A Particle Filter for Stochastic Advection by Lie Transport (SALT): A case study for the damped and forced incompressible 2D Euler equation111This work was partially supported by the EPSRC Standard Grant EP/N023781/1.

Abstract

In this work, we combine a stochastic model reduction with a particle filter augmented with tempering and jittering, and apply the combined algorithm to a damped and forced incompressible 2D Euler dynamics defined on a simply connected bounded domain.

We show that using the combined algorithm, we are able to assimilate data from a reference system state (the “truth”) modelled by a highly resolved numerical solution of the flow that has roughly degrees of freedom, into a stochastic system having two orders of magnitude less degrees of freedom, which is able to approximate the true state reasonably accurately for large scale eddy turnover times, using modest computational hardware.

The model reduction is performed through the introduction of a stochastic advection by Lie transport (SALT) model as the signal on a coarser resolution. The SALT approach was introduced as a general theory using a geometric mechanics framework from Holm, Proc. Roy. Soc. A (2015). This work follows on the numerical implementation for SALT presented by Cotter et al, SIAM Multiscale Model. Sim. (2019) for the flow in consideration. The model reduction is substantial: The reduced SALT model has degrees of freedom.

Results from reliability tests on the assimilated system are also presented.

1 Introduction

Data assimilation is the process by which observations (data) are integrated with mathematical models so that inference or prediction of the evolving state of the system can be made. For geoscience applications such as numerical weather prediction, it is an active area of research. There the typical global-scale state space dimension is of order , and observation data of dimension are assimilated every – hours. Current established methods used in operation centres include 4DVar, (various extended versions of) ensemble Kalman filter (EnKF) and variational assimilation methods. However, for fully nonlinear systems and complex observation operators these approaches are unsatisfactory. Our work presented in this paper is part of the wider effort to tackle high dimensional nonlinear geoscience problems using particle filters, as can be seen from the survey paper (van Leeuwen et al., 2019) and the references therein.

The idea of modelling uncertainty using stochasticity in geophysical fluid applications is well established, see Buizza et al. (1999); Majda et al. (1999, 2001). In this paper we work with the stochastic advection by Lie transport (SALT) approach, first formulated in Holm (2015). It can be thought of as a framework for deriving stochastic partial differential equation (SPDE) models for geophysical fluid dynamics (GFD). The stochasticity is introduced into the advection part of the dynamics via a constrained variational principle called the Hamilton-Pontryagin principle. What results is a stochastic Euler-Poincaré equation, in which the local acceleration part of the transport operator is in the geometric form represented by the Lie derivative of velocity one-form in the direction of a stochastic vector field (in the form of a Stratonovich semimartingale). This approach for adding stochasticity into GFD models is different from the current state-of-the-art in numerical weather prediction (NWP), where stochastic models of uncertainty is introduced into the forcing; for example stochastic perturbation by physical tendencies (SPPT) methodology, see Palmer (2018).

By adding stochasticity into the advection operator, one can model uncertain transport behaviour. In particular, the SALT stochastic term can be thought of as a model on the resolvable scale for the subgrid unresolvable fluid scales for transport. The main advantage of the SALT stochastic term is that it preserves the Kelvin’s Circulation Theorem (KCT). However energy is not conserved by SALT because as one can show, an extra term called line stretching results from the application of the Reynolds transport theorem to the time differential of the energy; and the extra term contributes positively to the rate of change of the energy. An alternative, energy conserving stochastic approach called Location Uncertainty (LU) has also been developed Mémin (2014), but LU models do not preserve circulation.

A fundamental ingredient in SPDEs with SALT noise is the spectrum of the velocity-velocity correlation tensor, which is prescribed in the form of scaled eigenvectors that are denoted by . These appear in the following Stratonovich stochastic differential equation for the Eulerian velocity field

| (1) |

Here denotes Eulerian position, denotes large-scale mean velocity field, and are independent 1D Brownian motions. The symbol denotes Stratonovich stochastic integration. Cotter et al. (2017) showed that taking the diffusive limit of a flow with two timescales leads to a stochastic differential equation in the form of (1), where should be rigorously understood as empirical orthogonal functions corresponding to the different modes of the fast flow.

For applications, the vector fields need to be supplied a priori. A data driven calibration methodology for obtaining is described in Cotter et al. (2018, 2019), in which the authors numerically investigated two example fluid systems: a damped and forced 2D Euler model with no-penetration boundary condition, and a two-layer 2D quasi-geostrophic model prescribed on a channel. In those works, the SPDE model is interpreted as a parameterisation for the antecedent partial differential equation (PDE) model. Using statistical uncertainty quantification tests, it is shown that by conditioning on a suitable initial prior, an ensemble of SPDE solutions is able to effectively capture the large scale behaviour of the deterministic system on a coarser resolution. It is important to stress the fact that the deterministic system has degrees of freedom, whilst the coarse stochastic system has degrees of freedom. Capturing large scale dynamics on coarse scales enables the reduction of the high resolution PDE system to the coarse scale as an SPDE. This motivates further investigation of the performance of SALT SPDEs using ensemble data assimilation algorithms, where the forecast model is the SPDE prescribed on coarse scales. This is the theme of the present work, where we utilise the calibrated described in Cotter et al. (2019) in a data assimilation set-up for the damped and forced 2D Euler dynamics.

For us, sequential data assimilation is mathematically formulated as a nonlinear filtering problem, which can be tackled using a particle filter, see Bain and Crisan (2009); Reich and Cotter (2015). A particle filter proceeds by alternating between forecast and analysis cycles. In each analysis cycle, observations of the current (and possibly past) state of a system are combined with the results from a prediction model (the forecast) to produce an analysis. The analysis step is typically performed either in the form of a “best estimate” or in terms of approximating conditional distributions. The model is then advanced in time and its result becomes the forecast in the next analysis cycle. However when applied to problems in high dimensions, without additional techniques a basic particle filter algorithm would almost certainly fail. This is due to the fact that in high dimensions the data are too informative.

Beside the model reduction described above, in this paper, we describe two additional techniques: tempering and jittering, which are incorporated into the basic bootstrap particle filter. The combined algorithm is applied to the damped and forced 2D Euler dynamics. These techniques are all necessary for the successful assimilation of data obtained from the true state of the system, which is modelled using a highly resolved numerical solution of degrees of freedom.

The theoretical justification of the tempering and jittering procedures is covered in Beskos et al. (2011). Here, we offer some intuition to provide a better understanding of their advantages. The success of particle filters can be understood by the fact that they process data in a sequential manner. In other words, at each data assimilation time, only the new observations are assimilated, without the need to (re-)assimilate all past observations. This is advantageous as it is much harder (if not impossible) to assimilate the entire set of data available from initial time up to the current time. For high dimensional problems, a large amount of data (observations) become available at each data assimilation step. This makes each individual data assimilation step (almost) as hard as processing data in a non-sequential manner. The tempering procedure alleviates this problem by incorporating the data gradually. It does so through several steps (in a sense mimicking the sequentiality of the particle filter as a whole). The number of steps is chosen adaptively so that at each step, only the ”right amount” data is incorporated. Not too much as this would make the procedure inefficient, and not too little as this would introduce too many tempering steps. The ”amount of data” is measured by the effective sample size statistic (ESS). The criteria used is to choose the so-called ”temperature” parameter so that the ESS does not fall below a chosen threshold (we have used 80% in our experiments). Through subsequent tempering steps, the entire set of data is eventually incorporated: At each tempering step the temperature is gradually increased from an initial value of 0 (this means no data is incorporated) to the final value of 1 (all data is incorporated). That is why, from a heuristic perspective, the tempering procedure succeeds when the standard particle filter would normally fail.

Let us describe the intuition of the jittering step. Each tempering step is followed by a resampling procedure that eliminates particles with small weights, and multiplies particles with large weights. As a result, an ”impoverishment” of the particle sample can occur. To counteract this, we use a jittering procedure that spreads the particles around. The procedure is chosen so that, asymptotically, no additional error or bias is added (in other words, should the particles be distributed according to the target posterior, they would remain distributed according to it). Outside the asymptotic regime, there is an inherent local error which controlled by the ”jittering parameter”. On one hand, the jittering parameter has to be chosen so that the local error remains small. On the other hand, it should be sufficiently large to introduce a reasonable spread in the sample in order to improve the quality of the sample. We explain the jittering procedure in section 3.3.

The rest of the paper is structured as follows. In section 2 we describe the damped and forced deterministic system and its SALT version. The deterministic system resolved on a fine resolution spatial grid is viewed as the simulated truth. The reduction to the SALT version is done via the variational approach formulated in Holm (2015). The numerical calibration of the subgrid parameters and the numerical methodologies for solving the two systems are described in Cotter et al. (2019).

In section 3 we formulate sequential data assimilation as a nonlinear filtering problem, in which the SALT equations are used as the signal. We describe in detail each algorithm: bootstrap particle filter, tempering and jittering, which are all required to tackle the high dimensional nonlinear filtering problem.

In section 4 we present and discuss the numerical experiments and results. Two main sets of experiments are considered. In the first set, which we call the perfect model scenario, the true underlying state is a realisation of the signal. In the second set, which we call the imperfect model scenario, data from the fine resolution true state is assimilated. All experiments were run on a modest workstation which has two Intel Xeon processors totalling logical cores and Gb memory. Additionally, an effective method for generating initial ensembles for SALT models is discussed.

Finally, section 5 concludes the present work and discusses the outlook for future research.

The following is a summary of the main numerical experiments and findings contained in this paper:

-

•

Using particles, we ran the particle filter over a period of eddy turnover times (ett, see (46) for definition) separately for two different initial ensembles and observation dimensions and . We chose an assimilation interval of eddy turnover times for the imperfect model scenario, and eddy turnover times for the perfect model scenario. Here eddy turnover time is 1000 fine resolution time steps. The root mean square error (rmse), ensemble spread (), effective sample size (ess) and computational cost (measured in terms of number of equation evaluations) are shown, in figures 5, 6 and 7 for the perfect model scenario, and in figures 13, 14 and 15 for the imperfect model scenario.

- •

-

•

Eulerian trajectories at four individual grid points are shown for the truth, the truth plus realised observation errors, the posterior ensemble mean, the prior ensemble mean and individual ensemble members. These are shown in figures 9 and 10 for the perfect model scenario, and in figures 17 and 18 for the imperfect model scenario.

-

•

In the perfect model scenario, using the tempering based particle filter, the numerical results show that, the data we assimilated, albeit low dimensional relative to the SPDE degree of freedom, gave sufficient information, to allow a reasonably accurate approximation of the true state. Further the posterior ensemble rmse is stable given the size of the observation noise and the data dimension. Reliability tests showed no features of bias, under-dispersion or over-dispersion.

-

•

In the imperfect model scenario, the SALT base model reduction was combined with the the tempering based particle filter. The numerical results show that, despite the discrepancy between model and data, the data we assimilated, albeit very low dimensional relative to the PDE degree of freedom, still provides sufficient information to control the posterior ensemble. We judge that the posterior ensemble mean offers a reasonably accurately approximation of the signal, with rmse errors in the same order as those in the perfect model scenario. Further, the combined algorithm is sufficiently robust, despite slight features of bias and skew shown by the reliability tests on the assimilated ensemble system.

2 Deterministic and stochastic advection by Lie transport GFD models

In this section, we describe the PDE and the SPDE models with Lie transport type stochastic terms. For the theory on SALT SPDEs see for example Holm (2015); Crisan et al. (2018a). We follow Cotter et al. (2019) (also Cotter et al. (2018)) and use a data-driven approach to numerically model the ’s. Thus information regarding the stochastic dynamics is complete except for initial and boundary conditions. Viewed as a parameterisation of the subgrid scales, numerically the SPDE shall be prescribed on a coarse resolution grid and the PDE prescribed on a fine resolution grid.

The spread of the SPDE dynamics from using parameters calibrated with the data-driven approach described in Cotter et al. (2019) adequately captures the large scale features of the PDE dynamics. Those results indicate the feasibility of the calibrated SPDE as model reduction, thus providing the foundation for the present work where we utilise the SPDE as the signal process in a nonlinear filtering formulation. Nonlinear filtering will be the topic of discussion in section 3.

In the following, the domain is assumed for both deterministic and stochastic models.

2.1 Deterministic model

We consider the vorticity version of an incompressible Euler flow with forcing and damping. Let denote the velocity field. Let denote the vorticity of , denotes the -axis. Note that for incompressible flows in two dimensions, is a scalar field. For a scalar field we write Let denote the stream function. The stream function is related to the fluid velocity and vorticity by and respectively, where is the Laplacian operator in . The existence of the stream function is guaranteed by the incompressibility assumption.

We now write down the deterministic model,

| (2) | |||||

| (3) | |||||

| (4) |

We choose the forcing to be given by

| (5) |

where and are constants having the following roles: controls the strength of the forcing; is an integer interpreted as the number of gyres in the external forcing; and can be seen as the damping rate. denotes the Lie derivative of with respect to the vector field . When applied to scalar fields, is simply the directional derivative with respect to , see Chern et al. (1999)

We consider a no-penetration spatial boundary condition

| (6) |

to close the system. This system is a special case of a nonlinear, one-layer quasi-geostrophic (QG) model that is driven by winds above.

2.2 Stochastic model

Consider the space of continuous function whose value at is zero. It is equipped with the Wiener measure and its natural filtration . Let be the canonical Brownian motion on , that is for , is the evaluation map. We write to denote the ’th component of . The SALT version of the Euler fluid equation (2) as derived in Holm (2015). Cotter et al. (2019) introduced damping and forcing to facilitate statistical equilibrium in the underlying resolved system, leading to the following stochastic partial differential equation (SPDE),

| (7) |

where the vector fields represent scaled eigenvectors of the velocity-velocity correlation tensor .

Equation (7) arises from a time-scale separation assumption for the deterministic Eulerian transport velocity , leading to the following Stratonovich stochastic differential equation

| (8) |

where and are divergence free vector fields, from which (7) may be derived. Here one can intuitively think of as the “large” scale mean part of . In this present work since we are interested in the practicality of (7) for data assimilation, we follow Cotter et al. (2019) and make the approximation that the sum in (8) is finite. Hence the stochastic term in (7) also consists of terms.

Let denote the stream function of , and let denote the stream function of , i.e.

Note that is constant in time. The can be solved for and stored on the computer after the are obtained. For this the boundary condition

| (9) |

is enforced for each Then (8) can be expressed in terms of and ,

| (10) |

Expressing the transport velocity in this form is useful because it allows us to introduce stochastic perturbation (i.e. terms with ) via the stream function when solving the SPDE system numerically, thereby keeping the discretisation of (7) the same as the deterministic equation (2), see Cotter et al. (2019).

The full set of stochastic equations is

| (11) | |||||

| (12) | |||||

| (13) |

with boundary condition

| (14) |

The forcing term is the same as the deterministic case.

Remark 1.

For the damped and forced stochastic system considered in this section, on the torus a global wellposedness theorem with the solution space is proved in Crisan and Lang (2019). In a forthcoming sequel to this work we also show the the wellposedness of the solution on the bounded domain with no-penetration boundary conditions. We make the following important assumption.

A 1.

3 Nonlinear Filtering

In this section, we formulate data assimilation as a nonlinear filtering problem in which the aim is to utilise observed data to correct the distribution of predictive dynamics. We describe a particle filter methodology which incorporates three additional techniques that are required to effectively tackle this high dimensional data assimilation problem.

In nonlinear filtering terminology the predictive dynamics is often called the signal 333 Also known as the forecast model in statistics and meteorology literature, (see Reich and Cotter, 2015).. The signal in our setting corresponds to the SALT SPDE. Data is obtained via an observation process which represents noisy partial measurements of the underlying true system state. The goal is to determine the posterior distribution of the signal at time given the information accumulated from observations. This is known as the filtering problem. This is different to inversion problems (also called smoothing problems), where one is interested in obtaining the posterior distribution of the system’s initial condition, see for example Stuart, A.M. (2010).

The stochastic filtering framework enables us not just to provide a solution to the data assimilation problem, but also offer a clear language in which to explain the details and the intricacies of the problem. We detail below an elementary introduction to the filtering problem.

Let denote a given state space, and let denote the set of probability measures on the state space. In what follows the state space will be , where is the dimension of the space. To avoid technical complications we will assume in the following that time runs discretely . We shall work in a Bayesian setting, in other words we will assume that we know the distribution of the signal for , which will be denoted by for . We also assume that partial observations, denoted by , of dimension with are available to us at times and we wish to approximate the signal given the accumulated observations . Of course we could aim to approximate using an arbitrary -adapted estimator , where is the -algebra . However, the best estimator is the conditional expectation of given , . In this context, by the best estimator, we mean the minimiser of the mean square error , where is the standard Euclidian norm on . Of course we would not just want to compute/estimate , but also the error that we would make if we approximate with , i.e., for .

The quantiles of the approximation error will also be of interest. Therefore, in general, the filtering problem consists in determining the condition distribution of the signal given given denoted by . Once is determined, then its first moment (the mean vector) will give us , its covariance matrix can be used to compute the mean square error , etc. So one can adopt one of two different approaches of estimation the signal given partial observations.

-

•

Develop a data assimilation algorithm that results in a a point approximation of the signal using the data . The approximation may or may not be optimal and only, on rare occasions, an estimate of the error will be available.

-

•

Develop a data assimilation algorithm that results in an approximation of the conditional distribution of the signal using the data . This in turn will offer an approximation of the optimal estimator as well as the approximation of the error, quantiles, occupation mesures, etc.

