On asymptotic relations between singular and constrained control problems of one-dimensional diffusions

Jukka Lempa

Jukka Lempa, Department of Mathematics and Statistics, University of Turku, FI - 20014 Turun Yliopisto, Finland, jumile@utu.fi and Harto Saarinen

Harto Saarinen, Department of Mathematics and Statistics, University of Turku, FI - 20014 Turun Yliopisto, Finland, hoasaa@utu.fi

Abstract.

We study the asymptotic relations between certain singular and constrained control problems for one-dimensional diffusions with both discounted and ergodic objectives. By constrained control problems we mean that controlling is allowed only at independent Poisson arrival times. We show that when the underlying diffusion is recurrent, the solutions of the discounted problems converge in Abelian sense to those of their ergodic counterparts. Moreover, we show that the solutions of the constrained problems converge to those of their singular counterparts when the Poisson rate tends to infinity. We illustrate the results with drifted Brownian motion and Ornstein-Uhlenbeck process.

This paper is concerned with asymptotic relations between certain discounted and ergodic control problems for one-dimensional diffusions. More precisely, the following control problems are considered:

(A)

Classical singular stochastic control problems with both discounted and ergodic criteria

(B)

Constrained bounded variation control problems where controlling is allowed only at the independent Poisson arrival times with both discounted and ergodic criteria

These control problems are expected to be linked to each other via certain limiting properties. For instance, it is often expected that in item (A), the values of the problems with discounted criterion are connected to the ergodic problems in an Abelian sense, when the discounting factor vanishes. This relationship, often called the vanishing discount method and sometimes used in a heuristic manner, can be used to solve the ergodic problems [22, 20, 11, 7].

Regarding item (B), the problems of this form have attracted attention in the recent years [15, 16, 23, 18, 19], for related studies in optimal stopping see [14, 10, 12]. In these problems, it is reasonable to expect that the value functions of the constrained problems should converge to the values of their singular counterparts as the Poisson arrival rate of the control opportunities tends to infinity.

The main contribution of this paper is that we prove these expectations to be correct for time-homogeneous control problems with one-dimensional diffusion dynamics; our findings are summarized in Figure 1. These diffusion models are important in many applications. Furthermore, the time-homogeneous structure allows explicit calculations, by which we can first solve the HJB-equations of both discounted and ergodic problems separately and then establish that the solutions satisfy the desired limiting properties. This is in contrast to the vanishing discount method, where the HJB-equation of the ergodic problem is solved using the solution of the discounted problem [20].

The remainder of the paper is organized as follows. In section 2, we set up the diffusion dynamics. In section 3, we introduce the control problems and study the functionals appearing in their analysis. The asymptotic relations are proved in section 4. Paper is concluded with an explicit examples in section 5.

2. Underlying dynamics

Let be a filtered probability space which satisfies the usual conditions. We consider an uncontrolled real-valued process defined on which is modelled as a strong solution to the Itô stochastic differential equation

(1)

where is the Wiener process and the functions and are well-behaved (see [13] chapter 5). For notional convenience, we consider the case where the process evolves in , even though all the results remain unchanged even if the state space would be replaced with any intervalin .

We define the second-order linear differential operator , which represents the infinitesimal generator of the diffusion , as

(2)

and for a given , we respectively denote the increasing and decreasing solutions to the differential equation by and . These solutions are often called the fundamental solutions and can be identified as the minimal -excessive functions of the diffusion (see [8] p. 19).

We denote by the first exist time from , i.e. and define a set of functions that satisfy the integrability condition . Using this notation, we define the inverse of the differential operator , called the resolvent , by

for all and . We also define the scale density of the diffusion by

which is the monotonic (and non-constant) solution to the differential equation .

Often in computations it is useful to use the formula

(3)

which connects the resolvent and the fundamental solutions and (see [8] p. 19). Here the positive constant, which does not depend on ,

is the Wronskian of the fundamental solutions and

denotes the density of the speed measure. We also recall the resolvent equation (see [8] p. 4)

(4)

3. The control problems

To pose the assumptions for the control problems, we define the function as , where is a positive constant and is the cost function. Here, the function is defined as , where is a positive constant called the discounting factor. In economic literature, the function can be understood as the net convenience yield of holding inventories [3, 9]. This function appears in wide range of control problems of one-dimensional diffusions, when the criteria to be minimized includes discounting [15, 3, 17].

