Online Linear Programming: Dual Convergence, New Algorithms, and Regret Bounds

chengli1, yyye@stanford.edu )

Abstract

We study an online linear programming (OLP) problem under a random input model in which the columns of the constraint matrix along with the corresponding coefficients in the objective function are generated i.i.d. from an unknown distribution and revealed sequentially over time. Virtually existing online algorithms were based on learning the dual optimal solutions/prices of the linear programs (LP), and their analyses were focused on the aggregate objective value and solving the packing LP where all coefficients in the constraint matrix and objective are nonnegative. However, two major open questions were: (i) Does the set of LP optimal dual prices learned in the existing algorithms converge to those of the “offline” LP, and (ii) Could the results be extended to general LP problems where the coefficients can be either positive or negative. We resolve these two questions by establishing convergence results for the dual prices under moderate regularity conditions for general LP problems. Specifically, we identify an equivalent form of the dual problem which relates the dual LP with a sample average approximation to a stochastic program. Furthermore, we propose a new type of OLP algorithm, Action-History-Dependent Learning Algorithm, which improves the previous algorithm performances by taking into account the past input data as well as the past decisions/actions. We derive an regret bound (under a locally strong convexity and smoothness condition) for the proposed algorithm, against the bound for typical dual-price learning algorithms, where is the number of decision variables. Numerical experiments demonstrate the effectiveness of the proposed algorithm and the action-history-dependent design.

1 Introduction

Sequential decision making has been an increasingly attractive research topic with the advancement of information technology and the emergence of new online marketplaces. As a key concept appearing widely in the fields of operations research, management science, and artificial intelligence, sequential decision making concerns the problem of finding the optimal decision/policy in a dynamic environment where the knowledge of the system, in the form of data and samples, amasses and evolves over time. In this paper, we study the problem of solving linear programs in a sequential setting, usually referred to as online linear programming (OLP) (See e.g., (Agrawal et al., 2014)). The formulation of OLP has been widely applied in the context of online Adwords/advertising (Mehta et al., 2005), online auction market (Buchbinder et al., 2007), resource allocation (Asadpour et al., 2019), packing and routing (Buchbinder and Naor, 2009), and revenue management (Talluri and Van Ryzin, 2006). One common feature in these application contexts is that the customers, orders, or queries arrive in a forward sequential manner, and the decisions need to be made on the fly with no future data/information available at the decision/action point.

The OLP problem takes a standard linear program as its underlying form (with decision variables and constraints), while the constraint matrix is revealed column by column with the corresponding coefficient in the linear objective function. In this paper, we consider the standard random input model (See (Goel and Mehta, 2008; Devanur et al., 2019)) where the orders, represented by the columns of the constraint matrix together with the corresponding objective coefficients, are sampled independently and identically from an unknown distribution . At each timestamp, the value of the decision variable needs to be determined based on the past observations and cannot be changed afterward. The goal is to minimize the gap (formally defined as regret) between the objective value solved in this online fashion and the “offline” optimal objective value where one has the full knowledge of the linear program data.

There were many algorithms and research results on OLP in the past decade due to its wide applications. Virtually all existing online algorithms were based on learning the LP dual optimal solutions/prices, and their analyses of OLP were focused on the aggregate objective value and solving the packing LP where all coefficients in the constraint matrix and objective are nonnegative. Two major open questions in the literature were: (1) Does the set of LP optimal dual prices of OLP converge to those of the offline LP, and (2) Could the results be extended to general LP problems where the coefficients can be either positive or negative. We resolve these two questions in this paper as part of our results. Moreover, we propose a new type of OLP algorithm and develop tools to analyze the regret of OLP algorithms. Our key results and main contributions are summarized as follows.

1.1 Key Results and Main Contributions

Dual convergence of online linear programs. We establish convergence results for the dual optimal solutions of a sequence of linear programs in Section 3. We first derive an equivalent form of the dual LP and discover that the sampled dual LP, under the random input model, can be viewed as a Sample Average Approximation (SAA) (Kleywegt et al., 2002; Shapiro et al., 2009) of a constrained stochastic programming problem. The stochastic program is defined by the LP constraint capacity and the distribution that generates the input of the LP. Our key result states that, under moderate regularity conditions, the optimal solution of the sampled dual LP will converge to the optimal solution of the stochastic program as the number of (primal LP) decision variables goes to infinity. Specifically, we establish that the L2 distance between the two solutions is under the random input model where is the number of constraints and is the number of decision variables. Moreover, the convergence results are not only pertaining to online packing LPs, but also hold for general LPs where the input data coefficients can be either positive or negative.

Action-history-dependent learning algorithm. We develop a new type of OLP algorithm – Action-history-dependent Learning Algorithm in Section 4.5. This new algorithm is a dual-based algorithm (as the algorithms in (Devanur et al., 2011; Agrawal et al., 2014; Gupta and Molinaro, 2014), etc.) and it utilizes our results on the convergence of the sampled dual optimal solution. One common pattern in the design of most existing OLP algorithms is that the choice of the decision variable at time only depends on the past input data, i.e., the coefficients in the constraints and the objective function revealed, but not the decisions already made (until time ). Our new action-history-dependent algorithm considers both the past input data and the past choice of decision variables. Similar idea was considered in a few specific problems such as network revenue management and online auction. Compared to the existing OLP algorithms, our new algorithm is more conscious of the constraints/resources consumed by the past decisions, and thus the decisions can be made in a more dynamic, closed-loop, and non-stationary way. We demonstrate in both theory and numerical experiments that this actions-history-dependent mechanism significantly improves the online performance than existing OLP algorithms without this mechanism.

Regret bounds for OLP. We analyze the worst-case gap (regret) between the expected online objective value and the “offline” optimal objective value. Specifically, we study the regret in an asymptotic regime where the number of constraints is fixed as a constant and the LP right-hand-side input scales linearly with the number of decision variables . As far as we know, this is the first regret analysis result in the general OLP formulation. We derive an regret upper bound (under a locally strong convexity and smoothness assumption) for the proposed action-history-dependent learning algorithm, which has a similar order of magnitude as the best achievable lower bound of the problem even with the exact knowledge of the underlying distribution (Bray, 2019). Our regret analysis provides an algorithmic insight for the constrained online optimization problem: a successful algorithm should have good control of the binding constraints (resources) consumption – not exhausting those constraints too early or having too much remaining at the end, an aspect usually overlooked by typical dual-price learning algorithms in OLP literature. The analysis extends the findings in the network revenue management literature (for example, the adaptive resource control in (Jasin and Kumar, 2012; Jasin, 2015)) to a more general non-parametric context. Moreover, the results and methodologies (such as Theorem 2) are potentially applicable to other online learning and online decision making problems.

1.2 Literature Review

Online optimization/learning/decision problems have been long studied in the community of operations research and theoretical computer science. We refer readers to the papers (Borodin and El-Yaniv, 2005; Buchbinder et al., 2009; Hazan et al., 2016) for a general overview of the topic and the recent developments. The OLP problem has been studied mainly under two models: the random input model (Goel and Mehta, 2008; Devanur et al., 2019) and the random permutation model (Molinaro and Ravi, 2013; Agrawal et al., 2014; Gupta and Molinaro, 2014). In this paper, we consider the random input model (also known as stochastic input model) where the columns of constraint matrix are generated i.i.d. from an unknown distribution . In comparison, the random permutation model assumes the columns are arriving in random order and the arrival order is uniformly distributed over all the permutations. Technically, the i.i.d. assumption in the random input model is stronger than the random permutation assumption in that the random input model can be viewed as a special case of the random permutation model ((Mehta, 2013)). Practically, the random input model can be motivated from the online advertising problem, network revenue management problems in flight and hotel bookings, or the online auction problem. In these application contexts, each column in the constraint matrix together with the corresponding coefficient in the objective function represents an individual order/bid/query. In this sense, the random input model can be interpreted as an independence assumption across different customers.

Our paper differs from the existing OLP literature in the right-hand-side assumption, i.e., the constraint capacity. A stream of OLP papers (Devanur and Hayes, 2009; Molinaro and Ravi, 2013; Agrawal et al., 2014; Kesselheim et al., 2014; Gupta and Molinaro, 2014) studied the trade-off between the algorithm competitiveness and the constraint capacity. They investigated the necessary and sufficient condition on the right-hand-side of the LP and the number of constraints for the existence of a -competitive OLP algorithm. Specifically, Agrawal et al. (2014) established the necessary part by constructing a worst-case example, stating that the right-hand-side should be no smaller than . Kesselheim et al. (2014); Gupta and Molinaro (2014) developed algorithms that achieve -competitiveness under this necessary condition and thus completed the sufficient part. In this paper, we research an alternative question, when the right-hand-side grows linearly with the number of decision variables , whether the algorithm could achieve a better performance than -competitiveness. In general, this linear growth regime will render the optimal objective value growing linearly with as well. Consequently, a -competitiveness performance guarantee will potentially incur a gap that is linear in between the online objective value and the offline optimal value. Thus we consider regret instead of competitiveness ratio as the performance measure and will analyze three algorithms that achieve sublinear regret under the linear growth regime. Moreover, a typical assumption in the OLP literature requires the data entries in the constraint matrix and the objective to be non-negative. We do not make this assumption in our model so that our model and analysis can capture a double-sided market with both buying and selling orders.

