study. DeMiguel, Garlappi and Uppal (2009) evaluated the out-of-sample performance of the sample-based mean-variance model, and compared with the naive 1/N portfolio. Based on the results of DeMiguel, Garlappi and Uppal (2009), we want to consider the effect of the number of risky assets to mean-variance model in this study. Dybvig (1988) proposed the cost-efficient approach to the optimal portfolio selection in a straightforward way. Based on the cost-efficient approach, Bernard and Vanduffel (2014) considered the problem of mean-variance optimal portfolio in the presence of a benchmark, further see Bernard, Vanduffel and Ye (2019). Bi, Jin and Meng (2018) considered the behavioral mean–variance portfolio selection problem in continuous time. We point out that the results of Bernard and Vanduffel (2014) can solve the first step of our problem which is consistent with the results of Zhou and Li (2000), see Example 1 in this paper.

The remainder of this paper is organized as follows. In Section 2, we formulate the varying terminal time mean-variance model. Then, in Section 3, we investigate an optimal strategy and the related terminal time for the proposed model. In Section 4, based on the main results of Section 3, we compare our varying terminal time mean-variance model with the classical mean-variance model. Finally, we conclude the paper in Section 5.

2 A new mean-variance model

In the following, we will use to denote a given terminal time, to denote the terminal time related with strategy , to denote the optimal strategy under a given terminal time, and to denote an optimal pair.

Let be a -dimensional standard Brownian motion defined in a complete filtered probability space , where is the -augmentation of the natural filtration generated by . One risk-free bond asset and risky stock assets are traded in the market. The bond satisfies the following equation:

and the ’th () stock asset is described by

where is the risk-free return rate of the bond, is the expected return rate of the risky asset, and is the corresponding volatility matrix. Given initial capital , , where . The investor’s wealth satisfies

| (2.3) |

where is the capital invested in the risky asset and is the capital invested in the bond. Thus, we have

In this study, we consider the following varying terminal time mean-variance model:

| (2.4) |

with the following constraint on the varying terminal time, for any given deterministic time , we define the criteria for deciding when to stop the investment as follows:

| (2.5) |

The definition of the deterministic terminal time shows that the mean value of wealth is moves with the target . Note that if , we have that and . This is the main difference between our model (2.4) with constraint (2.5) and the classical mean-variance model.

The set of admissible strategies is defined as follows:

is the set of all valued, measurable processes adapted to such that

If there exists an optimal strategy and the related deterministic terminal time that yields the minimum value of the cost functional (2.4), and if satisfies constraint (2.5), then we say is the optimal strategy of the varying terminal time mean-variance model (2.4).

Remark 2.1.

Consider a special case of model (2.4) with constraint (2.5). We suppose that the target of the mean value is a constant, , where is a constant. Here, we want to determine the optimal terminal time for a constant target. For any given , applying the result of Zhou and Li (2000), we obtain the following representation for the variance,

where . Note that, . Thus, let

| (2.6) |

We further suppose that is the solution of equation (2.6), and that the related optimal strategy is . Then, implies that we invest all capital into the bound until time . Thus, we need to provide the conditions for the function such that .

We assume the following conditions, which we use to obtain the optimal strategy for the proposed model (2.4):

: and are bounded deterministic continuous functions.

: , .

: is increasing and differentiable in with , and satisfies

where is a given constant and I is the identity matrix of .

Remark 2.2.

Note that can be viewed as the return of asset , with initial wealth . By denoting , we obtain

yielding Note that if , we have for any strategy .

3 Optimal strategy and terminal time

3.1 Standard mean-variance model

In this section, we investigate an optimal strategy for the problem defined in (2.4), with constraint (2.5) for varying terminal time . Here, we describe how to construct an optimal strategy for (2.4) with varying terminal time (2.5). The steps are as follows:

Step 1: For any given deterministic , we determine an optimal strategy for the related mean-variance model using the embedding technique proposed in Zhou and Li (2000).

Step 2: Verify that the optimal strategy from Step 1 is an element of the set of admissible strategies and . Thus .

Step 3: Minimize the variance over to obtain, the optimal strategy and the related terminal time for problem (2.4) with varying terminal time (2.5).