Of course, algorithmically we expect the first problem to be a lot easier than the second. The computation, of an estimator that is an element of would be expected to be a lot easier that that of a probability measure over The first one is a finite dimensional object the latter is an infinite dimensional one. However, in the exceptional case when the signal is a linear time-series and the observation has linear dependence on the signal and they are driven by Gaussian noise the two approaches more or less coincide. The reason is that, in this case is Guassian and one can explicitly write the recurrence formula for the pair , where is the covariance matrix of . So on one hand one can compute directly the optimal estimator and on the other hand the Gaussianity ensure that is fully described by . This is the so-called Kalman-Filter. There are numerous extensions of this method to non-linear filter that attempt a similar methodology for the non-Gaussian conditional distribution. Such approaches are not optimal in the sense that they don’t offer a point estimator that is the optimal one and the corresponding “covariance” matrix that is produced is not the covariance matrix of . The existing literature in this direction is vast, we cite here (Reich and Cotter, 2015; Evensen, 2009; Ljung, 1979).

Particle filters are a class of numerical methods that can be used to implement the second approach. They have been highly successful for problems in which the dimension of the state space has been low to medium. However, in recent works (Kantas et al., 2014; Beskos et al., 2017, 2014) they have been shown to also work in high dimensions . In this paper, we tackle a state space with dimension of order . For a filtering perspective, we overcome here one other hurdle as we explain below.

Let us denote by , the (prior) distribution of the signal on the path space . The prior distribution of the signal and the observations , are the building blocks of , . To be more precise, one can show that there exists a mapping

| (18) |

such that . Under very general conditions (for example, it is enough to assume that the likelihood functions are continuous in the variable and apply Lemma 2.4 from (Crisan et al., 2018b)) on the signal and the observation, this mapping is jointly continuous on the product space This would mean that will give a reasonable approximation of the conditional distribution of the signal as long as the distribution does not differ significantly from the one used to construct . The same will happen when the true law of the observation does not differ significantly from the chosen model. This property of the posterior distribution is crucial, see imperfect model in section 4 for details.

In the rest of this section we consider only the space-time discretised SPDE signal, of spatial dimension . The observation process is given by noisy spatial evaluations of an underlying true system state at discrete time steps. We consider two scenarios for the underlying true system state, henceforth called the truth.

In the first scenario, we aim to compute the conditional distribution of the signal given partial observations of a single realised trajectory of the SPDE system. In this case the predictive dynamics and the truth are from the same dynamical system. We call this the perfect model scenario (or twin experiment, see Reich and Cotter (2015)).

In the second scenario, we use instead noisy spatial evaluations of a space-time discretised solution corresponding to the PDE system (2) – (6). We call this the imperfect model scenario. The truth in this case is computed on a more refined grid than solutions of the SPDE. Nevertheless the solution of the SPDE converges to that of the PDE as the coarser grid converge, see Cotter et al. (2019). Similarly the corresponding observations will converge (provided the observation noise does not change). This ensures the successful assimilation of PDE data into the SPDE model, assurance from the uncertainty quantification tests shown in Cotter et al. (2019) is necessary to numerically guarantee that the mis-match between state spaces remains small.

To our knowledge, this is the first application of particle filters to the case where the signal is described by a SALT SPDE system. As we explain below a straight application of the classical bootstrap particle filter algorithm fails. To succeed we implement and incorporate the following procedures.

-

•

Model reduction – approximate a high dimensional system using a low dimensional system via stochastic modelling, the result of which can be further reduced by choosing a projection of the noise process onto a submanifold. This was accomplished in Cotter et al. (2019).

-

•

Tempering – compute a sequence of intermediate measures parameterised by a finite number of temperatures that control the smoothness of the density of . This procedure eases the problem of highly singular posteriors in high dimensions, which come from the fact that high dimensional observations are too informative.

-

•

Jittering – a Markov chain Monte Carlo (MCMC) based technique for recovering lost population diversity in particle filter algorithms.

These techniques are added to the basic bootstrap particle filter, and are demonstratively necessary, theoretically consistent and rigorously justified. In addition, we shall pay particular attention to the initialisation of the particle filter, though this is discussed in section 4.1.

Before proceeding to the problem formulation, we insert an important remark.

Remark 2.

Our spatial discretisations for the PDE and SPDE fields are defined on appropriate finite element spaces, see Cotter et al. (2019) for details of the numerical methods we use for the models under consideration. Under assumption 1, it is important to understand that instead of the finite state space , the actual problem involves measures defined on infinite dimensional function spaces, in particular it is highly plausible that in theory the state space for the SPDE is Sobolev for . Discussions of these technical complications are not the focus of this work. And since in practise we work with numerical solutions anyhow, we setup our filtering problem in a finite dimensional setting. However, the methods we use are all theoretically consistent in the limit, see Stuart, A.M. (2010); Dashti and Stuart (2017).

In light of remark 2, henceforth we drop the word “discretised” when describing the state space, signal and observation processes.

3.1 Filtering problem formulation

Consider discrete times . Let be a discrete time Markov process called the signal. Let be a discrete time process called the observation process. We assume almost surely (a.s.). We consider Eulerian data assimilation where the observations correspond to fixed spatial points , for all As already mentioned in the introduction, we denote the dimensions of and by and respectively.

We take and to correspond to the velocity vector field. Mathematically we could also consider the vorticity field or the stream function, but in real world scenarios those fields may be difficult to observe directly. We denote by and the path of the signal and of the observation process from time to time ,

Let and denote particular trajectories of and . For notational convenience, we may write in the subscripts to mean .

It is useful to introduce the following standard notation in the case when is a measure and is a measurable function, and is a Markov kernel

The marginal distribution of the signal changes according to

| (19) |

for , and is a probability transition kernel defined by the push-forward of using the (discretised) SPDE solution map from assumption 1.

In standard filtering theory the observation process is defined by

| (20) |

where is a Borel-measurable function, and for , are mutually independent Gaussian distributed random vectors with mean zero and covariance matrix . Thus

| (21) |

for and Gaussian density . For convenience, define which is commonly referred to as the likelihood function.

We can now define the filtering problem.

Problem (Filtering Problem).

For , we wish to determine the conditional distribution of the signal given the information accumulated from observations, i.e.

| (22) |

for all bounded measurable functions , with being the given initial probability distribution on the state space . In particular when for we have .

In statistics and engineering literature, is often called the Bayesian posterior distribution. Note that is a random probability measure. For arbitrary , denote

We also introduce predicted conditional probability measures and defined by

We have -almost surely the following Bayes recurrence relation, see Bain and Crisan (2009). For and ,

| prediction | (23) | |||

| update | (24) |

where

is a normalising constant. Due to (24), we may also write , thus .

In the general case for any bounded measurable function , we have for problem Problem the recurrence relation

| prediction | (25) | |||

| update | (26) |

Except for a few rare examples of the signal, it is extremely difficult to directly evaluate because there are no “simple” expressions. In section 3.2 we shall describe the particle filter methodology that we employ to tackle the filtering problem. Note that in statistics and engineering literature, particle filters are often called sequential monte carlo (SMC) methods.

3.2 Particle filter

Particle filter methods are among the most successful and versatile methods for numerically tackling the filtering problem. A basic algorithm implements the Bayes recurrence relation by approximating the measure valued processes and by -particle empirical distributions. The position of each particle is updated using the signal’s transition kernel. At the same time, individual weights are kept up-to-date in accordance with the updated particle positions. It is in the weights updating step that we take into account the information provided by the observations: particles are reweighted using the likelihood function. A new set of particle positions can be sampled based on the updated weights and the procedure iterates.

Due to the high dimensional nature of the systems in consideration, additional techniques are necessary in order to make the basic algorithm work effectively. We provide a concise presentation of the algorithms employed, and note that these methods are all mathematically rigorous. For more thorough discussions we refer the reader to Bain and Crisan (2009); Reich and Cotter (2015); Dashti and Stuart (2017); Kantas et al. (2014); Beskos et al. (2014).

3.2.1 Bootstrap particle filter

The basic algorithm, called the bootstrap particle filter or the sampling importance resampling (SIR) algorithm, proceeds in accordance with the Bayes recurrence relation (23) – (24) by repeating prediction and update steps. To define the method, we write an -particle empirical approximation of . Thus we have

| (27) |

where denotes Dirac measure. The discrete measure is completely determined by particle positions and weights , . We define the update rule

for advancing to to be given by the numerical implementation of the SPDE solution map G, see (17),

| (28) |

Note that each particle position is updated independently.

For the weights, suppose the particles , are independent samples from then we have equal weighting for each particle

This does not change in the prediction step, thus

| (29) |

To go from to , the weights need to be updated to take into account the observation data at time . This is done using the likelihood function (21),

| (30) |

Using (27) but with the collection of updated particle positions and normalised weights , we obtain .

In the above we assumed to have started with independent samples from before proceeding with prediction and update. Thus after we obtain we have to generate independent (approximate) samples from in order to iterate the above prediction and update steps for future times. This is done via selection and mutation steps. Otherwise the non-uniform weights are carried into future iterations until resampling is required.

- Selection

-

In high dimensions, can easily become singular due to the observations being too informative. This means after the update step, most of the normalised weights are very small. Thus with a finite support, does not have enough particle positions in around the concentration of the true distribution . Therefore it is desirable to add a resampling step so that particles with low weights are discarded, and replaced with (possibly multiple copies of) higher weighted particles. This selection is done probabilistically; for example, one could draw uniform random numbers in the unit interval and select particles based on the size of , see Bain and Crisan (2009); Reich and Cotter (2015).

- Mutation

-

Since the resampling step can introduce duplicate particle positions into the ensemble, without reintroducing the lost diversity, repeated iterations of resampling will eventually lead to a degenerate distribution (i.e. measures whose support are singletons). To tackle this issue we apply jittering after every resampling step. Jittering is based on Markov Chain Monte Carlo (MCMC) whose invariant measure is the target . The jittering step shifts duplicate particle positions whilst preserving the target distribution. We discuss this in section 3.3.

After resampling is applied, we obtain a new ensemble with equal weights , i.e.

When we do not resample, then the particles in the ensemble keep the weights given by , and use (27) for .

The resampling step should be done only when necessary to reduce computational cost, because the jittering step requires evaluating the solution map . Therefore we employ a test statistic to quantify the non-uniformity in the weights and only resample when the non-uniformity becomes unacceptable. For this we use the effective sample size (ess) statistic. It is defined by the inverse -norm of the normalised weights ,

| (31) |

The ess statistic measures the variance of the weights. If the particles have near uniform weights then the ess value is close to On the other hand if only a few particles have large weights then the ess value is close to In practice we resample whenever (31) falls below a given threshold

Algorithm 1 summarises the bootstrap particle filter. The algorithm starts with an empirical approximation of the initial prior and steps forward in time, assimilates observation data in repeating cycles of prediction-update steps. The ess statistic is employed. When resampling is required, selection-mutation steps are applied.

Let total number of iterations be given. Draw independent samples and set weights

3.3 MCMC and jittering

In this section we describe an effective Metropolis-Hastings MCMC based method called jittering with the proposal step chosen specifically for our signal. Jittering reintroduces lost diversity due to resampling by replacing an ensemble of samples that contain duplicates with a new ensemble without duplicates, such that the distribution is preserved.

MCMC is a general iterative method for constructing ergodic time-homogeneous Markov chains with transition kernel , that are invariant with respect to some target distribution , i.e.

By the Birkhoff’s ergodic theorem, we have the following identity

for any integrable and measurable function Practically, this means starting from an initial , each with can be treated as samples from the target distribution .

A generic Metropolis-Hastings MCMC algorithm is described in algorithm 2. A Markov transition kernel defined on the state space is used to generate proposals. Together with the right conditions on the acceptance probability function to guarantee detailed-balance, the algorithm produces a Markov chain with kernel that is reversible with respect to the target measure , see Dashti and Stuart (2017). In the Gaussian case, a classic and widely used choice for and is

| (32) | ||||

for any appropriate covariance operator and log likelihood function , see Kantas et al. (2014). The parameter controls the local exploration size of the Markov chain. In practise for high dimensional problems needs to be very close to 1 in order to achieve a reasonable average acceptance probability. For bad choices of the MCMC chain may mix very slowly and would require a burn-in step size that makes the whole algorithm computationally unattractive.

Let be a given measure on the state space. Let . Generate a -invariant Markov chain as follows

| (33) |

| (34) |

With (32), algorithm 2 is known as the Preconditioned Crank Nicolson (pCN) and is wellposed in the mesh refinement limit, see Dashti and Stuart (2017); Kantas et al. (2014). Thus when applied to discretised problems the algorithm is robust under mesh-refinement. It is commonly applied in Bayesian inverse problems where the posterior is absolutely continuous with respect to a Gaussian prior on Banach spaces. It is important to note that here the design of the algorithm is important because in high dimensions measures tend to be mutually singular, but for Metropolis-Hastings algorithms the acceptance probability is defined as the Radon-Nikodym derivative given by the stationary Markov chain transitions.

Our choice (57) for the prior is not Gaussian. The distribution (19) is also not Gaussian for any . The distribution of the SPDE solution is investigated numerically in Cotter et al. (2019), in which it is noted that non-Gaussian scaling is interpreted as intermittency in turbulence theory. Therefore it is important to choose and such that the following properties hold.

-

(i)

Robustness under mesh refinement. Although we are considering finite dimensional state spaces, in the limit the state spaces under assumption 1 are infinite dimensional function spaces.

-

(ii)

The chain should mix and stablise sufficiently quickly so that the number of burn-in steps required is reasonable.

Then with the appropriately chosen and , we apply algorithm 2 as a jittering step to shift apart duplicate particles introduced into the ensemble by the resampling step.

Given these considerations, we use directly the SPDE solution map (17) to define the transition kernel . Let the target distribution be the posterior distribution , . With a slight abuse of the notation introduced in (17), we write

to mean the solution of the SPDE at time along a realised Brownian trajectory over the time interval starting from position . When we consider and interval as fixed, then we view as a function on .

Let be the empirical approximation of with particles . We consider each particle a child of some parent at time for a realised Brownian trajectory over the interval , i.e.

To jitter , set and (see algorithm 2). At the -th MCMC iteration, , propose

| (35) |

where is a Brownian trajectory over generated independently from .

We use the canonical Metropolis-Hastings accept-reject probability function

| (36) |

where is the likelihood function, see (24). The proposal (35) is accepted with probability (36) independently of . In this case set

Otherwise the proposal is rejected, in which case set

and go to the next iteration in algorithm 2.

Algorithm 3 summarises our MCMC procedure. The algorithm includes tempering scaling of the accept-reject function (36). Tempering is explained in the next subsection. Practically, to save computation, we may apply jittering to just the duplicated particles after resampling, and run each jittering procedure for a fixed number of steps.

Proposition 1.

Proof.

The generic Metropolis-Hastings algorithm 2 defines the following Markov transition kernel

| (37) |

Since if is such that it satisfies the detailed balance condition with respect to

| (38) |

then using the accept-reject function (36)

we have is a Markov kernel that is -invariant, see Dashti and Stuart (2017).

Let denote the Wiener measure. Note that for a Brownian path it is standard to show that the noise proposal in (35)

for independent of . Thus due to the prediction formula (23) and Markov transition (19) for the signal, conditioned on the value , we have for , a sample obtained using the proposal (35) is thus

i.e. conditioned on , we have

which is symmetric in the pair giving us detailed balance (38).

∎

Remark 3.

The purpose of the jittering procedure is to introduce diversity in the samples, through a small perturbation, that is achieved via the Metropolis-Hastings algorithm. The perturbation is small as it is controlled by the parameter which we take it to be 0.9995 (if is equal to then no bias occurs). Therefore the error incurred in this step will be small, and this is the intention here rather than trying to preserve the underlying posterior distribution. The reason for this error is as follows. If one operates directly on the target posterior distribution, the jittering step preserves the posterior distribution and therefore no bias occurs. However, the jittering procedure is applied to the approximating measure (the one given by the particle filter combined with the tempering methodology). As a result, there will be a “local” error induced by the jittering step proportional to . In the rigorous analysis of the rate of convergence of the particle filter, this appears as a separate term. This is covered, for example in Crisan and Doucet (2002, lemma 4), and in Crisan and Míguez (2018, section 4.2) (albeit in a different context).

Let , . Let the number of MCMC steps be fixed. Given the ensemble of equal weighted particle positions , corresponding to the ’th tempering step with temperature , and proposal step size , repeat the following steps.

| (39) |

3.4 Tempering

Empirical approximations of defined on high dimensional space can very quickly become degenerate, which is indicated by low effective sample size (ess) statistic. In order to facilitate smoother transitions between posteriors, so that ensemble diversity is improved, we employ the tempering technique, see Neal (2001); Kantas et al. (2014); Beskos et al. (2017, 2014). Use of other techniques such as nudging and space-time particle filter (see Beskos et al. (2017)) will be explored in future research work.

We employ tempering when the ess value for an posterior ensemble, falls below an apriori threshold . The idea of tempering is to artificially scale the log likelihoods by a number called the temperature, which in effect increases the variance of the distribution so that the apriori ess threshold is attained. Once this done resampling can be applied (with MCMC if required) which leads to a more diverse ensemble. Of course particles in this new ensemble are samples of the altered distribution which is not what we desire, therefore the procedure is repeated by finding the next temperature value in the range . This is repeated until the temperature scaling is 1 so that the original distribution is recovered.

More precisely, let

| (40) |

be a sequence of temperatures. Let

| (41) |

be called the tempered posterior at the -th tempering step or simply the -th tempered posterior, where (compare with the recurrence formula (24)). Note that and . Thus with

we have

which suggests the iterative procedure,

| (42) |

Empirically this means, for each , assume we have equal weighted particle positions that give us the empirical -th tempered posterior

we compute unnormalised tempered weights

| (43) |

to obtain the empirical -th tempered posterior

Then we resample according to and apply the MCMC jittering algorithm 3 (see remark 4) to separate apart any duplicated particles before going to the ’th iteration step.

