Condition-based Maintenance for Multi-component Systems: Modeling, Structural Properties, and Algorithms

Abstract

Condition-based maintenance (CBM) is an effective maintenance strategy to improve system performance while lowering operating and maintenance costs. Real-world systems typically consist of a large number of components with various interactions between components. However, existing studies on CBM focus on single-component systems. Multi-component condition-based maintenance, which joins the components’ stochastic degradation processes and the combinatorial maintenance grouping problem, remains an open issue in the literature. In this paper, we study the CBM optimization problem for multi-component systems. We first develop a multi-stage stochastic integer model with the objective of minimizing the total maintenance cost over a finite planning horizon. We then investigate the structural properties of a two-stage model. Based on the structural properties, two efficient algorithms are designed to solve the two-stage model. Algorithm 1 solves the problem to its optimality and Algorithm 2 heuristically searches for high-quality solutions based on Algorithm 1. Our computational studies show that Algorithm 1 obtains optimal solutions in a reasonable amount of time and Algorithm 2 can find high-quality solutions quickly. The multi-stage problem is solved using a rolling horizon approach based on the algorithms for the two-stage problem.

keywords:

Condition-based maintenance, multi-component systems, multi-stage stochastic integer programming, endogenous uncertainty1 Introduction

Reliability is the central concern of many mission-critical systems, such as aerospace systems, electric power systems, and nuclear systems. Investigations show that many accidents are caused by equipment failures, which were attributed to the lack of effective maintenance methods. For example, the space shuttle Challenger accident [1] and the Deepwater Horizon drilling rig explosion [2] occur in part because of inadequate maintenance. As the complexity of modern engineering systems increases, it is imperative to develop cost-effective maintenance plans for complex systems.

Maintenance strategies can be generally classified into two categories: time-based maintenance (TBM) and condition-based maintenance (CBM). The literature on TBM and CBM for single-component systems is abundant [3, 4]. However, much less attention has been paid on multi-component systems. Existing studies on multi-component systems are mainly time-based [5, 6, 7]. Despite the fact that CBM can be more cost-effective compared to TBM [8, 9, 4], CBM for multi-component systems is underexplored.

A multi-component system is usually subject to various interactions among components, such as stochastic dependence, structural dependence, and economic dependence [7, 5]. Stochastic dependence means the state of one component influences the lifetime distributions of other components. Structural dependence applies if components structurally form a part, so that maintenance of a failed component implies maintenance of other components as well. Economic dependence occurs if any maintenance action incurs a fixed system-dependent cost, often referred to as setup cost, due to mobilizing repair crew, disassembling machines, and downtime loss [10]. This setup cost can be significant in many capital-intensive industries. For example, the production losses during the shutdown ranges from $500 to $100,000 per hour in a chemical plant and millions of dollars per day in offshore drilling refineries [11]. Therefore, significant cost savings can be achieved by maintaining multiple components jointly instead of separately.

In this paper, we study the CBM optimization problem for multi-component systems with economic dependence over a finite planning horizon using a stochastic programming approach. The objective is to minimize total maintenance cost by selecting components for maintenance at each decision period. This problem is challenging because it joins the components’ stochastic degradation processes and the combinatorial maintenance grouping problem [5, 12, 13]. In addition, the component state transition probability depends on the maintenance decision, making the problem decision-dependent, which is different from the standard approach to formulating stochastic programs based on the assumption that the stochastic process is independent of the optimization decisions. This endogenous uncertainty can make the stochastic programs more computationally challenging. There is a lack of general methods to efficiently solve this type of problem. Existing studies on multi-component maintenance planning often use simplified assumptions [9, 14, 15] or resort to simulation methods [16, 17] to reduce mathematical difficulties in modeling and solving this problem.

We develop a general multi-stage stochastic maintenance model and do not restrict any grouping opportunities. Due to the complexity of the multi-stage stochastic maintenance model with integer decision variables, we first consider a two-stage model and investigate its structural properties. Based on the structural properties, we design two efficient algorithms to solve the two-stage model. The multi-stage model is solved using a rolling horizon approach based on the algorithms for the two-stage model. The main contribution of this paper is threefold.

(1)Develop an analytical CBM model for multi-component systems using a stochastic programming approach. This model is among the very first efforts that provide analytical expressions for the cost function and maintenance decisions of multi-component CBM. The proposed model is general with no restrictions for grouping as opposed to exiting one that only allow grouping at PM or CM.

(2)Establish structural properties for the two-stage model. These theoretical properties provide the conditions and search directions of improving any feasible solution, and lead to significant reduction of the search space of the problem.

(3) Design efficient algorithms to find high-quality solutions. We develop algorithms for the two-stage problem based on its structural properties, which are then implemented on a rolling-horizon to solve the multi-stage problem. Computational studies show that our algorithms can provide satisfactory solutions within a reasonable amount of time, particularly for large-scale problems.

The remainder of this paper is organized as follows. Section 2 reviews the related studies on multi-component maintenance and stochastic programming methods. In Section 3, we develop a CBM model for multi-component systems over multiple decision periods. Section 4 investigates structural properties for the two-stage model. In Section 5, we design two algorithms for the two-stage problem and use rolling horizon technique to approximate the multi-stage model. Computational studies are presented in Section 6. Section 7 concludes this research and discusses the future research directions.

2 Literature review

We model the CBM optimization problem for multi-component systems using stochastic programming. We first examine the existing literature on multi-component maintenance, and then review the solution techniques for stochastic programming.

2.1 Multi-component maintenance

Most studies on multi-component maintenance are focused on TBM, which can be further divided into direct-grouping [18, 19] and indirect-grouping approaches [20, 21, 22, 23] . Direct-grouping approach partitions the components into several fixed groups and always maintains the components in a group jointly. By using this approach, the problem becomes a set-partitioning problem, which is NP-complete. Indirect-grouping groups preventive maintenance (PM) activities by making the PM interval a multiple of a basis interval, so that the maintenance of different components can coincide [20, 21], or performs major PM on all component jointly at the end of a common interval and allows minor or major PM within this interval [22, 23]. Unlike the fixed structure under direct-grouping, there is no fixed group structure under indirect-grouping. Some researchers formulate an indirect-grouping model as a mixed integer programming (MIP) problem [24, 22, 23]. Because of the simplified policy structure, the MIP model can be separated by components, which greatly reduces the computational complexity. However, both direct- and indirect-grouping approaches only group PM activities and ignore the grouping opportunities provided by CM. Patriksson et al. [25] use stochastic programming to model a time-based multi-component replacement problem. However, CM and PM have the same cost and are not distinguished in their paper.

