The implied Sharpe ratio

Abstract

In an incomplete market, including liquidly-traded European options in an investment portfolio could potentially improve the expected terminal utility for a risk-averse investor. However, unlike the Sharpe ratio, which provides a concise measure of the relative investment attractiveness of different underlying risky assets, there is no such measure available to help investors choose among the different European options. We introduce a new concept – the implied Sharpe ratio – which allows investors to make such a comparison in an incomplete financial market. Specifically, when comparing various European options, it is the option with the highest implied Sharpe ratio that, if included in an investor’s portfolio, will improve his expected utility the most. Through the method of Taylor series expansion of the state-dependent coefficients in a nonlinear partial differential equation, we also establish the behaviour of the implied Sharpe ratio with respect to an investor’s risk-aversion parameter. In a series of numerical studies, we compare the investment attractiveness of different European options by studying their implied Sharpe ratio.

Keywords: Sharpe ratio, PDE asymptotics, stochastic volatility, Heston, reciprocal Heston

1 Introduction

The Sharpe ratio, defined as the ratio of a portfolio’s expected return to its standard deviation, was introduced by Sharpe (1966) as a concise measure of mutual fund performance. Several other works have since used the idea under different settings to measure the performance of investment portfolios composed of risky assets. Jensen (1969) considered the effect of differential risk on required returns of different risky assets. Using a capital asset pricing model, he showed that the investment portfolios can be compared by looking at the difference between the actual returns on a portfolio and the expected returns on that portfolio conditional on its level of systematic risk and actual returns of the market portfolio. Another approach towards portfolio selection was proposed by Merton (1969) in which he incorporated the risk-preference of the investor through the risk-aversion parameter of a utility function. He considered an investor that trades risky assets in the market to maximise his expected terminal utility. Under the assumption that the log-asset returns are normally distributed with a constant Sharpe ratio, he showed that, assuming a constant relative risk-aversion utility function, the investor derives a higher expected utility from assets with higher Sharpe ratio.

Hodges and Neuberger (1989) used the idea of expected utility maximisation to create optimal replication portfolios for contingent claims in a market with transaction costs. Their work led to the idea of indifference pricing of contingent claims in incomplete markets (see Carmona (2008) for a collection of the related works). The framework of indifference pricing allows to identify an economically justifiable price of a contingent claim in an incomplete market. In such markets, it is not possible to perfectly replicate any contingent claim using a self-financing portfolio of the underlying risky assets and determine a unique price (see, for example, Section 10.3 Delbaen and Schachermayer (2006) for a complete mathematical characterisation of incomplete markets). Typically, the Hamilton-Jacobi-Bellman (HJB) equation satisfied by the indifference price is solved numerically. Recently, in an incomplete market framework based on a class of stochastic volatility models, Lorig (2018) approximately solved the HJB equation for the indifference price of a European option. He developed approximation techniques to solve nonlinear partial differential equations with state-dependent coefficients using a Taylor series expansion method developed in a series of papers: Pagliarani and Pascucci (2012), Lorig et al. (2015), Lorig et al. (2017). The corresponding approximate implied volatilities of the indifference prices are also provided by Lorig (2018).

As the underlying risky assets cannot be used to perfectly hedge a European option in an incomplete market, an investor looking to create an investment portfolio can benefit by including a European option in it. This raises an important question of how to measure the investment attractiveness of different European options available in the market. Similar to how the Sharpe ratio can be used to measure the performance of an underlying risky asset, in this paper we introduce the concept of an implied Sharpe ratio which can be viewed as a measure of a European option’s worth to an investor. Typically, the value of a European option is quantified in terms of its implied volatility. When comparing two options, it is the option with a higher implied volatility that is considered to be the more expensive option. However, an option’s implied volatility does not capture its worth to an investor. Relative to not owning the option, buying or selling an option at a given implied volatility may either increase or decrease an investor’s expected terminal utility. The implied Sharpe ratio, as defined in this work, aims to address the issue of measuring an option’s worth to an investor.

