Large-dimensional Factor Analysis without Moment Constraints

Large-dimensional factor model has drawn much attention in the big-data era, in order to reduce the dimensionality and extract underlying features using a few latent common factors. Conventional methods for estimating the factor model typically requires finite fourth moment of the data, which ignores the effect of heavy-tailedness and thus may result in unrobust or even inconsistent estimation of the factor space and common components. In this paper, we propose to recover the factor space by performing principal component analysis to the spatial Kendall’s tau matrix instead of the sample covariance matrix. In a second step, we estimate the factor scores by the ordinary least square (OLS) regression. Theoretically, we show that under the elliptical distribution framework the factor loadings and scores as well as the common components can be estimated consistently without any moment constraint. The convergence rates of the estimated factor loadings, scores and common components are provided. The finite sample performance of the proposed procedure is assessed through thorough simulations. An analysis of a financial data set of asset returns shows the superiority of the proposed method over the classical PCA method.

Keyword: Elliptical factor model; Ordinary least square regression; Multivariate Kendall’s tau matrix.

1 Introduction

Factor model is a classical statistical model that serves as an important dimension reduction tool by characterizing the dependency structure of variables via a few latent factors. In the “big-data era” where more and more variables are recorded and stored, large-dimensional approximate factor model is drawing growing attention as it provides an effective way of summarizing information from large data sets. The large-dimensional approximate factor models are widely used in genomics, neuroscience, computer science and financial economics. Theoretical analysis of large-dimensional approximate factor models has been studied by many researchers. Existing factor analysis procedures mainly fall into two categories: the principle component analysis (PCA) approach and the maximum likelihood estimation (MLE) method. The PCA-based method is easy to implement and provides consistent estimators for the factors and factor loadings when both the cross-section and time dimension are large. Representative works include, but not limited to, Bai and Ng (2002); Stock and Watson (2002a, b); Bai (2003); Onatski (2009); Ahn and Horenstein (2013); Fan et al. (2013); Trapani (2018). It turns out that the PCA approach is equivalent to the least square optimization. The MLE-based method is more efficient than the PCA-based approach but is also computationally more suffering. Representative works, to name a few, are Bai and Li (2012, 2014, 2016).

However, the aforementioned works all assume that the fourth moments (or even higher moments) of factors and idiosyncratic errors are bounded such that the least-squares regression, or maximum likelihood estimation can be applied. This assumption is really an idealization of the complex random real world. Heavy-tailed data are often encountered in scientific fields such as financial engineering and biomedical imaging. In finance, Fama (1963) discussed the power law behavior of asset returns. Cont (2001) provided extensive empirical evidence of heavy-tailedness in financial returns. Jing et al. (2012) and Kong et al. (2015) even suggested to model the log price dynamics of an asset by pure jump processes without any moment conditions. Thus, it is imperative to develop estimation procedures that are robust to heavy-tailedness for large-dimensional factor models.

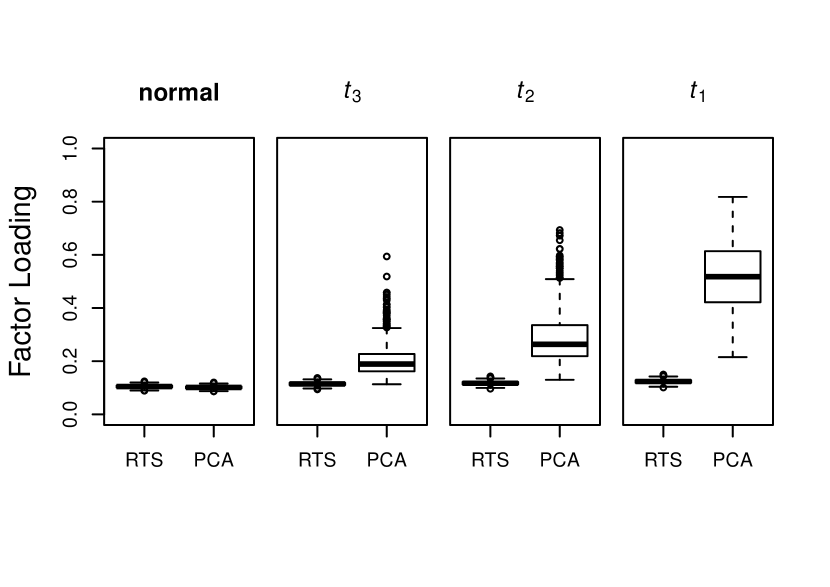

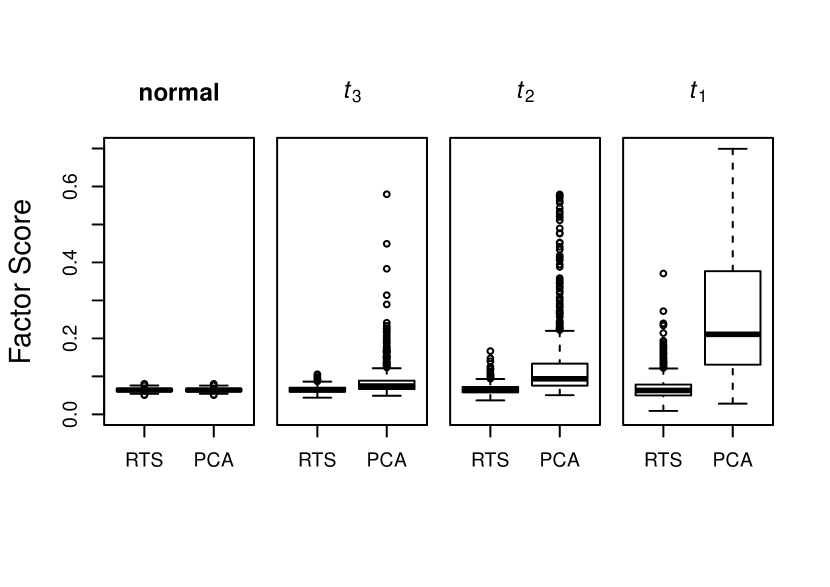

As an illustration, we check the sensitivity of the PCA (or Least Square Optimization) method to the heavy-tailedness of the factor and idiosyncratic errors with a synthetic data set. We generate the factors and idiosyncratic errors from joint normal, , and distributions that will be described in detail in Section 4. Figure 1 depicts the boxplots of the factor loading and factor score estimation errors based on 1000 replications. We observe that the PCA results in bigger biases and higher dispersions as the distribution tails become heavier. This is also consistent with the fourth moment condition imposed in existing papers.

In this article, we propose a robust two step (RTS) procedure to estimate the factor loadings, scores and common components without any moment constraint under the framework of elliptical distributions (FED). The FED assumes that the factors and the idiosyncratic errors jointly follow an elliptical distribution, which covers a large class of heavy-tailed distributions such as -distribution. The FED is drawing growing attention as an important tool to simultaneously simplify the structure and capture the heavy-tailedness of the data. For example, Fan et al. (2018) considered large-scale covariance estimation through the FED; and Yu et al. (2019) proposed robust estimator of the factor number of a large-dimensional factor model under the FED condition. In the first step, we recover the factor space, spanned by the columns of the factor loadings, by performing PCA to the estimated spatial Kendall’s tau matrix rather than the sample covariance matrix. The spatial Kendall’s tau matrix shares the same eigenspace with the scatter matrix of the elliptically distributed data vectors and the scatter matrix serves as a measure of the cross-sectional dependence of the data. Since the scatter matrix has nothing to do with the moment of the data, the resulting estimated factor space from RTS is consistent to the true factor space without any moment requirement. In a second step, we estimate the factor score by a cross-sectional least square regression based on the estimated factor loadings in the first step. Due to the polarization of the elliptical distribution, the estimated factor scores are consistent up to some orthogonal transformation without any moment restriction. To the best of our knowledge, this is the first work that can estimate the factor loadings and scores (up to some orthogonal transformations) and common components for heavy-tailed data without any moment requirement on the factors and idiosyncratic errors under the FED condition. Now, let us come back to the example mentioned earlier in Figure 1, in which we also presented the results using the RTS method. Figure 1 demonstrates that the estimated factor loadings and scores are not much sensitive to the heavy-tailedness of the factors and idiosyncratic errors. All the RTS estimates are substantially more accurate than the PCA estimates for the three -distribution settings.