Another stream of research originates from the revenue management literature and studies a parameterized type of the OLP problem. It models the network revenue management problem where heterogeneous customers arrive sequentially to the system and the customers can be divided into finitely many classes based on their requests and prices. In the language of OLP, the columns of the constraint matrix with the corresponding coefficients in the objective follow a well-parameterized distribution and have a finite and known support. Reiman and Wang (2008); Jasin and Kumar (2012, 2013); Bumpensanti and Wang (2018) among others studied the problem under a setting where the model parameters are known and discussed the performance of a re-solving technique that dynamically solves the certainty-equivalent problem according to the current state of the system. This line of work highlights the effectiveness of the re-solving technique in an environment with known parameters and investigates the desired re-solving frequency. In a similar spirit, Jasin (2015) analyzed the performance of the re-solving based algorithm in an unknown parameter setting, and Ferreira et al. (2018) studied a slightly different pricing-based revenue management problem. The OLP model generalizes the network revenue management problem in that it does not impose any parametric structure on the distribution. For the OLP problem, the distribution of the customer request and price may have an infinite support (such as secretary problem/Adwords problem) and negative values are allowed (such as a two-sided auction market). Comparatively, the revenue management literature focuses on the case where the underlying distribution has a parametric structure and finite support. For example, Jasin (2015) studied an unknown setting, but the paper still assumed the knowledge of the distribution’s support. Consequently, the parameter learning in (Jasin, 2015) was reduced to a simple intensity estimation problem for a homogeneous Poisson process and the algorithm therein relied on the estimation together with the re-solving technique. In fact, the algorithms developed along this line of literature fail for the more general OLP problem because when the distribution is fully non-parametric and unknown, there is no way to first estimate the distribution parameter and then to solve a certainty-equivalent optimization problem based on the estimated parameter. The dual-based algorithms developed in our paper can thus be viewed as a combination of this first-estimate-then-optimize procedure into one single step. In particular, our action-history-dependent algorithm implements the idea of re-solving technique in a non-parametric setting, and our algorithm analysis reinforces the effectiveness of the adaptive and re-solving design (mainly discussed in the revenue management literature) in a more general online optimization context.

Another line of research investigated the multi-secretary problem ((Kleinberg, 2005; Arlotto and Gurvich, 2019; Bray, 2019) among others). The multi-secretary problem is a special form of OLP problem that has only one constraint and all the coefficients in the constraint matrix are one. Arlotto and Gurvich (2019) showed that when the reward distribution is unknown and if no additional assumption is imposed on the distribution, the regret lower bound of the multi-secretary problem is . A subsequent work (Bray, 2019) further noted that even when the distribution is known, the regret lower bound is Balseiro and Gur (2019) studied a similar one-constraint but multi-agent online learning formulation motivated from the repeated auction problem. The results in our paper are positioned in a more general context and consistent with this line of works. We identify a group of assumptions that admits an regret upper bound for the more general OLP problem. Our action-history-dependent algorithm can also be viewed as a generalization of the elegant adaptive algorithms developed in (Arlotto and Gurvich, 2019; Balseiro and Gur, 2019). Together with (Bray, 2019), our results indicate that the action-history-dependent algorithm achieves a near-optimal regret performance for the multi-secretary problem even in a comparison with the optimal dynamic algorithm developed with knowledge of the distribution.

The OLP problem is also related to the general online optimization problem. Compared to the standard online optimization problem, our OLP problem is special in two aspects: (i) the presence of the constraints and (ii) a dynamic oracle as the regret benchmark. For the literature on online optimization with constraints (Mahdavi et al., 2012; Agrawal and Devanur, 2014b; Yu et al., 2017; Yuan and Lamperski, 2018), the common approach is to employ a bi-objective performance measure and report the regret and constraint violation separately. We contribute to this line of research by developing a machinery to analyze the regret of a feasible online algorithm. For the second aspect, the dynamic oracle allows the decision variables (in OLP) of different time steps to take different values. This is a stronger oracle than the static oracle (Mahdavi et al., 2012; Agrawal and Devanur, 2014b; Yu et al., 2017; Yuan and Lamperski, 2018) that requires the decision variables at different time steps to take the same (static) value. In other words, the OLP regret is computed against a stronger benchmark. This explains why OLP literature considers mainly the random input model and the random permutation model, instead of an adversarial setting.

2 Problem Formulation

In this section, we formulate the OLP problem and define the objective. Consider a generic LP problem

| (1) | ||||

| s.t. | ||||

where , and Without loss of generality, we assume for Throughout this paper, we use bold symbols to denote vectors/matrices and normal symbols for scalars.

In the online setting, the parameters of the linear program are revealed in an online fashion and one needs to determine the value of decision variables sequentially. Specifically, at each time the coefficients are revealed, and we need to decide the value of instantly. Different from the offline setting, at time , we do not have the information of the following coefficients to be revealed. Given the history , the decision of can be expressed as a policy function of the history and the coefficients observed in the current time period. That is,

| (2) |

The policy function can be time-dependent and we denote policy The decision variable must conform to the constraints

The objective is to maximize the objective

We illustrate the problem setting through the following practical example. Consider a market making company receiving both buying and selling orders, and the orders arrive sequentially. At each time we observe a new order, and we need to decide whether to accept or reject the order. The order is a buying/selling request for the resources, or it could be a mixed request, e.g., selling the first resource for unit and buying the second resource for units with a total order price of $1. Once our decision is made, the order will leave the system, and it is either fulfilled or rejected. In this example, the term can be interpreted as the total available inventory for the resource and the decision variables ’s can be interpreted as the acceptance and rejection of an order. In particular, we do not allow shorting of resources along the process. Our goal is to maximize the total revenue.

We assume the LP parameters are generated i.i.d. from an unknown distribution We denote the offline optimal solution of linear program (1) as , and the offline (online) objective value as (). Specifically,

in which online objective value depends on the policy . The quantity assumes the full knowledge of the realization (of the randomness), and it is also known as hindsight oracle in the literature of online learning and robust optimization. In this paper, we consider a fixed and large regime, and focus on the worst-case gap between the online and offline objective. We define the regret

and the worst-case regret

where denotes a family of distributions satisfying some regularity conditions (to be specified later). Throughout this paper, we omit the subscript in the expectation notation when there is no ambiguity. The worst-case regret takes the supremum regret over a family of distributions so that it is suitable as a performance guarantee when the distribution is unknown. We remark that the offline optimal solution can be interpreted as a dynamic oracle that allows the optimal decision variables to take different values at different time steps. This is an important distinction between the OLP problem and the problem of online convex optimization with constraints (Mahdavi et al., 2012; Agrawal and Devanur, 2014b; Yu et al., 2017; Yuan and Lamperski, 2018).

2.1 Notations

Throughout this paper, we use the standard big-O notations where and represent upper and lower bound, respectively. The notation further omits the logarithmic factor, such as and . The following list summarizes the notations used in this paper:

-

•

: number of constraints; : number of decision variables

-

•

: index for constraint; : index for the decision variables

-

•

: the -th coefficient in the objective function

-

•

: the -th column in the constraint matrix

-

•

: upper bound on ’s and ’s

-

•

: distribution of ’s; : a family of distributions to be defined in the next section

-

•

: Parameters that convey the meaning of strong convexity and smoothness; they are related to the condition distribution of to be defined in the next section

-

•

: the offline primal optimal solution

-

•

: the online solution

-

•

: the (random) offline dual optimal solution

-

•

: the (deterministic) optimal solution of the stochastic program (7)

-

•

: the offline optimal objective value

-

•

(sometimes when the policy is clear): the online return/revenue under policy

-

•

: the right-hand-side, constraint capacity

-

•

: the average constraint capacity, i.e.,

-

•

: lower and upper bounds for

-

•

: the region for , defined by

-

•

and : the index sets for binding and non-binding constraints defined by the stochastic program (7), respectively

-

•

: the remaining constraint capacity at the end of the -th period,

-

•

: the remaining average constraint capacity at the end of the -th period, i.e., ,

-

•

: minimum operator, for

-

•

: maximum operator, for

-

•

: indicator function; when is true and otherwise

3 Dual Convergence

Many OLP algorithms rely on solving the dual problem of the linear program (1). However, there is still a lack of theoretical understanding of the properties of the dual optimal solutions. In this section, we establish convergence results on the OLP dual solutions and lay foundations for the analyses of the OLP algorithms.

Let be an optimal solution for the dual LP (3). From the complementary slackness condition, we know the primal optimal solution satisfies

| (4) |

When , the optimal solution may take non-integer values. This tells us that the primal optimal solution largely depends on the dual optimal solution and thus motivates our study of the optimal dual solutions. An equivalent form of the dual LP can be obtained by plugging the constraints into the objective function (3):

| (5) | ||||

| s.t. |

where is the positive part function, also known as the ReLu function. The optimization problem (5), despite not being a linear program, has a convex objective function. It has the advantage of only involving which is closely related to the optimal primal solution. More importantly, the random summands in the second part of the objective function (5) are independent of each other, and therefore the sum (after a normalization) will converge to a certain deterministic function. To better make this point, let and divide the objective function in (5) by . Then the optimization problem can be rewritten as

| (6) | ||||

| s.t. |

The second term in the objective function (6) is a summation of i.i.d. random functions.

Consider the following stochastic program

| (7) | ||||

| s.t. |

where the expectation is taken with respect to . In the rest of the paper, unless otherwise stated, the expectation is always taken with respect to . Evidently,

for all This observation casts the dual convergence problem in the form of a stochastic programming problem. The function in (6) can be viewed as a sample average approximation (SAA) (See (Kleywegt et al., 2002; Shapiro et al., 2009)) of the function Specifically, the dual program associated with a primal linear program with decision variables is then an -sample approximation of the stochastic program (7). We denote the optimal solutions to the -sample approximation problem (6) and the stochastic program (7) with and , respectively. In this section, we provide a finite-sample analysis for the convergence of to . We first introduce the assumptions and then formally establish the convergence.

3.1 Assumptions and Basics

The first group of assumptions concerns the boundedness and the linear growth of the constraints.

Assumption 1 (Boundedness and Linear Growth Capacity).

We assume

-

(a)

are generated i.i.d. from distribution .

-

(b)

There exist constants such that and almost surely.

-

(c)

for , Denote

-

(d)

Throughout this paper, denotes the L2-norm of a vector.