In the investment literature, the behavioural preference of an investor is captured through the risk-aversion parameter of his utility function. Many classical studies of investment under uncertainty derive comparative statics with respect to the risk-aversion parameter. For example, it is well established that a risk-averse investor is willing to pay a higher premium to insure himself against risk. Jewitt (1987) extended this classical comparative static of risk-aversion parameter in the presence of an extra source of uncertainty. Eeckhoudt et al. (1995) studied the impact of cost and price changes on the inventory of a risk-averse newsboy who must decide to purchase newspapers in order to sell them later. Similarly in our work, we aim to express the implied Sharpe ratio in terms of the model parameters and an investor’s risk-aversion parameter in order to help him choose between European options with different strikes and times-to-maturity.

The rest of the paper is organised as follows: In Section 2, we define the implied Sharpe ratio and prove its uniqueness and existence in a general market setting. In Section 3, we introduce a general local stochastic volatility model which is popular among the practitioners and derive the equation for the implied Sharpe ratio in terms of the model parameters and risk-aversion parameter. In Section 4, we use a Taylor series expansion technique to develop semi-explicit approximations of the implied Sharpe ratio. In Section 5 we study the particular forms of implied Sharpe ratio using different examples of local stochastic volatility models and illustrate its importance in identifying the most suitable European option for investment among the available choices. Mathematical proofs and a collection of formulas for calculating the implied Sharpe ratio under different models are presented in Appendices A–B.

2 The implied Sharpe ratio

Let us consider a frictionless financial market consisting of one risk-less asset with constant price and one non-dividend paying risky asset represented by a real-valued semi-martingale defined on a filtered probability space satisfying the usual conditions. Let denote the wealth process of an investor who invests in number of shares of at time starting from initial wealth level . Then, the wealth process satisfies

| (1) |

where is a real-valued predictable process such that the stochastic integral above is well defined. In addition, we assume that the investor also owns European-style contingent claims on the risky asset. Over a fixed time horizon the investor trades the risky asset in order to maximise his expected terminal utility. We suppose the investor’s utility function is strictly concave, strictly increasing and belongs to the class of infinitely differentiable functions. The value of the investment to investor is captured by a function defined as follows:

Definition 1.

The value function of an investor with wealth process (1) and who owns European-style contingent claims, each with payoff function is defined as

where is the set of admissible strategies given as

When the investor is a seller of the contingent claim, and when he is a buyer. If for a given European option payoff we can explicitly solve for we can find out whether the investor will prefer to sell or buy that European option. In an analogy to the Black-Scholes price of a European option, we define the Merton value function as the value function of an investor when we assume that the risky asset price follows a geometric Brownian motion.

Definition 2.

Suppose the risky asset dynamics is given by the Black-Scholes model in which , and where, is the expected rate of return, is the volatility and is a standard Brownian motion. The Merton value function of an investor with wealth process (1) is then defined as

where is the Sharpe ratio.

The Merton value function is an increasing function with respect to Thus, a risky asset with higher Sharpe ratio will lead to a higher Merton value function. Just as the implied volatility is used to link the market-observed European option price to the Black-Scholes model’s European option price, we define the implied Sharpe ratio to link an investor’s value function in a general risky-asset price model to the Merton value function in the Black-Scholes model.

Definition 3.

Suppose an investor with wealth process (1) owns European-style contingent claims with unit price Further suppose that for all and any Then, the implied Sharpe ratio is the unique positive solution of the equation

| (2) |

where is the Merton value function and is the investor’s value function.

According to the above definition, if an investor assumes that the risky asset price follows a geometric Brownian motion with Sharpe ratio and invests only in that risky asset, he will obtain the same expected utility as he would by investing in a portfolio composed of the risky asset and a European option, in a general risky-asset price model. European calls and puts are usually compared based on their implied volatilities. When plugged in the Black-Scholes model’s European call/put formula, implied volatility provides the market price of the option. However, it does not provide any measure of the option’s worth to an investor who is looking to maximize his expected terminal utility. The implied Sharpe ratio rectifies this shortcoming of implied volatility.

