Transforming Gaussian correlations. Applications to generating long-range power-law correlated time series with arbitrary distribution

Abstract

The observable outputs of many complex dynamical systems consist in time series exhibiting autocorrelation functions of great diversity of behaviors, including long-range power-law autocorrelation functions, as a signature of interactions operating at many temporal or spatial scales. Often, numerical algorithms able to generate correlated noises reproducing the properties of real time series are used to study and characterize such systems. Typically, those algorithms produce Gaussian time series. However, real, experimentally observed time series are often non-Gaussian, and may follow distributions with a diversity of behaviors concerning the support, the symmetry or the tail properties. Given a correlated Gaussian time series, it is always possible to transform it into a time series with a different distribution, but the question is how this transformation affects the behavior of the autocorrelation function. Here, we study analytically and numerically how the Pearson’s correlation of two Gaussian variables changes when the variables are transformed to follow a different destination distribution. Specifically, we consider bounded and unbounded distributions, symmetric and non-symmetric distributions, and distributions with different tail properties, from decays faster than exponential to heavy tail cases including power-laws, and we find how these properties affect the correlation of the final variables. We extend these results to Gaussian time series which are transformed to have a different marginal distribution, and show how the autocorrelation function of the final non-Gaussian time series depends on the Gaussian correlations and on the final marginal distribution. As an application of our results, we propose how to generalize standard algorithms producing Gaussian power-law correlated time series in order to create synthetic time series with arbitrary distribution and controlled power-law correlations. Finally, we show a practical example of this algorithm by generating time series mimicking the marginal distribution and the power-law tail of the autocorrelation function of a real time series: the absolute returns of stock prices.

I Introduction

The observable outputs of a great diversity of dynamical systems consist in correlated time series, and the corresponding autocorrelation functions may have many different functional forms, characterizing the underlying dynamics which is tipically not explicitly known. For example, when the dynamics presents a characteristic time (or scale), exponentially decreasing autocorrelations functions are found. Also, when dealing with complex systems with interactions working at many time or spacial scales, then very often one finds time series with long-range, power-law decaying autocorrelation functions. Such time series can be found, for example, in Physiology (heartbeat dynamics Peng93 , brain activity correlations_brain , respiration respiration , postural control postural_control ; maite ), Biology (DNA and protein sequences) Peng_1992 ; voss_dna_1992 , Economics (stock market activity) economy , Music voss_music , Meteorology (temperature or rain precipitation) meteo ; geo01 , Geophysics (seismic signals seismic ), and many other fields. Although there exist other measures of dependence between variables, the analysis of the linear correlations as measured by the autocorrelation function is important since, in many cases only the linear correlations are considered to quantify the complexity and the scaling properties of natural time series, e.g. heart-rate variability heart-rate-review2006 or financial time series financial-wavelets2001 .

Indeed, no matter the functional form of the autocorrelation function of the observable time series, a common approach to study and characterize the underlying dynamical system is often based on numerical algorithms able to generate surrogate signals replicating the correlation properties of the real time series. For example, autoregressive processes of order 1 (AR(1)) are able to produce time series with exponentially decreasing correlations. As another example, the Fourier Filtering method (FFM) FFM1 ; FFM2 is probably the most successful algorithm able to produce power-law correlated time series. Other techniques are able to generate surrogate signals with the same autocorrelation function as the experimental time series: they obtain the power spectrum of the real signal, and modify the Fourier phases without altering the power spectrum values (see theiler and later generalizations schreiber ; kugiumtzis ; keylock , and applications, for instance, to climatic records halley ). When the signal is Fourier-transformed back into time domain, the autocorrelation function is identical to that of the real signal due to the Wiener-Khinchin theorem.

However, most of such algorithms produce Gaussian time series. In contrast, the marginal probability distribution of real-world correlated time series are often non-Gaussian Peng93 : Indeed, the distributions can exhibit very different behaviors, concerning the support (bounded or unbounded), the symmetry (symmetric or not) or the tail behavior (exponential decay, faster than exponential, heavy tail, etc). As a consequence, once the Gaussian output of any given algorithm is available, a final transformation is required to change the Gaussian distribution to the desired final marginal distribution of the experimental time series. Nevertheless, this last transformation always modifies the autocorrelation function of the Gaussian time series (identical to that of the real time series), so that the final time series follows the same marginal distribution as the real one but with a different autocorrelation function. Although this drawback may be reduced by iterative procedures (as the one in schreiber ), the difference between both the Gaussian and the final autocorrelation functions can be specially dramatic when the final marginal distribution is far from Gaussian.

Formally speaking, let us consider a Gaussian time series , , with an autocorrelation function given by:

| (1) |

where and are the mean and the variance of the Gaussian distribution respectively, and the subscript refers to Gaussian distribution from now on. Without loss of generality, the time series can be normalized to have 0 mean and unit standard deviation, so that , and then . In this case, the corresponding probability density and cumulative distribution are given by:

| (2) |

with the standard error function.

We note that can be transformed into a time series following any arbitrary destination marginal distribution characterized by a probability density and a cumulative distribution by using the standard technique of the inverse cumulative distribution numrec :

| (3) |

with the inverse cumulative distribution of the destination distribution. It is well known that strictly increasing transformations like (3), when applied to a pair of random variables such as and , do not modify the dependence between them copulas99 and therefore the corresponding values of the final time series, and , preserve their statistical dependence as measured by rank statistics like Kendall’s and Spearman’s copulas99 , or by Information Theory functionals like mutual information mi90 . Nevertheless, the transformation (3) does not preserve the linear correlations, as measured by the autocorrelation function. The autocorrelation of the original Gaussian series is (1), and after the transformation, the autocorrelation function of the final time series is defined as

| (4) |

with and the mean and variance of the arbitrary destination probability density . The transformation changes the correlations, so that , and in general, the behavior of depends on the final marginal distribution.

In this work, we study how the autocorrelation function of a given Gaussian time series changes when the marginal distribution is modified from Gaussian to the desired final distribution. This problem has been intensively investigated in several contexts theiler ; schreiber ; kugiumtzis ; keylock ; halley ; li75 ; chen01 ; kugi10 ; cario , but we focus here on how depends on for a diversity of destination probability distributions with fundamentally different statistical properties (support, symmetry and tail behavior), in order to find out which properties of the final distribution control the behavior of , and the differences between and .

In addition, we also study under which conditions the asymptotic properties of (for large ) are preserved after the transformation (3), so that exhibits the same asymptotic behavior as . This is of special relevance when studying time series with fractal, long-range power-law decaying autocorrelation functions, that appear ubiquitously in many complex dynamical systems Peng93 ; correlations_brain ; respiration ; postural_control ; maite ; Peng_1992 ; voss_dna_1992 ; economy ; voss_music ; meteo ; geo01 ; seismic as we mentioned above, and that are typically non-Gaussian. Note that the FFM algorithm FFM1 ; FFM2 produces Gaussian time series with controlled, power-law behaved . When the transformation (3) preserves the asymptotic behavior of , we can generalize the FFM algorithm to produce time series with arbitrary distribution and with autocorrelation function with the same controlled power-law behavior.

The paper is organized as follows: In Sec. II we consider two Gaussian variables with a linear correlation value given by , and we transform them using (3) into two non-Gaussian variables with arbitrary marginal distribution and with linear correlation given by , and obtain some general properties of the function. The specific results of the function for several destination distributions with different statistical properties are shown in Sec. III. The extension of these results to time series is addressed in Sec. IV, where we also include two applications: 1) A generalization of the FFM algorithm able to synthesize generic power-law correlated time series with arbitrary marginal distribution; and 2) a practical example where we generate a time series mimicking the distribution and the power-law tail of the autocorrelation function of a real-world power-law correlated time series: the absolute returns of the stock price of a technological company. Finally, in Sec. V we present our conclusions.

II Transforming Gaussian correlations

Let us consider a generic Gaussian time series , and without loss of generality, let us also assume that , so that the corresponding probability density and cumulative distribution are given in Eq. (2).