Assumption 1 (a) states that parameters (coefficients in the objective function and columns in the constraint matrix) of linear program (1) are generated i.i.d. from an unknown distribution The vectors are independent of each other, but their components may be dependent. Assumption 1 (b) requires the parameters are bounded. The bound parameters and are introduced only for analysis purposes and will not be used for algorithm implementation. Assumption 1 (c) requires the right-hand-side of the LP constraints grows linearly with . This guarantees that for the (optimal) solutions, a constant proportion of the ’s could be . It means the number of orders/requests that can be fulfilled is on the order of and thus ensures a constant service level (percentage of orders satisfied). On the contrary, if this is not true and all the requests are buying orders (), the service level may go to zero when the business running period goes to infinity. The parameter has the interpretation of available constraint/resource per period. Also, we require that the number of decision variables is larger than the number of constraints . While discussing the dual convergence, the dimension of the dual variable is equal to the number of constraints and the number of primal decision variables can be viewed as the number of samples used to approximate The assumption of restricts our attention to a low-dimensional setting.

Proposition 1 summarizes several basic properties related to the dual LP (3) and the stochastic program (7). It states that both the objective functions in the SAA problem and the stochastic program are convex. In addition, the optimal solutions to these two problems are bounded.

Proposition 1.

Given the boundedness of the optimal solutions, we define

where is an all-one vector. We know that covers all possible optimal solutions to (6) and (7).

Next, we introduce the second group of assumptions on the distribution . Here and hereafter, denotes the indicator function.

Assumption 2 (Non-degeneracy).

We assume

-

(a)

The second-order moment matrix is positive-definite. Denote its minimum eigenvalue with

-

(b)

There exist constants and such that if ,

holds for any .

-

(c)

The optimal solution to the stochastic optimization problem (7) satisfies if and only if

Assumption (c) (a) is mild in that the matrix is positive semi-definite by definition; the positive definiteness holds as long as the constraint matrix of the LP always has a full row rank, which is a typical assumption for solving linear programs. Assumption (c) (b) states that the cumulative distribution function of should not grow too fast or too slowly. Assumption (c) (c) imposes a strict complementarity for the stochastic program. Essentially, Assumption (c) altogether imposes a non-degeneracy condition for both the primal and dual LPs. It can be viewed as a generalization of the non-degeneracy condition in (Jasin and Kumar, 2012; Jasin, 2015) and as a stochastic version of the general position condition in (Devanur and Hayes, 2009; Agrawal et al., 2014).

We remark that all three parts of Assumption (c) are crucial for the analyses in the rest of the paper. While Assumption (c) (a) and (c) are not necessarily true for all the stochastic programs, a slight perturbation of the distribution (for example, through adding small random noises to and ) would result in them being satisfied. In addition, we provide three examples that satisfy Assumption (c) (b). In Example 1, we can simply choose and and then Assumption (c) (b) is satisfied. The analyses of Example 2 and Example 3 are postponed to Section A3.

Example 1.

Consider a multi-secretary problem where and all the constraint coefficients for . The reward is a continuous random variable and its distribution has a density function s.t. for Here .

Example 2.

Consider such that where is a continuous random variable independent with and with bounded support. In addition, the distribution of ’s has a density function such that there exists such that for and for all .

Example 3.

Consider such that the conditional distribution has a density function and the density function satisfies for with and for . In addition, there exists such that almost surely.

According to Assumption 2 (c), we define two index sets

where the subscripts “B” and “N” are short for binding and non-binding, respectively. Assumption (c) (c) implies and Throughout the paper, the binding and non-binding constraints of the OLP problem are always defined according to the stochastic program (7).

Now, we derive more basic properties for the stochastic program (7) based on Assumption (c). First, define a function ,

and function ,

where and . The function is the partial sub-gradient of the function with respect to ; in particular, when . We know that

and we define

| (8) |

where both expectations are taken with respect to The caveat is that the function is not necessarily differentiable under our current assumptions. As we will see shortly in Lemma 1 and Proposition 2, the definition of constitutes a meaning of sub-gradient for function .

Lemma 1 represents the difference between and with the sub-gradient function . Note that the identity (9) holds regardless of the distribution . Its derivation shares the same idea with the Knight’s identity in (Knight, 1998). Intuitively, the lemma can be viewed as a second-order Taylor expansion for the function The first and second term on the right-hand side of the identity can be interpreted as the first- and second- order term in Taylor expansion. They are disguised in this special form due to the non-differentiability of the positive part function at the origin.

Lemma 1.

For any we have the following identity,

| (9) |

where the expectation is taken with respect to

Proposition 2 applies Assumption (c) to the identity (9) and it leads to a local property around for the function . Our motivation for the proposition is to provide more intuitions for Assumption (c) from a technical perspective. Moreover, the proposition asserts the uniqueness of which makes our notion of convergence to well-defined.

Proposition 2 (Growth and Smoothness of ).

The proposition gives a technical interpretation for the distributional conditions in Assumption (c). Essentially, the role of the assumption on the distribution is to impose a locally strong convexity and smoothness around . This is weaker than the classic notion of strong convexity and smoothness for convex functions which requires the inequality (10) to hold globally. Assumption (c) (b) and Proposition 2 both concern a local property for the optimal solution As we will see in the later chapter, this local property on is crucial and sufficient to ensure a fast convergence rate of and a sharp regret bound for OLP algorithms.

We use the notation to denote the family of distributions that satisfy Assumption 1 and (c). In the rest of the paper except for Section 4.5, all the theoretical results on the dual convergence and the analyses of OLP algorithms are established under Assumption 1 and (c). In Section 4.5, we will present a stronger version of Assumption (c) and analyze the action-history-dependent algorithm accordingly.

3.2 Dual Convergence

Now, we discuss the convergence of to . First, the SAA function can be expressed by

where and the function is as defined earlier. Lemma 2 is a sample average version of Lemma 1 and it represents the difference between and with the sub-gradient function .

Lemma 2.

For any we have the following identity,

| (11) |

In the following, we will establish the convergence of based on an analysis of the identity (11). The idea is to show that the right-hand-side of (11) concentrates around its expectation as on the right-hand-side of (9). The following two propositions analyze the first-order and second-order terms respectively. Proposition 3 tells that the sample average sub-gradient stays close to its expectation (8) evaluated at with high probability. Proposition 4 states that the second-order term – the integral on the right hand of (11), is uniformly lower bounded by a strongly convex quadratic function with high probability. Intuitively, the analysis only involves the local property of the function around This explains why we impose only local (but not global) conditions on the function in Assumption (c). Specifically, Assumption (c) (a) and (b) concern the Hessian, while Assumption (c) (c) concerns the gradient, with both being evaluated at

Proposition 3.

We have

hold for any , all and .

Proposition 3 is obtained by a direct application of a concentration inequality. Notably, the probability bound on right-hand-side is not dependent on the distribution and the inequality holds for any From the optimality condition of the stochastic program, we know for and for . Therefore, the proposition implies that the sample average sub-gradient (first-order term in (11)) concentrates around zero for binding dimensions and concentrates around a positive value for non-binding dimensions. As noted earlier, the binding and non-binding dimensions are defined by the stochastic program (7).

Proposition 4.

We have

| (12) | |||

holds for any and Here

where is the floor function.

Proposition 4 discusses the second-order term in (11). The inequality (12) tells that the second-order term is uniformly lower bounded by a quadratic function with high probability. To prove the inequality for a fixed can be easily done by a concentration argument as in Proposition 3. The challenging part is to show that the inequality (12) holds uniformly for all The idea here is to find a collection of sets that covers and then analyze each covering set separately. We utilize the same covering scheme as in (Huber et al., 1967) which is originally developed to analyze the consistency of non-standard maximum likelihood estimators. The advantage of this covering scheme is that it provides a tighter probability bound than the traditional -covering scheme. The parameters involved in the proposition are dependent on the parameters in Assumption 1 and (c): and are specified in Assumption 1; and are specified in Assumption (c). For the newly introduced parameters, can be viewed as a constant parameter and is on the order of . All of these parameters are not dependent on the specific distribution and thus the result creates convenience for our later regret analysis of OLP algorithms. Importantly, both probability bounds in Proposition 3 and 4 have an exponential term of , and we utilize this fact to establish the convergence rate of as follows.

With Proposition 3 and 4, the identity (11) can be written heuristically as

| (13) |

with high probability, that is, (13) is violated with a probability decreasing exponentially in . Note that the right side in above is a quadratic function of . From the optimality of ,

| (14) |

By putting together (13) with (14) and then integrating with respect to , we can obtain the following theorem.

Theorem 1.

Theorem 1 states the convergence rate in terms of the L2 distance. The second inequality in the theorem can be directly implied from the first one, and here we present both inequalities for later usage. Also, to simplify the notations in the rest of the paper, we adopt the same constant for both inequalities without loss of generality. The theorem formally connects the dual LP and the stochastic program, by characterizing the distance between the optimal solutions of the two problems. As mentioned earlier, it resolves the open question of the convergence of dual optimal solutions in the OLP problem. The conclusion and the proof of the theorem are all based on finite-sample argument, in parallel with the classic stochastic programming literature where asymptotic results are derived (Shapiro, 1993; Shapiro et al., 2009). The finite-sample property is crucial in the regret analysis of the OLP algorithms. In the Theorem 2 of the next section, we will show how the regret of an OLP algorithm can be upper bounded by the L2 approximation error of This explains why we focus on the convergence and the approximation error of instead of the function value As for the convergence rate, recall that Assumption (c) (a) and (b) impose a curvature condition around the optimal solution . They are critical to the quadratic form (12) in Proposition 4 and consequently the convergence rate in Theorem 1. An alternative proof of the convergence results in Theorem 1 may also be obtained by using the notion of local Rademacher Complexity. Bartlett et al. (2005) proposed this local and empirical version of Rademacher complexity and employed the notion to derive the fast rate of estimator convergence. We remark that this possible alternative treatment also requires certain growth and smoothness condition around the optimal solution as Assumption (c) (a) and (b).