Next, we consider Step 1 in greater detail. For any given deterministic time , we introduce the following mean-variance problem: minimize the cost functional,

| (3.1) |

To solve the cost functional (3.1), we employ the following model:

| (3.2) |

Applying the embedding technique of Zhou and Li (2000) for mean-variance models in the continuous time case, we have the following results. For , and denoting

the optimal strategy for (3.1) is given as follows:

Here, and satisfy the following linear ordinary differential equations:

| (3.3) |

and

| (3.4) |

Note that ; thus, we have

Let . Then, it follows that,

By assumption , we have . Thus, we can choose such that where satisfies

| (3.5) |

Based on the explicit solution for , the following theorem presents the main results from Step 1.

Theorem 3.1.

Let Assumptions and hold. For any given deterministic time , is an optimal pair for the mean-variance problem in (3.1). The efficient frontier is given as follows:

| (3.6) |

Example 1.

In Step 1, we use the embedding technique of Zhou and Li (2000) to solve the mean-variance model in continuous time. Now, we consider a one-dimensional Black-Scholes setting: there is bond with a constant risk-free rate , and a risky stock :

By Theorem 3.1, we have

| (3.8) |

where .

Applying Proposition 3.1 of Bernard and Vanduffel (2014), also see Subsection 3.2 in Bernard and Vanduffel (2014), we have

| (3.9) |

where

and

It follows that . With expectation on both sides of equation (3.9), and by plugging into it, one obtains,

which is same with equation (3.8) and is consistent with the results of Theorem 3.1.

Bernard and Vanduffel (2014) applied the cost-efficient approach to optimal portfolio selection in a straightforward way, and obtained the optimal payoff . Furthermore, we have

| (3.10) |

From equation (3.10), the optimal payoff can be divided into two parts: risk-free return , risky return , which shows that high return comes with high risk.

Next, we consider Step 2 in further details, and show that .

Lemma 3.1.

Let Assumptions , and hold. Then, we have , , and .

Proof: The proof is given in Appendix A.

Lastly, we examine Step 3 more closely. We want to obtain an optimal strategy for model (2.4) and the related deterministic terminal time . For simplicity of notation, we consider the following decomposition of ,

| (3.11) |

where

Here, can be viewed as the excess return of over the return of bond , where in denotes the optimal strategy with terminal time .

Remark 3.1.

For any given , we have

Based on the discounted factor , we call that and have the same excess return. Therefore, we can compare the variance of the asset with different terminal time under the same excess return. In the following, we show the existence of the minimum value of over under the same excess return.

Lemma 3.2.

Let Assumptions , and hold. We have the following results:

(i). If

for a constant and

there exist and related deterministic terminal time such that

where in denotes the optimal strategy with terminal time , and

(ii). If

we have that

where

Proof: The proof is given in Appendix A.

Remark 3.2.

The results of Lemma 3.2 show that if we consider the mean-variance model for a given terminal time, the variance may not determine the minimum value. Thus, we consider a varying terminal time mean-variance model with a constraint on the varying terminal time. In the following, we prove that the optimal strategy and optimal terminal time in Lemma 3.2 solve model (2.4) with constraint (2.5).

Theorem 3.2.

Let Assumptions , and hold. Then, we have the following results:

Proof: The proof is given in Appendix A.

Remark 3.3.

Comparing with results of Lemma 3.2 and Theorem 3.2, we find that the optimal strategy of is the same with the optimal strategy of model (2.4) with constraint (2.5). For any given , takes the minimum value at strategy , with . Note that in the constraint

which includes all strategies such that at , where is the minimum time such that . Lemma 3.1 shows that satisfies constraint (2.5). We conclude that the optimal strategy of the classical mean-variance model is consistent with constraint (2.5) at a given terminal time .

3.2 Multi-dimensional Black-Scholes setting

Now, we apply the results of Theorem 3.2 to consider a multi-dimensional Black-Scholes market. The bond satisfies the following equation:

and the price of the ’th () stock asset is given by

where are deterministic parameters and independent from time , and is a given -dimensional Brownian motion.

Let , where are given constants. In the following, we show the assumption for the parameters and function as follows:

: , , .

Remark 3.4.

Notice that in Assumption , we suppose , which is natural in the financial market. Here, means that the investor wants to obtain excess return exceeding the return of the asset bond. The condition on shows that the target of the mean value is increasing with the holding time.