Much less attention has been paid to CBM for multi-component systems [4]. Opportunistic maintenance (OM) has been considered for multi-component CBM [14, 26, 15]. OM takes advantage of CM by performing PM on functioning components when any failure happens. Castanier et al. [15] consider both PM and CM as opportunities for maintaining other functioning components and formulate the problem as a semi-regenerative process. However, they only consider a two-component system because of the exponential growth of problem size. Some studies have used Markov decision process (MDP) to solve the multi-component maintenance optimization problem. However, due to the state space grows exponentially as the number of components and/or the number of states increase, this method is limited to small scale problems. For example, Jia [27] models the OM problem as an MDP and investigate the structural property of the optimal policy. A two-component system is studied in [27]. Several studies use simulation methods to find optimal opportunistic CBM policies [16, 17], which also suffers from curse of dimensionality.

Proportional hazard model (PHM) incorporates both event data and CM data by modeling the lifetime of a component as a hazard rate process [4, 28]. Tian et al. extends the PHM from single-component CBM to multi-component CBM [9]. They study two practical cases with systems of two components and three components.

2.2 Stochastic programming

Various methods and techniques have been developed to solve a stochastic programming problem. For a two-stage stochastic linear program, Benders decomposition [29, 30] and progressive hedging algorithm (PHA) [31, 32] are two major decomposition methods. Benders decomposition is a vertical decomposition approach that decomposes the problem into a master problem that consists of the first-stage decisions and the subproblems that consist of second-stage decisions of all scenarios. PHA is a horizontal decomposition approach that decomposes the problem by scenarios. It first independently solves all subproblems at each iteration and then forces the non-anticipatively constraints converge.

Multi-stage stochastic programming extends two-stage stochastic programming by allowing revised decisions at each stage based on uncertainty realizations observed so far [33]. For a multi-stage stochastic linear program, nested Benders decomposition [34, 35] that extended from Benders decomposition and PHA are also two common solution approaches. However, because the size of the scenario tree grows exponentially as the number of stages increases, both approaches are computationally intractable. Stochastic dual dynamic programming (SDDP) [36, 37] overcomes the exploding scenario tree size problem in nested Benders decomposition by combining scenario tree nodes. The drawback of the SDDP approach is that it relies on special problem structure such as stage-wise independence [38]. Rolling horizon provides a heuristic approach to approximating a multi-stage stochastic program by solving the two-stage problem on a rolling basis and utilizing the first-stage solution [39, 40, 41]. This approximation approach requires the two-stage problem to be computationally tractable. Recently, rule-based method has attracted some interests in addressing the intractability issue in multi-stage stochastic programming [42, 43, 44, 38]. This method restricts the solution to have some specific function forms, such as linear [38], piece-wise linear [44], and polynomial [43]. Because the optimal decision rules of arbitrary multi-stage stochastic programs do not have general forms, rule-based methods cannot guarantee the solution quality in general [42].

A stochastic integer program further combines the difficulty of stochastic programming and integer programming and is challenging to solve. Nested Benders decomposition and SDDP that utilize Benders cuts become prohibited to this problem because strong duality does not hold due to integrality constraints. Moreover, PHA does not perform well for this problem in general because the non-anciticipativity constraints may converge slowly due to the integrality constraints and the intractability of solving each integer subproblem. Integer L-shaped method is another approach in solving stochastic integer program by using integer L-shaped cuts within the Benders decomposition framework [29, 45]. However, this method is typically inefficient because it needs to generate an integer L-shaped cut for every feasible solution in the worst case scenario.

Stochastic programming with endogenous uncertainty draws some attentions recently because this type of uncertainty presents in a large number of applications [46, 47, 48]. Endogenous uncertainty implies that the underlying stochastic process is influenced by the decisions. Therefore, the probabilities of scenarios are decision-dependent and usually nonlinear [47, 48]. There is a lack of efficient method to solve this type of problem.

Our review shows that there is no general method to solve the proposed multi-stage stochastic maintenance model with integer decision variables and endogenous uncertainty. Efficient algorithms are needed to find high-quality solutions.

3 Model development

Notation.

-

number of components

-

component set,

-

number of decision stages

-

decision-stage set,

-

node set at stage

-

index of node at stage , i.e.,

-

ancestor node of ,

-

child nodes of ,

-

state of component i at stage t

-

state of component i in scenario at stage

-

state transition probability from state to for component

-

PM cost of component i

-

CM cost of component i

-

setup cost

-

maintenance decision of component i at stage t without considering economic dependence

-

optimal maintenance decision of component at stage without considering economic dependence

-

equals to 1 if any maintenance is performed on component at stage and 0 otherwise

-

in scenario

-

vector of for all at stage :

-

vector of for all at stage in scenario :

-

equals to 1 if CM is performed on component at stage and 0 otherwise

-

in scenario

-

equals to 1 when any maintenance is performed at stage and 0 otherwise

-

in scenario

-

do-nothing set at the first stage,

-

maintenancce set at the first stage,

We consider condition-based maintenance optimization for multi-component systems. The system consists of multiple components with economic dependence. Significant cost savings can be achieved by maintaining multiple components jointly rather than separately. We focus on systems with hidden failure which can only be revealed through inspection. For example, a production system may have failed but still operates, producing non-conforming products, and the failure can only be detected by inspection [49]. We assume components deteriorate independently. Such an assumption is common for systems where components are not subject to common cause failures or the deterioration dependence among components is weak [9, 18, 19, 17]. Each component has condition states, where a larger state represents a worse yet functioning condition and state is the failure state. All components are subject to stochastic degradation. Without maintenance intervention, the condition of a component cannot return to a better state. Inspection is performed periodically on the system to reveal the states of all components and each inspection is a decision stage. In some real-world problems, an inspection schedule is already in place based on experiences or required by regulations. For example, many refinery and chemical plants conduct annual or biannual turnarounds during which they inspect their equipment. In cases where the interval length needs to be determined, an optimal interval length can be determined using decomposition methods [6, 19] or numerical search methods. At each decision stage, all failed components need to be correctively maintained and all functioning ones can be preventively maintained if desired. Both CM and PM restore a component to an as-good-as-new state, i.e., state 1.

This maintenance optimization problem is naturally a multi-stage stochastic integer program. At each stage , we first observe all components’ states , . We then decide whether a component needs to be maintained (). All failed components are correctively maintained (). If there is any maintenance performed at stage , the setup cost is incurred ().