The sequence of temperatures is chosen so that at each tempering iteration , the empirical tempered distribution attains the apriori ESS threshold , i.e.

| (44) |

where are the normalised weights corresponding to (43). This way the choice for the temperatures can be made on-the-fly by using search algorithms such as binary search at each tempering iteration.

Remark 4.

Proposition 1 shows the MCMC jittering algorithm preserves the target distribution with the accept-reject function (36). The same argument shows the algorithm preserves the tempered posteriors as long as the accept-reject function is chosen to be (39). The Markov transition kernel satisfies the detailed balance condition with respect to independent of tempering.

Using tempering to smooth out the transition between consecutive filtering measures (i.e. from to ) ensures that the importance weights in (41) exhibit low variance, so that no small group of particles are favoured much more than the rest when resampling, see Kantas et al. (2014), thus leading to a more diverse population.

In algorithm 4 we summarise the complete procedure for one filtering step, i.e. from to , incorporating adaptive tempering and MCMC jittering for SALT into the bootstrap particle filter.

Consider the ’th filtering step corresponding to . Given the ensemble of equal weighted particle positions that define the empirical posterior , we wish to assimilate observation data at time to obtain a new equally weighted ensemble that define . Define

for , and are the normalised values of the unnormalised tempered weights (43).

4 Numerical setup and experiment results

The setup for the numerical experiments follow on from the calibration and uncertainty quantification work presented in Cotter et al. (2019). Thus the parameter choices for the models are as follows: forcing strength , number of gyres and damping rate .

The PDE (2) and SPDE (7) are prescribed on mesh of size cells and cells respectively for the spatial domain. We use a Galerkin finite element discretisation for the spatial variable and a third order stability preserving Runge-Kutta for the time stepping, see Cotter et al. (2019) for details. This means spatially each mesh cell contains six grid points. Thus the PDE and SPDE velocity fields are of and degrees of freedom respectively. Henceforth we shall refer to the PDE spatial dimension as fine resolution and the SPDE spatial dimension as coarse resolution444However since we are using an explicit in time method for solving the SPDEs, the coarse time step may need to be smaller to accommodate the fact that Brownian increments are unbounded..

The time step for the fine resolution is chosen in accordance with the CFL condition and in this case is . The CFL time step for the coarse resolution is .

The initial reference fine resolution PDE trajectory was spun-up from the configuration

| (45) | ||||

until some energy equilibrium state, see Cotter et al. (2019). We call the equilibrium state’s corresponding time point the initial time .

We use eddy turnover time (abbrev. ett) as the time dimension for the PDE system. It describes the time scale of flow features correponding to a given length scale, and is defined by

| (46) |

where is the magnitude of the stabilised mean velocity555Our PDE system is spun-up from (45) to an energy stable state. By stabilised mean velocity, we mean the norm of the velocity field that corresponds to the energy stable state. Thus is constant in time., and a length scale. Here corresponds to the axis length of the domain . For our experiments, we choose . It is estimated that ett roughly equals to numerical time units, or (fine resolution) CFL numerical time steps. Since the SPDE is thought of as a stochastic parameterisation for the PDE, we shall use the same eddy turnover time dimension for the SPDE. Thus 1 ett is coarse resolution CFL numerical time steps.

For the SPDE model, we use the calibrated EOFs from Cotter et al. (2019) with corresponding to of the total spectrum. This choice is informed by uncertainty quantification tests and amounts to when the SPDE is prescribed on a mesh of size cells.

For the numerical filtering experiments, we consider two scenarios for the observations.

-

1.

Perfect model: the observations correspond to a single path-wise solution of the SPDE. Thus there is no discrepancy between the model and the true state. In this scenario the theoretical filtering formulation applies directly. We treat this scenario as a test case for the filtering algorithm.

-

2.

Imperfect model: the observations correspond to the solution of the PDE, i.e. (20) is changed to

where corresponds to the coarse grained PDE velocity field, see remark 5. Here there is mismatch between the truth and the signal. As shown in Cotter et al. (2019), the law of the SPDE discretised on the chosen grid converges to the law of the PDE as the discretisation grid gets refined. Implicity also the law of the sequence of true observations is close to the law of the model observations. As stated in (18), is a continuous function of the law of the signal and the observations so we expect a reasonable approximation of even when we don’t use the true law of the signal666The true law of the signal is the push-forward of , the initial distribution of the signal . In the case when is deterministic then the distribution of the signal is a Dirac delta distribution. but the model law.777For continuous time models, this property is called the robustness of the filter. See Clark and Crisan (2005) for results in this direction.

Remark 5.

In the imperfect model scenario, since the SPDE solution is meant to capture the large-scale features of the deterministic fine resolution dynamics that are resolvable at the coarse resolution, we should obtain observations from the coarse grained PDE solution. For coarse graining, we use the inverse Helmholtz operator

| (47) |

and apply to the PDE stream function (4) to average out its small scale features. The boundary condition we impose on the coarse grained stream function is the same Dirichlet condition as for (4). The value in the definition of corresponds to the coarse resolution, in this case . To obtain the coarse grained PDE velocity field, apply the linear operator to the coarse grained stream function. The coarse grained PDE velocity field is then used to generate the observation data in the imperfect model filtering scenario. It is important to note that this coarse graining procedure is only applied when we obtain observation data, the underlying fine resolution dynamics is unchanged.

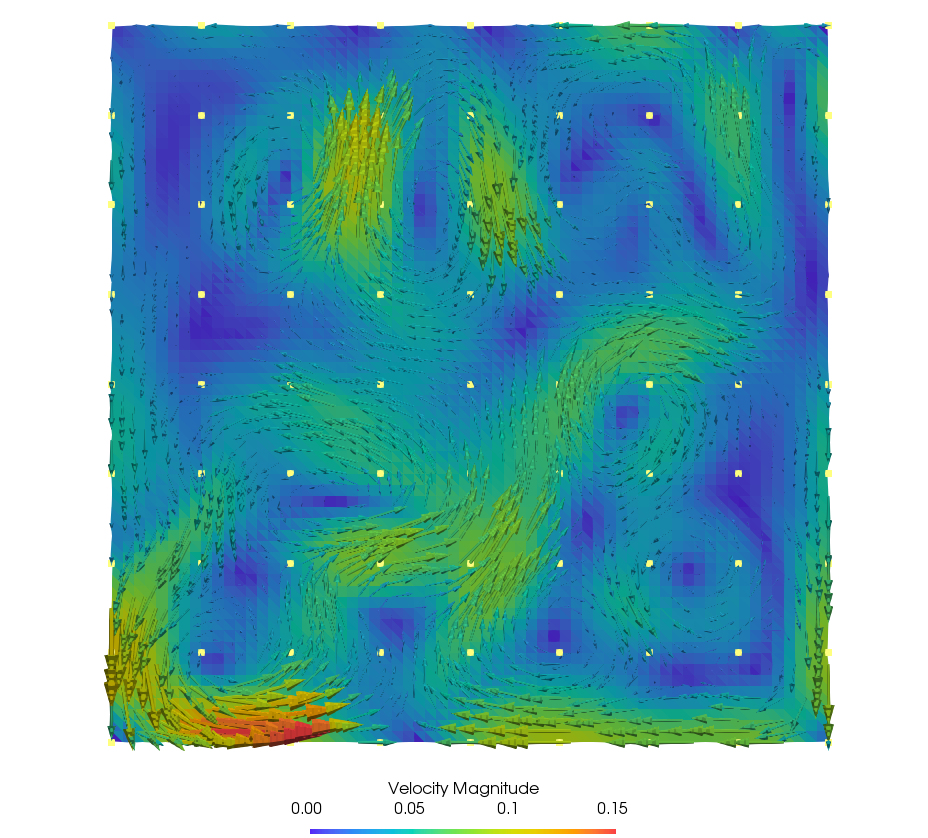

In both scenarios the observations are defined as noisy point measurements of the truth’s velocity field. The observation locations (thought of as “weather stations”) are given by a uniform regular grid of dimension ; see section 3.1 for the problem’s mathematical formulation. We investigate the impact of the number of weather stations using , and in some experiments. For this paper we only consider fixed uniform geometry for the weather stations. Further the weather stations are a subset of the weather stations , and the weather stations in turn are a subset of the weather stations. Figure 1(a) visually illustrates a snapshot of the coarse grained numerical PDE solution velocity vector field overlaid with the positions of the weather stations.

Remark 6.

The dimension of the observation space compared to the dimension of the underlying truth is very small. Using weather stations amounts to of the overall degrees of freedom in the perfect model scenario, and of the overall degrees of freedom in the imperfect model scenario. Observation error size and/or observation data dimension affects the number of tempering and jittering steps. For our observation error size choice, these parameter choices are the best we can do given our computational hardware, so that we can obtain numerical results in a reasonable amount of time. Figures 7 and 15 provide computation cost estimates for the numerical experiments, measured in terms of number of equation evaluations. For reference, all numerical experiments for this paper were run on a workstation equipped with two Intel Xeon CPUs totalling logical processors, and GB of memory. To evaluate SPDE ensembles, the ensemble members were run in parallel, in batches of 25.

Remark 7.

To illustrate the difference in computational cost between the fine resolution and the coarse resolution models, we ran a benchmark test. For a time interval of 0.1 time units, the fine resolution PDE (time step 0.0025 time units) took 24 seconds to run on our workstation. The coarse resolution SPDE (time step 0.02 time units) took 0.6 seconds to run on our workstation.

The observation error covariance (see (20) for definition) is calibrated by computing the standard deviation of the fine resolution PDE velocity field within coarse cells, and then averaged along the time axis. More precisely, let denote the discretised PDE state space. Let denote a snapshot in time of the PDE velocity field. Let superscript indices denote vector component. Define by

for coarse cells corresponding to the coarse resolution mesh. Thus are the local coarse cell averages of . Then we define by

| (48) |

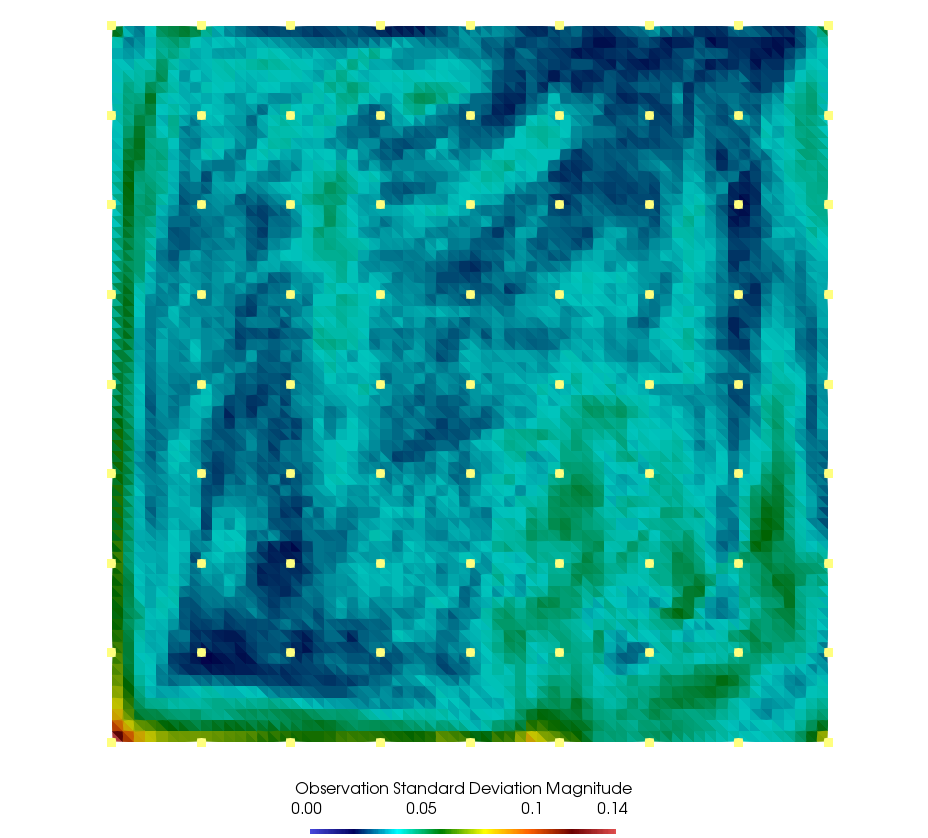

where is a scaling we use to control the magnitude of the observation error. We choose for our numerical experiments. The idea is at the observation locations represent the local variability of the truth at the observation locations. The computed using (48) is a vector field defined on the fine resolution grid. It is evaluated at the observation locations when used in (20). Figure 1(b) visually illustrates the magnitude of overlaid with the observation locations. We use the same calibrated in both problem scenarios.

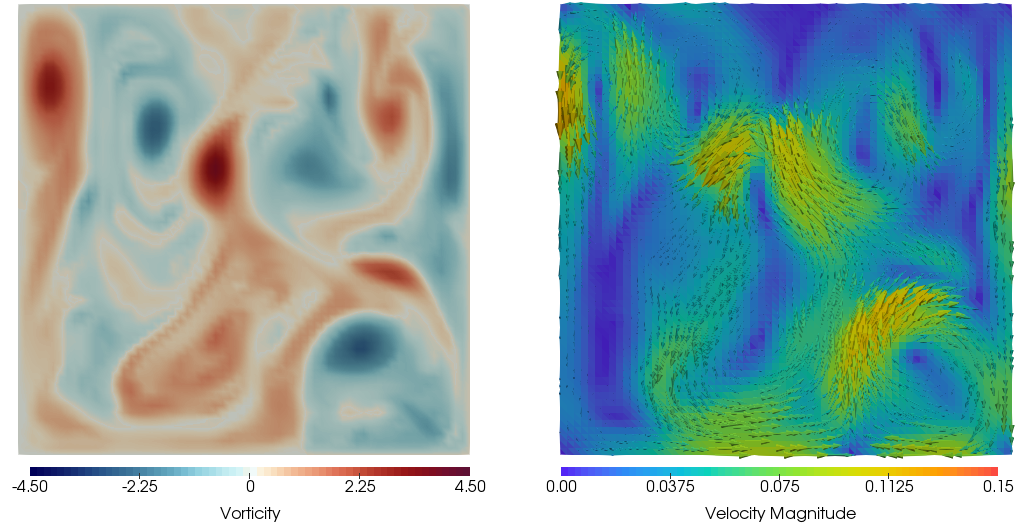

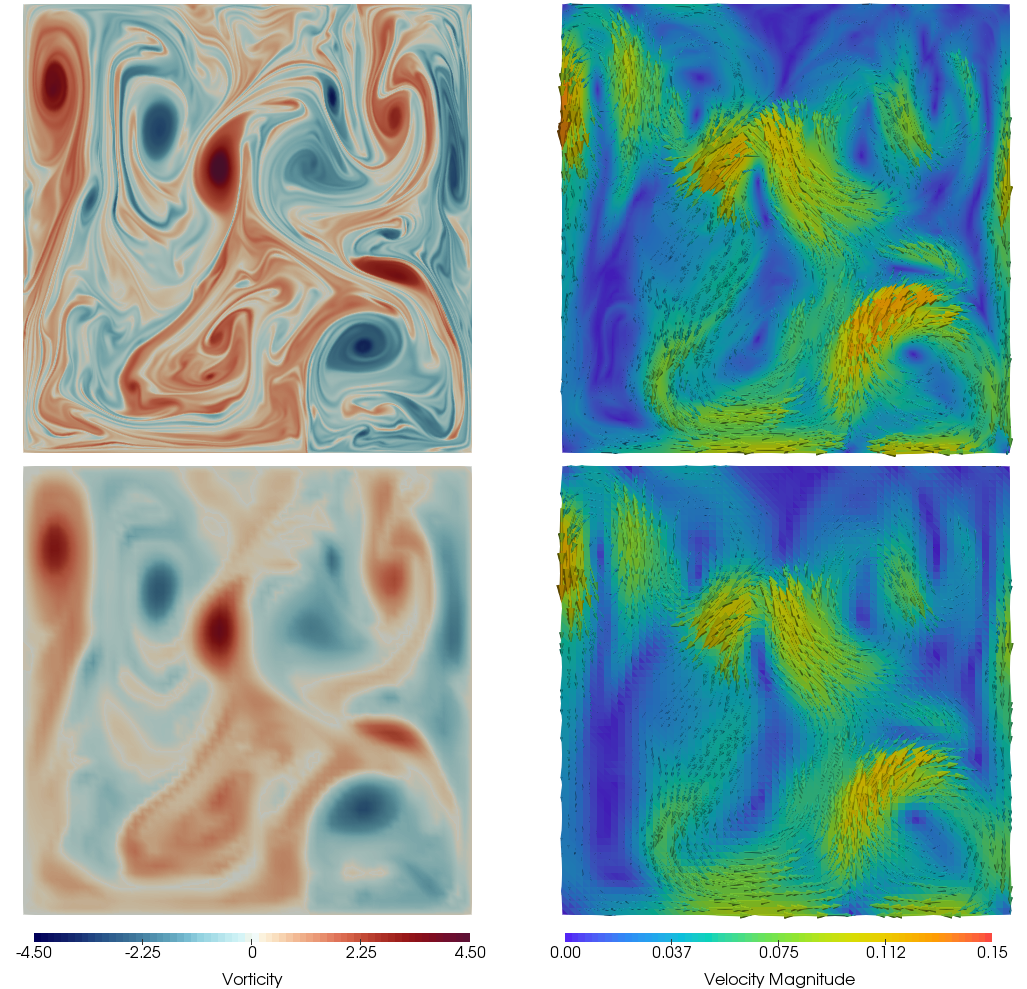

In the perfect model scenario, the truth from which we obtain the observations is a single simulated realisation of the SPDE. The initial condition for the SPDE truth is a particular sample from . See figure 2 for a visualisation of the SPDE truth without observation noise at the initial time . We discuss what is and how we sample from it in section 4.1. In the imperfect model scenario the truth is the coarse grained PDE velocity field. Figure 3 shows a visualisation of the PDE truth without observation noise at the initial time .