Now, we discuss some implications of Theorem 1 on the OLP problem. The theorem tells that the sequence of will converge to , and that when gets large, stays closer to . From an algorithmic perspective, an OLP algorithm can form an approximate for based on the observed inputs at each time . If is sufficiently large, the approximate dual price should be very close to both and Then, the algorithm can use (as an approximate to the optimal ) to decide the value of the current decision variable. This explains why OLP algorithms in literature always solve a scaled version of the offline LP (based on the observations available at time ). However, in the literature, due to the lack of convergence knowledge of the dual optimal solutions, papers devised other approaches to analyze the online objective value. Our convergence result explicitly characterizes the rate of the convergence and thus provides a powerful and natural instrument for the theoretical analysis of the online algorithms.

The dual convergence result also contributes to the literature of approximate algorithms for large-scale LPs. Specifically, we can perform one-time learning with the first inputs and then use as an approximation for . In this way, we obtain an approximate algorithm for solving the original LP problem by only accessing the first columns The approximate algorithm can be viewed as a constraint sampling procedure (De Farias and Van Roy, 2004; Lakshminarayanan et al., 2017) for the dual LP. It also complements the recent work (Vu et al., 2018) in which approximate algorithms for large-scale LP are developed under certain statistical assumptions on the coefficients of the LP problem.

4 Learning Algorithms for OLP

4.1 Dual-based Policy, Constraint Process, and Stopping Time

In this section, we present several online algorithms based on the dual convergence results. We first revisit the definition of online policies and narrow down our scope to a class of dual-based policies that rely on the dual solutions. Specifically, at each time , a vector is computed based on historical data

where . Inspired by the optimality condition of the offline/static LP, we attempt to set

In other words, a threshold is set by the dual price vector . If the reward is larger than the threshold, we intend to accept the order. Then, we check the constraints satisfaction and assign

We formally define policies with this structure as a dual-based policy. We emphasize that in this dual-based policy class, is first computed based on history (up to time ), and then is observed. This creates a natural conditional independence

This matches the setting in online convex optimization where at each time , the online player makes her decision before we observe the function (See (Hazan et al., 2016)). We will frequently resort to this conditional independence in the regret analysis. In this policy class, an online policy could be fully specified by the sequence of mappings ’s, i.e., To facilitate our analysis, we introduce the constraint process ,

In this way, represents the vector of remaining resources at the end of the -th period. In particular, represents the remaining resources at the end of the horizon. By the definition of OLP, for Also, the process of is pertaining to the policy . Based on the constraint process, we define

for In this way, denotes the first time that there are less than units for some type of constraints. Precisely, is a stopping time adapted to the process . Similar to the process , the stopping time is also pertaining to the policy When executing an online policy, we do not close the business at the first time that some constraints are violated. This is because we are considering double-sided problems that include both buying and selling orders. If a certain type of resource is exhausted, we may accept selling orders containing that resource as a way of replenishment. We will see that a careful design of the algorithm will ensure the constraint violation/resource depletion only happens at the very end. So, the decisions afterward will not affect the cumulative revenue significantly.

In the rest of this section, we first derive a generic upper bound for the regret of OLP algorithms and then present three OLP algorithms. These three algorithms all belong to the dual-based policy class, and their regret analyses all rely on the dual convergence and the generic upper bound. We restrict our attention to large- and small- setting, and the regret bounds will be presented with big-O notation which treats and the parameters in Assumption 1 and (c) as constants.

4.2 Upper Bound for OLP Regret

We first construct an upper bound for the offline optimal objective value. Consider the optimization problem

| (15) | ||||

| s.t. |

where the expectation is taken with respect to There are two ways to interpret this optimization problem. On one hand, we can interpret this problem as a “deterministic” relaxation of the primal LP (1). We substitute both the objective and constraints of (1) with an expectation form expressed in dual variable On the other hand, we can view this optimization problem as the primal problem of the stochastic program (7). The consideration of a deterministic form for an online decision making problem has appeared widely in the literature of network revenue management (Talluri and Van Ryzin, 1998; Jasin and Kumar, 2013; Bumpensanti and Wang, 2018), dynamic pricing (Besbes and Zeevi, 2009; Wang et al., 2014; Lei et al., 2014; Chen and Gallego, 2018), and bandits problem (Wu et al., 2015). The idea is that when analyzing the regret of an online algorithm in such problems, the offline optimal value usually does not have a tractable form (such as the primal LP problem (1)). The deterministic formulation serves as a tractable upper bound for the offline optimal value, and then the gap between the deterministic optimal and the online objective values is an upper bound for the regret of the online algorithm. Different from the literature, we consider the Lagrangian of the deterministic formulation to remove the constraints. Specifically, define

where the expectation is taken with respect to and is the optimal solution to the stochastic program (7). We can view as the Lagrangian of the optimization problem (15) with a specification of the multiplier by Lemma 3 establishes that the deterministic formulation indeed provides an upper bound for the offline optimal value and that the optimization problems (7) and (15) share the same optimal solution.

Lemma 3.

The presence of constraints makes the regret analysis challenging, because the way the constraints affect the objective value in an online setting is elusive and problem-dependent. The Lagrangian form resolves the issue by incorporating the constraints into the objective. Intuitively, it assigns a cost to the constraint consumption and thus unifies the two seemingly conflicting sides – revenue maximization and constraint satisfaction. The importance of Lemma 3 is two-fold. First, it provides a deterministic upper bound for the expected offline optimal objective value. The upper bound is not dependent on the realization of a specific OLP instance, so it is more convenient to analyze than the original offline optimal objective value. Second, a dual-based online algorithm employs a dual price at time and its instant reward at time can be approximated by . Then the single-step regret of the algorithm at time can be upper bounded with (16). Theorem 2 builds upon Lemma 3 and compares the online objective value against . A generic upper bound is developed for dual-based online policies. The upper bound consists of three components: (i) the cumulative “approximation” error, (ii) the remaining periods after the constraint is almost exhausted, and (iii) the remaining resources at the end of time period . The first component relates the regret with studied in the last section. It justifies why the dual convergence (Theorem 1) is studied in the last section. The second component concerns , where is defined in Assumption 1 and it is the maximal possible constraint consumption per period. The intuition for is that an order , if necessary, can always be fulfilled when Though selling order (with negative ’s) may still be accepted after , from the standpoint of deriving regret upper bound, we simply ignore all the orders that come after . The third component considers the constraint leftovers for binding constraints. Intuitively, binding constraints are the bottleneck for producing revenue, so wasting those resources at the end of the horizon will induce a cost.

Theorem 2.

Theorem 2 provides important insights for the design of an online policy. First, a dual-based policy should learn . Meanwhile, the online policy should have stable control of the resource/constraint consumption. Exhausting the constraints too early may result in a large value of the term while the remaining resources at the end of the horizon may also induce regret through the term . Essentially, both components stem from the fluctuation of the constraint consumption. The ideal case, although not possible due to the randomness, is that the -th constraint is consumed by exactly units in each time period. The following corollary states that the result in Theorem 2 holds for a general class of stopping times.

Corollary 1.

Remark. Theorem 2 and Corollary 1 reduce the derivation of regret upper bound to the analysis of approximation errors and the analysis of the constraint process. To highlight the usefulness of this reduction, we briefly discuss the existing techniques developed for analyzing online learning problems with the presence of constraints. The simplest approach is to propose a bi-objective performance measure: one for the objective value and one for the constraint violation. The bi-objective performance measure is adopted in the problem of online convex optimization with constraints (Mahdavi et al., 2012; Agrawal and Devanur, 2014b; Yu et al., 2017; Yuan and Lamperski, 2018). In these works, the regret for the objective value and the constraint violation are reported separately. Our results provide a method to convert the bi-objective results into one performance measure. When the upper bound on the constraint coefficients is known, one approach to combine the bi-objective performance measure is to penalize the excessive usage of the constraints, such as the regret analysis in (Ferreira et al., 2018). However, this approach only works for non-adaptive algorithms (like Algorithm 2) but fails when the constraint process affects the decision (like Algorithm 3 and other re-solving algorithms). In this light, Theorem 2 and Corollary 1 provide a unified treatment for non-adaptive and adaptive algorithms. Another approach to deal with the constraints is to use the “shrinkage” trick. The idea is to perform the online learning as if the constraint is shrunk by a factor of , and then the output online solution will be feasible with high probability for the original problem. This shrinkage trick is used in the OLP literature (Agrawal et al., 2014; Kesselheim et al., 2014) and also in the bandits with knapsacks problem (Agrawal and Devanur, 2014a). The downside of the shrinkage is that it will probably result in an over-conservative decision and may have too many remaining resources at the end of the horizon. The regret analysis closest to our approach is the analysis in (Jasin and Kumar, 2012; Jasin, 2015; Balseiro and Gur, 2019). The regret derivation therein also involves analyzing the stopping time related to the constraint depletion. Our generic upper bound can be viewed as a generalization of their analysis for the case when no prior knowledge on the support of ’s is available. For the network revenue management problem, the support of customer orders ’s is assumed to be finite and known. In this case, the offline optimal solution can be explicitly specified by the optimal quantity of each type of customer orders that should be accepted. Then the performance of an online algorithm can be analyzed by the deviation from the optimal quantity. In a general OLP problem, there is no explicit representation of the offline optimal solution. Theorem 2 and Corollary 1 resolve the issue by identifying the approximation error of as a non-parametric generalization of the deviation from the optimal quantity in the network revenue management context. A subsequent work (Lu et al., 2020) also applied similar ideas from Theorem 2 and Corollary 1 in their regret analysis for an online allocation problem which has a finite support of ’s.

4.3 When the Distribution is Known

We first present an algorithm for the situation when we know the distribution that generates the LP coefficients. With the knowledge of the stochastic programming problem (7) is well-specified. We study the algorithm mainly for benchmark purposes, so we do not discuss the practicability of knowing the distribution . Moreover, we assume that the stochastic programming problem (7) can be solved exactly. In Algorithm 1, the optimal solution is computed before the online procedure and can be viewed as prior knowledge. So, there is “no need to learn” the dual price throughout the procedure, and the pre-computed can be used for thresholding rule.

