Elements of asymptotic theory with outer probability measures

Abstract.

Outer measures can be used for statistical inference in place of probability measures to bring flexibility in terms of model specification. The corresponding statistical procedures such as Bayesian inference, estimators or hypothesis testing need to be analysed in order to understand their behaviour, and motivate their use. In this article, we consider a class of outer measures based on the supremum of particular functions that we refer to as possibility functions. We then characterise the asymptotic behaviour of the corresponding Bayesian posterior uncertainties, from which the properties of the corresponding maximum a posteriori estimators can be deduced. These results are largely based on versions of both the law of large numbers and the central limit theorem that are adapted to possibility functions. Our motivation with outer measures is through the notion of uncertainty quantification, where verification of these procedures is of crucial importance. These introduced concepts shed a new light on some standard concepts such as the Fisher information and sufficient statistics and naturally strengthen the link between the frequentist and Bayesian approaches.

1. Formulation

The general objective of statistical inference is to find the true value of a parameter of interest given some observed data. The set of all possible parameters values is denoted . It is assumed that the observed data, denoted , is the realisation of a random variable on some observation space which is related to the parameter via a parametric family of probability distributions , often referred to as the likelihood. Different estimators for the true value of the parameter can then be considered, but the most common is the maximum likelihood estimator (MLE) (Hald, 1999; Aldrich, 1997), defined as

| (1.1) |

In the frequentist approach (Berger and Casella, 2001; Fisher, 1922), the uncertainty about the value of can be quantified via a confidence interval which is computed for a given confidence level. It is however important to note that it is the interval itself that is random (as a function of the observation ) so that it is the interval that has a coverage probability, i.e. a probability of containing the true parameter, instead of the parameter having some probability to be contained in the interval. From a computational viewpoint, the MLE is often relatively easy to compute; however, confidence intervals are usually more difficult to deal with and offer a limited understanding of the uncertainty about the parameter.

The principle of the Bayesian approach (Robert and Casella, 2013) is to infer the posterior probability distribution of a random variable of interest given the observed data. Even if the quantity of interest is fixed, the uncertainty about this quantity is modelled as a random variable on some space related to , e.g. . One can then represent prior knowledge about as a probability distribution on and then, through Bayes’ formula, characterise the posterior distribution of as

| (1.2) |

for any , where the likelihood is now a conditional probability distribution defined for any . The integral in the denominator of (1.2) is called the marginal likelihood. In this context, the analogue of the MLE (1.1) is the maximum a posterior (MAP) estimate . Bayesian inference is generally more computationally demanding than frequentist inference but offers a full characterisation of the posterior uncertainty. For a given confidence level, a credible interval can be calculated. In this interpretation, it is the random variable that is contained in the fixed credible interval with a certain probability. The marginal likelihood is also a useful quantity as it reflects the coherence between the observation and the considered modelling. It appears naturally in hierarchical models where it can be interpreted as a likelihood for the higher-order parameters. However, it is often difficult to compute and most of the techniques in computational statistics avoid the explicit calculation of this term.

In spite of the ever increasing available computational resources, the determination of the posterior probability distribution can be difficult to achieve due to the complexity of the model, to the amount of data or to physical constraints such as in real-time applications. Furthermore, discrepancies between the model and the actual mechanisms underlying real data can be at the origin of a range of issues, from the unreliability of the computed posterior distributions to the divergence of the considered algorithm.

1.1. Proposed approach

The purpose of this article is to propose an alternative representation of uncertainty that will lead to 1) the strengthening of the connection between the frequentist and Bayesian approaches, with the objective of providing a more pragmatic computational framework, and to 2) the possibility of a less conservative modelling, with the objective of improving the overall robustness and decreasing the sensitivity to misspecification.

We follow the same premise as possibility theory (Dubois and Prade, 2015), which can be motivated as follows. As in the frequentist approach, we consider that the unknown true parameter of a statistical model is not random and, therefore, the uncertainty about this parameter might not be best modelled by a probability distribution on the set . When representing deterministic uncertainty with a probability measure , the most stringent assumption is additivity. Indeed, if there is no available information regarding as an element of , one might not be able to define a meaningful credibility for the event for some in a way that verifies with the complement of in . Instead, it would be convenient to have a measure of credibility for which both and could have a credibility equal to if there is no objection against these events. When removing the assumption of additivity from the concept of probability measure, one obtains the concept of outer measure. Since we still want the corresponding set function, say , to give value to the entire parameter set , we call an outer probability measure (o.p.m.). The corresponding type of uncertainty, which relates to non-random phenomena, is often referred to as epistemic uncertainty (Shackle, 1961; Walley, 1991). The two main differences between o.p.m.s and probability measures are that 1) they are sub-additive, i.e. for any and the equality does not have to hold even if and are disjoint, and 2) they can be evaluated on all subsets, hence avoiding some measure-theoretic technicalities even though they have been mostly used as a measure-theoretic tool, e.g. for constructing the Lebesgue measure. In particular, up to measurability conditions, a probability measure can be seen as a special case of an o.p.m.

In the case where there is no information about whether is in or not, one would like to set . Seeing the value that a probability measure gives to a subset as an integral of the corresponding p.d.f., also denoted by , over the set , i.e. , it is natural to seek an analogous expression for an o.p.m. on . An operator allowing for is the maximum, or, more generally the supremum. We therefore consider , with a suitable function. The assumptions on yield the constraints and . Although these functions are called possibility distributions in possibility theory, we refer to them as possibility functions so as to better distinguish them from probability distributions.

In order to characterise the relations between different unknown quantities of interest, it is useful to introduce an analogue of the concept of random variable as follows: let be the sample space for deterministic but uncertain phenomena, then an uncertain variable111The concept of uncertain variable as introduced by Houssineau (2018a) includes both random and deterministic forms of uncertainty; in that context, uncertain variables as introduced here would be called deterministic uncertain variables on is a surjective mapping222Assuming that the mapping is surjective is not a limitation since can always be made large enough to satisfy it. from to . The main differences with a random variable are that the sample space is not equipped with a -algebra and a probability measure, and there is no measurability condition on the mapping; instead, there is a true “state of nature” which is such that is the true value of the parameter. Yet, the concepts of realisation and event are meaningful for uncertain variables. Since possibility functions only model information, it follows that an uncertain variable does not induce a unique possibility function. Instead, different possibility functions represent different levels of knowledge about an uncertain variable. For this reason, we say that a possibility function describes an uncertain variable. Analogous constructions have been considered in (Del Moral and Doisy, 1999, 2000), where a connection between probability theory and control theory has been made in the context of algebras (Butkovič, 2010; Maslov, 1992), as well as in (Terán, 2014), where a law of large numbers is derived for a fuzzy-set-related notion of mean value (Carlsson and Fullér, 2001). Constantinou and Dawid (2017) also considered extending statistical concepts to non-random variables in the context of causal inference.

The ultimate goal of the proposed approach is to allow for inference to be performed in the presence of both deterministic and random sources of uncertainty so that the different components of complex statistical models can be modelled as faithfully as possible. One way of achieving this goal is to consider more general o.p.m.s of the form

with a subset of some given set and a measurable subset of , where represents the uncertainty about the true parameter in and is described by a possibility function on and where is a random variable on characterising the random components of the model with law . These o.p.m.s are studied more formally in Houssineau (2018a) and their application in the context of Bayesian inference for some complex systems is considered in Houssineau (2018b). Applying Bayes’ theorem to the o.p.m. yields

| (1.3) |

When the prior possibility function is equal to the indicator function of , denoted , which corresponds to the case where there is no information about , this posterior possibility function can be written as with the MLE. The idea of considering quantities of the form (1.3) has been discussed in the literature, see for instance (Chen, 1995; Walley and Moral, 1999); however, some of the theoretical foundations backing this approach are lacking.