We use an ensemble size of particles. Each particle’s initial condition is a sample from the initial distribution . Also we do not assimilate at since the initial distribution is assumed given, see section Problem.

Additionally, we introduce the following two distributions, whose ensemble approximations are utilised in our numerical experiments. We let

| (49) |

be the step forecast distribution. We let

| (50) |

denote the prior distribution. In section 3.2, we have used superscript to denote the particle approximation of a distribution. For notational convenience, throughout this section, we drop the superscript when referring to the ensembles.

To analyse the numerical results, we evaluate the following statistics.

-

•

The root mean square error ( rmse) between the ensemble mean of a particle measure and a verification. For example, the rmse between the step forecast ensemble mean and the true system state at time index is given by

(51) -

•

The ensemble spread () of a particle measure. For example, the ensemble spread of the forecast distribution is given by

(52) -

•

The effective sample size (ess) statistic (31) for measuring the variance of the ensemble weights. Throughout, We choose the threshold to be of the ensemble size, i.e.

-

•

Rank histograms for assessing the reliability of the particle filter, see Broecker (2018); Reich and Cotter (2015). This is a standard measure of ensemble reliability. At any reference grid location, given the ensemble values that corresponds to the forecast distribution (23), and an observation value , define the rank function

(53) The rank function takes values in . If the ensemble forecast is reliable then is a uniform random variable, meaning the verification and the ensemble members are indistinguishable. Thus collecting the rank values over time , we should obtain a “flat” histogram plot if the particle filter gives reliable results. Further it is shown in Broecker (2018) that the rank statistic is of distribution with degrees of freedom.

| Initial ens. set 1 | Perfect model scen. | ||

| Imperfect model scen. | |||

| Initial ens. set 2 | Perfect model scen. | ||

| Imperfect model scen. |

4.1 Initial distribution

The initial distribution comes from the following construction which we call deformation, see Cotter et al. (2019). The procedure can be understood as applying a random temporal scaling to a given field. Let be a fine resolution PDE vorticity field. Using the coarse graining operator (defined in (47)), define operator by

| (54) |

where is the (vorticity) solution of the linear PDE

| (55) | ||||

| (56) |

is a centered Gaussian weight with an apriori variance parameter and is random draw from a uniform distribution on . and are independent. Then

| (57) |

Remark 8.

Practically, we randomly draw a vorticity field from the energy stable period prior to the initial data assimilation time point . The drawn vorticity state is then used to compute its corresponding stream function by inverting the Laplacian and using the same Dirichlet condition as for (4). The velocity field in (55) is then obtained from the stream function. Thus for the linear system (55) the boundary condition is supplied via the sampled .

In Hamiltonian mechanics, the conservation laws associated with relabelling symmetries are called Casimirs. In lemma 2 we show our choice for the prior distribution is physical in the sense that any sample generated by the procedure preserves the Casimirs of the truth .

Definition 1 (Casimir, see Gay-Balmaz and Holm (2013)).

For 2D incompressible ideal fluid motion, the Casimirs are

for any .

Lemma 2 (Preservation of Casimirs).

Let the domain be bounded with piecewise smooth boundary. Assume the sampled vector field is divergence free and with being the normal to the boundary , then preserves the Casimir values of .

Proof.

We have

where the last equality follows from integration by parts and the conditions assumed on . ∎

To investigate the impact the initial distribution can have on the filtering experiment, we generate two different sets of initial ensemble. Each set contains ensemble members. For both sets, is taken to be the imperfect model observation’s initial condition (see figure 3 for visualisations), and we choose for the random scaling parameter . For the first set, equation (55) is solved for fine resolution CFL time steps. For the second set, equation (55) is solved for fine resolution CFL time steps. This way, we obtain two initial ensembles whose ensemble average rmse differ by two orders of magnitude, see table 1.

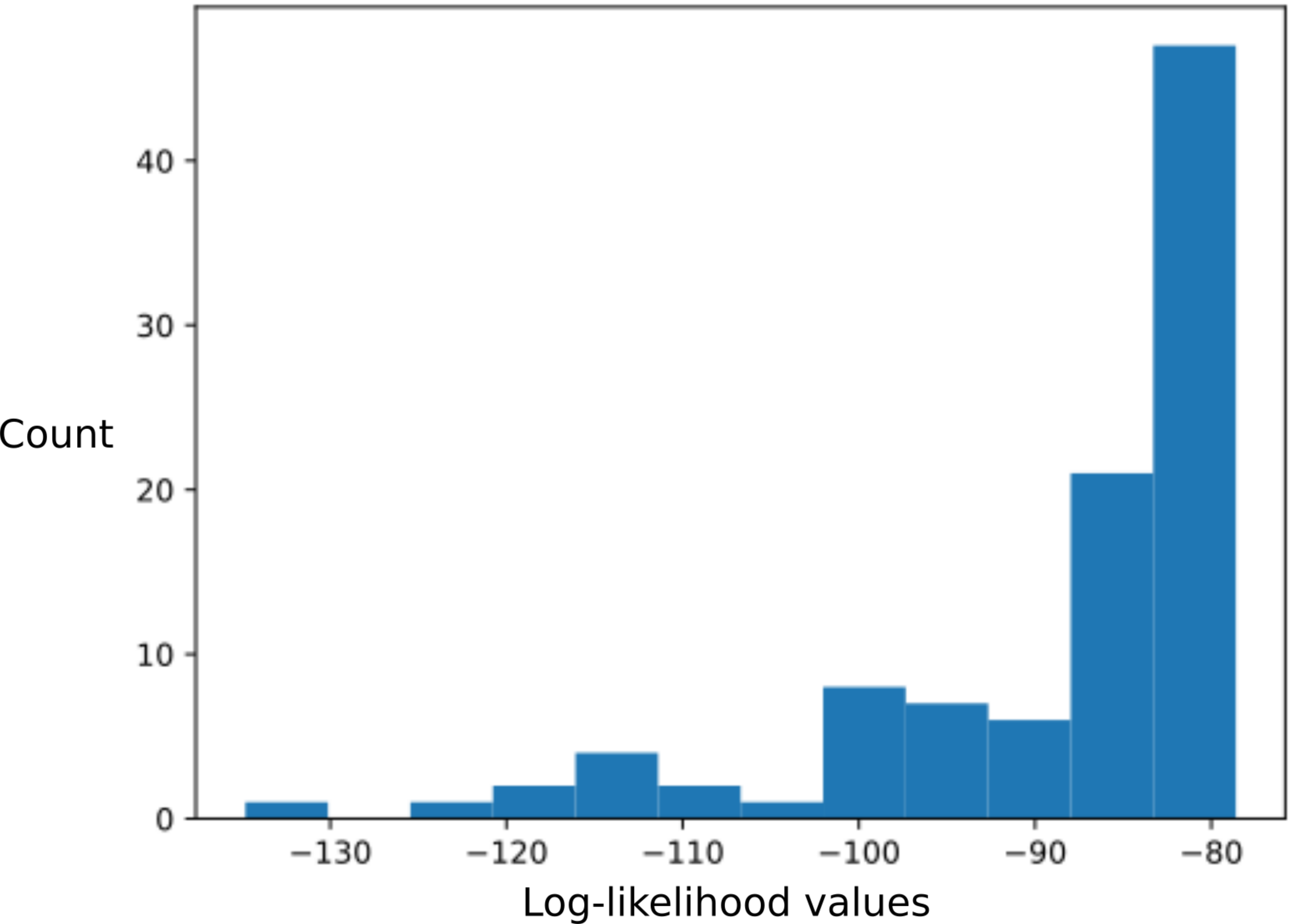

Before discussing experiment results, figure 4 shows a histogram of the log-likelihood values for an ensemble of particles that defines the forecast distribution , with ett. It shows straightforwardly the singular nature of and that without tempering and MCMC jittering, a plain bootstrap particle filter algorithm would fail in the sense that particle diversity would be lost very quickly, leading to degenerate posteriors .

4.2 Perfect model scenario

A single realisation of the SPDE was used as the truth for the experiments in this scenario. The data assimilation experiments are defined by the following parameters: time interval between assimilations ett (every coarse time steps), number of weather stations , observation error scaling . We ran the same experiment setup for each of the two initial ensembles (see table 1), using ensemble size and for a total experiment period of ett. Note that ett is equivalent to coarse resolution time steps. For our assimilation interval choice, ett amounts to data assimilation steps. The experiments were run independently of each other.

This scenario serves as an important test case for the filtering algorithm because there is no discrepancy between the model and the true state. We want to see a stable rmse error between the posterior ensemble mean and the truth. This is an important indicator to show that the filter does not lose track of the signal over the experiment period. If the results do not show this, then it would be very unlikely that the filtering algorithm can be made to work with the PDE to SPDE model reduction.

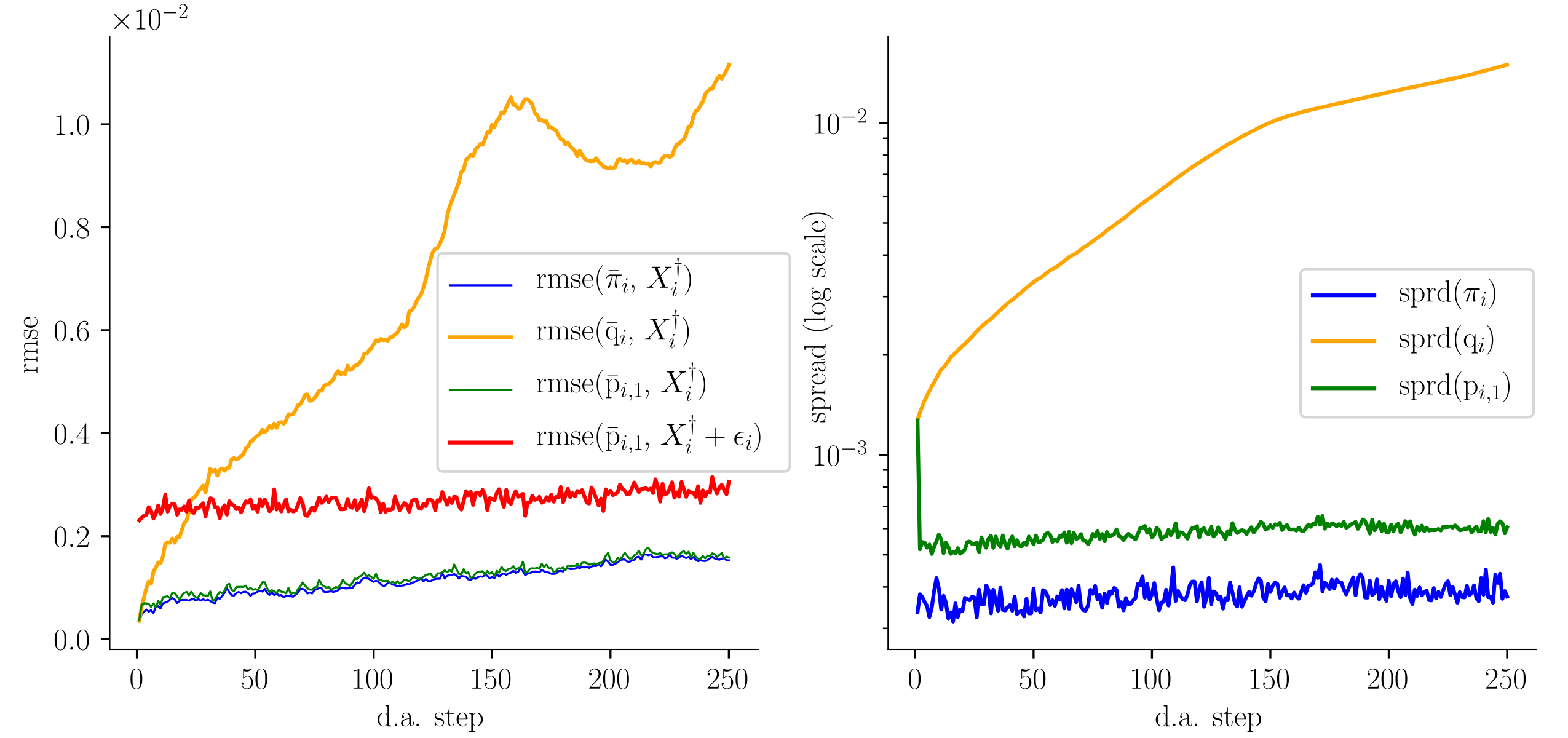

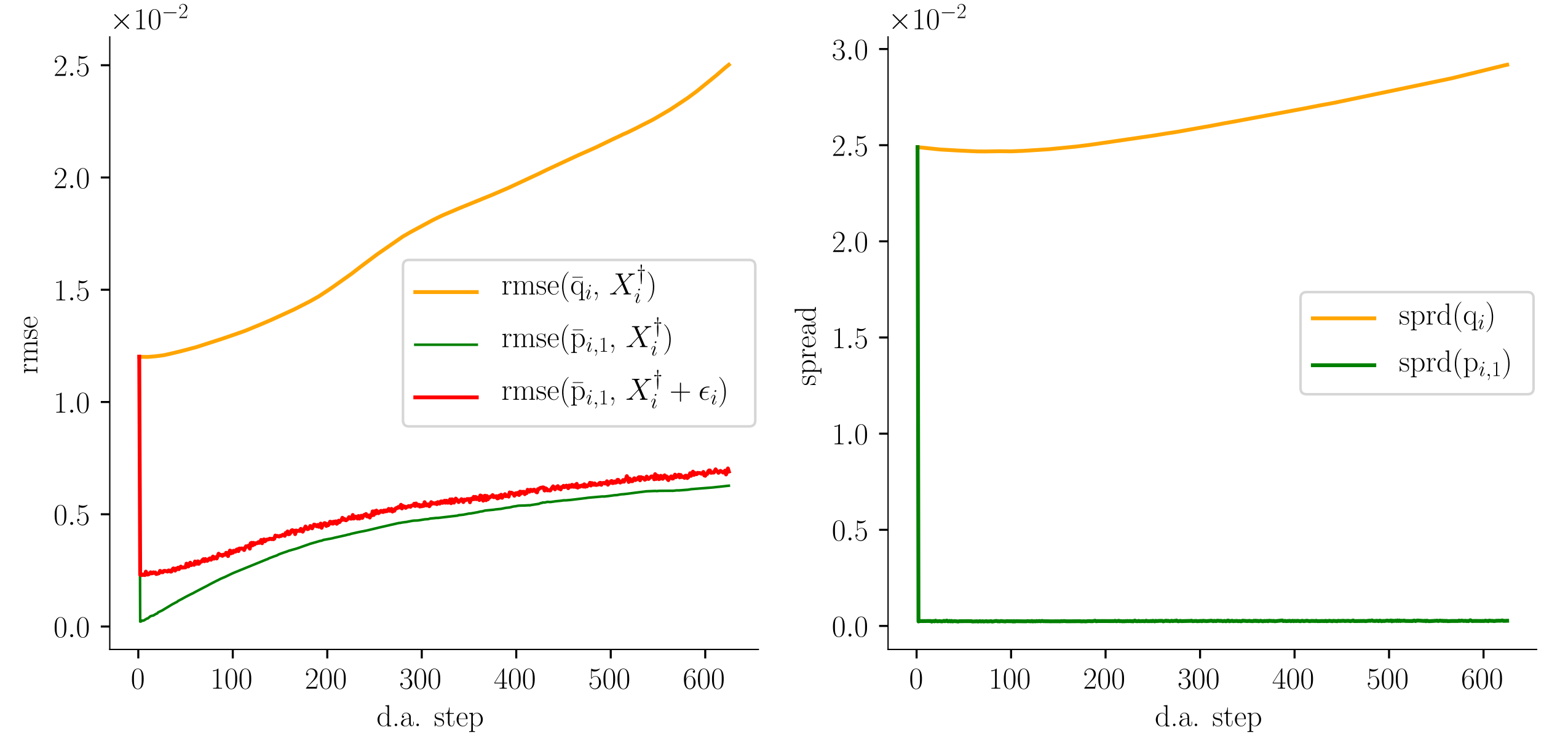

The left subplot in figure 5 shows comparisons of the rmse between the posterior ensemble mean and the true state (in blue)

the rmse between the one step forecast ensemble mean and the true state (in green)

the rmse between the prior ensemble mean and the true state (in orange)

and lastly the rmse between the one step forecast ensemble mean and the true state plus observation noise (in red)

In figure 6, the rmse subplot shows comparisons of (in green), (in orange) and (in red).

In both rmse subplots of figure 5 and figure 6, the rmse between the one step forecast ensemble mean and the true state plus observation noise (in red) is stable. It is (roughly) a few times larger than the rmse between the one step forecast ensemble mean and the truth without observation noise (in green). This suggests that the size of the observation noise is dominating. Because of this, we treat the positive trend in (in blue) and in (in green) as minimal – the positive trend is within the “accuracy tolerance” measured by the likelihood function. Thus is sufficiently stable. This is further supported by a comparison with the increase in the rmse between the prior ensemble mean and the truth (in orange). Therefore, the data we assimilated, albeit low dimensional relative to the SPDE degree of freedom, gives sufficient information to be able to offer a reasonably accurate approximation of the signal.