For the sake of simplicity, in this section we work with the pair of variables and defined respectively as and (i.e. we omit the dependence), and therefore the linear correlation between and is given by , i.e. . Similarly, given a destination marginal distribution characterized by a probability density and cumulative distribution , we use the transformation (3) to obtain the final variables and given by

| (5) |

or, in other words, we also define and . The linear correlation between these two variables is then

| (6) |

with and the mean and variance of destination marginal distribution.

The natural question is how depends on the Gaussian correlation , , or, in other words, how the correlation changes when the distributions change from Gaussian to an arbitrary destination probability density . Obviously, will depend on the specific properties of . In this work, we have investigated several destination probability distributions which have been selected to reflect different fundamental statistical properties: (i) We have considered distributions with bounded and unbounded support; (ii) For the unbounded support case, we study examples of distributions with different tail behavior ranging from faster than exponential to heavy tail cases including power-law tail behavior; and (iii), we have also considered symmetric and non-symmetric probability distributions. In this context, symmetric means that there exists a ’central point’ such that , from where it is easy to obtain that corresponds to the median and the mean of the distribution. For convenience, in Table I we show separately symmetric and non-symmetric distributions because, as we will see later, both groups exhibit different behavior.

| Symmetric distributions | ||||||

| name | support | , | ||||

| uniform | ||||||

| arcsine | ||||||

| logistic | ||||||

| Laplace | ||||||

|

||||||

| Non-symmetric distributions | ||||||

| name | support | , | ||||

| exponential | , | |||||

| Weibull | ||||||

| lognormal | ||||||

| Pareto | , | |||||

The problem of determining how depends on can be tackled as follows: First, we recall that the correlation between the Gaussian variables and is purely linear, and this is equivalent to affirm that the joint probability density of the pair is the bivariate Gaussian distribution, , given by:

| (7) |

Second, given the destination probability density , the corresponding and in (6) are known. Then, the problem of calculating is reduced to obtaining . As and depend functionally on and respectively (Eq. 5), and as the joint probability density of and is (Eq. (7)) then

| (8) |

where we have written explicitly the dependence of on . The integral in (8) does not admit an analytical solution in general (except in two cases, discussed below). Therefore, it has to be solved numerically, and after introducing in Eq. (6), the final result is obtained. A similar approach to the to the one we have presented above and the numerical solution of the integral in Eq. (8) was firstly considered in li75 when addressing the problem of generating random numbers with specific marginal distribution and prescribed correlations, later extended to -dimensional vectors chen01 . Also, parametric solutions of the integral in Eq. (8) has been proposed kugi10 .

However, even without solving the integral in Eq. (8), some important properties of can be inferred:

-

(i)

The transformation (5) maps uncorrelated Gaussian variables into uncorrelated variables. Note that when the Gaussian variables are uncorrelated, , then their joint probability distribution factorizes, . As a consequence, the double integral factorizes in the product of two identical integrals each one giving , the mean of the destination distribution, and then . By inserting in Eq. (6) we get .

-

(ii)

If , then . Also, if then . This fact is inherited from the properties of : let and be two non-decreasing functions of the Gaussian variables and with joint distribution . Then, the covariance is positive for and negative for joint . Considering and , since by construction is a non-decreasing function, the property holds.

- (iii)

-

(iv)

For symmetric destination marginal distributions is and odd function. In general, the transformation (and similarly for ) converts trivially the median of the Gaussian density into the median of since by definition and . When is symmetric, then and without loss of generality we can fix them to 0, i.e. as it happens with for which . Let us consider a given value such that . Then, for some , and then . Therefore, a positive is transformed into a positive . Similarly, if we consider , then for some , and therefore , thus implying that a negative is transformed into a negative . Finally, if we take and and transform both, since is symmetric then and both with the same . But since is also symmetric, if then . Altogether, we get that if is transformed into then is transformed into , or formally speaking is an odd function. Now, consider the integral in Eq. (8) giving , and let us try to calculate , i.e. we invert the sign of the Gaussian correlation. But due to the form of , we note that , and as we have just shown that , from Eq. (8) we get that . Since is symmetric with fixed , we finally obtain that

(9) -

(v)

The function maps the interval into with . Note that implies that the Gaussian variables and are identical, . Then, they are transformed to identical non-Gaussian variables, so that . The result for , i.e., with is proved in Sec. II.1. The equality holds for symmetric marginal distributions since , while in general for non-symmetric marginal distributions .

II.1 Series expansion and approximate solution

As we have stated above, the 2D integral in Eq. (8) does not admit an analytical solution in general. Then, given a destination density , one has to solve it numerically for any value of . However, the 2D integral can be approximated by using a Taylor expansion in terms of , which will be of interest in Sec. IV. Then, we can write

| (10) |

where we have used that , and

| (11) |

It is not difficult to check that when evaluating the partial derivatives of at then the result factorizes in terms of the one-variable Gaussian densities and :

| (12) |

Therefore, the 2D integral in Eq. (11) is given by the product of two 1D identical integrals on and or

| (13) |

and, using the properties of the derivatives of the Gaussian density ,

| (14) |

with the -th order Hermite’s polynomial. Then, we finally get

| (15) |

After inserting the final expression for (11) into Eq. (10), then by introducing into Eq. (6) we finally obtain

| (16) |

with

| (17) |

Then, any coefficient is obtained in general by solving numerically a 1D integral. From the computational point of view, it may be interesting to consider terms in the expansion (16) as an approximation to thus solving 1D integrals instead of the 2D integral in Eq. (8). In addition, the expansion coefficients present some convenient properties:

- (i)

-

(ii)

The extreme value corresponds to the case since both stochastic variables are of type. Therefore, when we transform and we obtain thus implying that as we have shown above, and from Eq. (16) we get

(19) Then, each coefficient corresponds to a normalized weight characterizing the contribution of the -th term in the expansion (16). In this sense, the first coefficient is a measure of the linearity of the function and will be important in Sec. IV.1.

-

(iii)

As we have shown above, when the probability density of the stochastic variables and is symmetric, then is an odd function (Eq. (9)). In such case, for even and only the odd terms are present in the expansion of Eq. (16):

(20) Since for symmetric distributions , for sufficiently small values is essentially linear, with profound implications in the generation of power-law correlated time series as we see in Sec. IV.1.

-

(v)

We can use the previous properties to prove that with . We already know that since negative Gaussian correlations are mapped into negative correlations. In addition, from (16) we get

(21) thus completing the prove. Also, the equality is valid only if , so that the expansion (16) only contains odd terms, as in (20). This implies that is an odd function, and therefore the final marginal distribution must be symmetric. Altogether, for symmetric distributions, and for non-symmetric ones.

In addition to these general properties, the results of the specific behavior of the function for the distributions shown in Table I are discussed in the next section.

III Results for several distributions

After analyzing the general properties of , in this section we present the specific results of for the symmetric and non-symmetric distributions in Table I. Apart from the symmetry, the criteria we have followed for selecting these examples are varied: First, we have tried to consider distributions found in real data with different fundamental properties such as the support (bounded or unbounded) and, for the unbounded cases, the behavior of the tail of the distribution (exponential, faster decay than exponential and heavy-tail cases). In addition, all the selected examples present an inverse cumulative distribution that can be written explicitly in terms of elementary functions with the single exception of the lognormal distribution. However, for this latter case the function can be calculated analytically.

Prior to present the results, we note that the correlation given in Eq. (6) can be also expressed in terms of the standardized variables and (with zero mean and unit standard deviation) defined by

| (22) |

with and the corresponding mean and standard deviation of the probability density (and ). Indeed, starting from Eq. (6) we can write

| (23) |

As a consequence, given any of the distributions in Table I and for any choice of the corresponding distribution parameters, the function can be calculated simply as . Therefore, using and , is given directly by Eq.(8) but where the inverse cumulative distribution has to be obtained from the standardized cumulative distribution (and ). Similarly, when using and , the Taylor expansions given in Sec. II.1 have to be calculated using the inverse of and, in addition, the expansion coefficients defined in Eq. (17) are identical to the coefficients in Eq. (11) since .