Through the implied Sharpe ratio, we can connect an investor’s value function in an incomplete market to the classical Merton value function In doing so, our aim is two-fold: First, by computing the implied Sharpe ratio for (buying the option) or (selling the option), we can compare it to the case (no position in the option). From Definition 3, it is clear that a higher implied Sharpe ratio, compared to the other possibilities, will deliver a higher value to an investor who is looking to maximise his expected terminal utility over a finite time horizon. Thus, the implied Sharpe ratio can tell us whether buying () or selling () a contingent claim can improve the investor’s utility as opposed to just investing in the risky asset () underlying the option. This comparison can also be made directly by comparing the value functions corresponding to the different possibilities (). However, as we will see later, in the case of an exponential utility function, the implied Sharpe ratio is independent of the starting wealth level. Thus, it provides a standard measure of investment worth as opposed to the value function which is dependent on the starting level of wealth.

Second, by computing the implied Sharpe ratio for two European options with different strikes and maturities, we can compare their relative worth to an investor. The European option with the higher implied Sharpe ratio will be more attractive to the investor. Such a comparison can be made across the whole range of available European options, thus making the implied Sharpe ratio a better measure than the implied volatility to assess the worth of an option for investment. The implied volatility is a unitless quantity which provides a better comparison between different European options than their respective prices. In the same spirit, the implied Sharpe ratio allows a more intuitive comparison between the different European options than their respective expected utility values which is dependent on initial wealth. As mentioned earlier, in the case of an exponential utility function, the implied Sharpe ratio will be independent of the starting wealth level, thus making it a better choice than directly observing the value function, which depends on the starting wealth. Investors with different wealth levels can just use the implied Sharpe ratio to make informed investment decisions instead of using the value function. Next, we establish the theoretical result which ensures the existence and uniqueness of the implied Sharpe ratio.

Theorem 1.

The implied Sharpe ratio defined in (2) exists and is unique.

Proof.

The function is the solution of the following partial differential equation:

| (3) |

It is also strictly increasing and strictly concave with respect to the state variable . Thus, we have Next, suppose and let and denote the solutions to Equation (3) for and respectively. Then, we get

Therefore, is a subsolution to the equation solved by with the terminal condition which is independent of and Thus, we have that for and In other words, is strictly increasing in Moreover, for any which guarantees the existence and uniqueness of the solution to (2). ∎

In the next section, we study the implied Sharpe ratio in a class of incomplete market models that are Markov. In the absence of closed-form formulas of the implied Sharpe ratio, we use a Taylor series expansion technique for nolinear PDEs developed by Lorig (2018) to find semi-explicit approximation in terms of the risk-aversion parameter and other model parameters.

3 Markov market setting

To study the behaviour of the implied Sharpe ratio with respect to market parameters, we specialize to the setting of a Markov market model. We suppose that the dynamics of are of the following form

| (4) | ||||

| (5) |

where and are independent Brownian motions. We assume that the system of stochastic differential equations (3)-(5) admits a unique strong solution adapted to filtration Next, for units of currency invested in at time the investor’s wealth process satisfies the following equation

The value function of an investor with European-style options and initial wealth level is given as

| (6) |

Each European option with payoff function and maturity is assumed to have price , which is obtained by computing the expectation of the option’s payoff under the market’s chosen pricing measure. We adopt the primal approach to solve for and assume that the value function belongs to Under this assumption, by following the usual dynamic programming principle (see, for example, Chapter 3 Pham (2009)), satisfies the Hamilton-Jacobi-Bellman (HJB) equation

| (7) |

where the operators and are given as

The candidate optimal strategy is obtained by maximizing which gives us

| (8) |

In the above formula, we have suppressed the arguments for simplicity of notation. We will do so from now on, wherever it causes no confusion, in order to keep the notation manageable.