Another feature to note in the rmse subplots in figure 5 is, the rmse between the one step forecast ensemble mean and the truth (in green) is slightly larger than the rmse between the posterior ensemble mean and the truth (in blue). This feature is due to the resampling step at each assimilation time. The same reason applies to the differences between the ensemble spreads of the posterior (in blue) and one step forecast (in green), shown in the right subplot in figures 5 and 6. One can also see that the posterior ensemble spreads are reasonably stable. However, in the absence of data assimilation corrections, for the prior distribution (in orange) we see a continuous increase in both the rmse and spread.

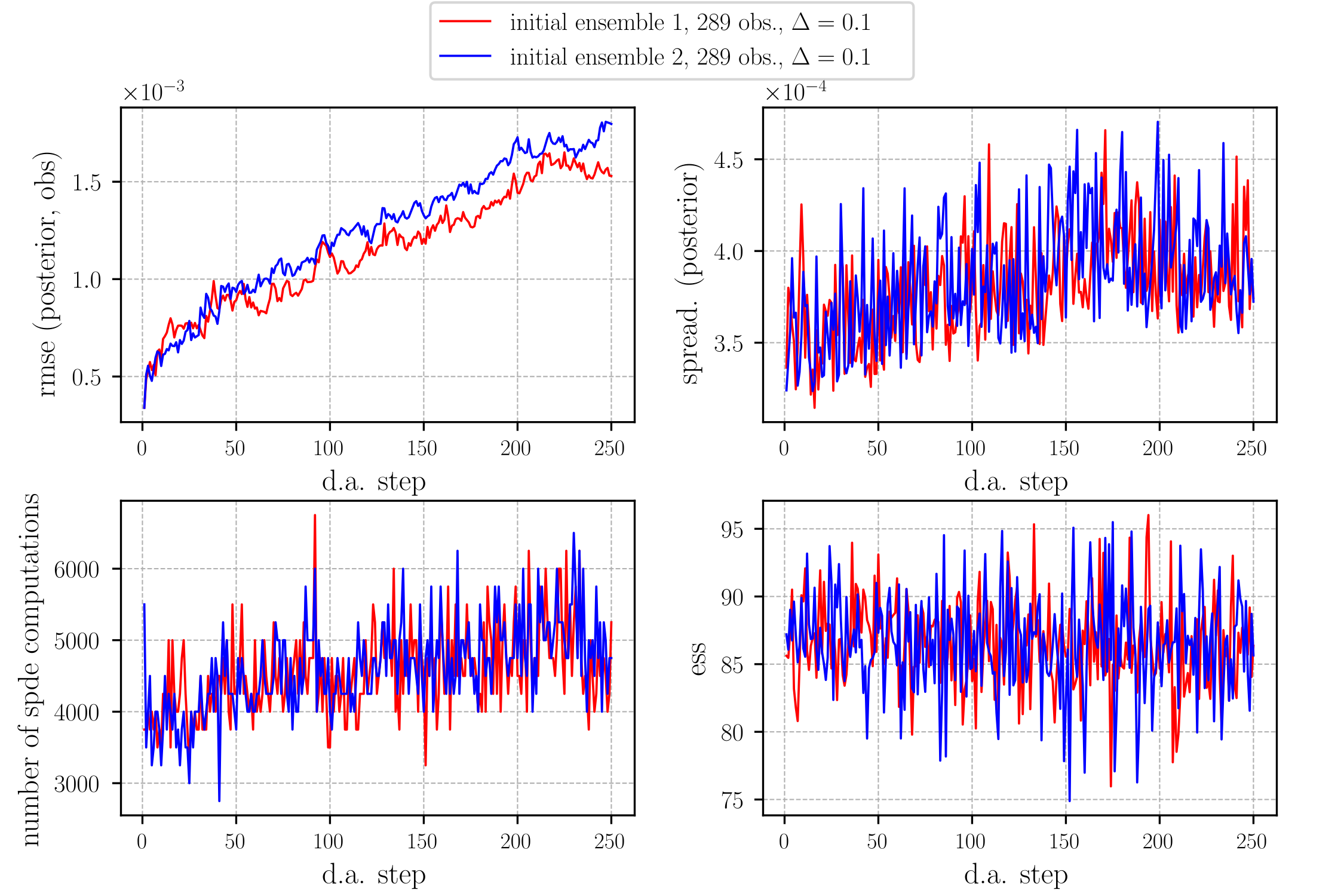

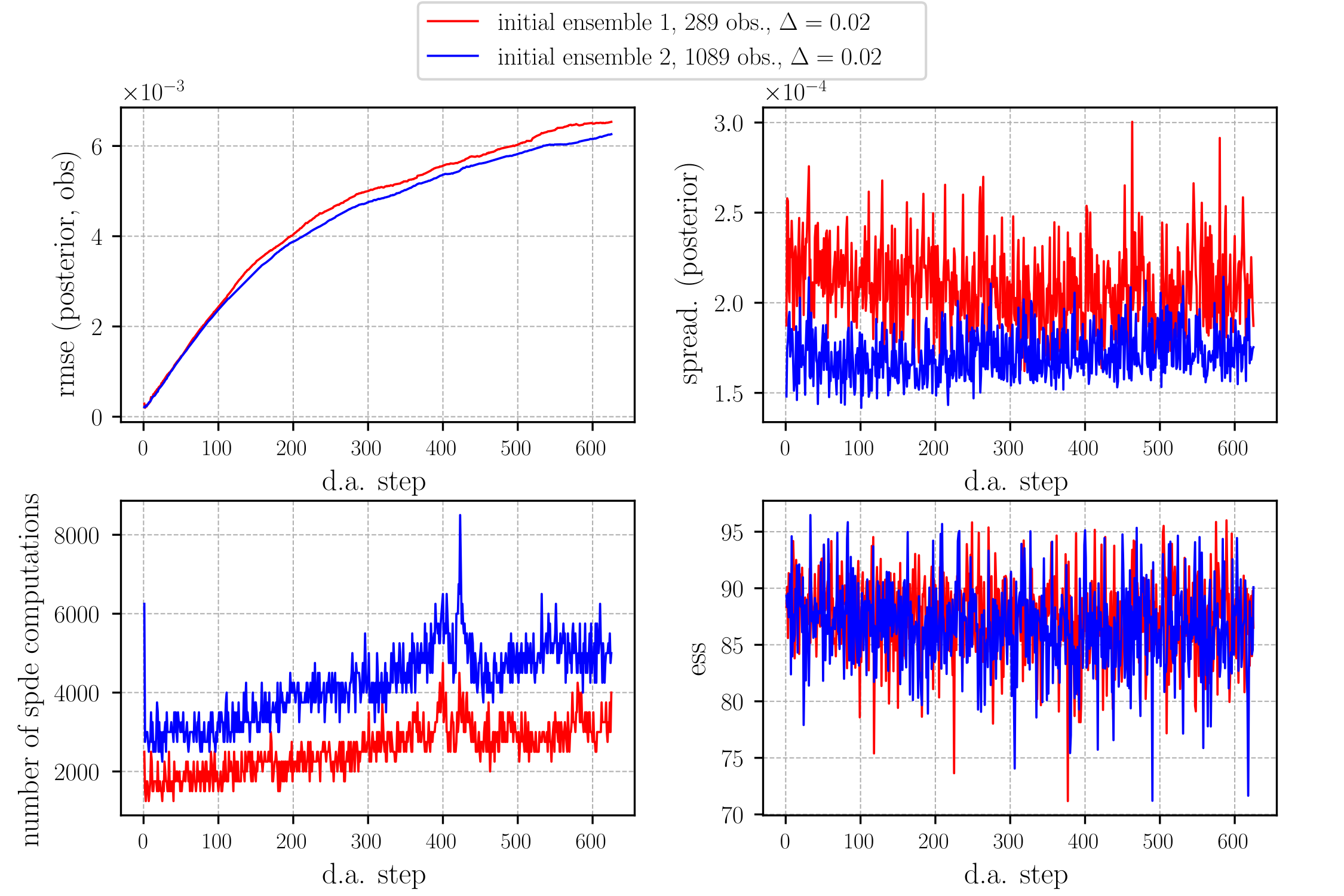

Figure 7 compares the effect of the two initial ensembles on the experiments. In the figure, the four subplots compare , , number of SPDE computations and ess. The two different experiments produced very close results.

As shown in table 1, the two initial ensembles produce very different initial rmse and ensemble spread. The rmse values of initial ensemble 1’s ensemble mean are two orders of magnitude smaller than initial ensemble 2’s rmse values. The ensemble spread of initial ensemble 1 is also one order of magnitude smaller than the ensemble spread of initial ensemble 2. Despite these relatively large initial differences, after one data assimilation step is completed, the spread and rmse of the corresponding ensembles become comparable. The reason is that all unlikely particles are immediately eliminated whilst the diversity of the ensemble is kept high through the tempering procedure. This is also visualised in figure 6, indicated by the initial sharp decrease in the one step forecast rmse, , and one step forecast ensemble spread, (both plotted in green).

The bottom left subfigure of figure 7 shows the amount of computation taken at each assimilation time, measured in terms of the number of SPDE evaluations. The values used to obtain these plots can be accurately estimated from the number of tempering steps. For each tempering step, we have to solve SPDEs (number of ensemble members), followed by a fixed number of jittering steps (we use a fixed value of jittering steps, see step 4 of algorithm 3) for each duplicate resampled ensemble member. We assume a duplicate rate of 888The duplicate rate is more or less the average number of duplicates per assimilation step from our numerical experiments.. Thus the computational cost in terms of number of SPDE evaluations can be estimated by

Finally, the ess value in figure 7 shows that the tempering procedure is successful in keeping the ess values near the chosen threshold of .

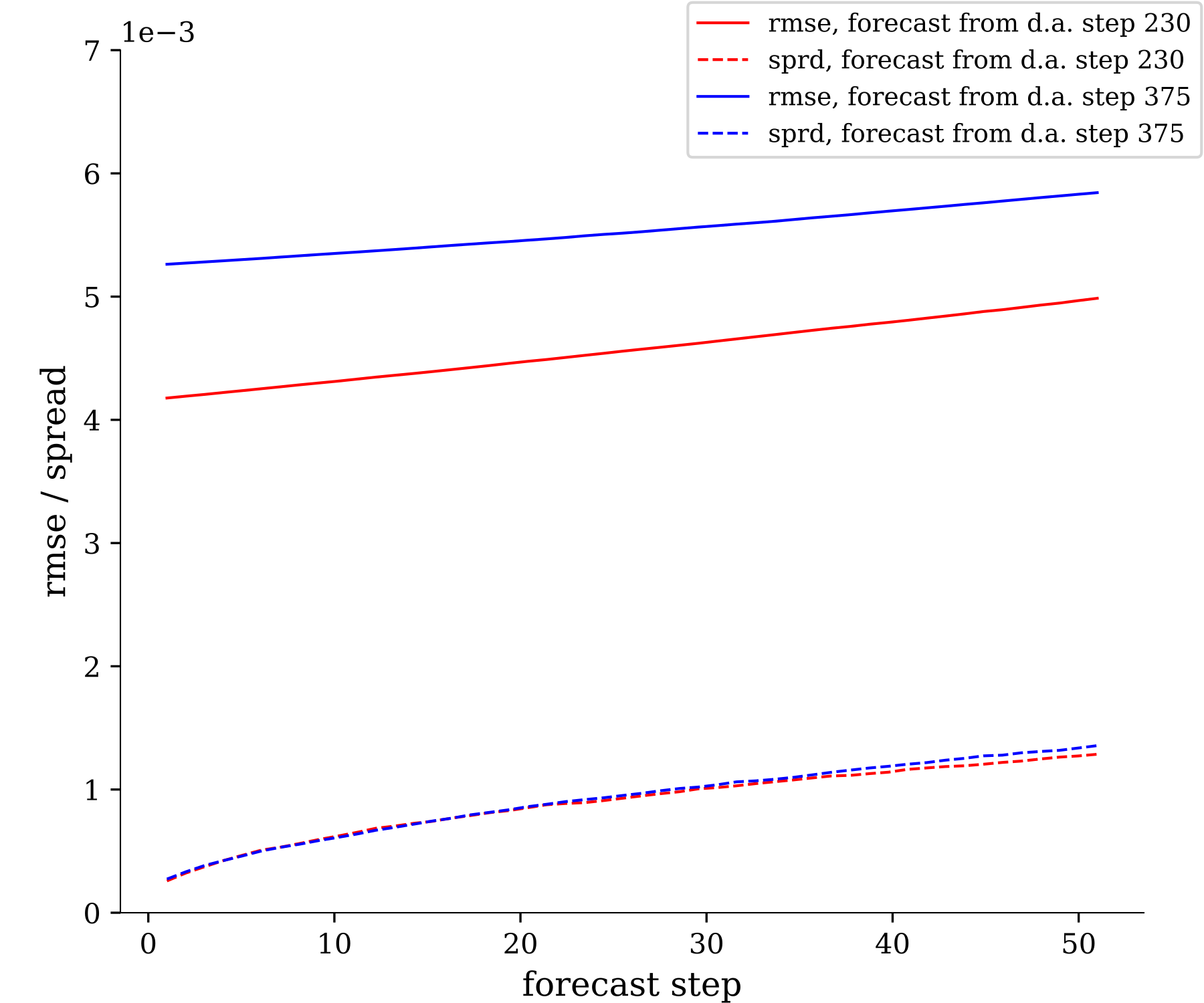

The uncertainty quantification results in Cotter et al. (2019) focused on the prior ensemble. In figure 8, we compare forecast rmse with forecast ensemble spread, i.e.

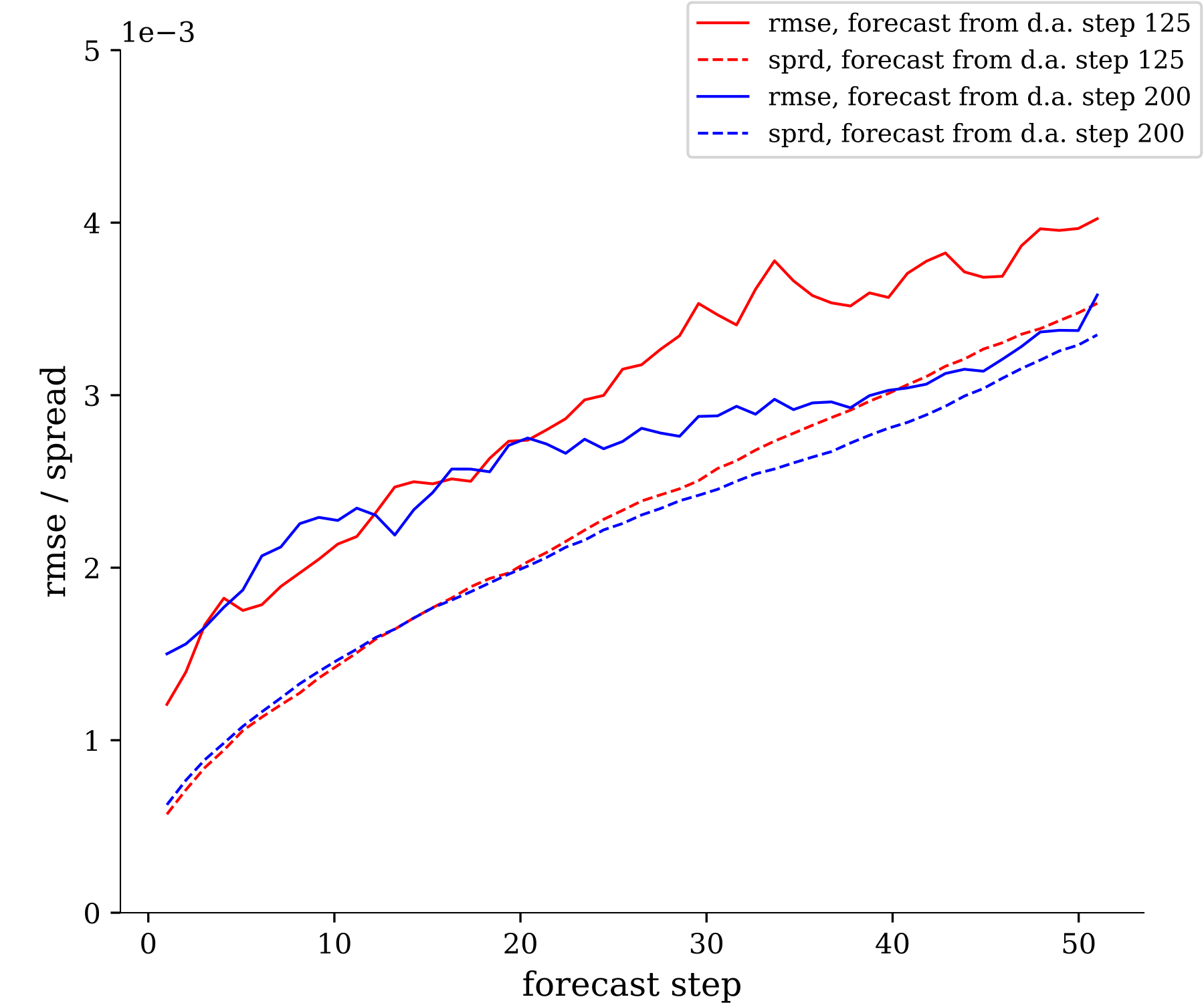

taking . The plots show that the forecast rmse and forecast ensemble spread are comparable. Further, the difference between corresponding rmse and spread, whether starting with or , are more or less equal. Both features indicate the filter is keeping track of the signal. Otherwise it is unlikely that the difference between forecast rmse and forecast spread is maintained starting from different posterior distributions. Note that there are 75 assimilation steps between and , which amounts to ett.