The critical tool in the current paper, spatial Kendall’s tau matrix, is first introduced in Choi and Marden (1998), also named as multivariate Kendall’s tau matrix in the literature. Its applications on covariance matrix estimation and principal component analysis in low dimensions can be found in but not limited to Marden (1999); Visuri et al. (2000) and Croux et al. (2002). For high-dimensional settings, Han and Liu (2018) studied the eigen-analysis of spatial Kendall’s tau matrix for elliptical distributions. Similar rank-based methods in high dimensions are also discussed in Han and Liu (2012) and Han and Liu (2014). The mentioned literatures provide a sound framework of constructing Bernstein’s type concentration inequalities for high-dimensional matrix-form U-statistics, but none focused on the factor models. As a result, the existing convergence rates for robust principal component analysis are not optimal if the observed vectors contain some low-rank factor structures. To the best of our knowledge, Fan et al. (2018) is the the first to consider factor structures with spatial Kendall’s tau matrix in high dimensions, which proposed the elliptical factor model exactly the same as the model considered in the current paper. However, the motivations of the two works are quite different. Fan et al. (2018) focused on robust covariance estimation while our work focused on robust estimation for the factor loadings and scores.

The contributions of the current paper lie in the following aspects. Firstly, it’s the first to estimate the factor scores and loadings using spatial Kendall’s tau matrix in high-dimensional settings. The proposed method is computationally efficient and easy to implement. Secondly, our theoretical analysis shows that the proposed robust estimators are consistent without any moment constraints on the underlying distributions, which is the first in the literature and makes the method applicable to analyzing heavy-tailed datasets such as financial returns and macroeconomic indicators. Thirdly, the convergence rates of the RTS estimators are the same as those in Bai (2003), which makes RTS a safe replacement of the conventional PCA approach. We overcome two major challenges in the technical proofs: 1) the summing terms in the sample spatial Kendall’s tau matrix are dependent, which makes the typical Bernstein’s inequities unapplicable; 2) the sample spatial Kendall’s tau matrix is a nonlinear function of the observed vectors, which in essence makes the theoretical analysis more challenging.

We introduce the notations adopted throughout the paper. For any vector , let , . For a real number , denote as the largest integer smaller than or equal to . Let be the indicator function. Let be a diagonal matrix, whose diagonal entries are . For a matrix , let (or ) be the entry of , the transpose of , the trace of , the rank of and a vector composed of the diagonal elements of . Denote as the -th largest eigenvalue of a nonnegative definitive matrix , and let be the spectral norm of matrix and be the Frobenius norm of . For two series of random variables, and , means and . For two random variables (vectors) and , means the distributions of and are the same. Let be a vector with all elements 1. The constants in different lines can be nonidentical.

The rest of the paper proceeds as follows. In Section 2, we introduce the setup assumptions and multivariate Kendall’s tau matrix. Estimators of the factor loadings, scores and common components are also provided. In Section 3, we establish the consistency including the convergence rate for the estimated factor loadings, scores and common components. Section 4 is devoted to a thorough numerical study. A real financial data set of asset returns is analyzed in Section 5. We discuss the possible future research directions and conclude the article in Section 6. The proofs of the main theorems are collected in the Appendix and additional details are put in the supplement.

2 Methodology

2.1 Elliptical distribution and spatial Kendall’s tau matrix

Consider the large-dimensional factor model for a large panel data set ,

| (2.1) |

where , are the unobserved factors, is the factor loading matrix, and represents the idiosyncratic errors. The term is referred to as the common component of . For the large-dimensional approximate factor model introduced in Chamberlain and Rothschild (1983), is assumed to be cross-sectionally weakly dependent.

As mentioned in the introduction and precisely stated in Assumption A below, we assume that is a series of temporally independent and identically distributed random vectors generated from an elliptical distribution. For a random vector following an elliptical distribution, denoted by , we mean that

where , is a random vector uniformly distributed on the unit sphere in , is a scalar random variable independent of , is a deterministic matrix satisfying with called scatter matrix whose rank is . Let the scatter matrices of and be and , respectively. If is sparse, the model (2.1) is indeed an approximate factor model including the strict factor model, in which is diagonal, as a special case. Another equivalent characterization of the elliptical distribution is by its characteristic function, which has the form , where is a properly defined characteristic function and .

The factor loadings and scores, and , are not separately identifiable as they are unobservable. For an arbitrary invertible matrix , one can always have and such that . For reason of identifiability, we impose the following constraints:

This identification condition is also used in Han and Liu (2014) and Yu et al. (2019), and it is not unique and one may refer to Bai and Li (2012) for more detailed discussion on identification issues.

It is worthy of pointing out that elliptical distributions have some nice properties as Gaussian distributions, e.g., the marginal distributions, conditional distributions and distributions of linear combinations of elliptical vectors are also elliptical. Thus, for the factor model (2.1) under the FED condition, the scatter matrix of , , is composed of a low-rank part and a sparse part , i.e, . For Gaussian distribution, is simply the population covariance matrix of . For non-Gaussian distributions, especially distributions with infinite variances, the scatter matrix is still a measure of the dispersion of a random vector. So, naturally the eigenspace of the scatter matrix sheds light into the recovery of the factor space, but this can not be reached by performing PCA to the sample covariance matrix because the covariance is meaningless for pairs of random variables with infinite variances. To tackle with this difficulty, we introduce the population spatial Kendall’s tau matrix. Let and be an independent copy of . The population spatial Kendall’s tau matrix is defined as

can be estimated by a second-order U-statistic. Specifically, assume is a series of independent data points following the distribution . The sample version spatial Kendal’s tau matrix is

The spatial Kendall’ tau matrix was first introduced in Choi and Marden (1998) and has been used for covariance matrix estimation in Visuri et al. (2000); Fan et al. (2018) and principal component estimation in Marden (1999); Han and Liu (2018). A critical result is that the spatial Kendall’s tau matrix shares the same ordering of eigenvalues and the same eigenspace as those of the scatter matrix . We cite this result directly without proof in the following Lemma 2.1.

Lemma 2.1.

Let be a continuous elliptically distributed random vector, i.e., with and be the population multivariate Kendall’s tau statistic. Further assume that , we have

where , and in addition and share the same eigenspace with the same descending order of the eigenvalues.

2.2 Robust two-step estimation procedure

In this section, we introduce an innovative two-step estimation procedure for large-dimensional elliptical factor model. In the first step, we propose to estimate by the eigenvectors of the spatial Kendall’s tau matrix. First, we estimate the spatial Kendall’s tau matrix of by

| (2.2) |

As the eigenvectors of the spatial Kendall’s tau matrix is identical to the eigenvectors of the scatter matrix , thus we estimate the factor Loading matrix by times the leading eigenvectors of . In detail, let be the leading eigenvectors of and let . We take as the estimator of the factor loading matrix . The number of factors is relatively small compared with and . We first assume that is known and fixed. If is unknown, we can estimate consistently as in Yu et al. (2019).

