Technical Report: Partial Dependence through Stratification

Abstract

Partial dependence curves (FPD) introduced by Friedman (2000), are an important model interpretation tool, but are often not accessible to business analysts and scientists who typically lack the skills to choose, tune, and assess machine learning models. It is also common for the same partial dependence algorithm on the same data to give meaningfully different curves for different models, which calls into question their precision. Expertise is required to distinguish between model artifacts and true relationships in the data.

In this paper, we contribute methods for computing partial dependence curves, for both numerical (StratPD) and categorical explanatory variables (CatStratPD), that work directly from training data rather than predictions of a model. Our methods provide a direct estimate of partial dependence, and rely on approximating the partial derivative of an unknown regression function without first fitting a model and then approximating its partial derivative. We investigate settings where contemporary partial dependence methods—including FPD, ALE, and SHAP methods—give biased results. Furthermore, we demonstrate that our approach works correctly on synthetic and plausibly on real data sets. Our goal is not to argue that model-based techniques are not useful. Rather, we hope to open a new line of inquiry into nonparametric partial dependence.

1 Introduction

Partial dependence, the isolated effect of a specific variable or variables on the response variable, , is important to researchers and practitioners in many disparate fields such as medicine, business, and the social sciences. For example, in medicine, researchers are interested in the relationship between an individual’s demographics or clinical features and their susceptibility to illness. Business analysts at a car manufacturer might need to know how changes in their supply chain affect defect rates. Climate scientists are interested in how different atmospheric carbon levels affect temperature.

For an explanatory matrix, , with a single (column) variable, , a plot of the against visualizes the marginal effect of feature on exactly. Given two or more features, one can similarly plot the marginal effects of each feature separately, however, the analysis is complicated by the interactions of the variables. Variable interactions and codependencies between features result in marginal plots that do not isolate the specific contribution of a feature of interest to the response. For example, a marginal plot of sex (male/female) against body weight would likely show that, on average, men are heavier than women. While true, men are also taller than women on average, which likely accounts for most of the difference in average weight. It is unlikely that two “identical” people, differing only in sex, would be appreciably different in weight.

Rather than looking directly at the data, there are several partial dependence techniques that interrogate fitted models provided by the user: Friedman’s original partial dependence (Friedman, 2000) (which we will denote FPD), functional ANOVA (Hooker, 2007), Individual Conditional Expectations (ICE) (Goldstein et al., 2015), Accumulated Local Effects (ALE) (Apley and Zhu, 2016), and most recently SHAP (Lundberg and Lee, 2017). Model-based techniques dominate the partial dependence research literature because interpreting the output of a fitted model has several advantages. For example, models have a tendency to smooth over noise. Models act like analysis preprocessing steps, potentially reducing the computational burden on model-based partial dependence techniques; e.g., ALE is for the records of . Model-based techniques are typically model-agnostic, though for efficiency, some provide model-specific optimizations, as SHAP does. Partial dependence techniques that interrogate models also provide insight into the models themselves; i.e., how variables affect model behavior. It is also true that, in some cases, a predictive model is the primary goal so creating a suitable model is not an extra burden.

Model-based techniques do have two significant disadvantages, however. The first relates to their ability to tease apart the effect of codependent features because models are sometimes required to extrapolate into regions of nonexistent support or even into nonsensical observations; e.g., see discussions in Apley and Zhu (2016) and Hooker (2007). As we demonstrate in Section 4, using synthetic and real data sets, model-based techniques can vary in their ability to isolate variable effects in practice. Second, there are vast armies of business analysts and scientists at work that need to analyze data, in a manner akin to exploratory data analysis (EDA), that have no intention of creating a predictive model. Either they have no need, perhaps needing only partial dependence plots, or they lack the expertise to choose, tune, and assess models (or write software at all).

Even in the case where a machine learning practitioner is available to create a fitted model for the analyst, hazards exist. If a fitted model is unable to accurately capture the relationship between features and accurately, for whatever reason, then partial dependence does not provide any useful information to the user. To make interpretation more challenging, there is no definition of “accurate enough.” Also, given an accurate fitted model, business analysts and scientists are still peering at the data through the lens of the model, which can distort partial dependence curves. Separating visual artifacts of the model from real effects present in the data requires expertise in model behavior (and optimally in the implementation of model fitting algorithms).

