A Note on Costs Minimization with Stochastic Target Constraints

Abstract.

We study the minimization of the expected costs under stochastic constraint at the terminal time. The first and the main result says that for a power type of costs, the value function is the minimal positive solution of a second order semi–linear ordinary differential equation (ODE). Moreover, we establish the optimal control. In the second example we show that the case of exponential costs leads to a trivial optimal control.

Key words and phrases:

Optimal stochastic control, backward stochastic differential equations2010 Mathematics Subject Classification:

49J15, 60H30, 93E201. Introduction and Main Results

This note was inspired by a series of papers which dealt with stochastic tracking problems; see, e.g., [1, 2, 3, 4, 5, 6, 7, 8, 10] and the references therein.

Consider a complete probability space together with a standard one–dimensional Brownian motion and the Brownian filtration completed by the null sets.

For any and a progressively measurable processes which satisfies the integrability condition a.s. we denote

For any let be the set of all progressively measurable processes (with the above integrability condition) which satisfy a.s. As usual, we set if an event occurs and if not.

For a given introduce the stochastic control problem

| (1.1) |

For a given we say that is optimal if Let be the set of all such that a.s. and a.s.

Lemma 1.1.

For any

Proof.

Let . Define

and

Observe that,

and

This completes the proof. ∎

The following Proposition will be crucial for deriving the main results.

Proposition 1.2.

For any

Proof.

The statement is obvious for . Thus assume that .

We use the scaling property of Brownian motion. Define the Brownian motion , . Let be the filtration generated by completed with the null sets. Clearly, , . Let be the set of all stochastic processes which are non negative, progressively measurable with respect to and satisfy

We notice that there is a bijection which is given by

Thus, from Lemma 1.1

∎

Next, let be the cumulative distribution function of the standard normal distribution. For any and consider the martingale given by

| (1.2) |

Now, we are ready to state the main results which will be proved in Section 2.

Theorem 1.3.

(I) Let be given by

The function is a non increasing solution of the ODE

| (1.4) |

with the boundary conditions

| (1.5) |

Moreover, the following minimality holds. If is another solution to (1.4) ( for some ) and satisfies

| (1.6) |

then for all .

(II)

Let .

The optimal control is given by

Namely, for the optimal control we have the ODE:

(III) Let and . Then the pair given by

is the minimal solution of the backward stochastic differential equation (BSDE)

| (1.7) |

with the singular terminal condition . This terminal condition means that a.s. where we use the convention .

Remark 1.4.

It is easy to see that the optimal control is unique. Indeed, if by contradiction are optimal controls and . Then, the process satisfies and from the strict convexity of the function we have

which is a contradiction.

2. Proof of the Main Results

We start with the following regularity result.

Lemma 2.1.

The function is concave, non increasing and satisfies .

Proof.

The fact that is non increasing is obvious.

Next, we establish the equality . From the Jensen inequality it follows that for any

Thus, and we conclude that .

It remains to prove concavity. Fix . Let us show that

Let . Choose . There exists such that

| (2.1) |

Consider the martingale given by (1.2). Observe that . Define the stopping time

Clearly, a.s. and so from the equality we conclude that

| (2.2) |

Next, let . From the Holder inequality

| (2.3) |

From (1.3), the fact that is a Brownian motion independent of , and the inequality (notice that ) we get

Thus,

| (2.4) |

By combining (2.1)–(2.4), the fact that and the simple inequality for we obtain

Since was arbitrary we complete the proof. ∎

The proof of the main results will be based on the theory developed in [8]. We start with preparations. For any introduce the optimal position targeting problem

where the infimum is taken over all progressively measurable processes , and as before, we use the convention .

Using same arguments as in Lemma 1.1 gives that

where is the set of all progressively measurable processes such that a.s., a.s. and on the event .

Clearly, there is a bijection given by . Moreover, for any we have

| (2.5) |

Thus, from Lemma 1.1 we conclude that

| (2.6) |

This brings us to the following corollary.

Corollary 2.2.

Proof.

Remark 2.3.

Now, we are ready to prove Theorem 1.3.

Proof.

Proof of Theorem 1.3.

First step: Proving that the minimal supersolution is a solution.

Fix and . Let .

Let us show that the supersolution from Corollary 2.2 is actually a solution. To that end,

we need to establish the

inequality

.

We wish to apply Theorem 4 in [9]. There is a technical problem that the indicator function is not continuous and so condition (4) in [9] does not hold. Still, this issue can be simply solved by the following density argument. Define a sequence of functions , by

Observe that for any , satisfies condition (4) in [9]. Hence, from Theorem 4 in [9] there exists a pair which satisfies the BSDE (1.7) with the terminal constraint . Since , then from the minimality property of we obtain that for any , a.s. for any . Thus,

as required.