Theorem 3.

With the online policy specified by Algorithm 1,

Theorem 3 tells that the worst-case regret under an online policy with the knowledge of full distribution is . Recall the generic regret upper bound in Theorem 2, there is no approximation error for Algorithm 1 because is employed as the dual price. So the regret of Algorithm 1 stems only from the fluctuation of the constraint process. Intuitively, the fluctuation is on the order of when it approaches the end of the horizon. Our next algorithm and its according regret analysis show that the contribution of the approximation error of (when the distribution is unknown) is indeed dominated by the regret caused by the fluctuation of the constraint process.

4.4 Simplified Dynamic Learning Algorithm

Algorithm 2 approximates the dual price in Algorithm 1 by solving an SAA for the stochastic program based on the past observations. From the OLP perspective, it can be viewed as a simplified version of the dynamic learning algorithm in (Agrawal et al., 2014). In Algorithm 2, the dual price vector is updated only at geometric time intervals and it is computed based on solving the -sample approximation, i.e., minimizing . The key difference between this simplified algorithm and the dynamic learning algorithm in (Agrawal et al., 2014) is that we get rid of the shrinkage term in the constraints. Specifically, the algorithm in that paper considers on the right-hand side of the constraints in Step 6 of Algorithm 2. In the random input model, the shrinkage factor results in an over-estimated dual price and hence will be more conservative in accepting orders. The conservativeness is probably helpful under the random permutation model studied in (Agrawal et al., 2014) but may cause the remaining resources to be linear in under the random input model.

| s.t. | |||

Theorem 4.

With the online policy specified by Algorithm 2,

Theorem 4 tells that the policy incurs a worst-case regret of . Its proof relies on an analysis of the three components in the regret bound in Theorem 2. The summation can be analyzed by the dual convergence result. Specifically, the dual price in Algorithm 2 is computed based on a -sample approximation to the stochastic program (7), and therefore Theorem 1 can be employed to upper bound the distance . It reiterates the importance of studying the dual convergence and expressing the approximation error in L2 distance. The two components related to the stopping time and remaining resources are studied based on a careful analysis of the process . The detailed proof can be found in Section C2.

4.5 Action-History-Dependent Learning Algorithm

Now, we present our action-history-dependent learning algorithm. In Algorithm 2, the dual price is a function of the past inputs but it does not consider the past actions . In contrast, Algorithm 3 integrates the past actions into the constraints of the optimization problem of . At the beginning of period , the first inputs are observed. Algorithm 2 normalizes to for the right-hand-side of the LP, while Algorithm 3 normalizes the remaining resource for the right-hand-side of the LP (Step 6 of Algorithm 3). The intuition is that if we happen to consume too much resource in the past periods, the remaining resource will shrink, and Algorithm 3 will accordingly push up the dual price and be more inclined to reject an order. On the contrary, if we happen to reject a lot of orders at the beginning and it results in too much remaining resource, the algorithm will lower down the dual price so as to accept more orders in the future. This pendulum-like design in Algorithm 3 incorporates the past actions in computing dual prices indirectly through the remaining resources.

| s.t. | |||

From an algorithmic standpoint, Algorithm 3 implements the re-solving technique in a learning environment, while the idea was implemented in a known-parameter environment by (Reiman and Wang, 2008; Jasin and Kumar, 2012; Bumpensanti and Wang, 2018). Unlike the work (Jasin, 2015) which explicitly estimated the arrival intensity and fed the estimate into a certainty-equivalent problem, the learning part of Algorithm 3 is implicit and integrated into the optimization part. For the optimization problem in Step 6 of Algorithm 3, the left-hand-side is specified by the history, while the right-hand-side is specified by the real-time constraint capacity. If we define as the average remaining resource capacity, then the optimization problem at time can be viewed as a -sample approximation to a stochastic program specified by . Importantly, the targeted stochastic program at each time period is dynamically changing according to the constraint process, while Algorithm 2 and all the preceding analyses in this paper focus on a static stochastic program specified by the fixed initial . To apply the dual convergence result in a changing setting, we need a uniform version of Assumption (c). Specifically, for , define

and denote denotes its optimal solution. Assumption (c) shares the same part (a) with Assumption (c) and extends the part (b) and (c) of Assumption (c) to a uniform condition for all . Accordingly, we update the definition of to denote the family of distributions that satisfy Assumption 1 and (c); for this subsection, we consider the distribution within this updated

Assumption 3 (Uniform version of Assumption (c)).

We assume

-

(a)

The second-order moment matrix is positive-definite. Denote its minimum eigenvalue with

-

(b)

There exist constants and such that if ,

holds for any and .

-

(c)

The optimal solution satisfies if and only if for any .

Theorem 5 states that Algorithm 3 incurs a worst-case regret of . Technically, the proof builds upon an analysis of the three components of the generic upper bound in Theorem 2. A caveat is that the SAA problem and the underlying stochastic program in Algorithm 3 are dynamically changing over time. To analyze the algorithm, we identify a subset around the initial and show that (i) when Assumption 1 and (c) are satisfied, and more importantly, all the stochastic programs specified by share the same binding and non-binding dimensions; (ii) the process exits the region only at the very end of the horizon. Since the constraint process and are more complicated, we adopt a different approach than the proof of Theorem 4. The proof of the theorem and more discussions are deferred to Section C3.

Theorem 5.