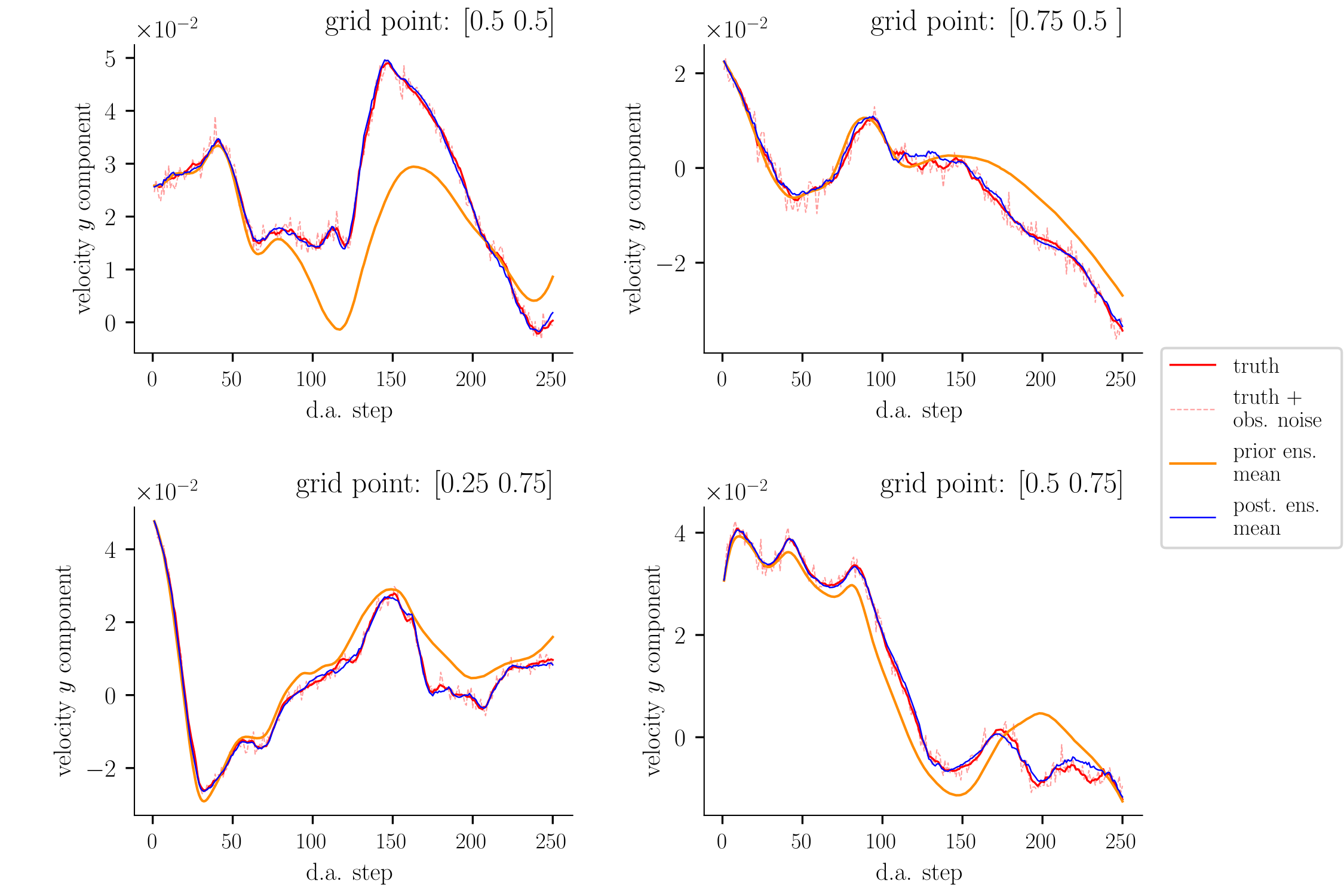

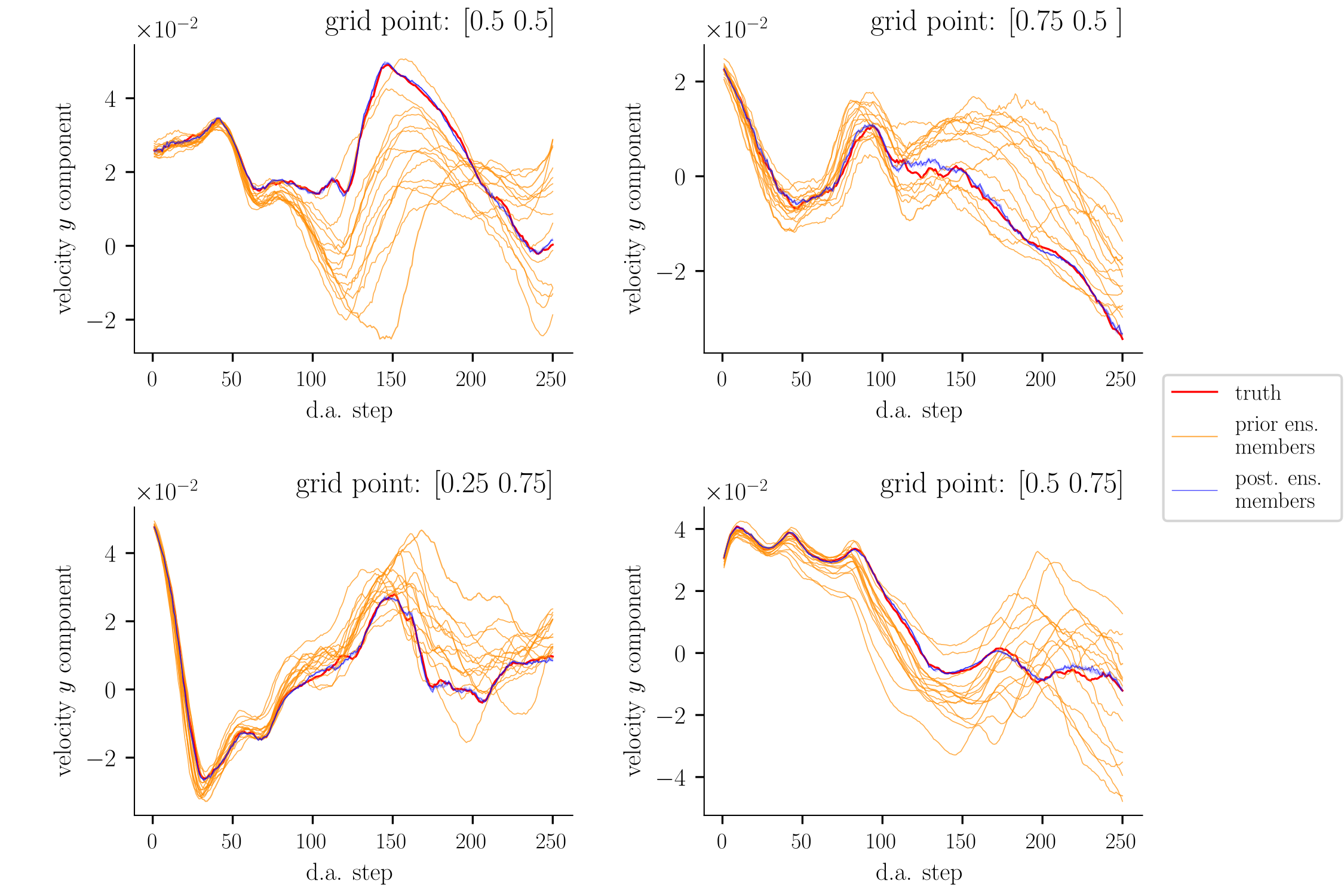

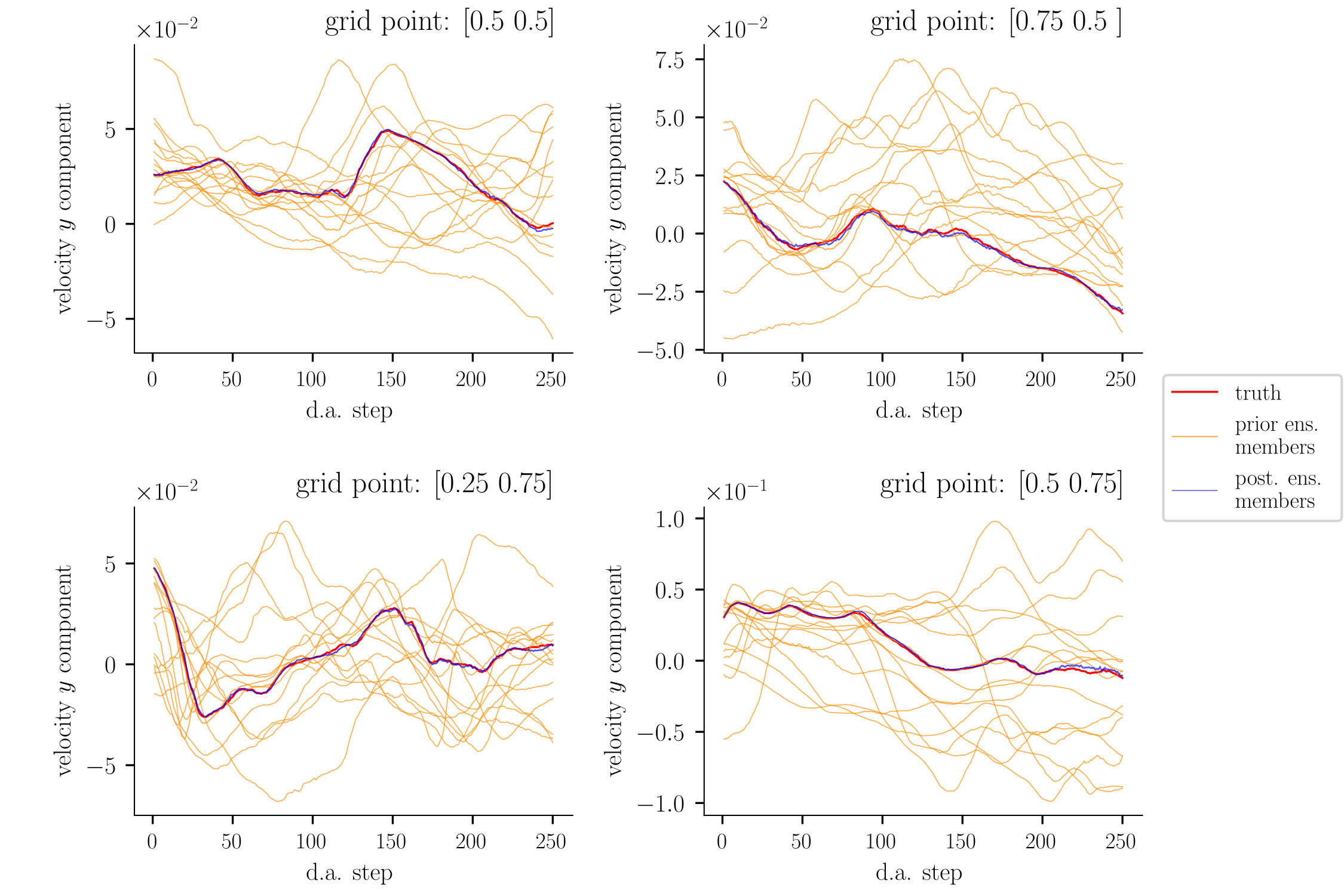

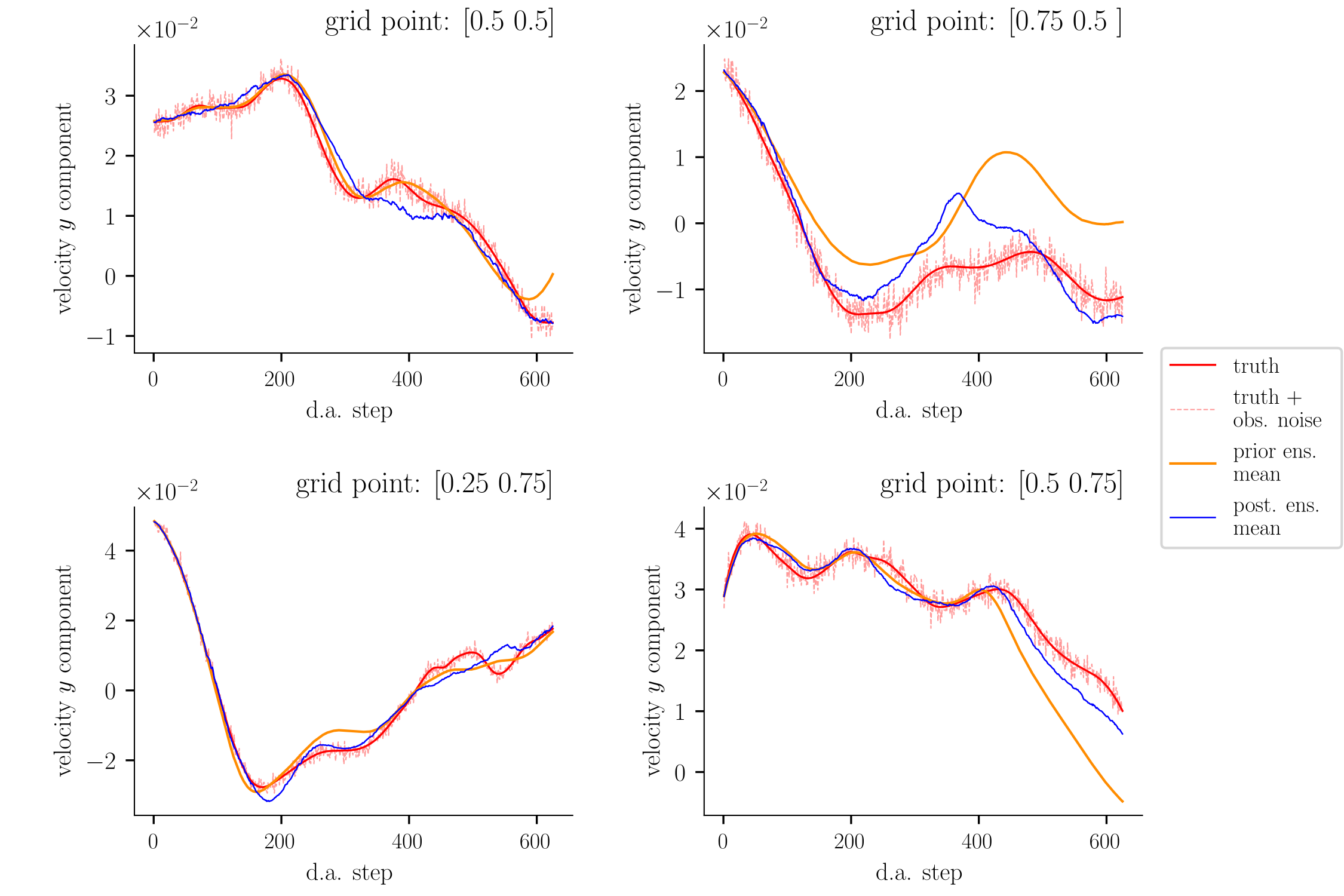

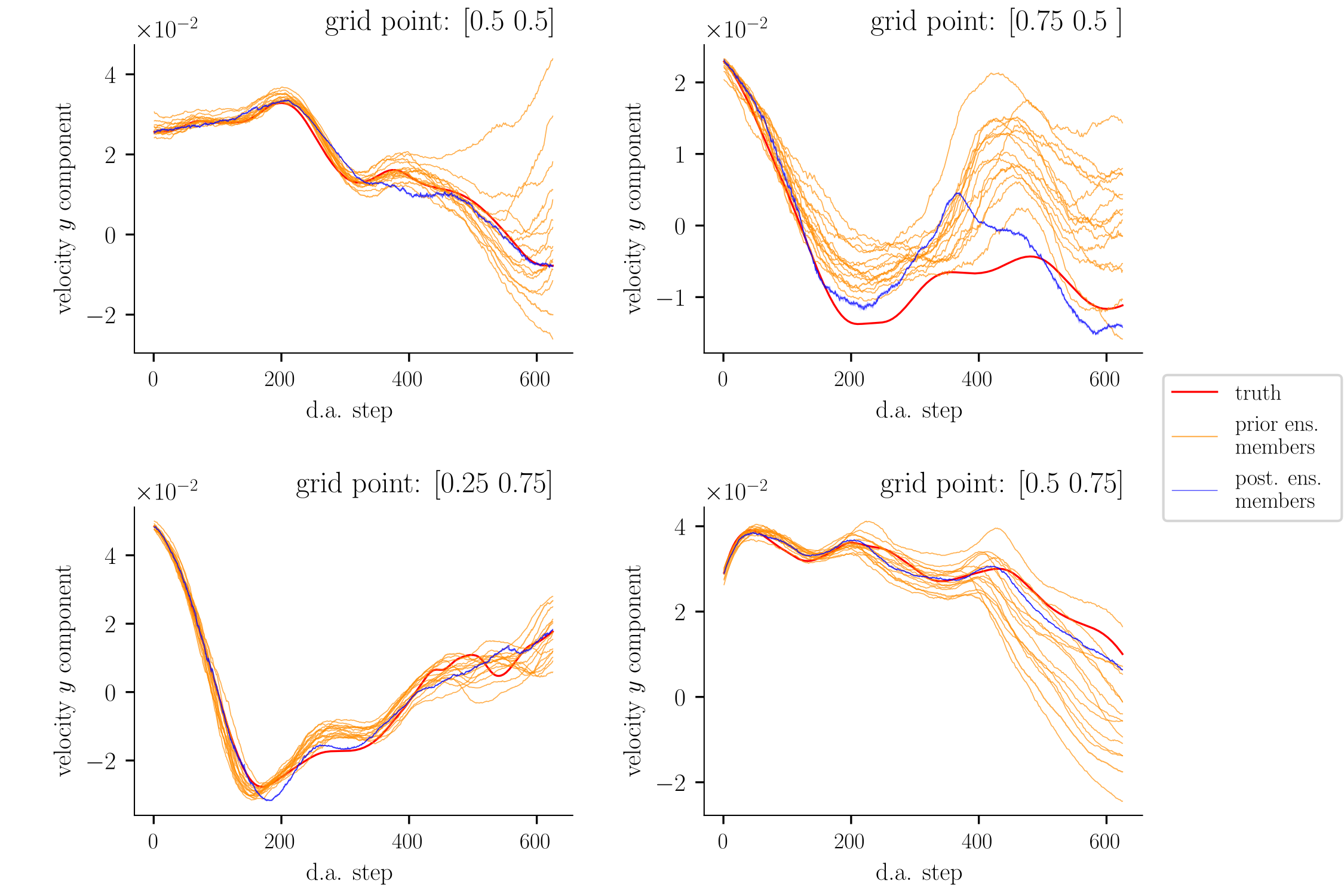

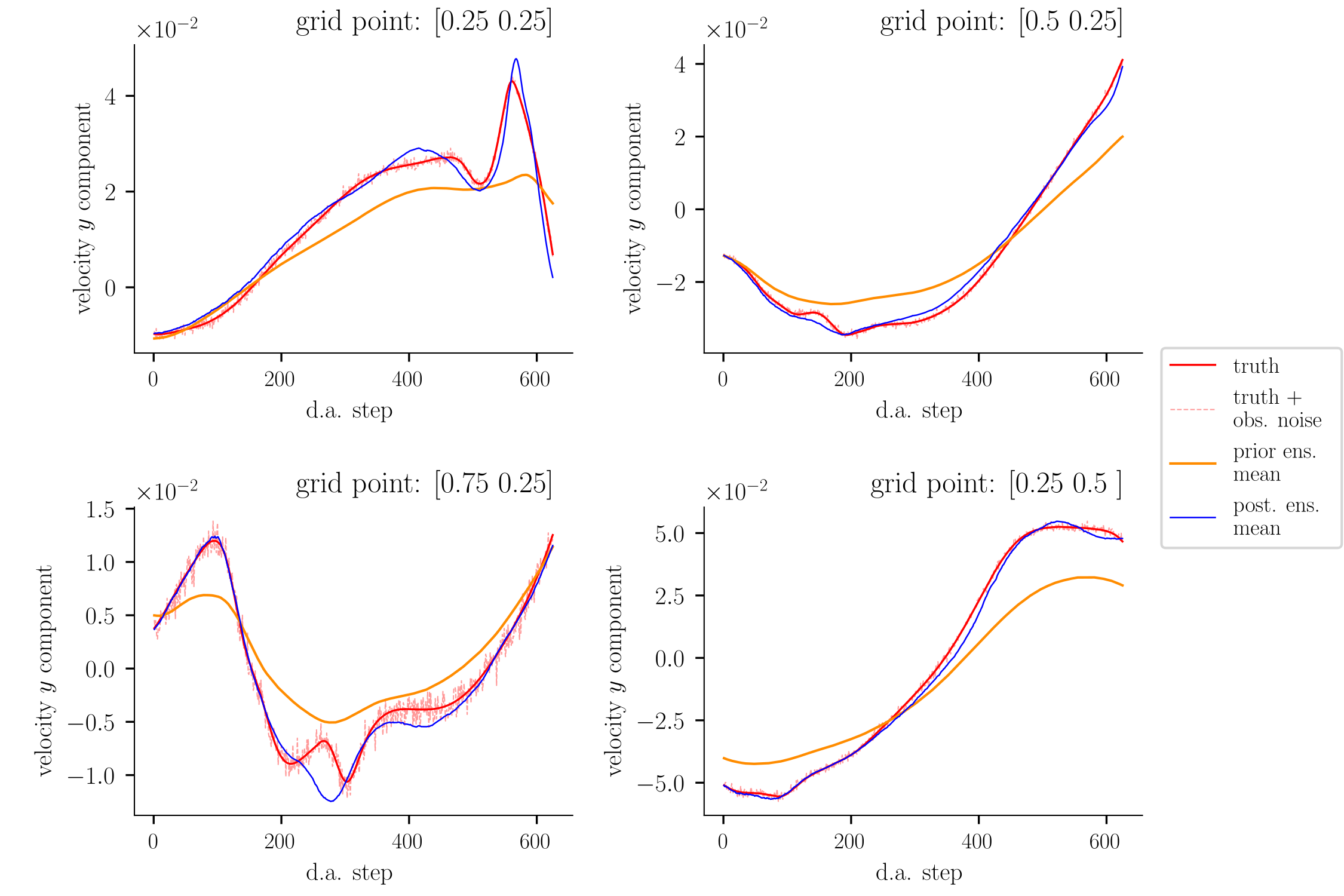

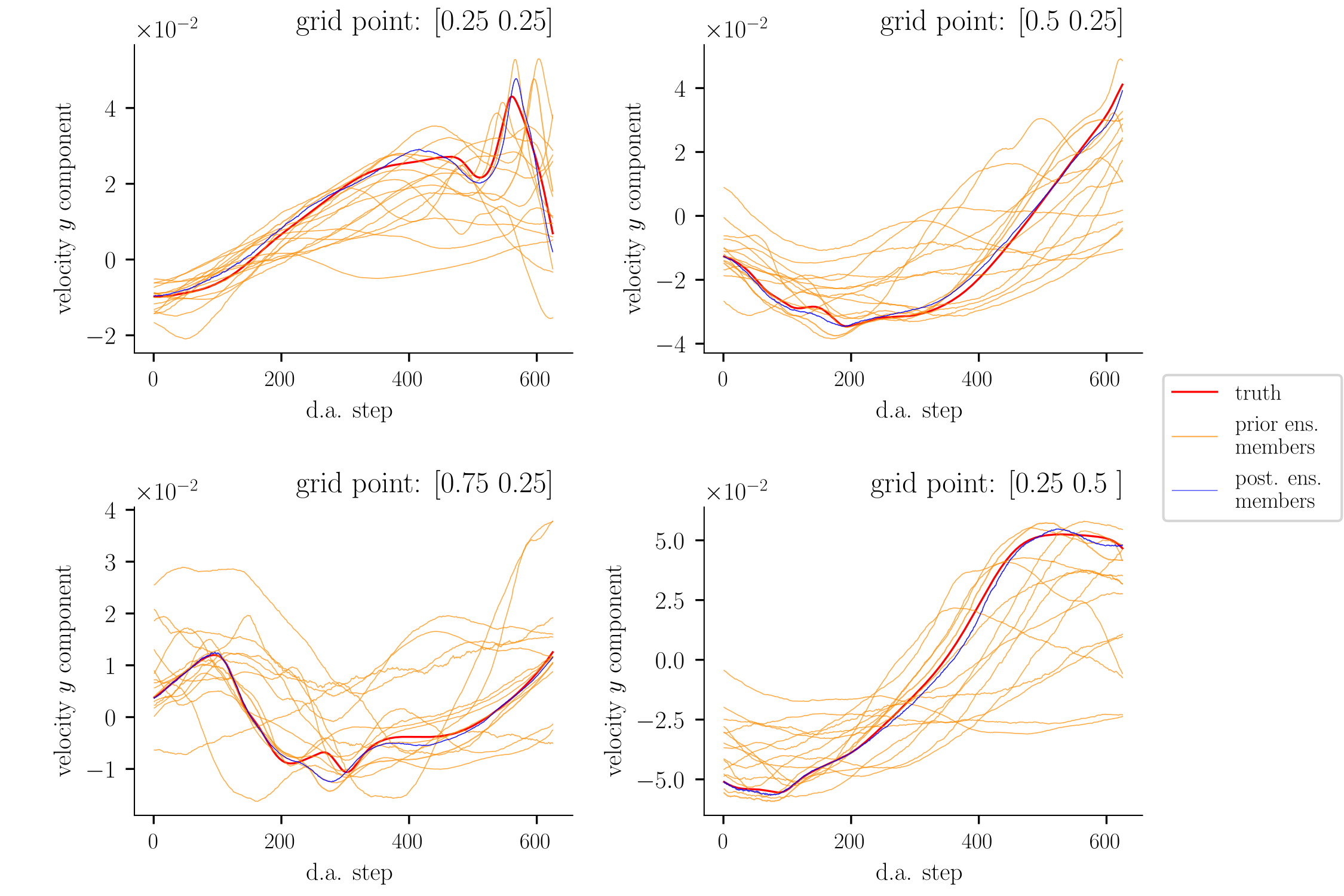

In figures 9 and 10 we show the Eulerian trajectories of the velocity y-component at four spatial locations. Figure 9 corresponds to the experiment using initial ensemble 1. Figure 10 corresponds to the experiment using initial ensemble 2. In each figure, the two subfigures correspond to the same experiment at the same grid locations.

In the subfigures 9(a) and 10(a), we plot the true state (in red), the true state plus observation noise (in dashed pink), the posterior ensemble mean (in blue) and the prior ensemble mean (in orange). Since initial ensemble 1 start very close to the initial truth, we see in subfigure 9(a) that the prior ensemble mean’s initial deviation from the truth is small. But the deviation become much more pronounced after assimilation step 100 at grid location . The posterior ensemble mean (in