Remark 1.1.

The quantification of uncertainty in frequentist inference is directly related to the true value of the parameter but can only be interpreted across different realisations of the observation. Bayesian posterior probability distributions focus on one realisation of the observation but assume the parameter to be random. The posterior quantification of uncertainty provided by focuses on one realisation of the observation and on the true value of the parameter. An important consequence is that greater prior uncertainty would typically reduce the posterior probability of a given event in the standard Bayesian framework whereas the posterior credibility of the same event will tend to increase in the same situation when using possibility functions. This aspect is particularly important in decision theory (Grünwald and Dawid, 2004; Smith, 2010).

In general, we might want to include prior information and consider an informative prior possibility function , that is for some . One way to obtain such possibility functions is to simply renormalise a bounded probability distribution, e.g. the normal possibility function with parameters and is defined as

| (1.4) |

We will show in Section 3 that and can be rightfully referred to as the expected value and the variance respectively. For the sake of simplicity, we will write when referring to the function . It would be more natural to parametrise the normal possibility function by the precision since the case is well-defined and corresponds to the uninformative possibility function equal to everywhere; yet, the parametrisation by the variance is considered for the sake of consistency with the probabilistic case.

It is important to extend widely-used probabilistic concepts to uncertain variables: consider two uncertain variables and on the respective spaces and and assume that these uncertain variables are jointly described by the possibility function on , then and are said to be independently described if there exists possibility functions and such that for any . This notion of independence models that the information we hold about is not related to and conversely. Another connection with standard statistical techniques can be made via the profile likelihood (Murphy and Van der Vaart, 2000) using the change of variable formula for possibility functions. Indeed, if is an uncertain variable on described by then, for any mapping , the uncertain variable can be described by

| (1.5) |

for any , where we can ensure that the inverse image is non-empty by assuming that is surjective, otherwise the appropriate convention is . Unlike the change of variable formula for p.d.f.s, (1.5) does not contain a Jacobian term since is not a density even when, say, . In the case where and , we find that , which is the analogue of marginalisation (Zadeh, 1978). This operation is often used when the number of parameters is too high and one wants to remove nuisance parameters. The motivation behind profile likelihood is shown here to be consistent with the general treatment of possibility functions, as detailed below in Example 1.2. There are existing results on the identifiability analysis (Raue et al., 2009) and uncertainty analysis (Vanlier et al., 2012) associated with profile likelihoods. If and are two uncertain variables on , jointly described by the possibility function then, using the change of variable formula (1.5), one can show that the uncertain variable , for any scalar , is described by

| (1.6) |

This formula is well known in possibility theory, see e.g. (Dubois and Prade, 1981). From a computational viewpoint, the expression of the possibility function describing is simpler than in the probabilistic case. We can easily show via (1.6) that the normal possibility function shares some of the properties of its probabilistic analogue. Indeed, if is an uncertain variable described by the possibility function then for any scalar , the uncertain variable is described by .

The concept of uncertain variable is also useful in the context of hypothesis testing because the different hypotheses, say, versus , corresponds to events which have non-zero credibility in general, e.g. the credibility of the event when is described by the possibility function is . Discussions about hypothesis testing can be found in Section 4.2.2.

This article aims to exploit further the principles introduced so far to define a likelihood for possibility functions, derive its usual asymptotic properties, and highlight the consequences of such modelling for estimation purposes. Therefore, we consider a conditional possibility function , , which describes the observation process, and we model the uncertainty about the true value of the parameter by an uncertain variable on . For a given possibility function modelling the prior knowledge about , the associated posterior possibility function is

| (1.7) |

This form of conditioning follows from applying Bayes’ rule in the context of possibility theory (De Baets et al., 1999). The marginal likelihood

is always a dimensionless scalar in the interval which can be easily interpreted as the degree of coherence between the model and the data. This is not the case when using the likelihood in general. This advantage, however, does not come for free since a value of that is close to one does not imply that the considered model is a good model, it only implies that the observation is compatible with the model. For instance, if there is no information about the observation process, then one can set , in which case any observation will receive the maximal marginal likelihood, i.e. for any . Although this might make the implementation of some tasks like model selection more challenging, it could also make other tasks such as checking for prior-data conflicts (Evans and Moshonov, 2006) more straightforward. With these additional notations, we can now come back to the topic of profile likelihood in the following example.

Example 1.2.

If there is no prior knowledge about , then one can set so that the posterior possibility function simplifies to

which can be seen as an inversion of the conditioning between and . If the uncertain variable is of the form , with and some uncertain variables on and respectively, and if we marginalise the variable , then we find that the marginal posterior possibility function describing is

Inverting the conditioning once again, we obtain the likelihood for only as

| (1.8) |

which justifies the maximisation over nuisance parameters in the profile likelihood. This also shows that care must be taken when considering the marginal likelihood since (1.8) contains a normalising constant.

In terms of interpretation, we do not view the possibility function as an upper bound for the true likelihood as suggested in (Dubois et al., 1995); instead, simply relates some characteristics of the data generating process of interest, expressed via the parameter , to the observation . This aspect will be further developed in the following sections. In the situation where there are several data points , we proceed consistently with the usual treatment and assume that these data points are realisations of uncertain variables that are conditionally-independently described by given . It follows that the associated posterior possibility function takes the form

where stands for the sequence . The practical motivation for considering a conditional possibility function as a likelihood comes from the need to derive equivalent tools for understanding the asymptotic behaviour of estimators when there is little knowledge about the true form of the distribution of the observations, as is often the case with real data. The analysis of statistical techniques expressed in this formalism will be conducted by simply relying on .

We have considered two possible models for the likelihood: as a probability distribution (1.3) or as a possibility function (1.7). In fact any conditional o.p.m. could be used as a likelihood. Crucially, the nature of the likelihood has no bearing on the nature of the posterior uncertainty. Indeed, if the prior is a possibility function then so will be the posterior. In particular, this highlights that although the information contained in the prior might be forgotten as the number of observations increases, the nature of the prior as a probability distribution or as a possibility function is never forgotten. The nature of the prior should therefore be chosen at least as carefully as its shape.

The idea of replacing some or all of the probabilistic ingredients in statistical inference is not new. Fiducial inference as introduced by Fisher (1935) is probably one of the first examples of such an approach. M-estimators (Godambe, 1991) and quasi-likelihoods (Wedderburn, 1974) are also attempts at replacing the standard likelihood model. Alternatives to the standard approach can also be introduced using belief functions (Dempster, 1968; Shafer, 1976; Smets and Kennes, 1994). Recently, Bissiri et al. (2016) proposed the use of exponentiated loss functions as likelihoods in a Bayesian inference framework. The idea of using upper bounds in order to bring flexibility in the Bayesian approach is also common, for instance, the so-called provably approximately correct (PAC) Bayes method (Langford, 2005) aims to minimise the upper bound for a given loss function. In spite of these connections, the proposed approach differs in many aspects from the existing literature and, to the best of the authors’ knowledge, the asymptotic properties that are derived in this article are novel. We review some of the features of the generalised Bayesian inference framework proposed by Bissiri et al. (2016) in the next section.

1.2. Generalised Bayesian inference

The main contribution of Bissiri et al. (2016) is to motivate the use of a loss function to describe the relation between the data sampled from a true distribution on a set and a parameter of interest in a set . It is then demonstrated by Bissiri et al. (2016) from two different approaches that

is a consistent/optimal update rule for the subjective prior probability given a realisation of . In this, situation, the “true” parameter is argued to be the minimiser of the expected loss . In order to calibrate the losses with respect to the prior distributions and to the data, it is suggested by Bissiri et al. (2016) that an additional term with can be used to ensure non-negativity and can be standardised by assuming that for any , leading to an overall loss of the form

with an annealing-type inverse temperature controlling the influence of the data point on the posterior probability distribution.