In a second step, we estimate the factors by regressing on . is estimated by the following least square optimization,

| (2.3) |

where is the -th row of , i.e, . For conventional factor model, when both and are large, the factor loadings and the factors can be estimated by PCA, which is equivalent to solving a double least-square regression problem, see Bai and Ng (2002) or (2.4) in Fan et al. (2018). The two-step estimation procedure is motivated by the idea of the regression formulation.

3 Theoretical results

In this section, we investigate the theoretical properties of the proposed estimators and . We need the following technical assumptions.

Assumption A We assume that

where ’s are independent samples of a scalar random variable , and ’s are independent Gaussian samples from . is fixed. Further, and are independent and as . Therefore, are independent samples from for where , and . To make the model identifiable, we further assume that .

Assumption B Assume as , where is a positive definite matrix. There exist positive constants such that .

Assumption C We assume .

Assumption A states that are i.i.d and follows the elliptical distribution, which further implies that are i.i.d. from elliptical distribution with scatter matrix . Assumption B assumes converges to a positive definite matrix with bounded maximum and minimum eigenvalues. We also require that are distinct to make corresponding eigenvectors identifiable. Assumption C requires that the eigenvalues of the are bounded from below and above, which in essence makes the idiosyncratic errors negligible relative to the common component. Compared with the moment assumptions of idiosyncratic errors in Bai (2003), Assumption C is another typical way to control the cross-sectional correlations of the idiosyncratic errors. The assumption is common in related literature, see for example, Fan et al. (2013) and Fan et al. (2018). In fact, under Assumption B and Assumption C, further with the Weyl’s theorem, we have that the eigenvalues of show the spiked structure which is a common assumption in the large-dimensional factor model literatures, see for example, Bai and Ng (2002); Bai (2003); Ahn and Horenstein (2013); Fan et al. (2013, 2018); Trapani (2018). In other word, the eigenvalues are asymptotically proportional to while the non-spiked eigenvalues are bounded.

In the following theorem, we show that the estimated loading matrix converges with the rate in terms of the averaged squared error after certain rotation.

Theorem 3.1.

Under Assumptions A, B, C, there exist a series of matrices (dependent on and ) so that and

In Theorem 3.1, we obtain the same convergence rate of the estimated factor loadings as that in Bai (2003). However, we impose no moment constrains on the factors and idiosyncratic errors. In the following theorem, we establish the convergence rate of the estimated factor scores .

Theorem 3.2.

Assume that Assumptions A, B, C hold, then for any ,

By the results in Theorem 3.1 and Theorem 3.2, we finally show that the estimated common components are consistent to the true ones.

Theorem 3.3.

Assume that Assumptions A, B, C hold, we have that for any ,

As far as we know, this is the first time that consistent estimators for the factor loadings, scores and common components are proposed without any moment constraints. Under the elliptical assumption containing heavy-tailed cases, our RTS estimators converge at the same rates as those of the PCA estimators with finite fourth moment constrains on the factors and errors, see Bai (2003).

4 Simulation Study

In this section, we conduct thorough simulation studies to compare the Robust Two-Step (RTS) estimator with the conventional PCA method. We use similar data-generating models as in Ahn and Horenstein (2013), Xia et al. (2017) and Yu et al. (2019). We generate the data from the following model,

where and are jointly generated from elliptical distributions. We let be independently drawn from the standard normal distribution. The parameter controls the SNR (signal to noise ratio), controls the serial correlations of idiosyncratic errors, and and control the cross-sectional correlations. We point out that although we assume ’s are temporally independent theoretically in Assumption A, we allow to be serially correlated in the simulation studies.

| Type | Method | ||||||

| MEE_CC | AVE_FL | AVE_FS | MEE_CC | AVE_FL | AVE_FS | ||

| RTS | 0.02(0.00) | 0.11(0.01) | 0.08(0.01) | 0.01(0.00) | 0.11(0.01) | 0.06(0.00) | |

| PCA | 0.02(0.00) | 0.10(0.01) | 0.08(0.01) | 0.01(0.00) | 0.10(0.01) | 0.06(0.00) | |

| RTS | 0.02(0.00) | 0.12(0.01) | 0.08(0.01) | 0.02(0.00) | 0.11(0.01) | 0.07(0.01) | |

| PCA | 0.04(0.03) | 0.20(0.06) | 0.10(0.04) | 0.04(0.03) | 0.20(0.06) | 0.08(0.04) | |

| RTS | 0.02(0.01) | 0.12(0.01) | 0.09(0.02) | 0.02(0.00) | 0.12(0.01) | 0.07(0.01) | |

| PCA | 0.09(0.11) | 0.30(0.10) | 0.14(0.09) | 0.09(0.10) | 0.29(0.10) | 0.12(0.08) | |

| RTS | 0.02(0.01) | 0.12(0.01) | 0.09(0.04) | 0.02(0.01) | 0.12(0.01) | 0.07(0.03) | |

| PCA | 0.29(0.29) | 0.52(0.12) | 0.27(0.16) | 0.29(0.29) | 0.52(0.12) | 0.26(0.16) | |

| Skewed | RTS | 0.02(0.00) | 0.12(0.01) | 0.08(0.01) | 0.02(0.00) | 0.11(0.01) | 0.07(0.01) |

| PCA | 0.04(0.03) | 0.20(0.06) | 0.10(0.03) | 0.04(0.03) | 0.20(0.06) | 0.09(0.04) | |

| -stable | RTS | 0.06(0.02) | 0.19(0.01) | 0.19(0.06) | 0.06(0.02) | 0.19(0.01) | 0.16(0.06) |

| PCA | 0.14(0.70) | 0.39(0.21) | 0.37(0.22) | 0.16(0.80) | 0.41(0.21) | 0.37(0.23) | |

| Type | Method | ||||||

| MEE_CC | AVE_FL | AVE_FS | MEE_CC | AVE_FL | AVE_FS | ||

| RTS | 0.01(0.00) | 0.09(0.00) | 0.06(0.00) | 0.01(0.00) | 0.07(0.00) | 0.06(0.00) | |

| PCA | 0.01(0.00) | 0.08(0.00) | 0.06(0.00) | 0.01(0.00) | 0.07(0.00) | 0.06(0.00) | |

| RTS | 0.01(0.00) | 0.09(0.00) | 0.06(0.01) | 0.01(0.00) | 0.08(0.00) | 0.06(0.01) | |

| PCA | 0.03(0.02) | 0.18(0.06) | 0.08(0.04) | 0.03(0.02) | 0.16(0.05) | 0.08(0.02) | |

| RTS | 0.01(0.00) | 0.10(0.01) | 0.07(0.01) | 0.01(0.00) | 0.08(0.00) | 0.06(0.01) | |

| PCA | 0.08(0.10) | 0.27(0.10) | 0.12(0.08) | 0.08(0.09) | 0.27(0.10) | 0.11(0.08) | |

| RTS | 0.01(0.01) | 0.10(0.01) | 0.07(0.03) | 0.01(0.00) | 0.09(0.00) | 0.07(0.04) | |

| PCA | 0.28(0.31) | 0.52(0.12) | 0.27(0.16) | 0.28(0.27) | 0.51(0.12) | 0.26(0.16) | |

| Skewed | RTS | 0.01(0.00) | 0.09(0.00) | 0.06(0.01) | 0.01(0.00) | 0.08(0.00) | 0.06(0.01) |

| PCA | 0.03(0.03) | 0.18(0.05) | 0.08(0.03) | 0.03(0.02) | 0.16(0.06) | 0.08(0.04) | |

| -stable | RTS | 0.04(0.01) | 0.16(0.01) | 0.15(0.05) | 0.04(0.01) | 0.14(0.01) | 0.15(0.06) |

| PCA | 0.15(0.82) | 0.39(0.23) | 0.37(0.24) | 0.13(0.83) | 0.39(0.24) | 0.38(0.24) | |

Before we give the data generating scenarios, we first review the multivariate distribution. The Probability Distribution Function (PDF) of a -dimensional multivariate distribution is

where is the gamma function. In fact, multivariate distribution with is the multivariate Cauchy distribution that has no finite mean. We also consider the following data generating scenarios in the simulation studies.