In addition, we note that in the absence of discounting, the function reduces to

which is in key role in many ergodic control problems of one-dimensional diffusions [16, 6].

We study the control problems under the following assumptionss.

Assumption 1.

We assume that:

(1)

the upper boundary and the lower boundary are natural,

(2)

the cost function is continuous, non-negative and non-decreasing,

(3)

the functions and id are in ,

(4)

there is a unique state such that (and also ) is decreasing on and increasing on and that it satisfies the limiting condition .

Assumption 2.

We assume that

(1)

and for all ,

(2)

.

We make some remarks on these assumptions. First, we assume that the uncontrolled state variable cannot become infinitely large or zero in finite time, see [8] pp. 18–20, for a characterization of the boundary behavior of diffusions. Second, the cost function is non-decreasing and non-negative which is in line with usual economic applications. Third, the resolvents and exists. Fourth, we restrict our attention to the case, where the function () has a unique global minimum at . Finally, the first part in assumption 2 guarantees that the underlying diffusion has a stationary distribution (see [8] p. 37).

Lastly, we assume that

Assumption 3.

The process is a Poisson process with a parameter and it is independent of the underlying diffusion . Furthermore, we assume that, the filtration is rich enough to carry the Poisson process . We denote the jump times of by .

Before stating the control problems, we define the auxiliary functions and as

where , are the same positive constants as in the definition of and is the intensity of the Poisson process in assumption 3. The next lemma gives useful relationships between these auxiliary functions, and . The lemma can be proved using the resolvent equation (4) and the harmonicity property .

Lemma 1.

Assume that . Then

(5)

(6)

(7)

The following functionals are in a key role in the main results of the study, as they offer convenient representations of the integral functionals that include and :

We now formulate downward singular control problems of one-dimensional diffusions and similar problems where controlling is allowed only at exogenously given Poisson arrival times. This latter problem is called constrained control problem.

We assume in all of the following theorems, that the controlled dynamics are given by the stochastic differential equation

where denotes the applied control policy and is positive constant (the coefficient is often interpreted as proportional transaction cost).

Assumption 4(Admissible control policies).

(1)

In the singular problems (theorems 1 and 2 below), we call a control policy admissible, if it is non-negative, non-decreasing, right-continuous, and -adapted, and denote the set of admissible controls by .

(2)

In the constrained problems (theorems 3 and 4 below) the set of admissible controls is given by those non-decreasing, left-continuous processes that have the representation

where is the signal process and the integrand is -predictable.

We introduce the main results of the control problems below and refer to [1, 4, 6, 5, 15, 16] for full discussions.

Theorem 1(Singular control with discounted criteria [1] pp.1701-1702, [4] pp.714-715).

Under the assumption 1, the optimal control policy minimizing the objective

where is

where denotes the local time push of the process at the boundary . The boundary is characterized by the unique solution to the equation

(8)

Moreover, the value of the problem reads as

Theorem 2(Singular control with ergodic criteria [6] pp.16-17, [5] p.7).

Under the assumptions 1 and 2, the optimal control policy minimizing the objective

where is

where denotes the local time push of the process at the boundary . The boundary is characterized by the unique solution to the equation

(9)

Moreover, the long run average cumulative yield reads as

Theorem 3(Control with discounted criteria and constraint [15] p.115).

Under the assumption 1, the optimal control policy that minimizes the objective

where , is as follows. If the controlled process is above the threshold at a jump time of , i.e. for any , the decision maker should take the controlled process to . Further, the threshold is uniquely determined by

which can be rewritten as

(10)

In addition, the value function of the problem reads as

(11)

where

Proof.

We only prove that the optimality condition can be rewritten as (10), and refer to [15] for the rest of the claim. To prove the representation, we first use the lemma 2, and then the formulas (5) and (7), to get

Utilizing the lemma 2 again, we see that the optimality condition has the form

∎

Theorem 4(Control with ergodic criteria and constraint [16] p.16).

Under the assumptions 1, 2 and that , where and are positive constants, the optimal control policy minimizing the objective

where , is as follows. If the controlled process is above the threshold at a jump time of , i.e. for any , the decision maker should take the controlled process to . Further, the threshold is uniquely determined by

(12)

and the long run average cumulative yield reads as

Remark 1.

The boundary classifications for the underlying diffusion can be relaxed in all of the above theorems. For example, in theorem 3 it can be shown that the results stays unchanged when the lower boundary is exit or killing, see [15] p. 5.