The motivation behind this generalised Bayesian inference framework is very similar to the one underlying the introduction of possibility functions. In fact, the information provided by a loss function as well as the subjective beliefs held a priori are often of a non-stochastic nature. Therefore, assuming that possibility functions, and o.p.m.s in general, provide a suitable framework for manipulating information, it is sensible to use this framework together with the exponentiated loss functions studied by Bissiri et al. (2016). Moreover, exponentiating the reward yields

where and can be identified with the likelihood and with the prior respectively. It holds that to the power remains a possibility function for any and it will appear in further sections that this operation preserves the expected value of the underlying uncertain variable while dividing its variance by . The case of non-stochastic data is also mentioned by Bissiri et al. (2016), which furthers the connection with the proposed approach. Seeing the likelihood as being related to a loss function will provide insights in the theory developed in further sections and will facilitate the interpretation of some of the results.

1.3. Structure and contributions

There are a number of original contributions in this article and we highlight the most important ones here:

- 1)

-

2)

A law of large numbers (LLN) and a central limit theorem (CLT) are derived for uncertain variables in Section 3. These results lead to the introduction of meaningful definitions of expected value and variance for uncertain variables and confirm the fundamental role of the normal possibility function in the proposed approach. In particular, the considered notion of expected value is related to the mode and, therefore, to the MAP in a Bayesian setting. The variance is also shown to be strongly related to the notion of Fisher information. These results allow for defining notions of identifiability and consistency.

-

3)

Asymptotic properties of the posterior possibility function are studied Section 4 using the available information only. This is crucial in applications since the true sampling distribution is unavailable. The connection between Bayesian inference and frequentists techniques such as likelihood ratio tests (LRTs) is then strengthened by showing that their asymptotic behaviour can be deduced from the Bernstein-von Mises (BvM) theorem.

| Notation | Description | Equation |

|---|---|---|

| , | Sample space for uncertain variables and o.p.m. | |

| , , | Uncertain variables | |

| Normal distribution | ||

| Normal possibility function | (1.4) | |

| , | Expectation and variance w.r.t. | (3.1), (3.2) |

| Convergence in o.p.m. | (3.4) | |

| Observed information based on observations | (4.1) | |

| Fisher information based on | (4.2) |

1.4. Notations

Deriving elements of asymptotic theory in a new context requires the introduction of a number of notations. These new notations are described in Table 1 together with their standard counterparts. Unless stated otherwise, the considered sets , , and are all assumed to subsets of the real line. Partial derivatives w.r.t. , , and will be denoted by , , and respectively.

2. Statistical modelling with o.p.m.s

Standard statistical inference uses a range of notions and techniques for the purpose of modelling, inference and analysis which are mostly based on probabilistic concepts. Introducing an alternative representation of uncertainty means that most, if not all, of these fundamental notions and techniques must be redefined. We show in this section that this can however be done easily without loosing the associated interpretations.

Location and scale parameters.

We consider a likelihood function of the form . The parameter is said to be a location parameter if there exists a possibility function on such that . Similarly, the parameter is said to be a scale parameter if there exists a possibility function on such that . Rate and shape parameters can then be defined as usual. The possibility function can be seen as providing an upper bound for subjective probability distributions related to as follows: the probability measure is upper-bounded set-wise by if

In particular, if is monotone increasing then this set-wise upper bound can be rephrased as for any and any with the cumulative distribution function (c.d.f.) induced by . This shows that possibility functions behave more closely to c.d.f.s than to p.d.f.s, as already hinted at by the definition of a scale parameter for possibility functions.

Conjugate prior.

The concept of conjugate prior can be extended straightforwardly to possibility functions whether the likelihood is a p.d.f. or a possibility function. In the former case, the renormalised version of any conjugate probability distribution is also a conjugate prior as a possibility function with the same parameters. For instance, the normal possibility function is conjugate for the expected value of a normal likelihood.333in fact, a Kalman filter can be derived as demonstrated in Houssineau and Bishop (2018) Another example is the gamma possibility function on defined as

with shape parameter and rate parameter , where is assumed to be equal to if . Note that this is not simply the renormalized version of the gamma probability distribution: the interval of definition of the shape parameter has been shifted by and the value is now possible. The latter modification allows for considering an uninformative gamma prior possibility function when . The gamma possibility function, like its probabilistic counterpart is a conjugate prior for the precision of a normal probability distribution. The inverse-gamma possibility function with shape parameter and scale parameter is simply defined as due to the simple form of the change of variable formula (1.5). Similarly, the beta possibility function is defined as

for any . Once again the parameters have been shifted by when compared to the usual parametrisation of the beta density function. This modification makes the value coincide with both the uninformative case and the interpretation of successes and failures a priori.

Introducing possibility functions.

It is generally easy to introduce new possibility functions since the assumption that the supremum is equal to is much easier to verify than the same assumption with an integral. For instance, any function of the form

with scale parameter and location parameter is a possibility function for any exponent and any norm . Renormalising a probability distribution often provides a meaningful candidate for a possibility function, though it is not always the case when the distribution is not a conjugate prior. A mechanism leading to the definition of a new probability distribution of interest can also inspire the introduction of a new possibility function. Applying this principle to the (non-central) chi-squared distribution leads to the computation of the possibility function describing the sum of squared normally-described uncertain variables as in the following proposition.

Proposition 2.1.

Let be a collection of uncertain variables independently described by the respective possibility functions , , for some parameters and . Then the uncertain variable is described by the possibility function

| (2.1) |

where and .

The proof of Proposition 2.1 can be found in the appendix, together with the proofs of all the other results in this article. As opposed to the chi-squared distribution, does not depend directly on the number of terms in the considered sum of squared normal uncertain variables. The analogue of the standard chi-squared distribution can be recovered when and yields the possibility function which can also be identified as the renormalised version of the exponential distribution. It is easy to prove that if is an uncertain variable described by for some parameters and then, for any constant , the uncertain variable is described by .

Sufficient statistics.

The notion of sufficient statistics can be defined for uncertain variables as follows: a statistics is sufficient for a model with observation , parameter and likelihood if it holds that , i.e. the observation is conditionally independent of the parameter given . The associated factorisation is

| (2.2) |

for some conditional possibility functions and . Indeed, since is a deterministic transformation of , it holds that which can then be expressed as in (2.2) based on the definition of the notion of sufficient statistics. The same operation is trickier in a probabilistic context since the joint distribution of the observation and the sufficient statistics does not admit a density in general. We emphasise that most statistical tests would be invariant under a change of sufficient statistics in this context since the change of variable formula does not include a Jacobian term and since the decomposition (2.2) involves two possibility functions instead of arbitrary functions as in the probabilistic case.

Example 2.2.

We consider observations that are independently and identically described by a normal possibility function , conditionally on . The uncertain variable corresponding to the sample average can be referred to as a sufficient statistics since the possibility function jointly describing given verifies

with the first term in the product not depending on and the second only depending on the realisation of the sufficient statistics instead of all observations . Therefore, if the sole objective is to estimate , then marginalising over all sequences of observations that have sample average makes sense, i.e. we consider the likelihood

which is indeed a conditional possibility function.

3. Expected value and variance of uncertain variables

3.1. LLN and CLT

In this section we aim to derive a LLN and a CLT for uncertain variables. These results will prove to be useful for our analysis later in the article. This is especially the case in Section 4, where we discuss various asymptotic properties of statistical procedures in the situation where the true sampling distribution is not accessible for analysis. The proofs of the theorems in this section can be found in the appendix. The more general notations and are used for uncertain variables to emphasise that the derived results can be useful in different contexts.