blue) stays close to the observed truth (in pink) at all four grid locations. In subfigure 9(b), trajectory of individual ensemble members are plotted. It shows how the prior ensemble spread increases as time goes on, but the posterior ensemble spread seems stable. This supports the features shown in figures 7, 5 and 6. In this scenario though, because there is no model error, we see in subfigure 9(b) that the truth does not deviate from the spread of the prior ensemble. The assimilated data allowed the posterior ensemble to offer a reasonably accurate approximation of the truth, whilst reducing the approximation uncertainty.

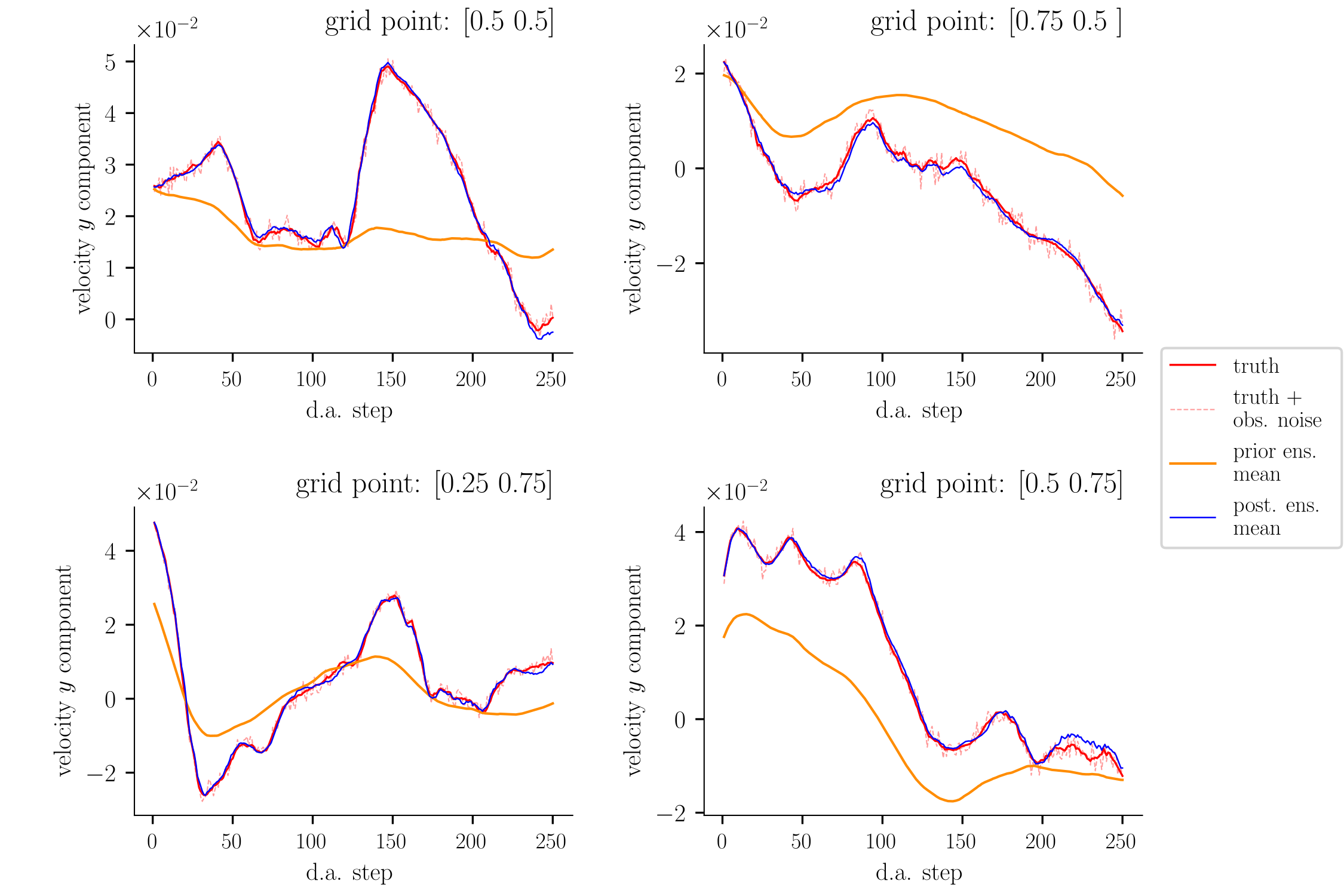

Initial ensemble 2 start alot farther from the initial truth compared to initial ensemble 1. In subfigures 10(a) and 10(b), we see that the prior ensemble mean deviates from the truth more greatly than shown in subfigures 9(a) and 9(b). This is further evidence to support the observation that the filtering algorithm was able to eliminate the unlikely particle positions whilst maintaining ensemble diversity, to reasonably approximate the truth.