Inserting the optimal strategy in HJB equation (7) yields the following:

where the Hamiltonian is a nonlinear term given as

| (9) | ||||

| (10) |

Note that defined above is the instantaneous Sharpe ratio of the risky asset . In the rest of the study, we fix the utility function to be of the exponential form:

where is the risk-aversion parameter. This choice of utility function allows us to obtain a form of the implied Sharpe ratio which is independent of the initial wealth level. The Merton value function in this case is given as

One can verify by direct substitution that the above expression satisfies (3). Inspired by the form of the Merton value function for exponential utility, we make the following ansatz to solve the HJB equation (9):

| (11) |

We find that the function satisfies the following equation

| (12) |

where the linear operator and the nonlinear operator are given by

To find a formula for the implied Sharpe ratio we solve the following equation

| (13) |

It can be checked that (13) is satisfied if and only if

| (14) |

where, as a reminder, is the price of the European option with payoff , as computed under the market’s chosen pricing measure. As is independent of we can obtain a relationship between the implied Sharpe ratio and investor’s risk-aversion parameter by solving for In equation (12), we observe that depends on only through the terminal condition. However, due to the presence of non-linearity in (12), deriving a closed-form formula for the relationship between and is not possible. Even without the non-linearity in (12), the standard theory of partial differential equations (see Chapter 2, Section 4 Friedman (2008)) is not directly applicable to derive the relationship.

4 Asymptotic approximation formulas

In this section, we will use a Taylor series expansion method, as developed by Lorig (2018), to derive asymptotic approximations for , the option price and the implied Sharpe ratio .

4.1 Asymptotic approximation formulas for

Let be any of the coefficient functions appearing in the operators or that is

Next, fix a point and define the following family of functions indexed by

| (15) |

Observe that

Suppose the functions are analytic in a neighbourhood of so that we have

For the final -th order approximation formula, we will only need the functions to be -times differentiable. However, it will simplify the presentation if, for now, we assume the stronger condition of analyticity. Using the coefficient functions indexed by , consider the following family of PDEs indexed by

| (16) |

where and are obtained from and and by replacing the coefficients in these operators with their -counterparts defined in (15)

Next, we suppose that is given in powers of as

| (17) |

Once we are able to solve for each the asymptotic approximation of is obtained by setting in (17). To obtain the respective order terms we insert the expansion of into (16) and collect the terms of like powers of . At the lowest order of we have the following

where we have defined

| (18) |

In the above, is a constant coefficient differential operator since we have that It can be seen that is only a function of As such the equation becomes

| (19) |

The higher order terms are given as

| (20) |

where the source terms are given as

In particular, the first and second order source terms are given by

| (21) | |||||

| (22) |

Before, we proceed to solve for terms we state a few fundamental results which will be useful for our calculations. The constant coefficient elliptic operator in (19), gives rise to the semigroup defined by

| (23) |

where is a generic test function and is the fundamental solution to the linear operator given as

The covariance matrix and vector are given as

The semigroup satisfies the following property:

By Duhamel’s principle, the unique classical solution (if it exists) to any PDE of the form:

is given as

In the above we have omitted the arguments for simplicity of notation. To obtain the terms in the expansion of and it will also be helpful to introduce the following operators

| (24) | |||||

| (25) |

By direct computations, we can check that the operators and commute and have the following property

| (26) |

Therefore, if function is a polynomial of and we have

| (27) |

It is assumed above and throughout the following computations that if an operator is followed by nothing, it acts on the constant 1. Next, we also introduce the following operator

| (28) |

where the notation indicates that the -dependence in coefficients has been replaced with For example, in the term

becomes

The following result is now in order:

Lemma 2 (Lemma 3.7 Lorig (2018)).

To obtain semi-explicit approximation formulas, we fix the European option payoff function as a call option, that is, where is the log strike. Using this choice of we obtain the second order approximation of in (17) using the following result:

Proposition 3.

Proof.

See Appendix A. ∎

To study the effect of the risk-aversion parameter on the implied Sharpe ratio we derive the asymptotic approximation formula only up to the second order. The second order approximation is sufficient to perform a comparative-static study with respect to the risk-aversion parameter.

4.2 Asymptotic approximation formulas for

In an incomplete market, the investors may not agree on their choice of the pricing measure. Thus, price of the European option with payoff will depend on the chosen model. In our study, as we fix the model for our reference investor in (3)-(5), it makes sense to obtain under the appropriate pricing measure based on the model instead of using a market-given European option price.