In Table II we present the standardized obtained from the cumulative distributions shown in Table I using the change of variable , with and the mean and standard deviation of . Note that the standardized probability densities can be obtained simply as .

We note that in the case of the distributions in Table I with only location and scale parameters (the cases of uniform, arcsine, logistic, Laplace and exponential distributions), the standardized distributions in Table II do not depend on any parameter and are therefore unique. This fact implies that for these distributions, no matter the choice of the parameters in the corresponding distributions in Table I, the function is also unique. However, for distributions which in addition depend on a shape parameter (as the cases of symmetric Pareto, Weibull, lognormal and Pareto) the corresponding depends also on the shape parameter and therefore is not unique but a family of distributions. Consequently, the function is not unique either, and depend on the particular value of the shape parameter.

| name | support | |||

|---|---|---|---|---|

| Uniform | ||||

| arcsine | ||||

| logistic | ||||

| Laplace | ||||

| symmetric Pareto | , | |||

| exponential | ||||

| Weibull |

|

|||

| lognormal | , | |||

| Pareto | , |

In the following, we present the results of the behavior of for the distributions in Tables I and II. For convenience, we separate the results corresponding to symmetric and non-symmetric distributions.

III.1 Symmetric distributions

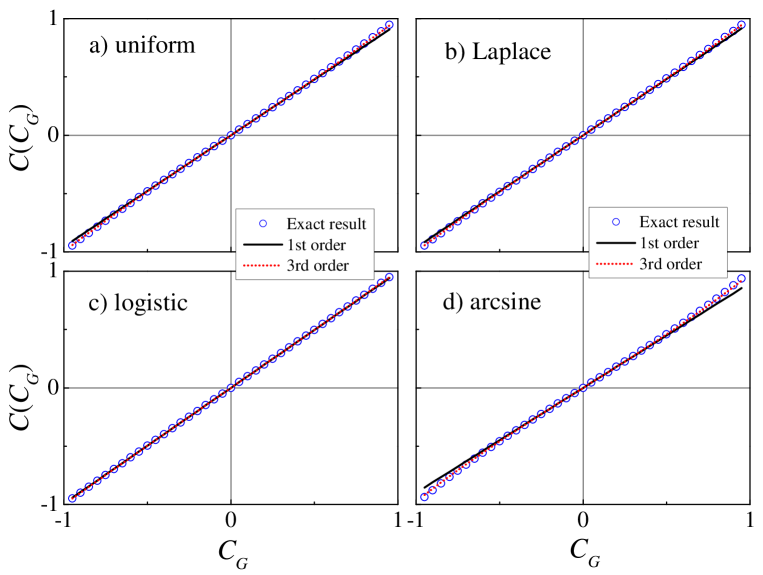

III.1.1 Uniform distribution

The uniform distribution is one of the few cases for which the function can be obtained analytically. Since the standardized distribution is unique in this case (see Table II), the same happens with the function and then it can be obtained using either (Table II) or with any choice of the parameters and (Table I). For simplicity, we use this latter option: we start with the uniform distribution defined in the interval so that for and otherwise, i.e. with and . This case is particularly simple since and are the identity function, and then the integral in Eq. (8) can be simplified as:

| (24) |

with (and ) the cumulative Gaussian distribution which is given in terms of the error function (Eq. (2)). Using the properties of the integrals of the error function erf and usual integration techniques, the integral in (24) can be solved to obtain

| (25) |

By introducing this result into the definition of in Eq. (6), and noting that for the uniform distribution in the interval and we finally get:

| (26) |

This function is shown in Fig 1a). As expected from the general properties deduced in the previous section, we have that and, since the uniform distribution is symmetric then . Also, by expanding in a Taylor series, only the odd terms are present. For the first term we have thus indicating a strong linearity of in this case, confirmed also by the small values of the coefficients and presented in Table III. The results of the expansion of up to first and third order are also shown in Fig 1a).

III.1.2 Logistic, Laplace and arcsine distributions

The three distributions, apart from being symmetric, share also another property: they lack a shape parameter. As a consequence, the corresponding does not have any parameter and is therefore unique in the three cases (Table II), so that each distribution presents a single function.

For the three distributions, there is no analytical solution of the integral in Eq. (8) which has to be solved numerically and used in Eq. (6). The exact numerical results of the function for the three cases are shown in Fig. 1b), c) and d) (symbols). As expected, since the three distributions are symmetric, is and odd function in all cases, and therefore the corresponding Taylor expansion given by Eq. (20) includes only odd terms. Indeed, we also show in Fig. 1 the results of the corresponding expansions up to first and third order. We note that the function is almost linear in the three cases and the deviation from the linear behavior only occurs for extreme values of . Specifically, this deviation is slightly larger for the arcsine distribution but almost visually undetectable for the Laplace and specially for the logistic case. To quantify this almost-linear behavior, we present in Table 3 the numerical results of the first three expansion coefficients , and . We recall that the coefficient quantify the weight of the -th term in the expansion, and then obviously the linear term is by far the one with the largest contribution: in all cases . For the extremely linear case of the logistic distribution, and then .

| distribution | |||

|---|---|---|---|

| uniform | |||

| logistic | |||

| Laplace | |||

| arcsine |

In general, we note that the four symmetric distributions (including the uniform) present similar results, with a quite linear behavior of since the corresponding expansion coefficient is the dominant one. This, together with the fact that for symmetric distributions only the odd expansion coefficients are nonzero, allows us to write or, in other words, the expression is essentially correct in general for small and moderate values since, in addition, in all cases. This result will prove to be important in Sec. IV.1, where the generation of power-law correlated time series with arbitrary distribution is discussed.

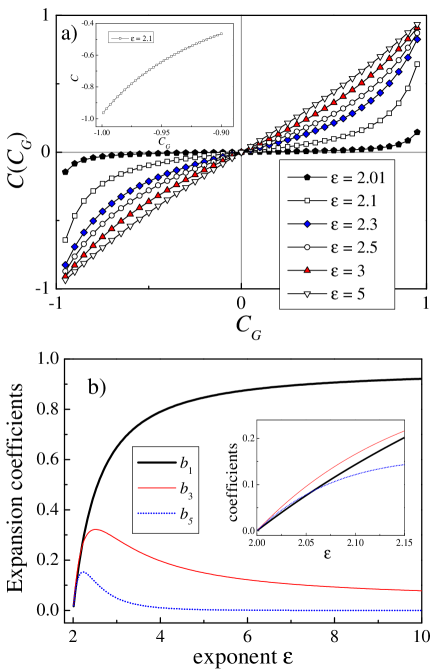

III.1.3 Symmetric Pareto distribution

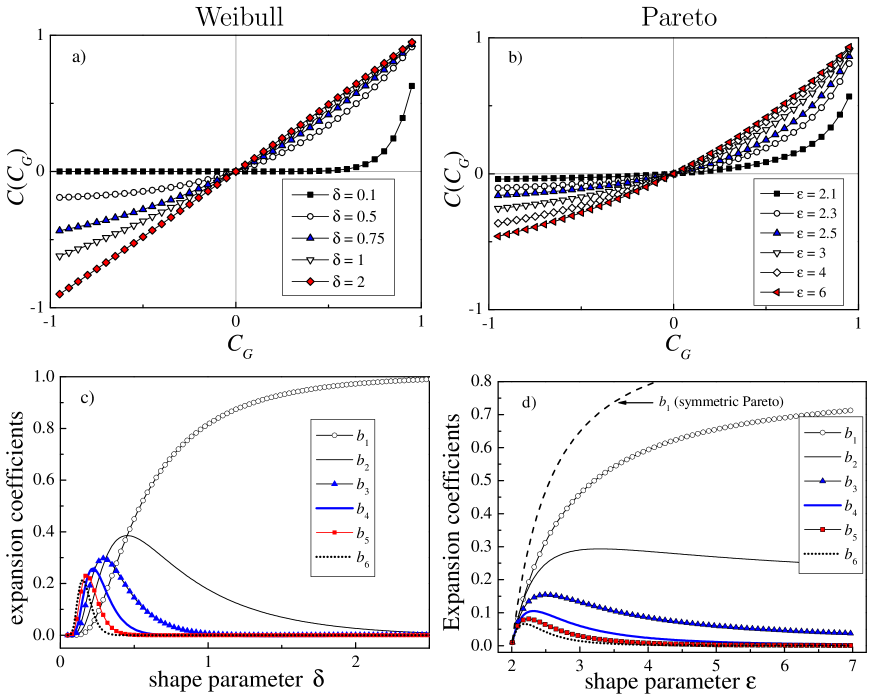

For this distribution the function has to be obtained numerically since there is no analytical solution of the integral in Eq. (8). The distribution is symmetric, so that is odd. However, is not unique since the distribution depends on three parameters (Table I): The location parameter and the scale parameter (positive), and also the shape parameter , restricted to values in order to have finite variance. Then, the corresponding is actually a family of distributions in terms of the shape parameter (see Table II), which controls the power-law tail of the distribution since asymptotically . Correspondingly, there is a family of functions depending on the value.