Scenario A Set , , are generated in the following ways: (i) are i.i.d. jointly elliptical random samples from multivariate Gaussian distributions ; (ii) are i.i.d. jointly elliptical random samples from multivariate centralized distributions with ; (iii) are i.i.d. samples from multivariate skewed- distribution; (iv) are i.i.d. random samples from multivariate Gaussian distributions while the elements of are i.i.d. random samples from symmetric -Stable distribution with skewness parameter , scale parameter and location parameter , .

Scenario B Set , are generated in the same ways as in Scenario A. .

Scenario C Set , are i.i.d. jointly elliptical random vectors from multivariate Gaussian and multivariate centralized distribution with , where is a diagonal matrix of dimension with and with SNR from .

| Type | Method | ||||||

| MEE_CC | AVE_FL | AVE_FS | MEE_CC | AVE_FL | AVE_FS | ||

| RTS | 0.02(0.01) | 0.11(0.02) | 0.09(0.01) | 0.02(0.00) | 0.11(0.01) | 0.07(0.01) | |

| PCA | 0.02(0.01) | 0.11(0.02) | 0.09(0.01) | 0.02(0.00) | 0.11(0.01) | 0.07(0.01) | |

| RTS | 0.02(0.01) | 0.13(0.02) | 0.10(0.02) | 0.02(0.01) | 0.13(0.02) | 0.08(0.02) | |

| PCA | 0.04(0.03) | 0.20(0.07) | 0.12(0.07) | 0.04(0.03) | 0.20(0.07) | 0.10(0.06) | |

| RTS | 0.03(0.02) | 0.15(0.03) | 0.12(0.05) | 0.02(0.01) | 0.14(0.03) | 0.09(0.05) | |

| PCA | 0.09(0.11) | 0.31(0.13) | 0.21(0.14) | 0.08(0.10) | 0.29(0.13) | 0.18(0.14) | |

| RTS | 0.08(0.16) | 0.29(0.14) | 0.28(0.17) | 0.06(0.11) | 0.27(0.14) | 0.25(0.18) | |

| PCA | 0.28(0.30) | 0.55(0.13) | 0.44(0.17) | 0.28(0.32) | 0.55(0.13) | 0.43(0.18) | |

| Skewed | RTS | 0.02(0.01) | 0.12(0.02) | 0.10(0.02) | 0.02(0.01) | 0.12(0.01) | 0.08(0.02) |

| PCA | 0.05(0.04) | 0.21(0.07) | 0.13(0.07) | 0.04(0.03) | 0.20(0.07) | 0.11(0.07) | |

| -stable | RTS | 0.14(0.14) | 0.30(0.10) | 0.30(0.13) | 0.12(0.11) | 0.29(0.09) | 0.27(0.13) |

| PCA | 0.35(0.78) | 0.46(0.18) | 0.43(0.20) | 0.43(0.86) | 0.48(0.19) | 0.43(0.21) | |

| Type | Method | ||||||

| MEE_CC | AVE_FL | AVE_FS | MEE_CC | AVE_FL | AVE_FS | ||

| RTS | 0.01(0.00) | 0.09(0.01) | 0.07(0.01) | 0.01(0.00) | 0.08(0.01) | 0.07(0.01) | |

| PCA | 0.01(0.00) | 0.09(0.01) | 0.07(0.01) | 0.01(0.00) | 0.07(0.01) | 0.07(0.01) | |

| RTS | 0.01(0.00) | 0.10(0.01) | 0.07(0.01) | 0.01(0.00) | 0.09(0.01) | 0.07(0.01) | |

| PCA | 0.03(0.02) | 0.17(0.06) | 0.09(0.05) | 0.03(0.02) | 0.15(0.06) | 0.09(0.04) | |

| RTS | 0.02(0.01) | 0.11(0.01) | 0.08(0.03) | 0.01(0.00) | 0.10(0.01) | 0.08(0.03) | |

| PCA | 0.07(0.10) | 0.28(0.13) | 0.17(0.14) | 0.07(0.09) | 0.27(0.13) | 0.16(0.14) | |

| RTS | 0.04(0.04) | 0.19(0.09) | 0.19(0.15) | 0.02(0.02) | 0.14(0.04) | 0.17(0.14) | |

| PCA | 0.27(0.31) | 0.55(0.13) | 0.43(0.18) | 0.27(0.28) | 0.54(0.13) | 0.42(0.18) | |

| Skewed | RTS | 0.01(0.00) | 0.10(0.01) | 0.07(0.02) | 0.01(0.00) | 0.09(0.01) | 0.07(0.01) |

| PCA | 0.03(0.02) | 0.17(0.06) | 0.10(0.04) | 0.03(0.02) | 0.16(0.06) | 0.09(0.05) | |

| -stable | RTS | 0.08(0.06) | 0.22(0.04) | 0.23(0.10) | 0.06(0.03) | 0.17(0.02) | 0.20(0.08) |

| PCA | 0.41(0.88) | 0.46(0.21) | 0.43(0.22) | 0.33(0.86) | 0.43(0.22) | 0.42(0.23) | |

In Scenario A, the setting perfectly fits to our assumption with no serial correlations of idiosyncratic errors and are from light-tailed Gaussian or heavy-tailed with . Note that when , it’s indeed the Cauchy distribution which does not have finite moments of order greater than or equal to one. We also consider the skewed and -stable distributions to gauge how sensitive the method is to the elliptical distribution assumption. We generate the multivariate skewed random samples from by function rmvst in R package fMultivar. Scenario B is a simple case containing both serially and cross-sectionally correlated errors from Gaussian distribution, distribution with degree 1,2,3, skewed distribution or -stable distribution. Scenario C corresponds to a case where both serially and cross-sectionally correlated errors, and strong and weak factors exist. To evaluate the empirical performance of different methods, we consider the following indices: the MEdian of the normalized estimation Errors for Common Components in terms of the matrix Frobenius norm, denoted as MEE-CC; the AVerage estimation Error for the Factor Loading matrices, denoted as AVE-FL; and the AVerage estimation Error for the Factor Scroe matrices, denoted as AVE-FS. Specifically,

where is the replication times, and are the estimators for the th replication, and for two orthogonal matrices and of sizes and ,