The optimal policies in the above theorems can be summarised as follows. In the singular control problems the optimal policies are local time type barrier policies. In other words, when the process is below some constant boundary the process should be left uncontrolled, but it should never be allowed to cross it, i.e. it is reflected at . The situation in the problems with constraint is similar: when the process is below some threshold we do not act, but if the process crosses the boundary, and the Poisson process jumps, we immediately push it down to and start it anew. In other words, the optimal strategy in all of the problems is to exert control at the ‘maximum rate’ when the process is at (or above) the corresponding boundary.

4. Main results

In the next lemma, we collect useful representations for functionals and .

Lemma 2.

The functions and have alternative representations

Proof.

The proof for the claim on is in [15] lemma 2 and the proof on is completely analogous.

∎

Under our assumption that the boundaries are natural, we have that

(13)

and thus, we can further rewrite

In the next proposition we prove that the just introduced functionals, often appearing in bounded variation control problems of one-dimensional diffusion processes, satisfy asymptotic properties that are needed to establish the relationships between different control problems.

Proposition 1.

Under the assumption 1, we have the following limiting properties

In addition, if the underlying diffusion is recurrent, i.e. for all , then

where

Proof.

Let . Then for all we have

(14)

Therefore, by letting we get by monotone convergence that

(15)

under the assumption that the underlying diffusion is recurrent. In addition, again by (14), we find that

(16)

Since , we see by using the above observations that by monotone convergence

Proposition 2(Asymptotics of the optimal thresholds).

Under the assumptions of proposition 1 the optimal thresholds satisfy the following asymptotic results in terms of the intensity of the Poisson process

and if the underlying diffusion is also recurrent, we have the vanishing discount factor limits

Proof.

We prove the first and the last claim, as the proof of the second claim can be found in [16], proposition 3, and the proof of the third claim in [5], lemma 3.1. Define the functions

and let , , be such that , and . Using these notations, the first claim can be re-expressed as

Now, utilizing the condition , together with the lemma 1, we have that

To prove the last claim, we first note, as above, that the claim is equivalent to

Similar limiting results hold also for the corresponding values of the defined control problems. However, it is clear that in terms of the vanishing discounting factor, the results hold only in the following Abelian sense.

Proposition 3(Asymptotics of the values).

Under the assumptions of proposition 1 the values of the control problems satisfy the following asymptotic results

Also, if the underlying diffusion is recurrent, we have the following Abelian limits

Proof.

For the last claim see lemma 3.1 of [5]. To prove the third, we first re-write the value function (11) using lemma 1 as

(17)

where

We notice that when , the value function has convenient presentation in terms of the limit . However, when we have to proceed as follows. Because is continuous across the boundary , we find

(18)

which can be re-organized as

(19)

Thus, we get that

Using the formula (3) and (LABEL:osamaara_limit_nollassa), we see that

and thus, by (LABEL:osamaara_limit_nollassa) we have

Therefore, by continuity and (2), the value function satisfies

Finally, utilizing (3), the limiting value reads as

which completes the proof of the third claim.

To prove the second claim, we notice that the value function is independent of when . Thus, we focus this time on the region . We re-organize the terms in the upper region as

(20)

where

Because diffusions are Feller-processes, we know that as (in sup-norm), see [21] pp. 235. Thus,

To deal with the remaining terms in (17), we note that by (18)

Utilizing the above we get by (LABEL:osamaara_limit_nollassa)

and

As the value function is continuous over the boundary , we further find that

Combining the above limits the result follows by continuity and proposition 2.

Lastly, the second claim of the proposition follows by continuity of the functions and proposition 2, as can also be represented as (see [6] pp. 17)

∎

Figure 1. Relations between the control problems. These relations hold for the optimal thresholds and also for the values, in the sense of propositions 1 and 2.

5. Illustration

5.1. Brownian motion with drift

Let the underlying process be defined by

(21)

where . Also, we let the process evolve in and choose a quadratic running cost .

The minimal excessive functions are in this case known to be

and the scale density and speed measure read as

respectively. The net convenience yield now takes the form . We notice immediately that our assumptions 1 and 3 hold and so the results apply in the case of the discounted problems (theorems 1 and 3).