In Fig. 2a) we show some functions obtained numerically for different values of . As expected, we first note that all the functions are odd due to the symmetry of the probability density. And second, we also find that the linearity of the function decreases as the value becomes smaller: while for large values (fast-decaying power-law tail) behaves quite linearly, as decreases (longer power-law tail) and approaches the limiting value , the function becomes smaller and more nonlinear, flattens and eventually tends to 0 as . This effect can be quantified by calculating the expansion coefficients in Eq. (20), which account for the weights of the successive expansion terms. In Fig. 2b) we plot the first non-zero expansion coefficients (, and ) obtained numerically from Eq. (17). We note that for large values, is the largest coefficient and close to one, confirming the strong linearity of in this range. However, for smaller values, we observe that all the expansions coefficients tend to zero as (see also the inset in Fig. 2b)), in agreement with the flattening of around .

These results indicate that when transforming Gaussian variables and with correlation into the variables and following the symmetric Pareto distribution, the correlation of and is smaller as the power-law tail of the distribution, controlled by , becomes longer. Eventually, and will be uncorrelated in the limit . The implication of this property in the generation of time series following the symmetric Pareto distribution will be discussed in Sec. IV.1.

III.2 Non-symmetric distributions

III.2.1 lognormal distribution

We start with the case of lognormal distribution because it is the only one (together with the uniform distribution discussed above) for which the function can be obtained analytically. In this case, noting that (Table I), and that is given in Eq. (2) we obtain that

and similarly for . Then, the integral in Eq. (8) is given by

| (27) |

which can be evaluated to obtain

| (28) |

Since for the lognormal distribution the mean and the variance are given respectively by and , we can insert these values and the result for in Eq. (28) into Eq. (6) to obtain finally

| (29) |

As expected from the standardized version of the lognormal distribution in Table II, the function is not unique but a family of functions controlled by the shape parameter of the distribution, , which is restricted to positive values. We show in Fig. 3a) the function for several values of . First, we note, as expected, that in this case the function is not odd, but the sign of the correlations is preserved, i.e., for positive values, and . The value increases (decreases in absolute value) with the parameter , which controls the tail of the lognormal distribution, longer for larger . Indeed, for moderately large values it is almost impossible to get anticorrelated lognormal variables since is practically zero for (see the case in Fig. 3a)), while the behavior for is substantially different. The behavior is systematically studied in Sec. III.3. And second, we also note that becomes more nonlinear as the shape parameter increases. The degree of nonlinearity can be quantified again using the expansion coefficients in Eq. (17) which in this case can be obtained analytically by expanding in a Taylor series Eq. (29):

| (30) |

The behavior of the first six expansion coefficients as a function of is depicted in Fig. 3b), and confirms the observed behavior of : while for small the linear behavior in dominates, for increasing the linear coefficient tends to zero and, depending on the range, a different expansion coefficient is the dominant one. These results imply that the validity of the linear approximation depends on the value: while for small values the linear approximation is essentially correct for small and moderately large values, for large the linear approximation will be correct only for very small values since will be the smallest coefficient in this range, and then very small values are required to neglect higher order expansion terms. This fact will affect the possible generation of power-law correlated, lognormally distributed time series (see Sec. IV.1).

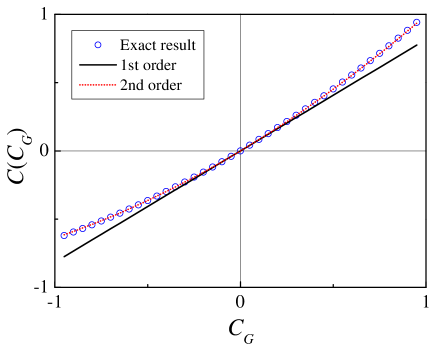

III.2.2 Exponential distribution

The exponential distribution lacks a shape parameter, and then there is a single standardized exponential distribution so that the function is unique (Table II). However, there is no analytical solution of the integral in Eq. (8) in this case, which has to be calculated numerically. The exact numerical result of the function for the exponential distribution is shown in Fig. 4.

Again, as the exponential distribution is not symmetric, the function is not odd either. However, is fairly linear, specially for intermediate and small values. This linearity can be quantified by calculating the corresponding expansion coefficients in Eq. (17). The first 4 coefficients result to be: , , and . Indeed, in Fig. 4 we also show the expansions of according to Eq. (16) up to first and second orders. In this case, the second order expansion is very precise in the whole range, and the first order suffices for . This property implies that it would be possible to generate power-law correlated and exponentially distributed time series (see Sec. IV.1).

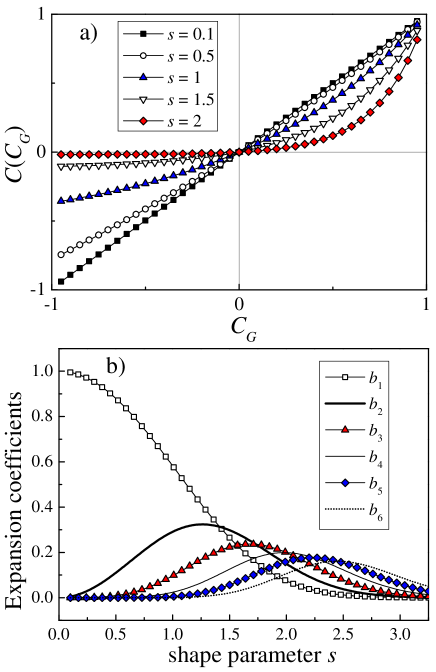

III.2.3 Weibull and Pareto distributions

We present these two distributions together because the corresponding functions present similar properties. As can be seen in Table II, the standardized forms of the Weibull and Pareto distributions have shape parameters, and respectively, which control the tail behavior. For the Weibull case, the parameter must be positive, . In the range , the tail decays faster than exponentially, and the larger , the faster the decay; the case corresponds to the exponential distribution, that we have studied above; and the case corresponds to a heavy tail distribution with a decay slower than exponential (stretched-exponential form), and the smaller the longer the tail of the distribution. For the Pareto case, the exponent controls the power-law tail of the distribution, with a probability density with asymptotic behavior . For both the Weibull and Pareto distributions, the existence of shape parameters implies that the function is not unique but a family of functions controlled by and , respectively. In the two cases, the integral in Eq. (8) does not admit an analytical solution, and has to be solved numerically. In Fig. 5a) and 5b) we show several examples of functions obtained numerically for different values of the Weibull shape parameter and the Pareto shape parameter , respectively.

Since both distributions are not symmetric, we first observe, as expected, that is not odd, but the sign of the correlations is preserved for both distributions. We also observe that the corresponding increases (decreases in absolute value) as and decrease and the tail of the distributions becomes heavier, so that it will be difficult to obtain Weibull and Pareto anticorrelated variables (See Sec. III.3). In the limits and , tends to zero in the whole range. Similarly, the degree of nonlinearity of is also controlled by and : while for large and values (fast-decaying tails) is more linear, as and decrease and tend to the respective limits 0 and 2, the function becomes strongly nonlinear. As in previous cases, the nonlinear behavior can be quantified by calculating the expansion coefficients of the function defined in Eq. (17). In Fig. 5c) and Fig. 5d) we plot the first six expansion coefficients as a function of the shape parameters and , respectively.