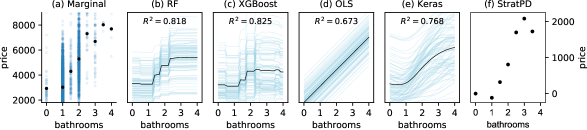

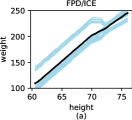

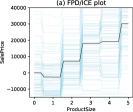

Consider the combined FPD/ICE plots shown in Figure 1 derived from several models (random forest, gradient boosting, linear regression, deep learning) fitted to the same New York City rent data set (Kaggle, 2017). The subplots in Figure 1(b)-(e) present starkly different partial dependence relationships and it is unclear which, if any, is correct. The marginal plot, (a), drawn directly from the data shows a roughly linear growth in price for a rise in the number of bathrooms, but this relationship is biased because of the dependence of bathrooms on other variables, such as the number of bedrooms. (e.g., five bathroom, one bedroom apartments are unlikely.) For real data sets with codependent features, the true relationship is unknown so it is hard to evaluate the correctness of the plots. (Humans are unreliable estimators, which is why we need data analysis algorithms in the first place.) Nonetheless, having the same algorithm, operating on the same data, give meaningfully different partial dependences is undesirable and makes one question their precision.

Experts are often able to quickly recognize model artifacts, such as the stairstep phenomenon in Figure 1(b) and (c) inherent to decision tree-based methods trying unsuccessfully to extrapolate. In this case, though, the stairstep is more accurate than the linear relationship in (d) and (e) because the number of bathrooms is discrete (except for “half baths”). The point is that interpreting model-based partial dependence plots can be misleading, even for experts.

An accurate mechanism to compute partial dependences that did not peer through fitted models would be most welcome. Such partial dependence curves would be accessible to users, like business analysts, who lack the expertise to create suitable models. (One can imagine a spreadsheet plug-in that produced partial dependence curves.) A mechanism that did not rely on a user-provided model would also reduce the chance of plot misinterpretation due to model artifacts and could even help machine learning practitioners to choose appropriate models based upon relationships exposed in the data.

In this paper, we propose a strategy, called stratified partial dependence (StratPD), that computes partial dependences directly from training data , rather than through the predictions of a fitted model, and that does not presume mutually-independent features. As an example, Figure 1(f) shows the partial dependence plot computed by StratPD. StratPD operates very much like a “model-free” ALE, at least for numerical variables. Our technique is also based upon the notion of an idealized partial dependence: integration over the partial derivative of with respect to the variable of interest for the smooth function that generated . As that function is unknown, we estimate the partial derivatives from the data non-parametrically. Colloquially, the approach examines changes in across while holding constant or nearly constant ( denotes all variables except ). To hold constant, we use a single decision tree to partition feature space, a concept used by Strobl et al. (2008) and Breiman and Cutler (2003) for conditional permutation importance and observation similarity measures, respectively. Our second contribution, CatStratPD, computes partial dependence curves for categorical variables that, unlike existing techniques, does not assume adjacent category levels are similar. Both StratPD and CatStratPD are quadratic in , in the worst case (like FPD), though StratPD behaves linearly on real data sets. Our prototype is currently limited to regression, isolates only single-variable partial dependence, and cannot identify interaction effects (as ICE can). The software is available via Python package stratx with source at github.com/parrt/stratx, including the code to regenerate images in this paper.

We begin by describing the proposed stratification approach in Section 2 then compare StratPD to related (model-based) work in Section 3. In Section 4, we present partial dependence curves generated by StratPD and CatStratPD on synthetic and real data sets, contrast the plots with those of existing methods, and use synthetic data to highlight possible bias in some model-based methods.