With the online policy specified by Algorithm 3,

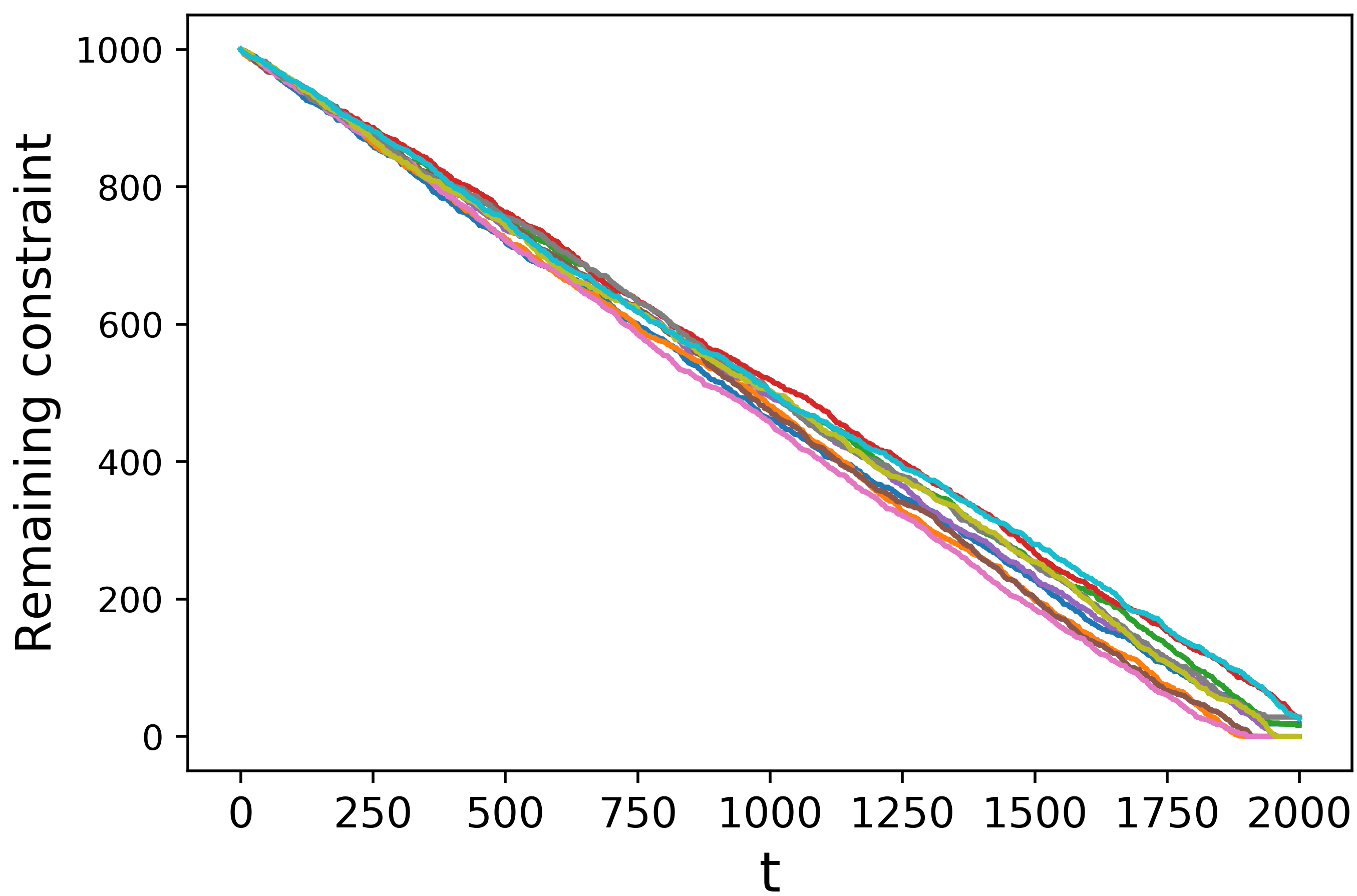

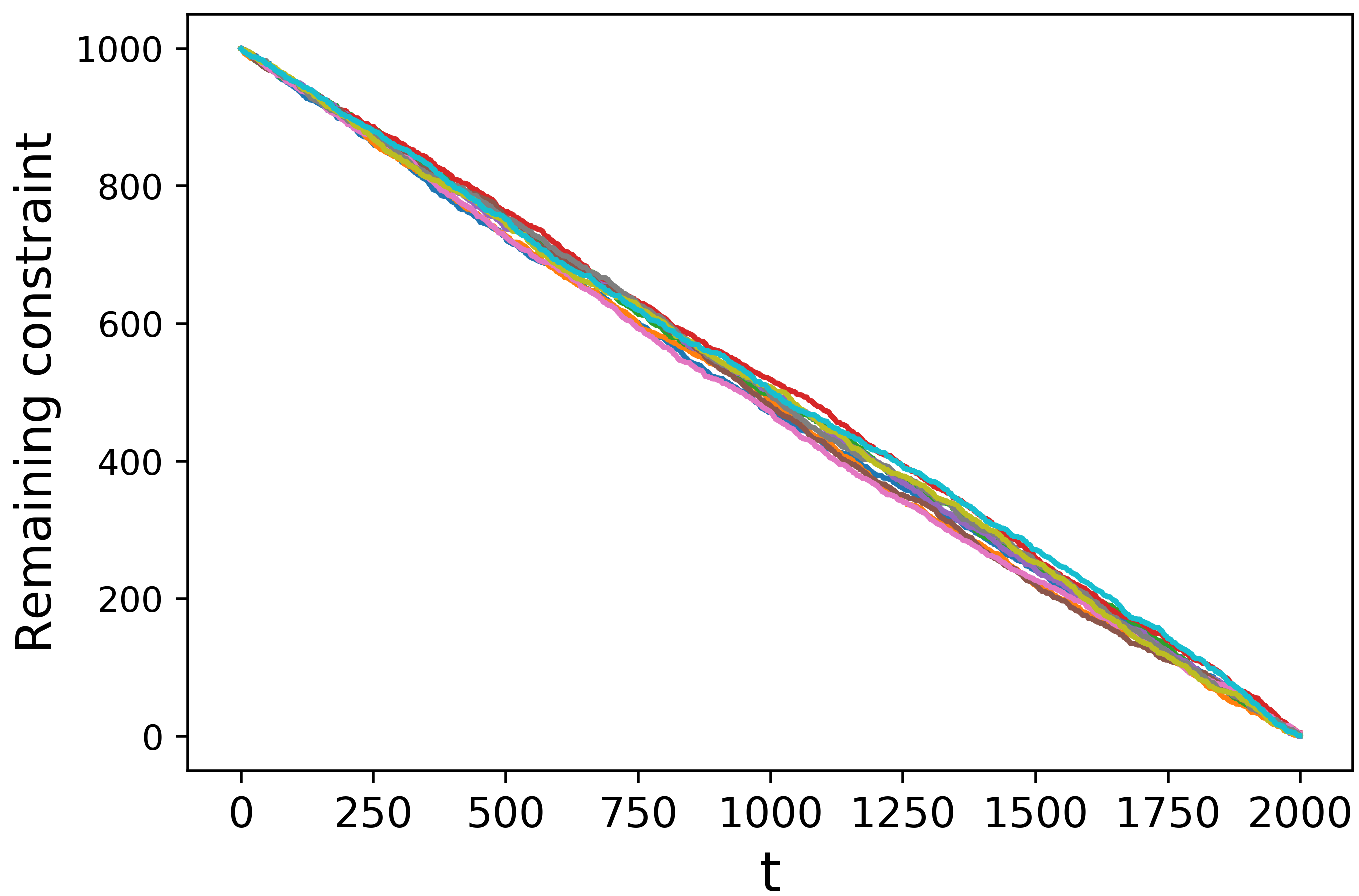

Figure 1 visualizes the constraint consumption under Algorithm 2 and Algorithm 3. We run simulation trials for each algorithm and plot the constraint consumption of a binding constraint from each random trial. The top two figures show that both algorithms seem to perform well in balancing the resource consumption: not to exhaust the constraint too early or to have too much leftover at the end. But if we zoom into the last 250 periods as the bottom two figures, the advantage of Algorithm 3 becomes significant. For Algorithm 2, some trials exhaust the constraint periods prior to the end, while some trials have an remaining at the end. Interestingly, for some curves (like the grey and green ones) in Figure 1(c), the remaining resource level stops decreasing periods prior to the end, though the remaining resource level is strictly positive. This is because some other constraint(s) has been exhausted at that time, and from that point on, we can not accept more orders even though there are still remaining resources for the plotted constraint. In comparison, the constraint consumption of Algorithm 3 is much more stable.

5 Experiments and Discussions

5.1 Numerical Experiments

We implement the three proposed algorithms on three different models, with model details given in Table 1. In the first model (Random Input I), the constraint coefficients ’s and objective coefficients ’s are i.i.d. generated as bounded random variables. All ’s are set to be . In the second model (Random Input II), the constraint coefficient is generated from a normal distribution, which violates the boundedness assumption. The assignment of is deterministic conditional of and thus violates Assumption (c) (b). Both and take negative values with a positive probability. In Random Input II, we set ’s alternatively to be and In the third model, we consider a random permutation model, the same as the worst-case example in (Agrawal et al., 2014). The number of decision variables is a random variable itself in this permutation model, so we specify its expectation to be and in the experiment.

| Model | ||

|---|---|---|

| Random Input I | and | |

| Random Input II | ||

| Permutation | (Agrawal et al., 2014) | |

Table 2 reports the estimated regrets of the three algorithms under different combinations of and The estimation is based on simulation trials and in each simulation trial, a problem instance (’s and ’s) is generated from the corresponding model. While solving the stochastic program in Algorithm 1, we use an SAA scheme with samples. We have the following observations based on the experiment results. First, Table 2 shows that Algorithm 3 performs uniformly better than Algorithm 1 and Algorithm 2. Importantly, Algorithm 3 also excels in the models of Random Input II and Permutation where the assumptions for theoretical analysis are violated. In particular, the random permutation problem instance is used in Agrawal et al. (2014) to establish the necessary condition on the constraint capacity and can thus be viewed as one of the most challenging OLP problems. As far as we know, Algorithm 3 is the first algorithm that employs the action-history-dependent mechanism in a generic OLP setting. In this regard, Algorithm 1 and Algorithm 2 stand for typical algorithms in OLP literature (Molinaro and Ravi, 2013; Agrawal et al., 2014; Gupta and Molinaro, 2014; Devanur et al., 2019), and the experiments demonstrate the effectiveness of the action-history-dependent design compared with these works. Besides, the advantage of Algorithm 3 becomes smaller as the ratio goes up. This can be explained by the fact that the dual convergence rate is of order and therefore a dual-based algorithm like Algorithm 3 would be more effective in a large- and small- regime.

| Model | Random Input I | Random Input II | Permutation | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Algorithm | A1 | A2 | A3 | A1 | A2 | A3 | A1 | A2 | A3 |

| m = 4, n = 100 | 28.17 | 37.68 | 27.14 | 11.75 | 23.85 | 5.29 | 33.17 | 37.62 | 7.42 |

| m = 4, n = 300 | 60.17 | 86.33 | 45.01 | 37.59 | 76.43 | 5.47 | 109.6 | 51.52 | 11.48 |

| m = 16, n = 100 | 30.21 | 45.16 | 27.59 | 93.34 | 81.02 | 52.69 | 24.96 | 21.96 | 12.88 |

| m = 16, n = 300 | 60.76 | 88.91 | 46.30 | 184.4 | 160.4 | 49.13 | 140.5 | 59.56 | 14.87 |

| m = 64, n = 100 | 36.84 | 40.52 | 34.77 | 493.2 | 461.7 | 414.5 | 37.70 | 20.31 | 15.97 |

| m = 64, n = 300 | 67.78 | 87.68 | 52.90 | 1017.6 | 881.9 | 611.1 | 145.9 | 47.22 | 18.76 |