To illustrate the results of proposition 2, we solve the optimality conditions (8) and (10). Conveniently the solution to these equations can be represented explicitly. To solve the equations we need to find the functions and . Elementary integration yields

where and . Plugging these representations to the equations (8) and (10), a simplification yields as solutions the thresholds

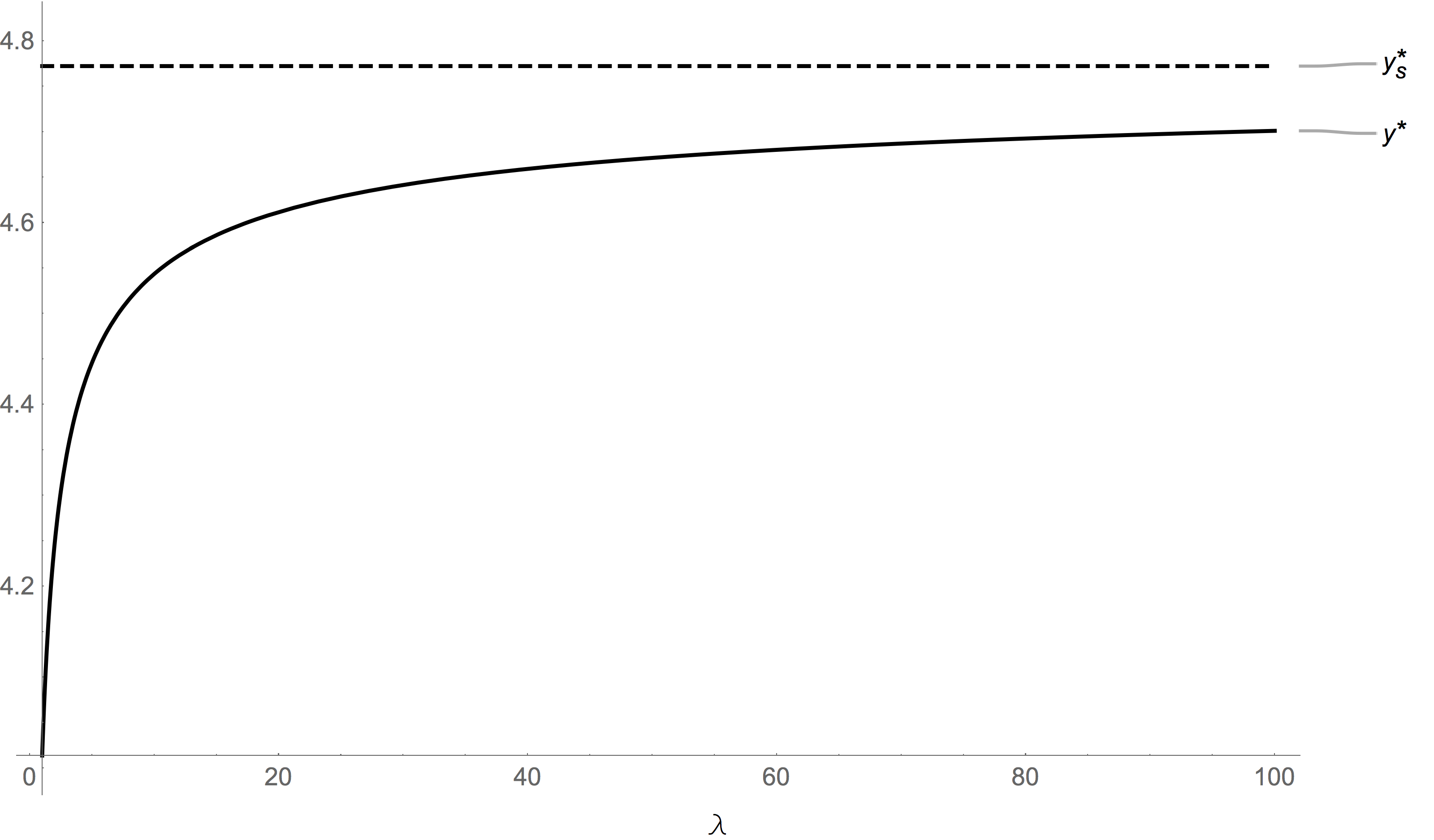

Using these explicit representation, we get a limit as in proposition 2. These thresholds are illustrated in the figure 2.

Figure 2. Threshold boundaries as a function of the intensity of the Poisson process with the parameters , and .