2 Partial dependence without model predictions

In special circumstances, we know the precise effect of each feature on response . Assume we are given training data pair () where is an matrix whose columns represent observed features and is the vector of responses. For any smooth function that precisely maps each row vector to response , , the partial derivative of with respect to gives the change in holding all other variables constant. Integrating the partial derivative then gives the idealized partial dependence of on , the isolated contribution of to :

Definition 1 The idealized partial dependence of on feature for continuous and smooth generator function evaluated at is the cumulative sum up to :

| (1) |

is the value contributed to by at and . The underlying generator function is unknown, and so other approaches begin by estimating with a fitted model, . Instead, we estimate the partial derivatives of the true function, , from the raw training data then integrate to obtain . We note that ALE also derives partial dependence by estimating and integrating across partial derivatives (e.g., see Equation 7 in Apley and Zhu 2016) but does so using local changes in predictions from rather than . The advantages of this definition are that it (i) does not require a fitted model or its predictions and (ii) is insensitive to codependent features.

The key idea is to stratify feature space into disjoint regions of observations where all variables are approximately matched across the observations in that region. Within each region, any fluctuations in the response variable are likely due to the variable of interest, . In the ideal case, the values for each variable within a region are identical and, because only is changing, changes should be attributed to , noise, or irreducible error. (More on this shortly.) Estimates of the partial derivative within a region are computed discretely as the changes in values between unique and ordered positions: for all in a region such that is unique and is the average at unique . This amounts to performing piecewise linear regression through the region observations, one model per unique pair of values, and collecting the model coefficients to estimate partial derivatives. The overall partial derivative at is the average of all slopes, found in any region, whose range spans . One could apply a nonparametric method to smooth through the discontinuities at points within a leaf, but this has not proven necessary in practice. The partial dependence curve points are often the result of two averaging operations, one within and one across regions, which tends to smooth the curve; e.g., see Figure 3(d) below.

Stratification occurs through the use of a decision tree fit to (, ), whose leaves aggregate observations with equal or similar features. The features can be numerical variables or label-encoded categorical variables (assigned a unique integer). StratPD only uses the tree for the purpose of partitioning feature space and never uses predictions from any model. See Algorithm 6 for more details.

For the stratification approach to work, decision tree leaves must satisfactorily stratify . If the observations in each region are not similar enough, the relationship between and is less accurate. Regions can also become so small that even the values become equal, leaving a single unique observation in a leaf. Without a change in , no partial derivative estimate is possible and these nonsupporting observations must be ignored (e.g., the two leftmost points in Figure 2(a)). A degenerate case occurs when identical or nearly identical and variables exist. Stratifying as part of would also match up values, leading to both exhibiting flat curves, as if the decision tree were trained on not (, ). Our experience is that using the collection of leaves from a random forest, which restricts the number of variables available during node splitting, prevents partitioning from relying too heavily on either or . Some leaves have observations that vary in or and partial derivatives can still be estimated.

StratPD uses a hyper parameter, min_samples_leaf, to control the minimum number of observations in each decision tree leaf. Generally speaking, smaller values lead to more confidence that fluctuations in are due solely to , but more observations per leaf prevent StratPD from missing nonlinearities and make it less susceptible to noise. As the leaf size grows, however, one risks introducing contributions from into the relationship between and . At the extreme, the decision tree would consist of a single leaf node containing all observations, leading to a marginal not partial dependence curve.

StratPD uses another hyper parameter called min_slopes_per_x to ignore any partial derivatives estimated with too few observations. Dropping uncertain partial derivatives greatly improves accuracy and stability. Partial dependences computed by integrating over local partial derivatives are highly sensitive to partial derivatives computed at the left edge of any ’s range because imprecision at the left edge affects the entire curve. This presents a problem when there are few samples with values at the extreme left (see, for example, the histogram of Figure 8(d)). Fortunately, sensible defaults for StratPD (10 observations and 5 slopes) work well in most cases and were used to generate all plots in this paper.

For categorical explanatory variables, CatStratPD uses the same stratification approach, but cannot apply regression of to non-ordinal, categorical . Instead, CatStratPD groups leaf observations by category and computes the average response per category in each leaf. Consider a single leaf and its -dimensional average response vector . Then choose a random reference category, refcat, and subtract that category’s average value from to get a vector of relative deltas between categories: = . The vectors from all leaves are then merged via averaging, weighted by the number of observations per category, to get the overall effect of each category on the response. The delta vectors for two leaves, and , can only be merged if there is at least one category in common. CatStratPD initializes a running average vector to an arbitrary starting leaf’s and then makes multiple passes over the remaining vectors, merging any vectors with a category in common with the running average vector. Observations associated with any remaining, unmerged leaves must be ignored. CatStratPD uses a single hyper parameter min_samples_leaf to control stratification. Both StratPD and CatStratPD have an optional hyper parameter called ntrials (default is 1) that averages the results from multiple bootstrapped samples, which can reduce variance.