In the following, we assume Assumption holds in the remainder of this paper. In addition, if Assumption holds, we can show that Assumptions are right. In the representation of , the term can be viewed as the excess return exceeding the return of asset bond . For any given deterministic time , and denoting

Remark 3.5.

Notice that, is the objective of mean value . The term denotes the return from bond at time , while represents the excess return exceeding the return of asset bond at time . In addition, we have

is the rate of excess return at time . is increasing with which is the number of risky assets, where is the sharp ratio of the ’th risky asset, .

Therefore, the optimal strategy is

where denotes the optimal strategy with terminal time , and We can choose such that

For the given , the efficient frontier for the classical mean-variance model (3.1) is given as follows:

| (3.14) |

where

Notice that, Remark 3.5 shows that is increasing with , which indicates that the variance is decreasing with the number of risky assets. We consider the relation of and as the efficient frontier.

If , Lemma 3.2 indicates that we cannot obtain an optimal terminal time. Thus, in the following, we suppose , for a constant . Based on the proof of Lemma 3.2, we have that the optimal terminal time is the smallest solution of the following equation:

| (3.15) |

Remark 3.6.

Notice that, is the rate of excess return of the objective of mean value . Thus, the investor needs to give the value of before investing. In general, it is convenient for the investor to suppose a constant rate of excess return. On the other hand, if is a constant, it is easy to check the condition in Lemma 3.2 and we can obtain an explicit solution for the optimal holding time .

4 Compare with classical mean-variance model

Following the results in Section 3, we compare the variance with . Based on Assumption , we first consider , and take

In addition, we have that

which satisfies the case of Theorem 3.2. Notice that, and are the variances of the classical mean-variance model and the functions of a given terminal time with , respectively.

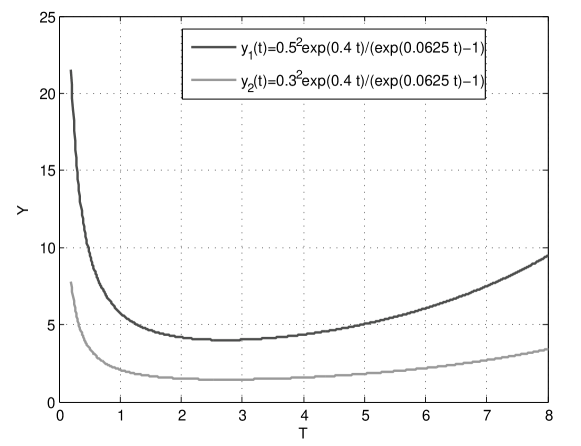

In Figure 1, we plot the functions of and over . We can verify that and take minimum values at , and is given by For the given parameters , from Figure 1, we can see that is decreasing in and increasing in . Note that and the optimal strategy yields, a high risk (variance) for a given small terminal time . At the same time, the optimal strategy of the investor could yield a high risk (variance) for a given big terminal time . These results show that we need to choose an optimal terminal time for a given rate of excess return . In addition, we show that is increasing with the parameter for a given terminal time in Figure 1.

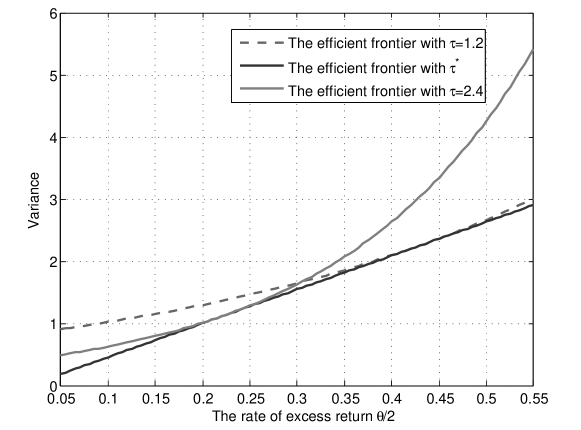

For the given parameters , we plot the relation between the rate of excess return and variance as the efficient frontier. In Figure 2, for the given terminal time , the related line shows the relation of the rate of excess return and the variance of classical mean-variance model. For the given terminal time , the related line shows the relation of the rate of excess return and the variance of classical mean-variance model. For the , the related line shows the relation of the rate of excess return and the variance of our varying terminal time mean-variance model, where varies with . The figure shows that the line of is always under the line with and line with . Therefore, the proposed model (2.4) can help to determine an optimal terminal time that varies with . In addition, for and , we find that the line with touches the line at and the line with touches the red line at , respectively. Therefore, the variance of classical mean-variance model takes the minimum at some rate of excess return for the given terminal time .