We obtain that for large and values the linear term is by far the most important, even with values close to 1 indicating an almost perfect linear behaviour of (see the case in Fig. 5a)). As and decrease, becomes smaller indicating a loss of linearity, and higher order expansion coefficients can be important. These results imply that the first-order approximation is essentially correct for small and moderately large values if the shape parameters and are large. However, for small and values, and especially for values close to zero and values close to 2, the approximation will be valid only for very small values. The implications of this fact when generating power-law correlated times series following Weibull and Pareto distributions are discussed in the next section.

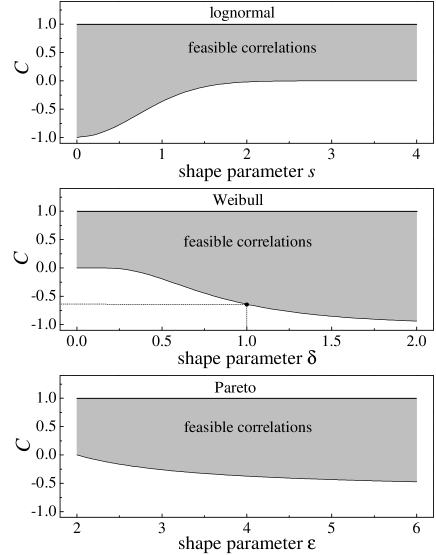

III.3 Feasible correlations for non-symmetric distributions

We have shown above that the function is increasing, maps positive (negative) values into positive (negative) values, with and . For symmetric distributions, in addition, is odd, so that and then the final non-Gaussian variables and can be correlated with any value in the interval . However, for non-symmetric distributions, with . This means that for this kind of distributions, the values in the interval are not reachable no matter the original value, and therefore the range of feasible correlations corresponds to the interval .

In general, the particular value of depends on the final marginal non-symmetric distribution considered, and for a given distribution can be calculated by evaluating the integral (8) using values close to . A non-symmetric distribution with shape parameter corresponds actually to a family of distributions, so that is also a function of the particular value of the shape parameter. We have determined the interval of feasible correlations for the non-symmetric distributions of Table I, which are shown in Fig. 6. Since the lognormal, Weibull and Pareto cases have a shape parameter, the bottom curve in the three panels shows the value of as a function of the respective shape parameter, so that the feasible correlations correspond to the shaded areas. The exponential distribution is a particular case of the Weibull distribution for , for which and is indicated in the central panel of Fig. 6) with a solid circle.

In general, we observe that the longer the tail of the non-symmetric distribution considered (controlled by its shape parameter), the larger the value (smaller in absolute value) and the shorter the interval of feasible correlations. In the extreme cases of very heavy tails, can be practically 0, so that it is almost impossible to obtain negative values, or in other words, is it almost impossible to get anticorrelated and variables via the transformation (5) when the final marginal distribution is very long-tailed. For the lognormal and Weibull cases, even for shape parameter values not even close to their limiting values ( and respectively), so that we see a practically flat curve in both cases when approaching the limiting values. For the Pareto case, we get for but the curve is not flat but decreasing when increases.

IV Application to time series

We have obtained the results of Secs. II and III by transforming two correlated Gaussian variables and into two variables and with the same arbitrary marginal distribution. These results can be naturally extended to the transformation of Gaussian correlated time series into time series with arbitrary marginal distribution, as we stated in the Introduction. Let us consider a Gaussian time series , , with autocorrelation function than can be calculated for any value of the lag . We can transform the Gaussian time series into a time series with arbitrary marginal distribution using (3). The autocorrelation function of is then determined by the behavior of the function. Indeed, simply by replacing back in Eq. (8) and by and respectively, and by and , and also by we obtain automatically that

| (31) |

i.e., the autocorrelation function of the final time series is determined by the function (depending only on the final marginal distribution) and the Gaussian autocorrelation function . We remark that this last result is correct since the Gaussian time series posseses a well-defined autocorrelation function, and the function can be obtained using the integral (8) for any final marginal distribution and for any value of , and therefore there are no feasibility problems when creating the final non-Gaussian time series since we are obtaining for the corresponding marginal distribution, and not imposing it. Note that feasibility problems can appear when imposing in a time series a marginal distribution and also an specific autocorrelation function, and both properties may not be compatible cario . For example, for non-symmetric distributions with long tails, negative values are likely non-feasible (see Sec. III.3). The validity of Eq. (31) for time series, inherited from Eq. (8) for pairs of variables, has been previously discussed for example in kugiumtzis ; kugi02 .

To illustrate the applicability of our results to time series, we consider two examples of Gaussian time series with well-defined autocorrelation functions , which are then transformed to have two different marginal distributions. The first Gaussian time series we consider are autoregressive processes of order 1, AR(1), defined as

| (32) |

where a Gaussian white noise such that and is a constant. AR(1) processses are Gaussian, and the corresponding autocorrelation function is given by:

| (33) |

equivalent to an exponentially decreasing function, of alternate sign for . The second example of Gaussian time series are the outputs of the Fourier Filtering method, described in more detail below (see Sec. IV.1), which present a power-law autocorrelation function with exponent controlled by the Hurst exponent Hurst (see Eq. (35)).

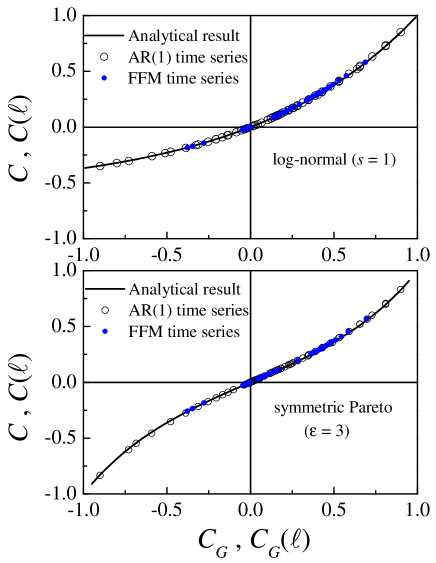

In Fig. 7 we consider two different final marginal distributions, lognormal (top panel) and symmetric Pareto (bottom panel). First, we represent as solid lines the theoretical functions obtained as explained in Secs. II and III. Then, we generate several AR(1) and FFM Gaussian time series with different and parameters. For each time series, we start calculating the autocorrelation function , then the time series is transformed to have the final marginal distribution considered using Eq. (3), and finally we obtain the autocorrelation function and represent vs. , as shown in symbols in Fig. 7. We note that the symbols fall perfectly on top of the theoretical functions, independently of the final marginal distribution or the values of and , showing the validity of Eq. (31).

We also remark that although the results in Secs. II and III for the function have been obtained for final marginal distributions with known analytical expressions, the same technique can be applied to experimental time series for which the marginal distribution is not known analytically. Indeed, it is enough to determine numerically the cumulative distribution and its inverse , and use it in the numerical solution of the integral in Eq. (8) to obtain how the correlations change when transforming correlated Gaussian variables into variables with the same marginal distribution of the experimental data. Indeed, we use this approach in one of the applications addressed below.

IV.1 Application I: Generation of power-law correlated time series with arbitrary distribution

Probably, fractional Gaussian noises (fGns) Beran are the reference for stochastic Gaussian time series with power-law autocorrelation functions. The autocorrelation function of a fGn is given by

| (34) |

where is the Hurst exponent Hurst . The power-law nature of arises in the limit of large where we have

| (35) |

The case corresponds to absence of correlations (white noise); the case corresponds to positive correlations, which decay slower with for larger values; and the case corresponds to negative correlations, which decay faster (in absolute value) as becomes smaller.