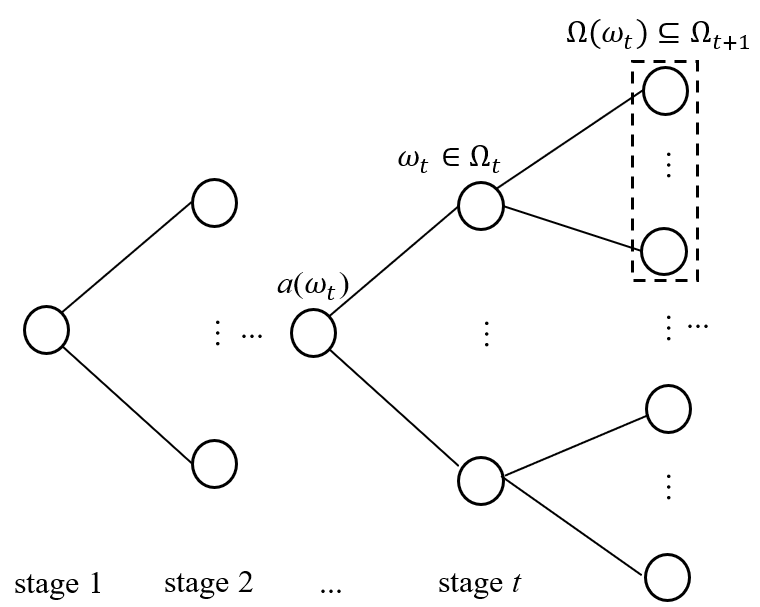

We illustrate the decision process using a scenario tree in Figure 1. In the scenario tree, we need to make maintenance decisions at each node . Each node is characterized by a combination of all components’ states, i.e., , and is the set of all nodes at stage . For each node , , it has a set of child nodes at stage , where collects all possible combinations of all components’ states. For each node , , it has a unique ancestor node at stage . A node path from the root node to a last stage node is referred to as a scenario. The total number of scenarios is , which grows exponentially as the number of components and/or stages increase.

Our objective is to minimize the total cost over the planning horizon , where the total cost includes the first-stage cost and the expected second-stage cost of all nodes . For the cost at each node at stage , it consists of current-node cost and the expected cost of all child nodes . For last stage nodes, i.e., , the cost concerns the current-node cost only.

Given the component states for all components at node in stage , the probability from node to its child node depends on the maintenance decision . For example, if the prior-maintenance state of a component in node is , the post-maintenance transition probability is () and () otherwise, and this leads to different node transition probabilities.

Denote as the probability from node to its child node given decision , and as the state transition probability from state to for component . Since components deteriorate independently, we have

Next, we develop the multi-stage stochastic model:

Decision variables :

: 1 if component is maintained at node in stage , and 0 otherwise.

: 1 if component is correctively maintained at node in stage , and 0 otherwise.

: 1 if there is any maintenance occurs at node in stage , and 0 otherwise.

Multi-stage stochastic model (P1):

| (1) |

s.t.

| (2) |

| (3) |

| (4) |

| (5) |

| (6) |

| (7) |

Objective function (1) consists of the total cost at the first stage and the expected total cost at the second stage. The objective function for node at stage is given by constraint (2). Constraints (3) ensure setup cost is incurred whenever a maintenance action is performed. Constraints (4) force CM actions on all failed components. Constraints (5) guarantee that the indicator of maintenance action is set to 1 when CM is performed. Constraints (6) and (7) are integrality constraints for all decision variables.

As illustrated in Figure 1, the problem size of P1 grows exponentially as the number of components increases. As discussed in the literature review, there is no general method to solve this problem due to the lack of structural properties in multi-stage stochastic integer programs with endogenous uncertainty. Therefore, we first consider a two-stage problem.

The two-stage problem can be simplified by eliminating the second stage because the closed-form solutions for all second-stage subproblems can be obtained. Note that for the ease of notation, we drop the subscripts of , and in the two-stage model. First, for any subproblem , the objective function and all constraints are independent of the first-stage decisions and only depends on the components’ states in scenario . Because the second stage is the last stage of the two-stage problem, to minimize any subproblem, it is obvious that we only need to correctively maintain all failed components to satisfy constraints (4) and do nothing on functioning components. Therefore, the optimal solutions in the second-stage subproblems are

| (8) |

| (9) |

and

| (10) |

Two-stage stochastic model (P2):

| (11) |

s.t.

| (12) |

| (13) |

| (14) |

| (15) |

| (16) |

where

| (17) |

The two-stage model can be directly used in mission-critical applications where successfully completing a mission (one-period) is the primary concern.

4 Structural properties of the two-stage model

In this section, we establish three structural properties for P2. The first property provides an optimal solution to P2 based on the optimal solution without considering economic dependence. Because the optimal solution without considering economic dependence can be obtained easily, we can quickly identify the optimal solution to P2 when the condition in Proposition 1 is satisfied. The second property establishes the condition when changing the decision(s) of certain component(s) from do-nothing to PM reduces the total maintenance cost. The third property establishes the condition when changing the decision(s) of certain component(s) from PM to do-nothing reduces the total maintenance cost. Propositions 2 and 3 are the theoretical foundation of Algorithm 1 that solves P2 optimally.

Proposition 1.

If , then . ∎

Proof.

See Appendix A.1. ∎

Proposition 1 shows that it is optimal to maintain all components (i.e. ) if all components need to be maintained when ignoring economic dependence (i.e. ). The optimal maintenance decision without considering economic dependence of component can be obtained easily as follows:

| (18) |

Proposition 1 leads to an optimal solution to P2 when for all components . However, the condition of for all is a special scenario. Next, we explore more general structural properties of the two-stage model.

Definition 1.

A partition of set , i.e., and , is a solution to P2, where is the do-nothing set that collects all components that are not maintained at the first stage, i.e., and is the maintenancce set that includes all components that are maintained at the first stage, i.e., . ∎

A partition of is feasible if every failed component at the first stage belongs to . Therefore, determining the optimal is now equivalent to find out a feasible and optimal partition of that minimizes the total cost. Next, we give two propositions regarding how to improve a feasible partition .

Proposition 2.

Consider two feasible partitions and of . Let and be their respective total costs. If and , we have if and only if , where

and

Proof.

See Appendix A.2. ∎

Proposition 2 helps to quickly identify a set to improve the current partition by moving set from the do-nothing set to the maintenance set. consists of two parts: and . The first part is determined by the components in set and the second part is the probability that all components will survive in the second stage given the current decision partition, i.e., . The probability increases as more components are maintained.

Let us first examine the condition in Proposition 2 when . Suppose , , Proposition 2 provides the condition of improving the current partition by maintaining component . When , we have

| (19) |

because is the state transition probability from the perfect state to the failed state and therefore holds in many scenarios (e.g., when inspection interval is not long). Based on Equation (19), we have several important observations: (1) increases as increases. The increase in indicates that it is less likely that we change the decision on from no maintenance to PM. This is because a higher PM cost makes it less cost-effective to perform PM at the first stage. (2) increases as decreases. It is less incentive to perform PM on component with other components at the first stage when CM cost of component is lower. (3) increases as decreases, because the decrease of setup cost makes sharing setup cost at the first stage less cost-effective. And (4) increases as decreases, meaning a better component condition makes it less worthy to maintain the component at the first stage. Similar patterns can be observed when . Proposition 2 also provides the maintenance action for a new component. Specifically, when , , we have , which implies we should never maintain a new component.

Proposition 3.

Consider two feasible partitions and of . Let and be their respective total costs. If and , we have if and only if , where

and values and are the defined in Proposition 2. ∎

Proof.

See Appendix A.3. ∎

Proposition 3 helps to quickly identify a set to improve the current partition by moving set from the maintenance set to the do-nothing set. Note that in contrast to considering in Proposition 2, Proposition 3 considers .