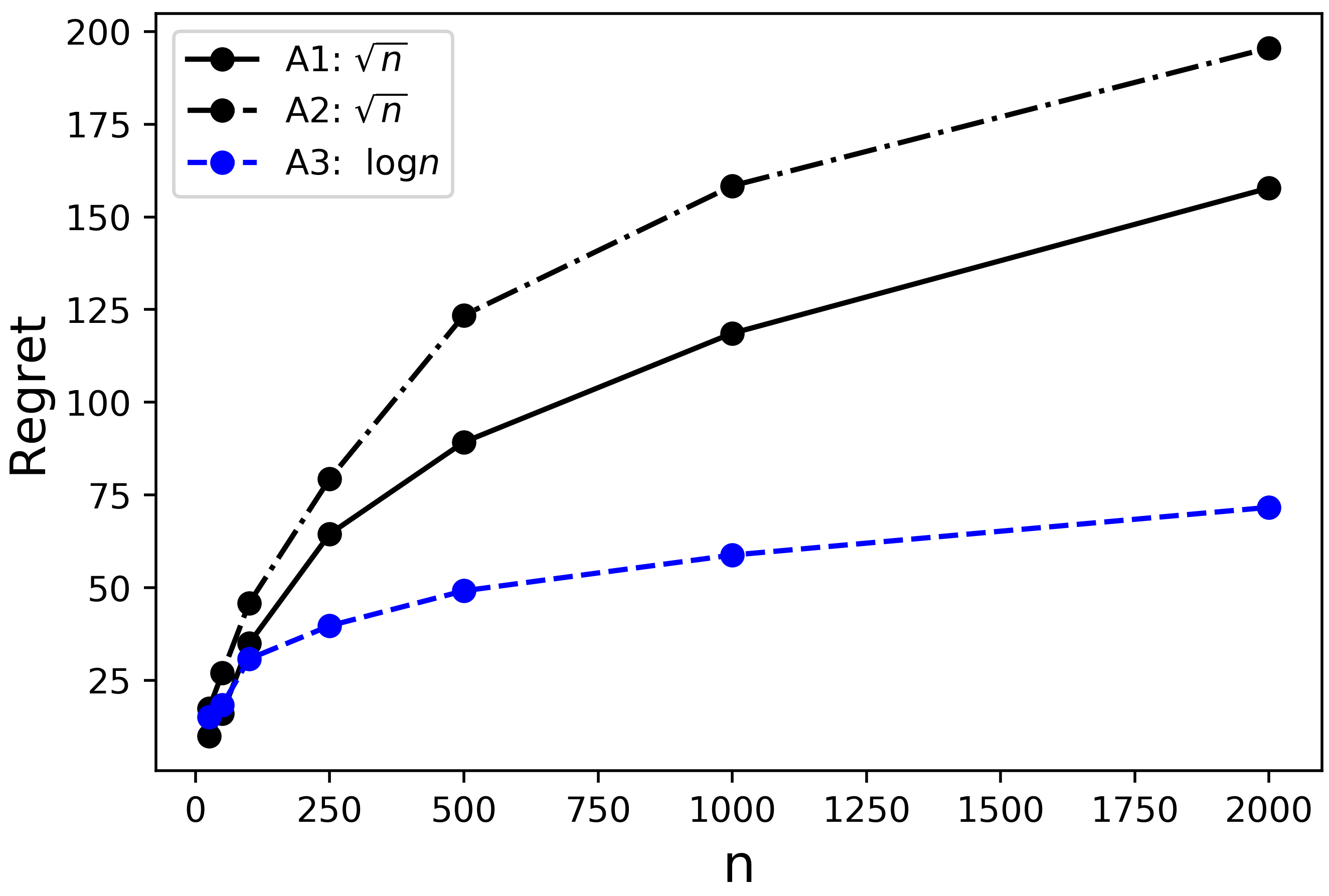

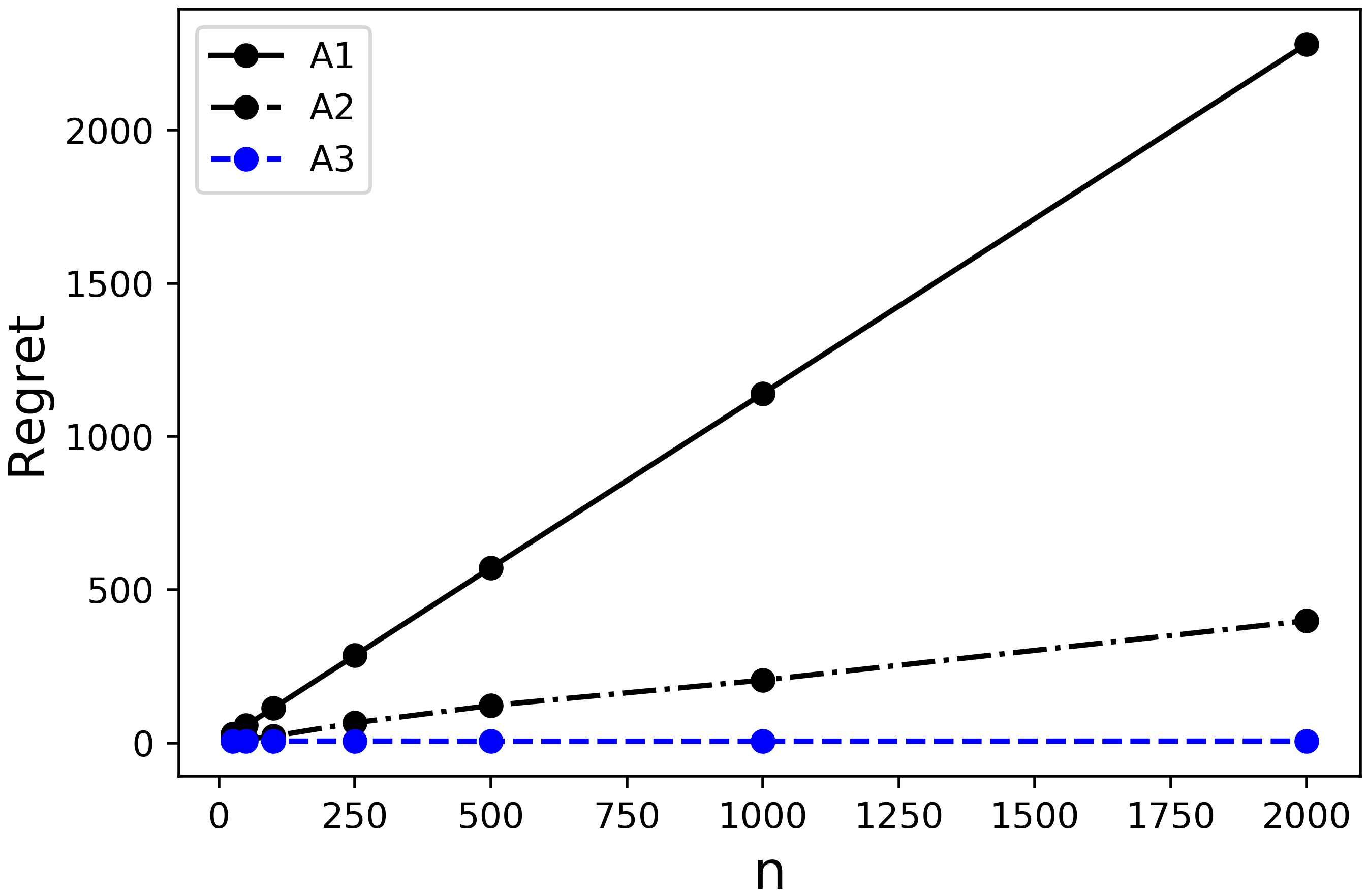

To illustrate how the regret scales with , we fix and run the experiments for different . The results are presented in Figure 2, where the curves are plotted by connecting the sample points. For the left panel, the curves verify the regret results in Theorem 3, 4 and 5. Meanwhile, the right panel looks interesting in that the regrets of Algorithm 1 and 2 scale linearly with while the regret of Algorithm 3 is (a horizontal line can be fitted). This phenomenon is potentially caused by the deterministic assignment of ’s in the Random Input II model.

In the numerical experiments (Figure 2 (a)), we observe empirically that the regrets for Algorithm 1 and for Algorithm 2 are both of order . This indicates that the geometric interval is already sufficient for Algorithm 2. In other words, the performance of Algorithm 2 cannot be further improved by simply increasing learning frequency. Furthermore, it means the consideration of past actions is necessary if we want to reduce the regret to . The same observation has been made for the network revenue management problem and thus motivates the study of the re-solving technique.

Table 3 reports numerical experiments based on the network revenue management problem (Jasin, 2015). The network revenue management problem therein can be formulated as an OLP problem by associating each arriving customer with a binary decision variable which denotes the decision of acceptance or rejection. The parameters in our experiment are the same as the numerical experiment in (Jasin, 2015): demand rate, deterministic price, itinerary structure, and flight capacity. We implemented the PAC (Probabilistic Allocation Control) algorithm in (Jasin, 2015) and the re-solving algorithm in (Jasin and Kumar, 2012). Two versions of the re-solving algorithm are implemented, one with the knowledge of true parameters (Re-solving (I)) and the other one with an imprecise parameter estimate (Re-solving (II)). Specifically, we perturb the arrival probability estimate by a magnitude of 0.005 for each customer type and re-normalize the perturbed probability. The imprecise estimate aims to capture the scenario that the decision maker has no access to the true parameters and can only calibrate the arrival probability through history data. Different re-solving frequencies and different horizons are tested for all four algorithms and the performance is reported based on an average over 200 simulation trials. Specifically, for the PAC algorithm, we set the initial learning period which means accepting all the customers when

| Algorithm 3 | PAC | Re-solving (I) | Re-solving (II) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Re-solving freq. | 2 | 10 | 2 | 10 | 2 | 10 | 2 | 10 | |

| Horizon | n = 200 | 63.73 | 64.83 | 123.49 | 168.32 | 60.04 | 84.61 | 62.59 | 87.34 |

| n = 400 | 82.67 | 92.01 | 141.32 | 183.14 | 121.62 | 129.68 | 131.29 | 140.52 | |

| n = 800 | 114.57 | 111.50 | 179.93 | 192.22 | 205.67 | 235.31 | 226.55 | 266.97 | |

| n = 1600 | 122.81 | 131.76 | 192.18 | 221.03 | 383.37 | 402.52 | 477.73 | 486.78 | |

Our action-history-dependent algorithm (Algorithm 3) has a better empirical performance than the other three algorithms. The result is a bit surprising in that the PAC algorithm can be viewed as a primal version of our action-history-dependent algorithm and it also has the adaptive design through re-solving and re-optimization. In addition, the Re-solving (I) algorithm even utilizes the knowledge of true parameter values. We believe the advantage of our algorithm is only up to a constant factor when is sufficiently large, and we provide two explanations for the observation. First, there are 41 different itinerary routes and 14 connecting flights () in this experiment. It means that the PAC algorithm needs to estimate 41 parameters, while Algorithm 3 only needs to estimate 14 parameters. Also, the nature of the problem may result in a smaller variance when estimating the optimal dual price. Specifically, the 41 parameters in the PAC algorithms are all probabilities and the average value is approximately 0.02. So the estimation suffers from the efficiency issues in the rare-event simulation (Asmussen and Glynn, 2007). In addition, the two-step procedure of the PAC algorithm feeds the estimation as input for an optimization problem and the optimization procedure may further amplify the estimation error. Second, all three re-solving algorithms are primal-based while our Algorithm 3 is dual-based. Note that the primal-based algorithms output a randomized allocation rule from the optimization procedure, and consequently this randomized rule induces more randomness when deciding the values of the primal variables. The additional randomness may cause more fluctuation of the constraint process. In contrast, our Algorithm 3 is dual-based and can thus be viewed as a smoother version of the three primal-based algorithms.