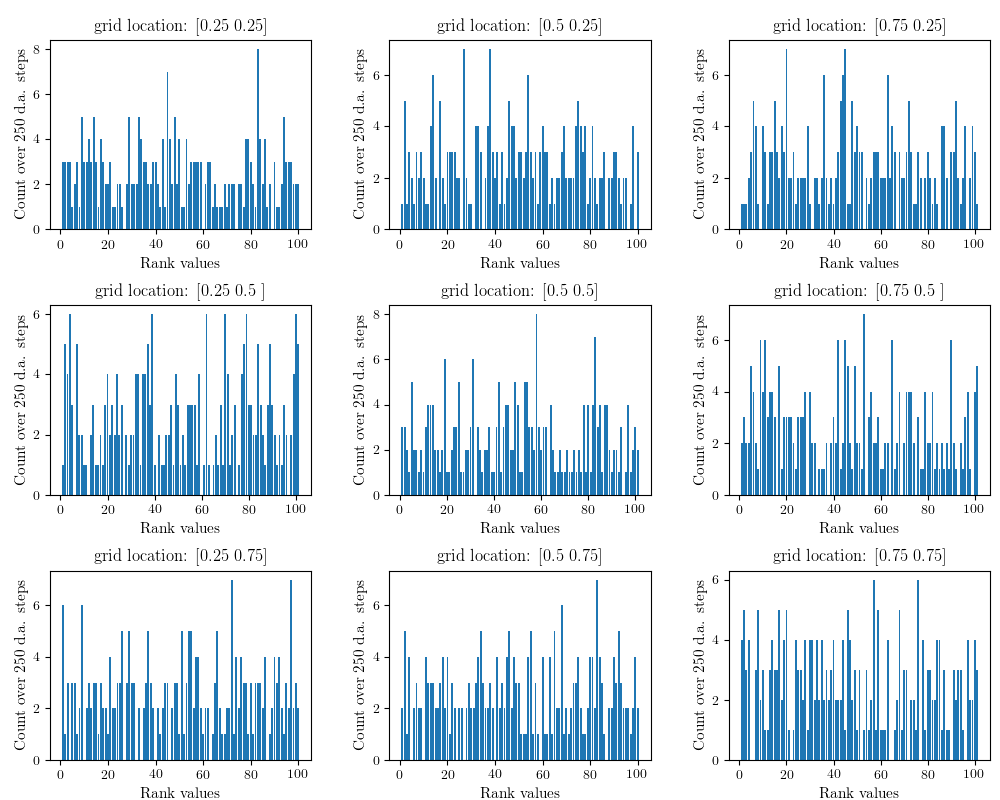

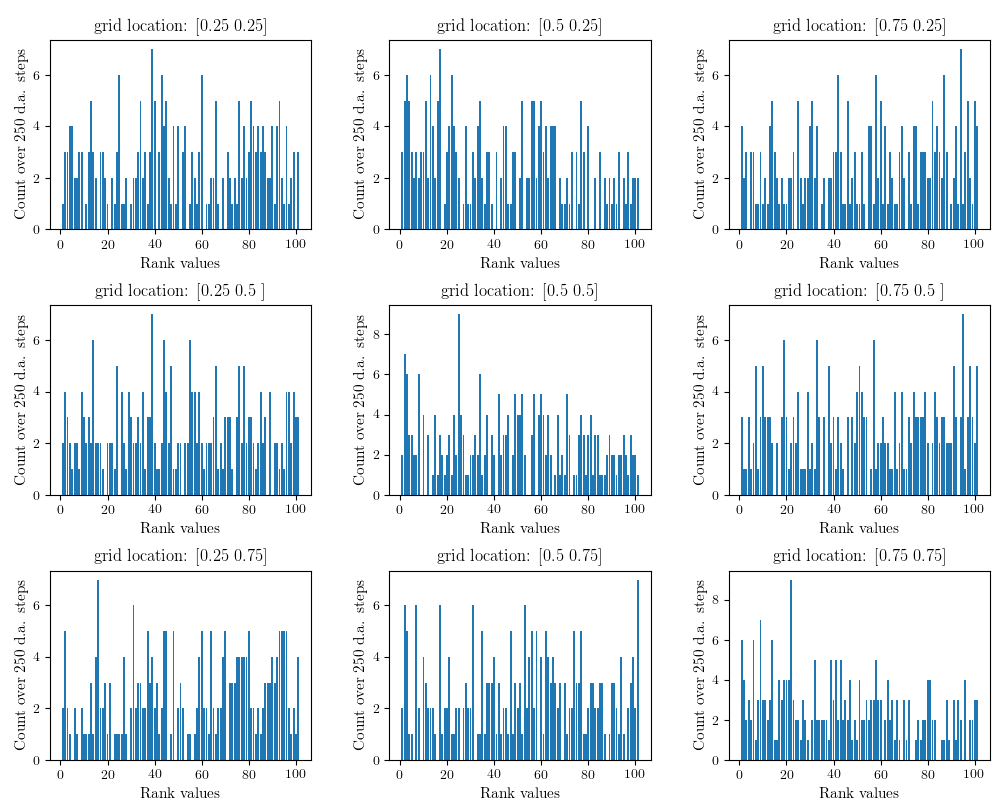

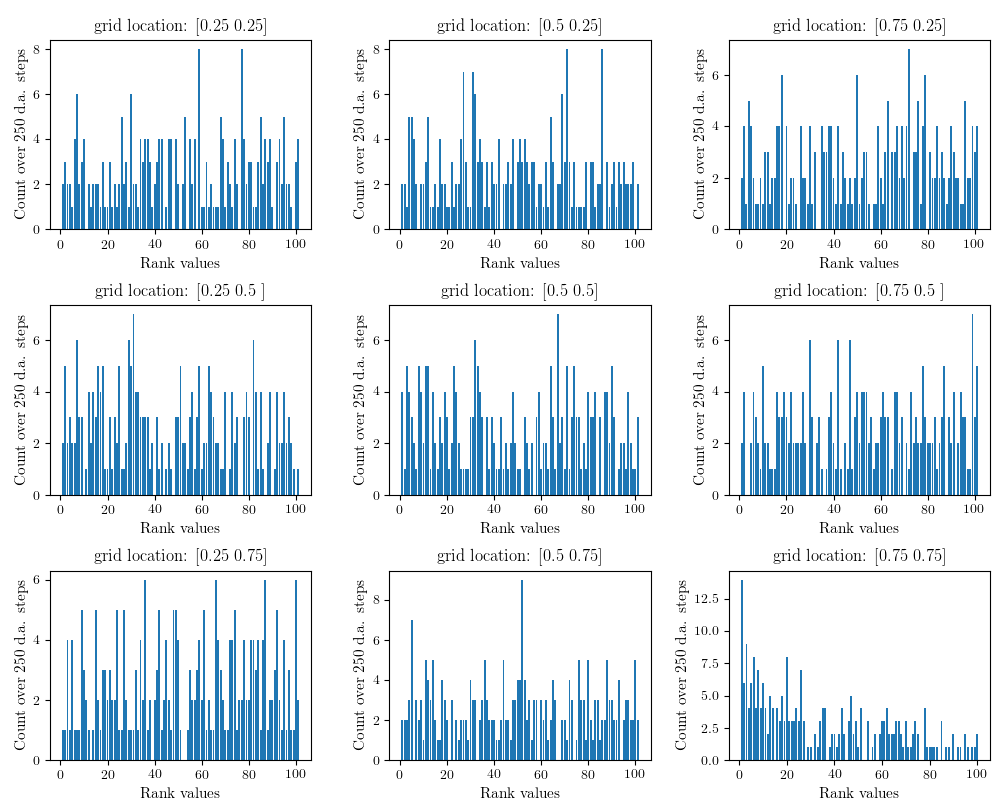

Lastly, in figures 11 and 12 we show rank histogram plots of the Eulerian velocity x-component, at nine grid locations. Figure 11 corresponds to the experiment using initial ensemble 1, observations, assimilation period ett and observation noise scaling . The plots do not show features of strong bias, under-dispersion or over-dispersion over the experiment period of ett. Figure 12 corresponds to the same repeated experiment but using a fewer number of weather stations ( observations). We observe that, assimilating less data leads to more pronounced features of skew, e.g. at grid locations , and .

4.3 Imperfect model scenario

The coarse grained fine resolution PDE solution is used as the true state in this experiment scenario, see remark 5. As explained in earlier sections, the calibrated SPDE is a result of model reduction applied to the fine resolution PDE. Given the adequate results shown in section 4.2, this scenario tests the feasibility of combining model reduction with the filtering algorithm.

We ran two different experiments independently of each other, for a total experiment time of ett:

-

1.

time interval between assimilations ett (every coarse time step), observation error scaling , initial ensemble set 1, number of weather stations ;

-

2.

time interval between assimilations ett, observation error scaling , initial ensemble set 2, number of weather stations .

For both, the assimilation interval choice amounts to a total of data assimilation steps.

It is to be expected that the results would not be comparable to those from the previous subsection. In this scenario the truth is from a different dynamical system (PDE) to the signal process (SPDE), see the discussion around (18). Additional sources of error are thus introduced into the particle filter algorithm, see Clark and Crisan (2005). Further, using weather stations amounts to observing of the truth state space in this scenario. This percentage is improved to when using weather stations in the experiment using initial ensemble 2. In either case, we have two orders of magnitude less information about the truth state than the experiments in section 4.2.

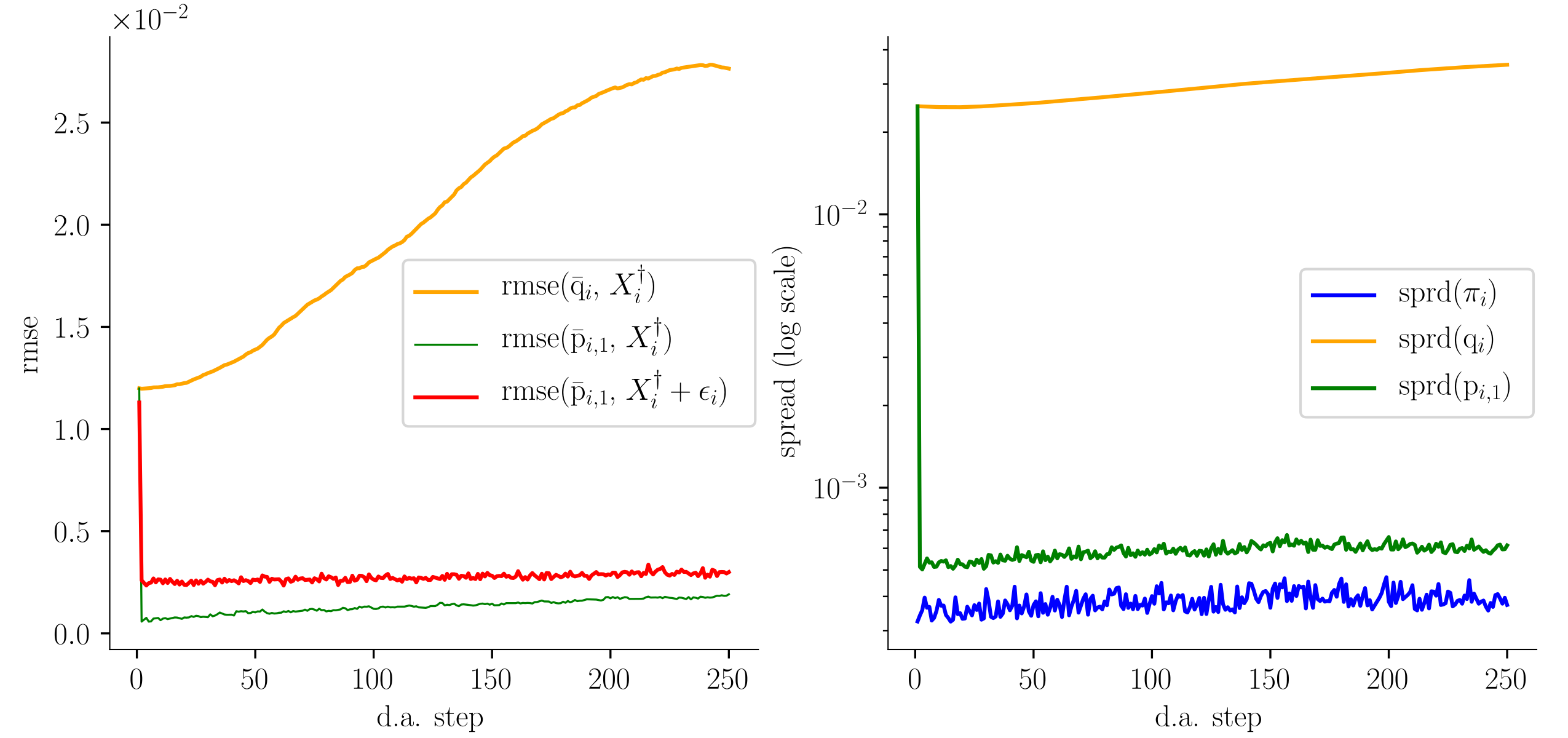

Figure 13 corresponds to the experiment using initial ensemble 1 and observations. Figure 14 corresponds to the experiment using initial ensemble 2 and observations. The left subplots in figures 13 and 14 show comparisons of the rmse between the one step forecast ensemble mean and the true state (in green)

the rmse between the prior ensemble mean and the true state (in orange)

and lastly the rmse between the one step forecast ensemble mean and the true state plus observation noise (in red)

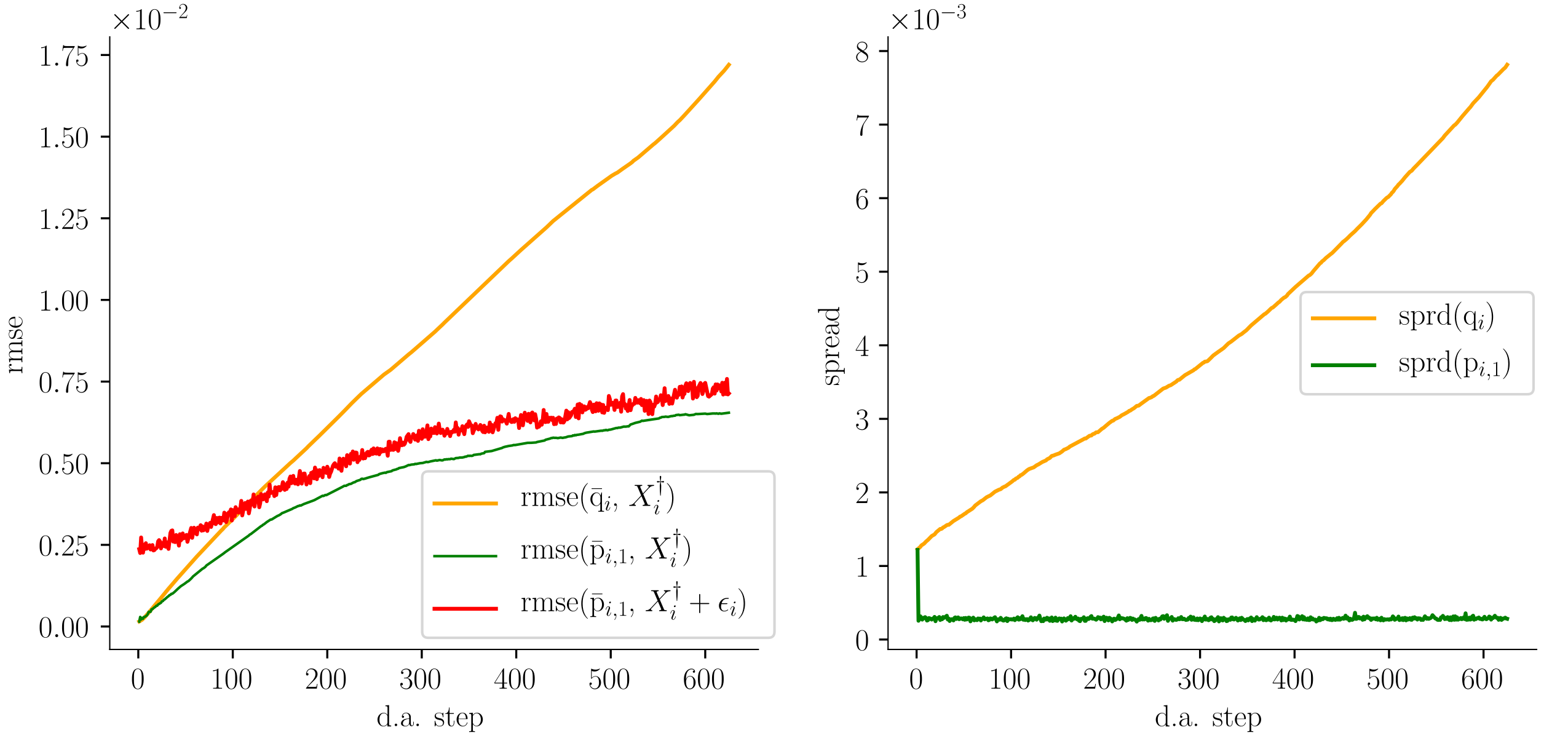

In both rmse subplots in figures 13 and 14, (in red) is not stable but show increasing trends. Thus the size of the observation noise is not the dominating factor (unlike in the perfect model scenario). The reason is most likely due to the difference between the SPDE and the PDE solution submanifolds. Better calibration, and additional data assimilation techniques such as nudging maybe help to improve this, see Cotter et al. (2020). In figure 13, the increase in at assimilation step is about times its initial value. In figure 14, the increase in at assimilation step is no more than times its value after the first assimilation (after the jump). The rmse values are of order , therefore are comparable to those shown in the perfect model scenario.

In both figures, increasing trends are also observed for the rmse between the one step forecast ensemble mean and the truth without observation noise (in green). We note that the green rmse values are all of order and therefore remain comparable to those shown in the perfect model scenario.

Comparing the evolution of the rmse of the forecast ensemble (in green) with that of the rmse of the prior ensemble (in orange), we see the former has considerably smaller increase. Taking this into account as well as the order of the rmse values, the data we assimilated, albeit very low dimensional relative to the PDE degree of freedom, still provides sufficient information to control the posterior ensemble. Therefore we judge that the posterior ensemble mean offers a reasonably accurate approximation of the signal.

In the ensemble spread subplots in figures 13 and 14, we see that due to the resampling step at each assimilation time, there is a small difference between the ensemble spreads of the posterior (in blue) and the one step forecast (in green). One can also see that the posterior ensemble spreads are reasonably stable. However, in the absence of data assimilation corrections, for the prior distribution (in orange) we see a continuous increase in both the rmse and spread.

Figure 15 compares the experiment which used initial ensemble 1 and observations, with the experiment which used initial ensemble 2 and observations. In the figure, the four subplots compare , , number of SPDE computations and ess.

As shown in table 1, the two initial ensembles produce very different initial rmse and ensemble spread. The rmse values of initial ensemble 1’s ensemble mean are two orders of magnitude smaller than initial ensemble 2’s rmse values. The ensemble spread of initial ensemble 1 is also one order of magnitude smaller than the ensemble spread of initial ensemble 2. Despite these relatively large initial differences, after one data assimilation step is completed, the rmse of the corresponding ensembles become comparable. The reason is that all unlikely particles are immediately eliminated whilst the diversity of the ensemble is kept high through the tempering procedure. This is also visualised in figure 14, indicated by the initial sharp decrease in the one step forecast rmse, , and one step forecast ensemble spread, (both plotted in green).

From the rmse subplot in figure 15 one can also see that, overall, the blue rmse plot show slight improvement on the red rmse plot. This is most likely because more data were assimilated. The dimension of the assimilated data also impacts the ensemble spread and computational cost. We see from the ensemble spread subplot in figure 15 that, increasing the observed data dimension led to smaller posterior ensemble spread.

The computational cost shown in the bottom left subfigure of figure 15 was computed in the same way as in section 4.2. We see that, increasing the observed data dimension from to , led to around – times computational increase. It is also interesting to note that the computation cost show an increasing trend. This perhaps reflects the increase in the rmse of the posterior ensemble.

Finally, the ess value in figure 15 shows that the tempering procedure is successful in keeping the ess values near the chosen threshold of .

In figure 16, we compare forecast rmse with forecast ensemble spread, i.e.

taking . Note that there are 145 assimilation steps between and , which amounts to ett. In this scenario, the plots show that the forecast rmse and forecast ensemble spread are less comparable (rmse seem to be about 5 times larger than the spread), than in the perfect model scenario, but the quantities remain the same order . Further, the difference between corresponding rmse and spread is not quite maintained – the distance between the blue solid line and blue dashed line, is a little larger than the distance between the red solid line and the red dashed line. These features reflect the evolution of the forecast ensemble rmse and spread, shown in figures 13 and 14, as well as the evolution of the posterior ensemble rmse and spread show in figure 15.

In figures 17 and 18 we show the Eulerian trajectories of the velocity y-component at four spatial locations. Figure 17 corresponds to the experiment using initial ensemble 1 and observations. Figure 18 corresponds to the experiment using initial ensemble 2 and observations. In each figure, the two subfigures correspond to the same experiment at the same grid locations.