Stratification of high-cardinality categorical variables tends to create small groups of category subsets, which complicates the averaging process across groups. (Such vectors are sparse and we use NaNs to represent missing values.) If both groups have the same reference category, merging is a simple matter of averaging the two delta vectors, where mean(z,NaN) = z. For delta vectors with different reference categories and at least one category in common, one vector is adjusted to use a randomly-selected reference category, , in common: . That equation adjusts vector so then adds the corresponding value from so , which renders the average of and meaningful. See Algorithm 6 for more details.

StratPD and CatStratPD both have theoretical worst-case time complexity of for observations. For StratPD, stratification costs , computing deltas for all observations among the leaves has linear cost, and averaging slopes across unique ranges is on the order of or when all are unique in the worst case. StratPD is, thus, in the worst case. CatStratPD also stratifies in and computes category deltas linearly in but must make multiple passes over the leaves to average all possible leaf category delta vectors. In practice, three passes is the max we have seen (for high-cardinality variables), so we can assume the number of passes is some small constant to get a tighter bound. Averaging two vectors costs , so each pass requires . The number of leaves is roughly and, worst-case, , meaning that merging dominates CatStratPD complexity leading to . Experiments show that our prototype is fast enough for practical use (see Section 4).

3 Related work

The mechanisms most closely related to StratPD and CatStratPD are FPD, ICE, SHAP, and ALE, which all define partial dependence in terms of impact on estimated models, , rather than the unknown true function . Let be the subset of features of interest where . Friedman (2000) defines the partial dependence as an expectation conditioned on the remaining variables:

| (2) |

where the expectation can be estimated by . The Individual Conditional Expectation (ICE) plot (Goldstein et al., 2015) estimates the partial dependence of the prediction on , or single variable , across individual observations. ICE produces a curve from the fitted model over all values of while holding fixed: ; the FPD curve for is the average over all ICE curves. The motivation for ICE is to identify variable interactions that average out in the FPD curve.

The SHAP method from Lundberg and Lee (2017) has roots in Shapley regression values (Lipovetsky and Conklin, 2001) and calculates the average marginal effect of adding to models, , trained on all possible subsets of features:

| (3) |

To avoid training a combinatorial explosion of models with the various feature subsets, , SHAP reuses a single model fitted to by running simplified feature vectors into the model. As Sundararajan and Najmi (2019) describes, there are many possible implementations for simplified vectors. One is to replace “missing” features with their expected value or some other baseline vector (BShap in Sundararajan and Najmi 2019). SHAP uses a more general approach (“interventional” mode) that approximates with where is called the background set and users can pass in, for example, a single vector with column averages or even the entire training set, , which is what we will assume (and is called CES() in Sundararajan and Najmi 2019 where ). To further reduce computation costs, SHAP users typically explain a small subsample of the data set, but with potentially a commensurate reduction in the explanatory resolution of the underlying population. SHAP has model-type-dependent optimizations for linear regression, deep learning, and decision-tree based models.

For efficiency, SHAP approximates with , which assumes feature independence. (Janzing et al., 2019) argues that “unconditional [as implemented] rather than conditional [as defined] expectations provide the right notion of dropping features.” But, using the unconditional expectation makes the inner difference of Equation 3 a function of codependency-sensitive FPDs:

| (4) |

If the individual contributions are potentially biased, averaging the contributions of many such feature permutations might not lead to an accurate partial dependence. Even if the conditional expectation is used, Sundararajan and Najmi (2019) points out that SHAP is sensitive to the sparsity of because condition will find few or no training records with the exact values of some input vector.