Likely, the algorithm most widely used to generate Gaussian power-law correlated time series of fGn type in different contexts is the Fourier Filtering Method (FFM) FFM1 ; FFM2 ; Fidelis ; Conchita ; Yosi_volatility ; cor-size ; manolo ; carpena_dfa ; bernaola ; uso_ffm_1 ; Hu2001 ; ChenPRE2005 ; escalas ; super . Although there are different approaches to implement FFM, probably the simplest is the following: 1) Given a time series size , consider a power spectrum as

| (36) |

with the input Hurst exponent. 2) Construct a Fourier transform such that and with a random phase uniformly distributed in the interval . 3) Fourier-transform back into real space to obtain the Gaussian time series , . By construction, the power spectrum of is given by (36), and then, via the Wiener-Khinchin theorem, the autocorrelation function of is power-law behaved as in Eq. (35) with well-defined Hurst exponent . In addition to power-law correlated, Gaussian and stationary, is also purely linear, since the Fourier phases are random. Without loss of generality, we can normalize to have zero mean and unit standard deviation, , and then with probability density and cumulative distribution as the ones given in Eq. (2).

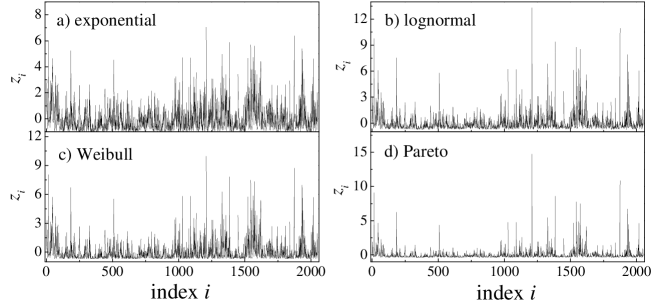

We suggest here to use FFM as the initial step of the algorithm able to generate power-law correlated time series with arbitrary distribution and controlled . Once the time series is generated with FFM, we propose to use Eq. (3) to transform into time series with arbitrary marginal distribution. As an example, in Figs. 8 and 9 we show several time series obtained via Eq. (3) from a Gaussian power-law correlated time series (shown in Fig. 8a)) generated with FFM. The final marginal distributions of correspond to the distributions in Table I, with the symmetric cases shown in Fig. 8, and the non-symmetric ones in Fig. 9.

Since the marginal distribution of the final time series is controlled via Eq. (3), the important question is whether the series are also power-law correlated with well defined Hurst exponent or not. We have shown above (Eq. (31) that . Therefore will show a power-law behavior with the same Hurst exponent as when behaves linearly. According to the expansion in Eq. (16), this happens whenever the first term in the expansion is the dominant one. In such case we can write

| (37) |

We note that, theoretically speaking, this linear approximation would be always correct for sufficiently small , where higher powers of can be neglected in the expansion. As is a decaying power-law (35), this means that the linear approximation will ultimately work for large enough and then, in the limit of large , will tend asymptotically to a power-law of the type written in Eq. (37) with the same Hurst exponent as , no matter the distribution of the final time series .

However, the asymptotic validity of the linear approximation (37) does not suffice in practical purposes to generate time series with observable power-law correlations. The reason is two-fold, since it depends on the length of the time series and , and the value of the marginal distribution. Note that for a FFM-generated time series of length , the expected noise level of the autocorrelation values is about Beran , and then values below this level are not significant. Indeed, a more precise value for the noise level of is , since only samples can be used to estimate . Therefore, the maximum value of the lag up to which there is observable and significant power-law correlated behavior in the Gaussian time series, , can be estimated by equating the autocorrelation function (34) at and the corresponding noise level

| (38) |

and solving numerically for . The solution, obviously, depends on and , and in general increases with and .

Similarly, we can estimate the maximum lag, , up to which the linear approximation to (Eq. (37) presents significant values by solving the equation

| (39) |

where we write the explicit expression of . The solution of this latter equation depends on and , and also on the marginal distribution of via its value. In general, increases with , and , and since , .

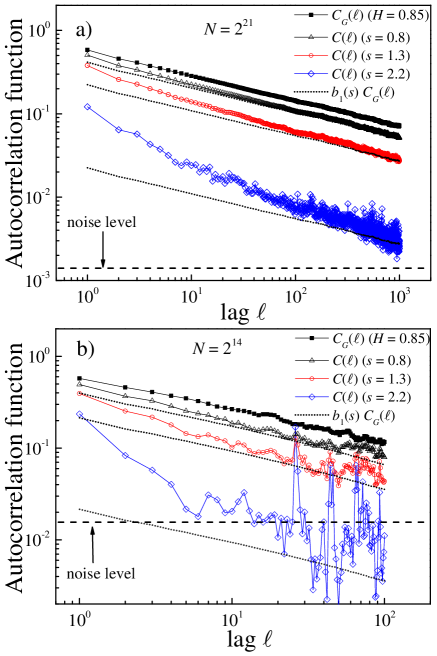

Indeed, given , and a final marginal distribution for with a particular value, the value obtained as solution of Eq. (39) provides a quantitative criterium to know a priori whether the power-law behavior in the autocorrelation function of is observable or not. Note that a small value typically implies an also small , so that the linear approximation becomes not significant for small values. In addition, the small value implies a poorly linear function, so that in order to neglect higher order terms in the expansion (37), small values are needed or, equivalently, large values. Therefore, when is small, the power-law behavior may be not observable since the values required can be larger than , where is not significant.

The general rule is then that the power-law behavior of is favoured to be observed when is large enough, corresponding to have a time series with large size and/or with marginal distribution with large value. Obviously, a large value can compensate a small value and viceversa, but if both and are small then the power-law behavior in will not be observable. We illustrate these arguments in Figs. 10a) and b) where we consider times series with and respectively. First, we show the autocorrelation functions of two Gaussian time series obtained via FFM with . Then, using Eq. (3), each Gaussian time series is transformed into three lognormally distributed time series with different values of the shape parameter (0.8, 1.3 and 2.2), and the corresponding autocorrelation functions are also shown in Figs. 10a) and b). We recall that the larger , the smaller (see Fig. 3). In particular, the values are 0.714 for , 0.382 for , and for . Using these values, we also plot for each case the linear approximations (37) in Figs. 10a) and 10b).

For the case (Fig. 10a)), we first observe that behaves almost as a perfect power-law, , in agreement with Eq. (35). For the lognormal time series, we find that the larger , the smaller the value where the power-law behavior is reached, as expected. Indeed, for the case , the corresponding lognormal time series exhibits power-law autocorrelation behavior practically in the whole -range. For the intermediate value, the linear approximation requires a larger to be correct, and the power-law behavior of happens at about . For the largest value, reaches the power-law behavior at larger values (). In this -range, is noisier than in previous cases, since the values are close to the noise level, which in this case turns out to be , and which is also shown in Fig. 10a) as a horizontal dashed line.

For the case (Fig. 10b)), the noise level (shown as a horizontal dashed line) is larger, around . As a consequence, although exhibits the correct power-law behavior, , although a bit noisier than in Fig. 10a). For the lognormal times series, the observed behavior depends on the shape parameter value. For , the corresponding value is large (0.72), and then the linear approximation is good enough to observe a power-law behavior of the corresponding . Similarly, for the intermediate value, and the power-law behavior of is also present for large , but with higher noise around the linear approximation . However, for , the value is very small () and then the linear approximation is never reached since before that happens, the values are in the noise level range, and no power-law behavior is observed at all. In other words, in practice it is not possible to generate a power-law correlated lognormally distributed time series of length and shape parameter .

The behavior shown in Figs. 10a) and b) can be understood using the solution of Eq. 39. Let us consider the worst case with . For the case, we obtain , large enough for (diamonds in Fig. 10a)) to reach the linear approximation before entering into the noise level range. This is a case where the small value is compensated with a large series size . However, for we obtain , too small for (diamonds int Fig. 10b)) to reach the validity region of the linear approximation before entering into the noise level range.