We similarly first investigate the condition in Proposition 3 when . Suppose , , Proposition 3 establishes the condition of improving the current partition by not maintaining component . When , we have

| (20) |

because in many scenarios. Examining Equation (20), we observe similar patterns regarding whether changing a component from PM to do-nothing reduces the total maintenance costs as the ones we see from Equation (19).

Corollary 1.

Let and be two feasible partitions of . For any set and , we have , where equality holds when . ∎

Proof.

See Appendix B.1. ∎

5 Solution algorithms

Based on Propositions 2 and 3, we design Algorithm 1 that finds the optimal partition for P2. Although the computational studies in the next section show that Algorithm 1 is fast for most test cases, the time complexity of Algorithm 1 is in the worst case scenario. Therefore, we develop Algorithm 2 to heuristically search a better solution based on the results from the early termination of Algorithm 1. We further use the two-stage model and rolling horizon technique to approximate the multi-stage problem P1.

5.1 Algorithm 1

Propositions 2 and 3 help to find a better solution given any feasible solution. However, they do not necessarily lead any feasible solution to an optimal one. Next we show that if Propositions 2 and 3 are applied following a certain procedure, an optimal solution can be obtained.

Let be the undetermined set in which all components’ first-stage decisions are not determined. Constructing an optimal partition implies optimally moving all subsets to or . The proposed procedure starts from searching all subsets with and increases the cardinality of by 1 until some is moved to based on Proposition 2 or based on Proposition 3. Because the conditions of Propositions 2 and 3 change after moving , the search restarts from . This process is repeated until . It can be easily verified that sets need to be examined in the worst case scenario.

Specifically, we initialize , to include all failed components to ensure the feasibility, and . If there is any subset with satisfies Proposition 2 (Proposition 3), we move from to () after all subsets with are searched. If there is no subset with satisfies Propositions 2 or 3, we search the subsets with in an ascending order until some satisfying the condition in Propositions 2 or 3 is obtained and moved out of . We then update and restart to search the subset from . The construction of the optimal partition terminates when . The optimality of partition given by Algorithm 1 is proved in Proposition 4.

Proposition 4.

The partition given by Algorithm 1 is an optimal partition. ∎

Proof.

See Appendix A.4. ∎

5.2 Algorithm 2

As stated previously, Algorithm 1 requires to examine sets in the worst case scenario. To ensure that we obtain a high-quality solution in a reasonable amount of time, we develop Algorithm 2 that heuristically finds a sub-optimal solution based on Algorithm 1.

Specifically, we first terminate Algorithm 1 after the cardinality of exceeds the maximum cardinality specified, which means we only search the component set that has no more than components. Based on and obtained from early termination of Algorithm 1, we randomly generate partitions of undetermined set , and select the best partition of . Note that it is suggested to include the options of maintaining all and none of undetermined components as candidate solutions, because many of our experiments show that it is likely that the optimal partition is either or .

5.3 Algorithm 3

We further use P2 to approximate the multi-stage model (P1) by utilizing the rolling horizon technique. At each decision period , we solve P2 which consists of periods and using Algorithm 2 and employ the first-stage solutions as the decisions for period . The states components transition to in the next period (i.e., period ) are determined by the decision made in the previous period (i.e., period ) and the transition probabilities. We then solve a new P2 consisting of decision periods and and use the first-stage solution as the decisions for period . This process is repeated until the last decision period is reached. This procedure is summarized in Algorithm 3.

In many real applications, when more degradation information becomes available upon inspection at each decision period, Bayesian updating can be easily performed to obtain more accurate degradation distributions and better-informed maintenance decisions can be made.

6 Computational study

In this section, we first linearize P2 so that small-scale problems of P2 can be solved by commercial solvers such as CPLEX for comparison purposes. We then conduct computational studies to examine the performance of Algorithms 1 and 2. The proposed models and algorithms are then illustrated by two real-world cases.

6.1 Linearization of P2

In Equation (17), the term is non-linear, which is linearized first. The term can be expanded to a polynomial function of , with degree of . After the expansion, we observe that all non-linear terms are the products of multiple (from 2 to ) binary decision variables . Standard linearization method for the multiplication of multiple binary variables are applied here [50]. After linearization, we replace Equation (17) by Equation (21) in model P2,

| (21) |

where

| (22) |

| (23) |

| (24) |

| (25) |

| (26) |

Note that set collects all subsets of that have cardinality and therefore , . For each set , we have and .

6.2 Computational studies

We first compare the computational time of Algorithm 1 with CPLEX for small-scale problems. We then examine the computational time and cost error of Algorithms 1 and 2 for large-scale problems.

We assume the degradation of all components can be described by gamma processes with shape parameter and rate parameter . The continuous degradation levels are divided into several intervals to represent different states, and the transition probabilities can be computed accordingly. Without loss of generality, we assume inspection interval is 1. We arbitrarily set , which is the maximum partitions generated in Algorithm 2. We consider systems with different number of components . For each , we consider 100 instances with different combinations of degradation processes, and costs of PM and CM. The degradation parameters, and the costs of PM and CM are drawn from uniform distributions . Therefore, a total of 10,000 experiments are run. Table 1 summarizes the baseline parameters.

|

|

|

instance | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 20 | 11 | 20 | 100 | 100 |

For each , we examine the average performance of 100 problem instances. Table 2 presents the computational times of solving P2 by CPLEX and Algorithm 1 for different numbers of components. NA is reported when the computational time is either longer than 1 day or out of memory. From Table 2, we can see that the computational time of using CPLEX grows exponentially as the number of components increases. In contrast, Algorithm 1 finds the optimal solutions in a short amount of time.

| solver | Algorithm 1 | solver | Algorithm 1 | ||

|---|---|---|---|---|---|

| 10 | 0.422 | 0.0002 | 15 | 186.171 | 0.0004 |

| 11 | 1.029 | 0.0003 | 16 | 832.674 | 0.0004 |

| 12 | 3.064 | 0.0003 | 17 | 5093.700 | 0.0005 |

| 13 | 11.943 | 0.0003 | 18 | NA | 0.0005 |

| 14 | 46.014 | 0.0004 | 19 | NA | 0.0005 |

Next, we investigate the performances of Algorithms 1 and 2 for large-scale problems. For each , we similarly examine 100 problem instances. Note that CPLEX cannot solve any large-scale cases tested. Table 3 summarizes the performance of Algorithms 1 and 2 for large-scale problems. For each in Algorithm 1, we are interested in the average computational time of the 100 problem instances (avg. time), the maximum computational time (max time), the average (avg. ) and the maximum (max ), where is the maximum set cardinality that Algorithm 1 searched. From Table 3, we can see that the average time in general increases as the number of components increases. It is also noted that the maximum search time of Algorithm 1 increases substantially as the number of components increases. This is because the solution space increases significantly as the number of components increases. As a result, Algorithm 1 may have to search more sets at higher cardinalities of before reaching the optimality criterion (i.e., undetermined set is empty). This is evidenced by the increase of . A higher cardinality generates more sets to be examined in Propositions 2 and 3, and this consumes more computational time. For Algorithm 2, we examine the computational time and cost error for different stopping criteria , which is the maximum set cardinality that Algorithm 1 allowed to search. We note that cost errors are all zero compared with the true objective value obtained by Algorithm 1, which shows Algorithm 2 can find high-quality solutions within a reasonable amount of time. We similarly observe that computational time increases as increases.