The goal of ALE (Apley and Zhu, 2016) is to overcome the bias in previous model-based techniques arising from extrapolations of far outside the support of the training data in the presence of codependent variables. ALE partitions range for variable into bins and estimates the “uncentered main effect” (Equation 15) at as the cumulative sum of the partial derivatives for all bins up to the bin containing . ALE estimates the partial derivative of at as for bin that contains . They also extend ALE to two variables by partitioning feature space into rectangular bins and computing the second-order finite difference of with respect to the two variables for each bin.

Another related technique that integrates over partial derivatives to measure effects is called Integrated Gradients (IG) from Sundararajan et al. (2017). Given a single input vector, , to a deep learning classifier, IG integrates over the gradient of the model output function at points along the path from a baseline vector, , to . IG can be seen as computing the partial dependence of at a single , but using multiple vectors would yield an partial dependence curve (relative to a baseline ).

StratPD is like a “model-free” version of ALE in that StratPD also defines partial dependence as the cumulative sum of partial derivatives, but we estimate derivatives using response values directly rather than predictions. An advantage to estimating partial dependence via fitted models is that removes variability from the potentially noisy response values, . However, in practice, this requires expertise to choose and tune an appropriate model for a data set. The fact that different models can lead to meaningfully different curves for the same data can lead to misinterpretation. Also, expertise is often required to distinguish between model artifacts and interesting visual phenomena arising from the data.

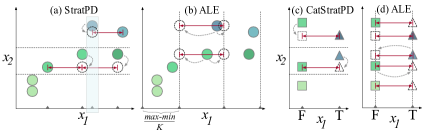

ALE partitions into bins then fixes as it shifts to bin edges to compute finite differences, as depicted in Figure 2(b) for . The wedges on the axis indicate the points of the computed partial dependence curve. StratPD partitions into regions of (hopefully) similar observations and computes finite differences between the average values at unique values in each region, as depicted in Figure 2(a). The leftmost two observations are ignored as there is no change in in that leaf. The shaded area illustrates that the partial derivative at any is the average of all derivatives spanning across regions. StratPD assumes all points within a region are identical in , effectively projecting points in space onto a hyperplane if they are not. ALE shifts values in a small neighborhood and StratPD depends on a suitable min_samples_leaf hyper parameter to prevent points in a regions from becoming too dissimilar. StratPD automatically generates more curve points in areas of high density, but ALE is more efficient.

Using decision trees for the purpose of partitioning feature space as StratPD does was previously used by Strobl et al. (2008) to improve permutation importance for random forests by permuting only within the observations of a leaf. Earlier, Breiman and Cutler (2003) defined a similarity measure between two observations according to how often they appear in the same leaf in a random forest. Rather than partitioning space like StratPD, those techniques partitioned all of space.

The model-based techniques under discussion treat boolean and label-encoded categorical variables (encoded as unique integers) as numerical variables, even though there is no defined order, as depicted in Figure 2(d). ALE does, however, take advantage of the lack of order to choose an order that reduces “extrapolation outside the data envelope” by measuring the similarity of sample values across categories. Adjacent category integers, though, could still represent the most semantically different categories, so any shift of an observation’s category to extrapolate is risky. Even the smallest possible extrapolation can conjure up nonsensical observations, such as pregnant males, as we demonstrate in Figure 7 below where FPD, SHAP, and ALE underestimate pregnancy’s effect on body weight. (For boolean , ALE behaves like FPD.) See Hooker and Mentch (2019) for more on the dangers of permuting features.

In contrast, CatStratPD uses a different algorithm for categoricals and computes differences between the average for all categories within the leaf to a random reference category; see Figure 2(c). These leaf delta vectors are then merged across leaves to arrive at an overall delta vector relating the relative effect of each category on . One could argue that StratPD also extrapolates because could include categorical variables and not all records would be identical. But, our approach only assumes values are similar and uses known training values for finite differences, rather than asking a model to make prediction for nonsensical records, which could be wildly inaccurate. Also, the decision tree would, by definition, likely partition space into regions that can be treated similarly, thus, grouping semantically similar categorical levels together.