We wish to study sums based on a sequence of independently described uncertain variables on with possibility function . Related results have been derived by Marinacci (1999), Maccheroni et al. (2005) and Terán (2014), but with different representations of uncertainty or with different notions of expected value. It follows from (1.6) that the possibility function describing the uncertain variable takes the form

for any . We can then obtain an analogue of the law of large numbers as follows.

Theorem 3.1.

If is a sequence of independent uncertain variables on with possibility function such that

-

(i)

is continuous on ,

-

(ii)

is a twice continuously differentiable function on an open neighbourhood of each point in and

-

(iii)

,

then the possibility function describing the uncertain variable verifies

where the limit is point-wise and where is the convex hull of a set .

Theorem 3.1 emphasises the importance of the point(s) where is maximised. In the limit, only a number of uncertain variables in the collection can have realisations that are not elements of the of , with verifying . It follows that the sample average is in the convex hull of the .

Theorem 3.1 also shows that the of , when it is a singleton, plays the role of the expected value in the standard formulation of this result. This suggests a definition of the notion of expectation for uncertain variables. First, a few steps are needed in order to lay some formal basis for such a definition: we consider an uncertain variable and define the o.p.m. on as

for any . If the only available information about outcomes and events in comes from the possibility function via , then also contains all that information, which could be used to deduce what is known about any other uncertain variable on . The credibility of any event for some can then be measured as by the standard identification between that event and the subset . In particular, the event is said to happen almost surely under if it holds that . If is a singleton then is simply written . We can now introduce a notion of expectation for uncertain variables as follows.

Definition 3.2.

Given an o.p.m. on a set , the expectation of an uncertain variable is defined as444The notation is sometimes used to refer to the concept of outer expectation which is unrelated to the definition considered here.

| (3.1) |

This definition of the expectation does not require assumptions on the space on which the uncertain variable is defined; however, it is important to note that is set-valued in general. It is consistent with the law of large numbers since

with the possibility function describing ; which follows from Proposition A.1.

This notion of expectation also displays some useful properties. For instance, if is a map on , then it follows from Definition 3.2 that . Unsurprisingly, this invariance property is shared with the MLE which is also based on an . If it holds that with and two uncertain variables, then it is easy to prove that . By considering the function for some , it follows that

that is, is linear. Conditional expectations can also be defined easily, see the appendix for more details.

Given the result of Theorem 3.1, it is natural to also consider the as the starting point of the CLT for uncertain variables. Before stating the theorem, we introduce a slightly more general way of defining the o.p.m. underlying a sequence of uncertain variables on as555A more formal definition would require the introduction of cylinder sets and the corresponding finite-dimensional o.p.m.s.

for any , where is the possibility function describing all the uncertain variables in the sequence jointly. Henceforth, when some collection of uncertain variables will be defined, the o.p.m. and the corresponding expectation will be implicitly assumed to be induced by the possibility function jointly describing that collection. This situation also occurs in the Bayesian interpretation of probability where probability distributions represent the state of knowledge rather than some intrinsically random phenomenon whose distribution is induced by the underlying probability space.

Theorem 3.3.

If is a sequence of uncertain variables on independently and identically described by a possibility function verifying

-

(i)

is strictly log-concave and

-

(ii)

is twice differentiable,

then the expected value of the uncertain variable is a singleton and the possibility function describing the uncertain variable verifies

for any , with .

Theorem 3.3 shows that there are two limiting possibility functions instead of a single one as in the standard formulation. Which limiting behaviour applies to depends on how quickly decreases around its . Theorem 3.3 confirms that normal possibility functions also play a special role in the considered framework.

In the same way that the law of large numbers hinted at the definition of the expectation, the form of the asymptotic variance in the CLT suggests a definition of the variance based on the second derivative of as

| (3.2) |

In the case where , the limiting possibility function is which is equal to the normal possibility function when the precision is set to . It is therefore natural to set in this situation. If is not twice differentiable but is instead twice left- and right-differentiable at then left/right variances can be introduced. We only consider the special case where both the left and right derivatives of are different from zero for which we define . Overall, the concepts of expected value and variance provide grounds for the Laplace approximation.

There is a natural link between the concept of variance for uncertain variables and the notion of Fisher information. Indeed, since any suitably smooth possibility function describing an uncertain variable verifies , it follows from the properties of the expectation that the variance of the uncertain variable can be expressed as the inverse of a natural analogue of the notion of Fisher information as

If is related to a parameter of interest via a loss function and if we consider that then , with .

In order to illustrate the type of values that and take in practice, we consider the different possibility functions introduced so far: if is described by

-

(i)

, with and , then and

-

(ii)

, with , then and

-

(iii)

, with , then and

These examples show that the expected value (and possibly the variance) can match between a probability distribution and the corresponding possibility function. Yet, this is not necessarily the case: if is described by then is described by the inverse-gamma possibility function and which differs from the mean of an inverse-gamma random variable with the same parameters. Similarly, if is described by the chi-squared possibility function for some parameter and then and since this possiblity function has non-zero left and right derivatives at . The expected value and variance can also help identify a natural parametrisation for a possibility function as illustrated in the following example.

Example 3.4.

If two random variables and are such that is gamma distributed and the conditional distribution of given is for some , then the marginal distribution of is a generalised Student’s t distribution. One can therefore consider two uncertain variables and such that is described conditionally by and for some and . In this situation, the parameter is marginally described by

| (3.3) |

Since the expected value and variance are and , it reasonable to define the generalised Student’s t possibility function as

with , and which verifies and .

The LLN and CLT for uncertain variables are expressed via point-wise convergence of possibility functions, which can be identified as a mode of convergence for uncertain variables: if we consider a sequence of uncertain variables on some state space then we say that this sequence converges in outer probability measure to another uncertain variable if

| (3.4) |

for any . This notion of convergence is denoted or where is the possibility function describing . This is equivalent to a point-wise convergence for the corresponding sequence of possibility functions and is therefore the convergence given by the CLT for uncertain variables. Note that this notion of convergence only makes sense for o.p.m.s defined as the supremum of a possibility function.

3.2. Inference with o.p.m.s

We consider that the received observations are realisations of i.i.d. random variables with unknown common distribution . The notion of expected value introduced in Definition 3.2 suggests that, whenever the prior uncertainty is modelled with a possibility function, the MAP is the most natural point estimator. Although the MAP is also important when representing the posterior as a probability distribution, there are some disadvantages, e.g., the (probabilistic) MAP might not transform coherently under reparametrisation (Druilhet and Marin, 2007). This is not the case with possibility functions since it holds that for any parameter of interest, any sequence of observations and any mapping .

3.2.1. With the likelihood as a probability distribution

We first consider the case where the likelihood is based on a family of probability distributions . There are several interesting connections between the Bayesian nature of as defined in (1.3) and frequentist inference when the prior is assumed to be uninformative, i.e. ; it indeed holds that

-

(i)

The posterior expected value is the MLE of the parameter, which we denote by .

-

(ii)

The function for a given point is the (simple) LRT for the hypothesis versus .

-

(iii)

The inverse of the posterior variance of is

which is the observed information, denoted by .

These aspects reinforce the fact that possibility functions represent information in a way that is compatible with frequentist inference. Before continuing with our analysis, we introduce in the next section a few additional concepts for the case where the likelihood is a possibility function.