| Algorithm 1 | Algorithm 2 | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| avg. time | max time | avg. | max | avg. time | max time | |||||||||||

| =1 | =2 | =3 | =4 | =5 | =6 | =1 | =2 | =3 | =4 | =5 | =6 | |||||

| 20 | 0.001 | 0.002 | 1.19 | 4 | 0.001 | 0.001 | 0.001 | 0.001 | 0.001 | 0.001 | 0.003 | 0.003 | 0.004 | 0.001 | 0.001 | 0.001 |

| 40 | 0.002 | 0.006 | 1.01 | 2 | 0.002 | 0.002 | 0.002 | 0.002 | 0.002 | 0.002 | 0.008 | 0.004 | 0.004 | 0.003 | 0.006 | 0.006 |

| 60 | 0.004 | 0.012 | 1.00 | 1 | 0.004 | 0.004 | 0.004 | 0.004 | 0.004 | 0.004 | 0.012 | 0.012 | 0.010 | 0.011 | 0.012 | 0.011 |

| 80 | 0.007 | 0.009 | 1.00 | 1 | 0.007 | 0.007 | 0.007 | 0.007 | 0.007 | 0.007 | 0.012 | 0.021 | 0.022 | 0.018 | 0.021 | 0.017 |

| 100 | 0.015 | 0.236 | 1.08 | 3 | 0.013 | 0.013 | 0.015 | 0.014 | 0.014 | 0.015 | 0.036 | 0.062 | 0.251 | 0.239 | 0.239 | 0.240 |

| 120 | 0.023 | 0.247 | 1.11 | 3 | 0.019 | 0.020 | 0.022 | 0.022 | 0.023 | 0.022 | 0.073 | 0.073 | 0.278 | 0.246 | 0.253 | 0.248 |

| 140 | 11.4 | 939 | 1.65 | 7 | 0.034 | 0.044 | 0.119 | 0.405 | 1.284 | 4.307 | 0.078 | 0.146 | 0.948 | 7.750 | 45.33 | 230.5 |

| 160 | 7.07 | 381 | 1.86 | 6 | 0.052 | 0.066 | 0.160 | 0.589 | 1.779 | 7.006 | 0.123 | 0.218 | 1.307 | 10.53 | 71.90 | 380.9 |

| 180 | 9.85 | 348 | 2.19 | 6 | 0.072 | 0.102 | 0.355 | 1.447 | 4.602 | 9.940 | 0.174 | 0.396 | 3.022 | 18.51 | 137.9 | 349.1 |

| 200 | 106 | 6379 | 2.65 | 8 | 0.091 | 0.134 | 0.515 | 2.559 | 9.622 | 24.75 | 0.173 | 0.317 | 2.494 | 23.79 | 185.4 | 1205 |

We further examine the performance the two-stage rolling horizon approach (Algorithm 3) in approximating the multi-stage model by comparing results from our approach with optimal results on small-scale problems where exact solutions can be obtained. We arbitrarily use one problem setting by taking a sample of parameters based on Table 1 and replicate the problem 1000 times to obtain the average cost using Algorithm 3. Enumeration approach is used to obtain the exact solutions, since the problem size is small. Table 4 summarizes the computational results of different instances that can be solved within one day. From Table 4, we can see that cost percentage errors are below 20% for all cases considered, which shows that the two-stage rolling horizon approach provides an acceptable approximation to the multi-stage problem.

in approximating multi-stage model

| multi-stage | two-stage rolling horizon | |||

|---|---|---|---|---|

| n | T | cost | avg. cost | error % |

| 2 | 3 | 24.49 | 24.85 | 1.47% |

| 4 | 31.37 | 34.83 | 11.03% | |

| 5 | 37.09 | 40.33 | 8.74% | |

| 3 | 3 | 30.34 | 35.72 | 17.73% |

| 4 | 40.67 | 47.92 | 17.83% | |

| 5 | 53.78 | 63.50 | 18.07% | |

6.3 Case 1: degradation of wind turbine blades

Offshore wind farms are rapidly [26] developing in recent years to provide the renewable energy for sustainable development. An offshore wind farm is usually built thousand meters away from the coastline and typically has hundreds of wind turbines. A wind turbine consists of multiple components, such as blade, main bearing, gearbox, and generator. If a maintenance team is sent to maintain a wind turbine, it is economically beneficial to jointly maintain other wind turbines [9].

Due to the tensile mechanical loading and corrosive marine environment, stress corrosion cracking (SCC) is one of the major contributors to blades’ degradation. Shafiee et al. [26] model the monthly propagation of SCC as a stationary gamma process with an estimated shape parameter and rate parameter .

We consider a three-blade wind turbine system in this case study. Consider a planning horizon and an inspection interval of 12 months. Based on some pilot studies, we discretize the condition of a blade into 11 states, because this number of states provides us an acceptable decision accuracy while ensuring that the discretized states are robust to measurement errors. The PM cost is 200,000 Monetary Unit (MU). We consider two levels of CM costs: 600,000 MU and 1,000,000 MU.The setup cost is 130,000 MU and the failure threshold is cm [26].

| \ | 1 | 2 | 3 | ||||

| state | decision | state | decision | state | decision | ||

| 1 | 6 | no action | 5 | no action | 8 | no action | 8 |

| 2 | 10 | PM | 7 | no action | 11 | CM | |

| 3 | 4 | no action | 10 | PM | 4 | no action | |

| 4 | 5 | no action | 4 | no action | 8 | no action | |

| 5 | 6 | no action | 9 | PM | 11 | CM | |

| 6 | 8 | no action | 2 | no action | 2 | no action | |

| 7 | 10 | PM | 5 | no action | 5 | no action | |

| 8 | 6 | no action | 8 | no action | 10 | PM | |

| 9 | 8 | PM | 10 | PM | 4 | no action | |

| 10 | 4 | no action | 4 | no action | 6 | no action | |

| Note: the decisions that are different from the decisions without | |||||||

| economic dependence are shown in boldface | |||||||

| \ | 1 | 2 | 3 | ||||

| state | decision | state | decision | state | decision | ||

| 1 | 6 | no action | 5 | no action | 8 | PM | 8 |

| 2 | 10 | PM | 7 | no action | 5 | no action | |

| 3 | 4 | no action | 10 | PM | 8 | PM | |

| 4 | 5 | no action | 4 | no action | 5 | no action | |

| 5 | 6 | no action | 9 | PM | 8 | PM | |

| 6 | 8 | PM | 2 | no action | 2 | no action | |

| 7 | 3 | no action | 5 | no action | 5 | no action | |

| 8 | 8 | PM | 7 | PM | 9 | PM | |

| 9 | 3 | no action | 3 | no action | 4 | no action | |

| 10 | 6 | no action | 5 | no action | 6 | no action | |

| Note: the decisions that are different from the decisions without | |||||||

| economic dependence are shown in boldface | |||||||

We use Algorithm 3 to solve this maintenance planning problem. We compare the decisions with and without considering economic dependence. Denote the PM threshold for each component in the two-stage model without considering economic dependence by : If the component state is below , no maintenance is performed, and if the component is functioning and the state exceeds or equals to , PM is performed.