Second step: Establishing statement (I) in Theorem 1.3.

From Corollary 2.2 and the previous step it follows that

on the event

. Clearly,

on the event , and so we conclude that

This together with the boundary condition

(was established in Lemma 2.1)

gives (1.5).

Next, we prove (1.4). Extend the function to the closed interval by and . Choose . Let . Consider the martingale . From Lemma 2.1 it follows that is concave and continuous. Thus, , is a continuous and uniformly integrable super–martingale. From Doob’s decomposition

where is a martingale and is a continuous, non decreasing process with .

Recall the minimal supersolution from Corollary 2.2. From the product rule and (1.7) we get

Hence,

We conclude that,

| (2.7) |

Next, observe that and define the function by

Notice that and , .

For any consider the stopping time . Clearly, a.s.

We notice that , and so from the Ito Formula and (2.7) we obtain

Hence,

| (2.8) |

Similarly, to (2.2)

This together with (2.8) yields that is a linear function on the interval . In particular

Since was arbitrary

we complete the proof of (1.4).

Finally, we prove minimality. Assume that there exists a positive function which satisfies (1.4) and (1.6). Define the pair by

From the Ito formula ( satisfies (1.4) and so continuously differentiable) it follows that the pair is a supersolution to the BSDE (1.7) with the singular terminal condition . From Corollary 2.2 we conclude that a.s. for any . Thus, for all .

Let us argue strict inequality.

Indeed, assume by contradiction that there is for which , then clearly is a minimum

point for the function . Hence, . Since is bounded away from zero if is bounded away from the end points , then

from standard uniqueness for initial value problems

we conclude that

on the interval . This is a contradiction and the proof of (I) is completed.

Third step: Completion of the proof.

In this step we complete the proof of statements (II)–(III) in Theorem 1.3.

Since

is continuously differentiable (satisfies (1.4)) then from the Ito formula,

Corollary 2.2 and the first step of the proof we obtain statement (III).

3. The Exponential Case

Let and consider the optimization problem

Namely, we consider a stochastic target problem with exponential costs and the same stochastic target as in (1.1).

The following result says that for any the optimal control is targeting towards with a constant speed.

Theorem 3.1.

Let . Then

and the unique optimal control is given by a.s.

Proof.

Choose . The statement is obvious for . Hence, without loss of generality we assume that . The cost function is strictly convex, and so, by using the same arguments as in Remark 1.4 we obtain that the optimal control is unique. Thus, in order to prove the theorem it is sufficient to show that the value function satisfies the inequality

| (3.1) |

Let be the set of all adapted, continuous and uniformly bounded processes. Let be the set of all strictly positive and uniformly bounded martingales with .

Applying the standard technique of Lagrange multipliers we obtain

Observe that for a given and a martingale the minimum of the above expression is obtained by taking , . Hence,

Clearly for a given and we have . We conclude that

and (3.1) follows from the following lemma. ∎

Lemma 3.2.

For any there exists such that

| (3.2) |

and

| (3.3) |

Proof.

Choose . First, assume that we found a strictly positive martingale with which satisfy (3.2)–(3.3). Then for any define by , where . Clearly,

Thus, from the Jensen inequality for the function and the Fubini theorem

Next, from the Fatou Lemma and the fact that as

We conclude that in order to prove the statement, it is sufficient to find a strictly positive martingale which satisfy (3.2)–(3.3).

To this end, consider a strictly positive martingale of the form

where is a continuous deterministic function. There exists a probability measure such that Moreover, from the Girsanov theorem the process , is a Brownian motion under . Thus,

| (3.4) |

and

| (3.5) |

Observe that for the sequence of continuous functions , given by

we have

and

This together with (3.4)–(3) yields that for sufficiently large the martingale given by , satisfies (3.2)–(3.3).