4 Experimental results

In this section, we demonstrate experimentally that StratPD and CatStratPD compute accurate partial dependence curves for synthetic data and plausible results for a real data set. Experiments also provide evidence that existing model-based techniques can provide meaningfully-biased curves. We begin by comparing the partial dependence curves from popular techniques on synthetic data with complex interactions.111All simulations in this section were run on a 4.0 Ghz 32G RAM machine running OS X 10.13.6 with SHAP 0.34, scikit-learn 0.21.3, XGBoost 0.90, TensorFlow 2.1.0, and Python 3.7.4; ALEPlot 1.1 and R 3.6.3. A single random seed was used across simulations for graph reproducibility purposes.

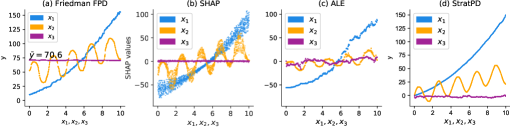

Figure 3 illustrates that FPD, SHAP, ALE, and StratPD all suitably isolate the effect of independent individual variables on the response for noiseless data generated via: for where does not affect . The shapes of the curves for all techniques look similar except that StratPD starts all curves at (as could the others). SHAP’s curves have the advantage that they indicate the presence of variable interactions. To our eye, StratPD’s curves are smoothest despite not having access to model predictions.

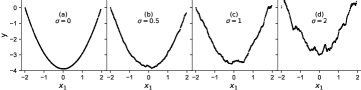

Models have a tendency to smooth out noise and a legitimate concern is that, without the benefit of a model, StratPD could be adversely affected. Figure 4 demonstrates StratPD curves for noisy quadratics generated from where and, at , 95% of the noise falls within [0,4] (since ), meaning that the signal-to-noise ratio is at best 1-to-1 for in . For zero-centered Gaussian noise and this data set, StratPD appears resilient, though does show considerable variation across runs. The superfluous noise variable in Figure 3 also did not confuse StratPD.

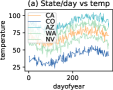

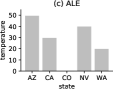

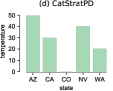

Turning to categorical variables, Figure 5 presents partial dependence curves for FPD, ALE, and CatStratPD derived from a noisy synthetic weather data set, where temperature varies in sinusoidal fashion over the year and with different baseline temperatures per state. (The vertical “smear” in the FPD plot shows the complete sine waves but from the side, edge on.) Variable state is independent and all plots identify the baseline temperature per state correctly.

The primary goal of the stratification approach proposed in this paper is to obtain accurate partial dependence curves in the presence of codependent variables. To test StratPD/CatStratPD and discover potential bias in existing techniques, we synthesized a body weight data set generated by the following equation with nontrivial codependencies between variables:

| (5) |

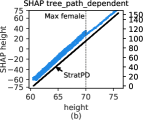

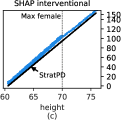

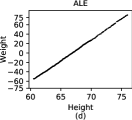

The partial derivative of with respect to is 10 (holding all other variables constant), so the optimal partial dependence curve is a line with slope 10. Figure 6 illustrates the curves for the techniques under consideration, with ALE and StratPD giving the sharpest representation of the linear relationship. (StratPD’s curve is drawn on top of the SHAP plots using the righthand scale.) The FPD and both SHAP plots also suggest a linear relationship, albeit with a little less precision. The ICE curves in Figure 6(a) and “fuzzy” SHAP curves have the advantage that they alert users to variable dependencies or interaction terms. On the other hand, the kink in the partial dependence curve and other visual phenomena could confuse less experienced machine learning practitioners and certainly analysts and researchers in other fields (our primary target communities).

Even for experts, explaining this behavior requires some thought, and one must distinguish between model artifacts and interesting phenomena. The discontinuity at the maximum female height location arises partially from the model having trouble extrapolating for extremely tall pregnant women. Consider one of the upper ICE lines in Figure 6(a) for a pregnant woman. As the ICE line slides above the maximum height for a woman, the model leaves the support of the training data and predicts a lower weight as height increases (there are no pregnant men in the training data). ALE’s curve is straight because it focuses on local effects, demonstrating that the lack of sharp slope-10 lines for FPD and SHAP cannot be attributed simply to a poor choice of model.