| SNR | Type | Method | ||||||

| MEE_CC | AVE_FL | AVE_FS | MEE_CC | AVE_FL | AVE_FS | |||

| 0.4 | RTS | 0.02(0.01) | 0.14(0.02) | 0.09(0.02) | 0.02(0.01) | 0.11(0.01) | 0.09(0.01) | |

| PCA | 0.02(0.01) | 0.13(0.02) | 0.09(0.01) | 0.02(0.01) | 0.11(0.01) | 0.09(0..01) | ||

| RTS | 0.03(0.01) | 0.16(0.03) | 0.11(0.03) | 0.02(0.01) | 0.13(0.02) | 0.10(0.02) | ||

| PCA | 0.05(0.06) | 0.26(0.10) | 0.16(0.10) | 0.04(0.04) | 0.23(0.10) | 0.15(0.10) | ||

| 0.5 | RTS | 0.02(0.01) | 0.13(0.02) | 0.08(0.01) | 0.02(0.01) | 0.10(0.01) | 0.08(0.01) | |

| PCA | 0.02(0.01) | 0.13(0.02) | 0.08(0.01) | 0.01(0.01) | 0.10(0.01) | 0.08(0.01) | ||

| RTS | 0.03(0.01) | 0.15(0.02) | 0.10(0.03) | 0.02(0.01) | 0.12(0.01) | 0.09(0.02) | ||

| PCA | 0.05(0.04) | 0.23(0.09) | 0.14(0.09) | 0.04(0.03) | 0.21(0.09) | 0.13(0.08) | ||

| 0.6 | RTS | 0.02(0.00) | 0.12(0.01) | 0.08(0.01) | 0.01(0.01) | 0.10(0.01) | 0.08(0.01) | |

| PCA | 0.02(0.00) | 0.12(0.01) | 0.08(0.01) | 0.01(0.01) | 0.10(0.01) | 0.08(0.01) | ||

| RTS | 0.02(0.01) | 0.14(0.02) | 0.09(0.03) | 0.02(0.01) | 0.11(0.01) | 0.08(0.02) | ||

| PCA | 0.05(0.04) | 0.22(0.08) | 0.12(0.08) | 0.03(0.03) | 0.19(0.08) | 0.11(0.07) | ||

| 0.7 | RTS | 0.02(0.00) | 0.12(0.01) | 0.08(0.01) | 0.01(0.01) | 0.09(0.01) | 0.07(0.01) | |

| PCA | 0.02(0.00) | 0.11(0.01) | 0.08(0.01) | 0.01(0.01) | 0.09(0.01) | 0.07(0.01) | ||

| RTS | 0.02(0.01) | 0.14(0.02) | 0.08(0.02) | 0.02(0.00) | 0.11(0.01) | 0.08(0.01) | ||

| PCA | 0.05(0.04) | 0.21(0.08) | 0.12(0.07) | 0.03(0.02) | 0.18(0.07) | 0.10(0.06) | ||

The Gram-Schmidt orthonormal transformation can be used when and are not column-orthogonal matrices. In fact, measures the distance between the column spaces of and , and it is a quantity between 0 and 1. It is equal to 0 if the column spaces of and are the same and 1 if they are orthogonal. As the factor loading matrix and factor score matrix are not separately identifiable, particularly suits to quantify the accuracy of factor loading/score matrices estimation.

The simulation results for Scenario A, Scenario B and Scenario C are reported in Table 1, Table 2 and Table 3, respectively. For Scenario A, from Table 1, we can see that in Gaussian setting, PCA performs slightly better than the RTS in terms of MEE_CC, AVE_FL and AVE_FS while the performances of the two methods are still comparable. In the heavy-tailed distribution settings with , the RTS outperforms the PCA by a large margin, in terms of MEE_CC, AVE_FL and AVE_FS, which indicates the robustness of the RTS procedure. The smaller the is, the more obvious the superiority of RTS over PCA is. Besides, as the time dimension or the cross-section get larger, the RTS performs better. In the skewed- and -stable distribution settings, the RTS still outperforms the PCA and performs satisfactorily, which indicates the RTS is not sensitive to the symmetric elliptical distribution assumption. For Scenario B, from Table 2, we can draw similar conclusions as for Scenario A. The results show that the proposed RTS procedure is also robust to the heavy tails in the case where both serial and cross-sectional correlations exist. For Scenario C, from Table 3, we see that RTS still performs well when both strong and weak factors exist. It performs comparably with PCA for data from while performs much better than PCA for heavy-tailed data from distribution. In addition, the performances of both the RTS and PCA methods become better as the time dimension gets larger (from 100 to 150). In a word, from the simulation study, the proposed RTS procedure can be used as a safe replacement of the conventional PCA method in practice.

5 Real Example: SP 100 Weekly Returns Panel

In this section, we apply the proposed method to study the weekly share returns of Standard & Poor 100 component companies during the period from January 1st, 2018 to December 31st, 2019. Details of the data set are available upon request, including the symbol list and names of the corresponding companies. The raw data set is a “105 weeks”“100 shares” panel without missing values. We firstly calculate the sample auto-correlation functions, which indicates that no significant serial correlations exist for most of the weekly return series. We also performed the Augmented Dickey-Fuller tests and found that all the series are stationary.

We use the centralized log returns to do factor analysis. We leave the centralized log returns unscaled since volatilities of all assets are themselves very informative in portfolio allocation, risk management and derivatives pricing. As for the factor number, the “eigenvalue-ratio” method proposed by Ahn and Horenstein (2013) and its robust version proposed by Yu et al. (2019) both lead to an estimate of just 1 common factor. Inspired by the Fama-French 3 factor model, we also consider in this example for comparison.