3.2.2. With the likelihood as a possibility function

We follow the approach of generalised Bayesian inference and consider the situation where it is not convenient to model the true data-generating process. Instead, in order to learn some characteristics of this process, we identify a likelihood (as a possibility function) for which the MLE tends to the quantity of interest as the number of observations tends to infinity. A posterior representation of the uncertainty can then be determined, potentially using some prior information about the parameter of interest if any is available. In this case, the uncertainty about the relation between the observations and the parameter of interest can also be modelled via a sequence of independently-described uncertain variable with common possibility function , conditionally on . In this context, the MAP is an uncertain variable defined as and depends on the choice of prior possibility function . If then is the MLE, denoted by and defined as

Since none of the possibility functions in the parametric family corresponds to the true sampling distribution of the observations, we must find another way to define the best-fitting parameter which we will refer to as the true parameter for simplicity. One possible approach is to follow the M-estimation literature (Godambe, 1991) and use consistency as a way to define rather than as a result about the convergence of the considered estimator to the actual true parameter as is standard. This approach is also the one used by Bissiri et al. (2016). Indeed, it follows from the standard LLN that

| (3.5) |

where and denote the convergence in probability and the expectation w.r.t. respectively. The true parameter is then defined as the point where the right hand side of (3.5) is maximized. If there is no such point then is not well-defined. The standard concept of identifiability translated for possibility functions, that is for any such that , is not sufficient to ensure the existence of such a point . We instead consider the following stronger assumption: is strictly log-concave for any . Indeed, it follows from this assumption that is strictly concave and has a single maximizer . This assumption is in line with the other ones made throughout the article, especially in the CLT for uncertain variables. In the remainder of this section, we will assume that is described by and we will denote by the expected value of .

Remark 3.5.

Since any estimator of is itself an uncertain variable, the usual characteristics of estimators have to be redefined. For instance, the bias of can be defined as and, naturally, one can refer to as an unbiased estimator if .

Having used the standard notion of consistency to define , we can now introduce a form of consistency for estimators based on uncertain variables. However, before introducing this weaker notion of consistency, we introduce a suitable version of the concept of identifiability as follows.

Definition 3.6.

Let be a parametrized family of conditional possibility functions on describing an uncertain variable and let be the true parameter. The parameter is said to be identifiable if, for any , is a singleton and implies .

This is a much stronger assumption than standard identifiability since any parameter that does not affect the mode of the corresponding likelihood would be unidentifiable. Location parameters are typically identifiable but they are not the only ones; for instance, if the likelihood is a gamma possibility function, then each of the two parameters is identifiable when assuming the other one is fixed. When considering loss functions, the identifiability assumption implies that the loss should be minimised at a point where no other loss function , , is minimised.

Example 3.7.

If the likelihood is equal to for some then any is identifiable. However, the likelihood , , is nowhere identifiable; indeed, the expected value is independent of . Therefore, one must use a p.d.f. as a likelihood when trying to learn the variance of a sequence of observations.

Some weak form of consistency can be obtained for the MLE by assuming that the parameter is identifiable. Indeed, the LLN for uncertain variables yields that

The identifiability assumption ensures that only has as a mode, so that is the unique maximizer of , and it holds that as in the situation where a probabilistic model is correctly specified.

A practical illustration of the use of the LLN and CLT is given in the next example.

Example 3.8.

We continue with the situation introduced in Example 2.2 where is equal to and where the sample average is a sufficient statistics. We now consider that the observations come from a sequence of i.i.d. random variables with unknown common law . The standard law of large numbers yields that the sample average tends to whereas Theorem 3.1 yields that tends to , with the true value of the parameter. Combining these two results, we obtain that , i.e., our model based on possibility functions targets although we did not provide a probabilistic model for . This type of result is usual in M-estimation, yet, we highlight that the proposed approach additionally provides a posterior quantification of the uncertainty via which can take into account a possibility function describing a priori. Under the considered modelling assumptions, the sequence of possibility functions describing converges point-wise to .

Example 3.8 gives a result of asymptotic normality for estimating the expected value with the likelihood defined as a normal possibility function. More general asymptotic normality results will be given in further sections.

4. Asymptotic analysis with unknown sampling distribution

In this section we analyse various asymptotic properties of statistical procedures in the situation where the true sampling distribution is not available for analysis. The likelihood of a parameter for the observations in can be either a probability distribution or a possibility function so we denote it by in general. The corresponding log-likelihood is denoted by . We model the uncertainty about the true parameter via an uncertain variable on and we consider that there is some prior information about taking the form of a prior possibility function . We formulate the following assumptions:

-

A.1

The parameter is well defined and the MLE is consistent

-

A.2

The prior possibility function is continuous in a neighbourhood of

The generality of Assumption A.1 makes it suitable for the two types of likelihood that are considered. The specific conditions under which Assumption A.1 holds for a probabilistic likelihood are the usual ones, see for instance Wald (1949) and Le Cam (1990).

4.1. Bayesian inference

One of the most important asymptotic results in Bayesian statistics is the BvM theorem which can be interpreted as follows: given some initial distribution, the posterior becomes independent of the prior as we take the number of observations to infinity, and the posterior tends to a normal distribution. The posterior possibility function describing given a sequence of observations can be expressed as

We omit the variables on which the possibility function describing is conditioned on in the posterior since they could be either random variables or uncertain variables. In this context, the BvM theorem takes the following form.

Theorem 4.1 (Bernstein-von Mises).

Theorem 4.1 states that the posterior possibility function is approximately normal with expected value (which tends to as tends to infinity) and with the inverse of as variance. An important aspect of the proof of the BvM theorem is that the nature of the likelihood (expressed as a probability distribution or as a possibility function) had no bearing on the calculations. Although the BvM theorem guarantees (under assumptions) that the prior information is forgotten in the limit, the nature of the prior information defines the nature of posterior representation of uncertainty as a probability distribution or as a possibility function. In the next section, we consider how we can predict the behaviour of the MAP and of the credibility of the true parameter value when varying the observations. When the prior is uninformative, these quantities are respectively the (generalised) MLE and likelihood ratio test as highlighted earlier.

4.2. Frequentist-type guarantees

The main reason for the weak dependency of the BvM theorem on the nature of the likelihood is that the observations are fixed in a Bayesian setting. However, in order to derive frequentist-type guarantees for the the MAP and for the credibility of the true parameter value , the variability of the sequence of observations must be taken into account. We henceforth consider the case where the likelihood is a possibility function and make explicit the dependency of the likelihood on the data by writing instead of and similarly for the log-likelihood. In order to model the fact that the data-generating process is not known, we define as the uncertain variable described by the possibility function where is the true value of the parameter.

The observations are assumed to be realisations of a sequence of independent uncertain variables identically described by , and we denote by the induced o.p.m. on . Since the observations are now uncertain variables, the MAP itself is an uncertain variable defined as .

Before deriving asymptotic normality results, we need to introduce the analogues of the probabilistic results used when performing a standard statistical analysis. A concept that is needed to state the assumptions and prove asymptotic normality is the analogue of the usual dominance property for sequences of random variables, which can be rephrased as: the sequence of uncertain variables on is dominated by another sequence on , or is , if for all there exist , such that for all , where is induced by the sequence . We can now formulate the assumptions required for the asymptotic analysis of this section:

-

(3)

is strictly log-concave

-

(4)

The mapping is twice-differentiable in as well as thrice-differentiable in

-

(5)

under the o.p.m.

Although Assumption 3 is restrictive, it is always possible to introduce a tempered version of the possibility function , with for any , which satisfies it. The cost of such a change of possibility function will induce an increase in asymptotic variance since the variance of under the tempered possibility function will be necessarily greater than under .

In this context, the score function is defined as and its expected value is equal to ; indeed . However, the Fisher information cannot be defined as the expectation of the squared score as is usual; in fact, the expected value of the latter is also equal to . Instead, we introduce the Fisher information as

| (4.2) |

The following example illustrates one of the advantages of this notion of Fisher information.

Remark 4.2.