∎

4. Numerical Results

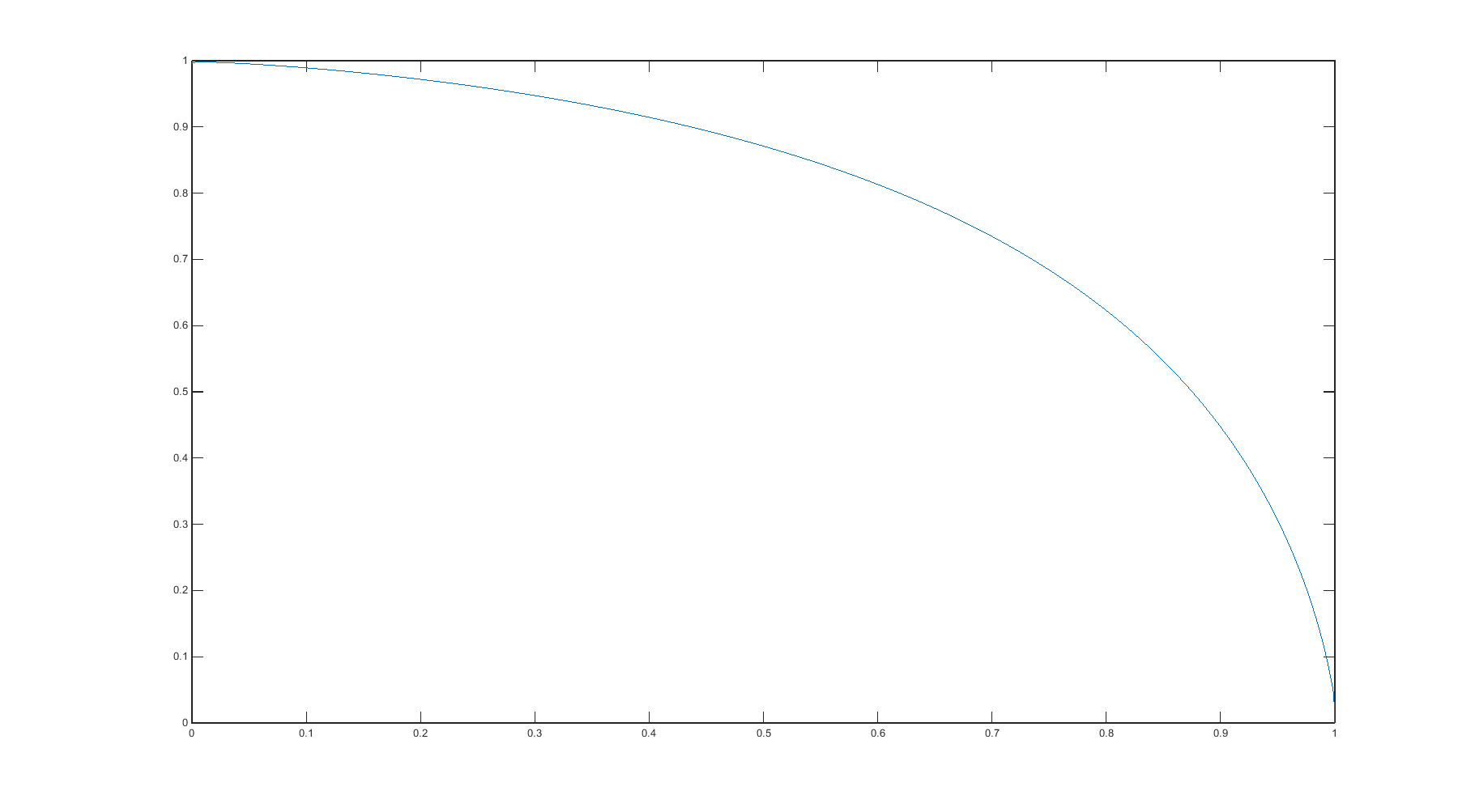

In this section we focus on the case of quadratic costs (i.e. ) and provide numerical results for the value function and simulations for the optimal control.

From (1.3) we have

By approximating the Brownian motion with scaled random walks we compute numerically the right hand side of the above equality. The result is . Then, we apply the shooting method and look for the correct value of the derivative . Namely we look for a real number such that the unique ( in the interval ) solution of the initial value problem

will satisfy the boundary conditions and . We get (numerically) a unique value . The result is illustrated in Figure 1.