We suppose that the pricing measure is related to the physical measure through the following Radon-Nikodym derivative:

| (29) |

Defining -Brownian motions and by

we see that the dynamics of can be written under as

where the function is given as

The price of a European-style option with payoff function with having risk-neutral dynamics under is given as

where denotes the expectation operator under defined in (29). The function satisfies the linear pricing PDE

where To obtain asymptotic approximation formulas, once again we seek a solution to the following family of PDEs

where is the -counterpart of obtained by replacing the coefficients in it with their -counterparts. Upon collecting the terms of like order of we find that the individual terms satisfy

| (30) | |||||||

| (31) |

where the th-order source term is given by

| (32) |

and is given by

Like in Section 4.1, gives rise to a semigroup defined by

where is a generic test function and is the fundamental solution to the linear operator given as

The covariance matrix and vector are given as

Analogous to and in Section 4.1, we define and as follows:

The operators and satisfy the same properties as and respectively, in Section 4.1. We obtain the following result for approximation of the European option price

Proposition 4.

Proof.

See Appendix A. ∎

4.3 Asymptotic approximation formulas for

We use the results in Proposition 3 and 4 to obtain an asymptotic formula for the implied Sharpe ratio Let us define is the positive solution of the following equation

| (33) |

which is obtained by replacing and in (14) by their counterparts. Recalling that and , it follows that . Thus, in order to find an asymptotic approximation for , we expand in powers of as follows

Once we obtain expressions for , our -th order approximation for will be obtained by truncating the above series at order and setting . In order to find explicit expressions for the terms we insert the expansions for , and into (33) and collect terms of like order in . We obtain

By solving for we obtain

Proposition 5.

Let be the unique classical solution of (30) and and be the unique classical solutions of (31) with source terms and , respectively, obtained from (32). Furthermore, let be the unique classical solution of (19) and and be the unique classical solutions of (20) with source terms (21) and (22), respectively. Assume that the coefficients and belong to the class of functions. Then, the second order approximation of the implied Sharpe ratio, defined as

is given explicitly by

The above result provides an approximate relationship between , the risk-aversion parameter and the instantaneous Sharpe ratio

Remark 1.

If we set in (29), the pricing measure corresponds to the minimal martingale measure as defined in Follmer and Schweizer (1991)

Moreover, if the market’s chosen pricing measure is the minimal marrtingale measure (), then the operators defined in Section 4.2 become identical to the operators respectively, as defined in Section 4.1. With as the chosen pricing measure, the first and second order correction terms in the approximation of simplify to:

| (34) | ||||

| (35) |

and the zeroth order term remains unaffected.

5 Examples

In this section, we consider different local stochastic volatility models which provide different functional forms of Using our approximation result in Proposition 5, we discuss its practical implications. For the purpose of simplification of presentation, we will assume that the pricing measure corresponds to the minimal martingale measure

5.1 Heston model

We first consider the famous Heston’s stochastic volatility model, which under the physical measure is given as

Comparing the above model with our formulation in (3), we have

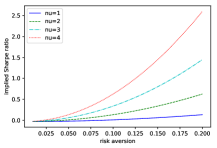

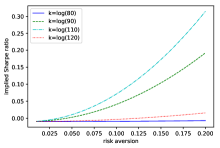

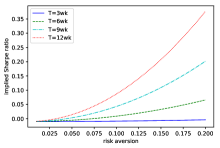

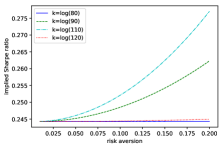

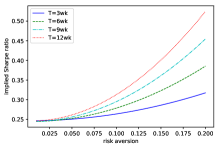

We suppose the following form of This particular choice keeps the model in the affine class (see Duffee (2002)). Other forms of the function can also be considered. For the chosen , we plot the second order approximation of the implied Sharpe ratio in Figure 1 with respect to the risk-aversion parameter for We observe that including European options in the investment portfolio increases the implied Sharpe ratio and its impact is greater for an investor with a higher value of . Thus, a risk-averse investor is better off including an European option in his portfolio when considering to invest using the utility maximisation approach.