Tables 5 and 6 summarize the results when CM cost is 600,000 MU and 1,000,000 MU respectively. The threshold is 8 in both cases. From Tables 5 and 6, we can observe that maintenance decisions with and without consideration of economic dependence are different. For example, at the first decision stage () in Table 5, we can see that component 3 is not preventively maintained as it would be without considering economic dependence, so it can share the setup cost with component 1 at decision stage 2. From Table 6, we can see that component 2 is preventively maintained at decision period 8 when it is in state 7, which is below the optimal PM threshold when ignoring economic dependence.

6.4 Case 2: degradation of crude-oil pipelines

The reliability of crude-oil pipelines are critical to the safety of liquid energy supply in modern industries. Due to the corrosion, crack and mechanical damage, pipelines gradually deteriorate, which result in the decrease of pipeline wall thickness.

Based on the degradation data of six pipelines provided by a local chemical plant, we model the degradation process as a gamma process with random effects, where the shape parameter is and the rate parameter is . Random effects is used to capture the heterogeneities among all pipelines by assuming the rate parameter follows a gamma distribution with shape parameter and rate parameter . We regard the as unknown for all pipelines, and use the expectation-maximization algorithm [51] to estimate the parameters of , and . Based on the data, we obtain the estimated parameters , and .

| \ | 1 | 2 | 3 | 4 | 5 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 4 | no action | 6 | no action | 9 | PM | 5 | no action | 9 | no action |

| 2 | 8 | PM | 4 | no action | 5 | no action | 10 | no action | 11 | CM |

| 3 | 10 | PM | 4 | no action | 7 | PM | 5 | no action | 9 | no action |

| 4 | 5 | no action | 10 | no action | 11 | CM | 3 | no action | 5 | no action |

| 5 | 4 | no action | 5 | no action | 9 | PM | 5 | no action | 7 | no action |

| 6 | 9 | PM | 3 | no action | 6 | PM | 4 | no action | 6 | no action |

| 7 | 2 | no action | 3 | no action | 5 | no action | 7 | no action | 9 | no action |

| 8 | 10 | PM | 4 | no action | 7 | PM | 4 | no action | 6 | no action |

| 9 | 9 | PM | 3 | no action | 6 | PM | 3 | no action | 6 | no action |

| 10 | 9 | PM | 3 | no action | 4 | no action | 7 | no action | 8 | no action |

| 11 | 10 | PM | 3 | no action | 5 | no action | 6 | no action | 9 | no action |

| 12 | 7 | PM | 5 | no action | 8 | PM | 3 | no action | 4 | no action |

| 13 | 9 | PM | 2 | no action | 5 | no action | 7 | no action | 10 | no action |

| 14 | 1 | no action | 5 | no action | 9 | PM | 3 | no action | 4 | no action |

| 15 | 5 | no action | 6 | no action | 8 | PM | 4 | no action | 6 | no action |

| 16 | 10 | PM | 3 | no action | 8 | PM | 2 | no action | 5 | no action |

| 17 | 2 | no action | 3 | no action | 4 | no action | 7 | no action | 10 | no action |

We consider 17 pipelines located in a small region and all pipes are shutdown when any pipe is maintained. For each pipeline, the wall thickness is when it is new, and the retirement thickness (failure threshold) . The number of decision stages is 5. Suppose the costs of PM and CM are 5 and 20, and setup cost is 200.

We solve this multi-stage pipeline maintenance problem by Algorithm 3. We similarly compare the decisions with and without economic dependence. In this case, the optimal PM threshold without considering economic dependence is . Table 7 presents the state and maintenance action for each component at stage . The decisions different from those without considering economic dependence are shown in boldface. Because setup cost is much higher than the CM cost, from Table 7, we can see that there is a large number of different decisions, which shows the necessity of considering economic dependence when it exists.

We further investigate the impacts of parameter estimation uncertainty by considering estimated parameters as random variables. Let be the vector of parameters to be estimated. Given a parameter estimation the conditional cost is denoted by and the PDF value of is denoted by . Based on the estimations, the unconditional cost is . The form of PDF is typically complicated, and therefore it is difficult to derive the closed-form of . We use the method in [52] to approximate the unconditional cost. Specifically, we first use the bootstrap method to generate 500 samples of parameters. We then use the average conditional costs based on these samples to approximate the unconditional cost . Our result shows that the mean and standard deviation of conditional costs are 770.57 and 260.5. Compared with the total maintenance cost 740 when parameter uncertainty is not considered, the impact of parameter estimation uncertainty is acceptable.

7 Conclusion and future research

In this paper, we study CBM optimization problem for multi-component systems over a finite planning horizon. We formulate the problem as a multi-stage stochastic integer program, providing analytical expressions for total cost and maintenance decisions. The proposed multi-stage stochastic maintenance optimization model has integer decision variables and non-linear transition probability due to the endogenous uncertainty, and is computationally intractable. We first investigate structural properties of the two-stage problem and design efficient algorithms to obtain high-quality solutions based on the structural properties. The multi-stage model is then approximated by the two-stage model using a rolling horizon approach. Computational studies show that Algorithm 1 can solve many cases to optimality quickly and Algorithm 2 can find high-quality solutions within a very short amount of time.

This work provides a new modeling approach in modeling multi-component condition-based maintenance. Future research will consider other practical assumptions, such as the limit of maintenance budget, the requirement of system’s reliability and availability, state-dependent PM cost, and state-dependent operational cost. In this paper, we mainly consider economic dependence, it is worth to further consider stochastic and structure dependences. It will also be interesting to address situations when we do not know the exact transition probabilities. A robust optimization approach may be applicable.

Appendix

A.1. Proof of Proposition 1

Proof.

(1) We first consider the case where there is no failed component in the first stage.

We need to compare the total costs among three cases for partition : (a) , (b) and and (c) . Denote , and by the total costs for the three cases respectively, we show that is minimum.

Denote the total cost for component without considering economic dependence by

Because , we have , .

Thus, we have

(1a) Prove .

Because

we have .

(1b) Prove

It is easy to show that function has for all , . Therefore, we have

and

Because for all , we have .

Therefore, is minimum.

(2) Consider the case where there exists at least one component failed at the first stage.

Let set collect all failed components and . Following proof (1), we only need to compare case (a) and feasible case (b) because case (c) is not feasible.

The cost of case (a) and feasible case (b) are denoted by and respectively, where

and

From in proof (1a), we have .