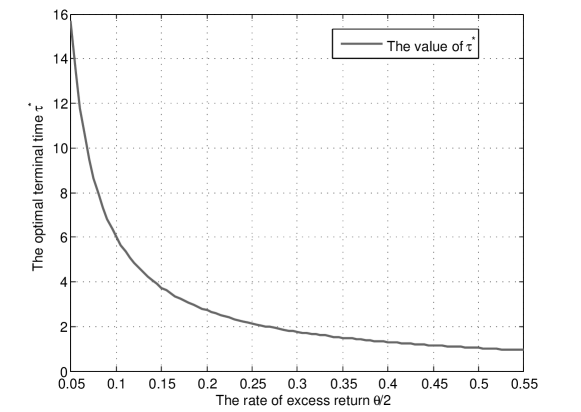

For the given parameters , we plot the relation between and the rate of excess return in Figure 3. Here, is decreasing with . In Figure 2, the variance is increasing with . These results show that if we consider a small rate of excess return in the investment plan, for example , then, we can keep the optimal strategy until with the variance . However, if we consider a high rate of excess return in the investment plan, for example , then, we can keep the optimal strategy until with the variance .

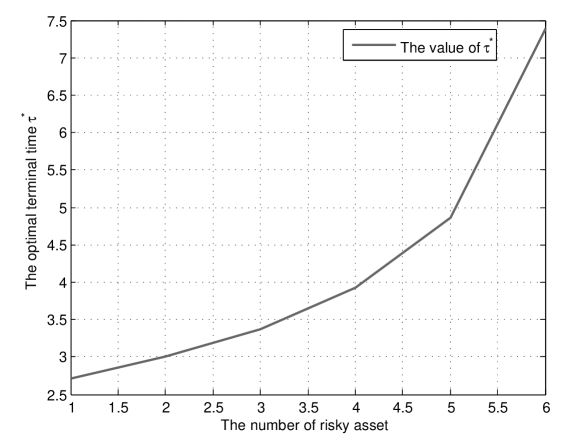

Now, we consider the relation between the number of risky assets and , let

5 Conclusion

To improve the efficient frontier of the mean-variance model, we propose a varying terminal time mean-variance model with a constraint on the varying terminal time. In the proposed model, we suppose that the investor’s target moves with the rate of return.

Our main results are as follows:

-

•

We minimize the variance of the assets in a portfolio, thus incorporating the advantages of the classical mean-variance model.

-

•

The constraint on the varying terminal time allows us to find the optimal deterministic terminal time and to minimize the variance.

-

•

The results of Section 4 show that the optimal terminal time is decreasing with the rate of excess return which suggests that the investor should change the holding time of an asset according to the rate of excess return.

-

•

The proposed varying terminal time mean-variance model improves the efficient frontier of the classical mean-variance model.

This study represents the first step in considering the varying terminal time mean-variance problem, based on which, we can further investigate topics such as bankruptcy prohibition, transaction costs, and random parameters in complete and incomplete markets.

Appendix A A Proofs:

Proof of Lemma 3.1: For any given , recall that

The derivative of at is given as follows,

From

it follows that

and

Thus, is increasing on , , and we have

Note that,

Thus and , which completes this proof.

The Proof of Lemma 3.2: By Theorem 3.1, for any given deterministic time , we have

| (A.1) |

Based on the decomposition of (3.11), we set

In the following, we calculate the derivative of at . Combining equations (A.1) and , we have

We set and have from Assumption . By Assumption , we have that and

If for a constant , there exists and such that on and on . Thus, is decreasing on and increasing on . By Assumption , we have that is a continuous function on . Thus there exists a minimum time , such that

If , we have on and

This completes the proof.