Lehmann (2004, Example 7.2.1) highlights some limitations of the standard notion of Fisher information by pointing out that for the likelihood at , which is counter-intuitive. With uncertain variables, the variance corresponding to the possibility function is infinite when , which is consistent with .

4.2.1. Asymptotic normality

One of the most important asymptotic results in frequentist statistics is the asymptotic normality of the MLE. We show in the following theorem that a similar result holds for the MAP , which is equal to the MLE when the prior is uninformative.

The advantage of Theorem 4.3 is that it provides some quantitative means of assessing the asymptotic performance of the MAP even when the true data generating process is not known. Indeed, the asymptotic variance in Theorem 4.3 only involves derivatives of the likelihood and no expectations w.r.t. the true data distribution.

It follows from Assumption 3 that the score is continuous and strictly monotone and is therefore invertible. Assuming that both and its inverse are twice differentiable and applying Proposition B.1, we can express the term in the asymptotic variance of Theorem 4.3 more explicitly as

with . It is interesting to see the second derivative in appear in the expression of the asymptotic variance (via the variance term ) since the latter usually only depends on the curvature of the log-likelihood as a function of via the Fisher information. The curvature of evaluated at is associated with the variation in the observations at the true parameter value, which might indeed influence the algorithm. In particular, a log-likelihood which would be “flat” as a function of around the point would yield a potentially infinite asymptotic variance via the term . Two special cases can then be identified: If is a location parameter then the asymptotic variance in Theorem 4.3 simplifies to since it holds that . If the likelihood is based on an exponentiated reward function then the asymptotic variance in Theorem 4.3 can be expressed as

with . This expression highlights the structure of the asymptotic variance as a combination of second-order derivatives.

4.2.2. Hypothesis testing

We consider a simple hypothesis test versus of the form , where, as opposed to LRTs, prior information can be taken into account via the prior . The null hypothesis is then rejected if is less than or equal to some threshold to be determined. We follow the usual approach and recast the problem of setting a value for into choosing a level of confidence and solving the inequality . Assuming for simplicity that is unimodal, the proposed interpretation facilitates the calculation of an -credible interval as

When interpreting the o.p.m. , characterised by , , as an upper bound for a subjective probability distribution , we can deduce that from the fact that . As is usual for LRTs, we use the asymptotic properties of to make the computation of feasible.

Using Theorem 4.4, it is easy to approximate the credibility of the event for large values of and deduce a threshold for a given confidence level .

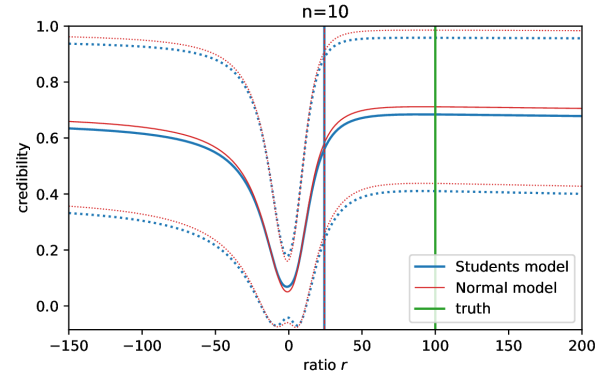

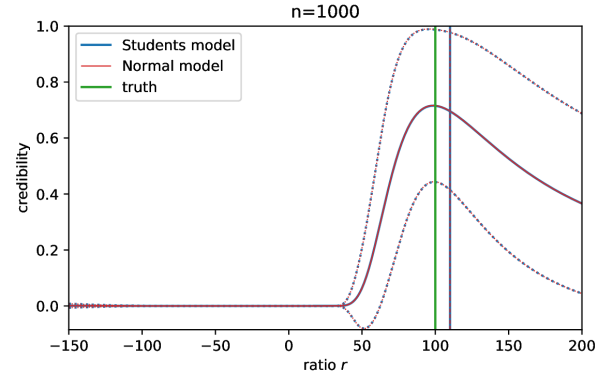

4.3. Numerical results: ratio of two means

Let be a collection of i.i.d. random variables sampled from an unknown distribution with and real-valued and independent. Consider the objective of estimating the ratio between and . The most natural estimator for such a quantity is with and the sample averages. In order to apply the proposed approach, we must identify likelihoods with a suitable MLEs in order to learn both and . The normal distribution is a suitable likelihood in this case, however, since the variances of these observations are not known either, they must also be estimated. We therefore consider the likelihoods and where both the means and the precisions are uncertain variables to be determined. We now focus on the prior possibility functions for and since the ones for and will be of the same form. The prior possibility function describing is assumed to be the gamma possibility function for some given . The prior possibility function for given is assumed to be the normal possibility function for some given and . The corresponding parameters for and are denoted by , , and . The posterior possibility functions describing and are of the same form as the priors, i.e.

with , and

where is the sample variance. These results are consistent with the probabilistic case as detailed, e.g., in (Gelman et al., 2013). The marginal possibility function describing given is

with degrees of freedom and variance . The possibility function describing given is

While this expression does not seem to have a simple closed-form expression, it is straightforward to compute numerically using any optimisation algorithm. Using the properties of the expected value , we find that

Considering the simplified case where , i.e. the case where there is no prior information on either of , , and (which would be improper for random variables), we recover the estimate . In this case, it holds that and , so that the expected value of is . Because of the properties of the expected value we have . With the probabilistic modelling, the inverse of the expected value of the precision () would not be equal to the expected value of the variance (). Although the proposed approach does not yield an improved estimator in the case where the prior is uninformative, a quantification of the posterior uncertainty is now available. We also consider the case where the variances of and are known, in which case is simply a ratio of normally-described uncertain variables. We refer to this simpler model as the “normal model” and use it to show that the results are not specific to the Students model introduced above.

We illustrate the form of the posterior possibility function in the case where is a -distributed random variable and where is independent of and is -distributed. This is a difficult case since is close to with a standard deviation allowing values of either signs. In order to show how the posterior possibility function depends on and on the specific realisations , two different values of and realisations of the observations are simulated and the mean and standard deviation of the corresponding posterior possibility function is displayed in Figure 1 together with the mean MAP for the Students model as well as for the normal model. This type of possibility function cannot be renormalised to a proper probability distribution since it is not integrable. Indeed, large values of cannot be excluded since the credibility of the event is positive for finite values of .

5. Conclusion

Through a number of practical and theoretical results, we have demonstrated how possibility functions can be used for statistical modelling in place of, or together with, probability distributions. Many features of standard probabilistic inference are retained when using possibility functions and the associated uncertain variables. The differences between the two approaches highlight the suitability of each representation of uncertainty for specific tasks. For instance, statistical modelling based on possibility functions enables the representation of a complete absence of prior information about some or all of the parameters of the model while avoiding the issue of improper posterior distributions. Crucially, although the influence of the information in the prior representation of uncertainty vanishes as the number of data points increases, the nature of the prior as a probability distribution or as a possibility function remains in the limit and influences the posterior quantification of uncertainty.

An interesting direction to take from this work is to develop an outer-measure approach in an infinite-dimensional setting. By doing so one can consider different avenues for uncertainty quantification, with applications in inverse problems and compressed sensing (Henn et al., 2012). In particular, due to the recent success of the Bayesian approach (Dashti et al., 2013; Engl et al., 1996; Stuart, 2010) for inverse problems one could use this as an instinctive application. Another direction could be the derivation of asymptotic properties for dynamical systems (Bickel et al., 1998; McGoff et al., 2015) in the context of o.p.m., which is not considered in the existing work on this topic (Houssineau, 2018b; Houssineau and Bishop, 2018).

References

- Aldrich [1997] J. Aldrich. R. A. Fisher and the making of maximum likelihood 1912–1922. Statistical science, 12(3):162–176, 1997.