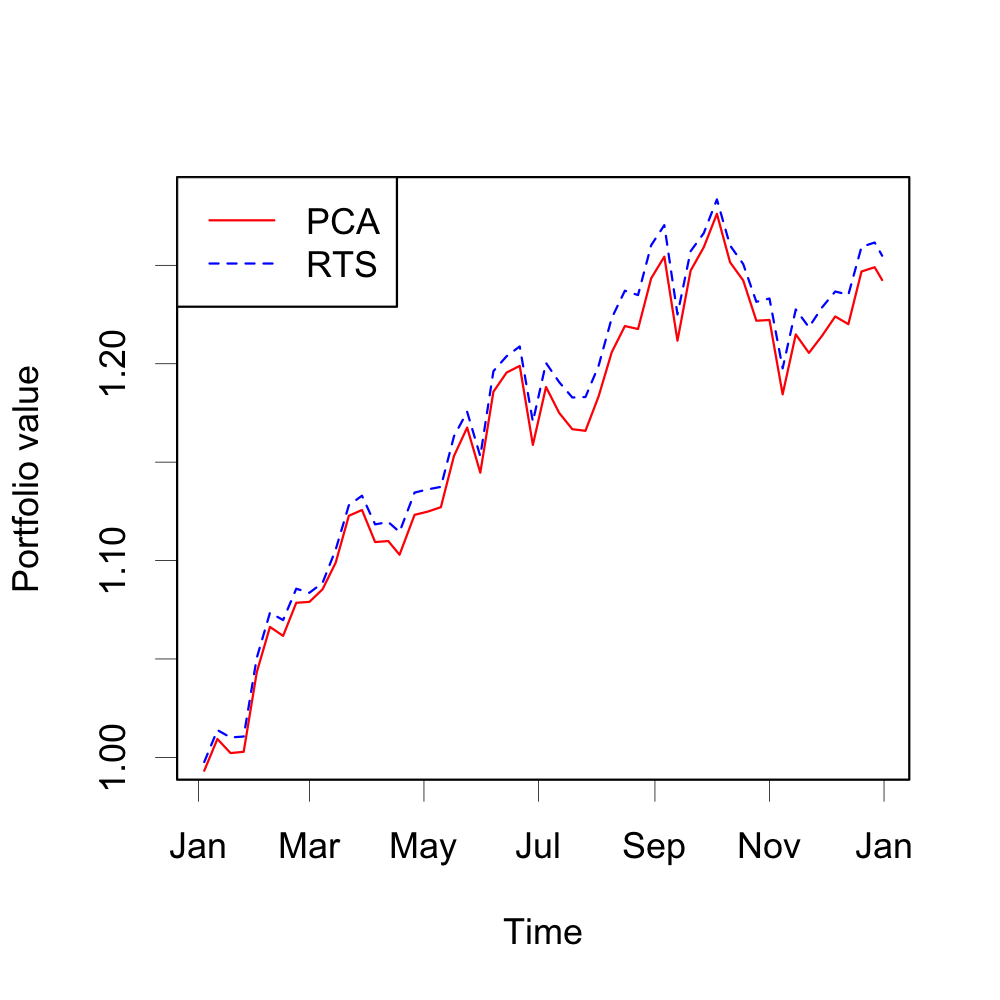

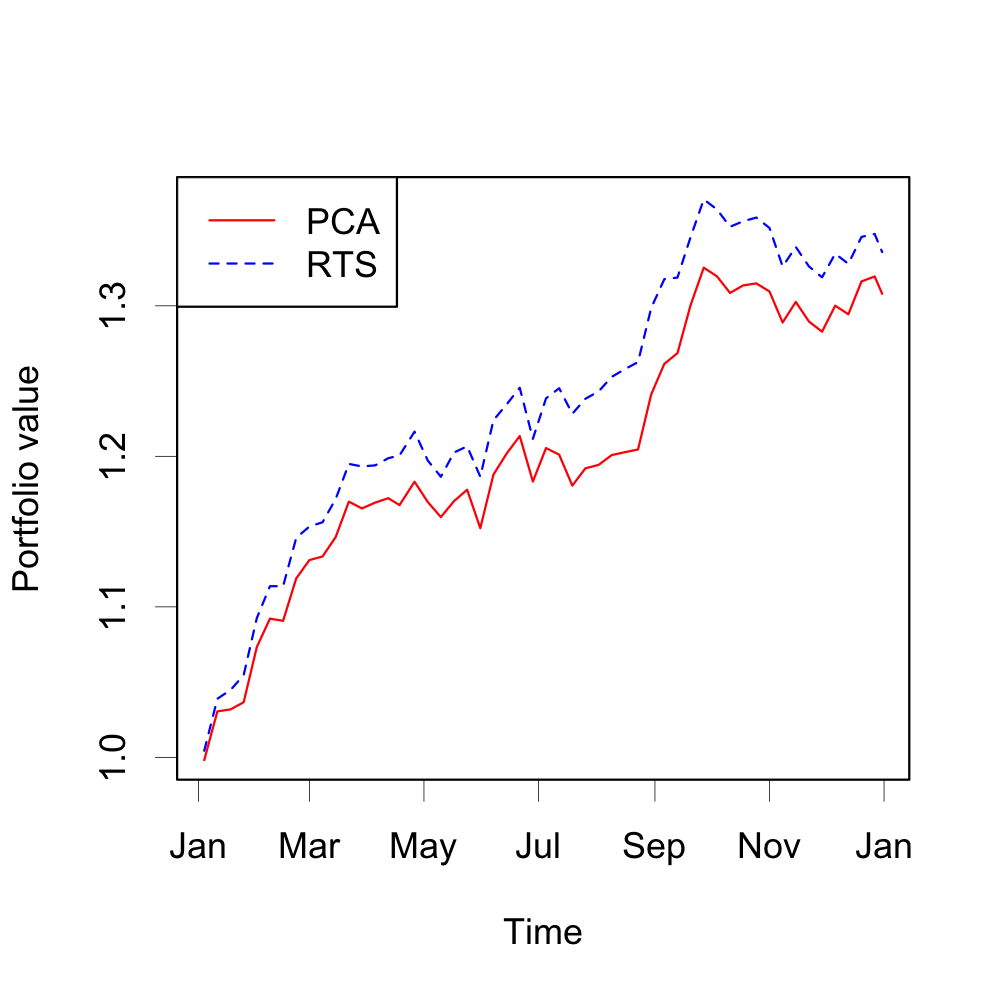

Firstly, we design a rolling scheme to evaluate the PCA and RTS methods based on their performances in the annual return by constructing risk-minimization portfolios. Given the scatter matrix of the share returns, a risk-minimization portfolio is given by

where determines the optimal weights on the shares. Since the scatter matrix is unknown in practice, we use the factor model with PCA or RTS method to estimate it. In detail, at the beginning of each week in the year 2019, we recursively use the returns during the past 52 weeks ( panel) to train factor models either by PCA or RTS method. The estimated common components and idiosyncratic errors are recorded as and , both of dimension . Then, we ignore the cross-sectional correlations of the idiosyncratic errors and estimate the scatter matrix of the 100 variables at week by

The portfolio weights are calculated using and the return of the portfolio at week is , where is the raw return vector at week . Figure 2 shows the net value curves of this strategy during the year 2019 by ignoring transaction cost and liquidity risk. It can be seen that when the factor models are trained by RTS method, the annual return of this portfolio is higher than that by PCA, regardless of taking or .