∎

A.2. Proof of Proposition 2

Proof.

Denote the total cost for component without considering economic dependence by

and let and , then we have

If , we have

Therefore, from , we have

From , we have .

Similarly, if ,

Therefore, from , we have

From , we have . ∎

A.3. Proof of Proposition 3

Proof.

Denote the total cost for component without considering economic dependence by

and let and , then we have

If , we have

From , we have . Therefore,

From , we have .

Similarly, if ,

From , we have

From , we have ∎

A.4. Proof of Proposition 4

Proof.

We prove this proposition by showing that the cost of partition is no worse than that of any other feasible partitions.

For any other feasible partition and the partition that is obtained by Algorithm 1, we always rewrite and respectively, where set , , and . We now show that the cost of partition is no worse than that of by the following three parts: (1) When , we have cost relationship , (2) when , we have cost relationship , and (3) we have cost if and only if and .

(1) When , we have cost relationship .

This is equivalent to show that given current partition , moving from the do-nothing set to the maintenance set can reduce cost. We next show that if we keep moving the component that arrives first in in Algorithm 1 to the maintenance set, the cost keeps reducing until , which implies moving the whole set to the maintenance set reduces cost.

Denote the costs of and by and respectively, and initialize . We prove by the following steps:

Step 1: If all components in are moved into after set does in Algorithm 1, then because the cost reduces if we repeat how Algorithm 1 moves to .

Step 2: In this step, there exists at least one component that joins no later than some component in . Suppose component is the earliest one in that joins and suppose joins along with set , i.e., , where and . Therefore, when joins , the current partition is , where set , and hence from Proposition 2, we have

| (27) |

Step 3: If , then . Denote the costs for partition by . From Inequation (27), we have and therefore . We then update and and go to Step 1.

Step 4: In this step, we have . From Algorithm 1, we know that any subset cannot join given current partition . From Proposition 2, we have

| (28) |

Let . We have

where the first inequality is from Inequation (28) and the second inequality is from Inequation (27). Therefore, we have and hence

where the last inequality is from . From Proposition 2, by denoting the cost of partition by , we have since . We then update and and go to Step 1.

Therefore, we can always lower the cost by moving one component from to the maintenance set. When , we have .

(2) When , we have cost relationship .

This is equivalent to show that moving set from the maintenance set to the do-nothing set can lower cost. From Proposition 3, we need to prove .

By using the same method as proof (1), we can also prove the cost relationship when . From Proposition 3, we have . Therefore,

(3) We have cost if and only if and .

When , we have .

The first equality holds if and only if . Otherwise, following the steps of proof (1), we can always have .

Given , the second equality is equivalent to , which happens if and only if based on Corollary 1.

∎

B.1. Proof of Corollary 1:

Proof.

We first show .

where equality holds when .

(1) When , we have

where equality holds when .

(2) When and , we have

(3)When and , we have

Therefore, when and when . ∎

References

- [1] R. Feynman, “Report of the presidential commission on the space shuttle challenger accident,” Appendix F, 1986.

- [2] M. E. Paté-Cornell, “Learning from the piper alpha accident: A postmortem analysis of technical and organizational factors,” Risk Analysis, vol. 13, no. 2, pp. 215–232, 1993.

- [3] S.-H. Ding and S. Kamaruddin, “Maintenance policy optimization—literature review and directions,” The International Journal of Advanced Manufacturing Technology, vol. 76, no. 5-8, pp. 1263–1283, 2015.

- [4] S. Alaswad and Y. Xiang, “A review on condition-based maintenance optimization models for stochastically deteriorating system,” Reliability Engineering & System Safety, vol. 157, pp. 54–63, 2017.

- [5] R. Dekker, R. E. Wildeman, and F. A. Van der Duyn Schouten, “A review of multi-component maintenance models with economic dependence,” Mathematical methods of operations research, vol. 45, no. 3, pp. 411–435, 1997.

- [6] R. P. Nicolai and R. Dekker, “Optimal maintenance of multi-component systems: a review,” in Complex system maintenance handbook, pp. 263–286, Springer, 2008.

- [7] L. Thomas, “A survey of maintenance and replacement models for maintainability and reliability of multi-item systems,” Reliability Engineering, vol. 16, no. 4, pp. 297–309, 1986.

- [8] R. Ahmad and S. Kamaruddin, “An overview of time-based and condition-based maintenance in industrial application,” Computers & Industrial Engineering, vol. 63, no. 1, pp. 135–149, 2012.

- [9] Z. Tian and H. Liao, “Condition based maintenance optimization for multi-component systems using proportional hazards model,” Reliability Engineering & System Safety, vol. 96, no. 5, pp. 581–589, 2011.

- [10] R. Laggoune, A. Chateauneuf, and D. Aissani, “Impact of few failure data on the opportunistic replacement policy for multi-component systems,” Reliability Engineering & System Safety, vol. 95, no. 2, pp. 108–119, 2010.

- [11] S. Amaran, T. Zhang, N. V. Sahinidis, B. Sharda, and S. J. Bury, “Medium-term maintenance turnaround planning under uncertainty for integrated chemical sites,” Computers & Chemical Engineering, vol. 84, pp. 422–433, 2016.

- [12] P. A. Scarf, “On the application of mathematical models in maintenance,” European Journal of operational research, vol. 99, no. 3, pp. 493–506, 1997.

- [13] R. Dekker and P. A. Scarf, “On the impact of optimisation models in maintenance decision making: the state of the art,” Reliability Engineering & System Safety, vol. 60, no. 2, pp. 111–119, 1998.

- [14] A. Grall, C. Bérenguer, and L. Dieulle, “A condition-based maintenance policy for stochastically deteriorating systems,” Reliability Engineering & System Safety, vol. 76, no. 2, pp. 167–180, 2002.

- [15] B. Castanier, A. Grall, and C. Bérenguer, “A condition-based maintenance policy with non-periodic inspections for a two-unit series system,” Reliability Engineering & System Safety, vol. 87, no. 1, pp. 109–120, 2005.

- [16] J. Barata, C. G. Soares, M. Marseguerra, and E. Zio, “Simulation modelling of repairable multi-component deteriorating systems for ‘on condition’maintenance optimisation,” Reliability Engineering & System Safety, vol. 76, no. 3, pp. 255–264, 2002.

- [17] R. Laggoune, A. Chateauneuf, and D. Aissani, “Opportunistic policy for optimal preventive maintenance of a multi-component system in continuous operating units,” Computers & Chemical Engineering, vol. 33, no. 9, pp. 1499–1510, 2009.

- [18] R. Dekker, R. E. Wildeman, and R. Van Egmond, “Joint replacement in an operational planning phase,” European Journal of Operational Research, vol. 91, no. 1, pp. 74–88, 1996.

- [19] R. E. Wildeman, R. Dekker, and A. Smit, “A dynamic policy for grouping maintenance activities,” European Journal of Operational Research, vol. 99, no. 3, pp. 530–551, 1997.