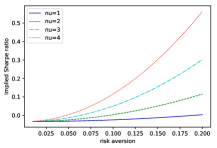

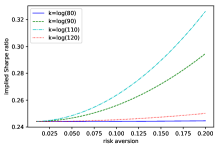

To compare different European options we plot the second order approximation of the implied Sharpe ratio with respect to the risk-aversion parameter for different values of log-strike and maturity in Figure 2 and Figure 3, respectively. In Figure 2, we observe that for a fixed maturity and the chosen parameter values, near-the-money European call options provide better implied Sharpe ratio than the far-from-the-money European options. Moreover, this impact is more pronounced for an investor with higher value of Thus, a risk-averse investor should consider to include near-the-money European options in the investment portfolio.

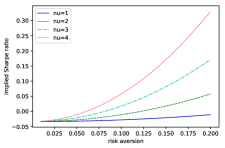

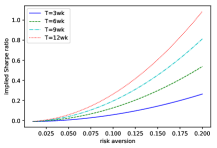

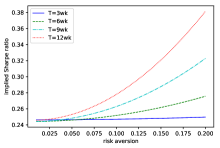

In Figure 3, we observe that for the chosen parameter values, the investor’s implied Sharpe ratio increases with increasing maturity irrespective of the moneyness of the European call option, with an increasing impact for higher values of . Thus, under the Heston model with the chosen form of the risk-averse investor should consider to include European options with longer time-to-maturity over options with shorter time-to-maturity.

5.2 Reciprocal Heston model

We consider another stochastic volatility model, which under the physical measure is given as

The above model is referred as reciprocal Heston model as is the reciprocal of a CIR process. Comparing the above model with our formulation in (3), we get that

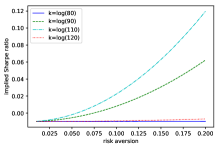

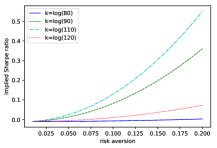

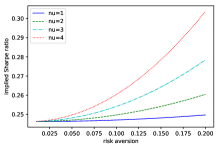

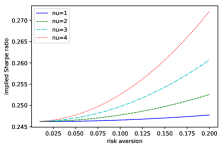

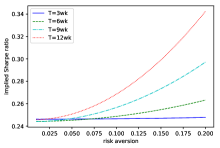

where must satisfy the usual Feller condition: This model choice leads to the functional choice of which is different from the choice of in Section 5.1. Once again we plot the second order approximation of the implied Sharpe ratio with respect to the risk-aversion parameter in Figure 4. We observe that in the reciprocal Heston model, the implied Sharpe ratio of a risk-averse investor increases by including the European option in the investment portfolio.

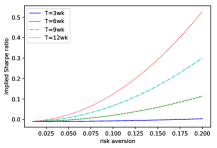

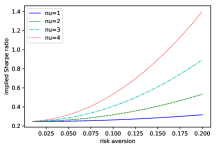

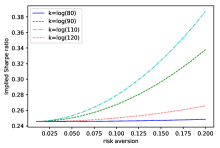

We also compare different European options by plotting the second order approximation of the implied Sharpe ratio with respect to the risk-aversion parameter for different values of log-strike and maturity in Figure 5 and Figure 6, respectively. In Figure 5, we observe that for a fixed maturity and the chosen parameter values, far-from-the-money European call options provide lower implied Sharpe ratio compared to the near-the-money options.

6 Conclusion

In this work, we introduced a new concept of the implied Sharpe ratio which allows a risk-averse investor to compare the worthiness of different European options for investment. In a general market setting, we prove the existence and uniqueness of the implied Sharpe ratio and derive its asymptotic approximation formulas under general local stochastic volatility models. In two stochastic volatility model settings, we used the implied Sharpe ratio approximation formulas to observe that including a European option in the investment portfolio increases the investor’s utility. Moreover, we observed that near-the-money and longer maturity options provide higher implied Sharpe ratio than far-from-the-money and shorter maturity options, respectively.

References

- Carmona (2008) Carmona, R. (2008). Indifference pricing: theory and applications. Princeton University Press.