Although we have used the lognormal distribution in the previous discussion, the conclusions are general: The controlled and observable power-law behavior of is favoured for time series following marginal distributions with large value, i.e, with very linear functions. In addition, for a fixed distribution (fixed ), the larger the time series length , the smaller the noise level, and the more likely to observe the power-law behavior of . Since the effect of the time series length is clear, we analyze the two properties of the marginal distribution of that, according to the results presented in Sec. III, control the value: i) the tail behavior, and ii) the distribution symmetry.

-

(i)

Concerning the behavior of the tail of the distribution, we note that in general is large for bounded and for short, exponentially-bounded tail distributions. This is the case of the logistic (), uniform (), arcsine , Laplace () and exponential () distributions. Note that all these values are larger than 0.72, which is the lognormal case shown in Fig. 10 for , and therefore the five corresponding autocorrelations functions will follow almost perfectly the linear approximation, and will behave practically as perfect power-laws. But can also be large even for distributions with heavy tails, controlled by a shape parameter: the faster the decay of the heavy tail, the larger the corresponding value. This is the case of the symmetric Pareto (Fig. 2b)), lognormal (Fig. 3b)), Weibull (Fig. 5c)) and Pareto (Fig. 5d)) distributions. Then, in general, we conclude that the faster the decay of the tail (even heavy) of the distribution of the time series, the larger the likelihood of observing a power-law behavior of , and viceversa.

-

(ii)

Concerning the symmetry, symmetric distributions are in general better indicated to generate power-law correlated time series than non-symmetric distributions. The reason is that in the symmetric case, the expansion in Eq. (16) only contains odd terms, as shown in (20). Then, the first order approximation (37) is more likely to be valid even for large values, or equivalently, for small values, than if the second order term is present, as it happens in non-symmetric distributions. We are aware that, since the behavior of the tail of the distribution also affects the value, one can have a non-symmetric short-tail distribution with a value larger than the one corresponding to a symmetric heavy-tail distribution. However, for symmetric and non-symmetric distributions with similar tail behavior, the value of the symmetric case is expected to be larger than for the non-symmetric one due to the absence of even terms in the expansion of the former. And indeed this is the case: for example, the non-symmetric exponential distribution and the symmetric Laplace distribution present identical exponential tail behavior, and the corresponding values are 0.81 and 0.96 respectively. As another example, for the symmetric Pareto and the Pareto distributions with the same value of shape parameter controlling the power-law tail (see Tables I and II), the value for the symmetric case is always larger than for the non-symmetric one, as shown in Fig. 5d).

IV.2 Application II: modeling absolute returns in stock markets

A well-known example of real-world time series with autocorrelation function exhibiting power-law tails is the series of absolute returns of stock market prices podobnik . Let us consider that is the stock price at time , where can be measured in minutes, hours, days, etc. The absolute return is defined as:

| (40) |

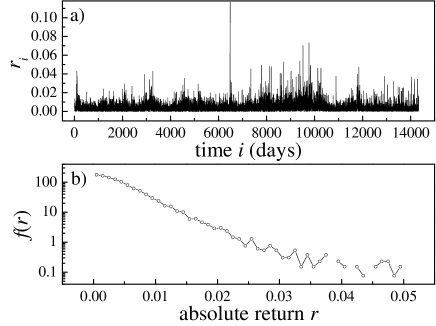

Typically, the time series present autocorrelation function with power-law tails, but the marginal distribution of is not Gaussian. As an example, we consider here the daily absolute returns of IBM obtained from the NYSE, which are shown in Fig. 11a) and the data cover the time range since 1962 with data points. The marginal distribution of the data is not Gaussian, as we show in Fig. 11b) where we plot the probability density obtained numerically. Since is very linear using log-scale in the vertical axis, this indicates an almost exponential distribution, although with a heavier tail than exponential for large values.

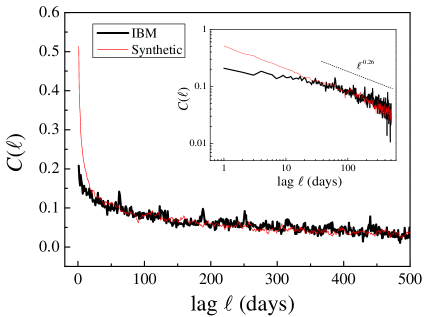

The autocorrelation function of is shown in Fig. 12 (thick line). As shown in the inset, presents a power-law tail of the form . Using the algorithm described above, we can generate a time series with the same power-law tail as the experimental data, and the same marginal distribution. To proceed, we first note that according to Eq. (35), so that . Then, we use FFM to generate a Gaussian time series with and . Next, we obtain numerically the cumulative distribution of the experimental data and its inverse , and finally we construct a final time series using with .

By construction, presents the same marginal distribution of the experimental IBM absolute returns . Using , we solve numerically the integral in Eq. (17) to obtain the value for the marginal distribution of , and we get , a quite large value, indicating that the linear approximation (37) is good. In addition, by solving Eq. (39) we obtain . Both results imply that the power-law behavior of the autocorrelation function of with the correct exponent is reached for small values, and is significant practically in the whole range of (large ). The autocorrelation function of is shown in Fig. 12 as a thin line. We note that both autocorrelation functions present almost identical values in the whole range (up to 500 days) with discrepancies only for small lags. In the inset, we observe in a log-log plot how the autocorrelation function of the synthetic time series matches perfectly the power-law tail of the experimental .

V Conclusions

Many real-world correlated time series are not Gaussian. However, very often the algorithms used to create surrogate time series produce correlated Gaussian time series with prescribed autocorrelation function, which are then transformed to have the desired final marginal distribution. However, this last transformation always modify the Gaussian autocorrelation function. In this work we have considered two stochastic Gaussian variables, and , and we have transformed them respectively into two stochastic variables and following any arbitrary marginal distribution. When the Gaussian variables are correlated with a given value, we have investigated how the correlation of the final variables and depends on . The function , which can be exactly determined by solving a 2D integral, turns out to depend on the properties of the destination distribution. We have obtained some general properties of , such that is an odd function when the destination distribution is symmetric. In addition, we have obtained analytically a power expansion of , which allows to weight the contribution of the different powers, and can be used to measure the linearity of using the value of the first-order expansion coefficient . We also have studied the specific behavior of for several destination distributions with different properties concerning the support, the symmetry and the tail behavior. In general, destination distributions with bounded support present large values and therefore highly linear functions. Also, the linearity of is favoured for symmetric distributions, and for distributions with fast-decaying tails of exponential or faster than exponential type. can behave also quite linearly even for heavy-tailed distributions of stretched-exponential or power-law type, but in general we observe that the longer the tail, the smaller the value and the linearity of . These results can be naturally extended to time series: when a Gaussian time series with autocorrelation is transformed into another time series with arbitrary marginal distribution, the final series autocorrelation function is determined by the function of the destination distribution via . In particular, for time series following marginal distributions with large values we have shown that . Using this property, we have extended the FFM algorithm, which produces Gaussian time series with a prescribed power-law autocorrelation function , to an algorithm able to create time series with arbitrary marginal distribution and the same prescribed asymptotic power-law behavior as the Gaussian time series. We have used this algorithm to create a time series replicating both the marginal distribution and the autocorrelation power-law tail of a real-world time series: the absolute returns of a technological company.

Acknowledgements.

We acknowledge financial support by the Consejería de Conocimiento, Investigación y Universidad, Junta de Andalucía and European Regional Development Fund (ERDF), ref. SOMM17/6105/UGR and FQM-362.References

- (1) C.-K. Peng, J. Mietus, J. M. Hausdorff, S. Havlin, H. E. Stanley, and A. L. Goldberger. Long-range anticorrelations and non-Gaussian behavior of the heartbeat. Phys. Rev. Lett. 70, 1343 (1993).

- (2) K. Likenkaer-Hansen, V. V. Nikouline, J. M. Palva, R. J. Ilmoniemi. Long-range temporal correlations and scaling behavior in human brain oscillations. Journal of Neuroscience 21, 1370 (2001).