The Proof of Theorem 3.2: We first consider the case . Applying Lemma 3.2, we have that if

for a constant , then there exists that yields the minimum value of for any . For any given , based on Theorem 3.1, it follows that yields the minimum values of for any with . Note that, if , we have . For the given , Theorem 3.1 shows that there exists optimal strategy such that

From Assumption , we have

Thus, yields the minimum value of for any and . By Lemma 3.1, we have that , which shows that solves model (2.4) with constraint (2.5).

Next, we consider the case . If

Then, similarly to case , we have that yields the minimum values of for any with and . Thus, for a given , admits the minimum values of model (2.4) for any with and cost functional (2.4) is decreasing with . Thus, model (2.4) does not provide an optimal strategy in finite time. This completes the proof.

Acknowledgement

The author would like to thank the editor and two anonymous reviewers for their careful reading and suggestions for improving the quality of this paper.

References

- [1] Bajeux-Besnainou, I. and Portait, R. (1998). Dynamic asset allocation in a mean-variance framework. Management Science, 11:79–95.

- [2] Basak, S. and Chabakauri, G. (2010). Dynamic mean-variance asset allocation. Review of Financial Studies, 23:2970–3016.

- [3] Bernard, C. and Vanduffel, S. (2014). Mean-variance optimal portfolios in the presence of a benchmark with applications to fraud detection. European Journal of Operational Research, 234:469–480.

- [4] Bernard, C., Vanduffel, S. and Ye, J. (2019). Optimal strategies under omega ratio. European Journal of Operational Research, 275:755–767.

- [5] Bi, J., Jin, H. and Meng, Q. (2018). Behavioral mean–variance portfolio selection. European Journal of Operational Research, 271:644–663.

- [6] Bielecki, T. R., Jin, H., Pliska, S. and Zhou, X. (2005). Continuous-time meanvariance portfolio selection with bankruptcy prohibition. Mathematical Finance, 15:213–244.

- [7] Björk, T., Murgoci, A. and Zhou X. (2014). Mean-variance protfolio optimization with state-dependent risk aversion. Mathematical Finance, 24:1–24.

- [8] Dai, M., Xu, Z., and Zhou, X. (2010). Continuous-time markowitz’s model with transaction costs. SIAM Journal on Financial Mathematics, 1:96–125.

- [9] DeMiguel, V., Garlappi, L., and Uppal, R. (2009). Optimal versus naive diversification: How inefficient is the 1/N portfolio strategy ? The Review of Financial Studies, 22:1916–1953.

- [10] Dybvig, P. H. (1988). Inefficient dynamic portfolio strategies or how to throw away a million dollars in the stock market. The Review of Financial Studies, 1:67–88.

- [11] Kydland, F. E. and Prescott, E. (1997). Rules rather than discretion: The inconsistency of optimal plans. Journal of Political Economy, 85:473–492.

- [12] Li, D. and Ng, W. L. (2000). Optimal dynamic portfolio selection: Multi-period mean-variance formulation. Mathematical Finance, 10:387–406.

- [13] Lim, A. E. B. (2004). Quadratic hedging and mean-variance portfolio selection with random parameters in an incomplete market. Mathematics of Operations Research, 29:132–161.

- [14] Lim, A. E. B. and Zhou, X. (2002). Quadratic hedging and mean-variance portfolio selection with random parameters in a complete market. Mathematics of Operations Research, 1:101–120.

- [15] Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7:77–91.

- [16] Markowitz, H. (1959). Portfolio Selection: Efficient Diversification of Investment. John Wiley & Sons, New York.

- [17] Markowitz, H. (2014). Mean-variance approximations to expected utility. European Journal of Operational Research, 234:346–355.

- [18] Merton, R. C. (1972). An analytic derivation of the efficient frontier. J. Finance Quant. Anal., 7:1851–1872.

- [19] Richardson, H. R. (1989). A minimum variance result in continuous trading portfolio optimization. Management Science, 9:1045–1055.

- [20] Xia, J. (2005). Mean-variance portfolio choice: Quadratic partial hedging. Mathematical Finance, 15:533–538.

- [21] Yang, S. (2019). Varying terminal time optimal control problem: Part I, stochastic maximum principle. arXiv:1905.03526, 1–27.

- [22] Zhou, X. and Li, D. (2000). Continuous-time mean-variance portfolio selection: A stochastic LQ framework. Appl. Math. Optim., 42:19–33.