5.2. Controlled Ornstein-Uhlenbeck process

Consider dynamics that are characterized by a stochastic differential equation

where . This diffusion is often used to model continuous time systems that have mean reverting behaviour. To illustrate the results we choose the running cost

and consequently . The scale density and the density of speed measure are in this case

and the minimal -excessive functions read as (see [8] p. 141)

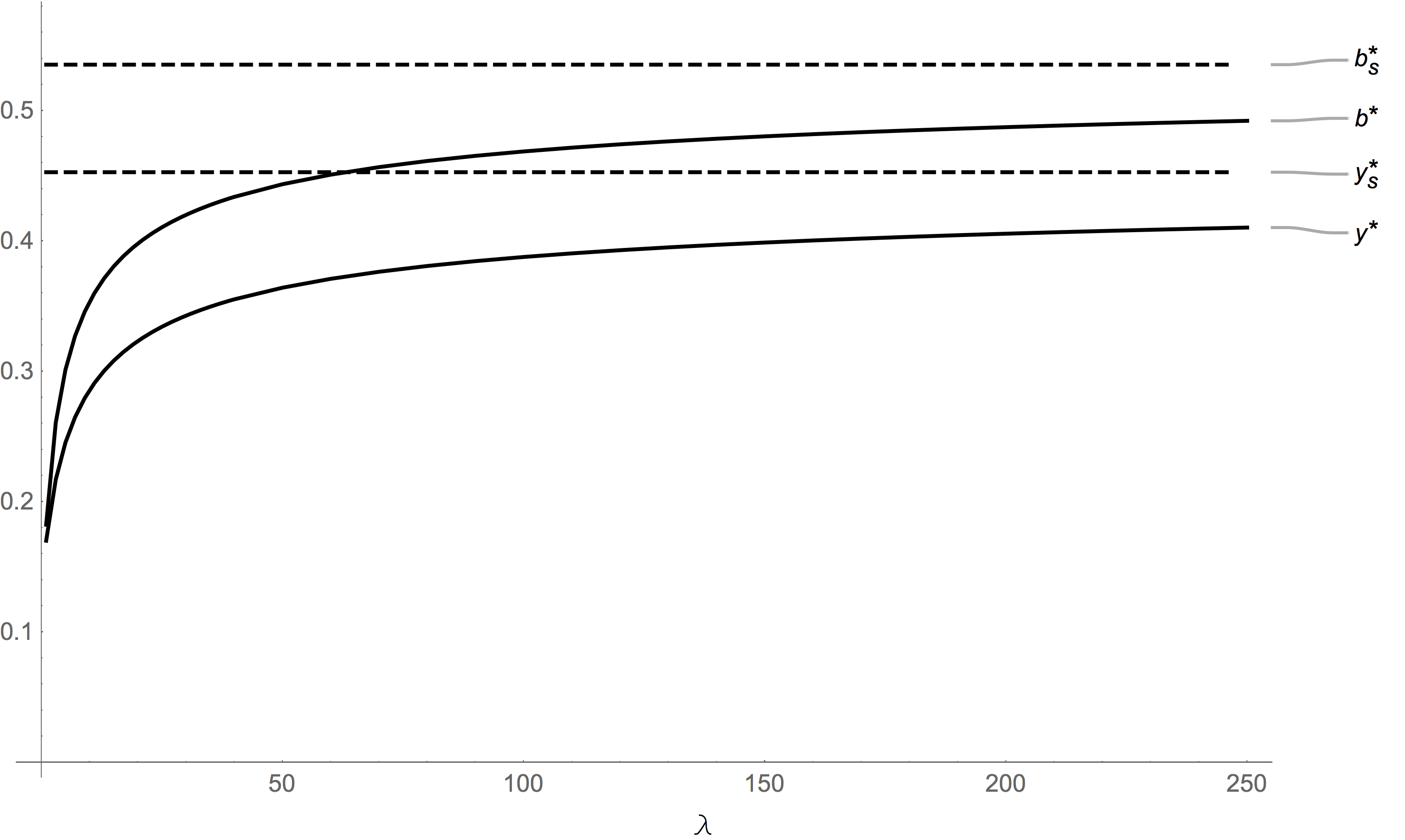

where is a parabolic cylinder function. We note that our assumptions 1 and 2 are satisfied and that this process is positively recurrent recurrent (see [8] p.141). Unfortunately, the equations for the optimal thresholds take rather complicated forms, and thus the results in proposition (2) are only illustrated numerically.