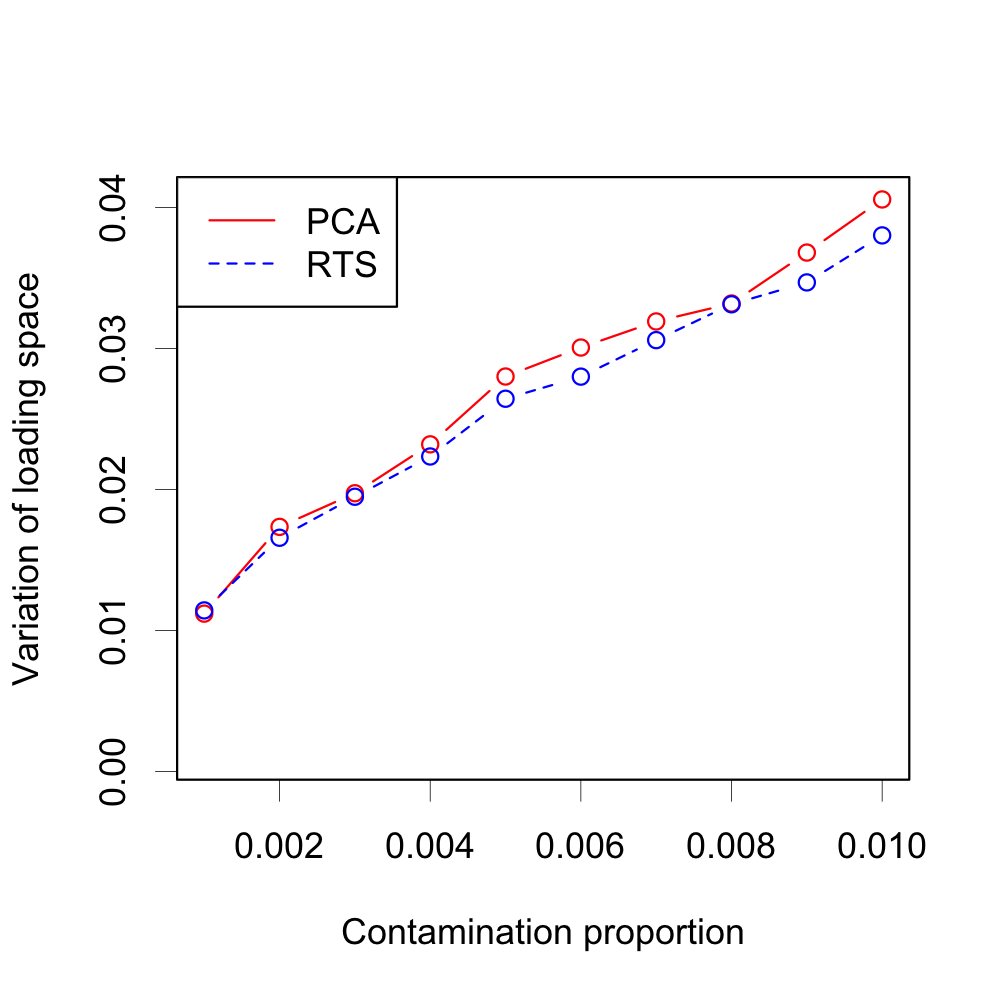

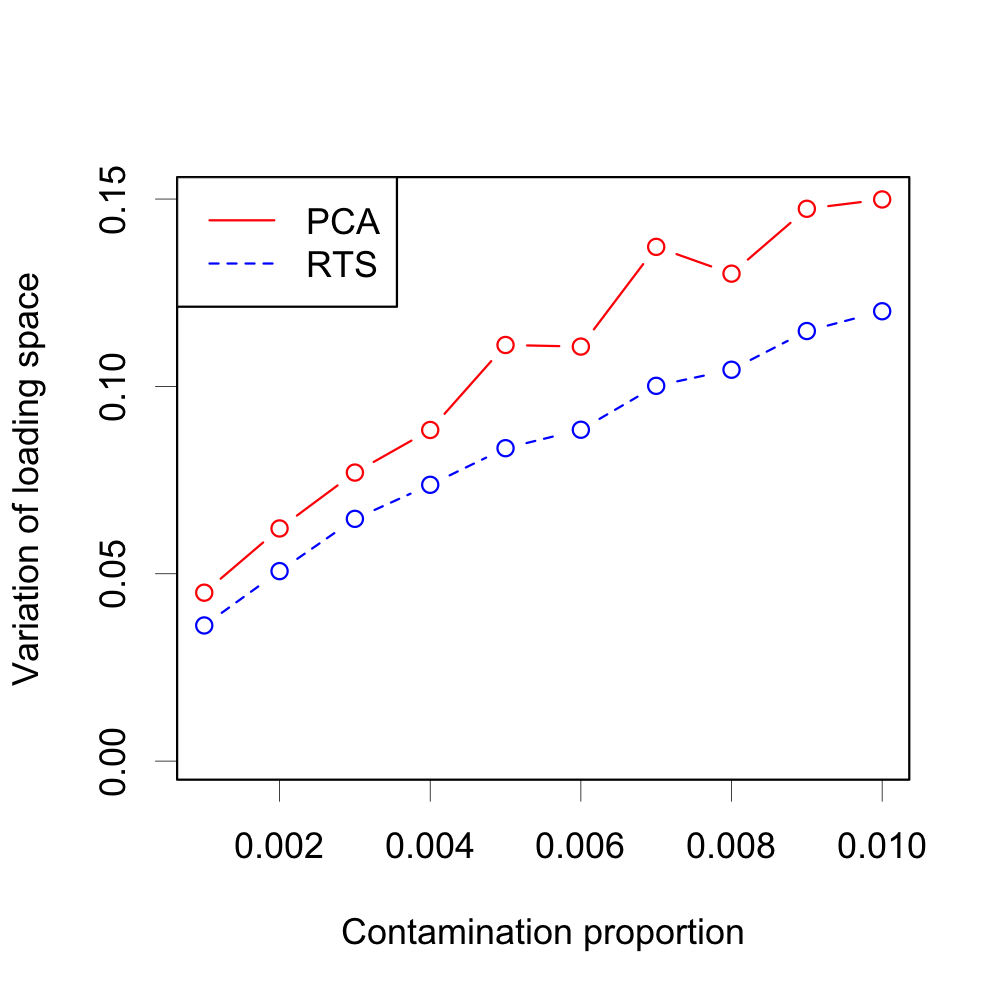

We then further compare the RTS and PCA methods by their sensitivity to outliers in this real example. The sensitivity is evaluated by the variation of estimated loading space , if we randomly select a small proportion of the demeaned log returns in the panel and double their values. We repeat the procedure for 100 times to reduce randomness, and report the mean variation in Figure 3 with various contamination levels. It’s seen that the estimated loading space can vary a lot with just a small number of outliers. When the contamination level grows, the discrepancy between the loading spaces becomes larger, and the phenomenon is more obvious in the case compared with . However, the RTS method is less sensitive to outliers than the PCA method in both cases, which is expected as the RTS is more robust.

6 Discussion

We proposed a robust two-step estimation procedure for large-dimensional elliptical factor model. In the first step, we estimate the factor loadings by the leading eigenvectors of the spatial Kendall’s tau matrix. In the second step, we resort to Ordinary Least Squares (OLS) regression to estimate the factor scores. We prove the consistency of the proposed estimators for factor loadings, scores and common components. Numerical studies show that the proposed procedure works comparably with the conventional PCA method when data are from Gaussian distribution while performs much better when data are heavy-tailed, which indicates that the proposed RTS procedure can be used as a safe replacement of the conventional PCA method.

In the future, we aim to propose a robust procedure for more general heavy-tailed data without the constraint of elliptical distribution. In fact, the elliptical assumption exerts a shape constraint on the distribution of the factors and the idiosyncratic errors, which may also constrain the real application. For more general case, we may consider the following optimization problem,

| (6.1) |

which is motivated by the equivalence of PCA and double least square estimation. We simply replace the quadratic loss function by the absolute loss function in (6.1) to achieve robustness. We may minimize the absolute loss function alternatively over and , each time optimizing one argument while keeping the other fixed. The theoretical analysis is more challenging and we leave this as a future work.

APPENDIX: PROOFS OF MAIN THEOREMS

Appendix A Proofs of Main Theorems

We first present three useful lemmas before we give the detailed proofs of main theorems. In the proofs, denotes some generic finite constant. We denote a random matrix of fixed dimensions as or when all of its entries are or .

Lemma A.1.

Assume that , then for any , we have

Proof.

Without loss of generality, we take for example. Define

then it’s easy to verify that

while by symmetry property,

∎

Lemma A.2.

Assume that , then for any deterministic matrix ,

Proof.

It’s sufficient to prove that the lemma holds with . Given a -dimensional deterministic vector , we have

By Lemma A.1, the second term is . For any we have

which concludes the lemma. ∎

Lemma A.3.

Under Assumptions A, B, C, as we have

Proof.

It is adapted from Lemma 3.1 and Lemma A.1 in Yu et al. (2019), so we omit the proof here. ∎

Proof of Theorem 3.1

Proof.

Define as the diagonal matrix composed of the leading eigenvalues of . Lemma A.3 implies that is asymptotically invertible, and . Because and is composed of the leading eigenvectors of , we have

Expand by its definition, then

For the ease of notations, we denote

and let , then

| (A.1) |

Lemma S2 to Lemma S4 in the online supplementary material show that

while

Therefore, by Cauchy-Schwartz inequality and triangular inequality, it’s easy to prove that

and the convergence rate for follows directly. To complete the proof, it remains to show . By Cauchy-Schwartz inequality,

Note that and , thus it holds that

which further implies , and concludes the theorem. ∎

Proof of Theorem 3.2

Proof.

Because , we have and is invertible with probability approaching to 1. By our robust estimation procedure,

Note that , then

Lemma S5 and Lemma S6 in our online supplementary material show that

Meanwhile, for any , by Assumption A and Lemma A.2 we have

Similarly, it’s not hard to prove that for any ,

Hence, by Cauchy-Schwartz inequality and triangular inequality, we have for any ,

which concludes the theorem.

∎

Proof of Theorem 3.3

References

- Ahn and Horenstein (2013) Ahn, S.C., Horenstein, A.R., 2013. Eigenvalue ratio test for the number of factors. Econometrica 81, 1203–1227.

- Bai (2003) Bai, J., 2003. Inferential theory for factor models of large dimensions. Econometrica 71, 135–171.