- Berger and Casella [2001] R. L. Berger and G. Casella. Statistical inference. Duxbury, 2001.

- Bickel et al. [1998] P. J. Bickel, Y. Ritov, and T. Ryden. Asymptotic normality of the maximum-likelihood estimator for general hidden Markov models. The Annals of Statistics, 26(4):1614–1635, 1998.

- Bissiri et al. [2016] P. G. Bissiri, C. C. Holmes, and S. G. Walker. A general framework for updating belief distributions. Journal of the Royal Statistical Society: Series B, 78(5):1103–1130, 2016.

- Butkovič [2010] P. Butkovič. Max-linear systems: theory and algorithms. Springer Science & Business Media, 2010.

- Carlsson and Fullér [2001] C. Carlsson and R. Fullér. On possibilistic mean value and variance of fuzzy numbers. Fuzzy sets and systems, 122(2):315–326, 2001.

- Chen [1995] Y. Y. Chen. Statistical inference based on the possibility and belief measures. Transactions of the American Mathematical Society, 347(5):1855–1863, 1995.

- Constantinou and Dawid [2017] P. Constantinou and A. P. Dawid. Extended conditional independence and applications in causal inference. The Annals of Statistics, 45(6):2618–2653, 2017.

- Dashti et al. [2013] M. Dashti, K. J. H. Law, A. M. Stuart, and J. Voss. MAP estimators and their consistency in Bayesian nonparametric inverse problems. Inverse Problems, 29(9):095017, 2013.

- De Baets et al. [1999] B. De Baets, E. Tsiporkova, and R. Mesiar. Conditioning in possibility theory with strict order norms. Fuzzy Sets and Systems, 106(2):221–229, 1999.

- Del Moral and Doisy [1999] P. Del Moral and M. Doisy. Maslov idempotent probability calculus, i. Theory of Probability & Its Applications, 43(4):562–576, 1999.

- Del Moral and Doisy [2000] P. Del Moral and M. Doisy. Maslov idempotent probability calculus. ii. Theory of Probability & Its Applications, 44(2):319–332, 2000.

- Dempster [1968] A. P. Dempster. A generalization of bayesian inference. Journal of the Royal Statistical Society: Series B (Methodological), 30(2):205–232, 1968.

- Druilhet and Marin [2007] P. Druilhet and J.-M. Marin. Invariant HPD credible sets and MAP estimators. Bayesian Analysis, 2(4):681–691, 2007.

- Dubois and Prade [1981] D. Dubois and H. Prade. Additions of interactive fuzzy numbers. IEEE Transactions on Automatic Control, 26(4):926–936, 1981.

- Dubois and Prade [2015] D. Dubois and H. Prade. Possibility theory and its applications: Where do we stand? In Springer Handbook of Computational Intelligence, pages 31–60. Springer, 2015.

- Dubois et al. [1995] D. Dubois, S. Moral, and H. Prade. A semantics for possibility theory based on likelihoods. In Proceedings of 1995 IEEE International Conference on Fuzzy Systems, volume 3, pages 1597–1604. IEEE, 1995.

- Engl et al. [1996] H. W. Engl, M. Hanke, and A. Neubauer. Regularization of inverse problems, volume 375. Springer Science & Business Media, 1996.

- Evans and Moshonov [2006] M. Evans and H. Moshonov. Checking for prior-data conflict. Bayesian analysis, 1(4):893–914, 2006.

- Fisher [1922] R. A. Fisher. On the mathematical foundations of theoretical statistics. Phil. Trans. R. Soc. Lond. A, 222(594-604):309–368, 1922.

- Fisher [1935] R. A. Fisher. The fiducial argument in statistical inference. Annals of eugenics, 6(4):391–398, 1935.

- Gelman et al. [2013] A. Gelman, J. B. Carlin, H. S. Stern, D. B. Dunson, A. Vehtari, and D. B. Rubin. Bayesian data analysis. CRC press, 2013.

- Godambe [1991] V. P. Godambe. Estimating functions. Oxford University Press, 1991.

- Grünwald and Dawid [2004] P. D. Grünwald and A. P. Dawid. Game theory, maximum entropy, minimum discrepancy and robust bayesian decision theory. the Annals of Statistics, 32(4):1367–1433, 2004.

- Hald [1999] A. Hald. On the history of maximum likelihood in relation to inverse probability and least squares. Statistical Science, 14(2):214–222, 1999.

- Henn et al. [2012] M.-A. Henn, H. Gross, F. Scholze, M. Wurm, C. Elster, and M. Bär. A maximum likelihood approach to the inverse problem of scatterometry. Optics Express, 20(12):12771–12786, 2012.

- Houssineau [2018a] J. Houssineau. Parameter estimation with a class of outer probability measures. arXiv preprint arXiv:1801.00569, 2018a.

- Houssineau [2018b] J. Houssineau. Detection and estimation of partially-observed dynamical systems: an outer-measure approach. arXiv preprint arXiv:1801.00571, 2018b.

- Houssineau and Bishop [2018] J. Houssineau and A. N. Bishop. Smoothing and filtering with a class of outer measures. SIAM/ASA Journal on Uncertainty Quantification, 6(2):845–866, 2018.

- Langford [2005] J. Langford. Tutorial on practical prediction theory for classification. Journal of machine learning research, 6(Mar):273–306, 2005.

- Le Cam [1990] L. Le Cam. Maximum likelihood: an introduction. International Statistical Review/Revue Internationale de Statistique, pages 153–171, 1990.

- Lehmann [2004] E. L. Lehmann. Elements of large-sample theory. Springer Science & Business Media, 2004.

- Maccheroni et al. [2005] F. Maccheroni, M. Marinacci, et al. A strong law of large numbers for capacities. The Annals of Probability, 33(3):1171–1178, 2005.

- Marinacci [1999] M. Marinacci. Limit laws for non-additive probabilities and their frequentist interpretation. Journal of Economic Theory, 84(2):145–195, 1999.

- Maslov [1992] V. P. Maslov. Idempotent analysis, volume 13. American Mathematical Soc., 1992.

- McGoff et al. [2015] K. McGoff, S. Mukherjee, A. Nobel, N. Pillai, et al. Consistency of maximum likelihood estimation for some dynamical systems. The Annals of Statistics, 43(1):1–29, 2015.

- Murphy and Van der Vaart [2000] S. A. Murphy and A. W. Van der Vaart. On profile likelihood. Journal of the American Statistical Association, 95(450):449–465, 2000.

- Raue et al. [2009] A. Raue, C. Kreutz, T. Maiwald, J. Bachmann, M. Schilling, U. Klingmüller, and J. Timmer. Structural and practical identifiability analysis of partially observed dynamical models by exploiting the profile likelihood. Bioinformatics, 25(15):1923–1929, 2009.

- Robert and Casella [2013] C. Robert and G. Casella. Monte Carlo statistical methods. Springer Science & Business Media, 2013.

- Shackle [1961] G. L. S. Shackle. Decision order and time in human affairs. Cambridge University Press, 1961.

- Shafer [1976] G. Shafer. A mathematical theory of evidence, volume 42. Princeton University Press, 1976.

- Smets and Kennes [1994] P. Smets and R. Kennes. The transferable belief model. Artificial intelligence, 66(2):191–234, 1994.

- Smith [2010] J. Q. Smith. Bayesian decision analysis: principles and practice. Cambridge University Press, 2010.

- Stuart [2010] A. M. Stuart. Inverse problems: a Bayesian perspective. Acta Numerica, 19:451–559, 2010.

- Terán [2014] P. Terán. Law of large numbers for the possibilistic mean value. Fuzzy Sets and Systems, 245:116–124, 2014.