Also, SHAP defines feature importance as the average magnitude of the SHAP values, which introduces a paradox. The spread of the SHAP values alerts users to variable interactions, but allows contributions from other variables to leak in, thus, potentially leading to less precise estimates of ’s importance. The average SHAP magnitude skews upward, in this case, because of the contributions from pregnant women.

It is conceivable that a more sophisticated model (in terms of extrapolation) could sharpen the FPD and SHAP curves for . There is a difference, however, between extrapolating to a meaningful but unsupported vector and making predictions for nonsensical vectors arising from variable codependencies. Techniques that rely on such predictions make the implicit assumption of variable independence, introducing the potential for bias. Consider Figure 7 that presents the partial dependence results for categorical variable (same data set). The weight gain from pregnancy is 40 pounds per Equation 5, but only CatStratPD identifies that exact relationship; FPD, SHAP, and ALE show a gain of 30 pounds.

CatStratPD stratifies persons with the same or similar sex, education, and height into groups and then examines the relationship between and . If a group contains both pregnant and nonpregnant females, the difference in weight will be 40 pounds in this noiseless data set (if we assume identical ). FPD and ALE rely on computations that require fitted models to conjure up predictions for nonsensical records representing pregnant males (e.g., ). Not even a human knows how to estimate the weight of a pregnant male. SHAP, per its definition, does not require such predictions, but in practice for efficiency reasons, SHAP approximates with , which does not restrict pregnancy to females. As discussed above, there are advantages to all of these model-based techniques, but this example demonstrates there is potential for partial dependence bias.

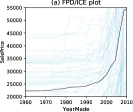

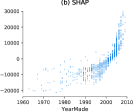

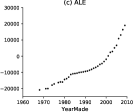

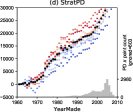

The stratification approach also gives plausible results for real data sets, such as the bulldozer auction data from Kaggle (2018). Figure 8 shows the partial dependence curves for the same set of techniques as before on feature YearMade, chosen as a representative because it is very predictive of sale price. The shape and magnitude of the FPD, SHAP, ALE, and StratPD curves are similar, indicating that older bulldozers are worth less at auction, which is plausible. The StratPD curve shows 10 bootstrapped trials where the heavy black dots represent the partial dependence curve and the other colored curves describe the variability.

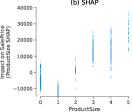

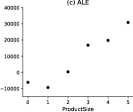

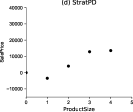

As a second example, consider the curves for feature ProductSize in Figure 9. All plots have roughly the same shape but the StratPD plot lacks a dot for ProductSize=5 because forward differences are unavailable at the right edge. (We anticipate switching switching to a central difference to avoid this issue with low-cardinality discrete variables.) It also appears that StratPD considers ProductSize’s 3 and 4 to be worth less than suggested by the other techniques, though StratPD’s might be in line with the average SHAP plot values.

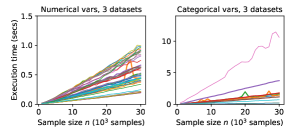

And, finally, an important consideration for any tool is performance, so we plotted execution time versus data size (up to 30,000 observations) for three real Kaggle data sets: rent, bulldozer, and flight arrival delays (Kaggle, 2015). Figure 10 shows growth curves for 40 numerical variables and 11 categorical variables grouped by type of variable. For these data sets, StratPD takes 1.2s or less to process 30,000 records for any numerical , despite the potential for quadratic cost. CatStratPD typically processes categorical variables in less than 2s but takes 13s for the high-cardinality categorical ModelID of bulldozer (which looks mildly quadratic). These elapsed times for our prototype show it to be practical and competitive with FPD/ICE, SHAP, and ALE. If the cost to train a model using (cross validated) grid search for hyper parameter tuning is included, StratPD and CatStratPD outperform these existing techniques (as training and tuning is often measured in minutes).