- [20] S. Goyal and M. Kusy, “Determining economic maintenance frequency for a family of machines,” Journal of the Operational Research Society, vol. 36, no. 12, pp. 1125–1128, 1985.

- [21] S. K. Goyal and A. Gunasekaran, “Determining economic maintenance frequency of a transport fleet,” International Journal of Systems Science, vol. 23, no. 4, pp. 655–659, 1992.

- [22] S. Epstein and Y. Wilamowsky, “Opportunistic replacement in a deterministic environment,” Computers & operations research, vol. 12, no. 3, pp. 311–322, 1985.

- [23] M. Hariga, “A deterministic maintenance-scheduling problem for a group of non-identical machines,” International Journal of Operations & Production Management, vol. 14, no. 7, pp. 27–36, 1994.

- [24] D. R. Sule and B. Harmon, “Determination of coordinated maintenance scheduling frequencies for a group of machines,” AIIE Transactions, vol. 11, no. 1, pp. 48–53, 1979.

- [25] M. Patriksson, A.-B. Strömberg, and A. Wojciechowski, “The stochastic opportunistic replacement problem, part ii: a two-stage solution approach,” Annals of Operations Research, vol. 224, no. 1, pp. 51–75, 2015.

- [26] M. Shafiee, M. Finkelstein, and C. Bérenguer, “An opportunistic condition-based maintenance policy for offshore wind turbine blades subjected to degradation and environmental shocks,” Reliability Engineering & System Safety, vol. 142, pp. 463–471, 2015.

- [27] Q.-S. Jia, “A structural property of optimal policies for multi-component maintenance problems,” IEEE Transactions on Automation Science and Engineering, vol. 7, no. 3, pp. 677–680, 2010.

- [28] K. L. Tsui, N. Chen, Q. Zhou, Y. Hai, and W. Wang, “Prognostics and health management: A review on data driven approaches,” Mathematical Problems in Engineering, vol. 2015, 2015.

- [29] J. R. Birge and F. Louveaux, Introduction to stochastic programming. Springer Science & Business Media, 2011.

- [30] M. Bodur, S. Dash, O. Günlük, and J. Luedtke, “Strengthened benders cuts for stochastic integer programs with continuous recourse,” INFORMS Journal on Computing, vol. 29, no. 1, pp. 77–91, 2016.

- [31] R. T. Rockafellar and R. J.-B. Wets, “Scenarios and policy aggregation in optimization under uncertainty,” Mathematics of operations research, vol. 16, no. 1, pp. 119–147, 1991.

- [32] J.-P. Watson and D. L. Woodruff, “Progressive hedging innovations for a class of stochastic mixed-integer resource allocation problems,” Computational Management Science, vol. 8, no. 4, pp. 355–370, 2011.

- [33] S. Ahmed, A. J. King, and G. Parija, “A multi-stage stochastic integer programming approach for capacity expansion under uncertainty,” Journal of Global Optimization, vol. 26, no. 1, pp. 3–24, 2003.

- [34] J. Naoum-Sawaya and S. Elhedhli, “A nested benders decomposition approach for telecommunication network planning,” Naval Research Logistics (NRL), vol. 57, no. 6, pp. 519–539, 2010.

- [35] P. Parpas and B. Rustem, “Computational assessment of nested benders and augmented lagrangian decomposition for mean-variance multistage stochastic problems,” INFORMS Journal on Computing, vol. 19, no. 2, pp. 239–247, 2007.

- [36] A. Shapiro, “Analysis of stochastic dual dynamic programming method,” European Journal of Operational Research, vol. 209, no. 1, pp. 63–72, 2011.

- [37] M. V. Pereira and L. M. Pinto, “Multi-stage stochastic optimization applied to energy planning,” Mathematical programming, vol. 52, no. 1-3, pp. 359–375, 1991.

- [38] M. Bodur and J. R. Luedtke, “Two-stage linear decision rules for multi-stage stochastic programming,” Mathematical Programming, pp. 1–34, 2017.

- [39] R. Kouwenberg, “Scenario generation and stochastic programming models for asset liability management,” European Journal of Operational Research, vol. 134, no. 2, pp. 279–292, 2001.

- [40] P. Beraldi, A. Violi, N. Scordino, and N. Sorrentino, “Short-term electricity procurement: A rolling horizon stochastic programming approach,” Applied Mathematical Modelling, vol. 35, no. 8, pp. 3980–3990, 2011.

- [41] T. Tolio and M. Urgo, “A rolling horizon approach to plan outsourcing in manufacturing-to-order environments affected by uncertainty,” CIRP annals, vol. 56, no. 1, pp. 487–490, 2007.

- [42] A. Shapiro and A. Nemirovski, “On complexity of stochastic programming problems,” in Continuous optimization, pp. 111–146, Springer, 2005.

- [43] D. Bampou and D. Kuhn, “Scenario-free stochastic programming with polynomial decision rules,” in 2011 50th IEEE Conference on Decision and Control and European Control Conference, pp. 7806–7812, IEEE, 2011.

- [44] X. Chen, M. Sim, P. Sun, and J. Zhang, “A linear decision-based approximation approach to stochastic programming,” Operations Research, vol. 56, no. 2, pp. 344–357, 2008.

- [45] G. Laporte and F. V. Louveaux, “The integer l-shaped method for stochastic integer programs with complete recourse,” Operations research letters, vol. 13, no. 3, pp. 133–142, 1993.

- [46] V. Goel and I. E. Grossmann, “A class of stochastic programs with decision dependent uncertainty,” Mathematical programming, vol. 108, no. 2-3, pp. 355–394, 2006.

- [47] Y. Zhan, Q. P. Zheng, J. Wang, and P. Pinson, “Generation expansion planning with large amounts of wind power via decision-dependent stochastic programming,” IEEE Transactions on Power Systems, vol. 32, no. 4, pp. 3015–3026, 2017.

- [48] S. Peeta, F. S. Salman, D. Gunnec, and K. Viswanath, “Pre-disaster investment decisions for strengthening a highway network,” Computers & Operations Research, vol. 37, no. 10, pp. 1708–1719, 2010.

- [49] C. R. Cassady, R. O. Bowden, L. Liew, and E. A. Pohl, “Combining preventive maintenance and statistical process control: a preliminary investigation,” Iie Transactions, vol. 32, no. 6, pp. 471–478, 2000.

- [50] R. L. Rardin and R. L. Rardin, Optimization in operations research, vol. 166. Prentice Hall Upper Saddle River, NJ, 1998.

- [51] Z.-S. Ye, M. Xie, L.-C. Tang, and N. Chen, “Semiparametric estimation of gamma processes for deteriorating products,” Technometrics, vol. 56, no. 4, pp. 504–513, 2014.

- [52] Z.-S. Ye, M. Xie, L.-C. Tang, and Y. Shen, “Degradation-based burn-in planning under competing risks,” Technometrics, vol. 54, no. 2, pp. 159–168, 2012.