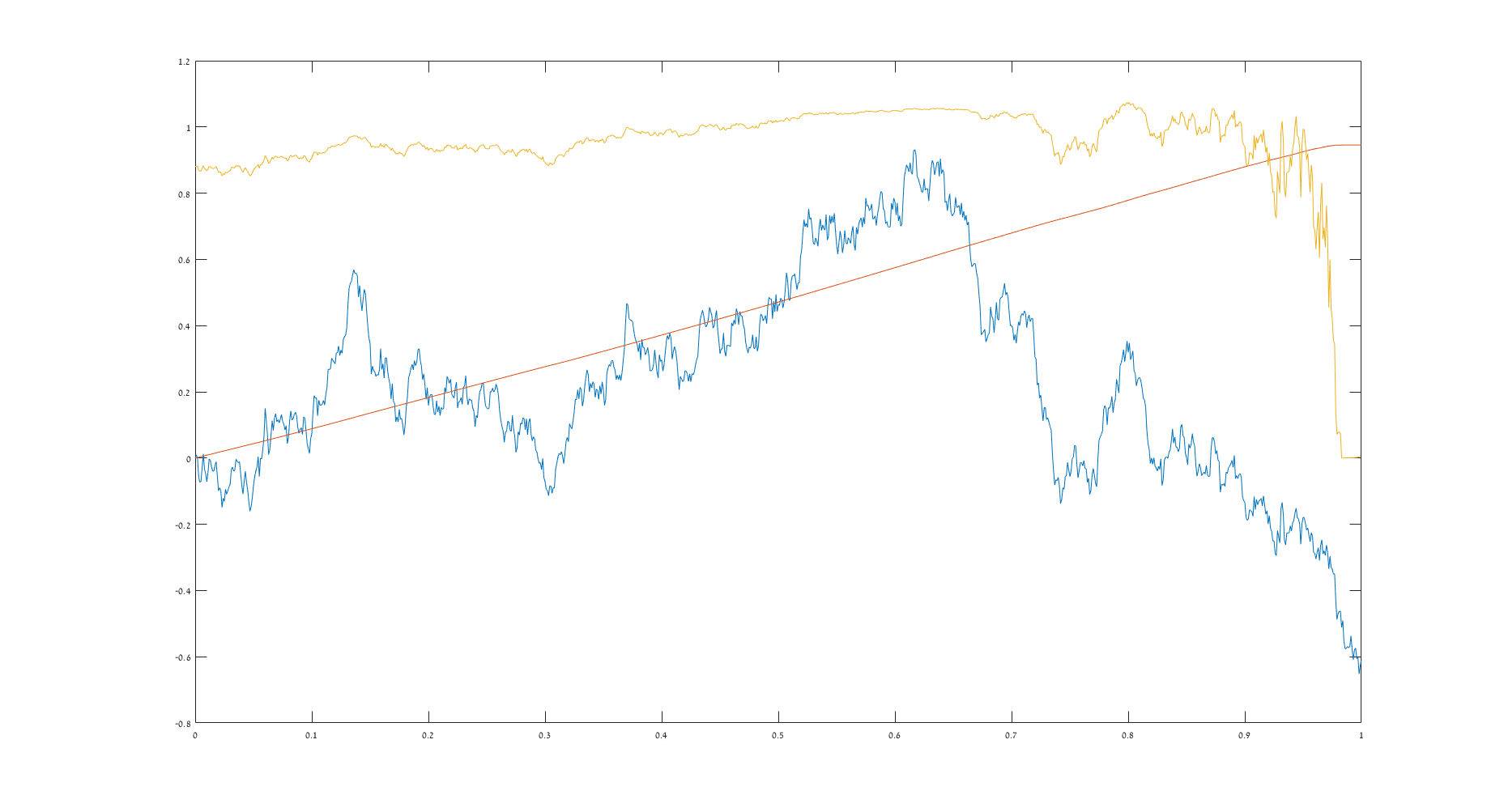

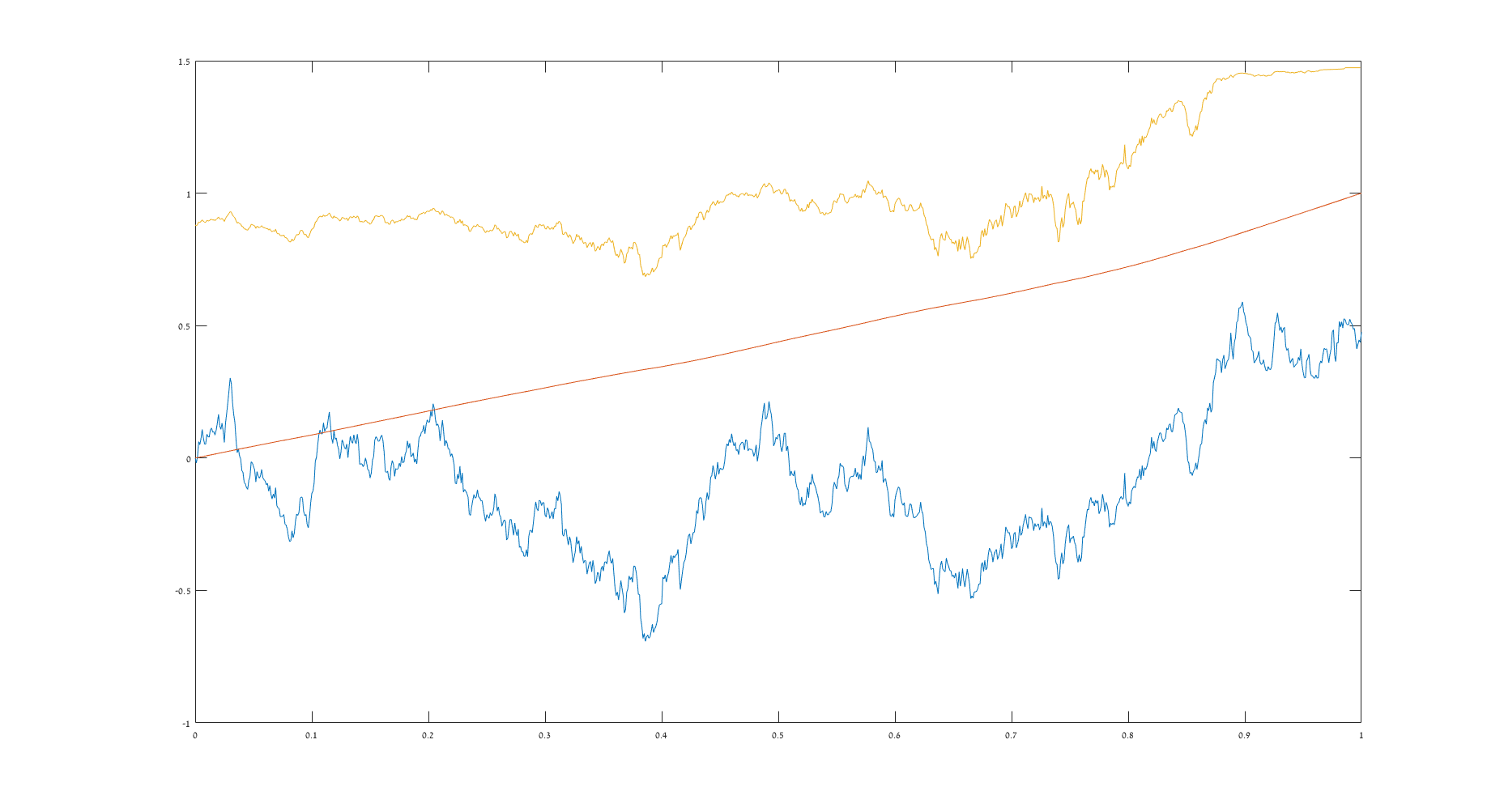

Next, for and we simulate a path of the optimal control and the corresponding strategy , . This is done by simulating a Brownian path and applying Theorem 1.3 (see Figures 2-3 below).

Acknowledgments

We would like to thank the anonymous reviewers for their suggestions and comments which improved the paper. We also would like to thank Peter Bank, Asaf Cohen and Ross Pinsky for valuable discussions. This research was partially supported by the ISF grant no 160/17 and the ISF grant no 1707/16.

References

- [1] S. Ankirchner, A. Fromm, T. Kruse and A. Popier, Optimal position targeting via decoupling fields, to appear in Annals of Applied Probability, (2019).

- [2] S. Ankirchner, M. Jeanblanc, and T. Kruse, BSDEs with singular terminal condition and a control problem with constraints, SIAM J. Control Optim., 52, 893–913, (2014).

- [3] S. Ankirchner and T. Kruse, Optimal position targeting with stochastic linear–quadratic costs, Banach Center Publications, 104, 9–24, (2015).

- [4] P. Bank, H.M. Soner, and M. Voss, Hedging with Temporary Price Impact, Mathematics and Financial Economics, 11, 215–239, (2017).

- [5] P. Bank and M. Voss, Linear quadratic stochastic control problems with singular stochastic terminal constraint, SIAM J. Control Optim., 56, 672–699, (2018).

- [6] P. Graewe, U. Horst, and J. Qiu, A non-Markovian liquidation problem and backward SPDEs with singular terminal conditions, SIAM J. Control Optim., 53, 690–711, (2015).

- [7] P. Graewe, U. Horst, and E. Séré, Smooth solutions to portfolio liquidation problems under price-sensitive market impact, Stochastic Processes and their Applications, 128, 976–1006, (2018).

- [8] T. Kruse and A. Popier, Minimal supersolutions for BSDEs with singular terminal condition and application to optimal position targeting, Stochastic Processes and their Applications, 126, 2554 –2592, (2016).

- [9] A. Popier, Backward stochastic differential equations with singular terminal condition, Stochastic Processes and their Applications, 116, 2014–2056, (2006).

- [10] A. Schied, A control problem with fuel constraint and Dawson–Watanabe superprocesses, Ann. Appl. Probab., 23, 2472–2499, (2013).