- Delbaen and Schachermayer (2006) Delbaen, F. and W. Schachermayer (2006). The mathematics of arbitrage. Springer Science & Business Media.

- Duffee (2002) Duffee, G. R. (2002). Term premia and interest rate forecasts in affine models. The Journal of Finance 57(1), 405–443.

- Eeckhoudt et al. (1995) Eeckhoudt, L., C. Gollier, and H. Schlesinger (1995). The risk-averse (and prudent) newsboy. Management science 41(5), 786–794.

- Follmer and Schweizer (1991) Follmer, H. and M. Schweizer (1991). Hedging of contingent claims. Applied stochastic analysis 5, 389.

- Friedman (2008) Friedman, A. (2008). Partial differential equations of parabolic type. Courier Dover Publications.

- Hodges and Neuberger (1989) Hodges, S. D. and A. Neuberger (1989). Optimal replication of contingent claims under transaction costs. The Review of Futures Markets 8(2), 222–239.

- Jensen (1969) Jensen, M. C. (1969). Risk, the pricing of capital assets, and the evaluation of investment portfolios. Journal of business 42(2), 167–247.

- Jewitt (1987) Jewitt, I. (1987). Risk aversion and the choice between risky prospects: the preservation of comparative statics results. The Review of Economic Studies 54(1), 73–85.

- Lorig (2018) Lorig, M. (2018). Indifference prices and implied volatilities. Mathematical Finance 28(1), 372–408.

- Lorig et al. (2015) Lorig, M., S. Pagliarani, and A. Pascucci (2015). Analytical expansions for parabolic equations. SIAM Journal on Applied Mathematics 75(2), 468–491.

- Lorig et al. (2017) Lorig, M., S. Pagliarani, and A. Pascucci (2017). Explicit implied volatilities for multifactor local-stochastic volatility models. Mathematical Finance 27(3), 926–960.

- Merton (1969) Merton, R. C. (1969). Lifetime portfolio selection under uncertainty: The continuous-time case. The Review of Economics and Statistics, 247–257.

- Pagliarani and Pascucci (2012) Pagliarani, S. and A. Pascucci (2012). Analytical approximation of the transition density in a local volatility model. Central European Journal of Mathematics 10(1), 250–270.

- Pham (2009) Pham, H. (2009). Continuous-time stochastic control and optimization with financial applications, Volume 61. Springer Science & Business Media.

- Sharpe (1966) Sharpe, W. F. (1966). Mutual fund performance. The Journal of Business 39(1), 119–138.

Appendix A Proofs

Proof of Proposition 3.

By applying Duhamel’s principle in (19), we see that the zeroth order term is given as

where

denotes the price of a European call option in a Black-Scholes model with volatility coefficient For the first order term, we have

Again by applying Duhamel’s principle, the results in Lemma 2 and (4.1), we get

In the above, we have also used the semi-group property of . For the second order term, we have

Once more, by Duhamel’s principle, we obtain

| (36) | ||||

| (37) |

In the above we note the following while using the results in Lemma 2 and the semi-group property of

Next, we have

| (38) |

First term can be computed as

The second term in (38) can be resolved as

The first of the two remaining terms in (36) can be computed using the property in (4.1):

The second term is computed as

| (39) | ||||

| (40) |

where we have defined and as

By straightforward computations, we have that

Next, we use the property in (26) to obtain the following:

To tackle the final term in (39), we note the following

Using the explicit expression for we obtain

where is the density function of standard normal distribution. Then, from the calculations in Appendix B of Lorig (2018), we obtain the following

∎

Proof of Proposition 4.

The linear operator is the infinitesimal generator of a diffusion in whose drift vector and covariance matrix are constant. Then, by Duhamel’s principle, the zeroth order term which is independent of is given as

where for standard normal cdf we have

For the first order term, we have the following equation

Once again, by using Duhamel’s principle, we obtain that

Then, by applying the result in Lemma 2, we get

Now, for the second order term, we have

By applying Duhamel’s principle, we get

From the result in Lemma 2 and the result for , we obtain that

∎