- Vanlier et al. [2012] J. Vanlier, C. A. Tiemann, P. A. J. Hilbers, and N. A. W. van Riel. An integrated strategy for prediction uncertainty analysis. Bioinformatics, 28(8):1130–1135, 2012.

- Wald [1949] A. Wald. Note on the consistency of the maximum likelihood estimate. The Annals of Mathematical Statistics, 20(4):595–601, 1949.

- Walley [1991] P. Walley. Statistical reasoning with imprecise probabilities. Chapman & Hall, 1991.

- Walley and Moral [1999] P. Walley and S. Moral. Upper probabilities based only on the likelihood function. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 61(4):831–847, 1999.

- Wedderburn [1974] R. W. Wedderburn. Quasi-likelihood functions, generalized linear models, and the Gauss-Newton method. Biometrika, 61(3):439–447, 1974.

- Zadeh [1978] L. A. Zadeh. Fuzzy sets as a basis for a theory of possibility. Fuzzy sets and systems, 1(1):3–28, 1978.

Appendix A Additional results and proofs for Section 3

A.1. Expected value

Let and be uncertain variables on and respectively, jointly described by a possibility function on . Let be the o.p.m. on induced by . The conditional o.p.m. is characterised by

for any and any such that . A conditional version of the expectation can then be introduced based on as follows:

We will write when there is no ambiguity.

Proposition A.1.

Let be an uncertain variable on a set and let be a surjective function from a set to . It holds that

Proof.

By definition of the argmax it holds that

By defining and by noticing that holds from the fact that is surjective, it follows that

which concludes the proof of the proposition. ∎

A.2. Proofs of the results in Section 3

Proof of Proposition 2.1.

The possibility function describing the uncertain variable is characterised by

for any . If then the result is trivial. To solve this maximization problem when , we define the Lagrange function

which easily yields , and , so that and

for any , which concludes the proof of the lemma. ∎

Proof of Theorem 3.1.

Before proceeding with the proof, we emphasize an abuse of notation where now denotes a point in , unrelated to previous notations in the document. We also write instead of for the sake of simplicity.

- Definitions:

-

We denote by the convex hull of , and by the distance to the set , i.e. the function

Since is convex, for any , there exists a unique point such that . We also recall, from the definition of , that

(A.1) - Outline:

-

We aim to prove that

We will consider the two cases above separately.

- Case ::

-

The result being evident on , let be an arbitrary point on the convex hull that does not belong to .

Using Carathéodory’s theorem, can be written as the convex combination of at most points of , i.e., there exists such that

where and , , with .

For any , we consider the sequence of points defined as

and one can easily verify that . We can also write

(A.2a) (A.2b) where

and

so that for any .

For any , then, since attains its supremum value in and is in some open neighbourhood of , Taylor’s theorem yields

where is the Hessian matrix of in . That is,

so that .

- Case ::

-

Let be an arbitrary point outside the convex hull , and let us denote by its distance to . We define the open set

and the sequence of increasing closed sets as

We define and , , and we note that

-

-:

Since is bounded and continuous and the sets are closed, the supremums are all reached and we have for . We define and we have .

-

-:

Since , .

Recall from (A.1) that, for any , we need to consider the sequences of points satisfying . We will focus first on the set

i.e., the admissible sequences whose points are all contained within , and then on the set

i.e, those with a least one point in the remaining space .

Denote by the minimum number of points in across every sequence in , and consider a sequence with points in , indexed from to . Since for any and is convex, we have . We may then write

It follows that , and thus . However, since

and , it follows that .

Any sequence in has at least one point in , and thus

Since , it follows that .

We can then write

and since for two convergent sequences and it holds that

it follows that .

-

-:

∎

Proof of Theorem 3.3.

One of the basic properties of strictly log-concave functions is that they are maximised at a single point which we denote by . We assume without loss of generality that and We write instead of for the sake of simplicity. To find the supremum of over the set of ’s verifying , we first use Lagrange multipliers to find that

for any so that a solution is . In order to show that this solution is local maximizer, we consider the bordered Hessian corresponding to our constrained optimisation problem, defined as

where and with . For the solution , , to be a local maximum, the sign of the principal minors of has to be alternating, starting with positive. Basic matrix manipulations for the determinant yield

| (A.3) |

which is alternating in sign. For to be positive, it has to hold that

This condition can be recognized as a necessary and sufficient condition for a function to be strictly log-concave. It also follows from the assumption of log-concavity that the condition , which can be expressed as can only be satisfied at so that this solution is a global maximum. We therefore study the behaviour of the function as and obtain

The result of the proposition follows easily by taking the limit and by noting that and that is non-positive since decreases in the neighbourhood of its . ∎

Appendix B Additional results and proofs for Section 4

We begin this section with a useful result regarding the evolution of the variance when transforming uncertain variables.

Proposition B.1.

Let be an uncertain variable on a set with expected value described by the possibility function , let be a bijective function in another set such that both and are twice differentiable and let be the uncertain variable , then is described by and the variance of can be expressed as

Proof of Proposition B.1.

Since is bijective, the possibility function describing is indeed

for any . The variance of is

The second derivative in the denominator can be computed as

Using the fact that as well as the standard rules for the derivative of the inverse of a function, it follows that

The result of the lemma follows from the identification of the term as the variance of . ∎

B.1. Proofs of the results in Section 4

Some additional technical concepts and results are needed to state the proofs of the results in Section 4. We say that the sequence converges in credibility to an uncertain variable in if for all

| (B.1) |

This is denoted . The LLN for uncertain variables can be proved to give a convergence in credibility to the expected value. Using these two concepts of convergence, we state without proving the analogue of Slutsky’s lemma as follows.

Proposition B.2.

Let and be two sequences of uncertain variables. If it holds that and for some uncertain variable and some constant then

given that is invertible.

We note that the proof of Slutsky’s lemma for uncertain variables is beyond the scope of this work.

Proof of Theorem 4.1.

Following the standard approach, we introduce the possibility function describing as

Again, as usual, we consider large values of within the argument of the prior only. Under Assumption A.2, noticing that the argument of the supremum in the denominator is maximized at the MLE leads to

where the MLE is deterministic since the observations are given. As opposed to the corresponding proof in a probabilistic context, the MLE appears naturally in the approximation of , this is due to the supremum in the denominator of Bayes’ rule for possibility functions. This difference suggests that the BvM theorem is indeed very natural with possibility functions. In order to relate to the true parameter , we expand the derivative of the log-likelihood at around as

for some in the interval formed by and . Since it holds that by construction, it follows that

| (B.2) |

The term is the observed information which we denote . It follows from Assumption A.1 that the second term in the denominator of (B.2) vanishes for large. The MLE therefore verifies

| (B.3) |

which yields

The expression of the posterior possibility function can be further simplified by expanding the log-likelihood around as

with also lying between and and by considering and . Using Assumption A.1 once more, we deduce the following approximation

| (B.4) |

Returning to the possibility function describing a posteriori and using the relation (B.3) once more, leads to the desired result. ∎

Proof of Theorem 4.3.

We make explicit the dependency of and on the observation by writing and instead. It follows from Theorem 4.1 and from Assumption 5 that

The LLN for uncertain variables, together with Assumption A.1, yields

| (B.5) |

and the CLT for uncertain variables yields

| (B.6) |

The desired result follows from Slutsky’s lemma for uncertain variables (Proposition B.2) and from the properties of normal uncertain variables. ∎

Proof of Theorem 4.4.

It follows from Theorem 4.1 and from Assumption 5 that

Expanding this expression based on the definition (B.3) of , we find that

The desired result follows from the convergence results (B.5) and (B.6) together with Slutsky’s lemma for uncertain variables as well as with the definition and properties of the (non-central) chi-squared possibility function. ∎