- Bai and Li (2012) Bai, J., Li, K., 2012. Statistical analysis of factor models of high dimension. The Annals of Statistics 40, 436–465.

- Bai and Li (2014) Bai, J., Li, K., 2014. Theory and methods of panel data models with interactive effects. The Annals of Statistics 42, 142–170.

- Bai and Li (2016) Bai, J., Li, K., 2016. Maximum likelihood estimation and inference for approximate factor models of high dimension. Review of Economics and Statistics 98, 298–309.

- Bai and Ng (2002) Bai, J., Ng, S., 2002. Determining the number of factors in approximate factor models. Econometrica 70, 191–221.

- Chamberlain and Rothschild (1983) Chamberlain, G., Rothschild, M., 1983. Arbitrage, factor structure, and mean-variance analysis on large asset markets. Econometrica 51, 1281–1304.

- Choi and Marden (1998) Choi, K., Marden, J., 1998. A multivariate version of kendall’s . Journal of Nonparametric Statistics 9, 261–293.

- Cont (2001) Cont, R., 2001. Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 223–236.

- Croux et al. (2002) Croux, C., Ollila, E., Oja, H., 2002. Sign and rank covariance matrices: statistical properties and application to principal components analysis, in: Statistical data analysis based on the L1-norm and related methods, pp. 257–269.

- Fama (1963) Fama, E.F., 1963. Mandelbrot and the stable paretian hypothesis. Journal of Business 36, 420–429.

- Fan et al. (2013) Fan, J., Liao, Y., Mincheva, M., 2013. Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 75, 603–680.

- Fan et al. (2018) Fan, J., Liu, H., Wang, W., 2018. Large covariance estimation through elliptical factor models. The Annals of Statistics 46, 1383–1414.

- Han and Liu (2012) Han, F., Liu, H., 2012. Semiparametric principal component analysis, in: Advances in Neural Information Processing Systems, pp. 171–179.

- Han and Liu (2014) Han, F., Liu, H., 2014. Scale-invariant sparse PCA on high-dimensional meta-elliptical data. Journal of the American Statistical Association 109, 275–287.

- Han and Liu (2018) Han, F., Liu, H., 2018. ECA: High-dimensional elliptical component analysis in non-gaussian distributions. Journal of the American Statistical Association 113, 252–268.

- Jing et al. (2012) Jing, B.Y., Kong, X.B., Liu, Z., 2012. Modeling high-frequency financial data by pure jump processes. The Annals of Statistics 40, 759–784.

- Kong et al. (2015) Kong, X.B., Liu, Z., Jing, B.Y., 2015. Testing for pure-jump processes for high-frequency data. The Annals of Statistics 43, 847–877.

- Marden (1999) Marden, J.I., 1999. Some robust estimates of principal components. Statistics & Probability Letters 43, 349–359.

- Onatski (2009) Onatski, A., 2009. Testing hypotheses about the number of factors in large factor models. Econometrica 77, 1447–1479.

- Stock and Watson (2002a) Stock, J.H., Watson, M.W., 2002a. Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association 97, 1167–1179.

- Stock and Watson (2002b) Stock, J.H., Watson, M.W., 2002b. Macroeconomic forecasting using diffusion indexes. Journal of Business & Economic Statistics 20, 147–162.

- Trapani (2018) Trapani, L., 2018. A randomised sequential procedure to determine the number of factors. Journal of the American Statistical Association 113, 1341–1349.

- Visuri et al. (2000) Visuri, S., Koivunen, V., Oja, H., 2000. Sign and rank covariance matrices. Journal of Statistical Planning & Inference 91, 557–575.

- Xia et al. (2017) Xia, Q., Liang, R., Wu, J., 2017. Transformed contribution ratio test for the number of factors in static approximate factor models. Computational Statistics & Data Analysis 112, 235–241.

- Yu et al. (2019) Yu, L., He, Y., Zhang, X., 2019. Robust factor number specification for large-dimensional elliptical factor model. Journal of Multivariate analysis 174, 104543.

Supplementary Material for “Large-dimensional Factor Analysis without Moment Constraints”

In the supplementary material, we give some useful lemmas and the corresponding detailed proofs. Lemma S1 provides some technical error bounds which facilitate presentation of the following proofs. Lemma S2 to Lemma S6 are critical to the proof of the main theorems and are mentioned in the main paper. We let and denote some generic random matrices in our proof and can be nonidentical in different lemmas. For two series and , means that as (or for random series).

Lemma S1. Under Assumptions A, B, C, as we have

where is the loading matrix and is the scatter matrix of .

Proof.

Because is positive definite, we have is always positive definite and invertible. Denote the Singular Value Decomposition (SVD) of as . is orthogonal matrix. The upper sub-matrix of () is diagonal and denoted as , while the left are 0. is orthogonal matrix. Hence, the diagonal entries of are of order and

Partitioning into where is submatrix, then is invertible, for and

By Cauchy-Schwartz inequality, it’s easy to prove that , then the first part of this lemma holds.

For the second part, denote the eigenvalue decomposition of as , where is composed of the leading eigenvectors. By Weyl’s theorem, it’s easy to prove that for and for . Hence, by definition,

Let , then and

Therefore,

Further,

Hence, by Cauchy-Schwartz inequality,

Now, we can calculate that

which concludes the second part of the lemma. ∎

Lemma S2. Under Assumptions A, B, C, as , we have

where and are defined in the proof of Theorem 3.1.

Proof.

Note that is ’s transpose so we only show the result with . Assume is even and , otherwise we can delete the last observation. Given a permutation of , denoted as , let , and be the rearranged factors, errors and observations, further define

Denote as the set containing all the permutations of , then it’s not hard to prove that

That is,

Now take as given, i.e., which is the original order. By the property of elliptical distribution, for any ,

where is determined by . and is independent of . . Hence,

where is composed of the first entries of and is composed of the left ones. Note that and are independently and identically distributed when , so

| (1.2) |

We first focus on the matrix . Define

where , then and are independent and

As a result,

| (1.3) |

Because and are zero-mean independent Gaussian vectors, we have

where is a Chi-square random variable with degree . Hence,

| (1.4) |

By Lemma S1, , then we have

| (1.5) |

For the second term, denote the spectral decomposition of as , then

Denote

then is diagonal with positive diagonal entries and

Consequently,

| (1.6) |

Now we move to the calculation of . Note that

then by Cauchy-Schwartz inequality,

As a result,

which concludes the lemma. ∎

Lemma S3. Under Assumptions A, B, C, we have and .

Proof.

Lemma S4. Under Assumptions A, B, C, we have

Proof.

By the decomposition that , we have

| (1.7) |

Lemma S5. Under Assumptions A, B, C, we have

Proof.

We will calculate the three error terms separately. Firstly, similarly to the proof of equations (1.2) and (1.3) in Lemma S2, we have

Then, it’s not hard to show that

As a result,

| (1.9) |

Similarly, and

| (1.10) |

For the last term, we can verify that

Some simple calculations lead to

Hence, and

| (1.11) |

Combine equations (1.8), (1.9), (1.10) and (1.11) we have

which concludes the lemma. ∎

Lemma S6. Under Assumptions A, B, C, we have for any ,

Proof.

Since are i.i.d., we assume . Apply equation (A.1) again, we have

| (1.12) |

We calculate the three error terms separately. Firstly by the definition of , we have

For the first term, by Cauchy-Schwartz inequality we have

By the proof of Lemma S2, for any ,

while by Lemma A.2 we have for any ,

Hence,

For the second term,

where and is independent of . By Lemma A.2,

Removing the first observations will not change the large-sample property of , then

As a result,

| (1.13) |

Secondly, it’s easy that

| (1.14) |