5.2 Lower Bound and Open Questions

Now, we present a lower bound result for the OLP problem for dual-based policies. Bray (2019) established that the worst-case regret of the multi-secretary problem is even with the knowledge of underlying distribution. We provide an alternative proof for the lower bound for two goals. First, the proof mimics the derivation of the lower bounds in (Keskin and Zeevi, 2014; Besbes and Muharremoglu, 2013) and the core part is based on van Trees inequality (Gill and Levit, 1995) – a Bayesian version of the Cramer-Rao bound. Thus, it extends the previous lower bound analysis from an unconstrained setting to a constrained setting. Second, recall that we develop a generic regret upper bound in Theorem 2. The lower bound proof shows that under certain conditions, the generic regret upper bound is rather tight. Intuitively, this indicates that an effective learning of and stable control of the constraint process are not only sufficient but also probably necessary to guarantee a sharp regret bound.

Theorem 6.

There exist constants and such that

holds for all and any dual-based policy

Based on the experiments and the theoretical results developed in this paper, we raise several open questions for future study. First, how does the regret depend on ? In the experiments of Random Input I, we observe that the regret increases but does not scale up much with . This is apparently not the case for Random Input II where the regret increases significantly as grows larger (See Section D6 for more experiments). A possible explanation is that the generation of ’s in Random Input II causes that scales with and consequently the offline optimal objective value scales linearly with A natural question then is what are the conditions that render the regret dependent on and in what way the regret depends on . Second, is it possible to relax the assumptions and extend the theoretical results for more general random input models and permutation models? We observe a good performance of Algorithm 3 when the assumptions are violated and even in the permutation model. For example, we observe an regret of Algorithm 3 in the experiment under Random Input II (Figure 2). Since the assumptions are violated, the lower bound does not hold in Random Input II. Also, it is an interesting question to ask if the dual convergence and the regret results still hold under the random permutation model. This question entails a proper definition of the stochastic program (7) in the permutation context. Third, in Assumption 1 (c), we require that the constraints scale linearly with . We have not answered the question of whether this linear growth rate is necessary for establishing the dual convergence results. In other words, how can the dual convergence and regret bounds be extended to a limited-resource regime? Besides, Algorithm 3 updates the dual price in every period. This raises the question if it is possible to have a less frequent updating/learning scheme but still to achieve the same order of regret. In the network revenue management setting where the distribution is known, Bumpensanti and Wang (2018) has shown the effectiveness of an infrequent updating scheme. The analysis therein highly relies on the finiteness of the distribution’s support as well as the knowledge of the distribution. We believe it is both interesting and challenging to derive a similar low-regret result with an infrequent updating scheme for the general OLP problem. The last question is on the type of regret bound: all the algorithm bounds we provide in this paper are on regret expectation. An interesting question is how a high-probability regret bound can be derived for the OLP problem (possibly with extra logarithmic terms). In fact, the results of dual convergence in our paper are probabilistic (as in Proposition 3 and 4), which may serve as a good starting point for deriving a high-probability regret bound.

Acknowledgment

We thank Yu Bai, Simai He, Peter W. Glynn, Daniel Russo, Zizhuo Wang, Zeyu Zheng, and seminar participants at Stanford AFTLab, NYU Stern, Columbia DRO, Chicago Booth, Imperial College Business School and ADSI summer school for helpful discussions and comments. We thank Chunlin Sun, Guanting Chen, and Zuguang Gao for proofreading the proof and Yufeng Zheng for assistance in the simulation experiments.

References

- Abernethy et al. (2008) Abernethy, Jacob, Peter L Bartlett, Alexander Rakhlin, Ambuj Tewari. 2008. Optimal strategies and minimax lower bounds for online convex games .

- Agrawal and Devanur (2014a) Agrawal, Shipra, Nikhil R Devanur. 2014a. Bandits with concave rewards and convex knapsacks. Proceedings of the fifteenth ACM conference on Economics and computation. 989–1006.

- Agrawal and Devanur (2014b) Agrawal, Shipra, Nikhil R Devanur. 2014b. Fast algorithms for online stochastic convex programming. Proceedings of the twenty-sixth annual ACM-SIAM symposium on Discrete algorithms. SIAM, 1405–1424.

- Agrawal et al. (2014) Agrawal, Shipra, Zizhuo Wang, Yinyu Ye. 2014. A dynamic near-optimal algorithm for online linear programming. Operations Research 62(4) 876–890.

- Arlotto and Gurvich (2019) Arlotto, Alessandro, Itai Gurvich. 2019. Uniformly bounded regret in the multisecretary problem. Stochastic Systems .

- Asadpour et al. (2019) Asadpour, Arash, Xuan Wang, Jiawei Zhang. 2019. Online resource allocation with limited flexibility. Management Science .

- Asmussen and Glynn (2007) Asmussen, Søren, Peter W Glynn. 2007. Stochastic simulation: algorithms and analysis, vol. 57. Springer Science & Business Media.

- Balseiro and Gur (2019) Balseiro, Santiago R, Yonatan Gur. 2019. Learning in repeated auctions with budgets: Regret minimization and equilibrium. Management Science 65(9) 3952–3968.

- Bartlett et al. (2005) Bartlett, Peter L, Olivier Bousquet, Shahar Mendelson, et al. 2005. Local rademacher complexities. The Annals of Statistics 33(4) 1497–1537.

- Besbes and Muharremoglu (2013) Besbes, Omar, Alp Muharremoglu. 2013. On implications of demand censoring in the newsvendor problem. Management Science 59(6) 1407–1424.

- Besbes and Zeevi (2009) Besbes, Omar, Assaf Zeevi. 2009. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research 57(6) 1407–1420.

- Borodin and El-Yaniv (2005) Borodin, Allan, Ran El-Yaniv. 2005. Online computation and competitive analysis. cambridge university press.

- Boucheron et al. (2013) Boucheron, Stéphane, Gábor Lugosi, Pascal Massart. 2013. Concentration inequalities: A nonasymptotic theory of independence. Oxford university press.

- Bray (2019) Bray, Robert L. 2019. Does the multisecretary problem always have bounded regret? arXiv preprint arXiv:1912.08917 .

- Buchbinder et al. (2007) Buchbinder, Niv, Kamal Jain, Joseph Seffi Naor. 2007. Online primal-dual algorithms for maximizing ad-auctions revenue. European Symposium on Algorithms. Springer, 253–264.

- Buchbinder and Naor (2009) Buchbinder, Niv, Joseph Naor. 2009. Online primal-dual algorithms for covering and packing. Mathematics of Operations Research 34(2) 270–286.

- Buchbinder et al. (2009) Buchbinder, Niv, Joseph Seffi Naor, et al. 2009. The design of competitive online algorithms via a primal–dual approach. Foundations and Trends® in Theoretical Computer Science 3(2–3) 93–263.

- Bumpensanti and Wang (2018) Bumpensanti, Pornpawee, He Wang. 2018. A re-solving heuristic with uniformly bounded loss for network revenue management. arXiv preprint arXiv:1802.06192 .

- Chen and Gallego (2018) Chen, Ningyuan, Guillermo Gallego. 2018. A primal-dual learning algorithm for personalized dynamic pricing with an inventory constraint. Available at SSRN .

- De Farias and Van Roy (2004) De Farias, Daniela Pucci, Benjamin Van Roy. 2004. On constraint sampling in the linear programming approach to approximate dynamic programming. Mathematics of operations research 29(3) 462–478.

- Devanur and Hayes (2009) Devanur, Nikhil R, Thomas P Hayes. 2009. The adwords problem: online keyword matching with budgeted bidders under random permutations. Proceedings of the 10th ACM conference on Electronic commerce. ACM, 71–78.

- Devanur et al. (2011) Devanur, Nikhil R, Kamal Jain, Balasubramanian Sivan, Christopher A Wilkens. 2011. Near optimal online algorithms and fast approximation algorithms for resource allocation problems. Proceedings of the 12th ACM conference on Electronic commerce. ACM, 29–38.

- Devanur et al. (2019) Devanur, Nikhil R, Kamal Jain, Balasubramanian Sivan, Christopher A Wilkens. 2019. Near optimal online algorithms and fast approximation algorithms for resource allocation problems. Journal of the ACM (JACM) 66(1) 7.

- Ferreira et al. (2018) Ferreira, Kris Johnson, David Simchi-Levi, He Wang. 2018. Online network revenue management using thompson sampling. Operations research 66(6) 1586–1602.

- Gill and Levit (1995) Gill, Richard D, Boris Y Levit. 1995. Applications of the van trees inequality: a bayesian cramér-rao bound. Bernoulli 1(1-2) 59–79.

- Goel and Mehta (2008) Goel, Gagan, Aranyak Mehta. 2008. Online budgeted matching in random input models with applications to adwords. Proceedings of the nineteenth annual ACM-SIAM symposium on Discrete algorithms. Society for Industrial and Applied Mathematics, 982–991.

- Gupta and Molinaro (2014) Gupta, Anupam, Marco Molinaro. 2014. How experts can solve lps online. European Symposium on Algorithms. Springer, 517–529.

- Hazan et al. (2016) Hazan, Elad, et al. 2016. Introduction to online convex optimization. Foundations and Trends® in Optimization 2(3-4) 157–325.

- Huber et al. (1967) Huber, Peter J, et al. 1967. The behavior of maximum likelihood estimates under nonstandard conditions.

- Jasin (2015) Jasin, Stefanus. 2015. Performance of an lp-based control for revenue management with unknown demand parameters. Operations Research 63(4) 909–915.

- Jasin and Kumar (2012) Jasin, Stefanus, Sunil Kumar. 2012. A re-solving heuristic with bounded revenue loss for network revenue management with customer choice. Mathematics of Operations Research 37(2) 313–345.

- Jasin and Kumar (2013) Jasin, Stefanus, Sunil Kumar. 2013. Analysis of deterministic lp-based booking limit and bid price controls for revenue management. Operations Research 61(6) 1312–1320.

- Keskin and Zeevi (2014) Keskin, N Bora, Assaf Zeevi. 2014. Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies. Operations Research 62(5) 1142–1167.