- (3) C.-K. Peng, J. E. Mietus, Y. Liu, C. Lee, J. M. Hausdorff, H. E. Stanley, A. L. Goldberger and L. A. Lipsitz. Quantifying fractal dynamics of human respiration: age and gender effects. Annals of biomedical engineering 30, 683 (2002).

- (4) M. Duarte & V. M. Zatsiorsky. On the fractal properties of natural human standing. Neuroscience letters 283, 173 (2000).

- (5) M. T. Blázquez, M. Anguiano, F. A. de Saavedra, A. M. Lallena and P. Carpena. Study of the human postural control system during quiet standing using detrended fluctuation analysis. Physica A 388, 1857 (2009).

- (6) C. K. Peng, S. V. Buldyrev, A. L. Goldberger, S. Havlin, F. Sciortino, M. Simons and H. E. Stanley. Long-range correlations in nucleotide sequences, Nature 53, 6365 (1992).

- (7) R. F. Voss. Evolution of long-range fractal correlations and 1/f nosie in dna base sequences. Phys. Rev. Lett. 68, 3805 (1992).

- (8) E. E. Peters. Fractal market analysis: applying chaos theory to investment and economics, (John Wiley & Sons, 1994).

- (9) R. F. Voss and J. Clarke. 1/f noise in musics: Music from 1/f noise. The Journal of the Acoustical Society of America 63, 258 (1978).

- (10) S. Lovejoy and B.B. Mandelbrot. Fractal properties of rain and a fractal model. Tellus A: Dynamic Meteorology and Oceaonography 37, 209 (1985).

- (11) I. Bartos and I .M. Jánosi: Nonlinear correlations of daily temperature records over land. Nonlin. Processes Geophys. 13, 571 (2006).

- (12) P. A. Varotsos, N. V. Sarlis and E. S. Skordas. Long-range correlations in the electric signals that precede rupture. Phys. Rev. E. 66, 011902 (2002).

- (13) U. R. Acharya, K. P. Joseph, N. Kannathal, C. M. Lim and J. S. Suri. Heart rate variability: a review. Med. Biol. Eng. Comput. 44, 1031 (2006).

- (14) Z. R. Struzik. Wavelet methods in (financial) time-series processing. Physica A 296, 307 (2001).

- (15) H. A. Makse, S. Havlin, M. Schwartz, and H. E. Stanley. Method for generating long-range correlations for large systems. Phys. Rev. E 53, 5445 (1996)

- (16) P. Bernaola-Galvan, J. L. Oliver, M. Hackenberg, A. V. Coronado, P. Ch. Ivanov, and P. Carpena. Segmentation of time series with long-range fractal correlations, Eur. Phys. J. B 85, 211 (2012).

- (17) J. Theiler, S. Eubank, A. Longtin, B. Galdrikian, and J. Doyne Farmer. Testing for nonlinearity in time series: the method of surrogate data. Physica D 58, 77 (1992).

- (18) T. Schreiber and A. Schmitz. Improved surrogate data for nonlinearity tests. Phys. Rev. Lett. 77, 635 (1996).

- (19) D. Kugiumtzis. Surrogate data test for nonlinearity including nonmonotonic transforms. Phys. Rev. E 62, R25 (2000).

- (20) C. J. Keylock. A wavelet method for surrogate data generation. Physica D 225, 219 (2007).

- (21) J. M. Halley and D. Kugiumtzis. Nonparametric testing and trend in some climatic records. Climatic Change 109, 549 (2011).

- (22) W.H. Press, S.A. Teukolsly, W.T. Vetterling and B.P. Flannery. Numerical Recipes in Fortran 90, (Cambridge University Press, Cambridge, 1990).

- (23) R. Nelsen. An Introduction to Copulas, (Springer, New York, 1999).

- (24) R. S. Calsaverini and R. Vicente. An information-theoretic approach to statistical dependence: Copula information. EPL 88, 68003 (2009).

- (25) S. T. Li and J. L. Hammond. Generation of pseudorandom numbers with specified univariate distributions and correlation coefficients. IEEE Trans. Syst. Man. Cyber. 5, 557 (1975).

- (26) H. Chen. Initialization for NORTA: generation of random vectors with specified marginals and correlations. INFORMS. J. Comput. 13, 312 (2001).

- (27) D. Kugiumtzis and E. Bora-Senta. Normal correlation coefficient of non-normal variables using piece-wise linear approximation. Comput. Stat. 25, 645 (2010).

- (28) Y. L. Tong. The multivariate normal distribution, (Springer, New York, 1990.)

- (29) M. C. Cario and B. L. Nelson. Autoregressive to anything: Time-series input processes for simulation. Operations Research Letters 19, 51 (1996).

- (30) E.W. Ng and M. Geller. A table of integrals of the error functions. Journal of research of the National Bureau of Standards B, Mathematical Sciences 73B, 73B1-281 (1969).

- (31) D. Kugiumtzis. Statically transformed autoregressive process and surrogate data test for nonlinearity. Phys. Rev. E 66, 025201(R) (2002).

- (32) H. E. Hurst. Long-term storage capacity of reservoirs. Transactions of American Society of Civil Engineers 116, 770 (1951).

- (33) Jan Beran. Statistics for Long-Memory Processes, (Chapman and Hall/CRC, 1998).

- (34) F. A. B. F. de Moura and M. L. Lyra. Delocalization in the 1D Anderson model with long-range correlated disorder. Phys. Rev. Lett. 81, 3735 (1998).

- (35) C. Carretero-Campos, P. Bernaola-Galván, P. Ch. Ivanov and P. Carpena: Phase transitions in the first-passage time of scale-invariant correlated processes. Phys. Rev. E 85, 011139 (2012).

- (36) T. Kalisky, Y. Ashkenazy and S. Havlin: Volatility of linear and nonlinear time series. Phys. Rev. E 72, 011913 (2005).

- (37) A. V. Coronado and P. Carpena, Size Effects on Correlation Measures, J. Biol. Phys. 31, 121 (2005).

- (38) M. Gómez-Extremera, P. Carpena, P. Ch. Ivanov and P. A. Bernaola-Galván. Magnitude and sign of long-range correlated time series: Decomposition and surrogate signal generation. Phys. Rev. E 93, 042201 (2016).

- (39) P. Carpena, M. Gómez-Extremera, C. Carretero-Campos, P. A. Bernaola-Galván and A. V. Coronado. Spurious Results of Fluctuation Analysis Techniques in Magnitude and Sign Correlations. Entropy 19, 261 (2017).

- (40) P. A. Bernaola-Galván, M. Gómez Extremera, P. Carpena and A. R. Romance. Correlations in magnitude series to assess nonlinearities. Application to multifractal models and hearbeat fluctuations. Phys. Rev. E 96, 032218 (2017).

- (41) T. Kawasaki, Y. Kakai, T. Ikuta and R. Shimizu. Wave field restoration using three dimensional Fourier filtering method. Ultramicroscopy 90, 47 (2001).

- (42) K. Hu, P. Ch. Ivanov, Z. Chen, P. Carpena and H. E. Stanley: Effect of trends on detrended fluctuation analysis. Phys. Rev. E 64, 011114 (2001).

- (43) Z. Chen, K. Hu, P. Carpena, P. Bernaola-Galvan, H. E. Stanley and P. Ch. Ivanov: Effect of nonlinear filters on detrended fluctuation analysis. Phys. Rev. E 71, 011104 (2005).

- (44) P. Carpena, P. Bernaola-Galvan, A. V. Coronado, M. Hackenberg and J. L. Oliver. Identifying characteristic scales in the human genome. Phys. Rev. E 75, 032903 (2007).

- (45) P. Carpena, J. L. Oliver, M. Hackenberg, A. V. Coronado, G. Barturen and P. Bernaola-Galvan. High-level organization of isochores into gigantic superstructures in the human genome. Phys. Rev. E 83, 031908 (2011).

- (46) B. Podobnik, D.F. Fu, H.E. Stanley and P. Ch. Ivanov. Power-law autocorrelated stochastic processes with long-range cross-correlations. Eur. Phys. J. B 56, 47 (2007).