Figure 3. Threshold boundaries as a function of the intensity of the Poisson process with the parameters , and .Figure 4. Threshold boundaries as a function of the discounting with the parameters , and .

Acknowledgements

We would like to gratefully acknowledge the emmy.network foundation under the aegis of the Fondation de Luxembourg, for its continued support.

References

[1] Alvarez, L. H. R., Singular Stochastic Control, Linear Diffusions, and Optimal Stopping: A Class of Solvable Problems, SIAM J. Control Optim., Volume 39, pp. 1697-1710, 2001.

[2] Alvarez, L. H. R., On the Properties of r-Excessive Mappings for a Class of Diffusions, Ann. Appl. Probab., Volume 13, pp. 1517-1533, 2003.

[3] Alvarez, L. H. R., A Class of Solvable Impulse Control Problems, Appl. Math. Optimization, Volume 49, pp. 265-295, 2004.

[4] Alvarez, L. H. R. and Lempa J., On The Optimal Stochastic Impulse Control of Linear Diffusions, SIAM J. Control Optim., Volume 47, pp. 703-732, 2008.

[5] Alvarez, L. H. R., and Hening, A., Optimal Sustainable Harvesting of Populations in Random Environments, e-print ArXiv:1807.02464, 2018.

[6] Alvarez, L. H. R.,

A Class of Solvable Stationary Singular Stochastic Control Problems,

e-print ArXiv:1803.03464, 2018.

[7] Arapostathis, A., Borkar, V. S. and Ghosh, M. K., Ergodic Control of Diffusion Processes.

Cambridge University Press, New York, 2012.

[8] Borodin, A. N. and Salminen, P.

Handbook of Brownian Motion - Facts and Formulae, 2nd edition.

Birkhäuser, Basel.

[9] Dixit, A. K. and Pindyck, R.S., Investment Under Uncertainty, Princeton Univ. Press, 1994.

[10] Dupuis, P. and Wang, H.,

Optimal Stopping with Random Intervention Times,

Adv. Appl. Prob., Volume 34, pp. 141-157, 2002.

[11] Gatarek, D. and Stettner, L., On the compactness method in general ergodic impulsive control of Markov processes, Stoch. Stoch. Rep., Volume 31, pp. 15–25, 1990.

[12] Guo, X. and Liu, J., Stopping at the maximum of geometric Brownian motion when signals are received.

J. Appl. Probab., Volume 42, pp. 826–838, 2005.

[13] Karatzas, I., Shreve, S. E.,

Brownian Motion and Stochastic Calculus,

Springer, New York, 1991.

[14] Lempa, J.,

Optimal Stopping with Information Constraint,

Appl. Math. Optimization, Volume 66, pp. 147-173, 2012.

[15] Lempa, J., Bounded Variation Control of Itô Diffusion with Exogenously Restricted Intervention Times, Adv. Appl. Prob., Volume 46, pp. 102-120, 2014.

[16] Lempa, J., and Saarinen, H., Ergodic Control of Diffusions with Random Intervention Times, e-print ArXiv:1909.05047, 2019.

[17] Matomäki P., On Solvability of a Two-sided Singular control Problem, Math. Math. Oper. Res., Volume 76, pp. 239-271, 2012.

[18] Menaldi, J. L. and Robin, M.,

On Some Impulse Control Problems with Constraint,

SIAM J. Control Optim., Volume 55, pp. 3204-3225, 2017.

[19] Menaldi, J. L. and Robin M.,

On Some Ergodic Impulse Control Problems with Constraint,

SIAM J. Control Optim., Volume 56, pp. 2690-2711, 2018.

[20] Robin, M.,

Long-Term Average Cost Control Problems for Continuous time Markov Processes: A Survey,

Acta Applicande Mathematicae, Volume 1, pp. 281-299, 1983.

[21] Rogers, L.C.G., Williams, D.: Diffusions, Markov Processes and

Martingales, vol. 1. Cambridge University Press, Cambridge, 2001.

[22] Sethsi, S., Zhang, H. and Zhang, Q., Average-Cost Control of Stochastic Manufacturing Systems, Springer-Verlag, New York, 2005.

[23] Wang, H.,

Some Control Problems with Random Intervention Times,

Adv. Appl. Prob., Volume 33, pp. 404-422, 2001.