5 Conclusion and future work

In this paper, we contribute a method for computing partial dependence curves, for both numerical and categorical explanatory variables, that does not use predictions from a fitted model. Working directly from the data makes partial dependences accessible to business analysts and scientists not qualified to choose, tune, and assess machine learning models. For experts, it can provide hints about the relationships in the data to help guide their choice of model. Our experiments show that StratPD and CatStratPD are fast enough for practical use and correctly identify partial dependences for synthetic data and give plausible curves on real data sets. StratPD relies on two important hyper parameters (with broadly applicable defaults) but model-based techniques should include the hyper parameters of the required fitted model for a fair comparison. Our goal here is not to argue that model-based techniques are not useful. Rather, we are pointing out potential issues and hoping to open a new line of nonparametric inquiry that experiments have shown to be applicable in situations and accurate in cases where model-based techniques are not. An obvious next goal for this approach is a version for classifiers and to extend the technique to two variables, paralleling ALE’s second order derivative approach.

References

- Apley and Zhu (2016) Apley DW, Zhu J (2016) Visualizing the effects of predictor variables in black box supervised learning models. arXiv preprint arXiv:161208468

- Breiman and Cutler (2003) Breiman L, Cutler A (2003) Random forests website. https://www.stat.berkeley.edu/~breiman/RandomForests/cc_home.htm, accessed: 2019-05-24

- Friedman (2000) Friedman JH (2000) Greedy function approximation: A gradient boosting machine. Annals of Statistics 29:1189–1232

- Goldstein et al. (2015) Goldstein A, Kapelner A, Bleich J, Pitkin E (2015) Peeking inside the black box: Visualizing statistical learning with plots of individual conditional expectation. Journal of Computational and Graphical Statistics 24(1):44–65, DOI 10.1080/10618600.2014.907095, URL https://doi.org/10.1080/10618600.2014.907095, https://doi.org/10.1080/10618600.2014.907095

- Hooker (2007) Hooker G (2007) Generalized functional anova diagnostics for high-dimensional functions of dependent variables. Journal of Computational and Graphical Statistics 16(3):709–732, DOI 10.1198/106186007X237892, URL https://doi.org/10.1198/106186007X237892, https://doi.org/10.1198/106186007X237892

- Hooker and Mentch (2019) Hooker G, Mentch L (2019) Please stop permuting features: An explanation and alternatives. 1905.03151

- Janzing et al. (2019) Janzing D, Minorics L, Blöbaum P (2019) Feature relevance quantification in explainable ai: A causal problem. 1910.13413

- Kaggle (2015) Kaggle (2015) 2015 flight delays and cancellations. https://www.kaggle.com/usdot/flight-delays, accessed: 2019-12-01

- Kaggle (2017) Kaggle (2017) Two sigma connect: Rental listing inquiries. https://www.kaggle.com/c/two-sigma-connect-rental-listing-inquiries, accessed: 2019-06-15

- Kaggle (2018) Kaggle (2018) Blue book for bulldozer. https://www.kaggle.com/sureshsubramaniam/blue-book-for-bulldozer-kaggle-competition, accessed: 2019-06-15

- Lipovetsky and Conklin (2001) Lipovetsky S, Conklin M (2001) Analysis of regression in game theory approach. Applied Stochastic Models in Business and Industry 17:319 – 330, DOI 10.1002/asmb.446

- Lundberg and Lee (2017) Lundberg SM, Lee SI (2017) A unified approach to interpreting model predictions. In: Guyon I, Luxburg UV, Bengio S, Wallach H, Fergus R, Vishwanathan S, Garnett R (eds) Advances in Neural Information Processing Systems 30, Curran Associates, Inc., pp 4765–4774, URL http://papers.nips.cc/paper/7062-a-unified-approach-to-interpreting-model-predictions.pdf

- Strobl et al. (2008) Strobl C, Boulesteix AL, Kneib T, Augustin T, Zeileis A (2008) Conditional variable importance for random forests. BMC Bioinformatics 9(1):307, DOI 10.1186/1471-2105-9-307, URL https://doi.org/10.1186/1471-2105-9-307

- Sundararajan and Najmi (2019) Sundararajan M, Najmi A (2019) The many shapley values for model explanation. ArXiv abs/1908.08474

- Sundararajan et al. (2017) Sundararajan M, Taly A, Yan Q (2017) Axiomatic attribution for deep networks. In: Proceedings of the 34th International Conference on Machine Learning - Volume 70, JMLR.org, ICML’17, p 3319–3328

6 Appendix

Pseudocode for StratPD and CatStratPD.